Exhibit 99.1

UNSN 2026-2

Unison Midgard Holdings LLC

Opus Capital Markets Consultants, LLC

5718 Westheimer Road – Suite 1000 | Houston, TX 77057 | www.opuscmc.com | 224.632.1300

| Page 1 of 14 |

Executive Narrative

June 8, 2026

Performed by

Opus Capital Markets Consultants, LLC

For

Unison Midgard Holdings LLC

This report summarizes the results of a due diligence review performed on three hundred fifty-six (356) Home Equity Investment (“HEI”) loans provided by Unison Midgard Holdings LLC (“Client”). The Client provided Opus Capital Markets Consultants, LLC (the “Consultant”) with a data tape consisting of one thousand two hundred ninety-four (1,294) loans. From this population, three hundred seventy-seven (377) loans, representing 29.13% of the total pool, were randomly selected by Opus and loaded into the LauraMac underwriting software. Twenty-one (21) loans were removed from the final population.

The scope of review completed by Opus is identified as Exhibit A below.

EXHIBIT A

Opus Capital Markets Consultants, LLC

STATEMENT OF WORK

DUE DILIGENCE SERVICES

The sample selected for the review described in this scope will be selected randomly by Opus and will represent at least 18.50% (by current intrinsic value) of the statistical portfolio.

| a. | Underwriting Review |

Opus will review the sample to determine whether each option meets the underwriting and investment criteria, as applicable for the selected option, in effect at the time of such option’s origination, and that adequate support for the underwriting decision was contained in the related option file. The investment guidelines and calculation notes are attached as Exhibit 2. For avoidance of doubt, the following underwriting criteria will be reviewed to determine adherence to the investment guidelines:

| i. | Program | |

| ii. | Maximum Investment Size ($) | |

| iii. | Maximum Price Appreciation (Max Investor Percentage) | |

| iv. | Maximum Investment as % of Property | |

| v. | Maximum Term | |

| vi. | Minimum Pricing | |

| vii. | Property Type / Exclusions | |

| viii. | Home Inspection Present (if applicable) | |

| ix. | Appraisal Present |

| Page 2 of 14 |

| x. | Income/Asset Verification Present | |

| xi. | Property Condition | |

| xii. | Debt Limit (CLTV) - allowing for a 1% degree of freedom | |

| xiii. | Minimum Homeowner Equity | |

| xiv. | Max # of Units | |

| xv. | Minimum FICO Score | |

| xvi. | Residency Requirements | |

| xvii. | Minimum Floor and Buyout Blackout | |

| xviii. | Property Approval | |

| xix. | Lien Restriction | |

| xx. | Title Restriction |

For avoidance of doubt, the following underwriting criteria contained in the investment guidelines in Exhibit 2 will not be reviewed:

| i. | Minimum Canada US FICO Score | |

| ii. | Metro Concentration Limit | |

| iii. | Minimum Mortgage Maturity | |

| iv. | Country Limit | |

| v. | Non-owner Occupied Limit | |

| vi. | Individual Owner Exposure |

b. Regulatory and Compliance Review

Opus will review the contract files to verify whether all contract approval conditions, origination requirements and disclosures required by the underwriter were satisfied and the information contained in the closing documents, including the application, senior mortgage statements (if applicable), credit report and settlement statement, is consistent with the underwriting decision and final terms of such option. For avoidance of doubt, the following files will be reviewed to confirm their existence and consistency with the data tape provided:

| i. | 1008 (applicable to HomeBuyer) | |

| ii. | Application |

| i. | The applicant can be found as its own document or in the Offer Package |

| iii. | Senior Mortgage Statements (applicable to New HomeOwner and HomeOwner) |

| iv. | Credit Report |

| v. | Home Inspection Present (if applicable) |

| vi. | Appraisal Present |

| vii. | Hazard Insurance (if applicable) |

| i. | As of May 2021, proof of hazard insurance was no longer required |

| viii. | Income/Asset Verification Present |

| i. | If applicable, the asset statement only needs to show the financial institution, balance and applicant name. Not every page of the statement is required. |

