EXHIBIT 99.2

1 Alcoa Announces Strategic Acquisition of South32’s Bauxite, Alumina, and Aluminum assets for $4.1 billion June 30, 2026, 7:00 p.m. EDT July 1, 2026, 9:00 a.m. AEST Please see the appendix of this presentation for disclaimers, additional important information, and a glossary of terms .

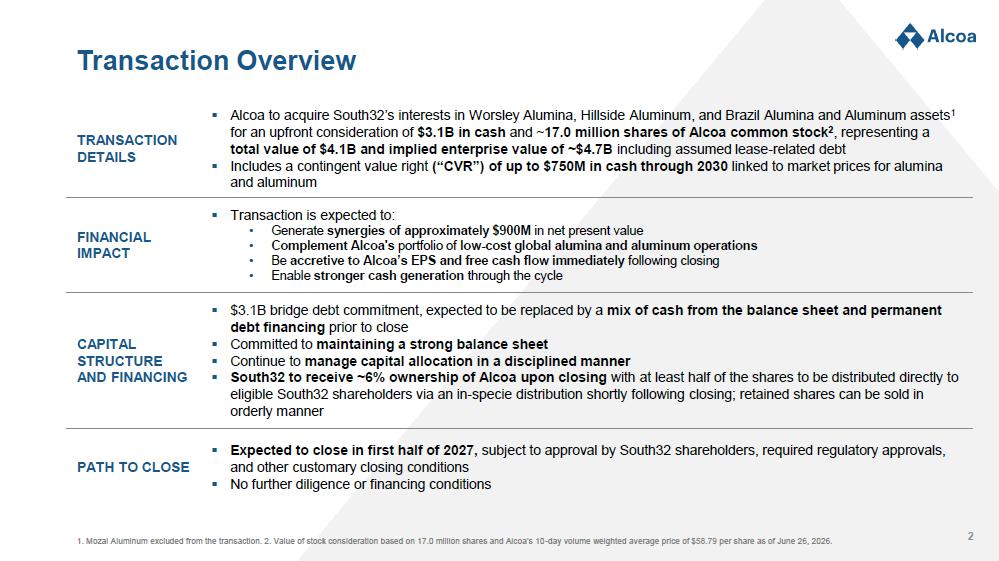

2 ▪ Alcoa to acquire South32’s interests in Worsley Alumina, Hillside Aluminum, and Brazil Alumina and Aluminum assets 1 for an upfront consideration of $3.1B in cash and ~ 17.0 million shares of Alcoa common stock 2 , representing a total value of $4.1B and implied enterprise value of ~$4.7B including assumed lease - related debt ▪ Includes a contingent value right (“CVR”) of up to $750M in cash through 2030 linked to market prices for alumina and aluminum TRANSACTION DETAILS ▪ Transaction is expected to: • Generate synergies of approximately $900M in net present value • Complement Alcoa's portfolio of low - cost global alumina and aluminum operations • Be accretive to Alcoa’s EPS and free cash flow immediately following closing • Enable stronger cash generation through the cycle FINANCIAL IMPACT ▪ $3.1B bridge debt commitment, expected to be replaced by a mix of cash from the balance sheet and permanent debt financing prior to close ▪ Committed to maintaining a strong balance sheet ▪ Continue to manage capital allocation in a disciplined manner ▪ South32 to receive ~6% ownership of Alcoa upon closing with at least half of the shares to be distributed directly to eligible South32 shareholders via an in - specie distribution shortly following closing; retained shares can be sold in orderly manner CAPITAL STRUCTURE AND FINANCING ▪ Expected to close in first half of 2027, subject to approval by South32 shareholders, required regulatory approvals, and other customary closing conditions ▪ No further diligence or financing conditions PATH TO CLOSE Transaction Overview 1. Mozal Aluminum excluded from the transaction. 2. Value of stock consideration based on 17.0 million shares and Alcoa’s 10 - day volume weighted average price of $58.79 per share as of June 26, 2026.

