Exhibit 99.1

Investor Presentation June 2026 CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Disclaimers 1 This presentation (including any accompanying oral presentation, this “Presentation”) is being furnished solely to recipients that are “qualified institutional buyers” (as defined in Rule 144 A of the Securities Act of 1933 , as amended (the “Securities Act”)), “accredited investors” (as defined in Rule 506 of Regulation D) or non - U . S . persons (as defined in Regulation S under the Securities Act) by Noble Africa LLC (the “Company” or “Noble Africa”), solely for informational purposes of considering the opportunity to participate in the proposed private placement of equity securities by the Company (the “Potential Offering”) in connection with a merger between ENDRA Life Sciences Inc . (“ENDRA”), the Company, Renergen Limited and ASP Isotopes, Inc . (“ASPI”) (collectively, the “Companies,” and the proposed merger transaction, the “Proposed Merger” and together with the Potential Offering, the “Proposed Transactions”) . By accepting this Presentation, the recipient acknowledges and agrees that all of the information contained herein is confidential, that the recipient will distribute, disclose and use such information only for such purpose and that the recipient shall not distribute, disclose or use such information for any other purpose other than the evaluation of the Proposed Transactions . THIS PRESENTATION SHALL NOT CONSTITUTE AN OFFER TO SELL, OR THE SOLICITATION OF AN OFFER TO BUY, OR A RECOMMENDATION TO PURCHASE, ANY SECURITIES IN ANY JURISDICTION, OR THE SOLICITATION OF ANY PROXY, VOTE, CONSENT OR APPROVAL IN ANY JURISDICTION IN CONNECTION WITH THE PROPOSED TRANSACTIONS, NOR SHALL THERE BE ANY OFFER OR SALE OF ANY SECURITIES IN ANY STATE OR OTHER JURISDICTION TO ANY PERSON TO WHOM IT IS UNLAWFUL TO MAKE SUCH OFFER OR SOLICITATION IN SUCH STATE OR JURISDICTION . ANY SECURITIES OF THE COMPANY TO BE OFFERED IN ANY TRANSACTION CONTEMPLATED HEREBY HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933 , AS AMENDED (THE “SECURITIES ACT”), OR ANY APPLICABLE STATE OR FOREIGN SECURITIES LAWS . ANY SECURITIES TO BE OFFERED IN ANY TRANSACTION CONTEMPLATED HEREBY HAVE NOT BEEN APPROVED OR DISAPPROVED BY THE SECURITIES AND EXCHANGE COMMISSION (THE “SEC”), ANY STATE SECURITIES COMMISSION, OR OTHER UNITED STATES OR FOREIGN REGULATORY AUTHORITY OR DETERMINED THAT THIS PRESENTATION IS TRUTHFUL AND COMPLETE . SUCH SECURITIES WILL BE OFFERED AND SOLD SOLELY IN RELIANCE ON THE EXEMPTION FROM THE REGISTRATION REQUIREMENTS PROVIDED BY THE SECURITIES ACT AND RULES AND REGULATIONS PROMULGATED THEREUNDER (INCLUDING REGULATION D OR REGULATION S UNDER THE SECURITIES ACT) . Any investment in the Company is speculative and involves a high degree of risk and uncertainty . This Presentation contains, and the accompanying oral presentation may contain “forward - looking statements” within the meaning of the safe harbor provisions of the U . S . Private Securities Litigation Reform Act of 1995 . Forward - looking statements are neither historical facts nor assurances of future performance . Instead, they are based only on our current beliefs, expectations, and assumptions regarding the future of our business, future plans and strategies, projections, anticipated events and trends, the economy, and other future conditions . Forward - looking statements can be identified by words such as “believes,” “plans,” “anticipates,” “expects,” “estimates,” “projects,” “will,” “may,” “might,” and words of a similar nature . Examples of forward - looking statements include, among others but are not limited to : he failure to realize the anticipated benefits of the Proposed Merger and any transactions contemplated thereby ; costs related to the Proposed Merger and as a result of becoming a public company ; the risk that the post - closing combined company experiences difficulties managing its growth and expanding operations following the consummation of the Proposed Merger ; the anticipated production quantities and timing for the commencement of commercial supply of helium and LNG upon completion of Phase 1 and 2 of the Renergen helium project ; the anticipated progress and timing for completion of Phase 1 and 2 of the Renergen helium project ; the ability to fund completion of the development of the Renergen helium project ; statements we make regarding expected operating results, such as future revenues and prospects from the potential commercialization of helium and LNG, future performance under contracts, and our strategies for product development or extraction of resources, engaging with potential customers, market position, and financial results . Because forward - looking statements relate to the future, they are subject to inherent uncertainties, risks, and changes in circumstances that are difficult to predict, many of which are outside our control . Our actual results, financial condition, and events may differ materially from those indicated in the forward - looking statements based upon a number of factors . Forward - looking statements are not a guarantee of future performance or developments . You are strongly cautioned that reliance on any forward - looking statements involves known and unknown risks and uncertainties . Therefore, you should not rely on any of these forward - looking statements . There are many important factors that could cause our actual results and financial condition to differ materially from those indicated in the forward - looking statements, including, but not limited to : the outcomes of various strategies and projects undertaken by the Company ; the potential impact of laws or government regulations or policies in South Africa ; our future capital requirements and sources and uses of cash ; our ability to obtain funding for our operations and future growth ; our reliance on the efforts of third parties ; the financial terms of any current and future commercial arrangements ; our ability to complete certain transactions and realize anticipated benefits from acquisitions and contracts ; the competitive nature of our industry ; the fact that the dual class structure of ENDRA following the Proposed Merger (as defined below) common stock will have the effect of concentrating voting power with ASPI and its affiliates, which may depress the market value of the Class A common stock and will limit a stockholder or a new investor’s ability to influence the outcome of important transactions, including a change in control, the market price, trading volume and marketability of ENDRA’s Class A common stock following the Proposed Merger may be significantly affected by numerous factors beyond ENDRA’s control ; because ENDRA will be a “controlled company” within the meaning of Nasdaq following the Proposed Merger, ENDRA’s stockholders may not have certain corporate governance protections that are available to stockholders of companies that are not controlled companies ; the outcome of any proceedings that may be instituted against ENDRA or the Company following the announcement of the Proposed Transactions ; the inability to recognize the anticipated benefits of the Proposed Merger, which may be affected by, among other things, competition, the ability of the combined company to grow and manage growth profitability and costs related to the Proposed Transaction ; and such other factors as are set forth in the “Risk Factor Summary” in this Presentation, and the other risks and uncertainties described in ENDRA’s periodic public filings with the SEC, including but not limited to those described under the headings “Risk Factors” and “Cautionary Note Regarding Forward - Looking Statements” in ENDRA's Annual Report on Form 10 - K for the fiscal year ended December 31 , 2025 , ENDRA's subsequent quarterly reports on Form 10 - Q and in ENDRA's other filings made with the SEC from time to time, which are available via the SEC’s website at www . sec . gov, and those described under the headings “Risk Factors” and “Cautionary Note Regarding Forward - Looking Statements” in ASPI Annual Report on Form 10 - K for the fiscal year ended December 31 , 2025 , ASPI's subsequent quarterly reports on Form 10 - Q and in ASPI's other filings made with the SEC from time to time, which are available via the SEC’s website at www . sec . gov . All forward - looking statements are qualified by reference to the cautionary statements set forth herein and should not be relied upon . Recipients are cautioned not to put undue reliance on forward - looking statements, and none of the Placement Agents (as defined below), the Companies or any of their respective representatives undertake any duty to update these forward - looking statements or the other information contained in this Presentation . None of the Companies nor any of their respective representatives gives any assurance that the Companies will achieve their respective expectations .

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Disclaimers (cont.) None of the Companies make any representation or warranty, express or implied, as to the accuracy or completeness of this Presentation or any other information (whether written or oral) that has been or will be provided to you . Nothing contained herein or in any other oral or written information provided to you is, nor shall be relied upon as, a promise or representation of any kind by the Companies . Without limitation of the foregoing, the Companies expressly disclaim any representation regarding any projections concerning future operating results or any other forward - looking statement contained herein or that otherwise has been or will be provided to you . The Companies shall not be liable to you or any prospective investor or any other person for any information contained herein or that otherwise has been or will be provided to you, or any action heretofore or hereafter taken or omitted to be taken, in connection with the Proposed Transactions . You will be entitled to rely solely on the representations and warranties made to you by the Companies in a definitive written agreement relating to the Potential Offering, when and if executed, and subject to any limitations and restrictions as may be specified in such definitive agreement . No other representations and warranties will have any legal effect . The Company has retained Lucid Capital Markets, LLC, and Ocean Wall Ltd . as placement agents (together with each of their respective affiliates, partners, directors, agents, employees, representatives and controlling persons, the “Placement Agents”) . The Placement Agents are acting solely as placement agents (and, for the avoidance of doubt, not as underwriters, initial purchasers, dealers or any other principal capacity) for the Company in connection with the Potential Offering . The analyses contained herein have been prepared or adopted by the Company, obtained from public sources or are based upon estimates and projections, and involve numerous and significant subjective determinations, and there is no assurance that such estimates and projections will be realized . The Placement Agents have not independently verified any of the information or analyses contained herein or any other information that has been or will be provided to you, and do not take responsibility for the analyses contained herein, or the basis on which they were prepared . The Placement Agents do not make any representation or warranty, express or implied, as to the accuracy or completeness of this Presentation or any other information (whether written or oral) that has been or will be provided to you . Nothing contained herein or in any other oral or written information provided to you is, nor shall be relied upon as, a promise or representation of any kind by the Placement Agents, whether as to the past, the present or the future . Without limitation of the foregoing, the Placement Agents expressly disclaim any representation regarding any projections concerning future operating results or any other forward - looking statement contained herein or that otherwise has been or will be provided to you . The Placement Agents shall not be liable to you or any prospective investor or any other person for any information contained herein that otherwise has been or will be provided to you, or any action heretofore or hereafter taken or omitted to be taken, in connection with the Proposed Transactions . The proposed terms of the Potential Offering reflected in this Presentation are indicative and non - binding . Any and all terms remain subject to further discussion, negotiation, and change . The Company and the Placement Agents are each free to conduct the process for any transaction as they in each of their sole discretion determine (including, without limitation, negotiating with any prospective investors and entering into an agreement with respect to any transaction without prior notice to you or any other person), and any procedures relating to such transaction may be changed at any time without notice to you or any other person . No sales will be made, no commitments to invest in the Company will be accepted, and no money is being solicited or will be accepted at this time . Any indication of interest from prospective purchasers in response to this document involves no obligation or commitment of any kind . This Presentation should not be distributed to any person other than the addressee to whom it was initially distributed . The information in this Presentation has not been reviewed by the SEC and certain information may not comply in certain respects with SEC rules . ENDRA intends to file a registration statement on Form S - 4 (the “Registration Statement”) that includes a proxy statement with respect to ENDRA's shareholder meeting to vote on the Proposed Transactions and a prospectus with respect to ENDRA’s securities to be issued in connection with the Proposed Transactions . After the Registration Statement is declared effective, ENDRA will mail a definitive proxy statement/prospectus relating to the Proposed Transactions to its shareholders as of a record date to be established for voting on the Proposed Transactions . ENDRA may also file other documents with the SEC regarding the Proposed Transactions . Shareholders and other interested persons are urged to read these documents and any amendments thereto, as well as any other relevant documents filed with the SEC when they become available because they will contain important information about ENDRA, the Company, Renergen and the Proposed Merger . Shareholders will also be able to obtain free copies of the preliminary proxy statement/prospectus, the definitive proxy statement/prospectus and other documents filed with the SEC, once available, without charge, at the SEC's website located at www . sec . gov, or by directing a request to Lucid Capital Markets, LLC, 570 Lexington Avenue, 40 th Floor, New York, NY 10022 . ENDRA and its directors and executive officers and other persons may be deemed to be participants in the solicitations of proxies from ENDRA's shareholders in respect of the Proposed Merger and the other matters set forth in the Registration Statement . Information regarding ENDRA's directors and executive officers is available in ENDRA's Annual Report on Form 10 - K for the year ended December 31 , 2025 , and is available free of charge at the SEC's website located at www . sec . gov, or by directing a request to ENDRA at the address above . Additional information regarding the participants in the proxy solicitation and a description of their direct and indirect interests by security holdings or otherwise, are contained in the proxy statement/prospectus relating to the Proposed Merger . This presentation includes market and industry data and forecasts that we obtained from internal research, publicly available information and industry publications and surveys . Such information could be wrong because of the method by which sources obtained their data and because information cannot always be verified with certainty due to the limits on the availability and reliability of raw data, the voluntary nature of the data - gathering process and other limitations and uncertainties . 2

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Risk Factors 3 Renergen’s business is subject to numerous material and other risks and uncertainties that you should be aware of in evaluating Renergen’s business . Please refer to the factors disclosed in Part I, Item 1 A . “Risk Factors” of ASP Isotopes Inc . ’s Annual Report on Form 10 - K for the fiscal year ended December 31 , 2025 , and any amendments thereto and in the company’s subsequent reports and filings with the U . S . Securities and Exchange Commission . These risks include, but are not limited to, the following : Risks Related to Renergen’s Limited Operating History, Financial Position and Need for Additional Capital – Renergen has incurred significant net losses since inception, and we expect to continue to incur significant net losses for the foreseeable future . – Renergen also has a limited operating history, which may make it difficult to evaluate Renergen’s prospects and likelihood of success . – Renergen currently has limited sales attributable to LNG and no sales attributable to liquefied helium . – Renergen will require substantial additional capital to finance its operations, which may not be available on acceptable terms, or at all . Risks Related to Operations in South Africa – Our operations in South Africa could be disrupted for a variety of reasons, including economic, political or social instability, which could prevent us from completing our development activities or have a material adverse effect on our operations and profits . Risks Related to the Expansion of the Virginia Gas Project – As we further expand Renergen’s current operations into Phase 2 , we may face additional problems associated with natural gas exploration and development projects, including potential problems securing additional supporting authorizations, licenses and permits, as well as unforeseen difficulties, delays and costs in construction (including potential cost - overruns, if underlying assumptions prove to be inaccurate) and operation of Phase 2 . – Managing a project as substantial in size as Phase 2 of the Virginia Gas Project requires sufficient technical, commercial and project management capacity . There can be no assurance that Renergen’s current management team has sufficient capacity, or that the project will operate as expected, incur costs within expected estimates, or that we will be able to obtain the necessary financing for Phase 2 in a timely manner and/or on acceptable terms, if at all . Risks Related to Renergen’s Business – Renergen’s drilling results in South Africa may be more uncertain than drilling results in areas that are developed and have established production . Additionally, Renergen’s identified drilling locations are scheduled out over many years, making them susceptible to uncertainties that could materially alter the occurrence or timing of their drilling . – Natural gas prices are volatile . A sustained decline in natural gas prices could adversely affect our business, financial condition and results of operations . Further, we may be unable to obtain, maintain or renew permits, leases or licenses necessary for Renergen’s operations, the failure of which could impair our ability to conduct Renergen’s operations . Risks Related to Renergen’s Indebtedness and Liquidity – The DFC Credit Facility Agreement and IDC Loan Agreement place operating restrictions on Renergen and create default risks . Further, we may not be able to generate sufficient cash to service all of Renergen’s indebtedness and may be forced to take other actions to satisfy Renergen’s obligations under applicable debt instruments, which may not be successful . – Renergen’s outstanding indebtedness under the IDC Loan Agreement bears interest at a variable rate, which makes us more vulnerable to increases in interest rates and could cause Renergen’s interest expense to increase and decrease cash available for operations and other purposes . Risks Related to the Proposed Merger and the Ownership of the Company's Units – The Proposed Merger may not be consummated in a timely matter or at all . – ENDRA may fail to realize the anticipated benefits of the Proposed Merger and any transactions contemplated thereby . – ENDRA may experience difficulties managing its growth and expanding operations following the consummation of the Proposed Merger . – The dual class structure of ENDRA's common stock following the proposed Merger will have the effect of concentrating voting power with ASPI and its affiliates, which may depress the market value of the Class A common stock following the Proposed Merger, into which the Company's units will convert following the proposed Merger, and will limit a stockholder or a new investor's ability to influence the outcome of important transactions, including a change in control . – The market price, trading volume and marketability of ENDRA's Class A common stock following the proposed Merger may be significantly affected by numerous factors beyond ENDRA's control . – ENDRA may need to raise additional capital to grow our business and may not be able to do so on favorable terms, if at all . Future issuances of equity or debt securities may adversely affect the value of ENDRA's common stock . – Future sales of Class A common stock following the proposed Merger may affect the market price of ENDRA's Class A common stock . – Because ENDRA is expected to be a “controlled company” within the meaning of the Nasdaq listing rules following the Proposed Merger, ENDRA's stockholders may not have certain corporate governance protections that are available to stockholders of companies that are not controlled companies .

