Exhibit 99.3

ICON plc and Subsidiaries

Consolidated Financial Statements

Year ended 31 December 2025

Registered number: 145835

Directors’ Report and Consolidated Financial Statements

| | | | | |

| Contents | Page |

| |

| Directors and Other Information | |

| |

| Directors’ Report | |

| |

| Statement of Directors’ Responsibilities in respect of the Directors’ report and the financial statements | |

| |

| Independent Auditor’s Report to the Members of ICON plc | |

| |

| Consolidated Statement of Profit and Loss | |

| |

| Consolidated Statement of Comprehensive Income | |

| |

| Consolidated Statement of Financial Position | |

| |

| Consolidated Statement of Changes in Equity | |

| |

| Consolidated Statement of Cash Flows | |

| |

| Notes to Consolidated Financial Statements | |

| |

| Company Statement of Financial Position | |

| |

| Company Statement of Changes in Equity | |

| |

| Notes to Company Financial Statements | |

| |

| Reconciliation from IFRS to US Accounting Policies (Unaudited) | |

| |

| Appendix A: Risk Factors | |

Directors and Other Information

| | | | | |

| Directors | Ciaran Murray (Irish – Chair) |

| Barry Balfe (Irish – Chief Executive Officer) |

| Rónán Murphy (Irish – Non-Executive) |

| Dr. John Climax (Irish – Non-Executive) |

| Dr. Linda Grais (American – Non-Executive) |

| Eugene McCague (Irish – Non-Executive) |

| Julie O'Neill (Irish – Non-Executive) |

| Anne Whitaker (American – Non-Executive) |

| Kevin Egan (Irish – Non-Executive) |

| Jeff Elliott (American – Non-Executive) |

| |

| Company secretary | Diarmaid Cunningham |

| |

| Registered office | South County Business Park |

| Leopardstown |

| Dublin 18 |

| Ireland |

| |

Auditor | Ernst & Young |

| Harcourt Centre |

| Harcourt Street |

| Dublin 2 |

| Ireland |

| |

| Solicitors | A & L Goodbody |

| 25 North Wall Quay |

| Dublin 1 |

| Ireland |

| |

| White & Case LLP |

| 1221 Avenue of the Americas |

| New York |

| NY 10020-1095 |

| USA |

| |

| Registrars | Computershare Investor Services (Ireland) Limited |

| 3100 Lake Drive |

| Citywest Business Park |

| Dublin 24 |

| Ireland |

| |

Bankers | Citibank |

| Canada Square |

| Canary Wharf |

| London E14 5LB |

| United Kingdom |

| |

| JP Morgan Chase Bank N.A. |

| 383 Madison Avenue |

| New York |

| NY 10179 |

| USA |

The Directors present their report and audited consolidated and company financial statements of ICON plc (“the Company”, “ICON”, “we”, “our” or “us”), a public limited company incorporated in the Republic of Ireland, and its subsidiary undertakings (“the Subsidiaries”), with the Company and the Subsidiaries being together (“the Group”) for the year ended 31 December 2025.

The Company’s ordinary shares are traded on the NASDAQ Global Select Market (“NASDAQ”). The Company is considered a foreign private issuer in the U.S. and accordingly it is not subject to the same ongoing regulatory requirements as a U.S. registered company with a primary listing on NASDAQ.

These Consolidated and Company financial statements (together “the financial statements”) for the year ended 31 December 2025 are prepared in accordance with International Financial Reporting Standards as adopted by the European Union (“IFRS”) and meet the reporting requirements pursuant to Irish Company Law. In addition to the Consolidated financial statements contained in this annual report, we also prepare consolidated financial statements on Form 20-F pursuant to the rules and regulations of the U.S. Securities and Exchange Commission (“SEC”) and in accordance with accounting principles generally accepted in the United States (U.S. GAAP). The Form 20-F (under U.S. GAAP) is a separate document, a copy of which may be obtained from the Company’s website www.iconplc.com. IFRS differs in certain respects from U.S. GAAP, details of which are set out on pages 151 to 155 of this annual report.

The Investigation

In October 2025, the Audit Committee initiated an investigation into certain accounting practices and controls, following concerns reported to the Audit Committee through Group management. The Audit Committee promptly engaged outside legal counsel, who were supported by forensic and technical accounting firms, to conduct the investigation (the “Investigation”) and notified the Group’s independent auditors. The Group has also self-reported the matter to the SEC and other relevant agencies. The Investigation primarily focused on revenue recognition practices, and, in connection with the Investigation, the Group has determined that improper adjustments were made to the clinical trial services revenue of the Group in 2023 and 2024. The Group also identified errors in determining the estimated cost to complete, the assessment of realizable value, and certain manual adjustments in respect of clinical trial services revenue contracts during 2023 and 2024.

[Continued on next page]

Directors’ Report (continued)

The impact of the errors on the Consolidated Statement of Operations is shown below. For additional information refer to Note 1 Basis of preparation and statement of accounting policies - Restatement due to prior year adjustments in Notes to the Consolidated Financial Statements.

| | | | | | | |

| | |

| | 31 December

2024 | |

| | (in thousands, except per share data) |

| Revenue | | | |

| As Reported | | $ | 8,281,676 | | |

| As Restated | | $ | 8,188,990 | | |

| Impact | | $ | (92,686) | | |

| Impact % | | (1.1) | % | |

| | | |

| Profit for the financial year | | | |

| As Reported | | $ | 779,425 | | |

| As Restated | | $ | 727,077 | | |

| Impact | | $ | (52,348) | | |

| Impact % | | (6.7) | % | |

| | | |

| Earnings per share - Basic | | | |

| As Reported | | $ | 9.45 | | |

| As Restated | | $ | 8.81 | | |

| Impact | | $ | (0.64) | | |

| | | |

| Earnings per share - Diluted | | | |

| As Reported | | $ | 9.38 | | |

| As Restated | | $ | 8.75 | | |

| Impact | | $ | (0.63) | | |

| | | |

| | | |

The errors on the Consolidated Statement of Financial Position as at 31 December 2024 represent 1.4% of Total Assets; and of Total Equity & Liabilities.

The restatement errors does not affect cash flows or net debt.

