Exhibit 99.1

| FALCON Copyright Quadrin Group 1 FALCON Due Diligence Review JUNE 2026 FALCON Copyright Quadrin Group |

| FALCON Copyright Quadrin Group 2 Contents Background and Terms of Reference Review of Scope and Key Findings File Completeness Underwriting, Servicing & Compliance Complaints Handling Vulnerable Customers 1 2 3 4 5 6 |

| FALCON Copyright Quadrin Group 3 Background and Terms of Reference Background • The report is in respect of a compliance due diligence exercise established and scoped by Goldman Sachs International and Penryn Funding 2024 DAC in respect of a portfolio of Irish residential mortgages serviced by Pepper Ireland (“the Company”). • Quadrin Financial Services Limited (“Quadrin”) conducted the review both on-site and remotely. Terms of Reference Sample • The sample will comprise of 100 loans for File Completeness, Underwriting, Servicing and Compliance and 5 cases with vulnerable customers. File Completeness • For each loan reviewed, Quadrin will check that the completeness of the mortgage documentation for Finance Ireland loans. This will include, but is not limited to: • Application Form • Credit Report • Customer Due Diligence Records • Valuation Report • Mortgage Deed • Certificate of Titie • Deed of Confirmation from any person/persons with an interest in the Property • Insurance Policy • Quadrin will confirm that except for the Mortgage Deeds relating to the Mortgage Loans which are held at the Land Registry, all the relevant mortgage documentation are held to the order of the Originator or its agents • Quadrin will review a sample of up to 100 loans to confirm the loan agreements are consistent with the templates provided for each product |

| FALCON Copyright Quadrin Group 4 Background and Terms of Reference Terms of Reference (cont.) Underwriting • Quadrin will review a sample of loans and will confirm from the Underwriting Criteria of Finance Ireland that: − The documents and underwriting decisions are in accordance with the lending and product guidelines provided. − All Mortgage Loans were advanced to Borrowers resident in Ireland − All Mortgage Loans were advanced to Borrowers aged 21 and over at the date of execution of the relevant Mortgage loan and Related Security − All Mortgage Loans are denominated in euro and are repayable by the Borrower in euro − A Valuation Report was available for each Mortgage Loan and contained nothing material that would cause a Prudent Mortgage Lender to decline the loan. − No Mortgage Loan is a lifetime loan or offset mortgage loan − No Mortgage Loan is a tracker mortgage loan, and the Mortgage Portfolio is not subject to Central Bank of Ireland’s industry-wide tracker mortgage examination. − No Borrower was a person with whom transactions were prohibited under any Sanctions at origination − Each Borrower has delivered a duly completed mandate authorizing monthly payments by Direct Debit − No Mortgage Loan has been provided to fund the construction of a self-built property, and any self built property was constructed in accordance with applicable laws and regulations − Review the underwriting decisions made to confirm they meet with an underwriting standard commonly applied by a prudent lender in the jurisdiction. − Quadrin will comment and provide feedback on any policies that it deems deficient or missing during the review |

| FALCON Copyright Quadrin Group 5 Background and Terms of Reference Terms of Reference (cont.) Servicing including Arrears Management • Verify compliance and prudence to servicing criteria and guidelines including standards expected of a prudent lender/servicer in the jurisdiction (including, but not limited to, the Code of Conduct on Mortgage Arrears 2013) • For a sample of 20 loans, Quadrin will check that the historical collections match the amounts due Complaints Handling • If made available, Quadrin will review the complaints log and comment on any material or thematic issues that have arisen, including what, if any, steps have been taken to remediate Vulnerable Customers • Using the sample of loans, Quadrin will review the vulnerable customer cases to ensure appropriate policies or processes have been followed Compliance • Quadrin will verify that all loans have been underwritten and serviced in compliance with Irish regulations (including any Bank of Ireland / ECB regulation) and with KYC and AML regulations (including, but not limited to the requirements of the Criminal Justice (Money Laundering and Terrorist Financing) Acts 2010 – 2021) • Quadrin will identify any mortgage deeds that contain abusive clauses including, but not limited to, interest rounding up, floors, default interest rates, multicurrency clauses, early termination or 365/360 Interest rate calculation method • Quadrin will seek to compare the procedures with good practice in the market • Quadrin will note if there is any evidence that borrowers have been in touch with any debtors’ associations |

| FALCON Copyright Quadrin Group 6 Contents Background and Terms of Reference Review of Scope and Key Findings File Completeness Underwriting, Servicing & Compliance Complaints Handling Vulnerable Customers 1 2 3 4 5 6 |

