Pacific

Admiral® VUL 2 PROSPECTUS May 1, 2026

Pacific

Admiral® VUL 2 a flexible

premium variable universal life insurance policy issued by Pacific Life Insurance

Company (“Pacific Life”) through the Pacific

Select Exec Separate Account of Pacific Life.

● Flexible premium means

you can vary the amount and frequency of your premium payments. You must, however, pay enough premiums

to cover the ongoing costs of Policy

benefits.

● Variable

means the Policy’s value depends on the performance of the Variable Investment

Options you choose available under the Policy. Other investment options that may be available under the

Policy include the Fixed Options and Indexed Fixed

Options.

● Universal

life insurance means you can accumulate cash value and the Policy provides

a Death Benefit to the Beneficiary you choose.

You should

be aware that the Securities and Exchange Commission (SEC) has not approved or disapproved of the securities

or passed upon the accuracy or adequacy of the

disclosure in this prospectus. Any representation to the contrary is a criminal offense.

Additional information about certain investment products,

including variable life insurance, has been prepared by the SEC’s staff and is available at

Investor.gov.

Certain

Investment Options, Policy features and benefits described in this prospectus may vary or may not be

available depending on the broker-dealer through which the Policy is sold. See APPENDIX:

FINANCIAL INTERMEDIARY VARIATIONS in this prospectus for more information.

If

you are a new investor in the Policy, you may cancel your Policy within 10 days of receiving it without

paying fees or penalties. In some states, this cancellation

period may be longer. Upon cancellation, you will receive either a full refund of the amount you paid

with your application or your total Policy value, plus any Policy charges

and fees deducted, less Policy Debt. You should review this prospectus, or consult with your financial

professional, for additional information about

the specific cancellation terms that apply. In order to sell this product, a financial professional must

be a properly licensed and appointed life insurance

producer.

Withdrawals are not permitted during the first

year of the Policy, but the Policy may be surrendered during the first year.

See WITHDRAWALS, SURRENDERS AND LOANS – Surrendering Your Policy

for more information about the consequences related to surrendering your Policy. You

should speak with your financial professional about Policy features, Investment Options, benefits, risks,

and fees and whether the Policy is appropriate for you when considering

your financial situation and objectives.

This

Policy is not available in all states. This prospectus is not an offer in any state or jurisdiction where

we are not legally permitted to offer the Policy. This Policy

is subject to availability, is offered at our discretion, and may be discontinued for purchase at any

time. The Policy is described in detail in this prospectus

and its Statement of Additional Information (SAI). Each Fund is described in its prospectus and in its

SAI. No one has the right to describe the Policy or any Fund any differently

than they have been described in these documents.

This

material is not intended to be used, nor can it be used by any taxpayer, for the purpose of avoiding

U.S. federal, state or local tax penalties. Pacific Life, its distributors

and their respective representatives do not provide tax, accounting or legal advice. Any taxpayer should

seek advice based on the taxpayer’s particular

circumstances from an independent tax advisor.

This Policy

is not a deposit or obligation of, or guaranteed or endorsed by, any bank. It’s not federally insured

by the Federal Deposit Insurance Corporation (FDIC), the Federal

Reserve Board, or any other government agency. Investment in a Policy involves risk, including possible

loss of principal and previous earnings.

1

TABLE OF CONTENTS

Where

To Go For More Information back cover

2

SPECIAL TERMS

In this

prospectus, you or your

mean the policyholder or Owner. Pacific Life, we, us or

our refer to Pacific Life Insurance Company. Policy

means a Pacific Admiral®

VUL 2 variable universal life insurance policy, unless we state otherwise.

We have tried to make this prospectus easy

to read and understand, but you may find some words and terms that are new to you. We have

identified some of these below.

If

you have any questions, please ask your financial professional or call us at (800) 347-7787. In order

to sell this product, a financial professional must be a properly

licensed and appointed life insurance producer.

1

– Year High Cap Plus Indexed Account – an Account that is part of our General

Account. We credit interest on the Indexed Account, in part, based on any

positive change in an Index. This Account offers a guaranteed participation rate of 100%, a 15% guaranteed

minimum Growth Cap, a guaranteed Segment Adjustment Factor

equal to 0.60, and a 0% guaranteed interest rate. This Account is called “1 Year Indexed Account

6” in your Policy.

1 –

Year Indexed Account – an Account that is part of our General Account. We

credit interest on the Indexed Account, in part, based on any positive change

in an Index. This Account offers a guaranteed participation rate of 100%, a 2% guaranteed minimum Growth

Cap, a guaranteed Segment Adjustment Factor equal to 1.00, and

a 0% guaranteed interest rate. This Account is called “1 Year Indexed Account” in your Policy.

(See the INDEXED

FIXED OPTIONS section in this prospectus for a summary table of the differences

between the Indexed Accounts.)

Accounts

– consist of the Fixed Account, the Variable Accounts, the Indexed Accounts,

and the Standard Loan Account, each of which may be referred to as an

Account.

Account Addition –

will increase the Fixed Account Value, Variable Account Value, and/or the Indexed Account Value based

on your allocation instructions, except Additional

Credits attributed to the Fixed Option will be added proportionately to the Fixed Option and Additional

Credits attributed to the Variable Options will

be added proportionately to the Variable Options. Account Additions may consist of Premium payments,

loan repayments and any applicable Additional Credits.

Account Deductions –

treated as a proportionate deduction from the Fixed and Variable Account Value until each have been reduced

to zero. Any remaining deductions will be deducted

proportionately from each Segment Value across all segments in the Indexed Accounts. In lieu of the above

and at our sole discretion, we may make

available the option for the Owner(s) to select the Fixed or Variable Accounts and amounts where the

Account Deductions are taken from. Call us to confirm

that this option is available.

Accumulated

Value – the total amount of your Policy’s Variable Account Value, Fixed

Account Value, Indexed Account Value and the Standard Loan Account

Value, on any Business Day.

Additional

Credit – Beginning as early as the 11th Policy Year, at our discretion and on a

non-guaranteed basis, we may credit the Accumulated Value with an additional amount. The additional amount,

if any, will be credited no less frequently than annually as an Account Addition. Once credited, the

additional amount is nonforfeitable except indirectly due to any Surrender Charge. The calculated additional

credited rate varies by multiple factors, including, but not limited to, the amounts of Coverage Layers

and whether they are Basic Life Coverage or provided under a Rider, and the Policy’s Net Accumulated

Value, and will vary across Policies.

Age –

the Insured’s age on his/her birthday nearest the Policy Date. We add one year to this Age on each

Policy Anniversary.

Alternate

Loan – a loan (available through the Alternate Loan Rider 3) that is secured

by the Designated Account Value (the loan amount secured remains in designated

Indexed Accounts). The amount you may borrow is determined, in part, by how much of your Accumulated

Value is allocated to the designated Indexed Accounts.

Alternate Loan Value –

the sum of the value of all Alternate Loans taken minus any Alternate Loan repayments

Alternate Policy Debt –

the amount necessary to repay any Alternate Loan in full. It is equal to the Alternate Loan Value plus

any accrued Alternate Loan Interest Charged.

Basic Face Amount –

is the sum of the Face Amounts of all Basic Life Coverage Layers on the Insured. The Basic Face Amount

of the initial Basic Life Coverage is shown in the Policy Specifications.

Basic Life Coverage – is insurance Coverage

on the Insured provided by the Policy as shown in the Policy Specifications and any related Supplemental

Schedule of Coverage. See “Basic Life Coverage Layer” and “Coverage

Layer” definitions.

3

Basic Life Coverage Layer –

is a layer of insurance Coverage on the Insured provided by the Policy. There will be one or more Basic

Life Coverage Layers created at issue. Multiple Basic Life Coverage Layers will be created at issue if

a Policy is issued with multiple Risk Classes and each Basic Life Coverage Layer will have a different

Basic Face Amount, Risk Class, and set of charges. In addition, each increase in Basic Face Amount will

create a new Basic Life Coverage Layer. Each Basic Life Coverage Layer has its own Basic Face Amount,

Risk Class, Coverage Layer Date, and set of charges. The Basic Life Coverage layer(s) at issue will be

shown in the Policy Specifications and any additional Basic Life Coverage Layer(s) added after issue

will be shown in the Supplemental Schedule of Coverage. Please see the DEATH BENEFITS

section for more information on Basic Life Coverage Layers.

