MANAGEMENT’S DISCUSSION AND ANALYSIS

For the year ended

December 31, 2024 and 2023

MANAGEMENT’S DISCUSSION AND ANALYSIS

GENERAL

The following Management Discussion and Analysis of financial condition and results of operations (“MD&A”) of NuRAN Wireless Inc. (“we”, “us”, “our”, the “Company” or “NuRAN”) for the year ended December 31, 2024 has been prepared by management and should be read in conjunction with the audited consolidated financial statements for the years ended December 31, 2024 and 2023 and the related notes thereto. The Company’s consolidated financial statements are prepared in accordance with International Financial Reporting Standards (“IFRS”). References to notes are with reference to the consolidated financial statements. Unless otherwise noted, all currency amounts are in Canadian dollars. These documents, as well as additional information on the Company, are filed electronically through the System for Electronic Document Analysis and Retrieval (SEDAR) and are available online at www.sedar.com.

Unless otherwise stated, this MD&A is prepared as of April 30, 2025.

DISCLAIMER FOR FOWARD LOOKING STATEMENTS

This MD&A contains forward-looking statements. Often, but not always, forward-looking statements can be identified by the use of words such as “plans”, “expects” or “does not expect”, “is expected”, “estimates”, “intends”, “anticipates” or “does not anticipate”, or “believes”, or variations of such words and phrases or state that certain actions, events or results “may”, “could”, “would”, “might” or “will” be taken, occur or be achieved. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Issuer (as defined herein) or NuRAN (as defined herein) to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Examples of such statements include expectations regarding NuRAN’s ability to raise capital, the intention to expand the business and operations of NuRAN and use of working capital and proceeds of capital raises. Actual results and developments are likely to differ, and may differ materially, from those expressed or implied by the forward-looking statements contained in this MD&A. Such forward-looking statements are subject to a number of risks as outlined below under “Risks and Uncertainties” and include risks such as the uncertainties regarding the continuing impact of COVID-19, and measures to prevent its spread, risks relating to NuRAN’s business and the economy generally; NuRAN’s ability to continue to develop its new NaaS model; the capacity of the Company to deliver its technical solution and to import inventory to Africa at a reasonable cost; NuRAN’s ability to obtain project financing for the proposed site build out under its NaaS agreements with Orange, MTN and other telecommunication providers; the potential loss of one or more significant suppliers or a reduction in significant volume from such suppliers; NuRAN’s ability to meet or exceed customers’ demand and expectations; significant current competition and the introduction of new competitors or other disruptive entrants in the Company’s industry; NuRAN’s ability to retain key employees and protect its intellectual property; compliance with local laws and regulations and ability to obtain all required permits for its operations; access to the credit and capital markets; changes in applicable telecommunications laws or regulations or changes in license and regulatory fees; downturns in customers’ business cycles; insurance prices and insurance coverage availability; the Company’s ability to effectively maintain or update information and technology systems; our ability to implement and maintain measures to protect against cyberattacks and comply with applicable privacy and data security requirements; the Company’s ability to successfully implement its business strategies or realize expected cost savings and revenue enhancements; business development activities, including acquisitions and integration of acquired businesses; the Company’s expansion into markets outside of Canada and the operational, competitive and regulatory risks facing the Company’s non-Canadian based operations. These forward-looking statements should not be relied upon as representing NuRAN’s views as of any date subsequent to the date of this MD&A.

1

MANAGEMENT’S DISCUSSION AND ANALYSIS

Although NuRAN has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. There can be no assurance that forward-looking statements will prove to be accurate, as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward looking statements. The factors identified above are not intended to represent a complete list of the factors that could affect NuRAN. Such statements made by the Company are based on current expectations, factors and assumptions and reflect our expectations as at December 31, 2024. Except as required by applicable law, we undertake no obligation to publicly update or revise any forward - looking statement, whether as a result of new information, future events or otherwise.

For a description of material factors that could cause the Company’s actual results to differ materially from the forward-looking statements in this MD&A, please see “Risks and Uncertainties” below.

CORPORATE STRUCTURE

NuRAN was incorporated under the Business Corporations Act (British Columbia) on September 23rd, 2014. The Company was initially a wholly owned subsidiary of Bravura Ventures Corp. (“Bravura”). On October 14th, 2014, the Company entered into an arrangement agreement with Bravura and 1014379 B.C. Ltd., pursuant to which the shareholders of Bravura exchanged certain common shares of Bravura for common shares of NuRAN by way of a plan of arrangement (the “Arrangement”) and NuRAN became a reporting issuer in the provinces of British Columbia and Alberta.

Following completion of the Arrangement, NuRAN entered into an amalgamation agreement dated March 11, 2015 with Nutaq Innovation Inc. (“Nutaq”) and 9215174 Canada Inc. (“Newco”), a wholly owned subsidiary of NuRAN formed for the purpose of the amalgamation, pursuant to which Nutaq amalgamated with Newco and NuRAN acquired all of the issued and outstanding shares of the amalgamated company in consideration of 32,999,994 common shares of NuRAN based on a ratio of 2.749 NuRAN common shares for each share of Nutaq issued and outstanding on the closing date. Nutaq and Newco completed the amalgamation on June 2nd, 2015, and the amalgamated company was named “Nutaq Innovation Inc.”. Following the closing of the transaction, NuRAN had 40,471,869 common shares issued and outstanding and former shareholders of Nutaq acquired 81.5% of the issued and outstanding common shares of NuRAN. Following the closing of the Amalgamation, Nutaq Innovation Inc. was a wholly owned subsidiary of NuRAN and NuRAN operated the business of Nutaq.

Nutaq was incorporated under the laws of Canada on May 30, 2005, under the name “Lyrtech RD Inc.”. Nutaq changed its name to “Nutaq Innovation Inc.” on August 31, 2012; its registered and head office is located at 2150 Cyrille-Duquet Street, Suite 100, Quebec, Quebec G1N 2G3. On August 28, 2020, the Board of Directors of Nutaq voted to cease operations and on that date all its board members, except Mr. Francis Letourneau, resigned their respective positions. On August 31, 2020, Nutaq announced the decision and filed an insolvency proceeding and on September 1, 2020, the Company approved the appointment of Lemieux Nolet as trustee for Nutaq’s bankruptcy proceedings. At the same time the trading of the Company’s stock was halted.

On September 22, 2020, the trustee and Nutaq’s first ranking secured creditors reached an agreement pursuant to which all the assets of Nutaq, including all inventory, equipment and R&D equipment, trademarks, patents, accounts receivables, bank account and SR&ED credits would be sold. On October 27, 2020, the parent company re-acquired these Nutaq Assets for $100,000.

2

MANAGEMENT’S DISCUSSION AND ANALYSIS

As a result of the insolvency proceedings, the Company eliminated/extinguished the obligation to repay certain creditors and recorded a $1.5M gain on the extinguishment of liabilities. Also, the Company assumed all obligations of Nutaq. Subsequently the management of NuRAN made the decision to unwind the bankruptcy of Nutaq in order to recover the significant losses accumulated, now estimated at over $24M, which can be used to offset future profits of the Company. The process began in 2021 and the final step was completed when NuRAN’s proposal to creditors was accepted by the bankruptcy court on March 17, 2022. A final payment of settlement was made and on March 25, 2022, Nutaq received a Certificate of Full Performance of Proposal issued by the Licensed Insolvency Trustee signifying that Nutaq is released from the debt included in the proposal.