| ix. | Settlement Statement |

| i. | For HomeBuyer, a Closing Disclosure can be accepted in lieu of a Settlement Statement |

| x. | Signed Offer Letter |

| Page 3 of 14 |

| i. | HomeBuyer deals used a Conditional Approval Package (CAP) in lieu of an Offer Package |

| ii. | While some Addendums and Schedule of Debts may be included in an Offer Package, they were not required to be executed with the Offer Package (required only during Closing) |

| xi. | Signed Conditions of Offer |

| i. | HomeBuyer deals used a Conditional Approval Package (CAP) in lieu of an Offer Package |

| xii. | Signed Important Information Notice and Total Unison Cost Estimate (TUCE) (applicable to New HomeOwner and HomeOwner) |

| xiii. | Executed Funding Package |

| xiv. | Recorded Memorandum |

| xv. | Recorded Security Instrument |

| xvi. | Recorded Assignment(s) (Only applicable for assets where Initial Investment Fund Number = 4) |

c. Insurance Review

Opus will review the contract files to verify that all required insurance was in place at origination and conformed to the underwriting guidelines. For avoidance of doubt, this includes confirming:

| i. | Hazard insurance was in force at the time of origination for each property prior to May 2021 |

| ii. | Flood insurance is present for all properties where any part of the structure is located in a Special Flood Hazard Area (SFHA) |

d. Origination Appraisal Review

Opus will review the appraisal conducted at the time of origination to verify:

| i. | The subject property address is correct |

| ii. | All subject buildings included in the collateral are included in the appraisal |

| iii. | The property condition rating is acceptable |

Note that if there are multiple appraisals provided, information from the most recent appraisal will be used to determine property conditions and property types.

e. Data Tape Review

Opus will verify, validate and recalculate (if applicable) the following data tape fields:

| i. | Program name | |

| ii. | Qualifying FICO at origination |

| Page 4 of 14 |

| iii. | Original investment price | |

| iv. | Original agreed value | |

| v. | Property value at origination | |

| vi. | Debt limit (CLTV) | |

| vii. | Pricing ratio | |

| viii. | Investor percentage | |

| ix. | Effective date | |

| x. | Expiration date | |

| xi. | Term | |

| xii. | Repurchase lockout | |

| xiii. | Homeowner equity at origination | |

| xiv. | CBSA | |

| xv. | State | |

| xvi. | Occupancy status | |

| xvii. | Property type | |

| xviii. | Property condition | |

| xix. | Number of units | |

| xx. | AVM | |

| xxi. | Current intrinsic value | |

| xxii. | Initial Investment Fund Number |

f. Tax and Title Review

Client will order a title search. Opus will confirm Unison has a lien position and ensure unreleased prior liens and delinquent taxes prior to Unison’s effective date has been resolved. Any lien added post effective date can be accepted.

g. Intrinsic Value Review

Opus will review the AVMs used in Unison’s proprietary valuation approach to recalculate the intrinsic value of each option contract.

