Exhibit 99.1 3 July 2026 David Lin Novel Inspiration International Co., Ltd David, This letter was drafted to comply with a recent resolution of the current board of directors (the “Board”) of Iridex Corporation (“Iridex” or the “Company”). Its purpose is to attempt to engage with Novel Inspiration (“Novel”) in pursuit of greater clarity, in both directions, as to why, and as to how, the Company’s largest stockholder has positioned itself adverse to a majority of the Board, and thereby, in practical effect, the Company itself. This letter follows several requests to schedule more informal calls or meetings, all of which requests have been refused. For convenience, included with this letter are the following: Attachment I: Memorandum of Law from Company’s outside counsel Attachment II: Draft Company 8-K Disclosure Filing Attachment III: Performance KPI slide from the Company’s Investor Relations deck Iridex’s CEO, Patrick Mercer, has informed other members of the Board that during one of your recent scheduled monthly call with him, you argued the Board focuses too much on governance processes and not enough on value creation (the “Process Argument”). In this letter, we will first review the intensity of the Company’s ongoing value creation efforts, including how most if not all of such efforts are being pursued in coordination or collaboration with Novel and its representatives and affiliates. Second, this letter will argue that inasmuch as the record of value creation activities easily overwhelms the Process Argument, the Process Argument should properly be viewed as an effort at misdirection. Together with talking points that may have been selectively whispered to stockholders as part of stealth proxy campaign currently targeting two of the Company’s independent directors, the Process Argument is cover for a control contest seeking to change the Company’s Board and its governance. While such control contests can be perfectly legitimate, this letter and Attachments I and II intend to remind the reader that with public companies, and particularly when done coincident to a public company’s annual shareholder meeting and proxy process, Federal and state laws cannot be ignored.

Answering the Process Argument The pursuit of strategies and activities targeting value creation have been hyper present at Iridex since at least October 2024. As detailed below, the Company has been heavily involved in a promising turnaround effort. This effort has consisted of: (1) replacement of senior management; (2) recruitment of a new strategic lead investor; (3) turnover of a majority of the Board; (4) implementation of very significant cost cuts, relating to; (5) a major reform in the Company’s glaucoma strategy; supported by, (6) the ongoing successful launch of a new Pascal retinal system; all while, (7) planning and beginning to relocate the Company’s headquarters and execute on the manufacturing outsourcing programs that have been discussed but not acted upon for more than a decade. While some might fault various elements of the above pursued strategic actions, anyone claiming not to see sincere and sustained efforts at value creation is being obviously disingenuous. Someone observing the Company’s recent burst of activities and seeing a Company being held back by governance processes (i.e., the Process Argument) seems likely to be projecting their own preoccupation with governance processes and control. Eighteen Months Into a Turnaround Iridex’s public stock currently trades at a very low price. This is a reflection of past mistakes made and failures in pursuit of a very aggressive growth business plan that was terminated in October 2024. It must be noted that but for these failures, Novel would not have been presented with the opportunity to acquire a large percentage of the Company’s equity at a low price. Having taken advantage of the market opportunity created by Iridex’s past mistakes, it would be disingenuous for Novel to argue today that it is suffering harm from the very mistakes its investment capitalized upon. Fair criticism must relate to current and ongoing mistakes and failures. Prior to October 2024, the Company’s growth-oriented business plan focused on an aggressive effort to commercialize its MicroPulse Transscleral Laser Therapy (“MP-TLT”). This plan originated more than 10 years ago, during the tenure of Will Moore, as the Company’s Chairman and CEO. In December 2016, Mr. Moore engaged Roth Capital to raise $16.1 million to pursue an aggressive rollout and sales strategy. Approximately two years later, Iridex’s then board of directors decided to replace Mr. Moore as CEO with one of its members, David Bruce. Two years after that, in March 2021, Mr. Bruce closed on a $19.5 million financing transaction with Topcon. During his tenure, Mr. Moore’s value creation strategy focused on MP-TLT laser console placements; Mr. Bruce’s strategy focused on increasing glaucoma probe utilization. Neither strategy was ultimately judged successful by the Board or the public markets. The combined MP-TLT effort consumed all $35.6 million in outside funds raised by the Company while Iridex reported nine consecutive years of negative earnings and cash flow.

