Exhibit 99.95

FORM 51-102F3

Material Change Report

Item 1: Name and Address of Company

NuRAN Wireless Inc. (the “Company” or “NuRAN”)

Suite 100, 2150 Cyrille-Duquet

Quebec, QC G1N 2G3

Item 2: Date of Material Change

December 22, 2025

Item 3: News Release

A news release announcing the material change was issued on January 28, 2026, and filed on SEDAR+ at www.sedarplus.ca, a copy of which is attached hereto as Schedule “A”.

Item 4: Summary of Material Change

The Company announced the submission of the prospectus-level disclosure information regarding the acquisition of Advance Factoring Inc., a factoring company (the “Factor”) has resulted in a restructuring transaction within the meaning of National Instrument 51-102 – Continuous Disclosure Obligations (the “Restructuring Transaction”), and that the Company would file this material change report containing the disclosure required by sections 5.2 of Form 51-102F3 and 14.2 of Form 51-102F5 – Information Prospectus-level disclosure in respect of the Factor.

On December 23, 2025, the Company announced that it closed a broad restructuring on December 22, 2025 (the “Closing Date”). The restructuring resulted in the Company issuing an aggregate of 10,380,618 units (each, a “Unit”), at $2.89 per Unit, for aggregate gross proceeds of approximately $30 million, which included cash subscriptions of $3,025,067.98, debt settlements of $6,172,629, and the acquisition of Factor for $20,802,303.09 as a debt settlement.

In addition, on December 22, 2025, the Company also completed the closing of an initial tranche of additional subscription amounts, issuing an aggregate of 2,115,064 Units, at $2.89 per Unit, for aggregate gross proceeds of approximately $6.11 million, which included cash subscriptions of $2,599,932.02 and debt settlements of $3,512,627.23. Following this the issued and outstanding shares of the Company totalled 12,905,118.

The Company completed the acquisition of the Factor, whose principal assets consisted of factored receivables representing claims against the Company. In connection with the acquisition of the Factor, the Company issued common shares representing 55.78% of the Company’s outstanding voting securities, and as a result the vendors of the Factor are able to materially affect the control of the Company. Accordingly, the transaction constitutes a “restructuring transaction” within the meaning of paragraph (c)(i) of the definition of that term in s.1 of National Instrument 51-102 – Continuous Disclosure Obligations (“NI 51-102”).

The British Columbia Securities Commission (the “Commission”) previously advised the Company that, pending the completion and filing of a material change report containing the disclosure required under section 14.2 of Form 51-102F5 in respect of the Factor, the Company was considered to be in default of certain continuous disclosure obligations in accordance with Canadian Securities Administrators Staff Notice 51-322 – Reporting Issuer Defaults.

The Company has prepared the disclosure required under sections 5.2 of Form 51-102F3 and 14.2 of Form 51-102F5 and is filing such disclosure with this material change report in order to address the default.

1

Item 5.1: Full Description of Material Change

The material change consists of the completion and filing of this material change report containing the disclosure required under sections 5.2 of Form 51-102F3 and 14.2 of Form 51-102F5 in respect of the Factor.

5.1.1 Financial Statements

The issuance of common shares and the elimination of the related indebtedness resulting from the restructuring transaction are reflected in the Company’s audited annual financial statements and related management’s discussion and analysis (“MD&A”) for the year ended December 31, 2025 that are included in this material change report in Schedule “B” and “C”, respectively.

In connection with the acquisition of the Factor, the Company assumed the liability represented by the preferred shares of the Factor (the “Preferred Shares”). The 726,752,667 Preferred Shares issued by the Factor on December 19, 2025 are recorded as a financial liability in the amount of $7,267,527, as these shares are redeemable and retractable at the option of the holder at a redemption price of $0.01 per share. Notwithstanding the foregoing, pursuant to the Restructuring Transaction, the indebtedness under the Preferred shares constitutes intercompany balances and are eliminated in the consolidated financial statements. The key terms of the Preferred Shares, and the risks associated with this liability, are described under ‘Description of Securities — Preferred Shares” and “Risk Factors” below.

The pro forma financial statements of the Company are included in Schedule “D”. The audited financial statements of the Factor required under sections 5.2 of Form 51-102F3 and 14.2 of Form 51-102F5, together with the related management’s discussion and analysis of the Factor (“MD&A”), are included in Schedule “E” and “F” respectively to this material change report.

Item 5.2 Disclosure for Restructuring Transactions

No securities regulatory authority has expressed an opinion about the securities described herein and it is an offence to claim otherwise. This document does not constitute a preliminary prospectus. The transaction described herein has been completed.

This document provides prospectus-level disclosure in respect of the acquisition (the “Restructuring Transaction”) by Nuran (the “Company”) of Advance Factoring Inc. (the “Factor”) in connection with the Transaction, the Company issued an aggregate of 7,198,026 Units to the vendors.

Each Unit consisted of one common share in the share capital of the Company (each, a “Common Share”) and half common share purchase warrant (each, a “Warrant”), with each Warrant entitling the holder thereof to acquire one additional Common Share at an exercise price of $4.335 per share until December 22, 2030. The Common Shares were issued by the Company on December 22, 2025, in connection with the Restructuring Transaction. The issuance was completed pursuant to prospectus exemptions under applicable securities laws. The deemed issue price of the Units was $2.89 Canadian Dollars (“CAD”). Unless otherwise indicated, all references to “$” are to CAD.

The Consideration Shares were issued at a fixed deemed price in connection with the Restructuring Transaction. The deemed issue price of the Units was determined by the board of directors of the Company, having regard to, among other things the value of the assets acquired, and the amount of indebtedness settled in connection with the Restructuring Transaction.

The common shares of the Company are listed on the Canadian Securities Exchange under the symbol “NUR”.

On December 22, 2025, the last closing price of the common shares was $2.78. An investment in the Factor is subject to significant risks. See “Risk Factors”.

2

No underwriters were involved in the Transaction. The Consideration Shares were issued directly by the Company to the vendors.

The Common Shares are subject to resale restrictions under applicable securities laws.

3

TABLE OF CONTENTS

| FORWARD LOOKING INFORMATION | 7 |

| DOCUMENTS INCLUDED IN THIS MATERIAL CHANGE REPORT | 7 |

| INFORMATION CONCERNING THE FACTOR | 8 |

| CORPORATE STRUCTURE | 8 |

| Name, Address and Incorporation | 8 |

| Intercorporate Relationships | 9 |

| DESCRIPTION OF THE BUSINESS OF THE FACTOR | 10 |

| General | 10 |

| Summary | 10 |

| Specialized Skills and Knowledge | 10 |

| Competitive Conditions | 10 |

| Business or Seasonal Cycles | 10 |

| Economic Dependence | 10 |

| Changes to Contracts | 11 |

| Employees | 11 |

| Three Year History | 11 |

| Recent Developments | 11 |

| Information Concerning the Factor Following Completion of the Transaction | 14 |

| PARTICULARS OF THE MATTER – MI 61-101 | 14 |

| DIVIDENDS OR DISTRIBUTIONS | 16 |

| SELECTED CONSOLIDATED FINANCIAL INFORMATION | 16 |

| MANAGEMENT DISCUSSION & ANALYSIS | 16 |

| DESCRIPTION OF SECURITIES | 16 |

| Authorized and Outstanding Capital | 16 |

| OPTIONS TO PURCHASE SECURITIES | 17 |

| CONSOLIDATED CAPITALIZATION | 17 |

| PRIOR SALES | 18 |

| Market for Securities | 18 |

| ESCROWED SECURITIES AND SECURITIES SUBJECT TO CONTRACTUAL RESTRICTION ON TRANSFER | 18 |

| PRINCIPAL SECURITYHOLDERS | 18 |

| DIRECTORS AND EXECUTIVE OFFICERS | 19 |

| Cease Trade Orders, Bankruptcies, Penalties or Sanctions | 19 |

| EXECUTIVE COMPENSATION | 20 |

4

| Employment, Consulting and Management Agreement | 20 |

| Equity Compensation Securities | 20 |

| Oversight and Description of Director and NEOs Compensation | 20 |

| Compensation Process and Objectives | 21 |

| Pension and Retirement Plans | 21 |

| INDEBTEDNESS OF DIRECTORS AND EXECUTIVE OFFICERS | 21 |

| LEGAL PROCEEDINGS OR REGULATORY ACTIONS | 21 |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 21 |