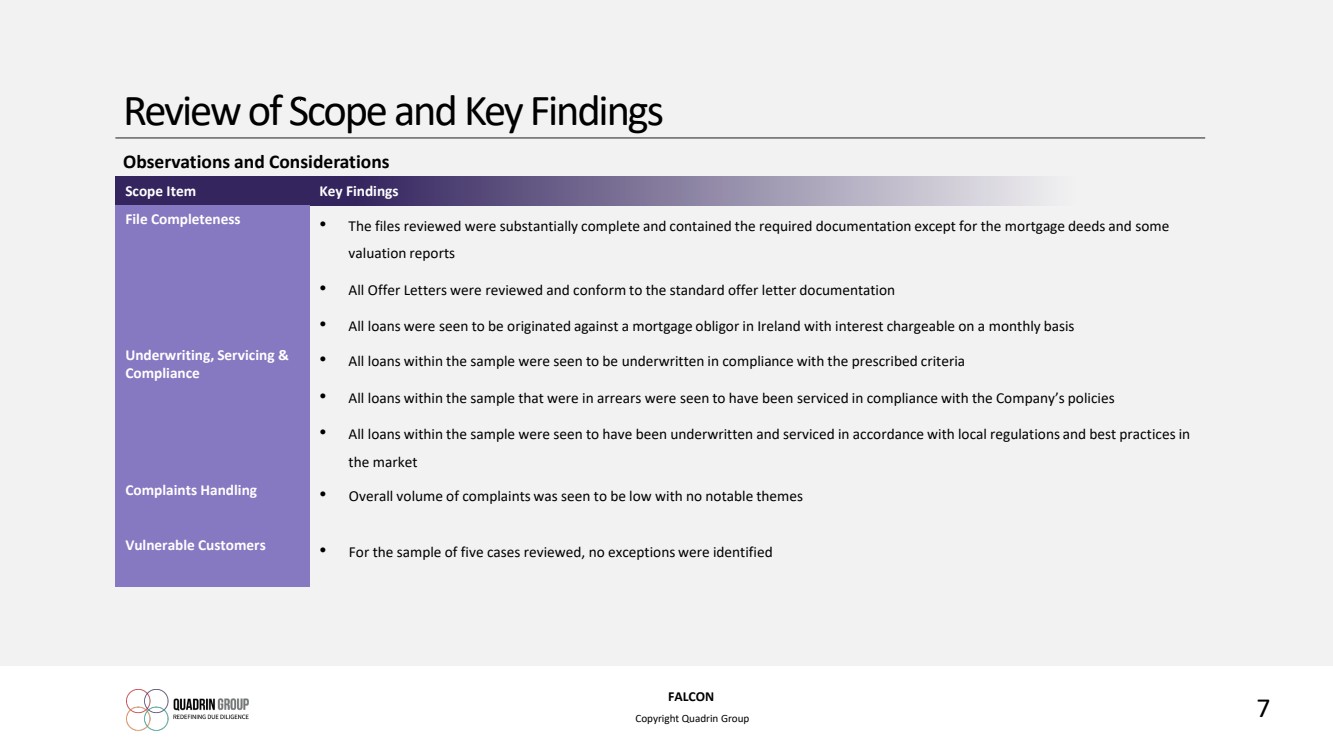

| FALCON Copyright Quadrin Group 7 Review of Scope and Key Findings Observations and Considerations Scope Item Key Findings File Completeness • The files reviewed were substantially complete and contained the required documentation except for the mortgage deeds and some valuation reports • All Offer Letters were reviewed and conform to the standard offer letter documentation • All loans were seen to be originated against a mortgage obligor in Ireland with interest chargeable on a monthly basis Underwriting, Servicing & Compliance • All loans within the sample were seen to be underwritten in compliance with the prescribed criteria • All loans within the sample that were in arrears were seen to have been serviced in compliance with the Company’s policies • All loans within the sample were seen to have been underwritten and serviced in accordance with local regulations and best practices in the market Complaints Handling • Overall volume of complaints was seen to be low with no notable themes Vulnerable Customers • For the sample of five cases reviewed, no exceptions were identified |

| FALCON Copyright Quadrin Group 8 Contents Background and Terms of Reference Review of Scope and Key Findings File Completeness Underwriting, Servicing & Compliance Complaints Handling Vulnerable Customers 1 2 3 4 5 6 |