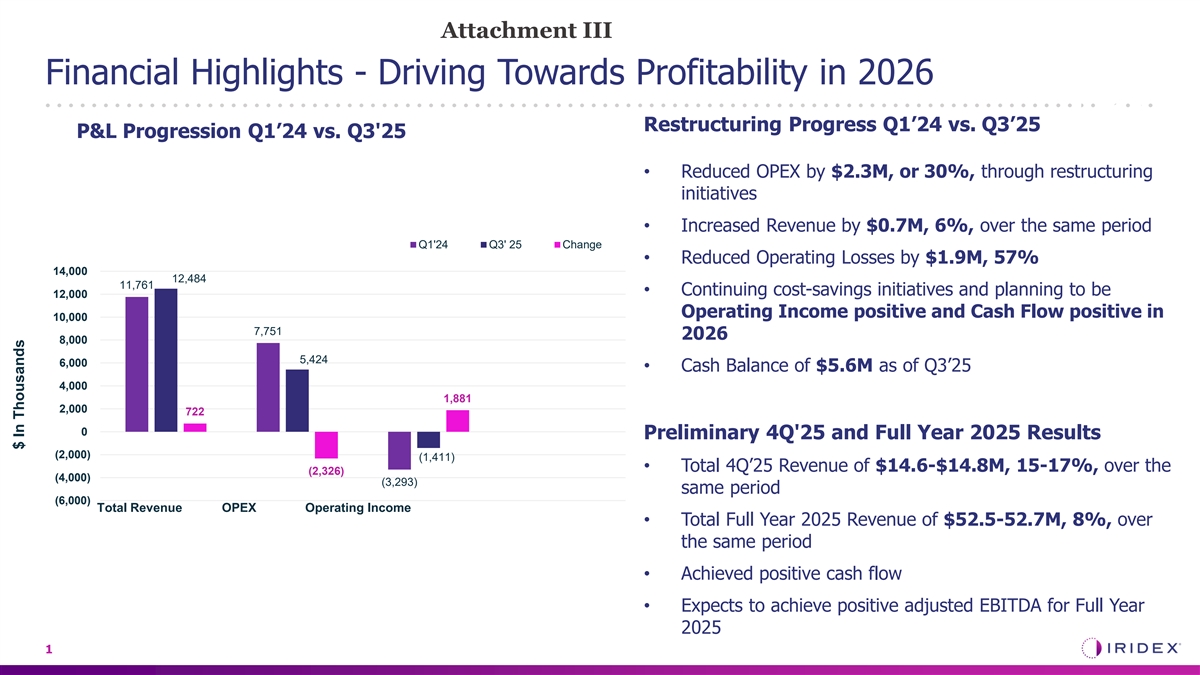

In October 2024, after efforts with its banker, Piper Sandler, to find a buyer for the Company failed, the Board named Patrick Mercer CEO and directed cuts that ended the MP-TLT deficit spending. Within two months, negotiations were well developed with Novel resulting in the March 2025 Series B Preferred investment. Prior to October 2024, the Board was split on strategic direction and the Novel investment. After March 2025 the Board was reconstituted with unanimous agreement around strategic and value creation priorities. Unanimous agreement can be said with confidence because the Board has repeatedly worked to articulate the Company’s strategic priorities in writing. Team efforts to isolate, articulate, and organize lists of issues and tasks (which were by design heavily weighted toward those articulated by Mr. Moore) were further built upon by the implementation of monthly status calls involving the Company’s CEO and Mr. Moore, meetings that were later supplemented by monthly calls between the CEO and Novel’s principal. The purpose of these articulated priorities, task lists, and update calls was to ensure communication and ongoing strategic alignment. Briefly recast here, the agreed priorities for the Company in 2025 and 2026 have been: 1. Cash preservation and reversal to cash flow positive operations. 2. Reducing California operations footprint and expense. 3. Outsourcing manufacturing. 4. Regulatory compliance – maintaining and improving ability to sell products in key markets. 5. Preserving the Company’s future product roadmap and momentum while lowering ongoing investment requirements. 6. Identification and pursuit of new product offerings. In the year since Novel’s investment, the Company has mostly delivered year-over-year revenue growth while reducing operating expenses by 34% and reducing operating losses by 90%. The Company delivered positive adjusted EBITDA and cash flow positive operations in the fourth quarter of 2025. Please see Attachment III hereto, a slide from the Company’s current Investor Relations deck providing more color on the Company’s recent financial achievements. Despite these successes and the sustained efforts to ensure agreement and alignment around strategic priorities and paths to value creation, there have been a couple topics generating friction within the Board. The first concerns cash utilization, and this has consistently puzzled a majority of the Board. For the last year, the Board has heard frequent criticism from Novel and its director nominees that much of the $10 million of investment proceeds from Novel’s investment has been deployed. But, this was exactly what was planned – paydown of the Lind Capital debt and catchup on vender accounts payable was the very purpose of the financing. Such planned cash usage was not only a major subject of

diligence prior to the investment, the amounts were repeatedly detailed in the Company’s publicly-filed quarterly financial statements. Indeed, when first contacted about the potential of making an investment, Novel’s representative told the Company, paraphrasing, “we calculate you need about $10 million now to fix your balance sheet…and Novel believes another $10 million to finance future growth.” That observation proved exactly right, making the subsequent complaints appear disingenuous. Another area consistently generating friction, despite persistent efforts made toward collaborative resolution, has concerned regulatory affairs, particularly involving required approvals to sell into China. Much could be said as numerous people and departments at the Company have for some time been working with numerous people and departments among Novel’s affiliates, usually with the coordination and frequent direction of Mr. Moore. While tension and complaints exist and are frequently heard, it remains unclear what more the Board or the Company can do after having delegated to its domain and regional experts, including Mr. Moore, the primary roles of strategy, coordination, and oversight in this area. Summary. The Company’s Board has created governance and business practices to ensure identification, communication, alignment, execution, and reporting around the Company’s strategic priorities relating to its current business operations. It is aware of only two areas of consistent friction and has summarized its perspective above. If there are other areas of disagreement, please advise and they will be addressed in similar fashion. How to Grow the Company Just as there is readily available documented and circulated records confirming the unanimous Board agreement concerning the Company’s operating priorities, there are numerous public documents recording the unanimous Board agreement concerning the Company’s growth strategy. Coincident to and for a period after Novel’s Series B investment, all of the Company’s press releases, public transcripts and filings articulated a product acquisition or partnering strategy (often referred to as the “Novel strategy”) that would seek to leverage Iridex’s global distribution network. During the investment negotiations with Novel and from time-to-time thereafter, Mr. Moore described the “Novel strategy” as a “string of pearls”. Further, during and shortly after the Novel investment, Mr. Moore privately communicated that he believed it necessary that he himself be the one articulating the Company’s new strategy to the public. The Board accommodated this. The Novel investment was announced on March 19, 2025 and on April 16, 2025, the Company conducted a public “Strategic Vision Conference Call.” To the great surprise of management and a majority of the Board, shortly before the already scheduled call, Mr. Moore announced it would be unwise to telegraph greater detail than had already been publicly disseminated. The call, thus lacking any new content, was overtaken by criticisms

from a prior investor that apparently had lost money during the Company’s period of aggressive MP-TLT spending. Over the past year, while there has been frequent suggestions that there exist multiple companies known to or affiliated with Novel that could one day become strategic partners, management and Board attention has been brought into only two situations: (1) a company run by physician academics that have developed a specialized vision screening test, and (2) a probe manufacturer in the Near East. With respect to the first, Mr. Shuda and Mr. Moore traveled to and met with that company’s leadership and worked through numerous discussions on a term sheet before Mr. Moore declared the effort futile. With respect to the second, it is believed that all Board members consider the prospect active, and something to be considered after there is agreement that management has successfully worked through its existing list of priorities relating to supplier and manufacturing outsourcing initiatives. While a majority of the Board believes it has accepted, leaned into, and diligently pursed the “string of pearls” strategy, it also believes every partnership/product acquisition idea initiated away from Novel and its Board nominees has been flatly rejected, without discussion, debate or diligence. In particular, two potentially highly synergistic dialogs with two international competitors were discontinued after the Novel investment was made due to the failure to obtain any engagement or interest from the Novel Board nominees. Further, it has been repeatedly emphasized to a majority of the Board that Novel has no interest in any transaction where Iridex is not the clear acquirer; this posture was reinforced when Novel demanded and received voting rights requiring that it approve any such transaction. It is understood that Novel has absolute discretion with respect to the $10 million of growth capital it has rights to deploy, but there has been nothing actionable presented to the Board with respect to what companies, products, or regions should be the targets for said $10 million. Summary. A majority of the Board has been instructed and has accepted since negotiations began relating to the Series B investment that Novel and its Board nominees expect and will insist that they provide direction with respect to the Company’s growth strategy via product acquisitions. We will remain open and seek to support every opportunity communicated with us, and if Novel has changed its stance, and is now open to ideas originating from the Company, we will be prepared for that conversation in short order. Prior Campaign Directed at CEO Prior to development of the current adverse position against two of the Board’s independent directors, management and the Board devoted significant attention to understanding and accommodating a campaign directed at the Company’s CEO. The original idea related to the Company’s CEO needing assistance in articulating the Novel-inspired product acquisition strategy, and gradually evolved into a