Beneficiary

– the person, people, entity or entities you name to receive the Death Benefit

Proceeds.

Business Day –

Each day the New York Stock Exchange (“NYSE”) is open for regular trading. Each Business

Day ends when the NYSE closes each day which is typically 4:00

p.m. Eastern Standard Time. In this Prospectus, references to “day” or “date”

means Business Day unless otherwise specified. If any transaction

or event called for under a Policy is scheduled to occur on a day that is not a Business Day, such transaction

or event will be deemed to occur on the next following Business

Day unless otherwise specified. If any transaction is requested for a day that does not exist in a given

calendar month, it will occur on the last day of

such month. Any systematic pre-authorized transaction scheduled to occur on December 30th or December

31st where that day is not a Business Day will be deemed

an order for the last Business Day of the calendar year and will be calculated using the applicable values

at the close of that Business Day. A Business

Day is also called a valuation day in your Policy.

Cash

Surrender Value – the Policy’s Accumulated Value less any Surrender

Charge.

Cash Value Accumulation Test

– one of two Death Benefit Qualification Tests available under the Policy,

and defined in Section 7702(b) of the Tax Code.

Class

–

is used in determining Policy charges, interest credited to your Policy, including but not limited to

Additional Credits, features of the Indexed Accounts, certain limitations on Policy features and benefits,

and depends on a number of factors, including but not limited to the, Death Benefit, Death Benefit Option,

Face Amount by Basic Life Coverage or Coverage provided under a Rider, Policy Date, Policy duration,

premiums paid, source of premium, Policy ownership structure, underwriting type, reinsurance, the Age

and Risk Class of the Insured, requested or scheduled additions or increases of Coverage Layers, and

the presence and attributes of Policy features, including optional Riders, and benefits. See the YOUR

INVESTMENT OPTIONS – Fixed Options and YOUR INVESTMENT OPTIONS – Indexed Fixed Options

sections in this prospectus for further details about how interest is credited.

Closing

Value – the value of the Index as of the close of the New York Stock Exchange,

which is usually 4:00 p.m. Eastern time. If an Index is traded on an exchange

other than the New York Stock Exchange, we will use that exchange’s Closing Value. If no Closing

Value is published for a given day, we will use the Closing

Value for the next day for which the Closing Value is published. In calculating the change in value of

the Index, we use the Closing Value of the Index.

Code or Tax Code – is the U.S. Internal

Revenue Code of 1986, as amended.

Coverage

– insurance coverage on the Insured as provided by the Policy or other attached

Riders.

Coverage Layer –

is insurance coverage on the Insured provided by the Policy or under an optional Rider. Generally, increases

in the Basic Face Amount under the Policy or additional life insurance Coverage added by a Rider are

referred to as a “Coverage Layer”.

Coverage

Layer Date – is the effective date of a particular Coverage Layer

and is the date used to determine Coverage Layer months, years and anniversaries.

The Coverage Layer Date for the initial Coverage Layer is the Policy Date as shown in the Policy Specifications.

Cutoff Date –

4:00 p.m. Eastern time, two Business Days before the Segment Start Date.

Death Benefit – the amount which

is payable on the date of the Insured’s death.

Death

Benefit Proceeds – the amount which is payable to the Beneficiary on

the date of the Insured's death, adjusted as provided in the Policy.

Death Benefit Qualification Test –

either the Cash Value Accumulation Test or the Guideline Premium Test. This test determines what the

lowest Minimum Death Benefit should be

in relation to a Policy’s Accumulated Value. Each test available under the Policy is defined in

Section 7702 of the Tax Code.

Designated

Account – an Indexed Account that we have classified as a Designated Account for

the purposes of securing an Alternate Loan. We may add or remove

Designated Accounts, at our discretion. See Changes to Designated Accounts

below for additional information.

Designated

Account Value – the sum of the Segment Values for all Segments in

each Designated Account.

4

Designated Amount – the amount you instruct

us to allocate to an Indexed Fixed Option classified as a Designated Account. We will only transfer the

Designated Amount (or such lesser amount if Policy charges have been deducted,

or if you have taken a withdrawal or Standard Loan) to an Indexed Fixed Option

on a Segment Start Date. Any interest earned on the Designated Amount while it is allocated to the Fixed

Account will not be transferred to an Indexed Fixed Option on

a Segment Start Date.

Evidence

of Insurability – is information, including among other things, medical

information, satisfactory to us that is used to determine insurability and the Insured’s

Risk Class, subject to our approval and issue limits.

Face

Amount – the amount used to determine the Death Benefit on the Insured provided

by the Basic Life Coverage or Coverage under a Rider, as shown in the Policy Specifications and any related

Supplemental Schedule of Coverage. The Face Amount is subject to increase or decrease as provided elsewhere

in the Policy.

Fixed Account –

an Account that is part of our General Account. Net Premiums and Accumulated Value under the Policy may

be allocated to this Account for accumulation at a fixed

rate of interest declared by us.

Fixed Account

Value – the total amount of your Policy’s value allocated to the Fixed Account.

Fixed Options –

Investment Options that are part of our General Account and that consist of one or more Fixed Accounts

available under this Policy. Currently, the only Fixed

Option available for investment as of the Policy Date is the Fixed Account.

Free Look Right – your right to cancel

(or refuse) your Policy and return it for a refund.

Free

Look Transfer Date – the day we transfer Accumulated Value from the Fidelity®

VIP Government Money Market Variable Account to the Investment Options

you chose.

Fund –

one of the funds providing underlying portfolios for the Variable Investment Options offered under the

Policy.

General Account –

includes all of our assets, except for those held in the Separate Account, or any of our other separate

Accounts.

Grace

Period – a

61-day period, beginning

on the date

we send you,

and anyone to

whom you have

assigned your Policy,

notice that your

Policy’s Accumulated

Value less Total

Policy Debt is

insufficient to pay

the Monthly Deduction.

The Grace Period

gives you 61

days in which

to pay sufficient

premium to keep your Policy In Force and prevent your Policy from lapsing.

Growth Cap –

the maximum total interest rate for a Segment over the Segment Term, as described in the Indexed Fixed

Options, including both Minimum Segment Guaranteed Interest

Rate and the Segment Indexed Interest Rate.

Guideline

Premium Limit –

the maximum amount

of premium or

premiums that can

be paid for

any given Face

Amount in order

to qualify the

Policy as life

insurance for tax purposes as specified in the Guideline Premium Test.

Guideline Premium Test –

one of two Death Benefit Qualification Tests available under the Policy, and defined in Section 7702(a)(2)

of the Tax Code.

Illustration

– a display of hypothetical Policy benefits over time to show how the Policy

and certain Riders operates based on the assumed Age and Risk Class of an Insured, Basic Coverage or

Coverage provided under a Rider, Death Benefit Option, premium payments, any other Rider requested, and

historical or hypothetical gross rate(s) of return, which are not guaranteed and likely not to occur

in the future.

Index –

The Standard & Poor’s 500®

Composite Stock Price Index, excluding dividends (“S&P 500®”).

Each Index is a price return index and the performance of an Index

does not include income from any dividends or other distributions paid by the Index’s component

companies. If dividends and other distributions were included,

the Index performance would be higher.

Indexed

Account – an Account that is part of our General Account under the Contract to which

Accumulated Value may be transferred or allocated to. The Indexed

Account provides for credited interest based in part on the positive performance of a particular Index.

Currently, there are two Indexed Accounts – the 1-Year

Indexed Account and the 1-Year High Cap Plus Indexed Account.

Indexed

Account Value – the total amount of your Policy’s Accumulated

Value allocated to the Indexed Accounts. The Indexed Account Value will not include

Segment Indexed Interest for any Segments that have not reached Segment Maturity.

Indexed Fixed Options –

Investment Options that are part of our General Account and that consist of one or more of the Indexed

Accounts available under this Policy. The Indexed

Accounts available as of the Policy Date are the 1-Year Indexed Account and the 1-Year High Cap Plus

Indexed Account.

