KPMG LLP

1 Sovereign Square

Sovereign Street

Leeds LS1 4DA

United Kingdom

Fax +44 (0) 113 231 3200

Helena.Lyons©KPMG.co.uk

Mobile +44 (0) 7825 245259

Exhibit 99.1

| |

KPMG LLP 1 Sovereign Square Sovereign Street Leeds LS1 4DA United Kingdom |

Tel

+44 (0) 113 231 3000 Fax +44 (0) 113 231 3200 Helena.Lyons©KPMG.co.uk Mobile +44 (0) 7825 245259 |

Private & confidential

| The Directors | Your ref | Falcon |

| GS Mortgage-Backed Securities Trust | ||

| 2026-IRPM1 Designated Activity Company | Our ref | HL/ES/UK010450 |

| 3rd Floor, Waterloo Exchange | ||

| Waterloo Road | Contact | Helena Lyons |

| Dublin 4, D04 E5W7 | +44 (0) 7825 245 259 | |

| Ireland |

Penryn Funding 2024 DAC

1-2 Haddington Square

Haddington Road

Dublin 4, D04 XN32

Ireland

Goldman Sachs International

Plumtree Court

25 Shoe Lane

London, EC4A 4AU

United Kingdom

1 July 2026

Dear All

Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation

In accordance with the terms of our engagement letter dated 18 June 2026 (the “Engagement Letter”), we have performed certain agreed-upon procedures in relation to the portfolio of Irish mortgage loans referred to above proposed to be the subject of a securitisation (the “Securitisation”). This letter reports on our performance of those agreed-upon procedures (the “Data AUP Letter”). This Data AUP Letter is confidential and agreed disclosure restrictions apply.

This Data AUP Letter is addressed to the directors of GS Mortgage-Backed Securities Trust 2026-IRPM1 Designated Activity Company (the “Issuer”), Penryn Funding 2024 DAC (the “Seller”) and Goldman Sachs International (the “Arranger”) and collectively all addressees of this Data AUP Letter are referred to as the “Data AUP Letter Recipients”.

The procedures that we will perform are solely for the purpose of assisting you in determining the accuracy of data that you are preparing in connection with the Securitisation and so may not be suitable for any other purpose. We will not accept any responsibility to any other party to whom our Data AUP Letter is shown or into whose hands it may come.

KPMG LLP, a UK limited liability partnership and a member firm of the KPMG global organisation of independent member firms affiliated with KPMG International Limited, a private English company limited by guarantee. |

Registered

in England No OC301540 Registered office: 15 Canada Square, London, E14 5GL For full details of our professional regulation please refer to ‘Regulatory information’ under ‘About’ at www.kpmg.com/uk |

Document Classification – KPMG Confidential

| KPMG

LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

Responsibilities of the Data AUP Letter Recipients

It is the responsibility of the Data AUP Letter Recipients to determine the sufficiency of these procedures agreed with them for their own purposes. Consequently, we make no representation regarding the sufficiency of the procedures described below either for the purposes for which this report has been requested or for any other purpose.

The Data AUP Letter Recipients have acknowledged that the agreed-upon procedures are appropriate for the purpose of the engagement. The Seller is responsible for the subject matter on which the agreed-upon procedures are performed.

Our Responsibilities

Our engagement was undertaken in accordance with International Standard on Related Services 4400 (Revised), Agreed-Upon Procedures Engagements issued by the International Auditing and Assurance Standards Board. An agreed-upon procedures engagement involves our performing the procedures that have been agreed with the Data AUP Letter Recipients, and reporting the factual findings, which are the factual results of the agreed-upon procedures performed. We make no representation regarding the appropriateness of the agreed-upon procedures.

This agreed-upon procedures engagement is not an assurance engagement. Accordingly, we do not express an opinion or an assurance conclusion.

Had we performed additional procedures, other matters might have come to our attention that would have been reported.

Professional Ethics and Quality Control

We have complied with the ethical requirements in the ICAEW Code of Ethics issued by the Institute of Chartered Accountants in England and Wales. For the purpose of this engagement, there are no independence requirements with which we are obliged to comply.

We apply International Standard on Quality Control (UK) 1 Quality Control for Firms that Perform Audits and Reviews of Financial Statements, and Other Assurance and Related Services Engagements. Accordingly, we maintain a comprehensive system of quality control including documented policies and procedures regarding compliance with ethical requirements and professional standards as well as applicable legal and regulatory requirements.

Procedures and Findings

The procedures performed were not intended to satisfy any criteria for due diligence published by any nationally recognised statistical rating organisation (“NRSRO”).

HL/ES/UK010450 | Document Classification – KPMG Confidential | 2 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

Service A — Pool Agreed-Upon Procedures

We have been provided with a data file entitled “Project Falcon Updated Loan ID for Sample.xlsx” containing a list of 2,131 Irish mortgage loans proposed to be the subject of a securitisation (the “Portfolio”). A sample of 401 items was drawn at random from the Portfolio (the “Sample”). The number of items in the Sample was determined on the basis described in the scope of services (the “Scope of Services”) attached as Appendix A.

The Seller, or the respective mortgage portfolio servicer, has subsequently provided to us data files entitled “Project Falcon Nua Funded Apr 2026.xlsx” and “Pepper AUP Tape - April 2026 v2.xlsx” (together, the “Extraction File”) containing details relating to items in the Sample as at 11 May 2026 for items in the Sample serviced by Nua Money Limited (“Nua”), and 30 April 2026 for items in the Sample serviced by Pepper Finance Corporation (Ireland) DAC (“Pepper”) (individually, and collectively, the “Portfolio Date”), together with source documentation relating to the Irish mortgage loans in the Sample.

The procedures were performed on the Extraction File and the source documentation (the “Sources”) provided to us by the Seller or the relevant mortgage portfolio servicer. We have not verified or evaluated such Sources and therefore we express no opinion or any other form of assurance regarding the reliability, accuracy or adequacy of the Sources, or as to whether any of the Sources omit any material facts. Furthermore, we express no opinion or any other form of assurance regarding the reliability, accuracy or adequacy of the disclosures in the Extraction File, or any legal matters relating to the Portfolio or the physical existence of the mortgaged properties.

