Exhibit 99.1

Investor Presentation June 2026 Vertically Integrated Rare Earth Platform Securing the Global Critical Minerals Supply Chain MKANGO RARE EARTHS LIMITED

This Presentation includes information relating to the proposed business combination between Mkango Rare Earths Limited ("MKAR" or the "Company") and Crown Proptech Acquisitions ("SPAC"), pursuant to a Business Combination Agreement, dated as of July 2, 2025 (as amended, the "Business Combination Agreement") between MKAR, SPAC and the other parties thereto (the "Proposed Business Combination"). MKAR has filed with the SEC a registration statement on Form F-4 relating to the Proposed Business Combination (the "Registration Statement") that includes a proxy statement/prospectus. By reviewing or reading this Presentation, you will be deemed to have acknowledged and agreed to the statements, obligations and restrictions set out below. In addition, this Presentation and any oral statements made in connection with this Presentation shall neither constitute an offer to sell or the solicitation of an offer to buy any securities, nor shall there be any sale of securities in any jurisdiction in which the offer, solicitation or sale would be unlawful prior to the registration qualification or use of a prospectus under the securities laws of any such jurisdiction. This Presentation and any oral statements made in connection with this Presentation do not constitute the solicitation of any proxy, vote, consent or approval in any jurisdiction in connection with the Proposed Business Combination or any related transactions in any jurisdiction where, or to any person to whom, such solicitation may be unlawful under the laws of such jurisdiction. This Presentation does not constitute either advice or a recommendation regarding any securities. No representations or warranties, express or implied are given in, or in respect of, this Presentation. To the fullest extent permitted by law, in no circumstances will MKAR or SPAC, or any of their respective subsidiaries, stockholders, affiliates, representatives, partners, directors, officers, employees, advisers or agents be responsible or liable for any direct, indirect or consequential loss or loss of profit arising from the use of this Presentation, its contents (including the internal economic models), its omissions, reliance on the information contained within it, or on opinions communicated in relation thereto or otherwise arising in connection therewith. Neither MKAR nor SPAC has independently verified the data obtained from these sources and cannot assure you of the data's accuracy or completeness. Recipients of this Presentation are not to construe its contents, or any prior or subsequent communications from or with MKAR or SPAC, or their respective representatives as investment, legal or tax advice. In addition, this Presentation does not purport to be all-inclusive or to contain all of the information that may be required to make a full analysis of MKAR or SPAC or the Proposed Business Combination. Recipients of this Presentation should each make their own evaluation of MKAR, SPAC, and the Proposed Business Combination and of the relevance and adequacy of the information and should make such other investigations as they deem necessary. This Presentation is based on the economic, regulatory, market and other conditions as in effect on the date hereof. Consequently, the information and data presented herein is subject to change. It should be understood that subsequent developments may affect the information contained in this Presentation, and none of MKAR, SPAC, nor any of their respective directors, officers, partners, employees, affiliates, agents, advisors or representatives undertakes any obligation to update, revise or affirm the contents hereof. This Presentation expresses current intentions only. The Presentation and the information contained in it do not constitute an offer capable of acceptance or intended to otherwise give rise to a binding contract. The Presentation and the information contained in it do not constitute a commitment to place any financing or securities in relation to the Proposed Business Combination. INVESTMENT IN ANY SECURITIES DESCRIBED HEREIN HAS NOT BEEN APPROVED OR DISAPPROVED BY THE SEC OR ANY OTHER REGULATORY AUTHORITY IN ANY JURISDICTION NOR HAS ANY AUTHORITY IN ANY JURISDICTION PASSED UPON OR ENDORSED THE MERITS OF THE OFFERING OR THE ACCURACY OR ADEQUACY OF THE INFORMATION CONTAINED HEREIN. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE. This Presentation does not constitute or form part of, and should not be construed as, an offer or invitation to subscribe for, underwrite or otherwise acquire any securities, nor should it or any part of it form the basis of, or be relied on in connection with, any contract to purchase or subscribe for any securities, nor shall it or any part of it form the basis of or be relied on in connection with any contract or commitment whatsoever. Information for Recipients Outside the United States In Canada, this Presentation is only addressed to and directed at (i) "permitted clients" as defined in Section 1.1 of National Instrument 31-103 Registration Requirements, Exemptions and Ongoing Registrant Relationships who are also (B) "accredited investors" as defined in Section 73.3(1) of the Securities Act (Ontario) and Section 1.1 of National Instrument 45-106 Prospectus Exemptions. You understand and acknowledge that no prospectus has been prepared or filed with any securities commission or similar regulatory authority in Canada in connection with the Presentation, no securities commission or similar regulatory authority in Canada has made any finding or determination as to the merit for investment in, or made any recommendation or endorsement with respect to, the Presentation and that any securities offered in connection with the Presentation may not be offered or sold, directly or indirectly, in the Canada, other than in accordance with an exemption from the prospectus requirement under applicable Canadian securities laws. In the United Kingdom (UK), this Presentation is not a prospectus for the purposes of Public Offers and Admissions to Trading Regulations 2024 ("POATRs"). For residents in the United Kingdom or a member state of the European Economic Area (the "EEA"), as applicable, Manufacturer Target Market (MiFID II and UK MiFIR Product Governance) is eligible counterparties and professional clients only (all distribution channels), and no Packaged Retail and Insurance-based Investment Products ("PRIIPS") key information document (KID) has been prepared as any securities issued will not be available to retail in the EEA. No disclosure document required by the Financial Conduct Authority's Product Disclosure Sourcebook ("DISC") for offering, selling or distributing the securities or otherwise making them available to retail investors in the UK has been prepared, and therefore offering, selling or distributing the securities or otherwise making them available to any retail investor in the UK may be unlawful under DISC and the Consumer Composite Investments (Designated Activities) Regulations 2024. In member states of the EEA, this Presentation is only directed at qualified investors ("Qualified Investors") within the meaning of the Regulation (EU) 2017/1129 and points (1) to (4) of Section I of Annex II to Directive 2014/65/EU. In the UK, this Presentation is only directed at (i) persons who have professional experience in matters relating to investments falling within Article 19(5) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 as amended (the "Order"), (ii) high net worth entities, and other persons to whom it may lawfully be communicated, falling within Article 49(2)(a) to (e) of the Order, or (iii) persons to whom an invitation or inducement to engage in investment activity (within the meaning of section 21 of the Financial Services and Markets Act 2000 as amended) in connection with the issue or sale of any securities may otherwise lawfully be communicated or caused to be communicated (all such persons being "Relevant Persons"). Participants in the Solicitation MKAR and SPAC and their respective directors, executive officers and other members of their management and employees, under SEC rules, may be deemed to be participants in the solicitation of proxies of SPAC's shareholders in connection with the Business Combination. Investors and security holders may obtain more detailed information regarding the names, affiliations and interests of SPAC's directors and officers in SPAC's SEC filings. Information regarding the persons who may, under SEC rules, be deemed participants in the solicitation of proxies to SPAC's shareholders in connection with the Merger will be set forth in the proxy statement/prospectus for the Merger when available. Information concerning the interests of Disclaimer 2

MKAR's and SPAC's participants in the solicitation, which may, in some cases, be different than those of their respective equityholders generally, are set forth in the Registration Statement and the proxy statement/prospectus. Stockholders, potential investors and other interested persons should read the Registration Statement and the proxy statement/prospectus carefully before making any voting or investment decisions. You may obtain free copies of these documents from the sources indicated below. Forward-Looking Statements All statements other than statements of historical facts contained in this Presentation, including statements regarding the future financial position of MKAR after the closing of the Proposed Business Combination ("PubCo"), results of operations, business strategy, and plans and objectives of their management team for future operations, are forward-looking statements. Any statements that refer to projections, forecasts or other characterizations of future events or circumstances, including any underlying assumptions, are also forward-looking statements. In some cases, you can identify forward-looking statements by words such as "estimate," "plan," "project," "forecast," "intend," "expect," "anticipate," "believe," "seek," "strategy," "future," "opportunity," "may," "target," "should," "will," "would," "will be," "will continue," "will likely result," "preliminary," or similar expressions that predict or indicate future events or trends or that are not statements of historical matters, but the absence of these words does not mean that a statement is not forward-looking. Forward-looking statements include, without limitation, SPAC, MKAR or their respective management teams' expectations concerning the outlook for their or PubCo's business, productivity, plans, goals for future operational improvements, capital investments, operational performance, future market conditions, economic performance, developments in the capital and credit markets, expected future financial performance, capital expenditure plans and timeline, mineral reserve and resource estimates, production and other operating results, productivity improvements, expected net proceeds, expected additional funding, the percentage of redemptions of SPAC's public shareholders, growth prospects and outlook of PubCo's operations, individually or in the aggregate, including the achievement of project milestones, commencement and completion of commercial operations of certain of PubCo's projects, future listing of PubCo on Nasdaq, as well as any information concerning possible or assumed future results of operations of PubCo. Forward-looking statements also include statements regarding the expected benefits of the Proposed Business Combination. The forward-looking statements are based on the current expectations of the respective management teams of SPAC and MKAR, as applicable, and are inherently subject to uncertainties and changes in circumstance and their potential effects. There can be no assurance that future developments will be those that have been anticipated. These forward-looking statements involve a number of risks, uncertainties or other assumptions that may cause actual results or performance to be materially different from those expressed or implied by these forward-looking statements. These risks and uncertainties include, but are not limited to, (i) the risk that the Proposed Business Combination may not be completed in a timely manner or at all, which may adversely affect the price of SPAC's or PubCo's securities, (ii) the risk that the Proposed Business Combination may not be completed by SPAC's business combination deadline, or at all, and the potential failure to obtain an extension of the business combination deadline if sought by SPAC or MKAR, (iii) the failure to satisfy the conditions to the consummation of the Proposed Business Combination, including the approval of the Business Combination Agreement by Mkango Resources Ltd. (the sole shareholder of MKAR ("Mkango")), the shareholders of SPAC or by any other required party, the satisfaction of the minimum cash amount following redemptions by SPAC's public shareholders and the receipt of certain governmental and regulatory approvals, (iv) market risks, including the price of rare earth materials, (v) the occurrence of any event, change or other circumstance that could give rise to the termination of the business combination agreement, (vi) the effect of the announcement or pendency of the Proposed Business Combination on SPAC's or MKAR's business relationships, performance, and business generally, (vii) the outcome of any legal proceedings that may be instituted against SPAC or PubCo related to the Business Combination Agreement or the Proposed Business Combination, (viii) failure to realize the anticipated benefits of the Proposed Business Combination, (ix) the inability to effect and maintain the quotation of SPAC's securities on the OTC Markets or the inability of MKAR to meet the listing requirements of the Nasdaq Stock Market, or if listed, the inability of PubCo to maintain the listing of its securities on the Nasdaq Stock Market, (x) the risk that the price of PubCo's securities may be volatile due to a variety of factors, including changes in the highly competitive industries in which PubCo plans to operate, variations in performance across competitors, changes in laws, regulations, technologies, natural disasters or health epidemics/pandemics, national security tensions, and macro-economic and social environments affecting its business, and changes in the combined capital structure, (xi) the inability to implement business plans, forecasts, and other expectations after the completion of the Proposed Business Combination, identify and realize additional opportunities, and manage its growth and expanding operations, (xii) the risk that PubCo may not be able to successfully develop its assets, (xiii) the risk that PubCo will be unable to raise additional capital to execute its business plan, which may not be available on acceptable terms or at all, (xiv) the potential for geopolitical instability in Europe, the political and social risks of operating in Malawi or Poland, and geopolitical impacts on markets and tariffs, (xv) operational hazards and risks that PubCo could face, and (xvi) the risk that additional financing in connection with the Proposed Business Combination or PubCo's operations may not be raised on favorable terms, in a sufficient amount to satisfy the desired outcomes, or at all. The foregoing list is not exhaustive, and there may be additional risks that SPAC or MKAR presently do not know or that they currently believe are immaterial. You should carefully consider the foregoing factors, any other factors discussed in this Presentation and the other risks and uncertainties described in SPAC's filings with the SEC, the risks to be described in the Registration Statement, which will include the proxy statement/prospectus, and those discussed and identified in filings made with the SEC by SPAC and PubCo, from time to time. SPAC and MKAR caution you against placing undue reliance on forward-looking statements, which reflect current beliefs and are based on information currently available as of the date a forward-looking statement is made. Forward-looking statements set forth in this Presentation speak only as of the date of this Presentation. None of SPAC or MKAR undertakes any obligation to revise forward-looking statements to reflect future events, changes in circumstances, or changes in beliefs. In the event that any forward-looking statement is updated, no inference should be made that SPAC or MKAR will make additional updates with respect to that statement, related matters, or any other forward-looking statements. Any corrections or revisions and other important assumptions and factors that could cause actual results to differ materially from forward-looking statements, including discussions of significant risk factors, may appear, up to the consummation of the Proposed Transaction or the Proposed Business Combination, in SPAC's or PubCo's public filings with the SEC, which are or will be (as appropriate) accessible at www.sec.gov, and which you are advised to review carefully. The forward-looking statements in this Presentation may also include financial outlooks and other forward-looking metrics relating to MKAR, SPAC and PubCo. To the extent any forward-looking statements in this Presentation constitute "future- oriented financial information" or "financial outlooks" within the meaning of applicable Canadian securities laws (collectively, "FOFI"), such information is being provided to demonstrate the internal projections of MKAR and SPAC and the reader is cautioned that this information may not be appropriate for any other purpose and the reader should not place undue reliance on such FOFI. FOFI, as with forward-looking statements generally, are, without limitation, based on the assumptions and subject to the risks and uncertainties set out above. The actual financial position and results of operations of MKAR, SPAC and PubCo may differ materially from management's current expectations and, as a result, the revenue and profitability of MKAR, SPAC and PubCo may differ materially from the revenue and profitability profiles provided in this Presentation. Such information is presented for illustrative purposes only and may not be an indication of the actual financial position or results of operations of MKAR, SPAC or PubCo. Use of Projections This Presentation contains projected financial information, including net present value amounts, and operational information with respect to MKAR and the assets it will own upon completion of the Proposed Business Combination. Such projected information constitutes forward-looking information, is for illustrative purposes only, and should not be relied upon as necessarily being indicative of future results. The assumptions and estimates underlying such projected information are inherently Disclaimer 3

uncertain and are subject to a wide variety of significant business, economic, competitive and other risks and uncertainties. See also "Forward-Looking Statements" above. Actual results may differ materially from the results contemplated by the projected information contained in this Presentation and the inclusion of such information in this Presentation should not be regarded as a representation by any person that the results reflected in such projections will be achieved. Neither MKAR nor SPAC intends to or undertakes any obligation to update or otherwise revise the projected information to reflect circumstances existing after the date when made or to reflect the occurrence of future events in the event that any or all of the assumptions underlying the projected financial information are no longer valid. Accordingly, they should not be viewed as "guidance" of any sort. Cautionary Note Regarding Mineral Resources and Mineral Reserves Estimates of "measured", "indicated" and "inferred" mineral resources as well as mineral reserves shown in this Presentation are defined in Subpart 1300 of Regulation S-K promulgated by the SEC ("S-K 1300"). Please see Slide 33 for more information. The estimation of measured resources and indicated resources involves greater uncertainty as to their existence and economic feasibility than the estimation of mineral reserves. The estimation of inferred resources involves far greater uncertainty as to their existence and economic viability than the estimation of other categories of resources. Investors are cautioned not to assume that any or all of the mineral resources are economically or legally mineable or that these mineral resources will ever be converted into mineral reserves. You are cautioned that mineral resources do not have demonstrated economic viability. Scientific and technical information contained in this Presentation related to the Songwe rare earth deposit has been approved and verified by Scott Swinden who is a "Qualified Person" in accordance with National Instrument 43-101 – Standards of Disclosure for Mineral Projects ("NI 43-101"). Scientific and technical information contained in this presentation relating to the mineral resource estimate has been approved and verified by Jeremy Charles Witley of The MSA Group who is a "Qualified Person" in accordance with NI 43-101. The Qualified Persons referred to above are independent of Mkango, MKAR and the SPAC. An NI 43-101 Technical Report supporting the results of the definitive feasibility study for the Songwe Hill Rare Earths Project in Malawi has been prepared by SENET, a DRA global company, under the guidance of Mr. Phil Bundo, The MSA Group, under the guidance of Jeremy Charles Witley, Swinden Geoscience Consultants Ltd., under the guidance of Scott Swinden, Digby Wells Environmental, under the guidance of Graham Erro Trusler, Bara Consulting (Pty) Ltd, under the guidance of Clive Syndham Brown, Epoch Resources (Pty) Ltd, under the guidance of Guy John Wiid, and Dahrouge Geological Consulting Ltd., under the guidance of Darren L. Smith. Each of Mr. Bundo, Mr. Witley, Mr. Swinden, Mr. Trusler, Mr. Brown, Mr. Wiid and Mr. Smith is a "Qualified Person" in accordance with NI 43-101. The 43-101 Technical Report was filed on Mkango's profile on SEDAR+ on April 30, 2026, with an effective date of June 30, 2025. Additional Information and Where to Find It In connection with the Proposed Business Combination, MKAR has filed the Registration Statement with the SEC on May 20, 2026, as amended on June 8, 2026, which includes a preliminary proxy statement of SPAC and a preliminary prospectus of MKAR with respect to the securities to be offered in the Proposed Business Combination. After the Registration Statement is declared effective, SPAC will mail a definitive proxy statement/prospectus to its shareholders as of a record date to be established for voting on the Business Combination. SPAC and MKAR urge investors and other interested persons to read the proxy statement/prospectus, as well as other documents filed with the SEC, because these documents will contain important information about the Proposed Business Combination. Such persons can also read SPAC's filings with the SEC for a description of the security holdings of its officers and directors and their respective interests as security holders in the consummation of the Proposed Business Combination. The proxy statement statement/prospectus and the Registration Statement can be obtained, without charge, at the SEC's website at www.sec.gov. Disclaimer 4

