Exhibit 99.1

Titan DFS Building a U.S. Supply Chain for Heavy Rare Earths, Titanium, Zirconium and

Hafnium A U.S. critical mineral-to-metals platform for defense, aerospace, nuclear, semiconductors, robotics and advanced manufacturing supply chains June 2026 IperionX LimitedNASDAQ and ASX: IPX

Disclaimers 2 Forward Looking Statements Information included in this release

constitutes forward-looking statements. Often, but not always, forward looking statements can generally be identified by the use of forward looking words such as “may”, “will”, “expect”, “intend”, “plan”, “estimate”, “anticipate”, “continue”,

and “guidance”, or other similar words and may include, without limitation, statements regarding plans, strategies and objectives of management, anticipated production or construction commencement dates and expected costs or production outputs.

Forward looking statements inherently involve known and unknown risks, uncertainties and other factors that may cause IperionX Limited’s (the “Company”) actual results, performance, and achievements to differ materially from any forecast

future results, performance or achievements. Relevant factors may include, but are not limited to, changes in commodity prices, foreign exchange fluctuations and general economic conditions, increased costs and demand for production inputs, the

speculative nature of exploration and project development, including the risks of obtaining necessary licenses and permits and diminishing quantities or grades of mineralization, the Company’s ability to comply with the relevant contractual

terms to access the technologies, commercially scale its closed-loop titanium production process, or protect its intellectual property rights, political and social risks, changes to the regulatory framework within which the company operates or

may in the future operate, environmental conditions including extreme weather conditions, recruitment and retention of personnel, industrial relations issues and litigation. Forward looking statements are based on the Company and its

management’s good faith assumptions relating to the financial, market, regulatory and other relevant environments that will exist and affect the Company’s business and operations in the future. The Company does not give any assurance that the

assumptions on which forward looking statements are based will prove to be correct, or that the Company’s business or operations will not be affected in any material manner by these or other factors not foreseen or foreseeable by the Company or

management or beyond the Company’s control. Although the Company attempts and has attempted to identify factors that would cause actual actions, events or results to differ materially from those disclosed in forward looking statements, there

may be other factors that could cause actual results, performance, achievements or events not to be as anticipated, estimated or intended, and many events are beyond the reasonable control of the Company. Accordingly, readers are cautioned not

to place undue reliance on forward looking statements. Forward looking statements in these materials speak only at the date of issue. Subject to any continuing obligations under applicable law or any relevant stock exchange listing rules, in

providing this information the company does not undertake any obligation to publicly update or revise any of the forward looking statements or to advise of any change in events, conditions or circumstances on which any such statement is

based. Cautionary Statements and Important Information This presentation has been prepared by the Company as a summary only and does not contain all information about assets and liabilities, financial position and performance, profits and

losses, prospects, and the rights and liabilities attaching to securities. Any investment in the Company should be considered speculative and there is no guarantee that they will make a return on capital invested, that dividends would be paid,

or that there will be an increase in the value of the investment in the future. The Company does not purport to give financial or investment advice. No account has been taken of the objectives, financial situation or needs of any recipient of

this presentation. Recipients of this presentation should carefully consider whether the securities issued by the Company are an appropriate investment for them in light of their personal circumstances, including their financial and taxation

position. Compliance Statement The information in this presentation that relates to the Ore Reserve estimate at the Titan Project is extracted from the Company's announcement titled "IperionX Titan DFS Confirms High-Return U.S. Rare Earths

and Critical Minerals Project" released to ASX on 4 June 2026 and which is available at www.asx.com.au. The Company confirms that it is not aware of any new information or data that materially affects the Ore Reserve estimate information

included in that original market announcement and confirms that all material assumptions and technical parameters underpinning the Ore Reserve estimate in that announcement continue to apply and have not materially changed. The Company confirms

that the form and context in which the findings of the Competent Person are presented have not been materially modified from the original market announcement. The Competent Person for the Ore Reserve estimate in that announcement was Mr. Justin

Douthat. The information in this presentation that relates to the Mineral Resource estimates at the Titan Project is extracted from the Company's announcement titled "IperionX Titan DFS Confirms High-Return U.S. Rare Earths and Critical

Minerals Project" released to ASX on 4 June 2026 and which is available at www.asx.com.au. The Company confirms that it is not aware of any new information or data that materially affects the Mineral Resource estimates information included in

that original market announcement and confirms that all material assumptions and technical parameters underpinning the Mineral Resource estimates in that announcement continue to apply and have not materially changed. The Company confirms that

the form and context in which the findings of the Competent Person are presented have not been materially modified from the original market announcement. The Competent Person for the Mineral Resources in that announcement was Mr. John

Eckman. The information in this Presentation that relates to the Company's production targets and financial forecasts for the Titan Project is extracted from the Company's ASX announcement titled "IperionX Titan DFS Confirms High-Return U.S.

Rare Earths and Critical Minerals Project" released to ASX on 4 June 2026 and which is available at www.asx.com.au. The Company confirms that all the material assumptions underpinning the production targets, and the forecast financial

information derived from the production targets, in that announcement continue to apply and have not materially changed. Not an offer in the United States This presentation does not constitute an offer to sell, or a solicitation of an offer

to buy, securities in the United States or any other jurisdiction. Any securities described in this presentation have not been, and will not be, registered under the US Securities Act of 1933 and may not be offered or sold in the United States

except in transactions exempt from, or not subject to, the registration requirements of the US Securities Act and applicable US state securities laws. This presentation has been authorized for release by the CEO and Managing

Director. IPERIONX LIMITED ABN 84 618 935 372

Why Titan Matters Strategic Minerals, Strong Economics, Shovel Ready 3

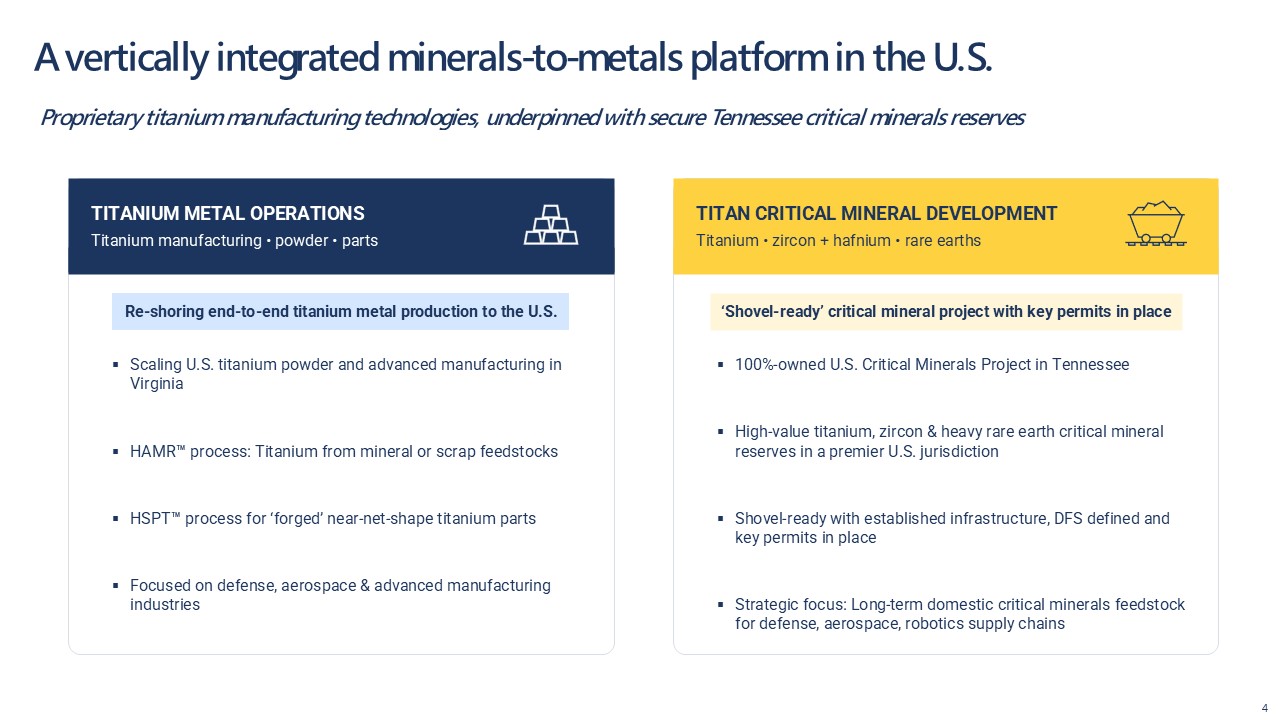

A vertically integrated minerals-to-metals platform in the U.S. 4 Proprietary titanium

manufacturing technologies, underpinned with secure Tennessee critical minerals reserves TITANIUM METAL OPERATIONS Titanium manufacturing • powder • parts Re-shoring end-to-end titanium metal production to the U.S. TITAN CRITICAL MINERAL

