2 The presentation is dated as of June 24, 2026 and speaks as of the date unless

otherwise specified. FORWARD-LOOKING STATEMENTS This presentation contains statements that may constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, including those related to the

expectations for future periods, possible or assumed future results of operations, financial conditions, liquidity and related sources or needs, business and/or integration strategies, plans and synergies, supply chain, growth opportunities, and

performance at our stores. There are a number of known and unknown risks, uncertainties, and other factors that may cause our actual results to differ materially from any results expressed or implied by these forward-looking statements, including

but not limited to the execution of our strategic plan, the integration and financial performance of acquired stores, wholesale fuel, inventory and ingredient costs, distribution challenges and disruptions, the impact and duration of conflicts in

oil producing regions or other geopolitical disruptions, as well as other risks, uncertainties and factors which are described in the Company’s most recent annual report on Form 10-K and quarterly reports on Form 10-Q, as filed with the

Securities and Exchange Commission and available on our website. Any forward-looking statements contained in this presentation represent our current views as of the date of this presentation with respect to future events, and Casey’s disclaims

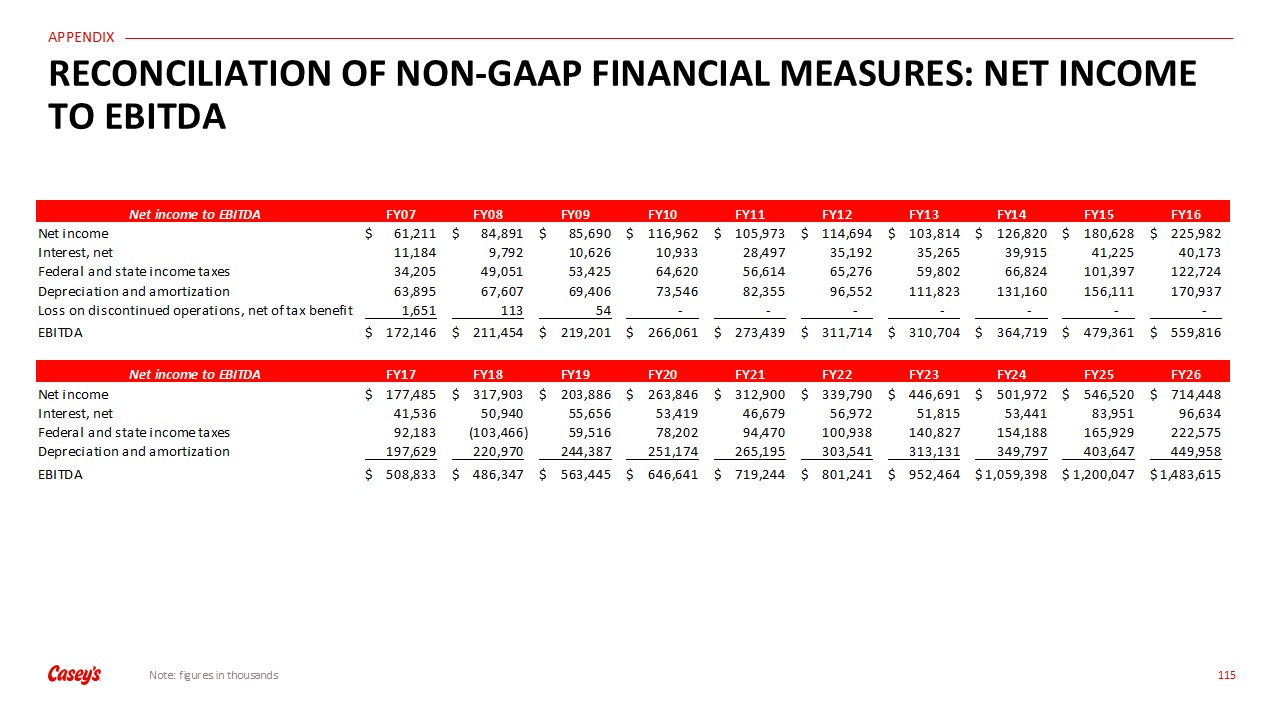

any intention or obligation to update or revise any forward-looking statements in the presentation whether as a result of new information, future events, or otherwise. USE OF NON-GAAP MEASURES This presentation includes references to "EBITDA,"

which we define as net income before net interest expense, income taxes, and depreciation and amortization. EBITDA is not presented in accordance with accounting principles generally accepted in the United States ("GAAP"). We believe EBITDA is

useful to investors in evaluating our operating performance because securities analysts and other interested parties use such calculations as a measure of financial performance and debt service capabilities, and it is regularly used by management

for internal purposes including our capital budgeting process, evaluating acquisition targets, and assessing store performance. EBITDA is not a recognized term under GAAP and should not be considered a substitute for net income, cash flows from