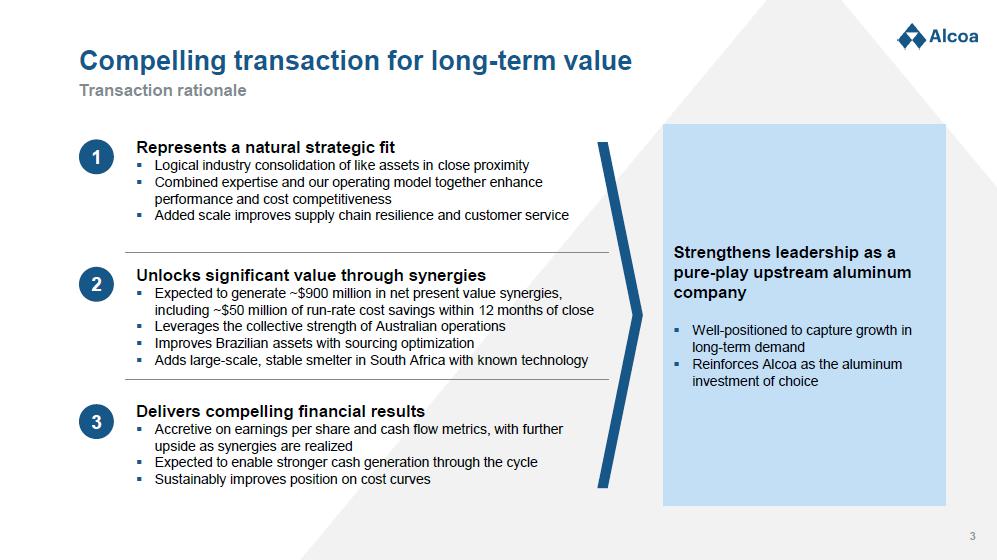

3 Compelling transaction for long - term value Transaction rationale Represents a natural strategic fit ▪ Logical industry consolidation of like assets in close proximity ▪ Combined expertise and our operating model together enhance performance and cost competitiveness ▪ Added scale improves supply chain resilience and customer service Unlocks significant value through synergies ▪ Expected to generate ~$900 million in net present value synergies, including ~$50 million of run - rate cost savings within 12 months of close ▪ Leverages the collective strength of Australian operations ▪ Improves Brazilian assets with sourcing optimization ▪ Adds large - scale, stable smelter in South Africa with known technology Delivers compelling financial results ▪ Accretive on earnings per share and cash flow metrics, with further upside as synergies are realized ▪ Expected to enable stronger cash generation through the cycle ▪ Sustainably improves position on cost curves 1 2 3 Strengthens leadership as a pure - play upstream aluminum company ▪ Well - positioned to capture growth in long - term demand ▪ Reinforces Alcoa as the aluminum investment of choice

4 1 Closed Bayside smelter in South Africa to join the Alcoa Transformation portfolio Acquired assets are complementary to Alcoa’s operations Logical industry consolidation of like assets Canada: Bauxite Brazil Acquiring interest in Alumar assets already operated by Alcoa and interest in MRN Hillside Large - scale, stable smelter with AP30 technology Worsley & Boddington Assets adjacent to Alcoa's existing WA refining system Alumina Aluminum Pro Forma Global Footprint 1 United States: Spain: Guinea: Brazil: Norway: Iceland: Australia: Asset interests being acquired 1 South Africa: Alcoa mines Boddington mine Kwinana Port Pinjarra Refinery Wagerup Refinery Worsley Refinery Bunbury Port Perth

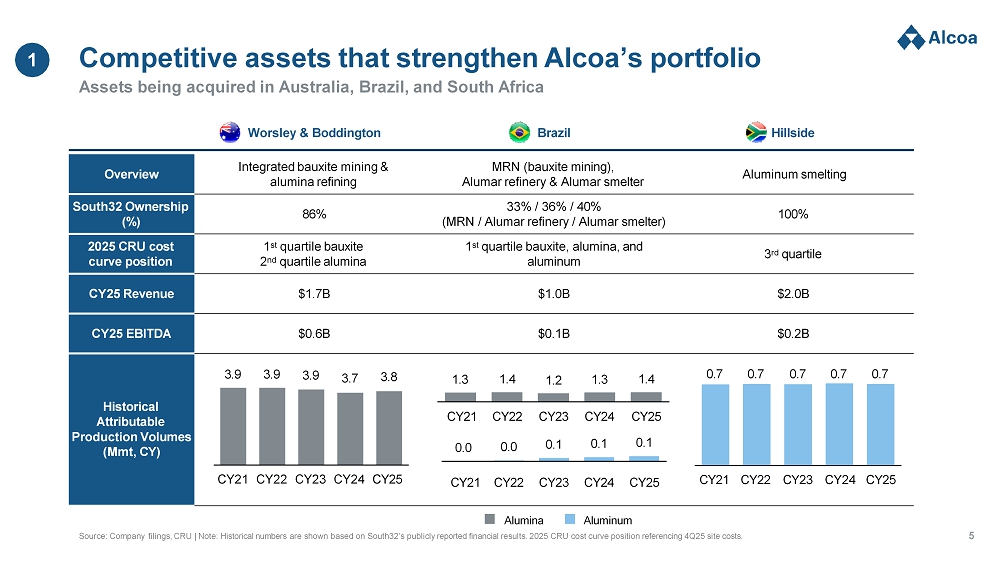

5 Competitive assets that strengthen Alcoa’s portfolio Assets being acquired in Australia, Brazil, and South Africa Alumina Aluminum Source: Company filings, CRU | Note: Historical numbers are shown based on South32’s publicly reported financial results. 2025 CRU cost curve position referencing 4Q25 site costs. Hillside Brazil Worsley & Boddington Aluminum smelting MRN (bauxite mining), Alumar refinery & Alumar smelter Integrated bauxite mining & alumina refining Overview 100% 33% / 36% / 40% (MRN / Alumar refinery / Alumar smelter) 86% South32 Ownership (%) 3 rd quartile 1 st quartile bauxite, alumina, and aluminum 1 st quartile bauxite 2 nd quartile alumina 2025 CRU cost curve position $2.0B $1.0B $1.7B CY25 Revenue $0.2B $0.1B $0.6B CY25 EBITDA 0.7 0.7 0.7 0.7 0.7 1.4 1.3 1.2 1.4 1.3 3.9 3.9 3.9 3.7 3.8 CY25 CY24 CY23 CY22 CY21 Historical Attributable 0.1 0.1 0.1 0.0 0.0 Production Volumes (Mmt, CY) CY24 CY25 CY23 CY22 CY21 CY25 CY24 CY23 CY22 CY21 CY21 CY22 CY23 CY24 CY25 1

