N-4

Jun. 18, 2026

USD ($)

yr

Dec. 31, 2025

Dec. 31, 2024

Dec. 31, 2023

Dec. 31, 2022

Dec. 31, 2021

Dec. 31, 2020

Dec. 31, 2019

Dec. 31, 2018

Dec. 31, 2017

Dec. 31, 2016

We do not guarantee that the Contract will always offer Indexed Accounts that limit Index losses, which would mean risk of loss of the entire amount invested.

| FEES, EXPENSES AND ADJUSTMENTS | ||||||||||||||

| Are there Charges or Adjustments for Early Withdrawals? | Yes. If you take a withdrawal during the first 6 Contract Years, you may be assessed a surrender charge of up to 8% of the amount withdrawn. For example, if you invest $100,000 in the Contract and make an early withdrawal, you could pay a surrender charge of up to $8,000. This loss will be greater if there is a negative Interim Value calculation, a negative MVA, taxes, or tax penalties. If all or a portion of the Contract Value is removed from an Indexed Account or from the Contract prior to the end of an Interest Term, we will apply an Interim Value calculation to the Indexed Account Value which may be negative. Surrenders, partial withdrawals (including repetitive withdrawals), death benefit payments, and annuitization from the Indexed Accounts prior to the end of an Interest Term will be based on the Interim Values of the Indexed Accounts. In extreme situations, you could lose up to 100% of your investment due to the Interim Value calculation. For example, if you allocate $100,000 to an Indexed Account with a 2-year Interest Term, and later withdraw the entire amount before the 2-years have ended, you could lose up to $100,000 of your investment. This loss will be greater if the amount withdrawn is also subject to a surrender charge, a negative MVA, taxes, or tax penalties. If you take a withdrawal during the MVA Term, we may apply an MVA to the amount withdrawn, which may be negative. Any aggregate withdrawals from the Contract in an Interest Term Year that exceed the Free Withdrawal Amount (including surrenders and partial withdrawals) may be subject to an MVA. which may be negative. In extreme situations, a negative MVA could result in a loss as high as 100% of the amount withdrawn in excess of the Free Withdrawal Amount. This loss will be greater if there is a surrender charge, a negative Interim Value calculation, taxes, or tax penalties. | |||||||||||||

| Are there Transaction Charges? | No. | |||||||||||||

Are there Ongoing Fees and Expenses (annual charges)? | Yes. The table below describes the fees and expenses that you may pay each year, depending on the investment options and optional benefits you choose. Please refer to your Contract data page for information about the specific fees you will pay each year based on the options you have elected. There is an implicit ongoing fee on Indexed Accounts to the extent that your participation in Index gains is limited by us through the use of the Cap, Participation Rate, Trigger Rate, or Dual Trigger Rate. This means that your returns may be lower than the Index’s returns. In return for accepting this limit on Index gains, you will receive some protection from Index losses. This implicit ongoing fee is not reflected in the tables below. | |||||||||||||

| Annual Fee | Minimum | Maximum | ||||||

Optional benefits available for an additional charge (for a single Indexed Account Interest Term, if elected)(1) | 1% | 6% | ||||||

| (1) Referred to as the “Indexed Account Charge” for certain Indexed Accounts. The Indexed Account Charge is 1% per year of the Interest Term and is deducted from the Indexed Account Value at the end of each Interest Term. The Indexed Account Charge is 1% for 1-year Interest Terms and 6% for 6-year Interest Terms. If you make a full withdrawal or exercise a full Return Lock, the amount of the charge for the full Interest Term is deducted at the time of the withdrawal or Return Lock. If you make a partial withdrawal or exercise a partial Return Lock, the amount of the Indexed Account Charge is adjusted proportionally by the percentage that the partial withdrawal or partial Return Lock reduced the Indexed Account Value. The partial Indexed Account Charge is then deducted from the partial withdrawal amount or deducted from the Indexed Account Value locked in for a partial Return Lock. The remaining Indexed Account Charge is deducted from the Indexed Account on the last day of the Interest Term after Indexed Interest, if any, is credited. | ||||||||

Because your Contract is customizable, the choices you make affect how much you will pay. To help you understand the cost of owning your Contract, the following table shows the lowest and highest cost you could pay each year, based on current charges. This estimate assumes that you do not take withdrawals from the Contract, which could add surrender charges, negative MVAs, and negative Interim Value calculations that substantially increase costs.

Lowest Annual Cost: $0 | Highest Annual Cost: $910.85 | ||||

Assumes the following: •Investment of $100,000 in an Indexed Account •5% annual appreciation •No Indexed Account Charge •No optional benefits •No sales charges •No additional transfers or withdrawals •0% loss due to the Interim Value calculation | Assumes the following: •Investment of $100,000 in an Indexed Account •5% annual appreciation •Indexed Account Charge •No sales charges •No additional transfers or withdrawals •0% loss due to the Interim Value calculation | ||||

Yes. If you take a withdrawal during the first 6 Contract Years, you may be assessed a surrender charge of up to 8% of the amount withdrawn. For example, if you invest $100,000 in the Contract and make an early withdrawal, you could pay a surrender charge of up to $8,000. This loss will be greater if there is a negative Interim Value calculation, a negative MVA, taxes, or tax penalties.

If all or a portion of the Contract Value is removed from an Indexed Account or from the Contract prior to the end of an Interest Term, we will apply an Interim Value calculation to the Indexed Account Value which may be negative. Surrenders, partial withdrawals (including repetitive withdrawals), death benefit payments, and annuitization from the Indexed Accounts prior to the end of an Interest Term will be based on the Interim Values of the Indexed Accounts. In extreme situations, you could lose up to 100% of your investment due to the Interim Value calculation. For example, if you allocate $100,000 to an Indexed Account with a 2-year Interest Term, and later withdraw the entire amount before the 2-years have ended, you could lose up to $100,000 of your investment. This loss will be greater if the amount withdrawn is also subject to a surrender charge, a negative MVA, taxes, or tax penalties.

If you take a withdrawal during the MVA Term, we may apply an MVA to the amount withdrawn, which may be negative. Any aggregate withdrawals from the Contract in an Interest Term Year that exceed the Free Withdrawal Amount (including surrenders and partial withdrawals) may be subject to an MVA. which may be negative. In extreme situations, a negative MVA could result in a loss as high as 100% of the amount withdrawn in excess of the Free Withdrawal Amount. This loss will be greater if there is a surrender charge, a negative Interim Value calculation, taxes, or tax penalties.

For more information, see “Charges and Adjustments”.

Yes. The table below describes the fees and expenses that you may pay each year, depending on the investment options and optional benefits you choose. Please refer to your Contract data page for information about the specific fees you will pay each year based on the options you have elected.

There is an implicit ongoing fee on Indexed Accounts to the extent that your participation in Index gains is limited by us through the use of the Cap, Participation Rate, Trigger Rate, or Dual Trigger Rate. This means that your returns may be lower than the Index’s returns. In return for accepting this limit on Index gains, you will receive some protection from Index losses. This implicit ongoing fee is not reflected in the tables below.

| Annual Fee | Minimum | Maximum | ||||||

Optional benefits available for an additional charge (for a single Indexed Account Interest Term, if elected)(1) | 1% | 6% | ||||||

| (1) Referred to as the “Indexed Account Charge” for certain Indexed Accounts. The Indexed Account Charge is 1% per year of the Interest Term and is deducted from the Indexed Account Value at the end of each Interest Term. The Indexed Account Charge is 1% for 1-year Interest Terms and 6% for 6-year Interest Terms. If you make a full withdrawal or exercise a full Return Lock, the amount of the charge for the full Interest Term is deducted at the time of the withdrawal or Return Lock. If you make a partial withdrawal or exercise a partial Return Lock, the amount of the Indexed Account Charge is adjusted proportionally by the percentage that the partial withdrawal or partial Return Lock reduced the Indexed Account Value. The partial Indexed Account Charge is then deducted from the partial withdrawal amount or deducted from the Indexed Account Value locked in for a partial Return Lock. The remaining Indexed Account Charge is deducted from the Indexed Account on the last day of the Interest Term after Indexed Interest, if any, is credited. | ||||||||

Lowest Annual Cost: $0 | Highest Annual Cost: $910.85 | ||||

Assumes the following: •Investment of $100,000 in an Indexed Account •5% annual appreciation •No Indexed Account Charge •No optional benefits •No sales charges •No additional transfers or withdrawals •0% loss due to the Interim Value calculation | Assumes the following: •Investment of $100,000 in an Indexed Account •5% annual appreciation •Indexed Account Charge •No sales charges •No additional transfers or withdrawals •0% loss due to the Interim Value calculation | ||||

Assumes the following:

•Investment of $100,000 in an Indexed Account

•5% annual appreciation

•No Indexed Account Charge

•No optional benefits

•No sales charges

•No additional transfers or withdrawals

•0% loss due to the Interim Value calculation

Assumes the following:

•Investment of $100,000 in an Indexed Account

•5% annual appreciation

•Indexed Account Charge

•No sales charges

•No additional transfers or withdrawals

•0% loss due to the Interim Value calculation

| RISKS | ||||||||

| Is there a Risk of Loss from Poor Performance? | Yes. You can lose money by investing in the Contract. The following chart shows the maximum percentage of your investment you could lose due to negative Index performance after taking into account the current limits on Index loss provided under the Contract. | |||||||

| Crediting Method | Maximum Potential Loss % for Negative Performance | ||||

1% Buffer | 99% | ||||

| 10% Buffer | 90% | ||||

| 15% Buffer | 85% | ||||

| 20% Buffer | 80% | ||||

| 30% Buffer | 70% | ||||

| 100% Buffer | 0% | ||||

10% Buffer Plus Rate | 90% | ||||

| 20% Buffer Plus Rate | 80% | ||||

30% Buffer Plus Rate | 70% | ||||

We do not guarantee that the Contract will always offer Indexed Accounts that limit Index losses, which would mean risk of loss of the entire amount invested.