Principal activities, business review and future developments

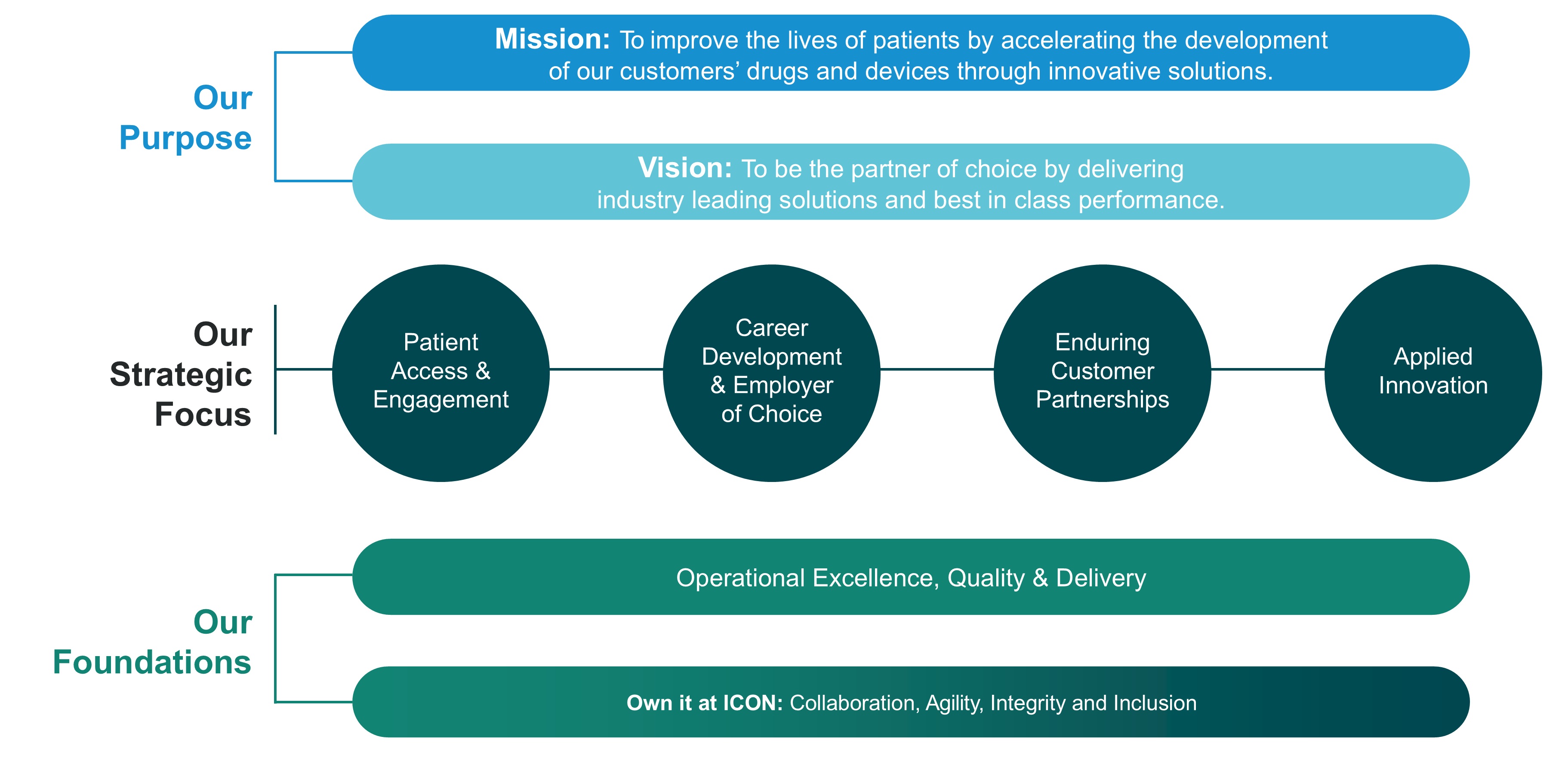

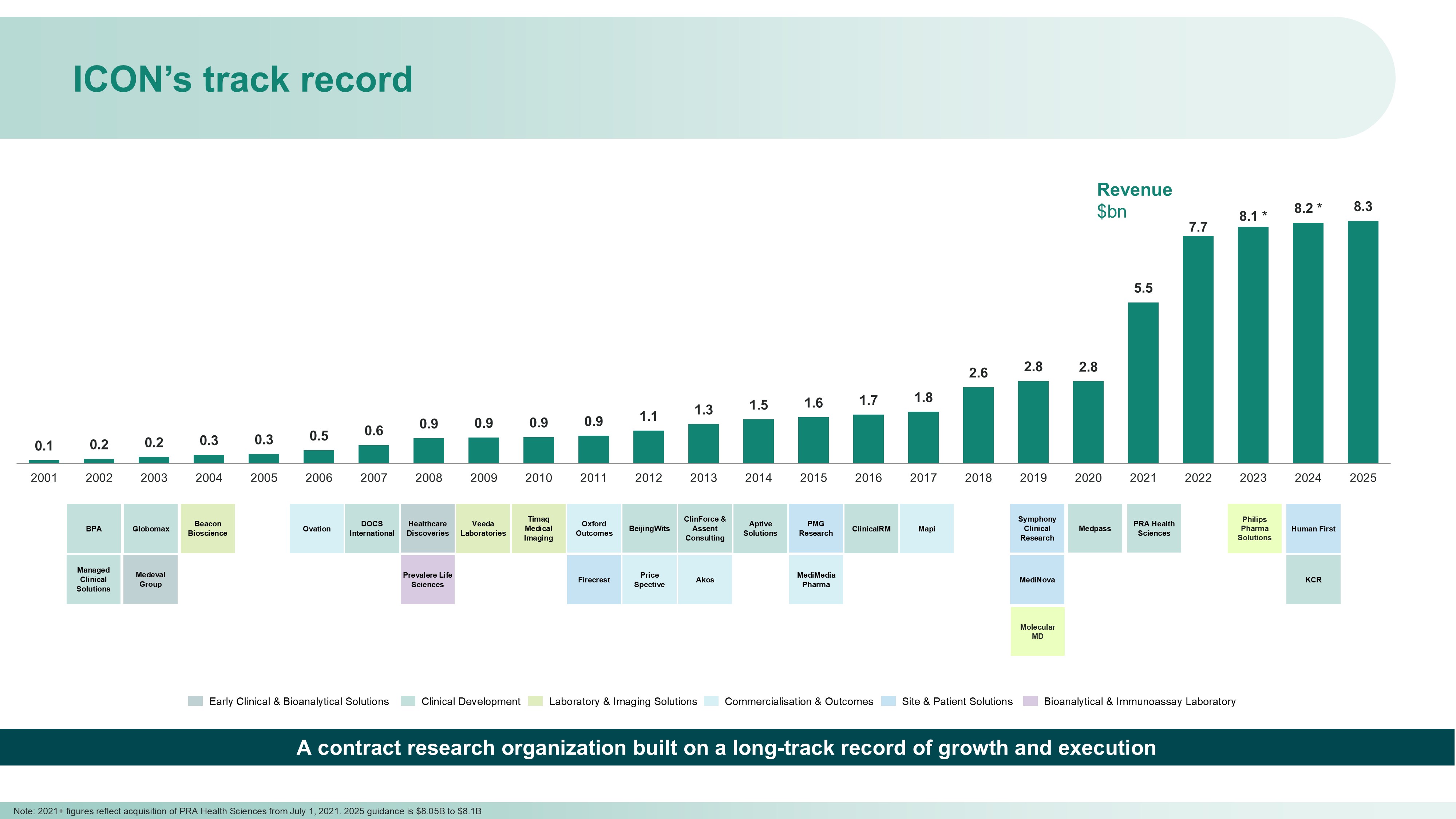

ICON is a contract research organisation (“CRO”), founded in Dublin, Ireland in 1990. For over thirty years we have grown significantly to become a global provider of outsourced development and commercialisation services to pharmaceutical, biotechnology, medical device and government and public health organisations. Our mission is to improve the lives of patients by accelerating the development of our customers’ drugs and devices through innovative solutions.

We are a public limited company in Ireland and operate under the Irish Companies Act. Our principal executive office is located at: South County Business Park, Leopardstown, Dublin 18, Republic of Ireland. The contact telephone number of this office is +353 1 2912000. Our website is www.iconplc.com.

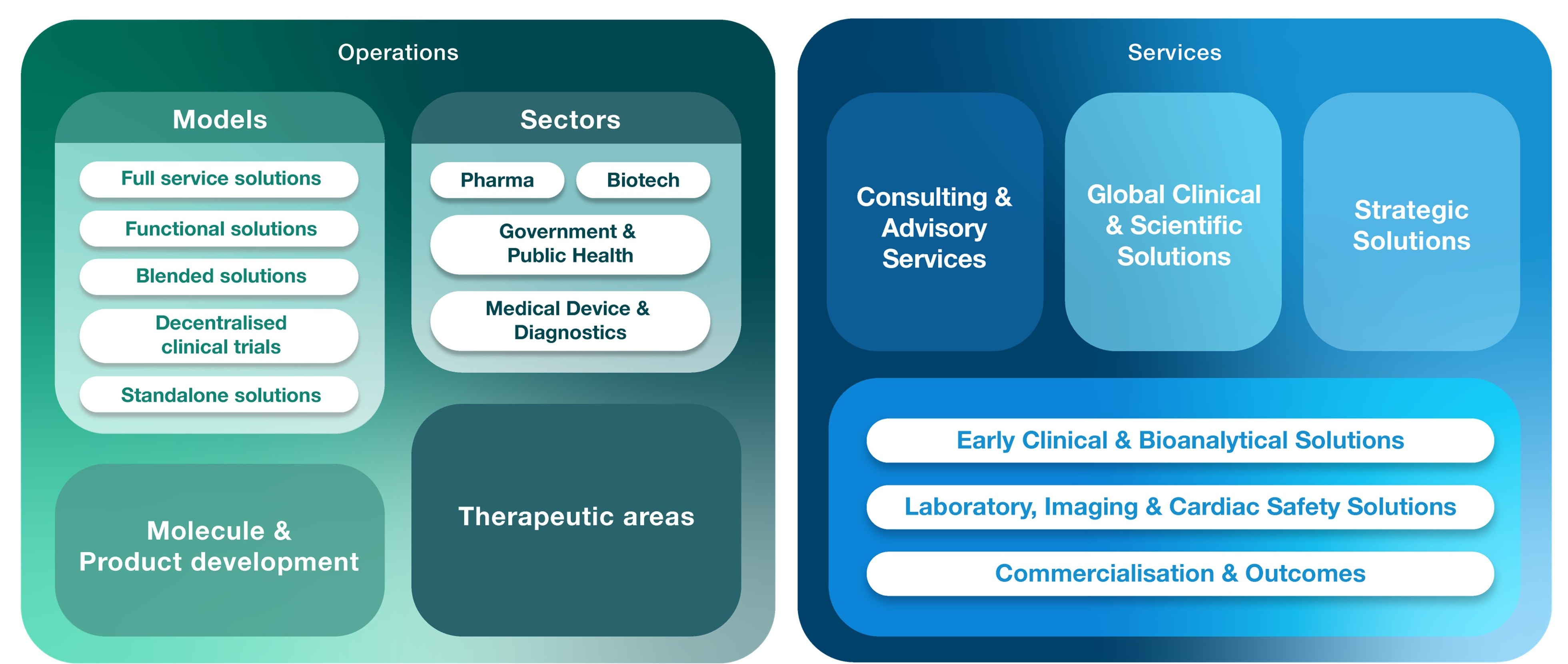

We offer a full range of clinical, consulting and commercial services that range from clinical development strategy, planning and trial design, to full study execution, and post-market commercialisation. ICON provides its services across a range of clinical outsourcing operating models including strategic partnerships, preferred provider, full-service delivery to functional service provision and stand-alone services.

Directors’ Report (continued)

We specialise in the strategic development, management and analysis of programmes that support all stages of the clinical development process, from compound selection to Phase I-IV clinical studies. We earn revenue by providing a number of different services to our customers. These services are integral components of the clinical development process and include clinical trial management, consulting, contract staffing, data solutions and laboratory services.

Our vision is to be the partner of choice by delivering industry leading solutions and best in class performance in clinical development. We believe that we are one of a select group of CROs with the expertise and capability to conduct clinical trials in the major therapeutic areas on a global basis and have the operational flexibility to provide development services on a stand-alone basis or as part of an integrated full-service solution. In order to achieve this vision, we continue to invest in technology and data analytics capabilities.