The procedures performed did not address, without limitation: (i) the conformity of the origination of the Portfolio to stated underwriting or credit extension guidelines, standards, criteria or other requirements, (ii) the value of any collateral securing the Portfolio, (iii) the compliance of the originator of the Portfolio with applicable laws and regulations, or (iv) any other factor or characteristic of the Portfolio that would be material to the likelihood that the issuer or the asset-backed security will pay interest and principal in accordance with applicable terms and conditions.

Service B — Lending Criteria Agreed-Upon Procedures

We have been provided with a data file entitled “Project Falcon Funded 5th June Cutoff Datatape STS.xlsx” containing details of 2,017 Irish mortgage loans included in the Portfolio as at 5 June 2026 (the “LC Portfolio Date”) (the “LC Extraction File”). Our work was based on this LC Extraction File.

The procedures were performed on the LC Extraction File provided to us by the Seller. We express no opinion or any other form of assurance regarding the reliability, accuracy or adequacy of the disclosures in the LC Extraction File, or any legal matters relating to the Portfolio or the physical existence of the mortgaged properties. We have performed the agreed-upon procedures set out in the Scope of Services.

HL/ES/UK010450 | Document Classification – KPMG Confidential | 3 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

Findings

Service A — Pool Agreed-Upon Procedures

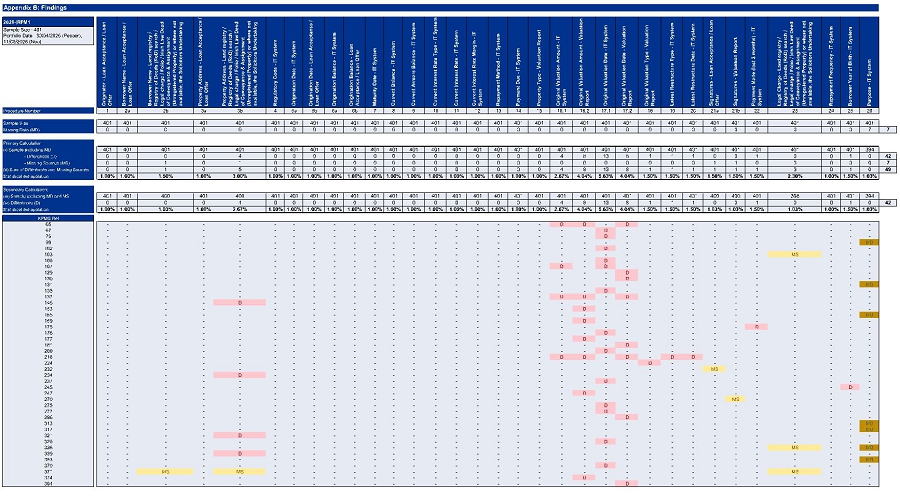

The findings from the agreed-upon procedures are set out in Appendix B.

Based on the instructions provided to us and the assumptions set out in the Scope of Services, the following statistical interpretation can be applied to the findings set out in Appendix B: on the basis of the number of differences between the Extraction File and the Sources identified in the Sample (as reported on the ‘Differences’ lines of Appendix B) and the number of missing sources relating to the Sample (as reported on the ‘Missing Sources’ line of Appendix B) it can be calculated that there is a 99% level of confidence that not more than X% of the population contains such findings relating to the specified procedure, where X is the relevant percentage reported on the ’Statistical extrapolation’ lines of Appendix B.

Details of the differences and missing documentation found as a result of the agreed-upon procedures, and listed in Appendix B, are set out in Appendix C.

In relation to Procedure 23, as instructed by the Data AUP Letter Recipients, for each item in the Sample serviced by Nua and for 16 items in the Sample where the Land Registry / Registry of Deeds (RoD) search / Legal Charge / Folio is unavailable and/or the first charge is not yet registered, we have checked that a signed Solicitors Undertaking exists for each loan and contains text relating to the solicitors confirmation regarding registration of the first charge.

Service B — Lending Criteria Agreed-Upon Procedures

The findings from the procedures are set out in the ‘Findings’ column in Appendix A —Service B — Agreed-Upon Procedures relating to lending criteria.

General

This Data AUP Letter may only be relied upon in respect of the matters to which it refers and as of its date. In relying upon this Data AUP Letter, you agree (save as may otherwise have been expressly agreed in writing) that we have no responsibility to, and we will not, perform any work subsequent to the date of this Data AUP Letter nor to consider, monitor, communicate or report the impact of any events or circumstances which may occur or may come to light subsequent to the date of this Data AUP Letter.

HL/ES/UK010450 | Document Classification – KPMG Confidential | 4 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

This Data AUP Letter is not issued in accordance with the professional standards of the American Institute of Certified Public Accountants or the US Public Company Accounting Oversight Board. We will provide separately an executed Form ABS Due Diligence-15E, Certification of Provider of Third-Party Due Diligence Services for Asset-Backed Securities (“Form ABS Due Diligence-15E”), using the form made available by the US Securities and Exchange Commission (“SEC”), to which this Data AUP Letter will be appended. The executed Form ABS Due Diligence-15E will be provided, without in any way or on any basis affecting or adding to or extending our duties and responsibilities to you or giving rise to any duty or responsibility being accepted or assumed by or imposed on KPMG to any party except you, to facilitate your compliance with SEC Release No. 34-72936, Nationally Recognized Statistical Rating Organizations (the “SEC Release”), pursuant to which you are required to make publicly available the findings and conclusions of any third-party due diligence report obtained. This Data AUP Letter alone is not to be relied on in the United States and we accept no responsibility for any use that you may make of this Data AUP Letter alone in the United States.