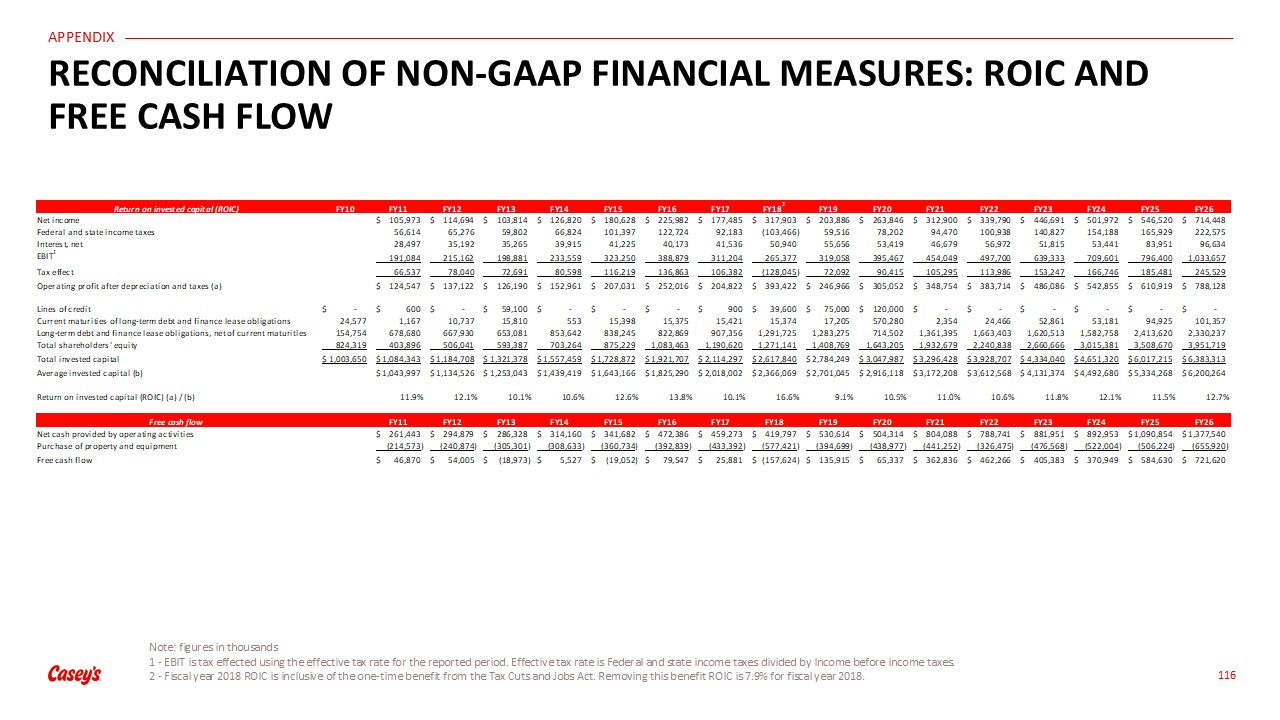

operating activities or other income or cash flow statement data. This presentation also includes references to “free cash flow," which we define as net cash provided by operating activities less purchases of property and equipment. Free cash

flow is not presented in accordance with GAAP. We believe free cash flow is useful to investors in evaluating our cash generation because securities analysts and other interested parties use such calculations as a measure of financial

performance, liquidity, and debt service capabilities, and it is regularly used by management for internal purposes including our capital budgeting process, evaluating acquisition targets, and evaluating debt service. This presentation also

includes references to “return on invested capital” or “ROIC,” which we define as operating profit after taxes (net income, plus net interest expenses, income taxes, tax effected) divided by average invested capital. ROIC is not presented in

accordance with GAAP. We believe ROIC is useful to investors as a measure of financial performance and prudent capital allocation and is regularly used by management for internal purposes including our capital budgeting process, evaluating

acquisition targets and assessing company performance. Neither EBITDA, free cash flow, nor ROIC are recognized terms under GAAP and should not be considered a substitute for net income, net cash provided by operating activities or other income or

cash flow statement data. EBITDA, free cash flow, and ROIC have limitations as an analytical tool, and should not be considered in isolation or as a substitute for analysis of our results as reported under GAAP. We strongly encourage investors to

review our financial statements and publicly filed reports in their entirety and not to rely on any single financial measure. Because non-GAAP financial measures are not standardized, EBITDA, free cash flow, and ROIC, as defined by us, may not be

comparable to similarly titled measures reported by other companies. It therefore may not be possible to compare our use of this non-GAAP financial measure with those used by other companies. For reconciliations of EBITDA, free cash flow, and

ROIC to GAAP net income and net cash generated by operating activities, for the completed applicable period shown, see the appendix attached hereto.