Helium Market Overview The Virginia Gas Project Is Truly Unique Project Overview – Phase 1 and Phase 2 LNG Market Overview Milestones Transaction Overview Table of Contents CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION 4

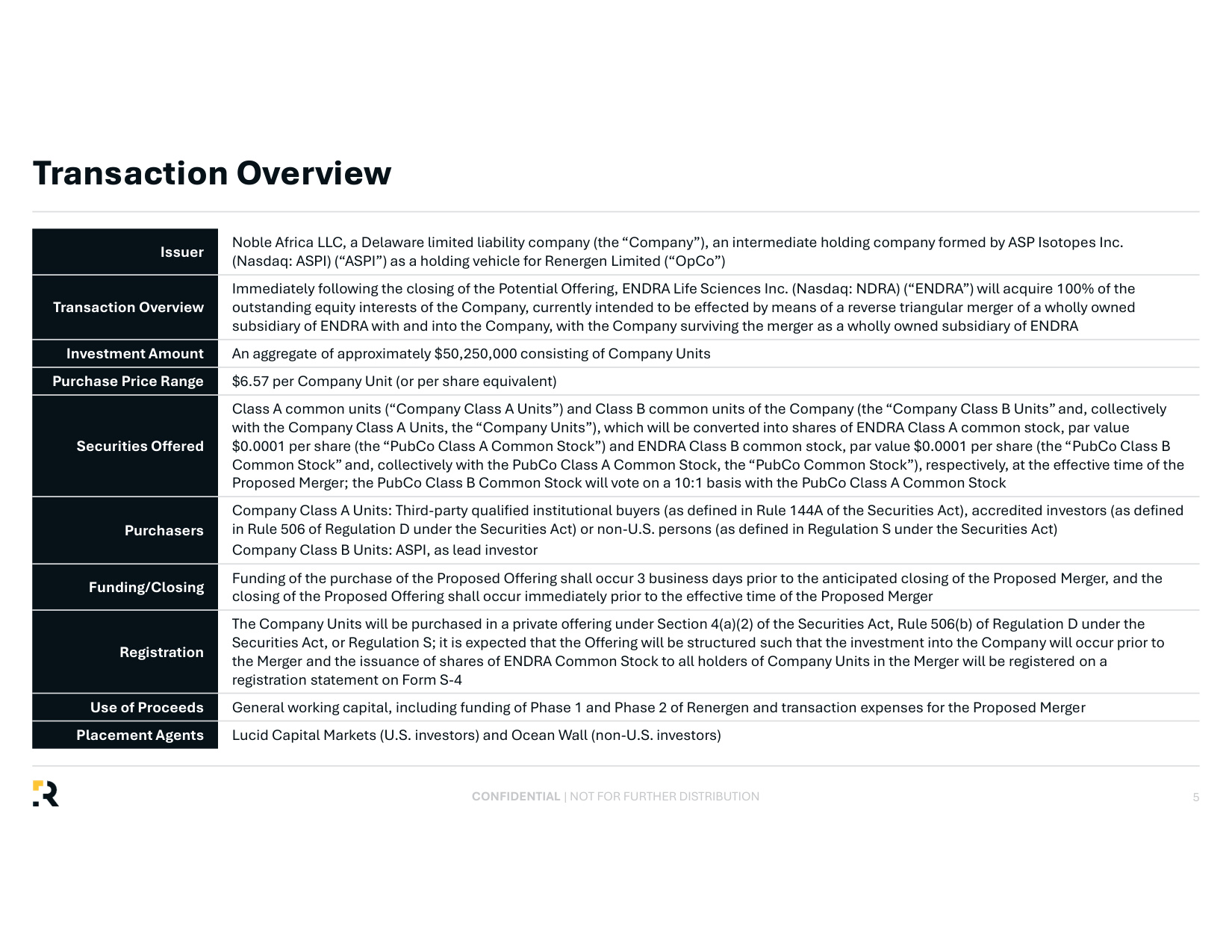

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Transaction Overview 5 Issuer Noble Africa LLC, a Delaware limited liability company (the "Company"), an intermediate holding company formed by ASP Isotopes Inc. (Nasdaq: ASPI) ("ASPI") as a holding vehicle for Renergen Limited ("OpCo") Transaction Overview Immediately following the closing of the Potential Offering, ENDRA Life Sciences Inc. (Nasdaq: NDRA) ("ENDRA") will acquire 100% of the outstanding equity interests of the Company, currently intended to be effected by means of a reverse triangular merger of a wholly owned subsidiary of ENDRA with and into the Company, with the Company surviving the merger as a wholly owned subsidiary of ENDRA Investment Amount An aggregate of approximately $50,000,000 consisting of Company Units Purchase Price Range $6.57 per Company Unit (or per share equivalent) Securities Offered Class A common units ("Company Class A Units") and Class B common units of the Company (the "Company Class B Units" and, collectively with the Company Class A Units, the "Company Units"), which will be converted into shares of ENDRA Class A common stock, par value $0.0001 per share (the "PubCo Class A Common Stock") and ENDRA Class B common stock, par value $0.0001 per share (the "PubCo Class B Common Stock" and, collectively with the PubCo Class A Common Stock, the "PubCo Common Stock"), respectively, at the effective time of the Proposed Merger; the PubCo Class B Common Stock will vote on a 10:1 basis with the PubCo Class A Common Stock Purchasers Company Class A Units: Third-party qualified institutional buyers (as defined in Rule 144A of the Securities Act), accredited investors (as defined in Rule 506 of Regulation D under the Securities Act) or non-U.S. persons (as defined in Regulation S under the Securities Act) Company Class B Units: ASPI, as lead investor Funding/Closing Funding of the purchase of the Proposed Offering shall occur 3 business days prior to the anticipated closing of the Proposed Merger, and the closing of the Proposed Offering shall occur immediately prior to the effective time of the Proposed Merger Registration The Company Units will be purchased in a private offering under Section 4(a)(2) of the Securities Act, Rule 506(b) of Regulation D under the Securities Act, or Regulation S; it is expected that the Offering will be structured such that the investment into the Company will occur prior to the Merger and the issuance of shares of ENDRA Common Stock to all holders of Company Units in the Merger will be registered on a registration statement on Form S-4 Use of Proceeds General working capital, including funding of Phase 1 and Phase 2 of Renergen and transaction expenses for the Proposed Merger Placement Agents Lucid Capital Markets (U.S. investors) and Ocean Wall (non-U.S. investors)

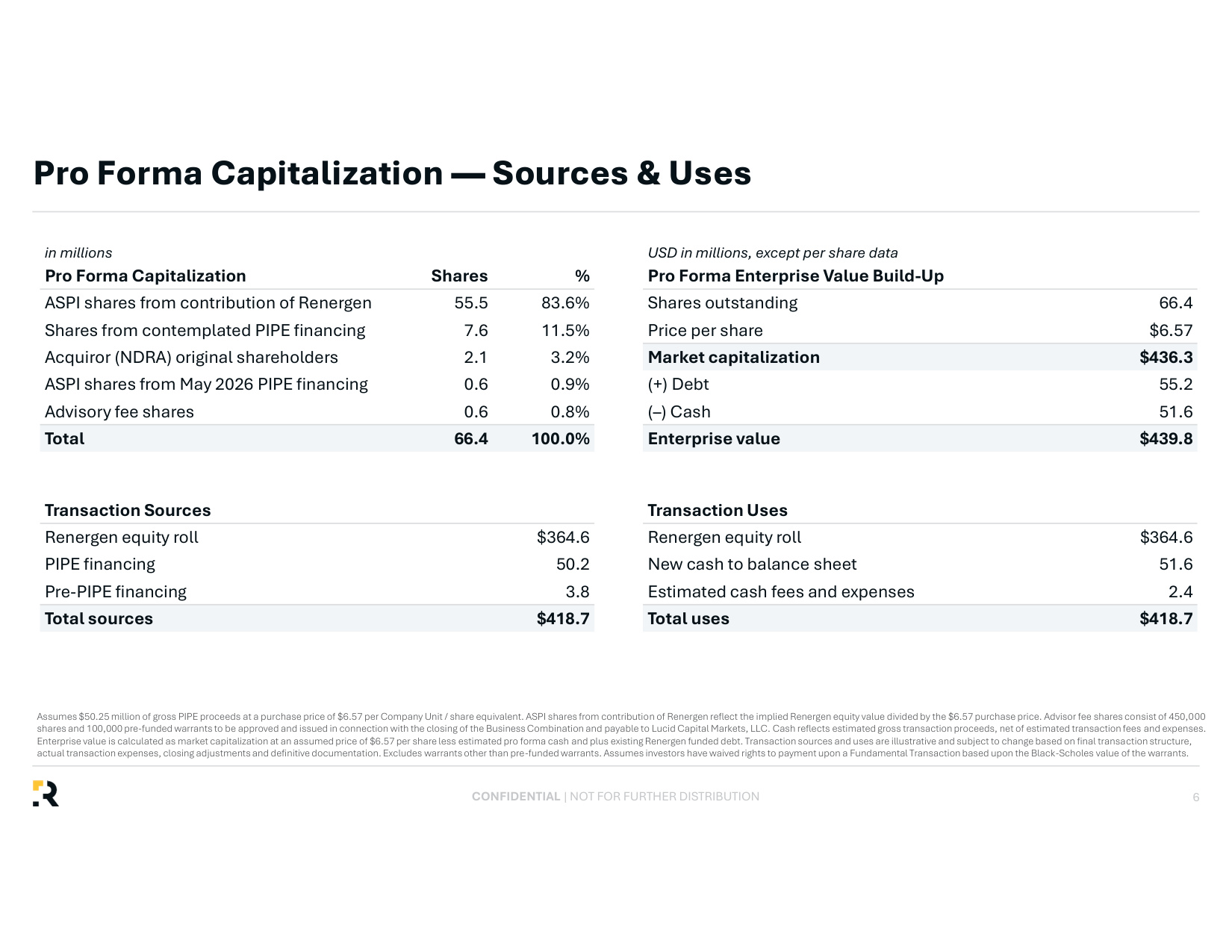

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Pro Forma Capitalization — Sources & Uses 6 in millions Pro Forma Capitalization Shares % ASPI shares from contribution of Renergen 55.5 83.6% Shares from contemplated PIPE financing 7.6 11.5% Acquiror (NDRA) original shareholders 2.1 3.2% ASPI shares from May 2026 PIPE financing 0.6 0.9% Advisory fee shares 0.6 0.8% Total 66.4 100.0% USD in millions, except per share data Pro Forma Enterprise Value Build-Up Shares outstanding 66.4 Price per share $6.57 Market capitalization $436.0 (+) Debt 55.2 (–) Cash 51.4 Enterprise value $439.8 Transaction Sources Renergen equity roll $364.6 PIPE financing 50.0 Pre-PIPE financing 3.8 Total sources $418.4 Transaction Uses Renergen equity roll $364.6 New cash to balance sheet 51.4 Estimated cash fees and expenses 2.4 Total uses $418.4 Assumes $50 million of gross PIPE proceeds at a purchase price of $6.57 per Company Unit / share equivalent. ASPI shares from contribution of Renergen reflect the implied Renergen equity value divided by the $6.57 purchase price. Advisor fee shares consist of 450,000 shares and 100,000 pre-funded warrants to be approved and issued in connection with the closing of the Business Combination and payable to Lucid Capital Markets, LLC. Cash reflects estimated gross transaction proceeds, net of estimated transaction fees and expenses. Enterprise value is calculated as market capitalization at an assumed price of $6.57 per share less estimated pro forma cash and plus existing Renergen funded debt. Transaction sources and uses are illustrative and subject to change based on final transaction structure, actual transaction expenses, closing adjustments and definitive documentation. Excludes warrants other than pre-funded warrants. Assumes investors have waived rights to payment upon a Fundamental Transaction based upon the Black-Scholes value of the warrants.

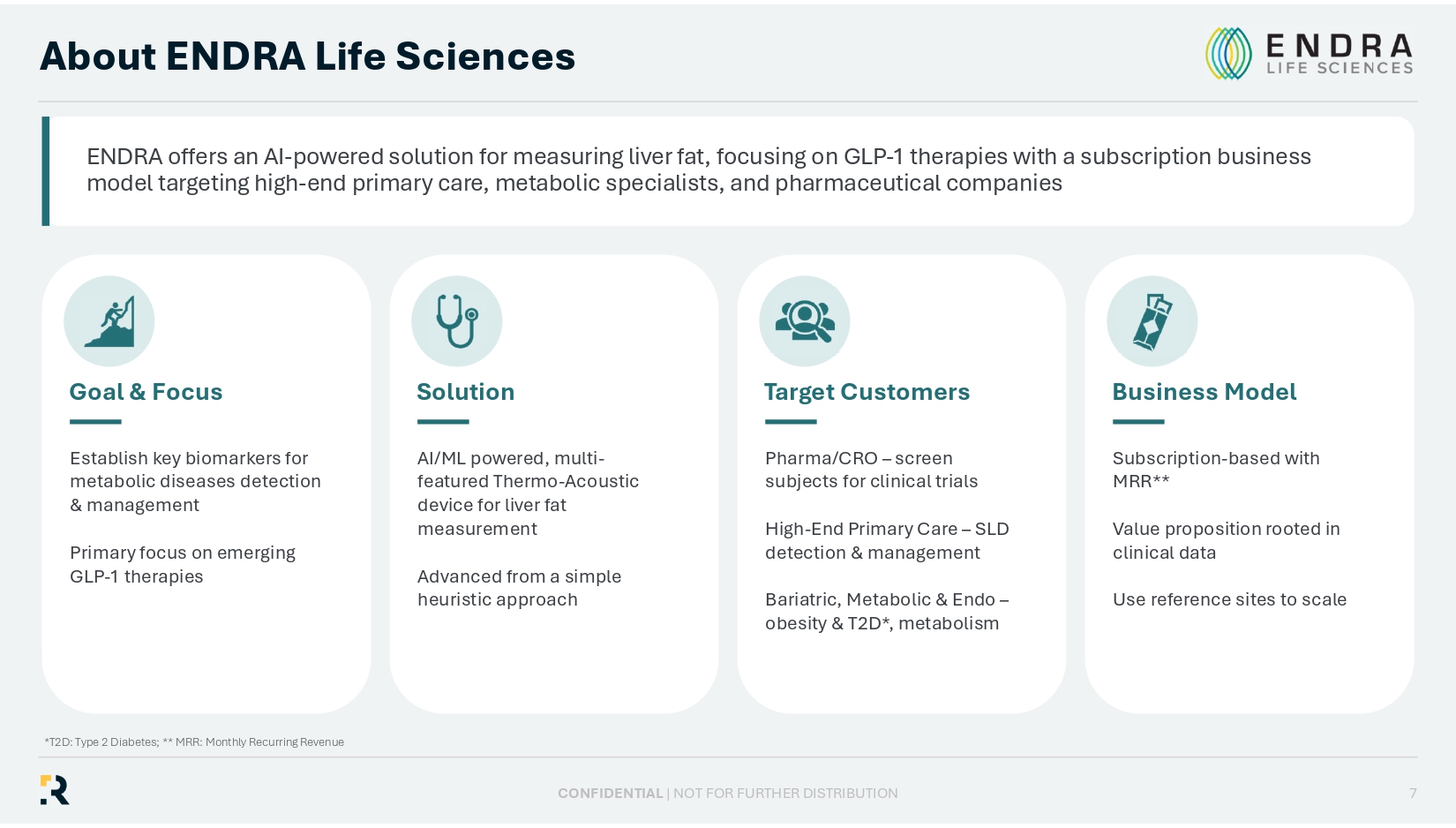

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Goal & Focus Establish key biomarkers for metabolic diseases detection & management Primary focus on emerging GLP - 1 therapies Solution AI/ML powered, multi - featured Thermo - Acoustic device for liver fat measurement Advanced from a simple heuristic approach Target Customers Pharma/CRO – screen subjects for clinical trials High - End Primary Care – SLD detection & management Bariatric, Metabolic & Endo – obesity & T2D*, metabolism Business Model Subscription - based with MRR** Value proposition rooted in clinical data Use reference sites to scale ENDRA offers an AI - powered solution for measuring liver fat, focusing on GLP - 1 therapies with a subscription business model targeting high - end primary care, metabolic specialists, and pharmaceutical companies About ENDRA Life Sciences 7 *T2D: Type 2 Diabetes; ** MRR: Monthly Recurring Revenue

