Exhibit (H)(26)

WISDOMTREE RULES-BASED

METHODOLOGY

U.S. High Yield Corporate

Bond Index Family

| |

Last Updated June 26, 2026 |

WisdomTree U.S. High Yield Corporate Bond Index Family

Overview of Core Index Methodology

Each index is designed to

capture the performance of selected issuers in the U.S. non-investment-grade corporate bond market with favorable fundamental and income

characteristics. Each index employs a multi-step process, which screens on fundamentals to identify bonds with favorable characteristics

and then tilts to those individual securities which offer favorable income characteristics (screen for favorable bonds and tilt towards

income). The goal is to improve the risk-adjusted performance of traditional market-cap approaches for high-yield corporate bond indices.

Each index utilizes a screen

and tilt approach to isolate bonds that have favorable fundamentals and tilts to those bonds with favorable income and valuation characteristics.

Each index defines the universe, scores the individual issues across a fundamental metric distinguishing cash flow characteristics (i.e.,

free cash flow) and momentum metrics based on relative equity market performance of issuers. Fundamentals are the principal driver for

inclusion or exclusion for credits within the index, with very strong and very weak equity return momentum scores offering a potential

adjustment to the long-term fundamental signal.

An income tilt score with

adjustments accounting for the probability of default and recovery values is then applied to the market capitalization of each remaining

security. The income tilt score incorporates the incremental income offered over Treasuries with similar maturities within the context

of the credit risk they entail. The income tilt scores are translated into a multiplier, which is applied to the market cap percentile

ranking to determine the issue weight within each index. As a final step, both issuer and issue exposure are capped as described in the

index methodology rules. The index is rebalanced every six months with bonds removed monthly due to ratings changes, if any.

Relevant Indices in the Family

| · | WisdomTree

U.S. High Yield Corporate Bond Index |

| · | WisdomTree

U.S. Short-term High Yield Corporate Bond Index |

| · | WisdomTree

U.S. High Yield Corporate Bond, Zero Duration Index |

Index Methodology

Each index is comprised of corporate bonds of public

issuers domiciled in the United States. All eligible bonds are denominated in U.S. dollars.

1.1 Liquidity

For the WisdomTree U.S. High Yield Corporate

Bond Index, each issue must have at least $500 million in par amount outstanding.

For the WisdomTree U.S. Short-term High Yield

Corporate Bond Index, each issue must have at least $350 million in par amount outstanding.

Each issue must have a remaining maturity of at least

one year, or equivalent of 365.25 days.

1.2 Rating

Each issue must be rated high-yield

(below BBB- or Baa3) by Standard & Poor’s or Moody’s to be eligible for the index. For selection purposes, the final

rating is determined by the lower rating from the rating agencies. Defaulted Bonds are not eligible for inclusion in the index.

Additionally, issues in a distressed state (rated

C or below by Standard & Poor’s or Moody’s; or at rebalance, the issue has an option-adjusted spread (OAS) that exceeds

the higher of 300% of the average OAS of the high yield corporate universe or an absolute OAS level of 1000 basis points) are excluded.

1.3 Maturity

For the WisdomTree U.S. High Yield Corporate Bond

Index and the WisdomTree U.S. High Yield Corporate Zero Duration Index, each underlying issue must have at least one year to maturity

at the time of rebalance.

For the WisdomTree U.S. Short-term High Yield

Corporate Bond Index, each issue must have at least one year to maturity and at most five years to maturity at the time of rebalance.

1.4 Sector

Each issue is classified into one of five sectors:

Industrial, Financial, Utility, Consumer, or Energy. Government, quasi-government, foreign agencies, or supra-national issuers are excluded.

1.5 Regulation S

Bonds issued under Regulation S

are excluded.

In the case that an issue no longer meets the ratings

criteria defined above (rise to investment grade, fall into distress or default), the issue(s) would be removed at month-end after the

ratings/default event is announced. With the removal, the weight of the remaining index constituents will be adjusted accordingly on

a pro-rata basis.

Free Cash Flow

Five-year annual average of Free Cash Flow, or such lesser

period based on available data.

Short-term Momentum Score

The percentage rank of the average of 1-month, 3-month,

and 6-month equity returns of an issue’s parent company across the public issuers of the universe.