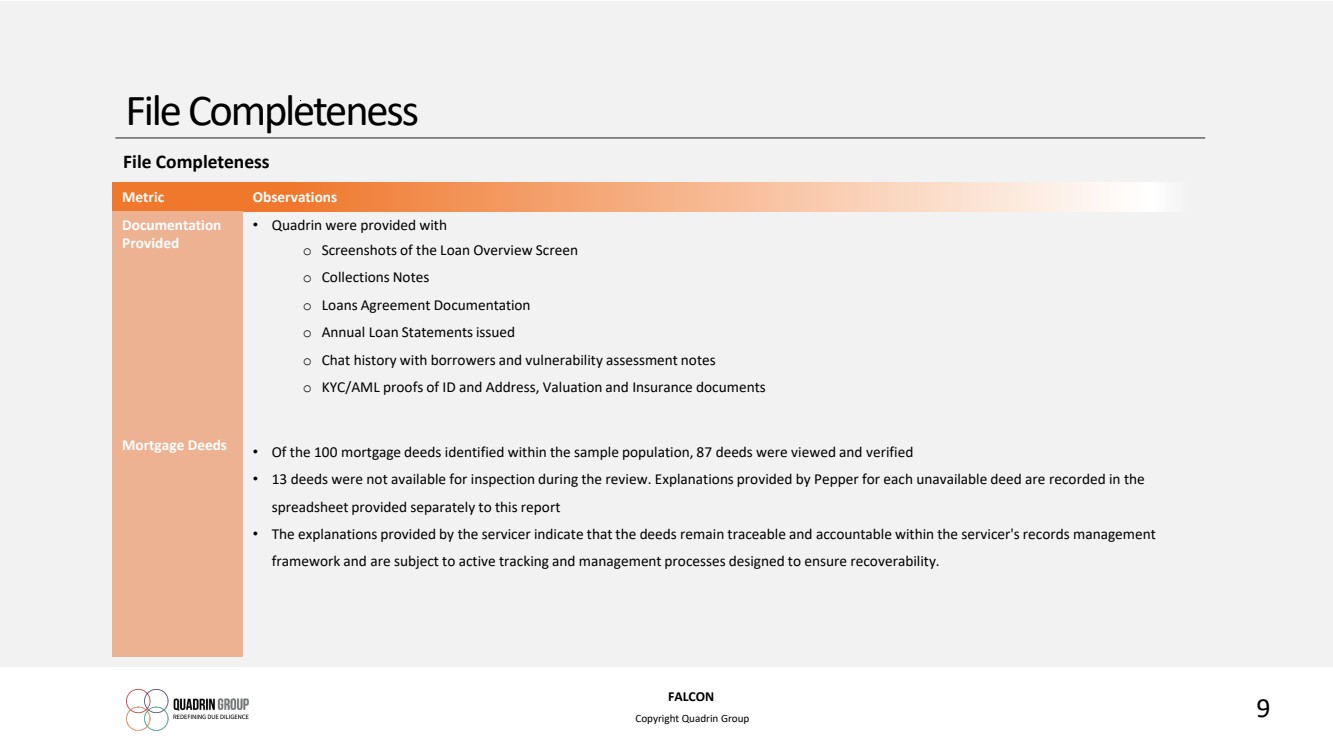

| FALCON Copyright Quadrin Group 9 File Completeness File Completeness Metric Observations Documentation Provided • Quadrin were provided with o Screenshots of the Loan Overview Screen o Collections Notes o Loans Agreement Documentation o Annual Loan Statements issued o Chat history with borrowers and vulnerability assessment notes o KYC/AML proofs of ID and Address, Valuation and Insurance documents Mortgage Deeds • Of the 100 mortgage deeds identified within the sample population, 87 deeds were viewed and verified • 13 deeds were not available for inspection during the review. Explanations provided by Pepper for each unavailable deed are recorded in the spreadsheet provided separately to this report • The explanations provided by the servicer indicate that the deeds remain traceable and accountable within the servicer's records management framework and are subject to active tracking and management processes designed to ensure recoverability. |