Today's Speakers 5 OVERVIEW Note: All references to $ are to US$ (1) Assumes GBP/USD exchange rate of 1.253 MICHAEL MINNICK Chief Executive Officer • Finance veteran with over 30 years of experience across global investment banking, private equity, and capital markets • CEO of Target Global Acquisition I Corp. • Co-CEO & Member of the Board at CIIG Capital Partners II from 2021 until its business combination • Co-founder and Managing Partner of IIG Holdings and Opus Music II LLC • Former senior leader at global investment banks, overseeing advisory, debt, and equity transactions exceeding $190B in total volume at JPMorgan Chase & Co. and The Royal Bank of Scotland Group WILLIAM DAWES President & Director Consolidated Contractors Company • Seasoned resource sector executive with over 30 years of experience, including 16 years in rare earths, encompassing investment banking, mineral exploration, mining, metallurgy, recycling, and magnetic materials • Trained geologist and former mining analyst for Rio Tinto as well as an investment banker with global mining transaction experience at Robert Fleming & Co, Chase Manhattan Bank, and JPMorgan • Founding Director and Chief Executive Officer of Mkango Resources Ltd (TSX-V/AIM: MKA), Director of subsidiaries Maginito Limited and HyProMag Ltd • Secured strategic partnerships with Talaxis, including ~$15M(1) in funding for Songwe Feasibility studies ALEXANDER LEMON Chief Executive Officer & Director Consolidated Contractors Company • Operator and executive with over 30 years of experience in mineral exploration, business development, international government relations and project management across global geographies, including 16 years in rare earths • Founding Director and President of Mkango Resources Ltd (TSX-V/AIM:MKA) and Director of its subsidiary Maginito Limited, developing sustainable sources of rare earths oxides from Malawi, UK, Germany, Poland and the US • Director of Kongiwe, a leading environmental consultancy in South Africa • Fellow of the Geological Society of London, Royal Geographical Society, and Member of the Southern African Institute of Mining & Metallurgy

SPAC Merger – Announced Business Combination 6 • Business Combination Agreement (BCA) signed with Crown Proptech Acquisitions (CPTK), a special purpose acquisition company • Upon closing of the business combination, Mkango Rare Earths Limited (MKAR) will directly hold Mkango Resource Ltd.'s Songwe Hill and Pulawy Rare Earths projects and is expected to be listed on NASDAQ • Implied MKAR Pro Forma Enterprise Value of $488M(1) • Transaction proceeds will support MKAR's strategic growth plan, including development of Songwe Hill and Pulawy, and to pay transaction expenses • Proposed Business Combination is expected to be completed in Q3 2026 Key Highlights OVERVIEW MKANGO RARE EARTHS LIMITED (1) See Slide 6 for calculation of Implied Pro Forma Enterprise Value

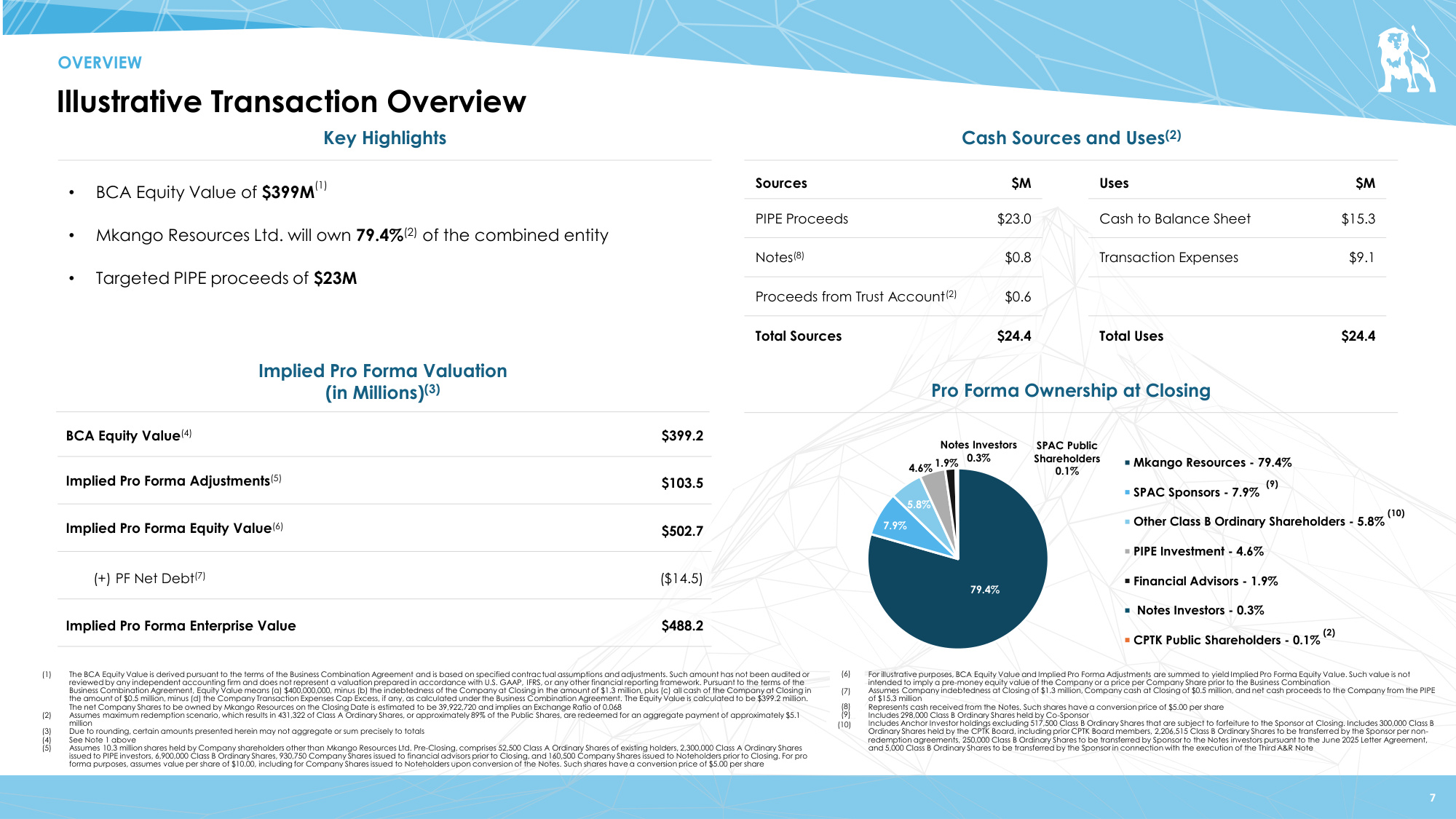

(1) For illustrative purposes, BCA Equity Value and Implied Pro Forma Adjustments are summed to yield Implied Pro Forma Equity Value. Such value is not intended to imply a pre-money equity value of the Company or a price per Company Share prior to the Business Combination (2) Assumes Company indebtedness at Closing of $1.3 million, Company cash at Closing of $0.5 million, and net cash proceeds to the Company from the PIPE of $15.3 million (3) Represents cash received from the Notes. Such shares have a conversion price of $5.00 per share (4) Includes 298,000 Class B Ordinary Shares held by Co-Sponsor (5) Includes Anchor Investor holdings excluding 517,500 Class B Ordinary Shares that are subject to forfeiture to the Sponsor at Closing. Includes 300,000 Class B Ordinary Shares held by the CPTK Board, including prior CPTK Board members, 2,206,515 Class B Ordinary Shares to be transferred by the Sponsor per non- redemption agreements, 250,000 Class B Ordinary Shares to be transferred by Sponsor to the Notes investors pursuant to the June 2025 Letter Agreement, and 5,000 Class B Ordinary Shares to be transferred by the Sponsor in connection with the execution of the Third A&R Note Notes Investors 0.3% 79.4% 7.9% 5.8% 4.6% 1.9% Mkango Resources - 79.4% SPAC Sponsors - 7.9% Other Class B Ordinary Shareholders - 5.8% PIPE Investment - 4.6% Financial Advisors - 1.9% Notes Investors - 0.3% CPTK Public Shareholders - 0.1% Illustrative Transaction Overview BCA Equity Value(4) $399.2 Implied Pro Forma Adjustments(5) $103.5 Implied Pro Forma Equity Value(6) $502.7 (+) PF Net Debt(7) ($14.5) Implied Pro Forma Enterprise Value $488.2 Sources $M PIPE Proceeds $23.0 Notes(8) $0.8 Proceeds from Trust Account(2) $0.6 Total Sources $24.4 (1) The BCA Equity Value is derived pursuant to the terms of the Business Combination Agreement and is based on specified contractual assumptions and adjustments. Such amount has not been audited or reviewed by any independent accounting firm and does not represent a valuation prepared in accordance with U.S. GAAP, IFRS, or any other financial reporting framework. Pursuant to the terms of the Business Combination Agreement, Equity Value means (a) $400,000,000, minus (b) the indebtedness of the Company at Closing in the amount of $1.3 million, plus (c) all cash of the Company at Closing in the amount of $0.5 million, minus (d) the Company Transaction Expenses Cap Excess, if any, as calculated under the Business Combination Agreement. The Equity Value is calculated to be $399.2 million. The net Company Shares to be owned by Mkango Resources on the Closing Date is estimated to be 39,922,720 and implies an Exchange Ratio of 0.068 (2) Assumes maximum redemption scenario, which results in 431,322 of Class A Ordinary Shares, or approximately 89% of the Public Shares, are redeemed for an aggregate payment of approximately $5.1 million (3) Due to rounding, certain amounts presented herein may not aggregate or sum precisely to totals (4) See Note 1 above (5) Assumes 10.3 million shares held by Company shareholders other than Mkango Resources Ltd. Pre-Closing, comprises 52,500 Class A Ordinary Shares of existing holders, 2,300,000 Class A Ordinary Shares issued to PIPE investors, 6,900,000 Class B Ordinary Shares, 930,750 Company Shares issued to financial advisors prior to Closing, and 160,500 Company Shares issued to Noteholders prior to Closing. For pro forma purposes, assumes value per share of $10.00, including for Company Shares issued to Noteholders upon conversion of the Notes. Such shares have a conversion price of $5.00 per share Cash Sources and Uses(2) Key Highlights Pro Forma Ownership at Closing Implied Pro Forma Valuation (in Millions)(3) • BCA Equity Value of $399M (1) • Mkango Resources Ltd. will own 79.4%(2) of the combined entity • Targeted PIPE proceeds of $23M 7 SPAC Public Shareholders 0.1% Uses $M Cash to Balance Sheet $15.3 Transaction Expenses $9.1 Total Uses $24.4 OVERVIEW (9) (10) (2) (6) (7) (10) (9) (8)

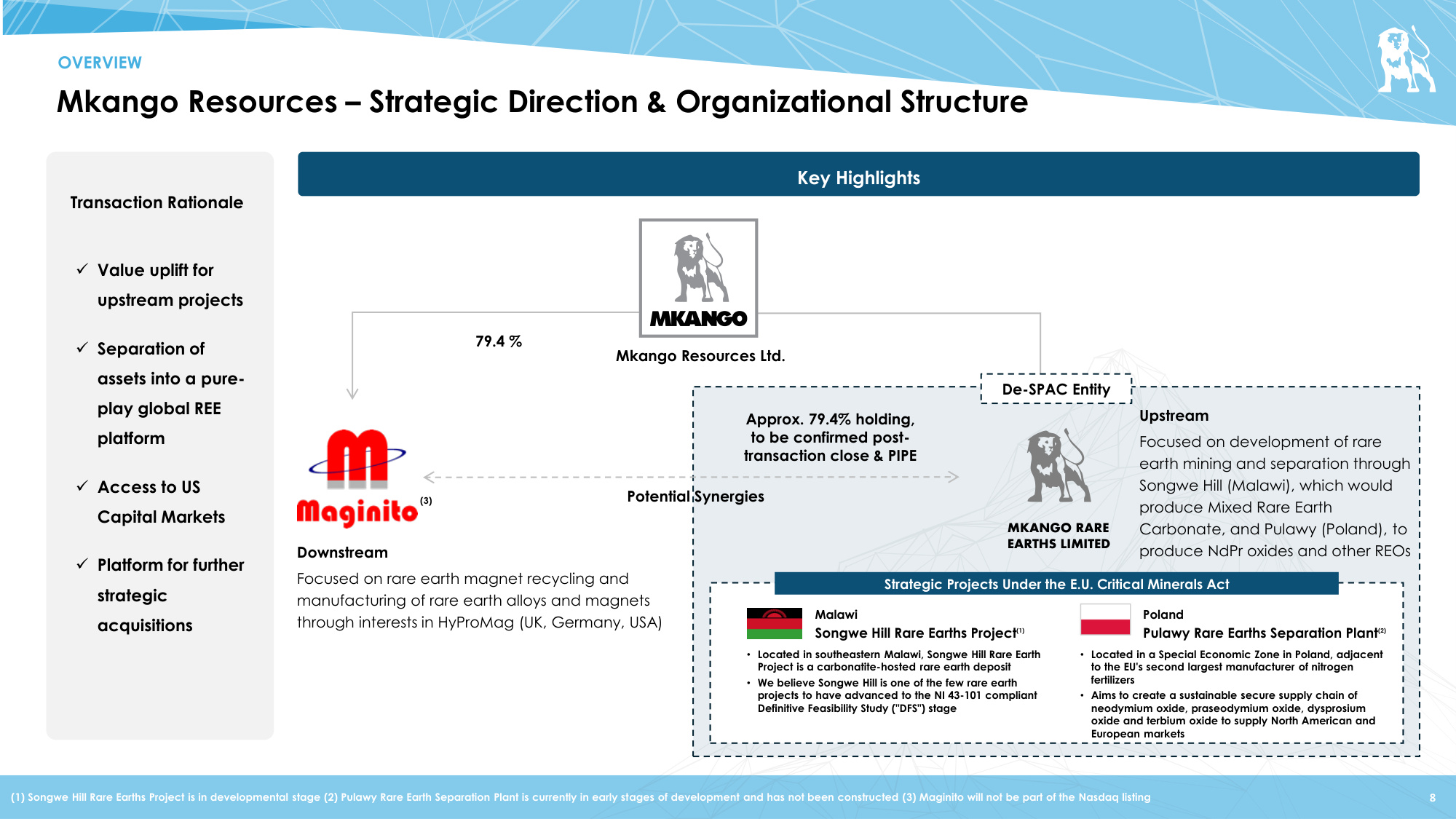

Mkango Resources – Strategic Direction & Organizational Structure 8 OVERVIEW Downstream Focused on rare earth magnet recycling and manufacturing of rare earth alloys and magnets through interests in HyProMag (UK, Germany, USA) 79.4 % Approx. 79.4% holding, to be confirmed post- transaction close & PIPE Upstream Focused on development of rare earth mining and separation through Songwe Hill (Malawi), which would produce Mixed Rare Earth Carbonate, and Pulawy (Poland), to produce NdPr oxides and other REOs Potential Synergies Mkango Resources Ltd. De-SPAC Entity ✓Value uplift for upstream projects ✓Separation of assets into a pure- play global REE platform ✓Access to US Capital Markets ✓Platform for further strategic acquisitions Transaction Rationale Key Highlights Malawi Songwe Hill Rare Earths Project (1) Poland Pulawy Rare Earths Separation Plant (2) • Located in southeastern Malawi, Songwe Hill Rare Earth Project is a carbonatite-hosted rare earth deposit • We believe Songwe Hill is one of the few rare earth projects to have advanced to the NI 43-101 compliant Definitive Feasibility Study ("DFS") stage • Located in a Special Economic Zone in Poland, adjacent to the EU's second largest manufacturer of nitrogen fertilizers • Aims to create a sustainable secure supply chain of neodymium oxide, praseodymium oxide, dysprosium oxide and terbium oxide to supply North American and European markets Strategic Projects Under the E.U. Critical Minerals Act (1) Songwe Hill Rare Earths Project is in developmental stage (2) Pulawy Rare Earth Separation Plant is currently in early stages of development and has not been constructed (3) Maginito will not be part of the Nasdaq listing (3) MKANGO RARE EARTHS LIMITED