Index Growth

Rate – a rate that represents the change in value (up or down) of an Index from

the Segment Start Date to Segment Maturity. We use this rate to help

determine what amount may be credited as interest to an Indexed Account.

5

Numerically, the Index Growth Rate is (b ÷ a) –

1, where:

a = The Closing Value of the Index as

of the day before the beginning of the Segment Term; and

b = The

Closing Value of the Index as of the day before the end of the Segment Term.

In Force – means a Policy is

in effect and provides a Death Benefit on the life of the Insured.

In

Proper Form – is when we will process your requests once we receive

all letters, forms or other necessary documents, completed to our satisfaction. In Proper

Form may require, among other things, a notarized signature or some other proof of authenticity that

is required for us to act on a Written Request.

We

do not generally require such proof, but we may ask for proof if it appears that your signature has changed,

if the signature does not appear to be yours, if we have

not received a properly completed application or confirmation of an application, or for other reasons

to protect you and us. Call us or contact your financial

professional if you have questions about the In Proper Form requirement for a request.

Insured – the person on whose

life the Policy is issued.

Investment

Option – consist of the Variable Options, any available Fixed Options, any available

Indexed Fixed Options, or any additional Investment Options

that may be added.

Lockout

Period – a 12-month period of time during which you may not make any transfers

into the Indexed Fixed Options. A Lockout Period begins any time

a deduction is taken from the Indexed Fixed Options as a result of a Standard Loan or withdrawal that

is not part of a Systematic Distribution Program.

Long

Term Performance Rider (“LTPR”) – an optional Rider

available with the Policy that provides additional insurance Coverage on the Insured along with the Basic

Face Amount of the Policy. LTPR Coverage cannot be issued on a Policy with SVER Coverage.

LTPR Termination Charge (“Termination Charge”) –

each LTPR Coverage Layer has its own Termination Charge that applies for 10 Policy Years after

the Coverage Layer Date. If you terminate the LTPR while the Policy is still In

Force, we will assess the Termination Charge against your Policy’s Accumulated

Value and the Policy Surrender Charge will be reduced by and no longer include the surrender charge associated

with the LTPR Coverage.

Each

subsequent increase in LTPR Coverage will result in an additional LTPR Coverage Layer that has its own

Termination Charge that applies for 10 Policy Years

following the Coverage Layer Date.

Minimum

Death Benefit – is based on the Death Benefit Qualification Test for

the Policy and at any time will be no less than the minimum amount we determine

to be required for this Policy to qualify as life insurance under the Code. The Minimum Death Benefit

is equal to the Minimum Death Benefit Percentage multiplied by

the Cash Surrender Value as determined under applicable tax law.

Minimum Death Benefit Percentage –

is a factor used to determine the Minimum Death Benefit. This factor will depend on the Death Benefit

Qualification Test that you have chosen.

The Minimum Death Benefit Percentages as of the Policy Date are shown in the Policy Specifications.

Minimum Segment Guaranteed Interest Rate –

the minimum annual rate that will be used to help determine the Segment Guaranteed Interest, if any,

and the Segment Indexed Interest Rate. Currently the rate is 0%

and is guaranteed to never be lower than 0%.

Modified

Endowment Contract – a type of life insurance policy as described in Section

7702A of the Tax Code, which receives less favorable tax treatment

on distributions of cash value than conventional life insurance policies. Classification of a Policy

as a Modified Endowment Contract is generally dependent

on the amount of premium paid during the first seven Policy Years, or after a material change has been

made to the Policy.

Monthly

Deduction – an amount that is deducted monthly from your Policy’s

Accumulated Value on the Monthly Payment Date until the Monthly Deduction

End Date. See the YOUR POLICY’S ACCUMULATED VALUE – Monthly Deductions

section in this prospectus for more information.

Monthly Deduction End Date –

is the date when Monthly Deductions end as shown in the Policy Specifications. This date is the Policy

Anniversary when the Insured attains age

121.

Monthly Payment Date –

the day we

deduct monthly charges

from your Policy’s

Accumulated Value. The

first Monthly Payment

Date is your

Policy Date, and

it is the same day each month thereafter.

Net Accumulated

Value – the Accumulated Value less any Total Policy Debt.

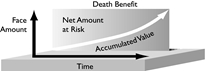

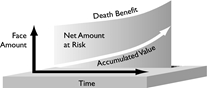

Net Amount At Risk – the difference between

the Death Benefit payable if the Insured died and the Accumulated Value of your Policy. We use a Net

Amount At Risk to calculate the Cost of Insurance Charge. For Cost of Insurance

Charge purposes, the Net Amount At Risk is equal to the Death Benefit as of

the most recent Monthly Payment Date divided by 1.0008295, reduced by the

6

Accumulated Value of your Policy.

Net Cash Surrender Value –

the Cash Surrender Value less any Total Policy Debt.

Net

Premium – premium paid less any premium load deducted.

Owner –

the person named on the application who makes the decisions about the Policy and its benefits while it

is In Force. Two or more Owners are called Joint Owners.

See the POLICY BASICS – Owners, the Insured, and Beneficiaries section

in this prospectus for more information.

Participation

Rate – the percentage of the Index Growth Rate used to calculate the Segment

Indexed Interest Rate.

Policy

Anniversary – the same day as your Policy Date every year after

we issue your Policy.

Policy

Date – the date upon which life insurance coverage under the Policy becomes effective.

The Policy Date is used to determine the Monthly Payment Date, Policy

months, Policy Years, and Policy monthly, quarterly, semi-annual and annual anniversaries.

Policy Specifications –

summarizes information specific to your Policy at the time the Policy is issued. We will send you updated

Policy Specification pages or supplemental schedules

if you change your Policy’s Face Amount or any of the Policy’s other benefits.

Policy Year –

starts on your Policy Date and each Policy Anniversary and ends on the day before the next Policy Anniversary.

Premium Band –

the amount used to determine any surplus premium load that may apply for premium paid that is greater

than the Premium Band amount.

Riders

– provide extra benefits, some at additional cost. Any optional Rider which

offers additional life insurance Coverage on the Insured will have an initial

Face Amount and any increase may also be referred to as a “Coverage Layer”.

Risk Class – is determined during

the underwriting process and is used to determine certain Policy charges. The Risk Class of each Insured

is shown in the Policy Specifications. The

Risk Class of each Insured for any additional coverage added after issue will be shown in the Supplemental

Schedule of Coverage.

Scheduled

Annual Renewable Term Rider (“S-ARTR”) – an optional Rider available

with the Policy that provides additional scheduled increases in insurance Coverage on the Insured generally

without the requirements for future medical underwriting.

Segment

– a portion of your Accumulated Value in an Indexed Fixed Option. We create

a Segment when Accumulated Value is transferred from the Fixed Account

to an Indexed Fixed Option.

Segment

Adjustment Factor – one factor

used in determining the final Segment Indexed Interest that is credited at Segment Maturity.

Segment Guaranteed Interest –

the interest we credit daily to each Segment in the 1-Year Indexed Account and 1-Year High Cap Plus Indexed

Account from the Segment Start Date to the Segment Maturity at an

annual rate equal to 0% for the Indexed Fixed Options.

Segment

Indexed Interest – at Segment Maturity, Segment Indexed Interest, if

any, will be credited to the Segment and is equal to the Segment Indexed Interest

Rate for that Segment multiplied by the average of all Segment monthly balances over the entire Segment

Term. That amount will then be multiplied by the Segment Adjustment

Factor to determine the final Segment Indexed Interest credited at Segment Maturity.

Segment Indexed Interest Rate –

this is the rate that will be applied to a Segment at Segment Maturity to determine the Segment Indexed

Interest after adjustment for any Participation

Rate or any Growth Cap limits. The calculation for the Segment Indexed Interest Rate is described below.

The Segment Indexed Interest Rate for the 1-Year

Indexed Account and the 1-Year High Cap Plus Indexed Account reflects any growth in the Index,

multiplied by the Participation Rate, subject to the Growth Cap, that exceeds

the Minimum Segment Guaranteed Interest Rate. It is equal to the lesser of (a × b)

and c - d, but not less than zero where:

a = Index

Growth Rate

b = Participation

Rate

c = Growth Cap

d = Minimum Segment Guaranteed Interest Rate

Segment Maturity –

the end of the Segment Term and the date we calculate any Segment Indexed Interest and credit it to the

7

Segment.