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Paul Mann CEO, Renergen CEO and Executive Chairman, ASP Isotopes Inc. – Co - founded ASP Isotopes in September 2021 – 25+ years of experience on Wall Street investing in healthcare and chemicals companies at Soros Fund Management, Highbridge Capital and Morgan Stanley – M.A. and M.Eng (Chemical Engineering) from Cambridge University – Research Scientist at Procter and Gamble – CFA charter holder Leadership Overview 8 – Almost two decades of upstream oil and gas experience, commercialising critical gas and helium assets – Co - developer of South Africa’s only onshore petroleum production right – Helped take the Virginia Gas Project to a globally significant reserve – Chairs ONPASA – Trustee of the Upstream Training Trust Nick Mitchell COO, Renergen Co - COO, ASP Isotopes Inc

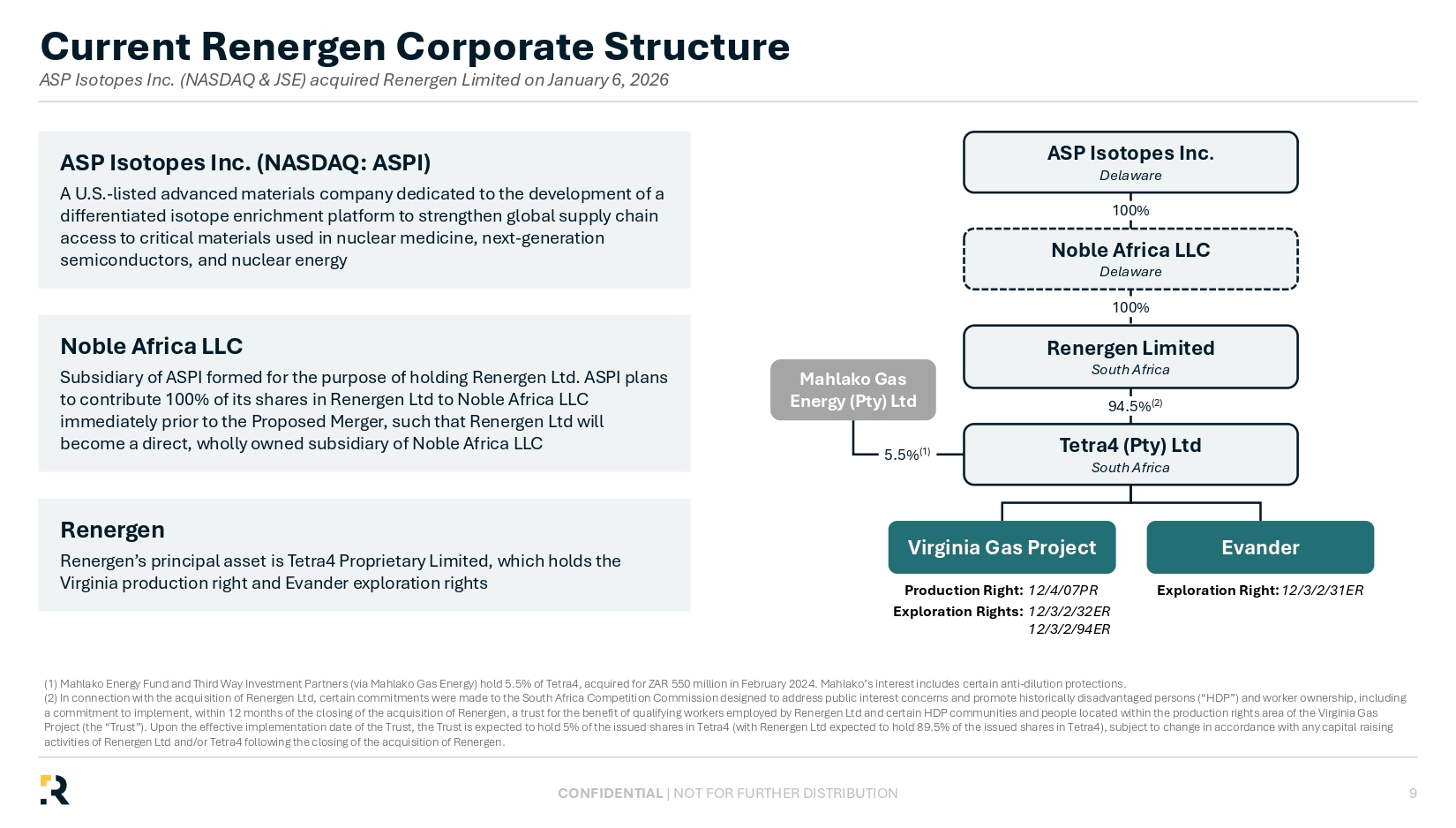

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION ASP Isotopes Inc. (NASDAQ: ASPI) A U.S. - listed advanced materials company dedicated to the development of a differentiated isotope enrichment platform to strengthen global supply chain access to critical materials used in nuclear medicine, next - generation semiconductors, and nuclear energy Renergen Renergen’s principal asset is Tetra4 Proprietary Limited, which holds the Virginia production right and Evander exploration rights Noble Africa LLC Subsidiary of ASPI formed for the purpose of holding Renergen Ltd. ASPI plans to contribute 100% of its shares in Renergen Ltd to Noble Africa LLC immediately prior to the Proposed Merger, such that Renergen Ltd will become a direct, wholly owned subsidiary of Noble Africa LLC ASP Isotopes Inc . Delaware Renergen Limited South Africa Mahlako Gas Energy (Pty) Ltd Tetra4 (Pty) Ltd South Africa Virginia Gas Project Evander Noble Africa LLC Delaware (1) Mahlako Energy Fund and Third Way Investment Partners (via Mahlako Gas Energy) hold 5.5% of Tetra4, acquired for ZAR 550 million in F eb ruary 2024. Mahlako’s interest includes certain anti - dilution protections. (2) In connection with the acquisition of Renergen Ltd, certain commitments were made to the South Africa Competition Commiss ion designed to address public interest concerns and promote historically disadvantaged persons (“HDP”) and worker ownership, inc lu ding a commitment to implement, within 12 months of the closing of the acquisition of Renergen , a trust for the benefit of qualifying workers employed by Renergen Ltd and certain HDP communities and people located withi n t he production rights area of the Virginia Gas Project (the “Trust”). Upon the effective implementation date of the Trust, the Trust is expected to hold 5% of the issued sh are s in Tetra4 (with Renergen Ltd expected to hold 89.5% of the issued shares in Tetra4), subject to change in accordance with a ny capital raising activities of Renergen Ltd and/or Tetra4 following the closing of the acquisition of Renergen . Current Renergen Corporate Structure ASP Isotopes Inc. (NASDAQ & JSE) acquired Renergen Limited on January 6, 2026 9 Production Right: 12/4/07PR 12/3/2/32ER 12/3/2/94ER Exploration Rights: Exploration Right: 12/3/2/31ER 5.5% (1) 100% 94.5% (2) 100%

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION WORLD - CLASS RESERVES ~3% average helium concentration across the field based on exploration to date vs. global mega - projects as low as 0.04% First - Mover Position Only onshore petroleum production right in South Africa Producing & Scaling Phase 1 drilling ~4 months ahead of schedule: Targets ~70 MCF/day helium and ~2,500 GJ/day LNG Phase 2 targets ~900 MCF/day helium and ~34,400 GJ/day LNG U.S. - Anchored Funding Principal lender is the U.S. Development Finance Corporation (DFC) Tetra4 has entered into a $40M secured credit facility with DFC, and DFC has conditionally approved to fund Phase 2 with up to $500M of senior secured debt Standard Bank of South Africa has also conditionally approved up to an additional $250M of senior secured debt funding for Phase 2 Scarcity Value One of few commercial - scale helium sources outside legacy regions Corporate Highlights Providing exposure to a rare strategic asset, combining high helium concentrations with high - purity methane, creating a distinct ive helium and LNG platform in South Africa 10 Government - Backed Mandate Designated a Strategic Integrated Project by the South African government Helium is classified as a critical mineral in the U.S.

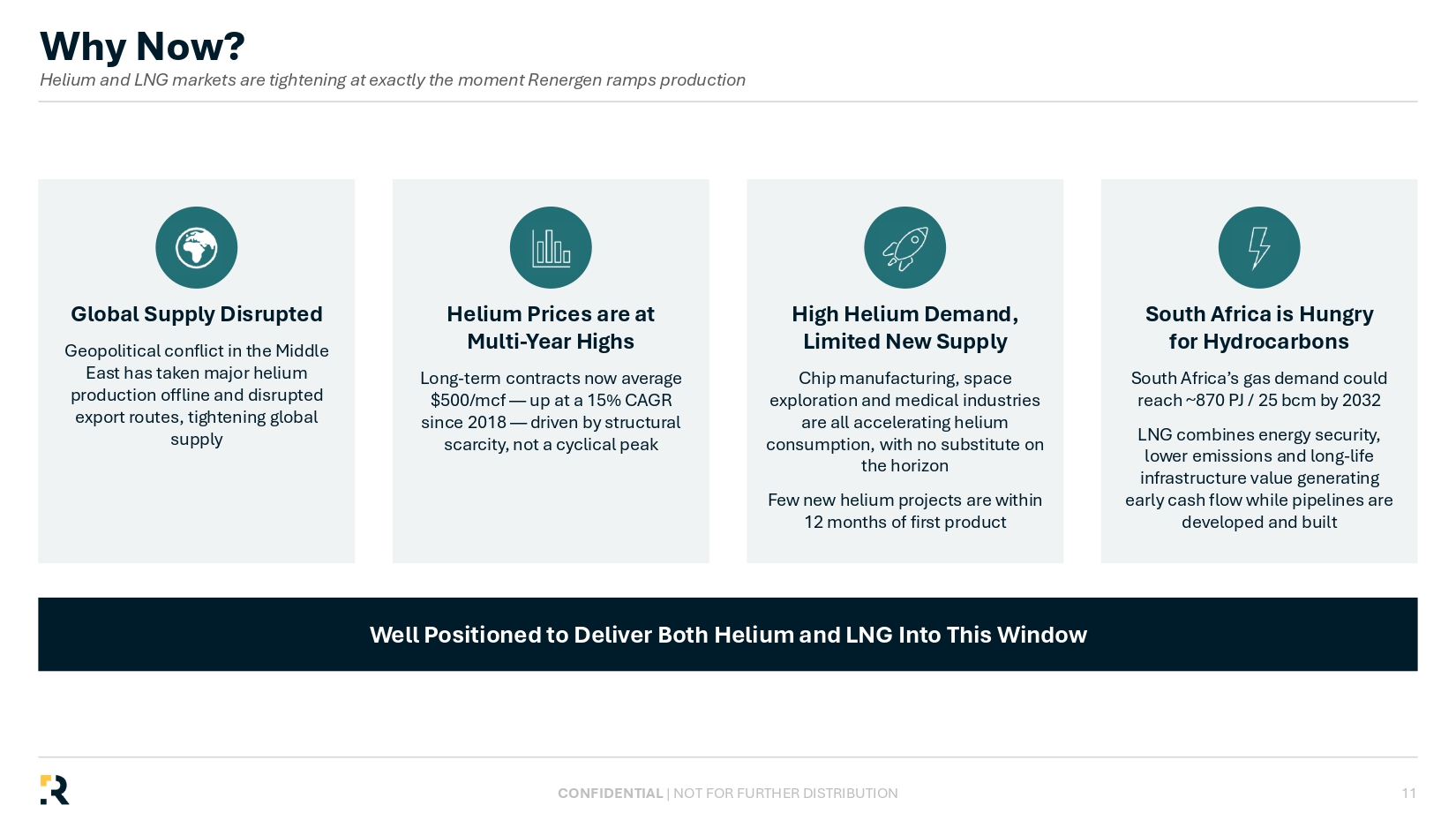

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Well Positioned to Deliver Both Helium and LNG Into This Window Global Supply Disrupted Geopolitical conflict in the Middle East has taken major helium production offline and disrupted export routes, tightening global supply Helium Prices are at Multi - Year Highs Long - term contracts now average $500/mcf — up at a 15% CAGR since 2018 — driven by structural scarcity, not a cyclical peak High Helium Demand, Limited New Supply Chip manufacturing, space exploration and medical industries are all accelerating helium consumption, with no substitute on the horizon Few new helium projects are within 12 months of first product South Africa is Hungry for Hydrocarbons South Africa’s gas demand could reach ~870 PJ / 25 bcm by 2032 LNG combines energy security, lower emissions and long - life infrastructure value generating early cash flow while pipelines are developed and built Why Now? Helium and LNG markets are tightening at exactly the moment Renergen ramps production 11

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Helium Market Overview

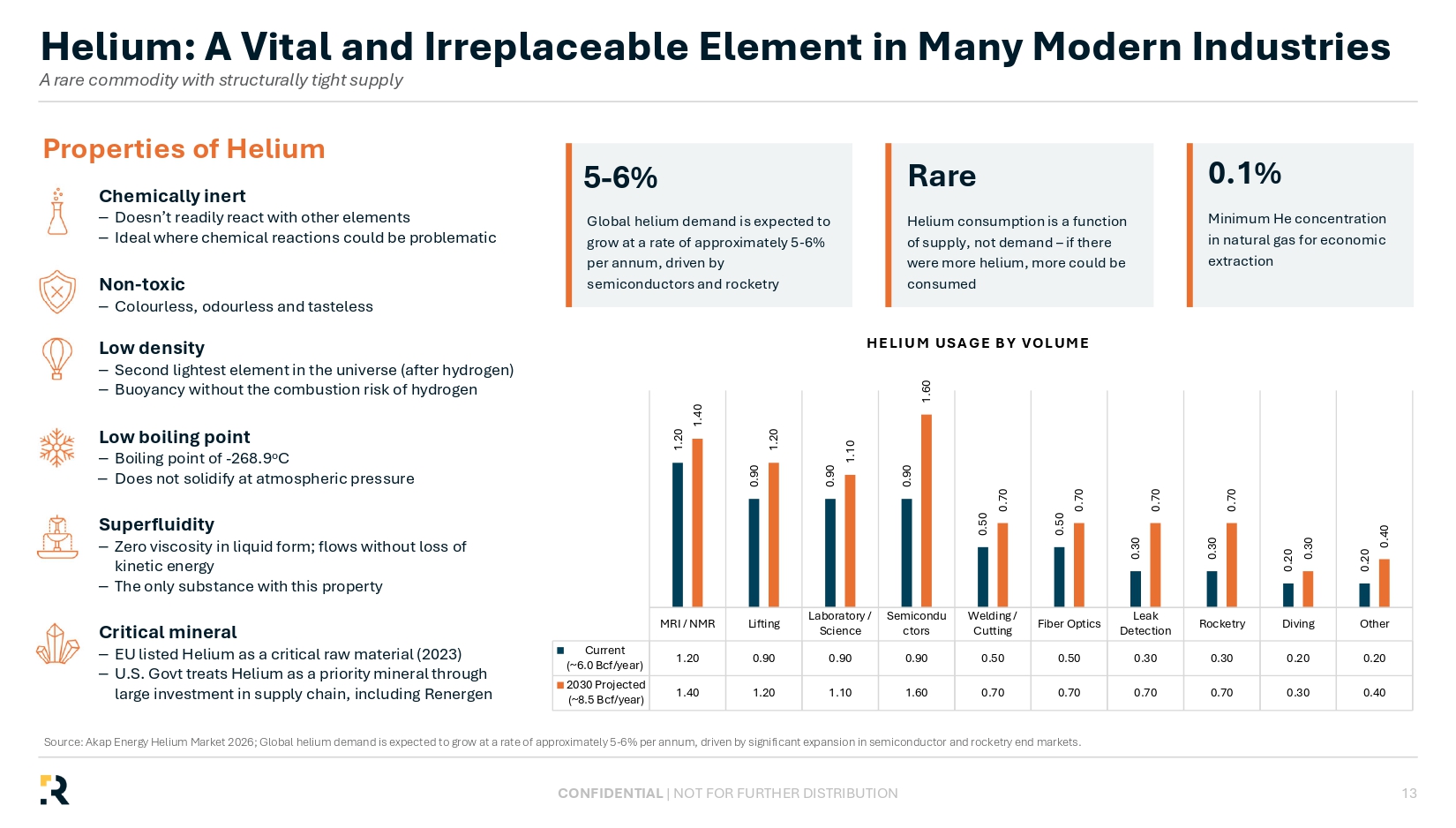

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION MRI / NMR Lifting Laboratory / Science Semicondu ctors Welding / Cutting Fiber Optics Leak Detection Rocketry Diving Other Current (~6.0 Bcf/year) 1.20 0.90 0.90 0.90 0.50 0.50 0.30 0.30 0.20 0.20 2030 Projected (~8.5 Bcf/year) 1.40 1.20 1.10 1.60 0.70 0.70 0.70 0.70 0.30 0.40 1.20 0.90 0.90 0.90 0.50 0.50 0.30 0.30 0.20 0.20 1.40 1.20 1.10 1.60 0.70 0.70 0.70 0.70 0.30 0.40 HELIUM USAGE BY VOLUME Properties of Helium Chemically inert – Doesn’t readily react with other elements – Ideal where chemical reactions could be problematic Non - toxic – Colourless, odourless and tasteless Low density – Second lightest element in the universe (after hydrogen) – Buoyancy without the combustion risk of hydrogen Low boiling point – Boiling point of - 268.9 o C – Does not solidify at atmospheric pressure Superfluidity – Zero viscosity in liquid form; flows without loss of kinetic energy – The only substance with this property Critical mineral – EU listed Helium as a critical raw material (2023) – U.S. Govt treats Helium as a priority mineral through large investment in supply chain, including Renergen 5 - 6% Global helium demand is expected to grow at a rate of approximately 5 - 6% per annum, driven by semiconductors and rocketry Helium consumption is a function of supply, not demand – if there were more helium, more could be consumed Rare 0.1% Minimum He concentration in natural gas for economic extraction Helium: A Vital and Irreplaceable Element in Many Modern Industries A rare commodity with structurally tight supply 13 Source: Akap Energy Helium Market 2026; Global helium demand is expected to grow at a rate of approximately 5 - 6% per annum, driven by signif icant expansion in semiconductor and rocketry end markets.

