Note 1 ORGANIZATION

Aurelion Inc. (formerly known as “Prestige Wealth Inc.”, “PWI”, or the “Company”) is a limited company established under the laws of the Cayman Islands on October 25, 2018. It is engaged in providing private wealth management services and asset management to high net worth and ultra-high net worth individuals and enterprises through its subsidiaries.

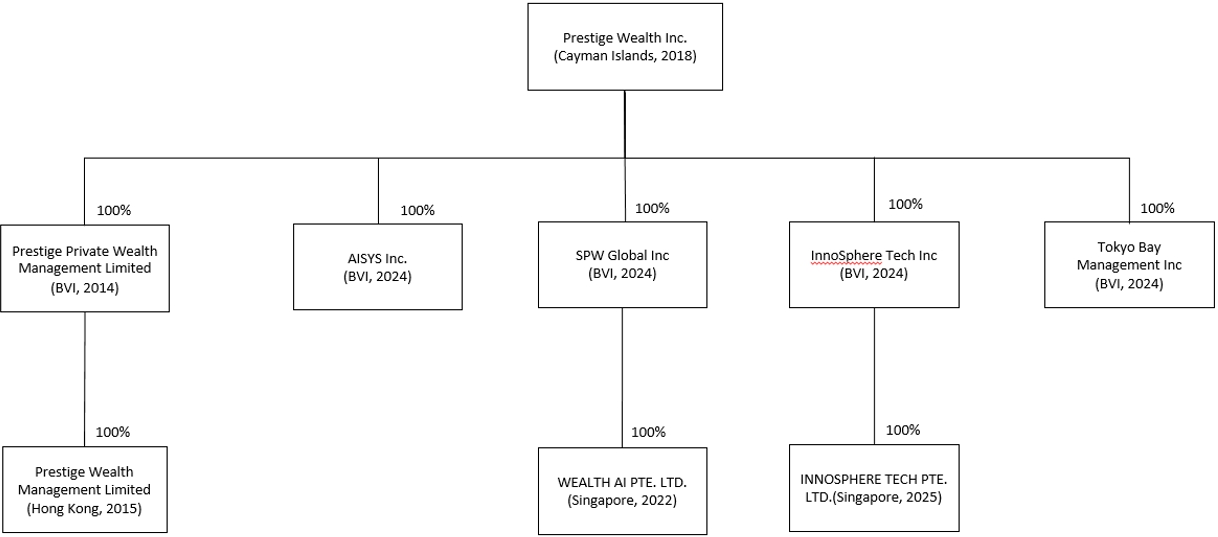

PRESTIGE PRIVATE WEALTH MANAGEMENT LIMITED (“PPWM”), which is 100% controlled by PWI, was incorporated in the British Virgin Islands on May 23, 2014, and is engaged in providing private wealth management services to third parties and earns referral fees.

Prestige Wealth Management Limited (“PWM”) is a wholly owned subsidiary of PPWM. It was established on January 26, 2015 in Hong Kong, which provides private wealth management services to third parties.

AISYS Inc. (“AISYS”) was incorporated in the British Virgin Islands on May 10, 2024 and is 100% controlled by PWI.

SPW Global Inc (“SPW”) was incorporated in the British Virgin Islands on March 11, 2024, which in turn wholly owns Wealth AI PTE LTD. (“Wealth AI”). On November 4, 2024, PWI completed its acquisition of all shares of SPW.

Wealth AI PTE LTD. (“Wealth AI”) is a wholly-owned subsidiary of SPW. It was established May 20, 2022 in Singapore, and offers personalized, cost-effective wealth management solutions using artificial intelligence.

Tokyo Bay Management Inc. (“Tokyo Bay”) was incorporated in the British Virgin Islands on April 05, 2024, Tokyo Bay is a company based in Tokyo, Japan, providing wealth management services, family affairs services, lifestyle management services and related value-added services to high-net-worth clients in Japan. PWI completed its acquisitions of Tokyo Bay on December 16, 2024.

InnoSphere Tech Inc. (“InnoSphere Tech”) was incorporated in the British Virgin Islands on October 28, 2024, and it is a technology company that leverages its advantages in web scraping technology to collect data on finance, wealth management, and related industries according to international standards. PWI completed its acquisitions of InnoSphere Tech on December 16, 2024.

InnoSphere Tech Pte. LTD. (“InnoSphere Singapore”) is a wholly-owned subsidiary of InnoSphere Tech. It was established on February 20, 2025 in Singapore, and it focuses on developing platforms integrating AI based technology.

Reorganization

In anticipation of an initial public offering (“IPO”) of its equity securities, the Company undertook a reorganization on December 27, 2018, and became the ultimate holding company of PPWM, PWM, PAI, PAM, PGAM, PGCI, PWAI and AISYS, which were all controlled by the same shareholders. The Company together with its subsidiaries were effectively controlled by the same shareholders before and after the reorganization and therefore the reorganization is considered under common control and was accounted for similar to the pooling method of accounting. The accompanying consolidated financial statements have been prepared as if the current corporate structure has been in existence throughout the periods presented. The consolidation of the Company and its subsidiaries (collectively referred to the “Group”) has been accounted for at historical cost as of the beginning of the first period presented in the accompanying consolidated financial statements.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 1 ORGANIZATION (cont.)

Disposal of Prestige Asset International Inc.(“PAII”) and discontinued operation

On June 25, 2025, the Group entered into an agreement with a third-party to sell its 100% interests in PAII for $55,534. The consolidated financial results of PAII and its wholly-owned subsidiaries were deconsolidated from the Groups financial statements beginning June 26, 2025.

The purchase price was settled entirely through a waiver and release of all outstanding receivables due from the Seller to the Group as of the agreement date. Accordingly, no cash or other consideration was received by the Group in connection with this disposal, and no receivable or payable remains outstanding after the transaction.

The gain on the disposal of PAII was calculated as the difference between:

| (i) | The fair value of the consideration received |

| (ii) | Share of the carrying value of net assets disposed of, as of the date of the transaction |

| | | Amounts | |

| | | | |

| The fair value of the consideration received | | | — | |

| | | | | |

| Less: net identifiable liabilities to be disposed | | | 54,121 | |

| Gain on disposal of subsidiaries | | | 54,121 | |

Below are the assets and liabilities of PAII as of date of disposal:

| | | Amounts | |

| Assets | | | |

| Cash | | | 366 | |

| Accounts receivables | | | 8,790 | |

| Tax receivable | | | 49,491 | |

| Prepaid expenses and other assets | | | 7,824 | |

| Total Assets | | | 66,471 | |

| | | | | |

| Liabilities | | | | |

| Accrued expenses and other current liabilities | | | (120,592 | ) |

| Total liabilities | | | (120,592 | ) |

| Net identifiable liabilities to be disposed | | | (54,121 | ) |

As of March 31, 2026 and September 30, 2025, the Group has reported related assets and liabilities as a discontinued operation. This classification is required under ASC205-20-45 when a disposal represents a strategic shift that has a major effect on the entity’s operations and financial results.

The disposal of the related business qualifies as such a strategic shift, primarily based on its revenue significance. The operations represented a distinct product line that accounted for approximately nil of the Group’s total consolidated revenue during the six months ended March 31, 2026 and 2025, but accounted for 59% and 78% of the Group’s total consolidated revenue during the years ended September 30, 2024 and 2023. This constitutes a significant portion of the Group’s operations, and its disposal represents a strategic shift with a major effect on the Group’s ongoing revenue profile.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 1 ORGANIZATION (cont.)