DEVELOPMENT Titanium • zircon + hafnium • rare earths ‘Shovel-ready’ critical mineral project with key permits in place Scaling U.S. titanium powder and advanced manufacturing in Virginia HAMR™ process: Titanium from mineral or scrap

feedstocks HSPT™ process for ‘forged’ near-net-shape titanium parts Focused on defense, aerospace & advanced manufacturing industries 100%-owned U.S. Critical Minerals Project in Tennessee High-value titanium, zircon & heavy rare

earth critical mineral reserves in a premier U.S. jurisdiction Shovel-ready with established infrastructure, DFS defined and key permits in place Strategic focus: Long-term domestic critical minerals feedstock for defense, aerospace, robotics

supply chains

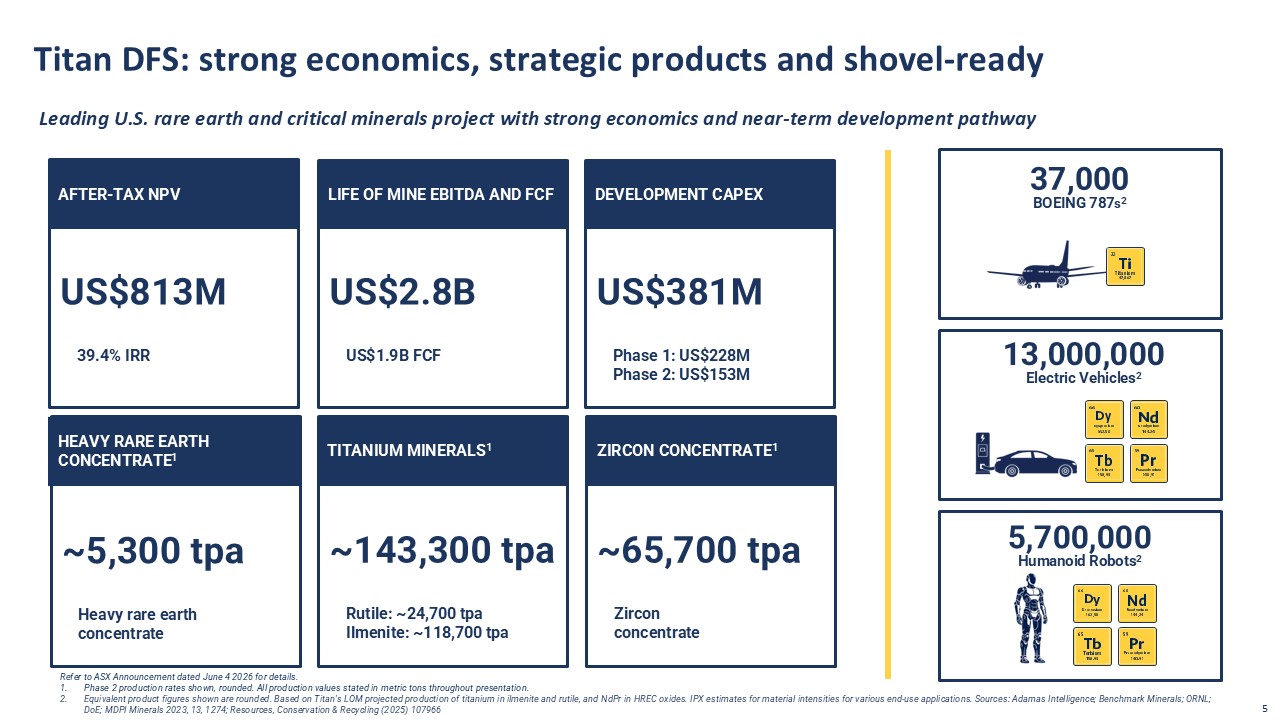

Titan DFS: strong economics, strategic products and shovel-ready 5 Leading U.S. rare

earth and critical minerals project with strong economics and near-term development pathway AFTER-TAX NPV DEVELOPMENT CAPEX LIFE OF MINE EBITDA AND FCF HEAVY RARE EARTH CONCENTRATE1 TITANIUM MINERALS1 ZIRCON

CONCENTRATE1 US$813M US$381M US$2.8B ~5,300 tpa ~143,300 tpa ~65,700 tpa 39.4% IRR Phase 1: US$228M Phase 2: US$153M US$1.9B FCF Heavy rare earth concentrate Rutile: ~24,700 tpa Ilmenite: ~118,700 tpa Zircon

concentrate 37,000 BOEING 787s2 13,000,000 Electric Vehicles2 5,700,000 Humanoid Robots2 Refer to ASX Announcement dated June 4 2026 for details. Phase 2 production rates shown, rounded. All production values stated in metric tons

throughout presentation. Equivalent product figures shown are rounded. Based on Titan’s LOM projected production of titanium in ilmenite and rutile, and NdPr in HREC oxides. IPX estimates for material intensities for various end-use

applications. Sources: Adamas Intelligence; Benchmark Minerals; ORNL; DoE; MDPI Minerals 2023, 13, 1274; Resources, Conservation & Recycling (2025) 107966

Four strategic material streams, one U.S. supply-chain platform Titan is a rare U.S.

critical minerals platform that can solve multiple supply chain chokepoints across defense, nuclear, semiconductors, AI infrastructure, robotics and advanced manufacturing Heavy rare earths Dysprosium • Terbium • Yttrium High-temperature

magnets, defense electronics, thermal-barriers, lasers and advanced sensors Light rare earths Neodymium • Praseodymium Permanent magnet foundation for motors, drones, robotics, EVs and precision actuation Zirconium + Hafnium Zirconium •

Hafnium Nuclear fuel systems, control rods, semiconductors, advanced ceramics, C103 alloys Titanium Titanium mineral feedstocks Defense, aerospace, naval, ground vehicle, robotics and advanced manufacturing metal pathways CORNERSTONE

PROJECT • FOUR STRATEGIC MATERIAL

STREAMS 22 Ti Titanium 47.867 60 Nd Neodymium 144.24 59 Pr Praseodymium 144.24 65 Tb Terbium 158.93 66 Dy Dysprosium 162.50 39 Y Yttrium 88.906 40 Zr Zirconium 91.22 72 Hf Hafnium 178.49 6