| Page 5 of 14 |

Exhibit 1

Guidelines and Calculations

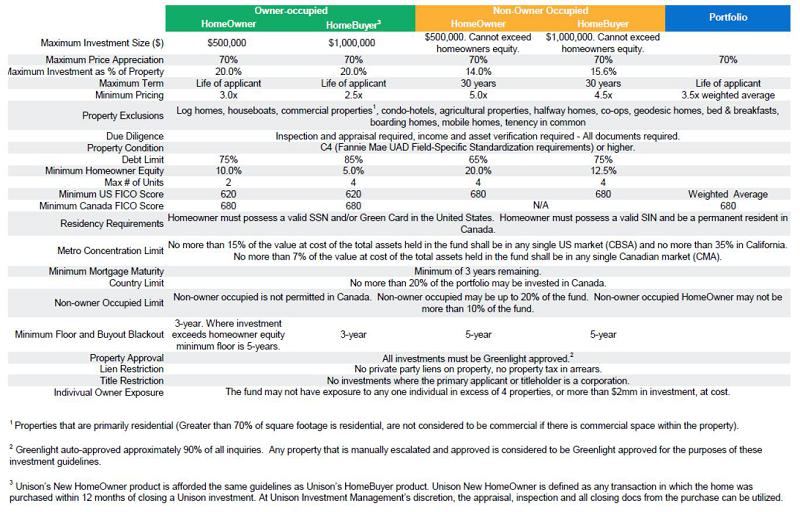

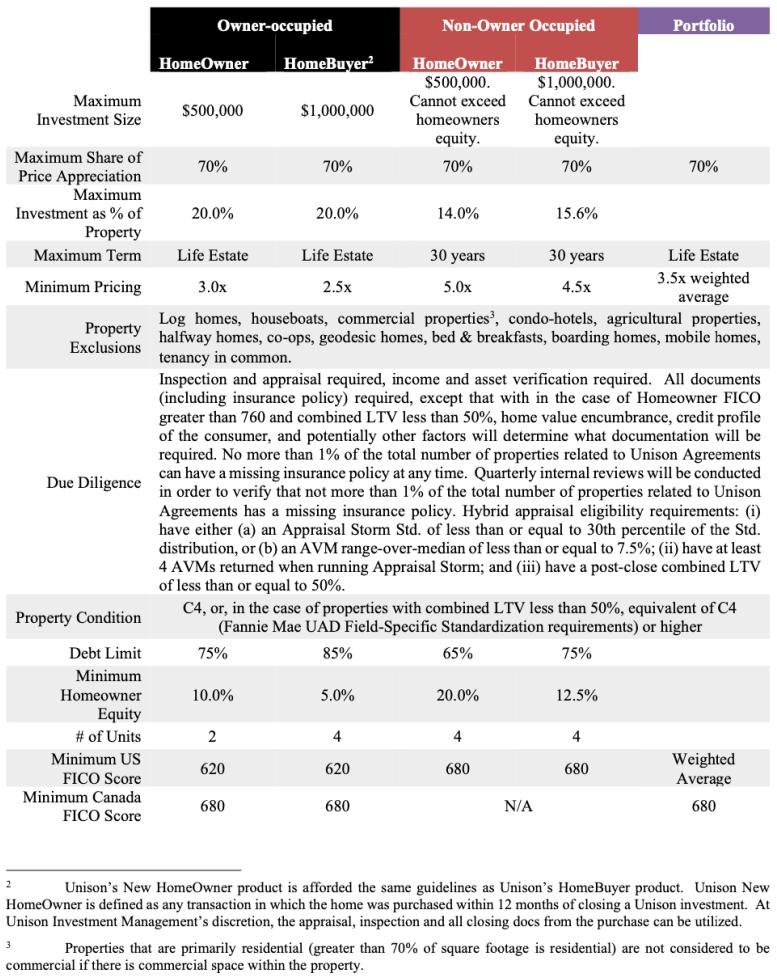

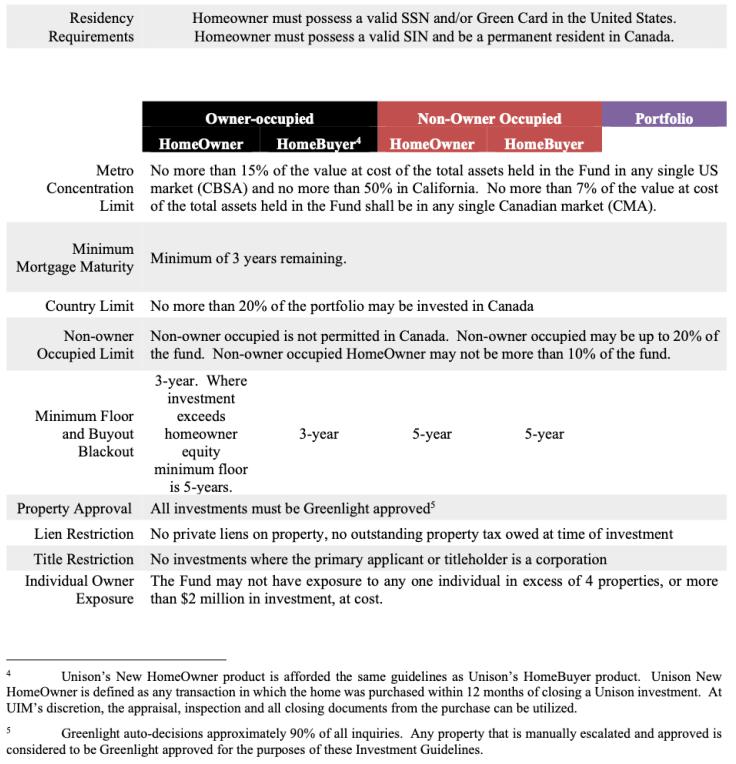

| a. | Investor Guidelines (April 2019 – April 2022) |

| Page 6 of 14 |

| b. | Investor Guidelines (May 2022 – December 2022) |

| Page 7 of 14 |

| Page 8 of 14 |

| c. | Additional Notes and Calculations |

HomeOwner + New HomeOwner

| ● | Debt Limit = Combined Loan to Value (CLTV) |

| ○ | CLTV = (Sum of all post close senior lien balances) / Property Value at Origination) |

| ○ | CLTV specifically refers to Post Close Combined Loan to Value |

| ○ | Please allow for a 1% degree of freedom |

| ○ | Sum of all post close senior lien balances accounts for all payoffs and paydowns |

| ■ | The mortgage/lien paydown or payoff amount can be identified on the schedule of debts in the funding package provided. Please verify the creditor and account numbers on the schedule of debts matches the credit report or mortgage statement to ensure the paydown is for the subject property. |

| ■ | Unison’s investment must not be included in the CLTV calculation |

| ○ | The mortgage used to calculate the sum of all post close senior lien balances uses the lower value between mortgage balance on the credit report and the mortgage balance from the mortgage statement. Exceptions include: |

| ■ | A mortgage statement may be used if a deferred balance is present on the mortgage statement. In which case the deferred balance must be added to the mortgage balance. |

| ■ | A closing disclosure may be used if the mortgage was recently (within the last 6 months) refinanced or newly originated |

| ■ | A credit supplement may be used if the mortgage has existed for more than 6 months but did not appear on the initial credit report |

| ○ | To verify that a mortgage is for the subject property, match the mortgage origination month and original balance on the credit report to the corresponding fields on the title report. Note that only mortgages for the subject property can count towards the sum of all post close senior lien balances |

| ■ | The origination month may differ by roughly +-2 months due to recording delays |

| ■ | There may be some variation in the origination balance on the title report and the original balance on the credit report if the credit report identifies “purchase money first” |

| ■ | The current balance must be used in CLTV calculation, not the original balance at the Option origination |

| ○ | If a line of credit (HELOC) is available for the subject property, the full credit limit will be included in the sum of all post close senior lien balances |

| ○ | Any liens on the title report prior to the effective date must count towards sum of all post close senior lien balances unless it was paid off |

| ○ | The property value at origination is determined by the appraised value in the appraisal |

| ■ | Some assets may have multiple appraisals, in which case the property value at origination is set as the average of the appraised values |

| ■ | If an OAV addendum is present in the closing documents, it will take precedence and determine the property value at origination |