| NON-ARM’S LENGTH PARTY TRANSACTIONS | 22 |

| AUDITOR, TRANSFER AGENT AND REGISTRAR | 22 |

| MATERIAL CONTRACTS | 22 |

| EXPERTS | 22 |

| OTHER MATERIAL FACTS | 23 |

| FINANCIAL STATEMENT DISCLOSURE | 23 |

| INFORMATION RELATING TO THE RESULTING ISSUER | 23 |

| Corporate Structure | 23 |

| Name and Incorporation | 23 |

| Intercorporate Relationships | 23 |

| NARRATIVE DESCRIPTION OF THE BUSINESS | 24 |

| Stated Business Objectives | 25 |

| DESCRIPTION OF SECURITIES | 25 |

| PRO FORMA CONSOLIDATED CAPITALIZATION | 25 |

| AVAILABLE FUNDS AND PRINCIPAL PURPOSE | 26 |

| DIVIDENDS | 26 |

| PRINCIPAL SECURITYHOLDERS | 27 |

| DIRECTORS, OFFICERS AND PROMOTERS | 27 |

| Name, Address, Occupation and Security Holdings | 27 |

| Biographies of Management and Directors | 29 |

| Relevant Education and Experience of Managers and Directors | 29 |

| Promoter Consideration | 30 |

| Corporate Cease Trade Orders or Bankruptcies | 30 |

| Penalties or Sanctions | 32 |

| Personal Bankruptcies | 32 |

| Conflicts of Interest | 32 |

| Other Reporting Issuer Experience | 33 |

| EXECUTIVE COMPENSATION | 36 |

5

| INDEBTEDNESS OF DIRECTORS AND EXECUTIVE OFFICERS | 40 |

| AUDIT COMMMITTEE | 40 |

| CORPORATE GOVERNANCE | 42 |

| RISK FACTORS | 43 |

| INVESTOR RELATIONS ARRANGEMENTS | 45 |

| OPTIONS TO PURCHASE SECURITIES | 45 |

| AUDITORS, TRANSFER AGENT AND REGISTRAR | 47 |

| EXPERTS | 47 |

| OTHER MATERIAL FACTS | 47 |

6

FORWARD LOOKING INFORMATION

This material change report contains certain statements that constitute “forward-looking information” within the meaning of applicable Canadian securities laws. Forward-looking information relates to future events or the anticipated performance of the Company and reflects management’s expectations or beliefs regarding future events. In some cases, forward-looking information can be identified by the use of words such as “expects,” “anticipates,” “believes,” “plans,” “intends,” “estimates,” “may,” “will,” “should,” or similar expressions suggesting future outcomes.

Forward-looking information in this disclosure includes, but is not limited to, statements regarding the anticipated benefits of the Restructuring Transaction, the integration of the Factor’s assets and liabilities into the Company, and the expected operational or financial effects of the transaction.

Forward-looking information is based on a number of assumptions that management believes are reasonable as of the date of this material change report, including assumptions regarding the successful integration of the assets and liabilities previously held by the Factor, the continued operation of the Company’s business in a manner consistent with past practice, and the absence of material undisclosed liabilities relating to the Factor.

Forward-looking information is subject to known and unknown risks, uncertainties and other factors that could cause actual results or events to differ materially from those expressed or implied by such forward-looking information. Such risks and uncertainties include, among others, risks associated with the integration of the acquired business and the potential existence of undisclosed liabilities of the Factor.

Readers are cautioned not to place undue reliance on forward-looking information. The forward-looking information contained in this material change report is made as of the date hereof and the Company does not undertake any obligation to update or revise any forward-looking information, except as required by applicable securities laws.

The Restructuring Transaction was completed on December 22, 2025. Following completion of the transaction, the Factor ceased to operate as a separate entity and its assets and liabilities were integrated into the Company. Management expects that the Restructuring Transaction will simplify the Company’s financing structure by internalizing the factoring arrangements previously carried out by the Factor. These statements constitute forward-looking information and should be read together with the cautionary statements set out above under “Forward-Looking Information.”

DOCUMENTS INCLUDED IN THIS MATERIAL CHANGE REPORT

This material change report has been prepared in accordance with the requirements of National Instrument 41-101 – General Prospectus Requirements and includes all disclosure required to be provided at the prospectus level in connection with the Restructuring Transaction completed on December 22, 2025, including the acquisition of Advance Factoring Inc.

The following documents are included in or form part of this disclosure:

| ● | the audited consolidated financial statements of the Company for the year ended December 31, 2025, together with the related auditor’s report; |

| ● | the management’s discussion and analysis of the Company for the year ended December 31, 2025; |

| ● | the annual audited financial statements of the Factor for the period ended December 22, 2025 and December 31, 2024, together with the related auditor’s report; |

| ● | the pro forma financial statements required in connection with the acquisition of Advance Factoring Inc.; |

| ● | the management’s discussion and analysis of the Factor for the period ended December 22, 2025 and December 31, 2024; and |

7

| ● | all other disclosure required under applicable securities legislation in respect of the Restructuring Transaction. |

Certain documents of the Company filed pursuant to its continuous disclosure obligations, including prior annual and interim financial statements, management’s discussion and analysis, material change reports and management information circulars, are available under the Company’s profile on SEDAR+. References to such documents are provided for informational purposes only. All information required to be disclosed in this material change report is contained herein, and no document is incorporated by reference into this material change report except as expressly required or permitted by applicable securities legislation.

INFORMATION CONCERNING THE FACTOR

The following is a summary of the Factor (the “Corporation”), its business and operations, which should be read in conjunction with the information concerning the Factor appearing elsewhere in this disclosure. The information contained in this material change report is given as at December 22, 2025 on a post-transaction basis, unless otherwise indicated.

Unless otherwise indicated, references to the Factor in this disclosure describe the business and operations of the Factor prior to the completion of the Restructuring Transaction. Following completion of the Restructuring Transaction, the Factor ceased to operate as a separate entity.

CORPORATE STRUCTURE

Name, Address and Incorporation

The Factor was incorporated under the laws of Ontario on September 9, 2022, pursuant to the Business Corporations Act (Ontario) (”OBCA”) and is a private company with its registered and head office located at 1 Adelaide Street East, Suite 801, Toronto, Ontario, M5C 2V9. Binyomin Posen, a director of the Company, was the sole director and officer of the Factor upon incorporation, and resigned from those roles on December 30, 2022. His roles were replaced by Shimshon (Shimmy) Posen.

The Factor is primarily engaged in the business of acquiring and holding receivables in connection with a factoring arrangement with the Company, and holding the related contractual arrangements. Substantially all of the efforts of the Factor are devoted to these business activities and to date the Factor has not earned significant revenues.

Since its incorporation, the Factor has amended its articles from time to time. On September 14, 2022, the Factor amended its articles to change its name from 1000307537 Ontario Inc. to Advance Factoring Inc.

On June 20, 2023, the Factor amended its articles to authorize the issuance of an unlimited number of Preferred Shares and to establish the rights, privileges, restrictions and conditions attaching to such Preferred Shares, including priority with respect to dividends and distributions on liquidation, redemption and retraction features, and conditional voting rights in certain limited circumstances.

On December 9, 2025, the Factor amended its articles to reclassify its common shares into Class A Common Shares and Class B Common Shares, each issuable in an unlimited number, and to reflect the resulting classes of shares in the authorized share capital of the Factor.

On December 17, 2025, the Factor further amended its articles to effect a subdivision of its issued and outstanding Class A Common Shares and Class B Common Shares on a 1,000,000 for 1 basis and to amend and restate the rights, privileges, restrictions and conditions attaching to the Preferred Shares, including provisions relating to voting rights, dividends, redemption, retraction and priority on liquidation.

8

Intercorporate Relationships

Prior to the completion of the Restructuring Transaction, the Factor was a privately held corporation operating independently from the Company. The Factor was owned by its existing shareholders and was not a subsidiary or affiliate of the Company. While the Factor held common shares and conversion units of the Company received as arrangement fees and recourse payments under the Factoring Agreement, there were no equity ownership relationships between the Company and the Factor immediately prior to the Restructuring Transaction.