In addition, withdrawals taken during the Surrender Charge Period may be subject to a negative MVA, which could result in loss.

For more information, see “Principal Risks of Investing in the Contract,” “Investment Options,” and “Additional Information on the Indexed Accounts.”

| RISKS | ||||||||

| Is this a Short-Term Investment? | No. The Contract is not a short-term investment and is not appropriate if you need ready access to cash. The benefits of tax deferral and living benefit protections also mean the Contract is more beneficial to investors with a long-time horizon. Tax penalties may apply to withdrawals taken before age 59 ½. Withdrawals from the Contract may be subject to a surrender charges, MVAs, taxes, and tax penalties. Amounts removed from an Indexed Account before the end of the Interest Term may also result in a negative Interim Value calculation and loss of positive performance. If you take a withdrawal prior to the end of an Interest Term, the withdrawal will cause a reduction (perhaps significant reduction) to your Base Value. Reductions to your Base Value will negatively impact your Indexed Account Value for the remainder of the Interest Term and may result in a lower amount of Indexed Interest being credited, if any, at the end of the Interest Term as well as reduce the amount of Death Benefit available to your Beneficiaries. | |||||||

At the end of each Interest Term or if the Return Lock feature has been exercised, at the end of the current or any subsequent Interest Term Year, you may elect to transfer your Contract Value between the Fixed Account and any Indexed Account(s) and between Indexed Account(s) and begin a new Interest Term. If we do not receive a transfer request from you by the Transfer Notice Deadline, your allocations will remain the same and no transfers will occur. If an Indexed Account in which you are invested is no longer offered or available to you under your Contract and we do not receive a transfer request, any amount in that Indexed Account will be transferred to the 1-year 100% Buffer Indexed Account tied to the same Index as your previous allocation. If the 1-year 100% Buffer Indexed Account tied to the same Index as your previous allocation is not available, we will transfer your Indexed Account Value to the Fixed Account. For example, assume you are allocated to the S&P 500 6-year Point to Point with 30% Buffer Indexed Account and we do not receive a transfer request by the Transfer Notice Deadline. Because the 6-year Interest Term is only available at the time of purchase, this Indexed Account is no longer available for your Contract. We will transfer your Indexed Account Value to the S&P 500 1-year Point to Point with 100% Buffer. If the S&P 500 1-year Point to Point with 100% Buffer is not available, we will transfer your Indexed Account Value to the Fixed Account. | ||||||||

What are the Risks Associated with the Investment Options? | Investment in the Contract is subject to the risk of poor investment performance and can vary depending on the performance of the investment options available under the Contract (e.g., the Indexed Accounts). Each investment option (including the Fixed Account) has its own unique risks. You should review the available investment options before making an investment decision. All of the Indices we currently offer are price return indices which do not reflect dividends or distributions paid on the components of the Indices. This reduces the Index Return and will cause the Index to underperform a direct investment in the securities composing the Index. The upside potential feature of the applicable Crediting Methods will limit positive Index Returns (e.g., limited upside). This may result in you earning less than the Index Return. For example: The Cap represents the maximum positive Adjusted Index Return for a given Interest Term and limits the amount of positive Indexed Interest that we may be obligated to credit for any Interest Term. If the Cap is 8%, the Participation Rate is 100% and the Index Return is 15%, we would credit Indexed Interest at the Adjusted Index Return of 8% (the Index Return up to the Cap) at the end of the Interest Term. The Participation Rate represents a percentage that can be applied to the Index Return for an Interest Term. If the Participation Rate is 100% with no Cap and the Index Return is 5%, we would multiply the Index Return of 5% by 100%. As a result, we would credit Indexed Interest to your Base Value at the Adjusted Index Return of 5% (100% of the Index Return) at the end of the Interest Term. If the Index Return is 0% or greater, the Adjusted Index Return equals the Trigger Rate. If the Trigger Rate is 5% and the Index Return is 10%, the Adjusted Index Return equals the 5% Trigger Rate. If the Index Return is positive, zero, or negative within the Buffer, the Adjusted Index Return equals the Dual Trigger Rate. If the Dual Trigger Rate is 4% and the Index Return is 10% (a positive Index Return), the Adjusted Index Return equals the 4% Dual Trigger Rate. Similarly, if the Index Return is -3% (negative within the Buffer), the Adjusted Index Return would equal the Dual Trigger Rate of 4%. | |||||||

Yes. You may allocate amounts under the Contract to one or more of the Indexed Accounts available to you. Certain Indexed Accounts are only available at the time of purchase or at the end of certain Contract Years.

We reserve the right to add, combine, restrict or remove any Indexed Account available as an investment option under your Contract.

We may also add or remove an Index or Crediting Method during the time that you own the Contract. There is no guarantee that any particular Indexed Account, Index, or Crediting Method will be available during the entire time that you own your Contract. We may replace an Index at any time during an Interest Term.

Transfers may only be made at the end of each Interest Term or, if the Return Lock feature has been exercised, at the end of the current or any subsequent Interest Term Year.

The amount of Contract Value allocated to an Indexed Account at the beginning of an Interest Term must be at least $2,000.

If any transfer or Indexed Account Charge reduces an Indexed Account Value to less than $2,000, the entire amount remaining in that Indexed Account will be automatically transferred to the Fixed Account.

You may exercise either a full or partial Return Lock during an Interest Term for each Indexed Account. Return Locks for the full Indexed Account Value can only be made once per Interest Term per Indexed Account. Partial Return Locks may be exercised four times per Interest Term Year per Indexed Account until the full Index Account Value is subject to Return Lock. Once you exercise the Return Lock feature, it may not be revoked.

The Contract is a single premium annuity contract. Additional Purchase Payments will not be accepted.

We may change the Caps, Participation Rates, Trigger Rates, and Dual Triggers Rates from one Interest Term to the next, subject to the guaranteed minimum rates for each upside potential feature.

Not all Indexed Accounts may be currently available in all states. Also, your selling firm may not recommend the selection of certain Indexed Accounts or other features available under the Contract based on criteria established by the selling firm. You should speak with your financial professional for details about the Indexed Accounts and features available to you.

Yes. Except as provided otherwise, Contract benefits may be modified or terminated by the Company.

All withdrawals will reduce the death benefit, perhaps significantly, and the reduction may be more than the amount of the withdrawal.

You may exercise either a full or partial Return Lock during an Interest Term for each Indexed Account. Return Locks for the full Indexed Account Value can only be made once per Interest Term per Indexed Account. Partial Return Locks may be exercised four times per Interest Term Year per Indexed Account until the full Indexed Account Value is subject to Return Lock. Once you exercise the Return Lock feature, whether for the entire Indexed Account Value or a portion of the Indexed Account Value, it may not be revoked.

For more information see “Principal Risks of Investing in the Contract,” "Return Lock,” and “Access to Your Money During the Accumulation Phase.”

You should consult a competent tax professional about your individual circumstances to determine the tax implications of an investment in and Purchase Payment received under the Contract. There is no additional tax benefit if you purchased the Contract through a tax-qualified vehicle including but not limited to an individual retirement account (IRA). Access to amounts held in a qualified Contract may be restricted or prohibited.

All distributions other than death benefits, including surrenders and withdrawals will be subject to ordinary income tax, and may be subject to tax penalties.

For more information, see “Taxes”.

Some investment professionals may receive compensation for selling the Contract to investors. Investment professionals who solicited sales of the Contracts receive a portion of the commission payable to the broker-dealer firm, depending on the agreement between the broker-dealer and the investment professional. We pay commissions as a percentage of the Purchase Payment invested in the Contract.

These investment professionals may receive different compensation for selling different investment products and may have a financial incentive to offer or recommend the Contract over another investment.

For more information, see “Distribution”.

An investment professional may have a financial incentive to offer you a new contract in the place of a contract you already own.

You should only exchange your contract for a new one if you determine, after comparing the features fees and risks of both contracts, and any fees or penalties to terminate the existing contract, that it is preferable for you to purchase the new contract rather than continue to own the existing contract.

For more information, see “Distribution”.

FEE TABLE

The first table describes the fees and expenses that you will pay at the time that you buy the Contract, or surrender or make withdrawals from an investment option or from the Contract. State premium taxes may also be deducted.

| TRANSACTION EXPENSES | MAXIMUM AMOUNT DEDUCTED | CURRENT AMOUNT DEDUCTED | ||||||

SURRENDER CHARGE (1) (As a percentage of the amount withdrawn) | 8% | Year 1 ........................... 8% Year 2 ........................... 8% Year 3 ........................... 7% Year 4 ........................... 6% Year 5 ........................... 5% Year 6 ........................... 4% Year 7+.......................... 0% | ||||||

(1) Surrender charges apply to withdrawals and surrenders in excess of the Free Withdrawal Amount. Surrender charges may be waived if you are eligible to exercise the Nursing Home and Terminal Illness Waiver.