Segment

Maturity Value – the value of the Segment at Segment Maturity, including

any Segment Indexed Interest.

Segment

Start Dates – the dates on which transfers or Segment Maturity reallocations

into the Indexed Fixed Options may occur, generally the 15th

of each month as shown in your Policy

Specifications. We use a Segment Start Date to determine Segment months and Segment years.

Segment Term –

a one-year period beginning on the Segment Start Date and ending on the Segment Maturity date.

Segment Value –

the amount transferred to an Indexed Fixed Option from the Fixed Account on the Segment Start Date. After

the Segment Start Date, the Segment Value equals a + b - c + d where:

a = The Segment Value as of the previous day;

b

= The Segment Guaranteed Interest since the previous day;

c

= Any Segment Deductions since the previous day; and

d

= Any Segment Indexed Interest credited only at Segment Maturity.

Separate

Account – the

Pacific Select Exec

Separate Account, a

separate account of

ours registered as

a unit investment

trust under the

Investment Company Act of 1940.

Standard Loan –

a loan taken under the Policy and secured by the Policy Accumulated Value amount transferred to the Standard

Loan Account.

Standard

Loan Account – an account which holds amounts transferred from the

Investment Options as collateral for Standard Loans.

Standard

Loan Account Value – the total amount of your Policy’s Accumulated

Value allocated to the Standard Loan Account.

Standard

Policy Debt – the amount necessary to repay any Standard Loan in

full. It is equal to the Standard Loan Account plus any accrued loan interest charge.

Supplemental Schedule of Coverage –

is the written notice we will provide you reflecting certain changes made to your Policy after the Policy

Date.

Surrender

Charge – a charge that will apply for the first 10 Policy Years

for the initial Basic Life Coverage Layer and the initial Long Term Performance Rider

Coverage Layer (“LTPR”), if any, that reduces the Policy’s Accumulated Value if you

surrender your Policy. If the LTPR is in effect, the total Policy Surrender

Charge is increased by the surrender charge associated with the LTPR Coverage. Each subsequent increase

in Basic Life or LTPR Coverage will result in an additional

Coverage Layer that has its own Surrender Charge that applies for 10 Policy Years following the Coverage

Layer Date.

Surrender

Value Enhancement Rider 3 (“SVER”) – an

optional Rider available under the Policy that provides additional insurance Coverage on the Insured

along with the Basic Face Amount of the Policy. SVER Coverage cannot be issued on a Policy with LTPR

Coverage.

Systematic Distribution Program

– a program of periodic distribution that we designate, which includes periodic

distribution of the Policy’s Accumulated Value

through Policy loans and withdrawals while the Insured is alive and the Policy is In Force.

Total Face Amount –

the sum of all Basic Face Amounts and the Face Amounts of any Riders providing life insurance coverage

on the Insured, unless specifically excluded. The

Total Face Amount is used in determining the Death Benefit under this Policy and the initial Total Face

Amount is shown on the cover of your Policy or

subsequent Supplemental Schedule of Coverage.

Total

Interest Credited – the sum of Segment Indexed Interest plus Segment Guaranteed

Interest that we credit to a Segment within the Indexed Fixed Options.

Total Policy Debt –

is equal to the sum of any Standard Policy Debt plus any Alternate Policy Debt.

Variable Account – a subaccount of

the Separate Account which invests in shares of a corresponding underlying Fund.

Variable Account Value –

the total amount of your Policy’s Accumulated Value allocated to the Variable Accounts.

Variable Investment Option (“Variable Option”)

– a Variable Account available under this Policy that is a subaccount of

the Separate Account.

When the

Policy is In Force – this Policy is In Force as of the latest of the Policy

Date, your acceptance of the delivered Policy, and your payment of the initial

premium.

8

Written Request or In Writing –

your signed request in writing, that is received by us at our Administrative Office In Proper Form, containing

information needed to act on the request. Written Request includes an

electronic request provided in a form acceptable to us.

IMPORTANT

INFORMATION YOU SHOULD CONSIDER ABOUT THE POLICY

| | | | | |

FEES AND EXPENSES | LOCATION IN PROSPECTUS |

Charges

for Early Withdrawals | If

you fully surrender your Policy within the first 10 years of Policy issue or any Basic Life Coverage

Layer or Long Term Performance Rider (“LTPR”) Coverage Layer added to the Policy (each Coverage

Layer will have its own 10-year Surrender Charge period from its Coverage Layer Date), you will be assessed

a Surrender Charge of up to a maximum of 1.71% ($17.10) per $1,000 of Basic Face Amount plus 5.70% ($57.00)

per $1,000 of Face Amount added by the LTPR. This charge will vary based on the individual characteristics

of the Insured and other options chosen. For example, if you fully surrender your

Policy within the first 10 years of Policy issue, you could pay a Surrender Charge up to $1,710 on $100,000

of Basic Face Amount. | Fee

Tables Surrendering Your Policy Optional Riders and Benefits |

Transaction

Charges | In

addition to Surrender Charges, you may also be charged for other transactions. These other charges may

include charges for each premium paid, withdrawal charges for partial withdrawals, Termination Charges

for terminating the LTPR, fees to exercise the Overloan Protection 3 Rider, transfer fees for transfers

among the Investment Options, fees for Illustration requests, unscheduled face amount increases for certain

Riders, and for requests to increase or exercise certain benefits under an optional Rider. | Fee

Tables Deductions From Your Premiums Making Withdrawals |

Ongoing

Fees and Expenses (annual charges) | In addition to Surrender Charges and transaction charges,

an investment in the Policy is subject to certain ongoing fees and expenses, including fees and expenses

covering the cost of insurance under the Policy, administrative charges, asset charges, coverage charges,

interest on any Policy loans, and the cost of optional benefits available under the Policy. Certain

fees and expenses are set based on characteristics of the Insured (e.g. age, sex, and rating classification).

Please review the Policy Specifications page of your Policy for rates applicable to your Policy. You

will also bear expenses associated with the Variable Investment Options you choose under the Policy,

as shown in the following table: | Fee Tables Monthly Deductions Appendix:

Funds Available Under the Policy |

| | ANNUAL FEE | MINIMUM | MAXIMUM |

| | Variable Investment Options (Fund fees

and expenses) | 0.03%1 | 1.10%1 |

1

9

| | | |

RISKS | LOCATION IN PROSPECTUS |

Risk

of Loss | You

can lose money by investing in the Policy, including loss of principal and any prior earnings. | Principal

Risks of Investing in the Policy |

Not a Short-Term Investment | This Policy is not a short-term

investment and is not appropriate for an investor who needs ready access to cash. The Policy is designed

to provide a Death Benefit. This Policy may not be the right kind of policy if you plan to withdraw money

or surrender your Policy for short-term needs. Withdrawals are not allowed in the first Policy Year. Surrender

Charges apply for up to 10 years after Policy issue and following each Basic Life or LTPR Coverage Layer

added to the Policy. A surrender and withdrawal may be subject to negative tax consequences, including

a potential 10% federal income tax penalty if taken before age 59½. If there is a reduction in the

Face Amount of a Basic Life Coverage Layer or LTPR Coverage Layer, including decreases due to withdrawals,

the Surrender Charge for the affected Coverage Layer will not change | Principal Risks of Investing

in the Policy Changing the Face Amount Surrendering Your Policy |

Risks

Associated with Investment Options | An

investment in this Policy is subject to the risk of poor investment performance and can vary depending

on the performance of the Investment Options available under the Policy (e.g. the Variable Investment

Options). Each Investment Option (including any Fixed Option or Indexed Fixed Option) will

have its own unique risks. You should review, working with your financial professional,

the Investment Options before making an investment decision. | Principal Risks of Investing in the Policy Investment

Options - Fixed Options Investment Options - Indexed Fixed Options Appendix:

Funds Available Under the Policy |

Insurance Company Risks | Investment in the Policy

is subject to the risks related to us, and any obligations (including any Fixed Option or Indexed Fixed

