Exhibit 99.2

CONFIDENTIAL | Chicago Atlantic BDC, Inc. Chicago Atlantic BDC, Inc. ("LIEN") & Chicago Atlantic Real Estate Finance, Inc. ("REFI") Overview of Proposed Merger Between LIEN and REFI June 18, 2026

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 2 The information contained in this presentation should be viewed in conjunction with the Agreement and Plan of Merger (the "Merger Agreement") among LIEN, REFI (together with LIEN, the "Companies"), Chicago Atlantic BDC Advisers, LLC (the "LIEN Adviser") and Chicago Atlantic REIT Manager, LLC (the "REFI Manager"), dated June 18, 2026, and the Companies' respective Current Reports on Form 8-K dated June 18, 2026. The information contained herein may not be used, reproduced or distributed to others, in whole or in part, for any other purpose without the prior written consent of the Companies. This presentation does not constitute a prospectus and should under no circumstances be understood as an offer to sell or the solicitation of an offer to buy either of the Companies' respective common stock or any other securities nor will there be any sale of the common stock or any other securities referred to in this presentation in any state or jurisdiction in which such offer, solicitation or sale would be unlawful prior to the registration or qualification under the securities laws of such state or jurisdiction. Nothing in these materials should be construed as a recommendation to invest in any securities that may be issued by either of the Companies or as legal, accounting or tax advice. An investment in securities of the type described herein presents certain risks. Nothing contained herein shall be relied upon as a promise or representation whether as to the past or future performance. Information regarding performance by each of the respective Companies' management teams and their affiliates is presented for informational purposes only. You should not rely on the historical record of the either of the Companies' management teams and their affiliates as indicative of the future performance of an investment in either of the Companies or the returns either of the Companies will, or are likely to, generate going forward. Certain information contained herein has been derived from sources prepared by third parties. While such information is believed to be reliable for the purposes used herein, neither of the Companies make no representation or warranty with respect to the accuracy of such information. This presentation contains references to trademarks and service marks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this presentation may appear without the ® or symbols, but such references are not intended to indicate, in any way, that the applicable licensor will not assert, to the fullest extent under applicable law, its rights to these trademarks and trade names. The Companies do not intend their use or display of other companies' trade names, trademarks or service marks to imply a relationship with, or endorsement or sponsorship of either of the Companies by, any other companies. The information contained in this presentation is summary information that is intended to be considered in the context of other public announcements that either of the Companies may make, by press release or otherwise, from time to time. Neither REFI nor LIEN undertakes any duty or obligation to publicly update or revise the information contained in this presentation, except as required by law. These materials contain information about each of the Companies, certain of their personnel and affiliates and their historical performance. You should not view information related to the past performance of either of the Companies as indicative of future results, the achievement of which cannot be assured. Past performance does not guarantee future results, which may vary. The value of investments and the income derived from investments will fluctuate and can go down as well as up. A loss of principal may occur. Certain information contained herein may constitute "forward-looking statements" that involve substantial risks and uncertainties. Such statements involve known and unknown risks, uncertainties and other factors and undue reliance should not be placed thereon. These forward-looking statements are not historical facts, but rather are based on current expectations, estimates and projections about each of the respective Companies, their current and prospective portfolio investments, their industry, their beliefs and opinions, and their assumptions. Words such as "anticipates," "expects," "intends," "plans," "will," "may," "continue," "believes," "seeks," "estimates," "would," "could," "should," "targets," "projects," "outlook," "potential," "predicts" and variations of these words and similar expressions are intended to identify forward-looking statements. These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond either of the Companies' control and difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements including, without limitation, the risks, uncertainties and other factors identified in each of REFI and LIEN's filings with the Securities and Exchange Commission (the "SEC"). Investors should not place undue reliance on these forward-looking statements, which apply only as of the date on which either of the Companies make them. Neither REFI nor LIEN undertakes any obligation to update or revise any forward-looking statements or any other information contained herein, except as required by applicable law.` Disclaimers and Forward-Looking Statements Filed by Chicago Atlantic BDC, Inc. pursuant to Rule 425 under the Securities Act of 1933 and deemed filed pursuant to Rule 425 under the Securities Act of 1933 and deemed filed pursuant to Rule 14a-12 under the Securities Exchange Act of 1934 Subject Company: Chicago Atlantic BDC, Inc. Commission File No.: 001-40564

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 3 LIEN, REFI and their respective directors and executive officers, the LIEN Adviser and the REFI Manager, and their respective directors, officers, members, managers, partners, employees and affiliates, and other persons may be deemed to be participants in the solicitation of proxies from the stockholders of LIEN and REFI in connection with the merger and the transactions related thereto set forth in the Merger Agreement (the "Merger") and the related proposals. Information regarding the persons who may, under the rules of the SEC, be deemed participants in the solicitation of the stockholders of LIEN and REFI in connection with the Merger and the related proposals, including a description of their direct or indirect interests, by security holdings or otherwise, will be included in the proxy statement/prospectus and other relevant materials to be filed with the SEC when they become available. Additional information regarding the ownership of LIEN and REFI securities by their respective directors and executive officers is included in such persons' SEC filings on Forms 3, 4 and 5, which can be found through the SEC's website at www.sec.gov. Information about the directors and executive officers of LIEN is also set forth in LIEN's proxy statement for its 2026 annual meeting of stockholders, filed with the SEC on April 30, 2026, and in LIEN's Annual Report on Form 10-K for the fiscal year ended December 31, 2025, filed with the SEC on March 19, 2026. Information about the directors and executive officers of REFI is also set forth in REFI's proxy statement for its 2026 annual meeting of stockholders, filed with the SEC on April 23, 2026, and in REFI's Annual Report on Form 10-K for the fiscal year ended December 31, 2025, filed with the SEC on March 12, 2026. Each of these documents is available free of charge at the SEC's website, www.sec.gov, or from LIEN's or REFI's investor relations website, as applicable. Some of the statements in this communication constitute forward-looking statements because they relate to future events, future performance or financial condition of LIEN, REFI or the Merger. These statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, to the extent applicable. Forward-looking statements may include statements as to: future operating results of the combined company and distribution projections; business prospects of the combined company and, to the extent applicable, the prospects of its portfolio companies; and the impact of the investments that the combined company expects to make. In addition, words such as "may," "might," "will," "intend," "should," "could," "can," "would," "expect," "believe," "estimate," "anticipate," "predict," "potential," "plan" or similar words indicate forward-looking statements. The forward- looking statements contained in this communication involve risks and uncertainties. Certain factors could cause actual results and conditions to differ materially from those projected, including the uncertainties associated with (i) the timing or likelihood of the Merger closing; (ii) the ability to realize the anticipated benefits of the Merger, including the risk that integration of the businesses of LIEN and REFI may be more difficult, time-consuming or costly than expected, and the risk of unanticipated transaction costs, loss of key personnel, or adverse effects on existing business relationships; (iii) the percentage of LIEN and REFI stockholders voting in favor of the proposals submitted for their approval; (iv) the possibility that competing offers or acquisition proposals will be made; (v) the possibility that any or all of the various conditions to the consummation of the Merger may not be satisfied or waived, including the risk that required regulatory approvals or non-objections, including effectiveness of the Registration Statement and Nasdaq listing authorization for the shares of LIEN common stock to be issued in the Merger, may not be obtained on the contemplated timeline or at all; (vi) risks related to diverting management's attention from ongoing business operations; (vii) the risk that stockholder litigation in connection with the Merger may result in significant costs of defense and liability; (viii) changes in the economy, financial markets, and political environment; (ix) future changes in laws or regulations, including with respect to the cannabis industry at the federal and state levels, federal enforcement policy, and any rescheduling or descheduling of cannabis under the Controlled Substances Act; (x) the risk that the Merger may not qualify as a "reorganization" within the meaning of Section 368(a) of the Internal Revenue Code; (xi) the risk that the surviving company may not qualify or maintain its qualification as a regulated investment company for U.S. federal income tax purposes; (xii) the risk that REFI may fail to maintain its qualification as a real estate investment trust through the effective time of the Merger; (xiii) the risk that REFI may be unable to complete the election to be a business development company ("BDC") on the contemplated timeline or at all; (xiv) the risk that the Exchange Ratio, which will be determined based on the Closing Net Asset Value of each of LIEN and REFI calculated shortly prior to closing, may differ from current expectations or may not reflect changes in market conditions or portfolio values between signing and closing; (xv) the risk that the amount, timing or tax treatment of the Tax Dividends required to be paid by REFI prior to the BDC Election Time may differ from current expectations, or that REFI may lack sufficient liquidity to pay such dividends on the contemplated timeline; (xvi) the risk that the conversion of REFI from a REIT to a regulated investment company may give rise to corporate-level tax on built-in gains or other tax consequences that may differ from current expectations; (xvii) the risk that operating as a BDC under the Investment Company Act of 1940, as amended (the "Investment Company Act") will subject the combined company to regulatory limitations, including with respect to leverage and affiliate transactions, that may adversely affect operating results or investment strategy; (xviii) the risk that the share repurchase program of up to $25.0 million may not be adopted, or, if adopted, may differ in size, scope, timing, or terms from current expectations; and (xix) other considerations that may be disclosed from time to time in publicly available documents filed by LIEN and REFI with the SEC. LIEN and REFI undertake no duty to update any forward-looking statements made herein. Disclaimers and Forward-Looking Statements

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 4 No Offer or Solicitation This communication is not intended to and shall not constitute an offer to sell or the solicitation of an offer to sell or the solicitation of an offer to buy any securities, or a solicitation of any vote or approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended (the "Securities Act"), or in a transaction exempt from the registration requirements of the Securities Act. Additional Information and Where to Find It This communication relates to the proposed Merger involving LIEN and REFI, along with related proposals for which stockholder approval will be sought. The Merger Agreement was unanimously approved by the Boards of Directors of both LIEN and REFI, each acting on the unanimous recommendation of its respective Special Committee comprised solely of independent directors. In connection with the proposals, LIEN intends to file relevant materials with the SEC, including a registration statement on Form N-14, which will include a joint proxy statement of LIEN and REFI and a prospectus of LIEN (the "Proxy Statement/Prospectus"). STOCKHOLDERS OF LIEN AND REFI ARE URGED TO READ THE PROXY STATEMENT/PROSPECTUS, AND OTHER DOCUMENTS THAT ARE FILED OR WILL BE FILED WITH THE SEC, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THESE DOCUMENTS, CAREFULLY AND IN THEIR ENTIRETY WHEN THEY BECOME AVAILABLE BECAUSE THEY WILL CONTAIN IMPORTANT INFORMATION ABOUT LIEN, REFI, THE MERGER AND THE PROPOSALS. Investors and security holders will be able to obtain the documents filed with the SEC free of charge at the SEC's website, www.sec.gov, or from each company's investor relations website at www.investors.chicagoatlanticbdc.com (LIEN) and www.investors.refi.reit (REFI), or by directing a request to LIEN@chicagoatlantic.com (LIEN) or IR@REFI.reit (REFI). Disclaimers and Forward-Looking Statements