The next table describes the adjustments, in addition to any transaction expenses, that apply if all or a portion of the Contract Value is removed from an investment option or from the Contract before the expiration of a specified period.

ADJUSTMENTS | |||||

Maximum Potential Loss Due to the Interim Value calculation (as a percentage of Contract Value at the start of an Interest Term or amount withdrawn, as applicable) (1) | 100% | ||||

Maximum Potential Loss Due to the Market Value Adjustment (as a percentage of Contract Value at the start of an Interest Term or amount withdrawn, as applicable) (2) | 100% | ||||

(1) Account value adjusts daily, known as the Interim Value. The Interim Value represents the daily value of the underlying hypothetical investments associated with your selected Indexed Account(s). Except for the first and last Business Day of an Interest Term, your Indexed Account Value is largely based on your Interim Value and is the amount available for withdrawals, surrenders, annuitization and death benefits. The Interim Value will also be used if you exercise the Return Lock feature. The maximum loss would only occur if there is a total surrender of the Indexed Account Value during the Interest Term at a time when the Index Value has declined to zero.

(2) MVAs may apply to withdrawals that exceed the Free Withdrawal Amount in a given Interest Term Year during the MVA Term. The maximum loss of the withdrawal amount in excess of the Free Withdrawal Amount would only occur under extreme circumstances. Certain withdrawals are not subject to an MVA. See “Market Value Adjustment” for more information.

The next table described the fees and expenses that you will pay each year during the time that you own the Contract. If you choose to purchase an optional benefit, you will pay additional charges, as shown below.

OPTIONAL BENEFIT EXPENSES | MAXIMUM GUARANTEED CHARGE | ||||

Indexed Account Charge (1) (as a percentage of the Indexed Account Base Value) | |||||

1-Year Interest Term | 1% | ||||

6-Year Interest Term (1% charge each year for the 6-year Interest Term) | 6% | ||||

(1) The Indexed Account Charge is only applicable to certain Indexed Accounts. See “Investment Options” for a listing of Indexed Accounts with the Indexed Account Charge.

In addition to the fees described above, we limit the amount you can earn on certain of the Indexed Account options. This means your returns may be lower than the Index's returns. In return for accepting this limit on Index gains, you will receive some protection from Index losses.

| TRANSACTION EXPENSES | MAXIMUM AMOUNT DEDUCTED | CURRENT AMOUNT DEDUCTED | ||||||

SURRENDER CHARGE (1) (As a percentage of the amount withdrawn) | 8% | Year 1 ........................... 8% Year 2 ........................... 8% Year 3 ........................... 7% Year 4 ........................... 6% Year 5 ........................... 5% Year 6 ........................... 4% Year 7+.......................... 0% | ||||||

(1) Surrender charges apply to withdrawals and surrenders in excess of the Free Withdrawal Amount. Surrender charges may be waived if you are eligible to exercise the Nursing Home and Terminal Illness Waiver.

(1) Surrender charges apply to withdrawals and surrenders in excess of the Free Withdrawal Amount. Surrender charges may be waived if you are eligible to exercise the Nursing Home and Terminal Illness Waiver.

(1) Account value adjusts daily, known as the Interim Value. The Interim Value represents the daily value of the underlying hypothetical investments associated with your selected Indexed Account(s). Except for the first and last Business Day of an Interest Term, your Indexed Account Value is largely based on your Interim Value and is the amount available for withdrawals, surrenders, annuitization and death benefits. The Interim Value will also be used if you exercise the Return Lock feature. The maximum loss would only occur if there is a total surrender of the Indexed Account Value during the Interest Term at a time when the Index Value has declined to zero.

(2) MVAs may apply to withdrawals that exceed the Free Withdrawal Amount in a given Interest Term Year during the MVA Term. The maximum loss of the withdrawal amount in excess of the Free Withdrawal Amount would only occur under extreme circumstances. Certain withdrawals are not subject to an MVA. See “Market Value Adjustment” for more information.

The next table describes the adjustments, in addition to any transaction expenses, that apply if all or a portion of the Contract Value is removed from an investment option or from the Contract before the expiration of a specified period.

ADJUSTMENTS | |||||

Maximum Potential Loss Due to the Interim Value calculation (as a percentage of Contract Value at the start of an Interest Term or amount withdrawn, as applicable) (1) | 100% | ||||

Maximum Potential Loss Due to the Market Value Adjustment (as a percentage of Contract Value at the start of an Interest Term or amount withdrawn, as applicable) (2) | 100% | ||||

(1) Account value adjusts daily, known as the Interim Value. The Interim Value represents the daily value of the underlying hypothetical investments associated with your selected Indexed Account(s). Except for the first and last Business Day of an Interest Term, your Indexed Account Value is largely based on your Interim Value and is the amount available for withdrawals, surrenders, annuitization and death benefits. The Interim Value will also be used if you exercise the Return Lock feature. The maximum loss would only occur if there is a total surrender of the Indexed Account Value during the Interest Term at a time when the Index Value has declined to zero.

(2) MVAs may apply to withdrawals that exceed the Free Withdrawal Amount in a given Interest Term Year during the MVA Term. The maximum loss of the withdrawal amount in excess of the Free Withdrawal Amount would only occur under extreme circumstances. Certain withdrawals are not subject to an MVA. See “Market Value Adjustment” for more information.

The next table described the fees and expenses that you will pay each year during the time that you own the Contract. If you choose to purchase an optional benefit, you will pay additional charges, as shown below.

OPTIONAL BENEFIT EXPENSES | MAXIMUM GUARANTEED CHARGE | ||||

Indexed Account Charge (1) (as a percentage of the Indexed Account Base Value) | |||||

1-Year Interest Term | 1% | ||||

6-Year Interest Term (1% charge each year for the 6-year Interest Term) | 6% | ||||

PRINCIPAL RISKS OF INVESTING IN THE CONTRACT

GENERAL LIQUIDITY RISK

We designed the Contract to be a long-term investment that you may use to help save for retirement. The Contract is not suitable as a short-term savings vehicle. If you take withdrawals from your Contract during the Surrender Charge Period, surrender charges and an MVA may apply as well as, taxes and a 10% additional federal tax if taken before age 59½. An MVA may apply to any aggregate withdrawal taken in an Interest Term Year that exceeds the Free Withdrawal Amount. See “Market Value Adjustment” below for additional information related to the MVA. In addition, withdrawals from the Indexed Accounts prior to the end of an Interest Term will be based on the Interim Value(s) of the Indexed Account(s) in which you are invested. In extreme circumstances, you could lose up to 100% of your Contract Value allocated to an Indexed Account due to a negative Interim Value calculation. See “Interim Value Risk” below for additional information about the risks related to Interim Values. If you plan on taking withdrawals that will be subject to surrender charges, MVAs, Interim Value calculations, or additional federal taxes, this Contract may not be appropriate for you.

You can transfer Contract Value among the Indexed Accounts and the Fixed Account generally only at the end of an Interest Term. This restricts your ability to react to changes in market conditions during Interest Terms. You should consider whether the inability to reallocate Contract Value during an Interest Term is consistent with your financial needs. We must receive your transfer request by the Transfer Notice Deadline. If we do not receive a transfer request, no transfers will occur and your current allocation will remain in place for the next Interest Term. This will occur even if the Index, Cap percentage, Participation Rate percentage, Trigger Rate or Dual Trigger Rate percentage associated with the Indexed Account has changed since you last selected the Indexed Account, in which case the Indexed Account may no longer be appropriate for your investment goals. If you fail to transfer your Indexed Account Value at the end of an Interest Term and do not wish to remain invested in a particular Indexed Account for another Interest Term, your only option, if you do not exercise the Return Lock feature, will be to surrender the related Indexed Account Value. Surrendering all or a portion of your Contract Value may cause you to incur surrender charges, an MVA, negative Interim Value calculations, and negative tax consequences, as discussed in this section. See “Return Lock Risk” below for more information about risks associated with the exercising the Return Lock feature.

We may defer payments made under this Contract for up to six months if the insurance regulatory authority of the state in which we issued the Contract approves such deferral.

The Contract is a single premium annuity contract. Additional Purchase Payments will not be accepted. You will not be able to increase your Contract Value through additional Purchase Payments.

Short-Term Investment Risk. The Contract is not suitable if you are looking for a short-term investment or if you cannot accept the risk of getting back less money than you put in. The Contract is designed to help you invest on a tax-deferred basis and meet long-term financial goals, such as retirement funding. The benefits of tax deferral and living benefit protections also mean the Contract is more beneficial to investors with a long time horizon. Tax penalties may apply to withdrawals taken before age 59 ½.

RISK OF LOSS RELATED TO SURRENDER CHARGES, MVA AND FEES

There is a risk of loss of principal and related earnings if you take a withdrawal from your Contract or surrender it during the first six Contract Years when we may deduct a surrender charge and an MVA. This risk exists even if you are invested in an Indexed Account with an Index that is performing positively as of the date of your withdrawal.