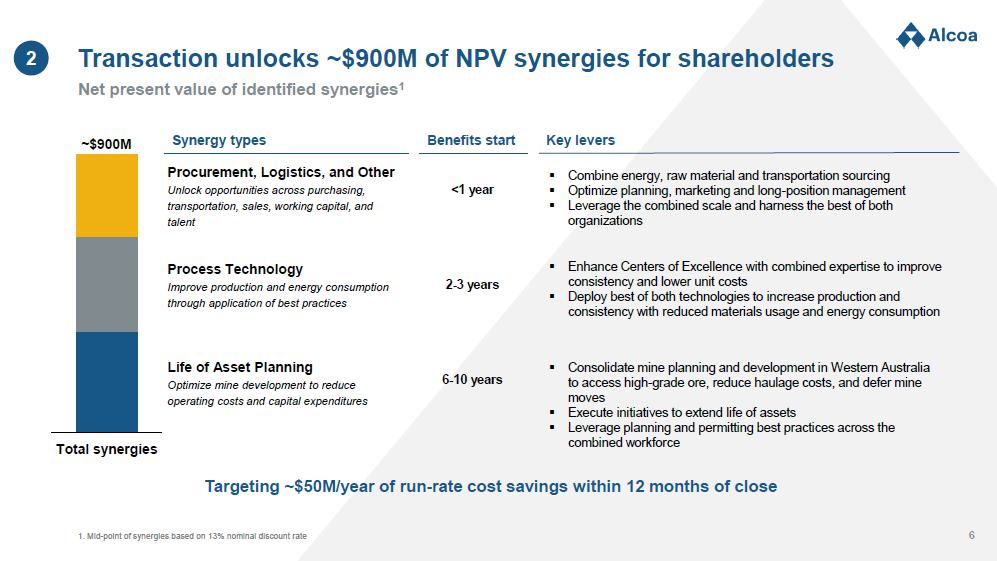

6 Benefits start 1. Mid - point of synergies based on 13% nominal discount rate Transaction unlocks ~$900M of NPV synergies for shareholders Net present value of identified synergies 1 ~$900M Total synergies Life of Asset Planning Optimize mine development to reduce operating costs and capital expenditures Process Technology Improve production and energy consumption through application of best practices Procurement, Logistics, and Other Unlock opportunities across purchasing, transportation, sales, working capital, and talent Synergy types Targeting ~$50M/year of run - rate cost savings within 12 months of close Key levers ▪ Combine energy, raw material and transportation sourcing ▪ Optimize planning, marketing and long - position management ▪ Leverage the combined scale and harness the best of both organizations ▪ Enhance Centers of Excellence with combined expertise to improve consistency and lower unit costs ▪ Deploy best of both technologies to increase production and consistency with reduced materials usage and energy consumption ▪ Consolidate mine planning and development in Western Australia to access high - grade ore, reduce haulage costs, and defer mine moves ▪ Execute initiatives to extend life of assets ▪ Leverage planning and permitting best practices across the combined workforce 2 <1 year 2 - 3 years 6 - 10 years

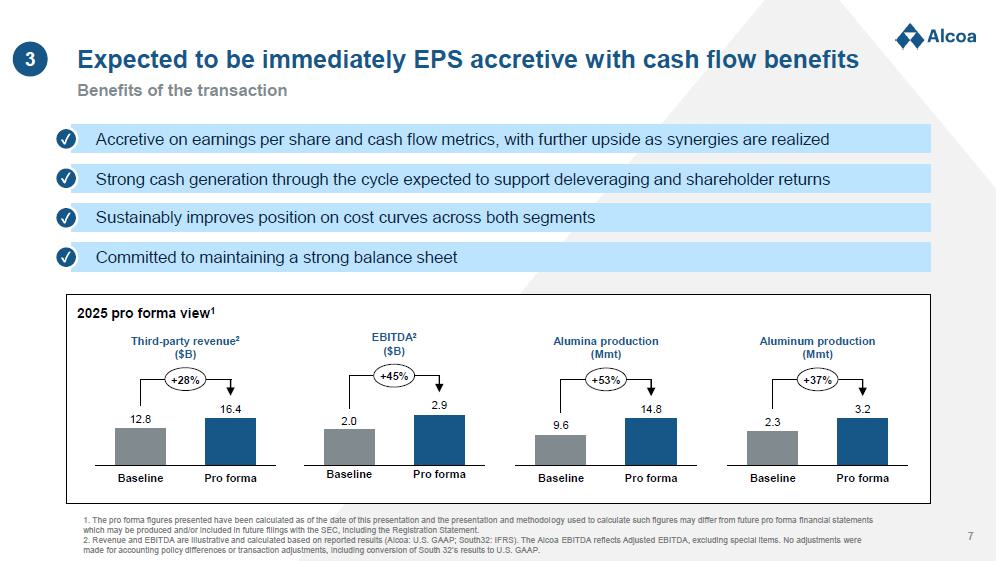

7 Accretive on earnings per share and cash flow metrics, with further upside as synergies are realized 1. The pro forma figures presented have been calculated as of the date of this presentation and the presentation and methodol ogy used to calculate such figures may differ from future pro forma financial statements which may be produced and/or included in future filings with the SEC, including the Registration Statement. 2. Revenue and EBITDA are illustrative and calculated based on reported results (Alcoa: U.S. GAAP; South32: IFRS). The Alcoa EBITDA reflects Adjusted EBITDA, excluding special items. No adjustments were made for accounting policy differences or transaction adjustments, including conversion of South 32’s results to U.S. GAAP. Expected to be immediately EPS accretive with cash flow benefits Benefits of the transaction Alumina production (Mmt) Aluminum production (Mmt) EBITDA 2 ($B) 2.9 +45% Baseline Pro forma 2025 pro forma view 1 Third - party revenue 2 ($B) 12.8 2.0 16.4 +28% Baseline Pro forma 9.6 14.8 +53% Baseline Pro forma 2.3 3.2 +37% Baseline Pro forma 3 Strong cash generation through the cycle expected to support deleveraging and shareholder returns Sustainably improves position on cost curves across both segments Committed to maintaining a strong balance sheet Accretive on earnings per share and cash flow metrics, with further upside as synergies are realized Strong cash generation through the cycle expected to support deleveraging and shareholder returns Sustainably improves position on cost curves across both segments Committed to maintaining a strong balance sheet