Alexander Lemon, Chief Executive Officer & Director • 30 years of experience in exploration, project development, and mining-focused business growth strategy, spanning a variety of executive and operational roles globally to co-founding and leading Mkango Resources Ltd with 16 years' experience in rare earths • Led mineral exploration and project development roles at Gold & Mineral Excavation, handling mine site exploration, government relations, and international exploration projects • BSc in Geological Sciences, MSc in Mineral Exploration William Dawes, President & Director • Seasoned resource sector executive with over 30 years of experience, including 16 years in rare earths across banking, exploration, mining, and metallurgy • Former Rio Tinto exploration specialist; experience in metals & mining investment-banking teams, executing global mining finance and M&A transactions • BSc in Geology, MSc in Mineral Exploration Scott Beattie, Senior Advisor • 20+ years' experience in international finance, originating and executing transactions across products and sectors • Extensive knowledge of the mining, oil & gas, and infrastructure sectors, combined with first-hand oilfield experience as a Wireline Field Engineer II at Halliburton • MBA, London Business School Jarosław Paczek, Country Director, Poland • Corporate financier by training with a career in private equity and as a lawyer for Washington-based firm Hogan and Hartson (now Hogan Lovells) • PhD (Law) Burton Kachinjika, Country Director, Malawi • Over 40 years of experience in natural resources across metals & mining, energy regulation, built environment, and roads administration • BSc Chemistry & Physics, B Eng. Hons Mineral Processing Proven Management Team in the Rare Earths Sector 9 OVERVIEW World-Class Metals & Mining Experience • Experienced management team with a proven 16-year record managing Mkango Resources Ltd., listed on the TSX Venture Exchange since 2011 and the London AIM since 2016 • Advanced the Songwe Hill Rare Earth project from exploration to Definitive Feasibility Study • Developed assets in the rare earth supply chain by implementing early mover recycling strategy, with rare earth permanent magnet manufacturing and recycling • Strong relationships across the rare earth supply chain, from mining through to end users of permanent magnets Consolidated Contractors Company

Non-Executive Board of Directors and Advisors 10 OVERVIEW Non-Executive Board of Directors Advisors General James L. Jones, Chairman • 40 years of leadership experience in military operations, energy security, foreign policy, and global strategic advisory roles • Former Commandant of the U.S. Marine Corps, Supreme Allied Commander Europe (SACEUR) of NATO, and Commander of U.S. European Command • Advised senior government, defense, and private sector organizations on national security and strategic affairs • B.S., Georgetown University United States Marine Corps United States European Command Michael Abbott, Director • 30+ years of experience in banking and finance • Previously founded a currency specialist hedge fund and served as CEO of a fund of hedge funds, and General Partner at a commodities specialist hedge fund • Serves on the boards of several companies in the healthcare sector • Bachelor of Laws, King's College London Ian Brzezinski • 30+ years of experience in U.S. national security, defense policy, and international affairs across government, Congress, and the private sector • Former Deputy Assistant Secretary of Defense for Europe and NATO Policy (2001–2005), leading NATO expansion and alliance transformation initiatives • Senior Fellow at the Atlantic Council's Scowcroft Center for Strategy and Security and founder of the Brzezinski Group, advising government and commercial clients on geopolitical strategy • Senior Advisor at Jones Group International, focusing on geopolitical risk and transatlantic security issues United States National Security Council John Raidt • Over two decades of public policy expertise in national security, energy, environment, and natural resource management • Former senior staff member on the 9/11 Commission and the U.S. Senate Committee on Commerce, Science and Transportation, supporting national security and infrastructure policy • Former Deputy to General James L. Jones for Middle East Regional Security, advising on energy security, governance, and geopolitical risk • M.P.A., Harvard University's Kennedy School of Government Daniel Mamadou, Director • 20+ years of experience in investment banking, commodity markets, and technology metals supply chain development • Former Executive Director at Talaxis (Noble Group's metals division), leading critical metal supply chains and investments in rare earths, lithium, cobalt, and graphite • Managing Director of Energy Transition Minerals (ASX: ETM), focused on exploring critical minerals for the clean energy transition • B.A. in Business Management and Marketing, ESIC, Madrid, Spain

Strong Relationships with Prominent Collaborators 11 OVERVIEW Facilitated by Global Government Funding & Support $4.6M commitment secured from the U.S. International Development Finance Corporation (DFC) to advance development of the Songwe Hill rare earth project in Malawi Continued support from the UK Foreign Commonwealth & Development Office (FCDO) in Malawi to establish a responsible supply chain The Songwe Hill Rare Earths and Pulawy projects are both recognized by the EU in 2025 as Strategic Projects essential to the EU's green transition and supply-chain security under the Critical Raw Materials Act ("CRMA") Feasibility and Pre-feasibility Studies Completed by World-Leading Technical Consultants

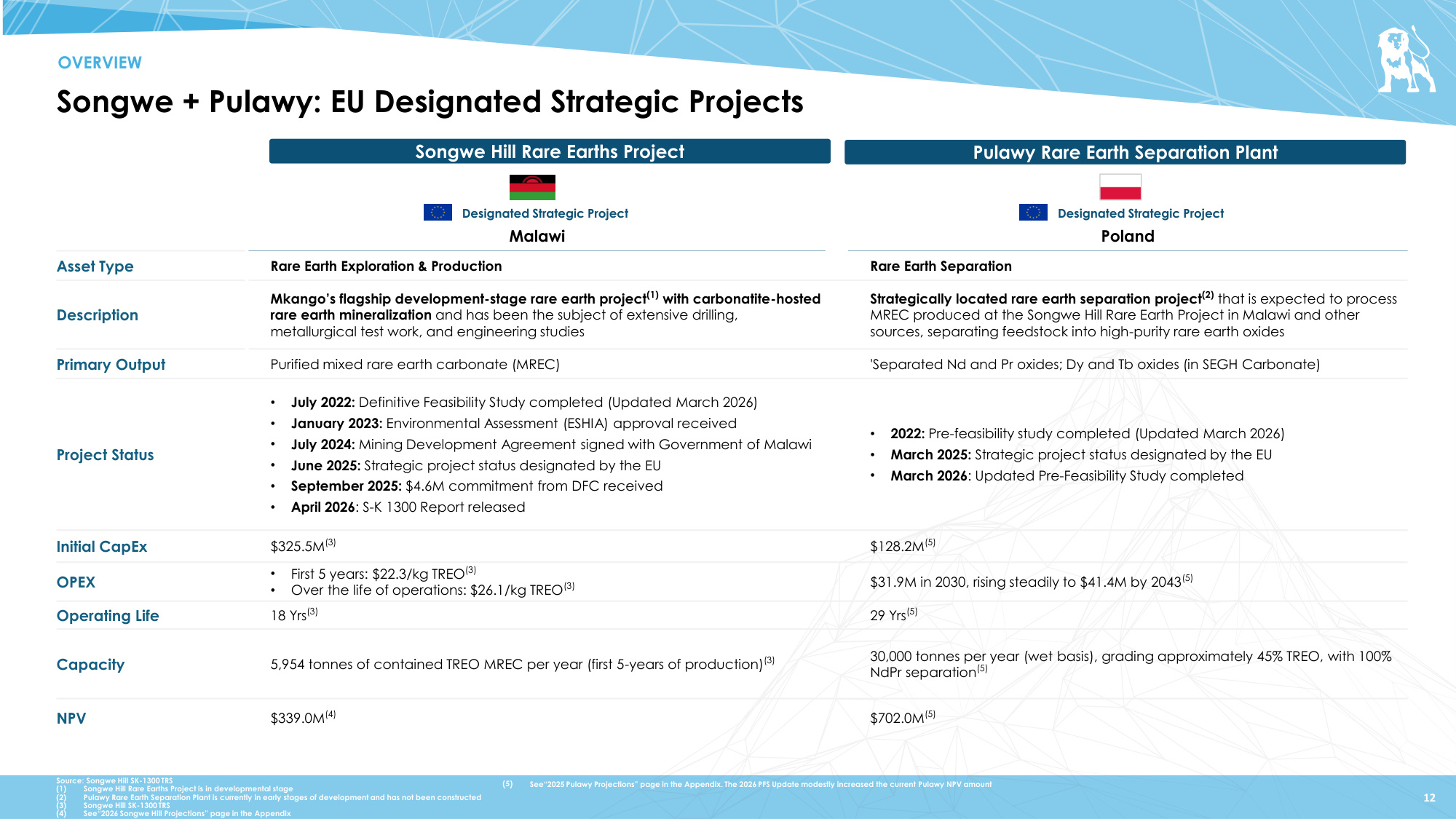

Songwe + Pulawy: EU Designated Strategic Projects 12 OVERVIEW M Malawi Poland Asset Type Rare Earth Exploration & Production Rare Earth Separation Description Mkango's flagship development-stage rare earth project(1) with carbonatite-hosted rare earth mineralization and has been the subject of extensive drilling, metallurgical test work, and engineering studies Strategically located rare earth separation project(2) that is expected to process MREC produced at the Songwe Hill Rare Earth Project in Malawi and other sources, separating feedstock into high-purity rare earth oxides Primary Output Purified mixed rare earth carbonate (MREC) 'Separated Nd and Pr oxides; Dy and Tb oxides (in SEGH Carbonate) Project Status • July 2022: Definitive Feasibility Study completed (Updated March 2026) • January 2023: Environmental Assessment (ESHIA) approval received • July 2024: Mining Development Agreement signed with Government of Malawi • June 2025: Strategic project status designated by the EU • September 2025: $4.6M commitment from DFC received • April 2026: S-K 1300 Report released • 2022: Pre-feasibility study completed (Updated March 2026) • March 2025: Strategic project status designated by the EU • March 2026: Updated Pre-Feasibility Study completed Initial CapEx $325.5M(3) $128.2M(5) OPEX • First 5 years: $22.3/kg TREO(3) • Over the life of operations: $26.1/kg TREO(3) $31.9M in 2030, rising steadily to $41.4M by 2043(5) Operating Life 18 Yrs(3) 29 Yrs(5) Capacity 5,954 tonnes of contained TREO MREC per year (first 5-years of production)(3) 30,000 tonnes per year (wet basis), grading approximately 45% TREO, with 100% NdPr separation(5) NPV $339.0M(4) $702.0M(5) Source: Songwe Hill SK-1300 TRS (1) Songwe Hill Rare Earths Project is in developmental stage (2) Pulawy Rare Earth Separation Plant is currently in early stages of development and has not been constructed (3) Songwe Hill SK-1300 TRS (4) See"2026 Songwe Hill Projections" page in the Appendix Songwe Hill Rare Earths Project Pulawy Rare Earth Separation Plant Designated Strategic Project Designated Strategic Project (1) See"2025 Pulawy Projections" page in the Appendix. The 2026 PFS Update modestly increased the current Pulawy NPV amount (5)

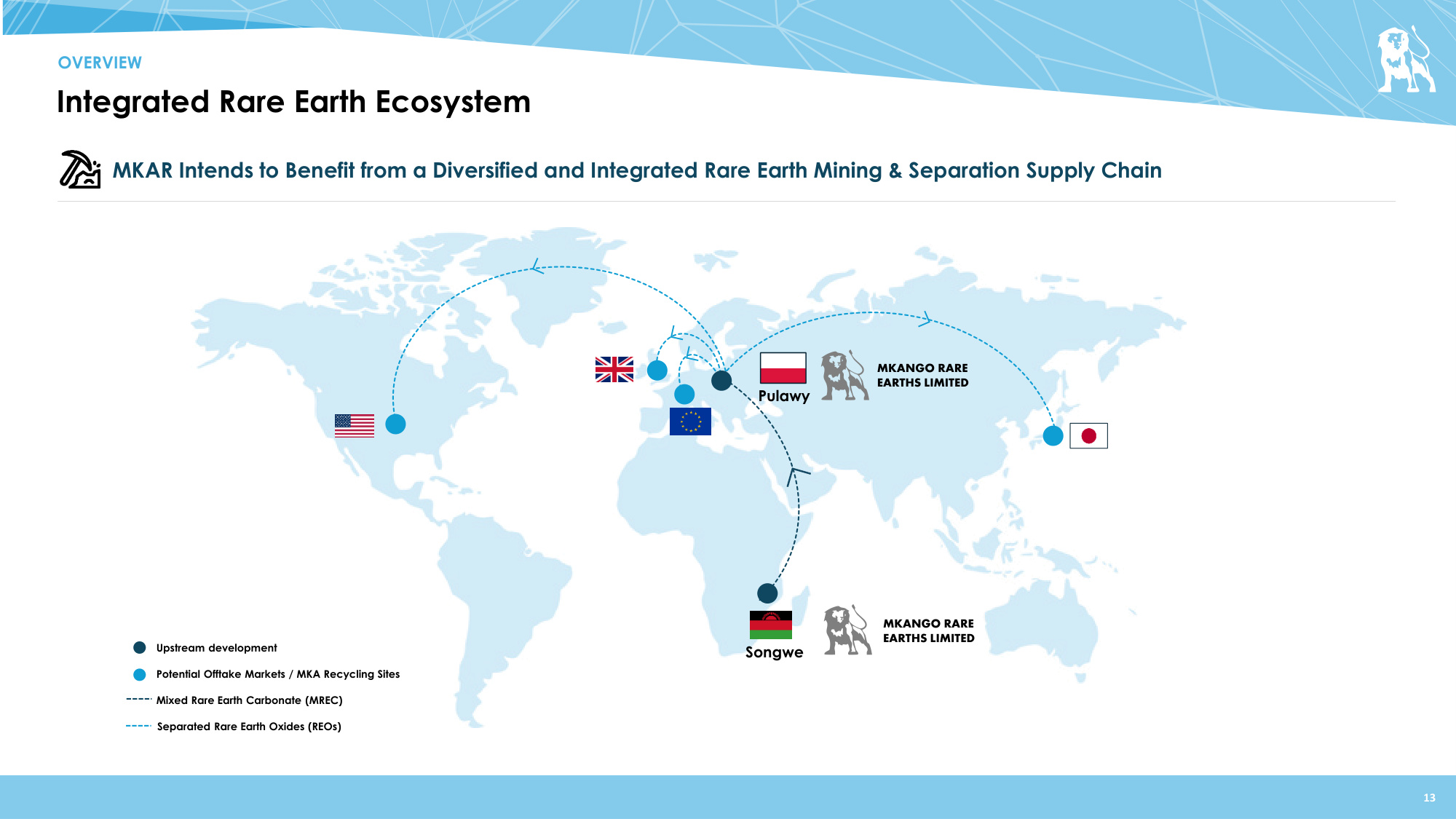

Pulawy Songwe 13 MKAR Intends to Benefit from a Diversified and Integrated Rare Earth Mining & Separation Supply Chain Integrated Rare Earth Ecosystem OVERVIEW Upstream development Potential Offtake Markets / MKA Recycling Sites Mixed Rare Earth Carbonate (MREC) Separated Rare Earth Oxides (REOs) MKANGO RARE EARTHS LIMITED MKANGO RARE EARTHS LIMITED

Songwe Hill, Malawi Rare Earths Project MKANGO RARE EARTHS LIMITED

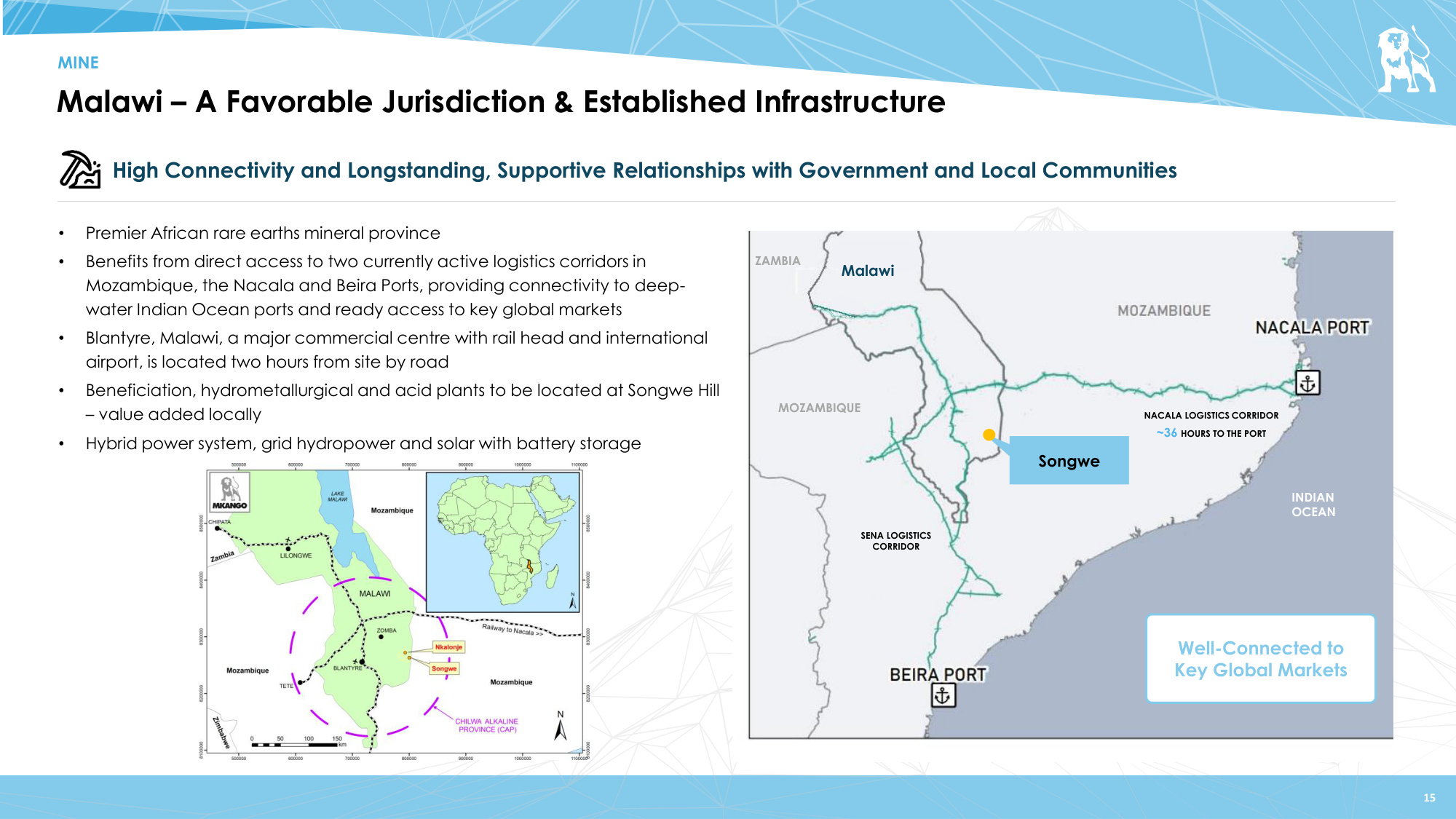

Malawi – A Favorable Jurisdiction & Established Infrastructure 15 MINE • Premier African rare earths mineral province • Benefits from direct access to two currently active logistics corridors in Mozambique, the Nacala and Beira Ports, providing connectivity to deep- water Indian Ocean ports and ready access to key global markets • Blantyre, Malawi, a major commercial centre with rail head and international airport, is located two hours from site by road • Beneficiation, hydrometallurgical and acid plants to be located at Songwe Hill – value added locally • Hybrid power system, grid hydropower and solar with battery storage High Connectivity and Longstanding, Supportive Relationships with Government and Local Communities NACALA LOGISTICS CORRIDOR ~36 HOURS TO THE PORT SENA LOGISTICS CORRIDOR Well-Connected to Key Global Markets Songwe Malawi MOZAMBIQUE ZAMBIA INDIAN OCEAN