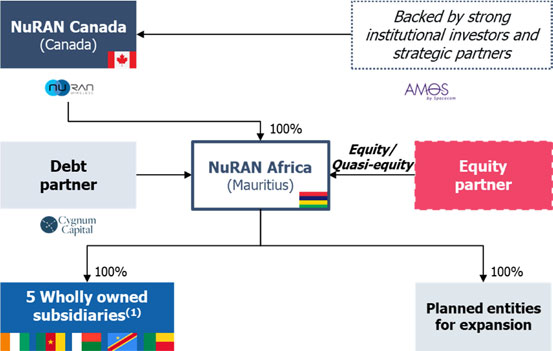

In 2021, NuRAN incorporated two wholly owned subsidiaries, NuRAN Wireless Cameroon Ltd. and NuRAN Wireless DRC SARLU, to own and manage the networks that the Company is developing in those countries. In April 2022 the Company incorporated NuRAN Wireless (Africa) Holding based in Mauritius, a regional holding company that will hold all of its African investments. During 2022 the shares in both subsidiaries were transferred to the holding company and in future this entity will be used to raise debt and equity to fund further growth. During 2023 NuRAN incorporated two other wholly owned subsidiaries of NuRAN Wireless (Africa) Holding; NuRAN Wireless Cote d’Ivoire SARLU and NuRAN Wireless Madagascar SARLU to own and manage networks in those countries. In September 2024, NuRAN Wireless DRC changed its status to SA, Societe Anonyme, and increased its capital to comply with local licensing requirements and in November 2024 NuRAN incorporated NuRAN Wireless Benin SARLU to own and manage a network in that country. The results therefore include the consolidated results of these African subsidiaries.

DESCRIPTION OF BUSINESS

NuRAN is a leading supplier of mobile and broadband wireless infrastructure solutions. Its innovative radio access network (RAN), core network, and backhaul products dramatically reduce the total cost of ownership, giving mobile network operators (MNOs) the ability to profitably serve remote, low income and low population density locations, an unfeasible proposition with existing systems.

NuRAN’s current business focus is to grow the market penetration of its Network as a Service (NaaS) offering, a communications solution whose backbone is its Wireless Infrastructure Systems (WIS).

NuRAN’s WIS are mobile wireless infrastructure equipment (e.g. base station radios) that use proprietary breakthrough small cell solutions to offer better coverage, the lowest installed cost, the most efficient power consumption combined with leading technology for satellite bandwidth reduction usage currently available in the global marketplace. This technology was subject to rigorous testing by leading MNOs proving its carrier-grade status and leading to broad acceptance for NaaS solutions in the years since.

Our design provides two key competitive advantages:

| ● | Low total cost of ownership, a key feature for developing countries and rural/low population density areas, and |

| ● | Small footprint, easy to deploy private networks, customizable for large scale deployments such as rural mobile networks and specific markets such as defense, utilities, industrial and machine-to-machine (“M2M”). |

3

MANAGEMENT’S DISCUSSION AND ANALYSIS

NuRAN’s NaaS model leverages the capabilities of its WIS as well as its extensive expertise in building cost-effective cellular infrastructure. The model provides not only network equipment, but NuRAN also finances, builds, manages and maintains the cellular sites in a very effective manner. Revenue to NuRAN comes in the form of either a revenue share with guaranteed minimum or threshold, or fixed monthly payments depending usually on the type of site being deployed. As demonstrated by the number of contracts signed, the NaaS model has received significant interest from MNOs as a carrier-grade mobile network infrastructure solution that allows MNOs to continue focusing their capital expenditure on building capacity in more dense urban and semi-urban areas while developing new technologies such as 4G and 5G. Another reason for this growing interest in the NaaS model is that it allows MNOs to reach previously uneconomic markets, thus meeting government license obligations to cover the vast majority of the population which is only possible by serving remote communities. The investment in the NaaS model is customer friendly but it also provides NuRAN with long-term recurring revenues resulting in a compelling return over contract periods which range from 5 to 10 years in length, and in many cases are of indefinite length because they incorporate continued asset ownership by NuRAN.

NuRAN’s wireless infrastructure solutions are also capable of supporting mobile payment transactions, a tremendous social and economic benefit for those in the developing world where 95% of all transactions are cash and 60% of adults don’t currently have a bank account, as well a significant potential market for MNOs. This is one of the key applications that MNOs are interested in rolling out when they deploy NaaS in rural areas where bank accounts are less prevalent.

By deploying communication infrastructure in uncovered areas, NuRAN also makes a very significant contribution to the socio-economic conditions of the areas it serves and meets a significant number of the seventeen sustainable development goals set by the United Nations. This includes improving the local economies and enabling access to e-learning, e-health and other social services not currently available to the local population.

GENERAL OBJECTIVES

NuRAN’s mission is to create a new possibility for over a billion people to communicate effectively over long distances. Our commitment combined with our ethical and ambitious values drive the company in its mission to connect the world.

Now more than ever, especially on the back of the COVID-19 pandemic and the need for remote connectivity, people need to be connected to the vast network that provides a window to the outside world and a connection with those around them. At NuRAN Wireless, we offer millions of people a universal possibility: connect to a global network and communicate over long distances efficiently and affordably in addition to contributing to the local economy. Our innovative, compact, and specialised solutions for rural regions allow users to stay connected with the world and keep in touch with family, friends, colleagues, and acquaintances.

NuRAN’s specialized telecommunications solutions satisfy the growing demand for wireless network coverage in remote and rural areas across the world. The fact that NuRAN’s solutions make it economically viable for MNOs to service small and isolated communities that have been previously ignored led to a truly disruptive technology. With its affordable solutions supporting 2G, 3G, 4G technologies and its innovative NaaS business model, NuRAN has the capability to build, optimize and manage rural connectivity expansion at an unprecedented rate.

4

MANAGEMENT’S DISCUSSION AND ANALYSIS

OVERALL PERFORMANCE AND OUTLOOK

Performance

During the year ended December 31, 2024, the Company continued to execute on its Network As A Service (‘‘NaaS’’) strategy to become the supplier of choice to MNOs across the world to connect remote and rural areas that until now could not take advantage of the economic and social benefits of connectivity. In fact, performance of most of the sites that are currently in operation have shown both rapid uptake and average performance that either meets or exceeds the Company’s business plan objectives on a per site basis, especially in Cameroon.

Management’s decision to redirect NuRAN’s efforts to the NaaS market was made with the awareness that this would require considerable initial investments in marketing, branding, sales, field tests and to prepare for increased production as well as working capital and capital investments to fund the rollout and installation of remote networks. Although not as rapid as expected, the recovery of this investment through recurring sustainable and more predictable revenues is being proven.

Despite the longer than expected timeframe that the MNOs rigorous qualification processes required before obtaining approval of NuRAN’s equipment and operating procedures and endorsing the use of our systems, the contracts executed to date, those currently being negotiated, and the growing sales pipeline confirms management’s vision.

The Company’s ongoing investments in research and development, engineering and manufacturing have been rewarded with the acknowledgment by leading industry organizations and participants that NuRAN’s Wireless Infrastructure Solutions are “at the top of their class”. For the past couple of years, the Company has clearly demonstrated that technology ownership is key to its success. The improvement of its solution has produced an important gain of sustainable capacity of its network resulting in significantly increased revenue.

To further support the growth of the NaaS model, management maintained its focus on raising capital to support its deployment plans and on continuous improvement of its operating sites.

In July 2021, the Company completed a $11M private placement led by strategic investor AMOS Spacecom who provided a $4M investment. Of this, over half of the proceeds were used to build an inventory of 240 sites in Cameroon and the Democratic Republic of the Congo (DRC). The Company then sought additional funding to complete the rollout.

As of the year ending December 31st, 2024, the Company has secured 9 contracts with MTN and Orange for 8 countries totalling 5,092 sites. NuRAN is now operating in 4 countries and has completed the incorporation of its operating subsidiaries in 1 more country Deploying the current backlog and the projected pipeline will require continued capital-raising efforts considering the requirements of all country operations. The progress on these efforts is highlighted further on in this document.

Powered by additional funding from the Cygnum Capital loan facility, the Cameroon operation’s cash contribution, the Societe Generale credit facility and Orange Cameroon’s payment of arrears, the Company was able to rollout additional sites, launch operations in new countries and prepare the network for the introduction of 3G capability. It therefore expects to achieve positive EBITDA in early 2025 with less sites than previously expected as Cameroon performance is exceeding revenue expectations.

As of December 31st, 2024, site revenue and traffic performance in Cameroon has completely exceeded management’s expectations. Supported by impressive network performance and capacity, NuRAN has doubled its revenue per site compared to its financial plan, mainly due to increased usage, and more than tripled its revenue since March 2023. Monthly Average Revenue Per User (ARPU) in Cameroon has reached US$ 5.70 compared to US$ 2.40 in 2023.