Option), guarantees, or benefits are subject to our claims-paying ability. If we experience financial

distress, we may not be able to meet our obligations to you. More information about us, including our

financial strength ratings, is available upon request by calling us at (800) 347-7787 or visiting our

website at www.PacificLife.com. | Principal

Risks of Investing in the Policy About Pacific Life |

Policy Lapse | Your

Policy remains In Force as long as you have sufficient Net Accumulated Value to cover your Policy’s

Monthly Deductions of Policy charges. Insufficient premium payments, poor investment performance, withdrawals,

and unpaid loans or loan interest may cause your Policy to lapse – which means no Death Benefit

will be paid. There are costs associated with reinstating a lapsed Policy and there is no guarantee that

a reinstatement will be approved. | Principal

Risks of Investing in the Policy Lapsing and Reinstatement |

10

| | | |

RESTRICTIONS | LOCATION IN PROSPECTUS |

Investments | Certain

Investment Options described in this prospectus may not be available depending on the broker-dealer through

which the Policy is sold. Transfers between Investment Options are generally limited

to 25 each calendar year. Any transfers to or from the Fixed Account will be counted towards the 25 allowed

each calendar year unless part of a transfer program (for example, the first year transfer service) or

the transfer is from the Fixed Account to an Indexed Fixed Option. Transfers to or from a

Variable Investment Option cannot be made before the seventh calendar day following the last transfer

to or from the same Variable Investment Option. Additional Fund transfer restrictions apply. There is

a $25 fee per transfer in excess of 12 transfers per Policy Year. We do not currently impose this charge.

Under the Fixed Options, there may be frequency, amount and/or percentage limits

on the amount that may be transferred into or out of the Fixed Options. These limits are significantly

more restrictive than those that apply to transfers into or out of the Variable Investment Options. It

may take several Policy Years to transfer your Accumulated Value out of the Fixed Options to the Variable

Investment Options. Additional Fixed Option transfer restrictions apply. Under

the Indexed Fixed Options, once a Segment is created, you cannot transfer out of a Segment until the

end of the Segment Term. Money may be transferred from a Segment for withdrawals and Standard Policy

Loans, however, if the withdrawal or loan was not part of a systematic distribution program, you will

not be able to transfer into an Indexed Fixed Option for a 12-month period. Additional Indexed Fixed

Option transfer restrictions apply. Certain Funds may stop accepting additional

investments into their Fund or may liquidate a Fund. In addition, if a Fund determines that excessive

trading has occurred, they may limit your ability to continue to invest in their Fund for a certain period

of time. We reserve the right to remove, close to new investment, or substitute Funds as

Investment Options. Additionally, we reserve the right to remove or change the Fixed Options and the

Fixed Indexed Options. | Transferring

Among Investment Options and Market-Timing Restrictions Transfer Services Loans Indexed

Fixed Options Appendix: Funds Available Under the Policy Appendix: Financial Intermediary

Variations |

Optional

Benefits | We

offer several optional benefits in the form of a Rider to the Policy that may only be selected at Policy

issue. A Rider may have an additional charge and could be subject to conditions to exercise or underwriting.

Your selection of certain optional Riders may result in restrictions on some Policy benefits. Not all

Riders are available in every state. There are conditions under which an optional benefit may be modified

or terminated by us, as provided in this prospectus. We may stop offering an optional benefit at any

time for new Policy purchases. If you purchased the Flexible Duration No-Lapse Guarantee Rider, at initial purchase

and during the entire time that you own this Rider, you must allocate 100% of the Accumulated Value among

the allowable Investment Options. as indicated under the APPENDIX: FUNDS AVAILABLE UNDER THIS POLICY

– Allowable Investment Options section in this prospectus. Certain

Policy features and benefits described in this prospectus may vary or may not be available depending

on the broker-dealer through which your Policy is sold. | Death Benefits Optional Riders and Benefits Appendix:

Funds Available

Under the Policy Appendix:

State Variations Appendix: Financial Intermediary Variations |

11

| | | |

TAXES | LOCATION IN PROSPECTUS |

Tax

Implications | Consult

with a tax professional to determine the tax implications of an investment in and payments received under

the Policy. Withdrawals may be subject to ordinary income tax and may be subject to tax penalties. Tax

consequences for loans and withdrawals generally differ. There is no additional tax benefit to you if

the Policy is purchased through a tax-qualified plan. | Variable Life Insurance and Your Taxes |

| | | |

CONFLICTS OF INTEREST | LOCATION IN PROSPECTUS |

Investment

Professional Compensation | Some

financial professionals may receive compensation for selling this Policy to you in the form of commissions,

additional cash compensation, and non-cash compensation. We may also provide additional payments in the

form of cash, other special compensation or reimbursement of expenses to the financial professional’s

selling broker dealer. These financial professionals may have a financial incentive to offer or recommend

this Policy over another investment. | Distribution

Arrangements |

Exchanges | Some

financial professionals may have a financial incentive to offer you a new policy in place of the one

you already own. You should only exchange your policy if you determine, after

comparing the features, fees, and risks of both policies, that it is preferable for you to purchase the

new policy rather than continue to own the existing policy. | Policy Exchanges Distribution Arrangements |

OVERVIEW OF THE POLICY

Purpose

The primary purpose of the Policy is to provide

life insurance Death Benefit protection and flexibility for premium payments, and investment selections

to meet your specific life insurance needs. This Policy may be

appropriate if you are looking to provide a Death Benefit for family members or others. Discuss

with your financial professional whether this Policy, its optional benefits and

its Investment Options are appropriate for you, taking into consideration your age,

income, net worth, tax status, insurance needs, financial objectives, investment goals, liquidity needs,

time horizon, risk tolerance and relevant information. Together you

can decide if this Policy is right for you. Also, before you purchase this Policy, you may request a

personalized illustration of your hypothetical future benefits

under the Policy based on your personal characteristics (e.g. age and risk class), Face Amount of your

Policy, Death Benefit Option, Death Benefit Qualification

Test, planned premium, any Rider requested, and historical or hypothetical gross rate(s) of return.

Premiums

After you pay the first premium payment, the Policy gives

you the flexibility to choose the amount and frequency of your additional premium payments

within certain limits. You may schedule your premium payments, referred to as

planned premium, on an annual, semi-annual, quarterly, or monthly basis.

You

are not required to pay any planned premiums. However, payment of insufficient premiums may result in

a lapse of the Policy. There is no guarantee that

your Policy will not lapse even if you pay your planned premium. Your Policy will lapse if the Accumulated

Value, less Total Policy Debt, is not enough to cover

the monthly charge on the day we make the deduction. If this occurs, your Policy will enter its Grace

Period. The Grace Period is 61 days from the date

we send you a notice that explains the sufficient amount to pay to keep your Policy In Force. During

the Grace Period, your Policy will remain In Force and continue

to provide a death benefit. If sufficient premium has not been made within the Grace Period, your Policy

will lapse. You should consider a periodic review of your

Coverage with your financial professional. This Policy offers riders that provide no-lapse protection

for a certain period if rider conditions are met. See

the No-Lapse Guarantee Rider and the Flexible Duration No- Lapse Guarantee Rider in the OTHER

BENEFITS AVAILABLE UNDER THE POLICY section

in this prospectus. Also see the YOUR POLICY’S ACCUMULATED VALUE - Lapsing

and Reinstatement section in this

prospectus.

12

Your Net Premium payments may be allocated to Variable Investment

Options (each of which invests in a corresponding Fund), the Fixed Options which provide

a guaranteed minimum interest rate, and/or Indexed Fixed Options which may credit interest based in part

on the performance of an underlying Index.

Additional information about the Funds is provided in the APPENDIX:

FUNDS AVAILABLE UNDER THE POLICY section in this prospectus.

Federal

tax law puts limits on the premium payments you can make in relation to your Policy’s Death Benefit.

We may refuse all or part of a premium payment you make, or remove

all or part of a premium from your Policy and return it to you under certain circumstances, for example,

if the amount of premium you paid would result

in your Policy no longer qualifying as life insurance or becoming a Modified Endowment Contract under

the Tax Code.