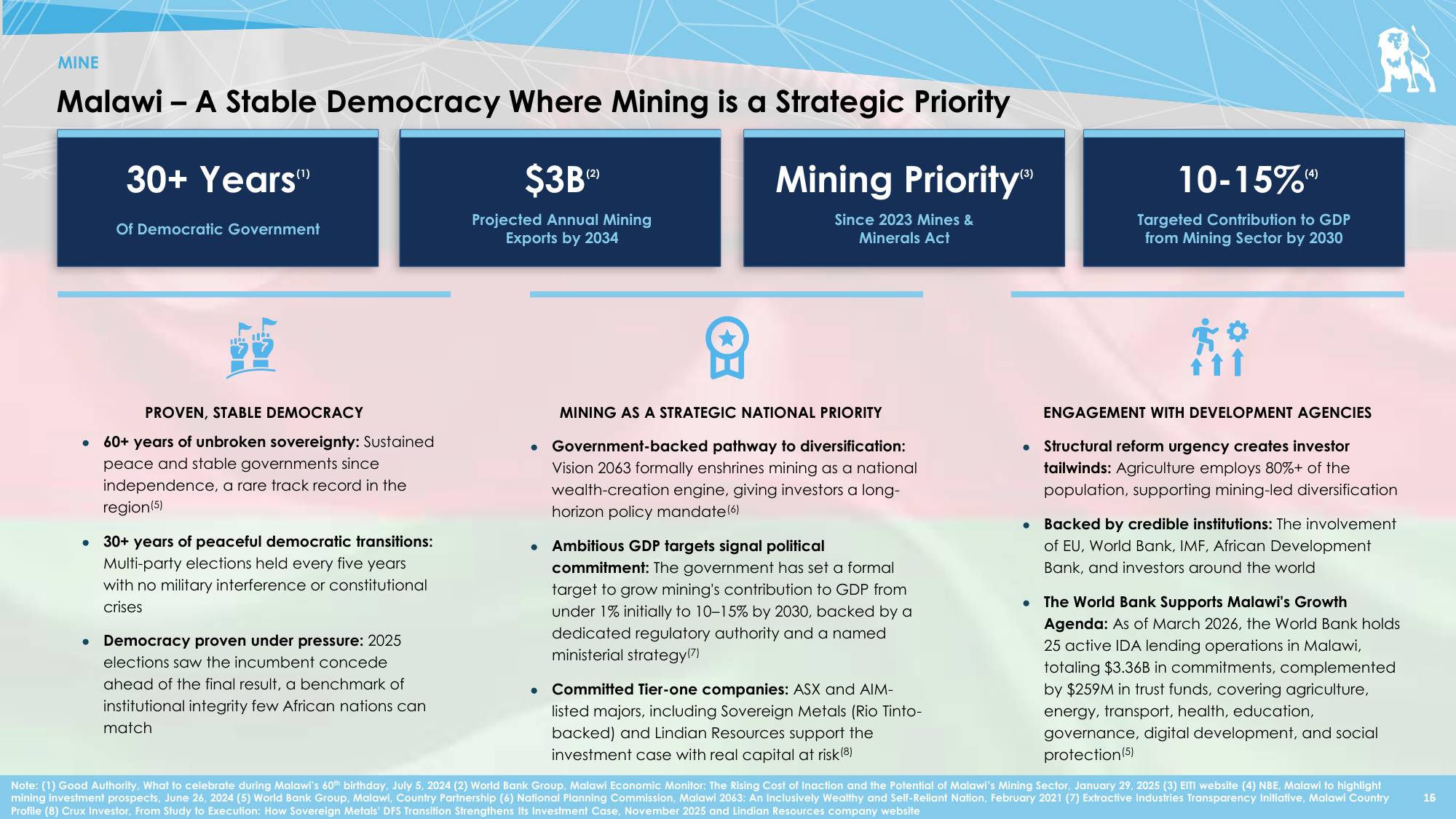

15 Malawi – A Stable Democracy Where Mining is a Strategic Priority 16 30+ Years (1) Of Democratic Government $3B (2) Projected Annual Mining Exports by 2034 Mining Priority (3) Since 2023 Mines & Minerals Act 10-15% (4) Targeted Contribution to GDP from Mining Sector by 2030 PROVEN, STABLE DEMOCRACY ● 60+ years of unbroken sovereignty: Sustained peace and stable governments since independence, a rare track record in the region(5) ● 30+ years of peaceful democratic transitions: Multi-party elections held every five years with no military interference or constitutional crises ● Democracy proven under pressure: 2025 elections saw the incumbent concede ahead of the final result, a benchmark of institutional integrity few African nations can match MINING AS A STRATEGIC NATIONAL PRIORITY ● Government-backed pathway to diversification: Vision 2063 formally enshrines mining as a national wealth-creation engine, giving investors a long- horizon policy mandate(6) ● Ambitious GDP targets signal political commitment: The government has set a formal target to grow mining's contribution to GDP from under 1% initially to 10–15% by 2030, backed by a dedicated regulatory authority and a named ministerial strategy(7) ● Committed Tier-one companies: ASX and AIM- listed majors, including Sovereign Metals (Rio Tinto- backed) and Lindian Resources support the investment case with real capital at risk(8) ENGAGEMENT WITH DEVELOPMENT AGENCIES ● Structural reform urgency creates investor tailwinds: Agriculture employs 80%+ of the population, supporting mining-led diversification ● Backed by credible institutions: The involvement of EU, World Bank, IMF, African Development Bank, and investors around the world ● The World Bank Supports Malawi's Growth Agenda: As of March 2026, the World Bank holds 25 active IDA lending operations in Malawi, totaling $3.36B in commitments, complemented by $259M in trust funds, covering agriculture, energy, transport, health, education, governance, digital development, and social protection(5) MINE Note: (1) Good Authority, What to celebrate during Malawi's 60th birthday, July 5, 2024 (2) World Bank Group, Malawi Economic Monitor: The Rising Cost of Inaction and the Potential of Malawi's Mining Sector, January 29, 2025 (3) EITI website (4) NBE, Malawi to highlight mining investment prospects, June 26, 2024 (5) World Bank Group, Malawi, Country Partnership (6) National Planning Commission, Malawi 2063: An Inclusively Wealthy and Self-Reliant Nation, February 2021 (7) Extractive Industries Transparency Initiative, Malawi Country Profile (8) Crux Investor, From Study to Execution: How Sovereign Metals' DFS Transition Strengthens Its Investment Case, November 2025 and Lindian Resources company website

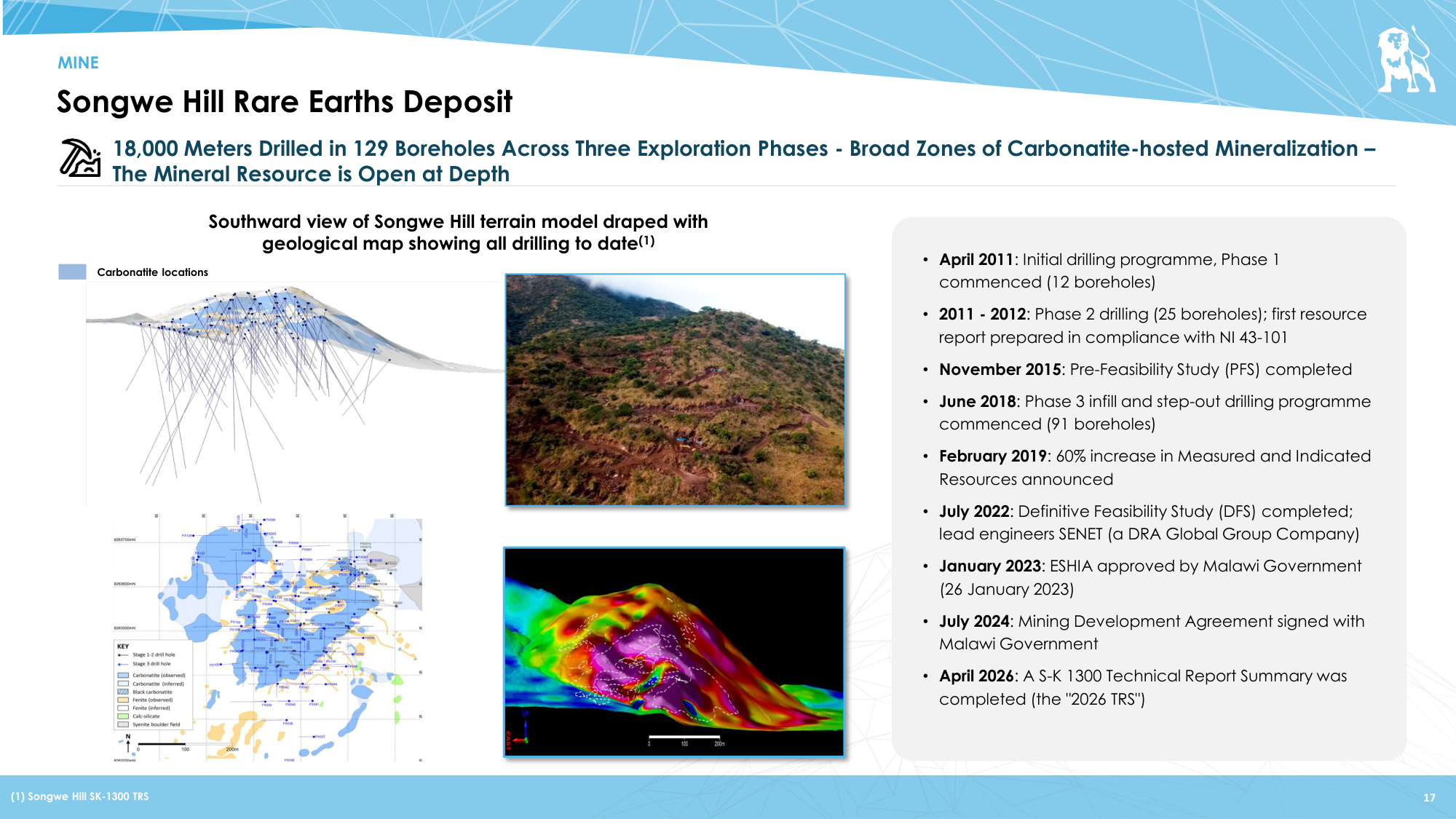

Songwe Hill Rare Earths Deposit Carbonatite locations 18,000 Meters Drilled in 129 Boreholes Across Three Exploration Phases - Broad Zones of Carbonatite-hosted Mineralization – The Mineral Resource is Open at Depth Southward view of Songwe Hill terrain model draped with geological map showing all drilling to date(1) 17 MINE • April 2011: Initial drilling programme, Phase 1 commenced (12 boreholes) • 2011 - 2012: Phase 2 drilling (25 boreholes); first resource report prepared in compliance with NI 43-101 • November 2015: Pre-Feasibility Study (PFS) completed • June 2018: Phase 3 infill and step-out drilling programme commenced (91 boreholes) • February 2019: 60% increase in Measured and Indicated Resources announced • July 2022: Definitive Feasibility Study (DFS) completed; lead engineers SENET (a DRA Global Group Company) • January 2023: ESHIA approved by Malawi Government (26 January 2023) • July 2024: Mining Development Agreement signed with Malawi Government • April 2026: A S-K 1300 Technical Report Summary was completed (the "2026 TRS") (1) Songwe Hill SK-1300 TRS

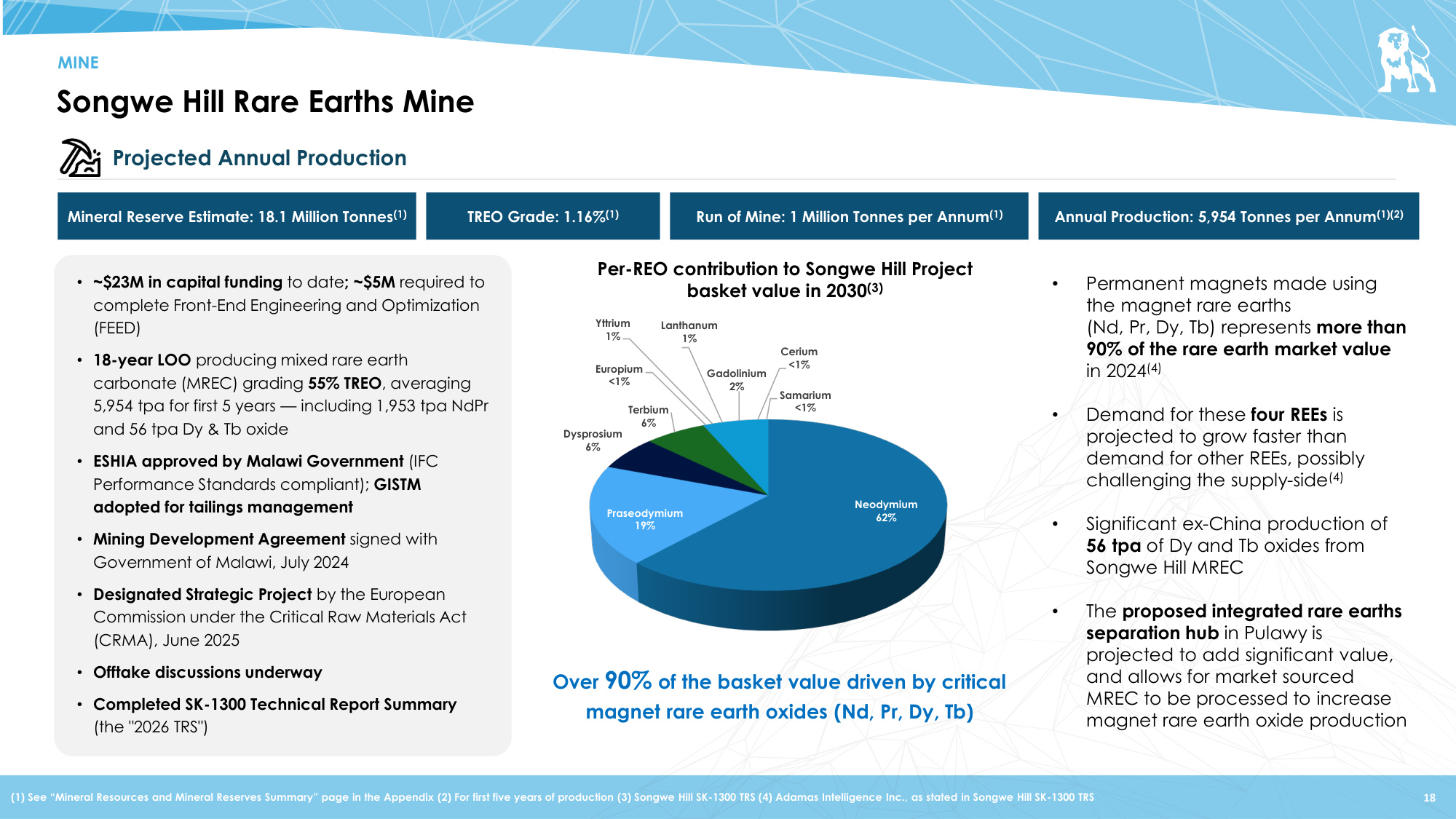

Songwe Hill Rare Earths Mine (1) See "Mineral Resources and Mineral Reserves Summary" page in the Appendix (2) For first five years of production (3) Songwe Hill SK-1300 TRS (4) Adamas Intelligence Inc., as stated in Songwe Hill SK-1300 TRS Projected Annual Production 18 MINE Mineral Reserve Estimate: 18.1 Million Tonnes(1) TREO Grade: 1.16%(1) Run of Mine: 1 Million Tonnes per Annum(1) Annual Production: 5,954 Tonnes per Annum(1)(2) Neodymium 62% Praseodymium 19% Dysprosium 6% Terbium 6% Europium <1% Yttrium 1% Lanthanum 1% Gadolinium 2% Cerium <1% Samarium <1% • ~$23M in capital funding to date; ~$5M required to complete Front-End Engineering and Optimization (FEED) • 18-year LOO producing mixed rare earth carbonate (MREC) grading 55% TREO, averaging 5,954 tpa for first 5 years — including 1,953 tpa NdPr and 56 tpa Dy & Tb oxide • ESHIA approved by Malawi Government (IFC Performance Standards compliant); GISTM adopted for tailings management • Mining Development Agreement signed with Government of Malawi, July 2024 • Designated Strategic Project by the European Commission under the Critical Raw Materials Act (CRMA), June 2025 • Offtake discussions underway • Completed SK-1300 Technical Report Summary (the "2026 TRS") Per-REO contribution to Songwe Hill Project basket value in 2030(3) Over 90% of the basket value driven by critical magnet rare earth oxides (Nd, Pr, Dy, Tb) • Permanent magnets made using the magnet rare earths (Nd, Pr, Dy, Tb) represents more than 90% of the rare earth market value in 2024(4) • Demand for these four REEs is projected to grow faster than demand for other REEs, possibly challenging the supply-side(4) • Significant ex-China production of 56 tpa of Dy and Tb oxides from Songwe Hill MREC • The proposed integrated rare earths separation hub in Pulawy is projected to add significant value, and allows for market sourced MREC to be processed to increase magnet rare earth oxide production