The following tables represent the financial information of the business classified as discontinued operations for the six months ended March 31, 2026 and 2025:

| | | For the six months ended

March 31, | |

| | | 2026 | | | 2025 | |

| DISCONTINUED OPERATIONS | | | | | | |

| Total net revenue | | | — | | | | — | |

| | | | | | | | | |

| Operation cost and expenses | | | | | | | | |

| Selling, general and administrative expenses | | | — | | | | 133,749 | |

| Total operation cost and expenses | | | — | | | | 133,749 | |

| | | | | | | | | |

| Other income | | | — | | | | (9,406 | ) |

| | | | | | | | | |

| Loss before income taxes benefit | | | — | | | | (124,343 | ) |

| Income taxes benefit | | | — | | | | 9,661 | |

| Net loss from discontinued operations | | $ | — | | | $ | (114,682 | ) |

| | | For the six months ended

March 31, | |

| | | 2026 | | | 2025 | |

| CASH FLOWS FROM OPERATING ACTIVITIES | | | | | | |

| Net losses | | | — | | | | (114,682 | ) |

| Adjustments to reconcile net loss to net cash used in operating activities: | | | | | | | | |

| Amortization of Right-of-use assets | | | — | | | | 99,343 | |

| Interest on Lease liabilities | | | — | | | | 5,030 | |

| Gain on Lease Termination | | | — | | | | (9,386 | ) |

| Changes in operating assets and liabilities | | | — | | | | 3,730 | |

| Net cash used in operating activities | | | — | | | | (15,965 | ) |

| | | | | | | | | |

| Effect of foreign exchange rate changes on cash and cash equivalents and restricted cash | | | — | | | | 14,691 | |

| | | | | | | | | |

| Net decrease in cash and cash equivalents and restricted cash | | | — | | | | (1,274 | ) |

| Cash and cash equivalents and restricted cash at the beginning of year | | | — | | | | 1,720 | |

| Cash and cash equivalents and restricted cash at the end of year | | $ | — | | | $ | 446 | |

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 1 ORGANIZATION (cont.)

Group chart of the Group after reorganization as of March 31, 2026 is set out below:

Details of the subsidiaries of the Group after reorganization are set out below:

| Name | | Date of

Incorporation | | | Place of

incorporation | | Percentage of

effective ownership | | Principal Activities |

| Subsidiaries | | | | | | | | | | |

| PRESTIGE PRIVATE WEALTH MANAGEMENT LIMITED (“PPWM”) | | | May 23, 2014 | | | British Virgin Islands | | 100% | | Private wealth management service provider |

| Prestige Wealth Management Limited (“PWM”) | | | January 26, 2015 | | | Hong Kong | | Wholly owned subsidiary of PPWM | | Private wealth management service provider |

| AISYS Inc. (“AISYS’) | | | May 10, 2024 | | | British Virgin Islands | | 100% | | Inactive |

| SPW Global Inc (“SPW”) | | | March 11, 2024 | | | British Virgin Islands | | 100% | | Inactive |

| Wealth AI PTE LTD. (“Wealth AI”) | | | May 20, 2022 | | | Singapore | | Wholly owned subsidiary of SPW | | Wealth management solutions provider |

| Tokyo Bay Management Inc. (“Tokyo Bay”) | | | April 05, 2024 | | | British Virgin Islands | | 100% | | Wealth management service provider |

| InnoSphere Tech Inc. (“InnoSphere Tech”) | | | October 28, 2024 | | | British Virgin Islands | | 100% | | Service provider based on AI technology |

| InnoSphere Tech Pte. LTD. (“InnoSphere Singapore”) | | | February 20, 2025 | | | Singapore | | Wholly owned subsidiary of InnoSphere Tech | | Service provider based on AI technology |

Note 2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Basis of presentation and consolidation

The accompanying consolidated balance sheet as of September 30, 2025, which has been derived from audited financial statements, and the unaudited interim consolidated financial statements as of March 31, 2026 and for the six months ended March 31, 2026 and 2025 have been prepared pursuant to the rules and regulations of the Securities and Exchange Commission (the “SEC”). A subsidiary is an entity (including a structured entity) that is directly or indirectly, controlled by the Company. Control is achieved when the Group is exposed, or has rights to, variable returns from its involvement with the investee and has the ability to affect those returns through its power over the investee (i.e., existing rights that give the Group the current ability to direct the relevant activities of the investee).

Generally, there is a presumption that a majority of voting rights results in control. When the Company holds less than a majority of the voting or similar rights of the investees, the Group considers all relevant facts and circumstances in assessing whether it has power over an investee, including: (a) the contractual arrangements with the other vote holders of the investee; (b) rights arising from other contractual arrangements; and (c) the Group’s voting rights and potential voting rights.

The financial statements of the subsidiaries are prepared for the same reporting period as the Company, using consistent accounting policies. The results of subsidiaries are consolidated from the date on which the Group obtains control and continue to be consolidated until the date such control ceases. All inter-company transactions and balances have been eliminated upon consolidation.

The Group reassesses whether or not it controls an investee if facts and circumstances indicate that there are changes to one or more of the three elements of control described above. A change in the ownership interest of a subsidiary, without a loss of control, is accounted for as an equity transaction.

If the Group loses control over a subsidiary, it derecognises the related assets (including goodwill), liabilities, any non-controlling interest and the exchange fluctuation reserve; and recognises the fair value of any investment retained and any resulting surplus or deficit in profit or loss. The Group’s share of components previously recognised in other comprehensive income is reclassified to profit or loss or retained profits, as appropriate, on the same basis as would be required if the Group had directly disposed of the related assets or liabilities.

This basis of accounting involves the application of accrual accounting and consequently, revenues and gains are recognized when earned, and expenses and losses are recognized when incurred. The Group’s financial statements are expressed in U.S. Dollars.

In February 2015, the Financial Accounting Standards Board (“FASB”) issued amended consolidation guidance with the issuance of ASU No. 2015-02, Consolidation (Topic 810): Amendments to the Consolidation Analysis (“ASU 2015-02”). The revised consolidation guidance, among other things, (i) modifies the evaluation of whether limited partnerships and similar legal entities are VIEs, (ii) eliminated the presumption that a general partner should consolidate a limited partnership, and (iii) modifies the consolidation analysis of reporting entities that are involved with VIEs through fee arrangements and related party relationships. In evaluating whether the investment funds in the legal form of limited partnership the Group manages as general partner should be consolidated or not, the Group firstly assesses whether there is any interest it has constituted a variable interest. The Group concludes that (i) the service fees it earns, including carried interest earned in the capacity of general partner, are commensurate with the level of effort required to provide such services, (ii) the Group does not hold other interest in the investment funds that individually, or in aggregate, would absorb more than an insignificant amounts of expected loss or receive more than an insignificant amount of the expected residual returns from the investment funds, (iii) the services arrangement includes only terms, conditions or amounts that are customarily present and at arm’s length, therefore are not deemed as variable interests. For purposes of the assessment, any variable interest in an entity that is held by a related party of the decision maker or service provider was considered in the analysis. Specifically, the Group includes its direct variable interests in the entity and its indirect variable interests in the entity held through related parties, considered on a proportionate basis. After evaluating the impact of the above guidance, the Group determined that there was no investment fund that should be consolidated as of March 31, 2026.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