more generalized critique relating to experience and current abilities. The ultimate resolution of this campaign was the creation of the priority lists and monthly status checks/meetings where the CEO regularly provides updates to both the Board and the lead stockholder. Also part of the campaign were three instances involving third party consultants promoted by Novel or its Board nominees. The first was a recent Santa Clara University graduate known to Mr. Moore who was going to help the Company develop a 3-5 year strategic plan. After evaluating that such individual had no relevant industry experience, the parties moved to embedding an executive from one of Novel’s affiliates into the Company’s Mountain View office for six weeks. Months later, no report, assessment, or planning document has been shared with the Board or management relating to that collaboration. The third and most recent instance involved an effort to engage a European executive in either a consulting or board role. This met mixed reactions, but efforts were underway to schedule Zoom calls that would introduce four of the five Board members to this individual. That process ended when Mr. Moore announced the idea was being abandoned. Among the non-Novel designated Board members, there was speculation that Mr. Moore had determined the executive a potential threat to his continuing position on the Board and had therefore found a rationale to quash the idea before it gained further momentum. Novel Proposal to Convert to Common at Conversion at New Price The only other issue known to potentially be the source of disagreement between Novel and its affiliates and the other members of the Board is a proposal to change the price for the conversion of the Novel Series B shares and the outstanding Novel notes into common stock, to a price that reflected the Company’s current stock market price. Novel has repeatedly stated its belief that stockholders would vote to approve the change in conversion price and not find the resulting dilution to be material. Novel argues the early conversion would deliver the benefit of: (1) replacing the existing 12% dividend, paid in- kind with shares of the Company’s stock, accruing on the outstanding Novel notes, and eliminate the quarterly interest expense of the notes for the remaining two years of the three-year term and (2) facilitate the conversion of the Novel Series B shares to common stock thereby simplifying the Company’s capitalization table. Sample calculations indicate Novel’s request to change the Series B conversion price would likely result in 2 million or more incremental shares being issued to Novel. Such 2 million shares would represent approximately 10% of the Company’s fully diluted equity capitalization, which reflects significant dilution. A majority of the Board believes the proposed transaction to not be in the interest of a majority of the Company’s stockholders and that merely proposing that stockholders vote to approve such change would be detrimental not just to the Company’s other stockholders, but, on an investor relations level, to the Company and to Novel.