ICON maintains a sustained focus on research and development. We continue to enhance our portfolio of data solutions and decentralised clinical trial technology through the development of industry-leading technologies and processes to support our clients. ICON is leading the industry transformation through four key levers: transforming clinical trials, site and patient centricity, applied innovation, and seamless, integrated service delivery.

At 31 December 2025, we employed approximately 40,100 employees in 97 locations in 55 countries. During the year ended 31 December 2025, we derived 30.6%, 57.9% and 11.5% of our revenue in the United States, Europe and Rest of World, respectively.

We have achieved strong growth since our foundation in 1990. We focus our innovation on those factors that are critical to our clients - reducing time to market, reducing cost and increasing quality. Our global team has extensive experience in a broad range of therapeutic areas. ICON has been recognised as one of the world's leading Contract Research Organisations (“CROs”) through a number of high-profile industry awards (see www.iconplc.com/awards).

As our market has evolved, biopharmaceutical companies are tackling productivity challenges, budget constraints and greater demands to demonstrate product value; all of which are placing increased pressure on their revenues and levels of profitability. However, these trends have generally been positive for CROs, as increased outsourcing has been adopted by these companies as they seek to create greater efficiencies in their development processes, convert previously fixed costs to variable, and accelerate time to market for new treatments. We believe innovation in the biopharma sector has been fuelled by recent advances in technology, improving scientific profiles of drug targets, and increasing the pipeline of quality assets that can be investigated for further development. This provides biopharma companies an opportunity to strengthen their development pipeline with promising drug candidates, particularly those that are facing challenging patent expiries to their current marketed products.

Directors’ Report (continued)

We believe regulatory and reimbursement pressures will continue to necessitate expansion of late stage (post marketing) research, as increasing requirements to demonstrate the economic value of new treatments are expected. As a result, we believe outcomes and comparative effectiveness research will most likely be required in order to secure on-going product reimbursement. Furthermore, we believe advances in molecular biology and genetics will drive further growth in innovation in the long term, which in turn should create further growth opportunities for both biopharma companies and their outsourced development partners.

We expect that continued outsourcing will be a core strategy of clients in the near and mid-term as they seek to optimise their development operations and adopt models that allow for increased efficiencies. Larger clients were the first to form strategic partnerships with global CROs in an effort to reduce the number of outsource partners with whom they engage and to reduce inefficiencies in their current clinical development models. More recently, we have seen the increasing adoption of this reduced partner model with mid-tier pharmaceutical and biotechnology firms as they also recognise the value of strategic engagement with their development partners. As outsourcing penetration increases, we believe clients may seek a greater level of integration of service offerings from CROs, although some will continue to purchase services on a stand-alone basis. Creating greater connectivity and “seamlessness” between our services and the sharing of real-time clinical, operational and “real world” data with clients will therefore become increasingly important for CROs. ICON will seek to benefit from this increased outsourcing by clients to grow our business by increasing market share with our existing client base and adding new clients within the Phase I-IV outsourced development services market; the aim being to ensure we will be considered for all major Phase I-IV projects.

Delivery of our mission and strategy is focused on our four strategic pillars, being (i) Patient Access & Engagement (ii) Career Development & Employer of Choice (iii) Enduring Customer Partnerships and (iv) Applied Innovation.

Patient Access & Engagement

ICON has a focused patient, site and data strategy, which is helping us to improve site identification, study placement and patient recruitment and retention.

Accellacare is ICON's global clinical research network offering customers a wide range of stand-alone and integrated solutions at site or in patients' homes as part of decentralised trials. Our patient centric approach accelerates study start-up and increases patient recruitment and retention for the pharmaceutical, biotechnology and medical device industries.

Accellacare In-Home Services takes study visits directly to patients where they live, work, study or play in all phases and therapeutic areas of clinical trials. By bringing trial visits directly to patients, we ease the burden of participating in clinical research to increase patient recruitment and retention. Accellacare In-Home Services has experience in more than 500 clinical trials, tailoring our services to fit each study's specific requirements across more than 55 countries. This cohesive approach is leading to higher patient recruitment and retention rates. Accellacare is also achieving faster study start-up for its customers through efficiencies gained in central process management including budget and contracting, which can otherwise be a source of delay. This combined with a finely tuned feasibility approach allows the network to identify and recruit more patients to studies, in a wide range of therapeutic areas, in a shorter time frame. Accellacare is an important

Directors’ Report (continued)

part of the integrated patient, site and data strategy, helping us to improve patient recruitment and retention. Through Accellacare, we are committed to delivering on the promise of patient centricity in clinical research whilst also providing investigators with innovative treatments for their patients with a quality-focused clinical research infrastructure supported by experienced professionals globally.

Accellacare Site Resourcing supports sites to address resource constraints and/or barriers to participation due to a lack of resources. This includes supporting sites with patient recruitment, for example conducting database searches, liaising with referral departments and following up with patients referred from digital patient recruitment campaigns. Accellacare Site Resourcing can also support sites with resources throughout the clinical trial conduct, for example administration support, Electronic Case Report Form (“eCRF”) data entry and query resolution and database lock preparation. The Accellacare Site Resourcing team provides a range of resources from Clinical Research Coordinators, Clinical Research Nurses, Clinical Trial Educators and other specialised resources for example, dieticians required for obesity studies. Accellacare Site Resourcing can deploy resources to site in approximately 20 countries. Through Accellacare Site Resourcing we are committed to delivering highly qualified staff to investigator sites and enable site success in clinical trial participation, delivery and performance.

The Accellacare Site Network encompasses 21 owned/embedded sites across the US, UK and Spain as well as a number of collaboration agreements with other sites. Accellacare offers a quality focused clinical research infrastructure delivering value and benefits to sponsors. Accellacare supports customers with faster start-up and the time from site selection to site initiation visit when compared to other sites. Furthermore, Accellacare achieves on average more patients per site when compared to other sites.

In 2025, Accellacare Site Network further expanded its site partnerships and focused on enhancing capabilities within its US and UK locations with a continued focus on central nervous system (“CNS”) capabilities and oncology. This included onboarding 27 new investigators across therapeutic areas and a specific increase in oncologists at our Chicago location, providing access to 12 investigators focused on oncology.

The Elite Sites, ICON's dedicated programme for top-tier site networks, was designed to offer an infrastructure for those networks who have set themselves apart. These networks have been selected for their high-performance quality, consistency with faster start-up, and ability to meet or exceed recruitment commitments. With the use of ICON’s Elite Site programme, the aim is for clients to increase reliability with delivery, reduce site or country footprint, shorten overall study timelines and ultimately get drugs to market faster. ICON Elite Sites have been selected to align with a few key therapeutic areas – oncology, neurosciences, and gastrointestinal/ non-alcoholic steatohepatitis (NASH) in which these networks have shown the ability to be true differentiators for our clients and study teams. The ICON Elite Sites programme has a global reach, including 5 networks presently, and will continue to expand to best support our clients.

Finding and engaging suitable patients to conduct clinical trials is one of the biggest issues facing the drug development industry today. The performance of investigative sites that do take part in research is uneven, hard to predict and many trials do not meet the initial recruitment goals. The current market challenge in patient enrolment creates an opportunity for ICON to differentiate its service offering and we are working to reduce patient recruitment times through enhanced site and investigator selection based on key performance metrics and through use of our proprietary FIRECREST technology which is used to train and support sites during the development process.

ICON's site networks enhance our ability to enrol patients onto the clinical studies we perform. We have also developed strategic alliances with investigator site groups and healthcare systems in all major global research markets. In partnership with others, we are pioneering patient recruitment solutions that leverage cognitive computing to transform clinical trial matching and allow a data-driven approach to deliver the right patients for trials. One Search is our intuitive, integrated workflow and interrogation tool that enables access to multiple data sources and provides the visualisation and tools necessary for optimum site identification based on ICON and industry data of capability, experience and performance. Scoring on enrolment performance, speed of start-up and quality supports better site selection.

Career development and employer of choice

ICON is an award-winning workplace that enables our employees to make a difference to patients’ lives by being part of a world-class clinical research organisation that helps deliver new medicines & medical devices that are benefiting patients worldwide.

Our global team of 40,100 employees is united in purpose, working together in an inclusive environment to help solve some of the world’s most complex healthcare challenges. We value integrity, inclusion, collaboration and agility, which together form our ‘Own it’ culture that fosters innovative ideas and a vibrant workplace.

Our success depends on the knowledge, skills and calibre of our people. That’s why we are committed to developing a continuous learning culture – one where we challenge employees with engaging work and where every experience adds to their professional development.

Directors’ Report (continued)

Through our industry leading learning management system, internally developed professional development programmes and partnerships with leading academic institutions, employees are encouraged to broaden their scientific, technical and business knowledge.

With a strong emphasis on personal and professional development, ICON equips employees with the skills, knowledge and expertise to navigate and succeed in a dynamic work environment. Employees have access to tools that will help them develop the skills to support their career aspirations. At ICON, we provide growth opportunities for every stage of an employee’s career, empowering them to progress and reach new heights.

From training and development programmes to mentorship and coaching, we're committed to helping our employees reach their full potential.

Our Total Reward philosophy is designed to attract, retain, and motivate top talent by offering a holistic and competitive package that reflects our commitment to fairness, equity, and employee wellbeing.

