Exhibit 99.2

![]()

Management’s Discussion and Analysis

This management’s discussion and analysis (“MD&A”) of operations and financial condition for the second quarter of fiscal 2026, dated June 1, 2026, should be read in conjunction with the unaudited interim consolidated financial statements for the period ended April 30, 2026, which have been prepared in accordance with International Financial Reporting Standards (“IFRS”). This MD&A should also be read in conjunction with VersaBank’s MD&A and Audited Consolidated Financial Statements for the year ended October 31, 2025, which are available on VersaBank’s website at www.versabank.com, SEDAR+ at www.sedarplus.ca and EDGAR at www.sec.gov/edgar. Except as discussed below, all other factors discussed and referred to in the MD&A for the year ended October 31, 2025, remain substantially unchanged. All currency amounts in this document are in Canadian dollars unless otherwise indicated.

|

Cautionary Note Regarding Forward-Looking Statements |

2 |

|

About VersaBank |

3 |

|

Strategy |

4 |

|

Reorganization |

7 |

|

Overview of Performance |

8 |

|

Selected Financial Highlights |

14 |

|

Financial Review – Earnings |

15 |

|

Financial Review – Balance Sheet |

20 |

|

Off-Balance Sheet Arrangements |

29 |

|

Related Party Transactions |

29 |

|

Capital Management and Capital Resources |

30 |

|

Results of Operating Segments |

33 |

|

Summary of Quarterly Results |

37 |

|

Subsequent events |

38 |

|

Non-GAAP and Other Financial Measures |

38 |

|

Material Accounting Policies and Use of Estimates and Judgements |

41 |

|

Controls and Procedures |

41 |

|

Additional Information |

41 |

Cautionary Note Regarding Forward-Looking Statements

VersaBank’s public communications often include written or oral forward-looking statements. Statements of this type are included in this document and may also be included in other filings with Canadian securities regulators or the US Securities and Exchange Commission (the “SEC”), or in other communications. All such statements are made pursuant to the “safe harbor” provisions of, and are intended to be forward-looking statements under, the United States Private Securities Litigation Reform Act of 1995 and any applicable Canadian securities legislation. The statements in this management’s discussion and analysis that relate to future events or future performance including, without limitation, statements regarding the proposed Reorganization (see Reorganization section below) are forward-looking statements.

By their very nature, forward-looking statements involve inherent risks and uncertainties, both general and specific, many of which are beyond VersaBank’s control. There is a risk that predictions, forecasts, projections and other forward-looking statements will not be achieved. Readers are cautioned not to place undue reliance on these forward-looking statements, as a number of important factors could cause actual results to differ materially from the plans, objectives, expectations, estimates and intentions expressed in such statements. These factors include, but are not limited to: the strength of the Canadian and US economies in general and the local economies in which VersaBank operates; the effects of changes in monetary and fiscal policy, including changes in interest rate policies of the Bank of Canada and the US Federal Reserve; global commodity prices; the effects of competition in the markets in which VersaBank operates; inflation; capital market fluctuations; the timely development and introduction of new products in receptive markets; the impact of changes in laws, including trade laws and tariffs, and regulations applicable to financial services; changes in tax laws; technological changes, including the use of data and artificial intelligence (“AI”) in our business, including generative AI; unexpected judicial or regulatory proceedings; unexpected changes in consumer spending and savings habits; the impact of wars or conflicts and related effects on global supply chains and markets; the impact of outbreaks of disease or illness affecting local, national or international economies; the possible effects of terrorist activities; natural disasters and disruptions to public infrastructure (including transportation, communications, power or water supply); and VersaBank’s ability to anticipate and manage the risks associated with these factors.

Completion of the Reorganization is subject to numerous risks and uncertainties, many of which are beyond the Bank’s control, including but not limited to, the failure to obtain required shareholder, regulatory and other approvals, as well as other important factors disclosed previously and from time to time in the Bank’s filings with the SEC and with the securities commissions or similar regulatory authorities in each of the provinces or territories of Canada.

The foregoing list of important factors is not exhaustive. When relying on forward-looking statements to make decisions, investors and others should carefully consider the foregoing factors as well as other uncertainties and potential events. The forward-looking information contained in this management’s discussion and analysis is presented to assist VersaBank shareholders and others in understanding VersaBank’s financial position and may not be appropriate for any other purposes. Except as required by applicable securities laws, VersaBank does not undertake to update any forward-looking statement contained in this management’s discussion and analysis or made from time to time by VersaBank or on its behalf.

About VersaBank

Digital Banking Products and Services

VersaBank (“VersaBank” or the “Bank”) is a North American bank (federally chartered in Canada and the United States) with a difference. VersaBank was one of the world's first fully digital financial institutions. Today VersaBank employs a cloud-based, branchless, business-to-business model based on its proprietary state-of-the-art technology that enables it to profitably address underserved segments of the banking industry. The Bank’s business model is based on obtaining its deposits and providing financing digitally through other third-party financial intermediaries (referred to as “partners”) who, themselves, engage with the actual depositors and borrowers. This provides VersaBank with significant operating leverage, which drives efficiency and return on common equity, and significantly reduces the Bank’s risk.

VersaBank’s recent and expected continued growth is primarily the result of its unique Structured Receivable Program (“SRP”) (formerly referred to as the Receivable Purchase Program, or “RPP”), which invests in cash flow streams generated by credit assets originated and owned by companies that provide financing at the point of sale to consumers and small businesses for “big ticket” value purchases. In September 2024, following its acquisition of a US bank, VersaBank broadly launched its SRP, which has been highly successful in Canada for over 15 years, to the underserved multi-trillion-dollar US market.

Tokenized Deposit Services (Digital Meteor)

VersaBank has developed and owns proprietary intellectual property and technology to enable the next generation of digital assets for the banking and financial community, including the Bank’s revolutionary Real Bank Tokenized Deposits™ (“RBTD™”s) (formerly referred to as Digital Deposit Receipts, or DDRs). RBTD™s were developed exclusively by VersaBank using the Bank’s own banking and cybersecurity technologies, including VersaVault®. We believe that VersaVault® is the world’s first digital vault for security conscious organizations looking to secure their highly sensitive and confidential documents, data, code, blockchain-based assets and more.

VersaBank’s RBTD™s are proprietary bank-issued tokenized deposits that provide superior security, stability, and regulatory compliance compared to stablecoins, as highly encrypted digital representations of actual fiat currency deposits with the Bank, combining the safety and soundness of traditional banking with the efficiency, cost savings, security, and programmability of blockchain technology. In addition, the Bank expects its RBTD™s to be eligible for conventional federal deposit insurance (subject to confirmation by regulators in accordance with the FDIC and CDIC policies) and have the legal ability to pay interest, which non-bank issued stablecoins are not allowed to provide in the US.

VersaBank is also using its proprietary VersaVault® technology to address the need in both the United States and Canada to expand its regulated custody services to the digital asset market. The Bank signed a definitive agreement with Stablecorp Digital Currencies Inc. ("Stablecorp") in the first quarter of fiscal 2026 and now serves as the custodian for Stablecorp's QCAD stablecoin, which recently became Canada's first regulatory compliant Canadian-dollar stablecoin.

Cybersecurity Products and Services

VersaBank also owns Minnesota-based DRT Cyber Inc. (“DRTC”), a North America leader in the provision of cybersecurity services to address the rapidly growing volume of cyber threats challenging financial institutions, multi-national corporations and government entities. DRTC deploys technology solutions to support the functions of cybersecurity, privacy, and risk management, with experience across numerous sectors to enable it to develop and deploy flexible solutions to partners’ exact requirements. The majority of DRTC’s revenue is generated and the majority of DRTC’s costs are incurred by DRTC’s wholly owned subsidiaries, Digital Boundary Group, Inc. and Digital Boundary Group Canada Inc. (collectively “Digital Boundary Group”).

VersaBank’s common shares trade on the Toronto Stock Exchange and Nasdaq under the symbol VBNK. The underlying drivers of VersaBank’s performance changes for the current and comparative periods are set out in the following sections of this MD&A.

Strategy

VersaBank’s goal is to consistently and sustainably deliver outsized growth in earnings per share by utilizing its proprietary technology and established financial intermediary partner networks to deliver innovative digital banking, financial and related solutions to under-served markets, while maintaining its low-risk profile. The Bank’s use of proprietary technology in its cloud-based, branchless, business-to-business model enables significant operating leverage, enabling the Bank to grow its assets and resulting revenue at a significantly faster rate than its non-interest expenses. A significant portion of VersaBank’s workforce are software engineers and technology support staff who are continuously upgrading and enhancing VersaBank’s technologies and software, as well as developing new software to support new business initiatives.

Digital Banking Products and Services

VersaBank’s largest opportunity and primary focus is growth in revenue (driven primarily by growth in net interest income) from its Digital Banking Operations significantly in excess of growth in non-interest expense. VersaBank expects the majority of revenue growth to be driven by the ramp up of its unique SRP in the underserved multi-trillion-dollar US point-of-sale financing market. The SRP has driven the majority of VersaBank’s growth in Canada over the past five years.