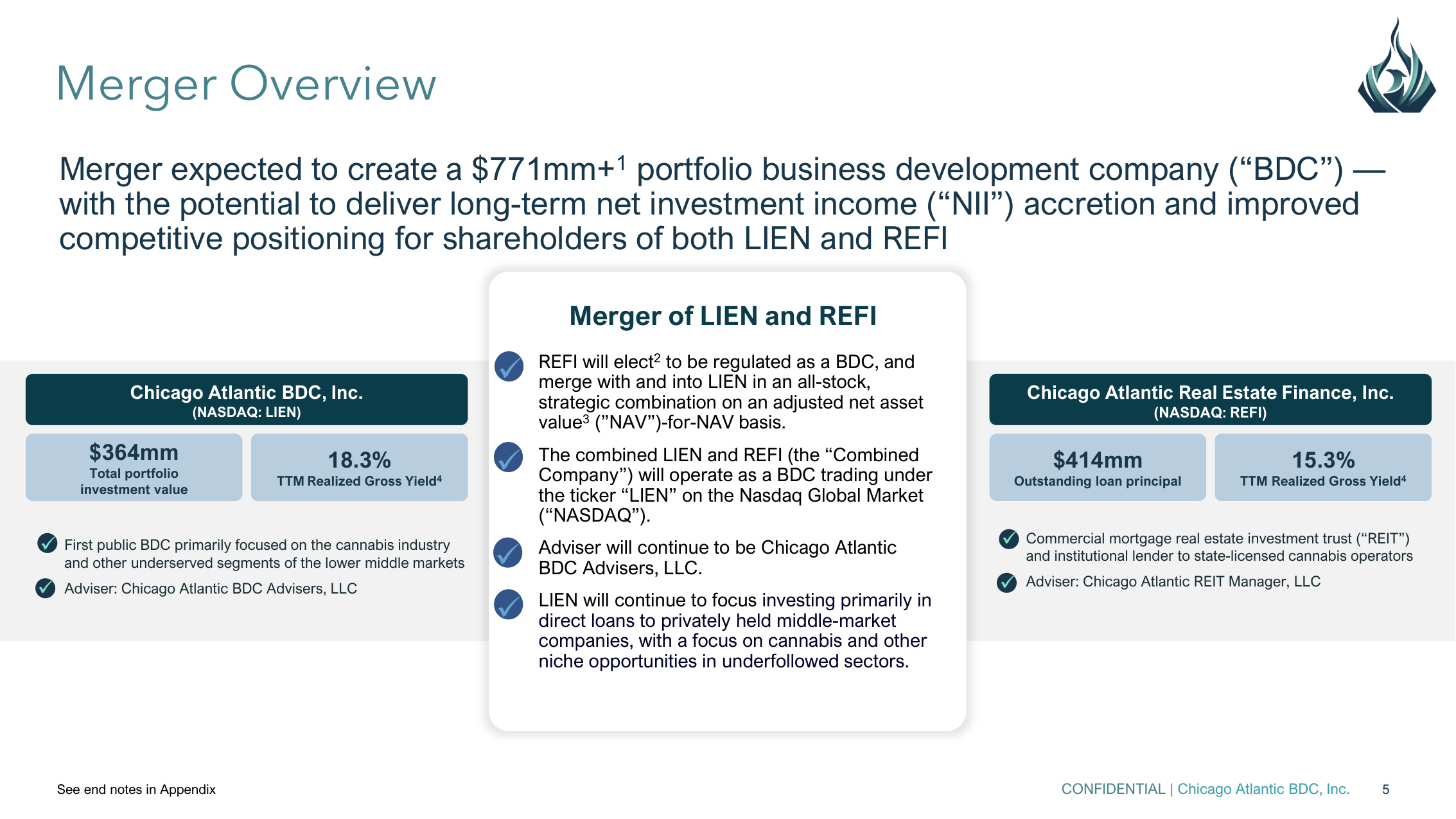

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 5 Merger expected to create a $771mm+1 portfolio business development company ("BDC") — with the potential to deliver long-term net investment income ("NII") accretion and improved competitive positioning for shareholders of both LIEN and REFI Merger Overview See end notes in Appendix Commercial mortgage real estate investment trust ("REIT") and institutional lender to state-licensed cannabis operators Adviser: Chicago Atlantic REIT Manager, LLC Chicago Atlantic Real Estate Finance, Inc. (NASDAQ: REFI) $414mm Outstanding loan principal 15.3% TTM Realized Gross Yield4 First public BDC primarily focused on the cannabis industry and other underserved segments of the lower middle markets Adviser: Chicago Atlantic BDC Advisers, LLC Chicago Atlantic BDC, Inc. (NASDAQ: LIEN) $364mm Total portfolio investment value 18.3% TTM Realized Gross Yield4 a REFI will elect2 to be regulated as a BDC, and merge with and into LIEN in an all-stock, strategic combination on an adjusted net asset value3 ("NAV")-for-NAV basis. The combined LIEN and REFI (the "Combined Company") will operate as a BDC trading under the ticker "LIEN" on the Nasdaq Global Market ("NASDAQ"). Adviser will continue to be Chicago Atlantic BDC Advisers, LLC. LIEN will continue to focus investing primarily in direct loans to privately held middle-market companies, with a focus on cannabis and other niche opportunities in underfollowed sectors. Merger of LIEN and REFI

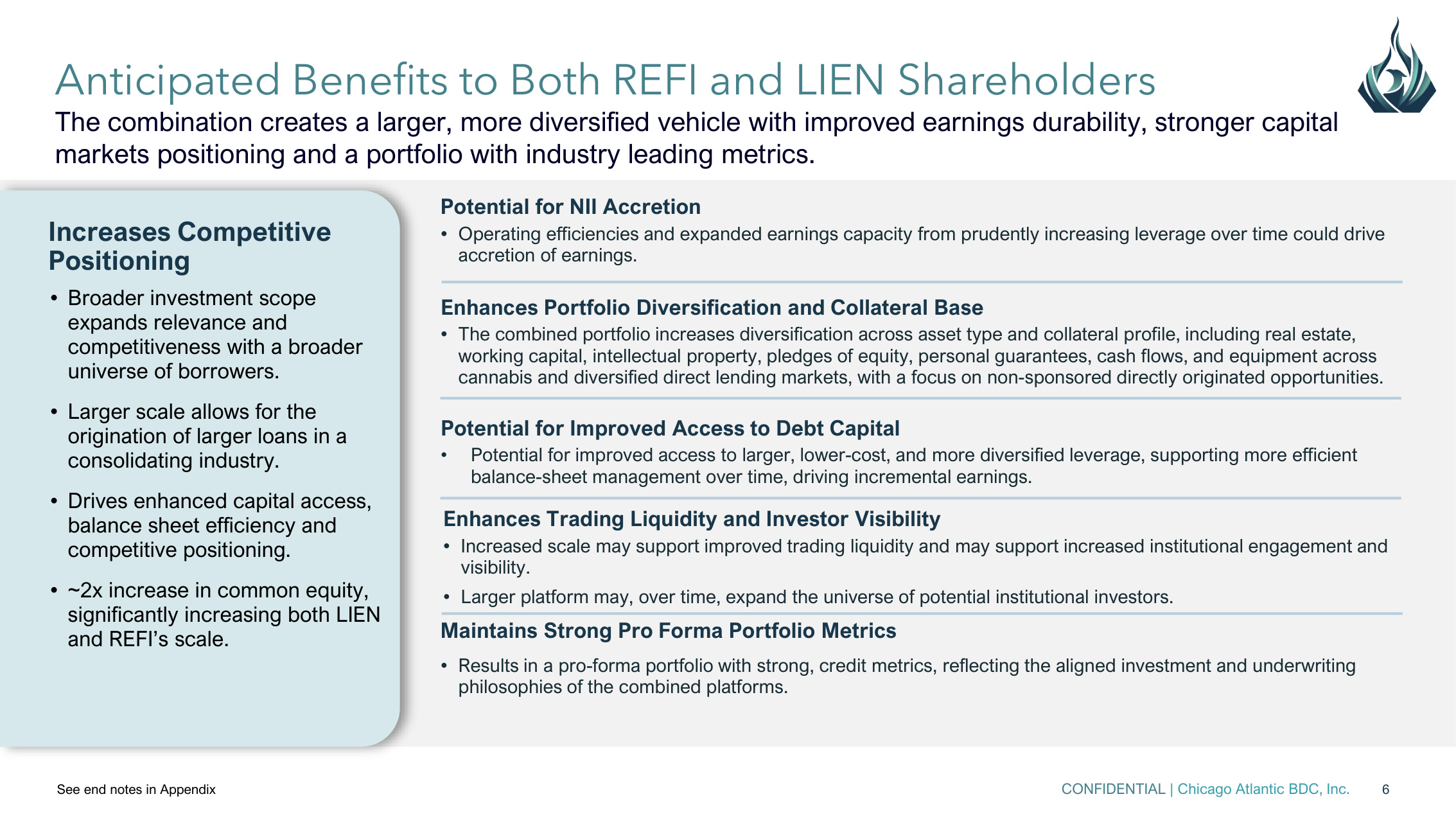

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 6 Increases Competitive Positioning • Broader investment scope expands relevance and competitiveness with a broader universe of borrowers. • Larger scale allows for the origination of larger loans in a consolidating industry. • Drives enhanced capital access, balance sheet efficiency and competitive positioning. • ~2x increase in common equity, significantly increasing both LIEN and REFI's scale. Anticipated Benefits to Both REFI and LIEN Shareholders The combination creates a larger, more diversified vehicle with improved earnings durability, stronger capital markets positioning and a portfolio with industry leading metrics. See end notes in Appendix Potential for NII Accretion • Operating efficiencies and expanded earnings capacity from prudently increasing leverage over time could drive accretion of earnings. Enhances Portfolio Diversification and Collateral Base • The combined portfolio increases diversification across asset type and collateral profile, including real estate, working capital, intellectual property, pledges of equity, personal guarantees, cash flows, and equipment across cannabis and diversified direct lending markets, with a focus on non-sponsored directly originated opportunities. Enhances Trading Liquidity and Investor Visibility • Increased scale may support improved trading liquidity and may support increased institutional engagement and visibility. • Larger platform may, over time, expand the universe of potential institutional investors. Maintains Strong Pro Forma Portfolio Metrics • Results in a pro-forma portfolio with strong, credit metrics, reflecting the aligned investment and underwriting philosophies of the combined platforms. Potential for Improved Access to Debt Capital • Potential for improved access to larger, lower-cost, and more diversified leverage, supporting more efficient balance-sheet management over time, driving incremental earnings.