We regularly benchmark our rewards to ensure our compensation and benefits remain competitive in the market. Our goal is to recognise and differentiate based on performance while maintaining a strong value proposition for our employees.

We are committed to pay practices that are transparent, consistent, and free from bias. Our commitment to achieving and maintaining fair pay is central to making ICON a truly inclusive workplace. Our approach ensures that employees are rewarded fairly for their skills, experience, and performance.

We prioritise the well-being of our employees. Across the world, our programmes include comprehensive health benefits, wellness initiatives, and resources that support work-life balance and resilience.

Through this philosophy, we aim to create an environment where employees feel valued, supported, and empowered to thrive both professionally and personally.

Enduring customer partnerships

We continue to focus on expanding and deepening our partnerships with existing customers, while also developing new customer relationships.

Strategic client relationships will increasingly manifest themselves in many different forms. Many of these relationships will require innovative forms of collaboration across ICON service areas and departments and will therefore require increased flexibility to offer services on both a standalone functional basis and as part of a fully integrated service solution. To support this objective, we continue to evolve our collaboration and delivery models, invest in technology that will enable closer data integration across our service areas and enhance our project and programme management capabilities.

To meet the evolving needs of both our existing and new clients we continue to enhance our capabilities through both organic service development and targeted acquisitions. In addition, we continue to enhance our scientific and therapeutic expertise to support our customers in specific areas including oncology, orphan and rare diseases, CNS, dermatology, infectious disease and women's health.

ICON has extensive experience in vaccine clinical development for commercial businesses, governments and NGOs. This experience enabled us to play a significant role in the search for vaccines and treatments for COVID-19.

We continue to target growth in under-penetrated CRO market segments. Penetration within medical device companies has lagged that of bio-pharma firms but is beginning to accelerate. EU regulatory reform enacted in 2017 is a further catalyst to growth in this segment as it included stricter requirements to perform clinical evaluations and post-sale surveillance. In early 2020, ICON acquired MedPass which has further enhanced our value offering in this area.

We also invested significantly in our site and patient network (Accellacare), and consider our expertise and offering in this area as one of our strategic pillars.

Applied innovation

At ICON plc, innovation is focused on the factors that are critical to our clients and patients. We develop and integrate technologies that significantly enhance the efficiency and productivity of drug and device development programmes, providing transparency across all areas of a study and improving the predictability of outcomes. Our approach combines best-in-class third-party platforms with a suite of differentiated proprietary solutions. Together, these enable smarter trial design and execution, faster and more reliable patient recruitment, and more patient-centric data collection and analysis, including the capture of digital health data directly from patients’ devices.

Directors’ Report (continued)

Operational excellence, quality and delivery

Quality is the foundation of our success. The quality of our work is vital to our mission of bringing better medications to patients around the world. We are committed to maintaining, supporting, checking and improving our quality systems to meet or exceed the quality standards demanded by our clients, patients and regulatory authorities. We focus our innovation on the factors that are critical to our clients – reducing time to market, reducing cost and increasing quality – and our global team of experts has extensive experience in a broad range of therapeutic areas.

Quality project execution underpins all that we do and we have an ongoing focus on developing our people and processes to continue to enhance our service delivery. We also deploy supporting technologies which we believe will enable faster and deeper insights into the quality of trial data.

We are focused on operational excellence across our support functions, and we operate a global business support infrastructure across functions including finance, information technology, facilities, human resources, legal and quality assurance. This enables us to enhance the service levels across these support areas whilst driving down the costs of the service provision.

Principal activities of the Company

The principal activity of the Company is to act as a holding Company. The Company also operates branch offices in Poland (Warsaw), Latvia (Riga), and a representative office in Lithuania (Vilnius), all of which provide contract research services to the pharmaceutical industry.

Acquisition activity

Since ICON was founded, the Group has expanded through organic growth, together with a number of strategic acquisitions to enhance its expertise and capabilities in certain areas of the clinical development process and to broaden the service portfolio and add scale to existing services.

Recent investments, which continue to strengthen our service offerings to meet the needs of our customers include:

On 19 August 2024, the Group acquired the KCR S.A Group (“KCR”), a CRO offering full service and functional services provision (“FSP”) clinical trial services. On 9 January 2024, the Group acquired HumanFirst, Inc. (“HumanFirst”), a life sciences technology company.

Directors’ Report (continued)

*Revenue figures for 2023 and 2024 have been adjusted for the Restatement.

Directors’ Report (continued)

Results and dividends

The results for the financial year and state of affairs of the Group are set out in the Consolidated Statement of Profit and Loss, the Consolidated Statement of Comprehensive Income, the Consolidated Statement of Financial Position, the Consolidated Statement of Changes in Equity and the Consolidated Statement of Cash Flows on pages 40 to 45 respectively. The Directors do not propose the payment of a dividend for the year ended 31 December 2025.

In the year ended 31 December 2025, the Group restated the prior year financial information. Details of the restatements are contained in Note 1 to the Consolidated Financial Statements.

The following table sets forth for the periods indicated certain financial data as a percentage of revenue and the percentage change in these items compared to the prior comparable period, being the key performance indicators used by management. The trends illustrated in the following table may not be indicative of future results.

| | | | | | | | | | | |

| 31 December

2025 | 31 December

2024

(As Restated) | Percentage increase/decrease |

| As a percentage of revenue | |

| Revenue | 100.0 | % | 100.0 | % | 0.8 | % |

| Costs and expenses | | | |

| Direct costs excluding exceptional items | 73.6 | % | 71.0 | % | 4.4 | % |

| Other operating expenses excluding exceptional items | 14.1 | % | 14.8 | % | (4.1) | % |

| Operating profit excluding exceptional items | 12.3 | % | 14.2 | % | (12.6) | % |

| Exceptional items: | | | |

| Transaction and integration related expenses | 0.3 | % | 0.4 | % | (14.6) | % |

| Restructuring expenses | 1.0 | % | 1.1 | % | (14.2) | % |

| Goodwill impairment | 4.5 | % | — | % | NM |

| Impairment of non-financial assets | 1.2 | % | — | % | NM |

| Provision for onerous contract | 0.1 | % | — | % | NM |

| Operating profit including exceptional items | 5.2 | % | 12.7 | % | (58.8) | % |

*NM - not meaningful

Twelve months ended 31 December 2025 compared to twelve months ended 31 December 2024 (As Restated)

Revenue

| | | | | | | | | | | | | | |

| 31 December

2025 | 31 December

2024

(As Restated) | Change |

| $’000 | $’000 | $’000 | % |

| Revenue | 8,251,340 | | 8,188,990 | | 62,350 | | 0.8 | % |

Revenue for the year ended 31 December 2025 increased by $62.4 million, or 0.8%, to $8,251.3 million, compared to $8,189.0 million for the year ended 31 December 2024. Revenue increased by 0.1% in constant currency terms.

For the year ended 31 December 2025, the Group derived approximately 30.6%, 57.9% and 11.5% of our revenue in the United States, Europe and Rest of World, respectively. Revenues from our top five customers amounted to $2,046.2 million in the year ended 31 December 2025 compared to $2,063.6 million in the year ended 31 December 2024 or 24.8% and 25.2% respectively. New customer accounts are continually added across the full portfolio of large pharma customers, mid-tier pharma customers and biotech customers.

Revenue in Ireland increased by $479.8 million for the year ended 31 December 2025, to $3,183.6 million, compared to $2,703.8 million for the year ended 31 December 2024. Revenue in Ireland during the year ended 31 December 2025 increased by 17.7% compared to an overall increase in Group revenue of 0.8%. Revenue in Ireland is principally a function of our global contracting model (see Note 2 Segmental information in Notes to the Consolidated Financial Statements).

Directors’ Report (continued)

Revenue in the Rest of Europe increased by $31.4 million or 2.0% for the year ended 31 December 2025, to $1,590.9 million in the year ended 31 December 2025, compared to $1,559.5 million for the year ended 31 December 2024. Revenue in the U.S. decreased by $458.2 million or 15.4% for the year ended 31 December 2025, to $2,524.9 million in the year ended 31 December 2025, compared to $2,983.1 million for the year ended 31 December 2024. Revenue in our Rest of World (‘Other’) region increased by $9.3 million or 1.0% for the year ended 31 December 2025, to $951.9 million compared to $942.6 million for the year ended 31 December 2024.

Direct costs

| | | | | | | | | | | |

| 31 December

2025 | 31 December

2024

(As Restated) | Change |

| $’000 | $’000 | $’000 |

| Direct costs | 6,076,286 | | 5,817,764 | | 258,522 | |

| % of revenue | 73.6 | % | 71.0 | % | 4.4 | % |

Direct costs for the year ended 31 December 2025 increased by $258.5 million or 4.4%, to $6,076.3 million from $5,817.8 million for the year ended 31 December 2024. Direct costs consist primarily of investigator and other reimbursable costs, compensation, associated fringe benefits and share based compensation expense for project-related employees and other direct project driven costs. The increase in direct costs for the year ended 31 December 2025 as compared to 31 December 2024, arose due to an increase in third party investigator / other reimbursable costs and laboratories partially offset by decreases in personnel related costs, and travel costs. As a percentage of revenue, direct costs have increased to 73.6% for the year ended 31 December 2025 compared to 71.0% for the year ended 31 December 2024.