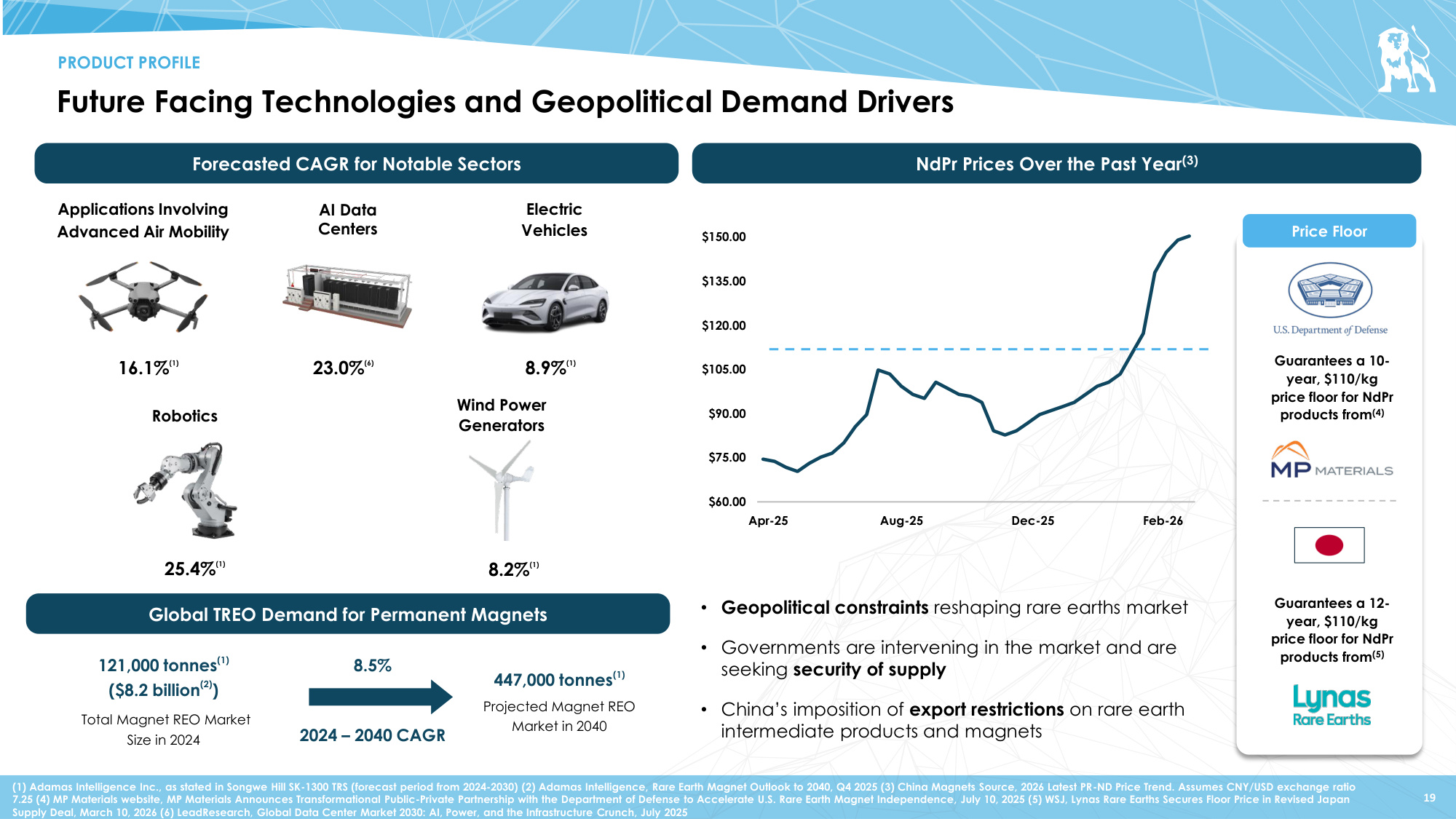

Future Facing Technologies and Geopolitical Demand Drivers 19 PRODUCT PROFILE (1) Adamas Intelligence Inc., as stated in Songwe Hill SK-1300 TRS (forecast period from 2024-2030) (2) Adamas Intelligence, Rare Earth Magnet Outlook to 2040, Q4 2025 (3) China Magnets Source, 2026 Latest PR-ND Price Trend. Assumes CNY/USD exchange ratio 7.25 (4) MP Materials website, MP Materials Announces Transformational Public-Private Partnership with the Department of Defense to Accelerate U.S. Rare Earth Magnet Independence, July 10, 2025 (5) WSJ, Lynas Rare Earths Secures Floor Price in Revised Japan Supply Deal, March 10, 2026 (6) LeadResearch, Global Data Center Market 2030: AI, Power, and the Infrastructure Crunch, July 2025 Global TREO Demand for Permanent Magnets Wind Power Generators Applications Involving Advanced Air Mobility 447,000 tonnes (1) Projected Magnet REO Market in 2040 121,000 tonnes (1) ($8.2 billion (2)) Total Magnet REO Market Size in 2024 8.5% AI Data Centers 8.2% (1) 23.0% (6) 16.1% (1) Guarantees a 10- year, $110/kg price floor for NdPr products from(4) Price Floor Guarantees a 12- year, $110/kg price floor for NdPr products from(5) Robotics 25.4% (1) NdPr Prices Over the Past Year(3) • Geopolitical constraints reshaping rare earths market • Governments are intervening in the market and are seeking security of supply • China's imposition of export restrictions on rare earth intermediate products and magnets 2024 – 2040 CAGR 8.9% (1) Electric Vehicles Forecasted CAGR for Notable Sectors $60.00 $75.00 $90.00 $105.00 $120.00 $135.00 $150.00 Apr-25 Aug-25 Dec-25 Feb-26

Pulawy Rare Earth Separation Plant MKANGO RARE EARTHS LIMITED

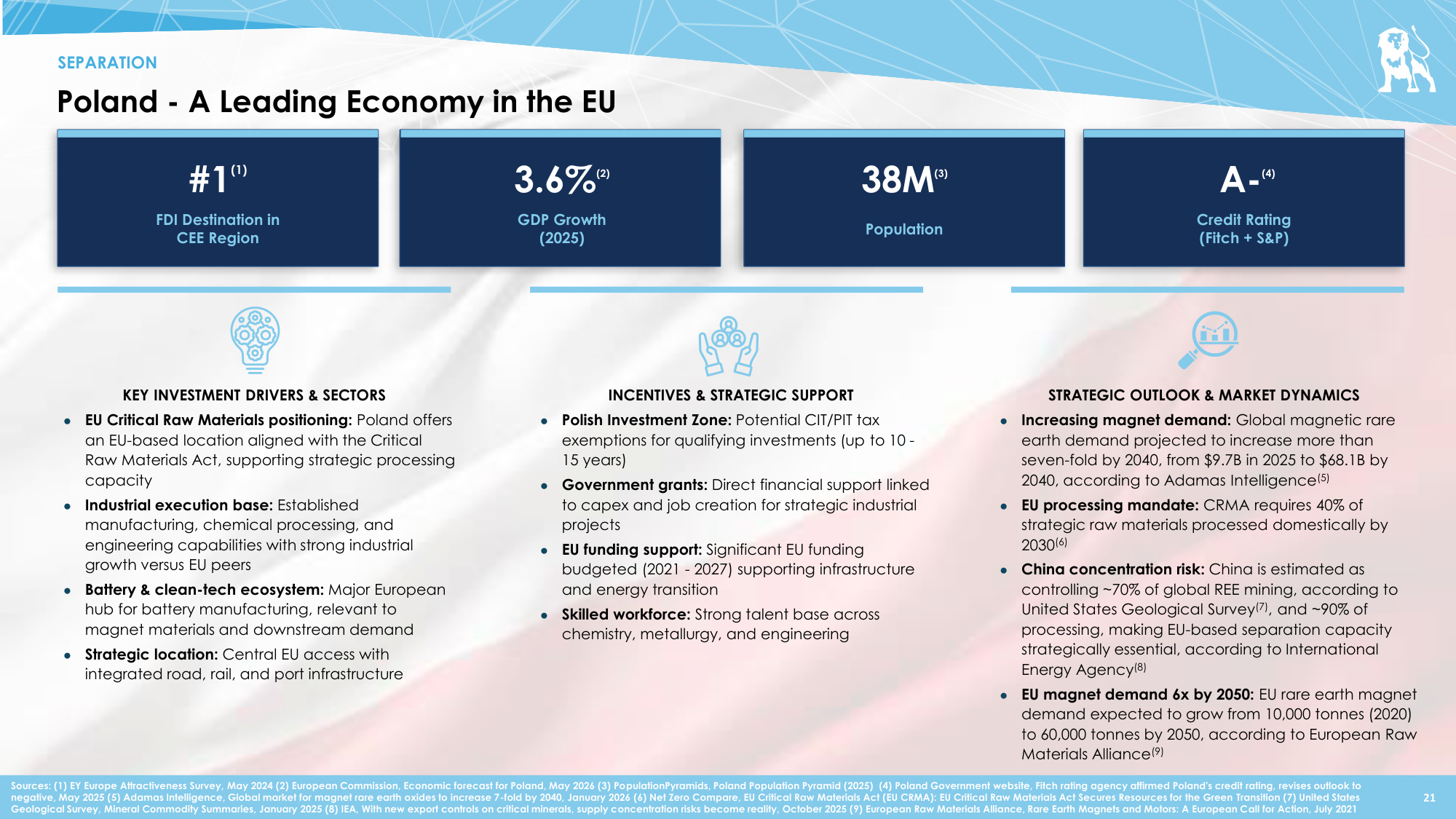

20 Poland - A Leading Economy in the EU 20 SEPARATION #1 (1) FDI Destination in CEE Region 3.6% (2) GDP Growth (2025) 38M (3) Population A- (4) Credit Rating (Fitch + S&P) KEY INVESTMENT DRIVERS & SECTORS ● EU Critical Raw Materials positioning: Poland offers an EU-based location aligned with the Critical Raw Materials Act, supporting strategic processing capacity ● Industrial execution base: Established manufacturing, chemical processing, and engineering capabilities with strong industrial growth versus EU peers ● Battery & clean-tech ecosystem: Major European hub for battery manufacturing, relevant to magnet materials and downstream demand ● Strategic location: Central EU access with integrated road, rail, and port infrastructure INCENTIVES & STRATEGIC SUPPORT ● Polish Investment Zone: Potential CIT/PIT tax exemptions for qualifying investments (up to 10 - 15 years) ● Government grants: Direct financial support linked to capex and job creation for strategic industrial projects ● EU funding support: Significant EU funding budgeted (2021 - 2027) supporting infrastructure and energy transition ● Skilled workforce: Strong talent base across chemistry, metallurgy, and engineering STRATEGIC OUTLOOK & MARKET DYNAMICS ● Increasing magnet demand: Global magnetic rare earth demand projected to increase more than seven-fold by 2040, from $9.7B in 2025 to $68.1B by 2040, according to Adamas Intelligence(5) ● EU processing mandate: CRMA requires 40% of strategic raw materials processed domestically by 2030(6) ● China concentration risk: China is estimated as controlling ~70% of global REE mining, according to United States Geological Survey(7), and ~90% of processing, making EU-based separation capacity strategically essential, according to International Energy Agency(8) ● EU magnet demand 6x by 2050: EU rare earth magnet demand expected to grow from 10,000 tonnes (2020) to 60,000 tonnes by 2050, according to European Raw Materials Alliance(9) Sources: (1) EY Europe Attractiveness Survey, May 2024 (2) European Commission, Economic forecast for Poland, May 2026 (3) PopulationPyramids, Poland Population Pyramid (2025) (4) Poland Government website, Fitch rating agency affirmed Poland's credit rating, revises outlook to negative, May 2025 (5) Adamas Intelligence, Global market for magnet rare earth oxides to increase 7-fold by 2040, January 2026 (6) Net Zero Compare, EU Critical Raw Materials Act (EU CRMA): EU Critical Raw Materials Act Secures Resources for the Green Transition (7) United States Geological Survey, Mineral Commodity Summaries, January 2025 (8) IEA, With new export controls on critical minerals, supply concentration risks become reality, October 2025 (9) European Raw Materials Alliance, Rare Earth Magnets and Motors: A European Call for Action, July 2021 21

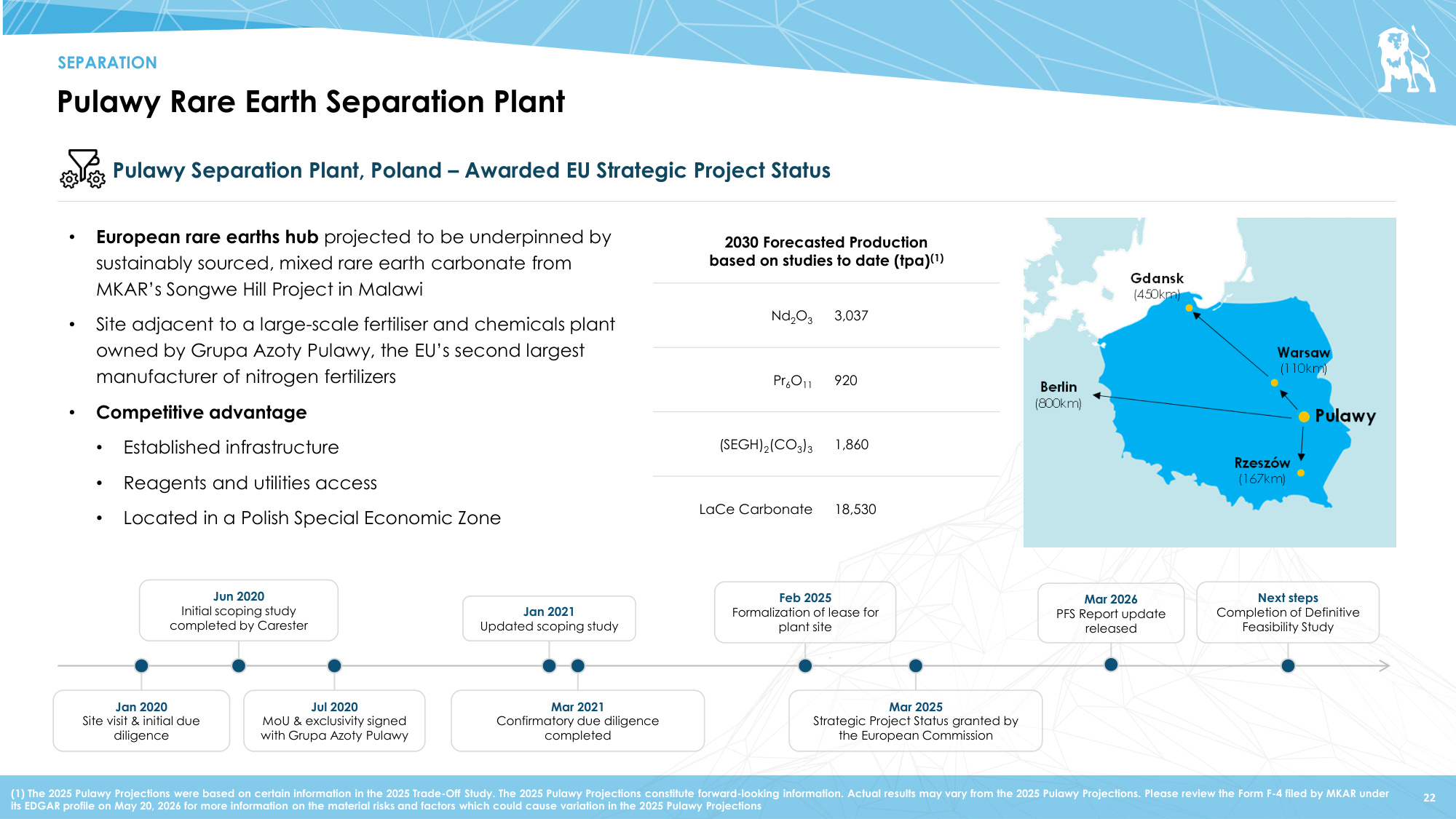

Pulawy Rare Earth Separation Plant Jan 2020 Site visit & initial due diligence Jun 2020 Initial scoping study completed by Carester Jul 2020 MoU & exclusivity signed with Grupa Azoty Pulawy Jan 2021 Updated scoping study Mar 2021 Confirmatory due diligence completed Next steps Completion of Definitive Feasibility Study 2030 Forecasted Production based on studies to date (tpa)(1) Nd2O3 3,037 Pr6O11 920 (SEGH)2(CO3)3 1,860 LaCe Carbonate 18,530 22 Pulawy Separation Plant, Poland – Awarded EU Strategic Project Status • European rare earths hub projected to be underpinned by sustainably sourced, mixed rare earth carbonate from MKAR's Songwe Hill Project in Malawi • Site adjacent to a large-scale fertiliser and chemicals plant owned by Grupa Azoty Pulawy, the EU's second largest manufacturer of nitrogen fertilizers • Competitive advantage • Established infrastructure • Reagents and utilities access • Located in a Polish Special Economic Zone SEPARATION Mar 2025 Strategic Project Status granted by the European Commission Mar 2026 PFS Report update released Feb 2025 Formalization of lease for plant site (1) The 2025 Pulawy Projections were based on certain information in the 2025 Trade-Off Study. The 2025 Pulawy Projections constitute forward-looking information. Actual results may vary from the 2025 Pulawy Projections. Please review the Form F-4 filed by MKAR under its EDGAR profile on May 20, 2026 for more information on the material risks and factors which could cause variation in the 2025 Pulawy Projections