5

MANAGEMENT’S DISCUSSION AND ANALYSIS

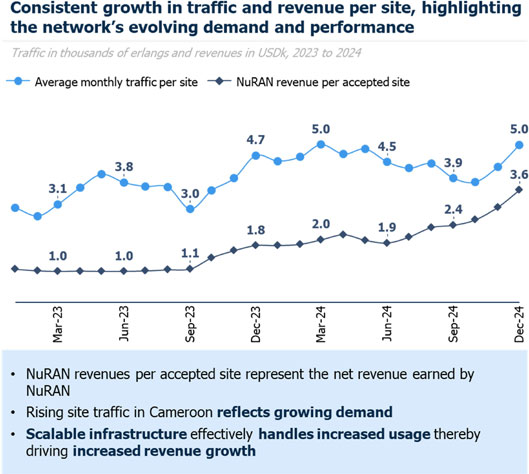

The following image demonstrates the evolution of traffic (measured in ERLANGs) and revenue per site and sets the trajectory for a highly profitable business model. On a per site basis, the Company is also reaching over 90% gross margin in Cameroon as the operation has established new standards of performance resulting in a significant cash contribution from the country. ERLANG is a traffic measure of channel occupancy, where 1 Erlang equates to one channel being used for an hour. The Cameroon network reached close to 500K ERLANGs in the month of December with over 100K active users.

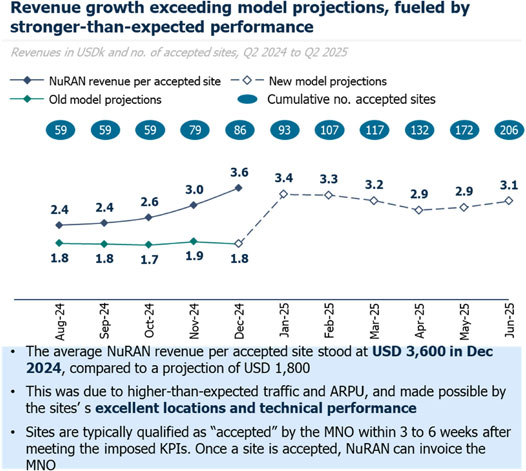

The image below shows how revenue per site in the last 5 months of December compared to NuRAN’s financial model. By December it was double the projection and NuRAN has reset its expectations based on this historical data trend.

6

MANAGEMENT’S DISCUSSION AND ANALYSIS

The Company has experienced significant revenue growth per site, alongside a notable reduction in the Cost of Goods Sold (COGS), culminating in a 91% Gross Margin as of December 31st, 2024, in Cameroon. The COGS encompasses expenses such as site lease, repair and maintenance, insurance, and satellite managed services. The comprehensive robustness and efficiency of NuRAN’s technical solution contributes to reduced preventive and curative maintenance costs, as well as lower satellite bandwidth utilization.

Given that local overheads have not increased at the same rate as the gross margin, the cash contribution locally reached 79% of monthly revenue per site in Cameroon during this period. Consequently, this increase in operational contribution from Cameroon offers greater flexibility to manage the cash needs of the organization across geographies including the parent company. With average site CAPEX of US$ 25,000, the current payback period is less than 8 months. Management’s focus on the operations in Cameroon should result in NuRAN achieving positive EBITDA in the very near future placing the company in a strong position to pursue its development plan.

Cameroon is performing well, but DRC is lagging. NuRAN has 25 billing sites in DRC, generating US$ 810 per month each—a 38.17% increase since December 2023. However, each site costs US$ 595, leading to losses due to insufficient gross profit to cover overhead costs. Management plans to relocate non-performing sites to improve revenue using better site selection. Based on last year’s learnings and commercial support, NuRAN aims to make DRC profitable and expand operations.

7

MANAGEMENT’S DISCUSSION AND ANALYSIS

The image above shows the level to which the actual results in Cameroon have outperformed management’s expectations. Early results for 2025 show a continued increasing trend so management is confident that it will achieve its forecast and reach positive EBITDA with fewer sites and therefore sooner than expected. The cumulative number of accepted sites is subject to these meeting Key Performance indicators (KPIs) and the mobile operators’ ability to accept these for billing in a timely manner. In conclusion, Cameroon has demonstrated its ability to independently drive the Company to profitability. The success seen in Cameroon will serve as a model for NuRAN to replicate in other target countries like Ivory Coast and Benin, where similar potential exists.

Operational and Business Highlights:

During the year 2024, NuRAN started to draw down from the recently signed a US$ 5M term loan facility agreement with Cygnum Capital (see below) and is progressing on other financing options. Management is now focusing on financing alternatives that it believes are efficient, reliable, and well aligned with its project objectives. As an example, the Company announced that NuRAN Wireless Africa Holding, a wholly owned subsidiary of NuRAN, has signed a non-binding Term Sheet and a Mandate Letter with a Global Asset Management Company (“The Lender” and “The Lead Arranger”) for a long-term senior secured credit facility (the “Loan Facility”) of which US$ 15,000,000 is to be provided by The Lender. The Loan Facility will include a mechanism for the Lead Arranger to increase the size of the Loan Facility to up to US$ 70,000,000 through a syndication with other lenders. This financing will facilitate the purchase of components and installation of network infrastructure sites across several African countries.

The long-term Loan Facility comprises much improved terms than those previously received from potential lenders and represents a crucial step forward in NuRAN’s strategic plans to bolster telecommunications infrastructure in Africa. This will allow NuRAN to implement network infrastructure rollouts, particularly in Cameroon, DRC, Ivory Coast, Benin and Madagascar. As of the date of these financial statements, the potential lender has completed its due diligence and subject to receiving an equity or quasi-equity term sheet, has indicated that it is ready to submit the file to its investment committee for final approval.

Regarding the equity raise, management remains dedicated to fulfilling the conditions requested by the potential investment partners. With positive EBITDA and the Q2 2025 commencement of operations in new countries—where we anticipate achieving results comparable to those in Cameroon—management is actively engaging with equity investors. Investors have been receptive and are continuously updated on our progress.

With the proceeds of the Cygnum Capital facility, site rollout has resumed in Cameroon. NuRAN’s operations team has been working on important improvements to the site selection and acquisition process and refining the improvements in network efficiency and capacity implemented during 2023 that have brought excellent results with significant increases in traffic and revenue on existing sites.

At the same time, management negotiated improved terms and pricing with key suppliers, resulting in, for example, a 50% reduction in monthly fees for satellite managed services leading to significantly increased gross margin.

As at the date of these consolidated financial statements, NuRAN has 5,092 NaaS sites under contract with Orange in Cameroon, the Democratic Republic of the Congo (DRC), and Madagascar and with MTN in South Sudan, Cameroon, Namibia, Sudan, Ivory Coast and Benin for a potential lifetime contract value of over US$ 900M. Following the announcement on July 21, 2022 of NuRAN’s entry into a Group Framework Agreement (“GFA”) with MTN Group (JSE: MTN) for up to 19,000 network sites in over 15 countries in the Middle East and Africa, the Company has been successful in engaging with a number of MTN operating companies. Management expects to bring additional contracts with MTN as well as other MNOs which will move the Company closer to meeting its objective of 10,000 sites under contract, especially as more traction is gained and cashflow generated in existing operations.

8

MANAGEMENT’S DISCUSSION AND ANALYSIS

The Company maintains its plan to develop and fund its 10,000 sites network objective in several phases and while discussions are at various stages, management reports high interest from several investors and lenders in participating in the next stages of financing. From the cash generated by its operations in Africa, the Company plans to reinvest in the project resulting in a reduction of the external capital required.

To achieve the 10,000-site goal, the business development strategy will focus on creating an economic hub around high-performing countries to leverage currency efficiency and cash movement within the hub, facilitating infrastructure consolidation and reducing CAPEX investment. Management aims to optimize financial efficiency based on market demand. For instance, Ivory Coast borders five countries and uses the West Africa CFA currency shared with seven countries, enabling cash generation to be invested in other countries.

This strategy involves forming what is termed as a “regional economic pole” (Pole), where high-performing countries act as central nodes that support surrounding nations economically. By consolidating infrastructure and investments within these hubs, NuRAN can ensure efficient use of resources and funds. The West Africa CFA currency allows seamless financial transactions across the region, minimizing currency exchange exposure and enhancing liquidity and cash flow.