The requirement to make publicly available findings and conclusions includes disclosure of the criteria against which loans were evaluated, and how the evaluated loans compared to those criteria, along with the basis for including any loans not meeting those criteria. This is accomplished by including such information, which will include this Data AUP Letter, in Form ABS-15G, Asset-Backed Securitizer Report Pursuant to Section 15G of the Securities Exchange Act of 1934 (“Form ABS 15G”), which is required to be furnished by the Issuer or underwriter to the SEC through the Electronic Data Gathering, Analysis, and Retrieval (“EDGAR”) system.

The Issuer, sponsor or underwriter of an asset—backed securitisation is required to maintain a website (the “Rule 17g-5 website”) pursuant to paragraph (a)(3) of Rule 17g-5 of the US Code of Federal Regulations (17 CFR 240.17g-5). The SEC Release requires any NRSRO producing a credit rating to which “third party due diligence services” relate, to publish with its rating any executed Form ABS Due Diligence-15E containing information about the relevant security or money market instrument that the NRSRO receives or obtains through a Rule 17g-5 website. The agreed-upon procedures performed by KPMG on which this Data AUP Letter reports amount to “third party due diligence services” as defined in the SEC Release.

To facilitate a relevant NRSRO meeting this publication obligation, we are required to furnish any executed Form ABS Due Diligence-15E to any such NRSRO. As envisaged by the SEC Release, we will do so by providing the prescribed form to the Issuer, sponsor, or underwriter of the securitisation that maintains the Rule 17g-5 website, or to any NRSRO that requests it. In addition, the SEC Release requires that an NRSRO producing a credit rating publicly disclose each prescribed form that was posted to the Rule 17g-5 website. Such information may therefore be posted on the website of any relevant NRSRO.

HL/ES/UK010450 | Document Classification – KPMG Confidential | 5 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

Any such publicity shall take place, without in any way or on any basis affecting or adding to or extending our duties and responsibilities to you or giving rise to any duty or responsibility being accepted or assumed by or imposed on KPMG to any party except you, to facilitate your compliance with the SEC Release. Accordingly, any party (including rating agencies and investors) obtaining access to this Data AUP Letter as appended to the executed Form ABS Due Diligence-15E or separately is not authorised by KPMG to use or rely upon the Data AUP Letter, any such use or reliance shall take place at the relevant party’s own risk and, to the fullest extent permitted by law, we will have no responsibility and will deny any liability to any such party.

Yours faithfully

KPMG LLP

Attached:

| Appendix A | Scope of the Services and Findings from Service B | |

| Appendix B | Findings from Service A | |

| Appendix C | Details of Findings from Service A |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 6 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

Appendix A: Scope of the Services and Findings from Service B

This Appendix sets out the procedures that the Data AUP Letter Recipients have instructed us, and that we have agreed, to perform.

Service A — Pool Agreed-Upon Procedures to be carried out on a sample basis

Provision of a data file

The Data AUP Letter Recipients have informed us that the Seller will provide a data file to us containing a list of Irish mortgage loans proposed to be the subject of a securitisation (the “Portfolio”). We will draw a sample of items at random from the data file (the “Sample”) and will notify the items selected to the Seller. The number of items in the Sample will be determined on the basis described under “Sampling” below.

The Seller will then provide a data file to us containing details relating to items in the Sample as at a date to be determined by the Data AUP Letter Recipients (the “Portfolio Date”) (the “Extraction File”).

The Seller or the relevant mortgage portfolio servicer will also provide source documentation to us that the Data AUP Letter Recipients wish us to use for the purposes of the agreed-upon procedures.

Sampling

Sampling is a process of examining less than the total number of items in a population in order to calculate a statistical interpretation about that population. Sampling techniques inherently assume that the sample is representative of the population as a whole. The Data AUP Letter Recipients have requested that we calculate the sample size based on the total number of items in the Portfolio using the following parameters:

Expected deviation rate: 0%

Tolerable deviation rate: 1%

Confidence level: 99%

on the basis that differences between the data attributes and their respective sources are hypergeometrically distributed. We make no representations regarding the use of, or assumptions underlying the sampling techniques.

Procedures

The procedures that the Data AUP Letter Recipients have instructed us, and that we have agreed, to perform in relation to the information contained in the Extraction File are set out in the table below.

HL/ES/UK010450 | Document Classification – KPMG Confidential | 7 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

During the course of our testing, where a loan has redeemed and certain source information is not available such that the full scope of services cannot be performed, these redeemed loans will be removed from the Sample and replaced with an alternative loan.

| No. | Data attribute in the Etraction File |

Level | Procedure | Source/ Recalculation |

Tolerance |

| 1 | Originator | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source. | Loan Acceptance / Loan Offer | None |

| 2a | Borrower Name | Borrower | For each item in the Sample check if the data attribute per the Extraction File matches the source. | Loan Acceptance / Loan Offer | Differences attributable to spelling mistakes or contractions are to be treated as matching the source |

| 2b | Borrower | For each item in the Sample check if the data attribute per the Extraction File matches the source.

As instructed by the Data AUP Letter Recipients, where a loan has multiple borrowers in the IT System, check that at least one borrower name per the IT System matches the source.

As instructed by the Data AUP Letter Recipients, where the Land Registry / Registry of Deeds (RoD) search / Legal Charge / Folio is unavailable and/or the first charge is not yet registered (see Procedure 23), the data attribute has been checked to the Solicitors Undertaking. |

Land Registry / Registry of Deeds (RoD) search / Legal Charge / Folio / Irish Law Deed of Conveyance & Assignment (Unregistered Property) or where not available, the Solicitors Undertaking | Differences attributable to spelling mistakes or contractions are to be treated as matching the source | |

| 3a | Property Address | Collateral | For each item in the Sample check if the data attribute per the Extraction File matches the source. | Loan Acceptance / Loan Offer | Differences attributable to spelling mistakes or contractions or missing data |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 8 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

| No. |

Data attribute in the Extraction |

Level | Procedure |

Source/ Recalculation |

Tolerance |

| (other than the first line of the address) where there are no contradictory elements are to be treated as matching the source | |||||

| 3b | Collateral |

For each item in the Sample check if the data attribute per the Extraction File matches the source.

As instructed by the Data AUP Letter Recipients, where the source is incomplete, use Land Direct website to search the property address per the IT System and cross-check the Folio number observed back to the source.