Liquidity and going concern

The Group’s unaudited consolidated financial statements have been prepared on a going concern basis, which contemplates the realization of assets and liquidation of liabilities during the normal course of operations. As of March 31, 2026, the Group had cash and cash equivalents of $2,071,983 and generated a net income of $16,653,306 and cash outflows of $2,909,187 from operating activities for the six months ended March 31, 2026. To mitigate the liquidity dynamic and support the Group’s going concern structure, management has developed a feasibility plan. The Group holds a significant portfolio of XAUt, which constitutes highly liquid digital assets pegged to physical gold. Management closely monitors the market depth and historical liquidation profiles of XAUt. In the event of immediate funding requirements, the Group is prepared to orderly liquidate a portion of its uncollateralized XAUt holdings through regulated third-party trading platforms and standard industry channels. Based on current market conditions and conservative haircut testing, management believes the realizable net proceeds will be sufficient to support the Group’s operational requirements and sustain its ongoing business activities over the next twelve months. Accordingly, management has concluded that the Group has adequate resources to continue operations for the foreseeable future, and no conditions or events raise substantial doubt about the Group’s ability to continue as a going concern. The consolidated financial statements do not include any adjustments related to liquidity uncertainties.

Use of estimates

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities as of the date of the financial statements and the reported amounts of revenues and expenses during the periods presented. Significant accounting estimates reflected in the Group’s consolidated financial statements include, but are not limited to, provision for credit losses of accounts receivable, contract assets, note receivables, prepaid expense and other receivables recorded in prepaid expenses and other assets and amounts due from related parties, assessment for impairment of long-lived assets, and the assessment of the valuation allowance on deferred tax assets. Actual results could differ from these estimates.

Fair value measurement

The Group applies ASC Topic 820, Fair Value Measurements and Disclosures which defines fair value, establishes a framework for measuring fair value and expands financial statement disclosure requirements for fair value measurements.

ASC Topic 820 defines fair value as the price that would be received from the sale of an asset or paid to transfer a liability (an exit price) on the measurement date in an orderly transaction between market participants in the principal or most advantageous market for the asset or liability.

ASC Topic 820 specifies a hierarchy of valuation techniques, which is based on whether the inputs into the valuation technique are observable or unobservable. The hierarchy is as follows:

Level 1 inputs to the valuation methodology are quoted prices (unadjusted) for identical assets or liabilities in active markets.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

Level 2 inputs to the valuation methodology include quoted prices for similar assets and liabilities in active markets, and inputs that are observable for the assets or liability, either directly or indirectly, for substantially the full term of the financial instruments.

Level 3 inputs to the valuation methodology are unobservable and significant to the fair value. Unobservable inputs are valuation technique inputs that reflect the Group’s own assumptions about the assumptions that market participants would use in pricing an asset or liability.

Financial assets and liabilities of the Group primarily consist of cash and cash equivalents, XAUt receivable host contract, other receivables, amount due to related parties, other payable and accrued liabilities. As of March 31, 2026, the carrying values of these financial instruments approximated their fair value.

The Group determines the fair value of crypto assets held (except for XAUt receivable host contract) and the embedded derivative component of XAUt on a recurring basis in accordance with ASC 820 Fair Value Measurement, based on quoted prices on the principal market, Level 1 inputs, based on all information that is reasonably available.

Cash and cash equivalents

Cash and cash equivalents consist of the Group’s demand deposit placed with financial institutions.

XAUt

XAUt tokens are digital assets issued by Tether Gold representing a contractual right to an undivided specific interest in physical gold. The Group accounts for XAUt tokens as hybrid financial instruments under ASC 815, Derivatives and Hedging. These instruments are bifurcated into two components:

Receivable Host Contract: The host contract is characterized as a non-derivative financial host representing a prepaid receivable from the issuer. It is initially measured at its allocated cost and subsequently carried at amortized cost. The host contract is subject to the expected credit losses (“ECL”) model under ASC 326, which requires the Group to maintain an allowance for expected credit losses based on the issuer’s credit risk.

Embedded Derivative: The feature providing the right to receive the value of one fine troy ounce of gold is identified as an embedded derivative because its value fluctuates based on the underlying price of gold. This embedded derivative is bifurcated from the host contract as its economic characteristics and risks are not clearly and closely related to the financial host. It is measured at fair value on a recurring basis, with changes in fair value recognized in operating income within the consolidated statements of operations. The Group determines the fair value using observable market inputs, primarily quoted prices of XAUt in active markets (Level 1).

XAUt collateral receivable from related party

On October 10, 2025, Prestige Wealth Management Limited, a wholly-owned subsidiary of the Company, as the borrower, entered into a $50 million term loan agreement (the “Loan Agreement”) with Northstar Digital (HK) Limited, as lender. The term loan is for a three-year period and bears interest at 6% per annum, with the principal and all accrued interest due and payable in a single lump-sum payment at maturity, and will be secured by first priority perfected liens on XAUt of the Group with an aggregate market value of $66,666,667 to be held in a collateral account. On December 31, 2025, Prestige Wealth Management Limited entered into an amendment agreement with Northstar Digital (HK) Limited to permit partial early repayment of the term loan. Collateral pledged to the related party is shown under “XAUt collateral receivable from related party” in the consolidated balance sheets. XAUt pledged as collateral are initially measured at fair value on the date they are received. Subsequently, the fair value of the pledged collateral is reassessed periodically, with any changes in fair value recognized in the Group’s financial statements.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

Under the loan agreements, the related party is required to grant the Group monitoring access to the transferred collateral held at the designated address, and the related party is not permitted to transfer the collateral to another address without the Group’s prior written consent, which provides the Group transparency and oversight over the collateralized assets. Upon the Group’s full repayment of its obligations, the related party is obligated to return the same quantity and type of crypto assets originally posted as collateral. For XAUt collateral receivables from related party, the fair value changes are recorded in “Unrealized gain on XAUt and XAUt collateral receivables due from related party”.

Business combinations

The Group accounts for its business combinations using the acquisition method of accounting in accordance with Accounting Standards Codification (“ASC”) 805 “Business Combinations.” The cost of an acquisition is measured as the aggregate of the acquisition date fair values of the assets transferred and liabilities incurred by the Group to the sellers and equity instruments issued. Transaction costs directly attributable to the acquisition are expensed as incurred. Identifiable assets and liabilities acquired or assumed are measured separately at their fair values as of the acquisition date, irrespective of the extent of any non-controlling interests. The excess of (i) the total costs of acquisition, fair value of the non-controlling interests and acquisition date fair value of any previously held equity interest in the acquiree over (ii) the fair value of the identifiable net assets of the acquiree is recorded as goodwill. If the cost of acquisition is less than the fair value of the net assets of the subsidiary acquired, the difference is recognized directly in the consolidated statements of comprehensive income. During the measurement period, which can be up to one year from the acquisition date, the Group may record adjustments to the assets acquired and liabilities assumed with the corresponding offset to goodwill. Upon the conclusion of the measurement period or final determination of the values of assets acquired or liabilities assumed, whichever comes first, any subsequent adjustments are recorded to the consolidated statements of comprehensive income.