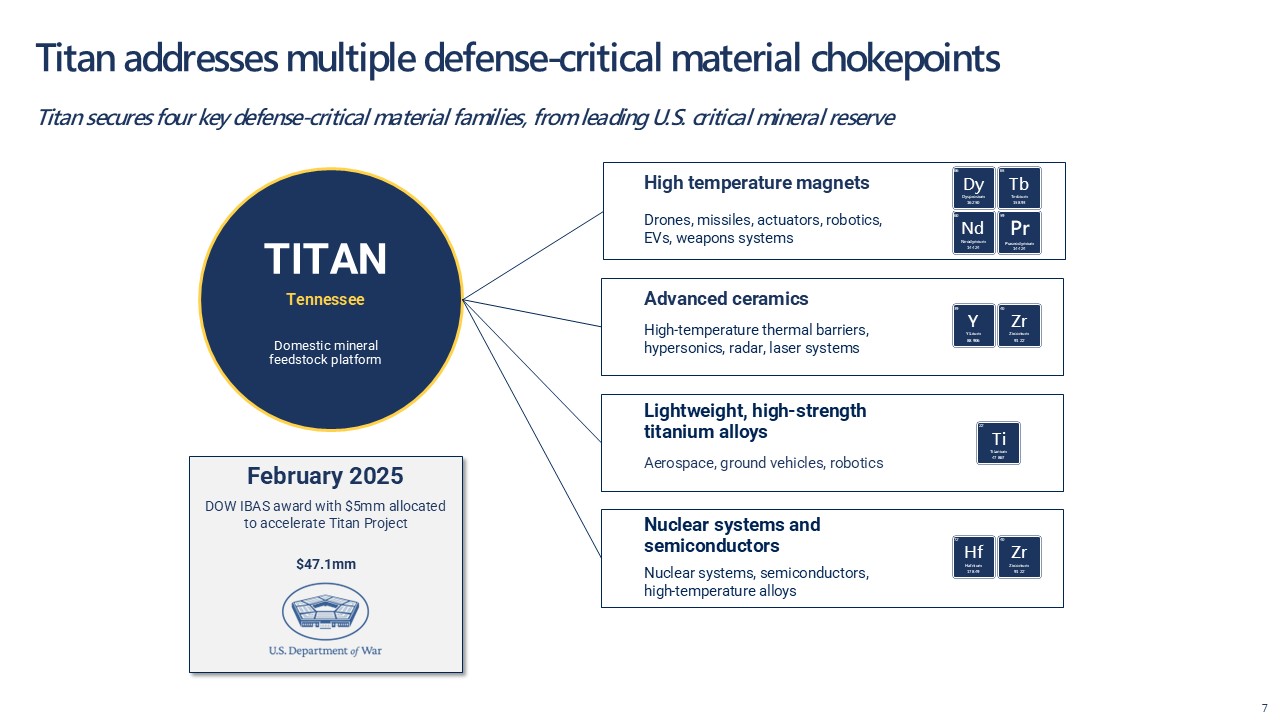

Titan addresses multiple defense-critical material chokepoints 7 High temperature

magnets Advanced ceramics Lightweight, high-strength titanium alloys Nuclear systems and semiconductors Drones, missiles, actuators, robotics, EVs, weapons systems High-temperature thermal barriers, hypersonics, radar, laser

systems Aerospace, ground vehicles, robotics Nuclear systems, semiconductors, high-temperature alloys Titan secures four key defense-critical material families, from leading U.S. critical mineral reserve TITAN Tennessee Domestic mineral

feedstock platform February 2025 DOW IBAS award with $5mm allocated to accelerate Titan

Project $47.1mm 22 Ti Titanium 47.867 60 Nd Neodymium 144.24 59 Pr Praseodymium 144.24 65 Tb Terbium 158.93 66 Dy Dysprosium 162.50 39 Y Yttrium 88.906 40 Zr Zirconium 91.22 72 Hf Hafnium 178.49 40 Zr Zirconium 91.22

With a suitable funding pathway, potential for a U.S. supply-chain solution

in 2028 Potential for Phase 1 production ramp-up to be complete by September 2028 1 H2 2026 Early works commence 2 Jan 2027 Construction commences 3 Jun 2028 Commission commences 4 Sep 2028 Ramp-up complete Titan is a

cornerstone for U.S. critical-mineral supply chain security Shovel ready U.S. critical mineral platform with key permits in place Robust economics US$813M NPV8 // 39.4% IRR // US$381M total capex High-value, critical products HREC for Dy +

Tb + Y + NdPr, titanium minerals, and zircon/Zr-Hf Key permits + execution path in place State Surface Mining and NPDES permits granted “Shovel-ready” path to 2028 production Potential for production ramp-up complete in September

2028 1 2 3 4 8

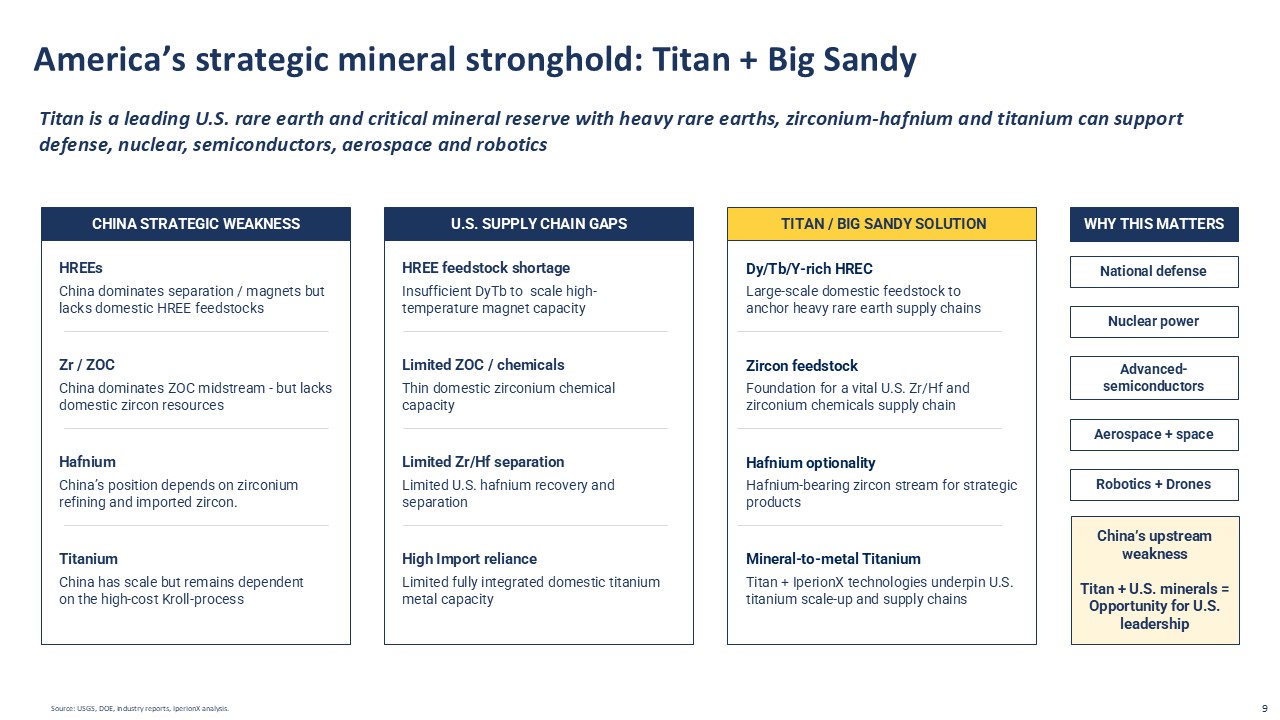

America’s strategic mineral stronghold: Titan + Big Sandy Source: USGS, DOE, industry

reports, IperionX analysis. 9 Titan is a leading U.S. rare earth and critical mineral reserve with heavy rare earths, zirconium-hafnium and titanium can support defense, nuclear, semiconductors, aerospace and robotics CHINA STRATEGIC

WEAKNESS HREEs China dominates separation / magnets but lacks domestic HREE feedstocks Zr / ZOC China dominates ZOC midstream - but lacks domestic zircon resources Hafnium China’s position depends on zirconium refining and imported

zircon. Titanium China has scale but remains dependent on the high-cost Kroll-process U.S. SUPPLY CHAIN GAPS HREE feedstock shortage Insufficient DyTb to scale high-temperature magnet capacity Limited ZOC / chemicals Thin domestic

zirconium chemical capacity Limited Zr/Hf separation Limited U.S. hafnium recovery and separation High Import reliance Limited fully integrated domestic titanium metal capacity WHY THIS MATTERS National defense Nuclear

power Advanced-semiconductors Aerospace + space Robotics + Drones China’s upstream weakness Titan + U.S. minerals = Opportunity for U.S. leadership TITAN / BIG SANDY SOLUTION Dy/Tb/Y-rich HREC Large-scale domestic feedstock to anchor

heavy rare earth supply chains Zircon feedstock Foundation for a vital U.S. Zr/Hf and zirconium chemicals supply chain Hafnium optionality Hafnium-bearing zircon stream for strategic products Mineral-to-metal Titanium Titan + IperionX

technologies underpin U.S. titanium scale-up and supply chains Dy/Tb/Y-rich HREC Zircon feedstock Hafnium optionality