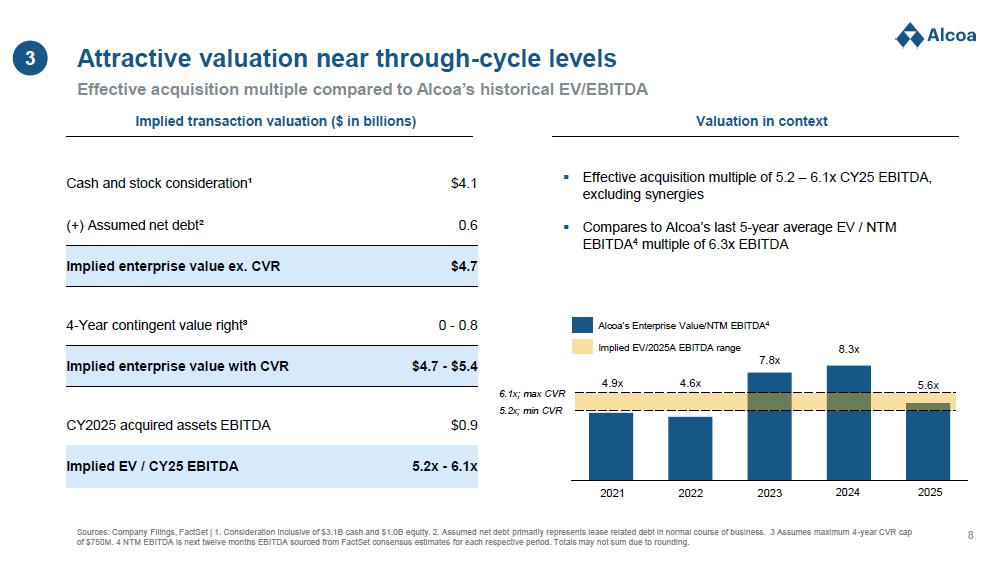

8 Attractive valuation near through - cycle levels Sources: Company Filings, FactSet | 1. Consideration inclusive of $3.1B cash and $1.0B equity. 2. Assumed net debt primarily represents lease related debt in normal course of business. 3 Assumes maximum 4 - year CVR cap of $750M. 4 NTM EBITDA is next twelve months EBITDA sourced from FactSet consensus estimates for each respective period. Totals may not sum due to rounding. ▪ Effective acquisition multiple of 5.2 – 6.1x CY25 EBITDA, excluding synergies ▪ Compares to Alcoa’s last 5 - year average EV / NTM EBITDA 4 multiple of 6.3x EBITDA Effective acquisition multiple compared to Alcoa’s historical EV/EBITDA Implied transaction valuation ($ in billions) 4.9x 4.6x 7.8x 8.3x 5.6x Alcoa’s Enterprise Value/NTM EBITDA 4 6.1x; max CVR 5.2x; min CVR 2023 2024 2025 2022 2021 Implied EV/2025A EBITDA range Valuation in context $4.1 Cash and stock consideration¹ 0.6 (+) Assumed net debt² $4.7 Implied enterprise value ex. CVR 0 - 0.8 4 - Year contingent value right³ $4.7 - $5.4 Implied enterprise value with CVR $0.9 CY2025 acquired assets EBITDA 5.2x - 6.1x Implied EV / CY25 EBITDA 3

9 Reinforces Alcoa as the investment of choice in aluminum Transaction rationale Represents a natural strategic fit Unlocks significant value through synergies Delivers compelling financial results 1 2 3 Strengthens leadership as a pure - play upstream aluminum company