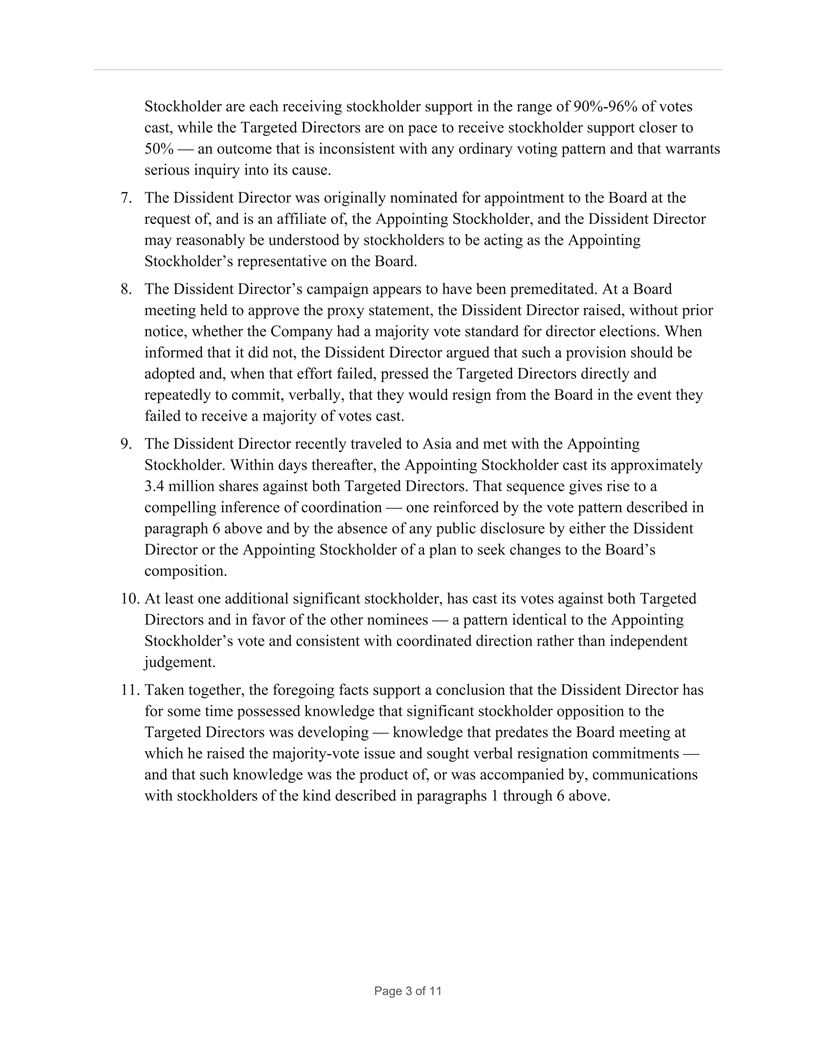

When an American public company is required to obtain stockholder consent via a vote of outstanding shares, the process involves filing a proxy statement providing detailed disclosure of the proposed action and the recommendation of the Board “for” the proposed action. A majority of the members of the Board have not been persuaded that it is consistent with their fiduciary duties to affirm a Board recommendation that stockholders vote “for” the proposed change in the Series B conversion price. Summary. As detailed above, the Board has welcomed Novel as the Company’s lead stockholder and consistently worked to integrate and support the agenda of Novel and its Board nominees. The only area where a majority of the Board is aware of a material and continuing disagreement relates to Novel’s proposal to seek to reprice the conversion of the Series B preferred subject to obtaining a majority stockholder vote. A majority of the Board does not believe such repricing, to reflect the Company’s current stock price, to be in the best interests of the Company and a majority of its stockholders. Stealth Proxy Campaign Against Two Directors As discussed in some detail within Attachment II, the Company’s draft 8-K disclosure filing, it has been alleged that Novel has been working with Mr. Moore to create a stockholder “group” that is working in concert to cast “withhold” proxy votes for two of the Company’s independent director nominees at the Company’s 2026 Annual Stockholders Meeting. It is important to affirm that a proxy contest can be used to resolve fundamental strategic or governance disagreements is an appropriate option provided applicable U. S, laws are adhered to in the process. Stockholder activism is periodically necessary to redirect public companies away from failing strategies or entrenched interests. Public companies are owned by their stockholders and annual meetings are the established process for testing and ratifying existing governance agendas. But it is also essential to affirm that U.S. public companies are subject to multiple layers of laws and regulations concerning required and proper governance process and conduct. The layers and authorities include U.S. Federal securities laws, regulations of the Securities and Exchange Commission (“SEC”), rules set out by national exchanges such as the Nasdaq Stock Market, and by state jurisdictions, and for Iridex this means Delaware and California law. Please see Attachments I and II, the Memorandum of Law prepared by the Company’s outside counsel and the Company’s draft SEC filing, for a brief review of the legal rules and standards at issue in the Company’s current governance contest. American public companies incur millions in expenses annually complying with the myriad legally required standards, engaging accountants, auditors, legal counsel, and boards of directors. These experts and fiduciaries are charged with pursuing and delivering legal and ethical compliance. For public companies, the central standard of compliance and good governance is disclosure – public disclosure, to

all stockholders, of performance measurements, liabilities, risks, and intent. And, the annual stockholder meeting is the focal point of such governance disclosure and accountability. Thousands of rules govern proxy statements and proxy contests. These rule are not optional, they set out the required processes, and form the foundation of what good governance means. The above review of the vast legal and regulatory landscape and the material continuing costs public companies annually incur to comply with such requirements provides a lead into the simple argument that the proxy rules relating to the conduct of annual public company stockholder votes are not optional. A majority of Iridex’s Board hereby contend that Novel has been led far astray by people who either have a very weak understanding of the public company legal landscape or believe, to their eventual peril, that the rules do not apply to them. Novel appears to be currently aligned with a “group” of people adverse to the Company that likely: • failed to first inspect Iridex’s bylaws to discover the Company’s plurality voting standard; • did not understand what the plurality voting standard meant when they discovered it; • and, therefore, waited until it was already too late in the proxy process to raise the issue of plurality voting via legitimate board governance processes; • grossly violated federal proxy filing and solicitation rules; • coordinated with multiple other stockholders in an undisclosed “group” subjecting them all to potential liability and censor; and • violated numerous fiduciary duties, especially those concerning the use of confidential information, in the process sowing distrust that will make collaboration very difficult going forward. All of this done in what will be an entirely futile display – due to the Company’s plurality voting standard, there will be no change in the Company’s Board, but rather an investigation into, and disclosure of all, the laws and ethical standards breached. This was a spectacularly ill-considered campaign that benefits no one, harms the reputation and future prospects of all involved, including the Company, and creates the potential for serious liability for all those unaware or unwilling to abide by the federal and state law requirements surrounding the conduct of annual stockholder meetings and proxy contests. Next Steps The Company is very glad to have Novel as an investor and its affiliates as strategic partners. A majority of the Board believes it has leaned in and has worked very hard to be good partners. We have acceded leadership of strategic direction, adopted the “Novel strategy” for growth, and accepted that Novel’s support is a necessary precondition for any Company strategic initiative. We have developed

communication and reporting systems to ensure alignment. But, we also believe being a good partner means telling you when we think you are making serious mistakes. You will decide the path forward. You can work with a majority of the Board to quickly unwind the developing governance crisis, or you can remain adverse, following the lead of your Board nominee, Mr. Moore, whom a majority of the Board believes has been working to create friction, provoke disagreements when there should be none, and to destroy the productive alignment and collaboration between the Company and its largest stockholder. Having spent much of the last year attempting to minimize and placate Mr. Moore’s deeply questionable behavior, the recent exposure of his likely violation of fiduciary duties in pursuit of his tactically ignorant and objectively illegal proxy campaign has done nothing to change the Board composition but has embarrassed the Company and risks inflicting reputational harm to several of its Board members. When first confronted with discovery of his misdeeds, Mr. Moore unprovoked and repeatedly stated that resolution and recovery from this situation may require his resignation. A majority of the Board agrees, but that alone does not solve the problem. To resolve the current crisis amicably, Novel needs to change its proxy vote. Failure to do so will require the Company to file disclosure documents, including this letter, revealing the realities behind Mr. Moore’s misinformation campaigns involving first Novel and more recently the undisclosed “group” of stockholders with whom he has communicated into order to coordinate a stealth proxy campaign. We stand ready to hear your response, listen to your concerns, and to work with you to solve the current governance crisis and to improve the working relationship within our very important strategic partnership. Scott Shuda Iridex Chairman of the Board Patrick Mercer Iridex President and CEO Beverly Huss Iridex Independent Board Director

Attachment I MEMORANDUM Director Conduct in Unauthorized Stealth Proxy Solicitation: Fiduciary Duty and Federal Securities Law Considerations TO: IRIDEX Corporation Board of Directors FROM: Wilson Sonsini Goodrich & Rosati, P.C. RE: Fiduciary Duties Under Delaware Law and Potential Violations of Regulations 14A and 14C and Section 13(d) of the Securities Exchange Act of 1934 and Related Exposure of the Affiliated Appointing Stockholder DATE: July 2, 2026 I. Executive Summary The board of directors (“Board”) of IRIDEX Corporation (the “Company” or “Iridex”) has asked us to address two related but distinct sets of legal issues arising from the conduct of one of its five directors (the “Dissident Director”), who is believed to be: (i) communicating directly and privately with the Company's stockholders, (ii) disclosing confidential, non-public information about the Company and the Board's deliberations in the course of those communications, and (iii) urging or implying that stockholders should withhold votes from, or vote against, two of his fellow directors (the “Targeted Directors”) at the 2026 Annual Meeting of Stockholders (the “Annual Meeting”) — all without any public disclosure, board notice, or filings with the Securities and Exchange Commission (the “SEC”). This campaign has already produced a material increase in withhold votes against the Targeted Directors. In brief: • Delaware law. The Dissident Director's conduct, as described, implicates the duty of loyalty (including the duty of confidentiality and the prohibition on self-dealing), and may also implicate the duty of care and the duty of candor owed to fellow directors and to the corporation. A director who uses boardroom information obtained in confidence to wage a covert campaign against fellow directors, for personal ends, is on weak footing under settled Delaware fiduciary principles, even though directors generally have wide latitude to express disagreement and even to run their own slate in a proxy contest using proper channels. • Federal securities law under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). ◦ Regulation 14A. The Dissident Director's communications with stockholders, if they were “reasonably calculated to result in the procurement, withholding or revocation of a proxy,” constitute a “solicitation” under Rule 14a-1(l) of Regulation 14A, triggering SEC filing, disclosure, and compliance with anti-fraud obligations under Regulation 14A. Page 1 of 11