| ○ | Example: |

| ■ | Property Value at Origination: $1,000,000 |

| ■ | Mortgage Balance: $800,000 |

| ■ | Mortgage Paydown Amount: $50,000 |

| ■ | CLTV = ($800,000 - $50,000) / $1,000,000 = 75% |

| ● | Qualifying FICO (April 2019 - April 2020) |

| ○ | 1 Applicant: qualifying FICO is the median FICO in the credit report |

| ○ | 2 Applicants: qualifying FICO is the lower median of the 2 applicants |

| ■ | If one applicant’s median FICO is lower than 620, use the other applicant’s median FICO |

| Page 9 of 14 |

| ■ | If an applicant’s income was not provided, their FICO was not required |

| ○ | If an applicant only has 2 FICOs on their credit report, use the lower FICO |

| ● | Qualifying FICO (May 2020 - December 2022) |

| ○ | 1 Applicant: qualifying FICO is the median FICO in the credit report |

| ○ | 2 Applicants: qualifying FICO is the higher median of the 2 applicants |

| ■ | If an applicant’s income was not provided, their FICO was not required |

| ○ | If an applicant only has 2 FICOs on their credit report, use the lower FICO |

| ● | Recorded Assignments |

| ○ | Only applicable for assets where Initial Investment Fund Number = 4 |

| ○ | Assets where Initial Investment Fund Number = 100 do not require recorded assignments |

| ● | Home Inspections |

| ○ | Home inspections were not required beginning May 2021 for assets that met the following criteria: |

| ■ | Appraisal condition of C3 or greater |

| ■ | Property type is a PUD, condominium, or townhouse |

| ■ | Property has an effective year built in, or after, 1980 |

HomeBuyer

| ● | Debt Limit = Combined Loan to Value (CLTV) |

| ○ | CLTV = (Sum of all post close senior lien balances) / Property Value at Origination) |

| ○ | CLTV specifically refers to Post Close Combined Loan to Value |

| ○ | Please allow for a 1% degree of freedom |

| ○ | The mortgage amount used to calculate the sum of all post close senior lien balances can be found in Form 1008 or Form 1004 |

| ○ | The property value at origination is determined by the sale price found in Form 1008 or Form 1003 |

| ■ | If applicable, the seller concession (also referred to as seller subsidy or credit to buyer) or temporary rent will be subtracted from the sale price to determine property value at origination |

| ● | The seller concession can be found in the purchase agreement, residential sale contract, or final settlement statement from the escrow company |

| ■ | If the sale price listed on Form 1008 or Form 1003 is less than the appraised value, the appraised value will be set as the property value at origination |

| ■ | The mortgage lien at Unison origination will not be on the Credit Report at the time of origination |

| ● | Qualifying FICO |

| ○ | Qualifying FICO is stated on Form 1008 or Form 1003 in the “Representative Credit/Indicator Score” field |

| ○ | A credit report is not required |

Intrinsic Value

| ● | Intrinsic Value = (Current AVM - Original Agreed Value) * Investor Percentage + OIP |

| ○ | Beginning October 2020, Original Agreed Value = Property Value at Origination * 97.5% |

Investment as Percent of Property

| ● | Investment Percent of Property = (OIP / Property Value at Origination) * 100 |

Investor Percentage

| ● | Investor Percentage = Investment as Percent of Property * Pricing Ratio |

HomeOwner Equity

| ● | HomeOwner Equity = 100 - (CLTV% + Investment as Percent of Property) |

| Page 10 of 14 |

Program Floor

| ● | Investment as Percent of Property ≥ HomeOwner Equity = 5 years |

| ● | Investment as Percent of Property < HomeOwner Equity = 3 years |

Property Type

| ● | Found in the appraisal report provided |

| ● | Mobile Home / Manufactured Home may be accepted if the appraisal meets the following criteria: |