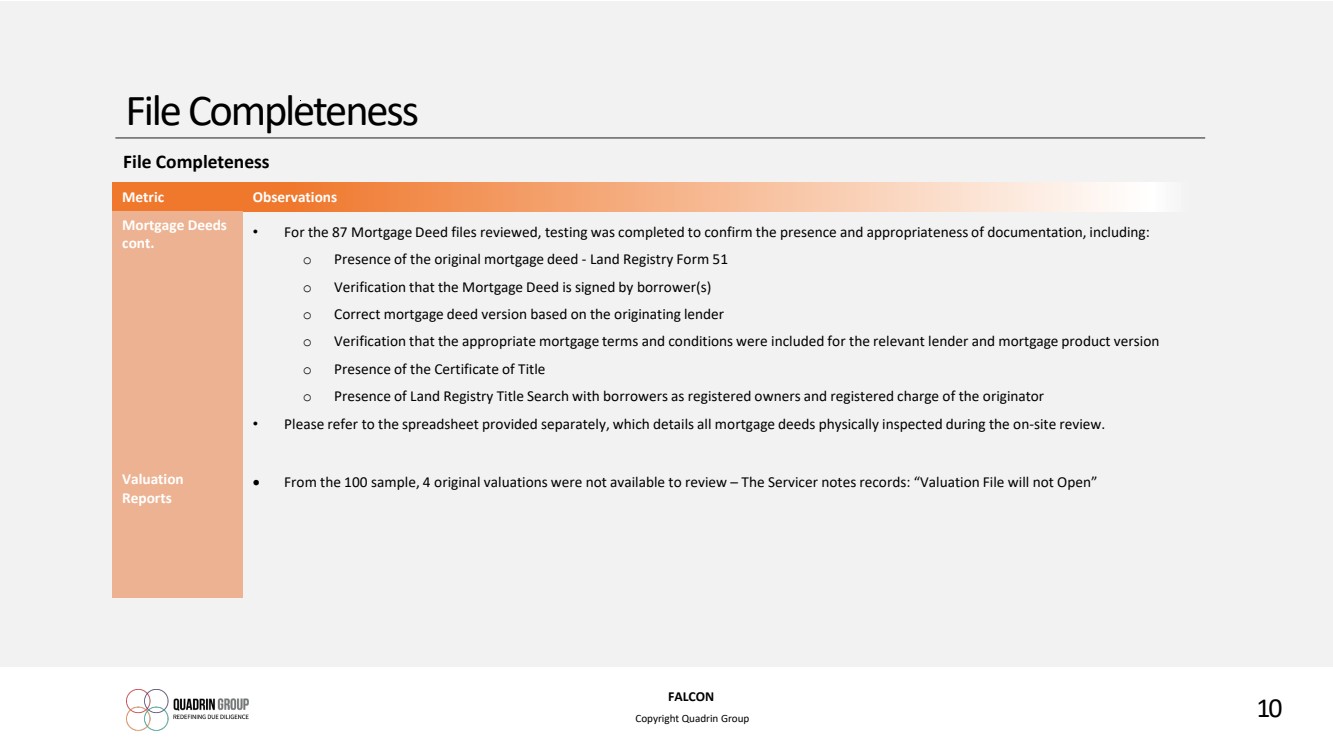

| FALCON Copyright Quadrin Group 10 File Completeness File Completeness Metric Observations Mortgage Deeds cont. • For the 87 Mortgage Deed files reviewed, testing was completed to confirm the presence and appropriateness of documentation, including: o Presence of the original mortgage deed - Land Registry Form 51 o Verification that the Mortgage Deed is signed by borrower(s) o Correct mortgage deed version based on the originating lender o Verification that the appropriate mortgage terms and conditions were included for the relevant lender and mortgage product version o Presence of the Certificate of Title o Presence of Land Registry Title Search with borrowers as registered owners and registered charge of the originator • Please refer to the spreadsheet provided separately, which details all mortgage deeds physically inspected during the on-site review. Valuation Reports • From the 100 sample, 4 original valuations were not available to review – The Servicer notes records: “Valuation File will not Open” |

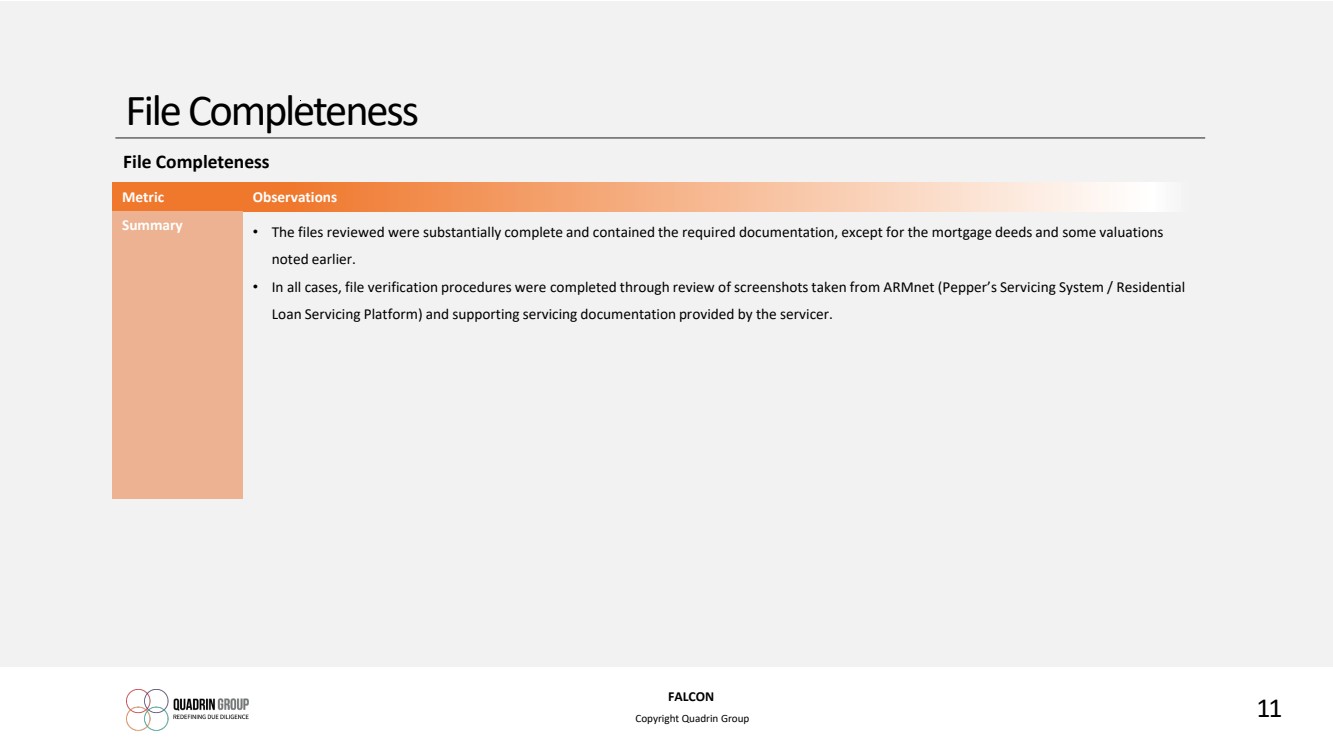

| FALCON Copyright Quadrin Group 11 File Completeness File Completeness Metric Observations Summary • The files reviewed were substantially complete and contained the required documentation, except for the mortgage deeds and some valuations noted earlier. • In all cases, file verification procedures were completed through review of screenshots taken from ARMnet (Pepper’s Servicing System / Residential Loan Servicing Platform) and supporting servicing documentation provided by the servicer. |

| FALCON Copyright Quadrin Group 12 File Completeness Mortgage Documentation Metric Observations Offer Letters • For the sample of 100 loans, all offer letters were reviewed and confirmed to follow the relevant Lender’s standard offer letter documentation. • They have also been checked against the Arthur Cox standard documentation provided. • The Offer Letters are - offer of a mortgage loan (the "Loan"), on the terms set out in the Offer Letter and the appropriate Lender Residential Mortgages General Loan Conditions, and the versions and variations of each of the Lenders have been recorded. These are as follows: o Pepper Homeloans' General Loan Conditions January 2016 (version 1.0) (the "Loan Conditions") o Pepper Money General Loan Conditions September 2016 (version 1.1) (the "Loan Conditions") o Pepper Money General Loan Conditions May 2017 (version1.1) (the "Loan Conditions") o Finance Ireland Residential Mortgages General Loan Conditions November 2018 (the "Loan Conditions") o Finance Ireland Residential Mortgages General Loan Conditions May 2021 (the "Loan Conditions") |

