Energy Fuels: A Global, Diversified and Vertically Integrated Critical Materials CompanyJuly 2026UUUU NYSE American EFR TSX

Forward-Looking Statements and Notice Regarding Technical Disclosure Certain of the information contained in this presentation constitutes “forward-looking information” (as defined in the Securities Act (Ontario)) and“forward-looking statements” (as defined in the U.S. Private Securities Litigation Reform Act of 1995) thatare based on expectations, estimates and projections of management of Energy Fuels Inc. (“Energy Fuels“or the “Company) as of today’s date. Such forward-looking information and forward-looking statements include but are not limited to: the business strategy for Energy Fuels; Energy Fuels expectations with regard to current and future uranium, vanadium, heavy mineral sands (“HMS”) and rare earth element (“REE”) market conditions; the uranium industry’s ability to respond to higher demand; the impacts of recent market developments; business plans; outlook; objectives; expectations as to the prices of U3O8, V2O5, HMS products and REE’s; expectations as to reserves, resources, results of exploration and related expenses; estimated future production and costs; changes in project parameters; expected permitting and production time lines; the Company’s belief that it has the ability to develop an innovative, low-cost U.S.-centered REE supply chain or to build a globally significant critical supply chain company; the potential for additional business opportunities including vanadium, REE,HMS, alternate feed materials, and the cleanup of historic mines on the Navajo Nation and in other areas.; the potential for optimizing mining and processing; the Company’s belief in its readiness to capitalize on improving markets; expectations with regard to thepotential for U.S. government support of U.S. uranium miners and REE producers; global uranium supply risks; expected worldwide uranium supply and demand fundamentals; any expectation that the White Mesa Mill will be successful in producing REE Carbonate or separated REEs on a commercial basis; any expectation that Energy Fuels will be successful in developing its expanded U.S. separation capability, or other value-added U.S. REE production capabilities at the White Mesa Mill, or otherwise; any expectation that the company will successfully acquire 100% of the share capital of Australian Strategic Minerals (“ASM”) by way of a scheme arrangement under Australian law; any expectation that the proposed acquisition of Vacuumschmelze GmbH & Co. KG, Ara VAC TopCoUS LLC, and their respective consolidated subsidiaries (collectively, "VAC") from Ara Partners for a total cash-and-stock consideration will be completed as planned or at all; that the Sumter Facility will scale-up its capacity to 12,000 tpa magnets or at all ;any expectation tthat the Korean Metals Plant and/or American Metals Plant will be scaled up in the future; any expectation that the Company will be successful in developing a fully integrated REE supply chain; any expectation that the Company will be successful in fully integrating the U.S REE supply chain in the future; any expectation with respect to the future demand for REEs; any expectation with respect to the quantities of monazite ore to be acquired by Energy Fuels, the quantities of REE Carbonate or separated REE oxides to be produced by the White Mesa Mill or the quantities of contained total rare earth oxides [TREO]in the Mill’s REE carbonate; any expectation as to future exploration results for the Bahia Project; any expectation that acceptable fiscal terms and stability mechanisms will be successfully negotiated with the government of Madagascar; any expectation that all government approvals will be obtained, such that development may proceed at the Vara Mada Project; any expectation that the recovery of monazite will be added to the permits for the Vara Mada Project; any expectation that all permits will be obtained for the Donald Project; any expectation that the Company will be successful in permitting and developing the planned Phase 2 and Phase 3 REE Separation Facility at the White Mesa Mill; and any expectation that the Company will be successful in recovering radioisotopes for use in emerging TAT cancer therapeutics or that the program will be economically viable; any expectation that all required conditions will be satisfied and that the proposed the Department of War, U.S. Office of Strategic Capital (the "OSC") financing will be completed; any expectation that any of the government funding conditionally committed and in-discussion, including the recently announced $725 million loan from the OSC, will be funded as contemplated or at all. All statements contained herein which are not historical facts are forward-looking statements that involve risks, uncertainties and other factors that could cause actual results to differ materially from those expressed or impliedby such forward-looking information and forward-looking statements. Factors that could cause such differences, without limiting the generality of the foregoing include: risks that the synergies and effects on value described herein may not be achieved; risks inherent in exploration, development and production activities; volatility in market prices for uranium, vanadium, HMS products and REEs; the impact of the sales volume of uranium, vanadium, HMS and REEs; the ability to sustain production frommines and the mill; competition; the impact of change in foreign currency exchange; imprecision in mineral resource and reserveestimates; environmental and safety risks including increased regulatory burdens; changes to reclamation requirements; unexpected geological or hydrological conditions; a potential deterioration in political support for nuclear energy; changes in government regulations and policies, including with respect to tariffs, trade laws and related policies; demand for nuclear power, vanadium, HMS and REEs; replacement of production and failure to obtain necessary permits and approvals from government authorities; weather and other natural phenomena; ability to maintain and further improve positive labor relations; operating performance of the facilities; success of planned development projects; other development and operating risks; the company not being successful at acquiring 100% of the share capital of ASM or VAC, the Company not being successful in selling any uranium into the proposed Uranium Reserve at acceptable quantities or prices, or at all in the future; available supplies of monazite sands; the ability of the White Mesa Mill to produce REE Carbonate or separated REE oxides to meet commercial specifications on a commercial scale at acceptable costs; market factors, including future demand for REEs; actions or inactions by foreign governments, such as the government of Madagascar; instability of foreign governments; the inability to receive or delays in the receipt of all required permits for the Vara Mada project and the Donald Project; the ability of Energy Fuels to potentially recover radioisotopes from its existing process streams for use in TAT therapeutics; the ability to obtain permits to support any scale-up of radioisotope or REE production at the Mill; and the future development of the TAT market. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, believed, estimated or expected. Although Energy Fuels believes that the assumptions inherent in the forward-looking statements are reasonable, undue reliance should not be placed on these statements, which only apply as of the date of this presentation. Energy Fuels does not undertake any obligation to publicly update or revise any forward-looking information or forward-looking statements after the date of this presentation to conform such information to actual results or to changes in Energy Fuels’ expectations except as otherwise required by applicable legislation. Additional information about the material factors or assumptions on which forward looking information is based or the material risk factors that may affect results is contained under “Risk Factors” in Energy Fuels’ annual report on Form 10-K for the year ended December 31, 2025. The annual report on Form 10-K is available on SEDAR at www.sedarplus.ca and on EDGAR at www.sec.gov. This presentation shall not constitute an offer to sell or a solicitation of an offer to purchase any securities in any state or jurisdiction in which such an offer, solicitation or sale would be unlawful. This presentation contains estimates, projections and other information concerning the Company’s industry, business and the markets for its products. Information that is based on estimates, forecasts, projections, market research or similar methodologies is inherently subject to uncertainties, and actual events or circumstances may differ materially from events and circumstances that are assumed in this information. Unless otherwise expressly stated, the Company obtains this industry, business, market and other data from its own internal estimates and research, as well as from reports, research surveys, studies and similar data prepared by market research firms and other third parties, industry and general publications, government data and similar sources. All technical information including mineral estimates constituting mining operations that are material to our business or financial condition included in this presentation, have been prepared in accordance with both 17 CFR Subpart 220.1300 and 229.601(b)(96) (collectively, “S-K 1300”) and Canadian National Instrument 43-101 - Standards of Disclosure for Mineral Projects (“NI 43-101”) and are supported by pre-feasibility studies and/or initial assessments prepared in accordance with both the requirements of S-K 1300 and NI 43-101. S-K 1300 and NI 43-101 both provide for the disclosure of: (i) “Inferred Mineral Resources,” which investors should understand have the lowest level of geological confidence of all mineral resources and thus may not be considered when assessing the economic viability of a mining project and may not be converted to a Mineral Reserve; (ii) “Indicated Mineral Resources,” which investors should understand have a lower level of confidence than that of a “Measured Mineral Resource” andthus may be converted only to a “Probable Mineral Reserve”; and (iii) “Measured Mineral Resources,” which investors should understand have sufficient geological certainty to be converted to a “Proven Mineral Reserve” or to a “Probable Mineral Reserve.” Investors are cautioned not to assume that allor any part of Measured or Indicated Mineral Resources will ever be converted into Mineral Reserves as defined by S-K 1300 or NI 43-101. Investors are cautioned not to assume that all or any part of an Inferred Mineral Resource exists or is economically or legally mineable, or that an Inferred Mineral Resource will ever be upgraded to a higher category. Qualified Person Statement The scientific and technical information disclosed in this news release was reviewed and approved byDaniel D. Kapostasy, PG, Registered Member SME and Vice President, Technical Services for the Company, who is a "Qualified Person" as defined in S-K 1300 and National Instrument 43-101.

Energy Fuels responsibly produces the critical materials that make many clean energy and advanced technologies possible. We are a leading U.S. producer of uranium, rare earths and critical minerals, transforming strategic resources into the advanced materials essential for energy security, electrification, advanced manufacturing and national defense. We are well positioned to provide a resilient and derisked supply chain through integrated mining, processing and magnets manufacturing capabilities for a more secure and sustainable future.

Uniquely Positioned to Supply the Most Critical Sectors of the Global Economy Energy Fuels poised to supply technical solutions that support the world’s growing demand for energy, mobility, advanced technologies & defense Defining Our Strategic Position Supplying Critical Materials to Strategic End Markets Driving Competitive Advantage Through a Differentiated Value Proposition Supplier of choice Leading global player Scalable multi-technology growth Leading industry returns Data centers CAGR: 28.1%1 Nuclear energy CAGR: 3.8%2 Uranium CAGR: 5.8%4 Robotics Automotive 19.0%3 REE Uranium Low operating cost Leading technical capabilities Derisked, fully vertically integrated platform from mine-to-magnet Strong government support Sustainable solutions Sources: GlobalData, Wood Mackenzie, IEA, Mordor Intelligence, Goldman Sachs, Barclays (1) Estimated data center demand (GWh) 2026E-2035E CAGR from Wood Mackenzie. (2) Global nuclear installed capacity 2026E –2035E CAGR projected by Wood Mackenzie. (3) Global fleet of EVs 2025A –2035E CAGR estimated by IEA. (4) Global uranium production 2026E –2035E CAGR forecasted by GlobalData. (5) 2025A –2035E CAGR for global humanoid robot shipments estimated by Goldman Sachs. (6) The Business Research Company: Global Aerospace & Defense Market Briefing 2025