Other Operating Expenses

| | | | | | | | | | | |

| 31 December

2025 | 31 December

2024 | Change |

| Other operating expenses excluding exceptional items ($'000) | 1,163,024 | | 1,212,972 | | (49,948) | |

| % of revenue | 14.1 | % | 14.8 | % | (4.1 | %) |

| Other operating expenses including exceptional items ($'000) | 1,747,976 | | 1,334,669 | | 413,307 | |

| % of revenue | 21.2 | % | 16.3 | % | 31.0 | % |

Other operating expenses (excluding exceptional items) for the year ended 31 December 2025 decreased by $49.9 million, or 4.1%, to $1,163.0 million compared to $1,213.0 million for the year ended 31 December 2024. Other operating expenses comprise primarily of compensation, related fringe benefits and routine share based compensation expense for non-project-related employees, recruitment expenditures, professional service costs, advertising costs, costs related to facilities and information systems, depreciation and amortisation. Further, costs incurred relating to the Investigation, including out of scope audit fees resulting from the impact of the Investigation, and in defence of the Putative Class Action (as referred to in Note 27 Litigation in Notes to the Consolidated Financial Statements) are classified within this category.

As a percentage of revenue, other operating expenses (excluding exceptional items) decreased to 14.1% of revenue for the year ended 31 December 2025, compared to 14.8% of revenue for the year ended 31 December 2024. The decrease in costs for the year ended 31 December 2025 primarily reflects decreases in amortisation of $110.6 million, decreases in professional fees, general and marketing costs of $22.3 million, offset by adverse foreign exchange movements ($39.3 million during the year ended 31 December 2025) and increases in facilities and depreciation cost of $19.1 million.

Directors’ Report (continued)

Exceptional items

Restructuring, transaction and integration-related expenses

| | | | | | | | | | | |

| 31 December

2025 | 31 December

2024 | Change |

| Transaction and integration related ($'000) | 25,269 | | 29,574 | | (4,305) | |

| % of revenue | 0.3 | % | 0.4 | % | (14.6) | % |

| Restructuring ($'000) | 79,069 | | 92,123 | | (13,054) | |

| % of revenue | 1.0 | % | 1.1 | % | (14.2) | % |

During the year ended 31 December 2025, the Group incurred $104.3 million for restructuring, transaction and integration-related expenses. The charge includes transaction and integration costs of $25.3 million associated with ongoing integration activities related to our recent acquisitions. Such costs include professional fees, legal costs and related integration costs.

The Group has also undertaken a restructuring programme aimed at realigning its workforce as well as reviewing its global office footprint and optimising its locations to best fit the requirements of the Group. This programme has resulted in a charge of $79.1 million in the year ended 31 December 2025. In the year ended 31 December 2024, a restructuring charge of $92.1 million was recognised. The restructuring plan reflects a workforce reduction of $74.6 million (31 December 2024: $74.5 million) and an office consolidation programme to optimise the Group's office footprint of $4.5 million (31 December 2024: $17.6 million).

Impairments & Provision for onerous contracts

| | | | | | | | | | | |

| 31 December

2025 | 31 December

2024 | Change |

| Goodwill impairment ($'000) | 367,587 | | — | | 367,587 | |

| % of revenue | 4.5 | % | — | | NM |

| Impairment of non-financial assets ($'000) | 101,027 | | — | | 101,027 | |

| % of revenue | 1.2 | % | — | | NM |

Provision for onerous contract ($'000) | 12,000 | | — | | 12,000 | |

| % of revenue | 0.1 | % | — | | NM |

During the year ended 31 December 2025, an impairment indicator was identified specific to the Group's Data Solutions reporting unit that indicated the carrying amount of the Data Solutions reporting unit may not be recoverable. This indicator related to the Group’s revised expectations on the future performance of the reporting unit considering specific external market participant factors.

As a result, the Group recorded a goodwill impairment charge of $367.6 million (31 December 2024: $nil) in the Consolidated Statements of Profit and Loss related to the Data Solutions reporting unit. This represented the entire balance of goodwill attributed to the Data Solutions reporting unit. This charge represents 4.5% of revenue for the year ending 31 December 2025. Impairment of non-financial assets of $101.0 million (31 December 2024: $nil) was recorded related to property, plant and equipment and intangible assets in the Data Solutions reporting unit. This charge represents 1.2% of revenue for the year ending 31 December 2025. Further the Group recorded a provision of $12.0 million (31 December 2024: $nil) for onerous contracts in respect of the Data Solutions reporting unit. This charge represents 0.1% of revenue for the year ending 31 December 2025.

Directors’ Report (continued)

Operating profit

| | | | | | | | | | | |

| 31 December

2025 | 31 December

2024

(As Restated) | Change |

| Operating profit excluding exceptional items ($'000) | 1,012,030 | | 1,158,254 | | (146,224) | |

| % of revenue | 12.3 | % | 14.2 | % | (12.6 | %) |

| Operating profit including exceptional items ($'000) | 427,078 | | 1,036,557 | | (609,479) | |

| % of revenue | 5.2 | % | 12.7 | % | (58.8 | %) |

Operating profit (excluding exceptional items) for the year ended 31 December 2025 decreased by $146.2 million, or 12.6%, to $1,012.0 million, compared to $1,158.3 million for the year ended 31 December 2024. As a percentage of revenue, operating profit (excluding exceptional items) for the year ended 31 December 2025 decreased to 12.3% compared to 14.2% for the year ended 31 December 2024.

Operating profit (including exceptional items) for the year ended 31 December 2025 decreased by $609.5 million, or 58.8%, to $427.1 million, compared to $1,036.6 million for the year ended 31 December 2024. As a percentage of revenue, operating profit (including exceptional items) for the year ended 31 December 2025 decreased to 5.2% compared to 12.7% for the year ended 31 December 2024.

Finance income and costs

| | | | | | | | | | | | | | |

| 31 December

2025 | 31 December

2024 | Change |

| $’000 | $’000 | $’000 | % |

| Finance income | 7,109 | | 8,609 | | (1,500) | | (17.4 | %) |

| Finance costs excluding exceptional items | (203,674) | | (242,616) | | 38,942 | | (16.1 | %) |

Finance costs decreased to $203.7 million for the year ended 31 December 2025 from $242.6 million for the year ended 31 December 2024. The decrease in the period reflects significant repayments of the Group's loan facilities in 2024, the repricing of the senior secured term loan facility and senior secured revolving credit facility in March 2024, and the impact of reduced interest rates on the New Notes issued in May 2024. Finance income for the year decreased to $7.1 million for the year ended 31 December 2025 from $8.6 million for the year ended 31 December 2024.

Income tax expense

| | | | | | | | | | | | | | |

| 31 December

2025 | 31 December

2024

(As Restated) | Change |

| Income tax expense excluding exceptional items ($'000) | 57,966 | | 96,749 | | (38,783) | | (40.1 | %) |

| Effective income tax rate (%) | 7.1 | % | 10.5 | % | | |

| Income tax expense including exceptional items ($'000) | 16,475 | | 75,473 | | (58,998) | | (78.2 | %) |

| Effective income tax rate (%) | 7.1 | % | 9.4 | % | | |

Income tax expense (including exceptional items) for the period decreased to $16.5 million for the year ended 31 December 2025 from $75.5 million for the year ended 31 December 2024. The Group’s effective tax rate (including exceptional items) for the year ended 31 December 2025 was 7.1% (7.1% excluding the effect of exceptional items) compared with 9.4% (10.5% excluding the effect of exceptional items) for the year ended 31 December 2024; primarily due to changes in various tax laws and the level of deferred tax benefit associated with the amortisation of intangible assets. With the exception of the foregoing, the Group's effective tax rate remains principally a function of the distribution of pre-tax profits amongst the territories in which it operates.

Risks and uncertainties

Under Irish Company Law (Section 327 of the Companies Act), the Directors are required to give a description of the principal risks and uncertainties which it faced at 31 December 2025. Details of the principal risks and uncertainties facing the Group are set out in Appendix A: Risk Factors of this annual report and form an integral part of the Directors’ Report.

Directors’ Report (continued)

Future developments

The Group looks forward to continuing to expand through organic growth, together with strategic acquisitions to enhance its expertise and capabilities in certain areas of the clinical development process and to continue to deliver on its mission to accelerate the development of drugs and devices that save lives and improve the quality of life.

Please see Note 29 Subsequent events in Notes to the Consolidated Financial Statements for details of events in the period from year-end to the approval of the financial statements.

Financial risk management

Group financial risk management is governed by policies and guidelines which are reviewed and approved annually by the Board of Directors. These policies and guidelines primarily cover foreign exchange risk, credit risk, liquidity risk and interest rate risk. The principal objective of these policies and guidelines is to ensure the minimisation of financial risk at reasonable cost. The Group’s financial instruments comprise cash and cash equivalents, current asset investments, lease obligations and negotiated debt facilities. The main purpose of these financial instruments is to fund the working capital requirements of the Group, the cost of new acquisitions and ensure continued growth. The Group also occasionally uses derivative financial instruments to reduce exposure to fluctuations in foreign exchange rates. The principal financial risk facing the Group is foreign exchange risk and interest rate risk (although interest rate risk is now limited: at 31 December 2025, 73% of the Group's outstanding debt was at a fixed interest rate (31 December 2024: 73%)). Other financial risks include credit risk and liquidity risk. Further details are set out in Note 24 Financial instruments in Notes to the Consolidated Financial Statements and Note 11 Financial instruments in Notes to the Company Financial Statements. The Group does not undertake any trading activity in financial instruments nor does it enter into any leveraged derivative transactions. The Group treasury function centrally manages the Group’s funding and liquidity requirements.

