Bright Rock Capital Management LLC

COMPLIANCE MANUAL

Written Policies and Procedures referenced to the Investment Company Act and Advisor Act.

Revised August 2024

I. Code of Ethics

A) Standard of Conduct

B) Confidential Information

C) Material Inside Information

D) Fiduciary Duty and Conflicts of Interest

E) Scalping or Frontrunning

F) Unfair Treatment of Certain Clients Vis-a-Vis Others

G) Dealing with Clients as Agent and Principal: Section

206(3) of the Investment Advisers Act of 1940

H) Personal Trading; Timely Reporting of Trades

I) Social Media Policy

J) Political Contribution Policy

K) Employee’s Responsibility to Know the Rules and Comply with Applicable Laws

L) Designation and Responsibilities of Chief Compliance Officer

M) Disclosure of Portfolio Holdings

N) Code of Ethics Records

II. Portfolio Management

A) Trade Allocation and Aggregation Policy and Procedures

B) Consistency with Client Objectives and Restrictions and Legal Mandates

C) Proxy Voting

D) Trading Errors

E) Cross Trades

F) Market Timing and Rule 22c-2 Procedures

G) Liquidity Risk Management Program

H) Derivatives

I) 12D-1 Compliance

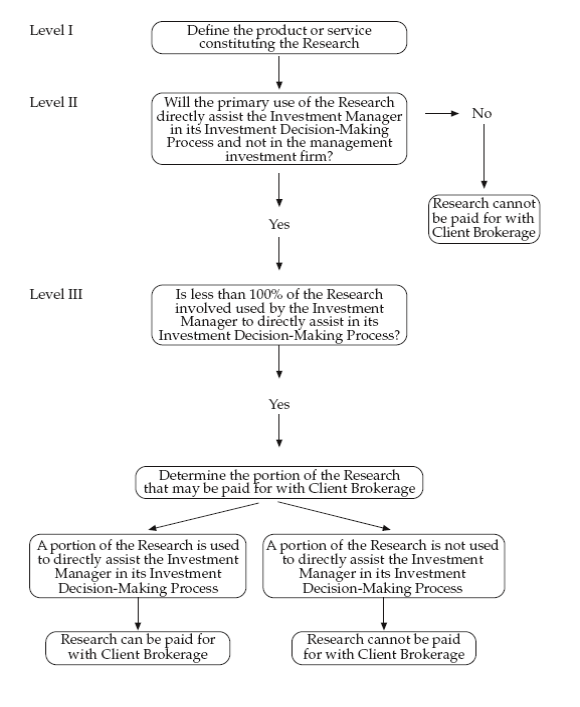

III. Best Execution and Soft Dollars

IV. Client Disclosures and Advertising

A) Account Statements

B) Advertising

C) Updating disclosure with respect to Privacy Policy, Proxy Voting Policy, Soft Dollars and Other Matters

V. Safeguarding of Client Assets

VI. Recordkeeping

A) Required Records

B) E-mail

VII. Valuation Policy

VIII. Privacy Policy

IX. Regulatory Filings

X. Business Continuity Plan/Cybersecurity

XI. Anti-Money Laundering Plan

XII. Enterprise Risk Management

Addendum:

a. Independent Bank Corp. and Subsidiaries Code of Ethics

b.Rockland Trust Company Computer Usage Standard

c.Rockland Trust Company Anti-Money Laundering (AML) Program

d.Business Continuity Plan

I. CODE OF ETHICS

Revised August 2021

TOPICS IN THIS CODE

A) Standard of Conduct

B) Confidential Information

C) Material Inside Information

D) Fiduciary Duty and Conflicts of Interest

E) Scalping or Frontrunning

F) Unfair Treatment of Certain Clients Vis-a-Vis Others

G) Dealing with Clients as Agent and Principal: Section 206(3) of the Investment Advisers Act of 1940

H) Personal Trading; Timely Reporting of Trades

I) Social Media Policy

J) Political Contribution Policy

K) Employee’s Responsibility to Know the Rules and Comply with Applicable Laws

L) Designation and Responsibilities of Chief Compliance Officer

M) Code of Ethics Records

A. STANDARD OF CONDUCT

Employees of Bright Rock Capital Management (the “Company”) are expected to comply with the Code of Ethics policy established for both Independent Bank Corp. (parent company of Rockland Trust which is the parent company of Bright Rock) as well as this Code of Ethics policy specifically established for Bright Rock. Any questions about interpretation of policy requirements for either Independent Bank or Bright Rock should be discussed with the Chief Compliance Officer.

The purpose of this Code of Ethics is to set forth certain key guidelines that have been adopted by Bright Rock Capital Management (the “Company”) as office policy for the guidance of all Company personnel and to specify the responsibilities of all Employees of the Company (as defined in B.2 below) to act in accordance with their fiduciary duty to the Company’s clients and to comply with applicable federal and state laws and regulations, including, but not limited to, securities laws, governing their conduct. In particular, Employees should be aware of the legal requirements of the Investment Advisers Act of 1940 (the “Advisers Act”). Careful adherence is essential to safeguard the interests of the Company and its clients. The Company expects that all Employees will conduct themselves in accordance with high ethical standards, which should be premised on the concepts of integrity, honesty and trust.

As noted, all Employees of the Company must conduct themselves in full compliance with all applicable federal and state laws and regulations concerning the securities industry. In particular, an Employee should be familiar with those laws and regulations governing “insider trading” and fiduciary duties. It is the responsibility of every Employee to know these laws and regulations and to comply with them. If an Employee needs copies of any laws and regulations concerning the securities business or has any questions about the legality of any transaction, the Employee should consult the Chief Compliance Officer. Failure to comply with such laws and regulations or this Code may result in sanctions and possibly, depending on the circumstances, immediate dismissal.

Although our fiduciary duties require more than simply avoiding illegal and inappropriate behavior, at a minimum, all Employees should be aware that, as a matter of policy and the terms of their employment with the Company, the following types of activities are strictly prohibited:

(1) Using any device, scheme or artifice to defraud, or engaging in any act, practice, or course of conduct that operates or would operate as a fraud or deceit upon, any client or prospective client or any party to any securities transaction in which the Company or any of its clients is a participant;

(2) Making any untrue statement of a material fact or omitting to state to any person a material fact necessary in order to make the statements the

Company has made to such person, in light of the circumstances under which they are made, not misleading;

(3) Engaging in any act, practice, or course of business that is fraudulent, deceptive, or manipulative, particularly with respect to a client or prospective client; and

(4) Causing the Company, acting as principal for its own account or for any account in which the Company or any person associated with the Company (within the meaning of the Investment Advisers Act), to sell any security to or purchase any security from a client in violation of any applicable law, rule or regulation of a governmental agency.

B. CONFIDENTIAL INFORMATION

1. What is confidential information?

An investment adviser has a fiduciary duty to its clients not to divulge or misuse information obtained in connection with its services as an adviser. Therefore, all information, whether of a personal or business nature, that an Employee obtains about a client’s affairs in the course of employment with the Company should be treated as confidential and used only to provide services to or otherwise to the benefit of the client. Such information may sometimes include information about non-clients, and that information should likewise be held in confidence. Even the fact that the Company advises a particular client should ordinarily be treated as confidential.

2. Who is subject to the Company’s policies concerning confidential information?

All Company personnel - officers and advisory, marketing, administrative and secretarial staff - are subject to these policies. (For the sake of convenience, this group is sometimes referred to in this Manual as “Employees”).