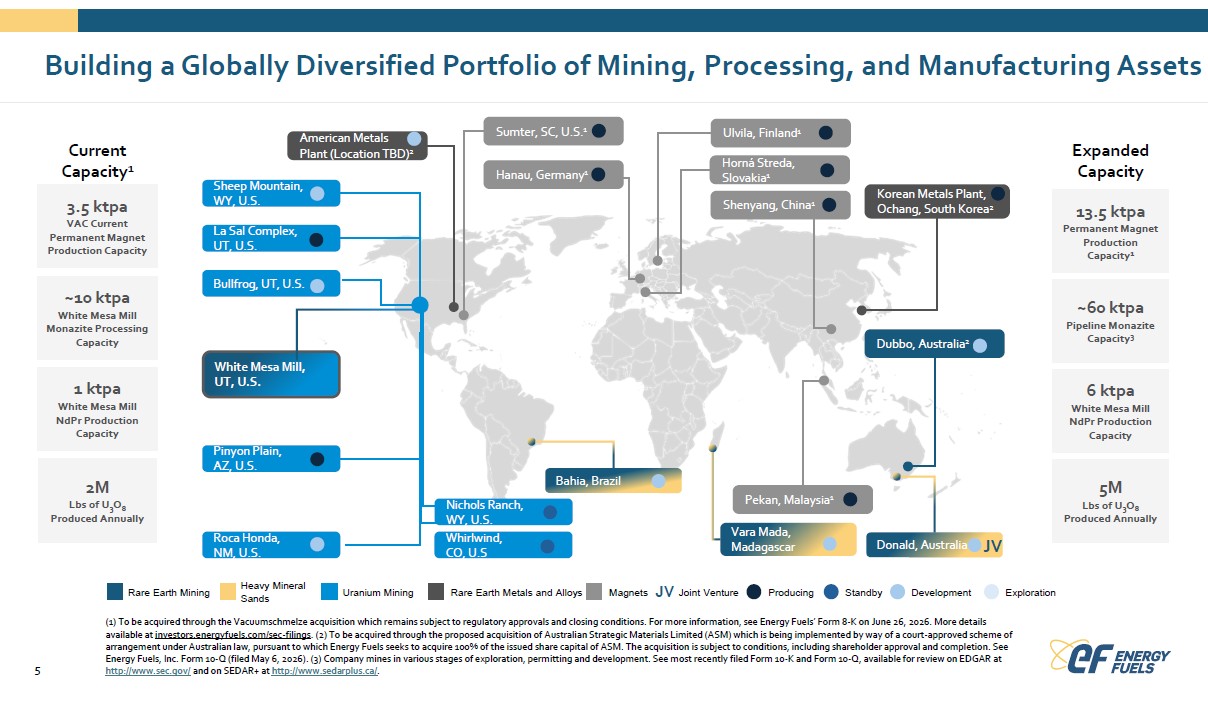

Building a Globally Diversified Portfolio of Mining, Processing, and Manufacturing Assets (1) To be acquired through the Vacuumschmelze acquisition which remains subject to regulatory approvals and closing conditions. For more information, see Energy Fuels’ Form 8-K on June 26, 2026. More details available at investors.energyfuels.com/sec-filings. (2) To be acquired through the proposed acquisition of Australian Strategic Materials Limited (ASM) which is being implemented by way of a court-approved scheme of arrangement under Australian law, pursuant to which Energy Fuels seeks to acquire 100% of the issued share capital of ASM. The acquisition is subject to conditions, including shareholder approval and completion. See Energy Fuels, Inc. Form 10-Q (filed May 6, 2026). (3) Company mines in various stages of exploration, permitting and development. See most recently filed Form 10-K and Form 10-Q, available for review on EDGAR at http://www.sec.gov/ and on SEDAR+ at http://www.sedarplus.ca/.

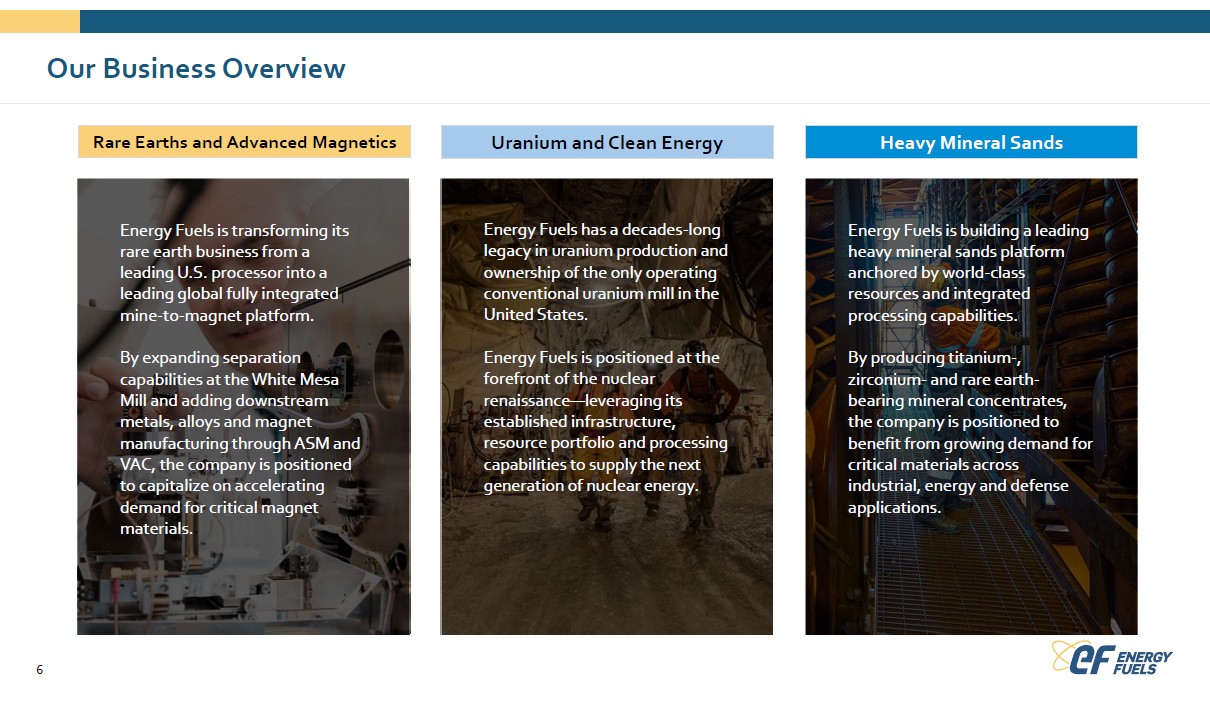

Our Business Overview Rare Earths and Advanced Magnetics Energy Fuels is transforming its rare earth business from a leading U.S. processor into a leading global fully integrated mine-to-magnet platform. By expanding separation capabilities at the White Mesa Mill and adding downstream metals, alloys and magnet manufacturing through ASM and VAC, the company is positioned to capitalize on accelerating demand for critical magnet materials. Uranium and Clean Energy. Energy Fuels has a decades-long legacy in uranium production and ownership of the only operating conventional uranium mill in the United States. Energy Fuels is positioned at the forefront of the nuclear renaissance—leveraging its established infrastructure, resource portfolio and processing capabilities to supply the next generation of nuclear energy. Heavy Mineral Sands Energy Fuels is building a leading heavy mineral sands platform anchored by world-class resources and integrated processing capabilities. By producing titanium-, zirconium- and rare earth-bearing mineral concentrates, the company is positioned to benefit from growing demand for critical materials across industrial, energy and defense applications.

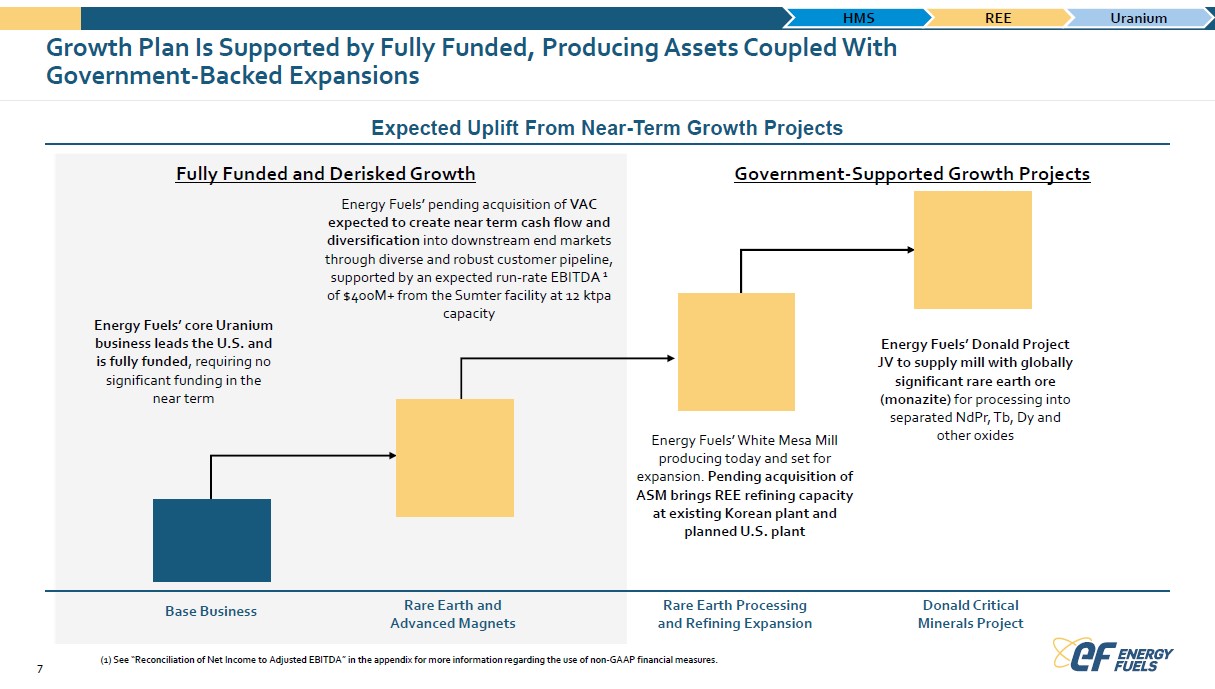

Growth Plan Is Supported by Fully Funded, Producing Assets Coupled With Government-Backed Expansions Expected Uplift From Near-Term Growth Projects Fully Funded and Derisked Growth Energy Fuels’ pending acquisition of VAC expected to create near term cash flow and diversification into downstream end markets through diverse and robust customer pipeline, supported by an expected run-rate EBITDA 1 of $400M+ from the Sumter facility at 12 ktpa capacity Energy Fuels’ core Uranium business leads the U.S. and is fully funded, requiring no significant funding in the near term Government-Supported Growth Projects Energy Fuels’ White Mesa Mill producing today and set for expansion. Pending acquisition of ASM brings REE refining capacity at existing Korean plant and planned U.S. plant Energy Fuels’ Donald Project JV to supply mill with globally significant rare earth ore (monazite) for processing into separated NdPr, Tb, Dy and other oxides Base Business Rare Earth and Advanced Magnets Rare Earth Processing and Refining Expansion Donald Critical Minerals Project (1) See “Reconciliation of Net Income to Adjusted EBITDA” in the appendix for more information regarding the use of non-GAAP financial measures.