10 Titan Products Critical Minerals for Key U.S. Supply Chains

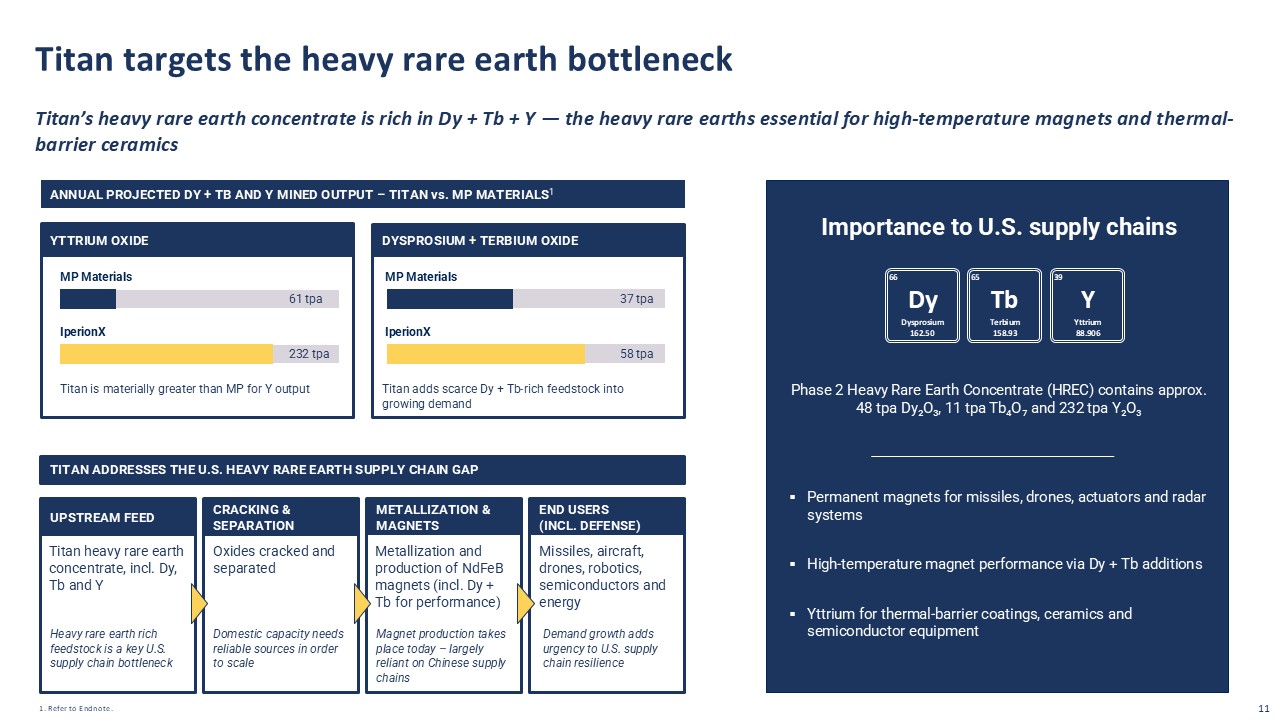

Titan targets the heavy rare earth bottleneck TITAN ADDRESSES THE U.S. HEAVY RARE EARTH

SUPPLY CHAIN GAP YTTRIUM OXIDE DYSPROSIUM + TERBIUM OXIDE ANNUAL PROJECTED DY + TB AND Y MINED OUTPUT – TITAN vs. MP MATERIALS1 MP Materials IperionX MP Materials IperionX 61 tpa 232 tpa 37 tpa 58 tpa Titan is materially greater

than MP for Y output Titan adds scarce Dy + Tb-rich feedstock into growing demand Importance to U.S. supply chains Phase 2 Heavy Rare Earth Concentrate (HREC) contains approx. 48 tpa Dy₂O₃, 11 tpa Tb₄O₇ and 232 tpa Y₂O₃ Permanent magnets

for missiles, drones, actuators and radar systems High-temperature magnet performance via Dy + Tb additions Yttrium for thermal-barrier coatings, ceramics and semiconductor equipment 1. Refer to Endnote. 11 Titan’s heavy rare earth

concentrate is rich in Dy + Tb + Y — the heavy rare earths essential for high-temperature magnets and thermal-barrier ceramics UPSTREAM FEED CRACKING & SEPARATION METALLIZATION & MAGNETS Titan heavy rare earth concentrate, incl. Dy,

Tb and Y Heavy rare earth rich feedstock is a key U.S. supply chain bottleneck END USERS (INCL. DEFENSE) Oxides cracked and separated Metallization and production of NdFeB magnets (incl. Dy + Tb for performance) Missiles, aircraft,

drones, robotics, semiconductors and energy Domestic capacity needs reliable sources in order to scale Magnet production takes place today – largely reliant on Chinese supply chains Demand growth adds urgency to U.S. supply chain

resilience UPSTREAM FEED 65 Tb Terbium 158.93 66 Dy Dysprosium 162.50 39 Y Yttrium 88.906

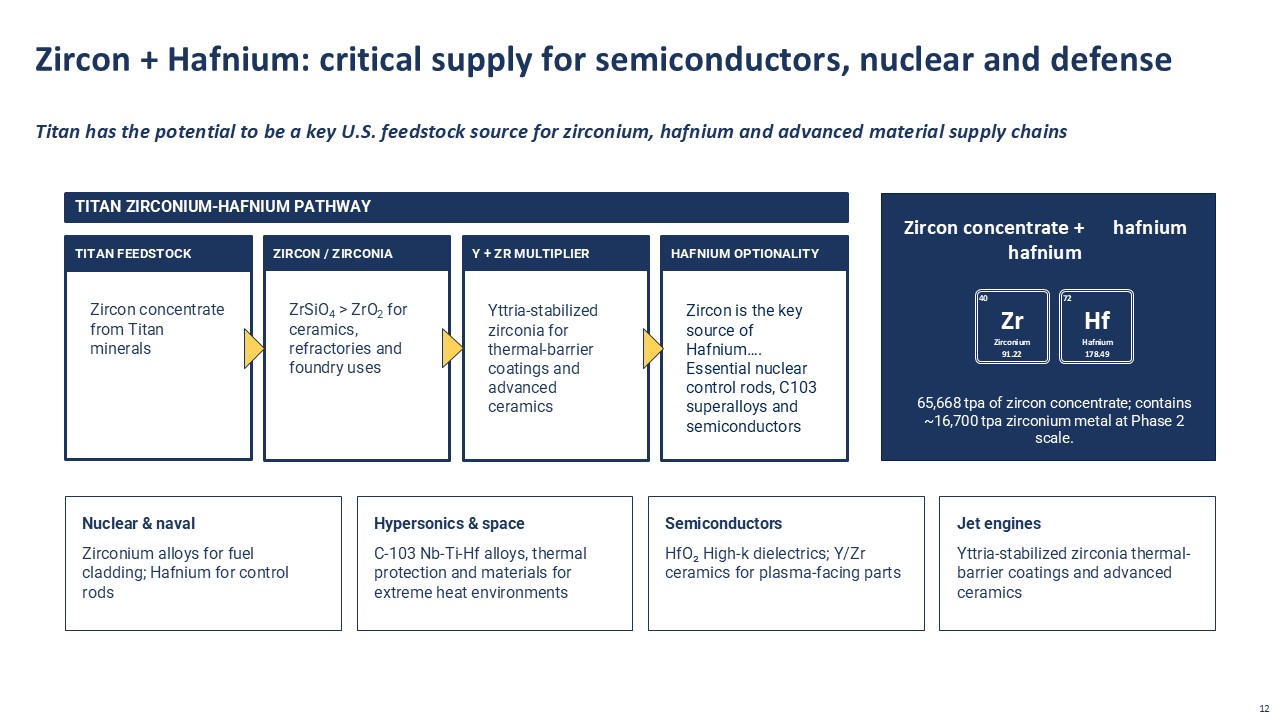

Zircon + Hafnium: critical supply for semiconductors, nuclear and defense 12 Zircon

concentrate + hafnium 65,668 tpa of zircon concentrate; contains ~16,700 tpa zirconium metal at Phase 2 scale. TITAN FEEDSTOCK ZIRCON / ZIRCONIA Y + ZR MULTIPLIER Zircon concentrate from Titan minerals TITAN ZIRCONIUM-HAFNIUM

PATHWAY HAFNIUM OPTIONALITY ZrSiO4 > ZrO2 for ceramics, refractories and foundry uses Yttria-stabilized zirconia for thermal-barrier coatings and advanced ceramics Zircon is the key source of Hafnium…. Essential nuclear control rods,

C103 superalloys and semiconductors Nuclear & naval Zirconium alloys for fuel cladding; Hafnium for control rods Hypersonics & space C-103 Nb-Ti-Hf alloys, thermal protection and materials for extreme heat

environments Semiconductors HfO₂ High-k dielectrics; Y/Zr ceramics for plasma-facing parts Jet engines Yttria-stabilized zirconia thermal-barrier coatings and advanced ceramics Titan has the potential to be a key U.S. feedstock source for

zirconium, hafnium and advanced material supply chains 40 Zr Zirconium 91.22 72 Hf Hafnium 178.49