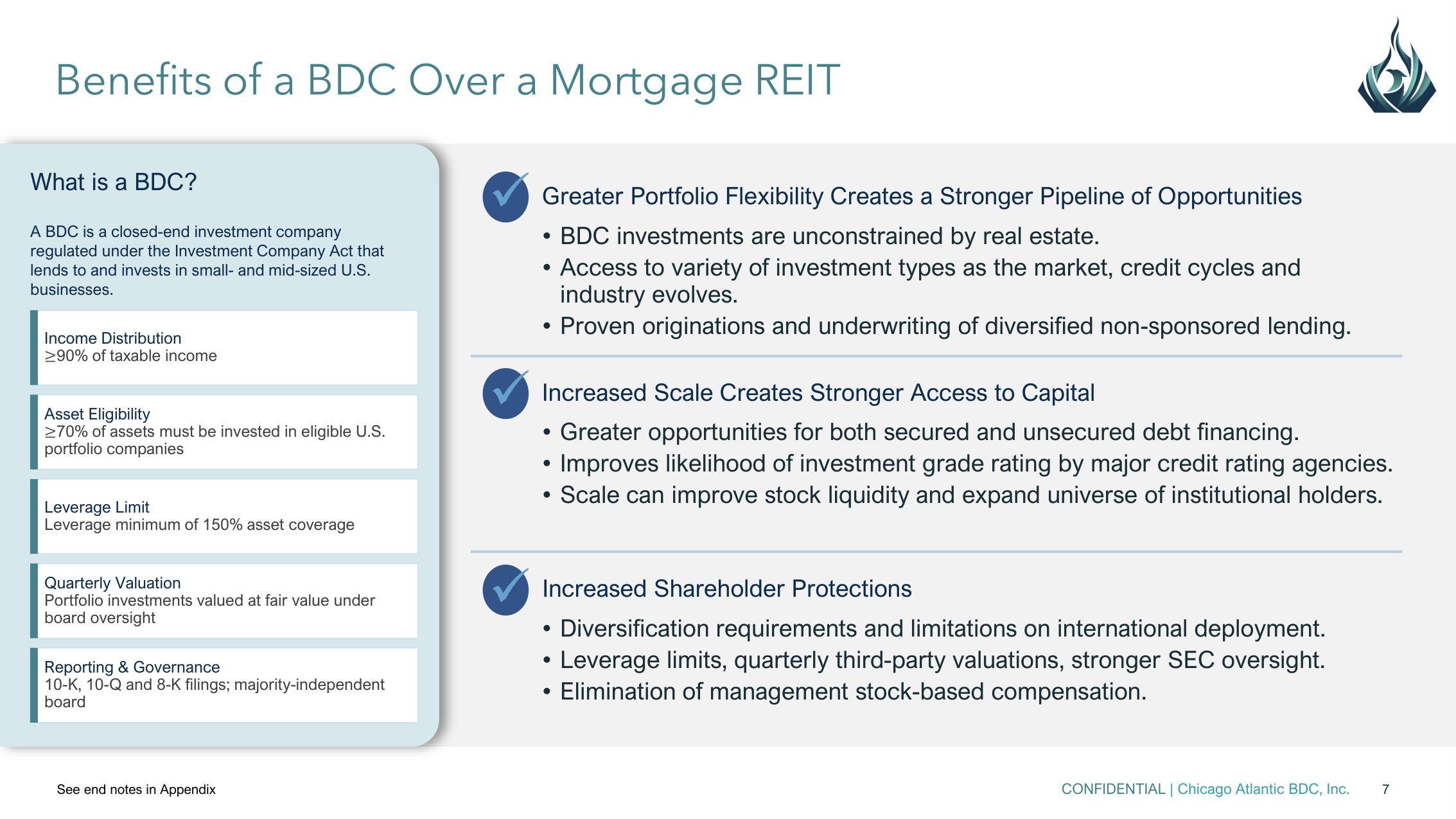

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 7 What is a BDC? A BDC is a closed-end investment company regulated under the Investment Company Act that lends to and invests in small- and mid-sized U.S. businesses. Benefits of a BDC Over a Mortgage REIT See end notes in Appendix Income Distribution ≥90% of taxable income Asset Eligibility ≥70% of assets must be invested in eligible U.S. portfolio companies Leverage Limit Leverage minimum of 150% asset coverage Quarterly Valuation Portfolio investments valued at fair value under board oversight Reporting & Governance 10-K, 10-Q and 8-K filings; majority-independent board • Diversification requirements and limitations on international deployment. • Leverage limits, quarterly third-party valuations, stronger SEC oversight. • Elimination of management stock-based compensation. Increased Shareholder Protections • BDC investments are unconstrained by real estate. • Access to variety of investment types as the market, credit cycles and industry evolves. • Proven originations and underwriting of diversified non-sponsored lending. Greater Portfolio Flexibility Creates a Stronger Pipeline of Opportunities • Greater opportunities for both secured and unsecured debt financing. • Improves likelihood of investment grade rating by major credit rating agencies. • Scale can improve stock liquidity and expand universe of institutional holders. Increased Scale Creates Stronger Access to Capital

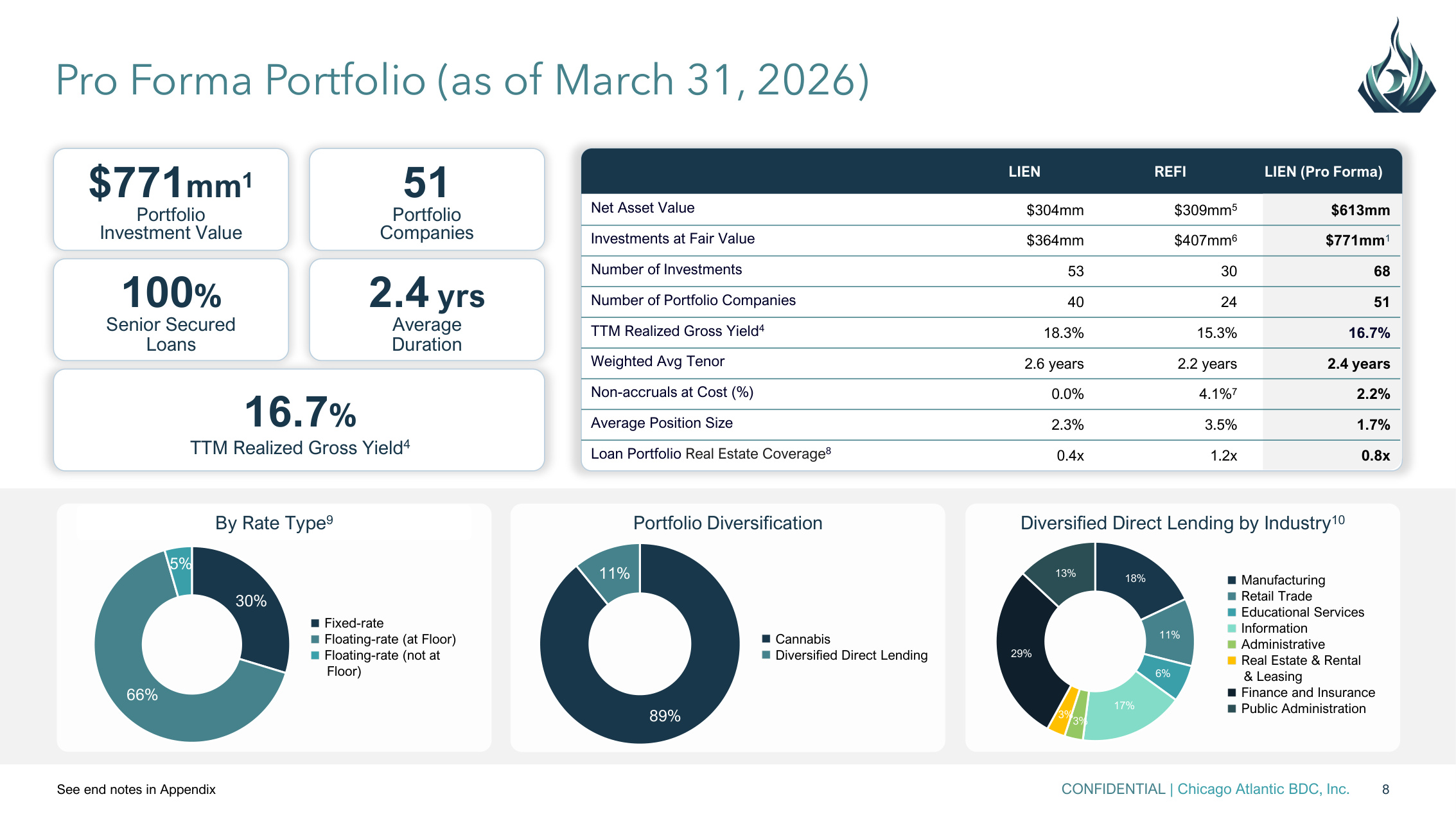

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 8 LIEN REFI LIEN (Pro Forma) Net Asset Value $304mm $309mm5 $613mm Investments at Fair Value $364mm $407mm6 $771mm1 Number of Investments 53 30 68 Number of Portfolio Companies 40 24 51 TTM Realized Gross Yield4 18.3% 15.3% 16.7% Weighted Avg Tenor 2.6 years 2.2 years 2.4 years Non-accruals at Cost (%) 0.0% 4.1%7 2.2% Average Position Size 2.3% 3.5% 1.7% Loan Portfolio Real Estate Coverage8 0.4x 1.2x 0.8x By Rate Type9 30% 66% 5% Fixed-rate Floating-rate (at Floor) Floating-rate (not at Floor) Portfolio Diversification Cannabis Diversified Direct Lending 89% 11% Diversified Direct Lending by Industry10 Manufacturing Retail Trade Educational Services Information Administrative Real Estate & Rental & Leasing Finance and Insurance Public Administration 18% 11% 6% 17% 3% 3% 29% 13% Pro Forma Portfolio (as of March 31, 2026) See end notes in Appendix 2.4 yrs Average Duration 51 Portfolio Companies 100% Senior Secured Loans 16.7% TTM Realized Gross Yield4 $771mm1 Portfolio Investment Value

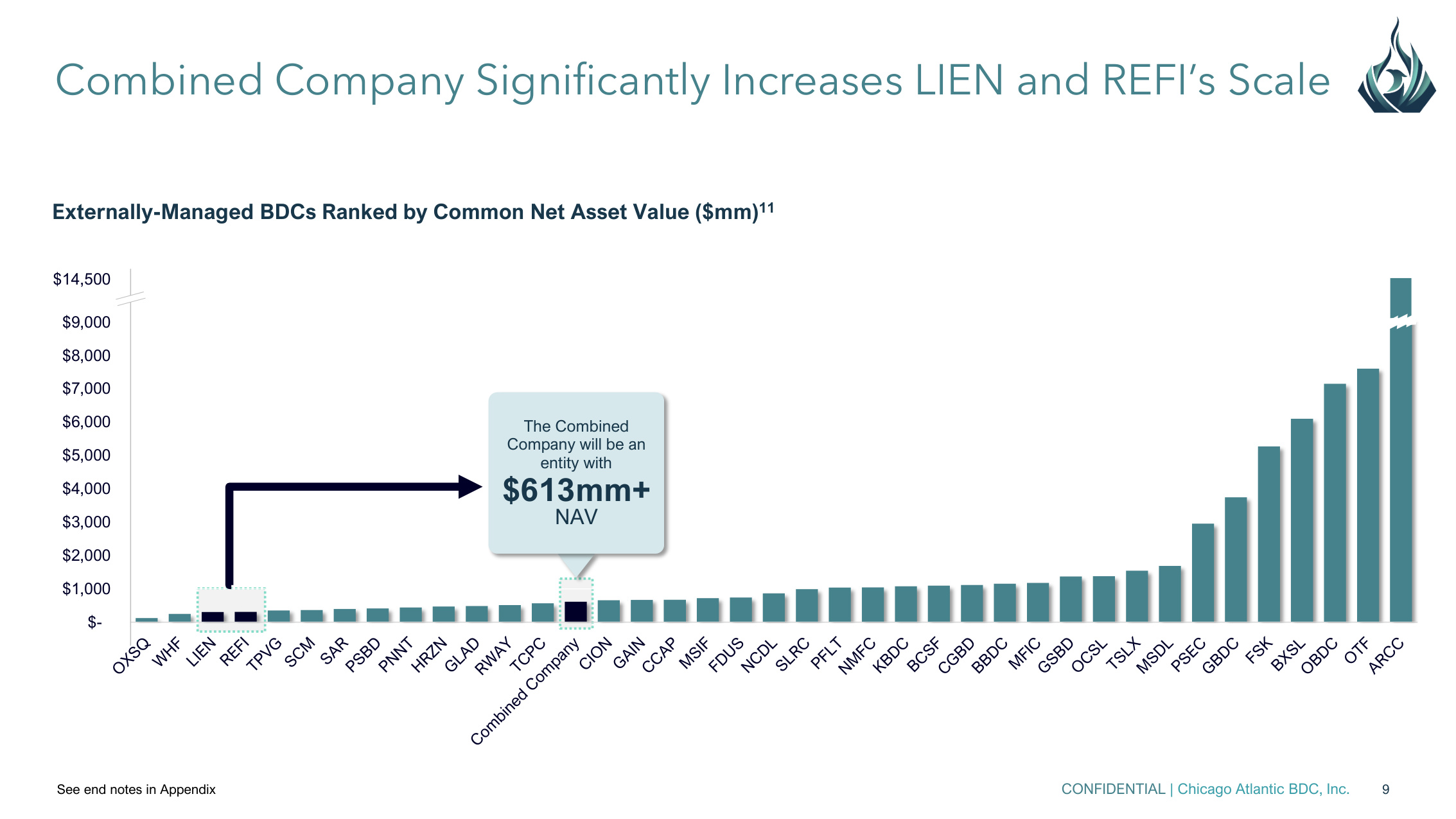

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 9 Combined Company Significantly Increases LIEN and REFI's Scale See end notes in Appendix $- $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000 $8,000 $9,000 Externally-Managed BDCs Ranked by Common Net Asset Value ($mm)11 The Combined Company will be an entity with $613mm+ NAV $14,500