3. What are the duties and responsibilities of Employees with respect to confidential information?

Since an investment adviser has a fiduciary duty to its clients not to divulge information obtained from or about a client in connection with its services as an adviser, Employees must not repeat or disclose confidential information received from or about clients outside the Company to anyone, including relatives, friends or strangers. Any misuse of confidential information about a client is a disservice to the client that may cause both the client and the Company substantial injury. Failure to comply with this policy may have very serious consequences for Employees and for the Company, including the possibility that Employees might be criminally prosecuted for misusing the information, as described in Part C below.

4. What are some steps that Employees can take to assure that confidential information is not disclosed to persons outside the office?

There are a number of steps Employees should take to help preserve client and other confidences, including the following:

(a) Employees should be sensitive to the problem of inadvertent or accidental disclosure. Careless conversation, naming names or describing details of a current or proposed trade, investment or transaction in a lounge, hallway, elevator or restroom, or in a train, taxi, airplane, restaurant or other public place, can result in the disclosure of confidential information and should be strictly avoided.

(b) Maintenance of confidentiality requires careful safeguarding of papers and documents, both inside and outside the Company. Documents and papers should be kept in appropriately marked file folders and locked in file cabinets when appropriate. Computer files or disks should be password protected.

(c) If an Employee uses a speakerphone, the Employee should be careful to refrain from using it in any way that might increase the likelihood of accidental disclosure. Use caution, for example, when participating in a speakerphone conversation dealing with confidential information if the office door is open, or if the speakerphone volume is set too high. The same applies if an Employee knows or suspects that a speakerphone or a second extension phone is being used at the other end of a telephone conversation.

(d) In especially sensitive situations, it may be necessary to establish barriers to the exchange of information within the Company and to take other steps to prevent the leak of confidential information.

(e) Employees should be aware that e-mail and information transmitted through the Internet may not be secure from hacking or interception and should be cautious in transmitting confidential information by e-mail or through the Internet.

C. MATERIAL INSIDE INFORMATION

All Employees are reminded that purchasing or selling securities on the basis of, or while in possession of, material nonpublic information for their own, for a client’s or for the Company’s account is a crime punishable by imprisonment as well as large fines. “Tipping” another person who engages in such activities is also a crime. The term “material” is described below.

The sanctions for trading while in possession of material “inside information”, as it is sometimes called, can be severe. In recent years, the Securities and Exchange

Commission (“SEC”) has aggressively sought and prosecuted persons who traded on “inside information.” Courts are now authorized to impose fines of up to three times the profit gained, or loss avoided, on such transactions. Criminal prosecution is also possible. Willful misuse of material nonpublic information will result in dismissal from employment by the Company.

Employees should be careful to avoid even the appearance of wrongdoing. Even an innocent purchase or sale of securities by an Employee who is unaware that other Employees possess material nonpublic information about an issuer may damage the Company’s reputation and may lead to protracted investigations and audits of both the Company and Employees.

The following sections of this Code of Ethics seek to answer some of the most commonly asked questions about insider trading. In the questions and answers that follow, the term “issuer” refers to an entity, such as a corporation, partnership or state agency, that has issued securities, and the term “securities” is used in the broadest sense to include privately held and publicly traded stocks, bonds, options and other investment vehicles that the SEC considers to be securities.

1. Who is subject to the insider trading rules?

All Employees and all persons - friends, relatives, business associates and others - who receive nonpublic material inside information from Employees concerning an issuer of securities (whether such issuer is a client or not) are subject to these rules. It does not matter whether the issuer is public or private.

At the Company, the rules apply to officers, marketing, advisory, administrative, secretarial and other staff. Furthermore, if any Employee gives nonpublic material inside information concerning an issuer of securities to a person outside the Company, and that person trades in securities of that issuer, the Employee and that person may both have civil and criminal liability.

2. What is material inside information?

Generally speaking, inside information is information about an issuer’s business or operations (past, present or prospective) that becomes known to an Employee and which is not otherwise available to the public. Although neither the courts nor the SEC has defined “material” precisely, the word is similar in meaning to “important” or “significant.”

While the exact meaning of the word “material” is not entirely clear, it is clear that if a person knows information about an issuer which the person believes would influence an investor in any investment decision concerning that issuer’s securities and which has not been disclosed to the public, the person should not buy or sell that issuer’s securities. Under current court decisions, it makes no difference whether the material inside information is good or bad. Needless to say, if the undisclosed information would influence an Employee’s own decision to buy or sell or to trade for a client or the

Company, the information probably is material and an Employee should not trade or permit the Company to trade for a client or itself until it has been publicly disclosed.

3. How does “material inside information” differ from “confidential information”?

Here is an example that should clarify the difference between the two. Suppose the Company is engaged by the president of a publicly-traded corporation to provide advice with respect to her personal pension fund and while working on the matter an Employee learns the amount of alimony she pays to her former spouse. That discovery should be kept confidential, but it almost certainly has no bearing on the value of her corporation’s securities (i.e., it is not material) and, in fact, it probably is not “inside information” about the corporation itself. Accordingly, an Employee of the Company could buy or sell securities of that issuer so long as the Employee possessed no material nonpublic information about the corporation. But disclosure of the president’s alimony payments would be embarrassing to her and improper.

In other words, confidential information should never be disclosed, but it is not always material inside information. Knowing it is not necessarily an impediment to participating in the securities markets concerning a particular issuer.

4. Are there certain kinds of information that are particularly likely to be “material inside information”?

Yes. While the following list is by no means complete, information about the following subjects is particularly sensitive:

(a) Dividends, stock dividends and stock splits.

(b) Sales and earnings and forecasts of sales and earnings.

(c) Changes in previously disclosed financial information.

(d) Corporate acquisitions, tender offers, major joint ventures or merger proposals.

(e) Significant negotiations, new contracts or changes in significant business relationships.

(f) Changes in control or a significant change in management.

(g) Adoption of stock option plans or other significant compensation plans.

(h) Proposed public or private sales of additional or new securities.

(i) Significant changes in operations.

(j) Large sales or purchases of stock by principal stockholders.

(k) Purchases or sales of substantial corporate assets, or decisions or agreements to make any such purchase or sale.

(l) Significant increases or declines in backlogs of orders.

(m) Significant new products to be introduced.

(n) Write-offs.

(o) Changes in accounting methods.

(p) Unusual corporate developments such as major layoffs, personnel furloughs or unscheduled vacations for a significant number of workers.

(q) Labor slowdowns, work stoppages, strikes, or the pending negotiation of a significant labor contract.

(r) Significant reductions in the availability of goods from suppliers or shortages of these goods.

(s) Extraordinary borrowings.

(t) Major litigation.

(u) Governmental investigations concerning the Company or any of its officers or directors.

(v) Financial liquidity problems.

(w) Bankruptcy proceedings.

(x) Establishment of a program to repurchase outstanding securities.

5. What is the law regarding the use of material inside information?

Federal law, and the policy of the Company, prohibit any Employee from using material inside information, whether obtained in the course of working at the Company or otherwise, for his or her private gain, for the Company’s gain or for a client’s gain and prohibit any Employee from furnishing such information to others for their private gain. This is true whether or not the information is considered “confidential.” When in doubt, the information should be presumed to be material and not to have been disclosed to the public. No trades should be executed for any Employee, any client or for the Company, if the person executing the trade or the Company has material inside information about the issuer.