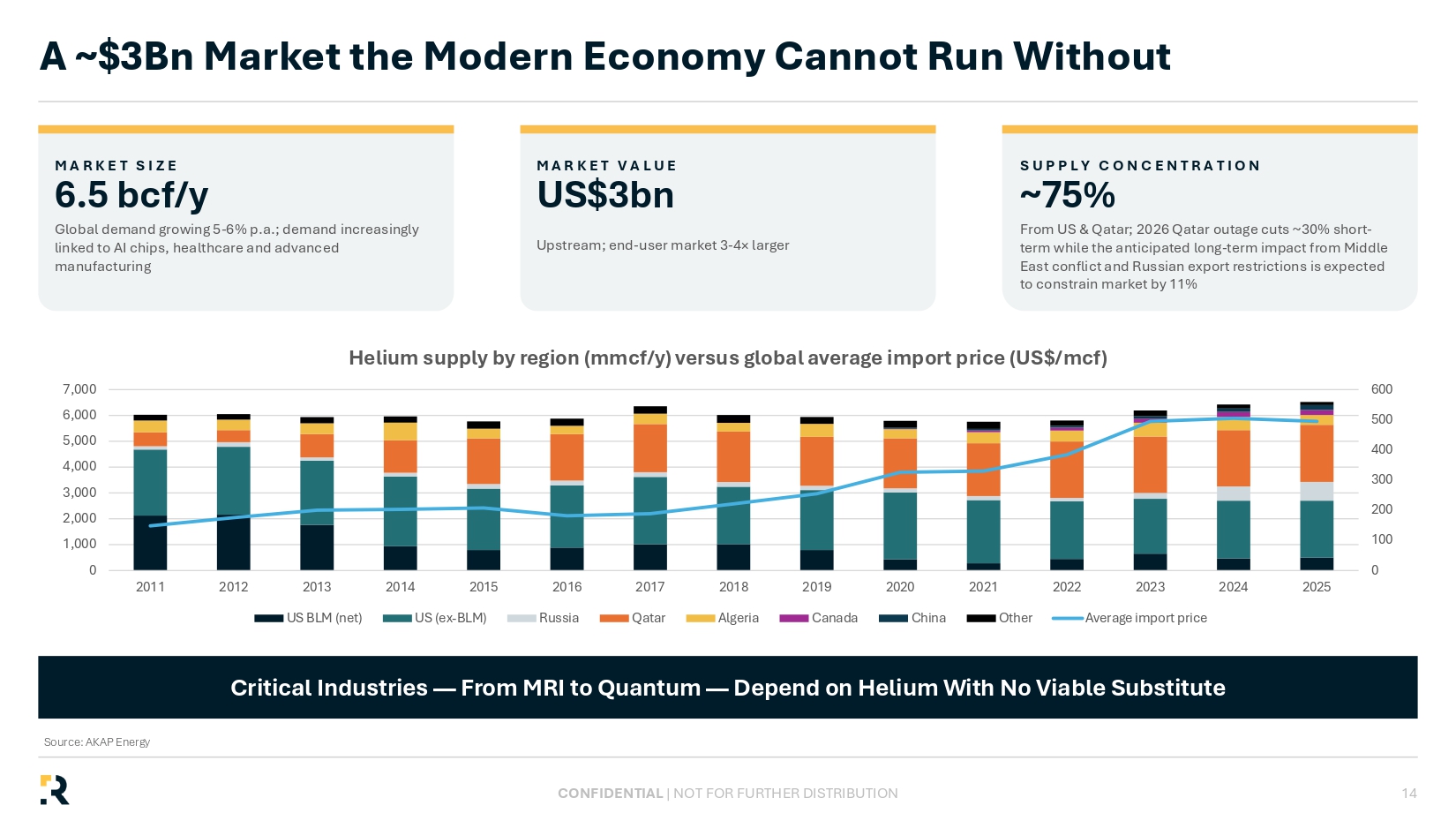

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION A ~$3Bn Market the Modern Economy Cannot Run Without 14 Critical Industries — From MRI to Quantum — Depend on Helium With No Viable Substitute MARKET SIZE 6.5 bcf/y Global demand growing 5 - 6% p.a.; demand increasingly linked to AI chips, healthcare and advanced manufacturing MARKET VALUE US$3bn Upstream; end - user market 3 - 4 × larger SUPPLY CONCENTRATION ~75% From US & Qatar; 2026 Qatar outage cuts ~30% short - term while the anticipated long - term impact from Middle East conflict and Russian export restrictions is expected to constrain market by 11% 0 100 200 300 400 500 600 0 1,000 2,000 3,000 4,000 5,000 6,000 7,000 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 Helium supply by region (mmcf/y) versus global average import price (US$/mcf) US BLM (net) US (ex-BLM) Russia Qatar Algeria Canada China Other Average import price Source: AKAP Energy

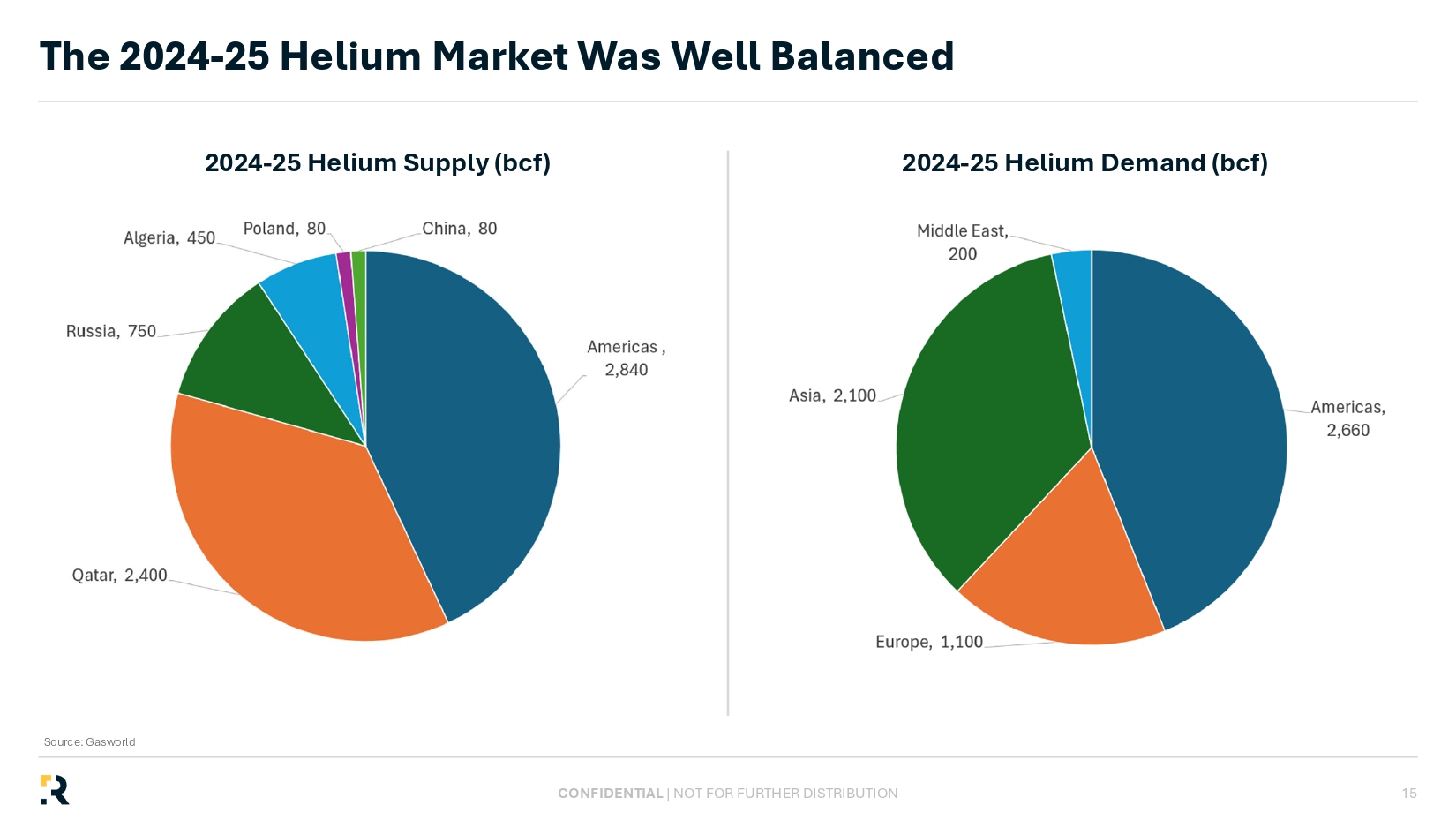

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION 15 2024 - 25 Helium Supply (bcf) 2024 - 25 Helium Demand (bcf) The 2024 - 25 Helium Market Was Well Balanced Source: Gasworld

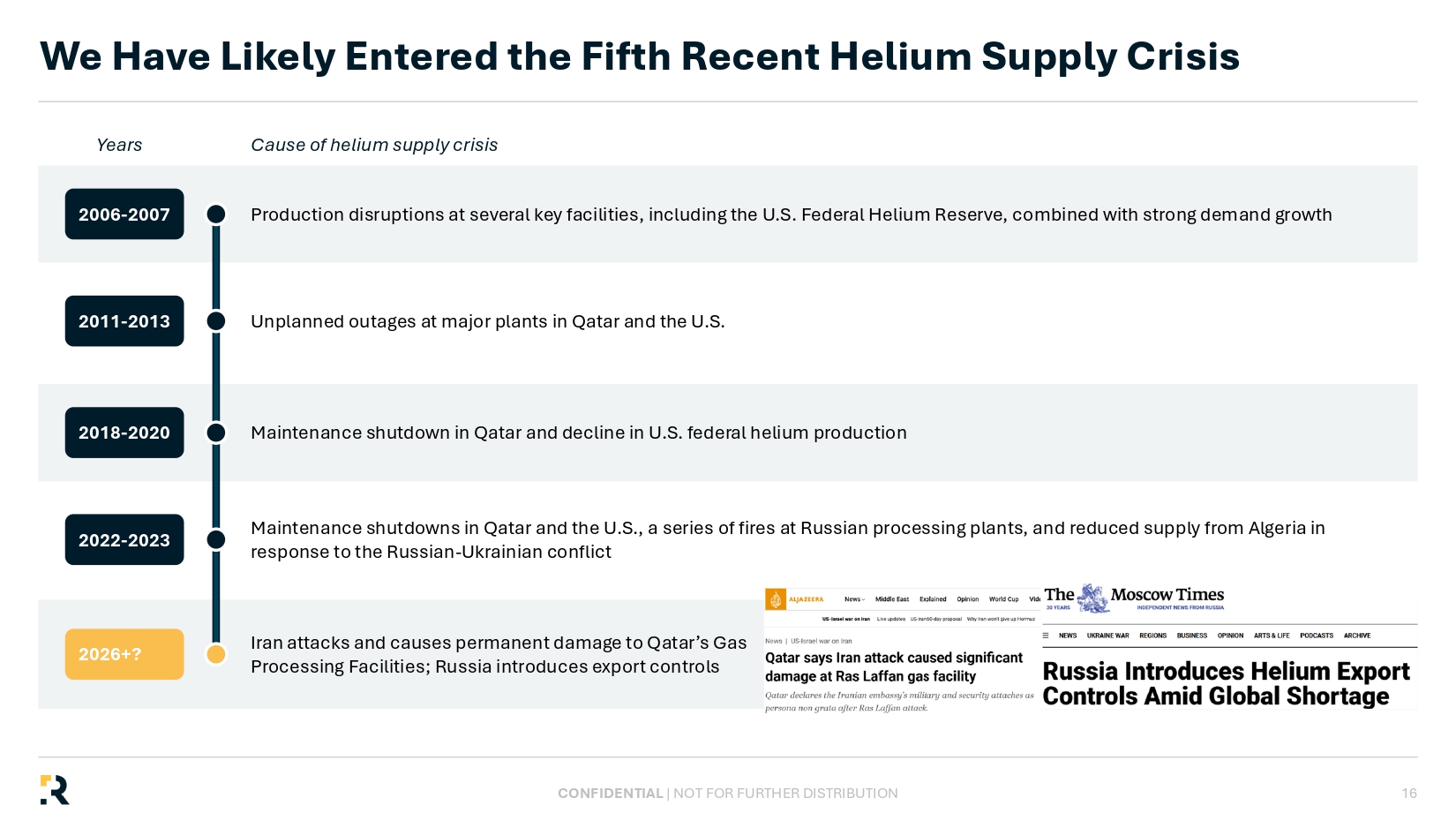

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION 2006 - 2007 2011 - 2013 2018 - 2020 2022 - 2023 2026+? Production disruptions at several key facilities, including the U.S. Federal Helium Reserve, combined with strong demand grow th Unplanned outages at major plants in Qatar and the U.S. Maintenance shutdown in Qatar and decline in U.S. federal helium production Maintenance shutdowns in Qatar and the U.S., a series of fires at Russian processing plants, and reduced supply from Algeria in response to the Russian - Ukrainian conflict Iran attacks and causes permanent damage to Qatar’s Gas Processing Facilities; Russia introduces export controls Years Cause of helium supply crisis We Have Likely Entered the Fifth Recent Helium Supply Crisis 16

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION The Virginia Gas Project is Truly Unique