If, during the MVA Term, you take aggregate withdrawals in an Interest Term Year that exceed the Free Withdrawal Amount, you may be subject to an MVA. An MVA is a positive or negative adjustment to the withdrawal amount to reflect the change in market interest rates between the Contract Date and the date of your withdrawal. The MVA is in addition to any applicable surrender charges and taxes. In extreme situations, a negative MVA could result in a loss as high as 100% of the amount withdrawn in excess of the Free Withdrawal Amount. The maximum loss would only occur under extreme circumstances when interest rates have risen significantly between the Contract Date and the date of the withdrawal.

There is also a risk of loss of principal and earnings as a result of the Indexed Account Charge. If you invest in an Indexed Account option with an Indexed Account Charge and any negative Indexed Interest does not exceed the Buffer, you could still experience losses due to our deduction of the charge. In addition, any positive Indexed Interest will be reduced by the deduction of the Indexed Account Charge at the end of each Interest Term.

If funds are allocated to an Indexed Account with an Indexed Account Charge but Indexed Interest for a given Interest Term does not exceed the amount which would have been credited without the higher Cap or higher Participation Rate, the Indexed Account Charge is not refunded. The Indexed Account Charge is not refunded if the Indexed Interest is negative for the Indexed Account for a given Interest Term. This means: (i) You bear the risk that amounts you have allocated to Indexed Accounts with a charge will never be credited with a greater amount of positive Indexed Interest than a similar Indexed Account without a charge;

and (ii) You assume the risk that funds allocated to an Indexed Account with an Indexed Account Charge will not be refunded regardless of the amount of Indexed Interest, positive or negative, credited to the Indexed Account.

INDEX RISK

If you allocate money to an Indexed Account for an Interest Term, the value of your investment depends in part on the performance of the applicable Index. The performance of an Index is based on changes in the values of the securities or other instruments that comprise or define the Index. The securities and instruments comprising or defining the Indexes are subject to a variety of investment risks, many of which are complicated and interrelated. These risks may affect capital markets generally, specific market segments, or specific issuers. The performance of the Indexes may fluctuate, sometimes rapidly and unpredictably. Negative Index performance may cause you to realize investment losses. The historical performance of an Index or an Indexed Account does not guarantee future results. It is impossible to predict whether an Index will perform positively or negatively over the course of an Interest Term. Each Crediting Method provides limited protection against negative interest.

The following chart shows the percentage of your investment you could lose due to negative Index performance in connection with an Indexed Account (at the end of the Interest Term) with a Buffer or Buffer Plus Rate. We do not guarantee that the Contract will always offer Indexed Accounts that limit losses, which would mean risk of loss of the entire amount invested.

Crediting Method | Maximum Potential Loss % for Negative Performance | ||||

1% Buffer | 99% | ||||

10% Buffer | 90% | ||||

15% Buffer | 85% | ||||

20% Buffer | 80% | ||||

30% Buffer | 70% | ||||

100% Buffer | 0% | ||||

10% Buffer Plus Rate | 90% | ||||

20% Buffer Plus Rate | 80% | ||||

30% Buffer Plus Rate | 70% | ||||

While it is not possible to invest directly in an Index, if you choose to allocate amounts to an Indexed Account, you are indirectly exposed to the investment risks associated with the applicable Index. Because each Index is comprised or defined by a collection of equity securities, each Index is largely exposed to market risk and issuer risk.

Market risk is the risk that market fluctuations may cause the value of a security to fluctuate, sometimes rapidly and unpredictably. Certain unanticipated events, such as wars, natural disasters and public health emergencies can negatively affect the global economy, economies of individual countries and the market in general. Any such impact could adversely affect the performance of the securities that comprise the Indexes and may lead to losses in your investment in the Indexed Accounts. The duration of these types of events cannot be determined with certainty. The full impact and duration of these events are difficult to determine. Any such impact could adversely affect the performance of the securities that comprise the Indexes and may lead to losses on your investment in the Indexed Accounts.

Issuer risk is the risk that the value of an issuer’s securities may decline for reasons directly related to the issuer, as opposed to the market generally.

Provided below is a summary of other important investment risks to which the Indexes are exposed. For more information on the Indexes, see the section titled “Indexes.”

•S&P 500® Index. The S&P 500® Index is comprised of equity securities issued by large-capitalization U.S. companies. In general, large-capitalization companies may be unable to respond quickly to new competitive challenges and may not be able to attain the high growth rate of successful smaller companies.

•Russell 2000® Index. The Russell 2000® Index is comprised of equity securities of small-capitalization U.S. companies. In general, the securities of small-capitalization companies may be more volatile and may involve more risk than the securities of larger companies. Small-capitalization companies are more likely to fail than larger companies.

•Nasdaq-100® Index. The Nasdaq-100® Index is comprised of equity securities of the largest U.S. and non-U.S. companies listed on the Nasdaq Stock Market, including companies across all major industry groups except financial companies. In general, large-capitalization companies may be unable to respond quickly to new competitive challenges and may not be able to attain the high growth rate of successful smaller companies. To the extent that the Nasdaq-100® Index is comprised of securities issued by companies in a particular sector, those securities may not

perform as well as the securities of companies in other sectors or the market as a whole. Also, any securities issued by non-U.S. companies (including related depository receipts) are subject to the risks related to investments in foreign markets (e.g., increased volatility; changing currency exchange rates; and greater political, regulatory, and economic uncertainty).

The Indexes available under the Contract do not reflect any dividends or distributions paid by the component companies. If dividends or distributions were reflected in the value of an Index, the Index’s performance would be higher, particularly over long periods of time. The Indexes that include non-U.S. companies use exchange rate methodologies that may impact an Index’s performance. These considerations may negatively impact the performance of your Indexed Accounts.

An investment in the Contract is not an investment in any Index or in the securities of companies that comprise the Indexes. You should understand that you will have no voting rights, no rights to receive cash dividends or other distributions, and no other rights with respect to the companies that comprise the Indexes.

RISKS RELATED TO UPSIDE POTENTIAL FEATURES

•Cap Risk. If you choose to allocate amounts to an Indexed Account with a Cap, the highest possible Adjusted Index Return that you may achieve is limited by the Cap. The Cap therefore limits the positive Indexed Interest, if any, that may be credited to your Contract for a given Interest Term. The Caps do not guarantee a certain amount of Indexed Interest. The Adjusted Index Return for an Indexed Account may be less than the positive return of the Index. This is because any positive return of the Index is subject to a maximum in the form of a Cap. For any Indexed Account with both a Cap and Participation Rate, the Adjusted Index Return will be limited by the Cap.

The Caps benefit us because they limit the amount of positive Indexed Interest that we may be obligated to credit for any Interest Term. We set the Caps in our discretion; however, they will never be less than 2% during the Surrender Charge Period or 1% thereafter. You bear the risk that we will not set the Caps higher than the Guaranteed Minimum Cap.

•Participation Rate Risk. We declare the Participation Rate immediately prior to the beginning of each Interest Term, and can declare a Participation Rate as low as 100%. You bear the risk that we will not declare a Participation Rate that is greater than 100%. We set the Participation Rates in our discretion; subject to the Guaranteed Minimum Participation Rate. For any Indexed Account with both a Cap and Participation Rate, the Adjusted Index Return will be limited by the Cap.

•Trigger Rate Risk. If you choose to allocate amounts to an Indexed Account with a Trigger Rate, the highest possible Adjusted Index Return that you may achieve is the Trigger Rate. If, at the end of the Interest Term, the Index Return is 0% or greater, the Adjusted Index Return is set to equal the Trigger Rate percentage. This would benefit you if a positive Index Return was less than the Trigger Rate percentage. However, if the Index Return exceeds the Trigger Rate percentage, your Adjusted Index Return is set to equal the lower Trigger Rate percentage. In that case, you would have lost the opportunity to realize the higher Index Return. The Trigger Rate does not guarantee a certain amount of Indexed Interest. We declare the Trigger Rate immediately prior to the beginning of each Interest Term and can declare a Trigger Rate as low as 1%.

The Trigger Rate benefits us where the Index Return exceeds the Trigger Rate percentage because that limits the amount of positive Indexed Interest that we may be obligated to credit for any Interest Term. We set the Trigger Rate in our discretion subject to the Guaranteed Minimum Trigger Rate.

•Dual Trigger Rate Risk. If you choose to allocate amounts to an Indexed Account with a Dual Trigger Rate, the highest possible Adjusted Index Return that you may achieve is the Dual Trigger Rate. If, at the end of the Interest Term, the Index Return is positive, zero, or negative within the Buffer, the Adjusted Index Return is set to equal the Dual Trigger Rate percentage. This would benefit you if the Index Return was equal to or above the Buffer and less than the Dual Trigger Rate percentage. However, if the Index Return exceeds the Dual Trigger Rate percentage, your Adjusted Index Return is set to equal the lower Dual Trigger Rate percentage. In that case, you would have lost the opportunity to realize the higher Index Return. The Dual Trigger Rate does not guarantee a certain amount of Indexed Interest. We declare the Dual Trigger Rate immediately prior to the beginning of each Interest Term and can declare a Dual Trigger Rate as low as 1%.

The Dual Trigger Rate benefits us where the Index Return exceeds the Dual Trigger Rate percentage because that limits the amount of positive Indexed Interest that we may be obligated to credit for any Interest Term. We set the Dual Trigger Rate in our discretion subject to the Guaranteed Minimum Dual Trigger Rate.