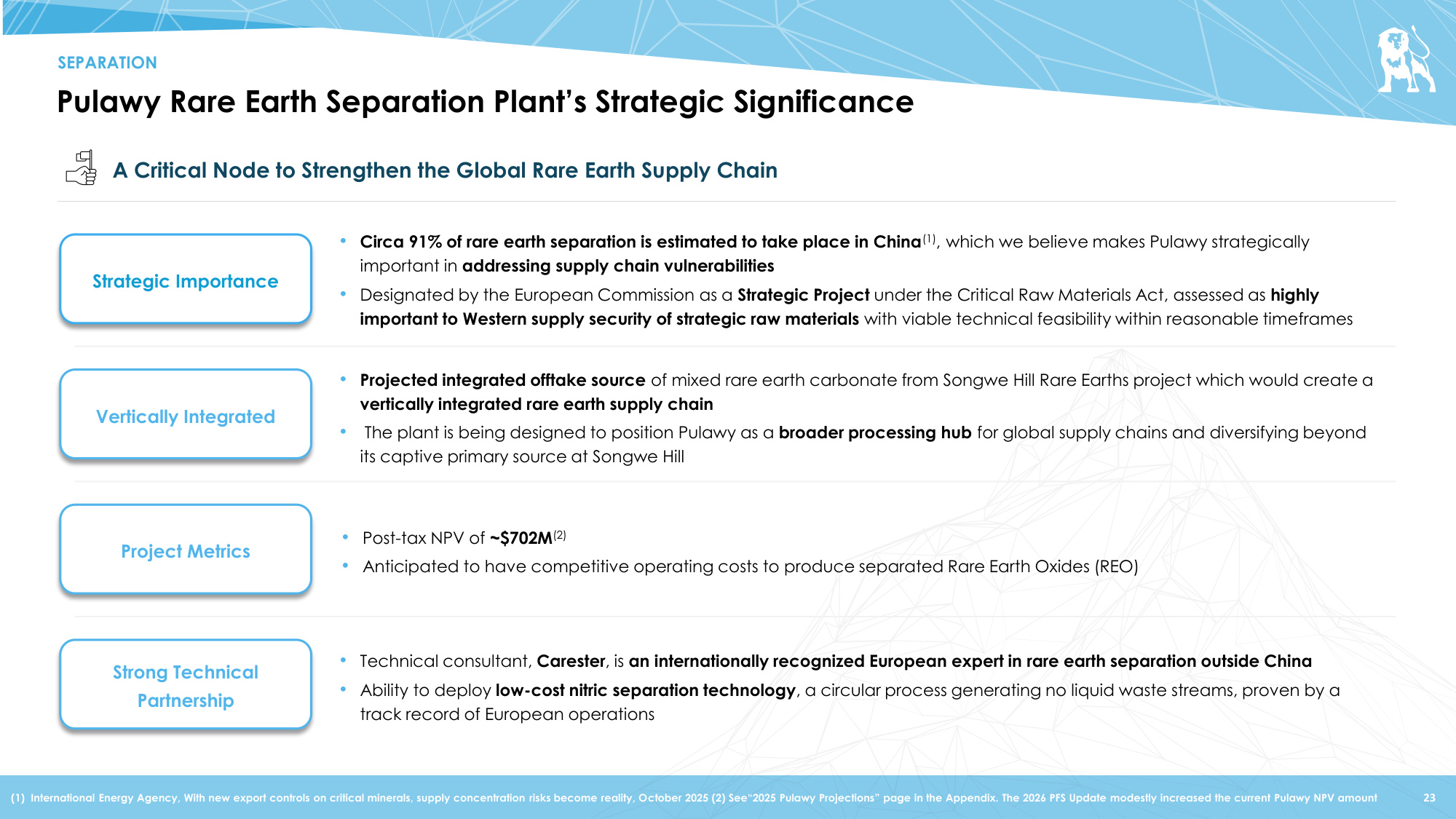

Pulawy Rare Earth Separation Plant's Strategic Significance 23 SEPARATION A Critical Node to Strengthen the Global Rare Earth Supply Chain Strategic Importance Vertically Integrated Project Metrics Strong Technical Partnership • Circa 91% of rare earth separation is estimated to take place in China(1), which we believe makes Pulawy strategically important in addressing supply chain vulnerabilities • Designated by the European Commission as a Strategic Project under the Critical Raw Materials Act, assessed as highly important to Western supply security of strategic raw materials with viable technical feasibility within reasonable timeframes • Projected integrated offtake source of mixed rare earth carbonate from Songwe Hill Rare Earths project which would create a vertically integrated rare earth supply chain • The plant is being designed to position Pulawy as a broader processing hub for global supply chains and diversifying beyond its captive primary source at Songwe Hill • Post-tax NPV of ~$702M(2) • Anticipated to have competitive operating costs to produce separated Rare Earth Oxides (REO) • Technical consultant, Carester, is an internationally recognized European expert in rare earth separation outside China • Ability to deploy low-cost nitric separation technology, a circular process generating no liquid waste streams, proven by a track record of European operations (1) International Energy Agency, With new export controls on critical minerals, supply concentration risks become reality, October 2025 (2) See"2025 Pulawy Projections" page in the Appendix. The 2026 PFS Update modestly increased the current Pulawy NPV amount

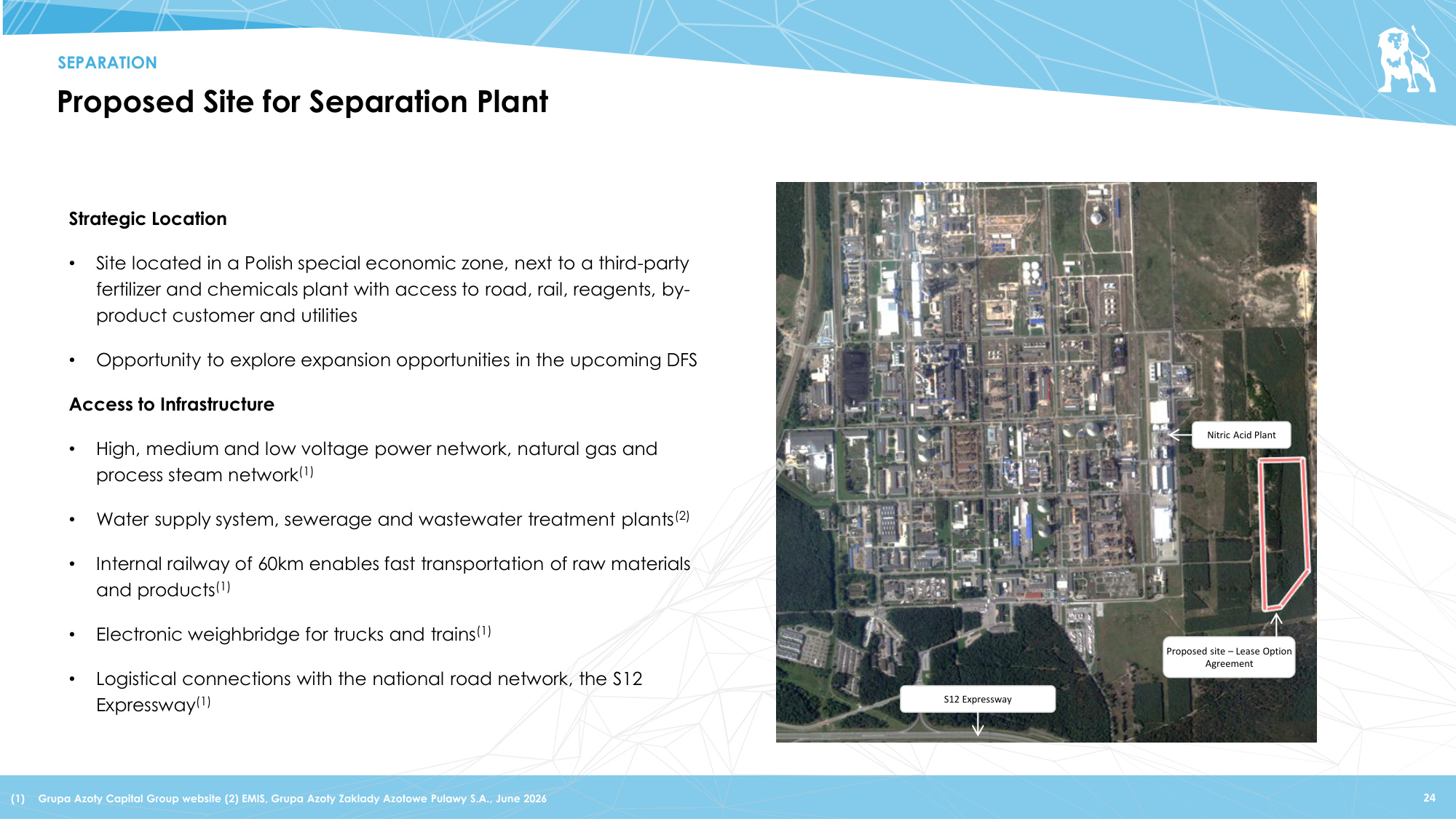

Proposed Site for Separation Plant SEPARATION 24 Strategic Location • Site located in a Polish special economic zone, next to a third-party fertilizer and chemicals plant with access to road, rail, reagents, by- product customer and utilities • Opportunity to explore expansion opportunities in the upcoming DFS Access to Infrastructure • High, medium and low voltage power network, natural gas and process steam network(1) • Water supply system, sewerage and wastewater treatment plants(2) • Internal railway of 60km enables fast transportation of raw materials and products(1) • Electronic weighbridge for trucks and trains(1) • Logistical connections with the national road network, the S12 Expressway(1) Proposed site – Lease Option Agreement S12 Expressway Nitric Acid Plant (1) Grupa Azoty Capital Group website (2) EMIS, Grupa Azoty Zaklady Azotowe Pulawy S.A., June 2026

Key Value Drivers MKANGO RARE EARTHS LIMITED

Mkango's Value Proposition at a Glance SNAPSHOT 26 Snapshot Across Key Value Drivers(1) Priced at a Significant Discount to Project Estimated NPVs • Songwe Hill Rare Earths Project NPV: $339M • Pulawy Separation Plant: $702M • $488M(2) Implied Pro Forma Enterprise Value represents a 53% discount to the combined NPV of $1.04B Reserve & Resource Potential • Total Reserves: 18.1Mt with 1.16% TREO • Measured & Indicated Resources: 4.1Mt (3) with 1.04% TREO • Inferred Resources: 55.9Mt with 1.05% TREO Projected High Conversion from Raw Resource to MREC • Songwe Hill Rare Earths Project is expected to produce a purified mixed rare earth carbonate (MREC) grading ~55% TREO on a dry basis • High conversion from raw resource to final MREC output • Critical magnet rare earth oxides (Nd, Pr, Dy, Tb) account for over 90% of the basket value Vertically Integrated Value Proposition • Integrated mine-to-separation model capturing full value chain economics • 3rd Party validation with recognition from global governments • $4.6M in DFC funding secured for Songwe Hill Rare Earths Project to advance FEED and value engineering studies Sources: Mkango F-4 filed on May 20, 2026 (1) See "2026 Songwe Hill Projections" "2025 Pulawy Projections" and "Mineral Resources and Mineral Reserves Summary" pages in the Appendix for more information (2) See Slide 6 for calculation of Implied Pro Forma Enterprise Value (3) Exclusive of mineral reserves MKANGO RARE EARTHS LIMITED

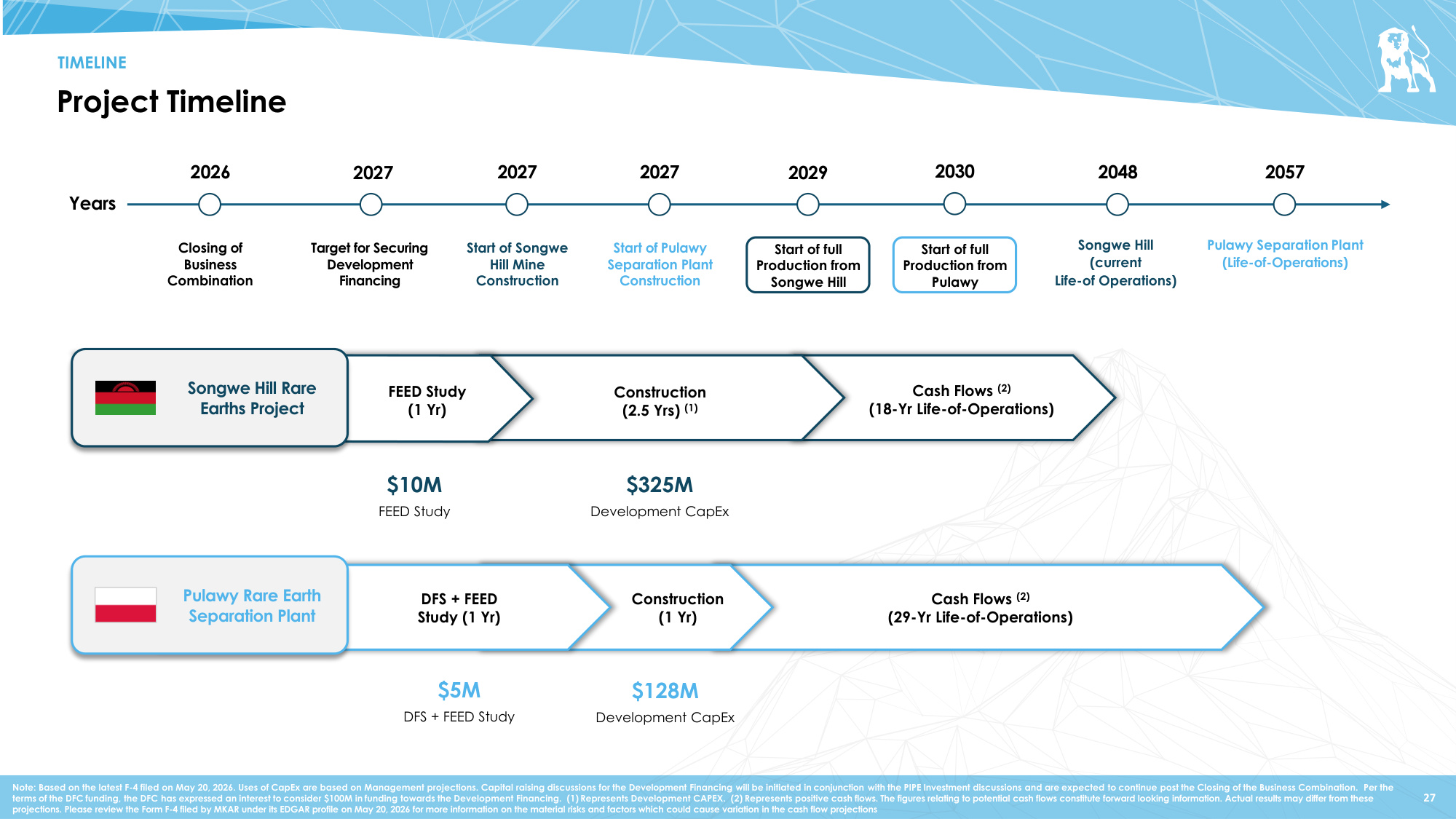

Project Timeline 27 Note: Based on the latest F-4 filed on May 20, 2026. Uses of CapEx are based on Management projections. Capital raising discussions for the Development Financing will be initiated in conjunction with the PIPE Investment discussions and are expected to continue post the Closing of the Business Combination. Per the terms of the DFC funding, the DFC has expressed an interest to consider $100M in funding towards the Development Financing. (1) Represents Development CAPEX. (2) Represents positive cash flows. The figures relating to potential cash flows constitute forward looking information. Actual results may differ from these projections. Please review the Form F-4 filed by MKAR under its EDGAR profile on May 20, 2026 for more information on the material risks and factors which could cause variation in the cash flow projections TIMELINE 2027 Start of Pulawy Separation Plant Construction 2057 Pulawy Separation Plant (Life-of-Operations) 2027 Start of Songwe Hill Mine Construction 2027 Target for Securing Development Financing 2026 Closing of Business Combination 2029 Start of full Production from Songwe Hill 2048 Songwe Hill (current Life-of Operations) Years FEED Study (1 Yr) Construction (2.5 Yrs) (1) Cash Flows (2) (18-Yr Life-of-Operations) DFS + FEED Study (1 Yr) Construction (1 Yr) Cash Flows (2) (29-Yr Life-of-Operations) $128M Development CapEx $10M FEED Study Songwe Hill Rare Earths Project Pulawy Rare Earth Separation Plant $325M Development CapEx $5M DFS + FEED Study 2030 Start of full Production from Pulawy