VersaBank's SRP is an innovative and highly attractive digital funding solution for finance companies that provide loans and leases to consumers and small businesses for "big ticket" value purchases (e.g. consumer home improvement/HVAC projects and a wide variety of commercial and recreational equipment). It was specifically designed to address an unmet need by point-of-sale financing companies for consistently available, readily accessible, and economically attractive capital using VersaBank's proprietary, state-of-the-art banking technology. Consistent with its branchless, business-to-business, partner-based digital banking strategy, VersaBank's SRP enables it to access the massive and growing consumer and small business financing market in an indirect, efficient and highly risk-mitigated manner.

Following its acquisition of a US bank in September 2024, VersaBank broadly launched its SRP to the underserved multi-trillion-dollar US point-of-sale financing market. The Bank has a strong and growing pipeline of prospective SRP partners that it is aggressively pursuing. The Bank surpassed its first-year target of US$290 million with total US SRP assets of US$310 million in fiscal 2025. The Bank expects to continue to expand its business with existing US partners while adding new US partners in fiscal 2026 as the program scales.

In Canada, VersaBank remains focused on expanding its well-established SRP portfolio by deepening relationships with existing partners, adding new partners, and capturing growth opportunities driven by broader economic recovery and continued demand for SRP financing. VersaBank has access to sufficient low-cost deposit sources to fund its expected strong growth in credit assets. The Bank’s low-cost deposit sources, combined with the efficiency of its technology-based, business-to-business model, supports its objectives of maintaining a stable net interest margin over the short term and expanding its net interest margin over time. Management believes that VersaBank has one of the strongest liquidity risk profiles among North American banks, attributable to the quality, stability and stickiness of its deposit base. The majority of VersaBank’s Canadian and US deposits are sourced through deposit brokers, specifically the investment dealers, wealth management firms and financial advisory firms that distribute the Bank’s term deposit products. VersaBank has high visibility into the fixed maturities of these deposits, further enhancing its liquidity risk profile. In Canada, the Bank also sources deposits through Licensed Insolvency Trustee firms, which value the ability to use proprietary technology developed by VersaBank to seamlessly and efficiently interface with their respective administrative software, which results in a lower cost of funds to the Bank compared to conventional deposits. The Bank expects its Insolvency Trustee deposits to increase in the short- to medium-term as the number of insolvency filings in Canada is expected to grow.

Cybersecurity Products and Services

VersaBank’s wholly owned, Minnesota-based subsidiary, DRTC, generates the vast majority of its revenue and incurs the vast majority of its costs through Digital Boundary Group, which addresses the high-growth market for cybersecurity and related IT privacy services arising from the growing volume of cyber threats and privacy issues challenging businesses of all sizes across all sectors (with a specialty in financial institutions) and government entities on a daily basis. DRTC has established itself as a North American leader in the markets it serves, with more than 400 clients, including large financial services companies, critical infrastructure companies and indispensable government organizations such as metropolitan police departments. DRTC is focused on growing revenue through offering new products and services to existing clients and adding new clients, capitalizing on the significant expected long-term growth in the cybersecurity and privacy market globally.

Under the US Federal Reserve’s approval of VersaBank’s 2024 acquisition of a US bank, the Bank is required to cease or divest of certain impermissible activities, including the cybersecurity services housed within DRTC and Digital Boundary Group before September 2026, or such later date as may be permitted. Such divestment could be accomplished through a number of corporate actions, and the Bank has initiated a process to identify and evaluate strategic alternatives with the objective to maximize the value derived from the divestiture for shareholders.

Tokenized Deposit Services (Digital Meteor)

VersaBank also expects to capitalize on its leading-edge, proprietary technology enabling highly encrypted digital assets that combine the safety and soundness of traditional banking with the efficiency, cost savings, security, and flexibility of blockchain technology. VersaBank believes that its technology provides superior security, stability, and regulatory compliance compared to conventional alternatives. Held within its wholly owned subsidiary, DRTC, VersaBank’s RBTD™s are tokenized deposits, which are digital representations of traditional bank deposits on a blockchain, offering enhanced efficiency, programmability, and security in financial transactions. RBTD™s provide a trusted alternative for mainstream financial applications, including efficient payments, addressing the rapidly growing propensity of consumers and businesses to hold assets in e-wallets and engage in financial transactions digitally. VersaBank believes its RBTD™s represent the next step in the evolution of such digital assets and a superior alternative to stablecoins. VersaBank’s RBTD™s were conceived of and have been developed in compliance with the evolving regulatory requirements. We expect our RBTD™s to be eligible for conventional federal deposit insurance (subject to confirmation by regulators in accordance with the FDIC and CDIC policies) and to have the legal ability to pay interest. By contrast, stablecoins issued in the United States under the US GENIUS Act will not be permitted to pay interest and will not be eligible for federal deposit insurance, and in Canada, where stablecoin legislation has not yet come into force and still requires regulatory development, it is possible that similar restrictions could apply.

Management believes that licensed banks, as the trusted, regulated safekeepers of personal and business cash assets and other valuables, are naturally positioned to do the same for tokenized deposits. VersaBank has established itself as a leader in digital asset innovation. Management believes its trusted and secure solutions, along with the potential for RBTD™s to be an ultra-low-cost source of deposit funding, will play a meaningful role in enabling banks and other entities to confidently engage in the rapidly developing field of digital commerce. Management is encouraged by the favorable stance of the current US administration with respect to digital assets and the role they can play in the future of banking and commerce in the United States, as well as around the world. As a digital asset with a continuously known value, VersaBank’s RBTD™s provide a trusted alternative for mainstream financial applications and can be seamlessly converted to and from other digital currencies such as Bitcoin.

VersaBank is also using its proprietary VersaVault® technology to address the need in both the United States and Canada for regulated custody services for stablecoin issuers. The VersaVault system was audited and confirmed as compliant with System Organization Controls 2 Type 1 (“SOC2 Type 1”) in 2022. The Bank signed a definitive agreement with Stablecorp in early fiscal 2026 and now serves as the custodian for Stablecorp's QCAD stablecoin, which recently became first Canadian-dollar stablecoin which is compliant with application regulations.

The Bank expects both the issuance of its RBTD™s and the provision of stablecoin custody services to be an incremental source of low-cost deposits for its credit asset businesses, predominantly its SRP business.

Although the intellectual property, software and other assets related to VersaVault and the RBTD™ and stablecoin custody services technology currently reside within DRTC, they are not expected to be part of any divestiture of the cybersecurity services business within DRTC.

In addition, VersaBank remains highly committed to, and focused on, further developing and enhancing its technology advantage, a key component of its value proposition that not only provides efficient access to VersaBank’s chosen underserved lending and deposit markets, but also delivers superior financial products and better customer service to its clients.

The underlying drivers of VersaBank’s performance for the current and comparative periods are set out in the following sections of this MD&A.

Reorganization

Subsequent to the end of the second quarter, the Bank publicly filed a Form S-4 registration statement (the “Registration Statement”) with the US SEC in connection with the Bank’s proposed plan to realign its corporate structure to a standard US bank framework (the “Reorganization”). Specifically, the Reorganization, among other things, will cause Versa Bancorp, a new Delaware corporation (the “Parent”) to become the holding company of VersaBank and VersaBank USA National Association. The Registration Statement has been confidentially reviewed and remains subject to additional review by the SEC prior to being declared effective. As a result, the information contained therein is subject to change. Upon the Registration Statement being declared effective by the SEC, the Bank will be at liberty to convene a special meeting of shareholders at which it would seek approval of the Reorganization. In addition to the approval of shareholders, the completion of the Reorganization remains subject to various regulatory approvals, including approval by the Office of the Superintendent of Financial Institutions and Ministry of Finance in Canada and the Federal Reserve Board in the United States. VersaBank intends to proceed with the shareholder matters, expeditiously, and in tandem with the other regulatory processes.

Overview of Performance

Note Regarding VersaBank’s Second Quarter Fiscal 2026 Financial Results: VersaBank’s financial results for the second quarter of fiscal 2026 reflect non-core non-interest expenses in the amount of $6.7 million, comprised of $4.5 million related to the project costs associated with the Reorganization and a $2.2 million write-down of an intangible asset related to the customer deposit base of the Bank’s sole physical branch, which received regulatory approval for sale in the second quarter, requiring the Bank to record the write-down in the same quarter. The branch was sold on May 1, 2026 (see Subsequent event below).

The Reorganization is intended to enhance shareholder value, mitigate risk and reduce corporate costs over the long term. The Bank expects that the anticipated benefits of the Reorganization will exceed the associated investment however, these expected benefits are subject to various assumptions and uncertainties. The Bank incurred a significant portion of the costs associated with the Reorganization in fiscal 2025 and expects the Reorganization to be completed in fiscal 2026.