| FALCON Copyright Quadrin Group 13 File Completeness Mortgage Documentation Metric Observations Offer Declarations • All the Acceptance of Offer Declarations were signed by the borrowers. • The PDH test requirement has been verified under “Section 2 – Your Loan Requirements” from the Offer Letter – all of the 100-loan sample confirm that The Offer Letter is based on a loan for a Principal Home. • All of the 100 loans reviewed are structured on capital and interest repayment method with the interest rate type and interest rate visibly recorded. There were no tracker rates within the sample • Interest rates on the loans are chargeable on monthly basis o Finance Ireland Offer Letter states - During the term of the Loan, interest is calculated on a daily basis and applied in accordance with the Loan Conditions. Variable interest rates are subject to change. o Pepper Money - During the variable interest rate period, interest is calculated on a daily basis and to the account on a monthly basis. Variable interest rates are subject to change. |

| FALCON Copyright Quadrin Group 14 File Completeness Mortgage Documentation Metric Observations Deed of Confirmation • The Deed of Confirmation and Donor Declarations are called for under Section 13 – Special Conditions of this Offer on both Lenders Standard Loan Offer Document. • From the 100 Sample tested 35 of the Offer Letters require a signed Donor Declaration Form, a Deed of Confirmation or both. • Proof of gifts / donations if they form part of the balance of funds to complete the purchase is also called for and these have all been recorded on column O of the Falcon Offer Letter Review 24.06.2026 excel provided separately • As these Special Conditions are generally a pre-drawdown special condition requirement, the relevant documentation may be retained within the Offer Pack where it has not been included in the Mortgage Deed Pack. • All special conditions relating to proof of balance of funds, including gifts, pledges, and donations, have been recorded. Any financial contributions from third parties used to assist with the property purchase will generally require a Deed of Confirmation or Donor Declaration signed by the donor waiving any beneficial interest in the property. • For example, account number M1001356766 includes a requirement for both a Donor Declaration and a Deed of Confirmation from the donor under the Special Conditions section. |

| FALCON Copyright Quadrin Group 15 File Completeness Mortgage Documentation Metric Observations Deed of Confirmation cont. • In general, two separate documents are required: o Gift / Donor Declaration o Deed of Confirmation (depending on the lender’s solicitor requirements) • These documents are typically treated as pre-drawdown conditions precedent (CPs) or, in some cases, as special conditions required prior to drawdown. Standard Documentation Referenced • All Documents Reviewed followed Standard Documents provided by Arthur Cox (AC). These were as follows: o Finance Ireland - Land Registry Mortgage Form 51 – Item 12 of the AC uploads o Pepper Money - Land Registry Mortgage Form 51 – Item 11 of the AC uploads o Certificate of Title - Law Society Approved Form (2011 Edition) reviewed were completed and signed by conveyancing solicitors. o Land Registry Folios – with the ownership in the borrower’s name and the charge of the relevant originator lender recorded under the burdens section – Refer to - FALCON DEEDS CATALOGUED 10 & 11 June 2026. o Lender Template – Valuation Reports |

| FALCON Copyright Quadrin Group 16 Contents Background and Terms of Reference Review of Scope and Key Findings File Completeness Underwriting, Servicing & Compliance Complaints Handling Vulnerable Customers 1 2 3 4 5 6 |

