MOST MORTGAGE DEPOSITOR, LLC ABS-15G

Exhibit 99.1

EXECUTIVE NARRATIVE:

This Executive Summary summarizes the independent third-party due diligence review (the “Review”) conducted on 476 reverse mortgage loans by inTENT Fulfillment, Inc. (“inTENT”) on behalf of its Client, Mutual of Omaha Mortgage, Inc. (“Client”).

inTENT’s reports, which are to be made available to the recipient by the Client, include the loan-level results of inTENT’s independent, third-party due diligence review conducted for the Client.

inTENT performed certain due diligence services described below on residential mortgages. The review was conducted on behalf of Client starting in May of 2026 and completed in July of 2026 via file images provided by the Client for the review.

DESCRIPTION OF SERVICES:

inTENT was instructed to perform a credit, data validation, and valuation review (the “Review Population”) in accordance with national recognized statistical rating organizations (“NRSRO(s)”) review standards in place as of the review date.

SAMPLE SIZE OF THE ASSETS REVIEWED:

The diligence review (the “Review”) was conducted by inTENT on 100% of the Reverse Mortgage Loans.

LOAN SAMPLING:

The population, to our knowledge, represents all of the reverse mortgage Loans in the securitization population.

The table below summarizes the reviews conducted by inTENT:

| Review | Reviewed Total | % of Sample |

| Data Integrity Population | 476 | 100.00% |

| Credit Population | 476 | 100.00% |

| Valuation Population | 476 | 100.00% |

DATA INTEGRITY:

Where available, inTENT compared the data fields below on the bid tape provided by the Client to the data found in the actual file as captured by inTENT. This information may not have been available for all mortgage loans. This comparison included the following data fields:

| Secure Equity | |||

| Borrower Last Name | Borrower First name | Borrower Gender | Borrower DOB |

| Borrower Median FICO (if applicable) | Co-Borrower Last Name | Co-Borrower First Name | Co-Borrower Gender |

| Co-Borrower DOB | Co-Borrower Median FICO (if applicable) | Sales Price (Purchase loan) | Appraisal 1 Effective Date |

| Appraisal 1 Value | Appraisal 2 Effective Date | Appraisal 2 Value | Desk Review (CDA) Report Date |

| Desk Review (CDA) Value | Property Street Address | Property City | Property State |

| Property Zip Code | Property Type | Closing Date | Funding Date |

| Beginning Interest Rate | Original Principal Limit | Payment Type | Original Repair Set Aside |

| Original Tax and Insurance Set Aside | Status | Interest Rate as of Cut-Off Date | Max Claim Amount |

| UPB | |||

| FHA Underwritten Mortgage Loans | |||

| Borrower Last Name | Borrower First name | Borrower Gender | Borrower DOB |

| Borrower Median FICO (if applicable) | Co-Borrower Last Name | Co-Borrower First Name | Co-Borrower Gender |

| Co-Borrower DOB | Co-Borrower Median FICO (if applicable) | Sales Price (Purchase loan) | Property Street Address |

| Property City | Property State | Property Zip Code | Property Type |

| Closing Date | Funding Date | Beginning Interest Rate | Original Principal Limit |

| Payment Type | Original Repair Set Aside | Original Tax and Insurance Set Aside | Max Claim Amount |

| UPB | MIP Rate | FHA Case Number | Due & Payable Appraisal Amount |

| Due & Payable Appraisal Date | FCL Appraisal Date | FCL Appraisal Value | Short Sale Appraisal Date |

| Short Sale Appraisal Value | DIL Appraisal Date | DIL Appraisal Value | Origination Appraisal Effective Date |

| Origination Appraisal Value | Due and Payable Date | Status | Interest Rate as of Cut-Off Date |

| MIC Endorsement Date | First Legal Endorsement Date | Foreclosure Sale Date | |

Additionally, inTENT verified (i) listed borrowers signed documents requiring signature, (ii) borrowers signing documents were sixty-two (62) years or older at the time of origination, sixty (60) years or older at the time of origination, or fifty-five (55) years or older at the time of origination, as provided in the related underwriting guidelines, (iii) that all riders required by the terms of the mortgage and mortgage note were attached to the respective document, (iv) that social security numbers across documents were consistent, and (v) that the calculated residual income was used in the assessment of the Life Expectancy Set-Aside Amount.