Similarly, Cameroon, which borders six countries, can serve as another Pole. With its stable economy and strategic location, revenue generated in Cameroon can be reinvested into neighboring countries, thereby accelerating the deployment of 10,000 sites. This approach not only maximizes financial efficiency but also promotes regional economic growth and connectivity.

Without deviating from its actual focus of delivering its backlog to reach profitability and to enable additional financings, management expects to structure its approach strategically. By prioritizing the completion of existing projects and ensuring that operational targets are met, the company aims to build a robust financial foundation. This involves meticulous planning and execution of site rollouts, optimizing resource allocation, and continuously improving network infrastructure. This nuanced approach is designed to enhance cash flow, attract further investments, and solidify NuRAN’s position in the telecommunications market. This comprehensive strategy encapsulates the goal of achieving the 10,000-sites milestone while ensuring sustainable growth and regional economic synergy.

The business development and sales strategy revolves around leveraging the established Poles to sign contracts with surrounding countries. By capitalizing on the infrastructure and resources within these hubs, management aims to extend its reach and secure new contracts. Ivory Coast and Cameroon, as central poles, will serve as the foundation for this expansion. The strategy involves forming partnerships with mobile network operators in neighboring countries, using the success and stability of the hubs as a selling point. This approach will not only maximize the efficiency of resource utilization but also foster regional economic growth and connectivity. Through strategic negotiations and targeted marketing efforts, NuRAN intends to achieve its objective of 10,000 sites under contract by tapping into the potential of both existing and new poles across Africa.

9

MANAGEMENT’S DISCUSSION AND ANALYSIS

There is no assurance that the Company will reach the target of 10,000 sites under contract as planned and the estimates above are subject to the risk factors and assumptions set out below under “forward looking statements”.

Managements’ belief in the increasing adoption of the NaaS model by MNOs and NuRAN’s ability to efficiently and effectively manage the rollout of NaaS contracts is supported by a number of achievements since 2022:

| ● | On July 21, 2022, and subsequent to its earlier announcement, the Company announced the signing of the Group Framework Agreement (GFA) with MTN Group as mentioned above which offers the potential to connect up to 50 million additional people. |

| ● | On July 26, 2022, NuRAN announced its first signing following the GFA of a definitive 10-year NaaS contract with MTN Sudan Company Ltd. for the deployment of a minimum of 500 rural sites in Sudan. The agreement is estimated to generate up to approximately US$ 125M in revenues over its life and will support 2G and 3G. Due to the current situation in Sudan as of the date of these financial statements the Company has placed further development on hold. |

| ● | On October 11, 2022, the Company announced its second largest contract in terms of number of sites with an agreement for the rollout of up to 1,000 sites with MTN Ivory Coast. Over the 5-year period of the agreement, gross revenue is expected to be over US$ 75M. The contract includes an automatic renewal for an additional 5 years and similar to the previously announced MTN Sudan and MTN Namibia agreements, NuRAN expects to retain the ownership of the infrastructure after the completion of the contract. This shift in business model to the ownership of infrastructure with no handover to the MNO potentially increases the value of the agreement substantively to NuRAN and its shareholders by providing a continuous revenue stream. |

| ● | On January 17, 2023, NuRAN announced the entry into NaaS agreement with Orange Madagascar for the deployment of up to 500 rural sites on the east coast of Madagascar with contracted revenue potential of US$ 90M. The 10-year agreement is the Company’s third contract with Orange and is expected to support 2G and 3G networks with variety of site categories to cover different population densities and coverage areas. NuRAN expects to retain the ownership of the infrastructure after completion of the contract which increases the overall value of the agreement. |

| ● | On February 21, 2023, the Company announced a US$ 1.41M purchase order from the Marshall Islands National Telecommunication Authority (MINTA) to extend and add 4G coverage to their existing network. MINTA is the end customer under a previous contract with Intelsat which NuRAN has deployed since 2021 which validates the strength of the Company’s technology solution and deployment capabilities. |

| ● | On October 17, 2023, NuRAN announced that NuRAN Wireless Cameroon SARLU had received its Category 1 License for delivering and operating shared passive infrastructure to support digital communication networks. This license allows the Company to not only deliver its NaaS business model for Orange Cameroon but to expand its business by allowing for multiple mobile network operator (MNOs) or “tenants” on sites. NuRAN now has this added flexibility and can provide services similar to other tower companies in the future. |

10

MANAGEMENT’S DISCUSSION AND ANALYSIS

| ● | On November 16, 2023, the Company also announced that its wholly owned subsidiary, NuRAN Wireless DRC SARLU, has completed its application for a network infrastructure license in the DRC. The license is similar to the Category 1 License in Cameroon in that it allows for expansion of the business model beyond NaaS as well as the addition of VSAT services. The decision follows a Ministerial Decree published on October 10, 2023 which simplifies the obligations of holders of the license, specifically related to ownership requirements. A condition of this application included converting the subsidiary to a SA which was completed in September 2024. |

| ● | On June 5, 2024, NuRAN announced a five-year NaaS agreement for the deployment of 250 sites in Africa with MTN further to its GFA in place with the Group. This agreement is the fifth agreement signed with MTN totaling 2,150 sites in five different countries, representing up to approximately US$ 27 million in revenues over the course of five years assuming that the 250 sites are completed. The five-year term of the NaaS pursuant to the GFA can be extended or renewed for an additional five years subject to an extension or renewal agreement. |

| ● | On July 16, 2024, the Company announced an agreement for up to 200 sites with MTN Benin for the deployment of rural 2G, 3G and 4G sites under the NaaS business model in Benin, West Africa. The 5-year agreement with MTN Benin includes a renewal for an additional 5 years at the end of the initial term. This agreement has been signed under the MTN Framework Agreement announced on July 21, 2022, serving as further evidence of the strong partnership between MTN and NuRAN both dedicated to empowering lives in rural communities across Africa. |

| ● | On December 9, 2024, The Company announced that it has achieved positive Earnings Before Interest, Tax, Depreciation and Amortization (EBITDA) in its wholly owned Cameroon subsidiary. The recent developments specifically pertaining to site acceptance have accelerated subscriptions and mark a clear turning point for the company in Cameroon. |

| ● | On March 7, 2025 NuRAN reported that it had been closely monitoring the recently proposed changes in customs tariffs between the United States (US) and Canada. The majority of NuRAN’s suppliers are not based in the US and are either in Canada or other international locations. Equipment sourced from the US accounts for less than 5% of the total material costs of base station radios. Other material from suppliers based in the United States is procured directly from Africa, avoiding any tariffs levied by the US on Canada. Therefore, the impact of the proposed tariffs on total operational costs will be negligible. |

Some of the financial achievements that support management’s belief in its ability to complete the building of the networks currently under development and those being negotiated include:

| ● | On January 3, 2024, the Company announced that it had signed a non-binding mandate letter for a US$ 5M Senior Secured Bridge Facility (the “Facility”) for (re)financing of renewable energy assets for NuRAN Wireless (Africa) Holding. The Facility will have a 2-year tenor and bullet principal repayment at maturity. It is to be refinanced by long-term senior debt at maturity and the term can be extended by the lender or converted into other long-term debt. On April 26, 2024, NuRAN announced the signing of the Loan Facility agreement with the Facility for Energy Inclusion (“FEI”), a fund managed by Cygnum Capital. The Loan Facility is for the purpose of financing the construction of renewable energy assets for mobile network infrastructure in respect of existing and new Network as a Service (“NaaS”) agreements with the intention of accelerating the build of NaaS sites primarily in Cameroon and DRC. This senior secured Loan Facility is intended to allow NuRAN to deploy more than 500 new sites. Combined with cash generated from operating sites, the Company intends to use the proceeds to cover all material and construction costs of new sites. The loan drawdowns are subject to customary drawdown conditions for a loan of this nature including evidence of new sites being funded and operational from the proceeds of drawdowns and the amounts are secured against the assets of the Company’s subsidiaries. |

