As filed with the Securities and Exchange Commission on July 17, 2026

Preliminary Offering Circular dated July 17, 2026

An offering statement pursuant to Regulation A relating to these securities has been filed with the Securities and Exchange Commission. Information contained in this Preliminary Offering Circular is subject to completion or amendment. These securities may not be sold nor may offers to buy be accepted prior to the time an offering circular that is not designated as a Preliminary Offering Circular is delivered and the offering statement filed with the Commission becomes qualified. This Preliminary Offering Circular shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sales of these securities in any state in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the laws of any such state. We may elect to satisfy our obligation to deliver a Final Offering Circular by sending you a notice within two business days after the completion of our sale to you that contains the URL where the Final Offering Circular or the offering statement in which such Final Offering Circular was filed may be obtained.

NOYACK LOGISTICS INCOME REIT II, INC.

Shares of Common Stock

$1,000,000 Minimum Offering Amount

$75,000,000 Maximum Offering Amount

Noyack Logistics Income REIT II, Inc., a Maryland corporation (“NREIT II,” the “Company,” “we,” “our,” or “us”), is offering up to $75,000,000 in shares (the “Shares”) of its common stock (the “Common Stock”) upon the terms and subject to the conditions set forth in this offering circular. NREIT II intends to focus, either directly or through special purpose entities or joint ventures with other entities, including affiliates of the Company, on the acquisition, renovation, leasing and management of a diversified portfolio of commercial real estate properties that encompass the supply chain and logistics infrastructure of North America, including dry warehouses, cold storage warehouses, life sciences buildings, and structured parking garages.

NREIT II intends to qualify as a real estate investment trust, or REIT, commencing with its taxable year ending December 31, 2027, and is structured as an umbrella partnership REIT, commonly called an “UPREIT.” As an UPREIT, NREIT II will own substantially all of its assets and conduct substantially all of its operations through NL REIT II OP, LP, its operating partnership (the “Operating Partnership”). NREIT II, as the sole general partner of the Operating Partnership, has exclusive control over the Operating Partnership. NREIT II is externally managed, meaning its day-to-day operations are managed by its external manager, Noyack Capital LLC (the “Manager” or “NOYACK”).

The Shares are being initially offered at a price of $20.00 per Share, a price that was arbitrarily determined by the Manager, until 12 months after the initial closing of this offering; however, the board of directors of the Company may decide to commence adjusting the Transaction Price (as defined below) at an earlier time in its sole discretion. Thereafter, the per Share purchase price will be adjusted every fiscal quarter as of January 1st, April 1st, July 1st, and October 1st of each year and will equal the sum of our net asset value, or NAV, divided by the number of Shares outstanding (on an as converted basis, assuming all the units of limited partnership of the Operating Partnership (“OP Units”) were converted as of the determination date) as of the end of the prior fiscal quarter (“NAV per Share”). The $20.00 per Share or NAV per Share, as applicable, is referred to in this offering circular as the “Transaction Price.” See “Plan of Distribution—Purchase Price per Share” for an explanation as to how the NAV will be calculated.

We will commence this offering promptly following the qualification of the offering statement of which this offering circular forms a part and will continue until December 31, 2027 (with a one-year extension at the sole discretion of NREIT II) or such earlier time as all the Shares have been sold or NREIT II ceases offering Shares at its sole discretion. NREIT II is offering a minimum of $1,000,000 of Shares and a maximum of $75,000,000 of Shares. Subscription proceeds will be held in escrow in a segregated account until closing. The minimum investment for initial purchases is $500, or 25 Shares based on the initial Transaction Price of $20.00 per Share. We will contribute the net proceeds from this offering to our Operating Partnership in exchange for OP Units.

The Shares will be offered primarily directly by NREIT II’s and the Manager’s officers on an ongoing and continuing basis. NREIT II may engage broker-dealers, who are members of FINRA, to sell the Shares.

This offering is intended to qualify as a “Tier 2” offering pursuant to Regulation A promulgated under the Securities Act of 1933, as amended, or the Securities Act. In preparing this offering circular, the Company has elected to comply with the offering circular disclosure requirements specified in Form 1-A under Regulation A.

Because this offering is being conducted pursuant to Regulation A under the Securities Act, the Company is subject to reduced reporting requirements than otherwise required for registration statements filed under the Securities Act. Consequently, investors in this offering will have less information about the Company than would be available regarding an issuer of registered securities. This lack of information may make it more difficult for an investor to evaluate an investment in the Shares. See “Risk Factors — We are subject to reduced reporting requirements which may make it more difficult for investors to evaluate an investment in the Shares.”

Generally, no sale may be made to you in this offering if the aggregate purchase price you pay is more than 10% of the greater of your annual income or net worth. Different rules apply to accredited investors and non-natural persons. Before making any representation that your investment does not exceed applicable thresholds, we encourage you to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage you to refer to www.investor.gov.

Investing in the Shares involves a high degree of risk, including material income tax risks and risks arising from potential conflicts of interest between the Manager and the Company. See “Risk Factors” beginning on page 10 for risks you should consider before buying the Shares. You should purchase these securities only if you can afford a complete loss of your investment.

NEITHER THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION NOR ANY STATE SECURITIES REGULATOR HAS PASSED UPON THE MERITS OF OR GIVEN ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERMS OF THIS OFFERING, NOR DO ANY OF THEM PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SELLING LITERATURE. THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION; HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED ARE EXEMPT FROM REGISTRATION. ANY REPRESENTATION TO THE CONTRARY IS UNLAWFUL.

| Price to public | Placement agent fees | Proceeds to us (2) | ||||||||||

| Per Share | $ | 20.00 | (1 | ) | $ | 20.00 | ||||||

| Total minimum | $ | 1,000,000 | (1 | ) | $ | 1,000,000 | ||||||

| Total maximum | $ | 75,000,000 | (1 | ) | $ | 75,000,000 | ||||||

| (1) | The Company has not retained any placement agent to engage in sales of the Shares. |

| (2) | Does not include other expenses of this offering, including organizational expenses and various offering costs including expenses associated with marketing this offering, which are estimated to be at least $150,000, exclusive of state filing fees. |

This Offering Circular follows the Offering Circular disclosure format.

The date of this offering circular is July 17, 2026

IMPORTANT INFORMATION ABOUT THIS OFFERING CIRCULAR

In this offering circular, Noyack Logistics Income REIT II, Inc. is referred to as “NREIT II,” “the Company,” “we,” “us,” or “our.” Noyack Capital LLC is referred to as the “Manager.”

Please carefully read the information in this offering circular and any accompanying offering circular amendments and supplements, which we refer to collectively as the offering circular. You should rely only on the information contained in this offering circular. We have not authorized anyone to provide you with different information. This offering circular may only be used where it is legal to sell these securities. You should not assume that the information contained in this offering circular is accurate as of any date later than the date hereof or such other dates as are stated herein or as of the respective dates of any documents or other information incorporated herein by reference.

This offering circular is part of an offering statement that we filed with the Securities and Exchange Commission (the “SEC”), using a continuous offering process. The offering statement we filed with the SEC includes exhibits that provide more detailed descriptions of the matters discussed in this offering circular. You should read this offering circular, and the related exhibits filed with the SEC and any offering circular supplement, together with additional information contained in our annual reports, semi-annual reports and other reports and information statements that we will file periodically with the SEC. See the section entitled “Additional Information” below for more details.