| ○ | Property Rights Appraised: Fee Simple |

| ○ | Units = 1 |

| ○ | Type = Detached |

Occupancy Status

| ● | Found in the Application, under “Property will be:”, “Property Use”, or “Occupancy Status” |

| ● | Also confirmed via the Appraisal, under “Occupant” |

Residency Status

| ● | SSN can be found in the credit report provided |

| d. | Updated Guidelines |

| a. | Updated Guidelines as of 2/15/2023 |

| i. | The risk adjustment increased from 2.5% to 5% |

| ii. | No buyout restriction during program floor |

| iii. | Original Appraised Property Value (OAPV) as Program Floor Basis |

| 1. | At minimum, payout to Unison will be based on the appraised value at origination. Previously, it was based on the discounted value of the original appraisal. |

| iv. | Equity Appreciation limit implemented |

| 1. | Maximum Appreciation Factor - 20% |

| b. | Updated guidelines as of 2/27/2023 |

| i. | Home inspections only needed to be ordered for properties in C4 condition, not a Condo or PUD, and built before 1980. |

| c. | Updated guidelines as of 6/6/2023 |

| i. | Digital home inspections eliminated for all deals that went to PDD on or after this date. All deals required a traditional home inspection. |

| ii. | Origination fee increased from 3% to 3.9% |

| iii. | Max Investor Percentage changed from 70% to 60% |

| d. | Update guidelines as of 12/1/2025 |

| i. | Updated Document Collections policy allowing only one paystub if qualifying with base salary only |

| e. | Updated guidelines as of 3/7/2026 |

| i. | PACE liens are not eligible senior liens |

| f. | Updated guidelines as of 4/22/2026 |

| i. | Deferred balances from forbearance no longer required to be paid off |

| g. | Updated guidelines as of 4/27/2026 |

| i. | No longer allow investment properties |

| Page 11 of 14 |

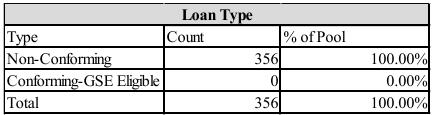

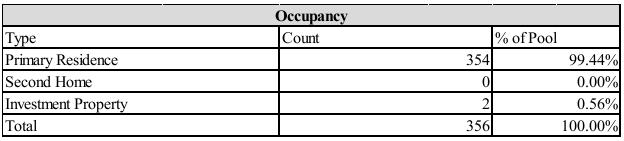

Sampling Information

Tape Discrepancies

Title Lien Review

Pool Details

| Page 12 of 14 |

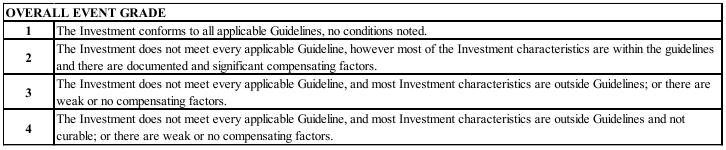

Option Grading Definitions

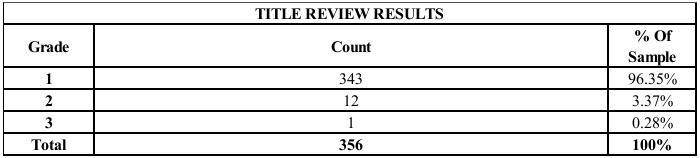

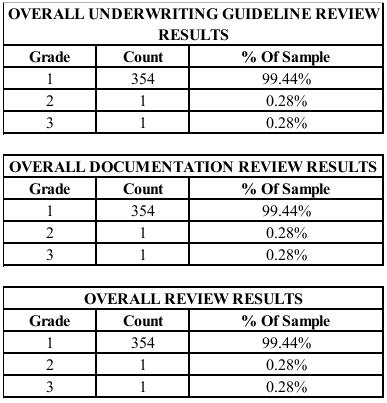

Option Review Findings

After completing a credit underwriting and valuation review of the 356 Home Equity Investments, 354 Investments had a rating grade of “1”, 1 Investment had a rating grade of “2”, 1 Investment had a rating grade of a “3.