6. What is “tipping”?

Under the federal securities laws, it is illegal to disclose (or “tip”) material inside information to another person who subsequently uses that information for his or her profit. In order to minimize this liability, all Company personnel should comply with the policies regarding protection of confidential information described in Part A above, which will include the following measures:

(a) To reduce the chances of inadvertent tipping of material inside information, any nonpublic information that might be considered material should not be discussed with any person outside the Company. Such information should be regarded as particularly sensitive, confidential information, and the Company’s policies for safeguarding such information should be strictly observed.

(b) Employees should avoid recommending to any person, including Company clients, the purchase or sale of client (or client-related) securities.

(c) Caution must especially be used when receiving information from securities analysts, corporations in the same business as the client and members of the press.

Questions regarding whether such information may constitute “inside information” should be referred to the Chief Compliance Officer.

7. To whom must material inside information be disclosed before an employee can trade?

To the public. Public disclosure of material events is usually made by means of an official press release or filing with the SEC. An Employee’s disclosure to a broker or other person will not be effective, and such Employee may face civil or criminal liability if such Employee (or the person to whom the Employee makes disclosure) trades on the basis of the information. Employees should be aware that in most cases they are not authorized to disclose material events about an issuer to the public and that right usually belongs to the issuer alone.

8. How does an Employee know whether particular material inside information has been publicly disclosed?

If an Employee sees information in a newspaper or public magazine, that information will clearly have been disclosed. Information in a filing with the SEC or a press release will also have been disclosed. However, the courts have said that one should wait for a reasonable period of time after the publication, filing or release date to assure that the information has been widely disseminated and that the public has had sufficient time to evaluate the news. If any Employee has any questions about whether information has been disclosed, such Employee should not trade in the affected securities. An Employee should contact the Chief Compliance Officer for advice in the matter.

9. What must an Employee do with respect to material inside information that such Employee may learn about an issuer that is not a client of the Company?

In connection with their work at the Company, Employees may come into possession of material inside information with respect to issuers that are not clients of the Company such as information with respect to issuers or securities of issuers which are being analyzed for purchase or sale. This is particularly likely to happen in connection with the recommendation of the purchase or sale of an issuer’s securities. All personnel receiving material, nonpublic information have the same duty not to disclose or use that information in connection with securities transactions as they have with respect to client securities. In other words, Employees may not purchase or sell any securities with respect to which they have inside information for their own, the Company’s or for a client’s account or cause clients to trade on such information until after such information becomes public. The foregoing prohibition applies whether or not the material inside information is the basis for the trade. Employees should be alert for information they receive about issuers on their recommendation or approved lists which may be material inside information. In addition, whenever Employees come into possession of what they believe may be material nonpublic information about an issuer; they must immediately notify the Chief Compliance Officer because the Company as a whole may have an obligation not to trade in the securities of the issuer. The Chief Compliance Officer shall maintain a list of all issuers about which the Company has inside information and shall circulate such list to the appropriate personnel at the Company so as to prevent any trading in securities of such issuers.

10. Who is available for additional advice or advice about a particular situation?

The Chief Compliance Officer designated from time to time by the Company will oversee matters relating to inside information and prohibitions on insider trading. If you have any questions about the identity of the Chief Compliance Officer, you should ask the Company’s Chief Investment Officer.

Disclosure outside the Company of confidential information by an Employee, or participation or tipping others to participate in business or securities transactions when in possession of material inside information, may be a violation of law and subject the employee to severe penalties, including criminal prosecution.

D. FIDUCIARY DUTY AND CONFLICTS OF INTEREST

The Company and the Employees have a fiduciary duty to Company clients to act for the benefit of the clients and to take action on the clients’ behalf before taking action in the interest of any Employee or the Company. The cornerstones of the fiduciary duty are the obligations to act for the clients’ benefit and to treat the clients fairly. Clients may therefore expect their fiduciaries to act for the clients’ benefit and not in their own when a conflict of interest between the client and the fiduciary arises. No Employee should ever enjoy an actual or apparent advantage over the account of any client.

This Manual attempts to highlight and address many of the common conflicts of interest that may arise between the Company and its employees on the one hand and clients on the other, and also between different client accounts. It is not possible for every conflict to be addressed in the Manual, however, and Employees should be particularly sensitive to the existence of actual or potential conflicts of interest not addressed herein and should promptly raise any such conflicts of which they become aware with the Chief Compliance Officer. The Chief Compliance Officer will maintain a Conflict of Interest Inventory and review at least annually by the CCO and the Compliance Committee. The inventory will also address any potential conflicts with its affiliated parties.

The manner in which any Employee discharges his or her fiduciary duty and addresses a conflict of interest depends on the circumstances. Sometimes general disclosure of common conflicts of interest may suffice. In other circumstances, explicit consent of the client to the particular transaction giving rise to a conflict of interest may be required or an Employee may be prohibited from engaging in the transaction regardless of whether the client consents.

The client’s consent will not in all cases insulate the Employee against a claim of breach of the Employee’s fiduciary duty. Full disclosure of all material facts must be given if consent is to be effective. As a result, consents concerning possible future breaches of laws will not usually work. However, waivers of known past violations may be effective. In addition, a client under the control and influence of the Employee or who has come to rely on the Employee’s investment decisions cannot effectively consent to a conflict of interest or breach of fiduciary duty. Consent must be competent, informed and freely given.

The duty to disclose and obtain a client’s consent to a conflict of interest must always be undertaken in a manner consistent with the Employee’s duty to deal fairly with the client. Therefore, even when taking action with a client’s consent, each Employee must always seek to assure that the action taken is fair to the client.

Conflicts of interest can arise in any number of situations. As noted, no comprehensive list of all possible conflicts of interest can be provided in this Code of Ethics. However, the following are common examples of conflicts of interest. For example, an Employee may seek to induce a bank to give the Employee a loan in exchange for maintaining excessive cash balances of a client with the bank or may execute trades for a client through a broker-dealer that provides research services for the Company but charges commissions higher than other broker-dealers. In the former case, such activity would be a violation of an employee’s fiduciary duty and might subject the employee and the Company to liability under the Investment Advisers Act of 1940 (the “Advisers Act”) and other applicable laws. In the latter case, if the Company determines in good faith that the higher commissions are reasonable in relation to the value of the brokerage and research services provided by a broker or dealer viewed in terms of either a particular transaction or the Company’s overall responsibilities with respect to an account as to which the Company exercises investment discretion and appropriate

disclosure is made to the client and in the Company’s Form ADV, the payment of higher commissions may be permitted under the safe harbor of Section 28(e) of the Securities Exchange Act of 1934.

Another common conflict of interest occurs when the Company pays some consideration to a person for recommending the Company as an adviser. In those circumstances, an Employee must make disclosure to any prospective client of any consideration paid for recommending the Company’s services to that prospective client and the Company must comply with Rule 206(4)-3 promulgated under the Advisers Act. This Rule governs situations involving cash payments for client solicitations and requires that specific disclosure documents are containing information about the solicitor and the adviser be provided to a prospective client at the time of the solicitation.

Commissions. Employees may negotiate with broker-dealers regarding the commissions charged for their personal transactions but may not enter into any arrangement to pay commissions at a rate that is better than the rate available to clients through similar negotiations.

Gifts. No Employee may receive any gift or other thing of more than nominal value ($100 or less) from any person or entity that does business with or on behalf of any client. However, Employees may attend business meals, sporting events and other similar events provided the cost is reasonable and the gift giver also is present at the event.