11

MANAGEMENT’S DISCUSSION AND ANALYSIS

| ● | Also on January 3, 2024, the Company announced that it extended the maturity date of the Convertible Debentures entered into in July 2022 to July 12, 2024. In addition the original issuance discount of 10% was increased to 16% leading to a maturity value of $ 2,645,502 and the principal amount is convertible into common shares of the Company at a fixed price of $0.40 at the option of the debenture holder during the term of the Convertible Debenture. The investor remains committed to the NuRAN business as the exclusive transmission equipment provider for a term of the earlier of seven years or until such time as the Company completes the purchase of a committed volume of equipment for its African operations. |

| ● | On February 6, 2024, the Company announced that it had received a non-binding Letter of Intent for up to US$ 15M of debt financing and on March 11, 2024, the Company announced that it received three additional expressions of interest from lenders to support the Company’s network infrastructure roll-out at the NuRAN Africa level. It is anticipated that the funding can be drawn individually or as co-lenders in a syndicated debt facility. The combined value of these four potential facilities as well the possible rollover of the US$ 5M bridge facility mentioned above can possibly fund at least 2,500 of the sites under contract. Moreover, the terms proposed by those potential lenders are actually more attractive to the Company than anything received previously and also provides much more flexibility allowing drawdown on a per country basis if necessary. This is a result of the positive progress made to date with current operations and contracts. |

| ● | On April 4, 2024, NuRAN announced the confirmation of US $800K credit facility from a local Cameroon Commercial Bank to NuRAN Cameroon and specifically to support the further deployment of sites. The announced credit facility has a 2-year tenor with a 9% interest rate per annum. By the end of the year, management had finalised the terms to work alongside the Cygnum Capital facility and agreed initial drawdown. |

| ● | On May 15, 2024, The Company announced that NuRAN Wireless Africa Holding, a wholly owned subsidiary of NuRAN, has signed a non-binding Term Sheet and a Mandate Letter with a Global Asset Management Company (“The Lender” and “The Lead Arranger”) for a long-term senior secured credit facility (the “Loan Facility”) of which US$ 15,000,000 is to be provided by The Lender. The Loan Facility will include a mechanism for the Lead Arranger to increase the facility to up to US$ 70,000,000 in funding including a syndication of other lenders. This financing will facilitate the procurement and installation of network infrastructure sites across several African countries. |

| ● | On July 16, 2024, the Company announced that the initial US$ 2.5M drawdown from the Facility for Energy Inclusion (“FEI”) had been received. As a result of this NuRAN resumed its rollout plan. While the majority of the amount will be dedicated to Cameroon, NuRAN expects to dedicate a portion to initiate site build in the Ivory Coast, Benin and Madagascar. On February 28, 2025, NuRAN announced that it had received approval for the second drawdown of US$ 1.05M to support expansion of its NaaS operations in Cameroon. |

12

MANAGEMENT’S DISCUSSION AND ANALYSIS

| ● | On August 19, 2024, NuRAN announced the closing of a non-brokered private placement of an unsecured convertible debenture (the “Debenture”) for aggregate gross proceeds of US$ 1.6M. The Debenture has a two-year term and accrues interest at a rate of 15% per annum until the Maturity Date. The principal amount of Debenture is US$ 2,194,772 after application of an original issuance discount of 25% and including all applicable fees. The Debenture may be converted into units of the Company (each, a “Unit”) at a conversion price of CDN$ 0.225 per Unit (the “Conversion Price”) with each Unit consisting of one common share and one common share purchase warrant exercisable into one common share at a price of CDN$ 0.25. Under the terms of the Debenture, the Company also granted a participation right in future equity financings up to a 9.9% equity interest in the Company. |

Equity Investments Supporting Lender’s facility

Since the announcement of proposed and closed loan facilities, management has been focusing on accelerating discussions with Investment Funds and potential strategic partners targeting infrastructure investments in emerging markets. To date the concerns expressed by those investors were mainly related to site performance, operational capacity, asset ownership, risk diversification across markets and the availability of debt finance. In parallel with these discussions, and as part of its ongoing work to strengthen NuRAN’s operating and financial position, management has been addressing all these areas of concern. The Company is utilising its flexible structure to allow for debt and equity fund-raising at various levels. The next financings are planned to occur at the NuRAN Wireless (Africa) Holding level in Mauritius to avoid share dilution at the parent level.

Results in Cameroon have exceeded expectations with growth in traffic and revenue supported by enhancements of NuRAN’s solution increasing network capacity. In addition, better site allocation and selection has ensured the success of new sites. We are adopting the same measures in DRC and have started to see signs of performance improvement. Technology effectiveness and ownership is a key criterion to NuRAN’s success in rural emerging markets, and our engineering team is working continuously on further upgrades. In addition to these measures, the DRC commercial team has established a strategy reselling Orange products and services that has already shown important growth in user adoption and traffic resulting in revenue growth.

Combined with the accumulated experience of its internal team, management has put together a comprehensive ecosystem of partners to support growth. This ecosystem works across service delivery from site selection to monitoring to share findings in both existing and new countries. The Company has also increased and diversified its supplier base to meet demand and reduce the risks associated with one single supplier.

13

MANAGEMENT’S DISCUSSION AND ANALYSIS

With over 5,000 sites currently under contract, NuRAN’s DRC exposure is now less than 50% reducing the concentration risk. The recently signed US$ 5M bridge facility from Cygnum Capital, the US$ 1.6M private placement along with the 2024 announced US$ 15M Term Sheet of a possible US$ 70M Facility will support management’s efforts to raise equity. While the Cygnum Facility is expected to allow the Company to reach operating 600 sites that will demonstrate/confirm the full potential of the NaaS business model, management is now focused on launching new countries starting with Benin and Ivory Coast in order to diversify its revenue sources.

All of the above are measures that have not only improved the Company’s financial performance but also increased its attractiveness to equity investors.

The team has been working to initiate operations in newly contracted countries and investment will therefore be utilised across the business to build diversified and growing coverage in Africa. Continued interest in the investment case and strong fundamentals of existing operations reinforce management’s belief in the success of the Company’s strategy and its belief that NuRAN is positioned to become the market leader in this very important and growing space.

Outlook

NuRAN’s wireless infrastructure solutions have long been deployed by MNOs as an integral part of their network operations and now under the NaaS model in extending rural coverage. NuRAN solutions have been either tested or are now operated by MNOs in more than 20 countries across Southeast Asia, Africa, South America and Latin America. NuRAN has also established alliances with other key industry participants such as tower, satellite and power companies to further increase its market reach. Management continues to believe that the successful acceptance and adoption of NuRAN’s system by MNOs and partnerships with key industry players place NuRAN in a position to generate significant sustainable business.

NuRAN previously announced its LiteRAN xG, a mobile wireless infrastructure solution that will provide operators with 2G, 3G & 4G capability from a single piece of equipment allowing them to run multiple technologies simultaneously and evolve their services over time. The addition of LiteRAN xG to the Company’s portfolio, planned for early 2025, will significantly widen the Company’s addressable market.

The strength of NuRAN’s NaaS offering is demonstrated by the 5,092 sites under contract with the two largest MNOs in Africa and we continue to build our pipeline towards the 10,000-site objective. Announced in July 2024, the 200-site contract with MTN Benin completes the 5,092 including Orange SA in Cameroon, Madagascar and DRC as well as MTN Group in Cameroon, South Sudan, Sudan, Ivory Coast and Namibia. The signed NaaS agreements with MTN in Sudan and South Sudan are on hold due to the volatile situation in those countries currently. NuRAN has also recently announced a Memorandum of Understanding (MOU) with Telecel in Ghana to resume the 7 sites delivered in the country powered by a GSMA Investment fund. The MOU established the framework to enter into a NaaS agreement in 2025 in line with the economic pole strategy mentioned above.

The additional contracts with MNOs and the signing of the Group Framework Agreement (GFA) with MTN Group is recognition of the quality of NuRAN’s carrier-grade mobile network infrastructure solutions, its extensive expertise in the installation and management of cost-effective cellular networks as well as the economic benefits of being able to reach a large base of customers, not reachable without NuRAN’s systems.

14

MANAGEMENT’S DISCUSSION AND ANALYSIS

The following discussion of the Company’s financial performance is based on the consolidated financial statements for the year ended December 31, 2024 and 2023.