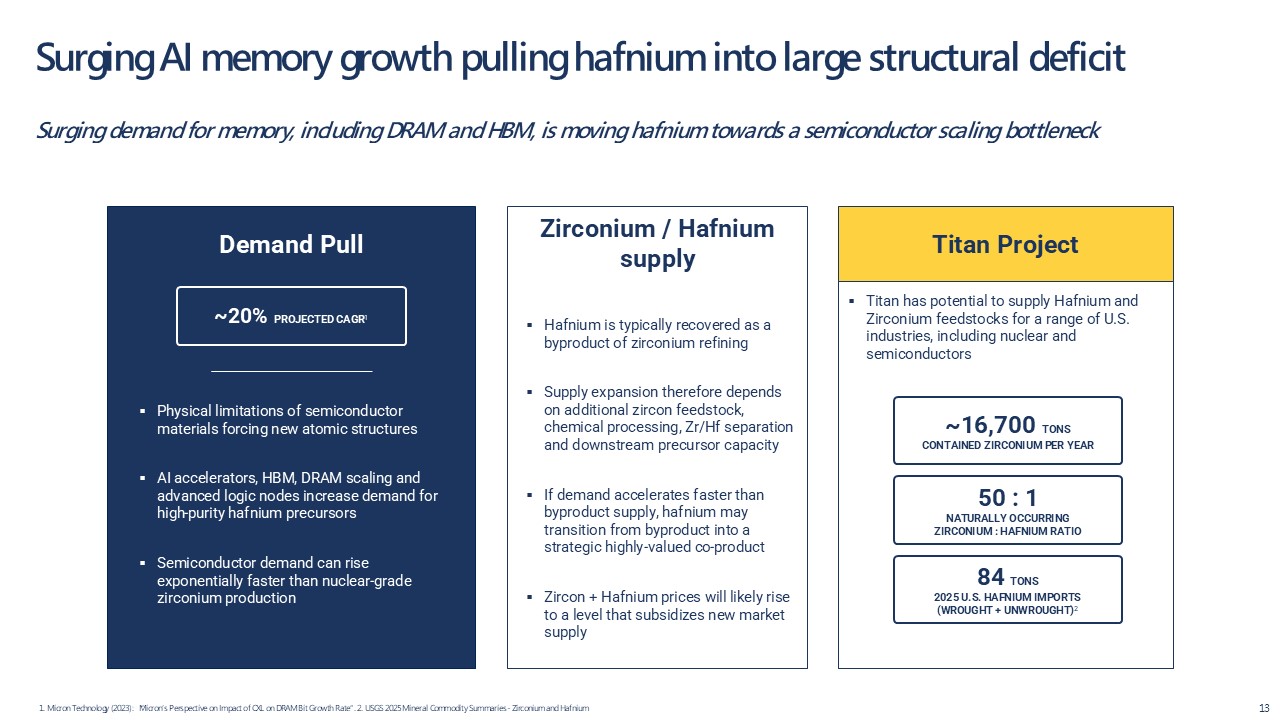

Surging AI memory growth pulling hafnium into large structural deficit 1. Micron

Technology (2023): “Micron’s Perspective on Impact of CXL on DRAM Bit Growth Rate”. 2. USGS 2025 Mineral Commodity Summaries - Zirconium and Hafnium 13 Surging demand for memory, including DRAM and HBM, is moving hafnium towards a

semiconductor scaling bottleneck Demand Pull ~20% PROJECTED CAGR1 Physical limitations of semiconductor materials forcing new atomic structures AI accelerators, HBM, DRAM scaling and advanced logic nodes increase demand for high-purity

hafnium precursors Semiconductor demand can rise exponentially faster than nuclear-grade zirconium production Zirconium / Hafnium supply Hafnium is typically recovered as a byproduct of zirconium refining Supply expansion therefore depends

on additional zircon feedstock, chemical processing, Zr/Hf separation and downstream precursor capacity If demand accelerates faster than byproduct supply, hafnium may transition from byproduct into a strategic highly-valued co-product Zircon

+ Hafnium prices will likely rise to a level that subsidizes new market supply Titan Project Titan has potential to supply Hafnium and Zirconium feedstocks for a range of U.S. industries, including nuclear and semiconductors ~16,700 TONS

CONTAINED ZIRCONIUM PER YEAR 50 : 1 NATURALLY OCCURRING ZIRCONIUM : HAFNIUM RATIO 84 TONS 2025 U.S. HAFNIUM IMPORTS (WROUGHT + UNWROUGHT)2

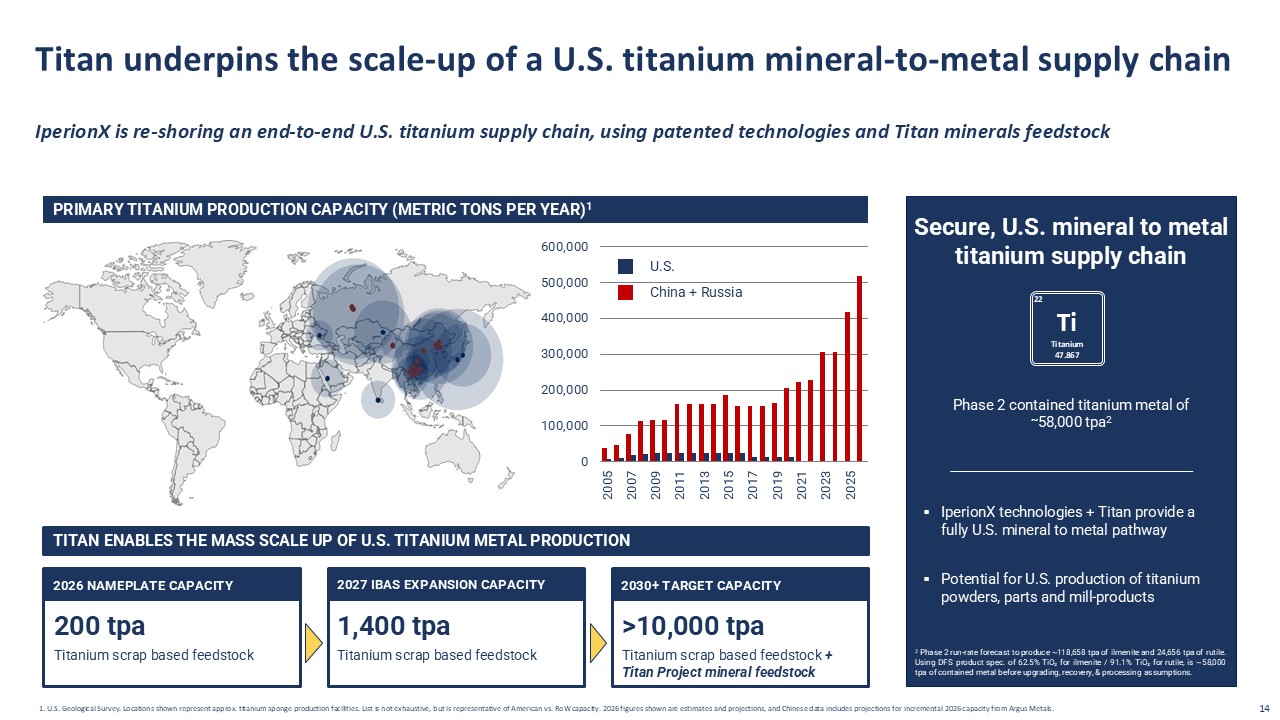

1. U.S. Geological Survey. Locations shown represent approx. titanium sponge production

facilities. List is not exhaustive, but is representative of American vs. RoW capacity. 2026 figures shown are estimates and projections, and Chinese data includes projections for incremental 2026 capacity from Argus Metals. 14 Secure, U.S.

mineral to metal titanium supply chain Phase 2 contained titanium metal of ~58,000 tpa2 IperionX technologies + Titan provide a fully U.S. mineral to metal pathway Potential for U.S. production of titanium powders, parts and

mill-products U.S. China + Russia PRIMARY TITANIUM PRODUCTION CAPACITY (METRIC TONS PER YEAR)1 2026 NAMEPLATE CAPACITY 2027 IBAS EXPANSION CAPACITY TITAN ENABLES THE MASS SCALE UP OF U.S. TITANIUM METAL PRODUCTION 2030+ TARGET