Long-term Momentum Score

The percentage rank of the 12-month equity returns of

an issue’s parent company across the public issuers of the universe.

| 4. | Fundamental Cut with Potential Adjustments for Extreme Momentum |

All issues with a non-positive factor (i.e.,

non-positive free cash flow) are isolated for potential exclusion. Very strong and very weak momentum signals calculated from parent

company stock returns can be used to enhance the fundamental signal. Issues of issuers with a positive fundamental factor, but very weak

momentum scores are excluded. Issues of issuers with a very strong momentum score but negative fundamental score are included.

The issues with no factor data (i.e., no free

cash flow) available are excluded.

For each issue, two momentum scores (a short-term

and long-term score) for equity returns are calculated and issues are ranked within the universe. The momentum scores will then be

considered together with a bond’s fundamental metric scores to enhance the selection process.

Momentum can be classified as neutral, positive.

or negative. Short-term momentum scores in the top 10% create a positive momentum classification. This classification will be retained

in subsequent rebalances as long as the long-term momentum ranking for the issuer does not fall below the Top 30%. Should this occur,

the momentum classification returns to neutral. Conversely, a short-term momentum ranking in the bottom 10% of all public issuers in

the high yield corporate debt universe will produce a negative momentum classification. This classification will be retained in subsequent

rebalances if long-term momentum does not rise above the bottom 30%. Should this occur, the momentum classification returns to neutral.

Momentum

Classification from

Previous Rebalance |

Looks

to… |

Momentum… |

| NEUTRAL |

Short-Term Momentum Rank (STMR) |

Turns POSITIVE,

if STMR is in the Top 10% Turns NEGATIVE if STMR is in the Bottom 10% |

| POSITIVE |

Long-term Momentum

Rank (LTMR) |

Remains

POSITIVE if LTMR is in the Top 30% Returns to NEUTRAL, if LTMR falls below Top 30% |

| NEGATIVE |

Long-term Momentum Rank (LTMR) |

Remains NEGATIVE if LTMR is in

the Bottom 30% Returns to NEUTRAL if LTMR rises above 30% |

A large majority of the issues will be designated

as NEUTRAL momentum and their inclusion in or exclusion from the index will be driven by the fundamental score. For the subset of bonds

with POSITIVE or NEGATIVE momentum, this factor is considered with the fundamental score in the following manner:

| · | A

bond issued by a company meeting the fundamental criteria, but showcasing significant negative

momentum would be excluded from the Index and |

| · | bonds

falling short of the fundamental criteria but showcasing POSITIVE momentum scores would be

included in the Index. |

Newly issued debt of existing issuers will reference

the issuers’ existing momentum classification when they are considered for inclusion during the next rebalance. Debt issued by

companies who are new to the high yield public universe will carry a momentum classification of NEUTRAL for the next rebalance.

A liquidity score is assigned to each issue, calculated

by:

liquidity = 0.5 * ln(amount outstanding)

− ln (age of issuance),

where amount outstanding is determined at index

reconstitution, and the age of issuance (in years) is calculated by the number of calendar days between the index reconstitution date

and the issuance date, divided by 365.25.

Issues that fall below the bottom 5% of the liquidity

scores within their respective sectors, and issues with no liquidity scores are removed from the index.

The reference constituents are defined

as all remaining bonds after the fundamental cut and the liquidity cut that are applied.

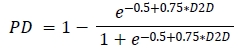

| 7. | Distance-to-Default (D2D) and Probability of Default (PD) Measure |

D2D is obtained using Merton’s formula. Denote

𝜎𝐸 as the annualized

volatility of trailing 1-year daily equity price changes, the firm’s asset volatility σ

is given by:

The distance to default of a firm is calculated as:

where Default

Barrier = Short Term Debt + 0.5 ∗ Long Term Debt and 𝑅𝐸

refers to the equity return. Correspondingly, each index uses a PD measure given by a transformation of the D2D:

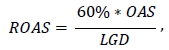

| 8. | Income Tilt and Amount Outstanding Adjustment |

For each issue an income tilt score is obtained

by its ROAS(1-PD), which is then ranked (in descending order) within each sector. The ROAS (in bp) is recovery-adjusted OAS calculated

by:

where LGD (loss given default) is determined using the

following look up table

| Senior

Unsecured |

60% |

| Senior

Subordinate |

70% |

| Subordinate |

70% |

| Junior |

75% |

| Junior

Subordinate |

80% |

The amount outstanding of each issue is adjusted

by 2𝛼 (a constant between 0 and 2), where 𝛼

is the percentage rank of the issue’s income tilt score within its sector. For an issue with the top tilt score within its

sector, its weight in the index would be doubled; for an issue with the worst tilt score within its sector, its weight in the index would

be set to 0.