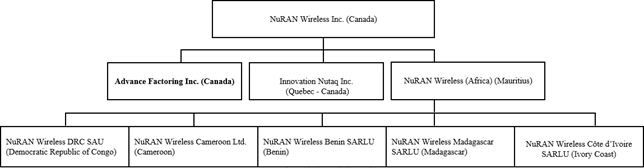

Upon completion of the Restructuring Transaction, the Company acquired all of the issued and outstanding shares of the Factor, as a result of which the Factor became a wholly-owned subsidiary of the Company. Following the completion of the Restructuring Transaction, the Factor continues to exist as a separate legal entity, but its results of operations are consolidated with those of the Company, and the Company exercises control over the Factor through its ownership of all of the Factor’s issued and outstanding shares.

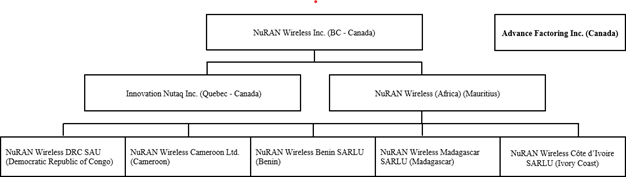

The intercorporate relationships between the Company and the Factor before and after the completion of the Restructuring Transaction are illustrated in the diagrams below.

Before the Restructuring Transaction

After the Restructuring Transaction

9

DESCRIPTION OF THE BUSINESS OF THE FACTOR

General

Summary

The Factor is a privately held Ontario company with its registered office in Toronto, Ontario. The Factor was established as a special purpose vehicle to acquire and hold receivables in connection with a factoring arrangement with the Company.

The Factor’s principal business consisted of acquiring certain receivables of the Company and holding those receivables and related contractual arrangements under the factoring agreement. While the Factor completed a limited number of additional factoring mandates, its activities were primarily focused on the factoring arrangement with the Company.

The Factor was incorporated with minimal capitalization and financed primarily through debt obligations, which were converted into equity immediately prior to the Closing.

Specialized Skills and Knowledge

The nature of the Factor’s business does not require significant operational infrastructure. Its activities consist primarily of acquiring and holding receivables pursuant to the factoring arrangement with the Company and administering the related contractual arrangements.

The Factor relies on the services of its sole director to manage its financial, administrative and contractual obligations. In addition, the Factor may engage third-party service providers and professional advisors, including legal, accounting and administrative consultants, as required in connection with its activities.

As of the date hereof, the Factor has been able to adequately meet its operational and administrative requirements.

Competitive Conditions

Competition in the receivables financing and factoring industry is significant. The Factor competes with a range of financial institutions, specialized factoring companies, private credit providers and other financing sources that offer receivables purchase or similar financing arrangements. Many of these competitors have greater financial resources, broader market presence and more established operating platforms than the Factor.

Competition in this sector is generally based on the availability and cost of capital, the terms offered in receivables purchase arrangements, speed and flexibility in structuring transactions, and the ability to effectively assess and manage credit risk associated with the underlying receivables.

The Factor’s activities have been primarily focused on the factoring arrangement with the Company. To the extent the Factor seeks additional opportunities in the receivables financing market, it may face competition from financial institutions and other market participants with greater operational capacity and access to capital.

Business or Seasonal Cycles

The Factor’s business is not materially impacted by seasonal weather patterns. While general economic conditions and business cycles may influence the volume and credit quality of receivables available for purchase, the Factor’s operations are not subject to significant seasonal fluctuations.

Economic Dependence

The Factor’s activities have been primarily focused on the factoring arrangement with the Company. As a result, the Factor has historically been substantially dependent on the factoring agreement with the Company and the related receivables acquired pursuant to that arrangement.

10

To the Restructuring Transaction date, the Factor had completed only a limited number of factoring mandates with other counterparties. Accordingly, the volume of the Factor’s activities has been closely linked to the receivables financing arrangements entered into with the Company.

The termination, non-renewal or material modification of such arrangements would have had a material impact on the Factor’s business and operations.

Changes to Contracts

Other than the arrangements relating to the factoring agreement with the Company and the transactions contemplated by the debt settlement, the Factor does not have material vendor agreements or third-party contracts that are expected to be affected by the Transaction. As of the date hereof, the Factor is not aware of any potential changes to its material contracts in the current financial year as a result of the Transaction.

Employees

As at the end of the most recent financial year of the Factor, the Factor had no employees and no consultants.

Three Year History

Recent Developments

2023

On August 28, 2023, the Factor entered into a factoring agreement (the “Factoring Agreement”) with NuRAN (the “Seller”), pursuant to which the Factor agreed to acquire certain receivables of the Seller. In connection with the Factoring Agreement, the Seller also entered into a general security agreement and a guarantee, each dated August 28, 2023, in favour of the Factor as secured party. The initial closing occurred on August 28, 2023, at which time Approved Accounts with an aggregate face value of CAD $10,075,289.36 (as subsequently restated) were sold to the Factor. The consideration paid by the Factor consisted of: (i) CAD $4,638,340.95 paid to repay prior indebtedness owed by the Seller to entities associated with the Factor; (ii) CAD $800,000 payable by September 30, 2023; (iii) CAD $215,000 payable by a subsequent date; and (iv) CAD $650,000 payable by December 31, 2023. As an arrangement fee, the Seller issued 2,500,000 common shares to the Factor at the initial closing. Under the original Factoring Agreement, the Seller was required to satisfy any recourse notice in cash at 107% of the Purchase Amount or by issuing Units at a conversion price of $0.35 per share, with warrants exercisable at $0.40 per share.

First Amending Agreement (September 27, 2023): The parties entered into the first factoring amending agreement dated September 27, 2023, which: (i) extended the deadline for the $800,000 cash payment under Section 4.5.2 from September 30, 2023 to October 31, 2023; (ii) extended the financing milestone deadline under Section 13.1.3 from September 30, 2023 to October 31, 2023; and (iii) extended the deadline for Quebec security to be effected from 30 days to 60 days.

Second Amending Agreement (November 29, 2023, effective September 30, 2023): The parties entered into the second factoring amending agreement dated November 29, 2023, which: (i) reduced the conversion price under the recourse mechanism from $0.35 to $0.225 per share; (ii) reduced the warrant exercise price from $0.40 to $0.25 per share; (iii) restated Section 4.5 to reflect updated payment tranches totalling CAD $6,303,340.95 (including the initial $4,638,340.95 debt settlement, and additional tranches of $800,000 by October 31, 2023, $215,000 by November 14, 2023, and $650,000 by December 31, 2023); (iv) restated the arrangement fee under Section 4.6 to include an additional 1,000,000 shares by January 31, 2024 and 900,000 shares by March 15, 2024; (v) extended the Section 13.1.3 financing deadline to January 31, 2024; (vi) extended the deadline for Quebec security to be effected from 60 days to 125 days; (vii) updated Schedule 3 to add anticipated MINTA receivables (18 monthly payments of US$47,554.10 each from December 2023 to May 2025), with the Factor having the option to collect or waive such payments; and (viii) updated Schedule 1 to extend the applicable deadline to January 31, 2024.

11

Third Amending Agreement (December 22, 2023, effective September 30, 2023): The parties entered into the third factoring amending agreement dated December 22, 2023, which: (i) extended the deadline for the $650,000 cash payment under Section 4.5.4 of the Second Amending Agreement from December 31, 2023 to January 31, 2024; and (ii) extended the deadline for Quebec security to be effected from 125 days to 156 days.

2024

Fourth Amending Agreement (April 2, 2024): The parties entered into the fourth factoring amending agreement, which: (i) restated Section 4.5 to update the aggregate face value of Approved Accounts to CAD $11,986,052.44 and the total Purchase Price to CAD $7,303,340.95 (reflecting the completion of additional cash payments, including $1,665,000 by January 31, 2024, $525,000 by March 19, 2024, and $475,000 by April 30, 2024); (ii) confirmed that all arrangement fee shares under Section 4.6 had been issued; (iii) replaced Schedule 3 with Schedule 3 (revised April 2024), which re-added certain invoices that had previously been the subject of Recourse Notices (totalling CAD $1,132,083.08 / USD $838,580.06):; (iv) provided that the Factor waived MINTA payments effective February 1, 2024, resulting in each such monthly amount plus US$15,000 being added to the face value of Approved Accounts; and (v) extended the deadline for Quebec security to be effected from 156 days to 246 days.