We are offering to sell, and seeking offers to buy, the Shares only in jurisdictions where such offers and sales are permitted. The information contained in this offering circular is accurate only as of its date, regardless of the time of its delivery or of any sale or delivery of our securities. Neither the delivery of this offering circular nor any sale or delivery of the Shares shall, under any circumstances, imply that there has been no change in our affairs since the date of this offering circular. This offering circular will be updated and made available for delivery to the extent required by the federal securities laws.

The offering circular and all supplements and reports that we have filed or will file in the future can be read at the SEC website, www.sec.gov.

The Manager will be permitted to make a determination that a purchaser of Shares in this offering is a “qualified purchaser” in reliance on the information and representations provided by the investor regarding the investor’s financial situation. Before making any representation that an investment does not exceed applicable thresholds, we encourage investors to review Rule 251(d)(2)(i)(C) of Regulation A. For general information on investing, we encourage investors to refer to www.investor.gov.

| -i- |

TABLE OF CONTENTS

| -ii- |

In order to comply with the investor qualification requirements applicable to Tier 2 offerings under Regulation A, purchasers of Shares in this offering must qualify as “qualified purchasers” within the meaning of Regulation A. The following summary describes the principal investor qualification standards applicable to this offering. Prospective investors should carefully review these requirements and consult their own legal, tax and financial advisors regarding their eligibility to invest.

The Shares are being offered and sold only to “qualified purchasers” (as defined in Regulation A under the Securities Act of 1933, as amended (the “Securities Act”)). As a Tier 2 offering pursuant to Regulation A under the Securities Act, this offering will be exempt from state law “Blue Sky” review, subject to meeting certain state filing requirements and complying with certain anti-fraud provisions, to the extent that the Shares offered hereby are offered and sold only to “qualified purchasers.” In order to be a “qualified purchaser,” a purchaser of Shares must satisfy one of the following:

| (1) | Non-Accredited Investors: If you are not an accredited investor (as defined below), your investment in Shares may not be more than 10% of the greater of: |

| (a) | If you are a natural person: |

| i. | your individual net worth, or joint net worth with your spouse, excluding the value of your primary residence (as described below); or |

| ii. | your individual income, or joint income with your spouse, received in each of the two most recent years and you have a reasonable expectation that an investment in the Shares will not exceed 10% of your individual or joint income in the current year. |

| (b) | If you are not a natural person, |

| i. | your revenue, as of your most recently completed fiscal year end; or |

| ii. | your net assets, as of your most recently completed fiscal year end. |

For purposes of this definition, “net worth” means the excess of total assets at fair market value over total liabilities, except that the value of the principal residence owned by a natural person will be excluded for purposes of determining such natural person’s net worth. In addition, for purposes of this definition, the related amount of indebtedness secured by the primary residence up to the primary residence’s fair market value may also be excluded, except in the event such indebtedness increased in the 60 days preceding the purchase of our common stock and was unrelated to the acquisition of the primary residence, then the amount of the increase must be included as a liability in the net worth calculation. Moreover, indebtedness secured by the primary residence in excess of the fair market value of such residence should be considered a liability and deducted from the natural person’s net worth. In the case of fiduciary accounts, the net worth and/or income suitability requirements may be satisfied by the beneficiary of the account or by the fiduciary, if the donor or grantor is the fiduciary and the fiduciary directly or indirectly provides funds for the purchase of the Shares; or

| (2) | Accredited Investors: You are an accredited investor. An “accredited investor” is: |

| (a) | If a natural person, a person that has: |

| i. | an individual net worth, or joint net worth with his or her spouse, that exceeds $1,000,000, excluding the value of the primary residence of such natural person (as described below); or |

| ii. | individual income in excess of $200,000, or joint income with his or her spouse in excess of $300,000, in each of the two most recent years and has a reasonable expectation of reaching the same income level in the current year. |

| (b) | If not a natural person, one of the following: |

| i. | a corporation, an organization described in Section 501(c)(3) of the Internal Revenue Code of 1986, as amended (the “Code”), a Massachusetts or similar business trust, or a partnership, not formed for the specific purpose of acquiring Shares, with total assets in excess of $5,000,000; |

| -1- |

| ii. | a trust, with total assets in excess of $5,000,000, not formed for the specific purpose of acquiring the securities offered and whose purchase is directed by a person who has such knowledge and experience in financial and business matters that he or she is capable of evaluating the merits and risks of an investment in a Share; |

| iii. | a broker-dealer registered pursuant to Section 15 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”); |

| iv. | an investment company registered under the Investment Company Act of 1940, as amended (the “Investment Company Act”); |

| v. | a business development company (as defined in Section 2(a)(48) of the Investment Company Act); |

| vi. | a Small Business Investment Company licensed by the United States Small Business Administration under Section 301(c) or (d) of the Small Business Investment Act of 1958; |

| vii. | an employee benefit plan within the meaning of the Employee Retirement Income Security Act of 1974, as amended (“ERISA”), if the investment decision is made by a plan fiduciary (as defined in Section 3(21) of ERISA), which is either a bank, savings and loan association, insurance company, or registered investment adviser, or if the employee benefit plan has total assets in excess of $5,000,000, or, if a self-directed plan, with investment decisions made solely by persons who are accredited stockholders; |

| viii. | a private business development company (as defined in Section 202(a)(22) of the Investment Advisers Act of 1940, as amended (the “Investment Advisers Act”)); |

| ix. | a bank as defined in Section 3(a)(2) of the Securities Act, or any savings and loan association or other institution as defined in Section 3(a)(5)(A) of the Securities Act whether acting in its individual or fiduciary capacity; or |

| x. | an entity in which all of the equity owners are accredited stockholders. |

| (c) | In addition, the SEC has issued certain no-action letters and interpretations in which it deemed certain trusts to be accredited investors, such as trusts where the trustee is a bank as defined in Section 3(a)(2) of the Securities Act and revocable grantor trusts established by individuals who meet the requirements of clause (1)(a)(i) or (1)(a)(ii) of this section. However, these no-action letters and interpretations are very fact specific and should not be relied upon without close consideration of your unique facts. |

We have the right to reject any investor’s subscription in whole or in part only if we determine, in our sole and absolute discretion, that such stockholder is not a “qualified purchaser” for purposes of Regulation A.

| -2- |

STATEMENTS REGARDING FORWARD-LOOKING INFORMATION

This offering circular contains forward-looking statements within the meaning of the federal securities laws. These forward-looking statements relate to future events, future performance, anticipated financial results, business plans, objectives and strategies, and other matters that are not historical facts.

Forward-looking statements may include, among other things, statements regarding our investment objectives and strategy; anticipated acquisitions and dispositions of properties; expected financing arrangements; projected operating results, cash flow and distributions; anticipated net asset value; qualification and taxation as a REIT; future liquidity events; portfolio growth; market opportunities; and our expectations regarding future performance and results of operations.

In some cases, forward-looking statements may be identified by words such as “may,” “should,” “expect,” “intend,” “plan,” “anticipate,” “believe,” “estimate,” “predict,” “project,” “potential,” “continue,” “will,” and similar expressions, including the negative of those terms.

Forward-looking statements are inherently subject to known and unknown risks, uncertainties, assumptions and other factors, many of which are beyond our control. These risks and uncertainties include, among others, changes in general economic conditions; fluctuations in interest rates; inflation; disruptions in the capital markets; the availability and cost of debt financing; real estate market conditions; tenant creditworthiness and occupancy levels; competition; and regulatory and tax law changes.