RISKS RELATED TO DOWNSIDE PROTECTION FEATURES

•Buffer or Buffer Plus Rate Risk. Index fluctuations may cause Indexed Interest to be negative even after the application of the Buffer or Buffer Plus Rate. This would reduce your Indexed Account Value. Any portion of your Contract Value allocated to an Indexed Account will benefit from the protection afforded under the Buffer or Buffer Plus

Rate only for that Interest Term. You assume the risk that you will incur a loss and that the amount of the loss will be significant. You also bear the risk that sustained negative Index Returns may result in zero or negative Indexed Interest being credited to your Indexed Account Value over multiple Interest Terms. If an Indexed Account is credited with negative Indexed Interest for multiple Interest Terms, the cumulative loss may exceed the stated limit of the Buffer or Buffer Plus Rate for any single Interest Term.

The Buffer and Buffer Plus Rate does not protect you from the Indexed Account Charge, even when your negative Adjusted Index Return is less than or equal to the Buffer or Buffer Plus Rate percentage.

The Buffer and Buffer Plus Rate percentage applicable to each Indexed Account will not change for the life of your Contract.

WITHDRAWAL RISK

If you withdraw Contract Value allocated to an Indexed Account prior to the end of an Interest Term (including through a repetitive withdrawal), the withdrawal will cause a reduction (perhaps significant reduction) to your Base Value. When you take such a withdrawal, your Base Value will be immediately reduced in a proportion equal to the reduction in your Indexed Account Value, which will be the Interim Value. A proportional reduction could be larger than the dollar amount of your withdrawal. Reductions to your Base Value will negatively impact your Indexed Account Value for the remainder of the Interest Term and may result in a lower amount of Indexed Interest being credited, if any, at the end of the Interest Term. Reductions will also impact the Death Benefit available for your Beneficiaries. If you plan on taking withdrawals, this Contract may not be appropriate for you. You should speak with a financial professional about how taking withdrawals, especially repetitive withdrawals, can negatively impact your investment in the Contract.

Once your Base Value is reduced due to a withdrawal, there is no way under the Contract to increase your Base Value during the remainder of the Interest Term. See “Impact of Withdrawals from Indexed Accounts” for additional information about how withdrawals affect your Indexed Account Values. See “Interim Value Risk” below for additional information about the risks related to Interim Values.

RETURN LOCK RISK

If you allocate Contract Value to an Indexed Account for an Interest Term, you may request to exercise the Return Lock feature at any time by notifying us prior to the end of the third to last Business Day of the Interest Term. You should consider the following risks related to the Return Lock feature:

•The portion of your Indexed Account Value subject to a Return Lock will no longer participate in the Index’s performance, whether positive or negative, for the remainder of the Interest Term. However, the portion of your Indexed Account Value subject to the Return Lock will be credited with interest at the Return Lock Rate from the Business Day following your exercise of the Return Lock until the end of the Interest Term Year when it can be reallocated to a different Indexed Account. If you choose not to reallocate at the end of the Interest Term Year, your locked in portion will continue to earn interest at the Return Lock Rate for the following Interest Term Year until the end of the Interest Term.

•You will not be credited with any Indexed Interest for the portion of your Indexed Account Value subject to the Return Lock at the end of the Interest Term.

•We use the Interim Value calculated at the end of the Business Day after we receive your request. This means you will not be able to determine in advance your “locked in” Indexed Account Value, and it may be higher or lower than it was on the Business Day we received your Return Lock request or your Indexed Account Value reached its target return for an automatic Return Lock.

•If you exercise the Return Lock feature at a time when your Interim Value has declined, you will lock in any loss. It is possible that you would have realized less of a loss or no loss if you exercised the Return Lock feature at a later time or not at all.

•We will not provide advice or notify you regarding whether you should exercise the Return Lock feature or the optimal time for doing so. We will not warn you if you exercise the Return Lock feature at a sub-optimal time. We are not responsible for any losses related to your decision whether or not to exercise the Return Lock feature.

•There may not be an optimal time to exercise the Return Lock feature during an Interest Term. It may be better for you if you do not exercise the Return Lock feature during an Interest Term. It is impossible to know with certainty whether or not the Return Lock feature should be exercised.

•After you exercise the Return Lock feature, you will have the opportunity to transfer your locked-in Indexed Account Value at the end of each Interest Term Year remaining in the Interest Term. If you remain in your current Indexed Account for the remainder of the Interest Term, your locked-in Indexed Account Value will not participate in the Index’s performance for the remainder of that Interest Term, and you will forego any opportunity to invest in a new Indexed Account and earn Indexed Interest.

•The earlier in an Interest Term that you exercise the Return Lock, the longer you may forego any opportunity to earn the potential for additional Indexed Interest. For example, if you are invested in an Indexed Account with a 6-year Interest Term, and you exercise the Return Lock feature on the first day of the second year of the Interest Term and choose not to transfer for the remainder of the Interest Term (i.e., you choose not to transfer your locked-in Indexed Account Value at the end of each Interest Term Year remaining in the Interest Term), your investment will not participate in the Index’s performance for five years.

See the section titled “Return Lock” for additional information regarding the Return Lock feature.

INTERIM VALUE RISK

On each Business Day of the Interest Term, other than the first and last day, we determine the Indexed Account Value for each Indexed Account by calculating its Interim Value and then subtracting any Indexed Account Charge. In order to calculate your Interim Value, we apply a formula which is not directly tied to the actual performance of the applicable Index. Instead, we calculate it by determining the value of hypothetical investments and derivatives that we may or may not actually hold. This means that even if the Index Return has increased, it is possible that the Interim Value may not have increased. For more information and to see how we calculate the Interim Value, see the section “Interim Value” under “Charges and Adjustments” and the Statement of Additional Information (“SAI”).

If you choose to allocate amounts to an Indexed Account, Indexed Interest will not be credited to your Contract Value until the end of the Interest Term. This means that amounts withdrawn prior to the end of an Interest Term will not be credited with Indexed Interest. This includes Contract Value applied to pay a death benefit or to an annuity payout option. Except for the first and last Business Day of an Interest Term, your Indexed Account Value is largely based on your Interim Value and is the amount available for withdrawals, surrenders, annuitization and death benefits. The Interim Value will also be used if you exercise the Return Lock feature. You should consider the risk that it could be less than your original investment even when the applicable Index is performing positively.

RISK THAT WE MAY ELIMINATE OR SUBSTITUTE AN INDEX, INDEXED ACCOUNT, OR CREDITING METHOD OR CHANGE CAPS AND RATES

There is no guarantee that any particular Index, Indexed Account, or Crediting Method will be available during the entire time that you own your Contract. We may replace an Index if it is discontinued or if there is a substantial change in the calculation of the Index, or if hedging instruments become difficult to acquire or the cost of hedging becomes excessive. If we substitute an Index, the performance of the new Index may differ from the original Index. This may negatively affect the Indexed Interest that you earn during that Interest Term or the Interim Values that you can lock-in under the Return Lock feature. We may replace an Index at any time during an Interest Term, however, we will notify you in writing at least 30 days prior to replacing an Index. If we replace an Index, this does not cause a change in the Cap, Participation Rate, Trigger Rate, Dual Trigger Rate, Buffer or Buffer Plus Rate for that Interest Term. You will have no right to reject the replacement of an Index, and you will not be permitted to transfer Indexed Account Values until the end of an Interest Term even if we replace the Index during such Interest Term. The new Index and the replaced Index (which you may have previously chosen) may not be similar with respect to their component securities or other instruments, although we will attempt to select a new Index that is similar to the old Index. At the end of the Interest Term, you may transfer your Indexed Account Value to another Indexed Account or to the Fixed Account without charge. If you do not want to remain invested in the relevant Indexed Account for the remainder of the Interest Term, your only option, if you do not exercise the Return Lock feature, will be to withdraw the related Indexed Account Value, which may cause you to incur surrender charges, an MVA, negative adjustments to certain values under your Contract, due to the Interim Value calculation, and negative tax consequences, as discussed in this section.

We reserve the right to add new Indexed Accounts or stop offering any of the Indexed Accounts to new and/or existing Contracts, and to close any of the Indexed Accounts to new transfers at the end of an Interest Term. There is no guarantee that a particular Indexed Account will be available during the entire time that you own your Contract. New Indexed Accounts may have different Indices, rates, upside potential features, and downside protection features than those currently offered, subject to any applicable guaranteed minimum rates for each upside potential feature.

Changes to the Caps, Trigger Rates, Dual Trigger Rates and Participation Rates (if any) occur at the beginning of the next Interest Term. We will provide written notice at least 30 days prior to each Interest Term instructing you how to obtain the available Caps, Trigger Rates, Dual Trigger Rates, and Participation Rates for the next Interest Term. You do not have the right to reject any new Caps, Trigger Rates, Dual Trigger Rates or Participation Rates (if any) for the next Interest Term. If you do not like any such new element for a particular Indexed Account, at the end of the current Interest Term, you may transfer your Indexed Account Value to another Indexed Account or to the Fixed Account without charge. If you do not want to invest in any investment option under the Contract, your only option will be to surrender your Contract. Surrendering your Contract may cause you to incur surrender charges, an MVA, negative adjustments to certain values under the Contract due to the Interim Value calculation, and may have negative tax consequences, as discussed in this section. The Buffer and Buffer Plus Rate percentage will not change for the life of your Contract. See the section titled “Indexes” for more information.