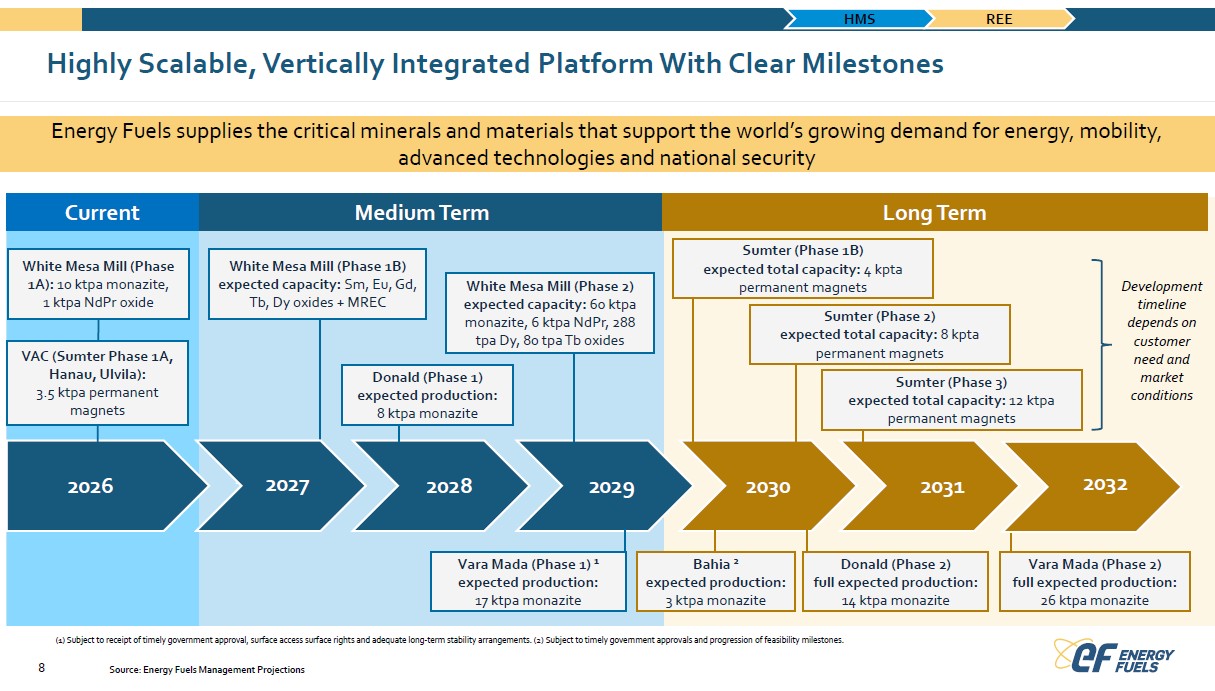

Highly Scalable, Vertically Integrated Platform With Clear Milestones Energy Fuels supplies the critical minerals and materials that support the world’s growing demand for energy, mobility, advanced technologies and national security (1) Subject to receipt of timely government approval, surface access surface rights and adequate long-term stability arrangements. (2) Subject to timely government approvals and progression of feasibility milestones. White Mesa Mill (Phase 1A): 10 ktpa monazite, 1 ktpa NdPr oxide VAC (Sumter Phase 1A, Hanau, Ulvila): 3.5 ktpa permanent magnets White Mesa Mill (Phase 1B) expected capacity: Sm, Eu, Gd, Tb, Dy oxides + MREC Donald (Phase 1) expected production: 8 ktpa monazite White Mesa Mill (Phase 2) expected capacity: 60 ktpa monazite, 6 ktpa NdPr, 288 tpa Dy, 80 tpa Tb oxides Sumter (Phase 1B) expected total capacity: 4 kpta permanent magnets Sumter (Phase 2)expected total capacity: 8 kpta permanent magnets Sumter (Phase 3) expected total capacity: 12 ktpa permanent magnets Development timeline depends on customer need and market conditions Vara Mada (Phase 1) 1 expected production: 17 ktpa monazite Bahia 2 expected production: 3 ktpa monazite Donald (Phase 2) full expected production: 14 ktpa monazite Vara Mada (Phase 2) full expected production: 26 ktpa monazite

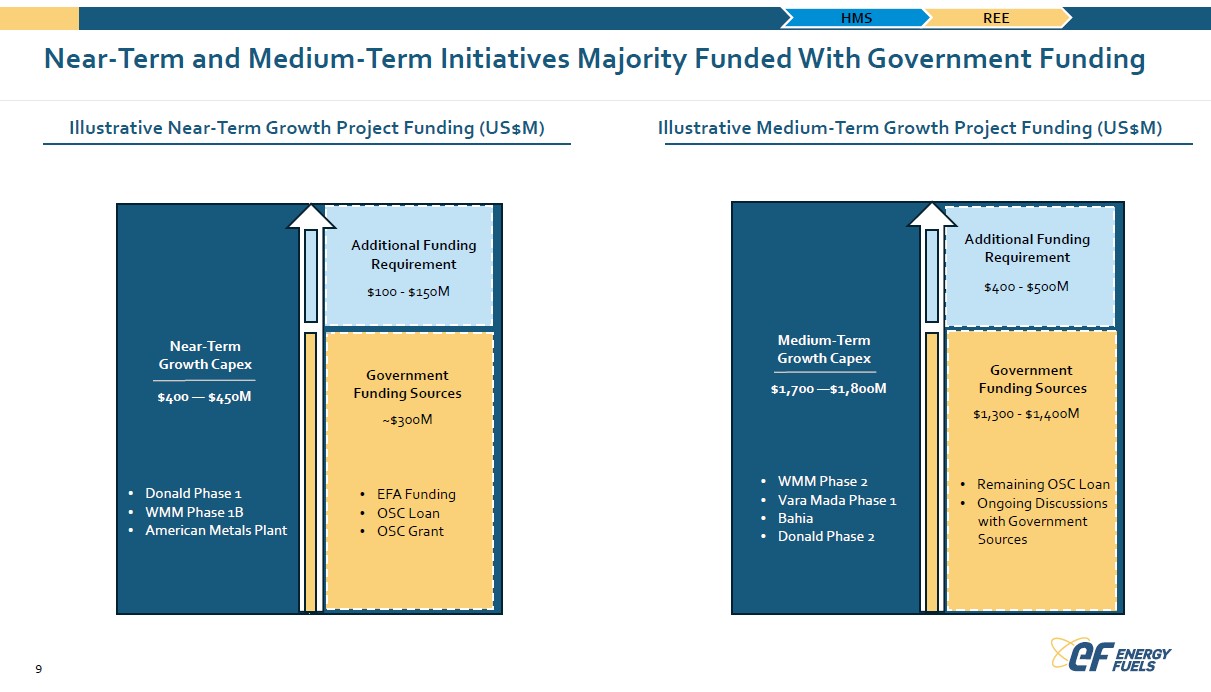

Near-Term and Medium-Term Initiatives Majority Funded With Government Funding Illustrative Near-Term Growth Project Funding (US$M) Illustrative Medium-Term Growth Project Funding (US$M)

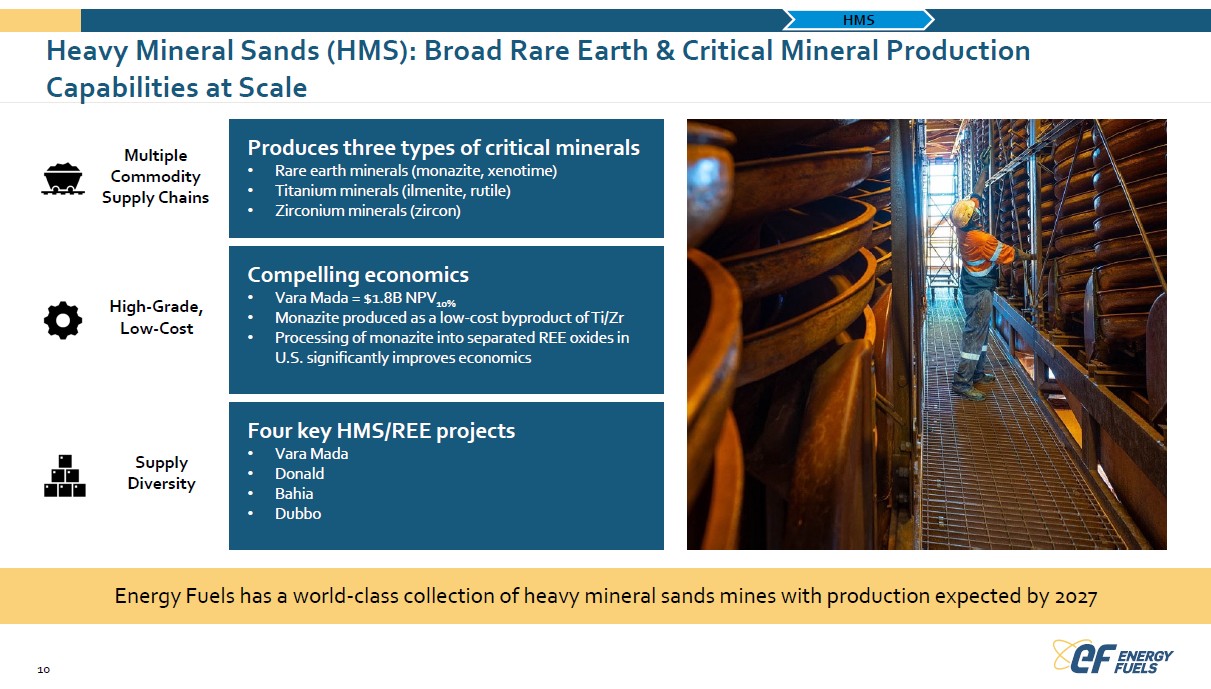

Heavy Mineral Sands (HMS): Broad Rare Earth & Critical Mineral Production Capabilities at Scale Multiple Commodity Supply Chains Produces three types of critical minerals Rare earth minerals (monazite, xenotime) Titanium minerals (ilmenite, rutile) Zirconium minerals (zircon) High-Grade, Low-Cost Compelling economics Vara Mada = $1.8B NPV10% Monazite produced as a low-cost byproduct of Ti/Zr Processing of mo nazite into separated REE oxides in U.S. significantly improves economics Supply Diversity Four key HMS/REE projects Vara Mada Donald Bahia Dubbo Energy Fuels has a world-class collection of heavy mineral sands mines with production expected by 2027