Note Regarding the Change in Name Of “Receivable Purchase Program” (“RPP”) To “Structured Receivable Program” (“SRP”): As part of its previously announced Reorganization (see note below), at the beginning of fiscal 2026, VersaBank has changed the name of its Receivable Purchase Program (“RPP”) to Structured Receivable Program (“SRP”). The underlying business model of the SRP has not changed in any way.

* See definition in the "Non-GAAP and Other Financial Measures" section below.

Recent Developments

|

The Bank continued to realize rapid expansion of its credit asset portfolio in the US through the successful ramp up of its SRP. Following the achievement of its first-year target for SRP credit assets and the signing of an agreement with its largest US SRP partner to date at the end of the Q4 2025, the Bank grew its total SRP assets to US$604.9 million at the end of the second quarter of fiscal 2026 and is on pace to achieve its target for additional US SRP fundings in fiscal 2026 of US$1 billion. |

|

The Bank commenced a pilot program with one of its major SRP partners, FinanceIt Canada Inc. ("FinanceIt"), for the Bank's new AI-enabled Real-Time Structured Receivable Program ("Real-Time SRP") (the "Pilot Program"). The Real-Time SRP is a breakthrough innovation in point-of-sale financing, providing the same reliable, economically attractive funding solution as the Bank's existing SRP, with the additional benefit of eliminating the need for SRP partners to warehouse multiple receivables over a period of time (typically from five to 30 or more days).The purpose of the Pilot Program is to demonstrate the functionality and operational integrity of the Real-Time SRP in a limited-scale, real-world scenario to refine the solution for full implementation by FinanceIt and simultaneous roll out to all of VersaBank's current and prospective SRP partners in both Canada and the United States. |

|

The Bank commenced a critical initiative to add foreign exchange functionality and other enhancements to its proprietary VersaView™ blockchain interface technology to support the commercialization of its RBTD™s. VersaView™ is the Bank's own highly secure RBTD™ Program Participant's user interface, enabling authorized RBTD™ partners and corporate customers (holders of RBTD™s) to view and transact with their RBTD™s stored in VersaVault®-managed wallets. The foreign exchange capability will be added to the integrated US and Canadian pilot programs for the Bank's RBTD™s that continue to steadily advance. |

|

The Bank began receiving QCAD deposits under its previously announced custody services agreement with Stablecorp, a pioneering Canadian digital asset infrastructure company and servicer of the QCAD Digital Trust and whose investors include Coinbase, Circle, DeFi Technologies and FTP Ventures. QCAD is Canada's first regulatory compliant Canadian-dollar stablecoin. |

|

The Bank entered into a definitive agreement for the sale of certain assets associated with its sole physical bank branch in Holdingford, Minnesota to Stearns Bank National Association. The sale was approved by the Office of the Comptroller of the Currency ("OCC") during the second quarter and the transaction closed on May 1, 2026 (see Subsequent event below). |

Q2 2026 vs Q2 2025

|

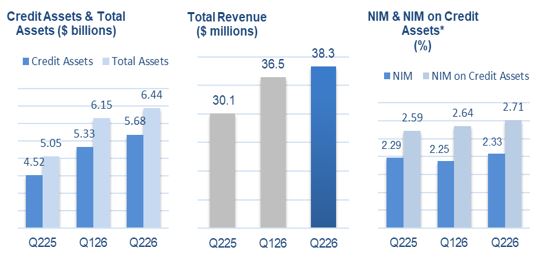

Credit assets increased 25% to a record $5.68 billion, driven primarily by strong growth in each of the US and Canadian SRP portfolios, which, combined, increased 32%. |

|

Total revenue increased 27% to a record $38.3 million, composed of record net interest income of $35.7 million and non-interest income of $2.6 million; |

|

Net interest margin (“NIM”) on credit assets was 2.71%, an increase of 12 bps. NIM was 2.33%, an increase of 4 bps. The increase in NIM was primarily due to lower cost of funds resulting from lower interest rates on renewals of maturing deposits throughout fiscal 2025 and the normalization of the yield curve from the atypically inverted yield curve that existed in the early part of fiscal 2025. The Bank’s NIM remains amongst the highest of the publicly traded Canadian Schedule I banks; |

|

Provision for credit losses (“PCL”) remain negligible at $428,000 compared with a PCL of $889,000, with the decrease being primarily due to updates in the forward-looking information used by VersaBank in its credit risk models; |

|

PCL as a percentage of average credit assets was 0.03% compared with 0.08%, which remains among the lowest of the publicly traded Canadian Schedule I banks; |

|

Non-interest expense, excluding the $6.7 million in non-core expenses composed of $4.5 million in project costs associated with the Reorganization and a $2.2 million intangible asset write-down, was $20.8 million compared with $17.5 million, with the increase primarily due to higher general operating costs consistent with increased business activities; |

|

Non-interest expenses, including the $6.7 million non-core costs noted above, were $27.5 million compared with $17.5 million; |

|

Adjusted (core) net income (excluding the $6.7 million charge noted above) was $12.4 million compared with $8.5 million (see Non-GAAP and Other Financial Measures), with the increase primarily due to higher revenues driven by growth in the Bank’s SRP portfolio, offset partially by incremental operating costs; |

|

Net income (including the $6.7 million in non-core expenses noted above) was $7.5 million compared with $8.5 million; |

|

Adjusted (core) income or earnings per common share (“Adjusted (core) EPS”) (excluding the $6.7 million in non-core expenses noted above) increased to $0.39 from $0.26, with the increase primarily due to higher revenues driven by the growth in the Bank’s SRP portfolio (see Non-GAAP and Other Financial Measures); |

|

Income or earnings per common share (“EPS”) (including the $6.7 million charge noted above) was $0.23 compared with $0.26; |

|

Adjusted (core) return on average common equity (excluding the $6.7 million in non-core expenses noted above) was 9.23% compared with 6.67% (see Non-GAAP and Other Financial Measures); |

|

Return on average common equity (including the $6.7 million in non-core expenses noted above) was 5.64% compared with 6.67%; |

|

Adjusted (core) efficiency ratio (excluding the $6.7 million in non-core expenses noted above) was 54% compared with 58% (see Non-GAAP and Other Financial Measures); and, |

|

Efficiency ratio (including the $6.7 million in non-core expenses noted above) was 72% compared with 58%. |

Q2 2026 vs Q1 2026

|

Credit assets increased 6% to a record $5.68 billion, driven primarily by strong growth in each of the US and Canadian SRP portfolios, which, combined, increased 7%; |

|

Total revenue increased 5% to a record $38.3 million, composed of a record net interest income of $35.7 million and non-interest income of $2.6 million; |

|

|

NIM on credit assets was 2.71%, an increase of 7 bps. NIM was 2.33%, an increase of 8 bps. The increase in NIM was primarily due to both an increase in yield generated on higher credit asset balance and lower cost of funds. The Bank’s NIM remains amongst the highest of the publicly traded Canadian Schedule I banks; |

|

PCL remained negligible at $428,000 compared with a provision for credit losses of $700,000, with the decrease being primarily due to updates in the forward-looking information used by VersaBank in its credit risk models; |

|

PCL as a percentage of average credit assets was 0.03% compared with 0.05%, which remains among the lowest of the publicly traded Canadian Schedule I banks; |

|

Non-interest expense, excluding the $6.7 million in non-core expenses composed of $4.5 million in project costs associated with the Reorganization and a $2.2 million intangible asset write down resulting from the sale of the Bank’s sole physical branch, was $20.8 million compared with $19.0 million (which excludes Reorganization project costs of $1.5 million); |

|

Non-interest expenses, including the $6.7 million charge noted above, were $27.5 million compared with $20.5 million (which included Reorganization costs of $1.5 million); |

|

Adjusted (core) net income (excluding the $6.7 million in non-core expenses noted above) was $12.4 million compared with $12.2 million (see Non-GAAP and Other Financial Measures), with the increase primarily due to higher revenues driven by growth in the Bank’s SRP portfolio; |

|

Net income (including the $6.7 million in non-core expenses noted above) was $7.5 million compared with $11.1 million, with the decrease primarily due to higher non-interest expenses, offset partially by higher revenues driven by the Bank’s expanding SRP portfolio; |

|

Adjusted (core) EPS (excluding the $6.7 million in non-core expenses noted above) increased to $0.39 from $0.38 (see Non-GAAP and Other Financial Measures); |

|

EPS (including the $6.7 million project non-core expenses noted above) was $0.23 compared with $0.35; |

|

Adjusted (core) return on average common equity (excluding the $6.7 million non-core expenses noted above) was 9.23% compared with 8.95% (see Non-GAAP and Other Financial Measures); |

|

Return on average common equity (including the $6.7 million in non-core expenses noted above) was 5.64% compared with 8.16%; |

|

Adjusted (core) efficiency ratio (excluding the $6.7 million charge noted above) was 54% compared with 52% (see Non-GAAP and Other Financial Measures); and, |

|

Efficiency ratio (including the $6.7 million charge noted above) was 72% compared with 56% and reflects the fixed cost structure of the Bank's US operations to support the US SRP program at scale during a period when the US SRP is in its ramp up phase. The Bank's US operations at scale are expected to be significantly more efficient than its Canadian operations. |