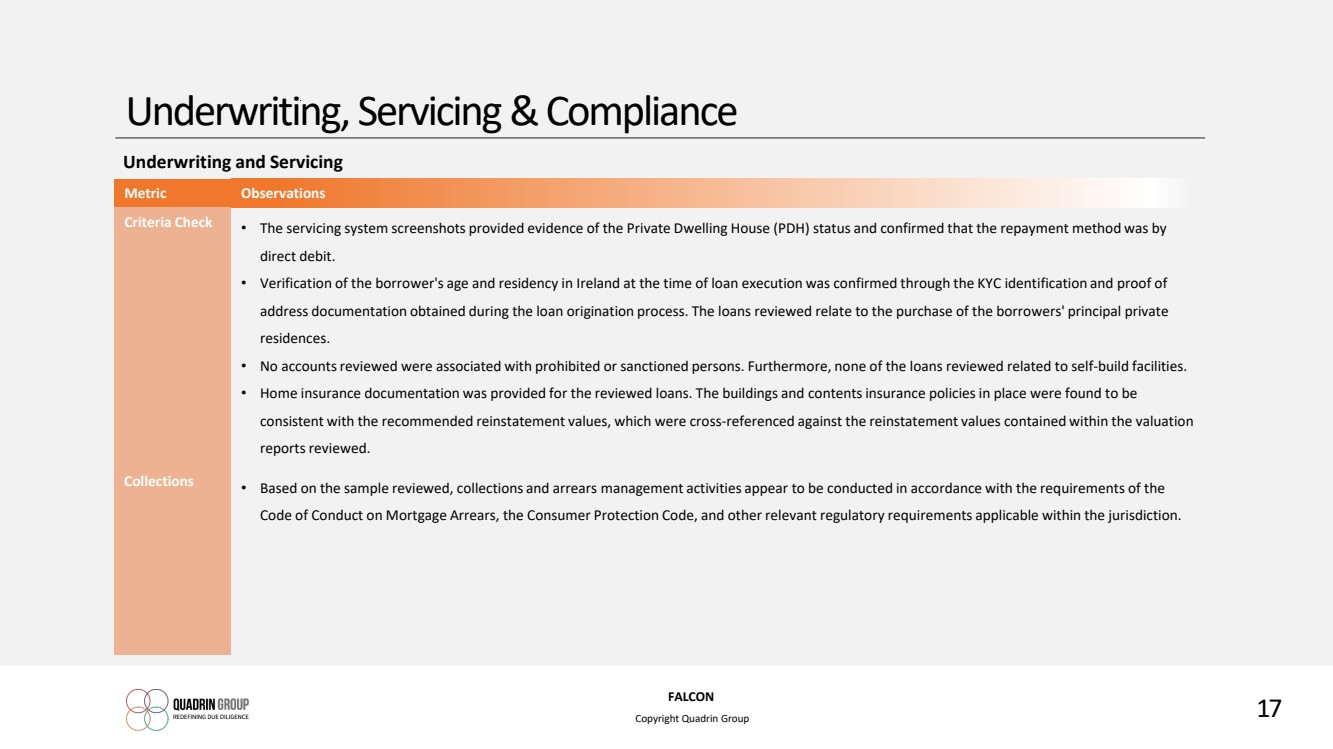

| FALCON Copyright Quadrin Group 17 Underwriting, Servicing & Compliance Underwriting and Servicing Metric Observations Criteria Check • The servicing system screenshots provided evidence of the Private Dwelling House (PDH) status and confirmed that the repayment method was by direct debit. • Verification of the borrower's age and residency in Ireland at the time of loan execution was confirmed through the KYC identification and proof of address documentation obtained during the loan origination process. The loans reviewed relate to the purchase of the borrowers' principal private residences. • No accounts reviewed were associated with prohibited or sanctioned persons. Furthermore, none of the loans reviewed related to self-build facilities. • Home insurance documentation was provided for the reviewed loans. The buildings and contents insurance policies in place were found to be consistent with the recommended reinstatement values, which were cross-referenced against the reinstatement values contained within the valuation reports reviewed. Collections • Based on the sample reviewed, collections and arrears management activities appear to be conducted in accordance with the requirements of the Code of Conduct on Mortgage Arrears, the Consumer Protection Code, and other relevant regulatory requirements applicable within the jurisdiction. |