In a business combination achieved in stages, the Group re-measures the previously held equity interest in the acquiree immediately before obtaining control at its acquisition-date fair value and the re-measurement gain or loss, if any, is recognized in the consolidated statements of comprehensive income.

When there is a change in ownership interests that results in a loss of control of a subsidiary, the Group deconsolidates the subsidiary from the date control is lost. Any retained non-controlling investment in the former subsidiary is measured at fair value and is included in the calculation of the gain or loss upon deconsolidation of the subsidiary.

For the Group’s majority-owned subsidiaries, a non-controlling interest is recognized to reflect the portion of their equity which is not attributable, directly or indirectly, to the Group. “Net income (loss)” on the consolidated income statements includes the “net loss attributable to non-controlling interests”. The cumulative results of operations attributable to non-controlling interests are also recorded as non-controlling interests in the Group’s consolidated balance sheets.

Goodwill

Goodwill is initially measured at cost, being the excess of the aggregate of the consideration transferred, the amount recognized for noncontrolling interests and any fair value of the Group’s previously held equity interests in the acquiree over the identifiable assets acquired and liabilities assumed. If the sum of this consideration and other items is lower than the fair value of the net assets acquired, the difference is, after reassessment, recognized in profit or loss as a gain on bargain purchase.

After initial recognition, goodwill is measured at cost less any accumulated impairment losses. Goodwill is tested for impairment annually or more frequently if events or changes in circumstances indicate that the carrying value may be impaired. For the purpose of impairment testing, goodwill acquired in a business combination is, from the acquisition date, allocated to each of the Group’s cash-generating units, or groups of cash generating units, that are expected to benefit from the synergies of the combination, irrespective of whether other assets or liabilities of the Group are assigned to those units or groups of units.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

Where goodwill has been allocated to a cash-generating unit (or group of cash-generating units) and part of the operation within that unit is disposed of, the goodwill associated with the operation disposed of is included in the carrying amount of the operation when determining the gain or loss on the disposal. Goodwill disposed of in these circumstances is measured based on the relative value of the operation disposed of and the portion of the cash-generating unit retained.

Intangible assets (other than goodwill)

Intangible assets acquired separately are measured on initial recognition at cost. The cost of intangible assets acquired in a business combination is the fair value at the date of acquisition. The useful lives of intangible assets are assessed to be either finite or indefinite. Intangible assets with finite lives are subsequently amortized over the useful economic life and assessed for impairment whenever there is an indication that the intangible asset may be impaired. The amortization period and the amortization method for an intangible asset with a finite useful life are reviewed at least at each financial year end.

During the six months ended March 31, 2026 and 2025, the amortization of intangible assets were nil.

Share-based compensation

The Group accounts for share-based compensation in accordance with ASC Topic 718, Compensation-Stock Compensation: Overall, (“ASC 718”).

In accordance with ASC 718, the Group determines whether an award should be classified and accounted for as a liability award or equity award. All grants of share-based awards to employees classified as equity awards are measured based on their grant date fair values and recognized as compensation expense over the requisite service period and/or performance period in the consolidated statements of operations.

The Group recognizes compensation expense using the accelerated method for share-based awards granted with service and performance conditions. According to ASC 718, the amount of compensation cost recognized (or attributed) when achievement of a performance condition is probable depends on the relative satisfaction of the performance condition based on performance to date. According to ASC 718, probable means the future event or events are likely to occur and the Group interprets “probable” to be generally in excess of a 70% likelihood of occurrence. The Group elected to account for forfeitures as they occur.

Warrants

Warrants issued by the Group are classified as equity instruments. The proceeds received, or the fair value of the warrants issued as part of a business combination or other equity financing, is recorded within additional paid-in capital upon issuance. Subsequent transactions, including the exercise or expiration of these warrants, are treated as reclassifications between equity accounts and do not result in the recognition of gain or loss in the consolidated statements of operations.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

Impairment of long-lived assets

The Group evaluates its long-lived assets, including right-of-use assets and intangible assets, for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable in accordance with ASC subtopic 360-10, Property, Plant and Equipment: Overall (“ASC 360-10”). When these events occur, the Group assesses the recoverability of the long-lived assets by comparing the carrying amount of the assets to future undiscounted net cash flow expected to result from the use of the assets and their eventual disposition. If the sum of the expected undiscounted cash flow is less than the carrying amount of the assets, the Group will recognize an impairment loss equal to the excess of the carrying amount over the fair value of the assets.

During the six months ended March 31, 2026 and 2025, the impairment of long-live assets were nil.

Accounts receivable, net

Accounts receivable represented amounts due from the Group’s customers and are recorded at net realizable value consisting of the carrying amount less an allowance for uncollectible accounts as needed. The Group adopted Accounting Standard Update (ASU) 2016-13, Financial Instruments-Credit Losses (codified as Accounting Standard Codification Topic 326), since October 1, 2022, which requires measurement and recognition of current expected credit losses for financial instruments held at amortized cost. Prior to October 1, 2022, the allowance for doubtful accounts is the Group’s best estimate of the amount of probable credit losses in the Group’s existing accounts receivable. The Group determines the allowance based on aging data, historical collection experience, customer specific facts and existing economic conditions. Accounts receivable balances are charged off against the allowance after all means of collection have been exhausted and the potential for recovery is considered remote. The allowance of accounts receivables for the six months ended March 31, 2026 and 2025 were nil.

Prepaid expenses and other assets, net

Prepaid expenses and other assets are comprised of other receivables and prepaid expenses, including prepaid staff insurance, the payment of company secretary fee. The Group reviews other receivables on a regular basis and also makes specific allowance if there is strong evidence indicating that other receivables are likely to be unrecoverable.

Other receivables balances were written off after all collection efforts had been exhausted. Bad debts allowance for the six months ended March 31, 2026 and 2025 were nil and $11,407, respectively.

Loan payables due to related party

The Group entered into a term loan agreement (the “Loan Agreement”) with Northstar Digital (HK) Limited, which are accounted for as “loan payables due to related party”. These loans are initially recognized at fair value, net of any directly attributable transaction costs, and subsequently measured at amortized cost using the effective interest method.

Discontinued operations

A component of a reporting entity or a group of components of a reporting entity that are disposed or meet the criteria to be classified as held for sale, such as the management, having the authority to approve the action, commits to a plan to sell the disposal group, should be reported in discontinued operations if the disposal represents a strategic shift that has (or will have) a major effect on an entity’s operations and financial results. Discontinued operations are reported when a component of an entity comprising operations and cash flows that can be clearly distinguished, operationally and for financial reporting purposes, from the rest of the entity is classified as held for disposal or has been disposed of, if the component either (1) represents a strategic shift or (2) have a major impact on an entity’s financial results and operations. In the consolidated statement of operations, result from discontinued operations is reported separately from the income and expenses from continuing operations and prior periods are presented on a comparative basis. Cash flows for discontinued operations are presented separately in consolidated statement of cash flows.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

If the disposal group does not yet meet the held-for-sale criteria but is reported as a discontinued operation, its assets and liabilities are presented as “Assets of Discontinued Operations” and “Liabilities of Discontinued Operations” in the comparative balance sheets.