We may also add or remove an Index or Crediting Method during the time that you own the Contract. We will not substitute any Index or Crediting Method until the new Index or Crediting Method has received any necessary regulatory clearances. Any addition, substitution, or removal of an Indexed Account, Index, or Crediting Method will be communicated to you in writing. If we add or remove an Index (as opposed to replacing an Index), the changes will not be effective for your Contract until the start of the next Interest Term. Replacing an Index does not cause a change in the Buffer or Buffer Plus Rate of an existing Indexed Account. Any Indexed Accounts based on the performance of the newly added Index will have a new Cap, Participation Rate, Trigger Rate or Dual Trigger Rate, subject to the guaranteed minimum rate, at the start of the next Interest Term.

You should evaluate whether our ability to make the changes described above, and your ability to react to such changes, are appropriate based on your investment goals. When such changes occur, you should also evaluate whether those changes are appropriate based on your investment goals and, if not, you should evaluate your options under the Contract, which may be limited and may have negative consequences associated with them, as described in this section.

CYBER SECURITY RISKS

We rely heavily on interconnected computer systems and digital data to conduct our annuity business activities. Because our annuity business is highly dependent upon the effective operation of our computer systems and those of our business partners, our business is potentially vulnerable to disruptions from utility outages and other problems, and susceptible to operational and information security risks resulting from information systems failure (hardware and software malfunctions) and cyber-attacks. These risks include, among other things, the theft, misuse, corruption and destruction of data maintained online or digitally, and unauthorized release of confidential customer information. For instance, cyber-attacks may: interfere with our processing of Contract transactions, including the processing of orders from our website; cause the release and possible destruction of confidential customer or business information; impede order processing; subject us and/or our service providers and intermediaries to regulatory fines and financial losses; and/or cause reputational damage. Also, the risk of cyberattacks may be higher during periods of geopolitical turmoil (such as the Russian invasion of Ukraine) and the responses by the United States and other governments.

Cyber security risks may also affect the Indexes. Breaches in cyber security may cause an Index’s performance to be incorrectly calculated, which could affect the calculation of values under the Contract. We are not responsible for the calculation of any Index. Breaches in cyber security may also negatively affect the value of the securities or other instruments that comprise or define the Indexes.

FIXED ACCOUNT RISK

The effective annual interest rate for an Interest Term will never be lower than 1%. The effective annual interest rate represents the rate of daily compounded interest over a 12-month period. You bear the risk that we will never declare an interest rate for the Fixed Account higher than the guaranteed minimum interest rate.

RISK ASSOCIATED WITH SYMETRA LIFE

Investment in the Contract is subject to the risks related to Symetra Life. Any obligations, including obligations related to the Symetra Fixed Account, guarantees, and benefits provided for under the Contract are subject to our financial strength and claims paying ability. The assets of our General Account support our insurance and annuity obligations and are subject to our general liabilities from business operations and to claims by our creditors. Contract Value in the Fixed Account, plus any guarantees under the Contract that exceed Your Contract Value (such as those that may be associated with the Death Benefit), are paid from our General Account. We maintain a minimum amount of capital in excess of assets that offset reserves, which acts as a cushion in the event that we suffer financial impairment, based on certain risks in our operations. For the Company, such risks include those associated with losses that We may incur as the result of defaults on the payment of interest or principal on assets held in our General Account, which include bonds, loans secured by mortgages, and equity securities, as well as the loss in value of these investments resulting from a loss in their market value.

We do not refund any fees regardless of the amount of Indexed Interest, positive or negative, credited to the Indexed Account. In addition, the Buffer does not protect you from the Indexed Account Charge, even when your negative Adjusted Indexed Return is less than or equal to the Buffer. The Indexed Account Charge will decrease your Indexed Account earnings.

The Buffer and Buffer Plus Rate provide only limited protection from downside risk. You should understand that the Buffer and Buffer Plus Rate do not provide absolute protection against negative Indexed Interest. You may lose money. The Buffer and Buffer Plus Rate does not protect you from the Indexed Account Charge, even when your negative Adjusted Index Return is less than or equal to the Buffer and Buffer Plus Rate percentage.

Every Indexed Account has its own Indexed Account Value. Any portion of your Contract Value that is not allocated to an Indexed Account with a Crediting Method that includes the Buffer or Buffer Plus Rate will not benefit from the protection afforded by the Buffer or Buffer Plus Rate.