Factors Concerning the Company’s Financial Performance and Results of Operations

To evaluate the results of the strategic shift, management closely monitors four key measures of the Company’s performance: Revenue, Gross Profit Margins (GPM), Earnings Before Interest, Taxes, Depreciation and Amortization (EBITDA) and Net Income.

Revenue growth measures the success of the NuRAN’s products and services, led by the NaaS solution, combined with our marketing and sales efforts. Growth is demonstrated by the Company’s ability to enter into contracts, build NaaS infrastructure, penetrate new markets and gain new customers for existing and new products and services. The investments in marketing and sales and the shift in direction to more of a services model have increased our sales pipeline, started to generate sales with first sites live and should produce increasing revenues as rural subscribers in previously covered and uncovered areas take advantage of more choice, availability and variety of mobile services to improve their economic position. The take-up of NaaS solutions and the resultant recurring revenue stream brought on by each live site is starting to already generate transformative growth in revenue for the Company.

GPM measures how efficiently and effectively NuRAN delivers its systems and services to its clients, both in terms of production of its product line, and increasingly, delivery of the NaaS solution in rural areas and direct costs of delivery incurred in local subsidiaries.

Some of NuRAN’s NaaS agreements include a guaranteed minimum revenue monthly fee (GMR) to ensure a return on each site, covering costs and interest. Recently, with high network performance, the Company is transitioning to a threshold model, whereby revenue is retained up the threshold but allowing them to retain more revenue and retain ownership of the sites. Under IFRS, current contracts require NuRAN to record site sales when operational, impacting revenue and gross profit margins. Future contracts without site transfer will better reflect invoicing and economic results. Management monitors three gross profit margin indicators: revenue per site, revenue share, and operational fees. This shift aims to create a stable and recurring revenue stream post-rollout completion.

EBITDA measures the entire operations by including selling and administrative costs in African subsidiaries as well as Canada. It should increase as sales grow due to the fixed nature of much of the support infrastructure including administrative, sales & marketing, research & development and other costs and the economies of scale that can be achieved in monitoring network operations and maximizing site performance.

Net income is a measure of how efficiently and effectively the business is running, however management recognises that, given the stage of NaaS rollout and implementation, the Company is likely to be loss-making for some time. To achieve an acceptable net income, the company needs to significantly increase its revenues, while maintaining or slightly increasing its selling and general administration costs and efficiently utilising the capital assets that it deploys, achievable through the NaaS model.

15

MANAGEMENT’S DISCUSSION AND ANALYSIS

Tower Outlook Disclosure

Regarding the outlook for site deployment, management continues to report on the status of its expected deployment of NaaS sites. In order to improve the accuracy of development plan expectations, management is pursuing site development in phases that are determined based on the confirmed availability of funds for a specific phase. As an example, the cash generated from its operation in Africa, the recently announced US$ 5M facility, local Cameroon financing and the investment in August from a long-time shareholder are now expected to contribute to the delivery of at least 600 sites. As of the date of these consolidated financial statements, an initial drawdown of US$ 2.5M was received in July 2024 and a further US$ 1.05M in March 2025 from the US$ 5M Facility from Cygnum Capital. Supported by continued strong cashflow from operations, subsequent drawdowns will fund the ongoing deployment plans.

As a result of the Company’s ongoing financing efforts, management continued to increase its pipeline of financing options from other groups with expressions of interest of over US$ 80M including the US$ 15M term sheet announced in May and agreed mandate to further increase this amount. With the Company’s contributed equity in NuRAN Wireless (Africa) Holding supporting this long-term debt, the additional financing options available, and cash generated in its subsidiaries, NuRAN is committed to showing regular progress in building the planned number of operating sites.

SELECTED ANNUAL FINANCIAL INFORMATION

The following is selected financial data derived from the annual consolidated financial statements of the Company as at December 31, 2024 and December 31 2023 and for the periods then ended:

| Year ended December 31, 2024 | Year ended December 31, 2023 | Year ended December 31, 2022 | |

| Total revenues | $ 4,364,327 | $ 3,199,125 | $ 4,871,890 |

| Total loss | $ (8,755,860) | $ (12,322,243) | $ (9,892,114) |

| Net loss per share – basic | $ (0.16) | $ (0.32) | $ (0.30) |

| Net loss per share – diluted | $ (0.16) | $ (0.32) | $ (0.30) |

| As at December 31, 2024 | As at December 31, 2023 | As at December 31, 2022 | |

| Total assets | $ 23,878,422 | $ 20,210,608 | $ 18,737,500 |

| Total non-current financial liabilities | $ 66,739 | $ 293,768 | $ 405,522 |

16

MANAGEMENT’S DISCUSSION AND ANALYSIS

RESULTS OF OPERATIONS

Revenue

Revenue for the year ended December 31 2024 of $4,364,327 was a significant increase of $1,165,202 from the year ended December 31, 2023 ($1,672,765 decrease for the year ended December 31, 2023 compared to the year ended December 31, 2022).

Of the total revenue for the year ended December 31, 2024, $3,431,300 was NaaS service revenue from site operations, including $793,341 invoiced in December related to sites not previously accepted as “live” by the mobile operator (disputed sites). This relates mostly to 2024 with a small portion from 2022 and 2023 and is $14k less than the estimate mentioned in our September 30, 2024 reporting. The dispute is now resolved. Also included in NaaS is $(120,875) that was an adjustment to comply with IFRS 15, which as mentioned earlier requires that we recognize a sale of the site and cost when it becomes operational. Over 90% of NaaS revenue relates to Cameroon and the remainder to DRC. Other revenue was related to CAPEX sales, including MINTA, of $933,027 for the year ended December 31, 2024.

Gross Profit

Gross profit for the year ended December 31, 2024 increased by $1,787,795 compared to the year ended December 31, 2023 (decreased by $1,492,787 for the year ended December 31, 2023 compared to the year ended December 31, 2022).

Gross margin for the year ended December 31 2024 increased to 53% from 17% for the year ended December 31, 2023 (decreased to 17% for the year ended December 31, 2023 from 42% for the year ended December 31, 2022).

The overall gross margin increased significantly and, although it includes the arrears revenue noted above, is more in line with the Company’s projections based on the level of direct costs for the NaaS offering, including VSAT. The gross margin % is impacted by IFRS 15 adjustments in 2023 and 2024 which includes the sale of sites as described above. Overall, in 2024 NaaS gross margin was 59%, and 74% excluding the IFRS 15 adjustment. The change in revenue recognition following the planned move from GMR to the threshold method will smooth out future reporting.

The direct costs of NaaS include site leases, insurance, repair & maintenance and VSAT costs with VSAT having a minimum capacity charge. As a result of more revenue being generated over this fixed capacity charge, the VSAT cost per site continues to fall. Further reductions will be realised in 2025 as a result of contract renegotiations as mentioned above as well as the expected increases in NaaS revenue.

Expenses

During the year ended December 31, 2024, total expenses decreased by $1,484,318 from the year ended December 31, 2023 (for the year ended December 31, 2023 total expenses increased by $907,911 from the year ended December 31, 2022). All cost categories including financial expenses but excluding research and development costs went down as a result of continued cost containment initiatives undertaken by management. Financial expenses decreased mainly because of the reduction in the interest rate agreed with the factoring company to 5% for the year. Approximately 90% of financial expenses are non-cash charges including interest costs of short-term borrowings and accretion expenses of convertible debentures. The Company booked a foreign exchange gain as a result of intercompany accounts with subsidiaries denominated in USD which was for the most part offset by a loss in the translation of foreign operations; at the consolidated level these have negligible impact. Research and development costs increased as a result of continued focus on the development of the 3G/4G platform which is a continuing emphasis of the Company as it responds to the needs of its MNO customers.

17

MANAGEMENT’S DISCUSSION AND ANALYSIS

Net Loss Before Other Elements and Income Taxes

As a result of all the factors mentioned above the Net Loss Before Other Elements and Income Taxes for year ended December 31, 2024 decreased to $8,560,812 from the year ended December 31, 2023 loss of $11,832,924 (for the year ended December 31, 2023 total Net Loss Before Other Elements and Income Taxes increased to $11,832,924 from the year ended December 31, 2022 loss of $9,432,226). The change for the year ended December 31, 2024 was a result of the increase in gross profit and the reductions in operating expenses including financial expenses. Going forward, expenses should not increase significantly whereas growth in revenue and gross profit related to more sites going live will allow the Company to realise operating leverage as management remains focused on achieving positive Earnings Before Interest, Tax, Depreciation and Amortisation (EBITDA). The Company will also look to shift the focus from short term credit facilities in Canada to long term for the African operations and continues to pursue several initiatives on this front.