CREDIT UNDERWRITING:

For each residential mortgage loan, inTENT performed a credit and guideline review utilizing the applicable specific guidelines furnished at the time of the review by Client. The review requirements generally included:

Verification that the characteristics listed below on the mortgage loan and borrower conform to the Client’s requirements:

| ● | LTV/CLTV |

| ● | Representative Credit Score |

| ● | Employment |

| ● | Income |

| ● | Assets |

| ● | Borrower Type (Citizenship) |

| ● | Loan Amount |

| ● | Loan Purpose |

| ● | Occupancy |

| ● | Property Type |

| ● | Note any Exception Approvals or waivers by the originator |

As part of the guideline review, inTENT performed a credit analysis during which various documents within the loan file were examined, as applicable:

● Loan Application - inTENT reviewed the application for: (i) was signed by all listed borrowers, and (ii) was substantially filled out

● Occupancy - inTENT confirmed the property occupancy is consistent with the mortgage loan approval and borrowers’ application disclosure based solely on information contained in the mortgage loan file and any fraud/background report obtained in connection with the mortgage loan.

● Employment documentation (VVOE, WVOE, The Work Number) – inTENT reviewed the employment documentation provide for the borrower(s) to support current and/or past employment as required.

● Income documentation – inTENT reviewed and calculated income using all income documentation provided for each borrower.

● Tax Transcripts (IRS Form 4506-T) – If Tax Transcripts were provided, inTENT compared the Tax Returns and/or W2 to verify income amounts are supported and accurate.

● Entity Document – For loans made to a Business Entity, inTENT reviewed the Certificate of Good Standing, Articles, Bylaws/Operating Agreement and other Entity Documents for compliance with the applicable guidelines.

● Asset Documentation - inTENT reviewed the asset documentation provided in the loan files to the applicable guideline requirements. Utilizing this documentation, inTENT completed a review of sufficient cash to close and reserve calculation

● Letters of Explanation – inTENT reviewed any letter provided for employment or credit

● Credit Report - Client provided the credit report for each borrower used at origination and inTENT reviewed the credit profile & representative credit score for adherence to applicable guidelines

● Fraud Report/Background Check – inTENT reviewed documentation for any red flags or alerts. If there were any high level or critical warning, we looked to ensure these were addressed. If the Fraud Report or Background check was not in the loan file, a material Finding was triggered.

● Title – inTENT Reviewed and confirmed borrower name(s), chain of title, Loan policy amount, lien holder position, look for discrepancies, delinquent taxes, and/or additional liens at time of consummation, based on applicable guideline requirements. Checked that the real estate taxes have been noted in Title or other RE Tax Form were paid as directed by applicable guidelines and closing instructions

● Insurance - inTENT reviewed the insurance was present on the mortgage loan, as applicable per guidelines. Reviewed each mortgaged property had a policy in place and proper coverage amount in adherence to the applicable underwriting guidelines. Checked the lender’s name and it included “its successors and assigns,” confirmed that the premium amount on both the hazard insurance and flood insurance are included in the DTI calculations.

● Flood Certification - inTENT reviewed Flood Certification to determine if Flood Insurance was required. Checked the Name, Address, and verified Life of Loan. If in a Flood Zone, reviewed for presence of Flood Insurance.

● Reverse Mortgage Counseling - inTENT reviewed the file to determine if the Certificate of Reverse Mortgage Counseling was in the file and executed by the borrower(s).

● FACTA Disclosure - inTENT reviewed the file to determine if the Disclosure was in the file.

● Financial Assessment Worksheet – inTENT reviewed the file to determine if the worksheet was in the file and complete.

● Occupancy Certification – inTENT reviewed the file to determine if the Certificate was in the file and executed.