CAPACITY 200 tpa Titanium scrap based feedstock 1,400 tpa Titanium scrap based feedstock >10,000 tpa Titanium scrap based feedstock + Titan Project mineral feedstock IperionX is re-shoring an end-to-end U.S. titanium supply chain,

using patented technologies and Titan minerals feedstock Titan underpins the scale-up of a U.S. titanium mineral-to-metal supply chain 2 Phase 2 run-rate forecast to produce ~118,658 tpa of ilmenite and 24,656 tpa of rutile. Using DFS product

spec. of 62.5% TiO₂ for ilmenite / 91.1% TiO₂ for rutile, is ~58,000 tpa of contained metal before upgrading, recovery, & processing assumptions. 22 Ti Titanium 47.867

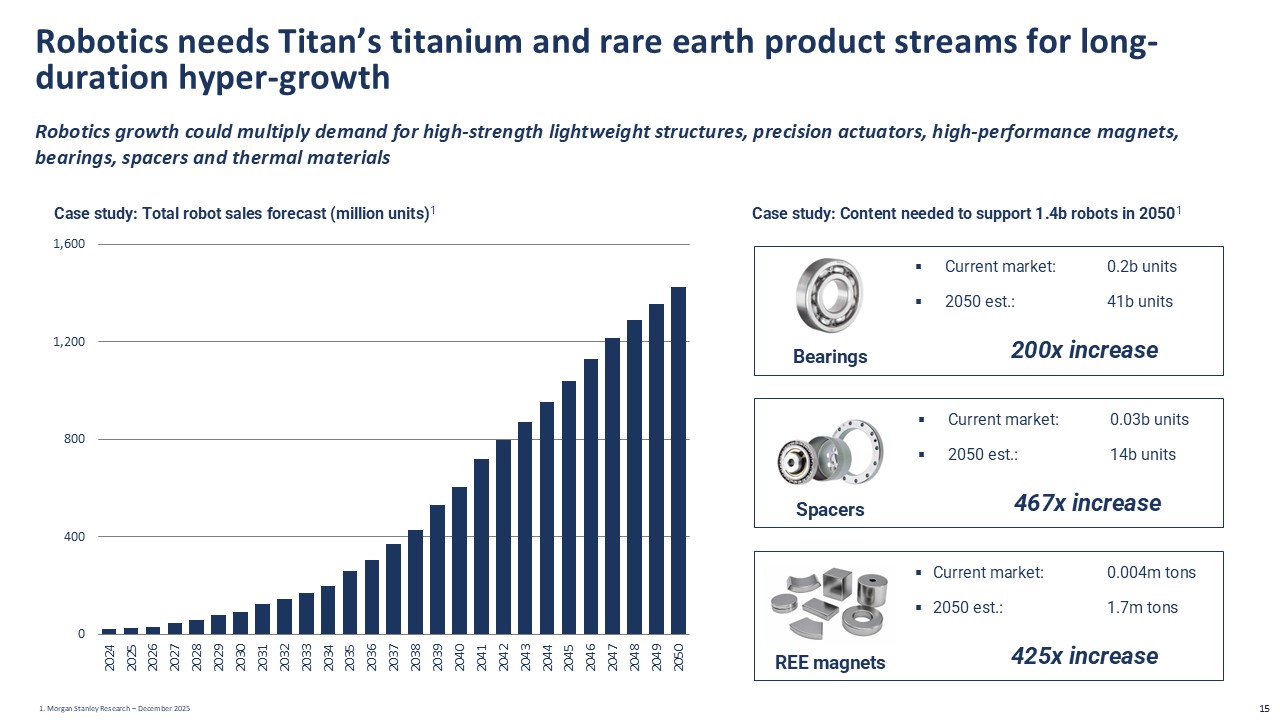

Case study: Total robot sales forecast (million units)1 Case study: Content needed to

support 1.4b robots in 20501 Bearings Spacers REE magnets Current market: 0.2b units 2050 est.: 41b units 200x increase Current market: 0.03b units 2050 est.: 14b units 467x increase Current market: 0.004m tons 2050 est.: 1.7m

tons 425x increase 1. Morgan Stanley Research – December 2025 15 Robotics needs Titan’s titanium and rare earth product streams for long-duration hyper-growth Robotics growth could multiply demand for high-strength lightweight

structures, precision actuators, high-performance magnets, bearings, spacers and thermal materials

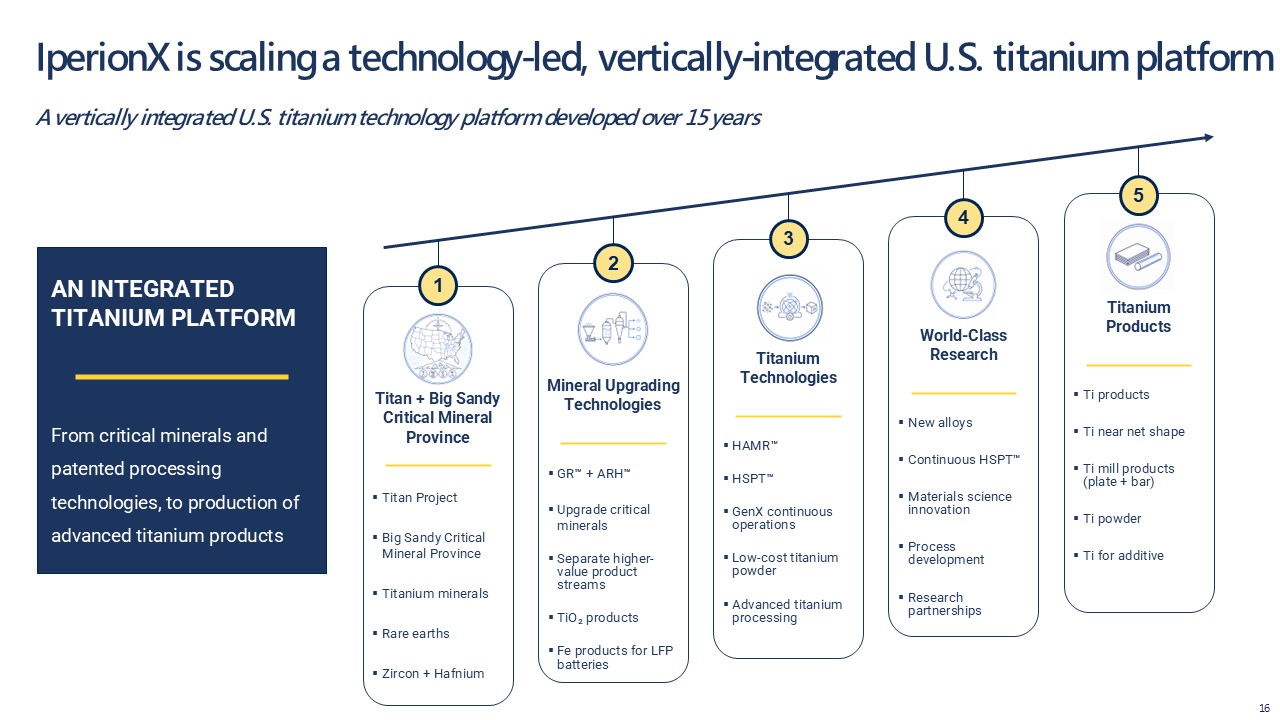

IperionX is scaling a technology-led, vertically-integrated U.S. titanium platform A

vertically integrated U.S. titanium technology platform developed over 15 years 16 AN INTEGRATED TITANIUM PLATFORM From critical minerals and patented processing technologies, to production of advanced titanium

products 1 2 3 4 5 Titan + Big Sandy Critical Mineral Province Titan Project Big Sandy Critical Mineral Province Titanium minerals Rare earths Zircon + Hafnium Mineral Upgrading Technologies GR™ + ARH™ Upgrade critical

minerals Separate higher-value product streams TiO₂ products Fe products for LFP batteries Titanium

Technologies HAMR™ HSPT™ GenX continuous operations Low-cost titanium powder Advanced titanium processing World-Class

Research New alloys Continuous HSPT™ Materials science innovation Process development Research partnerships Titanium

Products Ti products Ti near net shape Ti mill products (plate + bar) Ti powder Ti for additive