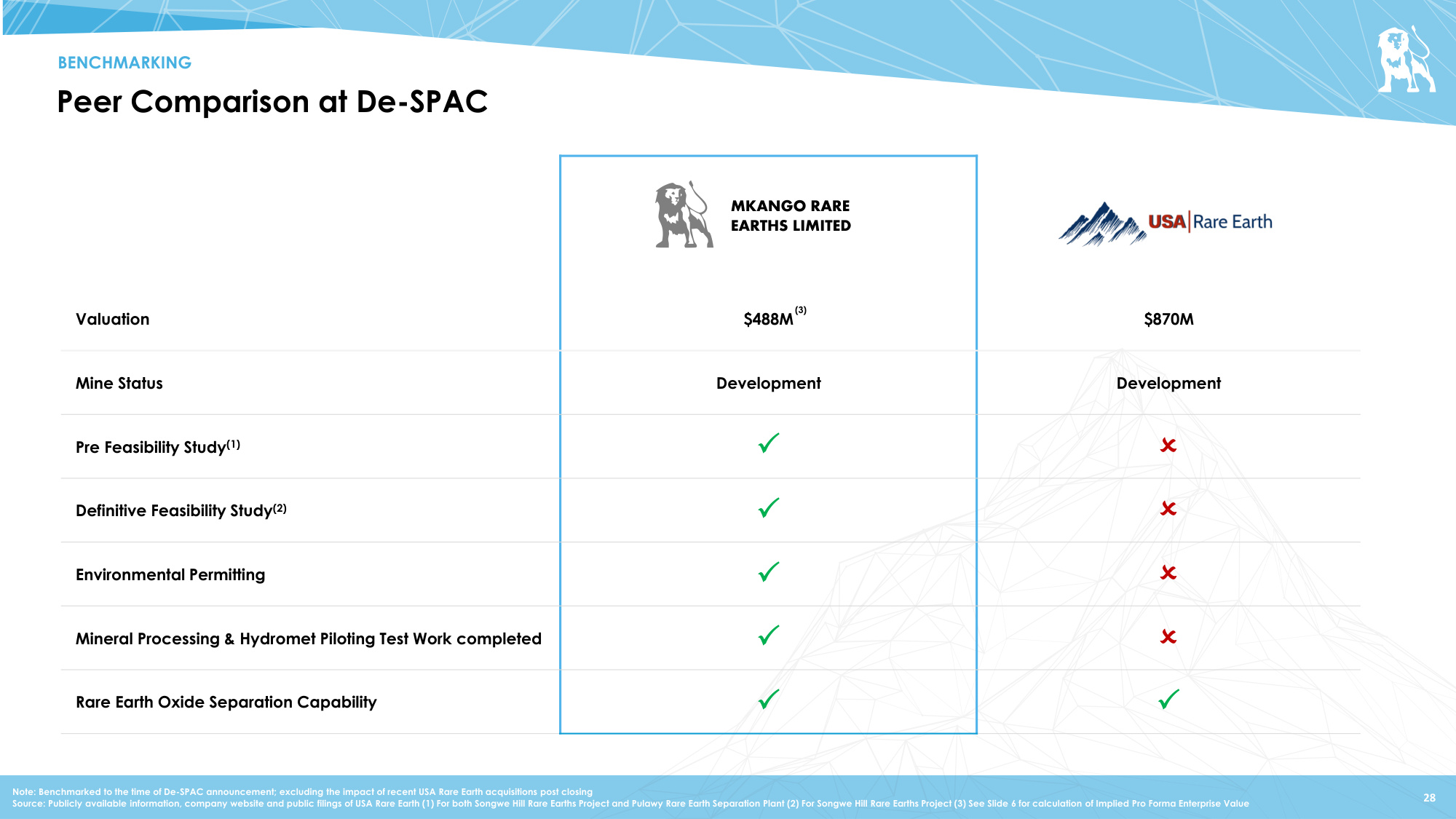

Valuation $488M $870M Mine Status Development Development Pre Feasibility Study(1) Definitive Feasibility Study(2) Environmental Permitting Mineral Processing & Hydromet Piloting Test Work completed Rare Earth Oxide Separation Capability Peer Comparison at De-SPAC BENCHMARKING 28 Note: Benchmarked to the time of De-SPAC announcement; excluding the impact of recent USA Rare Earth acquisitions post closing Source: Publicly available information, company website and public filings of USA Rare Earth (1) For both Songwe Hill Rare Earths Project and Pulawy Rare Earth Separation Plant (2) For Songwe Hill Rare Earths Project (3) See Slide 6 for calculation of Implied Pro Forma Enterprise Value MKANGO RARE EARTHS LIMITED (3)

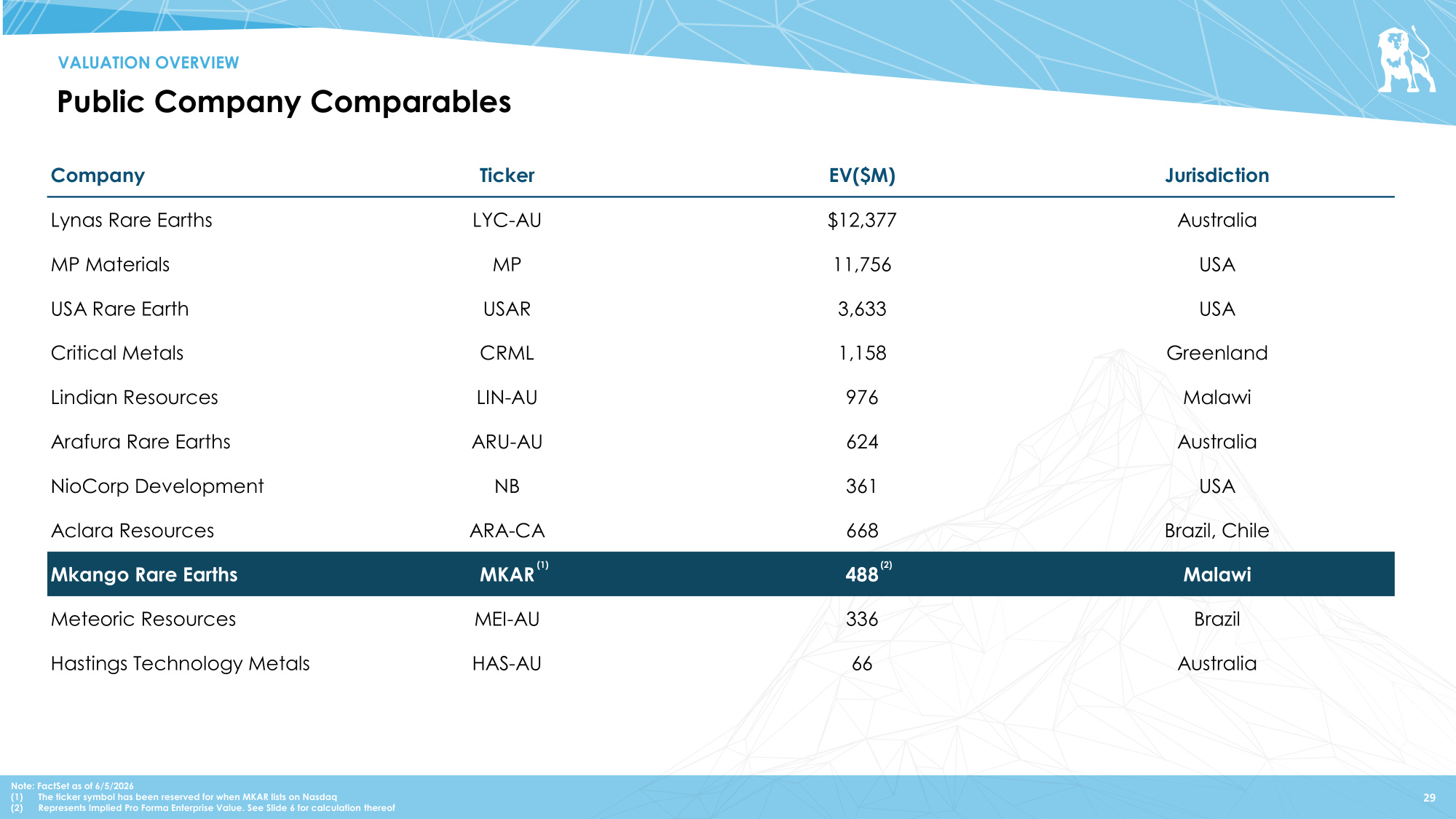

Company Ticker EV($M) Jurisdiction Lynas Rare Earths LYC-AU $12,377 Australia MP Materials MP 11,756 USA USA Rare Earth USAR 3,633 USA Critical Metals CRML 1,158 Greenland Lindian Resources LIN-AU 976 Malawi Arafura Rare Earths ARU-AU 624 Australia NioCorp Development NB 361 USA Aclara Resources ARA-CA 668 Brazil, Chile Mkango Rare Earths MKAR 488 Malawi Meteoric Resources MEI-AU 336 Brazil Hastings Technology Metals HAS-AU 66 Australia Public Company Comparables 29 VALUATION OVERVIEW Note: FactSet as of 6/5/2026 (1) The ticker symbol has been reserved for when MKAR lists on Nasdaq (2) Represents Implied Pro Forma Enterprise Value. See Slide 6 for calculation thereof (1) (2)

Appendix MKANGO RARE EARTHS LIMITED

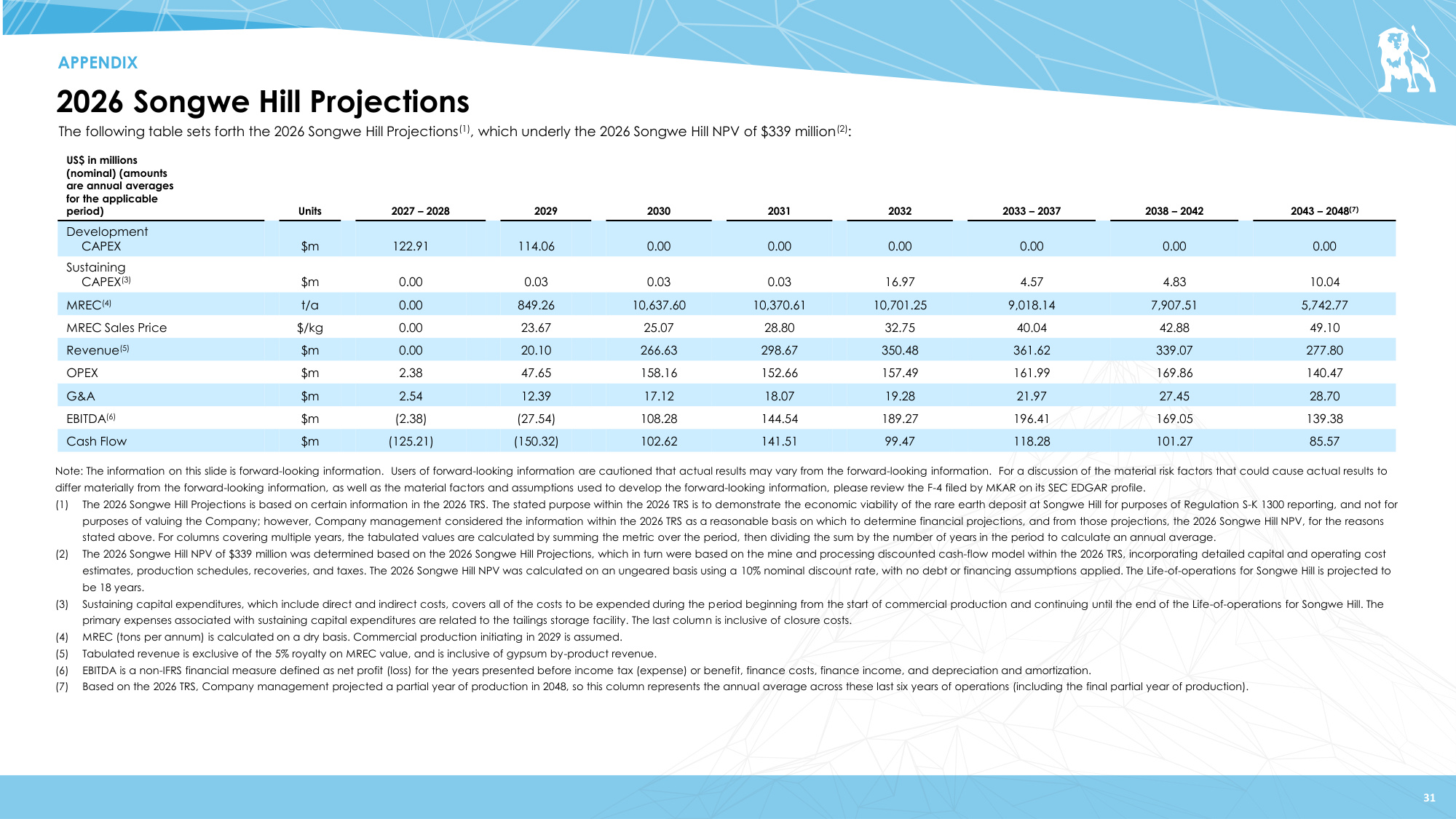

2026 Songwe Hill Projections 31 US$ in millions (nominal) (amounts are annual averages for the applicable period) Units 2027 – 2028 2029 2030 2031 2032 2033 – 2037 2038 – 2042 2043 – 2048(7) Development CAPEX $m 122.91 114.06 0.00 0.00 0.00 0.00 0.00 0.00 Sustaining CAPEX(3) $m 0.00 0.03 0.03 0.03 16.97 4.57 4.83 10.04 MREC(4) t/a 0.00 849.26 10,637.60 10,370.61 10,701.25 9,018.14 7,907.51 5,742.77 MREC Sales Price $/kg 0.00 23.67 25.07 28.80 32.75 40.04 42.88 49.10 Revenue(5) $m 0.00 20.10 266.63 298.67 350.48 361.62 339.07 277.80 OPEX $m 2.38 47.65 158.16 152.66 157.49 161.99 169.86 140.47 G&A $m 2.54 12.39 17.12 18.07 19.28 21.97 27.45 28.70 EBITDA(6) $m (2.38) (27.54) 108.28 144.54 189.27 196.41 169.05 139.38 Cash Flow $m (125.21) (150.32) 102.62 141.51 99.47 118.28 101.27 85.57 Note: The information on this slide is forward-looking information. Users of forward-looking information are cautioned that actual results may vary from the forward-looking information. For a discussion of the material risk factors that could cause actual results to differ materially from the forward-looking information, as well as the material factors and assumptions used to develop the forward-looking information, please review the F-4 filed by MKAR on its SEC EDGAR profile. (1) The 2026 Songwe Hill Projections is based on certain information in the 2026 TRS. The stated purpose within the 2026 TRS is to demonstrate the economic viability of the rare earth deposit at Songwe Hill for purposes of Regulation S-K 1300 reporting, and not for purposes of valuing the Company; however, Company management considered the information within the 2026 TRS as a reasonable basis on which to determine financial projections, and from those projections, the 2026 Songwe Hill NPV, for the reasons stated above. For columns covering multiple years, the tabulated values are calculated by summing the metric over the period, then dividing the sum by the number of years in the period to calculate an annual average. (2) The 2026 Songwe Hill NPV of $339 million was determined based on the 2026 Songwe Hill Projections, which in turn were based on the mine and processing discounted cash-flow model within the 2026 TRS, incorporating detailed capital and operating cost estimates, production schedules, recoveries, and taxes. The 2026 Songwe Hill NPV was calculated on an ungeared basis using a 10% nominal discount rate, with no debt or financing assumptions applied. The Life-of-operations for Songwe Hill is projected to be 18 years. (3) Sustaining capital expenditures, which include direct and indirect costs, covers all of the costs to be expended during the period beginning from the start of commercial production and continuing until the end of the Life-of-operations for Songwe Hill. The primary expenses associated with sustaining capital expenditures are related to the tailings storage facility. The last column is inclusive of closure costs. (4) MREC (tons per annum) is calculated on a dry basis. Commercial production initiating in 2029 is assumed. (5) Tabulated revenue is exclusive of the 5% royalty on MREC value, and is inclusive of gypsum by-product revenue. (6) EBITDA is a non-IFRS financial measure defined as net profit (loss) for the years presented before income tax (expense) or benefit, finance costs, finance income, and depreciation and amortization. (7) Based on the 2026 TRS, Company management projected a partial year of production in 2048, so this column represents the annual average across these last six years of operations (including the final partial year of production). APPENDIX The following table sets forth the 2026 Songwe Hill Projections(1), which underly the 2026 Songwe Hill NPV of $339 million(2):