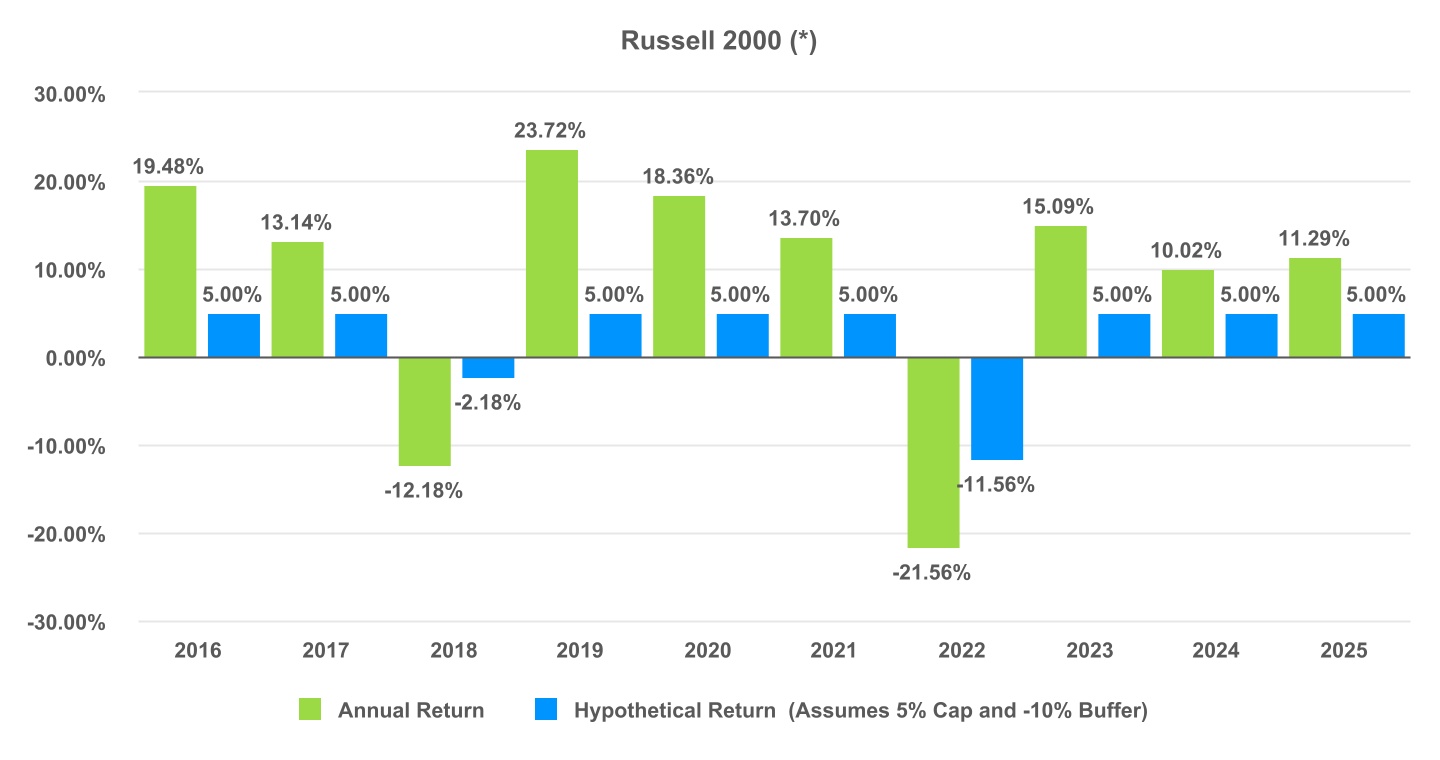

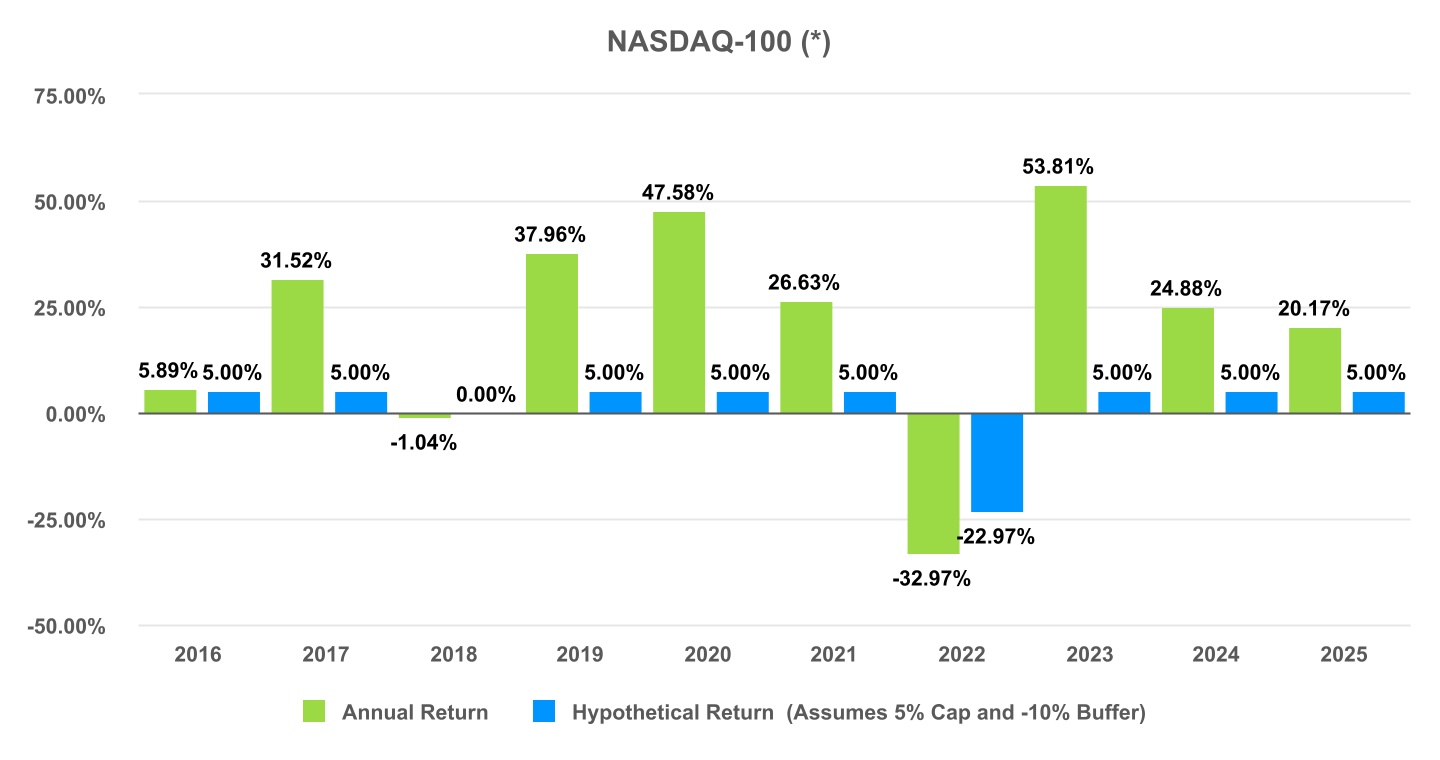

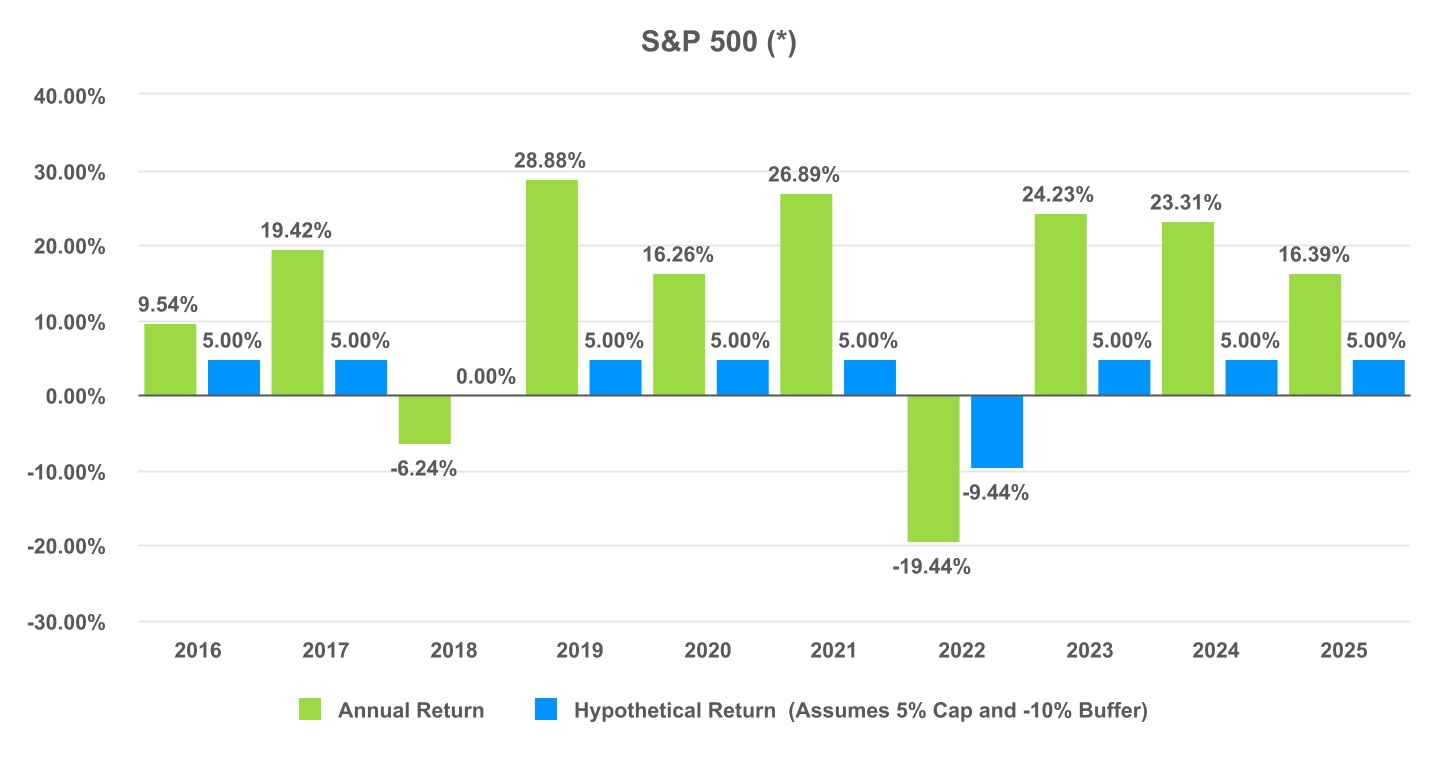

INDEX ANNUAL RETURNS

The bar charts shown below provide each Index’s annual returns for the last 10 calendar years (or for the life of the Index if less than 10 years), as well as the Index returns after applying a hypothetical 5% cap and a hypothetical -10% buffer. The chart illustrates the variability of the returns from year to year and shows how hypothetical limits on Index gains and losses may affect these returns. Past performance is not necessarily an indication of future performance.

The performance below is NOT the performance of any Indexed Account. Your performance under the Contract will differ, perhaps significantly. The performance below may reflect a different return calculation, time period, and limit on Index gains and losses than the Indexed Account, and does not reflect Contract fees and charges, including surrender charges, MVAs, and the Interim Value Calculation, which reduce performance.

The following examples illustrate how we calculate and credit interest under each Crediting Method assuming hypothetical Index Returns and hypothetical limits on Index gains and losses. The examples assume no withdrawals.

On the last Business Day of the Interest Term, your Indexed Account Value will equal your Base Value plus the amount of Indexed Interest credited to the Indexed Account which may be positive, negative, or equal to zero. This may also be expressed through the following formula: Base Value x (1 + Adjusted Index Return) – any Indexed Account Charge. Examples for how the Adjusted Index Return is determine by various Crediting Methods is shown below.

The Fixed Account credits compound interest based on rates that are set and guaranteed by us. Any portion of your Contract Value allocated to the Fixed Account for an Interest Term will be credited with the interest rate established for that Interest Term. This rate will apply for the entire Interest Term, which will be 1-year in length. Once an Interest Term is over, we will declare a new interest rate for the next Interest Term.

Payments from the Fixed Account are also subject to minimum amounts required by state law. These minimum amounts only apply upon annuitization from the Fixed Account, payment of a death benefit upon death of the Owner, or a full withdrawal from the Fixed Account. We guarantee that if one of these events occurs, then the proceeds from the Fixed Account (the amount applied to annuity payments or paid for a full withdrawal or death benefit) will be at least equal to the minimums required by state law. If necessary to meet this minimum, charges will be waived or reduced.

SURRENDER CHARGE

You may take partial withdrawals or surrender your Contract (i.e., take a full withdrawal) at any time during the Accumulation Phase. A surrender charge may be imposed when you take a partial or full withdrawal during the Surrender Charge Period. After the sixth Contract Year, there are no surrender charges under the Contract.

If a surrender charge applies to a withdrawal, the charge will be a percentage of the amount withdrawn in excess of your Free Withdrawal Amount. See “Free Withdrawal Amount” for more information. We will deduct the surrender charge from the amount withdrawn. If you take a full withdrawal, the surrender charge is calculated as part of your Cash Surrender Value.

The applicable surrender charge percentage will depend on the Contract Year during which the withdrawal is taken. The schedule below sets forth the surrender charge percentages under the Contract. The surrender charge schedule starts at 8% and declines until the seventh Contract Year when it reaches 0%.

| Contract Year | 1 | 2 | 3 | 4 | 5 | 6 | 7+ | ||||||||||||||||

| Surrender Charge (as a percentage of the amount withdrawn in excess of the Free Withdrawal Amount) | 8% | 8% | 7% | 6% | 5% | 4% | 0% | ||||||||||||||||

All withdrawals during the Surrender Charge Period are subject to surrender charges, except:

•withdrawals during a Contract Year that, in the aggregate, do not exceed the Free Withdrawal Amount;

•repetitive withdrawals based on life expectancy;

•eligible hospital and nursing home withdrawals; and

•eligible terminal illness withdrawals.