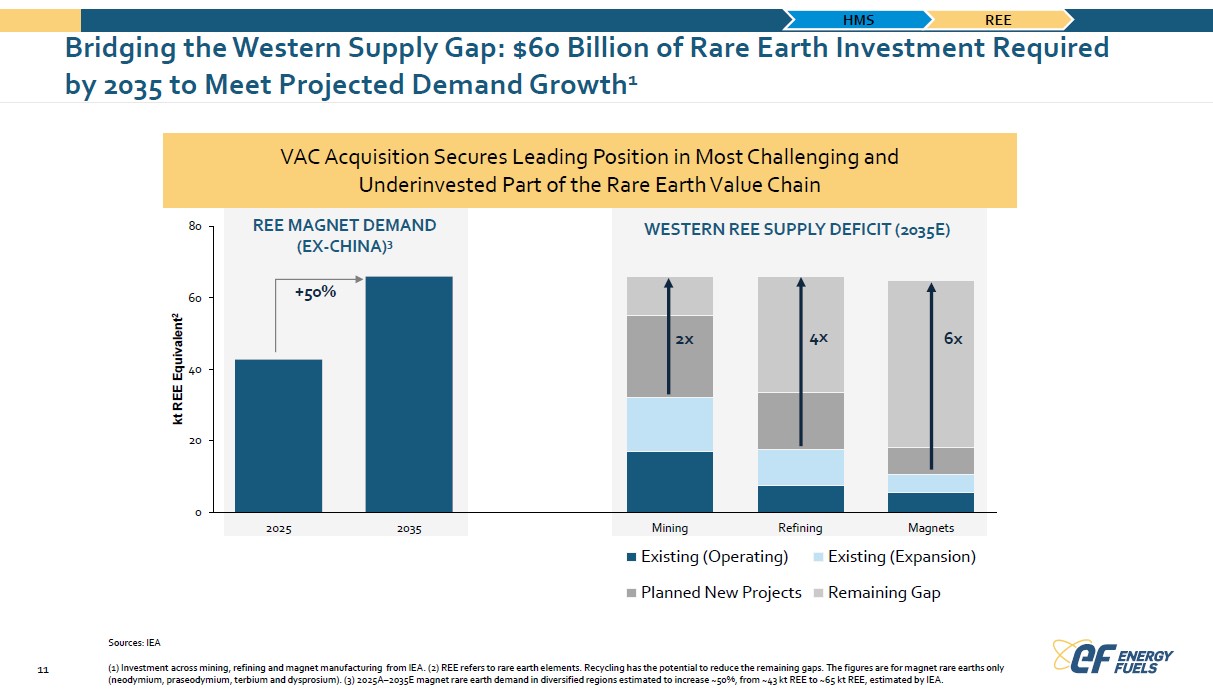

Bridging the Western Supply Gap: $60 Billion of Rare Earth Investment Required by 2035 to Meet Projected Demand Growth1 VAC Acquisition Secures Leading Position in Most Challenging and Underinvested Part of the Rare Earth Value Chain REE MAGNET DEMAND (EX-CHINA)3 WESTERN REE SUPPLY DEFICIT (2035E) Sources: IEA (1) Investment across mining, refining and magnet manufacturing from IEA. (2) REE refers to rare earth elements. Recycling has the potential to reduce the remaining gaps. The figures are for magnet rare earths only (neodymium, praseodymium, terbium and dysprosium). (3) 2025A–2035E magnet rare earth demand in diversified regions estimated to increase ~50%, from ~43 kt REE to ~65 kt REE, estimated by IEA.

Rare Earth Elements (REE): Delivering on All Aspects of a True Mine-to-Magnet Platform Expanding U.S. REE processing capacity WMM is the only U.S facility with existing commercial monazite processing capacity Planned expansion increases capacity to process 60,000 tpa of monazite into ~6,294 tpa of NdPr, 288 tpa of Dy and 80 tpa Tb oxides Rare earth (monazite, xenotime) Adding strategic metallization platform Pending acquisition of ASM adds existing rare earth metal and alloy production in South Korea with plans to expand in U.S. Enhances vertical integration and margin capture across the rare earth metals value chain Establishing global magnet leadership Pending acquisition of VAC adds leadership in NdFeB and SmCo magnet manufacturing in U.S., EU and Asia Diversified magnetics portfolio enhances cross-selling across electrification and industrial applications Energy Fuels is integrating mining, processing, metallization and advanced magnet manufacturing capabilities

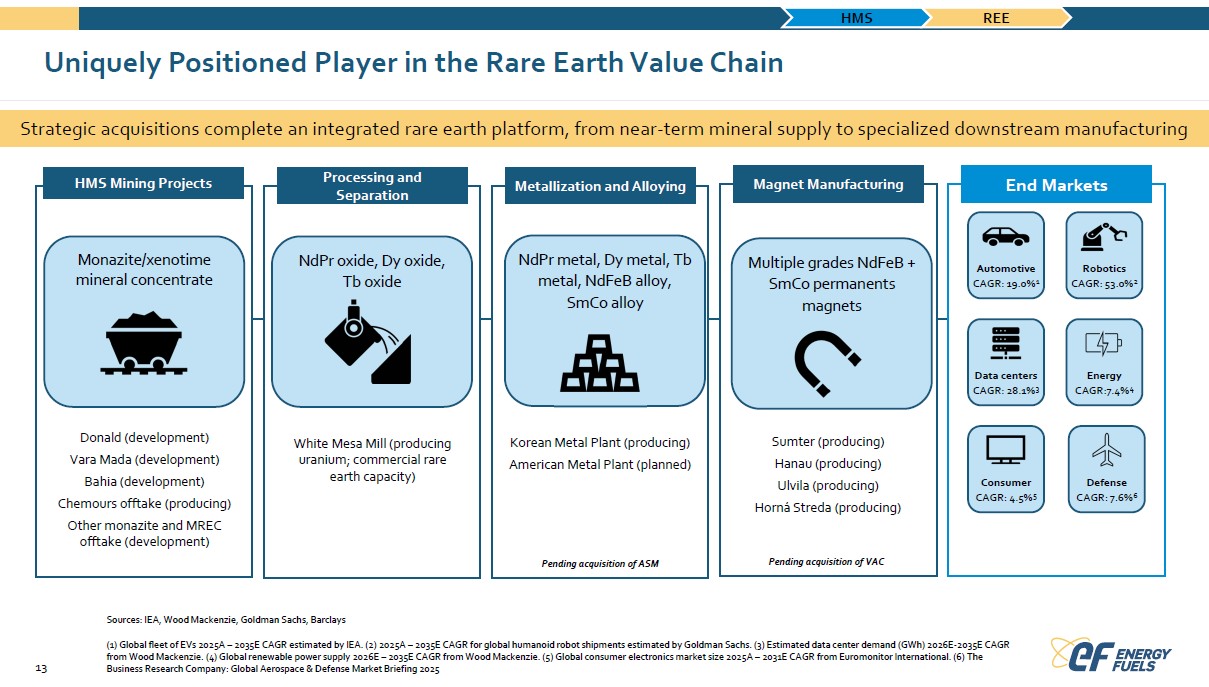

Uniquely Positioned Player in the Rare Earth Value Chain Strategic acquisitions complete an integrated rare earth platform, from near-term mineral supply to specialized downstream manufacturing HMS Mining Projects Processing and Separation Metallization and Alloying Magnet Manufacturing End Markets Donald (development)Vara Mada (development)Bahia (development)Chemours offtake (producing)Other monazite and MREC offtake (development) White Mesa Mill (producing uranium; commercial rare earth capacity Korean Metal Plant (producing) American Metal Plant (planned) Sumter (producing) Hanau (producing) Ulvila (producing) Horná Streda (producing) Sources: IEA, Wood Mackenzie, Goldman Sachs, Barclays (1) Global fleet of EVs 2025A – 2035E CAGR estimated by IEA. (2) 2025A – 2035E CAGR for global humanoid robot shipments estimated by Goldman Sachs. (3) Estimated data center demand (GWh) 2026E-2035E CAGR from Wood Mackenzie. (4) Global renewable power supply 2026E – 2035E CAGR from Wood Mackenzie. (5) Global consumer electronics market size 2025A – 2031E CAGR from Euromonitor International. (6) The Business Research Company: Global Aerospace & Defense Market Briefing 2025

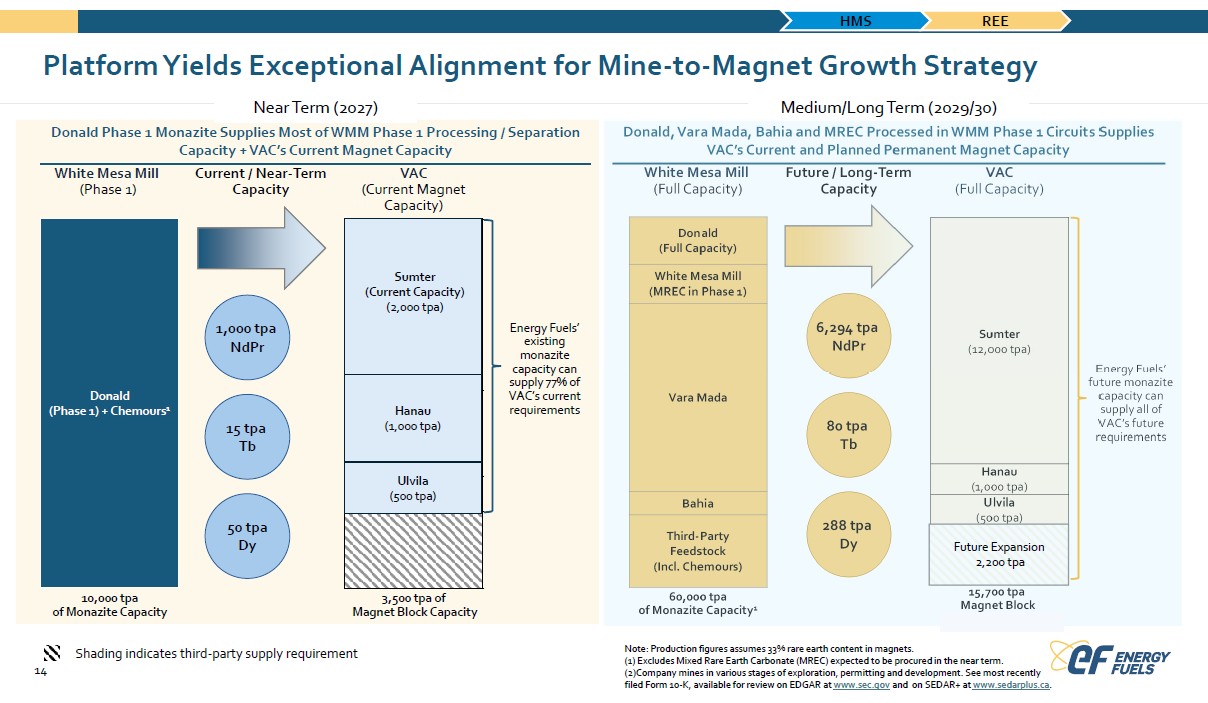

Platform Yields Exceptional Alignment for Mine-to-Magnet Growth Strategy Near Term (2027) Donald Phase 1 Monazite Supplies Most of WMM Phase 1 Processing / Separation Capacity + VAC’s Current Magnet Capacity Medium/Long Term (2029/30) Donald, Vara Mada, Bahia and MREC Processed in WMM Phase 1 Circuits Supplies VAC’s Current and Planned Permanent Magnet Capacity Shading indicates third-party supply requirement (1) Excludes Mixed Rare Earth Carbonate (MREC) Note: Production figures assumes 33% rare earth content in magnets. expected to be procured in the near term. (2) Company mines in various stages of exploration, permitting and development. See most recently filed Form 10-K, available for review on EDGAR at www.sec.gov and on SEDAR+ at www.sedarplus.ca.