10 Appendix

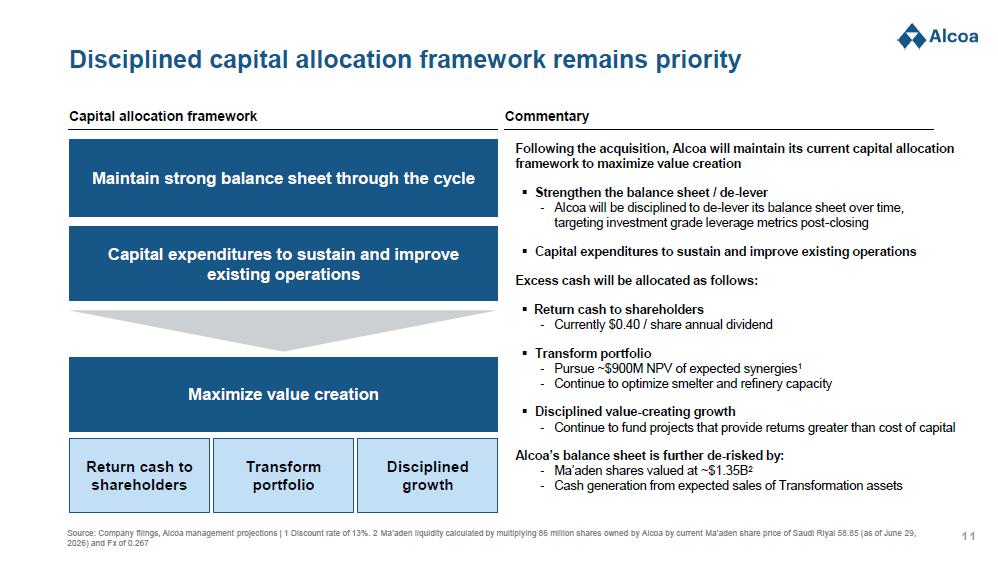

11 Disciplined capital allocation framework remains priority Source: Company filings, Alcoa management projections | 1 Discount rate of 13%. 2 Ma’aden liquidity calculated by multiplying 86 million shares owned by Alcoa by current Ma’aden share price of Saudi Riyal 58.85 (as of June 29, 2026) and Fx of 0.267 Capital allocation framework Commentary Maintain strong balance sheet through the cycle Capital expenditures to sustain and improve existing operations Maximize value creation Disciplined growth Transform portfolio Return cash to shareholders Following the acquisition, Alcoa will maintain its current capital allocation framework to maximize value creation ▪ Strengthen the balance sheet / de - lever - Alcoa will be disciplined to de - lever its balance sheet over time, targeting investment grade leverage metrics post - closing ▪ Capital expenditures to sustain and improve existing operations Excess cash will be allocated as follows: ▪ Return cash to shareholders - Currently $0.40 / share annual dividend ▪ Transform portfolio - Pursue ~$900M NPV of expected synergies 1 - Continue to optimize smelter and refinery capacity ▪ Disciplined value - creating growth - Continue to fund projects that provide returns greater than cost of capital Alcoa’s balance sheet is further de - risked by: - Ma’aden shares valued at ~$1.35B 2 - Cash generation from expected sales of Transformation assets

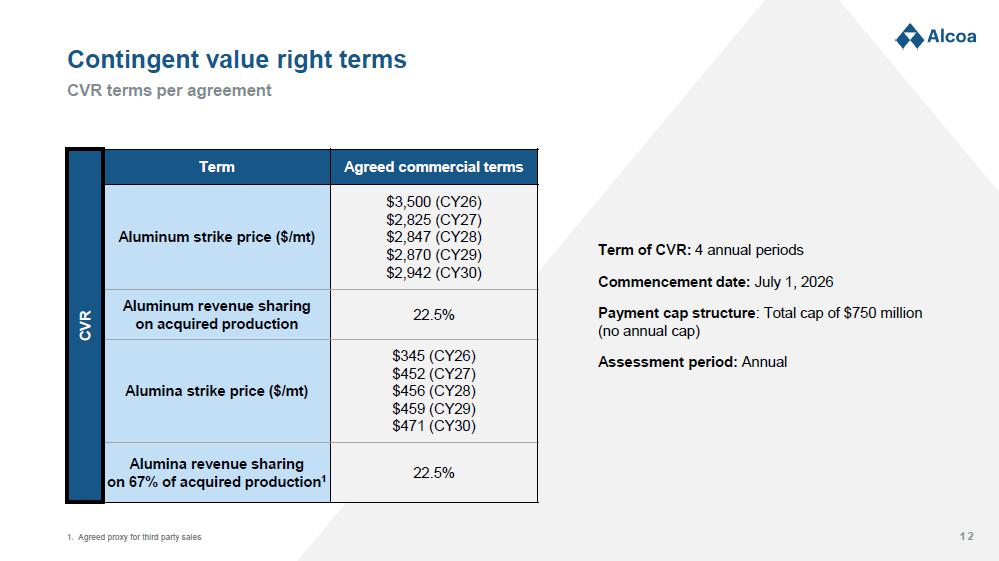

12 1. Agreed proxy for third party sales Contingent value right terms CVR terms per agreement Agreed commercial terms Term CVR $3,500 (CY26) $2,825 (CY27) $2,847 (CY28) Aluminum strike price ($/mt) $2,870 (CY29) $2,942 (CY30) 22.5% Aluminum revenue sharing on acquired production $345 (CY26) $452 (CY27) $456 (CY28) Alumina strike price ($/mt) $459 (CY29) $471 (CY30) 22.5% Alumina revenue sharing on 67% of acquired production 1 Term of CVR: 4 annual periods Commencement date: July 1, 2026 Payment cap structure : Total cap of $750 million (no annual cap) Assessment period: Annual