● Condominium Documentation – inTENT reviewed the Condo Questionnaire, Master Insurance Policy, and other Condo Docs for compliance to applicable guideline requirements

● Closing Documents - (including Note, Mortgage/Deed of Trust and any Riders or Addendums, Loan Agreement, Guaranty and/or CD/Settlement Statements/Final HUD-1) - inTENT reviewed the closing documents are present and complete (all pages), Borrower(s) names, Subject Property Address, Legal description, Signed by Borrowers

VALUATION REVIEW SCOPE:

For each residential mortgage loan, inTENT performed the following origination appraisal analysis:

| ● | Verified that the mortgage loan file contained an appraisal report (if required) and that it met the following criteria that conformed to the Client’s applicable underwriting guidelines: |

○ Appraisal report used standard GSE forms, appropriate to the property type:

- FNMA 1004/FHLMC 70 – Uniform Residential Appraisal Report. Used for 1-unit properties, units in planned unit developments (detached PUDs) and condominium projects that consist solely of detached dwelling (site condominium)

- FNMA 1073/FHLMC 465 – Individual Condominium Report. Used to appraise a unit in a condominium project or a condominium unit in a PUD (attached PUD)

- FNMA 1025/FHLMC 72 – Small Residential Income Property Appraisal Report. Used for all two-to-four unit residential income properties, including two-to-four-unit properties in a PUD

- FNMA 2000/FHLMC 1032 – One Unit Residential Appraisal Field Review

- FNMA 2000a/FHLMC 1072 – Two to Four Unit Residential Appraisal Field Review

○ Appraisal report was reasonably complete and included:

| - | Appraisal report form, certification, statement of limiting conditions and scope of work |

| - | Accurate identification of the subject property |

| - | Accurate identification of the subject loan transaction |

| - | Accurate identification of the property type, in both land and improvements |

○ All required attachments including:

| - | Subject front, rear and street photos and valued features |

| - | Subject interior photos – kitchen, all baths, main living area, updates/upgrades, deferred maintenance |

| - | Photos of all comparable sales and listings |

| - | Location map |

| - | Exterior sketch of property with dimensions |

| - | 1004MC Market Conditions Report |

○ Evidence that appraisal report was made “As Is” or provided satisfactory evidence of completion for all material conditions

○ Appraisal date met supplied Sponsor Acquisition Criteria

○ If applicable to Sponsor Acquisition Criteria requirements, a second full appraisal was furnished and met Sponsor Acquisition Criteria

| ● | Performed a general credibility assessment of the results of the appraisal per Title XI of FIRREA and USPAP based on the following criteria: |

○ Title XI of FIRREA:

○ If the appraisal was completed by a trainee or licensed appraiser unqualified to independently sign the report, an appropriately licensed appraiser co-signed as a supervisory appraiser and inspected the property

○ Determine that either the appraiser or supervisory appraiser was appropriately licensed by verifying the appraiser’s license included in the appraisal.

| ● | Reviewed for the presence of any “red flags” related to the mortgaged property that may have posed a risk to the property or occupants or USPAP |

○ Confirmed that the appraiser developed and communicated his / her analysis, opinion, and conclusion to intended users of their services in a manner that is meaningful and not misleading and that the appraisal is signed.

○ Property was complete. However, if the property was not 100% complete, then any unfinished portion had no material impact to the value, safety, soundness, structural integrity, habitability, or marketability of the subject property

○ Appraisal was reviewed for any indication of property or marketability issues. Utilized the following key points in making determination:

| - | Appraisal was made on an “As Is” basis or provides satisfactory evidence of completion of all material conditions |

| - | Property usage was reviewed for zoning compliance |

| - | Property utilization was reviewed to determine it was “highest and best use” |

| - | Neighborhood values were reviewed to determine if declining |

| - | Market conditions were reviewed to determine indication of possible marketability issues: |

| ■ | Location |

| ■ | % built up |

| ■ | Growth rate |

| ■ | Demand/supply |

| ■ | Marketing time |

| ■ | Predominant occupancy |

| - | Physical condition of the property was reviewed to determine that the property condition was average or better |

| - | Style of property was reviewed to determine if unique property |

| - | Any health and safety issues were noted and/or remediated |

| - | Locational and/or environmental concerns adequately addressed if present |

| ● | Property Eligibility Criteria – inTENT reviewed the property to determine that the property met the client supplied eligibility requirements. Examples of ineligible property types may include, but are ultimately determined by the Client’s applicable underwriting guidelines: |

○ 3 to 4 unit owner occupied properties

○ 2 to 4 unit second homes

○ Unwarrantable or limited review condominiums

○ Manufactured or mobile homes

○ Condotel units

○ Unique properties

○ Working farms, ranches or orchards

○ Mixed-use properties

○ Properties subject to existing oil or gas leases

○ Properties located in Hawaii Lava Zones 1 and 2

○ Properties exceeding Sponsor Acquisition Criteria requirements for excess acreage

Underwriter Accepted Value represents the value to be used for loan value determination and calculation of the loan amount. In scenarios where one appraisal is required for the loan, the appraised value, or the adjusted value by the Underwriter or Appraisal Review Department, was used for the Underwriter Accepted Value. In scenarios where more than one appraisal is required, the lower of the two appraised values, or the adjusted value by the Underwriter or Appraisal Review Department, was used for the Underwriter Accepted Value.