Policy

Features

Death Benefit

While the Policy is In Force, we will pay Death

Benefit Proceeds to the Beneficiary upon the death of the Insured. The Death Benefit Proceeds equal the

Death Benefit plus any additional benefit provided by a rider less any outstanding

loan or unpaid Policy charges. You may choose between three Death Benefit

Options:

● Option

A – the Total Face Amount of the Policy,

● Option B – the Total Face Amount of the

Policy plus the Accumulated Value, or

● Option C – the Total Face Amount of the

Policy plus the total premiums that have been paid, less any withdrawals or distributions that reduce

your Accumulated Value.

Policy

charges vary depending on which Death Benefit Option or Death Benefit Qualification Test is selected.

Withdrawals

You can withdraw part of the Accumulated Value starting on

your Policy’s first anniversary (no withdrawals may be made during the first year of the Policy

but the Policy may be surrendered during the first year). Each withdrawal must

be at least $200 and after a withdrawal, the remaining Accumulated Value less

any loan amount must be at least $500. Making a withdrawal may have tax consequences, increase the risk

of the Policy lapsing, and reduce Policy values and the Death Benefit,

perhaps significantly. Withdrawals may also be subject to a charge of $25 per withdrawal, but we are

not currently imposing this charge. Withdrawals

from an Indexed Account may result in a Lockout Period where no transfers into an Indexed Account can

occur for a 12-month period.

Surrender

You

can surrender your Policy at any time while the Insured is alive. Any outstanding loan, loan interest,

or Surrender Charge will be deducted and surrender proceeds

will be paid in a single lump sum check. Upon surrender, you will have no life insurance Coverage or

benefits under this Policy. The surrender proceeds, or a portion of,

may be subject to tax consequences, including a possible tax penalty on Modified Endowment Contract policies

for certain situations including, but

not limited to surrendering a policy owned by a natural person(s) before age 59 ½. Please consult

your tax advisor.

Loans

You can borrow money from us any time after

the Free Look Transfer Date to gain access to the Accumulated Value in the Policy. The maximum amount

available to borrow is less than 100% of your Accumulated Value. There are two

loan types that are available. The Standard Loan under your Policy and the Alternate

Loan available by rider. Generally, the minimum amount you can borrow is $200 for a Standard Loan and

$200 for an Alternate Loan. Loans may have tax consequences. See

the APPENDIX: STATE LAW VARIATIONS section in this prospectus

for a list of state variations to the minimum loan amount.

A Standard Loan is available based on the Accumulated

Value allocated to any of the Investment Options (including the Indexed Accounts). An Alternate

Loan is only available based on the Accumulated Value allocated to certain Indexed

Accounts (referred to as Designated Accounts for Alternate Loan purposes)

and is not available until Policy Year 3. Standard Loans using the Accumulated Value in an Indexed Account

may result in a Lockout Period where no transfers into an Indexed

Account can occur for a 12-month period.

When

you borrow money from us under a Standard Loan, we use your Policy’s Accumulated Value as security.

You pay interest on the amount you borrow which is due on your Policy

Anniversary. The Accumulated Value set aside to secure your loan is transferred to a Standard Loan Account

which earns interest daily. Taking out

a Standard Loan, whether or not you repay it, will affect the growth of your Policy’s Accumulated

Value since the amount used to secure the loan will not

participate in the investment experience of the Investment Options, will not be available to pay any

Policy charges, may increase the risk of the Policy lapsing,

and could reduce the amount of the Death Benefit. When you borrow money from us under an Alternate Loan,

we

13

use the Accumulated

Value in the Designated Accounts but the amount borrowed remains in the Indexed Accounts subject to the

performance of that applicable Designated Account. We keep

track of the amount borrowed as Alternate Loan Value and there is no loan interest earned for the amount

tracked by that value. However, you pay

interest on the amount you borrow which is due on your Policy Anniversary.

Optional Benefits

The

Policy offers the following Investment Option transfer services at no additional cost: dollar cost averaging,

portfolio rebalancing, first year transfer, Fixed Option interest sweep,

and the Scheduled Indexed Transfer program. You may only participate in one transfer service at any time.

You can find additional information about

the transfer services in the OTHER BENEFITS AVAILABLE UNDER THE POLICY section

in this prospectus.

The Policy

offers several riders (some for an additional charge) that provide supplemental benefits under the Policy.

Your financial professional can help you determine if any of these

riders are suitable for you. These riders may not be available in all states.

Any

charges associated with each rider are presented in the FEE

TABLES section in this prospectus.

Riders

available:

| | |

Alternate

Loan Rider 3 | Premier Chronic Illness Rider |

Conversion Rider | Premier Living Benefits Rider 2 |

Flexible Duration No-Lapse

Guarantee Rider | Premier LTC Rider |

Long

Term Performance Rider | Scheduled

Annual Renewable Term Rider |

Minimum Indexed Benefit Rider | Surrender Value Enhancement Rider 3 |

No-Lapse Guarantee Rider | Terminal Illness Rider |

Overloan Protection 3 Rider | |

You can

find additional information about the riders in the OTHER BENEFITS AVAILABLE UNDER

THE POLICY and OPTIONAL RIDERS AND

BENEFITS sections in this prospectus.

FEE TABLES

The following

tables describe the fees and expenses that you will pay when buying, owning, and surrendering or making

withdrawals from the Policy. Please refer to your

Policy Specifications page for information about the specific fees you will pay each year based on the

options you have elected.

The first table describes the fees and expenses that you will

pay at the time you buy the Policy, surrender or make withdrawals from the Policy, or transfer

Accumulated Value between Investment Options.

| | | |

| | TRANSACTION FEES |

CHARGE | WHEN CHARGE IS DEDUCTED | AMOUNT DEDUCTED |

Maximum

Sales Charge Imposed on Premiums (Load)

Basic

premium load

| Upon

receipt of premium5 | 6.90% of basic premium |

Surplus premium load | Upon receipt of premium that exceeds the Premium band amount5 | 20.00%

of surplus premium |

Internal premium load | Upon receipt of a replacement or conversion of a policy you have

with us5 | 6.90% of internal premium |

14

| | | |

Maximum Surrender Charge1 | Upon full surrender of the Policy, a Surrender Charge applies for

10 Policy Years from Policy issue and applies for 10 Policy

Years from the Coverage Layer Date for each Basic Life

Coverage increase. In addition,

if you elect LTPR, upon full surrender of the Policy

while the LTPR is in effect, a Surrender Charge applies

for 10 Policy Years from Policy issue and for 10 Policy

Years from the Coverage Layer Date for each additional

LTPR Coverage Layer increase.2 | $17.10 per $1,000 of Basic Face Amount $57.00 per $1,000 of LTPR Face Amount |

LTPR Termination Charge3 | Upon terminating the LTPR while the Policy remains In Force,

a Termination Charge applies for 10 Policy Years from Policy

issue and following each additional LTPR Coverage Layer. | $57.00 per $1,000 of LTPR Face

Amount |

Withdrawal charge (including

any withdrawals under the Automated Income Program)4 | Upon partial withdrawal of Accumulated Value | $25 per withdrawal |

Transfer fees4 | Upon transfer of Accumulated Value between Investment Options | $25 per transfer in excess of 12 per Policy Year |

Illustration request4 | Upon request of Policy illustration in excess of 1 per year | $25 per request |

Face Amount Increase4 Administrative charge for increase in Face Amount of LTPR

or SVER Coverage | Upon effective date of requested Face Amount increase | $100 per request |

Terminal Illness Rider Processing Charge4 | Upon approval of specific request | $100 per request |

Overloan Protection 3 Rider Minimum and Maximum guaranteed charge Charge for a representative Insured | At exercise of benefit | 1.12%-4.52% of Accumulated Value on date of exercise6 Maximum guaranteed charge for a male standard

non tobacco who exercises the Rider at Age 85 is

3.1% of Accumulated

Value on date of exercise3 |

1

2

3

4

5

6

We offer different underwriting methods such as guaranteed

issue, simplified issue, or regular issue. The cost of

15

insurance rates are generally higher

if guaranteed issue or simplified issue are used, than if the Policy is issued through regular underwriting.