Issues with no income tilt score are excluded from each

index.

If the tilting process results in a position change

of 5 basis points of less for a particular issue from the previous rebalance, the positions from the last rebalance are maintained.

For the WisdomTree U.S. High Yield Corporate

Bond Index and the WisdomTree U.S. High Yield Corporate Zero Duration

Index, an issuer cap of 2% in total market value is applied to the index at rebalance. For the WisdomTree U.S. Short-term High

Yield Corporate Bond Index, an issuer cap of 3% in total market value is applied to the index at rebalance. Issues with the same

ultimate parent ticker are aggregated under the same issuer. Individual issues are capped at 0.50% at the time of rebalance.

Excess exposures above the caps are redistributed

to the remaining bonds on a pro-rata basis. If an issuer in an index exceeds the cap, the total market value of the issues under this

issuer would be scaled down to conform with the cap at rebalance. Caps are implemented as part of the rebalance process, but weights

for both issuers and individual issues could drift higher between rebalances as driven by market conditions and corporate actions.

| 10. | Index Constitution and Rebalancing |

Each index is rebalanced semi-annually on the last business

day of May and November.

10.1 Determination of the

Reference Constituents

The reference constituents are determined seven

business days (T-7) preceding each rebalancing date, using the fundamental and momentum screen described in this methodology. Reference

constituents are confirmed for the adherence to universe selection criteria (ratings, size and whether they have been called) again before

conducting the tilting step on T-5.

10.2 Determination of Constituent

Positions and Weights

Five business days (T-5) preceding each rebalancing

date, the tilt step and the issuer and issue caps are applied to the reference constituents based on the most current pricing data. The

tilting process produces the constituent exposures that will be applied on the rebalance date. The exposures and initial weights are

disseminated to the public on T-3. This allows for advanced notice concerning potential exposures and weight changes in the index. This

projected universe will become the new index universe at the close of business on the rebalance date (T).

10.3 Maintenance of Eligibility

Criteria Intra-Rebalance

Except as otherwise noted here (e.g., ratings

changes), the Index may include constituents that no longer meet the Index’s eligibility criteria as described above intra-rebalance.

| 11. | Exclusion due to a Delayed or Unfiled Annual Report |

If a company filed an NT 10-K report stating that

it is not going to file the annual 10-K report within the extension period as dictated by the SEC based on reasons involving financial

or accounting aspects solely pertaining to this company, all bonds issued by this company will be excluded from the reference universe.

If such company is already in the index, its bonds will be dropped on the 3rd business day after the filing.

If a company filed an NT 10-K report and subsequently

did not file the annual 10-K report during the extension period based on reasons involving financial or accounting aspects solely pertaining

to this company, all bonds issued by this company will be excluded from the reference universe.

If such company is already in the index, its bonds

will be dropped on the 3rd business day after the end of the extension period.

If a company has been excluded from the reference

universe or the index due to the reasons listed above, it will need to file or restate its 10-K and then file the next 10-Q on time before

the next reference universe determination date to be eligible for inclusion into the reference universe.

Index Maintenance includes monitoring and implementing

the adjustments for redemptions, conversions, ratings changes, calls, exchanges or other corporate actions.

Bonds that are fully called will exit the index

at their call price. Bonds that are fully called or are subject to ratings change that would push them into distress or up into investment

grade status (during a particular month) will be removed from the index at the end of month. Additionally, bonds that are partially called

or tendered and reduced to outstanding par amount levels below $200 million will also be removed at their final price at month-end. After

these removals, the weights of the remaining components are adjusted proportionately to reflect the change in composition of the index

at month end.

Cash payments received through coupon payments during

the month are retained within the index and captured in the total return as coupon return. At month end, the cash is effectively reinvested

pro-rata across the entire index.

Debt Exchanges

Securities that are originated

under US Rule 144A with registration rights and later registered with the SEC are treated as the same security for the index. Once the

SEC registered identifier becomes available, it is used in the index.