Forward-looking statements are also subject to risks relating to our business and investment strategy, including our ability to acquire suitable properties on favorable terms, our ability to successfully operate and manage acquired properties, our ability to qualify and maintain qualification as a REIT, and the other risks described in the section entitled “Risk Factors.”

Actual results, performance, achievements and outcomes may differ materially from those expressed or implied by any forward-looking statements. Accordingly, investors should not place undue reliance on forward-looking statements.

Although we believe that the expectations reflected in our forward-looking statements are reasonable, we cannot assure you that such expectations will prove to be correct. No assurance can be given that the future results, performance, achievements or outcomes expressed or implied by any forward-looking statement will be realized.

Except as required by applicable law, we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise, after the date of this offering circular.

| -3- |

The following summary highlights information continued elsewhere in this offering circular and should be read in conjunction with, and is qualified in its entirety by, the detailed information appearing elsewhere in this offering circular. To understand this offering fully, you should read the entire offering circular carefully, including the “Risk Factors” section, before making a decision to invest in our securities.

| Securities Offered: | We are offering up to $75,000,000 in shares of our common stock (collectively, the “Shares”). The Shares will be sold at the then-current Transaction Price. The minimum purchase is 25 Shares, or $500, based on the $20.00 initial Transaction Price). See “Description of Capital Stock” and “The Manager and the Management Agreement.” | |

| Issuer: | We were formed for the purpose of purchasing, either directly or through special purpose entities and joint ventures with other entities, including affiliates of the Company, a diversified portfolio of commercial real estate properties that encompass the supply chain and logistics infrastructure of North America, including dry warehouses, cold storage warehouses, life sciences buildings, and structured parking garages (collectively, the “Properties”). | |

| Properties – Description: | NREIT II intends to use the offering proceeds of this offering (the “Offering Proceeds”) to acquire the Properties. There are no limitations on the number or size of the Properties to be acquired by NREIT II or the percentage of Offering Proceeds that may be invested in a single Property. We are a development stage company and as of the date of this offering circular have engaged in no operations. The total number of Properties acquired by NREIT II will be determined in the sole discretion of the Manager and will depend, in part, on the number of Shares that are sold by NREIT II in this offering, the real estate market and financing conditions and other circumstances outside the control of NREIT II and the Manager.

As of the date of this offering circular, NREIT II has not entered into any binding agreement to acquire any property.

NREIT II’s primary strategy will be to identify and acquire Properties that are either stabilized, providing consistent current income, or represent value-add opportunities to provide for capital appreciation. NREIT II currently intends to seek Properties that have one or more of the following characteristics: (i) relating to or supporting the supply chain and logistics infrastructure of North America, (ii) have current or projected cash flow, (iii) provide a “value-add” opportunity through a combination of redevelopment, expense management and revenue improvement, (iv) located in an established area, (v) favorable location, such as in a high growth area or an area with relatively few competing properties, and (vi) purchase price that is below the replacement cost of the Property, as determined in the Manager’s sole discretion. NREIT II may acquire Properties that do not meet one or more of these criteria. See “Description of the Business.” | |

Properties – Acquisition: |

NREIT II intends to purchase the Properties primarily from unaffiliated sellers; however, the Manager has the discretion to acquire Properties from affiliates of NREIT II. The terms of the purchase and sale agreements are not currently known. It is anticipated that NREIT II will wholly own the Properties either directly or indirectly; however, NREIT II may purchase some of the Properties together with joint venture partners and NREIT II may acquire long-term ground lease interests. See “Our REIT Structure.” | |

| Properties – Financing: | NREIT II anticipates that it will enter into financing arrangements with various third-party lenders to acquire the Properties. Once NREIT II’s portfolio of Properties has been stabilized, the Manager expects that the aggregate loan-to-value ratio for the portfolio of Properties will not exceed a cap of 75% but our optimal leverage ratio is 65%. There can be no assurance that actual leverage levels will remain within these targets. The Manager has not obtained any additional financing commitments beyond the existing financing for any Properties. The terms of the loans to acquire the Properties will vary. It is anticipated that the loans will have terms of five to 10 years and will require balloon payments at the end of the loan term. NREIT II will not incur any recourse indebtedness. |

| -4- |

| Properties – Operations: | It is anticipated that the Properties will be operated by either affiliates of the Manager or third-party property managers hired by the Manager; however, the Manager has the discretion to retain one or more additional or replacement entities to manage the operations at the Properties. The property managers will be entitled to receive a portfolio average fee in an amount up to 3% of gross revenues from each Property the property managers manage (the “Property Management Fee”). The Manager will be entitled to receive an asset management fee in an amount up to 0.75% of the net asset value of NREIT II (the “Asset Management Fee”). | |

| Investment Period: | NREIT II intends to hold and operate the properties for a five (5) to seven (7) year period. While NREIT II expects to seek a liquidity transaction within this time frame, there can be no assurance that an acceptable transaction will be available or that the market conditions for a transaction will be favorable during that time period. As a result, investors may be required to hold their Shares beyond the projected liquidity date. To the extent permitted by applicable REIT regulations, dispositions of individual Properties may be made strategically as needed to maximize both short- and long-term returns. | |

| NREIT II Objectives: | NREIT II’s investment objectives are to generate consistent current income through the acquisition of stabilized Properties with predictable net operating income and to achieve superior risk-adjusted returns principally through acquiring Properties that provide the prospect of significant capital appreciation through value-add opportunities resulting from redevelopment, expense management, and revenue improvement. By targeting properties at opportunistic pricing via acquisition strategies described below, NREIT II intends to implement a disciplined investment strategy that will use a proprietary investment rating system to identify and compare the relative value of a large number of acquisition opportunities across a variety of asset classes in multiple geographic regions.

NREIT II will generally seek to avoid acquisitions that are subject to competitive auction environments. Instead, NREIT II will seek to leverage its relationships with family office owners of logistics properties and developers of logistics properties. NREIT II may pursue forward commitment agreements with developers of logistics properties where management believes such arrangements are commercially attractive and consistent with NREIT II’s investment objectives. With respect to family office property owners, NREIT II will seek to acquire their assets in return for OP Units at pricing that management believes may be attractive to both parties. NREIT II believes these acquisition strategies will enable it to obtain pricing that management believes may improve investment returns, establish long-term relationships with creditworthy tenants, and maximize financing flexibility. | |

| Closings: | The initial closing (the “Initial Closing”) of this offering will occur at such time as NREIT II has received subscription agreements for an aggregate of $1,000,000 of Shares (the “Minimum Amount”). Subscription proceeds will be held in escrow in a segregated account until the Initial Closing; however, investors will not have the right to revoke their subscriptions prior to the Initial Closing. Thereafter, closings will occur on the final business day of each calendar quarter (each, a “Subsequent Closing” and, together with the Initial Closing, the “Closings”). This offering will continue until December 31, 2027 (with a one-year extension at the sole discretion of NREIT II) or such earlier time as all of the Shares have been sold or NREIT II ceases offering Shares at its sole discretion. |

| -5- |

| Our REIT Structure: | We believe that our currently contemplated business operations will enable us to qualify as a REIT beginning with our taxable year ending December 31, 2027. Our qualification and taxation as a REIT depend upon our ability to meet, on a continuing basis, various qualification requirements imposed upon REITs by the Internal Revenue Code of 1986, as amended (the “Code”), relating to, among other things, compliance with the REIT income and asset tests. See “U.S. Federal Income Tax Considerations—Requirements for Qualification as a REIT.” There is no assurance that we will qualify as a REIT or, if qualified, will maintain such qualification in the future. See “Risk Factors—Federal Income Tax Risks.” | |