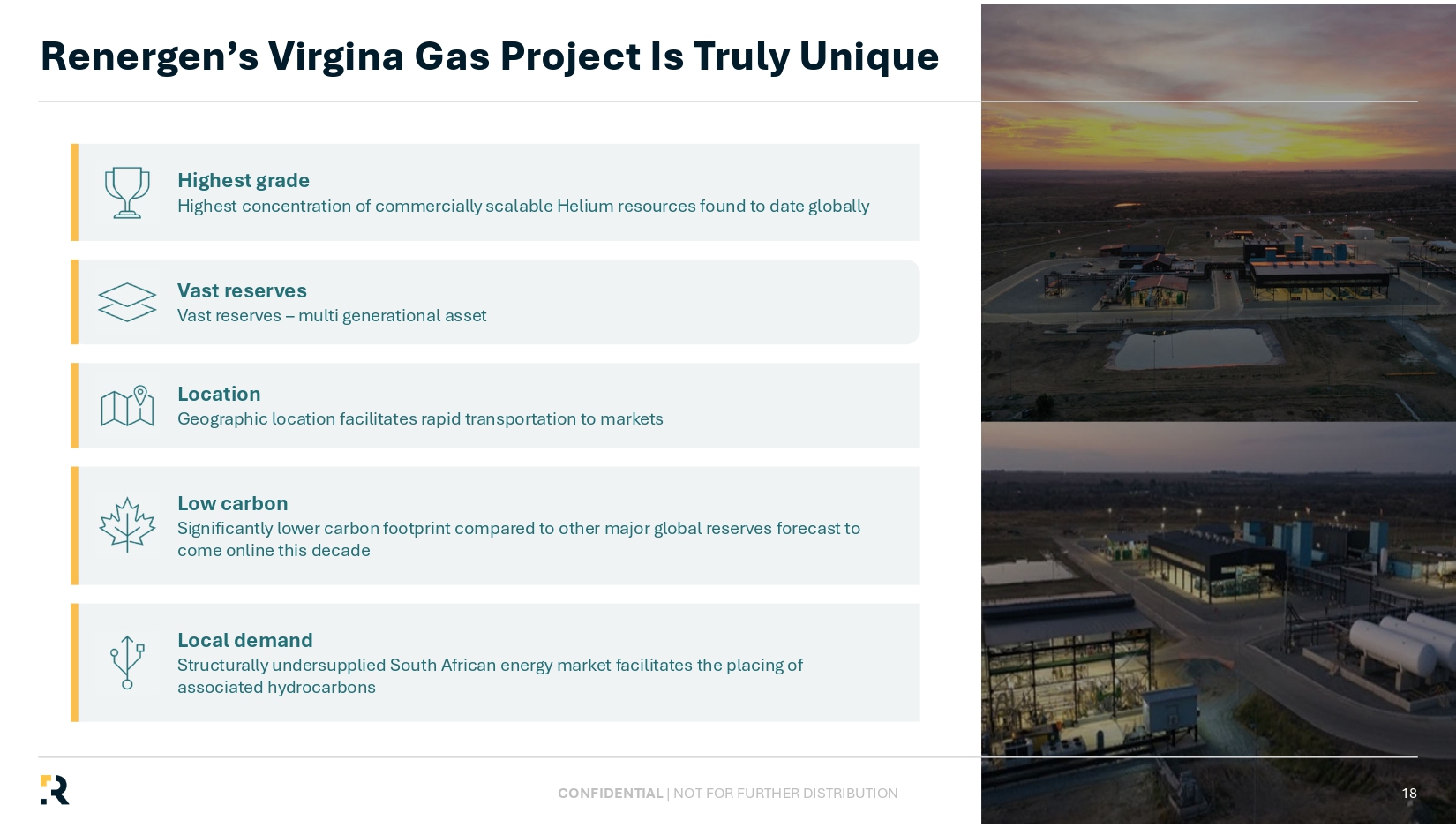

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Highest grade Highest concentration of commercially scalable Helium resources found to date globally Vast reserves Vast reserves – multi generational asset Location Geographic location facilitates rapid transportation to markets Low carbon Significantly lower carbon footprint compared to other major global reserves forecast to come online this decade Local demand Structurally undersupplied South African energy market facilitates the placing of associated hydrocarbons Renergen’s Virgina Gas Project Is Truly Unique 18

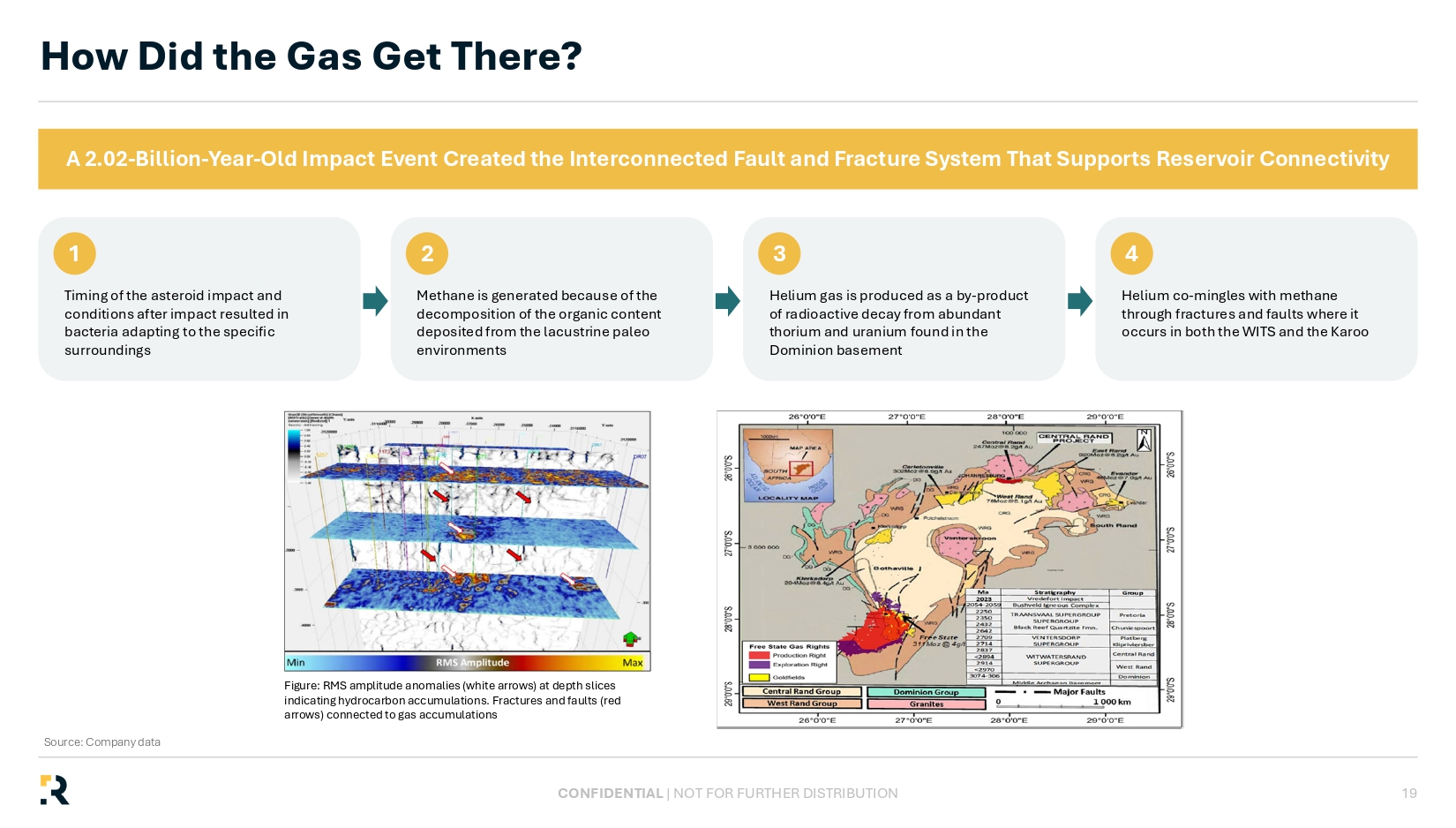

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Free State 311Moz @ 4g/t Figure: RMS amplitude anomalies (white arrows) at depth slices indicating hydrocarbon accumulations. Fractures and faults (red arrows) connected to gas accumulations 1 Timing of the asteroid impact and conditions after impact resulted in bacteria adapting to the specific surroundings 2 Methane is generated because of the decomposition of the organic content deposited from the lacustrine paleo environments 3 Helium gas is produced as a by - product of radioactive decay from abundant thorium and uranium found in the Dominion basement 4 Helium co - mingles with methane through fractures and faults where it occurs in both the WITS and the Karoo 19 How Did the Gas Get There? Source: Company data A 2.02 - Billion - Year - Old Impact Event Created the Interconnected Fault and Fracture System That Supports Reservoir Connectivity

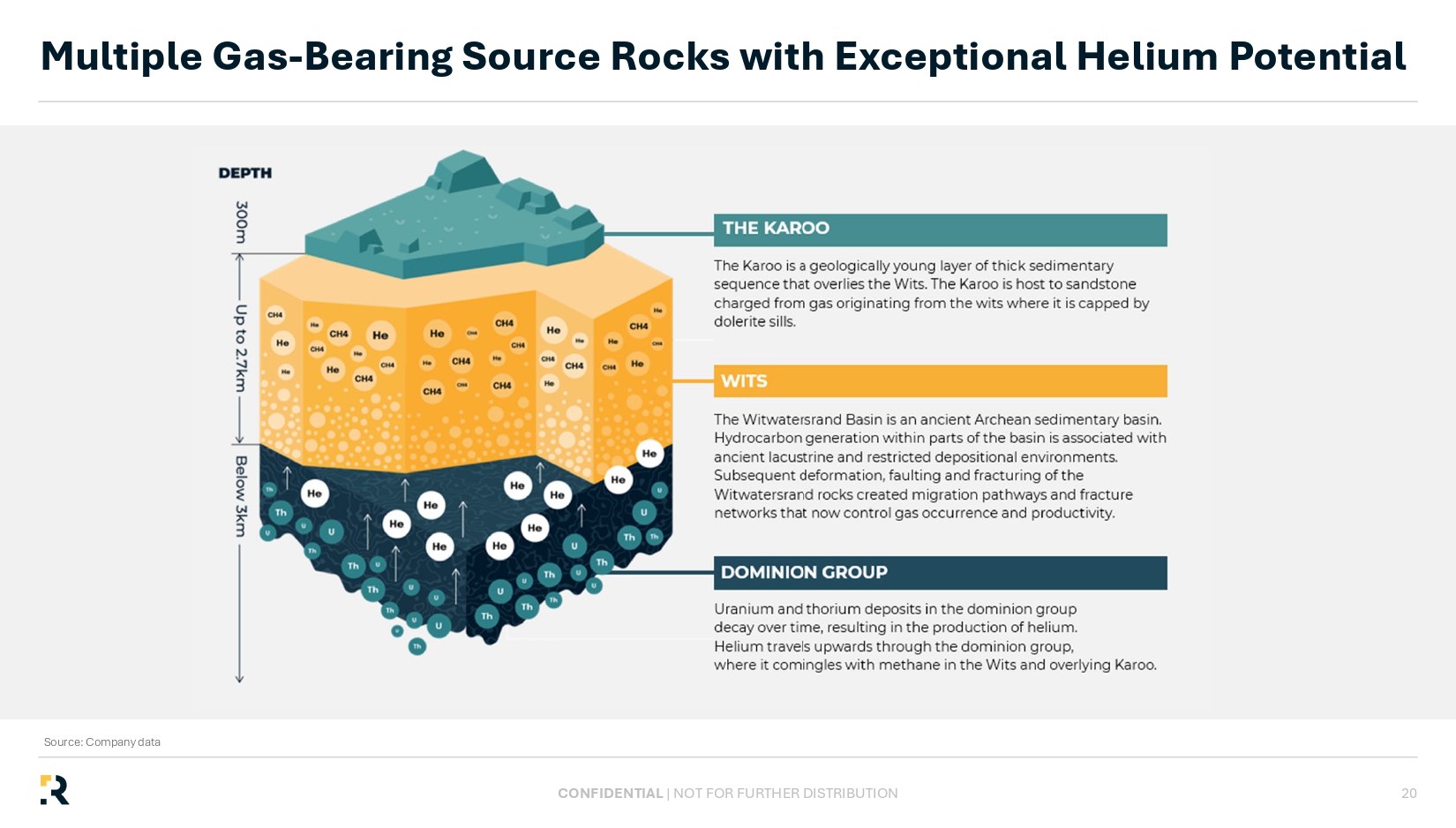

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Multiple Gas - Bearing Source Rocks with Exceptional Helium Potential 20 Source: Company data

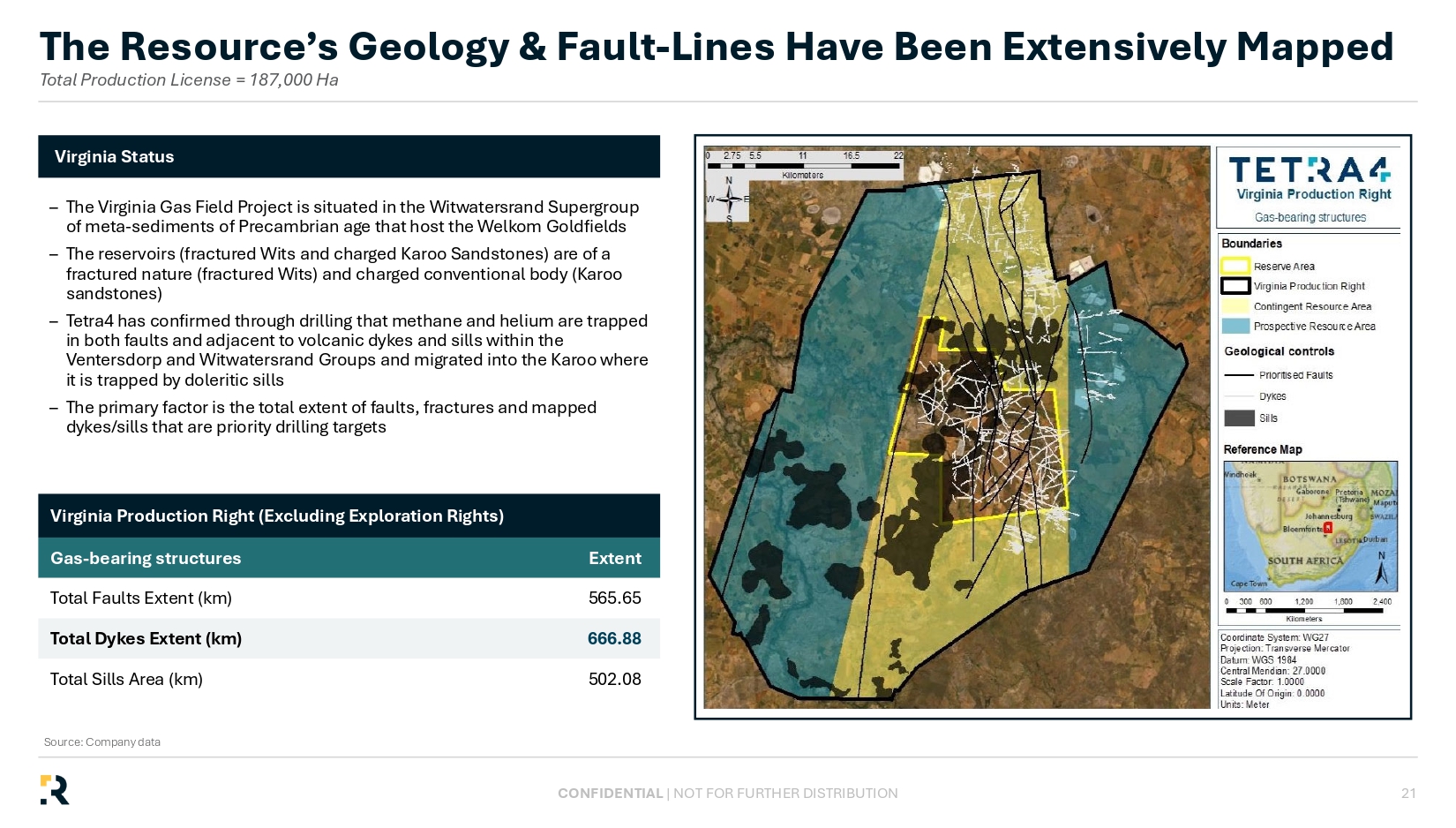

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION The Resource’s Geology & Fault - Lines Have Been Extensively Mapped Total Production License = 187,000 Ha 21 – The Virginia Gas Field Project is situated in the Witwatersrand Supergroup of meta - sediments of Precambrian age that host the Welkom Goldfields – The reservoirs (fractured Wits and charged Karoo Sandstones) are of a fractured nature (fractured Wits) and charged conventional body (Karoo sandstones) – Tetra4 has confirmed through drilling that methane and helium are trapped in both faults and adjacent to volcanic dykes and sills within the Ventersdorp and Witwatersrand Groups and migrated into the Karoo where it is trapped by doleritic sills – The primary factor is the total extent of faults, fractures and mapped dykes/sills that are priority drilling targets Virginia Status Virginia Production Right (Excluding Exploration Rights) Extent Gas - bearing structures 565.65 Total Faults Extent (km) 666.88 Total Dykes Extent (km) 502.08 Total Sills Area (km) Source: Company data