| Page 13 of 14 |

Option Reviewed (356)

| FRX-501487 | FRX-470657 | FRX-454880 | FRX-438329 | FRX-422141 | FRX-404898 | FRX-386655 | FRX-228318 |

| FRX-500809 | FRX-469978 | FRX-454326 | FRX-438082 | FRX-422065 | FRX-404485 | FRX-386361 | FRX-228124 |

| FRX-499234 | FRX-469123 | FRX-453717 | FRX-436290 | FRX-421705 | FRX-404042 | FRX-385831 | FRX-226621 |

| FRX-499064 | FRX-468663 | FRX-453674 | FRX-435962 | FRX-421544 | FRX-403578 | FRX-385271 | FRX-226609 |

| FRX-498823 | FRX-468450 | FRX-453164 | FRX-435639 | FRX-421239 | FRX-403402 | FRX-385156 | FRX-226223 |

| FRX-498503 | FRX-468368 | FRX-453150 | FRX-434771 | FRX-421121 | FRX-403379 | FRX-385081 | FRX-225416 |

| FRX-497889 | FRX-468363 | FRX-452895 | FRX-434713 | FRX-420930 | FRX-402011 | FRX-384925 | FRX-222041 |

| FRX-497748 | FRX-467956 | FRX-452359 | FRX-434610 | FRX-420870 | FRX-401354 | FRX-384720 | FRX-221121 |

| FRX-497686 | FRX-467933 | FRX-452066 | FRX-434182 | FRX-420713 | FRX-401308 | FRX-384659 | FRX-217009 |

| FRX-496643 | FRX-467206 | FRX-451073 | FRX-433963 | FRX-419703 | FRX-400446 | FRX-379299 | FRX-186391 |

| FRX-496273 | FRX-466892 | FRX-450654 | FRX-433616 | FRX-418308 | FRX-400298 | FRX-378727 | FRX-181877 |

| FRX-494537 | FRX-466835 | FRX-449841 | FRX-433213 | FRX-417199 | FRX-399281 | FRX-305049 | FRX-181130 |

| FRX-494452 | FRX-466744 | FRX-449765 | FRX-433036 | FRX-416490 | FRX-398664 | FRX-288832 | FRX-180466 |

| FRX-494366 | FRX-466459 | FRX-449711 | FRX-432964 | FRX-416311 | FRX-398660 | FRX-285697 | FRX-177881 |

| FRX-493803 | FRX-466230 | FRX-449316 | FRX-432845 | FRX-415589 | FRX-398619 | FRX-280882 | FRX-177316 |

| FRX-489311 | FRX-466207 | FRX-448325 | FRX-432589 | FRX-414995 | FRX-398135 | FRX-280709 | FRX-177186 |

| FRX-488956 | FRX-466055 | FRX-447967 | FRX-432213 | FRX-414579 | FRX-397662 | FRX-280128 | FRX-175452 |

| FRX-488076 | FRX-465973 | FRX-447554 | FRX-432146 | FRX-414466 | FRX-397392 | FRX-280062 | FRX-175235 |

| FRX-487866 | FRX-465865 | FRX-446993 | FRX-431713 | FRX-414420 | FRX-397370 | FRX-278650 | FRX-173999 |

| FRX-486386 | FRX-465659 | FRX-446179 | FRX-431592 | FRX-414195 | FRX-397232 | FRX-272820 | FRX-173005 |

| FRX-486377 | FRX-465549 | FRX-446163 | FRX-431333 | FRX-413971 | FRX-397013 | FRX-271120 | FRX-172700 |

| FRX-486126 | FRX-465500 | FRX-446151 | FRX-431306 | FRX-413081 | FRX-396768 | FRX-270789 | FRX-171060 |

| FRX-486027 | FRX-465492 | FRX-445998 | FRX-430805 | FRX-413076 | FRX-396149 | FRX-270641 | FRX-168751 |