Service as a Director or Member of Investment Committee. Any Employee who wishes to serve as an officer or director of any public company, or of any organization where such duties might require involvement in investment decisions, or who wishes to serve on the investment committee of any organization, must obtain the prior written consent of the Chief Compliance Officer, which shall be granted in his discretion and only if he is satisfied that such service shall not create a conflict with such Employee’s fiduciary duty to clients.

If any Employee is faced with any conflict of interest, he or she should consult the Chief Compliance Officer prior to taking any action.

E. SCALPING OR FRONTRUNNING

As a general rule, if any Employee knows of a pending “buy” recommendation and buys stock before the Company makes a recommendation to its non-discretionary clients or takes action on the recommendation for its clients for which it has investment discretion, or if any Company Employee is aware of a pending “sell” recommendation and sells stock under such circumstances, such Employee is engaged in a practice known as “scalping” or “front running.”

An Employee or family member residing in that Employee’s household or person or entity over which the Employee has control (the “Related Person(s)”) may not engage in the practice of purchasing or selling stock before a buy or sell recommendation, as the case may be, is made to a non-discretionary client or the Company takes action for its clients for which it has investment discretion. Such activities put the Company and the Employee in a conflict of interest and give the Employee or the Related Person an advantage at the client’s expense. Limited exceptions may be granted for liquid securities where the Employee is selling or selling a non-material number of shares. Any trades undertaken for an Employee’s own account, for the account of the Company, for the account of any non-Company client or for a Related Person must be done so as not to disadvantage a Company client in any way. This means that all Employees and their Related Persons must generally wait to trade a security until all trading in that security for all accounts of the Company’s clients is completed, although in some cases it may be appropriate to aggregate a personal trade with client trades (see Section II, Part A). If all client trades are not completed before an Employee or Related Person trades, the antifraud provisions of the Advisers Act may be violated.

In order to preclude the possibility that material nonpublic information about the Company’s investment decisions and recommendations, and client securities holdings and transactions, could be misused, the Company has taken steps to restrict access to such information to employees who need such information to perform their duties, including the use of password protection on computer files and limiting physical access to paper storage records. Employees who are not authorized to access such information may be subject to termination if they attempt to do so.

F. UNFAIR TREATMENT OF CERTAIN CLIENTS VIS-A-VIS OTHERS

An Employee who handles one or more clients may be faced with situations in which it is possible to give preference to certain clients over others. Employees must be careful not to give preference to one client over another even if the preferential treatment would benefit the Company or the Employee.

For example, an Employee should not (i) provide better advice to a large, prestigious client than is given to a smaller, less influential one, (ii) give sale advice to one client ahead of another, or (iii) direct securities of a limited supply and higher potential return to particular clients because they generate larger fees for the Company.

As in other instances, the fiduciary duty of an Employee to a client must govern the Employee’s actions in each situation and the extent of the fiduciary duty of an Employee to a client is determined by the specific relationship between the parties and the reasonable inferences to be drawn from the relationship. In the absence of express or implied agreements between the parties, usage and custom should be used to determine how an Employee should discharge his or her duty. Each situation should be examined closely to determine whether the client has consented to the Employee’s actions favoring another client and whether the resulting relationship with the client which was not favored is fair and consistent with the securities laws. If both parts of this test have been

satisfied, most likely there has been no breach of fiduciary duty. If a question arises about action that may give rise to a conflict of interest involving preferential treatment of one client over another, an Employee should consult the Chief Compliance Officer prior to taking any action.

G. DEALING WITH CLIENTS AS AGENT

AND PRINCIPAL: SECTION 206(3) OF THE ADVISERS ACT

Section 206(3) of the Advisers Act addresses specifically two conflict of interest situations: sale and purchase of securities to and from a client either as a broker for another person or as a principal for the account of the adviser. Section 206(3) makes it unlawful for an investment adviser “acting as principal for his own account, knowingly to sell any security to or purchase any security from a client, or acting as broker for a person other than such client, knowingly to effect any sale or purchase of any security for the account of such client, without disclosing to such client in writing before the completion of such transaction the capacity in which he is acting and obtaining the consent of the client to such transaction.”

Thus, Section 206(3) requires that Employees involved in the situations where the Company is buying or selling securities from a client or where the Company acts as a broker-dealer for a non-client in a transaction with an advisory client disclose to the client the capacity in which the Company acts and obtain the client’s consent. Disclosure under Section 206(3) must be in writing. The Company must, under Section 206(3), disclose to the client its capacity, its profits (if it acts as principal) and its commissions (if it acts as agent for another). These types of transactions can be particularly troublesome under applicable laws and must not be entered into without prior consultation with the Chief Compliance Officer.

H. PERSONAL TRADING; TIMELY REPORTING OF TRADES

Personal Trading

Set forth below are the Company’s policies regarding personal trading. These policies apply to all Access Persons. Under the Advisers Act, Access Persons include any of the Company’s partners, officers, interns, temporary, contract employees, directors (or other persons occupying a similar status or performing similar functions) and employees who have access to nonpublic information regarding clients’ purchases or sales of securities, is involved in making securities recommendations to clients or who has access to such recommendations that are nonpublic. Because the Company’s primary business is providing investment advice, the Advisers Act presumes that all officers, directors and partners are Access Persons. Because of the Company’s size and the range of duties that Employees may have, all Employees are considered “Access Persons,” and “Access Person” procedures, standards and restrictions that might be imposed only on a limited subset of employees in another, larger organization, apply to all Employees. Many of the procedures, standards and restrictions in this section govern activities in “Covered Accounts.” Covered Accounts include each securities account registered in an Employee’s

name and each account or transaction in which an Employee has any direct or indirect “beneficial ownership interest.” The term “beneficial ownership interest” has a very broad meaning, discussed more completely below, and can include accounts of corporations owned by the Employee and even accounts owned by certain family members. An Employee has a “beneficial ownership” interest in not only securities he or she owns directly, and not only securities owned by others specifically for his or her benefit, but also (i) securities held by the Employee’s spouse, minor children and relatives who live full time in the Employee’s home, and (ii) securities held by another person if by reason of any contract, understanding, relationship, agreement or other arrangement the Employee obtains benefits substantially equivalent to ownership. Examples of some of the most common of those arrangements are as follows:

1. By an Employee for his/her own benefit, whether bearer, registered in his/her own name, or otherwise;

2. By others for the Employee’s benefit (regardless of whether or how registered), such as securities held for the Employee by custodians, brokers, relatives, executors or administrators;

3. For an Employee’s account by a pledge;

4. By a trust in which an Employee has an income or remainder interest unless the Employee’s only interest is to receive principal if (a) some other remainderman dies before distribution or (b) if some other person can direct by will a distribution of trust property or income to the Employee;

5. By an Employee as trustee or co-trustee, where either the Employee or any member of his/her immediate family (i.e., spouse, children and their descendants, stepchildren, parents and their ancestors, and stepparents, in each case treating a legal adoption as blood relationship) has an income or remainder interest in the trust.

6. By a trust of which the Employee is the settlor, if the Employee has the power to revoke the trust without obtaining the consent of all the beneficiaries;

7. By any non-public partnership in which the Employee is a partner;

8. By a personal holding company controlled by the Employee alone or jointly with others;

9. In the name of the Employee’s spouse unless legally separated;

10. In the name of minor children of the Employee or in the name of any relative of the Employee or of his/her spouse (including an adult child) who is presently sharing the Employee’s home. This applies even if the securities were not received from

the Employee and the dividends are not actually used for the maintenance of the Employee’s home;

11. In the name of any person other than the Employee and those listed in (9) and (10) above, if by reason of any contract, understanding, relationship, agreement, or other arrangement the Employee obtains benefits substantially equivalent to those of ownership;

12. In the name of any person other than the Employee, even though the Employee does not obtain benefits substantially equivalent to those of ownership (as described in (11) above), if the Employee can vest or revest title in himself/herself.