Manager: |

Noyack Capital LLC, a New York limited liability company, is the manager of NREIT II and will manage and control NREIT II’s affairs. The mailing address of the Manager is 33 Park Place, Suite 400, New York, New York 10007 and its telephone number is (813) 438-6542. See “The Manager and the Management Agreement.” | |

| Experience of the Manager: | The Manager was formed nearly 20 years ago and since inception has acted as a multi-family office providing, among other things, investment and estate planning advice to multiple families and family offices. During this time, the Manager acquired medical/healthcare facilities, single family homes, development properties for multifamily housing, and other unimproved land. The founder and Managing Principal of the Manager is Charles J. (“CJ”) Follini. The management team has an aggregate of over 70 years of experience in the acquisition, ownership and management of commercial properties. See “The Manager and the Management Agreement.” | |

| Compensation to the Manager and its Affiliates: | The Manager and its affiliates are entitled to receive fees, compensation and distributions as set forth below. | |

| The Manager will be entitled to receive a quarterly Asset Management Fee equal to an annualized rate of up to 0.75% of the net asset value of NREIT II. | ||

| The Manager or an affiliate will be entitled to receive a Disposition Fee in an amount up to 1.0% of the gross sales price of each Property in connection with any sale, exchange or other disposition of the applicable Property. | ||

| Cash distributions will be made by NREIT II at such times and in such amounts as determined by our board of directors at its sole discretion. In addition, upon the liquidation of our assets, a merger or other combination into a publicly-traded entity or other liquidity event such as an initial public offering, we will pay the Manager an incentive fee equal to 50% of all returns AFTER (a) the value of the Shares as established in any such transaction, plus the total of all distributions paid by NREIT II to our stockholders from inception until the date such value is determined exceeds (b) the sum of (1) the number of Shares issued multiplied by the issue prices paid by the stockholders (the “Gross Investment Amount”) and (2) the amount of cash flow necessary to generate a 15% internal rate of return on our stockholders’ Gross Investment Amount from our inception through the date such value is determined. This incentive fee may substantially reduce the amount otherwise distributable to stockholders upon a liquidity event. |

| -6- |

| The Manager will be entitled to be reimbursed for organization and offering expenses associated with this offering in an aggregate amount not to exceed Five Hundred Thousand Dollars ($500,000). Organization and offering expenses include the legal, accounting, online presence development, charges of our deposit account and transfer agent, charges of the Manager for administrative services related to the issuance of the Shares in this offering, the reimbursement of bona fide due diligence expenses of broker-dealers, reimbursement of the Manager for costs in connection with preparing supplemental sales materials, the cost of bona fide training and education and education meetings held by NREIT II (primarily the travel, meal and lodging costs of registered representatives of broker-dealers), attendance and sponsorship fees payable to participating broker-dealers hosting retail seminars and travel, and meal and lodging costs for officers and employees of the Manager and its affiliates to attend retail seminars conducted by broker-dealers and promotional items. | ||

| See “Compensation to the Manager and its Affiliates.” | ||

| Use of Proceeds: | The proceeds of this offering, coupled with proceeds from anticipated financings, will be primarily used to acquire the Properties. See “Estimated Use of Proceeds.” | |

| Minimum Purchase: | A minimum purchase of 25 Shares, or $500, based on the $20.00 initial Transaction Price, will be required. See “Plan of Distribution – Capitalization.” | |

| Dividends: | The Company does not expect to declare regular dividends until such time as the Properties it acquires begin to generate positive cash flow. Once commenced, we expect to declare and pay them on a quarterly basis, or less frequently as determined by our board of directors following consultation with the Manager, in arrears. Any dividends we pay will be based on, among other factors, our present and projected future cash flow. We expect that we will set the rate of dividends at a level that will be reasonably consistent and sustainable over time.

The REIT distribution requirements generally require that we make aggregate annual dividend payments to our stockholders of at least 90% of our REIT taxable income, computed without regard to the dividends paid deduction and excluding net capital gain. Moreover, even if we make the required minimum dividends under the REIT rules, we will be subject to U.S. federal income and excise taxes on our undistributed taxable income and gains. As a result, we may make such additional distributions, beyond the minimum REIT distribution, to avoid such taxes. See “Dividend Policy” and “U.S. Federal Income Tax Considerations.”

Any dividends that we pay will directly impact our NAV, by reducing the amount of our assets. Over the course of your investment, your dividends plus the change in NAV (either positive or negative) will produce your total return. | |

| Certain Affiliate Transactions: | Affiliates of the Manager may be retained by NREIT II from time to time, on a non-exclusive basis and on commercially competitive terms, to provide various services in connection with NREIT II’s business, including, without limitation, financial, development, sales and marketing, leasing, and other similar services. Transactions between the Manager or its affiliates and NREIT II will require the Independent Representative’s approval. |

| -7- |

| Reports to Investors: | The Manager will cause to be furnished to the stockholders, within 120 days after the end of each fiscal year, the following: (i) an annual report containing formal audited financial statements of NREIT II; (ii) a statement setting forth any distributions to the stockholders for the last fiscal year; and (iii) a statement of all investments. Such a report will also detail the activities of NREIT II during each fiscal year. NREIT II will also furnish to the stockholders, within 90 days after the close of each semi-annual fiscal period, a report containing a formal unaudited: (i) balance sheet; (ii) statement of income and (iii) cash flow statement. | |

| Indemnification: | The Manager and its affiliates, members, directors, officers, agents, and employees (collectively, “Indemnified Parties”) will not be liable to NREIT II or its direct or indirect subsidiaries or the stockholders for any act or omission on their part, except for any liability primarily attributable to such party’s gross negligence or willful misconduct. NREIT II will indemnify the Indemnified Parties for any loss or damage incurred by them in connection with the performance of their duties, responsibilities and obligations to NREIT II, except for losses which are primarily attributable to their gross negligence or willful misconduct. At the expense of NREIT II, the Manager may purchase general liability insurance to cover the Manager, its principal, CJ Follini, and related persons. | |

| Fiscal Year: | NREIT II’s fiscal year will end on December 31 of each year. | |

Subscription To Purchase Shares:

|

Each prospective Investor who meets the qualifications described in “Investor Suitability” above and desires to purchase any Shares must:

(1) Subscribe for an initial investment in the Shares in an amount of at least $500 (subject to reduction if this offering is over-subscribed or in the sole discretion of the Manager); and