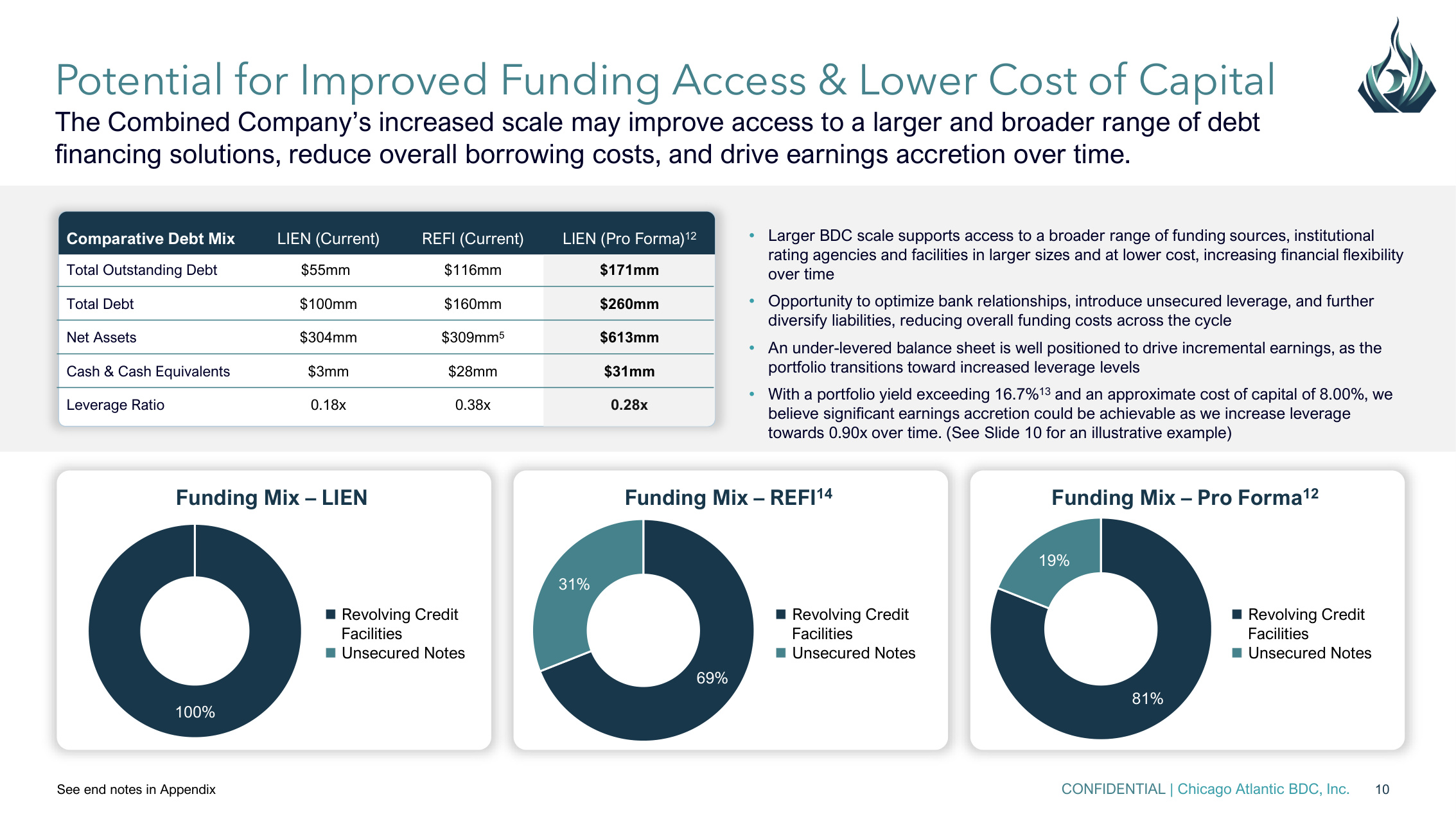

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 10 Potential for Improved Funding Access & Lower Cost of Capital The Combined Company's increased scale may improve access to a larger and broader range of debt financing solutions, reduce overall borrowing costs, and drive earnings accretion over time. See end notes in Appendix Funding Mix – REFI14 69% 31% Revolving Credit Facilities Unsecured Notes Funding Mix – LIEN Revolving Credit Facilities Unsecured Notes 100% Funding Mix – Pro Forma12 81% 19% Revolving Credit Facilities Unsecured Notes Comparative Debt Mix LIEN (Current) REFI (Current) LIEN (Pro Forma)12 Total Outstanding Debt $55mm1 $116mm $171mm Total Debt $100mm $160mm $260mm Net Assets $304mm $309mm5 $613mm Cash & Cash Equivalents $3mm $28mm $31mm Leverage Ratio 0.18x 0.38x 0.28x • Larger BDC scale supports access to a broader range of funding sources, institutional rating agencies and facilities in larger sizes and at lower cost, increasing financial flexibility over time • Opportunity to optimize bank relationships, introduce unsecured leverage, and further diversify liabilities, reducing overall funding costs across the cycle • An under-levered balance sheet is well positioned to drive incremental earnings, as the portfolio transitions toward increased leverage levels • With a portfolio yield exceeding 16.7%13 and an approximate cost of capital of 8.00%, we believe significant earnings accretion could be achievable as we increase leverage towards 0.90x over time. (See Slide 10 for an illustrative example)

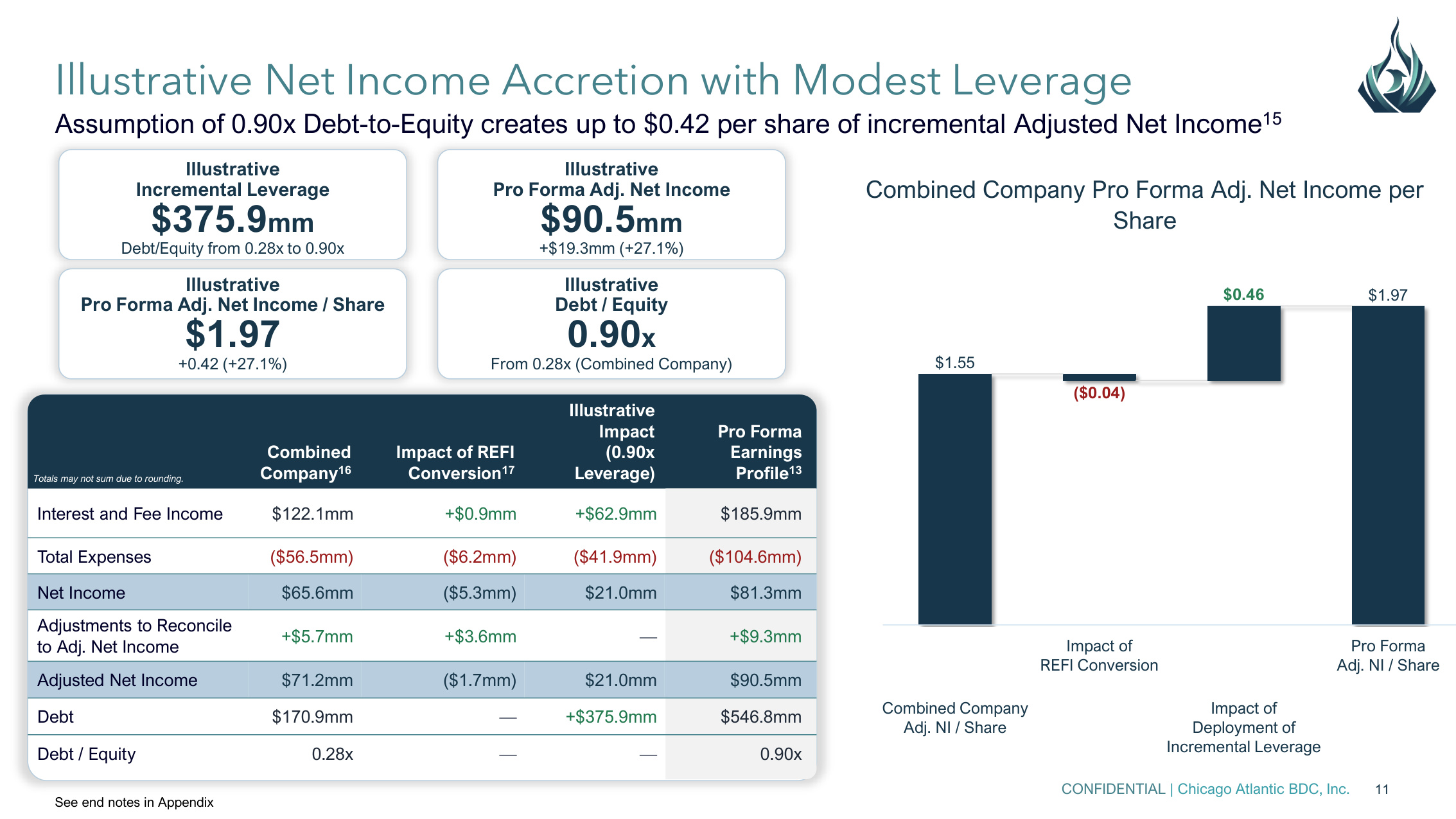

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 11 Combined Company16 Impact of REFI Conversion17 Illustrative Impact (0.90x Leverage) Pro Forma Earnings Profile13 Interest and Fee Income $122.1mm +$0.9mm +$62.9mm $185.9mm Total Expenses ($56.5mm) ($6.2mm) ($41.9mm) ($104.6mm) Net Income $65.6mm ($5.3mm) $21.0mm $81.3mm Adjustments to Reconcile to Adj. Net Income +$5.7mm +$3.6mm — +$9.3mm Adjusted Net Income $71.2mm ($1.7mm) $21.0mm $90.5mm Debt $170.9mm — +$375.9mm $546.8mm Debt / Equity 0.28x — — 0.90x Illustrative Debt / Equity 0.90x From 0.28x (Combined Company) Illustrative Pro Forma Adj. Net Income $90.5mm +$19.3mm (+27.1%) Illustrative Pro Forma Adj. Net Income / Share $1.97 +0.42 (+27.1%) Illustrative Incremental Leverage $375.9mm Debt/Equity from 0.28x to 0.90x Illustrative Net Income Accretion with Modest Leverage Assumption of 0.90x Debt-to-Equity creates up to $0.42 per share of incremental Adjusted Net Income15 See end notes in Appendix Combined Company Pro Forma Adj. Net Income per Share $1.55 $1.97 ($0.04) $0.46 Combined Company Adj. NI / Share Impact of REFI Conversion Impact of Deployment of Incremental Leverage Pro Forma Adj. NI / Share Totals may not sum due to rounding.