Other Elements

Other Elements for the year ended December 31, 2024 generated a net loss of $50,160 compared with a net loss of $473,558 in the year ended December 31, 2023 (a net loss of $473,558 for the year ended December 31, 2023 compared to a net loss of $459,400 for the year ended December 31, 2022). These relate mostly to a gain on the settlement of short-term borrowing facilities during the period offset a write-off of inventory booked in Canada.

Net Loss

As a result of all the factors mentioned above the Net Loss for the year ended December 31, 2024 decreased to $8,755,860 from the year ended December 31, 2023 loss of $12,322,245, a significant improvement of $3,695,511 (for the year ended December 31, 2023 increased to $12,322,245 from the year period ended December 31, 2022 loss of $9,892,114).

Total Comprehensive Loss

The difference in the foreign exchange translation of foreign operations for the year ended December 31, 2024 was a net loss of $1,170,878 (compared with a net gain of $191,355 for the year ended December 31, 2023). Even after taking this into account, the Total Comprehensive Loss for the year ended December 31, 2024 improved to $9,926,738 compared to $12,130,890 for the year ended December 31, 2023 (a Total Comprehensive Loss of $12,130,890 for the year ended December 31, 2023 compared to a Total Comprehensive Loss of $10,060,902 for the year ended December 31, 2022).

Expenses

Below is a discussion of the expenses for the year ended December 31, 2024, and the year ended December 31, 2023.

| 2024 | 2023 | % change from 2023 | |

| Selling expenses | 798,660 | 910,662 | -12.30% |

| Administrative expenses | 6,821,129 | 7,380,941 | -7.58% |

| Employee share-based compensation | — | 6,264 | -100% |

| Financial expenses | 2,596,960 | 3,599,987 | -27.86% |

| Research and development costs | 675,678 | 478,889 | +41.09% |

| 10,892,426 | 12,376,744 | - 11,99% |

18

MANAGEMENT’S DISCUSSION AND ANALYSIS

Selling expenses

Selling expenses consist of salaries to sales and marketing staff, commissions on sales, travel expenses, trade shows, presentations and costs associated with the IR online marketing campaign. The decrease shows the impact of reduced headcount of sales staff as the business continues to focus on operations, rollout of sites under contract and financing rather than signing new contracts. Marketing efforts are also seeing less emphasis although the management team makes a point of attending events in Africa, especially where these can be combined with raising finance and visiting operating subsidiaries.

Administrative expenses

Administrative expenses consist of staff remuneration, legal fees, audit and accounting fees, insurance, rent, consulting fees and general office expenses. These costs decreased from the previous year, with the most significant reduction being in outside advisory and professional fees as management internalised activities and focused on advancing and closing existing financing relationships. Some financing advisory costs will continue as management continues to raise debt and equity finance until the business becomes cashflow positive.

Financial expenses

Financial expenses consist of bank charges, convertible debenture and lease interest, charges associated with short term financing and gain/loss on foreign exchange. The decrease in financial expenses for the year ended December 31, 2024, compared to the year ended December 31, 2023, is mainly a result of a reduction in the interest rate charged on factoring as well as costs associated with the debt restructuring at year end. Management’s focus in 2024 continues to be on creating the conditions to repay these short-term facilities and to reduce the emphasis on these types of financing. As mentioned, a foreign exchange gain was booked offsetting a loss in the translation of foreign operations. The Company does have foreign exchange exposure to the US dollar which many sales and component costs are denominated in as well as the Communauté Financière Africaine (CFA) which is the denomination of revenue in Cameroon, and which is pegged to the Euro.

Research and development

Research and development costs for the year ended December 31, 2024 increased over the year ended December 31, 2023 as the Company continued to focus on control and continuous improvement of its technical solution and enhancements to its product line towards 3G/4G capabilities in line with its unique positioning and awareness of requirements in the markets it operates in.

In general, management has streamlined operations as evidenced in the reduction in Selling and Administrative expenses. This follows a restructuring initiative that took place in 2023 to organise operations globally based on function rather than geography. It shows the Company’s commitment to reach positive EBITDA which it expects to do in 2025. With the funding of Cygnum Capital, increased operating cashflow and other facilities the Company is building more sites generating an increasing amount of recurring revenue. With operating costs covered by NaaS revenue any new funds raised can be directed to site construction and servicing and repaying other debt. This will support management’s efforts to continue to negotiate better financing terms including existing and new financing initiatives.

19

MANAGEMENT’S DISCUSSION AND ANALYSIS

SUMMARY OF QUARTERLY RESULTS

| Three Months Ended | Total revenues ($) | Total loss ($) | Basic and Diluted Loss Per Share ($) |

| 31-Dec-24 | 663,422 | (371,968) | (0.01) |

| 30-Sep-24 | 1,563,061 | (3,220,575) | (0.06) |

| 30-Jun-24 | 1,512,457 | (2,425,969) | (0.05) |

| 31-Mar-24 | 572,727 | (2,355,685) | (0.05) |

| 31-Dec-23 | 1,125,235 | (2,861,581) | (0.07) |

| 30-Sep-23 | 797,067 | (3,302,317) | (0.08) |

| 30-Jun-23 | 602,255 | (2,823,600) | (0.07) |

| 31-Mar-23 | 671,961 | (3,365,516) | (0.09) |

| 31-Dec-22 | 1,193,772 | (1,313,868) | (0.04) |

Fourth Quarter

During the three months ended December 31, 2024, the Company earned revenues of $663,422, including approximately $250,000 of NaaS service revenue related to sites not previously invoiced from 2024 in Cameroon. This compared to $1,128,235 during the three months ended December 31, 2023, a decrease of $464,813. This was a result of reduced revenue recognised for Capex sales as well as an adjustment for IFRS 15 resulting from sites going live in the quarter.

During the three months ended December 31, 2024, the Company generated gross margin of $289,704 compared to $612,057 during the three months ended December 31, 2023, a decrease of $322,353 resulting in a 44% gross profit. This was a result of the Capex sale and IFRS 15 adjustments mentioned above, both which contributed negatively.

During the three months ended December 31, 2024, the Company incurred a net loss of $371,968 compared to net loss of $2,861,581 for the three months ended December 31, 2023.

LIQUIDITY AND CAPITAL RESOURCES

The Company’s cash increased to $1,171,558 as at December 31, 2024, from $172,880 as at December 31, 2023. Current assets increased to $16,125,341 as at December 31 2024, from $12,448,920 as at December 31, 2023 due to increases in Trade and other receivables, accrued revenues, inventories, work in progress and security deposits.

20

MANAGEMENT’S DISCUSSION AND ANALYSIS

The cash position as at December 31, 2024 reflected inflows from financing from Cygnum Capital and the private placement not yet deployed. Given the ongoing deployment of network infrastructure for NaaS sites, the Company expects to be consuming cash and in a loss position for the foreseeable future. With the Cameroon entity now generating positive cash contribution based on its NaaS income, management sees the benefit of increasing scale in country operations to provide funding to continue to accelerate site construction. Additional cash at the Canada HQ level will be generated from product sales and services provided to external customers (e.g. MINTA). The current focus on site construction in Cameroon and other countries in the short term will allow the Company to improve its cash situation in as short a period as possible.

The recently closed US$ 5M Senior Secured Bridge Facility allowed the Company to refinance its expenditures on energy assets both on existing sites and in inventory, estimated at over US$ 1.5M. These funds, along with the US$ 1.6M private placement proceeds from a long-time shareholder brought additional liquidity to the Company allowing for implementation of site construction plans and continuity of operations. In addition, the Company has invested in its Radio Access Network production to support future installations of up to 250 sites. The Company also reduced accounts payable representing strategic supplier balances and repaid short term debt facilities amounting to almost $1.5M.