The following Recourse Notices were issued and settled by the Seller through the issuance of Units during 2024:

| Recourse # | Date | Amount | Units Issued |

| 1 | January 31, 2024 | $170,634.14 | 758,373 |

| 2 | February 2, 2024 | $106,093.80 | 471,528 |

| 3 | February 7, 2024 | $79,411.79 | 352,941 |

| 4 | February 12, 2024 | $79,103.83 | 351,572 |

| 5 | February 13, 2024 | $149,190.13 | 663,067 |

| 6 | February 22, 2024 | $166,564.96 | 740,288 |

| 7 | March 7, 2024 | $149,190.13 | 663,067 |

| 8 | March 20, 2024 | $231,894.29 | 1,030,641 |

| 9 | April 15, 2024 | $149,190.13 | 663,067 |

| 10 | April 25, 2024 | $339,799.98 | 1,510,222 |

| 11 | June 24, 2024 | $244,780.45 | 1,087,913 |

| 12 | August 5, 2024 | $235,329.76 | 1,045,910 |

| 13 | September 18, 2024 | $145,794.03 | 647,973 |

| 14 | November 7, 2024 | $230,533.85 | 1,024,594 |

Fifth Amending Agreement (June 25, 2024): The parties entered into the fifth factoring amending agreement, which: (i) confirmed all payments under the restated Section 4.5 had been made; (ii) the Factor agreed to execute a Waiver and Subordination Request in connection with the FEI Financing (a facility agreement entered into on April 26, 2024 between NuRAN Wireless Africa Holding and Facility for Energy Inclusion, FEI-ONGRID LP), pursuant to which the Factor subordinated its security interests under the Factoring Agreement, the General Security Agreement, and the Guarantee to the security granted to the FEI lenders, and waived non-compliance with Section 13.1.3 of the Factoring Agreement; (iii) increased the aggregate Approved Accounts to CAD $17,886,251.50 through the addition of approximately USD $2,000,000 of new receivables, with a corresponding new draw facility of up to USD $2,000,000 available to the Seller in tranches not exceeding USD $100,000 with at least 10 business days between requests; (iv) replaced Schedule 3 with Schedule 3 (revised June 2024), which re-added certain invoices previously subject to Recourse Notices totalling CAD$733,770.56 / USD $543,533.75; (v) updated the deemed USD/CAD exchange rate from 1.35 to 1.37; and (vi) extended the deadline for Quebec security to be effected from 246 days to one year.

12

Sixth Amending Agreement (December 23, 2024): The parties entered into the sixth factoring amending agreement, which: (i) agreed that 2024 interest would accrue at 5% per annum (non-compounding) until January 1, 2025, reverting thereafter to 15% per annum; (ii) updated the aggregate Approved Accounts to CAD $25,486,251.50, with Paid Accounts of $18,508,740.23 and Unpaid Accounts of $4,500,000; (iii) updated the total Purchase Price to $10,043,340.95, of which $8,247,202.85 had been paid and $1,796,138.10 remained outstanding (Unpaid Purchase Price); (iv) provided for a new short-term loan facility of up to $300,000 available to the Seller, with each loan bearing a 2% lending fee (increasing by 1% per calendar month to a maximum of 10%), interest at 15% per annum, default interest at 25% compounding, and subject to conversion to Paid Accounts if not repaid within 45 days; (v) reduced the conversion price from $0.225 to $0.20 per share; (vi) extended the term of any outstanding warrants held by the Factor from three years to five years, including extending any warrant expiring on August 28, 2026 to August 28, 2028; (vii) increased the cash recourse threshold from 107% to 135% of the Purchase Amount; (viii) extended the deadline for Quebec security to be effected from one year to 18 months; (ix) increased the aggregate Approved Accounts cap from $15,000,000 to $25,500,000; and (x) replaced Schedule 3 with Schedule 3 (revised December 2024), re-adding certain invoices previously subject to Recourse Notices, totalling CAD $611,657.64 / USD $446,465.43.

2025

Seventh Amending Agreement (April 15, 2025): The parties entered into the seventh factoring amending agreement, which: (i) settled three short-term promissory notes issued pursuant to Section 7 of the Sixth Amending Agreement, the December 23, 2024 Note ($150,000), the January 22, 2025 Note ($63,405.12), and the February 4, 2025 Note ($146,030.00), as credits against additional Paid Accounts, with accrued interest of $1,962.74 on the December Note paid in cash; (ii) updated the aggregate Approved Accounts to CAD $26,808,020.43 (Paid Accounts: $21,775,356.63; Total Purchase Price: $10,402,776.07; Purchase Price Paid: $9,622,392.97; Unpaid Accounts: $780,383.10); (iii) provided for an additional short-term loan facility of up to $200,000; and (iv) extended the deadline for Quebec security to be effected from 18 months to 24 months; and (v) increased the aggregate Approved Accounts cap to $27,000,000.

Eighth Amending Agreement (August 19, 2025): The parties entered into the eighth factoring amending agreement, which settled 14 additional short-term promissory notes (the April 15 Note through August 19 Note, totalling approximately $1.35 million in principal) as credits against Paid Accounts, with the Seller having the option to repay each such note in cash by August 25, 2025 in lieu of the credit being applied to Paid Accounts.

The following additional Recourse Notices were issued and settled by the Seller through the issuance of Units during 2025:

| Recourse # | Date | Amount | Units Issued |

| 15 | January 2, 2025 | $300,000.00 | 1,500,000 |

| 16 | February 12, 2025 | $300,000.00 | 1,500,000 |

| 17 | April 2, 2025 | $300,000.00 | 1,500,000 |

| 18 | May 2, 2025 | $300,000.00 | 1,500,000 |

| 19 | May 20, 2025 | $600,000.00 | 3,000,000 |

| 20 | June 26, 2025 | $500,000.00 | 2,500,000 |

| 21 | July 14, 2025 | $500,000.00 | 2,500,000 |

| 22 | July 22, 2025 | $500,000.00 | 2,500,000 |

On December 9, 2025, the Factor amended its articles to reclassify its common shares into Class A Common Shares and Class B Common Shares, each issuable in an unlimited number. On December 16, 2025, the Factor completed a 1,000,000-for-1 share split, resulting in 100,000,000 common shares issued and outstanding. On December 19, 2025, the Factor issued 726,752,667 preferred shares at a fair value of $0.01 per share for the settlement of debt with certain shareholders and related parties.

13

On December 22, 2025, the Restructuring Transaction closed. NuRAN acquired all of the issued and outstanding shares of the Factor pursuant to a share purchase agreement, in exchange for 7,198,026 Units of NuRAN at a deemed price of $2.89 per Unit, representing aggregate consideration of approximately $20,802,303.09. Following completion of the Restructuring Transaction, the Factor ceased to operate as an independent entity and its assets and liabilities were integrated into the Company.

Information Concerning the Factor Following Completion of the Transaction

As a result of the Restructuring Transaction, the Company acquired all of the issued and outstanding common shares and Preferred Shares of the Factor. Any related indebtedness under the Preferred Shares constitutes intercompany balances and are eliminated in the consolidated financial statements. The Company expects to dissolve the Factor at a later date.

On a pro forma basis, before transaction costs related to the Transaction, as at December 31, 2025, the Factor had approximately $6, less transaction costs, in cash. See “Information Concerning Resulting Issuer - Consolidated Capitalization” in this material change report, as well as the pro forma consolidated financial information and the accompanying notes thereto attached as Schedule “B”.

PARTICULARS OF THE MATTER – MI 61-101

In the Management Information Circular (the “Circular”) dated September 9, 2025, the Company determined that the proposed Restructuring Transaction may constitute a “related party transaction” and/or a “business combination” within the meaning of Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions (“MI 61-101”), depending on the final participation of certain debt holders and subscribers and the resulting ownership of the Company following completion of the Restructuring Transaction.

The Restructuring Transaction described in the Circular involved:

(a) the settlement of up to $25,000,000 of outstanding indebtedness (including accrued interest) through the issuance of equity securities; and

(b) the concurrent issuance of additional equity securities for gross proceeds of up to $5,000,000,

which, in the aggregate, could have resulted in the issuance of securities representing more than 100% of the then issued and outstanding Common Shares of the Company on a non-diluted basis.

Under the Transaction, the Company acquired all of the issued and outstanding shares of the Factor from its Shareholders (the “Vendors”).

As previously disclosed, the Company sought to implement a restructuring transaction involving the settlement of indebtedness and the raising of additional equity capital.

The transaction constitutes an acquisition that may be characterized as a business combination for accounting or NI 51-102 purposes; however, it does not meet the definition of a “business combination” under Multilateral Instrument 61-101, as it does not involve the termination of the interests of equity security holders without their consent or otherwise fall within the scope of that definition.