(2) Complete, date, execute and deliver to NREIT II one copy of the Subscription Agreement. | |

| Independent Auditors: | dbbmckennon | |

Additional Information:

|

Each prospective investor will be furnished or given access to any additional information reasonably available or obtainable which may be needed to verify or supplement any information contained herein and in the exhibits hereto or to assist such prospective investor in making an informed decision with respect to an investment in NREIT II. Persons desiring any additional information, copies of documents, or a meeting with a representative of the Manager may contact NREIT II at 33 Park Place, Suite 400, New York, New York 10007; Telephone: (813) 438-6542. |

| -8- |

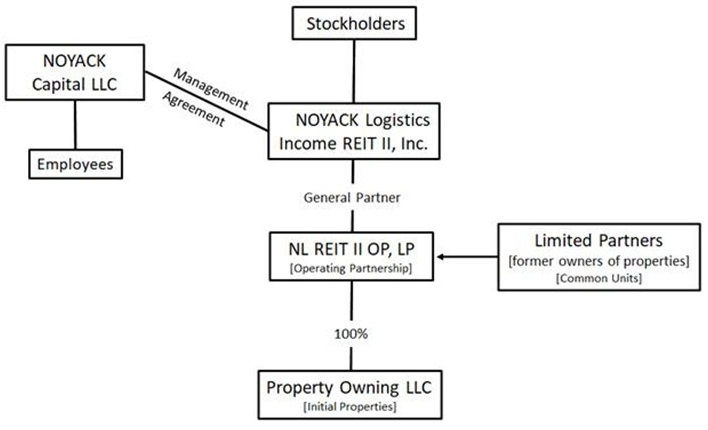

Organizational Chart

The following chart sets forth the organizational structure of NREIT II.

| -9- |

An investment in the Shares involves substantial risks. You should carefully consider the following risk factors in conjunction with the other information contained in this offering circular before purchasing the Shares. The risks discussed in this offering circular could materially and adversely affect our business, operating results, prospects and financial condition. This could cause the value of the Shares to decline and could cause you to lose all or part of your investment. The risks and uncertainties described below represent those risks and uncertainties that we believe are material to our business, operating results, prospects and financial condition as of the date of this offering circular.

Risks Related to NREIT II

We have a limited operating history, no established financing sources and no prior operating results upon which investors may evaluate our future performance.

NREIT II was formed in January 2022 and has a limited operating history. As of the date of this offering circular, we have not acquired any properties or other investments, have not commenced meaningful operations and do not have established financing sources or committed credit facilities. As a result, investors have limited information upon which to evaluate our business, investment strategy and prospects.

Although affiliates of the Manager have experience in commercial real estate investing and asset management, the prior performance of other investment programs sponsored, managed or advised by affiliates of the Manager should not be considered indicative of our future results. Our future performance will depend on numerous factors, many of which are beyond our control.

To be successful, we must raise sufficient capital, identify and acquire suitable investments, establish and expand our operations, attract and retain qualified personnel and compete effectively for investment opportunities and investors. We may not be successful in accomplishing these objectives, and there can be no assurance that we will achieve our investment goals or generate positive operating results.

If we are unable to successfully implement our business strategy, obtain adequate financing or acquire and manage investments effectively, our business, financial condition, operating results and ability to make distributions to holders of Common Stock could be adversely affected, and investors could lose all or a portion of their investment.

There is no public trading market for the Common Stock; therefore, it will be difficult for you to sell your Common Stock. If you are able to sell your Shares, you may have to sell them at a substantial discount from the established offering price.

There is no public market for the Common Stock. In addition, the price you receive for the sale of any Common Stock is likely to be less than the proportionate value of our investments. Therefore, you should acquire the Common Stock only as a long-term investment.

An investment in our Shares should be considered illiquid. Because no public market currently exists for the Common Stock and none may develop in the future, investors should be prepared to hold their Shares for an indefinite period of time. Accordingly, you should not invest in our Shares if you need immediate access to your invested capital or if you are unable to bear the risk of a complete loss of your investment.

Although we have adopted a Stockholder Redemption Plan, the plan is intended to provide limited liquidity only and should not be relied upon as a means of disposing of your Shares promptly or at a desired price. Redemptions will be subject to the terms, conditions, limitations and funding availability set forth in the Stockholder Redemption Plan. In addition, our board of directors may amend, suspend, or terminate the Stockholder Redemption Plan at any time in its sole discretion. As a result, stockholders may be unable to have their Shares redeemed when desired or at all.

| -10- |

We may not be able to successfully operate our business or generate sufficient cash flows to make distributions to holders of Common Stock.

Our ability to successfully operate our business, implement our investment strategy and generate cash flows depends on numerous factors, many of which are beyond our control. These factors include our ability to identify and acquire attractive investment opportunities, operate and maintain our properties efficiently, maintain occupancy levels and rental income, manage operating expenses, obtain financing on favorable terms and compete effectively for investments, tenants and capital.

Our operating results and cash flows also may be adversely affected by economic conditions, interest rate fluctuations, inflation, changes in real estate market conditions, adverse regulatory developments, supply chain disruptions, labor shortages, weather-related events, litigation, increases in taxes or insurance costs and other factors affecting the ownership and operation of commercial real estate.

In addition, the value and operating performance of our properties may decline after acquisition, and we may be unable to achieve anticipated occupancy levels, rental rates, operating efficiencies or investment returns. We also may be unable to secure financing for our properties or refinance existing indebtedness on favorable terms or at all.

If we are unable to successfully implement our business strategy, operate our properties effectively or generate sufficient cash flows from operations, we may be unable to pay our operating expenses, satisfy our debt service obligations or make distributions to holders of Common Stock. Any such event could adversely affect our business, financial condition, operating results, cash flows and ability to make distributions to holders of Common Stock.

We may experience delays in identifying, acquiring, developing or leasing investments, which could adversely affect our operating results and the timing of distributions to holders of Common Stock.

Our ability to achieve our investment objectives depends on the Manager’s ability to identify, acquire, finance, develop and lease suitable investments on favorable terms. The market for supply chain and logistics infrastructure real estate assets is highly competitive, and we compete with numerous investors, developers and real estate operators for acquisition opportunities, financing, tenants and other resources.

As we raise additional capital, we may experience increased difficulty deploying offering proceeds into investments that satisfy our investment criteria. In addition, investors generally will not have the opportunity to evaluate potential investments before they are acquired and therefore must rely on the judgment of our board of directors, the Manager and our property managers.

We also may experience delays in acquiring investments as a result of competition for investment opportunities or the allocation of opportunities among us and other investment programs sponsored, managed or advised by affiliates of the Manager. Furthermore, investments involving development, redevelopment, renovation or lease-up activities may require significant time to complete construction, obtain permits and approvals, attract tenants and generate operating income.

If we are unable to deploy capital in a timely manner or if our investments do not generate income as quickly as anticipated, our operating results, cash flows and ability to make distributions to holders of Common Stock could be adversely affected. In such circumstances, offering proceeds may remain invested in cash, cash equivalents or other short-term investments pending deployment, which may reduce overall returns to investors.

| -11- |

We may not be able to effectively manage our growth, which could adversely affect our business, financial condition and operating results.

Our future success will depend in part on our ability to effectively manage the growth of our business. As we acquire additional investments and expand our operations, we may face increased demands on our management, operational, financial, compliance and technological resources.

Our ability to successfully manage growth will depend on numerous factors, including our ability to attract, integrate and retain qualified personnel, maintain effective relationships with third-party service providers, develop and maintain appropriate operational and financial controls, enhance reporting systems and scale our infrastructure to support a larger and more complex organization.

Growth may also increase the complexity of our operations and require significant additional expenditures. If we are unable to effectively manage the expansion of our business, maintain adequate controls and systems or successfully integrate new investments into our portfolio, our operating efficiency and financial performance could decline, and our ability to execute our business strategy could be impaired.