Q2 YTD 2026 vs Q2 YTD 2025

|

Credit assets increased 25% to a record $5.68 billion, driven primarily by strong growth in each of the US and Canadian SRP portfolios, which, combined, increased 32%; |

|

Total revenue increased 29% to a record $74.8 million, composed of a record net interest income of $69.6 million and non-interest income of $5.2 million; |

|

NIM on credit assets was 2.65%, an increase of 21 bps. NIM was 2.29%, an increase of 10 bps. The increase in NIM was primarily due to lower cost of funds resulting from lower interest rates on renewals of maturing deposits throughout fiscal 2025 and the normalization of the yield curve from the atypically inverted yield curve that existed in the early part of fiscal 2025, offset partially by lower yield stemming from the continued growth in the SRP portfolio, which is composed of lower regulatory risk-weighted, lower yielding assets compared to the some higher yielding, higher regulatory risk-weighted Multi-Family Residential Loans (“MROL”). The Bank’s NIM remains amongst the highest of the publicly traded Canadian Schedule I banks; |

|

PCL remained negligible at $1.1 million compared with $1.9 million, with the decrease being primarily due to updates in the forward-looking information used by VersaBank in its credit risk models; |

|

PCL as a percentage of average credit assets was 0.04% compared with 0.09%, which remains among the lowest of the publicly traded Canadian Schedule I banks; |

|

Non-interest expense, excluding the $8.2 million of non-core expenses composed of $6.0 million in costs associated with the Reorganization and a $2.2 million intangible asset write down resulting from the sale of the Bank’s sole physical branch, was $39.8 million compared with $33.2 million, with the increase primarily due to higher general operating costs consistent with increased business activities; |

|

Non-interest expenses, including the $8.2 million in non-core expenses noted above, were $48.0 million compared with $33.2 million; |

|

Adjusted (core) net income (excluding the $8.2 million in non-core expenses noted above) was $24.5 million compared with $16.7 million (see Non-GAAP and Other Financial Measures), with the increase primarily due to higher revenues driven by growth in the Bank’s SRP portfolio, offset partially by higher non-interest expenses; |

|

Net income (including the $8.2 million in non-core expenses noted above) increased to $18.6 million compared with $16.7 million; |

|

Adjusted (core) EPS (excluding the $8.2 million in non-core expenses noted above) increased to $0.77 from $0.54, with the increase primarily due to higher revenues driven by the Bank’s expanding SRP portfolio with the growth of VersaBank USA operations (see Non-GAAP and Other Financial Measures); |

|

EPS (including the $8.2 million in non-core expenses noted above) was $0.58 compared with $0.54; |

|

Adjusted (core) return on average common equity (excluding the $8.2 million in non-core expenses noted above) was 9.07% compared with 7.25% (see Non-GAAP and Other Financial Measures); |

|

Return on average common equity (including the $8.2 million charge noted above) was 6.91% compared with 7.25%; |

|

Adjusted (core) efficiency ratio (excluding the $8.2 million project costs noted above) was 53% compared with 57% (see Non-GAAP and Other Financial Measures); and, |

|

Efficiency ratio (including the $8.2 million charge noted above) was 64% compared with 57% and reflects the fixed cost structure of the Bank's US operations to support the US SRP program at scale during a period when the US SRP is in its ramp up phase. The Bank's US operations at scale are expected to be significantly more efficient than its Canadian operations. |

Selected Financial Highlights

|

(unaudited) |

for the three months ended |

for the six months ended |

||||||||||||||

|

April 30 |

April 30 |

April 30 |

April 30 |

|||||||||||||

|

(thousands of Canadian dollars, except per share amounts) |

2026 |

2025 |

2026 |

2025 |

||||||||||||

|

Results of operations |

||||||||||||||||

|

Interest income |

$ | 83,060 | $ | 70,976 | $ | 164,276 | $ | 144,222 | ||||||||

|

Net interest income |

35,679 | 28,032 | 69,560 | 53,756 | ||||||||||||

|

Non-interest income |

2,614 | 2,107 | 5,247 | 4,210 | ||||||||||||

|

Total revenue |

38,293 | 30,139 | 74,807 | 57,966 | ||||||||||||

|

Provision for credit losses |

428 | 889 | 1,128 | 1,913 | ||||||||||||

|

Non-interest expenses |

27,486 | 17,516 | 48,032 | 33,215 | ||||||||||||

|

Digital Banking |

25,052 | 14,418 | 42,825 | 27,196 | ||||||||||||

|

DRTC |

2,509 | 2,734 | 5,344 | 5,700 | ||||||||||||

|

Digital Meteor |

268 | 719 | 552 | 1,028 | ||||||||||||

|

Net income |

7,525 | 8,529 | 18,594 | 16,672 | ||||||||||||

|

Adjusted (Core) net income* |

12,378 | 8,529 | 24,540 | 16,672 | ||||||||||||

|

Income per common share: |

||||||||||||||||

|

Basic |

$ | 0.23 | $ | 0.26 | $ | 0.58 | $ | 0.54 | ||||||||

|

Diluted |

$ | 0.23 | $ | 0.26 | $ | 0.58 | $ | 0.54 | ||||||||

|

Adjusted (Core) income per common share basic and diluted* |

$ | 0.39 | $ | 0.26 | $ | 0.77 | $ | 0.54 | ||||||||

|

Dividends paid on common shares |

$ | 802 | $ | 813 | $ | 1,601 | $ | 1,626 | ||||||||

|

Yield* |

5.42 | % | 5.81 | % | 5.41 | % | 5.88 | % | ||||||||

|

Cost of funds* |

3.09 | % | 3.52 | % | 3.12 | % | 3.69 | % | ||||||||

|

Net interest margin* |

2.33 | % | 2.29 | % | 2.29 | % | 2.19 | % | ||||||||

|

Net interest margin on credit assets* |

2.71 | % | 2.59 | % | 2.65 | % | 2.44 | % | ||||||||

|

Return on average common equity* |

5.64 | % | 6.67 | % | 6.91 | % | 7.25 | % | ||||||||

|

Adjusted (Core) return on average common equity* |

9.23 | % | 6.67 | % | 9.07 | % | 7.25 | % | ||||||||

|

Book value per common share* |

$ | 17.15 | $ | 16.25 | $ | 17.15 | $ | 16.25 | ||||||||

|

Efficiency ratio* |

72 | % | 58 | % | 64 | % | 57 | % | ||||||||

|

Adjusted (Core) efficiency ratio* |

54 | % | 58 | % | 53 | % | 57 | % | ||||||||

|

Return on average total assets* |

0.49 | % | 0.70 | % | 0.61 | % | 0.68 | % | ||||||||

|

Provision for (recovery of) credit losses as a % of average credit assets* |

0.03 | % | 0.08 | % | 0.04 | % | 0.09 | % | ||||||||

|

as at |

||||||||||||||||

|

Balance Sheet Summary |

||||||||||||||||

|

Cash |

$ | 568,161 | $ | 340,186 | $ | 568,161 | $ | 340,186 | ||||||||

|

Securities |

106,277 | 104,807 | 106,277 | 104,807 | ||||||||||||

|

Credit assets, net of allowance for credit losses |

5,675,879 | 4,523,812 | 5,675,879 | 4,523,812 | ||||||||||||

|

Average credit assets |

5,504,579 | 4,435,280 | 5,371,129 | 4,379,964 | ||||||||||||

|

Total assets |

6,440,700 | 5,047,133 | 6,440,700 | 5,047,133 | ||||||||||||

|

Deposits |

5,520,909 | 4,205,185 | 5,520,909 | 4,205,185 | ||||||||||||

|

Subordinated notes payable |

100,688 | 101,844 | 100,688 | 101,844 | ||||||||||||

|

Shareholders' equity |

552,238 | 528,306 | 552,238 | 528,306 | ||||||||||||

|

Capital ratios** |

||||||||||||||||

|

Risk-weighted assets |

$ | 4,285,370 | $ | 3,551,398 | $ | 4,285,370 | $ | 3,551,398 | ||||||||

|

Common Equity Tier 1 capital |

527,758 | 507,222 | 527,758 | 507,222 | ||||||||||||

|

Total regulatory capital |

631,623 | 615,770 | 631,623 | 615,770 | ||||||||||||

|

Common Equity Tier 1 (CET1) ratio |

12.32 | % | 14.28 | % | 12.32 | % | 14.28 | % | ||||||||

|

Tier 1 capital ratio |

12.32 | % | 14.28 | % | 12.32 | % | 14.28 | % | ||||||||

|

Total capital ratio |

14.74 | % | 17.34 | % | 14.74 | % | 17.34 | % | ||||||||

|

Leverage ratio |

7.94 | % | 9.61 | % | 7.94 | % | 9.61 | % | ||||||||

|

* See definition in "Non-GAAP and Other Financial Measures" section below. |

|

** Capital management and leverage measures are in accordance with OSFI's Capital Adequacy Requirements and Basel III Accord. |

Financial Review – Earnings

Total Revenue

Total revenue, which consists of net interest income and non-interest income, for the quarter ended April 30, 2026 increased 27% to a record $38.3 million compared with the same period a year ago and increased 5% compared with the first quarter of fiscal 2026. Total revenue for the six months ended April 30, 2026 increased 29% to $74.8 million compared with the same period last year.