Following further negotiations with creditors and prospective investors, on December 22, 2025, the Company implemented a transaction structured as an acquisition of the Factor (the “Acquisition”), which achieved substantially the same economic objectives as the originally proposed Restructuring Transaction, including the reduction of indebtedness and improvement of the Company’s financial position.

14

While the Acquisition resulted in significant dilution to existing shareholders, it did not involve the termination of the interests of holders of equity securities of the Company without their consent, nor did it otherwise constitute a transaction of the nature contemplated by the definition of “business combination” under MI 61-101.

The Acquisition involved the acquisition of 100% of the shares of the Factor; the settlement of $26,222,524.26 of indebtedness; and the issuance of equity securities with an aggregate value of approximately $30,000,000.

The issuance of securities exceeded 100% of the Company’s issued and outstanding Common Shares on a non-diluted basis. This issuance of securities was approved by the shareholders in the Annual General and Special Meeting that took place on October 29, 2025.

The acquisition of the Factor pursuant to the Share Purchase agreement dated December 22, 2025 (the “Transaction”) does not constitute a related party transaction within the meaning of Multilateral Instrument 61-101 – Protection of Minority Security Holders in Special Transactions (MI 61-101).

Although Binyomin Posen and Francis Letorneau are “related parties” of the Company for purposes of MI 61-101. Binyomin Posen and Francis Letorneau, and their affiliates and representatives, representing approximately 19.68% of the Company’s issued and outstanding voting securities, did not vote on this resolution.

Upon completion of the Restructuring Transaction, the Company had 12,905,118 common shares issued and outstanding, of which 7,198,026 common shares were issued to the shareholders of Factor as consideration. As at December 31, 2025, a total of 13,052,785 common shares were issued and outstanding. The chart below summarizes the shareholdings:

Factor Shareholder |

Holdings on a Post- Consolidation Basis Prior to the Restructuring Transaction |

Units |

Total |

Percentage of Common Shares Held as of December 23, 2025 |

Percentage of Common Shares Held as of December 31, 2025 |

| 1. Shimshon Posen | 4,519 | 1,159,966 | 1,164,485 | 9.02% | 8.92% |

| 2. AK Holdings Group Inc. | — | 1,288,927 | 1,288,927 | 9.99% | 9.87% |

3. Joseph and Marla Posen Family Trust |

— | 1,288,927 |

1,288,927 |

9.99% |

9.87% |

| 4. Xorax Family Trust | 33,333 | 1,124,567 | 1,157,900 | 8.97% | 8.87% |

| 5. Donal Carroll | 33,333 | 1,124,567 | 1,157,900 | 8.97% | 8.87% |

6. Pacific Investment Holdings Limited |

33,333 | 1,124,567 |

1,157,900 |

8.97% |

8.87% |

| 7. Roxanne Letourneau | 75 | 86,505 | 86,580 | 0.67% | 0.66% |

| Total | 104,593 | 7,198,026 | 7,302,619 | 56.59% | 55.95% |

15

Certain vendors of the Factor are related to insiders of the Company. Shimshon Posen, a vendor of the Factor, received 1,159,966 Units upon closing of the Restructuring Transaction; Binyomin Posen, a director of the Company, is the brother of Shimshon Posen. The Joseph and Marla Posen Family Trust, also a vendor of the Factor, received 1,288,927 Units upon closing; Binyomin Posen has a familial relationship with Chana Posen, who serves as trustee of such trust. In addition, Roxanne Letourneau, a vendor of the Factor, received 86,505 Units upon closing; Ms. Letourneau is the daughter of Francis Létourneau, a director and the Chief Executive Officer of the Company, and does not reside at the same address as Mr. Létourneau.

DIVIDENDS OR DISTRIBUTIONS

The Factor has not declared or paid any cash dividends on any of its issued shares since incorporation. The Factor does not have a dividend policy and, given the current stage of the Factor’s corporate development, the Factor does not intend to adopt such a policy in the foreseeable future. Any decision to declare and pay dividends will be made by the Factor’s board of directors on the basis of earnings, financial requirements and other conditions existing at such future time.

SELECTED CONSOLIDATED FINANCIAL INFORMATION

The following table sets out selected financial information for the Factor for the periods indicated and should be considered in conjunction with the more complete information contained in the financial statements of the Factor attached as Schedule “C” to this material change report. Unless otherwise indicated, all currency amounts are stated in Canadian dollars.

Period ended December 22, 2025 ($) |

Fiscal year ended December 31, 2024 ($) | |

| Total revenues | 1,970 | 178,997 |

| Total operating expenses | (174,271) | (153,676) |

| Net income (loss) | (172,301) | (8,361) |

| Basic net loss per share | (0.00) | (0.00) |

| Total Assets | 7,619,168 | 7,239,654 |

| Total Liabilities | 7,267,527 | 6,715,712 |

MANAGEMENT DISCUSSION & ANALYSIS

The Factor’s Management Discussion and Analysis for the period ended December 22, 2025 and December 31, 2024, are incorporated herein as Schedule “D”.

DESCRIPTION OF SECURITIES

Authorized and Outstanding Capital

The authorized share capital of Advance Factoring Inc. consists of an unlimited number of Class A Common Shares, Class B Common Shares and Preferred Shares. The Class A Common Shares and Class B Common Shares rank junior to the Preferred Shares with respect to dividends and the distribution of assets upon liquidation, dissolution or winding-up of the Factor and otherwise carry the rights of common shares under the OBCA and the articles of the Factor.

16

Each Common Share entitles the holder to receive notice of, attend and vote at all meetings of shareholders of the Factor, except meetings at which only holders of another class or series of shares are entitled to vote, with one vote per Common Share. Holders of Common Shares are entitled to receive dividends if and when declared by the board of directors. In the event of any liquidation, dissolution or winding-up of the Factor, holders of Common Shares are entitled to receive the remaining assets of the Factor available for distribution after satisfaction of the rights of any shares ranking in priority to the Common Shares.

The Preferred Shares rank in priority to the Class A Common Shares and Class B Common Shares with respect to dividends and distributions on liquidation. The Preferred Shares are generally non-voting and holders are not entitled to receive notice of or attend meetings of shareholders, except in certain limited circumstances expressly provided for in the articles, including meetings relating to the dissolution of the Corporation or the sale of all or substantially all of its assets. In addition, if the Factor fails to redeem or retract Preferred Shares as required under the articles, the holders thereof become entitled to one vote per Preferred Share at meetings held after the applicable redemption date. The Preferred Shares are redeemable and retractable at a redemption amount of $0.01 per share, carry non-cumulative dividends declared at the discretion of the board of directors within the limits set out in the articles, and entitle holders, on liquidation, to receive the redemption amount together with any declared and unpaid dividends, in priority to the common shares.

As the Preferred Shares include a holder-controlled redemption option, they are recorded as a financial liability in the Factor’s audited financial statements. Through the Restructuring Transaction, the Company has assumed this liability. As of the Closing Date, the aggregate redemption amount of the Preferred Shares is $7,267,527 (726,752,667 shares x $0.01 per share). Notwithstanding the foregoing, pursuant to the Restructuring Transaction, the indebtedness under the Preferred shares constitutes intercompany balances and are eliminated in the consolidated financial statements.

As of the date of the Restructuring Transaction, 100,000,000 Class A Shares and 726,752,667 Preferred Shares were issued and outstanding. No Class B Shares were issued or outstanding as of such date.

The equity securities distributed under the material change report are issued by NuRAN Wireless Inc. in connection with the Restructuring Transaction. The Factor is not distributing any securities, and no securities of the Factor are being offered or issued.

OPTIONS TO PURCHASE SECURITIES

As at November 21, 2025, being a date within 30 days prior to the date of the effective date of this material change report, there were no options to purchase securities of the Factor. outstanding or issuable, including options held by or issued to executive officers or former executive officers of the Factor, as a group, or directors or former directors of the Factor, as a group; executive officers or former executive officers of any subsidiary of the Factor, as a group, or directors or former directors of such subsidiaries, as a group; employees or former employees of the Factor or any of its subsidiaries; consultants of the Factor or any of its subsidiaries; or any other person or company.

CONSOLIDATED CAPITALIZATION

Other than as disclosed herein, there have been no material changes in the share capitalization or indebtedness of the Factor since December 22, 2025, the date of the Factor’s most recent financial statements. The following table sets forth the consolidated capitalization of the Factor as at December 22, 2025, and on a pro forma basis giving effect to the Restructuring Transaction as if it had occurred on January 1, 2025. This table should be read in conjunction with the Factor’s comparative financial statements for the period ended December 22, 2025, and the related notes thereto, as well as management’s discussion and analysis.