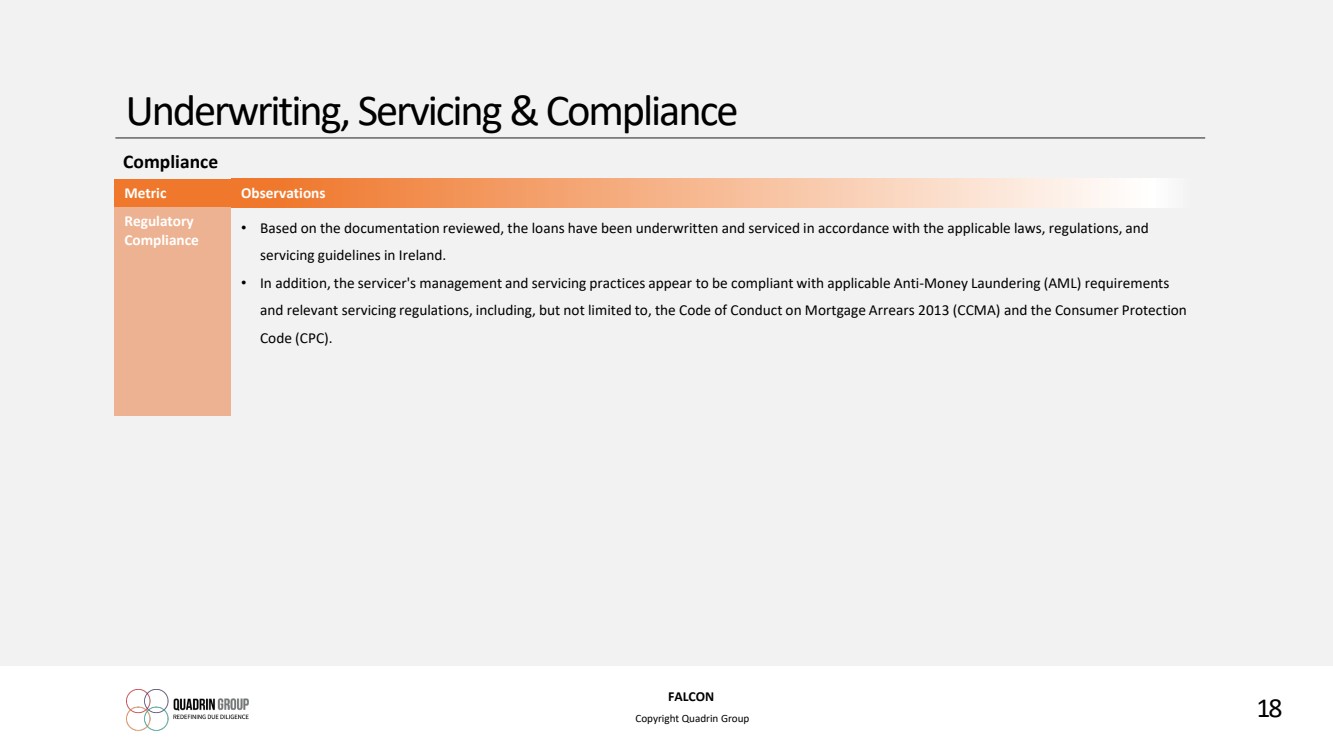

| FALCON Copyright Quadrin Group 18 Underwriting, Servicing & Compliance Compliance Metric Observations Regulatory Compliance • Based on the documentation reviewed, the loans have been underwritten and serviced in accordance with the applicable laws, regulations, and servicing guidelines in Ireland. • In addition, the servicer's management and servicing practices appear to be compliant with applicable Anti-Money Laundering (AML) requirements and relevant servicing regulations, including, but not limited to, the Code of Conduct on Mortgage Arrears 2013 (CCMA) and the Consumer Protection Code (CPC). |

| FALCON Copyright Quadrin Group 19 Contents Background and Terms of Reference Review of Scope and Key Findings File Completeness Underwriting, Servicing & Compliance Complaints Handling Vulnerable Customers 1 2 3 4 5 6 |

| FALCON Copyright Quadrin Group 20 Complaints Handling Complaints Handling Metric Observations Sample Review • Across the Project Falcon perimeter (2,069 loans), we have completed a 24-month lookback of complaints volumes. • The overall volume of complaints was seen to be low • A summary of complaint activity can be seen on the following slide alongside a separate spreadsheet with the data behind the complaints as part of the review (Tab 1 Complaints) • There has been no FSPO activity. (To note that Pepper issue Final Response Letters on behalf of Finance Ireland but they manage their own FSPO cases. That said there has been no FSPO Complaints in this Perimeter) |

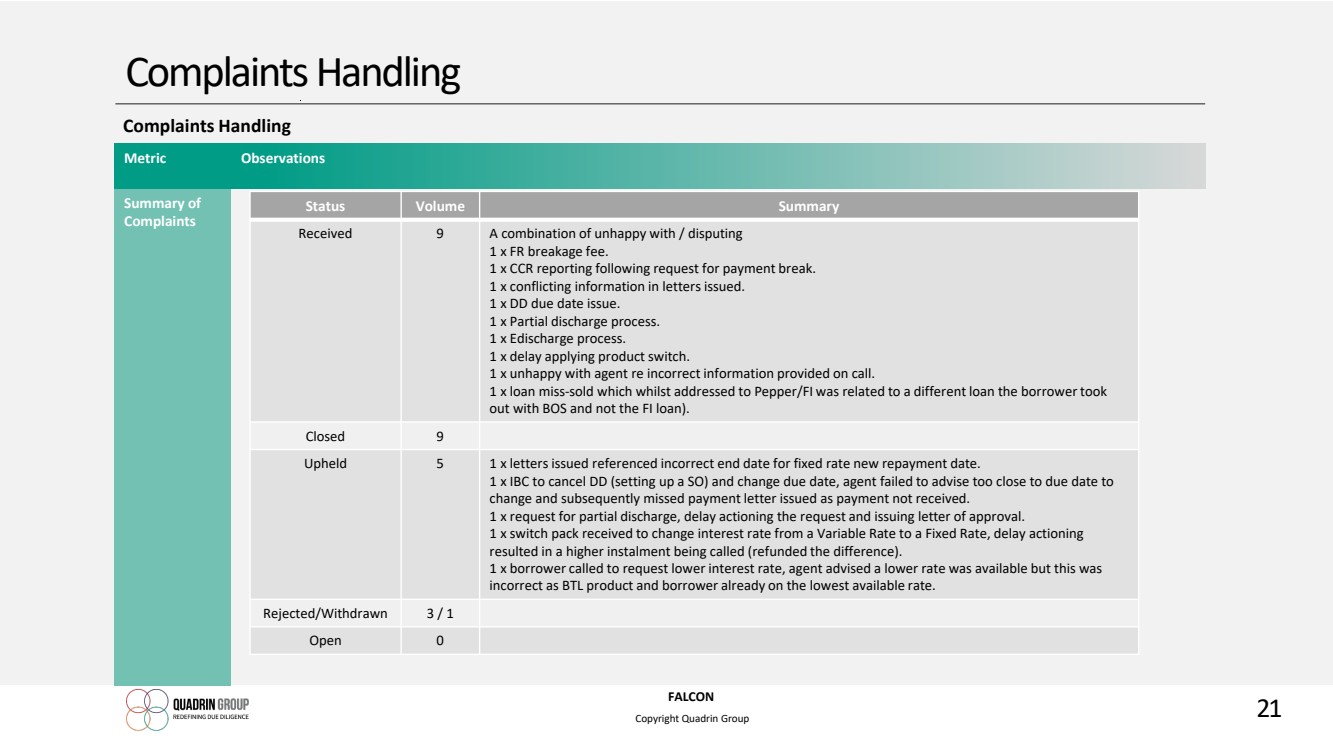

| FALCON Copyright Quadrin Group 21 Complaints Handling Complaints Handling Metric Observations Summary of Complaints Status Volume Summary Received 9 A combination of unhappy with / disputing 1 x FR breakage fee. 1 x CCR reporting following request for payment break. 1 x conflicting information in letters issued. 1 x DD due date issue. 1 x Partial discharge process. 1 x Edischarge process. 1 x delay applying product switch. 1 x unhappy with agent re incorrect information provided on call. 1 x loan miss-sold which whilst addressed to Pepper/FI was related to a different loan the borrower took out with BOS and not the FI loan). Closed 9 Upheld 5 1 x letters issued referenced incorrect end date for fixed rate new repayment date. 1 x IBC to cancel DD (setting up a SO) and change due date, agent failed to advise too close to due date to change and subsequently missed payment letter issued as payment not received. 1 x request for partial discharge, delay actioning the request and issuing letter of approval. 1 x switch pack received to change interest rate from a Variable Rate to a Fixed Rate, delay actioning resulted in a higher instalment being called (refunded the difference). 1 x borrower called to request lower interest rate, agent advised a lower rate was available but this was incorrect as BTL product and borrower already on the lowest available rate. Rejected/Withdrawn 3 / 1 Open 0 |