Any failure to effectively manage our growth could adversely affect our business, financial condition, operating results, cash flows and ability to make distributions to holders of Common Stock.

Competition for acquisition opportunities, rising acquisition costs and changing market conditions may limit our ability to grow our portfolio and achieve attractive investment returns.

Our long-term growth depends in part on our ability to identify and acquire investments that satisfy our investment criteria at acceptable prices. Competition for supply chain and logistics infrastructure real estate assets has increased in recent years as institutional investors, private investment funds, REITs and other market participants have devoted significant capital to the sector. Increased competition may reduce the availability of attractive acquisition opportunities and increase acquisition prices.

In addition, improvements in economic conditions, increased demand for logistics-related real estate, favorable financing conditions, rising construction costs and other market factors may increase the cost of acquiring, developing or redeveloping investments. These factors may make it more difficult for us to identify investments that meet our return objectives.

We have not adopted a policy requiring acquisitions to be immediately accretive to existing yields or distributable cash flows. As a result, we may pursue acquisitions that we believe offer attractive long-term returns even if such acquisitions initially reduce operating performance or cash available for distribution.

If acquisition opportunities become less available, acquisition costs increase significantly or market conditions change adversely, our ability to expand our portfolio, implement our investment strategy and generate attractive returns for stockholders could be adversely affected.

Our future growth depends in part on our ability to obtain debt and equity financing on favorable terms, and any inability to do so could adversely affect our business and operating results.

Our business strategy depends in part on our ability to access debt and equity capital to acquire investments, fund operations, satisfy obligations, refinance existing indebtedness and pursue growth opportunities. The availability of financing depends on numerous factors, including general economic conditions, financial market conditions, interest rates, lender and investor sentiment, our financial performance and leverage levels, and the market’s perception of our business prospects.

We cannot assure you that debt or equity financing will be available when needed, on favorable terms or at all. Adverse conditions in the capital markets, rising interest rates, reduced lender activity, declining property values or other factors could limit our access to capital or increase our cost of financing.

If we are unable to obtain sufficient financing, we may be required to delay or reduce acquisitions, curtail investment activities, dispose of assets at unfavorable times or prices, or pursue alternative financing arrangements that are more costly or less advantageous. In addition, if we rely more heavily on equity financing, existing stockholders may experience dilution.

Any inability to obtain adequate financing could adversely affect our business, financial condition, operating results, cash flows and ability to make distributions to holders of Common Stock.

| -12- |

If we are unable to raise substantial funds or engage in a significant number of OP Unit exchanges, we may be unable to achieve a diversified investment portfolio, which could increase the risks associated with an investment in us.

We cannot assure you that we will raise sufficient proceeds through this or future offerings of Common Stock. If we are unable to raise substantial funds or engage in a significant number of OP Unit exchanges, we will make fewer investments, resulting in less diversification in terms of the number of investments owned, the geographic regions in which our investments are located and the types of investments that we acquire. As a result, our operating results and profitability may be disproportionately affected by the performance of any single investment. Your investment in the Common Stock will be subject to greater risk to the extent that we lack a diversified portfolio of investments. In addition, if we are unable to raise substantial funds, our fixed operating expenses, as a percentage of gross income, would be higher, and our financial condition and ability to pay distributions could be adversely affected.

The offering price of our Shares was not established in reliance on a valuation of our assets and liabilities; the actual value of your investment may be substantially less than what you pay.

We established the offering price of our Shares on an arbitrary basis. The selling price of our Shares bears no relationship to our book or asset values or to any other established criteria for valuing shares. We plan to determine the net asset value of our common stock beginning twelve months after the Initial Closing of this offering. Thereafter, the per share purchase price will be adjusted every fiscal quarter as of January 1st, April 1st, July 1st, and October 1st of each year and will equal our net asset value, or NAV, divided by the number of shares of our common stock outstanding as of the end of the prior fiscal quarter on a fully diluted basis (NAV per Share). See “Plan of Distribution—Price per Share.”

Our NAV per Share will be calculated by our Manager and reviewed and approved by our board of directors at the end of each fiscal quarter on a fully diluted basis, beginning twelve months after the Initial Closing of this offering using a process that reflects several components, including (1) estimated values of each of our commercial real estate assets and investments, including related liabilities, based upon (a) market capitalization rates, comparable sales information, interest rates, net operating income, and (b) in certain instances individual appraisal reports of the underlying real estate provided by an independent valuation expert, (2) the price of liquid assets for which third party market quotes are available, (3) accruals of our periodic dividends and (4) estimated accruals of our operating revenues and expenses. In instances where we determine that an independent appraisal of the real estate asset is necessary, including, but not limited to, instances where our Manager is unsure of its ability on its own to accurately determine the estimated values of our commercial real estate assets and investments, or instances where third party market values for comparable properties are either nonexistent or extremely inconsistent, we may engage an appraiser that has expertise in appraising commercial real estate assets, to act as our independent valuation expert. The independent valuation expert will not be responsible for, or prepare, our NAV per Share. However, we may hire a third party to calculate, or assist with calculating, our NAV per Share. The use of different judgments or assumptions would likely result in different estimates of the value of our real estate assets. Moreover, although we evaluate and provide our NAV per Share on a quarterly basis, our NAV per Share may fluctuate daily, so that the NAV per Share in effect for any fiscal quarter may not reflect the precise amount that might be paid for your Shares if you were to transfer your Shares to a third-party in a privately negotiated transaction. Further, our published NAV per Share may not fully reflect certain material events to the extent that they are not known or their financial impact on our portfolio is not immediately quantifiable. Any resulting potential disparity in our NAV per Share may be in favor of either stockholders who redeem their shares, or stockholders who buy new shares, or existing stockholders. In cases where we believe there has been a material change (positive or negative) to our NAV per Share since the beginning of the applicable quarter, we will update a previously disclosed Transaction Price. If we update the Transaction Price during any quarter, we will notify potential investors through the filing of a supplement to this Offering Circular. Note, in addition, that the determination of our NAV per Share is not based on, nor intended to comply with, fair value standards under generally accepted accounting principles (“GAAP”) and our NAV per Share may not be indicative of the price that we would receive upon the sale of our assets or the price at which our Shares could be bought or sold in the market. See “Plan of Distribution—Valuation Policies.”

| -13- |

Because a significant portion of our expenses are fixed or semi-fixed, we may not be able to reduce our costs in response to declines in revenue.

Many of the expenses associated with our business, including property operating expenses, maintenance and repair costs, real estate taxes, insurance premiums, utilities, payroll expenses, capital expenditures and general corporate expenses, are relatively fixed and may not decrease if our revenues decline. In addition, inflation and other factors may increase our operating costs and capital expenditure requirements, and certain cost increases may exceed the rate of inflation.

By contrast, our revenues may fluctuate as a result of factors beyond our control, including changes in rental rates, tenant demand, occupancy levels, economic conditions, competition and the availability of competing supply chain and logistics infrastructure real estate assets. Regulatory requirements also may require us to incur significant maintenance, repair, capital improvement or compliance costs regardless of the profitability of a particular property.

As a result, increases in expenses or capital expenditures may not be offset by corresponding increases in revenues. If our revenues decline or fail to grow at a rate sufficient to offset rising costs, our financial condition, operating results, cash flows and ability to make distributions to holders of Common Stock could be adversely affected.