◦ Section 13(d). When a Dissident Director is acting in concert with other stockholders and has formed a “group” within the meaning of Section 13(d)(3), reporting obligations under Section 13(d) (Schedule 13D) are triggered by virtue of the group’s aggregate holdings — regardless, of how much the Dissident Director beneficially owns individually or through his affiliation with other Company stockholders. ◦ Risk to the Appointing Stockholder. The stockholder that appointed the Dissident Director and with whom it is affiliated in not a mere bystander. Depending on what the investigation reveals about its knowledge of, involvement in, or coordination with the Dissident Director’s campaign, Novel Inspiration International Co., Ltd. (the “Appointing Stockholder”) faces meaningful exposure of its own — including potential aiding-and-abetting liability for the Dissident Director’s fiduciary duty breaches, and “group” and “control person” liability under the federal securities laws. II. Summary of Relevant Facts The Company is a public company organized under the laws of the State of Delaware, with a five- member board of directors. For purposes of this memorandum, we have assumed the following additional facts: 1. The Dissident Director has, without Board authorization or knowledge, been communicating directly with stockholders of the Company regarding the Annual Meeting — communications that, as described herein, appear to have begun well in advance of the Board meeting during which the proxy statement was approved. 2. In those communications, the Dissident Director has disclosed confidential, non-public information concerning the Company and/or Board deliberations. 3. The Dissident Director has recommended, or implied that stockholders should, withhold votes from or vote against two of the other four directors (the “Targeted Directors”) in connection with their re-election. In direct conversation, the Dissident Director has confirmed as much, stating that his concern is not with other members of the Board but that his problem is specifically with the Targeted Directors. 4. Notwithstanding the foregoing, the Dissident Director voted in favor of, and raised no objection to, the nomination of the Targeted Directors as part of the slate of directors submitted to stockholders for election at the Annual Meeting — a vote that was unanimous and taken without debate or the presentation of any alternative candidates. 5. The Dissident Director has made no public disclosure of this activity and has not filed, or caused to be filed, any solicitation materials, exempt-solicitation notice, or other documents with the SEC in connection with these communications. 6. These communications have already resulted in a significant number of withhold votes being submitted against the Targeted Directors. Current vote tallies reflect this disparity in stark terms: the Dissident Director and the two directors affiliated with the Appointing Page 2 of 11

Stockholder are each receiving stockholder support in the range of 90%-96% of votes cast, while the Targeted Directors are on pace to receive stockholder support closer to 50% — an outcome that is inconsistent with any ordinary voting pattern and that warrants serious inquiry into its cause. 7. The Dissident Director was originally nominated for appointment to the Board at the request of, and is an affiliate of, the Appointing Stockholder, and the Dissident Director may reasonably be understood by stockholders to be acting as the Appointing Stockholder’s representative on the Board. 8. The Dissident Director’s campaign appears to have been premeditated. At a Board meeting held to approve the proxy statement, the Dissident Director raised, without prior notice, whether the Company had a majority vote standard for director elections. When informed that it did not, the Dissident Director argued that such a provision should be adopted and, when that effort failed, pressed the Targeted Directors directly and repeatedly to commit, verbally, that they would resign from the Board in the event they failed to receive a majority of votes cast. 9. The Dissident Director recently traveled to Asia and met with the Appointing Stockholder. Within days thereafter, the Appointing Stockholder cast its approximately 3.4 million shares against both Targeted Directors. That sequence gives rise to a compelling inference of coordination — one reinforced by the vote pattern described in paragraph 6 above and by the absence of any public disclosure by either the Dissident Director or the Appointing Stockholder of a plan to seek changes to the Board’s composition. 10. At least one additional significant stockholder, has cast its votes against both Targeted Directors and in favor of the other nominees — a pattern identical to the Appointing Stockholder’s vote and consistent with coordinated direction rather than independent judgement. 11. Taken together, the foregoing facts support a conclusion that the Dissident Director has for some time possessed knowledge that significant stockholder opposition to the Targeted Directors was developing — knowledge that predates the Board meeting at which he raised the majority-vote issue and sought verbal resignation commitments — and that such knowledge was the product of, or was accompanied by, communications with stockholders of the kind described in paragraphs 1 through 6 above. Page 3 of 11

III. Fiduciary Duties Under Delaware Law Delaware directors owe fiduciary duties to the corporation and its stockholders, not to any individual director, faction of stockholders, or constituency. Those duties are traditionally analyzed under two headings — the duty of care and the duty of loyalty — with candor and good faith treated as components or correlates of those two core duties. The facts described above implicate primarily the duty of loyalty, though the duty of care and the special duties directors owe to one another in their conduct of board business are also relevant. The Dissident Director previously joined his fellow directors in approving the slate of nominees that included the Targeted Directors, and only later — without disclosing any change of view to the Board — began organizing a covert campaign to defeat the very nominees he had voted to put forward. A director who casts his vote in favor of a board-approved slate and then secretly works to undermine that same slate, rather than raising his objections candidly within the boardroom or pursuing a properly disclosed proxy contest, may be subject to severe censure. That sequence of events — public assent followed by private sabotage — is itself probative of bad faith and sharpens each of the fiduciary concerns discussed below, because it shows the Board and the Company relied on the Dissident Director's apparent support in proceeding with the slate as approved. On the facts as described, the Director's conduct presents several significant, and potentially overlapping, fiduciary violations: A. Violation of the Duty of Disclosure (Candor) Directors owe a duty of complete candor to the corporation and to their fellow board members. This duty requires directors to deal honestly with one another regarding matters affecting the corporation's governance and to refrain from withholding information that the Board, acting collectively, would reasonably need in order to discharge its own duties. Intentionally withholding material information — such as the fact that a sitting director is actively organizing a campaign to alter the Board's composition — is a direct omission of the truth and a serious violation of the trust the Board and the Company are entitled to place in each of its members. This is particularly acute where, as here, the Dissident Director continued to participate in board meetings, executive sessions, and committee work alongside the Targeted Directors while concealing his contrary agenda, depriving the Board of the opportunity to address his concerns directly, to seek his recusal from matters where his interests had become adverse, or to take any other appropriate governance steps. B. Misuse of Corporate Information Directors have access to non-public, confidential corporate information — board minutes, management presentations, financial projections, strategic plans, and the substance of deliberations and executive sessions — solely by virtue of their office, and that information belongs to the corporation rather than to any individual director personally. Using that insider status to quietly orchestrate an opposition campaign against fellow directors constitutes a Page 4 of 11