As instructed by the Data AUP Letter Recipients, where the Land Registry / Registry of Deeds (RoD) search / Legal Charge / Folio is unavailable and/or the first charge is not yet registered (see Procedure 23), the data attribute has been checked to the Solicitors Undertaking. |

Land Registry / Registry of Deeds (RoD) search / Legal Charge / Folio / Irish Law Deed of Conveyance & Assignment (Unregistered Property) or where not available, the Solicitors Undertaking | Differences attributable to spelling mistakes or contractions or missing data (other than the first line of the address) where there are no contradictory elements are to be treated as matching the source | |

| 4 | Regulatory Code | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source. | IT System | None |

| 5a | Origination Date | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source. | IT System | None |

| 5b | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source. | Loan Acceptance / Loan Offer | +/- 180 days |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 9 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

| No. | Data attribute in the Extraction |

Level | Procedure | Source/ Recalculation |

Tolerance |

|

As instructed by the Data AUP Letter Recipients, for each item in the Sample serviced by Nua, where there is a difference noted to the source due to an extension of the loan offer by a maximum of 2 weeks, which can be agreed to the IT System, this will not be marked as a difference. |

|||||

| 6a | Origination Balance |

Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source. | IT System | None |

| 6b | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source. | Loan Acceptance / Loan Offer | None | |

| 7 | Maturity

Date |

Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source.

As instructed by the Data AUP Letter Recipients, where there is a difference noted to the source due to a post Portfolio Date change, check if the maturity date can be recalculated using the Loan Offer (including subsequent term reduction / extension letters). |

IT System | +/- 30 days |

| 8 | Current Balance | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source.

As instructed by the Data AUP Letter Recipients, for each item in the Sample serviced by Pepper, where the difference between the Extraction File and the source is due to an amount held in the repayment account, this will not be marked as a difference. |

IT System | +/- €0.02 |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 10 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

| No. | Data

attribute in the Extraction File |

Level | Procedure | Source/ Recalculation |

Tolerance |

| 9 | Current

Arrears Balance |

Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source.

As instructed by the Data AUP Letter Recipients, for each item in the Sample serviced by Pepper, where the Current Arrears Balance per the source is less than €10, and the Extraction File states €0, this will not be marked as a difference. |

IT System | +/- €0.02 |

| 10 | Current Interest Rate Type | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source. | IT System | None |

| 11 | Current Interest Rate | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source. | IT System | None |

| 12 | Current Interest Rate Margin | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source.

As instructed by the Data AUP Letter Recipients, for each item in the Sample serviced by Pepper which is a Standard Variable Rate loan as at the Portfolio Date, the margin is 0%.

As instructed by the Data AUP Letter Recipients, where the Current Interest Rate Type is ‘Fixed’ as at the Portfolio Date (Procedure 10), the Current Interest Rate Margin (Procedure 12) is equal to the Current Interest Rate (Procedure 11). |

IT System | None |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 11 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

| No. | Data attribute in the Extraction File |

Level | Procedure | Source/ Recalculation |

Tolerance |

| 13 | Repayment Method | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source. | IT System | None |

| 14 | Payment

Due |

Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source.

As instructed by the Data AUP Letter Recipients, for each item in the Sample serviced by Pepper, this procedure was performed with reference to the April 2026 payment due and for each item in the Sample serviced by Nua, this procedure was performed with reference to the next payment due after the Portfolio Date. |

IT System | None |

| 15 | Property

Type |

Collateral | For each item in the Sample, check whether the source indicates that the property is a residential property. As instructed by the Data AUP Letter Recipients, for the purpose of this procedure, a residential property is defined as a detached or semi-detached house, terraced house, flat, apartment, bungalow or cottage, as described in the source. For the avoidance of doubt, we have not checked the specific property type sub- category included in the ‘Property Type’ field in the Extraction File. | Valuation Report | None |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 12 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

| No. | Data

attribute in the Extraction File |

Level | Procedure | Source/ Recalculation |

Tolerance |

| 16.1 | Original Valuation Amount | Collateral | For each item in the Sample check if the data attribute per the Extraction File matches the source. | IT System | None |

| 16.2 | Original Valuation Amount | Collateral | For each item in the Sample check if the data attribute per the Extraction File matches the source.

As instructed by the Data AUP Letter Recipients, for each item in the Sample serviced by Pepper, where the Extraction File reflects the lower of purchase price or the market value, and both can be agreed to the source, this will not be marked as a difference. |

Valuation Report | None |

| 17.1 | Original

Valuation Date |

Collateral | For each item in the Sample check if the data attribute per the Extraction File matches the source. | IT System | None |

| 17.2 | Original

Valuation Date |

Collateral | For each item in the Sample check if the data attribute per the Extraction File matches the source.

As instructed by the Data AUP Letter Recipients, where the Extraction File states the date from a subsequent report performed pre-origination, this will not be marked as a difference. |

Valuation Report | +/- 31 days |

| 18 | Original

Valuation Type |

Collateral | For each item in the Sample check if the data attribute per the Extraction File matches the source. | Valuation Report | None |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 13 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

| No. | Data attribute in the Extraction File |

Level | Procedure | Source/ Recalculation |

Tolerance |

| 19 | Latest Restructure Type | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source.

As instructed by the Data AUP Letter Recipients, for each item in the Sample serviced by Pepper, the Extraction File does not contain restructure information relating to ‘Reduced NMI’ or ‘Deferral of Payments’ between April 2020 — October 2020. If the source is populated with this information, but the Extraction File is ‘blank’, this will not be marked as a difference. |

IT System | None |

| 20 | Latest Restructure Date | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source.

