Exhibit 99.3

Q1 2026 Earnings Presentation BW LPG Kristian Sørensen and Samantha Xu 2 June 2026

NOT FOR RELEASE, PUBLICATION, DISTRIBUTION OR FORWARDING, IN WHOLE OR IN PART, DIRECTLY OR INDIRECTLY, IN OR IN TO ANY JURISDICTION IN WHICH THE SAME WOULD BE UNLAWFUL . BY ATTENDING THE MEETING WHERE THIS PRESENTATION IS MADE, OR BY READING THE PRESENTATION SLIDES, YOU ACKNOWLEDGE AND AGREE TO COMPLY WITH THE FOLLOWING RESTRICTIONS . This presentation has been produced by BW LPG Limited (“BW LPG”) exclusively for information purposes . This presentation may not be reproduced or redistributed, in whole or in part, to any other person . Matters discussed in this presentation and any materials distributed in connection with this presentation may constitute or include forward – looking statements . Forward – looking statements are statements that are not historical facts and may be identified by words such as “anticipates”, “believes”, “continues”, “estimates”, “expects”, “intends”, “may”, “should”, “will” and similar expressions, such as “going forward” . These forward – looking statements reflect BW LPG’s reasonable beliefs, intentions and current expectations concerning, among other things, BW LPG’s results of operations, financial condition, liquidity, prospects, growth and strategies . Forward – looking statements include statements regarding : objectives, goals, strategies, outlook and growth prospects ; future plans, events or performance and potential for future growth ; liquidity, capital resources and capital expenditures ; economic outlook and industry trends ; developments of BW LPG’s markets ; the impact of regulatory initiatives ; and the strength of BW LPG’s competitors . Forward – looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future . The forward – looking statements in this presentation are based upon various assumptions, many of which are based, in turn, upon further assumptions, including without limitation, management’s examination of historical operating trends, data contained in BW LPG’s records and other data available from Fourth parties . Although BW LPG believes that these assumptions were reasonable when made, these assumptions are inherently subject to significant known and unknown risks, uncertainties, contingencies and other important factors which are difficult or impossible to predict and are beyond its control . Forward – looking statements are not guarantees of future performance and such risks, uncertainties, contingencies and other important factors could cause the actual results of operations, financial condition and liquidity of BW LPG or the industry to differ materially from those results expressed or implied in this presentation by such forward – looking statements . No representation is made that any of these forward – looking statements or forecasts will come to pass or that any forecast result will be achieved, and you are cautioned not to place any undue influence on any forward – looking statement . Disclaimer and forward - looking statements 2 No representation, warranty or undertaking, express or implied, is made by BW LPG, its affiliates or representatives as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of the information or the opinions contained herein, for any purpose whatsoever . Neither BW LPG nor any of its affiliates or representatives shall have any responsibility or liability whatsoever (for negligence or otherwise) for any loss whatsoever and howsoever arising from any use of this presentation or its contents or otherwise arising in connection with this presentation . All information in this presentation is subject to updating, revision, verification, correction, completion, amendment and may change materially and without notice . In giving this presentation, none of BW LPG, its affiliates or representatives undertakes any obligation to provide the recipient with access to any additional information or to update this presentation or any information or to correct any inaccuracies in any such information . The information contained in this presentation should be considered in the context of the circumstances prevailing at the time and has not been, and will not be, updated to reflect material developments which may occur after the date of the presentation . The contents of this presentation are not to be construed as legal, business, investment or tax advice . Each recipient should consult its own legal, business, investment or tax adviser as to legal, business, investment or tax advice . By attending this presentation, you acknowledge that you will be solely responsible for your own assessment of the market and the market position of BW LPG and that you will conduct your own analysis and be solely responsible for forming your own view on the potential future performance of the business of BW LPG . This presentation must be read in conjunction with the recent financial information and the disclosures therein . A number of measures are used to report the performance of our business, which are non - IFRS measures, such as TCE income – Shipping per available day, TCE income – Shipping per calendar day and Return on capital employed (ROCE) . These measures are defined and reconciliations to the nearest