Net Interest Income

|

(thousands of Canadian dollars) |

||||||||||||||||||||||||||||||||

|

For the three months ended: |

For the six months ended: |

|||||||||||||||||||||||||||||||

|

April 30 |

January 31 |

April 30 |

April 30 |

April 30 |

||||||||||||||||||||||||||||

|

2026 |

2026 |

Change |

2025 |

Change |

2026 |

2025 |

Change |

|||||||||||||||||||||||||

|

Interest income |

||||||||||||||||||||||||||||||||

|

Structured receivable program |

$ | 64,419 | $ | 61,322 | 5 | % | $ | 50,584 | 27 | % | $ | 125,741 | $ | 101,039 | 24 | % | ||||||||||||||||

|

Multi-family residential loans and other |

13,266 | 14,330 | (7 | %) | 15,314 | (13 | %) | 27,596 | 31,818 | (13 | %) | |||||||||||||||||||||

|

Other |

5,375 | 5,564 | (3 | %) | 5,078 | 6 | % | 10,939 | 11,365 | (4 | %) | |||||||||||||||||||||

|

Interest income |

$ | 83,060 | $ | 81,216 | 2 | % | $ | 70,976 | 17 | % | $ | 164,276 | $ | 144,222 | 14 | % | ||||||||||||||||

|

Interest expense |

||||||||||||||||||||||||||||||||

|

Deposit and other |

$ | 46,033 | $ | 45,970 | 0 | % | $ | 41,551 | 11 | % | $ | 92,003 | $ | 87,681 | 5 | % | ||||||||||||||||

|

Subordinated notes |

1,348 | 1,365 | (1 | %) | 1,393 | (3 | %) | 2,713 | 2,785 | (3 | %) | |||||||||||||||||||||

|

Interest expense |

$ | 47,381 | $ | 47,335 | 0 | % | $ | 42,944 | 10 | % | $ | 94,716 | $ | 90,466 | 5 | % | ||||||||||||||||

|

Net interest income |

$ | 35,679 | $ | 33,881 | 5 | % | $ | 28,032 | 27 | % | $ | 69,560 | $ | 53,756 | 29 | % | ||||||||||||||||

|

Non-interest income |

$ | 2,614 | $ | 2,633 | (1 | %) | $ | 2,107 | 24 | % | $ | 5,247 | $ | 4,210 | 25 | % | ||||||||||||||||

|

Total revenue |

$ | 38,293 | $ | 36,514 | 5 | % | $ | 30,139 | 27 | % | $ | 74,807 | $ | 57,966 | 29 | % | ||||||||||||||||

Q2 2026 vs Q2 2025

Net interest income increased 27% to a record $35.7 million primarily due to:

|

Higher interest income attributable to continued SRP portfolio growth in Canada and in US. |

Offset partially by:

|

Higher interest expense attributable primarily to higher corresponding deposit balance growth to support the credit asset growth; and, |

|

The impact of the planned transition of some higher yielding, higher regulatory risk-weighted MROL to lower yielding, lower regulatory risk-weighted MROL as part of the Bank’s strategy to capitalize on opportunities for lower regulatory capital risk-weighted credit assets with a higher return on capital deployed. |

Q2 2026 vs Q1 2026

Net interest income increased by 5% to $35.7 million primarily due to:

|

Higher interest income attributable to continued SRP portfolio growth in Canada and in US. |

Offset partially by:

|

The impact of the planned transition of some higher yielding, higher regulatory risk-weighted MROL to lower yielding, lower regulatory risk-weighted MROL as part of the Bank’s strategy to capitalize on opportunities for lower regulatory capital risk-weighted credit assets with a higher return on capital deployed. |

Q2 YTD 2026 vs Q2 YTD 2025

Net interest income increased 29% to a record $69.6 million primarily due to:

|

Higher interest income attributable to continued SRP portfolio growth in Canada and in US. |

Offset partially by:

|

Higer interest expense attributable primarily to higher corresponding deposit balance growth to support the credit asset growth; and, |

|

The impact of the planned transition of some higher yielding, higher regulatory risk-weighted MROL to lower yielding, lower regulatory risk-weighted MROL as part of the Bank’s strategy to capitalize on opportunities for lower regulatory capital risk-weighted credit assets with a higher return on capital deployed. |

Net Interest Margin

|

(thousands of Canadian dollars) |

||||||||||||||||||||||||||||||||

|

For the three months ended: |

For the six months ended: |

|||||||||||||||||||||||||||||||

|

April 30 |

January 31 |

April 30 |

April 30 |

April 30 |

||||||||||||||||||||||||||||

|

2026 |

2026 |

Change |

2025 |

Change |

2026 |

2025 |

Change |

|||||||||||||||||||||||||

|

Interest income |

$ | 83,060 | $ | 81,216 | 2 | % | $ | 70,976 | 17 | % | $ | 164,276 | $ | 144,222 | 14 | % | ||||||||||||||||

|

Interest expense |

47,381 | 47,335 | 0 | % | 42,944 | 10 | % | 94,716 | 90,466 | 5 | % | |||||||||||||||||||||

|

Net interest income |

35,679 | 33,881 | 5 | % | 28,032 | 27 | % | 69,560 | 53,756 | 29 | % | |||||||||||||||||||||

|

Average assets |

$ | 6,293,355 | $ | 5,977,243 | 5 | % | $ | 5,009,433 | 26 | % | $ | 6,124,588 | $ | 4,942,809 | 24 | % | ||||||||||||||||

|

Yield* |

5.42 | % | 5.39 | % | 1 | % | 5.81 | % | (7 | %) | 5.41 | % | 5.88 | % | (8 | %) | ||||||||||||||||

|

Cost of funds* |

3.09 | % | 3.14 | % | (2 | %) | 3.52 | % | (12 | %) | 3.12 | % | 3.69 | % | (15 | %) | ||||||||||||||||

|

Net interest margin* |

2.33 | % | 2.25 | % | 4 | % | 2.29 | % | 2 | % | 2.29 | % | 2.19 | % | 5 | % | ||||||||||||||||

|

Average gross credit assets |

$ | 5,487,247 | $ | 5,183,260 | 6 | % | $ | 4,418,243 | 24 | % | $ | 5,354,227 | $ | 4,362,411 | 23 | % | ||||||||||||||||

|

Net interest margin on credit assets* |

2.71 | % | 2.64 | % | 3 | % | 2.59 | % | 5 | % | 2.65 | % | 2.44 | % | 9 | % | ||||||||||||||||

|

* See definition in "Non-GAAP and Other Financial Measures" section below. |

Q2 2026 vs Q2 2025

Net interest margin increased 4 bps primarily due to:

|

Reductions in the cost of funds due to lower rates on renewals of maturing deposits over the course of fiscal 2025, and; |

|

The normalization of the yield curve from the atypically inverted yield curve that existed in the early part of fiscal 2025. |

Offset partially by:

|

The continued growth in the SRP portfolio, which is composed of lower regulatory risk-weighted, lower yielding assets; and a reduction in cost of funds resulting from the renewal of maturing deposits at lower interest rates; and, |

|

The impact of the planned transition of some higher yielding, higher regulatory risk-weighted MROL to lower yielding, lower regulatory risk-weighted MROL as part of the Bank’s strategy to capitalize on opportunities for lower-risk weighted credit assets with a higher return on capital. |

Q2 2026 vs Q1 2026

Net interest margin increased 8 bps primarily due to:

|

Reduction in cost of funds resulting from the renewal of maturing deposits at lower interest rates; and, |

|

Higher yield on favourable asset mix resulting from increased deployment of liquid assets to the SRP portfolio in the current quarter. |

Q2 YTD 2026 vs Q2 YTD 2025

Net interest margin increased 10 bps primarily due to:

|

Reductions in the cost of funds due to lower rates on renewals of maturing deposits over the course of fiscal 2025; and, |

|

The normalization of the yield curve from the atypically inverted yield curve that existed in the early part of fiscal 2025. |

Offset partially by:

|

The continued growth in the SRP portfolio, which is composed of lower regulatory risk-weighted, lower yielding assets; and a reduction in cost of funds resulting from the renewal of maturing deposits at lower interest rates; and, |

|

The impact of the planned transition of some higher yielding, higher regulatory risk-weighted MROL to lower yielding, lower regulatory risk-weighted MROL as part of the Bank’s strategy to capitalize on opportunities for lower-risk weighted credit assets with a higher return on capital. |

The Bank’s NIM remains amongst the highest of the publicly traded Canadian Schedule I banks.