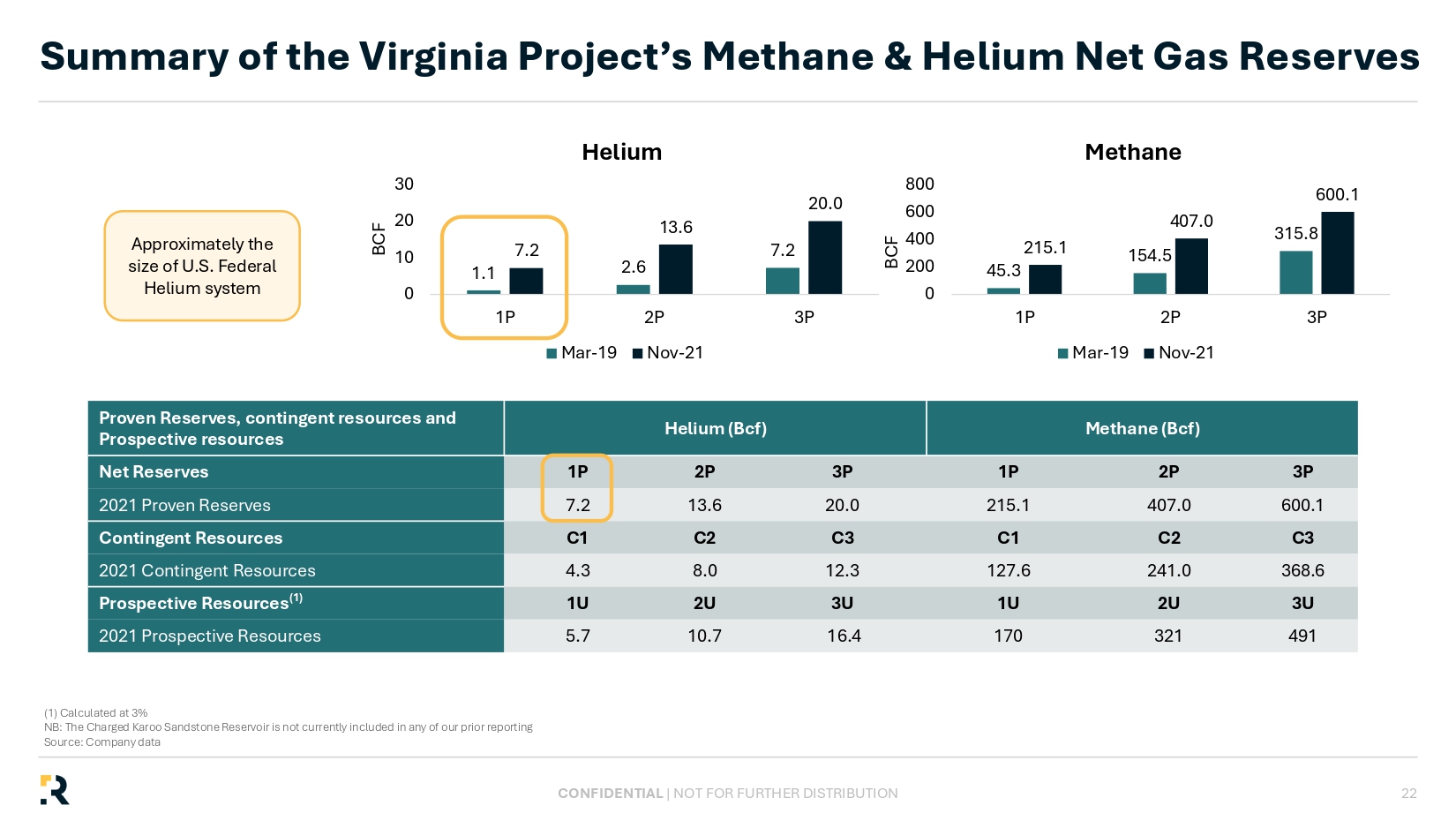

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION 45.3 154.5 315.8 215.1 407.0 600.1 0 200 400 600 800 1P 2P 3P BCF Mar-19 Nov-21 1.1 2.6 7.2 7.2 13.6 20.0 0 10 20 30 1P 2P 3P BCF Mar-19 Nov-21 Approximately the size of U.S. Federal Helium system Methane (Bcf) Helium (Bcf) Proven Reserves, contingent resources and Prospective resources 3P 2P 1P 3P 2P 1P Net Reserves 600.1 407.0 215.1 20.0 13.6 7.2 2021 Proven Reserves C3 C2 C1 C3 C2 C1 Contingent Resources 368.6 241.0 127.6 12.3 8.0 4.3 2021 Contingent Resources 3U 2U 1U 3U 2U 1U Prospective Resources (1) 491 321 170 16.4 10.7 5.7 2021 Prospective Resources Helium Methane 22 Summary of the Virginia Project’s Methane & Helium Net Gas Reserves (1) Calculated at 3% NB: The Charged Karoo Sandstone Reservoir is not currently included in any of our prior reporting Source: Company data

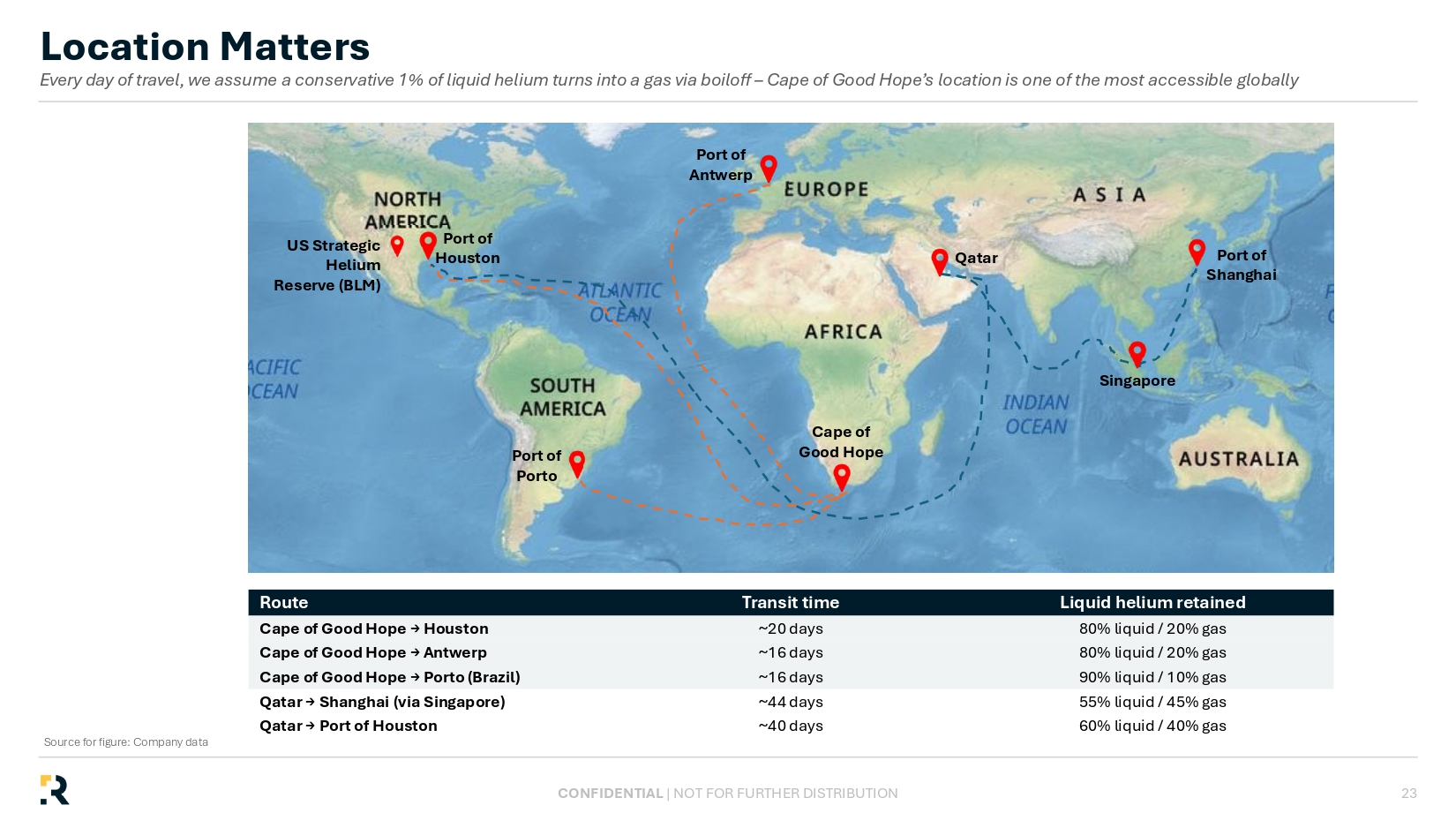

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Cape of Good Hope Port of Porto Port of Houston US Strategic Helium Reserve (BLM) Port of Antwerp Qatar Port of Shanghai Singapore Liquid helium retained Transit time Route 80% liquid / 20% gas ~20 days Cape of Good Hope → Houston 80% liquid / 20% gas ~16 days Cape of Good Hope → Antwerp 90% liquid / 10% gas ~16 days Cape of Good Hope → Porto (Brazil) 55% liquid / 45% gas ~44 days Qatar → Shanghai (via Singapore) 60% liquid / 40% gas ~40 days Qatar → Port of Houston 23 Location Matters Every day of travel, we assume a conservative 1% of liquid helium turns into a gas via boiloff – Cape of Good Hope’s location is one of the most accessible globally Source for figure: Company data

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Project Overview — Phase 1 and Phase 2

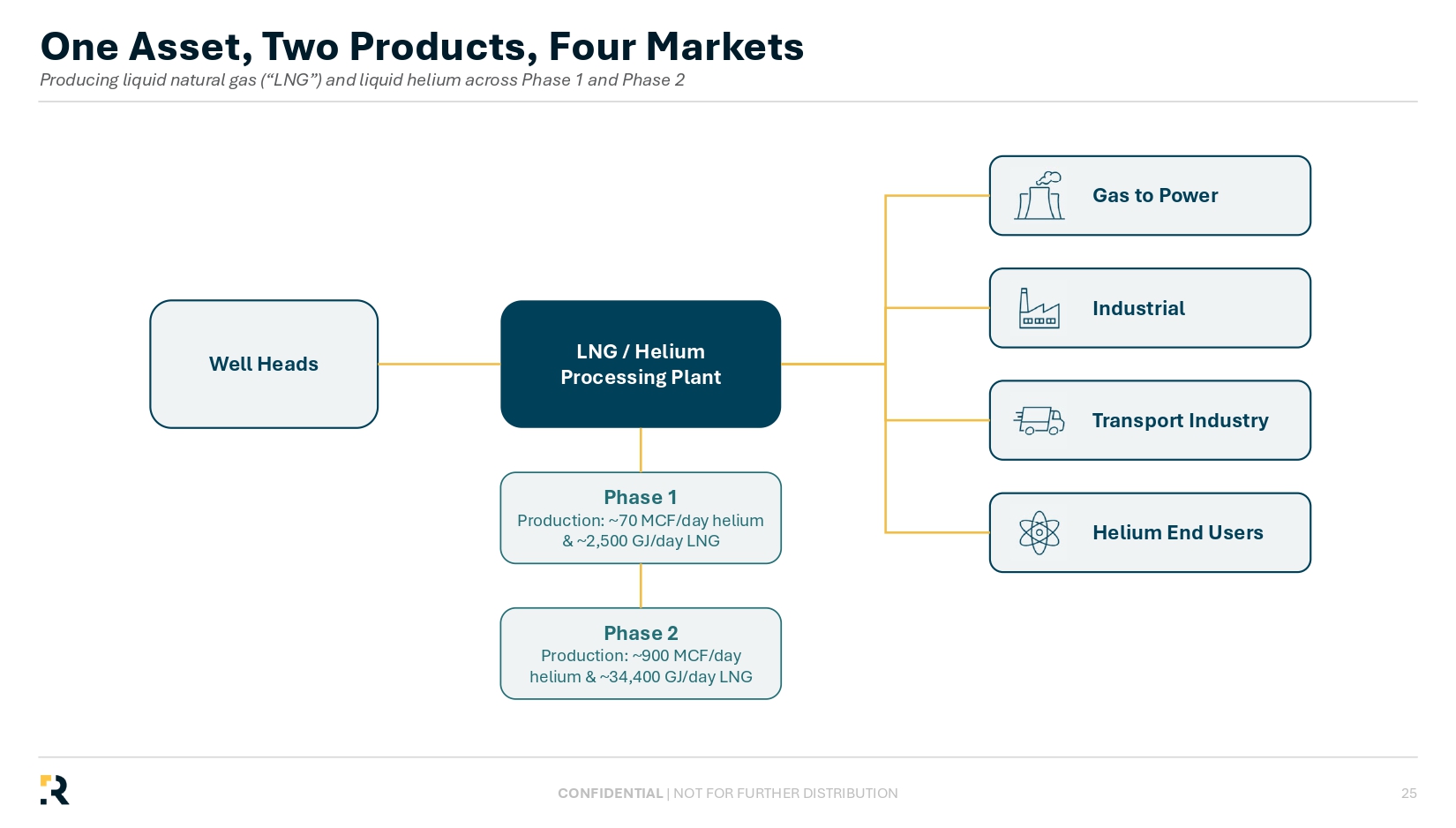

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION One Asset, Two Products, Four Markets Producing liquid natural gas (“LNG”) and liquid helium across Phase 1 and Phase 2 25 Well Heads Phase 1 Production: ~70 MCF/day helium & ~2,500 GJ/day LNG Phase 2 Production: ~900 MCF/day helium & ~34,400 GJ/day LNG LNG / Helium Processing Plant Gas to Power Industrial Transport Industry Helium End Users

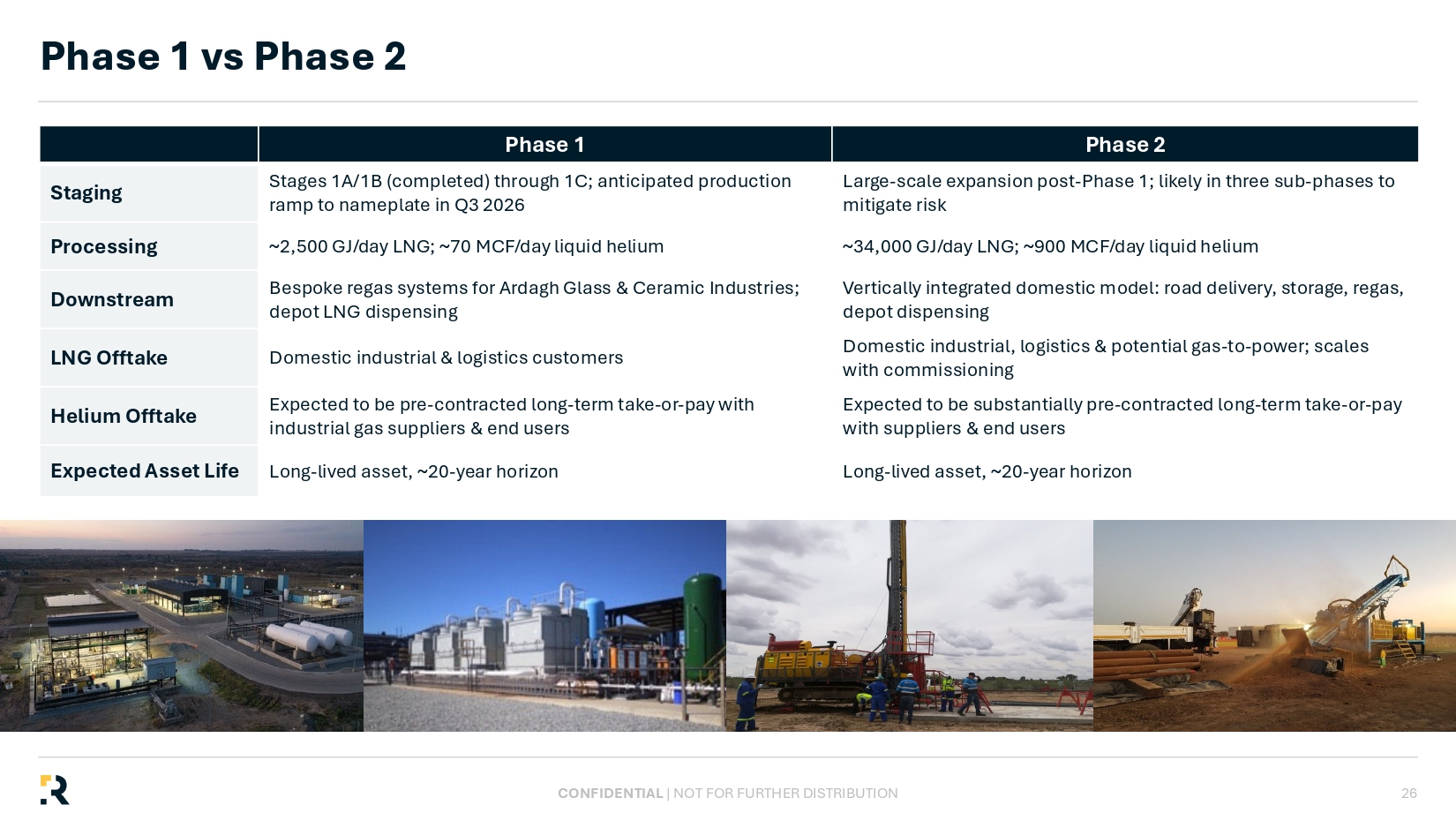

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Phase 2 Phase 1 Large - scale expansion post - Phase 1; likely in three sub - phases to mitigate risk Stages 1A/1B (completed) through 1C; anticipated production ramp to nameplate in Q3 2026 Staging ~34,000 GJ/day LNG; ~900 MCF/day liquid helium ~2,500 GJ/day LNG; ~70 MCF/day liquid helium Processing Vertically integrated domestic model: road delivery, storage, regas , depot dispensing Bespoke regas systems for Ardagh Glass & Ceramic Industries; depot LNG dispensing Downstream Domestic industrial, logistics & potential gas - to - power; scales with commissioning Domestic industrial & logistics customers LNG Offtake Expected to be substantially pre - contracted long - term take - or - pay with suppliers & end users Expected to be pre - contracted long - term take - or - pay with industrial gas suppliers & end users Helium Offtake Long - lived asset, ~20 - year horizon Long - lived asset, ~20 - year horizon Expected Asset Life 26 Phase 1 vs Phase 2