As instructed by the Data AUP Letter Recipients, for each item in the Sample serviced by Pepper, the Extraction File does not contain restructure information relating to ‘Reduced NMI’ or ‘Deferral of Payments’ between April 2020 — October 2020. If the source is populated with this information, but the Extraction File is ‘blank’, this will not be marked as a difference. |

IT System | None |

| 21a | Signatures | Loan | For each item in the Sample check that the source has been signed in the designated space by the borrower. | Loan Acceptance / Loan Offer | None |

| 21b | Loan | For each item in the Sample check that the source has been signed in the designated space by the valuer. | Valuation Report | None |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 14 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

| No. | Data attribute in the Extraction |

Level | Procedure | Source/ Recalculation |

Tolerance |

| 22 | Payment Made (last 3 months) | Loan | For each item in the Sample serviced by Pepper, this procedure should be performed by checking that a payment has been made in relation to the payments due between February 2026 — April 2026.

For each item in the Sample serviced by Nua, this procedure should be performed by checking at least one payment has been made by the borrower in the last 3 months prior to the date of this Data AUP Letter. |

IT System | None |

| 23 | Legal

Charge |

Collateral | For each item in the Sample check if Pepper Finance Corporation (Ireland) DAC, Finance Ireland Credit Solutions DAC or Nua Money Limited are described as having the first charge over the property.

As instructed by the Data AUP Letter Recipients, for each item in the Sample serviced by Nua and for 16 items in the Sample serviced by Pepper where the Land Registry / Registry of Deeds (RoD) search / Legal Charge / Folio is unavailable and/or the first charge is not yet registered, we have checked that a signed Solicitors Undertaking exists for each loan which contains the following text |

Land registry / Registry of Deeds (RoD) search / Legal charge / Folio / Irish Law Deed of Conveyance & Assignment (Unregistered Property) or where not available, the Solicitors Undertaking | None |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 15 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

| No. | Data

attribute in the Extraction File |

Level | Procedure | Source/ Recalculation |

Tolerance |

within the solicitor confirmation:

“so that on completion the Mortgage ranks as a first legal mortgage/charge on the Property”; or

“to lodge the purchase deed/transfer and the Mortgage in the application Registry so as to ensure that the Lender obtains a first legal mortgage/charge on the Property”. |

|||||

| 24 | Repayment Frequency | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source. | IT System | None |

| 25 | Borrower Year of Birth | Borrower | For each item in the Sample check if the data attribute per the Extraction File matches the source. | IT System | None |

| 26 | Purpose | Loan | For each item in the Sample check if the data attribute per the Extraction File matches the source.

As instructed by the Data AUP Letter Recipients, for each item in the Sample serviced by Pepper, where the source states “Remortgage with Equity Release” or “Debt Consolidation”, and the Extraction File states “Remortgage”, this will not be marked as a difference. |

IT System | None |

Notes in relation to the manner of reporting certain findings

1) Reporting the findings

HL/ES/UK010450 | Document Classification – KPMG Confidential | 16 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

Where within the Extraction File a data attribute for a particular mortgage loan is missing, this is to be reported as ‘missing data’ or ‘MD’.

Where a data attribute contained in the Extraction File for an individual mortgage loan does not match the source, this is to be reported as a ‘difference’ or ‘D’.

Where a source document has not been provided, or the data attribute is missing from the source document, this is to be reported as ‘missing source’, ‘missing from source’ or ‘MS’.

2) Statistical interpretation

For the purposes of the statistical interpretation, the Data AUP Letter Recipients require us to present the statistical extrapolation for each procedure as follows:

Primary calculation:

| (i) | Calculation to be based on the total number of items in the Sample except where within the Extraction File a data attribute for a particular mortgage loan is missing in which event the calculation is to be based on the total number of items in the Sample after subtracting the number of items with missing data. |

| (ii) | Calculation to be performed treating as errors both differences and missing sources. |

Secondary calculation:

| (iii) | Calculation to be based on the total number of items in the Sample after subtracting the number of items with missing data and the number of items with missing sources. |

| (iv) | Calculation to be performed treating as errors differences only. |

Where a procedure specifies agreement to specific documentation, and the Seller or the relevant mortgage portfolio servicer has provided as part of the source documentation written evidence of amendments or additions to an original document or documents, the instruction of the Data AUP Letter Recipients to us is to conduct the relevant procedure on the basis of the information contained in the amendments or additions to the original documentation and not the information contained in the original documentation.

In reporting findings on the basis of the procedures to be undertaken, the Data AUP Letter Recipients have specified that results are to be reported as being in agreement if any difference found is below the tolerance level, if any, set out above.

HL/ES/UK010450 | Document Classification – KPMG Confidential | 17 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

Service B — Agreed-Upon Procedures relating to lending criteria

Provision of a data file

The Data AUP Letter Recipients have informed us that the Seller will provide a data file to us containing details of mortgage loans proposed to be the subject of a securitisation (the “Portfolio”) as at a date to be determined by the Data AUP Letter Recipients (the “LC Portfolio Date”) (the “LC Extraction File”).

Procedures

The procedures that the Data AUP Letter Recipients have instructed us, and that we have agreed, to perform in relation to the information contained in the LC Extraction File are set out in the table below.

| No. | Lending Criteria | Procedure | Findings |

| For all mortgage loans in the Portfolio: | |||

| 1 | As at the Closing Date, there are no Mortgage Loans, where the Outstanding Principal Balance in respect of a single Borrower exceeds 2 per cent. of the aggregate Outstanding Principal Balance of the aggregate of all Mortgage Loans within the Mortgage Portfolio. | Check that the sum of the ‘Current Balance’ field in the LC Extraction File for each Borrower (as identified by the ‘Borrower Identifier’ field in the LC Extraction File) as a % of the sum of the ‘Current Balance’ field in the LC Extraction File is less than or equal to 2%. | No findings noted |

| For mortgage loans in the ‘Pepper’ Portfolio only: | |||

| 2 | The loans comprised in the Portfolio will all consist of loans secured by a first charge against residential properties located in Ireland. All relevant Borrowers are required to have good and marketable title or long lease title to the relevant Property free from any encumbrance (except the relevant Mortgage) which would adversely affect such title. | For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Pepper Finance Corporation (Ireland) DAC’, check that the ‘Property Type’ field in the LC Extraction File is equal to ‘1’, ‘2’, ‘3’, ‘4’ or ‘ND,5’.