17

| Designation of Security | Amount Authorized or to be authorized | Amount outstanding as of the date of the most recent balance sheet(1) | Amount outstanding as of the date prior to giving effect to the Restructuring Transaction |

| Common Shares | Unlimited | 100,000,000 | 100,000,000 |

| Preferred Shares | Unlimited | 726,752,667 | 726,752,667 |

| Warrants | Unlimited | Nil | Nil |

| Options | Unlimited | Nil | Nil |

| RSUs | Unlimited | Nil | Nil |

PRIOR SALES

The Factor has issued the following securities within the 12 months preceding December 22, 2025:

| Date | Type | Deemed Price |

Number of Securities |

| December 19, 2025(1) | Preferred Shares | $0.01 | 726,752,667 |

Note:

| (1) | The Factor issued 726,752,667 preferred shares at a fair value of $0.01 per share for the settlement of debt with certain shareholders and related parties. |

Market for Securities

No securities of the Factor are listed or traded on any exchange or quotation system. Upon completion of the Transaction and subject to receipt of all required regulatory approvals, the Factor Shares will be exchanged for shares of the Resulting Issuer. The shares of the Resulting Issuer are expected to be listed on the Canadian Securities Exchange.

ESCROWED SECURITIES AND SECURITIES SUBJECT TO CONTRACTUAL RESTRICTION ON TRANSFER

As of the date hereof, no securities of the Factor are held in escrow or are subject to any contractual restrictions on transfer.

PRINCIPAL SECURITYHOLDERS

To the best of the knowledge of the directors and executive officers of the Factor, as of the material change report, the following persons beneficially owned, or exercise control or direction over, directly or indirectly, over more than 10% of the issued and outstanding common shares of the Factor as at the date of the Restructuring Transaction:

| Name of Shareholder | Number of Voting Securities | Percentage of Voting Shares Held |

| Shimshon Posen | 24,768,073 | 24.77% |

| AK Holdings Group Inc. | 20,978,317 | 20.98% |

| Xorax Family Trust | 17,468,839 | 17.47% |

| Donal Carroll | 17,468,839 | 17.47% |

| Pacific Investment Holdings Limited | 17,468,839 | 17.47% |

| Roxanne Letourneau | 1,847,093 | 1.85% |

18

DIRECTORS AND EXECUTIVE OFFICERS

As at the date of the Restructuring Transaction, the board of directors of the Factor is comprised of one (1) director, who is elected at each annual meeting of shareholders to hold office for one year or until his successor is elected or appointed, unless he resigns or his office becomes vacant.

The following table sets forth the name and residence of each director and executive officer of the Factor, as well as such individuals position with the Factor, period of service as a director and/or officer (as applicable), and principal occupation(s) within the five preceding years:

Name, Municipality of Residence and Position Held |

Principal Occupation for the Past Five Years(1) |

Director or Officer of the Factor Since |

Shares Beneficially Owned, Directly or Indirectly, or Over Which Control or Direction is Exercised |

Shimshon (Shimmy) Posen Toronto, ON |

Partner at Garfinkle Biderman LLP |

December 30, 2022 |

24,768,073 common shares (24.77%) |

| CEO, CFO, Secretary and Director |

Immediately before the Restructuring Transaction, the sole director of the Factor owns 24,768,073 common shares of the Factor, representing approximately 24.77% of the outstanding common shares of the Factor.

Cease Trade Orders, Bankruptcies, Penalties or Sanctions

Other than as stated below, no director or officer of the Factor is, as at the date of this material change report, or has been within the last ten years, a director, chief executive officer or chief financial officer of any company that: (a) was subject to a cease trade order, an order similar to a cease trade order, or an order that denied the relevant company access to any exemption under applicable securities legislation, and which in all cases was in effect for a period of more than 30 consecutive days (an “Order”), which Order was issued while the director or executive officer was acting in the capacity as director, chief executive officer or chief financial officer of such company; or (b) was subject to an Order that was issued after the director ceased to be a director, chief executive officer or chief financial officer and which resulted from an event that occurred while that person was acting in the capacity as director, chief executive officer or chief financial officer of such company.

Other than as stated below, no director or officer of the Factor is, as at the date of this material change report, or has been within the last ten years, a director or executive officer of any company that, while that person was acting in that capacity, or within a year of that person ceasing to act in that capacity, became bankrupt, made a proposal under any legislation relating to bankruptcy or insolvency or was subject to or instituted any proceedings, arrangement or compromise with creditors or had a receiver, receiver manager or trustee appointed to hold its assets; (b) has, within the last ten years, become bankrupt, made a proposal under any legislation relating to bankruptcy or insolvency or become subject to or instituted any proceedings, arrangement or compromise with creditors or had a receiver, receiver manager or trustee appointed to hold his, her or its assets; (c) has been subject to any penalties or sanctions imposed by a court relating to securities legislation or by a securities regulatory authority or has entered into a settlement agreement with a securities regulatory authority; or (d) has been subject to any other penalties or sanctions imposed by a court or regulatory body that would likely be considered important to reasonable investor in making an investment decision regarding the Factor.

19

EXECUTIVE COMPENSATION

The following table sets forth the information required under Form 51-102F6V-Statement of Executive Compensation-Venture Issuers of Regulation 51-102 respecting Continuous Disclosure Obligations (the “Form 51-102F6V”), regarding all compensation paid, payable, granted or otherwise provided during the last three financial years of years Factor, to all persons acting as directors or as “Named Executive Officers” (the “NEOs”), as this expression is defined in Form 51-102F6V, for the period ended December 22, 2025 and December 31, 2024. The Chief Executive Officer (the “CEO”) and the Chief Financial Officer (the “CFO”) is the only NEO of Factor for the period ended December 22, 2025 and December 31, 2024 is Shimmy Posen.

Director and named executive officer compensation, excluding compensation securities

| Table of compensation excluding compensation securities | |||||||

Name and position |

Year |

Salary, consulting fee, retainer or commission ($) |

Bonus ($) |

Committee or meeting fees ($) |

Value of perquisites(1) ($) |

Value of all other compensation ($) |

Total compensation ($) |

Shimshon (Shimmy) Posen President, CEO, CFO and Director |

2025 | Nil | Nil | Nil | Nil | Nil | Nil |

2024 |

Nil |

Nil | Nil | Nil | Nil | Nil | |

Employment, Consulting and Management Agreement

Management functions of the Company are not, to any substantial degree, performed other than by directors or NEOs of the Factor. There are no agreements or arrangements that provide for compensation to NEOs or directors of the Factor, or that provide for payments to a NEO or director at, following or in connection with any termination (whether voluntary, involuntary or constructive), resignation, retirement, severance, a change of control in the Factor or a change in the NEO or director’s responsibilities.

Equity Compensation Securities

The Factor did not have in place an incentive compensation plan.

Oversight and Description of Director and NEOs Compensation

The Factor’s board of directors (the “Board”) has no compensation committee. Considering its small size, the Board assumes the responsibility to establish the objectives of the Factor’s executive compensation program which are to attract, motivate, engage and retain qualified, high performance individuals and to meet performance objectives designed to increase shareholder returns. The Board: (i) establishes the objectives that will govern Factor’s compensation program for the NEOs and the directors; (ii) oversees and approves the compensation and benefits; and (iii) promotes the clear and complete disclosure to shareholders of material information regarding executive compensation.

20

Compensation Process and Objectives

The Board relies on the knowledge and experience of its members to set appropriate levels of compensation for the NEOs. The Board reviews the NEOs compensation on an annual basis and, in doing such task, it evaluates the NEOs achievements during the preceding year. The Factor has not retained any third party advisors to conduct compensation reviews of its competitors’ pay levels and practices.

The Factor’s principal business consisted of acquiring certain receivables of the Company and holding those receivables and related contractual arrangements pursuant to the factoring agreement with the Company. While the Factor completed a limited number of additional factoring mandates, its activities were primarily focused on the factoring arrangement with the Company.

As a result, the Board did not consider traditional performance metrics, such as corporate profitability, to be appropriate in evaluating the performance of Factor’s Named Executive Officers (“NEOs”). The compensation of the officers was determined having regard to the limited scope of the Factor’s operations, industry compensation practices and the execution of the Factor’s business objectives, including the management of the receivables and related financing arrangements.