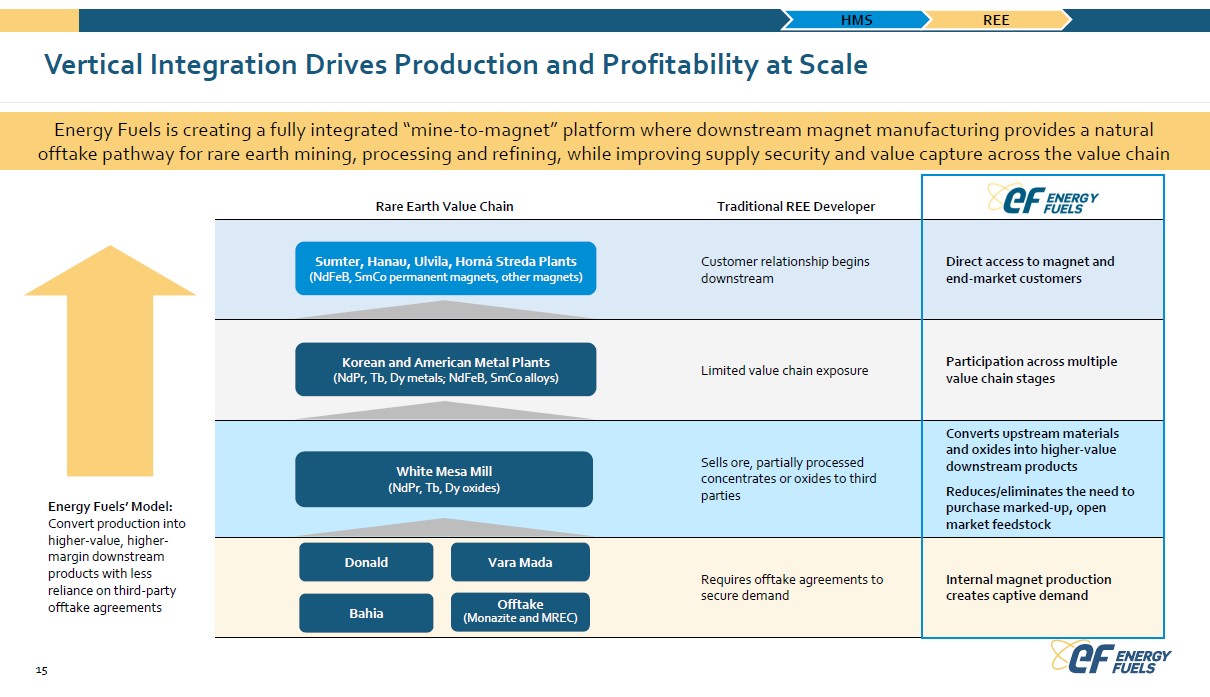

Vertical Integration Drives Production and Profitability at Scale Energy Fuels is creating a fully integrated “mine-to-magnet” platform where downstream magnet manufacturing provides a natural offtake pathway for rare earth mining, processing and refining, while improving supply security and value capture across the value chain

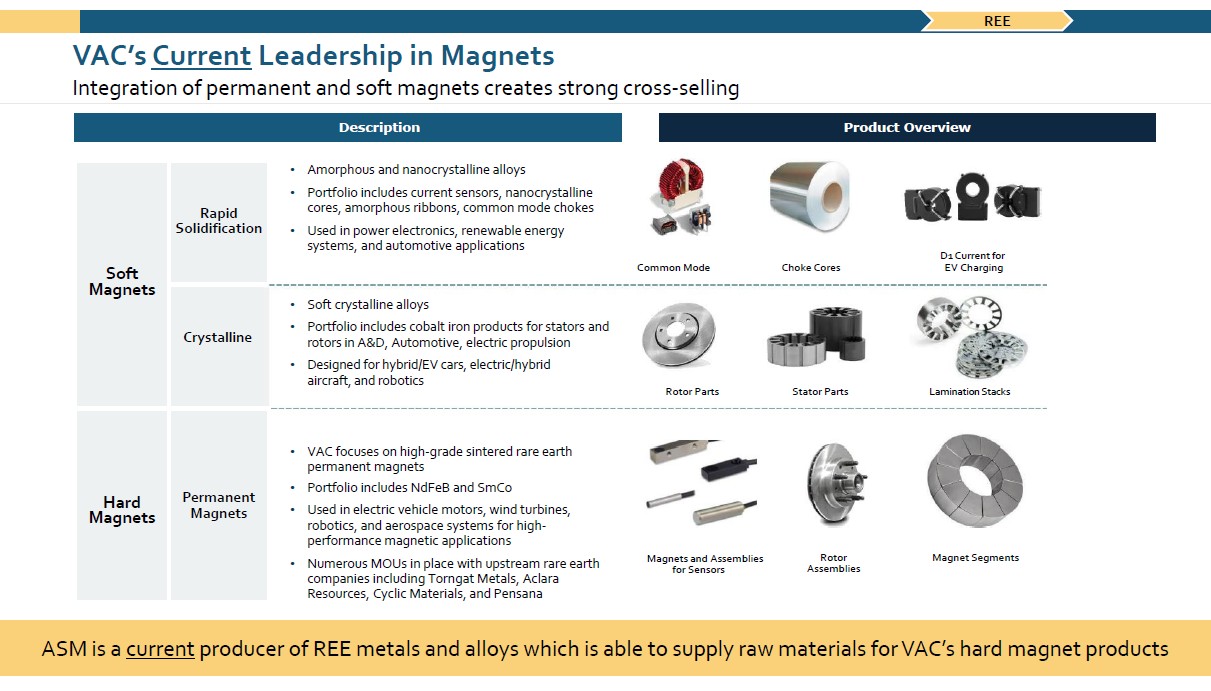

VAC’s Current Leadership in Magnets Integration of permanent and soft magnets creates strong cross-selling• Amorphous and nanocrystalline alloys • Portfolio includes current sensors, nanocrystalline cores, amorphous ribbons, common mode chokes

• Used in power electronics, renewable energy systems, and automotive applications• Soft crystalline alloys • Portfolio includes cobalt iron products for stators and rotors in A&D, Automotive, electric propulsion • Designed for hybrid/EV cars, electric/hybrid

aircraft, and robotics • VAC focuses on high-grade sintered rare earth permanent magnets • Portfolio includes NdFeB and SmCo• Used in electric vehicle motors, wind turbines, robotics, and aerospace systems for high-performance magnetic applications

• Numerous MOUs in place with upstream rare earth companies including Torngat Metals, Aclara Resources, Cyclic Materials, and Pensana ASM is a current producer of REE metals and alloys which is able to supply raw materials for VAC’s hard magnet products

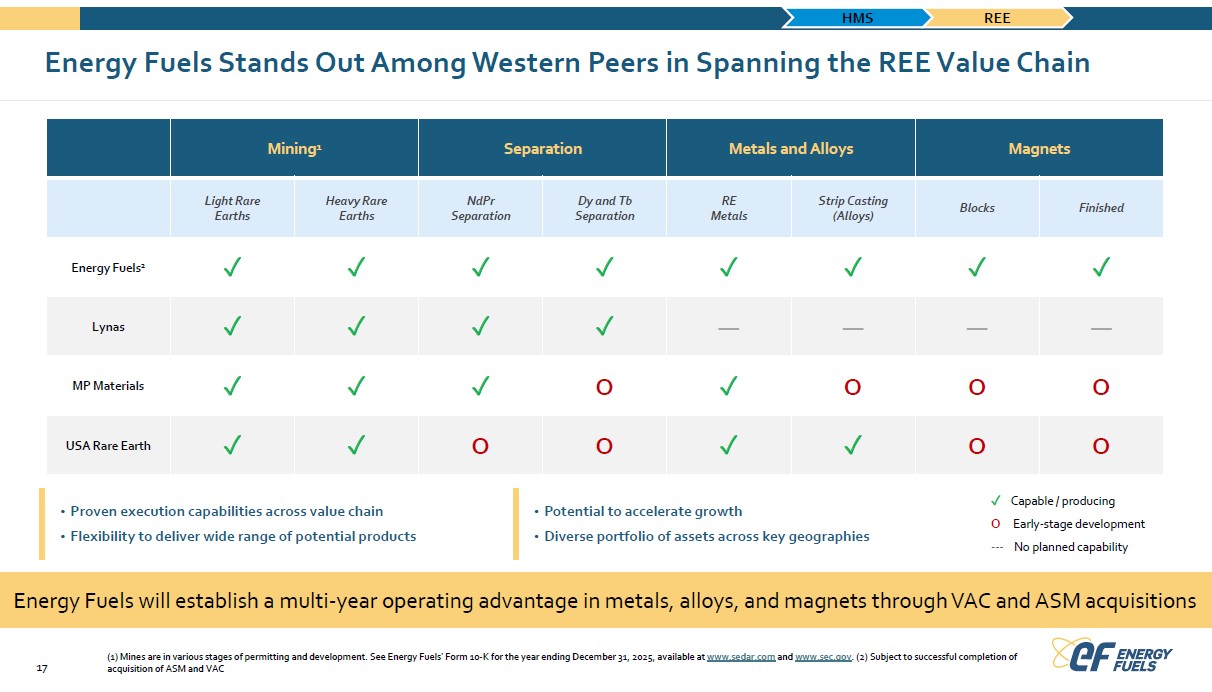

Energy Fuels Stands Out Among Western Peers in Spanning the REE Value Chain Energy Fuels will establish a multi-year operating advantage in metals, alloys, and magnets through VAC and ASM acquisitions (1) Mines are in various stages of permitting and development. See Energy Fuels’ Form 10-K for the year ending December 31, 2025, available at www.sedar.com and www.sec.gov. (2) Subject to successful completion of acquisition of ASM and VAC

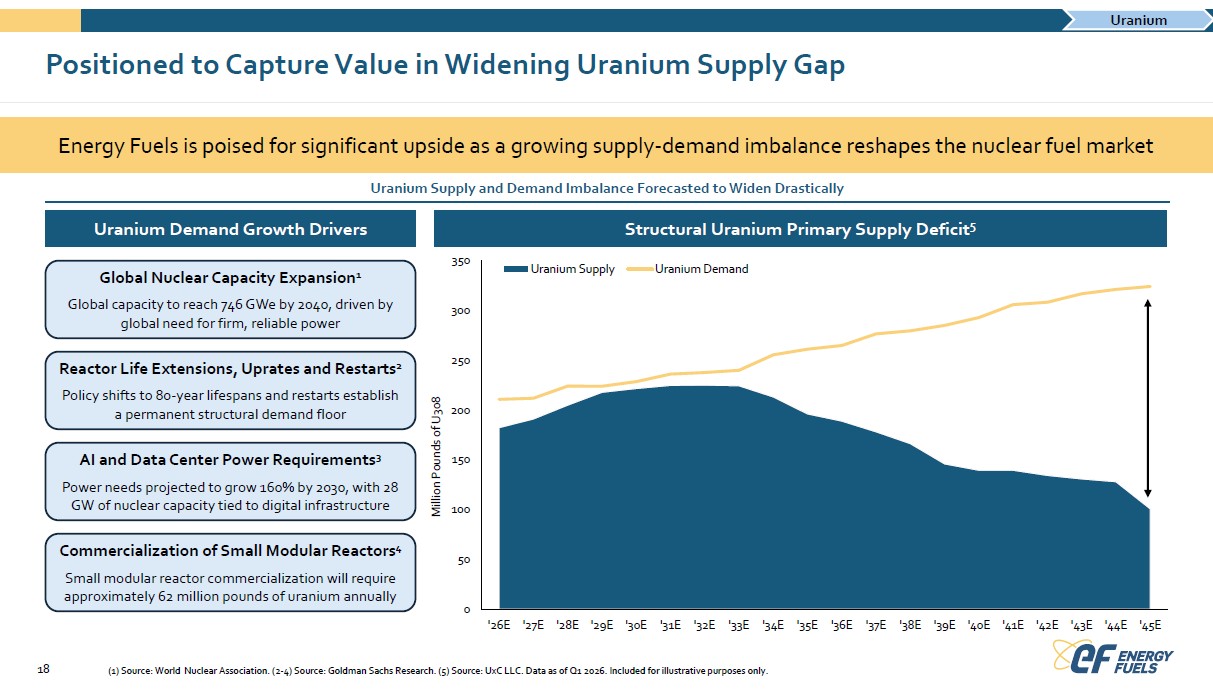

Positioned to Capture Value in Widening Uranium Supply Gap Energy Fuels is poised for significant upside as a growing supply-demand imbalance reshapes the nuclear fuel market Uranium Supply and Demand Imbalance Forecasted to Widen Drastically Uranium Demand Growth Drivers Structural Uranium Primary Supply Deficit5 Global Nuclear Capacity Expansion1 Global capacity to reach 746 GWe by 2040, driven by global need for firm, reliable power Reactor Life Extensions, Uprates and Restarts2