Financing

On 1 July 2021, the Group completed the acquisition of PRA Health Sciences, Inc. (“PRA”) by means of a merger whereby Indigo Merger Sub, Inc., a Delaware corporation and subsidiary of ICON, merged with and into PRA, the parent of PRA Health Sciences (the “Merger”). In conjunction with the completion of the merger, ICON entered into a credit agreement (the “Credit Agreement”) providing for a senior secured term loan facility of $5,515 million and a senior secured revolving loan facility in an initial aggregate principal amount of $300 million (the “Senior Secured Credit Facilities”).

In addition to the Senior Secured Credit Facilities, the Group issued $500 million in aggregate principal amount of 2.875% senior secured notes in a private offering (the “2026 Notes”). On 2 May 2023, the Group agreed with its lenders to increase the aggregate principal amount of the senior secured revolving loan facility from $300 million to $500 million.

The New Notes

On 8 May 2024, ICON Investments Six Designated Activity Company (the “Issuer”), a wholly-owned subsidiary of ICON plc, issued $2 billion senior secured notes (“the New Notes”). The New Notes were issued in aggregate principal amounts of: $750 million 5.809% Senior Secured Notes due 2027 (the “2027 Notes”), $750 million 5.849% Senior Secured Notes due 2029 (the “2029 Notes”) and $500 million 6.000% Senior Secured Notes due 2034 (the “2034 Notes”). The proceeds from the issuance were used to repay a portion of the senior secured term loan outstanding under the Senior Secured Credit Facilities and to pay fees, costs and expenses related to the offering.

Repricing - senior secured term loan facility

On 14 March 2024, the parties to the Credit Agreement entered into a Third Amendment to the Credit Agreement (the “Third Amendment”) in connection with the repricing of the senior secured term loan facility and the senior secured revolving credit facility (The Third Amendment in relation to the senior secured revolving credit facility was further amended by the Fourth Amendment as referred to below).

With respect to the senior secured term loan facility, the repricing culminated in a margin reduction of 25 basis points, from 2.25% (based on the then-current first lien net leverage ratio) to 2.0%; and the elimination of the credit adjustment spread. The combination of the above resulted in an overall reduction of 51 basis points on the senior secured term loan facility (assuming quarterly refixing).

Directors’ Report (continued)

Repricing and extension – senior secured revolving credit facility

On 26 November 2025, the parties to the Credit Agreement entered into a Fourth Amendment (the “Fourth Amendment”) to reprice and extend the senior secured revolving credit facility.

As a result of the Fourth Amendment, the maturity was extended from a five-year term to a seven-year term ending 1 July 2028. Reflecting the Fourth Amendment, the interest rate margin applicable to borrowings under the revolving loan facility will be, at the option of the borrower, either (i) the applicable base rate plus an applicable margin of 0.35% or 0.00%, based on the Company’s current corporate family rating assigned by S&P of BB (or lower) or BB+ (or higher), respectively, or (ii) Term SOFR plus an applicable margin of 1.35%, 1.00%, 0.75%, 0.55%, or 0.40% based on the Company’s current corporate family rating assigned by S&P of BB (or lower), BB+, BBB-, BBB or BBB+ (or higher), respectively. In addition, lenders under the revolving loan facility are entitled to commitment fees as a percentage of the applicable margin at the time of drawing and utilisation fees dependent on the proportion of the facility drawn.

Senior Secured Credit Facilities repayment

During the year ended 31 December 2025, the Group made mandatory principal repayments of $29.8 million (31 December 2024: mandatory and voluntary principal repayments of $2,304.8 million) of the senior secured term loan facility. There have been no voluntary repayments made during the year ended 31 December 2025. For the year ended 31 December 2024, voluntary repayments resulted in an accelerated charge associated with previously capitalised fees of $16.9 million.

In addition, during the year ended 31 December 2025, the Group drew $50.0 million (31 December 2024: $318.0 million) of the senior secured revolving loan facility and repaid $50.0 million (31 December 2024: $373.0 million). At 31 December 2025, $nil was drawn under the senior secured revolving loan facility (31 December 2024: $nil). Refer to Note 21 Bank credit lines and loan facilities in Notes to the Consolidated Financial Statements for further details on the Company's Senior Secured Credit Facilities.

Bridge Secured Credit Facility

On 27 April 2026, ICON Global Treasury Unlimited Company (the “Bridge Facility Borrower”) entered into a bridge facility credit agreement for an aggregate principal amount of $500 million (the "Bridge Secured Credit Facility"). The proceeds of the Bridge Secured Credit Facility may be used to discharge and repay in full $500 million aggregate principal amount of 2.875% Senior Secured Notes (the “2026 Notes”) issued by a subsidiary of the Group in July 2021. The Bridge Secured Credit Facility will mature on 26 April 2027.

The borrowings under the Bridge Secured Credit Facility do not amortise and are due at final maturity. The interest rate margin applicable to borrowings under the Bridge Secured Credit Facility is USD Term SOFR plus a fixed calendared applicable margin ranging from 1.00% to 2.25%. At 25 June 2026 , the applicable margin was 1.00%.

The Bridge Facility Borrower’s obligations under the Bridge Secured Credit Facility are guaranteed by ICON and the subsidiary guarantors party thereto. The Bridge Secured Credit Facility is secured by a lien on substantially all of the assets (subject to certain exceptions) of ICON, the Bridge Facility Borrower and each of the subsidiary guarantors, and the Bridge Secured Credit Facility will have a first-priority lien on such assets which will rank pari passu with the lien securing ICON’s other first lien secured indebtedness and is subject to other permitted liens. The Company is permitted to make voluntary prepayments under the Bridge Secured Credit Facility without premium or penalty (subject to customary break funding payments).

The Bridge Secured Credit Facility contains customary negative covenants, including, but not limited to, restrictions on the ability of ICON and its subsidiaries to merge and consolidate with other companies, incur indebtedness, grant liens or security interests on assets, pay dividends or make other restricted payments, sell or otherwise transfer assets or enter into transactions with affiliates.

The Bridge Secured Credit Facility provides that, upon the occurrence of certain events of default, the obligations under the credit agreement may be accelerated. Such events of default will include payment defaults to the lenders thereunder, material inaccuracies of representations and warranties, covenant defaults, cross-defaults to other material indebtedness, voluntary and involuntary bankruptcy proceedings, material monetary judgments, material pension-plan events, change of control and other customary events of default.

The Group has contractual liabilities for lease arrangements of $153.4 million which will be predominantly settled over the next five year period through cash payments.

Subsequent events

Details of subsequent events are set out in Note 29 Subsequent events in Notes to the Consolidated Financial Statements.

Directors’ Report (continued)

Directors and Company Secretary

The following table sets forth information concerning the composition of the Company’s Board and its committees as of 31 December 2025:

| | | | | | | | |

| Name | | Position |

| Ciaran Murray | | Chair and Director |

Barry Balfe (1)(5) | | Chief Executive Officer and Director |

| | |

Rónán Murphy (2)(3)(5) | | Lead Independent Director |

| Dr. John Climax | | Director |

| Dr. Steve Cutler | | Director |

Eugene McCague (3)(4) | | Director |

Julie O'Neill (2)(3) | | Director |

Dr. Linda Grais (2)(4) | | Director |

Anne Whitaker (4) | | Director |

| Diarmaid Cunningham | | Company Secretary |

(1)Named Executive Officer of the Company.

(2)Member of Compensation and Organisation Committee.

(3)Member of Audit Committee.

(4)Member of Nominating, Sustainability and Governance Committee.

(5)Member of Execution Committee.

On 4 September 2025, the Group announced that Chief Executive Officer (“CEO”), Dr. Steve Cutler, would retire from his role as CEO effective 1 October 2025 and Mr. Barry Balfe, ICON's Chief Operating Officer (“COO”), would succeed Dr. Cutler on that date. Mr. Balfe was also appointed to the Board of Directors effective 3 September 2025. Dr. Cutler resigned from the Board effective 21 May 2026.

Effective 1 June 2026, Mr. Kevin Egan and Mr. Jeff Elliott joined the Board of Directors.

Directors’ remuneration and interests

Details required by Companies Act, section 329, of Directors’ interests in the Group’s shares are set out in Note 10 Payroll and related benefits in Notes to the Consolidated Financial Statements.

Details of the Directors’ remuneration are set out in Note 6 Profit before taxation and Note 10 Payroll and related benefits in Notes to the Consolidated Financial Statements.

Directors’ authority to allot and purchase shares

Under the provisions of the Companies Act 2014 and the Company’s Constitution, the Directors are authorised to allot relevant securities, subject to approval by the shareholders of the Company in general meeting. Such authority is granted by ordinary resolution and is limited in amount and duration in accordance with applicable law. At each Annual General Meeting, shareholders renew the Directors’ authority to allot shares, to disapply statutory pre-emption rights, and to authorise the Company to purchase its own shares within specified limits.

On 18 February 2025, the Company's Board of Directors authorised an additional share repurchase programme under which the Company could acquire up to $750.0 million of the outstanding ordinary shares of the Company (by way of redemption). On 22 July 2025, the Company's Board of Directors authorised a further additional repurchase programme under which the Company could repurchase up to $500.0 million of the outstanding ordinary shares of the Company (by way of redemption).