misappropriation of company information for an unauthorized, personal purpose. This is true even though the Dissident Director, like any stockholder, is generally free to express disagreement with the Board's direction or to seek to replace fellow directors through a proper, disclosed proxy contest. The problem is not that the Dissident Director disagrees; it is that he has used confidential information obtained solely by virtue of his board seat — withheld from his fellow directors and from the Company — to advance a personal campaign for control of two board seats. C. Breach of the Duty of Loyalty Directors must act in good faith and in the best interests of the corporation as a whole, not in furtherance of a personal or private agenda. Undermining the Board's collective, vetted decisions in secret — here, the Board's decision to nominate the Targeted Directors, which the Dissident Director himself approved — prioritizes a private agenda over corporate stability and is squarely a duty-of-loyalty problem, not merely a matter of indiscretion or poor judgment. A director who uses confidential information to entrench his own position, expand his influence, or remove directors who may oppose him is acting for personal benefit in a manner adverse to the corporation, implicating the core of the duty of loyalty even absent a classic self-dealing transaction. Delaware case law applying the duty of loyalty to directors who misuse confidential corporate information for personal advantage — including in the context of competing for corporate control or advancing a personal slate — treats such conduct as a breach of fiduciary duty. D. Duty of Care Although the principal concern here is loyalty and candor, the duty of care may also be implicated to the extent the Dissident Director's conduct reflects a broader pattern of inattention to, or disregard for, his obligations as a director — for example, if confidential information was disclosed carelessly, or if the Dissident Director failed to inform himself adequately before making representations to stockholders about Company matters. Delaware's business judgment rule will ordinarily protect good-faith, informed director decisions; it does not protect conduct outside the scope of loyal, good-faith director decision-making, and in any event the business judgment rule presupposes the absence of a disabling conflict of interest of the kind discussed above. E. Whose Duties Run to Whom It bears emphasis that director fiduciary duties under Delaware law run to the corporation and the stockholders as a whole — not to any individual stockholder, slate, or faction, and not to a director's personal view of the corporation's best interests when that view conflicts with his obligation to act through proper, disclosed channels. A director who believes the Board, or particular directors, should be replaced has legitimate avenues available — raising the issue at the Board level, requesting a special meeting, communicating concerns to the full Board or a committee, or, if he wishes to take the matter to stockholders, doing so openly and in compliance with the federal proxy rules discussed further in Section IV below, including by resigning or recusing himself from confidential discussions to the extent his interests have become adverse to the Board's. Page 5 of 11

F. Available Corporate Remedies If, after investigation, the Board concludes that the Dissident Director has breached his fiduciary duties, potential remedies and responses include: • Cease-and-desist communication to the Dissident Director, demanding that further unauthorized solicitation and disclosure of confidential information stop immediately, and reserving all rights. • Corrective public disclosure and stockholder communication by the Company to address any material misstatements or omissions in the Dissident Director's communications and to give stockholders complete and accurate information before they vote. • Civil claims against the Dissident Director for breach of fiduciary duty, including potential claims for injunctive relief, damages, and disgorgement of any benefit obtained through the breach. • Removal from the Board. Under Delaware General Corporation Law (“DGCL”) § 141(k), directors of a corporation without a classified board generally may be removed by stockholders, with or without cause. • Indemnification and insurance considerations. Breach of the duty of loyalty or conduct not in good faith is typically excluded from indemnification and insurance coverage under the DGCL and standard director and officer insurance policies and indemnification agreements. IV. Potential Federal Securities Law Violations The Dissident Director's conduct, as described, also raises significant issues under the federal proxy rules and the beneficial ownership reporting rules of the Exchange Act. Public company director elections are strictly regulated by the SEC. The SEC's proxy rules are built around three core objectives: full disclosure, market integrity, and stockholder transparency. Conducting and concealing a coordinated effort to influence a stockholder vote bypasses the mandatory disclosures required by Schedule 14A and circumvents the very purpose those rules serve. As discussed below, an unannounced campaign of this kind potentially violates not only the general anti-fraud and filing provisions of Regulation 14A, but specifically Rule 14a-3 (which prohibits furnishing a proxy statement, or soliciting at all, without first providing stockholders the required Schedule 14A disclosure) and Rule 14a-6 (which requires the soliciting party to file its proxy statement and other soliciting materials with the SEC, in most cases in preliminary form before distribution to stockholders). Page 6 of 11