As a result, a healthy individual who uses regular issue for

the Policy may pay lower cost of insurance rates than if the individual uses guaranteed or simplified

issue.

The

next table describes the fees and expenses that you will pay periodically during the time you own the Policy, not including Fund fees

and expenses.

| PERIODIC CHARGES OTHER THAN FUND OPERATING EXPENSES |

| CHARGE | WHEN CHARGE IS DEDUCTED | AMOUNT DEDUCTED |

| Base Policy Charges: |

| Cost of Insurance1,2 Minimum and Maximum guaranteed charge Minimum and Maximum current charge Charge for a representative Insured | Monthly

Payment Date | $0.01 - $83.34 per $1,000 of Net Amount At Risk

$0.01 - $83.34 per $1,000 of Net Amount At Risk

Maximum guaranteed charge during Policy Year 1 is $0.22 per $1,000 of Net Amount At Risk for a male standard non tobacco who is Age 45 at Policy issue3

Current charge during Policy Year 1 is $0.05 per

$1,000 of Net Amount At Risk for a male standard non tobacco who is Age 45 at Policy issue3 |

| Administrative charge1 Maximum guaranteed and current charge | Monthly Payment Date | $10.00 |

| Asset charge1 Maximum guaranteed charge Current charge | Monthly Payment Date | Maximum guaranteed charge is 0.36% annually (0.03%

monthly) of unloaned Accumulated Value

Current charge is 0.15% annually (0.0125% monthly)

of unloaned Accumulated Value |

| Indexed Fixed Option charge1 Maximum guaranteed charge Current charge | Monthly Payment Date | Maximum guaranteed charge is 3% annually (0.25% monthly) of Accumulated Value allocated to the 1-Year High Cap Plus Indexed Account)

Current charge is 3% annually (0.25% monthly) of Accumulated Value allocated to the 1-Year High Cap Plus Indexed Account)

|

| Coverage charge1,4 Minimum and Maximum guaranteed charge Minimum and Maximum current charges Charge for a representative Insured | Monthly Payment Date, beginning on effective date of each Basic Life Coverage Layer | $24.50 per Policy plus $0.18 - $11.99 per $1,000 of Basic Life Coverage Layer $7.35 - $24.50 per Policy plus $0.02 - $4.55 per $1,000 of Basic Life Coverage Layer Maximum guaranteed charge during Policy Year 1 is $24.50 per Policy plus $0.76 per $1,000 of Basic Life Coverage Layer for a male standard non tobacco who is Age 45 at Policy issue, with Death Benefit Option A3. Current charge during Policy

Year 1 is $15.00 per Policy plus $0.52 per $1,000 of Basic Life Coverage Layer for a male standard non tobacco who is Age

45 at Policy issue, with Death Benefit Option A3 |

| |

Optional

Benefit Charges7: |

16

| | | |

Standard Loan interest charge Maximum guaranteed and current charge | Policy Anniversary | 2.25% of Policy’s Standard Loan Account balance annually5 |

Alternate Loan Rider 3 Interest charge Maximum guaranteed charge | Policy Anniversary | Maximum guaranteed rate is 8% (0.67% monthly)

of the Alternate Loan Value balance

annually6 |

Long Term

Performance Rider Cost

of Insurance1,2 Minimum

and Maximum guaranteed charge Minimum

and Maximum current charges

Charge

for a representative Insured

Coverage

charge1,4

Minimum

and Maximum guaranteed charge Minimum

and Maximum current charges

Charge

for a representative Insured |

Monthly

Payment Date

Monthly

Payment Date

| $0.01-$83.34 per $1,000 of Net Amount At Risk $0.01-$83.34 per $1,000 of Net Amount At Risk

Maximum

guaranteed charge during Policy Year 1 is $0.22 per $1,000 of Net Amount

At Risk for a male standard non tobacco who is Age 45 at Policy issue3 Current charge during Policy Year 1 is $0.05 per $1,000 of Net Amount At Risk for

a male standard non tobacco who is Age 45 at Policy issue3 $0.18-$12.79 per $1,000 of Rider Coverage Layer $0.01-3.19 per

$1,000 of Rider Coverage Layer Maximum

guaranteed charge during Policy Year 1 is $0.80 per $1,000 of Rider Coverage

Layer for a male standard non- tobacco who is Age 45 at Policy issue with

Death Benefit Option A3 Current

charge during Policy Year 1 is $0.35 per $1,000 of Rider Coverage Layer

for a male standard non tobacco who is Age 45 at Policy issue with Death Benefit

Option A3 |

Surrender Value Enhancement Rider 3 Cost

of Insurance1, 2 Minium

and Maximum guaranteed charge

Minimum

and Maximum current charge

Charge

for a representative Insured Coverage

charge1, 4 Minimum

and Maximum guaranteed

Minimum

and Maximum and current charge

Charge

for a representative Insured |

Monthly Payment Date

Monthly

Payment Date

| $0.01-$83.34

per $1,000 of Net Amount At Risk $0.01-$83.34

per $1,000 of Net Amount At Risk

Maximum

guaranteed charge during Policy Year 1 is $0.22 per $1,000 of Net Amount

At Risk for a male standard non tobacco who is Age 45 at Policy issue3

Current charge during Policy Year 1 is $0.06 per $1,000 of

Net Amount At Risk for a male standard non tobacco

who is Age 45 at Policy issue3

$0.00 - $12.32

per $1,000 of Rider Coverage Layer

$0.00

- $4.88 per $1,000 of Rider Coverage Layer

Maximum

guaranteed and current charge during Policy Year 1 is $0.00 per

$1,000 of

Rider Coverage Layer for a male standard non tobacco who is Age 45 at Policy

issue 3

|

Flexible Duration No-Lapse

Guarantee Rider Minimum

and Maximum guaranteed charge

Minimum and Maximum current charge

Charge

for a representative Insured

| Monthly

Payment Date | $0.02-$1.10 per $1,000 of Net Amount At Risk9

$0.02-$1.10 per $1,000 of Net Amount At Risk9

Maximum

guaranteed and current charge is $0.10 per $1,000 of Net Amount

At Risk at the end of Policy Year 1 for a male

standard non tobacco who is Age 45 at Policy

issue3

|

17

| | | |

Scheduled Annual Renewable Term Rider Cost of Insurance1,2 Minimum and Maximum guaranteed charge

Minimum

and Maximum current charge Charge

for a representative Insured Coverage

charge1,4 Minimum

and Maximum guaranteed charge

Minimum

and Maximum current charges

Charge

for a representative Insured

| Monthly Payment Date | $0.01-83.34 per $1,000 of Net Amount

At Risk

$0.01-83.34

per $1,000 of Net Amount At Risk

Maximum

guaranteed charge during Policy Year 1 is $0.80 per $1,000 of Net Amount

At Risk for a male standard non tobacco who is Age 45 at Policy issue3

Current charge during Policy Year 1 is $0.00

per $1,000 of Net Amount At Risk for a

male standard non tobacco who is Age 45 at Policy issue3

$0.18-$12.79 per $1,000 of Rider Coverage

Layer

The current

Coverage charge for this Rider is $0.00

Maximum

guaranteed charge during Policy Year 1 is $0.80 per $1,000 of Rider Coverage

Layer for a male standard non- tobacco who is Age 45 at Policy issue with

Death Benefit Option A3

|

Premier LTC

Rider Minimum

and Maximum guaranteed charge

Minimum

and Maximum current charge

Charge

for a representative Insured | Monthly

Payment Date | $0.02-$1.87

per $1,000 of LTC Net Amount at Risk9

$0.01-$1.15

per $1,000 of LTC Net Amount at Risk9

Maximum

guaranteed charge is $0.20 per $1,000 of LTC Net Amount

at Risk for a male, who is Age 45 at

Policy issue3

Current

charge is $0.07 per $1,000 of LTC Net Amount

at Risk for a single male, who is

Age 45 at Policy issue with a 2% benefit3

|

Premier

Chronic Illness Rider Minimum

and Maximum guaranteed charge

Charge

for a representative Insured

Minimum

and Maximum current charge

Charge

for a representative Insured

| Monthly

Payment Date | $0.09-$1.70

per $1,000 of Rider Net Amount at Risk9

Maximum guaranteed charge is $0.28 per

$1,000 of Rider Net Amount at Risk for a single

male, who is Age 45 at Policy issue with a 2.0% benefit3

$0.01-$1.24 per $1,000 of Rider Net Amount at Risk9

Current charge is $0.10 per

$1,000 of Rider Net Amount At Risk for a single male, who is

Age 45 at Policy issue with a 2.0% benefit3

|

1.