Policy shifts to 80-year lifespans and restarts establish a permanent structural demand floor AI and Data Center Power Requirements3 Power needs projected to grow 160% by 2030, with 28 GW of nuclear capacity tied to digital infrastructure Commercialization of Small Modular Reactors4 Small modular reactor commercialization will require approximately 62 million pounds of uranium annually (1) Source: World Nuclear Association. (2-4) Source: Goldman Sachs Research. (5) Source: UxC LLC. Data as of Q1 2026. Included for illustrative purposes only.

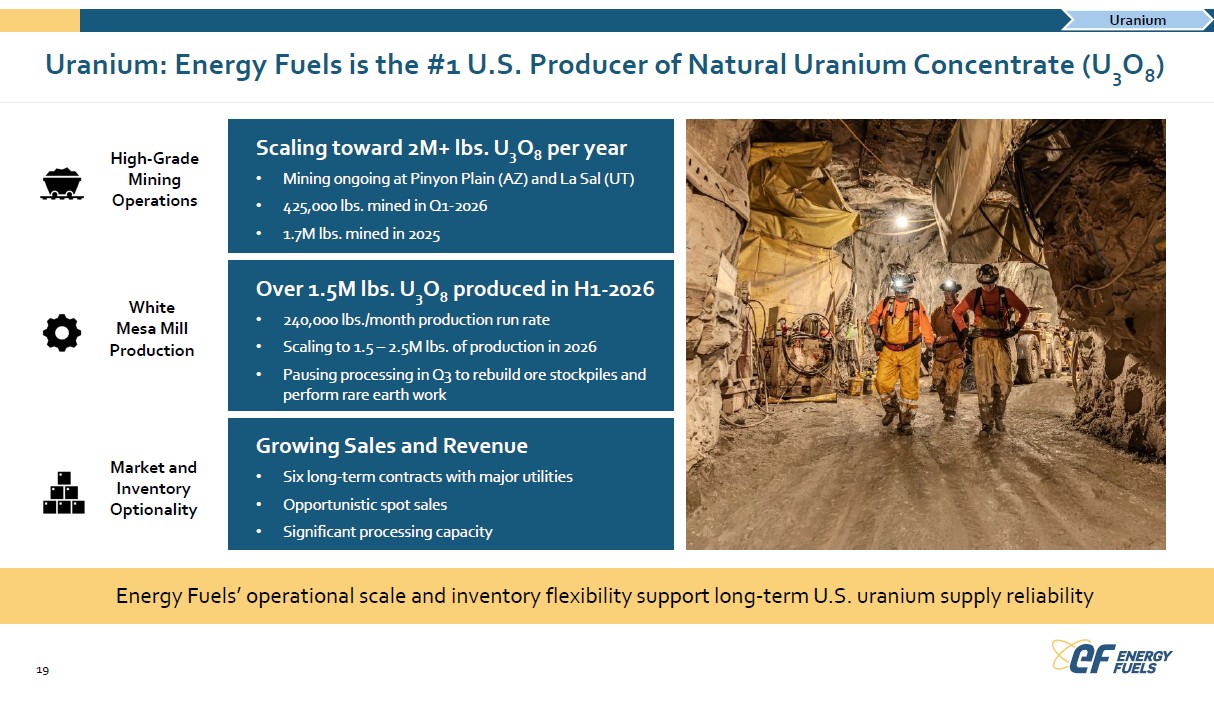

Uranium: Energy Fuels is the #1 U.S. Producer of Natural Uranium Concentrate (U3O8) Scaling toward 2M+ lbs. U3O8 per year • Mining ongoing at Pinyon Plain (AZ) and La Sal (UT) • 425,000 lbs. mined in Q1-2026 • 1.7M lbs. mined in 2025Over 1.5M lbs. U3O8 produced in H1-2026 • 240,000 lbs./month production run rate • Scaling to 1.5 – 2.5M lbs. of production in 2026 • Pausing processing in Q3 to rebuild ore stockpiles and perform rare earth work Growing Sales and Revenue • Six long-term contracts with major utilities • Opportunistic spot sales • Significant processing capacity Energy Fuels’ operational scale and inventory flexibility support long-term U.S. uranium supply reliability

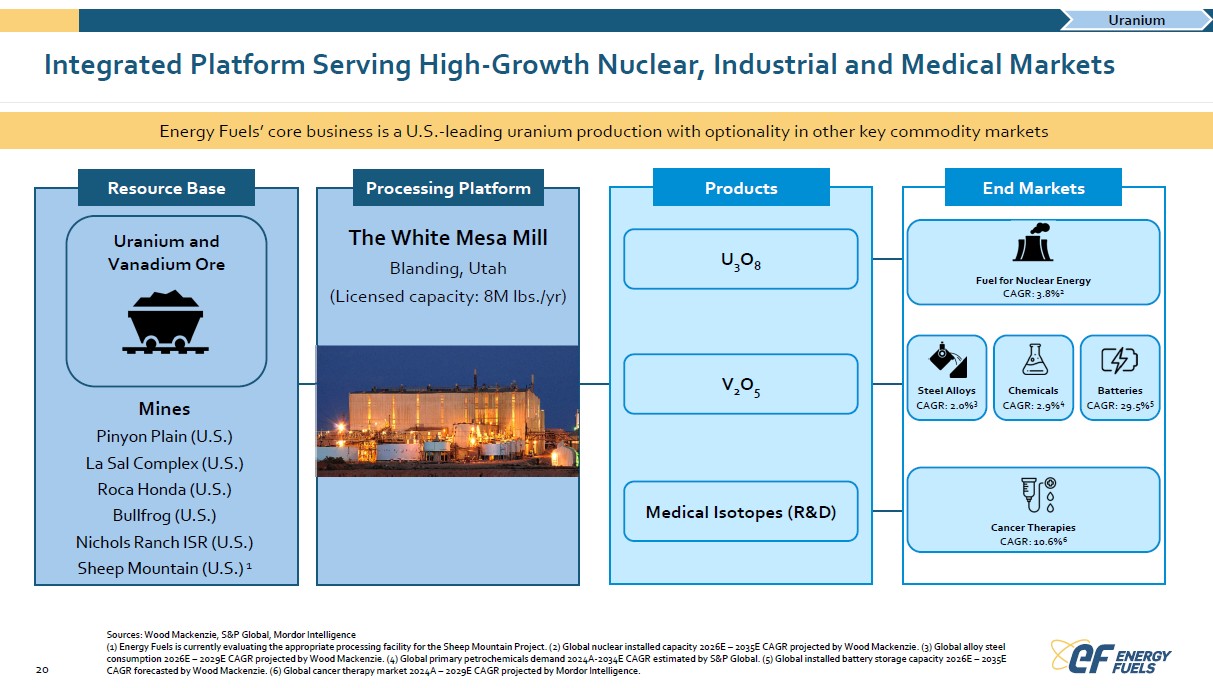

Integrated Platform Serving High-Growth Nuclear, Industrial and Medical Markets Energy Fuels’ core business is a U.S.-leading uranium production with optionality in other key commodity markets Sources: Wood Mackenzie, S&P Global, Mordor Intelligence

(1) Energy Fuels is currently evaluating the appropriate processing facility for the Sheep Mountain Project. (2) Global nuclear installed capacity 2026E –2035E CAGR projected by Wood Mackenzie. (3) Global alloy steel consumption 2026E – 2029E CAGR projected by Wood Mackenzie. (4) Global primary petrochemicals demand 2024A-2034E CAGR estimated by S&P Global. (5) Global installed battery storage capacity 2026E –2035E CAGR forecasted by Wood Mackenzie. (6) Global cancer therapy market 2024A –2029E CAGR projected by Mordor Intelligence.

Empowering the world’s most strategic industries as a global, diversified and vertically integrated critical materials company Established and Soon-To-Be Acquired Businesses Underpin Growth: Acquisitions of ASM and VAC advance Energy Fuels’ mine-to-magnet REE strategy, complementing established U.S.-leading uranium operations. Building a Derisked and Differentiated Critical Materials Platform: Combining world-class rare earth, heavy mineral sand, magnets, and uranium assets across the U.S. and allied nations to create a globally competitive and scalable critical minerals company. Leveraging Unique Processing and Integration Capabilities: The White Mesa Mill is the only U.S. facility capable of producing monazite-derived rare earth oxides for downstream processing into rare earth metals, alloys and magnets through pending acquisitions of ASM and VAC. Creating Value Across Critical Mineral Supply Chains: Advancing from mining into separation, metallization, alloying and magnet manufacturing to enhance margins, secure demand and reduce reliance on third-party suppliers and manufacturers. Positioned for Long-Term Secular Growth: Supplying materials essential to nuclear energy, electrification, robotics, defense systems, industrial automation, data centers and other advanced technologies benefiting from growing demand for secure Western supply chains.