Future Financing

Management closely monitors the cash position and short and long-term cash requirements. The Company has broadened its search for capital to support its growth objectives for the NaaS business which included reaching out to Development and Impact Funds as well as other sources such as equity and hybrid investors. Management also recognizes the opportunity for improved cash flow from converting inventory to operating NaaS sites utilising the recent cash injection and given the strong results it has seen from existing operations. It is transitioning some inventory from DRC to Cameroon and Ivory Coast as a means of improving the return on these assets. In addition to spending on site rollout, the Company will continue to look for additional financing to fund operations and maintain its growth strategy (including continuous development of next generation wireless solutions such as the multi-Standard 2G, 3G, 4G platform, as well as the deployment of mobile infrastructure and extended services under the NaaS model).

Current revenues are not sufficient to cover its selling, administrative and R&D costs and finance the capital investment necessary to implement its NaaS contracts. The Company continues to depend on its ability to convert its signed contracts into recurring revenue (for example the agreements with Orange SA for Cameroon, DRC and Madagascar and with MTN for South Sudan, Namibia, Sudan, Ivory Coast and Benin), raise debt to finance NaaS projects and future equity issuances or other means to finance its operations, including funding into NuRAN Wireless (Africa) Holding in Mauritius. Due to the current situation in Sudan and South Sudan as of the date of these financials the Company has placed on hold any effort to pursue the development of this network.

While the company remains reliant on external funding for CAPEX spending and short-term debt repayment and restructuring, it has become increasingly less dependent on external funding for day-to-day operations. Boosted by the recent US$ 5M Loan facility, the US$ 1.6M private placement and the term sheet and mandate letter aimed at raising up to US$ 70-80 million, management believes that the company will be able to raise the necessary financing, and that its financial position is expected to improve significantly. However, while showing continued promise, there can be no guarantee that these efforts will be successful.

21

MANAGEMENT’S DISCUSSION AND ANALYSIS

RISKS and Uncertainties

Additional Financing Requirements and Access to Capital

NuRAN’s ability to realize its assets and discharge its liabilities depends on the continued financial support of its shareholders, the growth and profitability of the future sales of its products and services and from obtaining additional financing.

Sales Risks

NuRAN’s sales efforts target large corporations that require sophisticated data capture and production execution systems to collect and analyze data relating to various operational activities. NuRAN spends significant time and resources educating prospective customers about the features and benefits of its solutions. NuRAN’s sales cycle usually ranges from 3 to 18 months and sales delays could cause its operating results to vary. NuRAN balances this risk by continuously assessing the condition of its sales pipeline and making the appropriate adjustments as far in advance as possible. NuRAN’s strategy also includes a comprehensive program to build and improve relationships with long-standing customers to better understand needs and proactively manage incoming business levels effectively.

Foreign Exchange Risk

NuRAN’s sales are mainly outside Canada and are generally conducted in currencies other than the Canadian dollar, while a majority of our product research and development expenses, integration services, customer support costs and administrative expenses are in Canadian dollars. Fluctuations in the value of foreign currencies relative to the Canadian dollar and Cameroon CFA can negatively, or positively, impact NuRAN’s financial results. The company monitors this risk and will enter/consider entering into forward/ derivatives contracts to minimize the exposure.

Outsourcing Risk

NuRAN outsources the manufacture of its products to third parties. If they do not properly manufacture the products or cannot meet the needs in a timely manner, NuRAN may be unable to fulfill its product delivery obligations and its costs may increase, and its revenue and margins could be negatively impacted. The Company’s reliance on third-party manufacturers subjects it to a number of risks, including the absence of guaranteed manufacturing capacity and the inability to control the amount of time and resources devoted to the manufacture of products. To mitigate this dependency, the Company has relationships with two separate manufacturing service providers and maintain contact with additional alternative suppliers in case the primary manufacturing sources should be disrupted.

Competition

NuRAN must contend with strong international competition. Therefore, there are no guarantees that NuRAN can maintain its competitive position. However, its unique mix of products combined with NaaS service delivery, and skilled human resources give it a competitive edge in several markets.

Availability and Cost of Qualified Professionals

The high-technology industry’s strong growth as well as the Company’s move into the NaaS model increased the demand for qualified staff. So far, NuRAN has successfully met its needs for personnel. NuRAN benefits from its location in Quebec City, which gives it access to a large pool of engineering resources but has also pursued hiring internationally. Aware that the satisfaction of its customers is directly tied to the quality of its employees, NuRAN continues to take measures to attract and retain well-qualified professionals from a global talent pool.

22

MANAGEMENT’S DISCUSSION AND ANALYSIS

Ability to Develop and Expand Mix of Products and Services to Keep Pace with Demand and Technological Trends

NuRAN uses several means to remain on the cutting edge and to meet its customers’ changing needs—steady investments in product development and improvements, business alliances with major industry suppliers and partners, ongoing training of its personnel and occasional business acquisitions that provide it with specific know-how.

Protection of Intellectual Property

To protect its intellectual property, NuRAN relies on a series of patent and trademark laws, provisions respecting trade secrets, confidentiality protection measures, and various contracts. Regardless of all the efforts made to retain and protect its exclusive rights, third parties could attempt to copy aspects of its products or obtain information regarded as exclusive without authorization. There can be no assurance that the measures taken by NuRAN to protect its exclusive rights will be sufficient.

Dependence on Customers

NuRAN is currently dependent on a limited number of customers for the sale of its products and services. If one or several of these customers should cease doing business with NuRAN for any reason or should reduce or defer their current or planned product purchases, NuRAN’s operating results and financial position could be adversely affected.

International Operations Risk

Our international operations are subject to various economic, political and other uncertainties that could adversely affect our business. Since 2014, approximately 52% of our sales were derived from sales outside North America, and economic conditions in the countries and regions in which we operate significantly affect our profitability and growth prospects. The following risks, associated with doing business internationally, could adversely affect our business, financial condition and results of operations:

| ● | regional or country specific economic downturns; |

| ● | the capacity of the Company to deliver in a technical capacity and to import inventory at a reasonable cost; |

| ● | fluctuations in currency exchange rates; |

| ● | complications in complying with a variety of foreign laws and regulations, including with respect to environmental matters, which may adversely affect our operations and ability to compete effectively in certain jurisdictions or regions; |

| ● | international political and trade issues and tensions; |

| ● | unexpected changes in regulatory requirements, up to and including the risk of nationalization or expropriation by foreign governments; |

| ● | higher tax rates and potentially adverse tax consequences including restrictions on repatriating earnings, adverse tax withholding requirements and double taxation; |

23

MANAGEMENT’S DISCUSSION AND ANALYSIS

| ● | greater difficulties protecting our intellectual property; |

| ● | increased risk of litigation and other disputes with customers; |

| ● | fluctuations in our operating performance based on our geographic mix of sales; |

| ● | longer payment cycles and difficulty in collecting accounts receivable; |

| ● | costs and difficulties in integrating, staffing and managing international operations, especially in rapidly growing economies; |

| ● | transportation delays and interruptions; |

| ● | natural disasters and the greater difficulty in recovering from them in some of the foreign countries in which we operate; |

| ● | uncertainties arising from local business practices and cultural considerations; |

| ● | customs matter and changes in trade policy, tariff regulations or other trade restrictions; and |

| ● | national and international conflicts, including terrorist acts. |

The percentage of our sales occurring outside of North America will increase over time largely due to increased activity in Africa, Central and South America and other emerging markets. The foregoing risks may be particularly acute in emerging markets, where our operations are subject to greater uncertainty due to increased volatility associated with the developing nature of the economic, legal and governmental systems of these countries. If we are unable to successfully manage the risks associated with expanding our global business or to adequately manage operational fluctuations, it could adversely affect our business, financial condition or results of operations.

Gross Margin May Not Be Sustainable

Our level of product gross margins may be adversely affected by numerous factors, including:

| ● | Changes in customer, geographic, or product mix, including mix of configurations within each product group; |

| ● | Introduction of new products, including products with price-performance advantages; |

| ● | Our ability to reduce production costs; |

| ● | Entry into new markets or growth in lower margin markets, including markets with different pricing and cost structures, through acquisitions or internal development; |