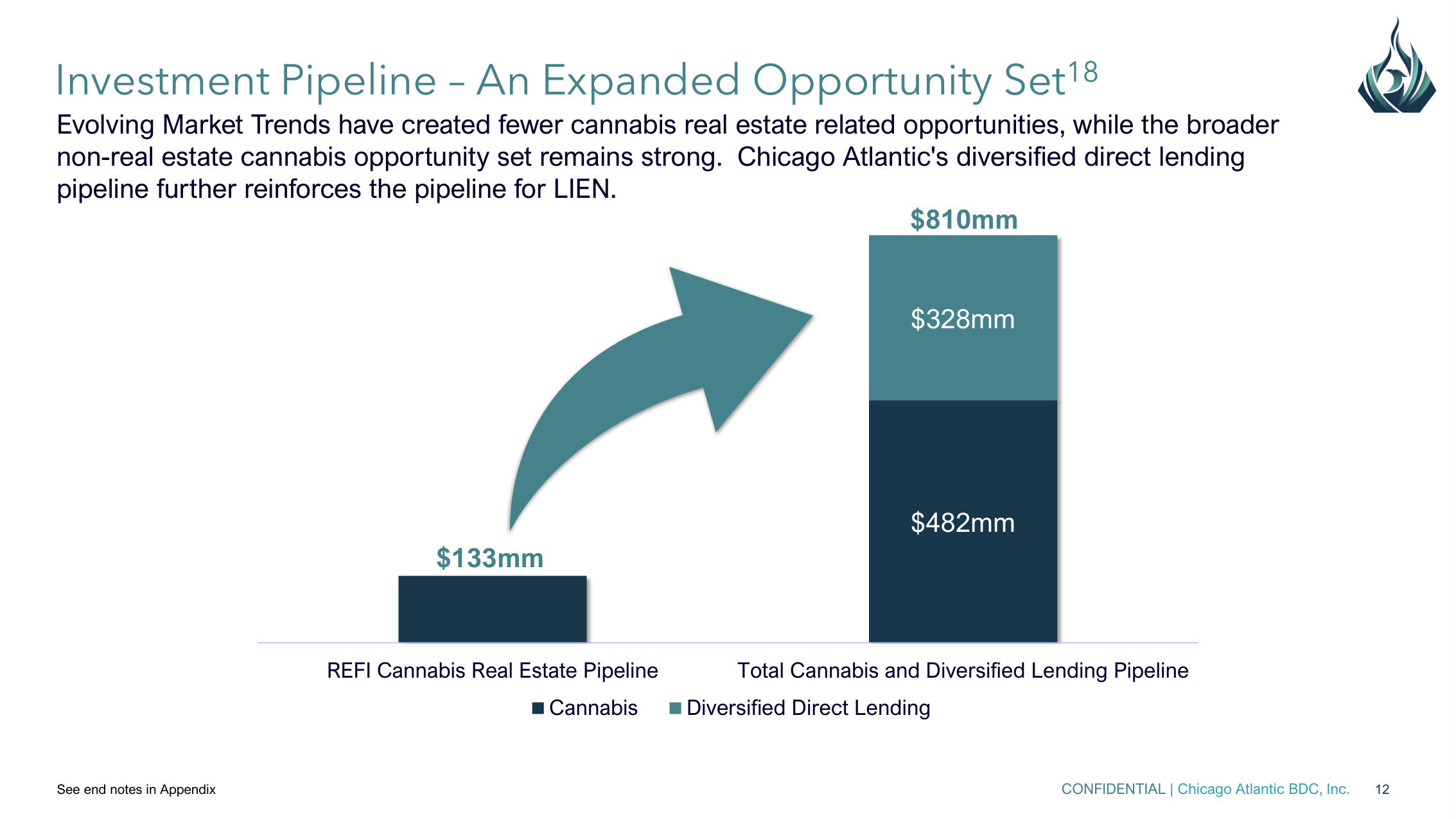

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 12 Investment Pipeline – An Expanded Opportunity Set18 $482mm $328mm REFI Cannabis Real Estate Pipeline Total Cannabis and Diversified Lending Pipeline Cannabis Diversified Direct Lending $810mm $133mm Evolving Market Trends have created fewer cannabis real estate related opportunities, while the broader non-real estate cannabis opportunity set remains strong. Chicago Atlantic's diversified direct lending pipeline further reinforces the pipeline for LIEN. See end notes in Appendix

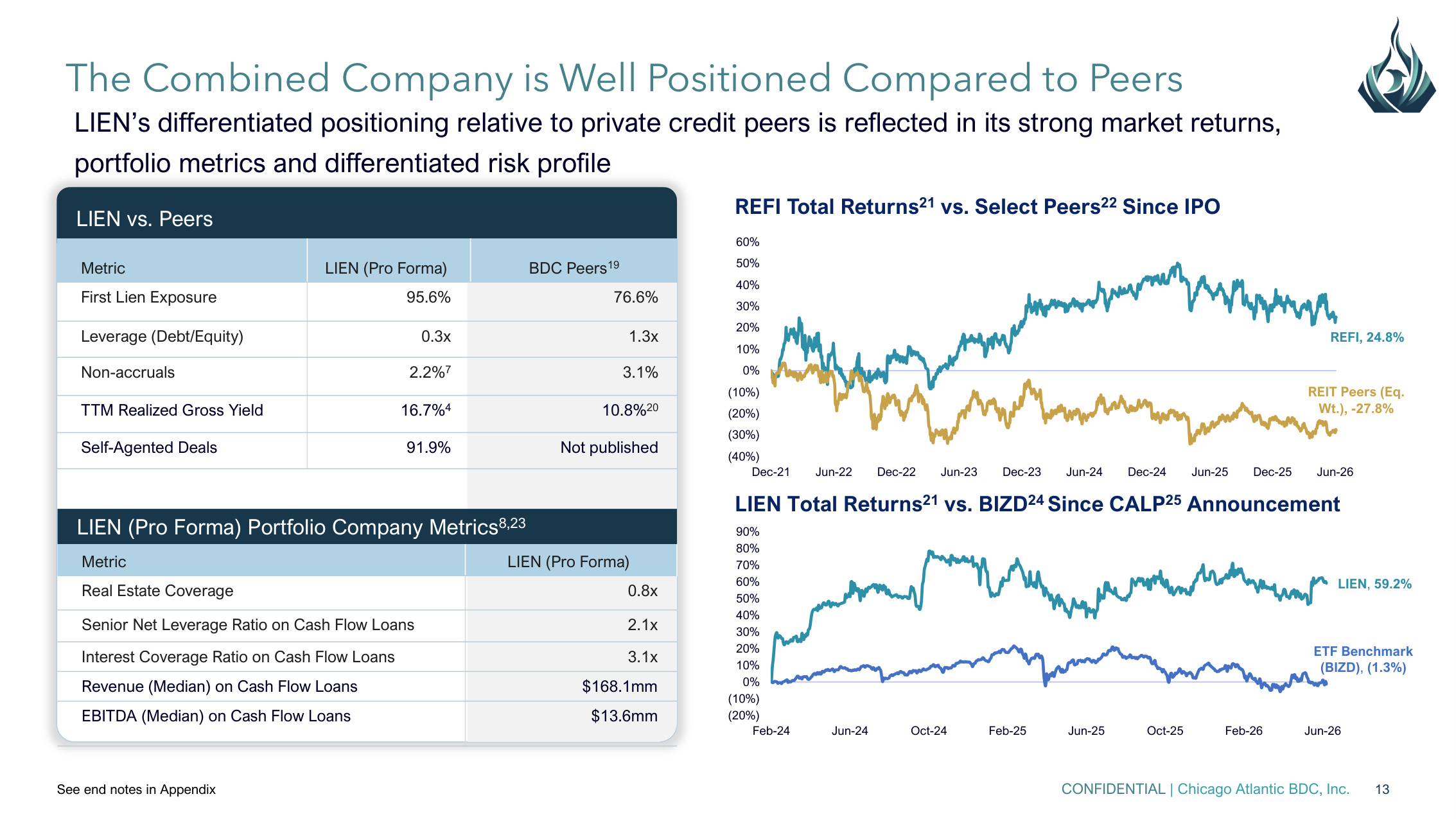

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 13 LIEN vs. Peers Metric LIEN (Pro Forma) BDC Peers19 First Lien Exposure 95.6% 76.6% Leverage (Debt/Equity) 0.3x 1.3x Non-accruals 2.2%7 3.1% TTM Realized Gross Yield 16.7%4 10.8%20 Self-Agented Deals 91.9% Not published The Combined Company is Well Positioned Compared to Peers LIEN's differentiated positioning relative to private credit peers is reflected in its strong market returns, portfolio metrics and differentiated risk profile See end notes in Appendix REFI, 24.8% REIT Peers (Eq. Wt.), -27.8% (40%) (30%) (20%) (10%) 0% 10% 20% 30% 40% 50% 60% Dec-21 Jun-22 Dec-22 Jun-23 Dec-23 Jun-24 Dec-24 Jun-25 Dec-25 Jun-26 LIEN, 59.2% ETF Benchmark (BIZD), (1.3%) (20%) (10%) 0% 10% 20% 30% 40% 50% 60% 70% 80% 90% Feb-24 Jun-24 Oct-24 Feb-25 Jun-25 Oct-25 Feb-26 Jun-26 REFI Total Returns21 vs. Select Peers22 Since IPO LIEN Total Returns21 vs. BIZD24 Since CALP25 Announcement LIEN (Pro Forma) Portfolio Company Metrics8,23 Metric LIEN (Pro Forma) Real Estate Coverage 0.8x Senior Net Leverage Ratio on Cash Flow Loans 2.1x Interest Coverage Ratio on Cash Flow Loans 3.1x Revenue (Median) on Cash Flow Loans $168.1mm EBITDA (Median) on Cash Flow Loans $13.6mm

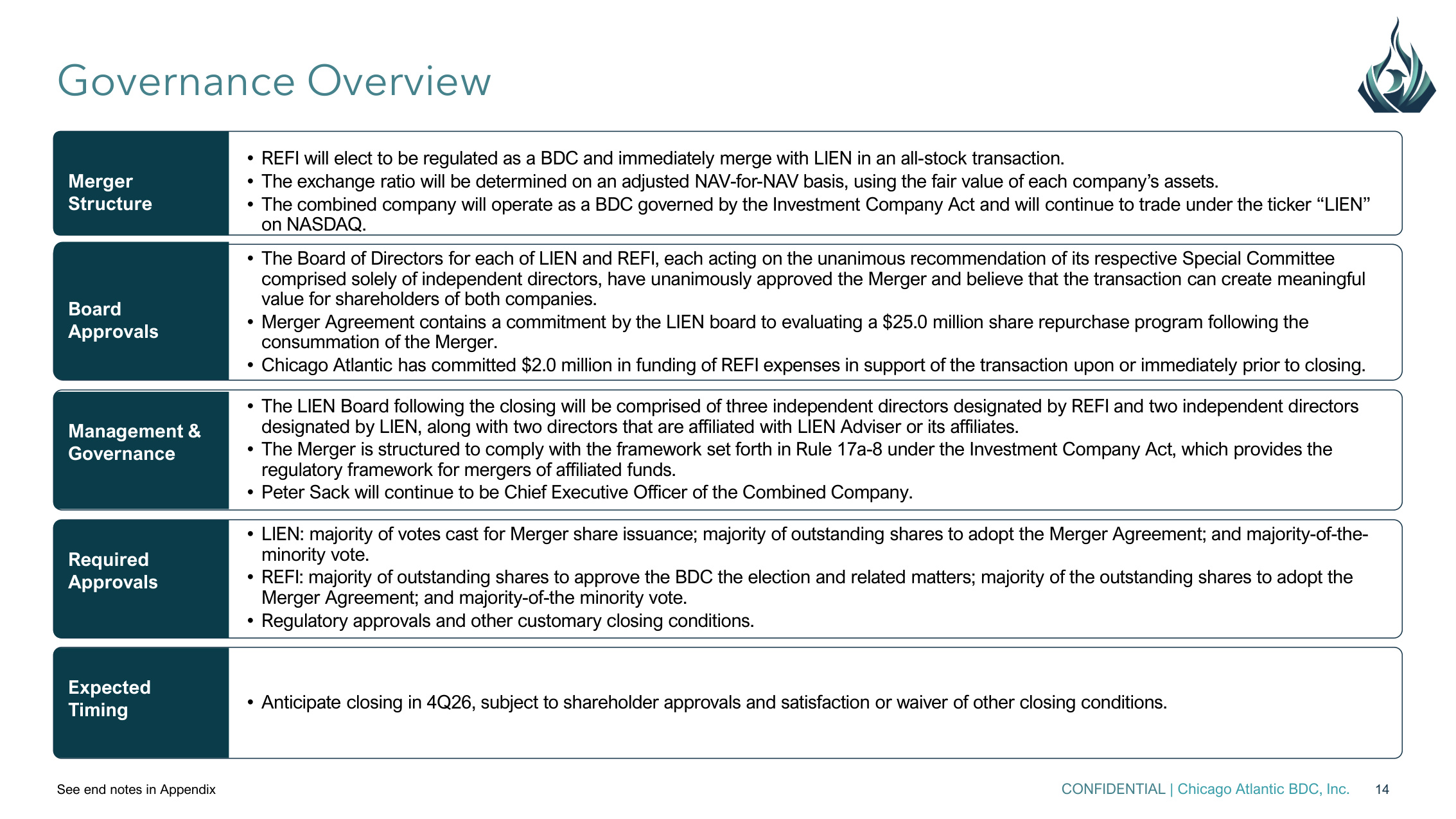

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 14 Governance Overview See end notes in Appendix • Anticipate closing in 4Q26, subject to shareholder approvals and satisfaction or waiver of other closing conditions. Expected Timing • LIEN: majority of votes cast for Merger share issuance; majority of outstanding shares to adopt the Merger Agreement; and majority-of-the- minority vote. • REFI: majority of outstanding shares to approve the BDC the election and related matters; majority of the outstanding shares to adopt the Merger Agreement; and majority-of-the minority vote. • Regulatory approvals and other customary closing conditions. Required Approvals • The LIEN Board following the closing will be comprised of three independent directors designated by REFI and two independent directors designated by LIEN, along with two directors that are affiliated with LIEN Adviser or its affiliates. • The Merger is structured to comply with the framework set forth in Rule 17a-8 under the Investment Company Act, which provides the regulatory framework for mergers of affiliated funds. • Peter Sack will continue to be Chief Executive Officer of the Combined Company. Management & Governance • The Board of Directors for each of LIEN and REFI, each acting on the unanimous recommendation of its respective Special Committee comprised solely of independent directors, have unanimously approved the Merger and believe that the transaction can create meaningful value for shareholders of both companies. • Merger Agreement contains a commitment by the LIEN board to evaluating a $25.0 million share repurchase program following the consummation of the Merger. • Chicago Atlantic has committed $2.0 million in funding of REFI expenses in support of the transaction upon or immediately prior to closing. Board Approvals • REFI will elect to be regulated as a BDC and immediately merge with LIEN in an all-stock transaction. • The exchange ratio will be determined on an adjusted NAV-for-NAV basis, using the fair value of each company's assets. • The combined company will operate as a BDC governed by the Investment Company Act and will continue to trade under the ticker "LIEN" on NASDAQ. Merger Structure