This broad definition of “beneficial ownership” is for purposes of this Code of Ethics only; it does not necessarily apply for purposes of other securities laws or for purposes of estate or income tax reporting or liability. To accommodate potential differences in concepts of ownership for other purposes, an Employee may include in his/her reports a statement declaring that the reporting or recording of any securities transaction shall not be construed as an admission that the reporting person has any direct or indirect beneficial ownership in the security.

Preclearance. No Employee may buy, sell, or pledge any security for any Covered Account without obtaining written clearance from the Chief Compliance Officer or a Compliance Officer before the transaction.It is each Employee’s responsibility to bring proposed transactions to the Chief Compliance Officer’s attention and to obtain from the Chief Compliance Officer follow-up written documentation of any oral clearance. Transactions effected without preclearance are subject, in the Chief Compliance Officer’s discretion (after consultation with other members of management, if appropriate), to being reversed or, if the Employee made profits on the transaction, to disgorgement of such profits. Additionally, the Chief Compliance Officer’s trades shall be approved by the Chief Investment Officer.

The Chief Compliance Officer or Compliance Officer need not specify the reasons for any decision to clear or deny clearance for any proposed transaction. As a general matter, due to the difficulty of showing that an Employee did not know of client trading activity or recommendations, the Chief Compliance Officer should not be expected to clear transactions in securities as to which the Company has client activity, although the Chief Compliance Officer may determine that a particular transaction in such a security does not, under the circumstances, create the appearance of impropriety and permit it.1

Transaction orders should be placed promptly after approval is given and in any case must be placed within two trading days after the day approval is granted. The Chief Compliance Officer may revoke a pre-approval at any time for any reason, and shall in

1 For example, if an Employee seeks to sell a security he or she has owned for a significant time and the Company is considering buying the same or a related security for clients, the Chief Compliance Officer may determine no appearance of impropriety exists.

such case promptly notify the Employee. A record is maintained for all preclearance trade approvals from the Compliance team.

“Blackout” Period. No Employee may (i) buy a security within seven calendar days before any client account buys the same or a related security, (ii) sell such a security within seven days before any client account sells the same or a related security, (iii) sell a security within seven days after any client account has bought the same or a related security or (iv) buy a security within seven days after any client account has sold the same or a related security. The Chief Compliance Officer may grant exemptions to the foregoing rules in his discretion (for example, when an Employee has sold a security and, before the expiration of seven days, external events make it important for a client to sell the same or a related security quickly). If an Employee completes a transaction during a “blackout” period, he or she may be required to turn over any profits realized on the transaction, in most cases for crediting to client accounts.

Limitation on Short-Term Trading. No Employee may engage in the purchase and sale, or sale and purchase, for a Covered Account of the same (or equivalent) securities within any period of 30 calendar days. In most cases, any profits realized by an Employee on trades within the 30-day period must be disgorged for crediting to client accounts. As a general principal, the Company believes that market timing is inappropriate and should not be practiced by Employees.

Options, Futures and Similar Derivative Securities. No Covered Account may buy, own, or trade in any futures contracts on any securities or securities indices; provided that the Chief Compliance Officer (CCO) may grant exceptions in circumstances in which the CCO determines that no potential exists for the appearance of impropriety and that this prohibition would result in unreasonable hardship for the Employee or other beneficial owners of a Covered Account. For example, it may be inappropriate to prohibit the spouse of an Employee from receiving and owning employee stock options from his or her employer, provided the exercise of the options is subject to preclearance and the other rules applicable to securities transactions by Covered Accounts.2

Options

Access Persons may not write naked call options or buy naked put options on a security owned by any portfolio managed by the advisor. Access Persons may purchase options on securities not held by any portfolio managed by the advisor, or purchase call options or write put options on securities owned by any portfolio managed by the advisor, subject to preclearance and the same restrictions applicable to other securities.

Access Persons may write covered call options or buy put options on a security owned by any portfolio managed by the advisor at the discretion of the compliance officer.

2 In such a circumstance, if the employer’s securities are held in client accounts, a further exemption will be required to allow the ownership and exercise of the options and the ownership and/or sale of the underlying stock.

However, investment personnel should keep in mind that the short-term trading profit rule might affect their ability to close out an option position at a profit.

New Issue Securities and Private Placements. No Employee may purchase any equity securities issued in an initial public offering (“New Issue Securities”) or any securities offered in a “private placement” for any Covered Account without the prior written approval of the Chief Compliance Officer. In determining whether to approve any such transaction for an Employee, the Chief Compliance Officer will consider, among other factors, whether the investment opportunity should be reserved for client accounts and whether the investment opportunity is being offered to the Employee by virtue of his or her position with the Company.

Employee Reporting

Report of Holdings. Each Employee must submit an initial Holdings Report disclosing to the Chief Compliance Officer the identities, amounts, and locations of all securities owned in all Covered Accounts -- i.e., accounts in which he or she has a “beneficial ownership interest.” Thereafter, each new Employee must submit such a report within 10 days of commencement of employment. In addition, an Annual Holdings Report must be submitted by each employee beginning no later than 30 days after end of each calendar year. Such reports must be current as of a date not more than 45 days prior to the Employee joining the Company (for an initial report) or the date the report is submitted (for the annual report). Annual Holding forms are completed and attached with the brokerage statements to display the holdings. Annual holding forms are completed with the attached brokerage statements and are maintained and reviewed by the CCO. A form of report is attached as Exhibit A to this Code of Ethics.

Brokerage Accounts. Each Employee must provide the Company with duplicates of all monthly or other periodic statements from each broker, bank, or other financial institution in which the Employee has a Covered Account (i.e., a securities trading account in which the Employee has any direct or indirect beneficial ownership interest). The statements will contain title of the account, number of shares and principal amount of each covered security.

Quarterly Reports. Each Employee must report to the Chief Compliance Officer within 30 days after the end of each calendar quarter all securities transactions in all of the mployee’s Covered Accounts during the preceding quarter. A form of report is attached as Exhibit B to this Code of Ethics. Quarterly certification is NOT required by the employee if a broker statement is already set up to be received by the CCO as an interested party on the account.

In filing holdings and transactional reports, Employees must note that:

a. Each Employee must file a transactional report every quarter whether or not there were any reportable transactions.

b. Transactional reports must show all sales, purchases, or other acquisitions or dispositions, including gifts, the rounding out of fractional shares, exercises of conversion rights, exercises or sales of subscription rights and receipts of stock dividends or stock splits.

c. Employees need not report holdings or transactions (i) effected pursuant to an automatic investment plan (however, any transaction that overrides or changes the preset contribution schedule or allocations under such plan should be reported), (ii) with respect to securities held in accounts over which the Employee has no discretion (such as a managed account)direct influence or control (such as a blind trust), (iii) in direct obligations of the U.S. Government , (iv) in money market instruments, bankers’ acceptances, bank certificates of deposit, commercial paper, repurchase agreements and other high quality short term debt instruments, (v) shares of money market funds, (vi) shares of open-ended mutual funds for which the Company does not serve as investment adviser (holdings of and transactions in exchange traded funds and closed-end funds must be reported) (vii) transactions in units of a unit investment trust if the unit investment trust is invested exclusively in unaffiliated open-end mutual funds and (viii) currency transactions.