2.

3.

4.

18

5.

6.

7.

The next item shows the minimum

and maximum total operating expenses charged by the Fund that you pay periodically during the time that

you own the Policy. A complete list of Funds available under the

Policy, including their annual expenses, may be found at the back of this document in the

APPENDIX: FUNDS AVAILABLE UNDER THE POLICY.

Annual Fund Expenses

| | | | | |

| | | Minimum | | Maximum |

Expenses that are deducted from Fund assets, including management fees, distribution

and/or service (12b-1) fees, and other expenses. | | 0.03% | | 1.10% |

PRINCIPAL RISKS OF INVESTING IN THE POLICY

Risk of Loss

You

can lose money by investing in this Policy, including loss of principal and previous earnings. The Policy

is not a deposit or obligation of, or guaranteed or endorsed

by any bank. It is not federally insured by the Federal Deposit Insurance Corporation (FDIC), the Federal

Reserve Board, or any other government agency.

Unsuitable as Short-Term Savings Vehicle (Surrender

and Withdrawal Risk)

The

Policy provides life insurance and is not intended to be used as a short-term investment and is not appropriate

for an investor who needs ready access to cash. The Policy is designed to provide a Death Benefit. The

Policy may be inappropriate for you if you do not have the financial ability to keep it in force for

a substantial period of time.

The Policy may not be the

right kind of policy for you if you plan to withdraw money or surrender your Policy for short-term needs.

A surrender will terminate the Policy and all of its benefits. Withdrawals cannot be taken until after

first year of the Policy and may be subject to a withdrawal fee. A withdrawal will reduce your Accumulated

Value and may significantly reduce the value of the Death Benefit or benefit Riders under the Policy,

potentially by more than the amount withdrawn, and could even terminate a benefit Rider. Withdrawals

may also significantly increase the risk of lapse.

If you

invest in the Indexed Accounts and you surrender your Policy before Segment Maturity, no interest will

be paid and you will forfeit any Segment Indexed Interest we would have otherwise credited. Once

a Segment is created, if money is transferred from the Segment for a withdrawals or Standard Loans, a

Lockout Period will apply if the withdrawal or Standard Loan is not part of a Systematic Distribution

Program. Once a Lockout Period begins, an investor may not make any transfers into the Indexed Fixed

Options for 12 months.

Surrender Charges reduce

the Cash Surrender Value of your Policy. Surrender Charges apply for up to 10 Policy Years after Policy

issue for any at-issue Basic Coverage or LTPR Coverage, and after the Coverage Layer Date for any added

Basic or LTPR Coverage Layer. A surrender and withdrawal may be subject to negative tax consequences,

including a potential 10% federal income tax penalty if taken before age 59½. Any decrease in the

Face Amount of Basic Life or LTPR, including a decrease due to withdrawals, does not reduce the Coverage

Charge or the Surrender Charge for the reduced Coverage Layer.

Please

discuss your insurance needs and financial objectives with your life insurance producer. Together you

can decide if the Policy

19

and any optional Riders are right for you. We are a variable

life insurance policy provider. We do not give advice or make recommendations regarding insurance or

investment products and are not a fiduciary.

Policy

Lapse

Your Policy

remains In Force as long as you have sufficient Net Accumulated Value to cover your Policy’s Monthly

Deductions. Insufficient premium payments, fees and expenses, poor investment performance, withdrawals,

and unpaid loans or loan interest may cause your Policy to lapse – which means no Death Benefit

or other benefits will be paid. There are costs associated with reinstating a lapsed Policy. There is

no guarantee that your Policy will not lapse even if you pay your planned premium. You should consider

a periodic review of your Policy with your life insurance producer.

Before

your Policy lapses, there is a Grace Period. The Grace Period gives you 61 days to pay enough additional

premium to keep your Policy In Force and to prevent your Policy from lapsing. The 61-day period begins

on the date we send notice that your Policy’s Net Accumulated Value is not enough to pay the Policy’s

Monthly Deductions.

The Policy may be eligible

for the No-Lapse Guarantee Rider or the Flexible Duration No-Lapse Guarantee Rider that may help prevent

the Policy from lapsing. See No-Lapse Guarantee Rider and Flexible Duration No-Lapse Guarantee Rider

in the OTHER BENEFITS AVAILABLE UNDER THE POLICY section in this prospectus.

If the Policy lapses, you have three years from the end of the Grace Period to

apply for reinstatement. Evidence of insurability is required when you apply for reinstatement and there

is no guarantee that reinstatement will be approved. The costs associated with reinstating a lapsed Policy

include sufficient net premium to:

• cover all due and unpaid Monthly Deductions

and loan interest charges that accrued during the Grace Period;

• keep

the Policy in force for three months after the date of reinstatement, and

• cover

any negative Accumulated Value if there was a policy loan or other outstanding debt at the time of lapse.

If the Policy is reinstated, the same

Risk Class(es) in use at the time of lapse will apply to the reinstated Policy.

Limitations

on Access to Accumulated Value through Withdrawals

Withdrawals

under the Policy are available starting on the first Policy Anniversary. Each withdrawal must be at least

$200. We will not accept a withdrawal request if the withdrawal

will cause the Policy to become a Modified Endowment Contract (MEC), unless you have told us In Writing

that you desire to have your Policy become a MEC.

See the Tax Implications section below for additional information on

MECs.

Risks Associated with Variable

Investment Options

You

should consider the Policy’s Investment Options as well as its costs. Your investment is subject

to the risk of poor investment performance and can vary depending on the performance of the Variable

Investment Options you have chosen. Each Variable Investment Option will have its own unique risks. The

value of each Variable Investment Option will fluctuate with the value of the investments it holds, and

returns are not guaranteed. You can lose money by investing in the Policy, including loss of principal.

You bear the risk of any Variable Investment Options you choose. You should read each Fund prospectus

carefully before investing. You can obtain a Fund prospectus by contacting your life insurance producer

or by visiting https://pacificlife.com/prospectuses. No assurance can be given that a Fund will achieve

its investment objectives.

We may add or remove Investment

Options at any time, and removal of Variable Investment Options may limit the number of such options

that are available to an investor under the

Policy in the future. We may significantly reduce the number of Variable Investment Options, including

reducing them to a single option. If, in the future,

an investor is not satisfied with the Variable Investment Options, they may choose to surrender their

Policy, but they may be subject to Surrender Charges, taxes,

and tax penalties. If they purchase another investment vehicle, it may have different features, fees,

and risks than the Policy. Investors should discuss

with their financial professional if the Policy is appropriate for them given the Company’s right

to make changes to the Investment Options.

Risks Associated with Policy Loans

When you borrow money from your Policy, we use your Policy’s

Accumulated Value as security. You pay interest, which accrues at the Loan

Account Charge Interest Rate, on the amount you borrow. Accrued interest is due on your Policy Anniversary.

Under a Standard Loan, the Accumulated Value set aside to secure your loan is transferred to a Loan Account

which earns interest daily at the Loan Account Credit Interest Rate. Taking out

a Standard Loan, whether or not you repay it, will affect the growth of your Policy’s Accumulated

Value since the amount used to secure the loan will not participate

in the investment experience of the Investment Options, will not be available to pay any Policy charges,

may increase the risk of the Policy lapsing, and could reduce

the amount of the Death Benefit.

Risks Associated

with the Fixed Options

20

Under the Fixed Options, there may be frequency, amount and/or

percentage limits on how much may be transferred from the Fixed Options. These limits are

significantly more restrictive than those that apply to transfers out of the Variable Investment Options

and it may take several Policy Years to transfer your Accumulated Value out of the Fixed Options to the

Variable Investment Options. Such restrictions on transfers from the Fixed Options may prevent you

from reallocating your Accumulated Value at the times and in the amounts that