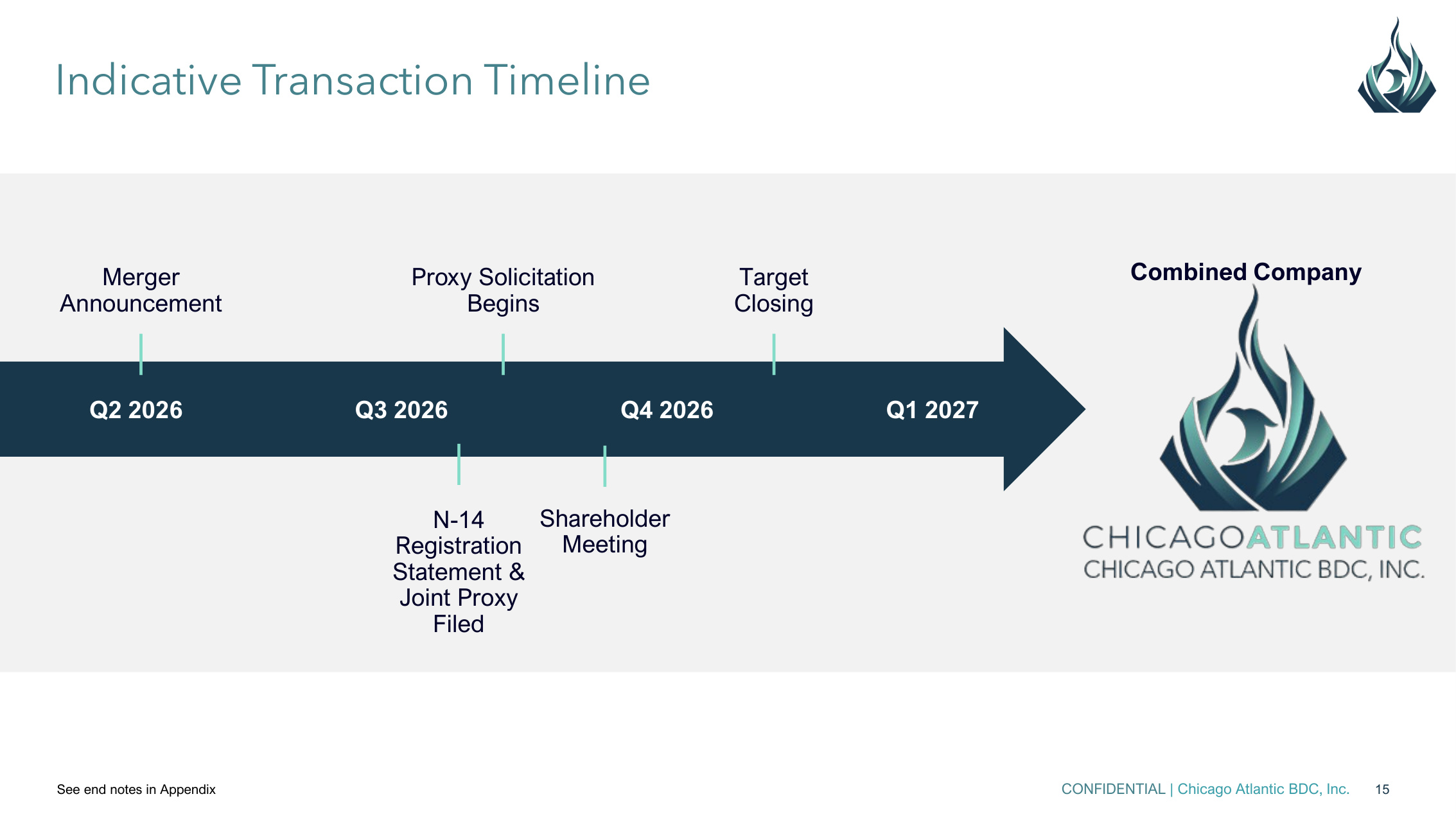

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 15 See end notes in Appendix Q2 2026 Merger Announcement Q3 2026 Q4 2026 Target Closing Proxy Solicitation Begins Combined Company Q1 2027 Indicative Transaction Timeline N-14 Registration Statement & Joint Proxy Filed Shareholder Meeting

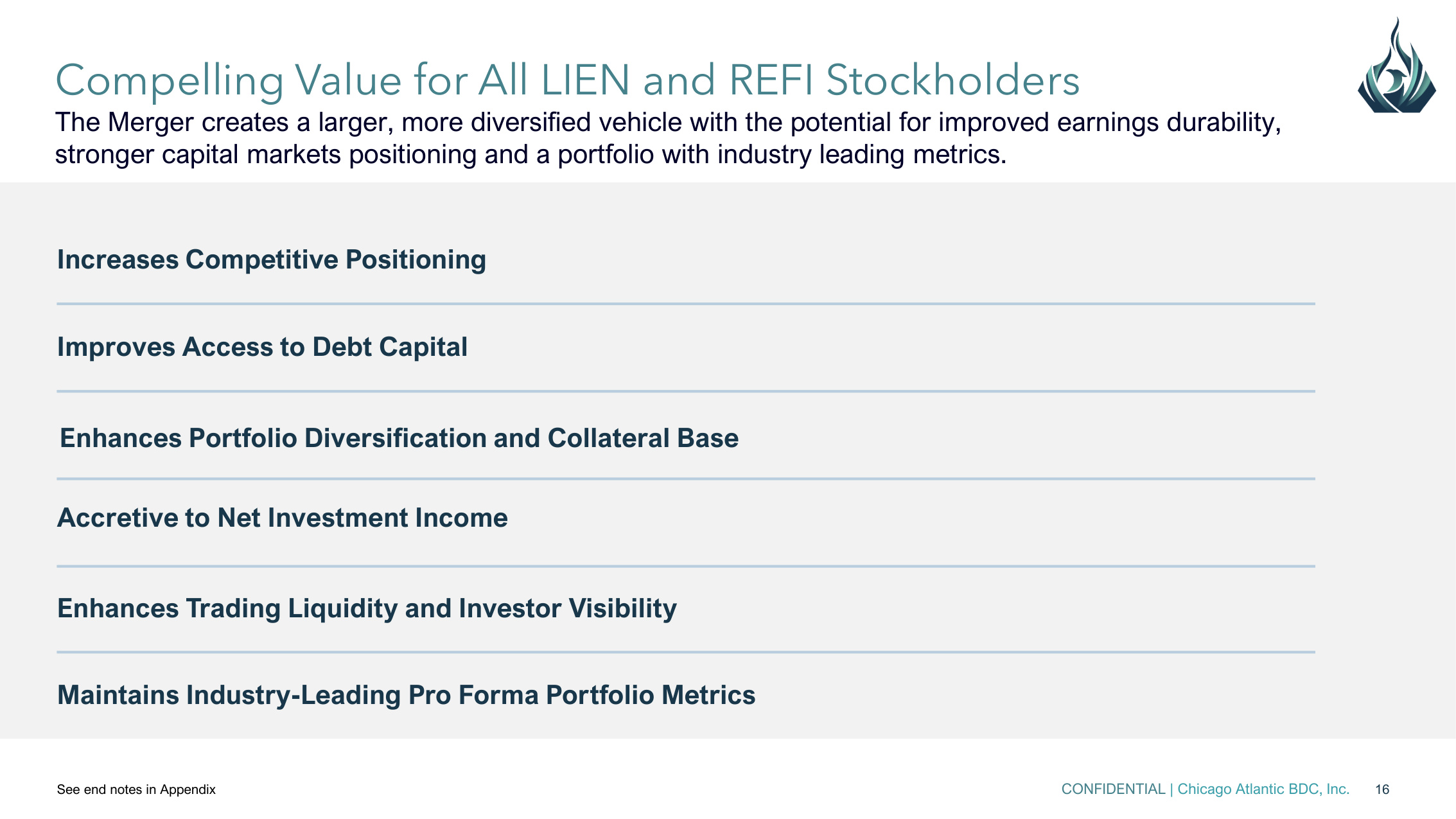

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 16 Compelling Value for All LIEN and REFI Stockholders The Merger creates a larger, more diversified vehicle with the potential for improved earnings durability, stronger capital markets positioning and a portfolio with industry leading metrics. See end notes in Appendix Improves Access to Debt Capital Maintains Industry-Leading Pro Forma Portfolio Metrics Enhances Trading Liquidity and Investor Visibility Accretive to Net Investment Income Increases Competitive Positioning Enhances Portfolio Diversification and Collateral Base