The Factor was incorporated with minimal capitalization and was financed primarily through debt obligations. Immediately prior to the Closing, certain debt obligations were settled through the issuance of 726,752,667 Preferred Shares of the Factor in favour of the holders of such debt. The Preferred Shares are recorded as a financial liability in the Factor’s financial statements. The Company acquired all of the issued and outstanding common shares and Preferred Shares of the Factor. Any related indebtedness under the Preferred Shares constitutes intercompany balances and are eliminated in the consolidated financial statements.

The Factor does not offer benefit programs, such as life insurance and health and dental benefits.

Pension and Retirement Plans

The Factor does not have any pension plan that provides for payments or benefits at, following, or in connection with retirement of any director or officer.

INDEBTEDNESS OF DIRECTORS AND EXECUTIVE OFFICERS

No director, officer, employee or previous directors, officers or employees of the Factor was indebted to the Factor at any time in its last completed financial year in connection with the purchase of securities of the Factor of for any other reason.

LEGAL PROCEEDINGS OR REGULATORY ACTIONS

As of the date of this material change report, the Factor is not or was not a party to any legal proceedings or regulatory actions and is not aware of any such proceedings or actions known to be contemplated.

INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS

Other than as disclosed, there were no material interests, direct or indirect, of Factor’s directors or executive officers, or any director or executive officer of a subsidiary of Factor, or any person who beneficially owns, or controls or directs, directly or indirectly, more than 10% of the outstanding common shares of Factor, or any associate or affiliate of such persons, in any transaction since the commencement of the Factor’s last completed financial year or in any proposed transaction that has materially affected, or would materially affect, the Factor.

21

NON-ARM’S LENGTH PARTY TRANSACTIONS

At December 22, 2025, amounts included in accounts payable and accrued liabilities due to related parties was $nil upon completion of the Restructuring Transaction (2024 -- $6,667,122). In addition, on December 19, 2025, 726,752,667 Preferred Shares were issued to related parties of the Company, including Shimshon Posen (CEO and director) and other shareholders, in settlement of existing debt obligations. The Preferred Shares are recorded as a financial liability in the amount of $7,267,527. The key terms of the Preferred Shares are described under “Description of Securities — Preferred Shares of the Factor” above.. Any related indebtedness under the Preferred Shares of the Factor constitutes intercompany balances and are eliminated in the consolidated financial statements.

AUDITOR, TRANSFER AGENT AND REGISTRAR

The auditor of the Factor is ND LLP located at 120 East Beaver Creek Rd, suite 200, Richmond Hill, ON L4B 4V1.

MATERIAL CONTRACTS

The material contracts entered into in connection with the Restructuring Transaction include the acquisition agreement relating to the Company’s acquisition of the Factor is filed on SEDAR+. The acquisition agreement includes customary representations, warranties, and indemnification provisions protecting NURAN against undisclosed liabilities and breaches by the Factor.

Other than the acquisition agreement and the contracts entered into in the ordinary course of business, the following material contracts were entered into by the Factor and effective up to December 22, 2025, and are still in effect as of the date of this material change report:

| (i) | the Factoring Agreement dated August 28, 2023 between NuRAN Wireless Inc. and Advance Factoring Inc., as amended by eight amending agreements; |

| (ii) | the General Security Agreement dated August 28, 2023; and |

| (iii) | the Guarantee dated August 28, 2023. |

The foregoing agreements are discussed in the section titled Description of The Business Of the Factor - Three Year History - Recent Developments (Current Financial Year)

EXPERTS

ND LLP, the auditors of the Factor, have advised that they are independent with respect to the Factor within the meaning of the Code of Professional Conduct of the Chartered Professional Accountants of Ontario.

None of the foregoing experts, nor any partner, employee or consultant of such an expert who participated in and who was in a position to directly influence the preparation of the applicable statement, report or valuation, has, has received or is expected to receive, registered or beneficial interests, direct or indirect, in common shares of the Factor or other property of the Factor or any of its associates or affiliates, representing 1% or more of the outstanding common shares of the Factor.

22

OTHER MATERIAL FACTS

There are no other material facts other than as disclosed herein that are necessary to be disclosed in order for this “Information Concerning the Factor” to contain full, true and plain disclosure of all material facts relating to the Factor.

FINANCIAL STATEMENT DISCLOSURE

The financial statements of the Factor included in this material change report as Schedule “E” are the audited annual financial statements for the period ended December 22, 2025 and December 31, 2024.

INFORMATION RELATING TO THE RESULTING ISSUER

The following information is presented on a post-Restructuring Transaction basis and is reflective of the projected business, financial and share capital position of the Resulting Issuer. This section only includes information respecting the Resulting Issuer that is materially different from information provided earlier in this material change report. Following the completion of the Transactions, the Resulting Issuer will carry on the businesses currently carried on by Nuran. See the various headings under “Information Concerning the Factor” for additional information regarding the Factor, respectively. See also the Pro Forma Financial Statements of the Resulting Issuer attached hereto as Schedule “D”

The following section of this material change report contains forward-looking information. Readers are cautioned that actual results may vary. See “Forward-Looking Information”.

Corporate Structure

Name and Incorporation

The corporate name of the Resulting Issuer is “NuRAN Wireless Inc.” The Resulting Issuer will be governed by the Business Corporations Act (British Columbia). Following completion of the Restructuring Transaction, the Resulting Issuer’s head office will be located at Suite 100, 2150 Cyrille-Duquet St., Quebec, Québec, G1N 2G3, Canada. The Resulting Issuer’s registered and records office is 1000 - 595 Burrard Street, Vancouver, BC V7X 1S8.

Intercorporate Relationships

Prior to the completion of the Transaction, the corporate structures of the Company and Factor are as follows:

23

Upon the completion of the Transaction, the corporate structure of the Resulting Issuer will be as follows:

Upon completion of the Restructuring Transaction, the indebtedness owed to the Factor was fully satisfied through the issuance of common shares, and the Factor ceased to be a creditor of the Issuer.

NARRATIVE DESCRIPTION OF THE BUSINESS

The Company continues to carry on the same business following completion of the Restructuring Transaction.

NuRAN is a leading supplier of mobile and broadband wireless infrastructure solutions. Its innovative radio access network (RAN), core network, and backhaul products dramatically reduce the total cost of ownership, giving mobile network operators (MNOs) the ability to profitably serve remote, low income and low population density locations, an unfeasible proposition with existing systems.

The Company’s current business focus is to grow the market penetration of its Network as a Service (NaaS) offering, a communications solution whose backbone is its Wireless Infrastructure Systems (WIS).

NuRAN’s WIS are mobile wireless infrastructure equipment (e.g. base station radios) that use proprietary breakthrough small cell solutions to offer better coverage, the lowest installed cost, the most efficient power consumption combined with leading technology for satellite bandwidth reduction usage currently available in the global marketplace. This technology was subject to rigorous testing by leading MNOs proving its carrier-grade status and leading to broad acceptance for NaaS solutions in the years since.

Our design provides two key competitive advantages:

• Low total cost of ownership, a key feature for developing countries and rural/low population density areas, and

• Small footprint, easy to deploy private networks, customizable for large scale deployments such as rural mobile networks and specific markets such as defense, utilities, industrial and machine-to-machine (“M2M”).

NuRAN’s NaaS model leverages the capabilities of its WIS as well as its extensive expertise in building cost-effective cellular infrastructure. The model provides not only network equipment, but NuRAN also finances, builds, manages and maintains the cellular sites in a very effective manner. Revenue to NuRAN comes in the form of either a revenue share with guaranteed minimum or threshold or fixed monthly payments depending usually on the type of site being deployed. As demonstrated by the number of contracts signed, the NaaS model has received significant interest from MNOs as a carrier-grade mobile network infrastructure solution that allows MNOs to continue focusing their capital expenditure on building capacity in denser urban and semi-urban areas while developing new technologies such as 4G and 5G. Another reason for this growing interest in the NaaS model is that it allows MNOs to reach previously uneconomic markets, thus meeting government license obligations to cover the vast majority of the population which is only possible by serving remote communities. The investment in the NaaS model is customer friendly but it also provides NuRAN with long-term recurring revenues over contract periods which range from 5 to 10 years in length, and in many cases are of indefinite length because they incorporate continued asset ownership by NuRAN.

24

NuRAN’s wireless infrastructure solutions are also capable of supporting mobile payment transactions, a tremendous social and economic benefit for those in the developing world where 95% of all transactions are cash and 60% of adults don’t currently have a bank account, as well a significant potential market for MNOs. This is one of the key applications that MNOs are interested in rolling out when they deploy NaaS in rural areas where bank accounts are less prevalent.