IFRS measure are available in BW LPG’s Q 1 2026 Interim Financial Report and BW LPG’s Registration Statement on Form 20 - F . Neither this presentation nor anything contained herein shall form the basis of, or be relied upon in connection with, any offer or purchase whatsoever in any jurisdiction and shall not constitute or form part of an offer to sell or the solicitation of an offer to buy any securities in the United States or in any other jurisdiction . The securities referred to herein may not be offered or sold in the United States absent registration with the United States Securities and Exchange Commission or an exemption from registration under the U . S . Securities Act of 1933 , as amended (the “Securities Act”) . BW LPG does not intend to register any part of any offering in the United States or to conduct a public offering in the United States of the shares to which this presentation relates . In the EEA Member States, with the exception of Norway (each such EEA Member State, a “Relevant State“), this presentation and the information contained herein are intended only for and directed to qualified investors as defined in Article 2 (e) of Regulation (EU) 2017 / 1129 of the European Parliament and of the Council of 14 June 2017 (the “Prospectus Regulation”) . The securities mentioned in this presentation are not intended to be offered to the public in any Relevant State and are only available to qualified investors except in accordance with exceptions in the Prospectus Regulation . Persons in any Relevant State who are not qualified investors should not take any actions based on this presentation, nor rely on it . In the United Kingdom, this presentation is directed only at, and communicated only to, persons who