Appendix

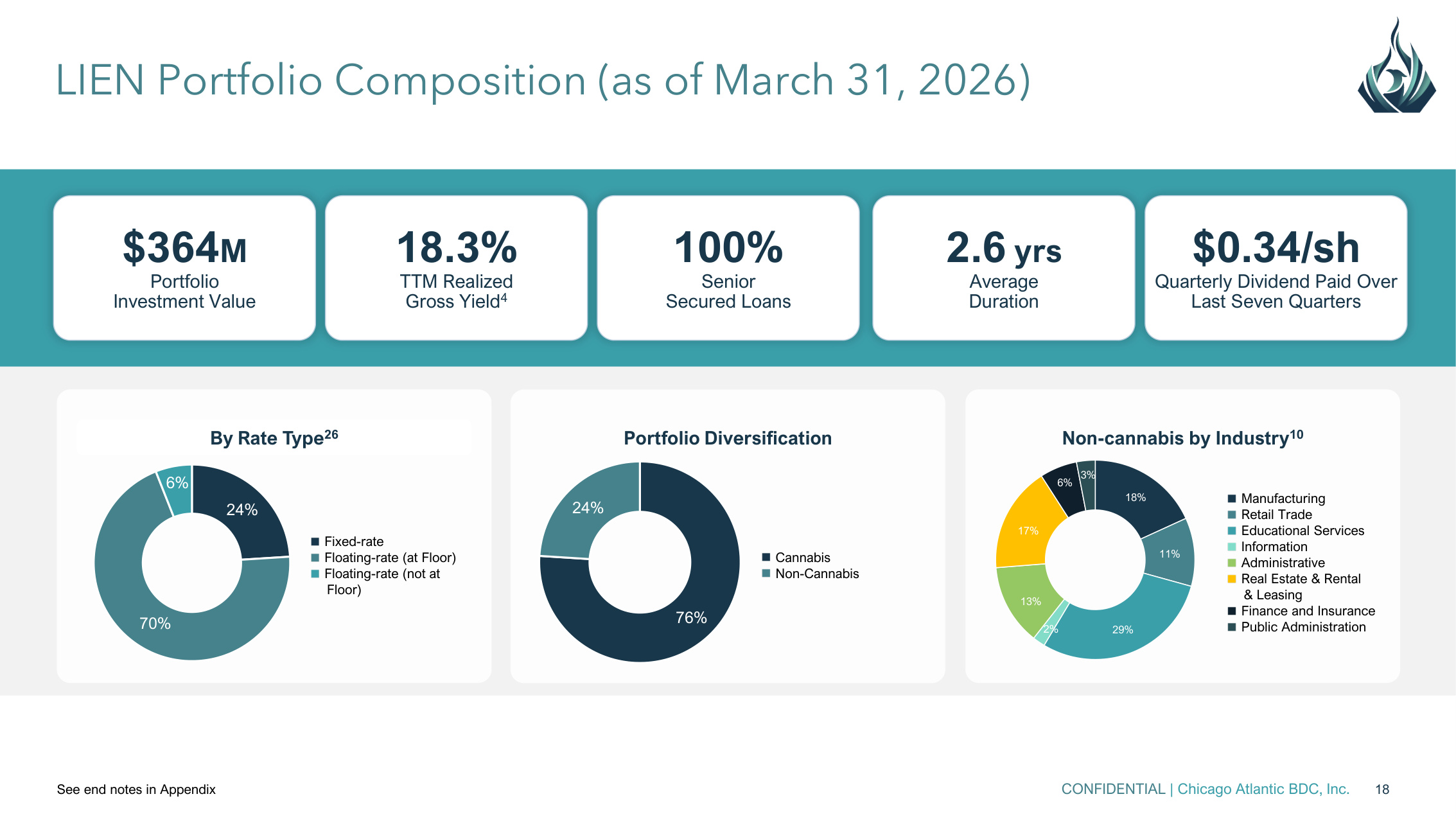

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 18 By Rate Type26 24% 70% 6% Fixed-rate Floating-rate (at Floor) Floating-rate (not at Floor) Portfolio Diversification Cannabis Non-Cannabis 76% 24% Non-cannabis by Industry10 Manufacturing Retail Trade Educational Services Information Administrative Real Estate & Rental & Leasing Finance and Insurance Public Administration 18% 11% 29% 2% 13% 17% 6% 3% 100% Senior Secured Loans $0.34/sh Quarterly Dividend Paid Over Last Seven Quarters 18.3% TTM Realized Gross Yield4 $364M Portfolio Investment Value 2.6 yrs Average Duration LIEN Portfolio Composition (as of March 31, 2026) See end notes in Appendix

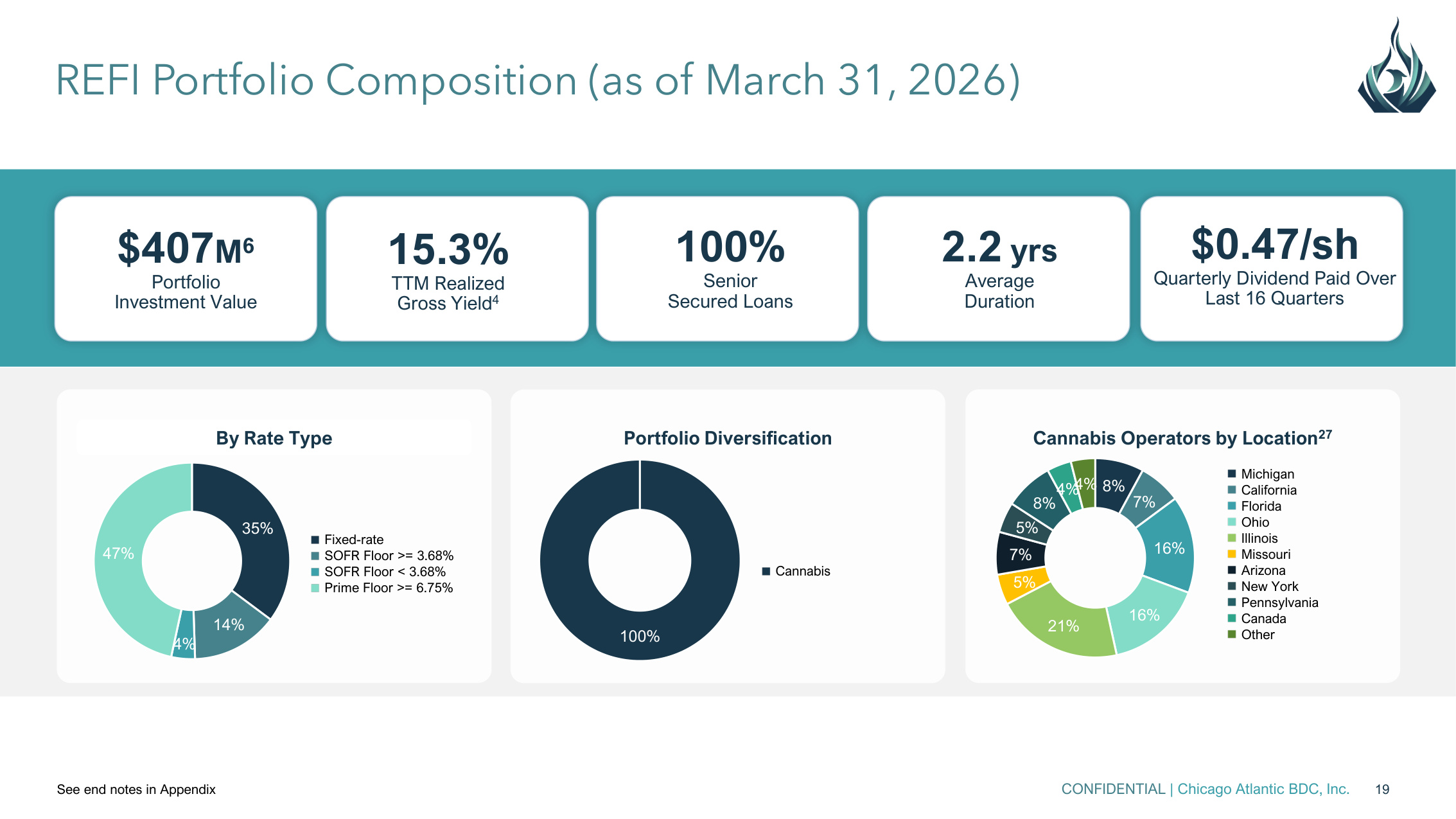

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 19 By Rate Type 35% 14% 4% 47% Fixed-rate SOFR Floor >= 3.68% SOFR Floor < 3.68% Prime Floor >= 6.75% Portfolio Diversification Cannabis 100% Cannabis Operators by Location27 Michigan California Florida Ohio Illinois Missouri Arizona New York Pennsylvania Canada Other 8% 7% 16% 16% 21% 5% 7% 5% 8% 4%4% REFI Portfolio Composition (as of March 31, 2026) See end notes in Appendix 100% Senior Secured Loans 15.3% TTM Realized Gross Yield4 $407M6 Portfolio Investment Value 2.2 yrs Average Duration $0.47/sh Quarterly Dividend Paid Over Last 16 Quarters

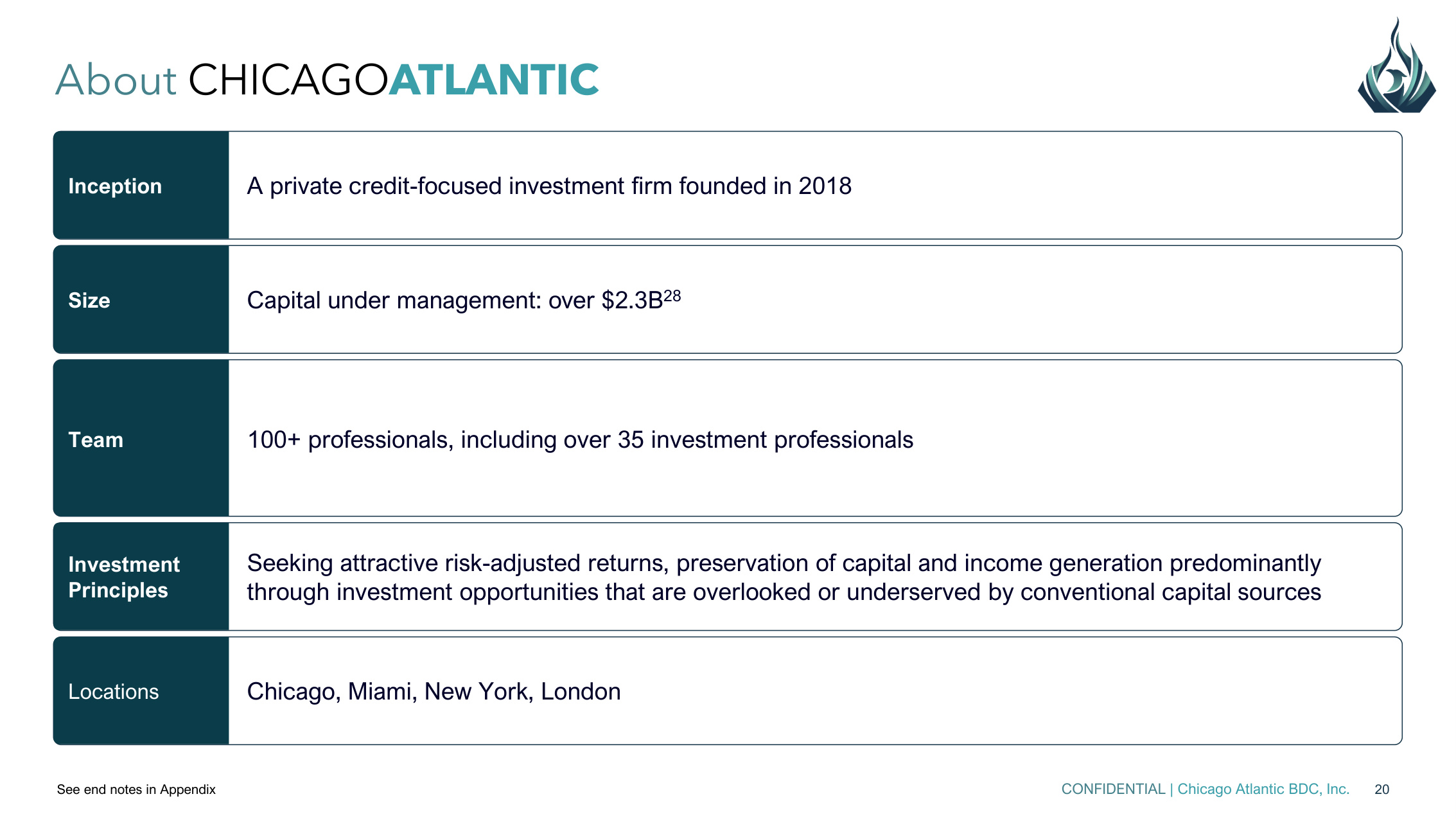

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 20 Chicago, Miami, New York, London Locations Seeking attractive risk-adjusted returns, preservation of capital and income generation predominantly through investment opportunities that are overlooked or underserved by conventional capital sources Investment Principles Capital under management: over $2.3B28 Size Team 100+ professionals, including over 35 investment professionals A private credit-focused investment firm founded in 2018 Inception About CHICAGOATLANTIC See end notes in Appendix