During the year ended 31 December 2025, 4,504,330 ordinary shares were redeemed by the Company at an average price of $166.51 per share for a total consideration of $750.0 million. As of 31 December 2025, the Company has remaining authorisation (which includes unutilised amounts from previous authorisations) to repurchase up to $750.0 million of ordinary shares under the repurchase programme.

All ordinary shares that were redeemed under the repurchase programmes were cancelled in accordance with the constitution of the Company and the nominal value of these shares transferred to other undenominated capital as required by Irish Company law.

Further detail on the share repurchase programmes is included in Note 22 Share capital in Notes to the Consolidated Financial Statements.

Directors’ Report (continued)

Rights and Obligations attaching to the Company’s shares

The authorised share capital of the Company is €6,000,000 divided into 100,000,000 ordinary shares of €0.06 at 31 December 2025. Holders of ordinary shares will be entitled to receive such dividends as may be recommended by the Board of Directors of the Company and approved by the shareholders and/or such interim dividends as the Board of Directors of the Company may decide. On liquidation or a winding up of the Company, all assets available for distribution will be paid out to the holders of the Company's ordinary shares. Holders of ordinary shares have no conversion or redemption rights. On a show of hands, every holder of an ordinary share present in person or proxy at a general meeting of shareholders shall have one vote with no individual having more than one vote.

Change of control

A certain number of the Group’s customer contracts allow the customer to terminate the contract in the event of a change in control of the Group.

The Senior Secured Credit Facilities, details of which are set out in Note 21 Bank credit lines and loan facilities in Notes to the Consolidated Financial Statements, provides that, upon the occurrence of a change of control, the obligations thereunder may be accelerated.

The New Notes, details of which are set out in Note 21 Bank credit lines and loan facilities in Notes to the Consolidated Financial Statements, provides that, unless the Issuer has previously or concurrently delivered a redemption notice with respect to all the outstanding notes within 30 days following such Change of Control Triggering Event, the Issuer will make an offer to purchase all of the notes on the terms set forth in the indenture.

Furthermore, certain Group companies have entered capital grant agreements with the Irish government agency, Enterprise Ireland, whereby the Group covenants that the controlling interest in the Company will not change without Enterprise Ireland’s prior written consent, which will not be unreasonably withheld.

Additionally, the Company's share option and restricted share unit plans contain change in control provisions which provide for the acceleration of the vesting and exercisability of outstanding options and awards of restricted share units in the event that a change in control occurs with respect to the Company.

Corporate Governance

The Company is listed on the NASDAQ Global Select Market. The Company complies with the corporate governance listing requirements under the NASDAQ marketplace rules.

NASDAQ may provide exemptions from certain NASDAQ corporate governance standards to a foreign private issuer if, among other reasons those standards are contrary to a law, rule or regulation of a public authority exercising jurisdiction over such issuer or contrary to generally accepted business practices in the issuer’s home country of domicile, provided, that, the foreign private issuer properly notifies NASDAQ and makes the required disclosure except to the extent that such exemptions would be contrary to United States federal securities laws.

The exemptions that the Company relies on, and the practices the Company adheres to, are as follows:

•The Company is exempt from provisions set forth in NASDAQ Rule 5620(c), which requires each issuer (other than limited partnerships) to provide for a quorum in its by-laws for any meeting of the holders of common stock, which shall in no case be less than 33.33% of the outstanding shares of the issuer’s common voting stock. The Company’s Constitution requires that only 3 members be present, in person or by proxy, at a shareholder meeting to constitute a quorum. This quorum requirement is in accordance with Irish law and generally accepted business practices in Ireland.

•The Company is exempt from provisions set forth in NASDAQ Rule 5635(c) which requires (other than for certain specified exceptions) shareholder approval prior to the establishment or material amendment of a stock option or purchase plan or other equity compensation arrangement made or materially amended, pursuant to which stock may be acquired by officers, Directors, employees or consultants. Irish law does not require shareholder approval with respect to equity compensation arrangements. Accordingly, the 2019 Consultants and Directors Restricted Share Unit Plan, the 2013 Employees Restricted Share Unit Plan and the amendments to the Employee Share Option Plan 2008 and Consultants Share Option Plan 2008 were adopted by the Board of Directors without shareholder approval.

Directors’ Report (continued)

•The Company is exempt from provisions set forth in NASDAQ Rule 5605(b)(2), which requires independent Directors to hold regularly scheduled meetings at which only independent Directors are present. Irish law does not require independent Directors to hold regularly scheduled meetings at which only independent Directors are present. The Company holds regularly scheduled meetings which all of the Directors may attend and the Lead Independent Director may call meetings of the independent Directors and non-employee Directors of the Board, as appropriate, in accordance with the Lead Independent Director Charter.

The Company's practices with regard to these requirements are not prohibited by Irish law.

Audit Committee

The Audit Committee meets a minimum of four times a year. It reviews the quarterly and annual financial statements, the effectiveness of the system of internal control and recommends the appointment and removal of the external auditors. It monitors the adequacy of internal accounting practices and addresses all issues raised and recommendations made by the external auditors. The Audit Committee pre-approves all audit and non-audit services provided to the Company by its external auditors typically on an annual basis, with updates to such pre-approvals considered on a quarterly basis. Additional audit and non-audit services not covered by the annual or quarterly pre-approvals may be approved by the Audit Committee on a case-by-case basis. Between scheduled meetings, the Chair of the Audit Committee may pre-approve such services, which are subsequently reported to the full Audit Committee at its next meeting. The Audit Committee reviews all services which are provided by the external auditor to review the independence and objectivity of the external auditor, taking into consideration relevant professional and regulatory requirements. The Chief Financial Officer, the Head of Internal Audit, the Chief Administrative Officer and General Counsel and the external auditors normally attend all meetings of the Audit Committee and have direct access to the Committee Chairperson at all times. The Audit Committee is responsible for the oversight and monitoring of the external reporting on environmental, social and governance (“ESG”) matters included in the financial statements and data quality related to such reporting in coordination with the Nominating, Sustainability and Governance Committee. The Audit Committee is currently comprised of three independent Directors: Mr. Rónán Murphy (Chairperson), Mr. Eugene McCague and Ms. Julie O'Neill.

Significant shareholdings

The Company has been notified of the following shareholdings in excess of 3% of the issued share capital of the Company as at 31 December 2025:

| | | | | | | | |

| Name | % | Number of Shares |

| Artisan Partners Limited Partnership | 9.0 | | 6,873,977 |

| Wellington Management Group, LLP | 5.7 | | 4,350,750 |

| Orbis Investment Management Ltd. | 5.5 | | 4,208,000 |

| Invesco Ltd. | 4.9 | | 3,757,896 |

| FMR LLC | 4.0 | | 3,097,895 |

| Principal Financial Group Inc | 3.9 | | 3,001,535 |

| Ninety One UK Limited | 3.8 | | 2,945,810 |

| Harris Associates L.P. | 3.3 | | 2,510,166 |

All Directors, officers and other key employees as a group (1) | 1.2 | | 915,240 |

(1)Includes 373,437 ordinary shares issuable upon the exercise of stock options granted by the Company, 94,875 RSUs awarded by the Company to Directors, officers and other key employees and 36,358 PSUs awarded by the Company to Directors, officers and other key employees. Of the PSUs, performance conditions determine how many of them will vest and, if performance targets are exceeded, additional PSUs will be issued and vest in accordance with the terms of the relevant PSU award, the figure included is the maximum amount of PSUs that may be issued.

Further detailed breakdown of the Directors' interest is included in Note 10 Payroll and related benefits in Notes to the Consolidated Financial Statements.

Subsidiary undertakings

The information required by the Companies Act in relation to subsidiary undertakings is presented in Note 30 Subsidiary undertakings in Notes to the Consolidated Financial Statements.

Political donations

The Group made no disclosable political donations in the period.

Directors’ Report (continued)

Going concern

The time period that the Directors have considered in evaluating the appropriateness of the going concern basis in preparing the 31 December 2025 Consolidated Financial Statements is a period of at least twelve months from the date of approval of these financial statements (the “period of assessment”).

The Group has considerable financial resources and a large number of customers across different geographic areas. Having assessed the relevant business risks (see Appendix A: Risk Factors) the Directors believe that the Group is well placed to manage these risks successfully and they have a reasonable expectation that ICON plc, and the Group as a whole, has adequate financial and other resources to continue in operational existence for the period of assessment with no material uncertainties. For this reason, the Group continues to adopt the going concern basis in preparing the consolidated financial statements.

Accounting records

The Directors are responsible for ensuring that adequate accounting records as outlined in Section 281-285 of the Companies Act, are kept by the Company. The Directors are also responsible for the preparation of the Annual Report. The Directors have appointed professionally qualified accounting personnel with appropriate expertise and have provided adequate resources to the finance function in order to ensure that those requirements are met. The accounting records of the Company are maintained at the Group’s principal executive offices at its registered office at South County Business Park, Leopardstown, Dublin 18.

Statement of relevant audit information

The Directors believe that they have taken all steps necessary to make themselves aware of any relevant audit information and have established that the Company's statutory auditor is aware of that information. In so far as they are aware, there is no relevant audit information of which the Company's statutory auditors are unaware.