Deferred Offering Costs

Pursuant to ASC 340-10-S99-1, costs directly attributable to an offering of equity securities are deferred and would be charged against the gross proceeds of the offering as a reduction of additional paid-in capital. These costs include legal fees and consulting fees related to the registration preparation. During the six months ended March 31, 2026, the Group recorded deferred offering costs of US$400,573 related to the at-the-market (ATM) offering programs. These costs will be recognized as a reduction of additional paid-in capital as long as the Group remains committed to the offering and it is probable that the program will be completed.

Current expected credit losses

The Group has adopted Accounting Standard Update (ASU) 2016-13, Financial Instruments-Credit Losses (codified as Accounting Standard Codification Topic 326), since October 1, 2022, which requires measurement and recognition of current expected credit losses for financial instruments held at amortized cost. The Group’s accounts receivables, contract assets, note receivables, prepaid expenses, deposits and other receivables recorded in prepaid expenses and other assets and amount due from related parties are within the scope of ASC Topic 326. The Group establishes an allowance for credit losses primarily based upon factors surrounding the credit risk, including creditworthiness of the counterparties and other specific circumstances related to the accounts. To estimate expected credit losses, the Group has identified the relevant risk characteristics of its customers and these receivables items are assessed on an individual basis for customers with low risk, medium risk, high risk and default. Such allowance of estimated credit losses will be recorded in general and administrative expenses in the consolidated statement of comprehensive (loss) income.

Commitments and contingencies

In the normal course of business, the Group is subject to commitments and contingencies, including operating lease commitments, legal proceedings and claims arising out of its business that relate to a wide range of matters, such as government investigations and tax matters. The Group recognizes a liability for such contingency if it determines it is probable that a loss has occurred and a reasonable estimate of the loss can be made. The Group may consider many factors in making these assessments including historical and the specific facts and circumstances of each matter.

Revenue recognition

The Group adopted ASC Topic 606 (“ASC 606”), Revenue from Contract with Customers, with effect from October 1, 2019, using the modified retrospective method applied to those contracts which were not completed as October 1, 2019.

Under Topic 606, the entity should recognize revenue to depict the transfer of promised goods or services to clients in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

To achieve that core principle, an entity should apply the following steps:

Step 1: Identify the contract(s) with a customer.

Step 2: Identify the performance obligations in the contract.

Step 3: Determine the transaction price.

Step 4: Allocate the transaction price to the performance obligations in the contract.

Step 5: Recognize revenue when (or as) the entity satisfies a performance obligation.

Revenue recognition policies for each type of service are discussed as follows:

Advisory service fees

The Group acts as ongoing advisor to the client and provides a package of advisory services, including but not limited to, advising on global asset allocation, selecting and recommending suitable promotion or distribution channels for the issuance of the fund, coordinating daily operation and setting up meetings during post-establishment period, selecting and coordinating with lawyers for legal agreements and documents preparation, selecting qualified fund service providers, etc., as needed during the agreed-upon service period. Each contract of advisory service is accounted for as a single performance obligation which is satisfied over the service period. The Group allocates the transaction price to the single performance obligation based on a fixed annual fee and recognized revenue over the service period on a monthly basis.

Referral fees

The Group enters into contracts with brokers and refers high net worth or ultra-high net worth clients who subscribe to wealth management products from the brokers, such referral service is regarded as the single performance obligation. The Group is then entitled to receive referral fees paid directly by the brokers; the referral fees are computed as a percentage of the premiums paid by the clients for purchase of the wealth management products distributed by the brokers.

When a client is referred to the broker, and relative wealth management products is successfully subscribed by the client, the performance obligation is satisfied. Revenue on first year premiums and renewal premiums is recognized at the point in time when a client referred by the Group subscribes to wealth management products through the use of brokers the Group works with and such client has paid the requisite premiums and the applicable free look period has

expired. Contract asset is recognized for the unbilled renewal referral fee as relevant service is provided, but payment contingent on the completion of the renewal.

AI Solutions services

The Group enters into fixed-price development contracts to deliver customized AI solutions, including private large model systems, enterprise knowledge bases, intelligent customer service platforms, and departmental AI assistants. Each contract of advisory and development service is accounted for as a single performance obligation which is satisfied over the service period. The Group allocates the transaction price to the single performance obligation based on the fixed total contract value and recognizes revenue over the project period on a straight-line basis, as the services are rendered evenly throughout the term and the customer simultaneously receives and consumes the benefits provided.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

Management fees

The Group is entitled to receive a management fee of one-twelfth of 0.4% to 1.5% of the net asset value attributable to client’s respective equity holding positions in PGA (before deduction of that months’ management fee and any accrued performance fee) on a monthly basis, and it is nonrefundable.

The Group is entitled to receive a management fee from either the discretionary account management or the fund the Group used to manage, Prestige Capital Markets Fund I L.P., which is of 1.5% to 2.5% of such investor’s subscription amount with respect to such investment as of the date of determination, and it is nonrefundable.

For the fund Prestige Capital Markets Fund I L.P., these customer contracts require the Group to provide fund management services, which represents a performance obligation that the Group satisfies over time. The management fee will be payable in U.S. dollars monthly in arrears as soon as the net asset value calculation was completed by the fund administrator and approved by the Group at the end of each month and recognized as revenue.

Disaggregation of revenue

The following table illustrates the disaggregation of revenue:

| | | For the six months ended

March 31, | |

| | | 2026 | | | 2025 | |

| Continuing Operations | | | | | | |

| Referral fees | | $ | — | | | $ | 287 | |

| Advisory service fees | | | — | | | | — | |

| AI Solutions service fees | | | — | | | | — | |

| Total Revenue from Continuing Operations | | | — | | | | 287 | |

| | | | | | | | | |

| Discontinued Operations | | | | | | | | |

| Advisory service fees | | | — | | | | — | |

| Management fees | | | — | | | | — | |

| Total Revenue from Discontinued Operations | | | — | | | | — | |

| Total Net Revenue | | $ | — | | | $ | 287 | |

| | | For the six months ended

March 31, | |

| | | 2026 | | | 2025 | |

| Timing of Revenue Recognition | | | | | | |

| Services transferred at a point in time | | $ | — | | | $ | 287 | |

| Services transferred over time | | | — | | | | — | |

| Balance at end of the year | | $ | — | | | $ | 287 | |

Leases

On October 1, 2022, the Group adopted ASU No. 2016-02, Leases (Topic 842), as amended, which supersedes the lease accounting guidance under Topic 840, and generally requires lessees to recognize operating and financing lease liabilities and corresponding right-of-use assets on the balance sheet and to provide enhanced disclosures surrounding the amount, timing and uncertainty of cash flows arising from leasing arrangements.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

The Group elected to apply practical expedients permitted under the transition method that allow the Group to use the beginning of the period of adoption as the date of initial application, to not recognize lease assets and lease liabilities for leases with a term of twelve months or less, to not separate non-lease components from lease components, and to not reassess lease classification, treatment of initial direct costs, or whether an existing or expired contract contains a lease. The Group used modified retrospective method and did not adjust the prior comparative periods. Under the new lease standard, the Group determines if an arrangement is or contains a lease at inception. Right-of-use assets and liabilities are recognized at lease commencement date based on the present value of remaining lease payments over the lease terms. The Group considers only payments that are fixed and determinable at the time of lease commencement.