are qualified investors within the meaning of Article 2 (e) of the Prospectus Regulation as it forms part of domestic law in the United Kingdom by virtue of the European Union (Withdrawal) Act 2018 who are ( i ) persons who fall within the definition of "investment professional" in Article 19 ( 5 ) of the Financial Services and Markets Act 2000 (Financial Promotion) Order 2005 , as amended (the “Order”), or (ii) persons who fall within Article 49 ( 2 )(a) to (d) of the Order, or (iii) persons to whom it may otherwise be lawfully communicated (all such persons referred to in ( i ), (ii) and (iii) above together being referred to as “Relevant Persons”) . This presentation must not be acted on or relied on by persons in the United Kingdom who are not Relevant Persons .

Agenda Q1 2026 Q1 2026 highlights and market outlook Market overview Company performance Q&A

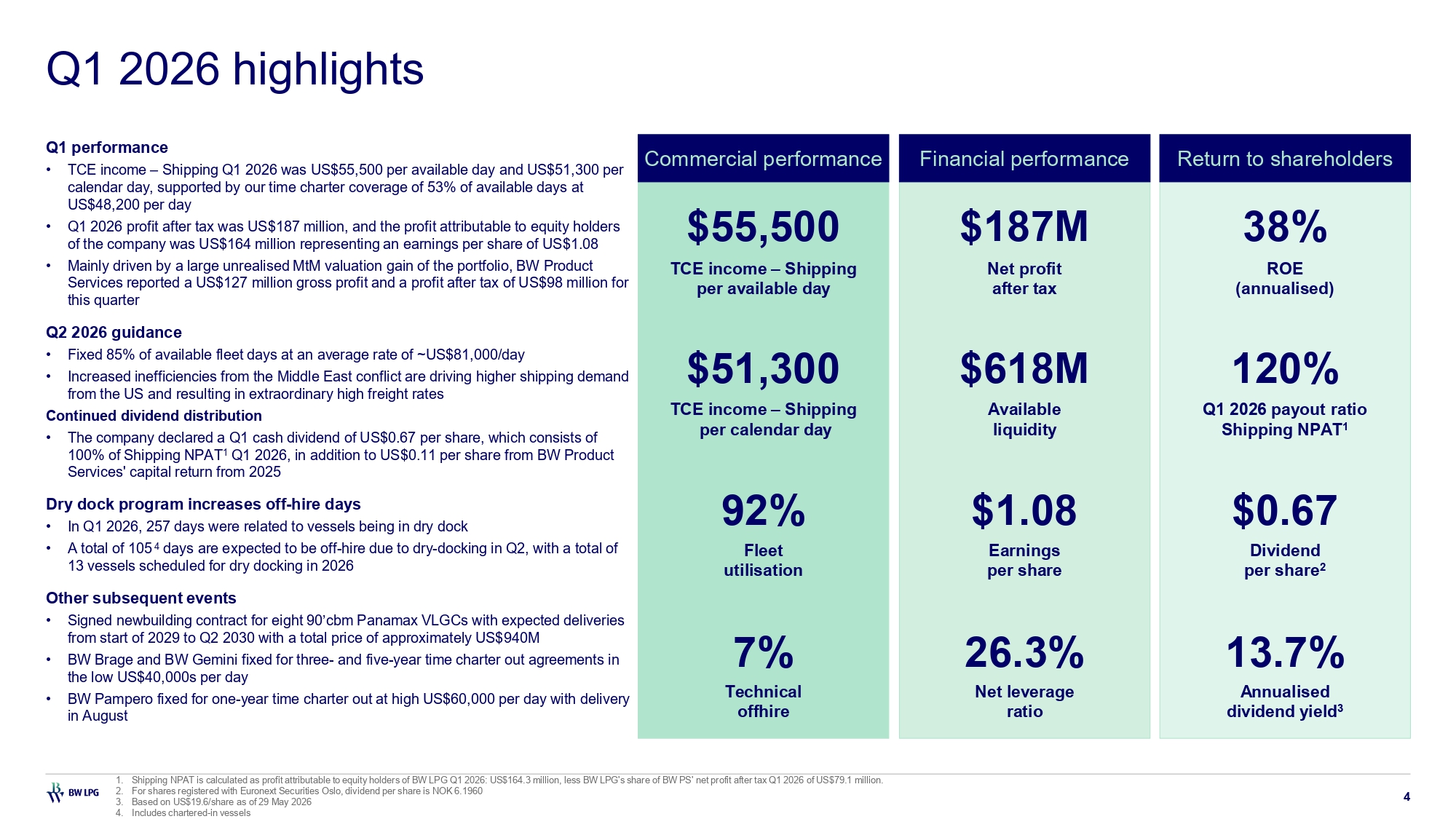

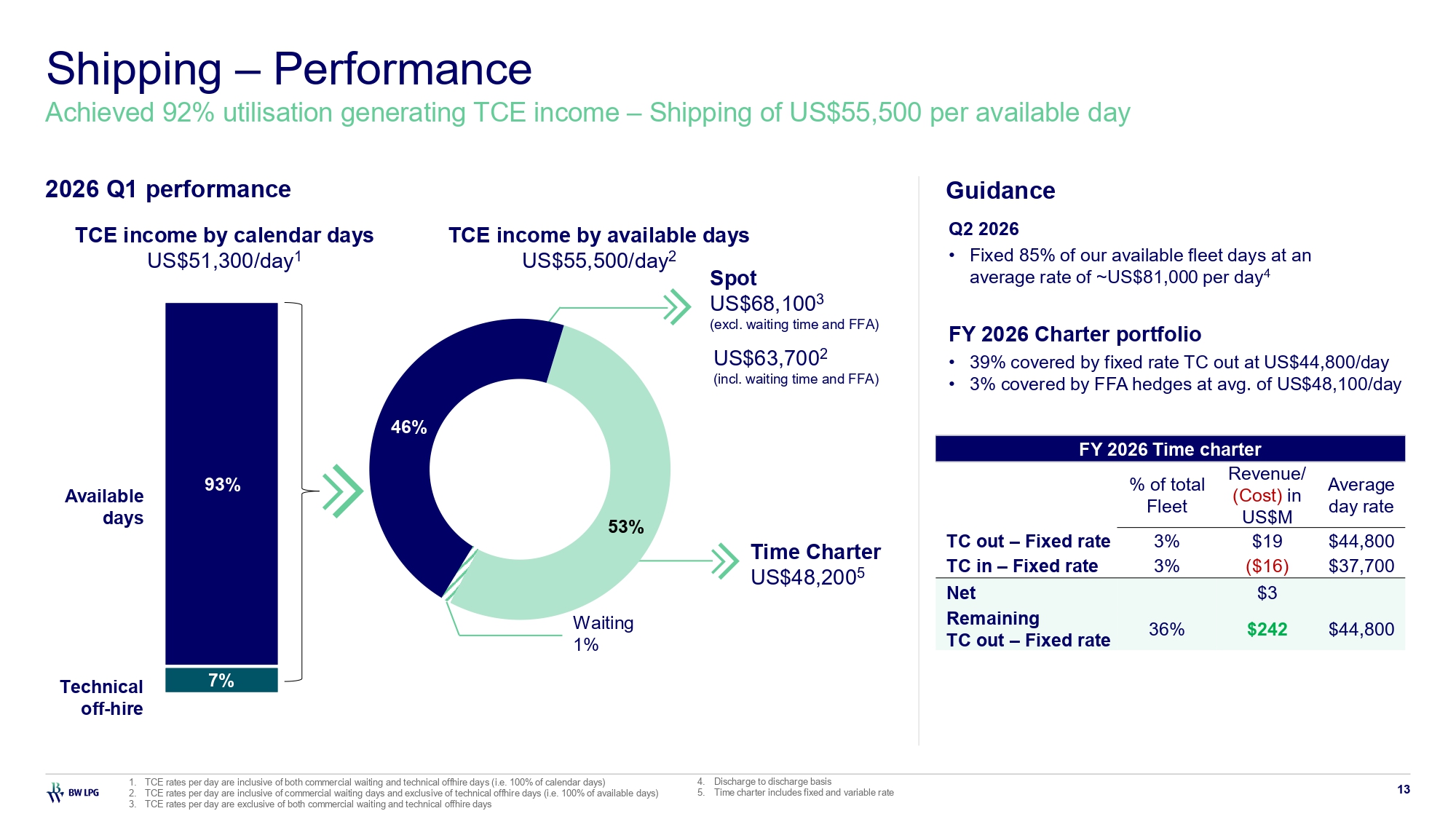

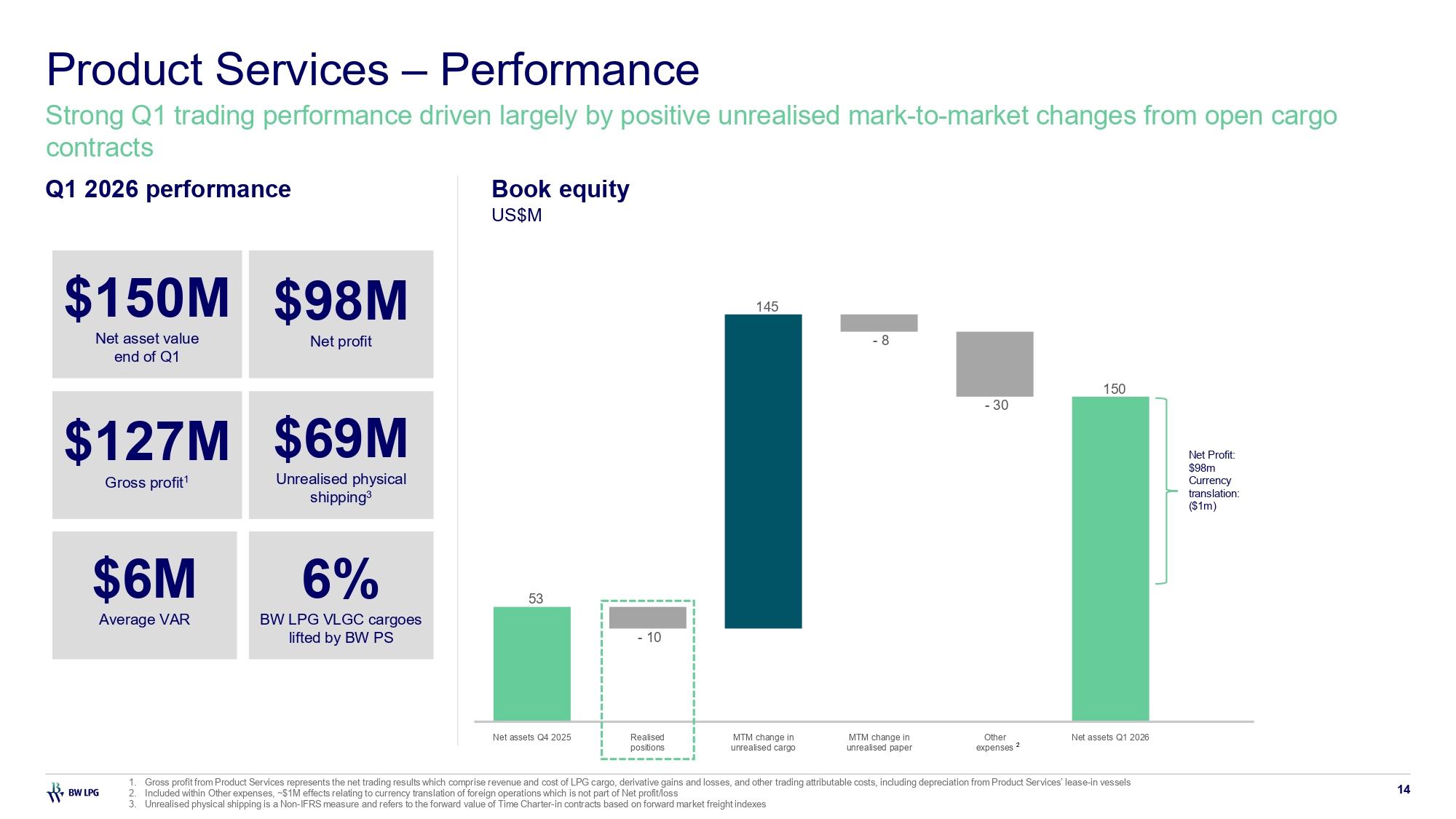

Q1 performance • TCE income – Shipping Q1 2026 was US$55,500 per available day and US$51,300 per calendar day, supported by our time charter coverage of 53% of available days at US$48,200 per day • Q1 2026 profit after tax was US$187 million, and the profit attributable to equity holders of the company was US$164 million representing an earnings per share of US$1.08 • Mainly driven by a large unrealised MtM valuation gain of the portfolio, BW Product Services reported a US$127 million gross profit and a profit after tax of US$98 million for this quarter Q2 2026 guidance • Fixed 85% of available fleet days at an average rate of ~US$81,000/day • Increased inefficiencies from the Middle East conflict are driving higher shipping demand from the US