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Pepper Finance Corporation (Ireland) DAC’, check that the ‘Lien’ field in the LC Extraction File is equal to ‘1’ and that the ‘Geographic Region List’ field in the LC Extraction File is equal to one of the following: |

No findings noted |

| IE011 | IE024 | IE053 | |||||

| IE012 | IE025 | IE061 | |||||

| IE013 | IE041 | IE062 |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 18 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

| IE021 | IE042 | IE063 | |||||

| IE022 | IE051 | ||||||

| IE023 | IE052 |

| 3 | The maximum single loan amount permitted by Finance Ireland is €1,250,000. A single borrower can have one loan up to a maximum permitted amount of €1,250,000, or up to a maximum of ten separate loans, subject to a maximum combined permitted amount of €1,250,000. The maximum term is 35 years for a PDH Loan. The minimum age of borrowers at the time of application is 18 years old. For PDH Loans, the Loan must be repaid normally before the oldest applicant’s 70th birthday. However, a 12 month extension period may be granted in exceptional cases due to extensions of a loan’s offer period. The minimum loan term is 5 years. | For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Pepper Finance Corporation (Ireland) DAC’, check that the sum of the ‘Original Balance’ field in the LC Extraction File for each Borrower (as identified by the ‘Borrower Identifier’ field in the LC Extraction File) is less than or equal to EUR 1,250,000.

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Pepper Finance Corporation (Ireland) DAC’, check that the maximum number of loans for each Borrower (as identified by the ‘Borrower Identifier’ field in the LC Extraction File) is less than or equal to 10.

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Pepper Finance Corporation (Ireland) DAC’, check that the difference between ‘Loan Origination Date’ field and ‘Date of Loan Maturity’ field rounded down to the nearest whole month in the LC Extraction File is greater than or equal to 60 and less than or equal to 420.

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Pepper Finance Corporation (Ireland) DAC’, check that the difference between (i) the maximum of the ‘Borrower Year of Birth’ field and where applicable, the ’Second Applicant Year of Birth’ field in the LC Extraction File; and (ii) the origination year (as identified by the ‘Loan Origination Date’ field in the LC Extraction File); is greater than or equal to 18. |

We have noted one mortgage loan with a term of 516 months (calculated as the difference between the ‘Loan Origination Date’ field in the LC Extraction File and the ‘Date of Loan Maturity’ field in the LC Extraction File), exceeds the maximum term criteria of 420 months.

No other findings noted. |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 19 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

| 4 | The loan to value (“LTV”) in relation to purchases is calculated by dividing the total amount of the loan (net of fees) by the current market value determined by the valuation or the purchase price of the property (whichever is the lower). At the date of origination, if any Loan is a PDH Loan, the maximum LTV (including fees) at the date of origination does not exceed 90 per cent, save in respect of Loans where the Borrower is a first time buyer in which case the relevant PDH Loan may have an LTV (including fees) at the date of origination of up to 95 per cent. All origination of PDH Loans is subject to the prevailing Central Bank of Ireland’s guidelines on Loan to Value. Valuations are carried out in accordance with a valuation methodology as would be acceptable to a Prudent Mortgage Lender | For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Pepper Finance Corporation (Ireland) DAC’, check that the Original LTV (calculated as the ‘Original Balance’ field in the LC Extraction File divided by the ‘Valuation Amount’ in the LC Extraction File, multiplied by 100) is less than or equal to 90%.

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Pepper Finance Corporation (Ireland) DAC’, check that the ‘Original Valuation Type’ field in the LC Extraction File is equal to ‘1’ (Full, internal and external inspection). |

No findings noted |

| For mortgage loans in the ‘Nua’ Portfolio only: | |||

| 5 |

Key Features of Lending Criteria

(a) Each Mortgage Loan must be secured by a first ranking legal mortgage over either (i) a freehold property or (ii) a leasehold property with a minimum of 70 years of unexpired lease term at the end of the term of the Mortgage Loan.

(b) The property must be located in Ireland and used as the Borrower’s primary residence

(c) The Borrower must be at least 21 years old at the time of advance. |

(a) and (b):

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Nua Money Limited’, check that the ‘Property Type’ field in the LC Extraction File is equal to ‘1’, ‘2’, ‘3’, ‘4’ or ‘ND,5’.

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Nua Money Limited’, check that the ‘Lien’ field in the LC Extraction File is equal to ‘1’ and that the ‘Geographic Region List’ field in the LC Extraction File is equal to one of the following: |

No findings noted |

| IE011 | IE024 | IE053 | |||||

| IE012 | IE025 | IE061 | |||||

| IE013 | IE041 | IE062 | |||||

| IE021 | IE042 | IE063 | |||||

| IE022 | IE051 | ||||||

| IE023 | IE052 |

| (C):

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Nua Money Limited’, check that the difference between (i) the maximum of the ‘Borrower Year of Birth’ and where applicable, the ’Second Applicant Year of Birth’ field in the LC Extraction File; and (ii) the origination year (as identified by the ‘Loan Origination Date’ field in the LC Extraction File); is greater than or equal to 21. |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 20 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

| 6 | Loan to Value

The LTV is calculated at origination by dividing the aggregate principal amount advanced to the Borrower at origination, by the valuation of the property obtained by Nua Money Limited at or prior to the completion of loan. |

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Nua Money Limited’, check that the Original LTV (calculated as the ‘Original Balance’ field in the LC Extraction File divided by the ‘Valuation Amount’ in the LC Extraction File, multiplied by 100) is less than or equal to 90%. | No findings noted |

| 7 | Valuations

In order for a valuation report to be accepted, it must be (i) valued in accordance with applicable international, European and national standards such as the International Valuation Standards Council, The European Group of Valuers Association, European Valuation Standards and the Royal Institution of Chartered Surveyors standards

and (ii) no older than 4 months prior to the relevant Mortgage Loan advance |

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Nua Money Limited’, check that the ‘Original Valuation Type’ field in the LC Extraction File is equal to ‘1’ (Full, internal and external inspection).