ASC 842 requires a lessee to discount its unpaid lease payments using the interest rate implicit in the lease or, if that rate cannot be readily determined, its incremental borrowing rate. As most of the Group’s leases do not provide an implicit rate, the Group uses its incremental borrowing rate as the discount rate for the lease. The Group’s incremental borrowing rate is estimated to approximate the interest rate on a collateralized basis with similar terms and payments. The right-of-use asset is initially measured at cost, which comprises the initial amount of the lease liability adjusted for lease payments made at or before the lease commencement date, plus any initial direct costs incurred less any lease incentives received. The Group’s lease terms may include options to extend or terminate the lease. Renewal options are considered within the right-of-use assets and lease liability when it is reasonably certain that the Group will exercise that option. The right-of-use assets are also subject to impairment. Refer to the accounting policies in Impairment of long-lived assets.

Lease expense for lease payments is recognized on a straight-line basis over the lease term.

Operating expenses

Operating expenses are recorded on the accrual basis, which mainly include unrealized gain on XAUt and XAUt collateral receivables due from related party, wages, rents and other operating expenses, such as administrative expenses, bank charges, accounting and audit fees unrelated with IPO or ATM. The Group recorded operating income of $18,135,996 and an operating expenses of $3,582,431 for the six months ended March 31, 2026 and 2025, respectively.

Income tax

The Group accounts for income taxes in accordance with U.S. GAAP. Under the asset and liability method as required by this accounting standard, the recognition of deferred income tax liabilities and assets is for the expected future tax consequences of temporary differences between the income tax basis and financial reporting basis of assets and liabilities. Provision for income taxes consists of taxes currently due plus deferred taxes. The charge for taxation is based on the results for the fiscal year as adjusted for items, which are non-assessable or disallowed. It is calculated using tax rates that have been enacted or substantively enacted by the balance sheet date.

Deferred taxes are accounted for using the asset and liability method in respect of temporary differences arising from differences between the carrying amount of assets and liabilities in the consolidated financial statements and the corresponding tax basis used in the computation of assessable tax profit. In principle, deferred tax liabilities are recognized for all taxable temporary differences. Deferred tax assets are recognized to the extent that it is probable that taxable profit will be available against which deductible temporary differences can be utilized. Deferred tax is calculated using tax rates that are expected to apply to the period when the asset is realized or the liability is settled. Deferred tax is charged or credited in the income statement, except when it is related to items credited or charged directly to equity, in which case the deferred tax is also dealt with in equity. Deferred tax assets are reduced by a valuation allowance when, in the opinion of management, it is more likely than not that some portion or all of the deferred tax assets will not be realized. For the six months ended March 31, 2026 and 2025, the Group had recognized nil valuation allowance against the deferred tax assets. As of March 31, 2026, the Group recognized nil deferred tax liabilities.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

Uncertain tax positions

The Group accounts for uncertainties in income taxes in accordance with ASC Topic 740, Income Taxes (“ASC 740”). An uncertain tax position is recognized as a benefit only if it is “more likely than not” that the tax position would be sustained in a tax examination, with a tax examination being presumed to occur. The amount recognized is the largest amount of tax benefit that is greater than 50% likely of being realized on examination. For tax positions not meeting the “more likely than not” test, no tax benefit is recorded. Penalties and interest incurred related to underpayment of income tax are classified as income tax expense in the period incurred. No significant penalties or interest relating to income taxes had incurred during the six months ended March 31, 2026 and 2025, and there were no uncertain tax positions as of March 31, 2026. All tax returns since the Group’s inception are still subject to examination by tax authorities. The Group does not believe that its unrecognized tax benefits will change over the next twelve months.

Segment Reporting

In accordance with ASC 280, Segment Reporting, an operating segment is identified as a component of an enterprise of which separate financial information and operating results are available and regularly reviewed by the Group’s chief operating decision maker (“CODM”). The Group has one operating and reportable segment with one business activity – earning referral fee from brokers. The Group’s CODM is its Chief Executive Officer. The Group’s CODM reviews financial information presented on a consolidated basis. The CODM uses the consolidated income or loss from operations and net income (loss) to evaluate financial performance, make decisions and allocate resources. The CODM also reviews the functional expenses such as selling and marketing expenses and general and administrative expenses at the consolidated level to manage the Group’s operations. The CODM does not use asset or liability information in assessing the Group’s operating segment.

Comprehensive income

Comprehensive income is comprised of the Group’s net income and other comprehensive income (loss). The component of other comprehensive income or loss is consisted solely of foreign currency translation adjustments, net of the income tax effect.

Functional currency and foreign currency translation and transactions

The Group’s reporting currency is the U.S. dollar (“US$”). The functional currency of PPWM, PWM and PAM is Hong Kong dollar, while the functional currency of PGAM and PAI is U.S. dollar and the functional currency of Wealth AI is Singapore dollar (“SGD”). In the consolidated financial statements, the financial information of the Group’s subsidiaries has been translated into US$. Assets and liabilities are translated at the exchange rates on each balance sheet date, while equity amounts are translated at historical exchange rates, except for changes in retained earnings (accumulated deficit) during the year which is the result of income statement translation process, and revenues, expenses, gains and losses are translated using the average exchange rates during each of the years. Translation adjustments are reported as foreign currency translation adjustments and are shown as a separate component of other comprehensive income or loss in the consolidated statements of comprehensive income (loss).

Earnings per share

Basic earnings per share are computed by dividing net income attributable to holders of ordinary shares by the weighted average number of ordinary shares outstanding during the year. Diluted earnings per share reflect the potential dilution that could occur if securities or other contracts to issue ordinary shares were exercised or converted into ordinary shares.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 2 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (cont.)

Recently issued accounting pronouncements not yet adopted

In April 2026, the FASB issued ASU No. 2026-01, Initial Measurement of Paid-in-Kind Dividends on Equity-Classified Preferred Stock (“ASU 2026-01”). ASU 2026-01 clarifies the initial measurement of paid-in-kind dividends on equity-classified preferred stock. The amendments are effective for all entities for annual reporting periods beginning after December 15, 2026, including interim periods within those annual periods. Early adoption is permitted. The Group does not currently issue preferred stock and therefore does not expect this ASU to have a material impact on its consolidated financial statements.

ASU No. 2025-05 Measurement of Credit Losses for Accounts Receivable and Contract Assets (“ASC 326”) becomes effective for fiscal years beginning after December 15, 2025, including interim periods within those fiscal years, and provides clarifications on the measurement of expected credit losses for receivables and contract assets. The Group is evaluating the impact of this ASU, but given the Group’s limited trade receivables, the impact is not expected to be material.

Note 9 TAXATION

The Group and its subsidiaries file tax returns separately.

1) Income tax

The Group is a Cayman Islands exempted company and currently conducts operations through subsidiaries that are incorporated in the Cayman Islands, the British Virgin Islands, Hong Kong and California.

The Cayman Islands

The Group, PGAM and PGCI are incorporated in the Cayman Islands and the Cayman Islands currently levy no taxes on individuals or corporations based upon profits, income, gains or appreciations and there is no taxation in the nature of inheritance tax or estate duty.