and resulting in extraordinary high freight rates Continued dividend distribution • The company declared a Q1 cash dividend of US$0.67 per share, which consists of 100% of Shipping NPAT 1 Q1 2026, in addition to US$0.11 per share from BW Product Services' capital return from 2025 Dry dock program increases off - hire days • In Q1 2026, 257 days were related to vessels being in dry dock • A total of 105 4 days are expected to be off - hire due to dry - docking in Q2, with a total of 13 vessels scheduled for dry docking in 2026 Other subsequent events • Signed newbuilding contract for eight 90’cbm Panamax VLGCs with expected deliveries from start of 2029 to Q2 2030 with a total price of approximately US$940M • BW Brage and BW Gemini fixed for three - and five - year time charter out agreements in the low US$40,000s per day • BW Pampero fixed for one - year time charter out at high US$60,000 per day with delivery in August Q1 2026 highlights Return to shareholders $0.67 Dividend per share 2 13.7% Annualised dividend yield 3 38 % ROE (annualised) 120% Q1 2026 payout ratio Shipping NPAT 1 Financial performance $ 187M Net profit after tax $618M Available liquidity $ 1.08 Earnings per share 26.3% Net leverage ratio Commercial performance $ 55,500 TCE income – Shipping per available day $51,300 TCE income – Shipping per calendar day 9 2 % Fleet utilisation 7% Technical offhire 4 1. Shipping NPAT is calculated as profit attributable to equity holders of BW LPG Q1 2026: US$164.3 million, less BW LPG's share of BW PS' net profit after tax Q1 2026 of US$79.1 million. 2. For shares registered with Euronext Securities Oslo, dividend per share is NOK 6.1960 3. Based on US$19.6/share as of 29 May 2026 4. Includes chartered - in vessels