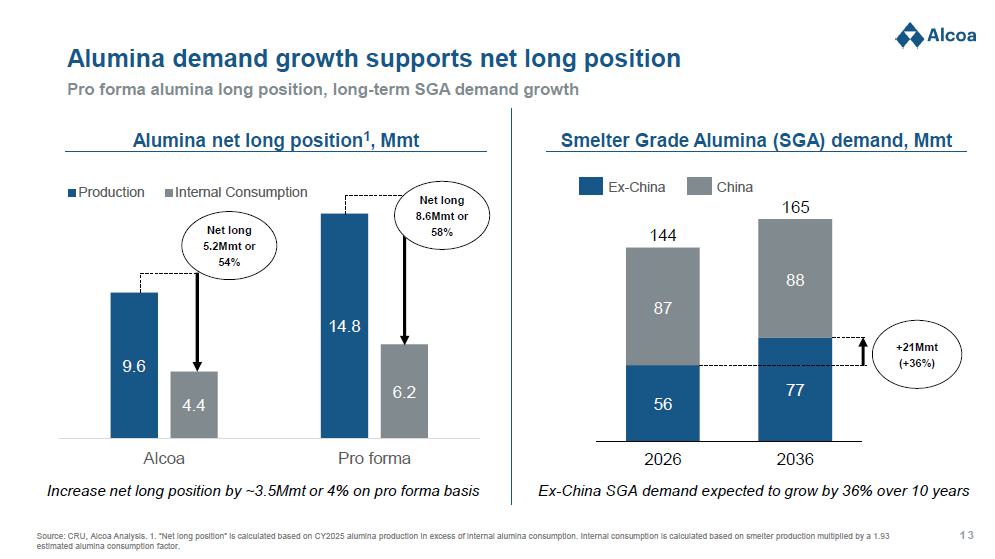

13 9.6 14.8 4.4 6.2 Alcoa Pro forma Increase net long position by ~3.5Mmt or 4% on pro forma basis Production Internal Consumption Net long 5.2Mmt or 54% Net long 8.6Mmt or 58% Alumina demand growth supports net long position Pro forma alumina long position, long - term SGA demand growth Alumina net long position 1 , Mmt Smelter Grade Alumina (SGA) demand, Mmt 56 87 2026 2036 Ex - China SGA demand expected to grow by 36% over 10 years 77 88 144 165 +21Mmt (+36%) Ex - China China Source: CRU, Alcoa Analysis. 1. “Net long position” is calculated based on CY2025 alumina production in excess of internal alumina consumption. Internal consumption is calculated based on smelter production multiplied by a 1.93 estimated alumina consumption factor.

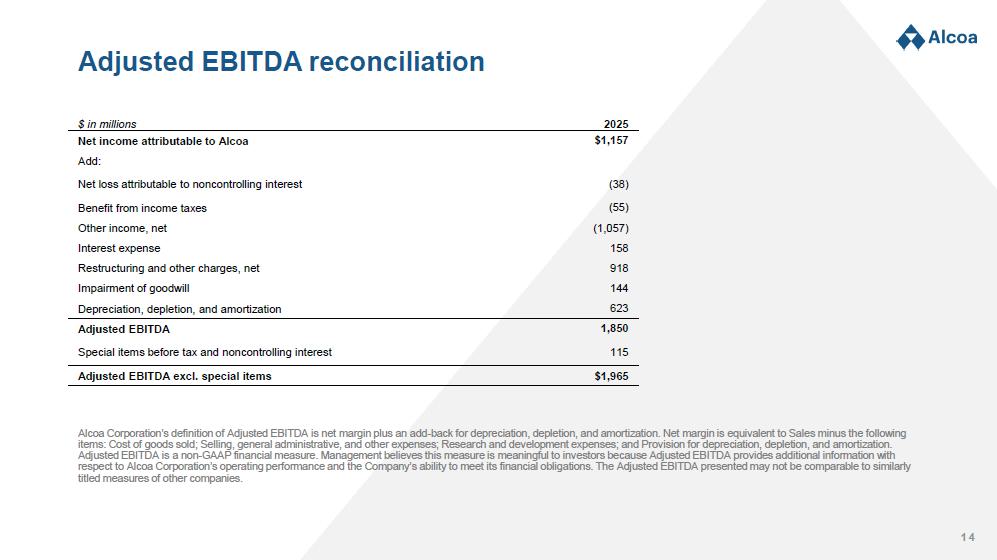

14 Adjusted EBITDA reconciliation 2025 $ in millions $1,157 Net income attributable to Alcoa Add: (38) Net loss attributable to noncontrolling interest (55) Benefit from income taxes (1,057) Other income, net 158 Interest expense 918 Restructuring and other charges, net 144 Impairment of goodwill 623 Depreciation, depletion, and amortization 1,850 Adjusted EBITDA 115 Special items before tax and noncontrolling interest $1,965 Adjusted EBITDA excl. special items Alcoa Corporation’s definition of Adjusted EBITDA is net margin plus an add - back for depreciation, depletion, and amortization. Net margin is equivalent to Sales minus the following items: Cost of goods sold; Selling, general administrative, and other expenses; Research and development expenses; and Provision for depreciation, depletion, and amortization. Adjusted EBITDA is a non - GAAP financial measure. Management believes this measure is meaningful to investors because Adjusted EBITDA provides additional information with respect to Alcoa Corporation’s operating performance and the Company’s ability to meet its financial obligations. The Adjusted EBITDA presented may not be comparable to similarly titled measures of other companies.