A. Regulation 14A — The Proxy Solicitation Rules 1. “Solicitation” Is Defined Broadly Rule 14a-1(l) under the Exchange Act defines “solicitation” and “solicit” expansively to include not only requests for a proxy, but any request to execute, not execute, or revoke a proxy, and - critically - any communication to security holders “under circumstances reasonably calculated to result in the procurement, withholding or revocation of a proxy.” The SEC and the courts have construed this definition to reach communications that do not in terms ask for a proxy card but are nonetheless designed or reasonably likely to influence how stockholders vote, including communications recommending that stockholders withhold votes from, or vote against, particular director nominees. Based on the facts described above - private communications to stockholders, disclosing Company information, recommending or implying that stockholders withhold votes from the Targeted Directors, undertaken in the run-up to the Annual Meeting, and already correlated with a measurable shift in voting behavior — the Director's communications likely constitute a “solicitation” within the meaning of Rule 14a-1(l), regardless of how the Dissident Director may have privately characterized them. This conclusion does not depend on the medium used. If a director communicates with stockholders — whether through private emails, text messages, phone calls, or in-person meetings such as one-on-one or small-group dinners — urging them to “vote no” or to withhold votes from peer directors, that communication legally constitutes a proxy solicitation regardless of its informal or private character. Taking that action without first filing the proxy statement required by Schedule 14A, and without satisfying Rules 14a-3 and 14a-6, violates the Exchange Act. The fact that a solicitation is conducted quietly, through informal or one-to-one channels, does not exempt it from Regulation 14A; if anything, the deliberately private and undisclosed nature of the Dissident Director's outreach — conducted outside any public forum and without any filed soliciting materials — cuts against any argument that the conduct was simply informal or inadvertent. Because the Dissident Director's apparent campaign was not preceded by any filed proxy statement or exempt-solicitation notice, the votes obtained through that campaign were procured in violation of the federal proxy rules. A covert solicitation conducted in violation of Regulation 14A creates a meaningful risk that the withhold votes thereby obtained could be challenged and potentially invalidated or disregarded in connection with the vote count for the Annual Meeting. 2. Filing and Disclosure Obligations Triggered by a Solicitation Absent an applicable exemption, a person who solicits proxies is required to furnish stockholders with a proxy statement meeting the disclosure requirements of Schedule 14A (Rule 14a-3) and to file that proxy statement, and other soliciting materials, with the SEC (Rule 14a-6), including, in a contested election, complying with the particular requirements for contested solicitations under Page 7 of 11

Rule 14a-12 and the related provisions governing director-nominee disclosure (e.g., Schedule 14A Item 5, requiring disclosure of the soliciting person's interests, arrangements, and any “substantial interest, direct or indirect” in the matters to be acted upon). No available exemption permits the Dissident Director to avoid these obligations. The exemption most likely to be invoked — Rule 14a-2(b)(1), which exempts solicitations by persons who do not seek proxy authority — is expressly unavailable to the Dissident Director on at least two independent grounds: first, Rule 14a-2(b)(1) (iv) categorically excludes any nominee for whose election proxies are being solicited, and the Dissident Director is himself a nominee on the Company’s slate; second, Rule 14a- 2(b)(1)(vi) excludes any person required to report beneficial ownership on a schedule 13D in connection with a contested solicitation for the election of directors — which, as discussed in Section IV.B below, the Dissident Director’s conduct has triggered. 3. Rule 14a-9 — Anti-Fraud Provision Independent of the filing question, Rule 14a-9 prohibits false or misleading statements, or omissions of material fact, in any communication, written or oral, that constitutes a solicitation. If the Dissident Director's communications included inaccurate characterizations of the Targeted Directors' conduct, the Company's affairs, or the confidential information disclosed, or omitted material facts necessary to make the statements made not misleading (for example, omitting the Director's own conflicting interest in unseating the Targeted Directors), those communications could separately violate Rule 14a-9, exposing the Dissident Director to SEC enforcement risk and, potentially, private liability. 4. Materiality and Insider Trading Considerations If the confidential Company information the Dissident Director disclosed was material and non- public, its disclosure to stockholders raises selective-disclosure and “tipping” concerns under Rule 10b-5 and Regulation FD considerations for the Company. Any recipient stockholder who traded the Company's securities while in possession of such information could face independent trading liability, and the Dissident Director could face tipper liability. B. Section 13(d) — Beneficial Ownership and “Group” Formation Section 13(d) of the Exchange Act and the rules thereunder require any person (or “group”) that acquires beneficial ownership of more than 5% of a class of an issuer's registered equity securities to file a Schedule 13D within the time period specified by the rule, disclosing, among other things, the purpose of the acquisition and any plans or proposals relating to (i) an extraordinary corporate transaction, (ii) a change in the board of directors, including “plans or proposals to change the number or term of directors or to fill any existing vacancies on the board,” and (iii) other enumerated matters (Schedule 13D, Item 4). A Schedule 13D, once filed, must be promptly amended to reflect any material change in the facts set forth in the schedule, including a material change in purpose or plans. Page 8 of 11

When two or more stockholders act together to acquire, hold, or vote securities for the purpose of influencing or changing control of the issuer — which expressly includes acting in concert to replace directors — they are deemed to be a “group” under Section 13(d)(3), and the group's combined holdings, not any single member's individual position, are tested against the 5% threshold. Two distinct issues arise on these facts: • The Dissident Director's own position. If the Dissident Director individually beneficially owns more than 5% of the Company's relevant class of voting securities (or is affiliated with the Appointing Stockholder, which is the case here), his undisclosed campaign to change the composition of the Board — a “plan or proposal” to effect a change in the board within the meaning of Item 4 of Schedule 13D — would likely require him to file an initial Schedule or to promptly amend any existing Schedule 13D to reflect his change in purpose from passive to control-oriented, and to disclose the plan to seek the removal or non-re-election of the Targeted Directors. • “Group” formation with other stockholders. If the Dissident Director is coordinating with one or more stockholders — even informally, through an agreement, arrangement, or mutual understanding to act in concert toward unseating the Targeted Directors — a “group” may have been formed. If the group's aggregate, collective voting power exceeds 5% of the Company's outstanding equity, the group is obligated to publicly file a beneficial ownership report on Schedule 13D (or to amend an existing filing) disclosing its composition, aggregate ownership, and the plan to seek changes to the Board, generally within the time period required by the rule. The SEC has actively pursued enforcement in this area in recent years, including against investors who coordinate proxy-related activity without making required Section 13(d) group disclosures, particularly in the context of activist campaigns conducted through informal coordination intended to stay under the radar of public disclosure. Failing to file, or intentionally concealing the existence of, a Section 13(d) group can expose the Dissident Director (and any coordinating stockholders) to significant SEC enforcement risk. The SEC has shown a willingness to seek injunctions compelling corrective disclosure, civil monetary penalties, and, in appropriate cases, trading bans or other restrictions on the non-compliant parties, in addition to the disgorgement and officer-and-director-bar remedies generally available to the SEC in enforcement actions. C. Potential Consequences of Non-Compliance Failure to comply with Regulation 14A's filing and anti-fraud provisions, and with Section 13(d)'s reporting requirements, can result in SEC enforcement action (including injunctive relief, civil penalties, and officer-and-director bars in appropriate cases), private litigation (courts have recognized an implied private right of action for violations of Section 14(a) and Rule 14a-9), and, in the Section 13(d) context, courts have at times granted injunctive relief, including barring the non-compliant party from voting shares or further soliciting, until corrective disclosure is made. Page 9 of 11