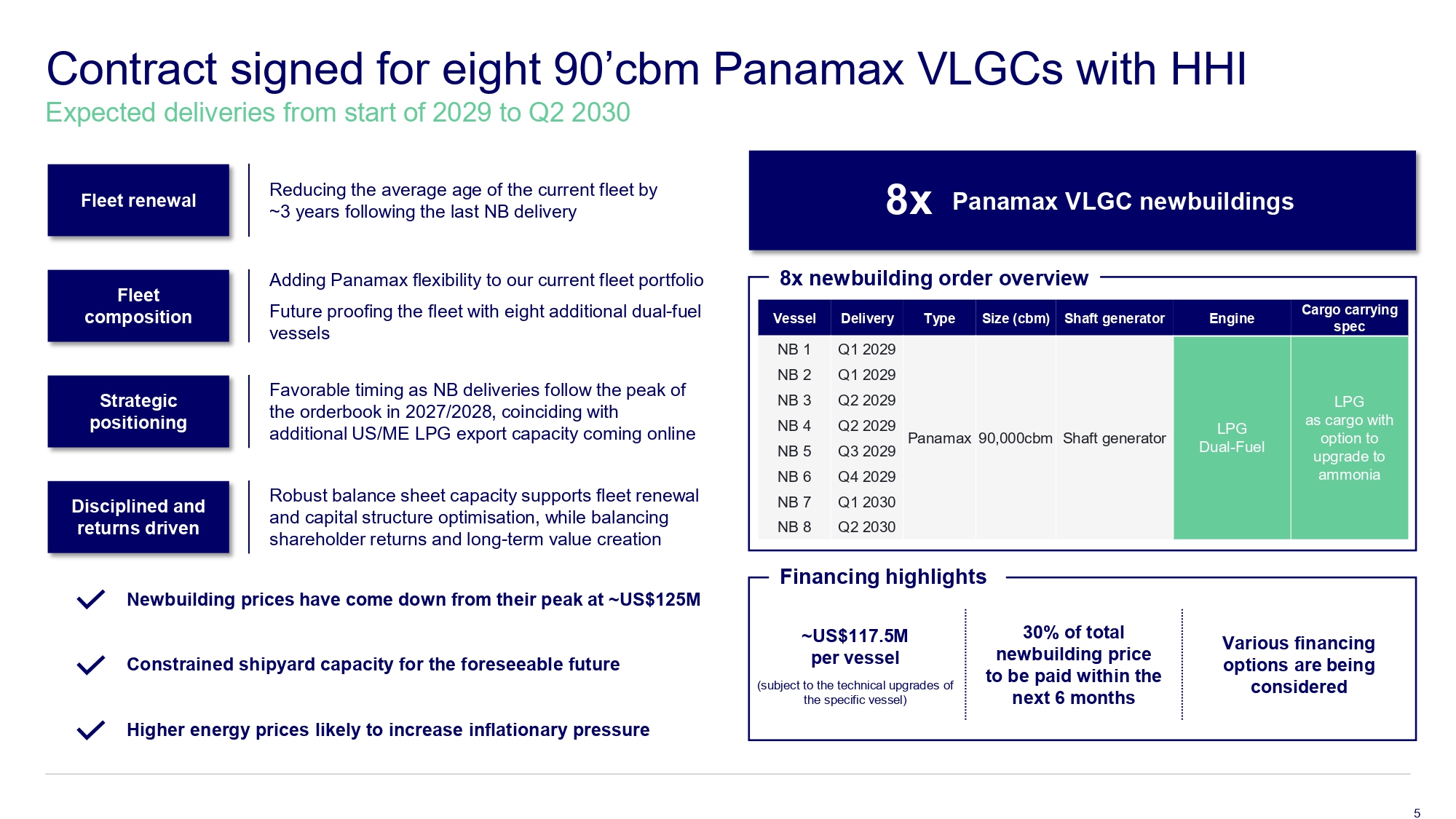

Contract signed for eight 90’cbm Panamax VLGCs with HHI Expected deliveries from start of 2029 to Q2 2030 5 Newbuilding prices have come down from their peak at ~US $125M Higher energy prices likely to increase inflationary pressure Constrained shipyard capacity for the foreseeable future Fleet renewal Reducing the average age of the current fleet by ~ 3 years following the last NB delivery Fleet composition Adding Panamax flexibility to our current fleet portfolio Future proofing the fleet with eight additional dual - fuel vessels Strategic positioning Favorable timing as NB deliveries follow the peak of the orderbook in 2027/2028, coinciding with additional US/ME LPG export capacity coming online Disciplined and returns driven Robust balance sheet capacity supports fleet renewal and capital structure optimisation, while balancing shareholder returns and long - term value creation Panamax VLGC newbuildings Cargo carrying spec Engine Shaft generator Size (cbm) Type Delivery Vessel LPG as cargo with option to upgrade to ammonia LPG Dual - Fuel Shaft generator 90,000cbm Panamax Q1 2029 NB 1 Q1 2029 NB 2 Q2 2029 NB 3 Q2 2029 NB 4 Q3 2029 NB 5 Q4 2029 NB 6 Q1 2030 NB 7 Q2 2030 NB 8 8x 8x newbuilding order overview Financing highlights ~ US$ 117.5M per vessel (subject to the technical upgrades of the specific vessel) 30% of total newbuilding price to be paid within the next 6 months Various financing options are being considered

Agenda Q1 2026 highlights and market outlook Market overview Company performance Q&A Q1 2026

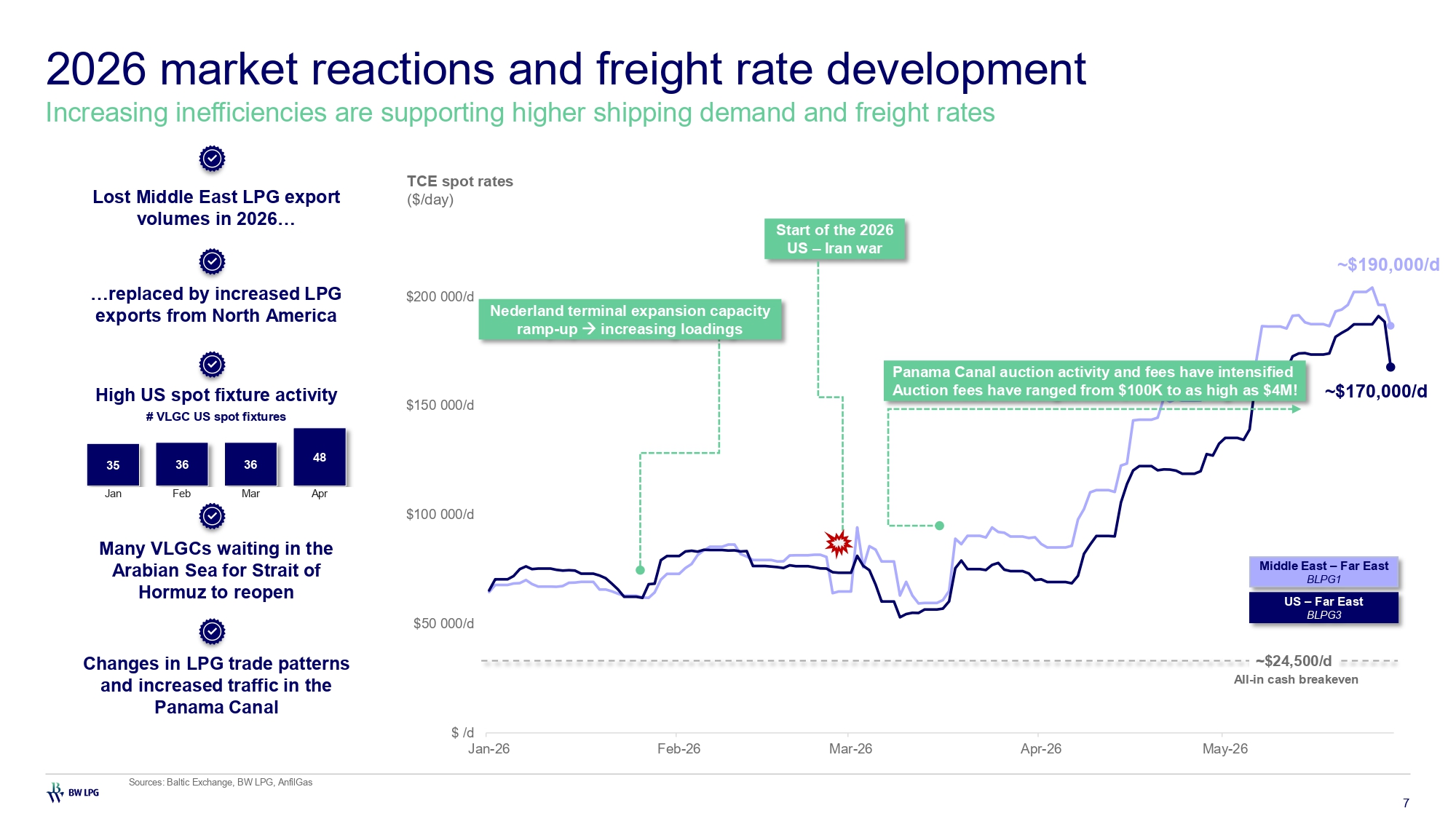