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Nua Money Limited’, check that the difference between the ‘Loan Origination Date’ field in the LC Extraction File and the ‘Valuation Date’ field in the LC Extraction File is no more than 4 calendar months. As instructed by the Data AUP Letter Recipients, this procedure has been performed with reference to the month and year of the Loan Origination Date and Valuation Date only. |

No findings noted |

| 8 | Loan Amount

The minimum loan amount is €50,000 and the maximum loan size on a single advance basis is €1,500,000. |

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Nua Money Limited’, check that the ‘Original Balance’ field in the LC Extraction File is greater than or equal to EUR 50,000 and less than or equal to EUR 1,500,000. | No findings noted |

| 9 | Mortgage Term

The minimum term of each Mortgage Loan is five years and the maximum term is 40 years, provided that the term of the Mortgage Loan ends before the primary Borrower’s 76th birthday. |

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Nua Money Limited’, check that the difference between ‘Loan Origination Date’ field and ‘Date of Loan Maturity’ field rounded down to the nearest whole month in the LC Extraction File is greater than or equal to 60 and less than or equal to 480. | No findings noted |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 21 |

| KPMG LLP Engagement to perform agreed-upon procedures in relation to a portfolio of Irish mortgage loans proposed to be the subject of a securitisation 1 July 2026 |

| 10 | Borrowers

(a) A minimum of one and a maximum of two Borrowers are allowed to be party to the Mortgage Loan and they must intend to live in the same household.

(c) Borrowers must be employed and/or self-employed and able to evidence the necessary repayment capacity based on the sustainable source of income.

(e) There is a minimum age requirement of 21 years of age at the time of the mortgage application. |

(a) For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Nua Money Limited’, check that the ‘Number of Debtors’ field in the LC Extraction File is less than or equal to 2.

(c) For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Nua Money Limited’, check that the ‘Borrowers Employment Status’ field in the LC Extraction File is equal to ‘1’ (Employment or Full loan is guaranteed) or ‘5’ (Self-employed).

For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Nua Money Limited’, check that the difference between (i) the maximum of the ‘Borrower Year of Birth’ and ‘Second Applicant Year of Birth’ fields in the LC Extraction File; and (ii) the origination year (as identified by the ‘Loan Origination Date’ field in the LC Extraction File); is greater than or equal to 21. |

No findings noted |

| 11 | Income and Repayment Capacity

(a) in order to be considered for a mortgage, single applicants must have a minimum income of €25,000 and joint applicants a combined minimum income of €50,000. Income must be confirmed either through PAYE or through a self-employed income confirmation mechanism;

(c) as part of the affordability assessment, an applicant’s or joint applicants’ sustainable income is estimated and verified that it is sufficient to cover the stressed cost of the proposed loan. When assessing this, a borrower’s credit commitments, other committed expenses, essential living costs and an expenditure buffer are taken into account. The different components of the calculation are derived from multiple data sources including information stated by the borrower, the Central Credit Register, payslips and bank statements and various statistical sources in Ireland and comparative benchmarks values from other mortgage lenders; |

(a) For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Nua Money Limited’:

- if the ‘Number of Debtors’ field in the LC Extraction File is equal to ‘1’, check that the ‘Primary Income’ field in the LC Extraction File is greater than or equal to EUR 25,000.

- if the ‘Number of Debtors’ field in the LC Extraction File is equal to ‘2’, check that the sum of the ‘Primary Income’ and ‘Secondary Income’ fields in the LC Extraction File is greater than or equal to EUR 50,000.

(c) For loans with a ‘Servicer Identifier’ field in the LC Extraction File equal to ‘Nua Money Limited’, check that the ‘Income Verification for Primary Income’ and ‘Income Verification for Secondary Income’ fields in the LC Extraction File are equal to ‘3’ (Verified). |

No findings noted |

HL/ES/UK010450 | Document Classification – KPMG Confidential | 22 |

|

Appendix C: Details of Findings

| KPMG Ref. | Procedure Nbr. | Data Attribute | Source | Extraction File Value | Finding | Source Value |

| 146 | Procedure 3b | Property Address | Land registry / Registry of Deeds (RoD) search / Legal charge / Folio / Irish Law Deed of Conveyance & Assignment (Unregistered Property) or where not available, the Solicitors Undertaking |

Does the address on the IT System match the source? |

D | Address

mismatch - Apartment number only |

| 234 | Procedure 3b | Property Address | Land registry / Registry of Deeds (ROD) search / Legal charge / Folio / Irish Law Deed of Conveyance & Assignment (Unregistered Property) or where not available, the Solicitors Undertaking |

Does the address on the IT System match the source? |

D | Address Unclear |

| 321 | Procedure 3b | Property Address | Land registry / Registry of Deeds (RoD) search / Legal charge / Folio / Irish Law Deed of Conveyance & Assignment (Unregistered Property) or where not available, the Solicitors Undertaking |

Does the address on the IT System match the source? |

D | Address

mismatch - Apartment number only |

| 339 | Procedure 3b | Property Address | Land registry / Registry of Deeds (RoD) search / Legal charge / Folio / Irish Law Deed of Conveyance & Assignment (Unregistered Property) or where not available, the Solicitors Undertaking |