We are dependent on the executive officers and personnel of the Manager, and the loss of key personnel or the inability to attract and retain qualified personnel could materially and adversely affect us.

Our operations and investment activities are highly dependent upon the experience, judgment and relationships of a limited number of executive officers and other key personnel of the Manager. Any of the Manager’s senior management personnel may cease providing services to us at any time. The loss of the services of any key management personnel, whether due to resignation, disability, death or other reasons, could disrupt our operations, impair the execution of our investment strategy and adversely affect our financial performance. Because certain investment, financing and operational decisions are concentrated among a limited number of individuals, the unexpected loss of one or more such persons could have a disproportionate impact on our business until suitable replacements are identified and integrated.

We do not maintain key-person life insurance on any of the Manager’s executive officers or other key personnel. Accordingly, there can be no assurance that we would receive any compensation to offset the loss of the services of such individuals.

In addition, as we expand our operations, the Manager will continue to need to attract and retain additional qualified personnel but may not be able to do so on acceptable terms or at all. Competition for highly skilled managerial, investment, financial and operational personnel is intense. As additional institutional real estate investors, logistics operators and private investment firms compete in the markets that we target, the Manager will face increased challenges in hiring and retaining personnel, and we cannot assure you that the Manager will be successful in attracting and retaining such skilled personnel. If the Manager is unable to attract, hire and retain qualified personnel as required, our business, growth prospects and operating results could be adversely affected.

Our investments are expected to be concentrated in our target markets and in the supply chain and logistics sector of the real estate industry, which exposes us to fluctuations in rental demand and downturns in our markets or in the supply chain and logistics properties sector.

Although we may acquire supply chain and logistics properties from time to time, our investments in real estate assets are expected to be concentrated in our target markets and in the supply chain and logistics properties sector of the real estate industry. A downturn or slowdown in the rental demand for these assets caused by adverse economic, regulatory or environmental conditions, or other events in our markets, may have a greater impact on the value of our properties or our operating results than if we had more fully diversified our investments. In addition, adverse developments affecting supply chain operators, transportation providers, e-commerce businesses, manufacturers, distributors or other users of logistics facilities could reduce demand for our properties and adversely affect occupancy levels, rental rates and property values.

In addition to general, regional, national and international economic conditions, our operating performance will be impacted by economic conditions in our target markets. We acquire, renovate and lease supply chain and logistics properties in these markets. Our business plan is based, in part, on assumptions regarding future property values, rental demand and operating fundamentals in our target markets. These assumptions may prove to be inaccurate. Many of these markets have experienced substantial economic downturns in recent years and could experience similar or more severe downturns in the future. We can provide no assurance that property values, rental demand or operating fundamentals in these markets will improve, if at all. If these markets experience future economic downturns, if conditions fail to improve as anticipated, or if we fail to accurately predict the timing or extent of any economic recovery, the value of our properties could decline and our ability to execute our business plan could be impaired, which, in turn, could negatively impact our financial condition, operating results and ability to make distributions to the holders of our Common Stock.

We may not be able to effectively control the timing and costs relating to the renovation of properties, which may adversely affect our operating results and our ability to make distributions to the holders of our Common Stock.

A portion of our properties acquired through traditional channels are expected to require some level of renovation immediately upon their acquisition or in the future following expiration of a lease or otherwise. We may acquire properties that we plan to renovate extensively. We also may acquire properties that we expect to be in good condition only to discover unforeseen structural deficiencies, environmental conditions, deferred maintenance issues or other defects that require significant renovation and capital expenditures. To the extent properties are leased to existing tenants, renovations may be postponed until the tenant vacates the premises, which could delay the implementation of our business plan and require additional capital expenditures. In addition, from time to time, in order to reposition properties in the rental market, we will be required to make ongoing capital improvements and replacements and perform significant renovations and repairs that tenant deposits and insurance may not cover.

| -14- |

Our properties will have infrastructure of varying ages and conditions. Consequently, we will routinely retain independent contractors and trade professionals to perform physical repair work and are exposed to all of the risks inherent in property renovation and maintenance, including potential cost overruns, increases in labor and materials costs, contractor delays, delays in obtaining necessary permits and certificates of occupancy, and poor workmanship. We may also experience delays or increased costs resulting from shortages of labor, construction materials, equipment or other resources required to complete renovation projects. If our assumptions regarding the costs, scope or timing of renovation and maintenance activities prove to be materially inaccurate, or if renovation projects are delayed or exceed budgeted costs, our financial condition, operating results and ability to make distributions to the holders of our Common Stock could be adversely affected.

We face significant competition for acquisitions of target investments, which may increase acquisition costs and limit our ability to grow our portfolio.

We compete with numerous real estate investors, developers, investment funds, REITs and other market participants for attractive acquisition opportunities. Many of our competitors have substantially greater financial resources, broader market access, more established operating platforms and lower costs of capital than we do.

In addition, significant amounts of institutional and private capital have been, and may continue to be, invested in supply chain and logistics infrastructure real estate assets. As competition for attractive investment opportunities increases, we may face higher acquisition prices, less favorable transaction terms and reduced availability of investments that satisfy our investment objectives.

As a result, we may be unable to acquire investments on desirable terms or at all, which could limit our ability to grow our portfolio, implement our business strategy and generate attractive returns for stockholders.

We face significant competition for tenants, which may reduce occupancy levels, rental income and operating results.

We depend on rental income for a substantial portion of our revenues and must attract and retain tenants to achieve our investment objectives. We compete with numerous owners, operators and developers of commercial real estate for tenants in our target markets. Competing properties may be newer, better located, offer more attractive amenities or incentives, or have owners with greater financial resources and lower operating costs.

In addition, continued development activity and the availability of competing properties and other supply chain and logistics infrastructure real estate assets may increase the supply of available space in our markets. Increased competition could reduce occupancy levels, limit our ability to increase rental rates, require us to offer greater concessions or otherwise reduce the profitability of our properties.

Economic downturns, rising unemployment, tenant bankruptcies and other adverse market conditions also may reduce tenant demand and impair the creditworthiness of existing and prospective tenants, which could increase vacancies and tenant defaults.

If we are unable to attract and retain tenants on favorable terms, our rental income, operating results, cash flows and ability to make distributions to holders of Common Stock could be adversely affected.

Our evaluation of investments is based on assumptions and estimates that may prove inaccurate, which could result in lower-than-expected returns and operating performance.

In evaluating potential investments, we make numerous assumptions regarding factors such as acquisition costs, renovation and capital expenditure requirements, operating expenses, market rental rates, occupancy levels, tenant demand, lease-up periods, tenant creditworthiness and future market conditions. These assumptions and estimates may prove to be inaccurate, and actual results may differ materially from our expectations.

In addition, our due diligence investigations may not identify all material facts, risks, liabilities or conditions affecting a property. Properties may be subject to physical defects, environmental issues, deferred maintenance, regulatory compliance matters or other conditions that are not identified prior to acquisition or that are more significant than anticipated.

Changes in market conditions, economic trends, regulatory requirements or other factors affecting supply chain and logistics infrastructure real estate assets may further increase the difficulty of accurately evaluating investments and forecasting future performance.

If our assumptions, estimates or due diligence assessments prove incorrect, we may overpay for investments, incur higher-than-expected costs, experience lower occupancy or rental income, or otherwise fail to achieve anticipated returns. Any such event could adversely affect our business, financial condition, operating results, cash flows and ability to make distributions to holders of Common Stock.

| -15- |

Our success in any development activities will depend in large part on our ability to acquire land that is suitable for construction and meets our investment criteria.