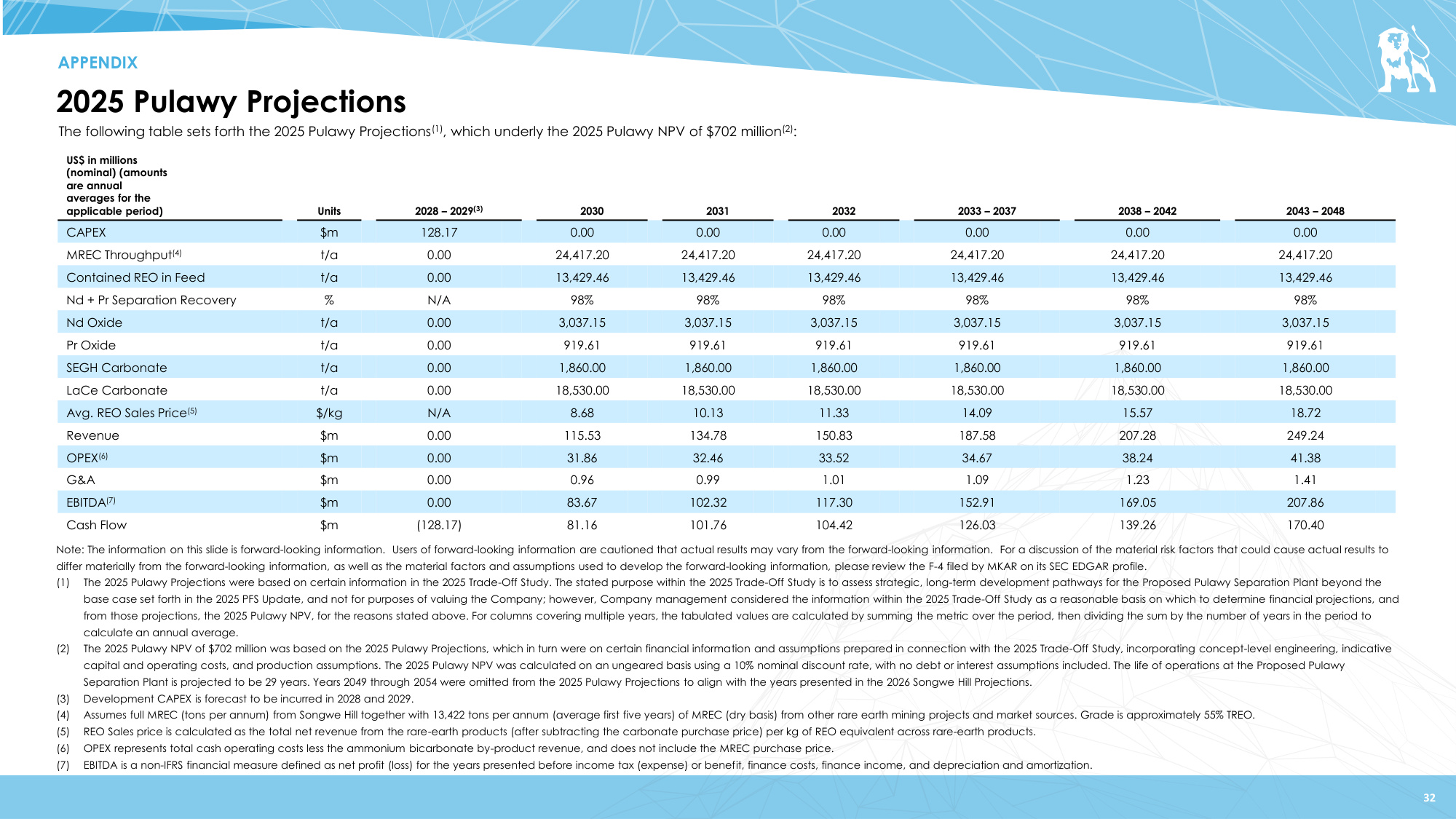

2025 Pulawy Projections 32 Note: The information on this slide is forward-looking information. Users of forward-looking information are cautioned that actual results may vary from the forward-looking information. For a discussion of the material risk factors that could cause actual results to differ materially from the forward-looking information, as well as the material factors and assumptions used to develop the forward-looking information, please review the F-4 filed by MKAR on its SEC EDGAR profile. (1) The 2025 Pulawy Projections were based on certain information in the 2025 Trade-Off Study. The stated purpose within the 2025 Trade-Off Study is to assess strategic, long-term development pathways for the Proposed Pulawy Separation Plant beyond the base case set forth in the 2025 PFS Update, and not for purposes of valuing the Company; however, Company management considered the information within the 2025 Trade-Off Study as a reasonable basis on which to determine financial projections, and from those projections, the 2025 Pulawy NPV, for the reasons stated above. For columns covering multiple years, the tabulated values are calculated by summing the metric over the period, then dividing the sum by the number of years in the period to calculate an annual average. (2) The 2025 Pulawy NPV of $702 million was based on the 2025 Pulawy Projections, which in turn were on certain financial information and assumptions prepared in connection with the 2025 Trade-Off Study, incorporating concept-level engineering, indicative capital and operating costs, and production assumptions. The 2025 Pulawy NPV was calculated on an ungeared basis using a 10% nominal discount rate, with no debt or interest assumptions included. The life of operations at the Proposed Pulawy Separation Plant is projected to be 29 years. Years 2049 through 2054 were omitted from the 2025 Pulawy Projections to align with the years presented in the 2026 Songwe Hill Projections. (3) Development CAPEX is forecast to be incurred in 2028 and 2029. (4) Assumes full MREC (tons per annum) from Songwe Hill together with 13,422 tons per annum (average first five years) of MREC (dry basis) from other rare earth mining projects and market sources. Grade is approximately 55% TREO. (5) REO Sales price is calculated as the total net revenue from the rare-earth products (after subtracting the carbonate purchase price) per kg of REO equivalent across rare-earth products. (6) OPEX represents total cash operating costs less the ammonium bicarbonate by-product revenue, and does not include the MREC purchase price. (7) EBITDA is a non-IFRS financial measure defined as net profit (loss) for the years presented before income tax (expense) or benefit, finance costs, finance income, and depreciation and amortization. APPENDIX US$ in millions (nominal) (amounts are annual averages for the applicable period) Units 2028 – 2029(3) 2030 2031 2032 2033 – 2037 2038 – 2042 2043 – 2048 CAPEX $m 128.17 0.00 0.00 0.00 0.00 0.00 0.00 MREC Throughput(4) t/a 0.00 24,417.20 24,417.20 24,417.20 24,417.20 24,417.20 24,417.20 Contained REO in Feed t/a 0.00 13,429.46 13,429.46 13,429.46 13,429.46 13,429.46 13,429.46 Nd + Pr Separation Recovery % N/A 98% 98% 98% 98% 98% 98% Nd Oxide t/a 0.00 3,037.15 3,037.15 3,037.15 3,037.15 3,037.15 3,037.15 Pr Oxide t/a 0.00 919.61 919.61 919.61 919.61 919.61 919.61 SEGH Carbonate t/a 0.00 1,860.00 1,860.00 1,860.00 1,860.00 1,860.00 1,860.00 LaCe Carbonate t/a 0.00 18,530.00 18,530.00 18,530.00 18,530.00 18,530.00 18,530.00 Avg. REO Sales Price(5) $/kg N/A 8.68 10.13 11.33 14.09 15.57 18.72 Revenue $m 0.00 115.53 134.78 150.83 187.58 207.28 249.24 OPEX(6) $m 0.00 31.86 32.46 33.52 34.67 38.24 41.38 G&A $m 0.00 0.96 0.99 1.01 1.09 1.23 1.41 EBITDA(7) $m 0.00 83.67 102.32 117.30 152.91 169.05 207.86 Cash Flow $m (128.17) 81.16 101.76 104.42 126.03 139.26 170.40 The following table sets forth the 2025 Pulawy Projections(1), which underly the 2025 Pulawy NPV of $702 million(2):

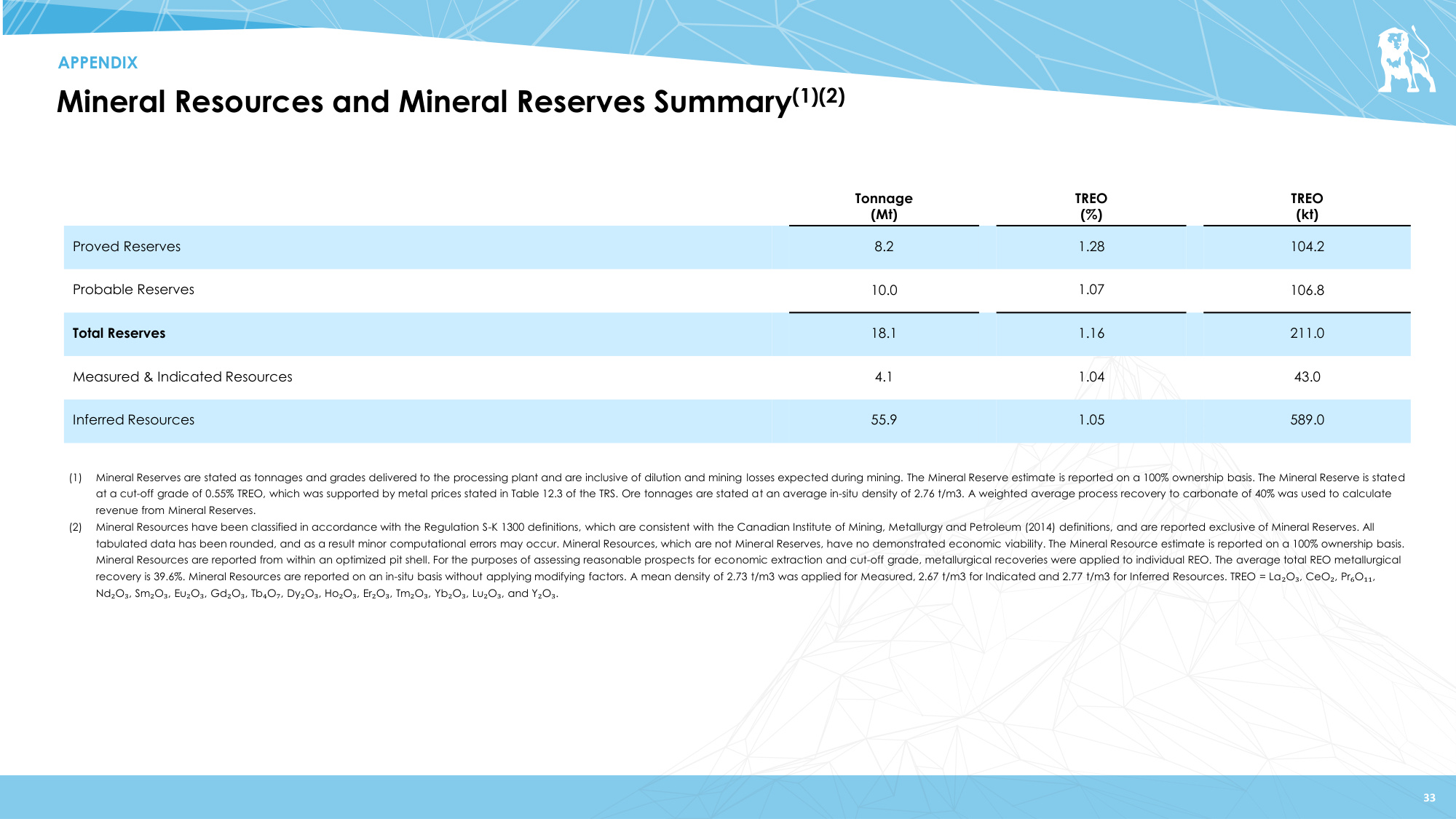

Mineral Resources and Mineral Reserves Summary(1)(2) 33 (1) Mineral Reserves are stated as tonnages and grades delivered to the processing plant and are inclusive of dilution and mining losses expected during mining. The Mineral Reserve estimate is reported on a 100% ownership basis. The Mineral Reserve is stated at a cut-off grade of 0.55% TREO, which was supported by metal prices stated in Table 12.3 of the TRS. Ore tonnages are stated at an average in-situ density of 2.76 t/m3. A weighted average process recovery to carbonate of 40% was used to calculate revenue from Mineral Reserves. (2) Mineral Resources have been classified in accordance with the Regulation S-K 1300 definitions, which are consistent with the Canadian Institute of Mining, Metallurgy and Petroleum (2014) definitions, and are reported exclusive of Mineral Reserves. All tabulated data has been rounded, and as a result minor computational errors may occur. Mineral Resources, which are not Mineral Reserves, have no demonstrated economic viability. The Mineral Resource estimate is reported on a 100% ownership basis. Mineral Resources are reported from within an optimized pit shell. For the purposes of assessing reasonable prospects for economic extraction and cut-off grade, metallurgical recoveries were applied to individual REO. The average total REO metallurgical recovery is 39.6%. Mineral Resources are reported on an in-situ basis without applying modifying factors. A mean density of 2.73 t/m3 was applied for Measured, 2.67 t/m3 for Indicated and 2.77 t/m3 for Inferred Resources. TREO = La₂O₃, CeO₂, Pr₆O₁₁, Nd₂O₃, Sm₂O₃, Eu₂O₃, Gd₂O₃, Tb₄O₇, Dy₂O₃, Ho₂O₃, Er₂O₃, Tm₂O₃, Yb₂O₃, Lu₂O₃, and Y₂O₃. APPENDIX Tonnage (Mt) TREO (%) TREO (kt) Proved Reserves 8.2 1.28 104.2 Probable Reserves 10.0 1.07 106.8 Total Reserves 18.1 1.16 211.0 Measured & Indicated Resources 4.1 1.04 43.0 Inferred Resources 55.9 1.05 589.0

S-K 1300 Definitions 34 Mineral Resources • A Mineral Resource is a concentration or occurrence of solid material of economic interest in or on the Earth's crust in such form, grade or quality and quantity that there are reasonable prospects for eventual economic extraction. The location, quantity, grade, continuity and other geological characteristics of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge, including sampling. • An Inferred Mineral Resource is that part of a Mineral Resource for which quantity and grade or quality are estimated based on limited geological evidence and sampling. Geological evidence is sufficient to imply but not verify geological and grade or quality continuity. An Inferred Resource has a lower level of confidence than that applying to an Indicated Mineral Resource and must not be converted to a Mineral Reserve. It is reasonably expected that the majority of an Inferred Mineral Resource could be upgraded to an Indicated Mineral Resource with continued exploration. • An Indicated Mineral Resource is that part of a Mineral Resource for which quantity, grade or quality, densities, shape and physical characteristics are estimated with sufficient confidence to allow the application of modifying factors in sufficient detail to support mine planning and evaluation of the economic viability of the deposit. Geological evidence is derived from adequately detailed and reliable exploration, sampling and testing and is sufficient to assume geological and grade or quality continuity between points of observation. • A Measured Mineral Resource is that part of a Mineral Resource for which quantity, grade or quality, densities, shape, and physical characteristics are estimated with confidence sufficient to allow the application of modifying factors to support detailed mine planning and final evaluation of the economic viability of the deposit. Geological evidence is derived from detailed and reliable exploration, sampling and testing and is sufficient to confirm geological and grade or quality continuity between points of observation. A Measured Mineral Resource has a higher level of confidence than that applying to either an Indicated or an Inferred Mineral Resource. It may be converted to either a Proven Mineral Reserve or a Probable Mineral Reserve. Mineral Reserves • A Mineral Reserve is the economically mineable part of a Measured and/or Indicated Mineral Resource. It includes diluting materials and allowances for losses, which may occur when the material is mined or extracted and is defined by studies at prefeasibility or feasibility level as appropriate that include application of modifying factors. Such studies demonstrate that, at the time of reporting, extraction could reasonably be justified. The reference point at which Mineral Reserves are defined, usually the point where the ore is delivered to the processing plant, must be stated. It is important that in all situations where the reference point is different, such as for a saleable product, a clarifying statement is included to ensure that the reader is fully informed as to what is being reported. • A Probable Mineral Reserve is the economically mineable part of an Indicated, and in some circumstances, a Measured Mineral Resource. The confidence in the modifying factors applying to a Probable Mineral Reserve is lower than that applying to a Proven Mineral Reserve. • A Proven Mineral Reserve is the economically mineable part of a Measured Mineral Resource. A Proven Mineral Reserve implies a high degree of confidence in the modifying factors. Feasibility Studies • A prefeasibility study is a comprehensive study of a range of options for the technical and economic viability of a mineral project that has advanced to a stage where a preferred mining method, in the case of underground mining, or the pit configuration, in the case of an open-pit, is established and an effective method of mineral processing is determined. It includes a financial analysis based on reasonable assumptions on the modifying factors and the evaluation of any other relevant factors which are sufficient for a competent person, acting reasonably, to determine if all or part of the Mineral Resource may be converted to a Mineral Reserve at the time of reporting. A prefeasibility study is at a lower confidence level than a feasibility study. • A feasibility study is a comprehensive technical and economic study of the selected development option for a mineral project that includes appropriately detailed assessments of applicable modifying factors together with any other relevant operational factors and detailed financial analysis that are necessary to demonstrate at the time of reporting that extraction is reasonably justified (economically mineable). The results of the study may reasonably serve as the basis for a final decision by a proponent or financial institution to proceed with, or finance, the development of the project. The confidence level of the study will be higher than that of a prefeasibility study. APPENDIX

MKANGO RARE EARTHS LIMITED THANK YOU