The Company itself may also have standing to seek injunctive relief against the Dissident Director to halt further violations and compel corrective disclosure, particularly given the timing related to reconvening the Annual Meeting and the demonstrated effect on the vote. V. The Stockholder That Appointed and Is Affiliated with the Dissident Director is at Risk The facts already established give rise to meaningful legal exposure now—not contingent on further investigation. The Dissident Director is the Appointing Stockholder’s affiliate and its designee. The Dissident Director met with the Appointing Stockholder in Asia immediately before the Appointing Stockholder cast 3.4 million votes against the Targeted Directors. The Appointing Stockholder’s existing Schedule 13D with respect to the Company does not disclose a campaign to change the Board’s composition. On these facts alone, the Appointing Stockholder faces the exposure described below. The Dissident Director did not arrive on the Board on his own. He was nominated for appointment at the request of, and remains affiliated with, the Appointing Stockholder, and that stockholders and the market may reasonably view him as the Appointing Stockholder's representative on the Board. That affiliation matters: it means the Appointing Stockholder itself — not just the Dissident Director individually — bears meaningful legal risk for the Dissident Director's conduct, particularly to the extent the investigation shows the Appointing Stockholder knew of, directed, financed, or otherwise participated in the campaign. A. Imputation and Knowing Participation in the Dissident Director's Breach As a general matter, the wrongful conduct of a board designee is not automatically attributed to the stockholder that appointed him; a designee director owes his fiduciary duties to the corporation and all stockholders, not to his appointing stockholder, and is expected to exercise independent judgment. That said, where an appointing stockholder is shown to have directed, encouraged, financed, or knowingly facilitated its designee's breach of fiduciary duty, the appointing stockholder steps outside the role of a passive principal and exposes itself to direct liability. Delaware law recognizes a cause of action against a third party who knowingly participates in a fiduciary's breach of duty, sometimes framed as aiding and abetting a breach of fiduciary duty. The elements generally require: (i) the existence of a fiduciary relationship (here, the Dissident Director's duties to the Company), (ii) a breach of that duty (addressed in Section III above), (iii) knowing participation in the breach by a non-fiduciary third party, and (iv) resulting damages. An appointing stockholder that was aware of, encouraged, or coordinated the Dissident Director's covert campaign — rather than merely receiving information from him after the fact — is at meaningful risk of satisfying this standard, particularly given the close affiliation between the Dissident Director and the Appointing Stockholder and the obvious alignment between the campaign's objective (unseating the Targeted Directors) and the Appointing Stockholder's own interest in board composition. B. “Group” Status and Derivative Section 13(d) Exposure Page 10 of 11

The affiliation between the Director and the Appointing Stockholder is also highly relevant to the Section 13(d) “group” analysis discussed above. A coordinated effort by a sitting designee director and his appointing stockholder to engineer a particular board outcome is close to a paradigmatic example of two or more persons acting together for the purpose of influencing control of the issuer. If the Dissident Director's campaign was undertaken with the knowledge, encouragement, or assistance of the Appointing Stockholder, that is strong evidence that the two are acting as a Section 13(d)(3) group, regardless of whether they ever executed a formal agreement. If their combined beneficial ownership exceeds 5% of the Company's outstanding voting securities, both the Dissident Director and the Appointing Stockholder — as members of the group — would be jointly responsible for the group's Schedule 13D filing and amendment obligations, and both would bear exposure for the group's failure to file or for any material omissions in the Appointing Stockholder's own existing Schedule 13D with respect to the Company (including, potentially, a failure to disclose the change in purpose from passive to control-oriented reflected in the campaign). C. Control Person Liability Under Section 20(a) of the Exchange Act Separately, Section 20(a) of the Exchange Act imposes joint and several liability on any person who “controls” a person liable for a violation of the Exchange Act (including violations of Section 14(a), Rule 14a-9, and Section 13(d)), unless the controlling person acted in good faith and did not directly or indirectly induce the act or acts constituting the violation. Whether the Appointing Stockholder is a “controlling person” of the Director for these purposes is a fact-specific inquiry that would typically consider the closeness of the affiliation, any contractual or governance rights the Appointing Stockholder holds over the Director (e.g., a right to designate, remove, or replace him), and the degree to which the Director's conduct was directed or influenced by the Appointing Stockholder. To the extent the facts support a control relationship and the Appointing Stockholder cannot establish the good-faith/non-inducement defense, it could face direct liability, alongside the Director, for the underlying securities law violations discussed in Section IV. VI. Conclusion The conduct described — a director's covert, undisclosed use of confidential corporate information to solicit stockholders against fellow directors, without complying with the federal proxy or beneficial ownership reporting rules — raises serious issues under both Delaware fiduciary duty law and the federal securities laws. The risk does not stop with the Dissident Director; depending on what the investigation shows about its knowledge of and participation in the campaign, the stockholder that appointed him and remains affiliated with him may bear independent exposure under Delaware aiding-and-abetting principles and Section 13(d) group and control person liability. We recommend the Board treat this matter with urgency given the proximity of the Annual Meeting and the documented effect on the vote to date, and that it proceed promptly to investigate the facts, secure independent advice, and determine an appropriate response to the Dissident Director’s conduct. Page 11 of 11

Attachment II (Intentionally Omitted)

Attachment III Financial Highlights - Driving Towards Profitability in 2026 CPT Restructuring Progress Q1’24 vs. Q3’25 P&L Progression Q1’24 vs. Q3'25 66710 • Reduced OPEX by $2.3M, or 30%, through restructuring initiatives • Increased Revenue by $0.7M, 6%, over the same period Q1'24 Q3' 25 Change • Reduced Operating Losses by $1.9M, 57% 14,000 12,484 11,761 • Continuing cost-savings initiatives and planning to be 12,000 Operating Income positive and Cash Flow positive in 10,000 7,751 2026 8,000 5,424 6,000 • Cash Balance of $5.6M as of Q3’25 4,000 1,881 2,000 722 0 Preliminary 4Q'25 and Full Year 2025 Results (2,000) (1,411) • Total 4Q’25 Revenue of $14.6-$14.8M, 15-17%, over the (2,326) (4,000) (3,293) same period (6,000) Total Revenue OPEX Operating Income • Total Full Year 2025 Revenue of $52.5-52.7M, 8%, over the same period • Achieved positive cash flow • Expects to achieve positive adjusted EBITDA for Full Year 2025 1 $ In Thousands