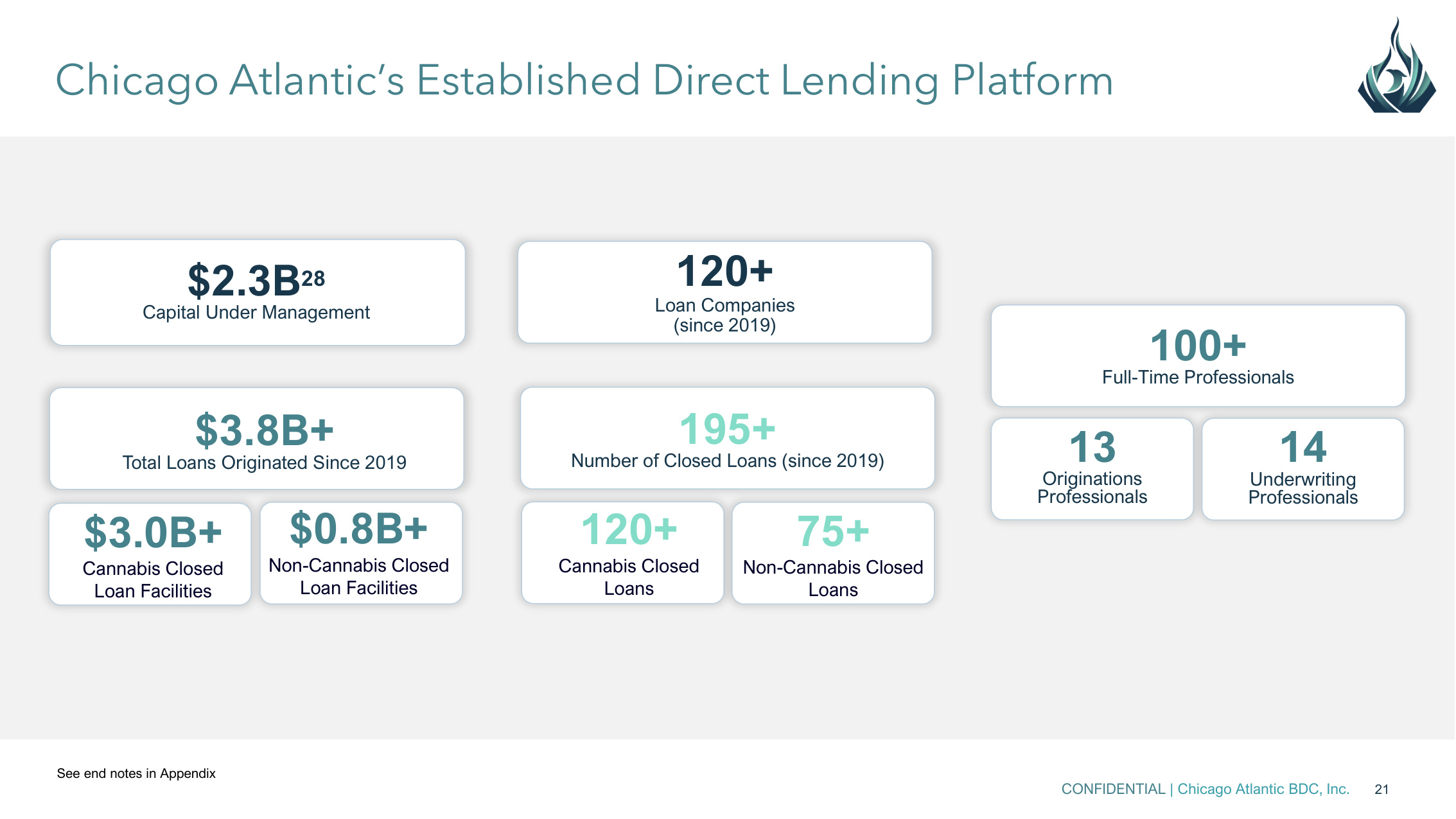

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 21 Chicago Atlantic's Established Direct Lending Platform $2.3B28 Capital Under Management 120+ Loan Companies (since 2019) 100+ Full-Time Professionals 13 Originations Professionals $3.8B+ Total Loans Originated Since 2019 $3.0B+ Cannabis Closed Loan Facilities $0.8B+ Non-Cannabis Closed Loan Facilities 195+ Number of Closed Loans (since 2019) 120+ Cannabis Closed Loans $0.8B+ Non-Cannabis Closed Loan Facilities 75+ Non-Cannabis Closed Loans 14 Underwriting Professionals See end notes in Appendix

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 22 End Notes 1) Represents the investment portfolio of the Combined Company, comprised of i) LIEN's investments at fair value as of March 31, 2026, as reported, and ii) REFI's investments as of March 31, 2026, adjusted to a fair value basis based on most recent third-party valuations. 2) Prior to the merger, REFI (currently a REIT) will elect BDC status by filing Form N-54A with the SEC and pay a special distribution to eliminate all accumulated earnings and profits. The merger is intended to qualify as a tax-free reorganization under Section 368(a) of the Code, such that REFI stockholders would generally not recognize gain or loss on their shares. A tax opinion confirming this treatment is a condition to closing. Investors should consult their own tax advisors. 3) Capitalized terms herein are as defined in the Merger Agreement dated June 18, 2026, as filed with the SEC. 4) "TTM Realized Gross Yield" Basis of calculation: The trailing-twelve-month ("TTM") effective yield presented for each issuer is computed as TTM income divided by the trailing five-quarter average loan principal outstanding; TTM income comprises the four most recent fiscal quarters of total gross investment income for Chicago Atlantic BDC (NASDAQ: LIEN) and of interest income for Chicago Atlantic Real Estate Finance (NASDAQ: REFI), in each case as reported in the respective issuer's Forms 10-Q and 10-K. The five-quarter average principal represents the simple arithmetic mean of total loan principal outstanding at the five consecutive quarter-end dates spanning the measurement period (i.e., the period-end balance together with the four immediately preceding quarter-ends). The "Combined" effective yield treats the two issuers as a single aggregated portfolio and is computed as the sum of both issuers' TTM income divided by the sum of their respective five-quarter average principal balances, thereby representing a principal-weighted blended yield rather than a simple average of the two individual yields. The foregoing measures are non-GAAP, are derived from publicly filed financial statements, and have not been independently audited, reviewed, or otherwise verified by us; accordingly, this information is presented solely for comparative analytical purposes and should be read in conjunction with each issuer's complete audited financial statements and related notes. The Gross Weighted-Average Portfolio Yield for LIEN as of 3/31/2026 was 15.8%. The yield to maturity rate of return as reported for REFI as of 3/31/2026 was 15.8%. 5) Net asset value presented for REFI reflects adjustment for REFI's GAAP stockholders' equity of $303.4 million to reflect the add-back the reversal of CECL reserves and the fair value of investments on a comparable basis with LIEN to present net assets consistent with BDC reporting standards. 6) Represents REFI's investments at fair value as of March 31, 2026, adjusted on a fair value basis based on most recent third- party valuations. 7) Excludes one non-accrual position with approximately $3.2 million of total outstanding principal value as of March 31, 2026. The borrower repaid the outstanding balance on this loan subsequent to the quarter ended March 31, 2026. Non-accrual investments as a percentage of cost, on an unadjusted basis, would be 4.8%. 8) Portfolio metrics are presented across two categories based on the primary underwriting metric applicable to each loan. The Real Estate ("RE") includes loans underwritten primarily on real estate collateral, for which the RE Coverage Ratio — defined as the Allocable RE Value, as determined by the most recent independent third-party appraisal, divided by the outstanding loan balance at fair value — is the key underwriting and monitoring metric. Allocable RE Value represents the portion of the total appraised real estate value attributable to LIEN's collateral position and may be less than the full appraised value of the underlying property. This metric is calculated based on the weighted average of all debt investments in the portfolio, based on the fair value. 9) Based on principal outstanding for the Combined Company, approximately $342.2 million (43.9%) and $205.3 million (26.3%) of total outstanding principal bears interest based on the Prime Rate and Secured Overnight Financing Rate ("SOFR"), respectively. 10) Industries follow NAICS 2-digit Sector categorizations. 11) Universe comprised of externally-managed BDCs with total assets greater than $100.0 million. Source: "Weekly BDC/RIC Market Overview", Keefe, Bruyette & Woods published June 5, 2026. 12) Assumes consents received from each of the senior secured and unsecured lending syndicates of both REFI and LIEN. 13) Represents the TTM as of March 31, 2026, pro forma performance of the Combined Company, adjusted for changes in fee contracts and stock compensation. Assumes incremental debt added to the balance sheet to obtain a debt-to-equity ratio of 0.90x, with an 8.00% cost of incremental debt capital, deployed capital assumes all in yield on investments of 16.73%, consisting of 15.8% plus 0.93% upfront fees collected on the deployment of the illustrative amount of incremental debt totaling approx. $376 million. Amounts assumed to be realized at t=0. Actual results may vary. 14) REFI revolving loan has $110.0 million of current borrowing capacity and may be increased to $150.0 million pursuant to a committed accordion feature. 15) "Adjusted Net Income" The Combined Company Net Income is adjusted for i) Provision (Benefit) for Current Expected Credit Losses, ii) Change in Unrealized Gain (Loss). Pro forma Net Income accounts for the impact of REFI election to be treated as a BDC (including stock-based compensation) and the impact on the entity for the assumption in new leverage. 16) Represents the TTM as of March 31, 2026, aggregate performance of the two entities. REFI performance includes stock- based compensation expense of $3.6 million an excludes estimated CECL reserve of $5.6 million. 17) Includes potential expense synergies of up to 0.18% of Combined Company pro forma total assets. 18) Includes potential refinancings of existing assets. Data as of March 31, 2026. 19) Source: "BDC Quarterly Report", Oppenheimer & Co. published May 27, 2026 (unless indicated otherwise). 20) Source: "BDC Weekly Insight", Raymond James published May 29, 2026. 21) Total return index assumes dividends reinvested on ex-dividend date; series initialized at 100 on first trading day. Methodology: IQ_CLOSEPRICE_ADJ (backward dividend-adjusted close price). Index_t = (P_adj_t / P_adj_base) × 100 — mathematically equivalent to chaining daily total returns. Source: S&P Capital IQ 22) Equal-weighted REIT peers: ABR, ACRE, ARI, BXMT, CMTG, RC, GPMT, KREF, LADR, STWD, TRTX.

CONFIDENTIAL | Chicago Atlantic BDC, Inc. 23 End Notes 23) Cash Flow Loans ("CFL") includes loans underwritten on enterprise cash flow, for which Senior Net Debt / EBITDA and Interest Coverage Ratio are the key underwriting and monitoring metrics. Classification into the CFL Bucket is determined at origination based on the primary underwriting methodology and is not changed unless there is a material change in the nature of the credit support. Excluded from the CFL portfolio metrics include: (i) loans on non-accrual status, (ii) portfolio companies that report negative or de minimis EBITDA, and (iii) investment funds and special purpose vehicles for which standard operating metrics are not applicable and (iv) investments classified as real estate loans, as described above. Amounts were derived from the portfolio company financial statements used in connection with determining the investment valuations as of March 31, 2026, have not been independently verified by LIEN, and may reflect a normalized or adjusted amount. Accordingly, LIEN makes no representation or warranty in respect of this information. Amounts were derived from the portfolio company financial statements used in connection with determining the investment valuations as of 3/31/2026, have not been independently verified by LIEN, and may reflect a normalized or adjusted amount. Accordingly, LIEN makes no representation or warranty in respect of this information. 24) ETF Benchmark: BIZD (VanEck BDC Income ETF). 25) On October 1, 2024, LIEN completed its previously announced acquisition from Chicago Atlantic Loan Portfolio, LLC ("CALP") of a portfolio of loans (the "Loan Portfolio") in exchange for newly issued shares of LIEN's common stock (the "Loan Portfolio Acquisition"), pursuant to the Purchase Agreement, dated as of February 18, 2024, between the LIEN and CALP (the "Loan Portfolio Acquisition Agreement"). In accordance with the terms of the Loan Portfolio Acquisition Agreement, at the effective time of the Loan Portfolio Acquisition, LIEN issued approximately 16.6 million shares of its common stock to CALP in exchange for the Loan Portfolio, which was determined by LIEN to have a fair value of approximately $219.6 million as of September 28, 2024. Refer to "Note 13 – Loan Portfolio Acquisition" in the notes to the financial statements of LIEN's annual 10-K report filed for the year ended December 31, 2024. 26) Based on principal outstanding as of March 31, 2026, approximately $149.7 million (40.9%) and $130.2 million (35.5%) of total outstanding principal bears interest based on the Prime Rate and Secured Overnight Financing Rate ("SOFR"), respectively. 27) "Other" location category includes approximately $16.8 million of loans (4%) domiciled primarily in West Virginia (2.0%), New Jersey (0.5%), Texas (0.4%), and Maryland (0.5%). 28) Capital Under Management represents gross fund assets, unfunded commitments, undrawn leverage capacity, and co- investments.