Pursuant to the Tax Concessions Act of the Cayman Islands, the Group has obtained an undertaking: (a) that no law which is enacted in the Cayman Islands imposing any tax to be levied on profits, income, gains or appreciation shall apply to the Group or its operations; and (b) that the aforesaid tax or any tax in the nature of estate duty or inheritance tax shall not be payable on the shares, debentures or other obligations of the Group.

The undertaking for the Group is for a period of twenty years from November 2, 2018.

There are no other taxes likely to be material to the Group levied by the Government of the Cayman Islands save certain stamp duties which may be applicable, from time to time, on certain instruments executed in or brought within the jurisdiction of the Cayman Islands.

The Cayman Islands are a party to a double tax treaty entered into with the United Kingdom in 2010 but are otherwise not a party to any other double tax treaties.

British Virgin Islands

PPWM and PAI are subsidiaries of the Group incorporated in the British Virgin Islands (BVI). There is no income or other tax in the British Virgin Islands imposed by withholding or otherwise on any payment to be made to or by the subsidiary incorporated in the British Virgin Islands.

United States

The U.S. subsidiary PWAI is subject to a federal corporate income tax rate of 21% and California state income tax at a rate of 8.84%. PWAI had no assessable income that was derived in the United States for the six months ended March 31, 2026 and 2025 and therefore no income tax has been provided.

Singapore

Wealth AI is subsidiary of the Group incorporated in Singapore. There is no income or other tax in the Singapore imposed by withholding or otherwise on any payment to be made to or by the subsidiary incorporated in the Singapore.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 9 TAXATION (cont.)

Hong Kong

In accordance with the relevant tax laws and regulations of Hong Kong, a company registered in Hong Kong is subject to income taxes within Hong Kong at the applicable tax rate on taxable income. From year of assessment of 2018/2019 onwards, Hong Kong profit tax rates are 8.25% on assessable profits up to HK$2 million, and 16.5% on any part of assessable profits over HK$2 million. The Group subsidiaries registered in Hong Kong are now subject to the new assessments in Hong Kong beginning in its fiscal year 2019. If, at the end of the basis period of the entity for the relevant year of assessment, the entity has one or more connected entities, the two-tiered profits tax rates would only apply to the one which is nominated to be chargeable at the two-tiered rates. The others would not qualify for the two-tiered profits tax rates and will continue to be subject to the rate of 16.5%. From the year of 2018/2019 onwards, Prestige Asset Management Limited elected the two-tiered profits tax rates. The Group’s subsidiary, PWM, in Hong Kong did not have assessable profits that were derived in Hong Kong for six months ended March 31, 2026 and 2025. Therefore, no Hong Kong profit tax has been provided for six months ended March 31, 2026 and 2025. PPWM, the Group’s BVI subsidiary, is doing business in Hong Kong and derives its income primarily in the region. PPWM is subject to Hong Kong profit tax with statutory tax rate of 16.5% according to the relevant tax laws and regulations of Hong Kong. PAM, the Group’s former Hong Kong subsidiary, was disposed of on June 26, 2025. Prior to its disposal, PAM was subject to Hong Kong profit tax at the two-tiered rates of 8.25% on assessable profits up to HK$2 million and 16.5% on any part of assessable profits over HK$2 million. Following the disposal of PAM, the Group’s remaining Hong Kong registered entity, PWM is eligible to elect for the two-tiered profits tax rates in future periods in which it has assessable Hong Kong-sourced profits, subject to the connected entity nomination rules under Hong Kong tax law.

The components of the income taxes (benefit) expense are:

| | | For the six months ended

March 31, | |

| | | 2026 | | | 2025 | |

| Current | | $ | — | | | $ | — | |

| Deferred | | | — | | | | (46,948 | ) |

| Total income taxes benefit | | $ | — | | | $ | (46,948 | ) |

According to tax regulations, net operating losses can be carried forward to offset operating income indefinitely.

Significant components of deferred tax assets were as follows:

| | | As of

March 31, 2026 | | | As of

September 30, 2025 | |

| Deferred tax assets | | $ | — | | | $ | — | |

| Current period addition(1) | | | — | | | | 251,333 | |

| Gross deferred tax assets | | | — | | | | 251,333 | |

| Less: valuation allowance(1) | | | — | | | | (251,333 | ) |

| Total deferred tax assets | | $ | — | | | $ | — | |

| (1) | As of September 30, 2025, the Group had net taxable losses arising from the operations of PPWM and WEALTH AI of HK$3,620,462 (US$462,442) and SGD$1,353,803 (US$1,027,649), respectively. These losses were available to reduce future taxable income, and all of these losses can be carried forward indefinitely. The Group considers positive and negative evidence to determine whether some portion or all of the deferred tax assets will more likely than not be realized. This assessment considers, among other matters, the nature, frequency and severity of recent losses, forecasts of future profitability, the duration of statutory carry forward periods, the Group’s experience with tax attributes expiring unused and tax planning alternatives. On the basis of this evaluation, the Group recognized a valuation allowance against deferred tax assets on tax loss carry-forwards of $251,333 for the years ended September 30, 2025. |

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 9 TAXATION (cont.)

Significant components of deferred tax liabilities were as follows:

| | | As of

March 31, 2026 | | | As of

September 30, 2025 | |

| Deferred tax liabilities(1) | | $ | — | | | $ | 11,390 | |

| Current year reversal(2) | | | — | | | | (11,362 | ) |

| Exchange rate effect | | | — | | | | 28 | |

| Balance at end of the year | | $ | — | | | $ | — | |

| (1) | As an impact of Topic 606, the Group recognized revenues from renewal premiums when performance obligation delivered by increasing the opening balance of retained earnings and recording a deferred tax liability of $11,390 at the beginning of the year ended September 30, 2025. The deferred tax liabilities resulted from a temporary difference between the accounting income before income taxes and taxable income. |

| (2) | The reversal of deferred tax liabilities for the years ended September 30, 2025 was HK$88,569. |

Net loss before income tax is attributable to the following tax jurisdictions:

| | | For the six months ended

March 31, | |

| | | 2026 | | | 2025 | |

| Hong Kong and BVI | | $ | 18,022,265 | | | $ | (354,493 | ) |

| Cayman | | | (1,343,092 | ) | | | (3,316,373 | ) |

| Singapore | | | (25,867 | ) | | | (11,170 | ) |

| Income/(loss) before income tax | | $ | 16,653,306 | | | $ | (3,682,036 | ) |

| Income/(loss) from continuing operations | | | 16,653,306 | | | | (3,557,693 | ) |

| Loss from discontinued operations | | | — | | | | (124,343 | ) |

Reconciliation between the Hong Kong statutory tax rates to income before income taxes benefit for income taxes is as follows:

| | | For the six months ended

March 31, | |

| | | 2026 | | | 2025 | |

| Income/(Loss) before income taxes expense | | $ | 16,653,306 | | | $ | (3,682,036 | ) |

| Income tax statutory rate | | | 16.5 | % | | | 16.5 | % |

| Income tax expense/(benefit) at statutory tax rate | | | 2,747,795 | | | | (607,534 | ) |

| Reconciling items: | | | | | | | | |

| Effect of tax-exempt for subsidiaries incorporated in Cayman Islands and BVI | | | 772,768 | | | | 549,045 | |

| Unrealized gain on change in fair value of XAUt | | | (3,520,563 | ) | | | — | |