| FALCON Copyright Quadrin Group 22 Contents Background and Terms of Reference Review of Scope and Key Findings File Completeness Underwriting, Servicing & Compliance Complaints Handling Vulnerable Customers 1 2 3 4 5 6 |

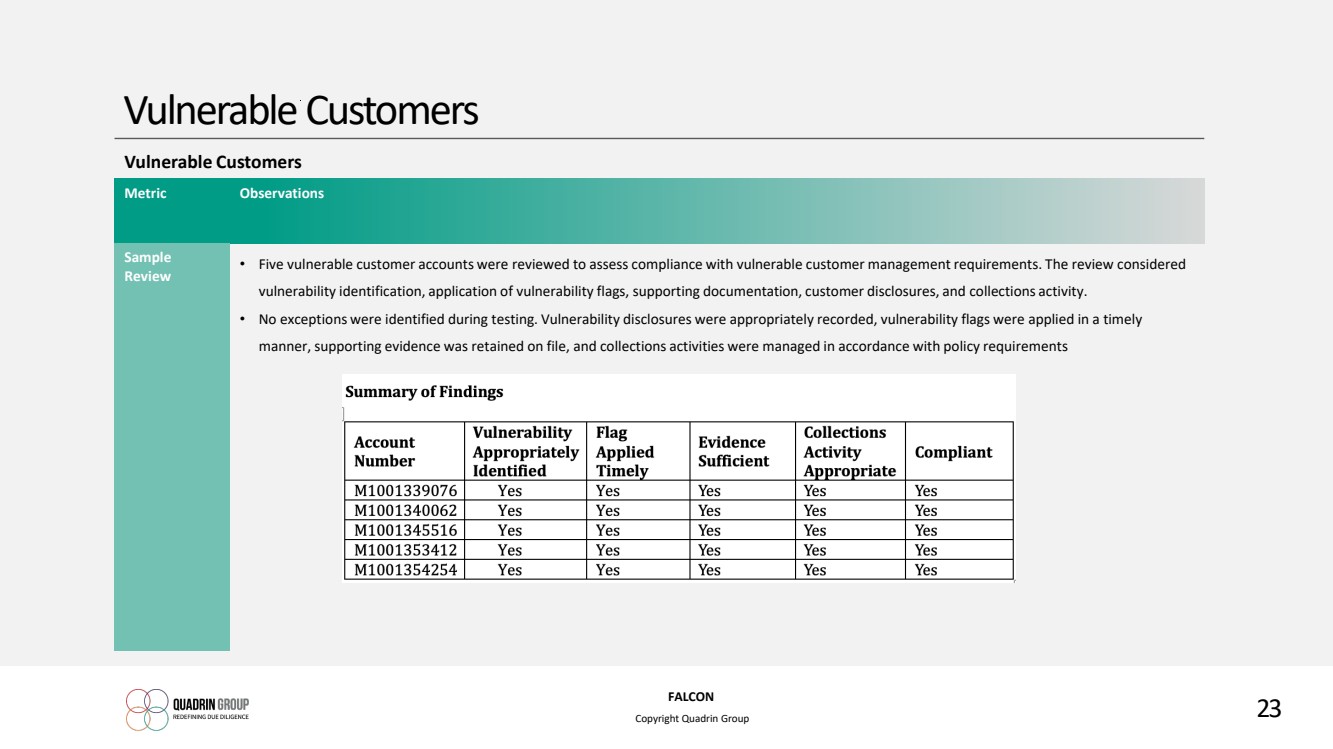

| FALCON Copyright Quadrin Group 23 Vulnerable Customers Vulnerable Customers Metric Observations Sample Review • Five vulnerable customer accounts were reviewed to assess compliance with vulnerable customer management requirements. The review considered vulnerability identification, application of vulnerability flags, supporting documentation, customer disclosures, and collections activity. • No exceptions were identified during testing. Vulnerability disclosures were appropriately recorded, vulnerability flags were applied in a timely manner, supporting evidence was retained on file, and collections activities were managed in accordance with policy requirements |

| FALCON Copyright Quadrin Group 24 FALCON 2 Brunel Way Slough Berkshire SL1 1FQ United Kingdom www.quadringroup.com +44 1753 900914 Disclaimer This report is intended for general guidance and information purposes only. This report is under no circumstances intended to be used or considered as financial or investment advice, a recommendation or an offer to sell, or a solicitation of any offer to buy any securities or other form of financial asset. Please note that this is not an offer document. The report is not to be considered as investment research or an objective or independent explanation of the matters contained herein, and is not prepared in accordance with the regulation regarding investment analysis. |