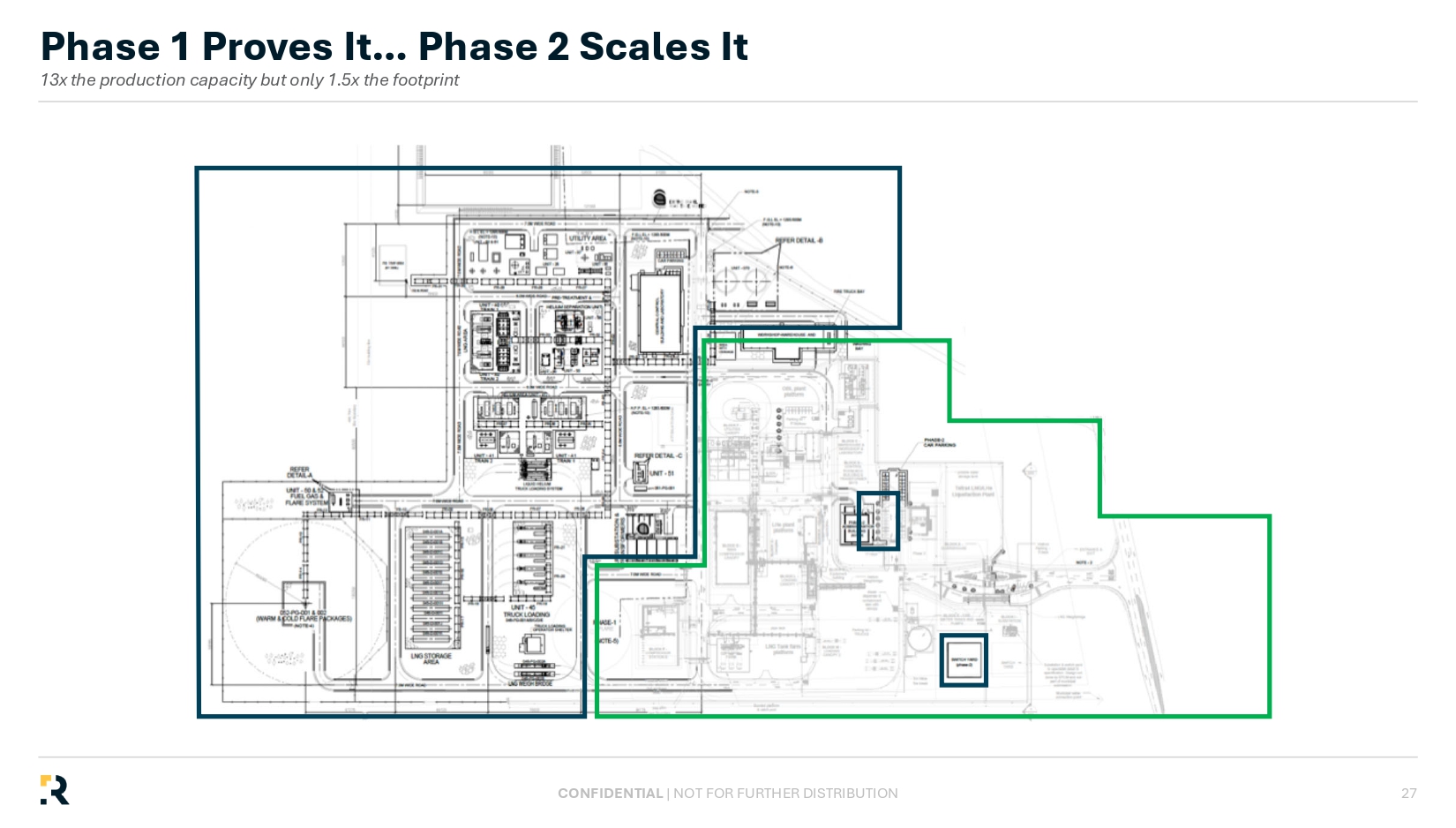

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Phase 1 Proves It… Phase 2 Scales It 13x the production capacity but only 1.5x the footprint 27

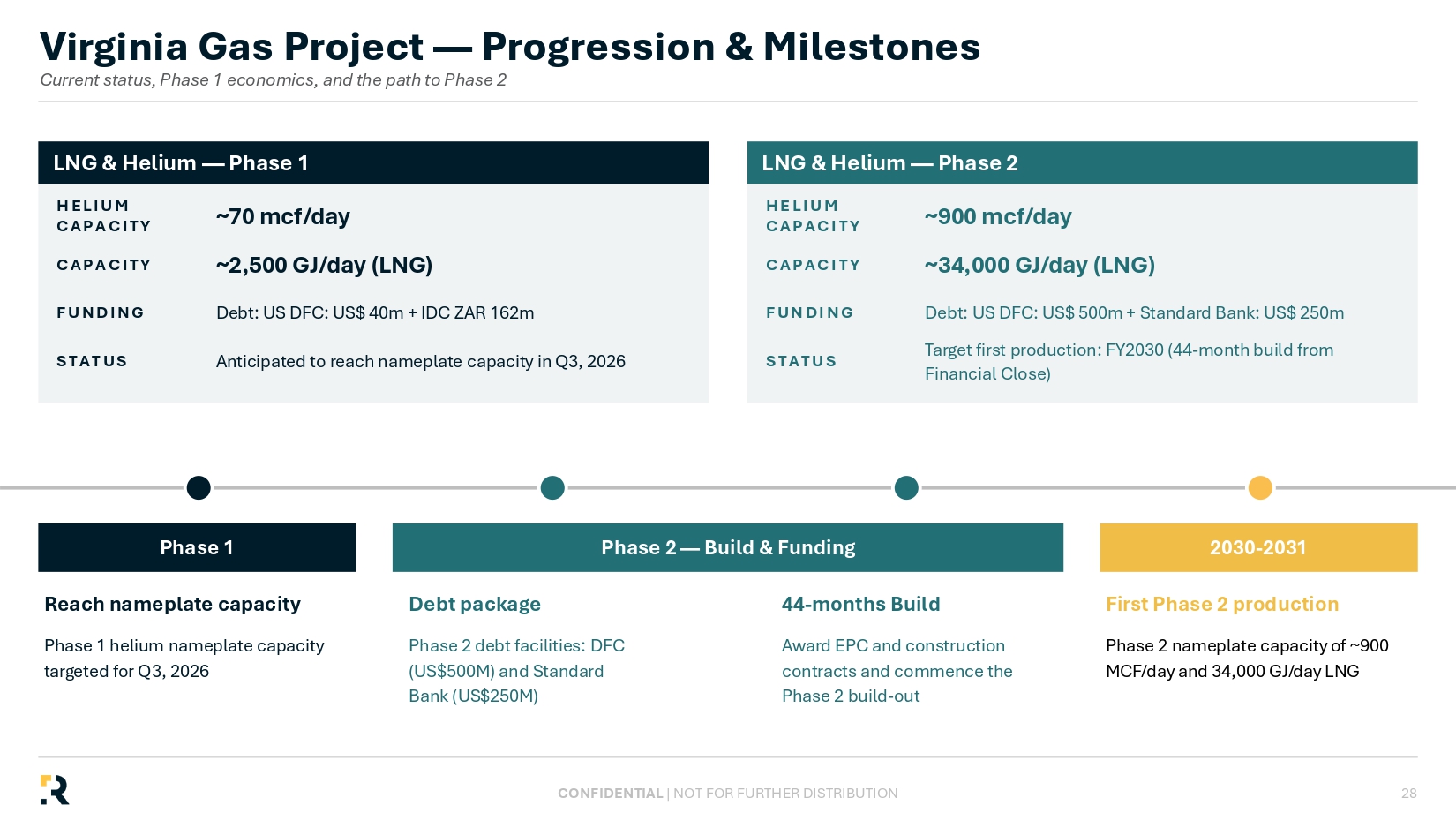

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION LNG & Helium — Phase 1 HELIUM CAPACITY ~70 mcf/day CAPACITY ~2,500 GJ/day (LNG) FUNDING Debt: US DFC: US$ 40m + IDC ZAR 162m STATUS Anticipated to reach nameplate capacity in Q3, 2026 LNG & Helium — Phase 2 HELIUM CAPACITY ~900 mcf/day CAPACITY ~34,000 GJ/day (LNG) FUNDING Debt: US DFC: US$ 500m + Standard Bank: US$ 250m STATUS Target first production: FY2030 (44 - month build from Financial Close) Phase 1 Reach nameplate capacity Phase 1 helium nameplate capacity targeted for Q3, 2026 Phase 2 — Build & Funding Debt package Phase 2 debt facilities: DFC (US$500M) and Standard Bank (US$250M) 44 - months Build Award EPC and construction contracts and commence the Phase 2 build - out 2030 - 2031 First Phase 2 production Phase 2 nameplate capacity of ~900 MCF/day and 34,000 GJ/day LNG Virginia Gas Project — Progression & Milestones Current status, Phase 1 economics, and the path to Phase 2 28

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION LNG Market Overview

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Transport (Rail) Transport (Long - haul) Industrial Thermal Energy - Intensive Electrical Power Users Natural Gas Users and Sectors 30

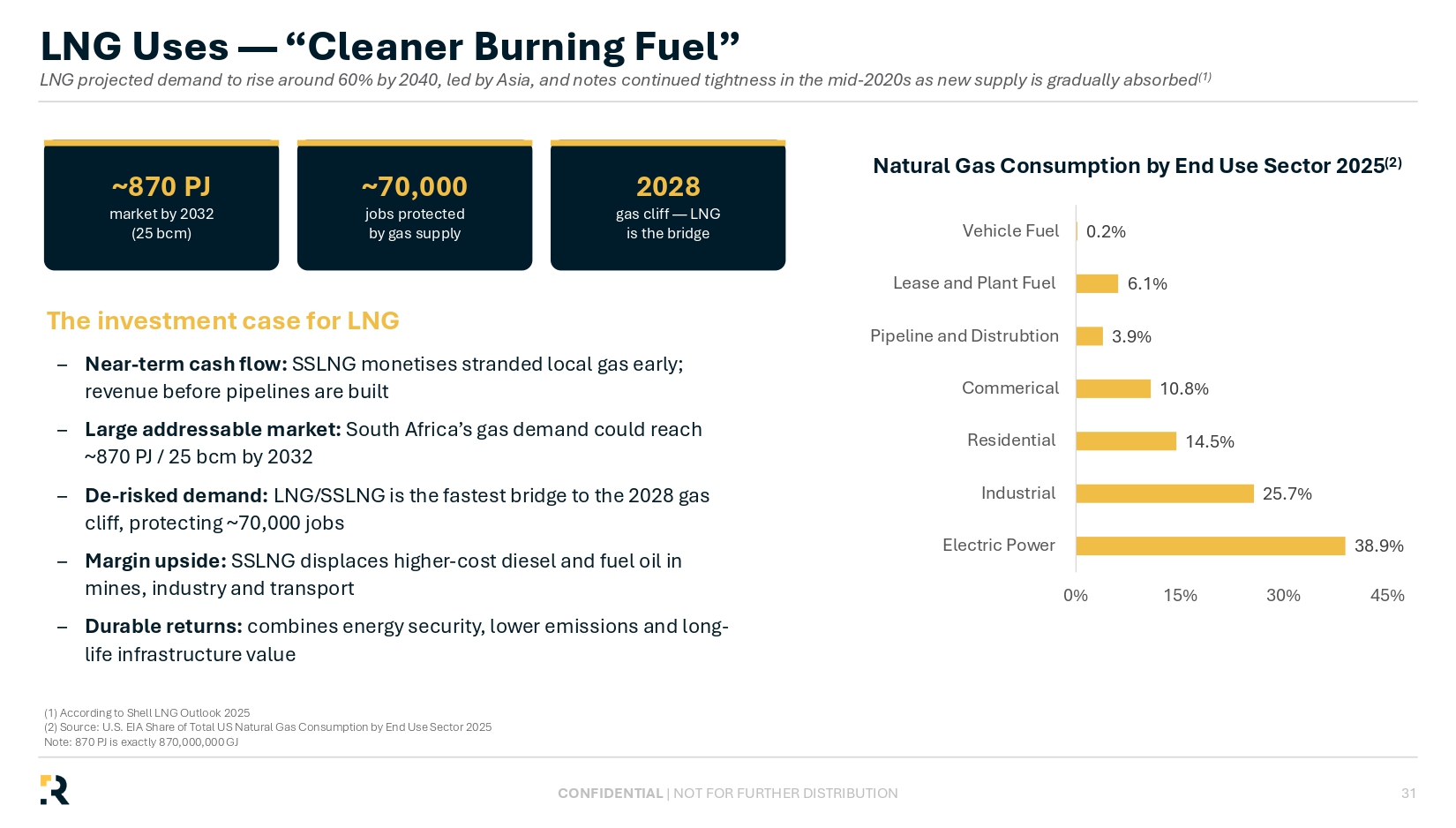

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION – Near - term cash flow: SSLNG monetises stranded local gas early; revenue before pipelines are built – Large addressable market: South Africa’s gas demand could reach ~870 PJ / 25 bcm by 2032 – De - risked demand: LNG/SSLNG is the fastest bridge to the 2028 gas cliff, protecting ~70,000 jobs – Margin upside: SSLNG displaces higher - cost diesel and fuel oil in mines, industry and transport – Durable returns: combines energy security, lower emissions and long - life infrastructure value The investment case for LNG Natural G as C onsumption by End Use Sector 2025 (2) 38.9% 25.7% 14.5% 10.8% 3.9% 6.1% 0.2% 0% 15% 30% 45% Electric Power Industrial Residential Commerical Pipeline and Distrubtion Lease and Plant Fuel Vehicle Fuel ~870 PJ market by 2032 (25 bcm) ~70,000 jobs protected by gas supply 2028 gas cliff — LNG is the bridge 31 LNG Uses — “Cleaner Burning Fuel” LNG projected demand to rise around 60% by 2040, led by Asia, and notes continued tightness in the mid - 2020s as new supply is gr adually absorbed (1) (1) According to Shell LNG Outlook 2025 (2) Source: U.S. EIA Share of Total US Natural Gas Consumption by End Use Sector 2025 Note: 870 PJ is exactly 870,000,000 GJ