Appendix 17

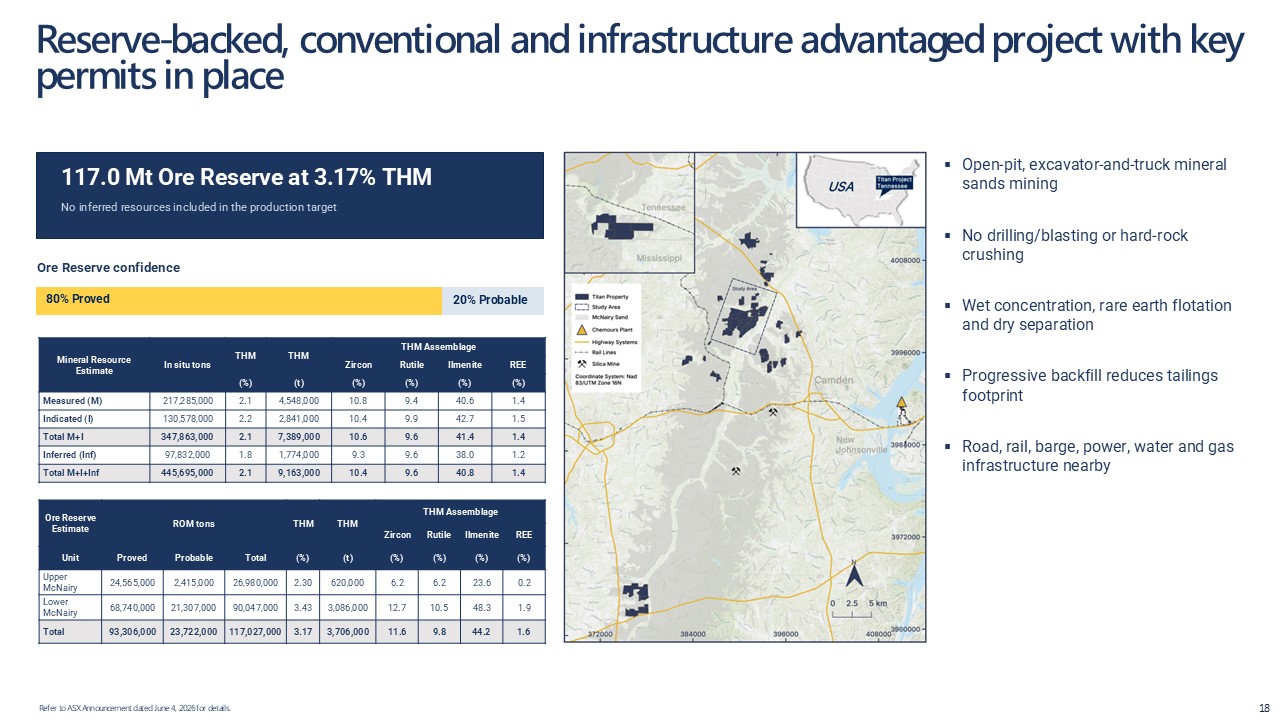

Reserve-backed, conventional and infrastructure advantaged project with key permits in

place Refer to ASX Announcement dated June 4, 2026 for details. 18 117.0 Mt Ore Reserve at 3.17% THM No inferred resources included in the production target Ore Reserve confidence 80% Proved 20% Probable Open-pit, excavator-and-truck

mineral sands mining No drilling/blasting or hard-rock crushing Wet concentration, rare earth flotation and dry separation Progressive backfill reduces tailings footprint Road, rail, barge, power, water and gas infrastructure

nearby Mineral Resource Estimate In situ tons THM THM THM Assemblage Zircon Rutile Ilmenite REE (%) (t) (%) (%) (%) (%) Measured (M) 217,285,000 2.1 4,548,000 10.8 9.4 40.6 1.4 Indicated

(I) 130,578,000 2.2 2,841,000 10.4 9.9 42.7 1.5 Total M+I 347,863,000 2.1 7,389,000 10.6 9.6 41.4 1.4 Inferred (Inf) 97,832,000 1.8 1,774,000 9.3 9.6 38.0 1.2 Total

M+I+Inf 445,695,000 2.1 9,163,000 10.4 9.6 40.8 1.4 Ore Reserve

Estimate ROM tons THM THM THM Assemblage Zircon Rutile Ilmenite REE Unit Proved Probable Total (%) (t) (%) (%) (%) (%) Upper McNairy 24,565,000 2,415,000 26,980,000 2.30 620,000 6.2 6.2 23.6 0.2 Lower

McNairy 68,740,000 21,307,000 90,047,000 3.43 3,086,000 12.7 10.5 48.3 1.9 Total 93,306,000 23,722,000 117,027,000 3.17 3,706,000 11.6 9.8 44.2 1.6

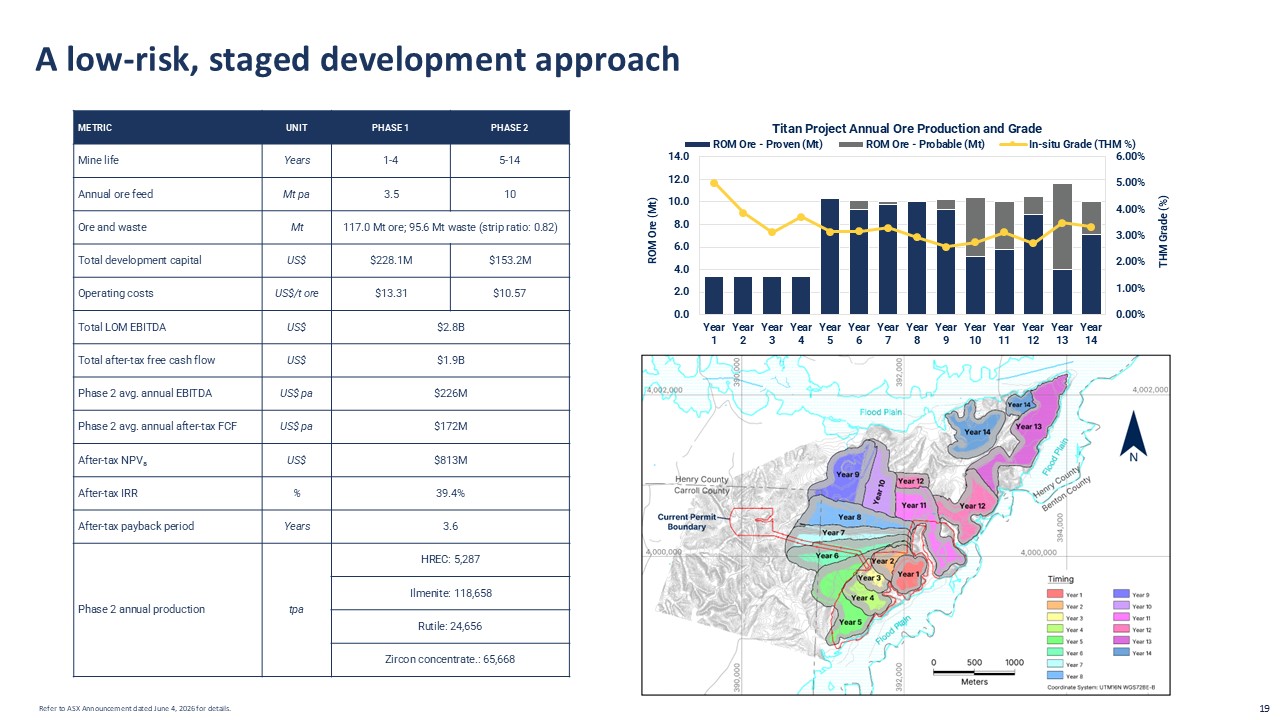

A low-risk, staged development approach Refer to ASX Announcement dated June 4, 2026 for

details. 19 METRIC UNIT PHASE 1 PHASE 2 Mine life Years 1-4 5-14 Annual ore feed Mt pa 3.5 10 Ore and waste Mt 117.0 Mt ore; 95.6 Mt waste (strip ratio: 0.82) Total development capital US$ $228.1M $153.2M Operating

costs US$/t ore $13.31 $10.57 Total LOM EBITDA US$ $2.8B Total after-tax free cash flow US$ $1.9B Phase 2 avg. annual EBITDA US$ pa $226M Phase 2 avg. annual after-tax FCF US$ pa $172M After-tax NPV₈ US$ $813M After-tax