I.Social Media Policy

The SEC has imposed strict guidelines on advertising and has issued guidance that the use of social media could be considered a form of advertising. Currently, Bright Rock does not use social media and has no plans to do so.

In order to avoid any potential violation of these SEC advertising restrictions, Bright Rock Capital Management LLC forbids employees from using social media to promote its Bright Rock services, to interact with clients or to build their business unless express permission to do so is granted by the CIO and CCO.

Accordingly, Bright Rock employees are prohibited from using any type of social media for example (LinkedIn )to promote Bright Rock Capital Management or Bright Rock Funds. These rules apply regardless of whether the employee is in the office, at home, on a public computer or using a personal device.

Any Bright Rock employee with questions regarding the use of social media should contact the Chief Compliance Officer to determine what activities are permitted and if so, what limitations may apply.

02/07/12

J. Political Contribution Policy

The SEC, in accordance with its Rule 206(4)-5, has imposed strict guidelines on making political contributions to elected officials or candidates where the advisor is providing or seeking government business. This rule, commonly referred to as the “Pay-to-Play rule, specifically prohibits investment advisers from receiving compensation for providing investment advice to a “government entity” within two years after a covered contribution has been made by the adviser or one of its “covered associates.” There are two de minimus exceptions. For an official are entitled to vote for, a covered associate can contribute up to $350 per election. That exception is lowered to $150 if they are not entitled to vote for the official.

Bright Rock Capital Management has adopted the policy that all political contributions must be pre-approved by the Chief Compliance Officer who will determine if a contribution is permissible and would not trigger the time out period. A political contribution log is maintained in the Compliance Department.

It should be noted, that Bright Rock as an advisor to mutual funds, is restricted from making contributions to any shareholder of the Bright Rock funds that is a “government entity,” political official or candidate.

K. EMPLOYEE’S RESPONSIBILITY TO KNOW THE RULES

AND COMPLY WITH APPLICABLE LAWS

Company employees are responsible for their actions under the law and therefore required to be sufficiently familiar with the Advisers Act and other applicable federal and state securities laws and regulations to avoid violating them. It is the policy of the Company to comply with all applicable laws, including securities laws, in all respects. Each Employee must promptly report any violation of the Code of Ethics of which he becomes aware to the Chief Compliance Officer, regardless of whether the violation was committed by the Employee or another Employee. The Chief Compliance Officer shall consider whether it is appropriate to protect the confidentiality of the identity of an Employee reporting a violation by another Employee. It is the strict policy of the

Company that no Employee shall be subject to any form of retaliation in connection with reporting a violation of the Code of Ethics, and any person found to have engaged in retaliation may be subject to dismissal or other sanction.

Employees must certify in writing on an annual basis, that they have read and understood this Manual, that they will conduct themselves professionally in complete accordance with the requirements and standards described here and that they are not aware of any violations of the Code of Ethics during the prior year. A copy of the Company’s current form of compliance certificate is attached to this Manual as Exhibit C to this Code of Ethics.

L. DESIGNATION OF AND RESPONSIBILITIES OF CHIEF COMPLIANCE OFFICER

Garth O’Leary shall serve as the Company’s Chief Compliance Officer (the “Chief Compliance Officer”) until such time as a new Chief Compliance Officer is appointed by the Company’s President. The Chief Compliance Officer will provide new employees with a copy of this memorandum as soon as possible after they join the firm and, upon their request, of the Advisers Act and other applicable laws and regulations. The Chief Compliance Officer shall conduct training for new and existing employees on the provisions and requirements of this manual from time to time as the Chief Compliance Officer determines to be appropriate.

The Chief Compliance Officer is responsible for staying current with significant new legal developments in the area of financial advisory services, fiduciary responsibilities, and insider trading and to convey such developments to the Company employees. As part of his duties, the Chief Compliance Officer shall review this Manual and Rule 206(4)-7 compliance reviews no less frequently than annually and recommend changes as appropriate or necessary. The review shall include consideration of any compliance matters that arose during the prior year, whether the existing policies have proven effective and any changes in the business activities of the Company and any changes in the Advisers Act and related regulations that might necessitate revisions to the Manual. The Chief Compliance Officer will submit the completed 206(4)-7 annual review to the Trust for Professional Managers (TPM) CCO. Significant compliance events will be escalated to the TPM CCO.

The Chief Compliance Officer will review all employee trading reports in a timely manner to identify any violation of the Code of Ethics’ approval procedures and any improper trades or any patterns of trading (including achieving execution or results which differ materially from the execution or results obtained for clients) which suggest that an Employee may be engaging in abusive practices, and take such action as he or she deems necessary to obtain compliance with the policies set forth in this Manual and with applicable laws provided, however, that the trading report of the Chief Compliance Officer shall be reviewed by the Chief Investment Officer of the Company.

As the investment adviser to Bright Rock Mid Cap Growth Fund and Bright Rock Quality Large Cap Fund, the Company has certain reporting obligations to the Board of Trustees of Trust for Professional Managers (the “Board”). No less frequently than annually, the Chief Compliance Officer shall furnish to the Board a written report (the “COE Report”) that: (A) describes issues arising under the Code of Ethics or related procedures since the last COE Report to the Board, including, but not limited to, any violations and sanctions under the Code; and (B) certifies the Company’s adoption of procedures reasonably necessary to prevent Access Persons from violating the Code.

The CCO and compliance area will be responsible for handling, documenting and resolving complaints. The CCO will notify promptly Legal and or Fund CCO if applicable.

M. Disclosure of Portfolio Holdings

Employees of Bright Rock may have access to the portfolio holdings of one or more Funds. Each employee has adopted a code of ethics pursuant to Rule 17j-1 of the Investment Company Act designed to prohibit fraudulent or deceitful conduct. The following policy is intended to elaborate on such codes of ethics to ensure that the disclosure of information about the Funds’ portfolio holdings is in the best interest of Fund shareholders.

Policy: Information about the Funds’ portfolio holdings should not be distributed to any person unless:

• The disclosure is required to respond to a regulatory request, court order or other legal

proceedings;

• The disclosure is to a mutual fund rating or, statistical agency or person performing

similar functions who has if necessary signed a confidentiality agreement with the Fund;

• The disclosure is made to internal parties involved in the investment process,

administration or custody of the Funds, including but not limited to U.S. Bancorp Fund

Services, LLC (“USBFS”) and the Trust’s Board of Trustees;

• The disclosure is (a) in connection with a quarterly, semi-annual or annual report that is

available to the public or (b) relates to information that is otherwise available to the

public (e.g. portfolio information that is available on a Fund’s website); or

• The disclosure is made pursuant to prior written approval of the Chief Compliance

Officer of Bright Rock and to the TPM, or other person so authorized.

Any suspected breach of this obligation should be reported immediately to the Bright Rock Compliance Officer.