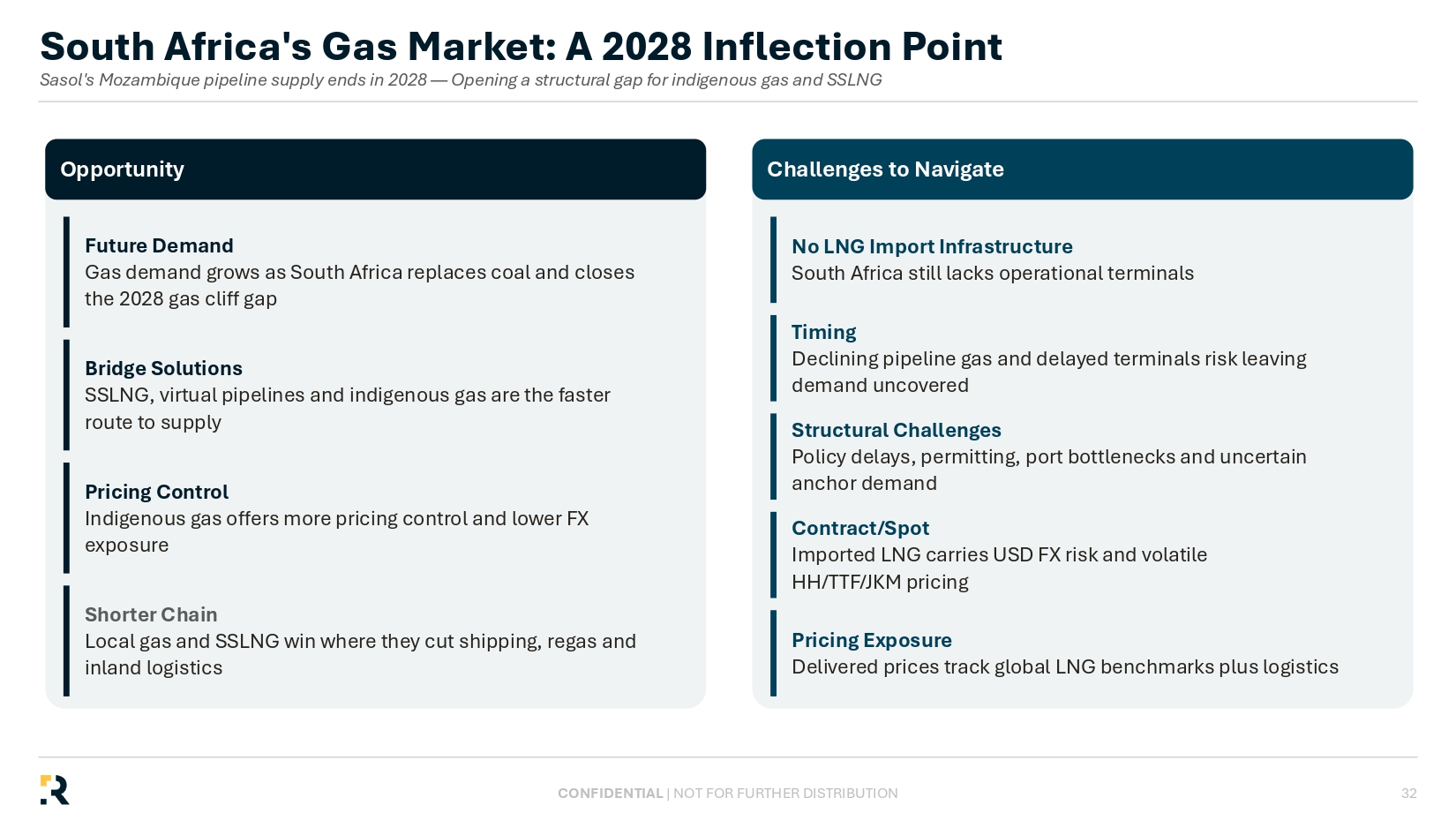

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Opportunity Future Demand Gas demand grows as South Africa replaces coal and closes the 2028 gas cliff gap Bridge Solutions SSLNG, virtual pipelines and indigenous gas are the faster route to supply Pricing Control Indigenous gas offers more pricing control and lower FX exposure Shorter Chain Local gas and SSLNG win where they cut shipping, regas and inland logistics Challenges to Navigate No LNG Import Infrastructure South Africa still lacks operational terminals Timing Declining pipeline gas and delayed terminals risk leaving demand uncovered Structural Challenges Policy delays, permitting, port bottlenecks and uncertain anchor demand Contract/Spot Imported LNG carries USD FX risk and volatile HH/TTF/JKM pricing Pricing Exposure Delivered prices track global LNG benchmarks plus logistics 32 South Africa's Gas Market: A 2028 Inflection Point Sasol's Mozambique pipeline supply ends in 2028 — Opening a structural gap for indigenous gas and SSLNG

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Target Milestones

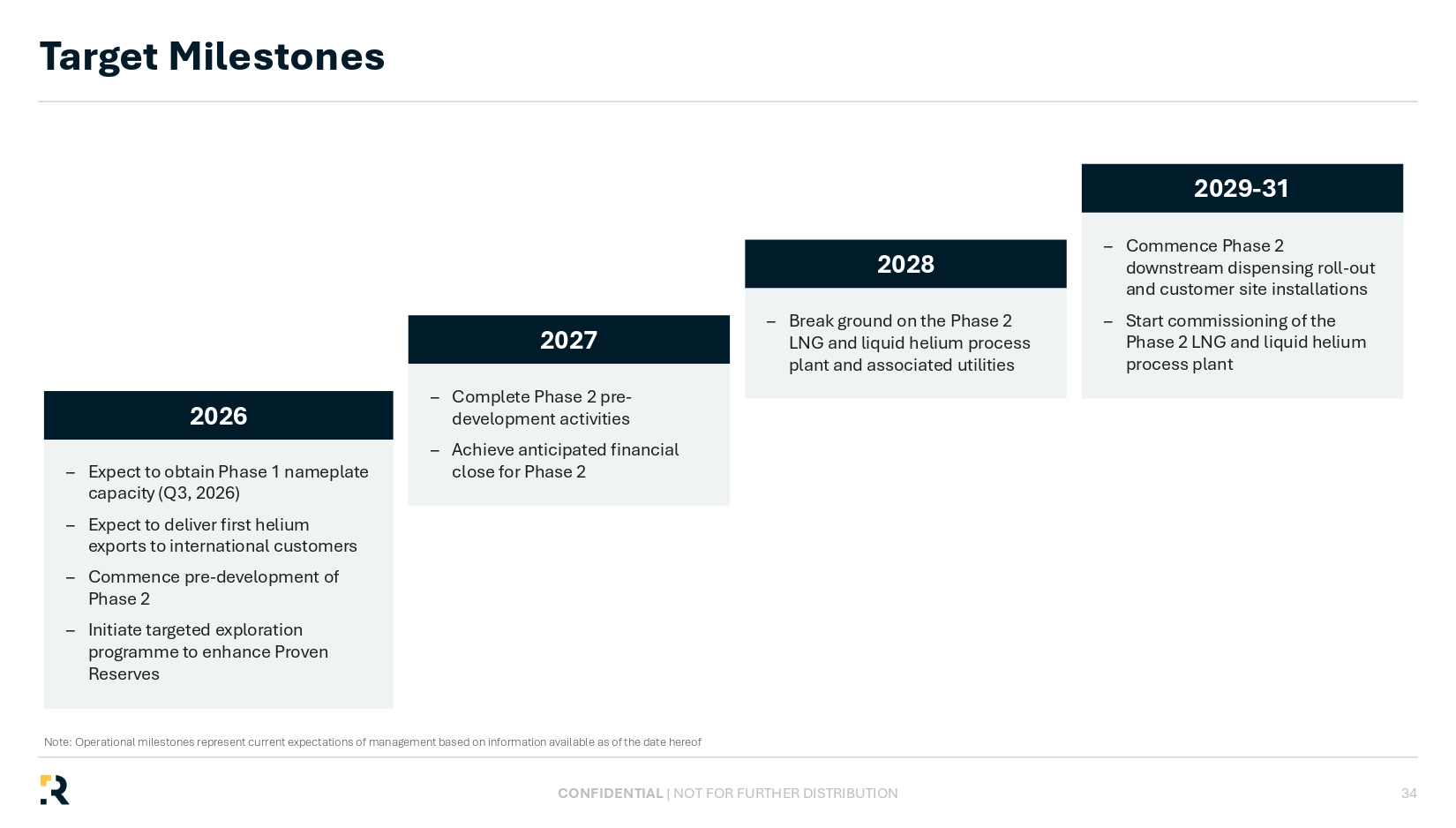

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION – Expect to obtain Phase 1 nameplate capacity (Q3, 2026) – Expect to deliver first helium exports to international customers – Commence pre - development of Phase 2 – Initiate targeted exploration programme to enhance Proven Reserves 2026 2027 2028 2029 - 31 Target Milestones 34 Note: Operational milestones represent current expectations of management based on information available as of the date hereo f – Commence Phase 2 downstream dispensing roll - out and customer site installations – Start commissioning of the Phase 2 LNG and liquid helium process plant – Break ground on the Phase 2 LNG and liquid helium process plant and associated utilities – Complete Phase 2 pre - development activities – Achieve anticipated financial close for Phase 2

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION The Virginia Gas Project is more than an energy play — it is a strategic supplier of two scarce and increasingly important products: helium for critical global industries and LNG for an energy - constrained South African market Investment is critical now: A first - mover advantage and an increasingly funded route to scale, at a time when both domestic gas security and global helium supply matter more than ever Rare Resource Base: Owns a rare, high - grade helium and LNG resource base in South Africa Non - Substitutable Demand: Supplies critical industries where helium is non - substitutable Energy Security: Supports domestic energy security through cleaner LNG supply De - Risked Scale - Up: Phase 2 funding materially de - risks the scale - up pathway Long - Duration Growth: offers long - duration growth from a strategic, hard - to - replicate asset Virginia Gas Project: A Strategic Helium & LNG Platform 35

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Appendix

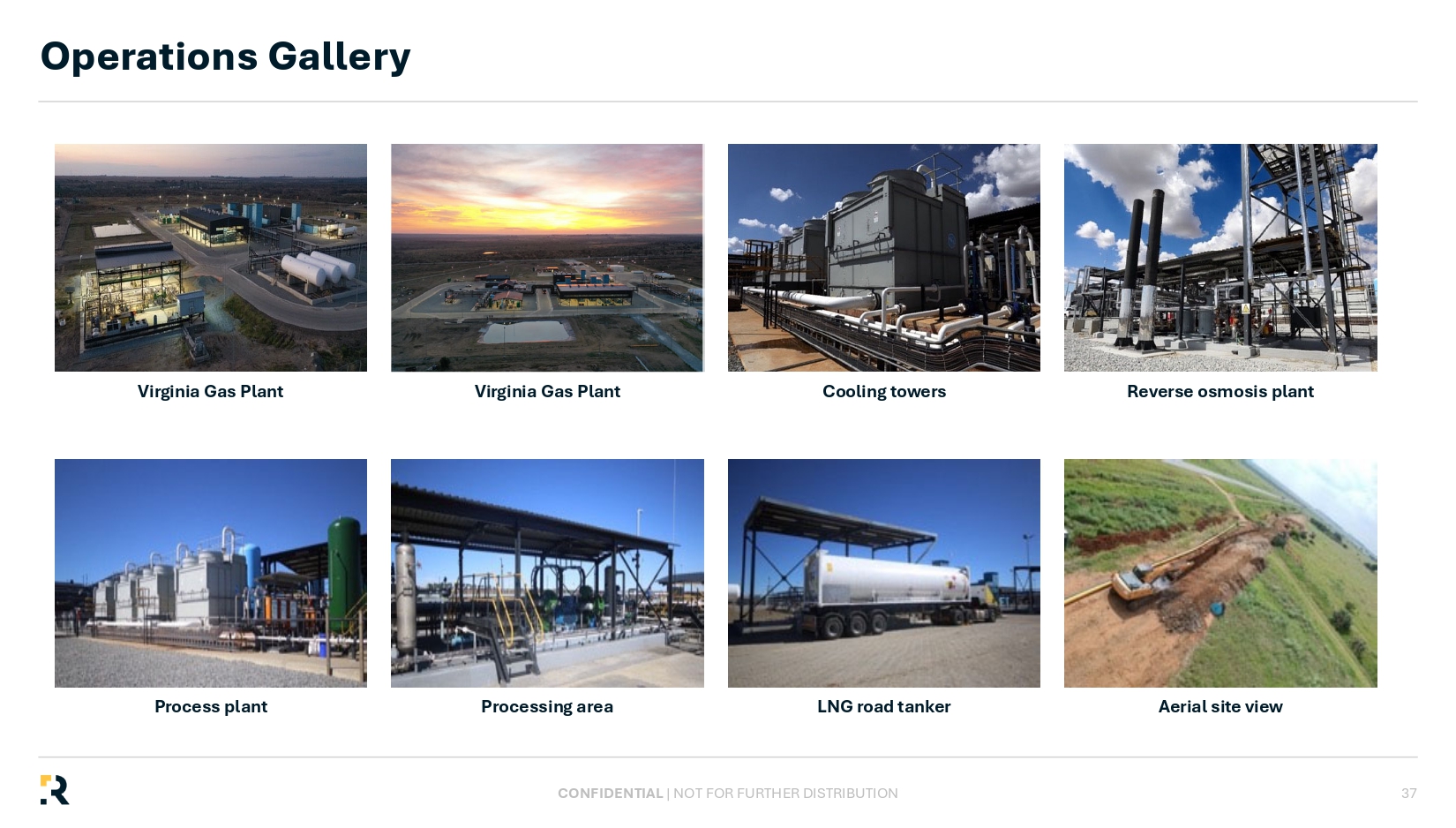

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Virginia Gas Plant Virginia Gas Plant Cooling towers Reverse osmosis plant Process plant Processing area LNG road tanker Aerial site view Operations Gallery 37

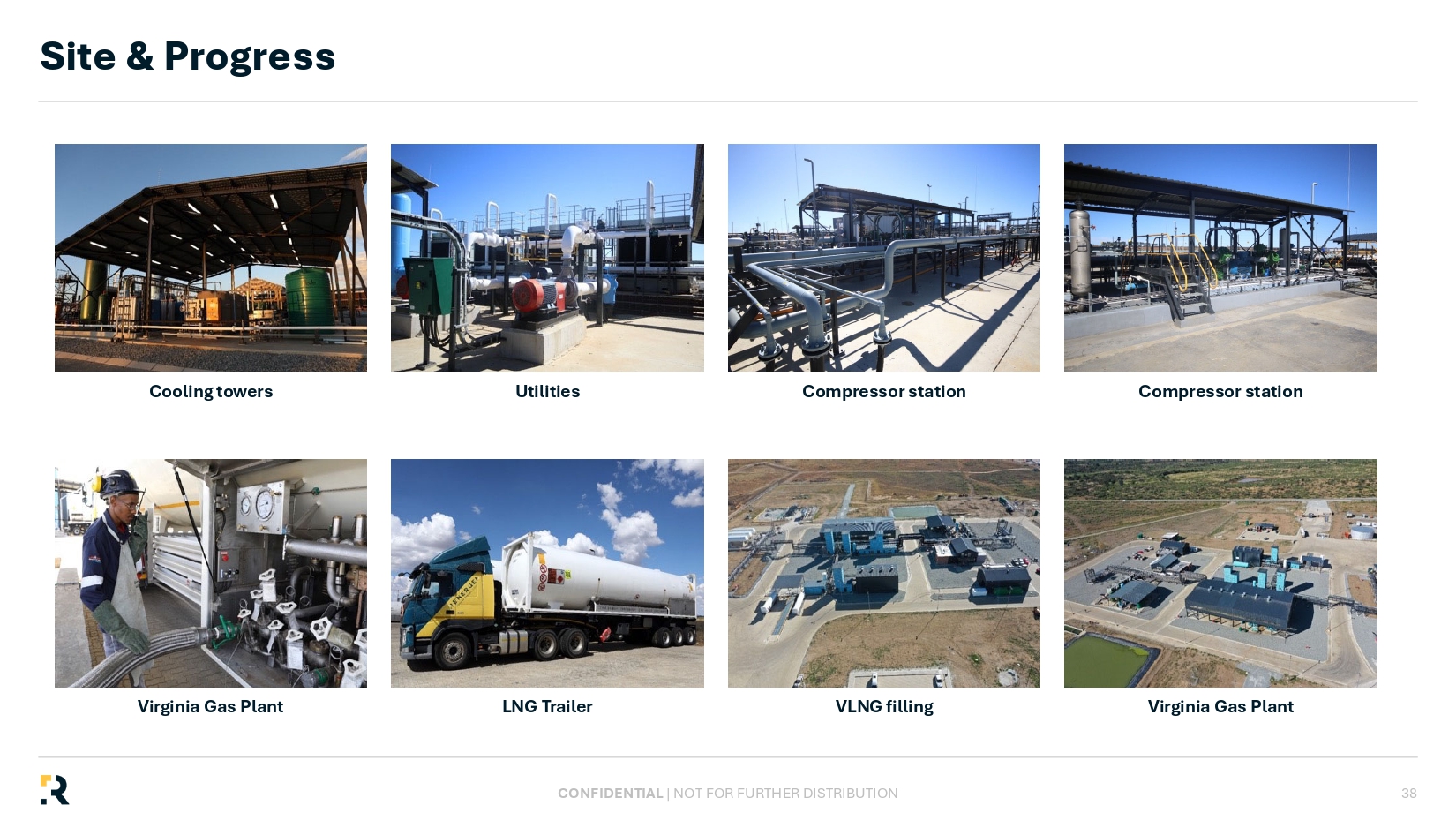

CONFIDENTIAL | NOT FOR FURTHER DISTRIBUTION Cooling towers Utilities Compressor station Compressor station Virginia Gas Plant LNG Trailer VLNG filling Virginia Gas Plant Site & Progress 38