| Effect on different tax rates for the first HK$2 million(1) | | | — | | | | 9,599 | |

| Effect of non-deductible item | | | — | | | | 1,942 | |

| Income taxes benefit | | $ | — | | | $ | (46,948 | ) |

| | | | | | | | | |

| Effective income tax rate | | | Nil | | | | 1.28 | % |

Note 13 NOMINAL SHARE ISSUANCE

On October 25, 2018, the Group issued 1,000,000 ordinary shares to Prestige Financial Holdings Group Limited, the Group’s controlling shareholder, at a par value of $0.001 per share with total consideration of $1,000. On November 20, 2018, the Group issued an additional 3,000,000 ordinary shares to Prestige Financial Holdings Group Limited, at a par value of $0.001 per share with total consideration of $3,000. On December 27, 2018, the Group issued an aggregate of 1,000,000 ordinary shares, at a par value of $0.001 per share with total consideration of $1,000, pro-rata to the shareholders of the Group as of such date. On July 6, 2023, the Group completed its qualified initial public offering of 1,000,000 ordinary shares, par value $0.000625 per share, at a price of $5.00 per share. On July 20, 2023 the Group completed its qualified over-allotment offering of 150,000 ordinary shares, par value $0.000625 per share, at a price of $5.00 per share. In accordance with Securities and Exchange Commission Staff Accounting Bulletin Topic 4, the nominal share issuance was accounted for as a stock split and that all share and per share information has been retrospectively restated to reflect such stock split for all periods presented. On June 25, 2024, the Group entered into a Business Development & Marketing Consulting Agreement and agreed to pay for the service in form of 1,416,667 newly issued restricted Class A ordinary shares, par value $0.000625 per share, at a price of $0.6 per share. On June 25, 2024, the Group entered into a Business Development & Marketing Consulting Agreement and agreed to pay for the service in form of 1,416,667 newly issued restricted Class A ordinary shares, par value $0.000625 per share, at a price of $0.6 per share. On July 2, 2024, the Group entered into a certain Software Technology Service Contract and agreed to pay for the service in form of 1,900,000 newly issued restricted Class A ordinary shares, par value $0.000625 per share, at a price of $0.6 per share. On August 23, 2024, the Group entered into a definitive acquisition agreement and agreed to pay partly of purchase price in form of 780,000 newly issued restricted Class A ordinary shares and 1,620,000 Class B ordinary shares, par value $0.000625 per share.

On October 1, 2024, the Group issued 5,454,545 Class A ordinary shares, par value $0.000625 per share, at a price of $0.55 per share for a total PIPE issuance consideration of $3 million. On November 5, 2024, the Group issued 3,500,000 Class B ordinary shares, par value $0.000625 per share, as part of the purchase consideration for the acquisition of InnoSphere Tech. On November 6, 2024, the Group issued 2,500,000 Class B ordinary shares, par value $0.000625 per share, as part of the purchase consideration for the acquisition of Tokyo Bay. On January 2, 2025, the Group issued 734,195 Class A ordinary shares, par value $0.000625 per share, upon the exercise of warrants related to the 2024 Business Development & Marketing Consulting Agreement agreements. On January 18, 2025, the Group issued 4,986,552 Class A ordinary shares, par value $0.000625 per share, upon the exercise of warrants from the 2024 PIPE issuance. On February 21, 2025, the Group issued 3,550,000 Class A ordinary shares, par value $0.000625 per share, under the 2025 S-8 incentive plan. On March 11, 2025, the Group issued 11,111,111 Class A ordinary shares, par value $0.000625 per share, at a price of $0.45 per share pursuant to the 1st Securities Purchase Agreement for the 2025 PIPE. On April 17, 2025, the Group cancelled 2,222,222 Class A ordinary shares. On April 19, 2025, the Group issued 23,719,807 Class A ordinary shares, par value $0.000625 per share, at a price of $0.421875 per share pursuant to the updated Securities Purchase Agreement for the 2025 PIPE. On May 13, 2025, the Group issued 10,000,000 Class A ordinary shares, par value $0.000625 per share, at a price of $0.50 per share for a project outsourcing

agreement. On July 24, 2025, the Group issued 950,000 Class A ordinary shares, par value $0.000625 per share, under the second round of the 2025 S-8 incentive plan.

On October 7, 2025, the Group entered into the Class A PIPE Subscription Agreements with certain accredited investors for an aggregate amount of approximately $51 million. The Group closed the transaction on October 10, 2025, agreeing to issue units consisting of: (i) Class A Ordinary Shares at a purchase price of $0.36 per share (or Pre-Funded Warrants to purchase Class A Ordinary Shares at $0.36 less $0.0001 per warrant with an exercise price of $0.0001), and (ii) Series A-1 Ordinary Warrants and Series A-2 Ordinary Warrants to purchase Class A Ordinary Shares with exercise prices of $0.47 and $0.54 per share, respectively. The consideration was received in cash and/or USDT.

AURELION INC.

NOTES TO UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

Note 13 NOMINAL SHARE ISSUANCE (cont.)

On October 7, 2025, concurrently with the Class A PIPE, the Group entered into the Class B Subscription Agreements with certain accredited investors for an aggregate amount of approximately $49 million. The transaction closed on October 10, 2025, pursuant to which the Group agreed to issue units consisting of: (i) Class B Ordinary Shares at a purchase price of $0.36 per share, and (ii) Series B-1 Ordinary Warrants and Series B-2 Ordinary Warrants to purchase Class B Ordinary Shares with exercise prices of $0.47 and $0.54 per share, respectively.

On October 7, 2025, the Group entered into a Primary Subscription Agreement with an accredited investor and subsequently closed the transaction on October 10, 2025. The Group issued 8,000,000 Class B Shares and Primary Warrants to purchase an additional 8,000,000 Class B Shares at an exercise price of $0.01 per share, for an aggregate purchase price of approximately $1.8 million.

In connection with and upon the completion of the PIPE Financing on October 10, 2025, the Group terminated several historical outstanding warrants to prevent equity dilution, including (i) Series C ordinary warrants to purchase up to 24,456,522 Class A Shares; (ii) Series D ordinary warrants to purchase up to 24,456,522 Class A Shares; (iii) Warrants to purchase up to 2,625,000 Class A Shares related to the InnoSphere Tech Inc. acquisition; and (vi) Warrants to purchase up to 1,875,000 Class A Shares related to the Tokyo Bay Management Inc. acquisition.

On November 20, 2025, the Group’s shareholders approved the 2025 Share Incentive Plan, with an initial maximum aggregate share pool of 76,187,375 Ordinary Shares. The plan features an automatic annual “evergreen” increase on January 1 of each calendar year equal to 1.5% of total outstanding shares and rights, capped at a maximum of 10% of total shares at any time. As of March 31, 2026, the Group has granted 913,333 restricted share units (RSUs) under this plan, each representing the right to receive one Class A ordinary share.

On December 12, 2025, the Group entered into a strategic consulting agreement with a non-affiliated service provider for wealth management and digital asset treasury growth. As equity consideration for the one-year service period, the Group issued a Class A Ordinary Share Purchase Warrant to the provider, allowing for the purchase of up to 31,698,046 Class A ordinary shares at an exercise price of $1.00 per share. The warrant is exercisable for a period of ten years.