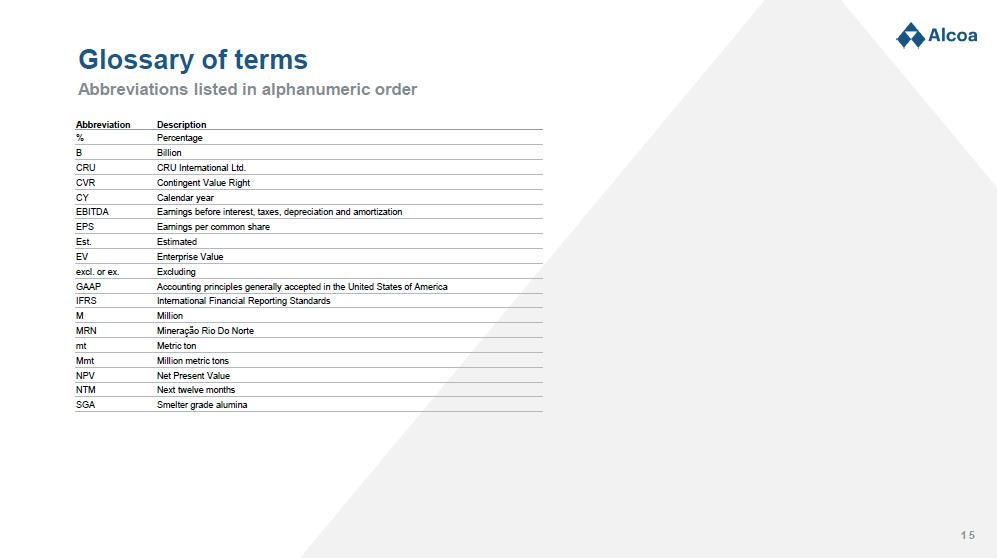

15 Glossary of terms Abbreviations listed in alphanumeric order Description Abbreviation Percentage % Billion B CRU International Ltd. CRU Contingent Value Right CVR Calendar year CY Earnings before interest, taxes, depreciation and amortization EBITDA Earnings per common share EPS Estimated Est. Enterprise Value EV Excluding excl. or ex. Accounting principles generally accepted in the United States of America GAAP International Financial Reporting Standards IFRS Million M Mineração Rio Do Norte MRN Metric ton mt Million metric tons Mmt Net Present Value NPV Next twelve months NTM Smelter grade alumina SGA

Cautionary Statement regarding Forward - Looking Statements This communication contains statements that relate to future events and expectations and as such constitute forward - looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 . Forward - looking statements include those containing such words as “aims,” “ambition,” “anticipates,” “believes,” “could,” “develop,” “endeavors,” “estimates,” “expects,” “forecasts,” “goal,” “intends,” “may,” “outlook,” “potential,” “plans,” “projects,” “reach,” “seeks,” “sees,” “should,” “strive,” “targets,” “will,” “working,” “would,” or other words of similar meaning . All statements by Alcoa Corporation (“Alcoa”) that reflect expectations, assumptions or projections about the future, other than statements of historical fact, are forward - looking statements, including, without limitation, statements regarding the proposed transaction ; the ability of the parties to complete the proposed transaction on the expected timeline or at all considering the closing conditions ; the expected benefits of the proposed transaction, including the anticipated synergies and earnings per share (“EPS”) and Free Cash Flow accretion ; the competitive ability and position following completion of the proposed transaction ; the ability to complete any proposed debt financing in connection with the proposed transaction ; forecasts concerning global demand growth for bauxite, alumina, and aluminum, and supply/demand balances ; statements, projections or forecasts of future or targeted financial results, or operating performance (including our ability to execute on strategies related to environmental, social and governance matters) ; statements about strategies, outlook, and business and financial prospects (including related to production and shipments) ; and statements about capital allocation and return of capital . These statements reflect beliefs and assumptions that are based on Alcoa’s perception of historical trends, current conditions, and expected future developments, as well as other factors that management believes are appropriate in the circumstances . Forward - looking statements are not guarantees of future performance and are subject to known and unknown risks, uncertainties, and changes in circumstances that are difficult to predict . Although Alcoa believes that the expectations reflected in any forward - looking statements are based on reasonable assumptions, it can give no assurance that these expectations will be attained and it is possible that actual results may differ materially from those indicated by these forward - looking statements due to a variety of risks and uncertainties . Such risks and uncertainties include, but are not limited to : (a) the non - satisfaction or non - waiver, on a timely basis or otherwise, of one or more closing conditions to the proposed transaction ; (b) the prohibition or delay of the consummation of the proposed transaction by a governmental entity ; (c) the risk that the proposed transaction may not be completed in the expected time frame or at all ; (d) unexpected costs, charges or expenses resulting from the proposed transaction ; (e) uncertainty of the expected financial performance following completion of the proposed transaction ; (f) uncertainty of any contingent payment required to be made in connection with the proposed transaction following completion ; (g) failure to realize the anticipated benefits of the proposed transaction ; (h) the occurrence of any event that could give rise to termination of the proposed transaction ; (i) potential litigation in connection with the proposed transaction or other settlements or investigations that may affect the timing or occurrence of the contemplated transaction or result in significant costs of defense, indemnification and liability ; (j) the impact of global economic conditions on the aluminum industry and aluminum end - use markets ; (k) volatility and declines in aluminum and alumina demand and pricing, including global, regional, and product - specific prices, or significant changes in production costs which are linked to the London Metal Exchange (LME) or other commodities ; (l) the disruption of market - driven balancing of global aluminum supply and demand by non - market forces ; (m) competitive and complex conditions in global markets ; (n) our ability to obtain, maintain, or renew permits or approvals necessary for our mining operations ; (o) rising energy costs and interruptions or uncertainty in energy supplies ; (p) unfavorable changes in the cost, quality, or availability of raw materials or other key inputs, or by disruptions in the supply chain ; (q) economic, political, and social conditions, including the impact of trade policies, tariffs, and adverse industry publicity ; (r) legal proceedings, investigations, or changes in foreign and/or U . S . federal, state, or local laws, regulations, or policies ; (s) changes in tax laws or exposure to additional tax liabilities ; (t) climate change, climate change legislation or regulations, and efforts to reduce emissions and build operational resilience to extreme weather conditions ; (u) disruptions in the global economy caused by ongoing regional conflicts and wars ; (v) fluctuations in foreign currency exchange rates and interest rates, inflation and other economic factors in the countries in which we operate ; (w) global competition within and beyond the aluminum industry ; (x) our ability to achieve our strategies or expectations relating to environmental, social, and governance considerations ; (y) claims, costs, and liabilities related to health, safety and environmental laws, regulations, and other requirements in the jurisdictions in which we operate ; (z) liabilities resulting from 16