N. CODE OF ETHICS RECORDS

The Company, at its principal place of business, will maintain records with respect to the Code of Ethics in the manner and to the extent set out below and will make

such records available to the SEC at any time and from time to time for reasonable periodic, special or other examination:

(A)A copy of the Company’s Code of Ethics that is effect, or at any time in the past five years was in effect, must be maintained in an easily accessible place;

(B)A record of any violation of the Code, and of any action taken as a result of the violation, must be maintained in an easily accessible place for at least five years after the end of the fiscal year in which the violation occurs;

(C)A copy of each report made by an Access Person as required by the Code of Ethics, including any information provided in broker trade confirmations or account statements in lieu of such reports, must be maintained for at least five years after the end of the fiscal year in which the report is made or the information is provided, the first two years in an easily accessible place;

(D)A record of all persons, currently or within the past five years, who are or were Access Persons, or who are or were responsible for reviewing Access Person reports, must be maintained in an easily accessible place; and

(E)A copy of each COE Report must be maintained for at least five years after the end of the fiscal year in which it is made, the first two years in an easily accessible place;

(F)A record of any decision, and the reasons supporting the decision, to approve the acquisition by investment personnel of New Issue Securities or any securities offered in a “private placement,” for at least five years after the end of the fiscal year in which the approval is granted; and

(G)Since the Company requires pre-approval of all trades, records of those pre-approvals must also be maintained.

Exhibit A

Bright Rock Capital Management LLC

Code of Ethics

Initial/Annual Holdings Report

Holdings Report for Year Ended ______

Please list all brokers, dealers and banks with whom you maintain accounts in which securities are held. Attach a copy your most recent statement(s).

____________________________________

____________________________________

____________________________________

____________________________________

| | | | | | | | |

| | |

| Signature | | Date |

| | |

| Receipt Acknowledged: | | |

| | |

| | Date |

Exhibit B

Rockland Trust Company

Bright Rock

Personal Security Transaction Report

Quarter ended:

Name: Date:

After reviewing the attached bank policy and definitions, I have determined that:

I do not have any reportable transactions this quarter.

I have the following reportable transactions this quarter:

List below or attach a copy of the relevant statement(s) or trade advice

The information you report will be reviewed by the Senior Investment Officer and otherwise be treated as confidential information made available to Examiner’s only upon request.

Description of Security Trade Date Buy/Sell # Shares Price $Amount Broker

____ attached

(initial here if statement or trade advice is attached

______________________________

(Signature)

(After signing this report, please return it to Garth O’Leary.

Do not respond by e-mail.)

Security Transaction Reporting by Officers and Employees

ROCKLAND TRUST COMPANY /BRIGHT ROCK CONFLICT OF INTEREST Policy # 9

DATE: September 10, 2008

Report of Personal Investment Transactions

Employees of the Investment Management Group will comply with Part 344 of the Federal Deposit Insurance Corporation regulations.

Part 344 of the Federal Deposit Insurance Corporation regulations require that bank officers and other employees who: 1) Make recommendations or decisions for the accounts of customers; 2) participate in the determination of such recommendations or decisions or; 3) in connection with their duties, obtain information concerning which securities are being purchased or sold or recommended for such action, must report to the Bank, within 30 days after the end of each calendar quarter, all transactions in securities made by them or on their behalf, either at the Bank or elsewhere, in which they have a beneficial interest.

These reports will be reviewed by the Chief Investment Officer to monitor for any potential conflict of interest.

Excluded from this requirement are:

1)Transactions for the benefit of an officer or other employee over which he or she has no direct or indirect influence or control;

2)Transactions in notes (including commercial paper), bankers acceptances and

i.Similar obligations having a maturity not exceeding nine months;

3)Transactions in U.S. government or federal agency obligations;

4)Transaction in mutual fund shares, including money market funds,

5)All transactions involving in the aggregate $10,000 or less principal amount during the calendar quarter.

Definition of Security: “Security” means any interest or instrument commonly known as a “security” whether in the nature of debt or equity, including any stock, bond, note, debenture, evidence of indebtedness or any participation in or right to subscribe to or purchase any of the foregoing. The term “security” does not include (1) A deposit or share account in a federally insured depository institution, (2) A loan participation, (3) A letter of credit or other form of bank indebtedness incurred in the ordinary course of business, (4) Currency, (5) Any note, draft, bill of exchange, or bankers acceptance which has a maturity at the time of issuance of not exceeding nine months, exclusive of days of grace, or any renewal thereof the maturity of which is likewise limited, (6) Units of collective investment fund, (7) Interests in a variable amount (master) note of a borrower of prime credit, or (8) U. S. Savings Bonds.

Definition of Beneficial Interest: In addition to the usual definition of beneficial interest, for the purpose of this policy it is considered that an individual subject to the reporting requirement has a beneficial interest in security transactions of or for his or her spouse and/or minor children. Accordingly, transactions of or for these family members are to be included in the aggregation and, when the $10,000 reporting threshold is met, included the officer’s or employee’s report.

Exhibit C

Bright Rock Capital Management LLC

Code of Ethics

Compliance Certificate

The undersigned employee of Bright Rock Capital Management LLC

(the “Company”), hereby certifies that he or she has read and understood the Company’s current memorandum entitled “Written Policies and Procedures Under Rule 206(4)-7” and that he or she will conduct himself or herself professionally in complete accordance with the requirements and standards described therein and will comply with all applicable federal and state securities and other laws and regulations regulating his or her conduct as an employee of the Company.

The undersigned employee has had the opportunity to ask questions of and receive answers from the Chief Compliance Officer and other persons acting on behalf of the Chief Compliance Officer with respect to the Investment Advisers Act of 1940 and other laws and regulations applicable to the undersigned in connection with his or her employment with the Company, and the undersigned employee acknowledges that such questions have been answered to his or her full satisfaction.

The undersigned employee acknowledges that:

(i) he or she is responsible for his or her actions under the law and is required to be sufficiently familiar with the Investment Advisers Act of 1940 and other laws and regulations that may govern his or her conduct as an employee of the Company;

(ii) the Company is relying upon the undersigned employee’s certification and acknowledgments contained herein and that the failure to comply with the policy set forth in the above-referenced Manual and with applicable federal and state securities and other laws and regulations may subject the Company and the undersigned to substantial liabilities including imprisonment and fines; and

(iii) the Company may dismiss the undersigned employee from his or her employment for failure to comply with the policies set forth in the above-referenced Manual and applicable federal and state securities and other laws and regulations governing the undersigned’s conduct as an employee of the Company.

(iiii) the employee also certifies that they are in compliance with the Bright Rock Capital Management Social Media Policy

______________________________

Signature.

_____________________________

Name. Please Print.

_____________________________

II. PORTFOLIO MANAGEMENT

A. TRADE ALLOCATION AND AGGREGATION POLICY AND PROCEDURES

1. Allocation Guidelines

A. Pre-Execution Allocations

Allocations of investment opportunities among the Fund, client accounts and affiliate accounts must be made in a fair and equitable manner. As a general rule, allocations among accounts with the same or similar investment objective should be made pro rata based on the total assets under management in the accounts. Allocation decisions should be made and documented before an order is placed. There should be no allocation to an account or set of accounts based on account performance or the amount or structure of fees. Allocations of limited opportunity investments such as IPOs will be allocated among eligible accounts in the same manner as other securities. However, since all clients must be accorded individual investment advice and treatment, an account’s allocation may be eliminated, reduced, or increased because of any of the following factors:

i. Specific investment restrictions, guideline limitations, investment policies, investment objectives, or client risk tolerance;

ii. Existing security positions, existing sector concentrations or a need to rebalance;

iii. Current cash position, outstanding commitment amounts or liquidity requirements; and

iv. Transaction tax consequences

With prior disclosure to and consent from the client, the Company may aggregate orders for the purchase or sale of securities on behalf of the client with orders on behalf of other portfolios the Company manages, or with orders for the Company’s account or that of its employees. Securities purchased or proceeds of securities sold through aggregated orders are allocated to the account of each portfolio that bought or sold such securities at the average execution price. If less than the total of the aggregated orders is executed, purchased securities or proceeds will generally be allocated pro rata among the participating portfolios in proportion to their planned participation in the aggregated orders.