Non-Interest Income

Non-interest income is composed of revenue generated by DRTC, multi-unit residential (“MUR”) securitization transactions and income derived from miscellaneous transaction fees not directly attributable to credit assets.

Non-interest income increased 24% to $2.6 million from $2.1 million last year and is consistent with last quarter. The increase was a function primarily of higher contribution from a gain on sale of a MUR securitization for $0.03 million and higher client engagements quarter over quarter.

Non-interest income for the six months ended April 30, 2026, was $5.2 million compared with $4.2 million for the same period a year ago. The year-over-year trend was primarily due to a gain on the sale of the Bank's legacy equity investment in Stablecorp and a MUR securitization, and higher client engagements.

Provision for Credit Losses

|

(thousands of Canadian dollars) |

||||||||||||||||||||

|

For the three months ended: |

For the six months ended: |

|||||||||||||||||||

|

April 30 |

January 31 |

April 30 |

April 30 |

April 30 |

||||||||||||||||

|

2026 |

2026 |

2025 |

2026 |

2025 |

||||||||||||||||

|

Provision for (recovery of) credit losses by credit asset: |

||||||||||||||||||||

|

Structured receivable program |

$ | 472 | $ | 796 | $ | 1,029 | $ | 1,268 | $ | 2,217 | ||||||||||

|

Multi-family residential loans and other |

(44 | ) | (96 | ) | (140 | ) | (140 | ) | (304 | ) | ||||||||||

|

Total provision for (recovery of) credit losses |

$ | 428 | $ | 700 | $ | 889 | $ | 1,128 | $ | 1,913 | ||||||||||

Q2 2026 vs Q2 2025 vs Q1 2026

VersaBank recorded a provision for credit losses in the amount of $428,000 in the current quarter compared to $889,000 last year and $700,000 last quarter primarily due to updates in the forward-looking information used by the Bank in its credit risk models. Provision for credit losses as a percentage of average credit assets was 0.03% compared with 0.08% last year and 0.05% last quarter, which remains among the lowest of the publicly traded Canadian Schedule I banks.

Q2 YTD 2026 vs Q2 YTD 2025

VersaBank recorded a provision for credit losses in the amount of $1.1 million in the current period compared to $1.9 million for the same period last year primarily due to updates in the forward-looking information used by the Bank in its credit risk models. Provision for credit losses as a percentage of average credit assets was 0.04% compared with 0.09% for the same period last year, which remains among the lowest of the publicly traded Canadian Schedule I banks.

Non-Interest Expenses

|

(thousands of Canadian dollars) |

||||||||||||||||||||||||||||||||

|

For the three months ended: |

For the six months ended: |

|||||||||||||||||||||||||||||||

|

April 30 |

January 31 |

April 30 |

April 30 |

April 30 |

||||||||||||||||||||||||||||

|

2026 |

2026 |

Change |

2025 |

Change |

2026 |

2025 |

Change |

|||||||||||||||||||||||||

|

Salaries and benefits |

$ | 11,202 | $ | 10,383 | 8 | % | $ | 9,155 | 22 | % | $ | 21,585 | $ | 17,769 | 21 | % | ||||||||||||||||

|

General and administrative |

14,400 | 8,367 | 72 | % | 6,720 | 114 | % | 22,767 | 12,209 | 86 | % | |||||||||||||||||||||

|

Premises and equipment |

1,884 | 1,796 | 5 | % | 1,641 | 15 | % | 3,680 | 3,237 | 14 | % | |||||||||||||||||||||

|

Total non-interest expenses |

$ | 27,486 | $ | 20,546 | 34 | % | $ | 17,516 | 57 | % | $ | 48,032 | $ | 33,215 | 45 | % | ||||||||||||||||

|

Efficiency Ratio |

72 | % | 56 | % | 29 | % | 58 | % | 24 | % | 64 | % | 57 | % | 12 | % | ||||||||||||||||

Q2 2026 vs Q2 2025

Non-interest expenses, including a $6.7 million charge consisting of $4.5 million in project costs associated with the Reorganization and a $2.2 million intangible asset write down resulting from the sale of the Bank’s sole physical branch, increased 57% to $27.5 million primarily due to:

|

Higher general operating costs consistent with increased business activities; |

|

Project costs associated with the Reorganization and the intangible asset write down resulting from the sale of the Bank’s sole physical branch; and, |

|

The onboarding cost of the RBTD platform for $0.6 million in the current quarter |

Q2 2026 vs Q1 2026

Non-interest expenses increased 34% primarily due to:

|

Higher project costs associated with the Reorganization and the intangible asset write down resulting from the sale of the Bank’s sole physical branch; |

|

The onboarding cost of the RBTD platform for $0.6 million in the current quarter; and, |

|

Higher general operating costs consistent with increased business activities. |

Q2 YTD 2026 vs Q2 YTD 2025

Non-interest expenses increased 45% primarily due to:

|

Higher general operating costs consistent with increased business activities; |

|

Project costs associated with the Reorganization and the intangible asset write down resulting from the sale of the Bank’s sole physical branch; and, |

|

The onboarding cost of the RBTD platform for $0.8 million in the current period |

Income Tax Provision

The Bank’s effective tax rate for the current year is estimated to be approximately 27% compared with approximately 27% a year ago. Shifts in the Bank’s effective tax rate from the statutory rates was a function primarily of adjustments to changes in assumptions on non-deductible expenses and other permanent tax differences, the foreign exchange impact on various assets, as well as changes in earnings allocation between different tax jurisdictions. Provision for income taxes for the current quarter was $2.9 million compared with $3.2 million last year and $4.2 million last quarter. Provision for income taxes for the six months ended April 30, 2026, was $7.1 million compared with $6.2 million for the same period a year ago.

Financial Review – Balance Sheet

|

(thousands of Canadian dollars) |

||||||||||||||||||||

|

April 30 |

January 31 |

April 30 |

||||||||||||||||||

|

2026 |

2026 |

Change |

2025 |

Change |

||||||||||||||||

|

Total assets |

$ | 6,440,700 | $ | 6,146,010 | 5 | % | $ | 5,047,133 | 28 | % | ||||||||||

|

Cash and securities |

674,438 | 729,278 | (8 | %) | 444,993 | 52 | % | |||||||||||||

|

Credit assets, net of allowance for credit losses |

5,675,879 | 5,333,279 | 6 | % | 4,523,812 | 25 | % | |||||||||||||

|

Deposits |

5,520,909 | 5,248,955 | 5 | % | 4,205,185 | 31 | % | |||||||||||||

Total Assets

Total assets as at April 30, 2026, were $6.44 billion compared with $5.05 billion a year ago and $6.15 billion last quarter. The year-over-year and sequential increases were primarily due to growth in VersaBank’s SRP portfolio.

Cash and securities

Cash and securities, which are held primarily for liquidity purposes, at April 30, 2026, were $674.4 million, or 10% of total assets, compared with $445.0 million, or 9% of total assets a year ago, and $729.3 million, or 12% of total assets last quarter. The increase in liquidity asset balances reflects the impact of the additional liquidity held at VersaBank USA in advance of the transactions with Stearns Bank National Association to divest of certain lending assets and deposits held at a branch in Holdingford, Minnesota, on May 1, 2026 (see Subsequent event below), as well as projected lending asset growth. The decrease in liquidity balances from last quarter reflects the deployment of funds to lending asset growth.

As at April 30, 2026, the Bank held securities totaling $106.3 million (October 31, 2025 - $80.9 million), including accrued interest, comprised of US Treasury Bills with a carrying value of $96.2 million, Government of Canada Treasury Bills with a carrying value of $2.1 million and other securities with a carrying value of $8.0 million.