IRR % 39.4% After-tax payback period Years 3.6 Phase 2 annual production tpa HREC: 5,287 Ilmenite: 118,658 Rutile: 24,656 Zircon concentrate.: 65,668

Industry standard flowsheet: wet concentration followed by mineral separation Refer to

ASX Announcement dated June 4, 2026 for details. 20 Wet Concentrator plant site layout Mineral separation plant site layout

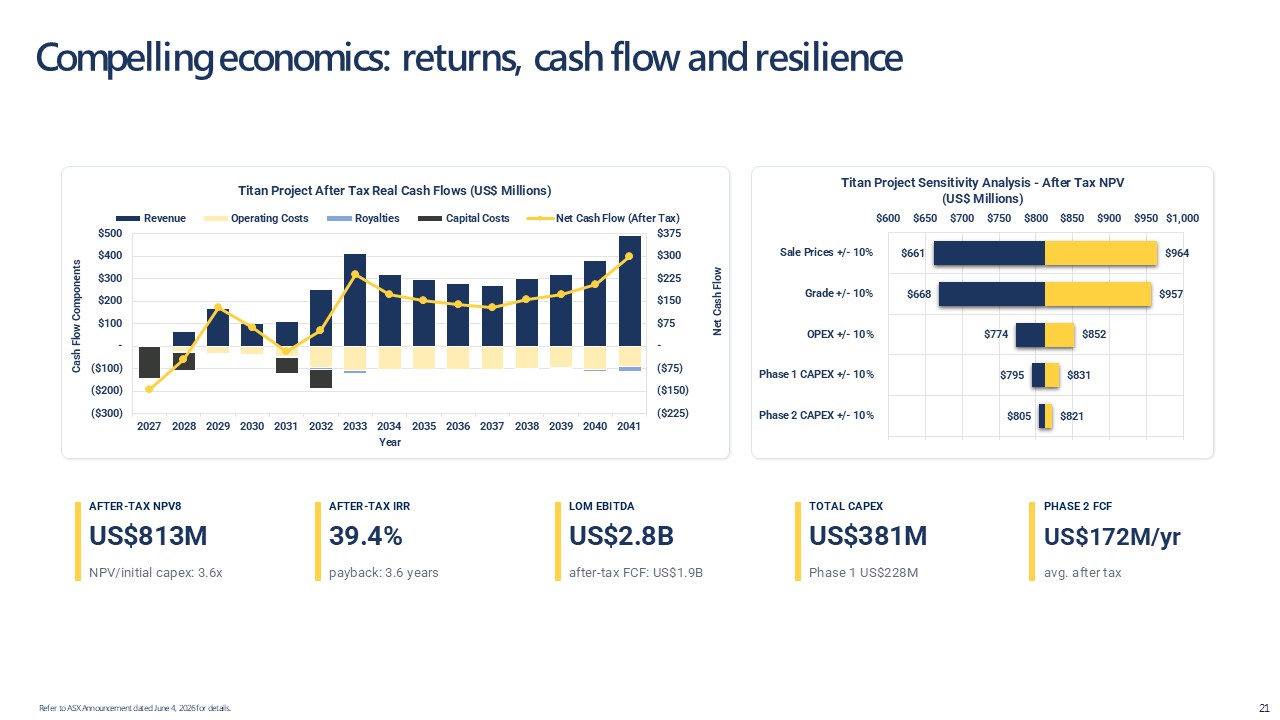

Compelling economics: returns, cash flow and resilience Refer to ASX Announcement dated

June 4, 2026 for details. 21 AFTER-TAX NPV8 US$813M NPV/initial capex: 3.6x AFTER-TAX IRR 39.4% payback: 3.6 years LOM EBITDA US$2.8B after-tax FCF: US$1.9B TOTAL CAPEX US$381M Phase 1 US$228M PHASE 2 FCF US$172M/yr avg. after

tax

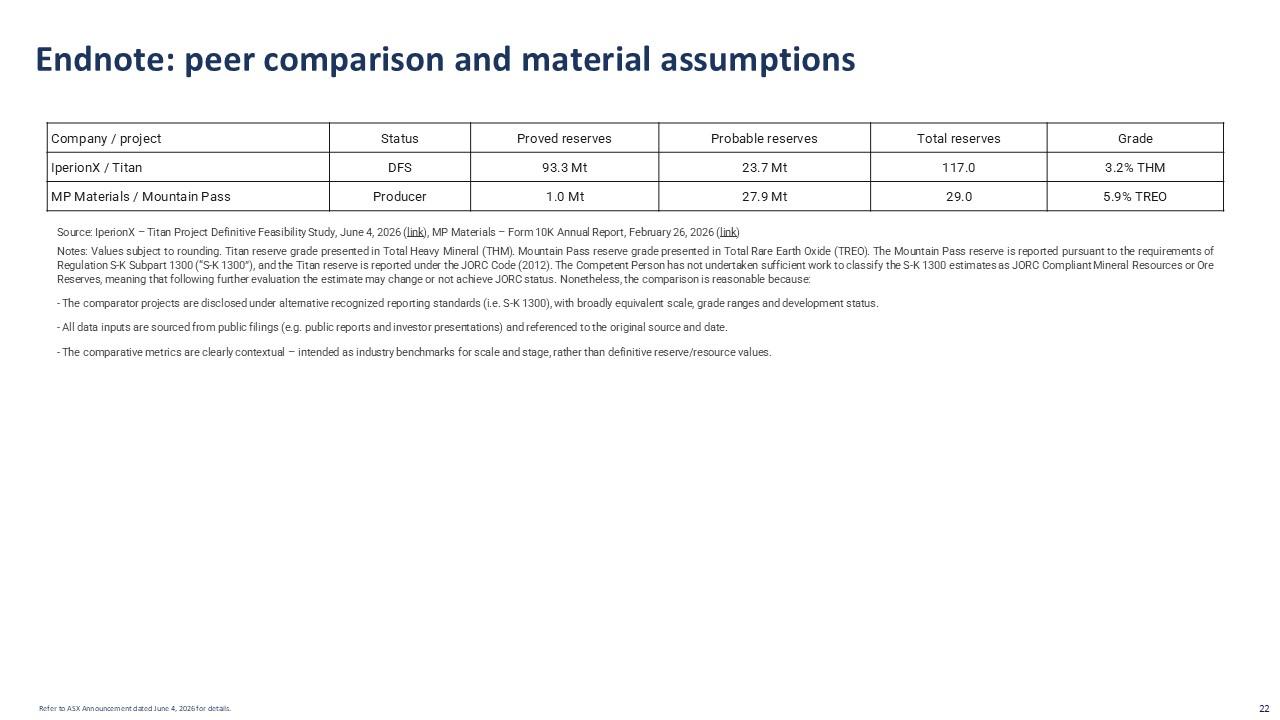

Endnote: peer comparison and material assumptions Refer to ASX Announcement dated June 4,

2026 for details. 22 Source: IperionX – Titan Project Definitive Feasibility Study, June 4, 2026 (link), MP Materials – Form 10K Annual Report, February 26, 2026 (link) Notes: Values subject to rounding. Titan reserve grade presented in

Total Heavy Mineral (THM). Mountain Pass reserve grade presented in Total Rare Earth Oxide (TREO). The Mountain Pass reserve is reported pursuant to the requirements of Regulation S-K Subpart 1300 (“S-K 1300”), and the Titan reserve is reported

under the JORC Code (2012). The Competent Person has not undertaken sufficient work to classify the S-K 1300 estimates as JORC Compliant Mineral Resources or Ore Reserves, meaning that following further evaluation the estimate may change or not

achieve JORC status. Nonetheless, the comparison is reasonable because: - The comparator projects are disclosed under alternative recognized reporting standards (i.e. S-K 1300), with broadly equivalent scale, grade ranges and development

status. - All data inputs are sourced from public filings (e.g. public reports and investor presentations) and referenced to the original source and date. - The comparative metrics are clearly contextual – intended as industry benchmarks for

scale and stage, rather than definitive reserve/resource values. Company / project Status Proved reserves Probable reserves Total reserves Grade IperionX / Titan DFS 93.3 Mt 23.7 Mt 117.0 3.2% THM MP Materials / Mountain

Pass Producer 1.0 Mt 27.9 Mt 29.0 5.9% TREO