Appendix

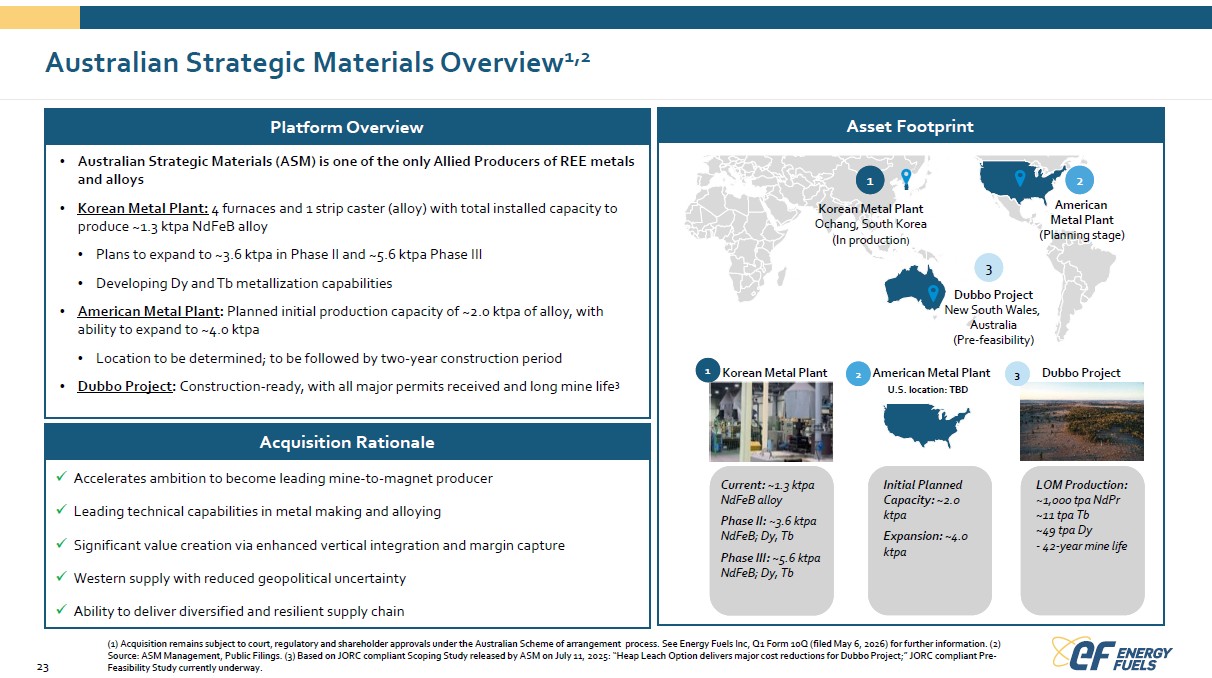

Australian Strategic Materials Overview1,2 Platform Overview Asset Footprint • Australian Strategic Materials (ASM) is one of the only Allied Producers of REE metals and alloys • Korean Metal Plant: 4 furnaces and 1 strip caster (alloy) with total installed capacity to produce ~1.3 ktpa NdFeB alloy • Plans to expand to ~3.6 ktpa in Phase II and ~5.6 ktpa Phase III • Developing Dy and Tb metallization capabilities • American Metal Plant: Planned initial production capacity of ~2.0 ktpa of alloy, with ability to expand to ~4.0 ktpa • Location to be determined; to be followed by two-year construction period • Dubbo Project: Construction-ready, with all major permits received and long mine life3 Acquisition Rationale Accelerates ambition to become leading mine-to-magnet producer Leading technical capabilities in metal making and alloying Significant value creation via enhanced vertical integration and margin capture Western supply with reduced geopolitical uncertainty Ability to deliver diversified and resilient supply chain

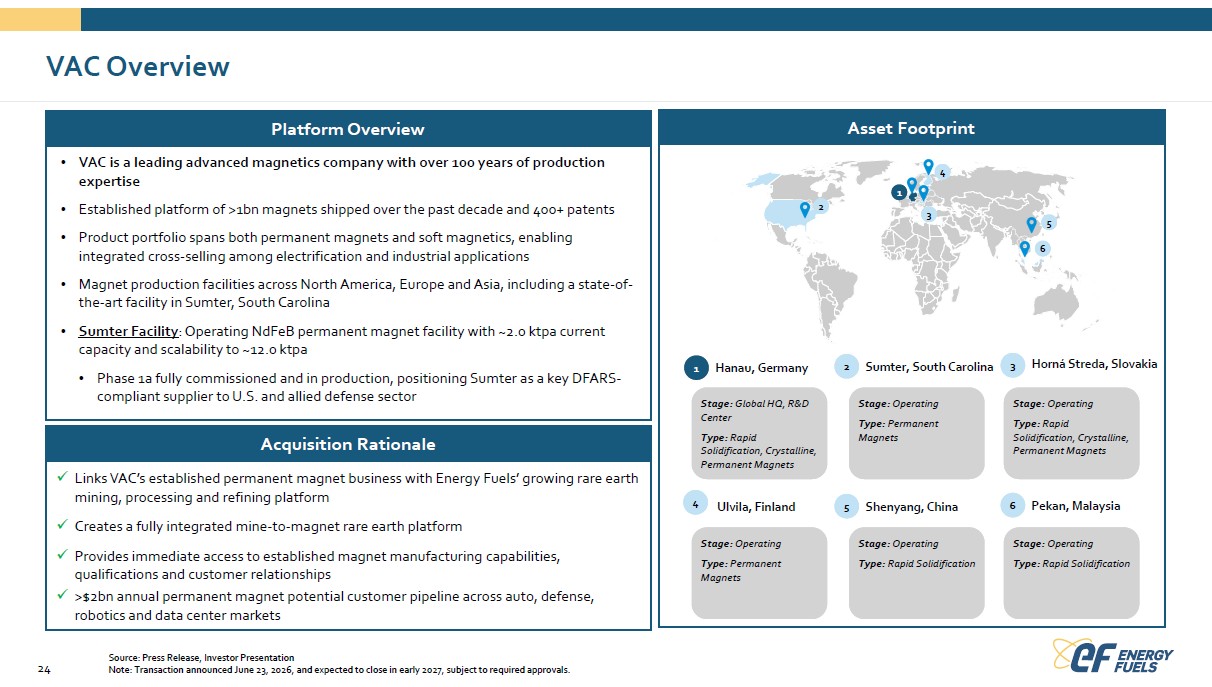

VAC Overview VAC Overview Asset Footprint • VAC is a leading advanced magnetics company with over 100 years of production expertise • Established platform of >1bn magnets shipped over the past decade and 400+ patents

• Product portfolio spans both permanent magnets and soft magnetics, enabling integrated cross-selling among electrification and industrial applications • Magnet production facilities across North America, Europe and Asia, including a state-of-the-art facility in Sumter, South Carolina • Sumter Facility: Operating NdFeB permanent magnet facility with ~2.0 ktpa current capacity and scalability to ~12.0 ktpa • Phase 1a fully commissioned and in production, positioning Sumter as a key DFARS-compliant supplier to U.S. and allied defense sector Acquisition Rationale Links VAC’s established permanent magnet business with Energy Fuels’ growing rare earth mining, processing and refining platform Creates a fully integrated mine-to-magnet rare earth platform Provides immediate access to established magnet manufacturing capabilities, qualifications and customer relationships >$2bn annual permanent magnet potential customer pipeline across auto, defense, robotics and data center markets

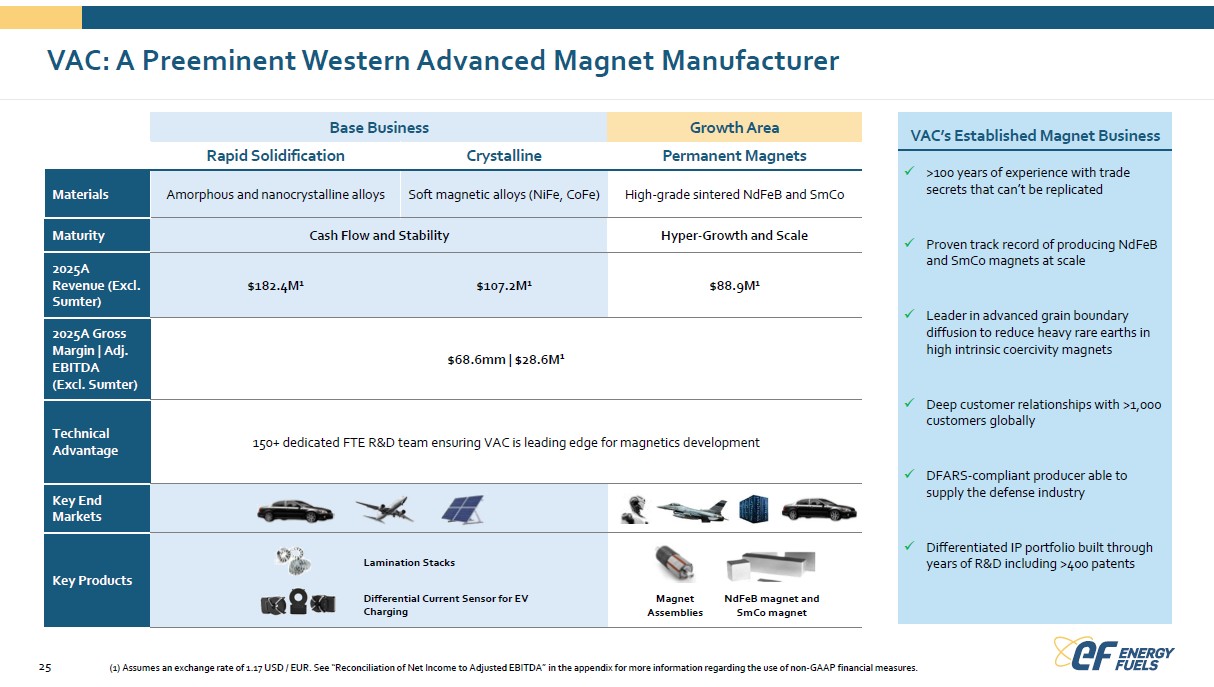

VAC: A Preeminent Western Advanced Magnet Manufacturer Base Business Growth Area VAC’s Established Magnet Business >10>1000 yearyears os off exper experiienence ce wwiith th trtrade ade secrets secrets that that can’t be replicatedcan’t be replicated Proven Proven ttrrack record ack record of of producing NdFeB producing NdFeB and SmCo and SmCo magnets magnets at at scalescale Leader Leader in advanced in advanced grain boundary grain boundary diffusion tdiffusion too reduce reduce hheeavyavy rare rare eartearthhss in in high intrinsic high intrinsic coercivity magnetscoercivity magnets Deep custDeep customer omer relatrelatiionshonships ips witwithh > >11,000 ,000 customers globallycustomers globally DFARS-compliant DFARS-compliant producer able to producer able to supply the defense supply the defense industryindustry DifferDiffereennttiated IP poiated IP porrttfofoliolio built thrbuilt throough ugh years of R&D years of R&D including including >400 >400 patentspatents (1) Assumes an exchange rate of 1.17 USD / EUR. See “Reconciliation of Net Income to Adjusted EBITDA” in the appendix for more information regarding the use of non-GAAP financial measures.