By deploying communication infrastructure in uncovered areas, NuRAN also makes a very significant contribution to the socio-economic conditions of the areas it serves and meets a significant number of the seventeen sustainable development goals set by the United Nations. This includes improving the local economies and enabling access to e-learning, e-health and other social services not currently available to the local population.

The Resulting Issuer’s assets can be found in its 2025 audited financial statements and consist primarily of cash and cash equivalents, trade and other receivables, telecommunications infrastructure and related equipment, intangible assets, right-of-use assets and investments in subsidiaries. Assets recognized in connection with the Restructuring Transaction were recorded in accordance with IFRS and primarily reflect the settlement of 7.6 million of receivables previously owed by the Issuer.

Stated Business Objectives

Upon completion of the Transaction, the Resulting Issuer’s business objectives will be to continue to develop, operate and expand its existing telecommunications business and to grow and realize value from its current operations. NuRAN Wireless is a specialist telecommunications company focused on providing affordable and innovative wireless network solutions, including 2G, 3G and 4G technologies, primarily in rural and remote regions that are underserved by traditional network infrastructure.

The Resulting Issuer’s objectives include expanding the deployment of its compact and cost-effective wireless solutions in developing and remote markets, supporting the delivery of reliable connectivity to populations with limited access to telecommunications services, and enhancing the scalability and efficiency of its network-as-a-service model. In pursuing these objectives, the Resulting Issuer seeks to improve long-term shareholder value while advancing its mission of bridging the digital divide by enabling affordable and reliable connectivity in underserved regions.

DESCRIPTION OF SECURITIES

The authorized share capital of the Resulting Issuer following completion of the Restructuring Transaction shall consist of an unlimited number of common shares. The authorized share capital of the Resulting Issuer and the rights and restrictions of the Resulting Issuer Shares will remain unchanged.

As of the date of this material change report, there are 12,905,118 common shares of the Resulting Issuer issued and outstanding.

PRO FORMA CONSOLIDATED CAPITALIZATION

The following table sets forth the consolidated capitalization of the Resulting Issuer as at the date of this material change report after giving effect to the Restructuring Transaction. For detailed information on the capitalization of the Company and Factor as at December 31, 2025, see the Company’s audited annual financial statements of the Company as at December 31, 2025 and the annual financial statements of the Factor for the period ended December 22, 2025 and December 31, 2024. See also the pro forma condensed consolidated financial statements of the Resulting Issuer which gives effect to the Transaction as set forth in Schedule “D” to this material change report.

25

Designation of Security |

Amount authorized or to be authorized |

Amount outstanding as of the date prior to giving effect to the Restructuring Transaction |

Amount outstanding after giving effect to the Restructuring Transaction (Resulting Issuer) | Amount outstanding after giving effect to December 31, 2025 (Resulting Issuer) |

| NURAN Shares | Unlimited | 5,707,092 | 12,905,118 | 13,069,567 |

| Total Shares Outstanding | 5,707,092 | 12,905,118 | 13,069,567 | |

| NURAN Warrants | Unlimited | 28,867 | 6,294,004 | 6,359,067 |

| NURAN Options | 10% of issued and outstanding | 9,566 | 9,566 | 9,566 |

| NURAN RSUs | 10% of issued and outstanding | Nil | Nil | Nil |

Total Capitalization fully diluted |

5,745,525 |

19,208,688 |

19,438,200 |

AVAILABLE FUNDS AND PRINCIPAL PURPOSE

The available funds of the Resulting Issuer are estimated to be approximately ($33,002,029) represented as current assets less current liabilities as at the date of this material change report on a pro-forma basis. Per the Restructuring Transaction, the Resulting Issuer purchased all of the issued and outstanding common and preferred shares of the Factor for consideration of $20,802,303, by way of issuance of 7,198,026 Units, broken down into 7,198,026 common shares and 3,599,013 warrants.

The Resulting Issuer reserves the right to allocate and reallocate available funds among its projects and uses as management may determine to be appropriate from time to time, where such reallocation is considered necessary for sound business reasons. The Resulting Issuer may require additional capital to fund its operations and growth initiatives, which may be obtained from a combination of existing cash flow, anticipated cash flow, equity financing and/or debt financing. There can be no assurance that additional capital will be available to the Resulting Issuer when required or that such financing will be available on terms acceptable to the Resulting Issuer. See “Risk Factors”.

DIVIDENDS

The payment of dividends following completion of the Restructuring Transaction will be at the discretion of the Resulting Issuer Board. The Company has not declared or paid dividends on the Company Shares to date and the Resulting Issuer is not currently expected to pay dividends following the completion of the Restructuring Transaction, as it is currently anticipated that it will retain future earnings for use in the development of the Resulting Issuer’s business and for general corporate purposes. Accordingly, dividends will only be paid when operational circumstances permit.

26

PRINCIPAL SECURITYHOLDERS

To the knowledge of the directors and executive officers of the Factor and NURAN, no person beneficially owns, controls or directs, directly or indirectly, shares carrying 10% or more of the voting rights attached to all shares of the Resulting Issuer.

DIRECTORS, OFFICERS AND PROMOTERS

Name, Address, Occupation and Security Holdings

Following completion of the Transaction, the board of directors of the Resulting Issuer are Francis Letourneau, Binyomin Posen, Brendan Purdy, Vitor Fonseca, Navindran Naidoo, Avi Minkowitz, and Joseph Labkowski. Binyomin Posen, Brendan Purdy, Vitor Fonseca, Navindran Naidoo, Avi Minkowitz, and Joseph Labkowski are independent. Francis Letourneau is not independent as he is the president and CEO of the Resulting Issuer. The directors of the Resulting Issuer will hold office until the next annual general meeting of the Resulting Issuer or until their respective successors have been duly elected or appointed, unless his or her office is earlier vacated in accordance with the articles and by-laws of the Resulting Issuer or within the provisions of the BCBCA.

The following table sets forth certain information regarding the individuals who serve as directors and officers of the Resulting Issuer, including their place of residence, status as independent or non-independent director (if applicable), the period of time for which each director or officer has served as a director or officer of the Company or the Factor, as applicable, each director’s principal occupation, business or employment for the past five years, and the number of securities of the Resulting Issuer that will be beneficially owned by each director or officer, directly or indirectly, or over which each director or officer will exercise control or direction.

Name, Province or State and Country of Residence and Position(s) with the Company |

Principal Occupation, Business or Employment for Last Five Years |

Periods during which Nominee has Served as a Director or Officer |

Number of Common Shares Owned(2)

|

Francis Letourneau Quebec City, QC

President, CEO and Director |

CEO and President of NuRAN Wireless since August 28, 2020 and October 16, 2020, respectively; VP, Sales & Marketing of NuRAN Wireless 2015 to 2020 | Since March 16, 2016 |

7,967 |

Jim Bailey Newbury, United Kingdom

CFO |

CFO of NuRAN Wireless; financial consultant to SMEs providing corporate finance advice in M&A, business planning |

Since October 16, 2020 |

3,042 |

Binyomin Posen(1) Toronto, ON

Director |

Senior Analyst at Plaza Capital Ltd. since 2017 |

Since October 16, 2020 |

Nil |

Brendan Purdy(1) Toronto, ON

Director |

Principal lawyer at Purdy Law since January 2014 |

Since October 16, 2020 |

Nil |

Vitor Fonseca(1) Toronto, ON

Director |

Treasurer and Vice President of Romspen Investment Corp. from February 2007 to February 2022; Director of Canntab Therapeutics Ltd. from April 11, 2018 to May 1, 2023 |

Since March 11, 2021 |

27,761 |

Navindran Naidoo Johannesburg, South Africa

Director |

Various Senior Management positions in Group Technology as well as being the Network Executive from 2013 to 2021. He has had previous assignments in Nigeria, Uganda, Cameroon, and Swaziland |

Since February 1st, 2024 |

Nil |

Avi Minkowitz Toronto, ON

Director |

Entrepreneur and finance professional with various private hedge funds |

Since September 30, 2025 |

Nil |

Joseph Labkowski Cape Coral, Florida

Director of Nuran |

Executive Director of the Chabad Jewish Center of Cape Coral |

Since December 22, 2025 |

Nil |

Notes:

(1) Member of audit committee for the fiscal year ending December 31, 2025.