Client provided the 3rd party valuation product (Desk Review/CDA and/or Field Review) to be used in the waterfall.

For the FHA-underwritten mortgage loans, the appraisals were submitted through the Electronic Appraisal Delivery (EAD) portal, which performs a risk assessment of the appraisal data and validates compliance with FHA requirements. The EAD appraisal logging results reflected an approval status with no conditions cited, indicating the appraisals satisfied FHA’s review requirements. Based on this review, the appraisals were determined to adequately support the concluded property values. In addition, no conditions were identified that would require a second appraisal under applicable FHA guidelines.

FEMA:

inTENT confirmed whether the property is located in an area that was listed as a FEMA disaster zone post origination, and if so, whether a post-disaster property inspection was obtained confirming there is no damage to the property.

VALUATION REVIEW WATERFALL:

inTENT applied a cascade methodology to determine if the Underwriter Accepted Value was reasonably supported when compared to an independent third-party valuation product. Loans will be held to a -10% tolerance utilizing the following waterfall:

| ○ | Second full appraisal in file within 10% to the Underwriter Accepted Value - no additional product will be ordered |

| ○ | FHA EAD (Electronic Appraisal Delivery) confirmation that a second appraisal was not required |

| ○ | Desk Review |

| ○ | Field Review |

Client expressly understands and agrees that inTENT makes no representation or warranty as to the value of any mortgaged property, notwithstanding that inTENT may have reviewed valuation information for reasonableness. inTENT is not acting as an “AMC” (Appraisal Management Company) and therefore it does not opine on the actual value of the underlying property. inTENT is not a creditor within the meaning of ECOA or other lending laws and regulations and therefore inTENT will not have any communication with or responsibility to any individual consumer concerning property valuation.

NRSRO GRADING CRITERIA:

Upon completion of the loan file review, inTENT assigned grading which considered factors based on the review criteria, product, and NRSRO requirements. The NRSRO criteria referenced for this report and utilized for grading descriptions is based upon the following:

| CREDIT EVENT GRADE | |

| A | The loan conforms to all applicable credit guidelines, no conditions noted. |

| B | The loan does not meet every applicable credit guideline, however most of the loan characteristics are within the guidelines and there are documented and significant compensating factors. |

| C | The loan does not meet every applicable credit guideline, and most loan characteristics are outside guidelines; or there are weak or no compensating factors. |

| D | The loan file is missing critical documentation required to perform the review. |

| VALUATION EVENT GRADE | |

| A | The loan conforms to all applicable property valuation guidelines, the appraisal was thorough and complete, and the appraised value appears to be supported |

| B | The loan does not meet every applicable property valuation guideline, however most of the loan characteristics are within the guidelines and there are documented and significant compensating factors. |

| C | The loan does not meet every applicable property valuation guideline; the appraisal was not thorough and complete; and/or the appraised value does not appear to be supported. |

| D | The file was missing the appraisal or there was insufficient valuation documentation to perform a review. |

| OVERALL EVENT GRADE | |

| A | Loan meets Credit and Valuation guidelines and has sufficient accuracy and completeness of data to conduct a thorough review. |

| B | The loan substantially meets published Client/Seller guidelines and/or eligibility in the validation of income, assets, or credit; is in material compliance with all applicable laws and regulations; and the value and valuation methodology are supported and substantially meet published guidelines. |

| C | The loan does not meet the published guidelines; and/or violates one material law or regulation; and/or the value and valuation methodology is not supported or did not meet published guidelines. |

| D | The loan file is missing critical appraisal or other valuation method documentation required to perform the review. |