17 Important information impoundment structures, which could impact the environment or cause exposure to hazardous substances or other damage ; (aa) dilution of the ownership position of the Company’s stockholders (including as a result of the proposed transaction), price volatility, and other impacts on the price of Alcoa common stock by the secondary listing of the Alcoa common stock on the Australian Securities Exchange ; (bb) our ability to obtain or maintain adequate insurance coverage ; (cc) our ability to execute on our strategy to reduce complexity and optimize our asset portfolio and to realize the anticipated benefits from announced plans, programs, initiatives relating to our portfolio, capital investments, and developing technologies ; (dd) our ability to integrate and achieve intended results from joint ventures, other strategic alliances, and strategic business transactions ; (ee) significant declines in the market value of our marketable securities ; (ff) our ability to fund capital expenditures ; (gg) deterioration in our credit profile or increases in interest rates ; (hh) impacts on our current and future operations due to our indebtedness and our ability to reduce indebtedness ; (ii) our ability to continue to return capital to our stockholders through the payment of cash dividends and/or the repurchase of our common stock ; (jj) cyber attacks, security breaches, system failures, software or application vulnerabilities, or other cyber incidents ; (kk) labor market conditions, union disputes and other employee relations issues ; and (ll) the other risk factors discussed in Alcoa’s Annual Report on Form 10 - K for the fiscal year ended December 31 , 2025 and other reports filed by Alcoa with the SEC . Certain illustrative pro forma information included herein may differ materially from pro forma information included in the SEC filings, including the Registration Statement (as defined below) . Alcoa cautions readers not to place undue reliance upon any such forward - looking statements, which speak only as of the date they are made . These risks, as well as other risks associated with the proposed transaction, will be more fully discussed in the Registration Statement . Alcoa disclaims any obligation to update publicly any forward - looking statements, whether in response to new information, future events or otherwise, except as required by applicable law . Neither Alcoa nor any other person assumes responsibility for the accuracy and completeness of any of these forward - looking statements . No Offer or Solicitation This communication is for informational purposes and is not intended to, and shall not, constitute an offer to sell or the solicitation of an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote of approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction . Additional Information and Where to Find It This communication relates to the proposed transaction . In connection with the proposed transaction, Alcoa plans to file with the SEC relevant materials, including a registration statement on Form S - 4 that will include a prospectus of Alcoa (including documents incorporated by reference therein, the “Registration Statement”) . This communication is not a substitute for the Registration Statement or any other document that Alcoa may file with the SEC in connection with the proposed transaction . Before making any investment decision, Alcoa’s investors and shareholders are urged to read the Registration Statement and all relevant documents filed or to be filed with the SEC, as well as any amendments or supplements to those documents, when they become available, because they will contain important information about Alcoa and the proposed transaction . Alcoa’s investors and shareholders will be able to obtain a free copy of the Registration Statement, as well as other filings containing information about Alcoa, free of charge, at the SEC’s website (www.sec.gov). Copies of the Registration Statement and other documents filed by Alcoa with the SEC may be obtained, without charge, by contacting Alcoa through its website at https://investors.alcoa.com/.

18 Important information Unless otherwise specified, all dollar amounts are in United States Dollar ( $ USD) . Non - GAAP Financial Measures This presentation contains reference to certain financial measures that are not calculated and presented in accordance with generally accepted accounting principles in the United States (GAAP) . Alcoa Corporation believes that the presentation of these non - GAAP financial measures is useful to investors because such measures provide both additional information about the operating performance of Alcoa Corporation and insight on the ability of Alcoa Corporation to meet its financial obligations by adjusting the most directly comparable GAAP financial measure for the impact of, among others, “special items” as defined by the Company, non - cash items in nature, and/or nonoperating expense or income items . The presentation of non - GAAP financial measures is not intended to be a substitute for, and should not be considered in isolation from, the financial measures reported in accordance with GAAP . Certain definitions, reconciliations to the most directly comparable GAAP financial measures and additional details regarding management’s rationale for the use of the non - GAAP financial measures can be found in the appendix to this presentation . Alcoa Corporation does not provide reconciliations of the forward - looking non - GAAP financial measure NTM EBITDA as such amounts are based on Factset consensus estimates for the applicable periods and as such it is impractical to provide such reconciliations . See South 32 ’s publicly reported financial results for a discussion on South 32 ’s EBITDA definition . A reconciliation of South 32 ’s CY 2025 EBITDA to the most comparable International Financial Reporting Standards financial measure is not provided, as South 32 ’s publicly reported financial results reconcile this information at the group level . Resources This presentation can be found under the “Events & Presentations” tab of the “Investors” section of the Company’s website, www.alcoa.com . Dissemination of Company Information Alcoa Corporation intends to make future announcements regarding company developments and financial performance through its website, www.alcoa.com, as well as through press releases, filings with the Securities and Exchange Commission, conference calls, media broadcasts, and webcasts. Alcoa does not incorporate the information contained on, or accessible through, its corporate website or such other websites or platforms referenced herein into this presentation.

19