There is strong competition among real estate developers for land suitable for development. The future availability of finished and partially completed developments, as well as undeveloped land that meets our investment criteria, depends on a number of factors outside our control, including overall land availability, competition with other developers and land buyers, inflation in land prices, zoning restrictions, permitting requirements, environmental regulations, infrastructure constraints, and other regulatory requirements. If suitable land becomes less available, our ability to develop properties could be reduced, and the cost of acquiring land could increase, potentially significantly, which could adversely affect our growth and results of operations.

We will rely on subcontractors for the construction of any newly developed properties and on building supply companies to provide components used in such construction. The failure of our subcontractors to properly construct our properties or defects in components supplied by building supply companies could have an adverse effect on us.

We will engage subcontractors to perform the actual construction of any newly developed properties and purchase components used in such construction. Despite our quality control efforts, we may discover that subcontractors have engaged in improper construction practices or that components supplied by building supply companies are defective or fail to perform as intended. The occurrence of such events could require us to repair or remediate the applicable properties in accordance with our standards and applicable legal requirements. The cost of satisfying our obligations in these instances, including the costs of repairs, litigation, claims administration, project delays and reputational harm, may be significant, and we may be unable to recover such costs from subcontractors, suppliers, or insurers.

We are subject to risks from natural disasters and severe weather.

Natural disasters and severe weather such as earthquakes, hailstorms, tornadoes, hurricanes or floods may result in significant damage to our properties. The extent of our casualty losses and any loss of rental income resulting from such events will depend on the severity of the event and the total amount of exposure in the affected area. The frequency and severity of certain weather-related events may increase as a result of changing climate conditions, which could increase the likelihood and magnitude of property damage, business interruption and related losses. In addition, insurance coverage may not be available on commercially reasonable terms, may be subject to significant deductibles or exclusions, or may not be sufficient to fully cover losses, business interruption, loss of rental income, or the costs of restoring our properties to their prior condition.

If occupancy levels and rental rates do not increase sufficiently to offset rising operating costs, our profitability and cash flows may decline.

Our operating results depend in part on our ability to maintain occupancy levels and increase rental rates at our properties. Market conditions affecting supply chain and logistics infrastructure real estate assets in our target markets may limit our ability to increase rents or maintain occupancy levels. Increased competition, new development activity, changing tenant demand and other market factors may place downward pressure on occupancy rates and rental income.

At the same time, many of our operating expenses, including property taxes, insurance premiums, utilities, maintenance costs, labor expenses and other property operating costs, may continue to increase regardless of market conditions. Inflation and other economic factors may further increase these expenses.

If rental income does not increase at a rate sufficient to offset rising operating costs, our profitability, operating results, cash flows and ability to make distributions to holders of Common Stock could be adversely affected.

We depend on our tenants for substantially all of our revenues. Poor tenant selection, tenant defaults and nonrenewals may adversely affect our financial performance and ability to make distributions to the holders of Common Stock.

We depend on rental income from tenants for substantially all of our revenues. As a result, our success depends in large part on our ability to attract and retain qualified tenants for our properties. Our evaluation of prospective tenants involves assumptions regarding their financial condition, business operations and future prospects, and those assumptions may prove to be inaccurate. Our financial performance and ability to make distributions to the holders of Common Stock could be adversely affected if a significant number of our tenants fail to meet their lease obligations or choose not to renew their leases. Tenants may default on rent payments, violate lease terms or use our properties in ways that are inconsistent with applicable laws or regulations. In addition, tenant defaults or bankruptcies may result in delays in enforcing our rights as landlord, as well as increased costs associated with re-leasing, repairing or repositioning the affected properties.

Damage to our properties by tenants or failure by tenants to comply with lease obligations may delay re-leasing after vacancy, require significant repair expenditures, or reduce the rental income or value of the property. Increases in unemployment levels and other adverse economic conditions in our markets could result in increased tenant defaults and reduced demand for our properties.

| -16- |

The expiration, nonrenewal or early termination of leases may adversely affect our occupancy levels, rental income, and ability to make distributions to holders of Common Stock.

Our ability to generate rental income depends on maintaining occupancy at our properties and renewing leases with existing tenants or replacing tenants whose leases expire or terminate. As leases expire, tenants may choose not to renew, may seek more favorable lease terms, or may vacate our properties. In addition, tenants may terminate leases early where permitted by the lease terms or as a result of financial distress, bankruptcy, changes in business operations or other circumstances.

If tenants do not renew their leases, if replacement tenants cannot be identified on favorable terms or within a reasonable period of time, or if market rental rates decline, our occupancy levels and rental income may be adversely affected. In addition, we may incur significant costs associated with re-leasing vacant space, including brokerage commissions, tenant improvement allowances, leasing incentives, marketing expenses and property restoration costs. Periods of vacancy may also increase operating expenses and reduce cash flow from affected properties.

The supply chain and logistics property markets in which we operate are subject to changing economic conditions, shifts in tenant demand, evolving supply chain patterns and increased competition from existing and newly developed properties. These factors may make it more difficult or costly to renew existing leases or attract replacement tenants. Any significant decline in occupancy levels, rental income or lease renewal rates could adversely affect our operating results, financial condition and ability to make distributions to holders of Common Stock.

Declining real estate values and impairment charges could adversely affect our financial condition and operating results.

We will periodically review the carrying value of our properties to determine whether their value has been permanently impaired based on market conditions and projected cash flows, in which case we may be required to recognize impairment charges in the applicable accounting period. Any such charges would reduce our net income in the period recognized and be reflected as a reduction in our balance sheet assets.

Property values may decline as a result of adverse economic conditions, rising interest rates, increased capitalization rates, oversupply of competing properties, changes in tenant demand, or other factors beyond our control. A reduction in net income resulting from impairment charges could reduce our ability to make distributions in the current or future periods. Any impairment charges would adversely affect our financial condition and operating results.

In addition, declines in the value of our properties could limit our ability to refinance indebtedness secured by such properties upon maturity or result in breaches of covenants under our loan agreements.

We will be self-insured against many potential losses, and uninsured or underinsured losses relating to our properties may adversely affect our financial condition, operating results, cash flows and ability to make distributions on Common Stock.

We intend to maintain insurance coverage for our properties against casualty losses; however, such policies are often subject to significant deductibles and exclusions, and we will be self-insured up to the amount of such deductibles and exclusions. In addition, certain types of losses, including losses from floods, windstorms, fires, earthquakes, acts of war, acts of terrorism or civil unrest, may be uninsurable or not economically insurable. Changes in the cost or availability of insurance may also result in higher deductibles or reduced coverage, thereby increasing our exposure to uninsured losses.

If any of our properties incur a casualty loss that is not fully covered by insurance, the value of our assets would be reduced by the amount of the uninsured loss, and we could experience a loss of invested capital and potential revenues from the affected properties and remain obligated under any related recourse debt. In addition, inflation, changes in building codes or ordinances, environmental conditions and other factors may prevent us from fully utilizing insurance proceeds to restore or replace damaged properties, and we may not have sufficient additional sources of funding available for reconstruction or repair.

| -17- |

Contingent or unknown liabilities could adversely affect our financial condition, cash flows and operating results.