Disclosure of non-financial information

The European Union (Disclosure of Non-Financial and Diversity Information by certain large undertakings and groups) Regulations 2017 require disclosure of certain non-financial information by certain large undertakings and groups.

We have sought to address the requirements of the legislation in the sections following.

Business Model

Our mission is to improve the lives of patients by accelerating the development of our customers’ drugs and devices through innovative solutions. We are passionate about providing innovative solutions for customers. ICON is a values-driven company. We focus on agility, collaboration, inclusion and integrity in our work and interactions with our colleagues, suppliers, customers and patients. We are advancing clinical research while offering customers broader and deeper experience, scale, and focus, complemented by continuity of delivery and speed to market. Our business model is described in the “Principal activities, business review and future developments” section of the Directors’ Report. Consistent with our values, we seek to not only operate in compliance with applicable laws but also to positively influence our global workforce, the communities that we operate in, the environment and society as a whole. Doing so makes us a stronger, more resilient organisation by every measure.

Our core values underpin our mission and drive a culture and mind-set of ownership at ICON. “Own it at ICON”, is a statement of values that has remained at the very heart of ICON’s culture, encouraging our people to seize the opportunity and bring flexibility, innovation, and determination to every situation. We believe our culture of ownership personifies who we are as a company - it also helps us apply our expertise, collaborate to get things done, and succeed at our mission. Our values also underpin how we work together to deliver on our mission to improve the lives of patients by accelerating the development of our customers’ drugs and devices through innovative solutions. These values and our Code of Ethical Conduct, which underpins these values, form the core of what we do, and how we do it. It applies to all of our officers, directors, employees, consultants and agents globally. All employees and temporary workers are mandated to complete annual global ethics training and confirm they have read and understood the Code of Ethical Conduct.

At ICON, we care about conducting business sustainably. We care about our people, patients, and the communities in which we live. We care about doing the right thing and we are committed to working to the highest ethical standards and demonstrating our commitment to honesty, transparency, and quality. As a testament to our commitment, we launched our “ICON Cares” programme at the start of 2023 which incorporates all our Environment, Social and Governance (“ESG”) initiatives into one programme. ICON’s Environment, Social, and Governance Committee (“ESG Committee”) brings together all these initiatives and efforts under one umbrella to ensure consistency, enhance monitoring, reveal areas for development and facilitate reporting to the Board.

Directors’ Report (continued)

The Nominating, Sustainability, and Governance Committee of the ICON plc Board has oversight responsibilities in respect to ESG-related strategies and initiatives. The Chief Administrative Officer and General Counsel (“CAO”) chairs the ESG Committee and reports on ESG matters to the Nominating, Sustainability and Governance Committee regularly and reports to the Board at least annually whilst also providing periodic ESG updates to the executive leadership team. ICON’s ESG programme office reports to the CAO and delivers centralised reporting and tracking of ESG initiatives. The Audit Committee has oversight responsibilities in respect to ESG-related reporting in the ICON financial statements. The Chief Financial Officer (“CFO”) reports to the Audit Committee on ESG-related reporting matters.

The ESG Committee is focused on developing our strategy and initiatives relating to the environment, social matters, health and safety, community engagement, corporate governance, sustainability, and other public policy matters relevant to the Company. The ESG Committee is a cross-functional management committee of the Company including representation from facilities, health and safety, corporate communications, finance, legal, investor relations, procurement, commercial, marketing, and human resources departments. The Committee meets regularly to assist and support executive management and the Board and its committees in:

•determining and setting the strategy relating to ESG matters;

•developing, implementing and monitoring initiatives and policies based on that strategy;

•managing ESG related impacts, risks and opportunities; and

•communicating these strategies, initiatives, and their results.

We are committed to building and developing our ESG strategies and reporting. We maintain an ESG page on the external ICON website and have an internal ICON Cares ESG page on our MyICON intranet portal to engage with employees and provide information and updates relating to ESG matters and our commitment to sustainability. In 2021, as a testament to our commitment to managing ICON responsibly and sustainably, we became a participant in the United Nations Global Compact (“UNGC”), a set of Ten Principles covering the areas of human rights, labour, environment, and anti-corruption. In our 2024 ESG report, released in 2025, we reported under the Global Reporting Initiative (“GRI, 2021”) standards, the International Financial Reporting Standards (“IFRS”) S2 index and the Sustainability Accounting Standards Board (“SASB”) index. The report also outlines several ways in which ICON contributes to selected 2030 United Nations Sustainable Development Goals (“SDGs”) and associated targets. The ICON Cares Report summarises our current policies, priorities, commitments, achievements, and progress in respect to ESG matters. In 2026, ICON was awarded a Platinum medal by EcoVadis, achieving a score of 87/100. This represents an improvement on the Silver medal and score of 72/100 received in 2025 in recognition of our environmental, social and governance performance and management efforts across the organisation.

The global landscape in respect to regulatory and legislative requirements relating to ESG reporting and disclosure requirements is rapidly evolving, and we are monitoring potential requirements so that we are positioned to adhere to any additional requirements in due course. This includes mandatory reporting under the Corporate Sustainability Reporting Directive (“CSRD”) from the EU and under the International Financial Reporting Standards (“IFRS”) S1 and S2 standards.

Building a sustainable future – our commitment to the United Nations Sustainable Development Goals

As a global company, we maintain an ethical and sustainable presence in hundreds of locations worldwide. At its core, ICON’s mission is to improve health and lives. We are also committed to contributing to the 2030 United Nations SDGs and are proud that our work contributes to their advancement.

Our research, our work with customers and patients and our on-the-ground efforts to meet the needs across our communities align with the SDGs. We focus these efforts on a subset of themes where we have identified the greatest opportunity to effect change:

•SDG 3 – Good health and well-being

•SDG 9 – Industry, innovation and infrastructure

•SDG 10 – Reduced inequalities

•SDG 12 – Responsible consumption and production

•SDG 13 – Climate action

•SDG 17 – Partnerships for the goals

Further details on the ways ICON contributes to these SDGs and their targets are set out in our ICON Cares Report.

Directors’ Report (continued)

Environment: Conducting business sustainably

ICON is committed to delivering excellence in care to our communities. To improve our overall sustainability, this commitment means tracking and improving our environmental performance across all business activities. We achieve this by pursuing sustainability strategies that recognise the impact of our operations as a CRO on the environment, addressing greenhouse gas (“GHG”) emissions, energy use, waste generation and procurement-related activities. Our employees, directors, officers, contractors, temporary workers, and suppliers are expected to support our sustainability objectives. Similarly, ICON endeavours to support our customers’ sustainability objectives.

Our Global Environmental Management Policy and Environmental Management Plan are part of our ICON Cares programme for managing environmental sustainability initiatives. They define our approach to managing environmental impacts and set goals and targets to reduce energy use and carbon emissions throughout the business. Our Global Environmental Management Policy articulates ICON’s commitment to environmental stewardship, regulatory compliance and climate action across our operations and supply chain. It establishes ICON’s ambition to achieve net‑zero carbon emissions by 2050 and outlines focus areas including energy efficiency, waste reduction, sustainable travel, responsible Policy mandate Risk assessment Targets Measurement procurement, renewable energy adoption and Scope 1, 2 and 3 emissions tracking, aligned with leading reporting frameworks. The implementation of the policy and plan is led by our facilities team, reporting to our CAO. The CAO is responsible for reporting on the ICON Cares programme and environmental initiatives and progress to the ICON executive leadership team and Nominating, Sustainability and Governance Committee and the Board.

ICON established environmental targets in 2019 focused on renewable energy usage and energy consumption reduction. These targets included achieving 100% renewable electricity by 2025 and a 20% reduction in electricity consumption (kWh) by 2030. In 2025, ICON achieved 97% renewable electricity usage. The remaining 3% reflects limitations in procuring credible Energy Attribute Certificates (“EACs”) due to geopolitical disruptions and regional market constraints in certain jurisdictions, specifically Russia, Belarus, Ukraine, Georgia, and Estonia.

In October 2024, the Science Based Target initiative (“SBTi”) validated ICON’s near- and long-term science-based emissions reduction targets. The SBTi has also verified ICON’s net-zero science-based target (“SBT”) by 2050. The SBTi is a corporate climate action organisation that enables companies and financial institutions worldwide to play their part in combating the climate crisis. ICON’s SBTi validated targets:

Near-term targets:

•Reduce absolute scope 1 and 2 GHG emissions 61.2% by FY2028 from a FY2019 base year.

•Reduce absolute scope 3 GHG emissions 20.0% by FY2028 from a FY2022 base year.

Long-term targets:

•Reduce absolute scope 1 and 2 GHG emissions 90.0% by FY2050 from a FY2019 base year.

•Reduce absolute scope 3 GHG emissions 90.0% by FY2050 from a FY2022 base year.

Net-zero target:

•Reach net-zero greenhouse gas emissions across the value chain by FY2050.

We have programmes in place to manage and minimise climate impacts of business activities. To continue to improve processes and reduce our environmental impact, we track, calculate, and report our Scope 1, Scope 2 and Scope 3 GHG footprint. We apply the GHG Protocol Corporate Accounting and Reporting Standard, which is the global corporate accounting and reporting standard for calculating carbon emissions. External verification of our 2025 Scope 1, 2 and 3 GHG emissions data is currently in progress. During 2024, we began our 2022 and 2023 Scope 3 emissions foot printing, incorporating this into our annual emissions reporting.