Exchanges through Consent Solicitation

If a substantial portion of an existing bond in

the index (more than 90%) is exchanged for another bond series through a consent solicitation or similar exchange, such that it reduces

the par amount of the original bond to under $200 M, the bonds received in the exchange would replace the existing bonds in the index

at month-end but their addition would be limited to the minimum of the current position or the outstanding par amount of the new bonds

(i.e. effective tilt will be less than 1 or less). The new bonds would also need to satisfy existing index criteria to be eligible.

Mergers and Acquisitions

Any corporate action will be implemented after the

close of trading on the day prior to the ex-date of such corporate actions.

| 13. | Pricing Timing and Frequency |

Constituents within the index are priced each business

day using 4pm New York BID prices from the BVAL pricing service of Bloomberg. Newly issued securities enter the index on the offer side.

When markets close early for holidays, prices may be taken earlier in the day. In these instances, the standard pricing time is 1pm New

York. Bond prices are not calculated on market holidays.

| 14. | Index Calculation Agent |

Bloomberg Index Services Limited serves as the index

calculation agent and monitors and calculates the daily total returns and statistics for the indices, based on the initial exposures

provided by WisdomTree prior to rebalance balance and in anticipation of changes to constituent composition at month-end due to rating

changes and bond calls.

| 15. | WisdomTree U.S. High Yield Corporate Bond Zero Duration Index |

The WisdomTree U.S. High Yield Corporate Bond,

Zero Duration Index measures the return of the WisdomTree U.S. High Yield Corporate Bond Index with its interest rate (duration)

exposure hedged to zero years using a short position in five on-the-run (OTR) US Treasury bellwether securities. The interest rate hedge

is rebalanced on a monthly basis to achieve the target duration exposure.

| 15.1 | Index Calculation Methodology |

The return of the WisdomTree U.S. High Yield

Corporate Bond, Zero Duration Index can be represented as the following:

WisdomTree U. S. High Yield

Corporate Bond, Zero Duration IndexTotal Return

Where:

WFCHYTotal Return

= published return of the WisdomTree U.S. High Yield

Corporate Bond Index, Including a price, coupon and paydown return component

WFCHYZero Duration Hedge

= the return of a portfolio of 6M, 2Y, 5Y, 10Y and

30Y OTR securities weighted to bring the duration of the WisdomTree U.S. High Yield Corporate Bond Index to zero years

Funding1MT– Bills

= the return of a basket of 1 month T –

Bills to make the total return a funded return

| 15.2 | Construction of Hedged Position |

| 1. | Bucketing of the Option Adjusted

Duration (OAD) of the WisdomTree U.S. High Yield Corporate Bond Index |

| 2. | Selection of on-the-run Treasury bellwethers for the hedge portfolio |

| 3. | Calculation of hedge portfolio weights |

| 4. | Calculation of hedge portfolio and funding returns |

Step 1: The hedge portfolio consists of OTR US

Treasury securities in four different tenors: 6m, 2y, 5y, 10y, and 30y. The first step to constructing the hedge portfolio is to sort

the underlying WisdomTree U.S. High Yield Corporate Bond Index (Statistics Universe) into five non-overlapping duration buckets, and

to identify the duration contribution to be hedged by each of these instruments in the hedge portfolio. The duration measure used is

OAD, as computed and reported by Bloomberg Barclays.

Contribution to OAD is calculated by multiplying

the market value percent of each duration bucket as of the month-end index rebalancing date by the OAD of each bucket.

Step 2: The selected securities for each monthly

rebalance match the instruments that are used for Bloomberg Barclays US Treasury Bellwether Indices. OTR instruments for the portfolio

are selected once a month on the last business day to include the most recently issued instrument for each tenor used in the hedge.

Step 3: To replicate the duration exposure from

Step 1 with the five on-the-run US Treasuries selected in Step 2, an optimization technique is employed that establishes an aggregate

duration equivalent to that of the underlying index (+/- 0.02 year) and minimizes the sum of squared differences of the contribution

to duration of the index in each bucket vs. the contribution to duration of the OTR US Treasuries.

Step 4: To calculate the return of the hedged position,

the weights assigned for each US Treasury security are multiplied by the total return of that security for the month.

10