Credit assets

|

(thousands of Canadian dollars) |

||||||||||||||||||||

|

April 30 |

January 31 |

April 30 |

||||||||||||||||||

|

2026 |

2026 |

Change |

2025 |

Change |

||||||||||||||||

|

Structured receivable program |

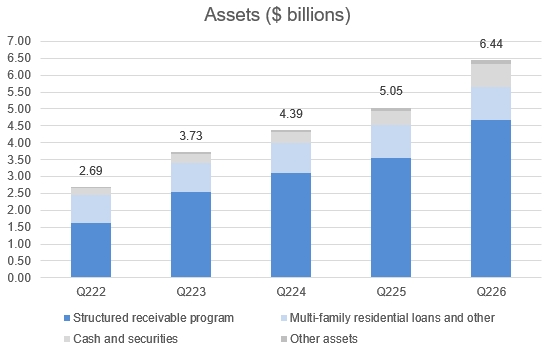

$ | 4,679,121 | $ | 4,393,457 | 7 | % | $ | 3,548,931 | 32 | % | ||||||||||

|

Multi-family residential loans and other |

979,093 | 922,823 | 6 | % | 958,249 | 2 | % | |||||||||||||

| 5,658,214 | 5,316,280 | 6 | % | 4,507,180 | 26 | % | ||||||||||||||

|

Allowance for credit losses |

(8,342 | ) | (7,916 | ) | (4,958 | ) | ||||||||||||||

|

Accrued interest |

26,007 | 24,915 | 21,590 | |||||||||||||||||

|

Total credit assets, net of allowance for credit losses |

$ | 5,675,879 | $ | 5,333,279 | 6 | % | $ | 4,523,812 | 25 | % | ||||||||||

VersaBank organizes its Credit Asset portfolios into the following two broad asset categories: Structured Receivable Program (previously referred to as “Receivable Purchase Program”) and Multi-Family Residential Loans and Other. These categories have been established in VersaBank’s proprietary, internally developed asset management system and have been designed to catalogue individual lending assets as a function primarily of their key risk drivers, the nature of the underlying collateral, and the applicable market segment.

The Structured Receivable Program (“SRP”) category is composed of investments in the expected cash flow streams derived primarily from consumer and small business loans and leases that are originated and owned throughout their lifetime by VersaBank’s SRP partners, as well as asset-backed securities that have similar underlying assets noted in the SRP portfolio.

The Multi-Family Residential Loans and Other (“MROL”) category is composed of two major sub-segments: Multi-Family Residential Loans, which consists of CMHC-insured (zero-risk weighted for regulatory capital purposes) loans and uninsured loans to real estate developers to finance the construction phase of development of multi-family, student residence, condominium and retirement home properties, as well as term and bridge loans to real estate developers secured by completed aforementioned properties and units. It also includes the public sector and infrastructure loans and leases. The majority of these loans are business-to-business loans with the underlying credit risk exposure being primarily residential in nature, given that the vast majority of the loans are related to properties that are designated primarily for residential use. The portfolio benefits from diversity in its underlying security in the form of a broad range of such collateral properties.

Credit assets increased 25% year-over-year and 6% sequentially to $5.68 billion primarily due to:

|

Higher SRP portfolio balances, which increased 32% year-over-year and 7% sequentially, primarily due to consistent demand for home improvement/HVAC receivable financing in Canada and the US. |

Residential Mortgage Exposures

In accordance with the OSFI Guideline B-20 – Residential Mortgage Underwriting Practices and Procedures, additional information is provided regarding the Bank’s residential mortgage exposure. For the purposes of the Guideline, a residential mortgage is defined as a loan to an individual that is secured by residential property (one-to-four-unit dwellings) and includes home equity lines of credit (“HELOCs”). This differs from the classification of residential mortgages used by the Bank which also includes multi-family residential mortgages.

Under OSFI’s definition, the Bank’s net exposure after credit risk mitigation to residential mortgages at April 30, 2026, was $5.6 million compared with $4.5 million a year ago and $5.6 million last quarter. The Bank does not currently offer residential mortgages to the public. The Bank did not have any HELOCs outstanding at April 30, 2026, last quarter or a year ago.

Credit Quality and Allowance for Credit Losses

VersaBank closely monitors its credit asset portfolio, the portfolio’s underlying borrowers, as well as its origination partners to ensure that management maintains effective visibility on credit trends that could provide an early warning indication of the emergence of any elevated risk in VersaBank’s credit asset portfolios.

Allowance for Credit Losses

The Bank maintains an allowance for expected credit losses (or ECL allowance) that is adequate, in management’s opinion, to absorb all credit-related losses in the Bank’s credit assets and treasury portfolios. Under IFRS 9 the Bank’s allowance for expected credit losses is estimated using the expected credit loss methodology and is comprised of expected credit losses recognized on both performing credit assets, and non-performing, or impaired credit assets, even if no actual loss event has occurred.

|

(thousands of Canadian dollars) |

||||||||||||||||||||

|

April 30 |

January 31 |

April 30 |

||||||||||||||||||

|

2026 |

2026 |

Change |

2025 |

Change |

||||||||||||||||

|

ECL allowance by lending asset: |

||||||||||||||||||||

|

Structured receivable program |

$ | 6,699 | $ | 6,227 | 8 | % | $ | 3,000 | 123 | % | ||||||||||

|

Multi-family residential loans and other |

1,643 | 1,689 | (3 | %) | 1,958 | (16 | %) | |||||||||||||

|

Total ECL allowance |

$ | 8,342 | $ | 7,916 | 5 | % | $ | 4,958 | 68 | % | ||||||||||

|

(thousands of Canadian dollars) |

||||||||||||||||||||

|

April 30 |

January 31 |

April 30 |

||||||||||||||||||

|

2026 |

2026 |

Change |

2025 |

Change |

||||||||||||||||

|

ECL allowance by stage: |

||||||||||||||||||||

|

ECL allowance stage 1 |

$ | 4,604 | $ | 5,014 | (8 | %) | $ | 3,760 | 22 | % | ||||||||||

|

ECL allowance stage 2 |

345 | 280 | 23 | % | 1,168 | (70 | %) | |||||||||||||

|

ECL allowance stage 3 |

3,393 | 2,622 | 29 | % | 30 | |||||||||||||||

|

Total ECL allowance |

$ | 8,342 | $ | 7,916 | 5 | % | $ | 4,958 | 68 | % | ||||||||||

VersaBank’s ECL allowance as at April 30, 2026, was $8.34 million compared with $4.96 million a year ago and $7.92 million last quarter primarily due to:

|

Updates in the forward-looking information used by the Bank in its credit risk models; and, |

|

Higher credit asset balances. |

Forward-looking information

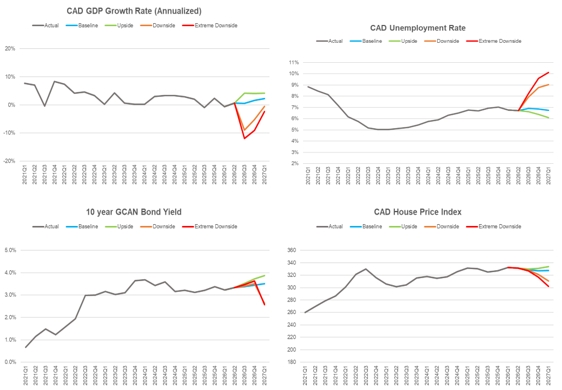

The Bank incorporates the impact of future economic conditions, or more specifically forward-looking information, into the estimation of expected credit losses at the credit risk parameter level. This is accomplished via the credit risk parameter models and proxy datasets that the Bank utilizes to develop probability of default (“PD”) and loss-given default (“LGD”) term structure forecasts for its credit assets. The Bank has sourced credit risk modeling systems and forecast macroeconomic scenario data from Moody’s Analytics, a third-party service provider for the purpose of computing forward-looking credit risk parameters under multiple macroeconomic scenarios that consider both market-wide and idiosyncratic factors and influences. These systems are used in conjunction with the Bank’s internally developed ECL models. Given that the Bank has experienced very limited historical losses and, therefore, does not have available statistically significant loss data inventory for use in developing internal, forward-looking expected credit loss trends, the use of unbiased, third-party forward-looking credit risk parameter modeling systems is particularly important for the Bank in the context of the estimation of expected credit losses.

The Bank utilizes macroeconomic indicator data derived from multiple macroeconomic scenarios in order to mitigate volatility in the estimation of expected credit losses, as well as to satisfy the IFRS 9 requirement that future economic conditions are to be based on an unbiased, probability-weighted assessment of possible future outcomes. More specifically, the macroeconomic indicators set out in the macroeconomic scenarios are used as inputs for the credit risk parameter models utilized by the Bank to sensitize the individual PD and LGD term structure forecasts to the respective macroeconomic trajectory set out in each of the scenarios (see Expected Credit Loss Sensitivity below). Currently the Bank utilizes upside, downside and baseline forecast macroeconomic scenarios and assigns discrete weights to each for use in the estimation of its reported ECL. The Bank has also applied expert credit judgement, where appropriate, to reflect, amongst other items, uncertainty in the Canadian and US macroeconomic environments.

The macroeconomic indicator data sourced from Moody’s Analytics and utilized by the Bank for the purpose of sensitizing probability of default and loss given default term structure data to forward economic conditions include, but are not limited to: real GDP, the national unemployment rate, long term interest rates, the consumer price index, the S&P/TSX Index and the price of oil. These specific macroeconomic indicators were selected in an attempt to ensure that the spectrum of fundamental macroeconomic influences on the key drivers of the credit risk profile of the Bank’s assets, including: corporate, consumer and real estate market dynamics; corporate, consumer and SME borrower performance; geography; as well as collateral value volatility, are appropriately captured and incorporated into the Bank’s forward macroeconomic sensitivity analysis.