| FRX-484276 | FRX-465313 | FRX-445885 | FRX-430021 | FRX-413041 | FRX-395813 | FRX-268715 | FRX-167256 |

| FRX-483885 | FRX-465257 | FRX-445776 | FRX-429096 | FRX-412961 | FRX-395482 | FRX-263714 | FRX-166963 |

| FRX-483844 | FRX-465088 | FRX-445682 | FRX-428845 | FRX-412553 | FRX-395071 | FRX-258475 | FRX-164944 |

| FRX-483698 | FRX-464417 | FRX-445660 | FRX-428682 | FRX-412491 | FRX-394373 | FRX-257952 | FRX-161061 |

| FRX-483100 | FRX-464375 | FRX-445528 | FRX-428595 | FRX-411790 | FRX-393662 | FRX-256622 | FRX-158294 |

| FRX-482679 | FRX-462884 | FRX-445183 | FRX-428593 | FRX-410317 | FRX-392674 | FRX-256342 | FRX-157966 |

| FRX-481866 | FRX-462058 | FRX-444858 | FRX-428468 | FRX-410064 | FRX-392572 | FRX-254112 | FRX-156917 |

| FRX-481338 | FRX-461372 | FRX-444054 | FRX-427804 | FRX-409988 | FRX-391967 | FRX-253682 | FRX-156159 |

| FRX-481253 | FRX-461315 | FRX-444000 | FRX-427673 | FRX-409425 | FRX-391476 | FRX-253275 | FRX-153578 |

| FRX-480496 | FRX-461290 | FRX-443029 | FRX-426123 | FRX-409103 | FRX-391306 | FRX-249667 | FRX-151695 |

| FRX-480250 | FRX-460943 | FRX-442764 | FRX-425891 | FRX-408447 | FRX-390995 | FRX-247732 | FRX-149752 |

| FRX-478790 | FRX-460512 | FRX-441797 | FRX-425710 | FRX-407772 | FRX-390989 | FRX-244288 | FRX-144830 |

| FRX-478521 | FRX-460263 | FRX-441794 | FRX-425624 | FRX-407059 | FRX-389956 | FRX-241565 | FRX-137845 |

| FRX-477028 | FRX-459856 | FRX-441762 | FRX-425399 | FRX-406425 | FRX-389524 | FRX-241162 | FRX-137662 |

| FRX-476844 | FRX-458738 | FRX-440198 | FRX-424616 | FRX-406261 | FRX-389333 | FRX-236061 | FRX-128073 |

| FRX-476792 | FRX-457530 | FRX-440175 | FRX-424377 | FRX-406027 | FRX-388581 | FRX-234208 | FRX-121664 |

| FRX-475790 | FRX-457444 | FRX-440030 | FRX-424237 | FRX-405851 | FRX-388569 | FRX-233941 | FRX-114775 |

| FRX-475100 | FRX-457247 | FRX-439713 | FRX-424012 | FRX-405685 | FRX-388536 | FRX-233487 | FRX-114278 |

| FRX-473542 | FRX-456870 | FRX-439448 | FRX-423748 | FRX-405592 | FRX-388330 | FRX-233367 | |

| FRX-473486 | FRX-455743 | FRX-438899 | FRX-422958 | FRX-405544 | FRX-387322 | FRX-228670 | |

| FRX-473310 | FRX-455342 | FRX-438350 | FRX-422388 | FRX-405402 | FRX-386700 | FRX-228343 | |

| FRX-401097 | FRX-440592 | FRX-465157 | FRX-051803 | FRX-066430 | FRX-084175 | FRX-100657 |

If you have any questions, please contact Uriah Clavier at Uriah.Clavier@opuscmc.com.

| Page 14 of 14 |