B. Post-Execution Allocations

Post-execution allocations of orders should be used only where an aggregated order is not filled in its entirety. Such allocations must be consistent with treating all client accounts fairly and equitably Post-execution allocations must be determined by the close of business on the trade date and must comply with the same general guidelines set forth above for pre-execution allocations. 2. Allocation Procedures

A. Preparation of Allocation Statement

Prior to entering an order, the portfolio manager will prepare a statement in written or electronic form such as the trade blotter or order management system (the “Allocation Statement”) specifying participating accounts and the allocation of the order among such accounts.

B. Allocation of Executed Orders

If an aggregated order is filled in its entirety, it will be allocated among participating accounts in accordance with the Allocation Statement. If an aggregated order is partially unexecuted at the end of a trading day, the executed trades will be allocated among participating accounts pro rata based upon the Allocation Statement unless allocated post-execution pursuant to Section I, Part B above. Notwithstanding the foregoing, all accounts need not be given their pro rata share of a filled order if full pro rata allocation would result in certain clients receiving an odd share amount or would result in increased transaction costs due to per ticket charges (vs. per share charges). Pro rata amounts allocated may also be rounded depending on the size of the client account. The Company will endeavor to distribute partially filled orders among clients so that all clients are treated fairly over the long term.

C. When Full Aggregation is not Possible

In some circumstances, it may be appropriate to buy or sell a security on behalf of more than one advisory client account over a period of time. In those instances, although it may not be possible for aggregated orders to be entered for all of the Company’s

clients, the portfolio manager still must allocate advisory clients’ orders on an equitable basis.

D. Procedures for Related Party Accounts

In aggregated trades involving related party accounts (proprietary accounts of the Company, affiliated accounts, accounts owned beneficially by any individual officer or Employee of the Company or a family member of such officer or Employee, or pooled investments in which any of these participates), the additional procedures set forth below are also to be followed to ensure that such trades are allocated fairly and equitably among all clients.

oAny portfolio manager who is responsible for both client accounts and related party accounts shall determine prior to each transaction in which client and related party orders may be aggregated whether such aggregation is in the interests of best execution of the trade.

oFor related party accounts owned entirely by the Company, by officers or employees of the Company or by family members of such officers and employees, in the event that an aggregated trade is partially filled such accounts will have their allocation reduced to zero before any reductions are made in the allocation to client accounts (this sentence does not apply to pooled investment vehicles in which the Company, its officers or employees or their family members participate as investors along with clients of the Company). If such trades involving related party accounts are otherwise allocated on a basis different from that specified in the Allocation Statement, the reason for any such difference must be explained in writing and approved by the Chief Compliance Officer no later than the close of the markets on the day the order was executed.

oIn conducting the review of trade allocations, the Chief Compliance Officer (or his/her designee) will review specifically allocations of trades to related party accounts to ascertain that such accounts have not been favored over other accounts. Periodically (but not less than quarterly), the Chief Compliance Officer will review all trades in which securities are allocated to related party accounts specifically to ascertain that such accounts were not favored over the long term over other client accounts in the allocation process.

o The Company may block trade with their affiliates when appropriate. In aggregated trades involving affiliated accounts and the Fund, the portfolio managers and trader use the additional procedures set forth above to ensure that such trades are allocated

fairly and equitably among all clients to the extent possible. The trade blocks executed on the same day with the same security will receive an average price for the entire block. Any exceptions to the procedure will be documented with the reason.

oA dispersion analysis will be performed quarterly in the Bright Rock Compliance Committee to compare the Bright Rock Large Cap Composite vs. Rockland Trust Tax Exempt Composite.

B. CONSISTENCY WITH CLIENT OBJECTIVES AND RESTRICTIONS AND LEGAL MANDATES

It is essential that each client’s portfolio conform with the client’s investment objectives as well as with any specific investment restrictions or limitations imposed by the client. The portfolio manager in charge of the client account has primary responsibility for ensuring consistency between the portfolio and the applicable objectives, guidelines and restrictions. Portfolio managers will use software tools, whenever possible, to assist in tracking and monitoring the performance of the portfolios (including the Funds), and will work with Employee traders and outside brokerage firms to put in place procedures to prevent violation of such investment restrictions or limitations (such as automatically blocking a short order for an account that does not permit short selling). A portfolio manager must review each account under its management no less frequently than quarterly for consistency with the applicable objectives, guidelines and restrictions; in some cases more frequent reviews may be appropriate. Portfolio managers should also familiarize themselves with applicable regulations for short sales, margin and the use of commodities, and should review portfolios which utilize such techniques for compliance with any such regulations as part of the quarterly review.

C. PROXY VOTING

The Company has adopted a written proxy voting policy and related procedures which are intended to assure that the Fund and client securities are voted in the best interests of the client, and which address material conflicts of interest that may arise between the investment adviser and its clients. A copy of the policy is set forth below. All Employees involved in portfolio management and/or the voting of client proxies must familiarize themselves with and adhere to this policy, a copy of which is set forth below. A summary of the Company’s proxy voting policies is set forth in the Company’s Form ADV Part II, along with information about how each client may learn of the Company’s

specific votes of proxies with respect to the client’s securities. The Company will furnish a copy of the policy to clients upon request.

VOTING PROXIES

The voting or non-voting of proxies shall be the responsibility of the Portfolio Managers. The following polices are guidelines in voting the proxies:

Generally, proxies will be voted along management’s guidelines as indicated on the proxy. Any non-routine matters (e.g., proxy fights and issues of similar significance) will be referred to the Investment Policy Committee.

A record of our proxy voting is maintained by a third party proxy voting service and can be made available upon request as to the date and number of shares voted.

Where Bright Rock has shared authority, Bright Rock will vote the proxy unless otherwise directed.

Bright Rock has given the authority for US Bank to retrieve the proxy log information directly from BroadRidge, this is to help with the completion of Form N-PX.

D. TRADING ERRORS

Any trading errors must be reported immediately to the Chief Compliance Officer. The Chief Compliance Officer will determine whether it is possible and appropriate for the trade to be unwound. If the trade cannot be unwound, the Chief Compliance Officer will review the error and determine whether any clients have been harmed. If they have, the Company will reimburse the affected clients in full. If a client benefits from a trading error, that client will generally be entitled to keep such benefit. The Chief Compliance Officer will review any trading errors to determine if new policies and procedures should be adopted to prevent a similar error from occurring in the future. The Chief Compliance Officer maintains a Trade Error Log with all the applicable details of the error. All trade errors will be reported to the TPM CCO.

E. CROSS TRADES

In certain cases, it may make sense for two client accounts to engage in a trade directly. Such cross trades can result in lower commission expenses for the clients. Cross trades require the prior written approval of both the Chief Compliance Officer and the clients. The Company shall not charge any commission or other fee in connection with facilitating a cross trade, and any such trade should be conducted at the then current market price. Cross trades may not be conducted with any ERISA accounts. If the cross

trade involves a mutual fund, the Chief Compliance Officer will also determine whether the cross-trade complies with Rule 17a-7 of the Investment Company Act.

F. Market Timing and Rule 22c-2 Procedures

Bright Rock will follow the TPM’s Market Timing & Excessive Trading Policy and Procedures adopted pursuant to Rule 22c-2 under the Investment Company Act of 1940.

G. Liquidity Risk Management Program