FINDINGS SUMMARY:

| OVERALL REVIEW RESULTS | ||

| NRSRO Grade | Count | % of Loans Reviewed (by count) |

| A | 476 | 100.00% |

| B | 0 | 0.00% |

| C | 0 | 0.00% |

| D | 0 | 0.00% |

| CREDIT REVIEW RESULTS | ||

| NRSRO Grade | Count | % of Loans Reviewed (by count) |

| A | 476 | 100.00% |

| B | 0 | 0.00% |

| C | 0 | 0.00% |

| D | 0 | 0.00% |

| VALUATION REVIEW RESULTS | ||

| NRSRO Grade | Count | % of Loans Reviewed (by count) |

| A | 476 | 100.00% |

| B | 0 | 0.00% |

| C | 0 | 0.00% |

| D | 0 | 0.00% |

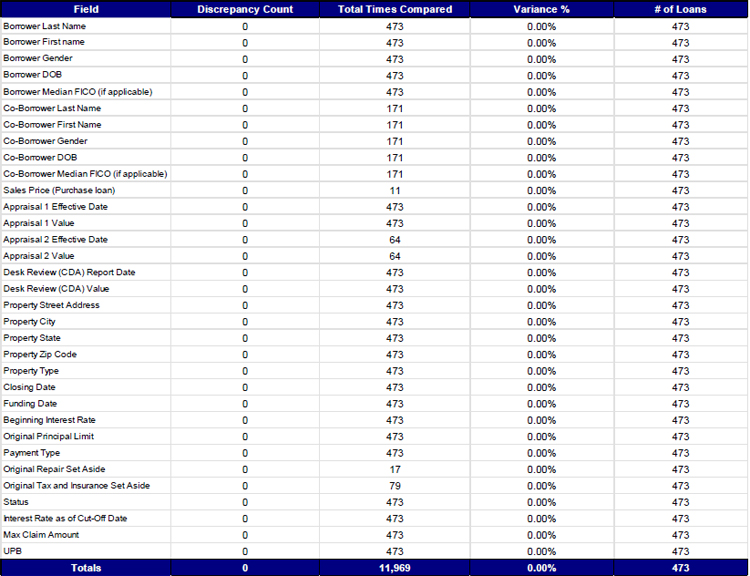

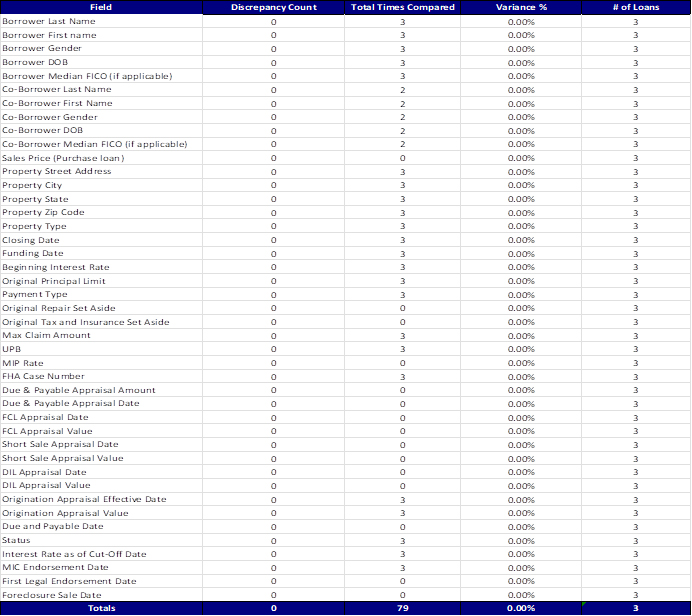

DATA INTEGRITY REVIEW RESULTS SUMMARY TABLE (476 Reverse Mortgage Loans):

inTENT compared data fields on the securitization tape provided by the Client to the data found in the actual file. Of the 476 Reverse Mortgage loans (473 Secure Equity and 3 FHA Underwritten Mortgage Loans) reviewed, none of the loans had a data integrity variance.

Secure Equity

FHA Underwritten Mortgage Loans

VALUE REVIEW RESULTS SUMMARY (476 Reverse Mortgage Loans):

inTENT confirmed that each Reverse Mortgage loan file contained the required appraisals per the Client’s applicable guidelines as well as a secondary valuation product that supported the Clients value used for LTV within -10% or confirmation that Second Appraisal product was not required.