If you request a withdrawal from an Indexed Account with an Indexed Account Charge during the Surrender Charge Period that qualifies for a waiver of surrender charges, this waiver does not extend to the Indexed Account Charge. The Indexed Account Charge is not waived. See the section titled, “Indexed Account Charge.”

Annuity payments and death benefits under the Contract are not subject to surrender charges.

Surrender charges are intended to compensate us for expenses incurred in connection with the promotion, sale, and distribution of the Contracts. We intend to use revenue generated from surrender charges for any legitimate corporate purpose.

MARKET VALUE ADJUSTMENT

An MVA is a positive, negative or zero adjustment to the withdrawal amount based on market conditions at the time of the withdrawal. Any aggregate withdrawal beyond the Free Withdrawal Amount may be subject to an MVA during the MVA Term. After the sixth Contract Year, there is no MVA under the Contract. In addition to any MVA, surrender charges, taxes and tax penalties may apply and any amounts withdrawn from the Indexed Accounts will also be subject to Interim Value calculations. The MVA is applied after the Interim Value calculation (which includes the deduction of any Indexed Account Charges) and

before the deduction of any surrender charges. The MVA reflects relative changes in interest rates from the Contract Date to the date of the withdrawal. An MVA can be a positive, negative or zero adjustment to the withdrawal amount and protects us from risks related to the fixed investments that support the Contract guarantee if amounts are withdrawn early. If there is no change in interest rates, no adjustment to your withdrawal will occur.

If not zero, the MVA will increase or decrease the amount you receive as a withdrawal. In general, if the MVA is negative, it will decrease the amount you receive as a withdrawal, and if the MVA is positive, it will increase the amount you receive as a withdrawal. In extreme situations, a negative MVA could result in a loss as high as 100% of the amount withdrawn in excess of the Free Withdrawal Amount. This would only occur if interest rates have risen significantly between the Contract Date and the date of the withdrawal. If you take a full withdrawal, the MVA is calculated as part of your Cash Surrender Value.

For withdrawals involving more than one Indexed Account, we calculate the applicable MVA for each Indexed Account and add those amounts together. For withdrawals involving the Indexed Account(s) and the Fixed Account, we calculate the MVA for each investment option and add those amounts together. Any applicable MVA on a full withdrawal from the Fixed Account will never result in a withdrawal amount less than the minimums required by state law. If necessary to meet this minimum, the MVA will be reduced or waived in order to meet any required minimum.

Certain transactions are not subject to an MVA, including:

•withdrawals during a Contract Year that, in the aggregate, do not exceed the Free Withdrawal Amount;

•annuity payments;

•death benefits;

•repetitive withdrawals based on life expectancy;

•eligible hospital and nursing home withdrawals; and

•eligible terminal illness withdrawals.

In addition, if a spouse continues a Contract during the MVA Term, no MVA will apply to withdrawals taken.

Market Value Adjustment Calculation: To determine if an MVA will apply to your withdrawal, we look at the change in interest rates from the Contract Date to the date of the withdrawal using the Bloomberg USD US Corporate A+ AA BVAL Yield Curve 6 Year index rate (“reference rate”). When we calculate the MVA, we use the reference rate published on the Contract Date and the withdrawal date. If the reference rate is not published on the Contract Date, we will use the reference rate for the Business Day prior to the Contract Date. In general, if the reference rate has increased since the Contract Date, the MVA will be negative, and if the reference rate has decreased since the Contract Date, the MVA will be positive.

To determine the dollar amount of the MVA that will apply to your withdrawal, we use a formula that takes into account the reference rate determined on the Contract Date, the reference rate determined on the date of the withdrawal, the calendar days remaining to the end of the sixth Contract Year, the amount of the withdrawal and any remaining Free Withdrawal Amount. Please see the Statement of Additional Information for examples on how we calculate the MVA in certain scenarios.

You may contact our Home Office to obtain a quote for the MVA based on the current reference rate. However, you will not know the MVA used in advance. This is because the reference rate fluctuates daily, and we use the reference rate calculated at the end of the withdrawal date. The quoted MVA may be higher or lower than the actual MVA on the withdrawal date.

FREE WITHDRAWAL AMOUNT

After the Allocation Date and before the end of the sixth Contract Year you may take withdrawals up to the Free Withdrawal Amount without the imposition of surrender charges or MVAs. Any aggregate withdrawals in excess of your Free Withdrawal Amount may be subject to surrender charges and MVAs. After the sixth Contract Year, no surrender charge or MVA applies under the Contract.

We determine your Free Withdrawal Amount at the beginning of each Interest Term Year. Your Free Withdrawal Amount at the beginning of an Interest Term Year will be equal (in dollars) to the greater of:

(a)The free withdrawal percentage of 15% of the Contract Value as of the beginning of the current Interest Term Year. If you take more than one withdrawal in an Interest Term Year, the previous withdrawals during the Interest Term Year are taken into account to determine whether more than the free withdrawal percentage has been withdrawn in that Interest Term Year; or

(b)The accumulated interest earned in the Contract (net of any Indexed Account Charges) less any accumulated interest withdrawn previously as of the beginning of the current Interest Term Year.

HOSPITAL AND NURSING HOME WAIVER

If approved in your state, there is no surrender charge or MVAs on withdrawals you make while you are confined in a nursing home or a hospital for a period of at least 30 consecutive days or within 90 days of your release thereafter. If you were confined to a nursing home or hospital on the Contract Date, you are not eligible to rely on this waiver of surrender charges and MVAs until after the first Contract Year. The 30-day requirement may be satisfied by confinement in a combination of eligible hospitals

or eligible nursing homes. Separate periods of confinement, for the same or a related condition, with start dates that are no more than 30 days apart will be considered the same confinement. A new 30 consecutive day period will be applied for a confinement due to a new or non-related cause or to a confinement occurring more than 30 days from the most recent confinement for the same or related condition.

For you to rely on this waiver while you are confined, we may require proof of your confinement in an eligible nursing home or hospital, that your confinement has continued for 30 or more consecutive days, and that your confinement began after your Contract Date. For you to rely on this waiver after your release, we may require proof that you were confined to an eligible nursing home or hospital for at least 30 consecutive days, that your confinement began after your Contract Date, and that you were released within 90 days of your withdrawal request. Proof of confinement and release may include a billing statement from the eligible nursing home or hospital showing the dates of confinement and services rendered or a certification of confinement by an eligible attending physician of the Owner.

An eligible hospital includes any lawfully operated institution that is licensed as a hospital by the Joint Commission on Accreditation of Healthcare Organizations, or any lawfully operated institution that provides in-patient treatment under the direction of a staff of physicians and has 24-hour per day nursing services. An eligible nursing home is any facility licensed by the state that provides convalescent or chronic care for in-patients who, by reason of illness or infirmity, are unable to properly care for themselves. An eligible attending physician is any health care practitioner licensed, board certified or board eligible, who is qualified to practice in the area of medicine or in a specialty appropriate to treat the Owner’s condition or disease. It does not include the Owner or a member of the Owner’s family.

If the Contract is owned by a non-natural person, the confinement of the Annuitant in an eligible healthcare facility will be treated as confinement of the Owner for purposes of relying on this waiver.

TERMINAL ILLNESS WAIVER

If approved in your state and after the first Contract Year, there is no surrender charge or MVAs on withdrawals that you make while you are terminally ill and not expected to live more than 12 months. For you to rely on this waiver, we must receive an eligible attending physician’s certification regarding your illness and life expectancy and stating that your illness was diagnosed after your Contract Date. Only an original Owner continuously listed since the Contract Date, or a spousal Beneficiary who continued the Contract, may rely on this waiver. If the Contract is owned by a non-natural person, the Annuitant will be treated as the Owner for purposes of determining eligibility.

An eligible attending physician is any health care practitioner licensed, board certified or board eligible, who is qualified to practice in the area of medicine or in a specialty appropriate to treat the Owner’s condition or disease. It does not include the Owner or a member of the Owner’s family.

DENIAL OF WAIVER CLAIMS

If we do not waive surrender charges or MVAs for a hospital or nursing home confinement, or a terminal illness, we will notify you of the denial, and will not process the withdrawal until we have received confirmation from you to proceed with the withdrawal.

INDEXED ACCOUNT CHARGE

Certain Indexed Accounts in your Contract have an Indexed Account Charge. If an Indexed Account has such a charge it is reflected in Appendix A under the Current Limit on Index Loss column. Not all Indexed Accounts have an Indexed Account Charge. Electing to allocate funds to an Indexed Account with an Indexed Account Charge offers the potential of increased Indexed Interest from a higher Cap or a higher Participation Rate for the Interest Term.

The Indexed Account Charge is an amount deducted from the Indexed Account for each Interest Term. The Indexed Account Charge rate will not change during the life of your Contract. The current Indexed Account Charge rate is 1% per Interest Term year. We calculate the amount of the Indexed Account Charge at the beginning of each Interest Term. The amount of the charge is equal to the Base Value of the Indexed Account multiplied by the Indexed Account Charge rate and further multiplied by the number of years in the Interest Term. For example, if the Indexed Account Base Value on the first day of the Interest Term is $10,000 and the length of the Interest Term is six years the Indexed Account Charge equals $600. This is arrived at by multiplying the Base Value of $10,000 by the charge rate of 6% and further multiplying by 6, the number of years in the Interest Term.