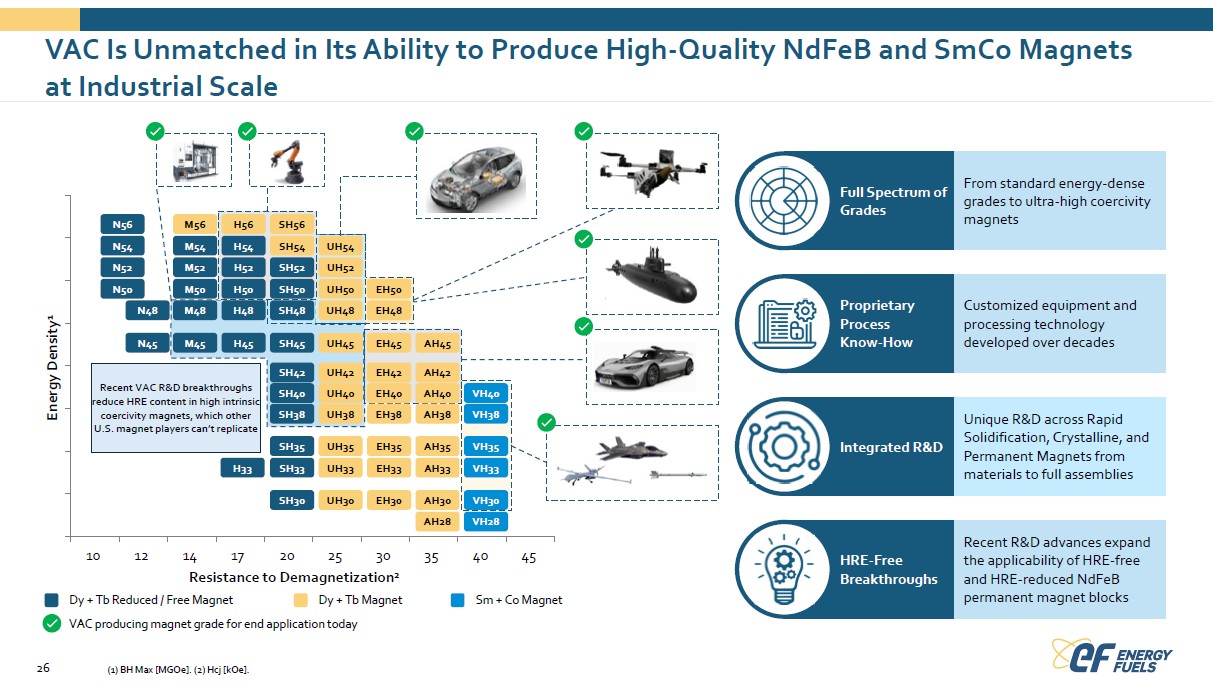

VAC Is Unmatched in Its Ability to Produce High-Quality NdFeB and SmCo Magnets at Industrial Scale Full Spectrum of Grades From standard energy-dense grades to ultra-high coercivity magnets Proprietary Process Know-How Customized equipment and processing technology developed over decades Integrated R&D Unique R&D across Rapid Solidification, Crystalline, and Permanent Magnets from materials to full assemblies HRE-Free Breakthroughs Recent R&D advances expand the applicability of HRE-free and HRE-reduced NdFeB permanent magnet blocks

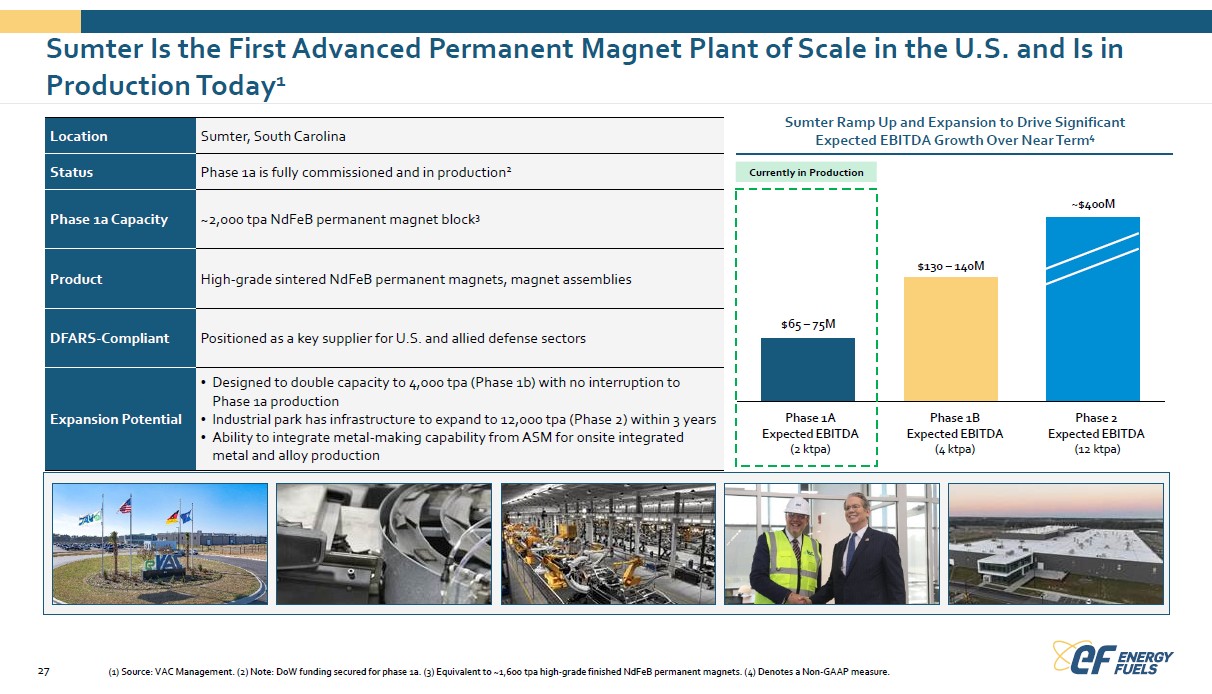

Sumter Is the First Advanced Permanent Magnet Plant of Scale in the U.S. and Is in Production Today1 Sumter Ramp Up and Expansion to Drive Significant Expected EBITDA Growth Over Near Term4 Location Sumter, South Carolina Status Phase 1a is fully commissioned and in production2 Phase 1a Capacity ~2,000 tpa NdFeB permanent magnet block3 Product High-grade sintered NdFeB permanent magnets, magnet assemblies DFARS-Compliant Positioned as a key supplier for U.S. and allied defense sectors Expansion Potential • Designed to double capacity to 4,000 tpa (Phase 1b) with no interruption to Phase 1a production • Industrial park has infrastructure to expand to 12,000 tpa (Phase 2) within 3 years • Ability to integrate metal-making capability from ASM for onsite integrated metal and alloy production

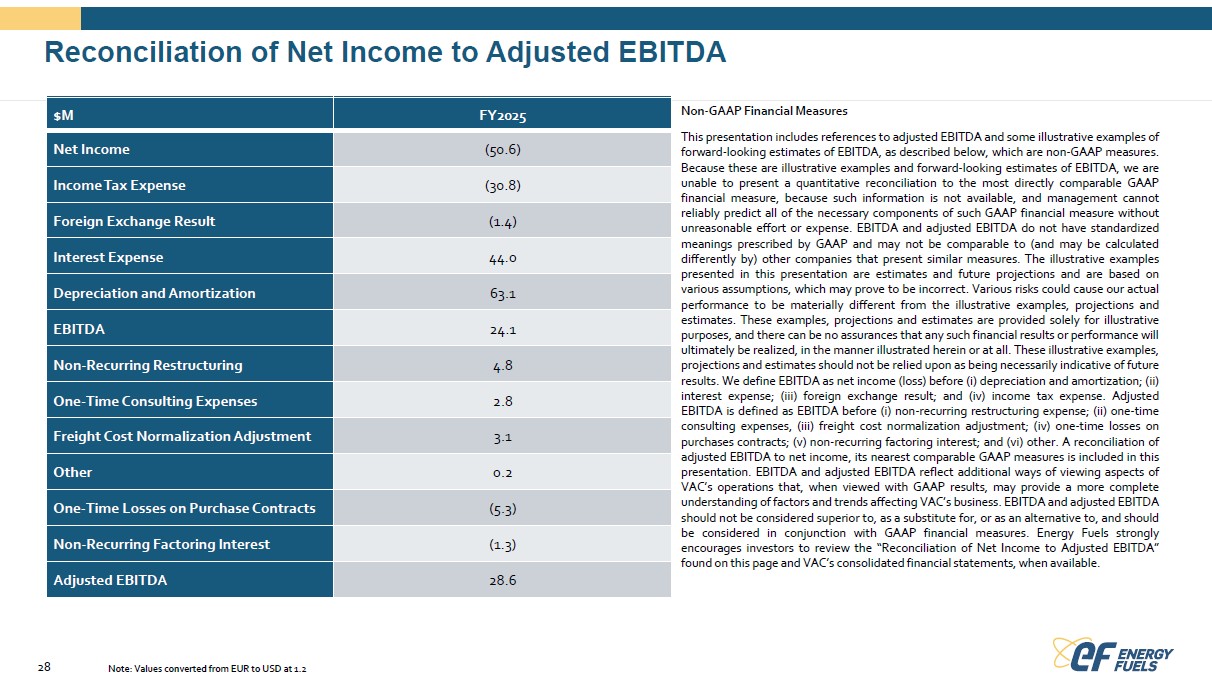

Reconciliation of Net Income to Adjusted EBITDA Non-GAAP FinancialMeasures This presentation includes references to adjusted EBITDA andsomeillustrative examples of forward-looking estimates of EBITDA, as described below, which are non-GAAP measures. Because these are illustrative examples and forward-looking estimates of EBITDA, we are unable to present a quantitative reconciliation to the most directly comparable GAAP financial measure, because such information is not available, and management cannot reliably predict all of the necessary components of such GAAP financial measure without unreasonable effort or expense. EBITDA and adjusted EBITDA do not have standardized meanings prescribed by GAAP and may not be comparable to (and may be calculated differently by) other companies that present similar measures. The illustrative examples presented in this presentation are estimates and future projections and are based on various assumptions, which may prove to be incorrect. Various risks could cause our actual performance to be materially different from the illustrative examples, projections and estimates. These examples, projections and estimates are provided solely for illustrative purposes,and therecan be no assurances that any suchfinancial results orperformance will ultimately be realized, inthe manner illustratedherein oratall. These illustrative examples, projectionsand estimatesshould not be relied upon as beingnecessarily indicative of future results. We defineEBITDAas net income(loss)before (i) depreciation and amortization; (ii) interest expense; (iii) foreign exchange result; and (iv) income tax expense. Adjusted EBITDA is defined as EBITDA before (i) non-recurring restructuring expense; (ii) one-time consulting expenses, (iii) freight cost normalization adjustment; (iv) one-time losses on purchases contracts; (v) non-recurring factoring interest; and (vi) other. A reconciliation of adjusted EBITDA to net income, its nearest comparable GAAP measures is included in this presentation. EBITDA and adjusted EBITDA reflect additional ways of viewing aspects of VAC’s operations that, when viewed with GAAP results, may provide a more complete understandingoffactors andtrendsaffectingVAC’s business.EBITDAand adjusted EBITDA should not beconsidered superior to, asasubstitute for, orasanalternative to, and should be considered in conjunction with GAAP financial measures. Energy Fuels strongly encourages investors to review the “Reconciliation of Net Income to Adjusted EBITDA” foundonthispage and VAC’sconsolidated financial statements,whenavailable.

Energy Fuels Inc. 225 Union Blvd., Suite 600 Lakewood, Colorado 80228 303.974.2140 investorinfo@energyfuels.com NYSE American TSX EFR UUUU Titanium Zirconium Uranium Rare Earths Vanadium Medical Isotopes Recycling Metallization & Alloying Permanent Magnets