Does the address on the IT System match the source? |

D | Address mismatch - Street / Road |

| 65 | Procedure 16.1 | Original Valuation Amount | IT System | 420,000 | D | 310,000 |

| 107 | Procedure 16.1 | Original Valuation Amount | IT System | 1,460,000 | D | 1,550,000 |

| 137 | Procedure 16.1 | Original Valuation Amount | IT System | 360,000 | D | 277,000 |

| 216 | Procedure 16.1 | Original Valuation Amount | IT System | 510,000 | D | 317,000 |

| 65 | Procedure 16.2 | Original Valuation Amount | Valuation Report | 420,000 | D | 310,000 |

| 137 | Procedure 16.2 | Original Valuation Amount | Valuation Report | 360,000 | D | 277,000 |

| 153 | Procedure 16.2 | Original Valuation Amount | Valuation Report | 228,000 | D | 320,000 |

| 159 | Procedure 16.2 | Original Valuation Amount | Valuation Report | 322,000 | D | 300,000 |

| 177 | Procedure 16.2 | Original Valuation Amount | Valuation Report | 465,000 | D | 480,000 |

| 216 | Procedure 16.2 | Original Valuation Amount | Valuation Report | 510,000 | D | 317,000 |

| 247 | Procedure 16.2 | Original Valuation Amount | Valuation Report | 470,000 | D | 495,000 |

| 374 | Procedure 16.2 | Original Valuation Amount | Valuation Report | 368,000 | D | 330,000 |

| 67 | Procedure 17.1 | Original Valuation Date | IT System | 14/09/2021 | D | 04/09/2024 |

| 75 | Procedure 17.1 | Original Valuation Date | IT System | 18/05/2021 | D | 09/09/2024 |

| 102 | Procedure 17.1 | Original Valuation Date | IT System | 18/02/2021 | D | 30/07/2024 |

| 106 | Procedure 17.1 | Original Valuation Date | IT System | 01/11/2018 | D | 05/05/2023 |

| 107 | Procedure 17.1 | Original Valuation Date | IT System | 06/12/2018 | D | 23/11/2021 |

| 135 | Procedure 17.1 | Original Valuation Date | IT System | 10/12/2021 | D | 10/01/2025 |

| 176 | Procedure 17.1 | Original Valuation Date | IT System | 29/06/2022 | D | 28/05/2025 |

| 209 | Procedure 17.1 | Original Valuation Date | IT System | 03/08/2018 | D | 18/09/2025 |

| 237 | Procedure 17.1 | Original Valuation Date | IT System | 01/03/2022 | D | 05/01/2025 |

| 275 | Procedure 17.1 | Original Valuation Date | IT System | 16/08/2021 | D | 23/09/2024 |

| 277 | Procedure 17.1 | Original Valuation Date | IT System | 25/04/2022 | D | 12/12/2023 |

| 326 | Procedure 17.1 | Original Valuation Date | IT System | 03/06/2021 | D | 11/06/2024 |

| 370 | Procedure 17.1 | Original Valuation Date | IT System | 02/03/2020 | D | 11/02/2025 |

| 65 | Procedure 17.2 | Original Valuation Date | Valuation Report | 04/08/2022 | D | 24/08/2017 |

Appendix C: Details of Findings

| KPMG Ref. | Procedure Nbr. | Data Attribute | Source | Extraction File Value | Finding | Source Value |

| 129 | Procedure 17.2 | Original Valuation Date | Valuation Report | 14/09/2018 | D | 27/11/2018 |

| 130 | Procedure 17.2 | Original Valuation Date | Valuation Report | 24/01/2022 | D | 13/07/2021 |

| 137 | Procedure 17.2 | Original Valuation Date | Valuation Report | 28/03/2022 | D | 22/07/2016 |

| 181 | Procedure 17.2 | Original Valuation Date | Valuation Report | 01/12/2022 | D | 01/12/2021 |

| 216 | Procedure 17.2 | Original Valuation Date | Valuation Report | 07/12/2021 | D | 13/09/2017 |

| 286 | Procedure 17.2 | Original Valuation Date | Valuation Report | 19/11/2021 | D | 30/08/2021 |

| 394 | Procedure 17.2 | Original Valuation Date | Valuation Report | 21/11/2021 | D | 20/10/2021 |

| 224 | Procedure 18 | Original Valuation Type | Valuation Report | Full, internal and external inspection | D | Subsequent |

| 216 | Procedure 19 | Latest Restructure Type | IT System | No restructure | D | Payment Break 14/01/2021 |

| 216 | Procedure 20 | Latest Restructure Date | IT System | No restructure | D | Payment Break 14/01/2021 |

| 175 | Procedure 22 | Payment Made (last 3 months) | IT System | Have there been payment made for the last 3 months (February 2026, March 2026, and April 2026)? |

D | No

payment made in February 2026, March 2026 and April 2026 by the Borrower |

| 245 | Procedure 25 | Borrower Year of Birth | IT System | 1980 & 1985 | D | 1980 & 1975 |

| 371 | Procedure 2b | Borrower Name | Land registry / Registry of Deeds (RoD) search / Legal charge / Folio / Irish Law Deed of Property) or where not available, the Solicitors Undertaking |

Does the name on the IT System match the source? |

MS | Source |

| 371 | Procedure 3b | Property Address | Land registry / Registry of Deeds (RoD) search / Legal charge / Folio / Irish Law Deed of Property) or where not available, the Solicitors Undertaking

|

Does the address on the IT System match the source? |

MS | Source |

| 232 | Procedure 21a | Signatures | Loan Acceptance / Loan Offer | Is the source signed? | MS | Missing from Source |

| 270 | Procedure 21b | Signatures | Valuation Report | Is the source signed? | MS | Missing from Source |

| 103 | Procedure 23 | Legal Charge | Land registry / Registry of Deeds (RoD) search / Legal charge / Folio / Irish Law Deed of Conveyance & Assignment (Unregistered Property) or where not available, the Solicitors Undertaking |

Does

Pepper Finance Corporation (Ireland) DAC or Finance Ireland Credit Solutions DAC hold the First Charge over the property? |

MS | No charge registered |

| 336 | Procedure 23 | Legal Charge | Land registry / Registry of Deeds (RoD) search / Legal charge / Folio / Irish Law Deed of Conveyance & Assignment (Unregistered Property) or where not available, the Solicitors Undertaking |

Does

Pepper Finance Corporation (Ireland) DAC or Finance Ireland Credit Solutions DAC hold the First Charge over the property? |

MS | No charge registered |

| 371 | Procedure 23 | Legal Charge | Land registry / Registry of Deeds (RoD) search / Legal charge / Folio / Irish Law Deed of Conveyance & Assignment (Unregistered Property) or where not available, the Solicitors Undertaking |

Does

Pepper Finance Corporation (Ireland) DAC or Finance Ireland Credit Solutions DAC hold the First Charge over the property? |

MS | Missing Source |