The key assumptions driving the quarterly outlook for 2026 continue to be shaped by global trade policy and tariff-related uncertainty, although volatility in average tariff rates has eased. Trade uncertainty remains a material constraint on cross-border activity, weighing on supply chains, exports and business investment in both Canada and the United States, with upcoming North American trade milestones still a notable source of risk. In addition, the situation in the Middle East has emerged as a significant new macroeconomic shock, pushing global energy prices higher and increasing near-term inflation uncertainty. The Bank of Canada expects economic growth to remain modest through 2026, with inflation rising temporarily due to higher energy prices before easing back toward target as price pressures moderate. The U.S. Federal Reserve continues to signal a cautious policy stance, with uncertainty elevated and limited scope for near-term easing. Labour market conditions are expected to soften further but not deteriorate sharply; Canadian labour market data point to weaker hiring and a higher unemployment rate, while U.S. labour conditions remain comparatively resilient. Overall, growth is expected to remain modest rather than recessionary, with trade-related risks and energy driven inflation pressures potentially limiting monetary policy flexibility later in the year.

Management developed ECL estimates using credit risk parameter term structure forecasts sensitized to individual baseline, upside and downside forecast macroeconomic scenarios, each weighted at 100%, and subsequently computed the variance of each to the Bank’s reported ECL as at April 30, 2026 in order to assess the alignment of the Bank’s reported ECL with the Bank’s credit risk profile, and further, to assess the scope, depth and ultimate effectiveness of the credit risk mitigation strategies that the Bank has applied to its lending portfolios.

A summary of the key forecast macroeconomic indicator data trends utilized by VersaBank for the purpose of sensitizing lending asset credit risk parameter term structure forecasts to forward looking information, which in turn are used in the estimation of VersaBank’s reported ECL, as well as in the assessment of same are presented in the charts below (see Expected Credit Loss Sensitivity below).

Expected Credit Loss Sensitivity:

The following table presents the sensitivity of the Bank’s estimated ECL to a range of individual forecast macroeconomic scenarios, that in isolation may not reflect the Bank’s actual expected ECL exposure, as well as the variance of each to the Bank’s reported ECL as at April 30, 2026:

|

(thousands of Canadian dollars) |

||||||||||||||||

|

Reported |

100% |

100% |

100% |

|||||||||||||

|

ECL |

Upside |

Baseline |

Downside |

|||||||||||||

|

Allowance for expected credit losses |

$ | 8,342 | $ | 7,819 | $ | 8,266 | $ | 8,926 | ||||||||

|

Provision (recovery) from reported ECL |

(523 | ) | (75 | ) | 584 | |||||||||||

|

Variance from reported ECL (%) |

(6 | %) | (1 | %) | 7 | % | ||||||||||

The uncertainty associated with interest rates, inflation and unemployment trends given the expectation of an economic slowdown in both Canada and the US, as well as elevated geopolitical risk, may result in VersaBank’s estimated ECL amounts exhibiting some future volatility, which in turn may result in the Bank recognizing higher provisions for credit losses in the future.

Considering the analysis set out above and based on management’s review of the credit asset and credit data comprising VersaBank’s lending portfolio, combined with management’s interpretation of the available forecast macroeconomic and industry data, management is of the view that its reported ECL allowance represents a reasonable proxy for potential future credit losses.

Deposits

VersaBank has established three core low-cost deposit funding channels: Deposit brokers in Canada and the US, Licensed Insolvency Trustee firms in Canada, and cash reserves retained from VersaBank’s SRP partners, which are classified as other liabilities.

|

(thousands of Canadian dollars) |

||||||||||||||||||||

|

April 30 |

January 31 |

April 30 |

||||||||||||||||||

|

2026 |

2026 |

Change |

2025 |

Change |

||||||||||||||||

|

Licensed insolvency trustee firms |

$ | 935,323 | $ | 880,034 | 6 | % | $ | 822,260 | 14 | % | ||||||||||

|

Deposit brokers |

4,585,586 | 4,368,921 | 5 | % | 3,382,925 | 36 | % | |||||||||||||

|

Total deposits |

$ | 5,520,909 | $ | 5,248,955 | 5 | % | $ | 4,205,185 | 31 | % | ||||||||||

The majority of VersaBank’s Canadian and US deposits are sourced through deposit brokers, specifically investment dealers, wealth management firms and financial advisory firms that distribute the Bank’s term deposit products to their respective end clients.

In Canada, the Bank also sources deposits through Licensed Insolvency Trustee firms that value the ability to use VersaBank’s proprietary technology to seamlessly and efficiently interface with their administrative software, which results in a lower cost of funds to the Bank compared to conventional deposits.

The Bank's primary deposit products are eligible for insurance, by CDIC and FDIC, up to their respective limits.

Q2 2026 vs Q2 2025

Deposits increased 31% to $5.5 billion primarily due to:

|

Higher deposits from brokers attributable to VersaBank increasing activity in its broker market network to fund balance sheet growth; and, |

|

Higher deposits from Licensed Insolvency Trustee firms attributable to an increase in the volume of Canadian consumer and commercial bankruptcy and proposal restructuring proceedings year-over-year. |

Q2 2026 vs Q1 2026

Deposits increased 5% primarily due to:

|

Higher deposits from brokers attributable to VersaBank increasing activity in its broker market network to fund balance sheet growth; and, |

|

Higher deposits from Licensed Insolvency Trustee firms attributable to an increase in the volume of Canadian consumer and commercial bankruptcy and proposal restructuring proceedings year-over-year. |

Subordinated Notes Payable

|

(thousands of Canadian dollars) |

||||||||||||

|

April 30 |

January 31 |

April 30 |

||||||||||

|

2026 |

2026 |

2025 |

||||||||||

|

Issued April 2021, unsecured, non-viability contingent capital compliant, subordinated notes payable, principal amount of US $75.0 million, effective interest rate of 5.38%, maturing May 2031. The fixed rate applies only until May 1, 2026, at which point the obligation converted to a floating rate based on a CORRA-derived reference rate plus 3.61% payable quarterly in arrears. Subsequent to April 30, 2026, the notes became redeemable by the Bank, subject to regulatory approval. |

$ | 100,688 | $ | 100,160 | $ | 101,844 | ||||||

| $ | 100,688 | $ | 100,160 | $ | 101,844 | |||||||

Subordinated notes payable, net of issue costs, were $100.7 million as at April 30, 2026, compared with $101.8 million a year ago and $100.2 million last quarter. The year-over-year and quarter-over-quarter variances were a function primarily attributable to the change in the USD/CAD foreign exchange spot rate related to the US $75.0 million subordinated note.

Shareholders’ Equity

Shareholders’ equity was $552.2 million as at April 30 2026, compared with $528.3 million a year ago and $543.1 million last quarter.

On December 18, 2024, the Bank completed a treasury offering of 5,660,378 common shares at a price of USD $13.25 per share, at the time the equivalent of CAD $18.95 per share, for gross proceeds of USD $75.0 million. On December 24, 2024, the underwriters of the aforementioned offering exercised their full over-allotment option to purchase an additional 849,056 common shares (15% of the 5,660,378 common shares issued via the base offering referenced above) at a price of USD $13.25 per share, or at the time the equivalent of CAD $19.07 per share, for gross proceeds of USD $11.2 million. Total net cash proceeds from the common share offering was CAD $116.0 million. However, the Bank’s share capital increased by CAD $116.3 million corresponding to the common share offering and tax effected issue costs in the amount of CAD $6.2 million.

At April 30, 2026, there were 32,195,697 common shares outstanding compared with 32,518,786 common shares outstanding a year ago and 32,069,447 common shares outstanding last quarter.

The Bank issued 126,250 Common Shares in connection with the exercise of stock options during the current quarter for proceeds of $2.0 million. In the same period a year ago, no common shares were issued in connection with the exercise of stock options. In the sequential quarter, the Bank issued 123,912 Common Shares in connection with the exercise of stock options during the current quarter for proceeds of $2.0 million.

On April 28, 2026, the Bank received approval from the TSX to renew its Normal Course Issuer Bid ("NCIB") for its common shares. Pursuant to the NCIB, VersaBank may purchase for cancellation up to 2,000,000 of its common shares, representing approximately 9.14% of its public float. As of April 16, 2026, the public float comprised 21,876,251 common shares and there were 32,167,347 issued and outstanding common shares in total. The average daily trading volume ("ADTV") of VersaBank's common shares on the TSX for the six months of October 1, 2025 – March 31, 2026 (the "Preceding Six Month Period") was 26,510 common shares. Daily purchases under the NCIB will be limited to 25% of the ADTV, which is 6,627 common shares, other than block purchase exceptions. During the Preceding Six-Month Period, 11,929,689 VersaBank common shares were traded on all exchanges. Of that total, 3,313,798 common shares were traded on the TSX, and the remaining 8,615,891 common shares were traded on other exchanges including the Nasdaq.