$ /d $50 000/d $100 000/d $150 000/d $200 000/d $250 000/d Jan-26 Feb-26 Mar-26 Apr-26 May-26 2026 market reactions and freight rate development Increasing inefficiencies are supporting higher shipping demand and freight rates 7 Middle East – Far East BLPG1 US – Far East BLPG3 Start of the 2026 US – Iran war ~$170,000/d ~$1 90 ,000/d Panama Canal auction activity and fees have intensified Auction fees have ranged from $100K to as high as $4M! TCE spot rates ($/day) All - in cash breakeven ~$24,500/d Lost Middle East LPG export volumes in 2026… Changes in LPG trade patterns and increased traffic in the Panama Canal …replaced by increased LPG exports from North America 35 36 36 48 Jan Feb Mar Apr # VLGC US spot fixtures High US spot fixture activity Many VLGCs waiting in the Arabian Sea for Strait of Hormuz to reopen Sources: Baltic Exchange, BW LPG, AnfilGas Nederland terminal expansion capacity ramp - up increasing loadings

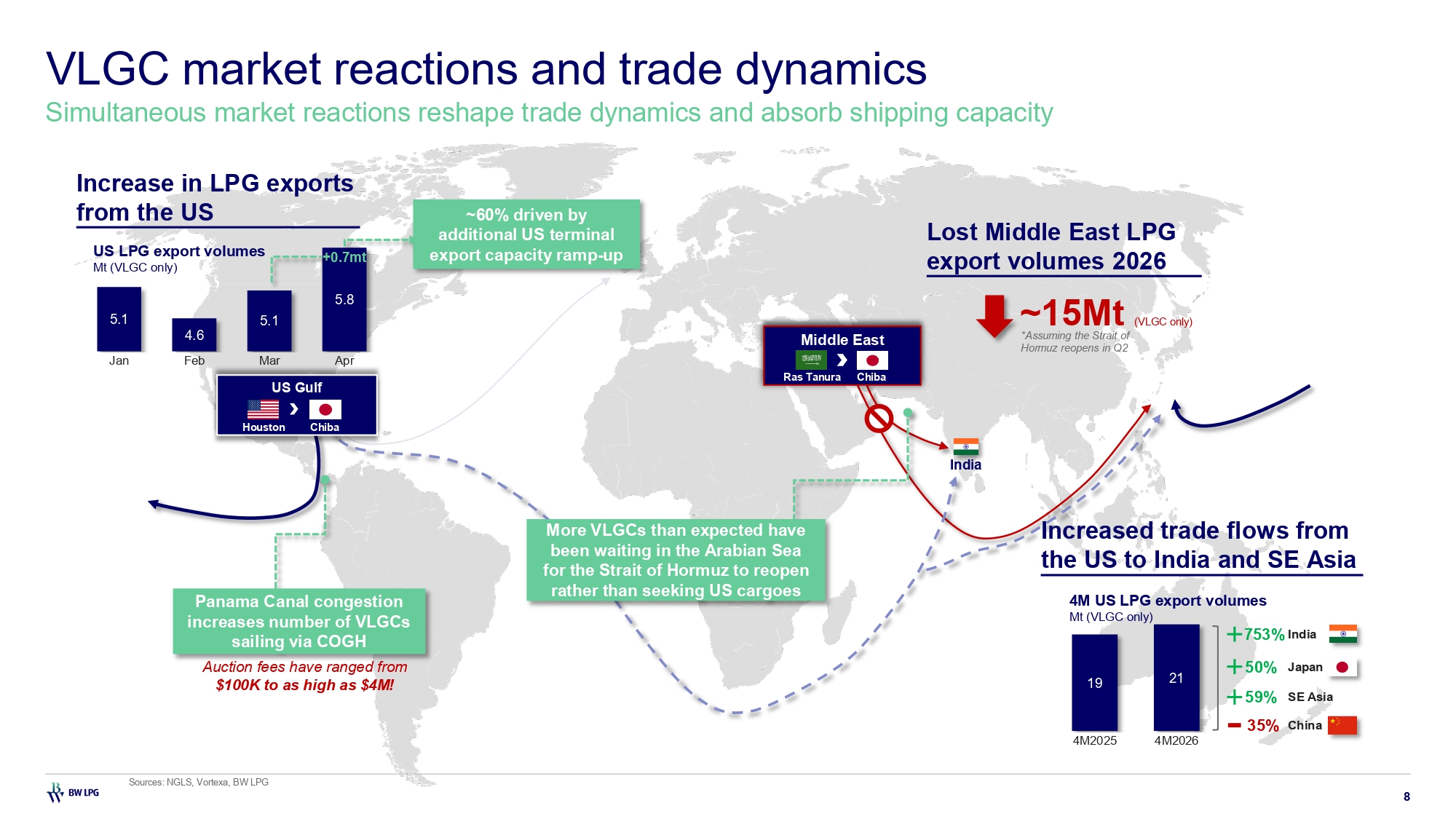

VLGC market reactions and trade dynamics Simultaneous market reactions reshape trade dynamics and absorb shipping capacity India 8 US LPG export volumes Mt (VLGC only) 5.1 4.6 5.1 5.8 Jan Feb Mar Apr US Gulf Houston Chiba Middle East Ras Tanura Chiba +0.7mt ~15Mt (VLGC only) 19 21 4M2025 4M2026 Japan India China 753% 50% 59% 35% SE Asia 4M US LPG export volumes Mt (VLGC only) *Assuming the Strait of Hormuz reopens in Q2 More VLGCs than expected have been waiting in the Arabian Sea for the Strait of Hormuz to reopen rather than seeking US cargoes Increase in LPG exports from the US Lost Middle East LPG export volumes 2026 Increased trade flows from the US to India and SE Asia Panama Canal congestion increases number of VLGCs sailing via COGH ~60% driven by additional US terminal export capacity ramp - up Auction fees have ranged from $100K to as high as $4M! Sources: NGLS, Vortexa , BW LPG

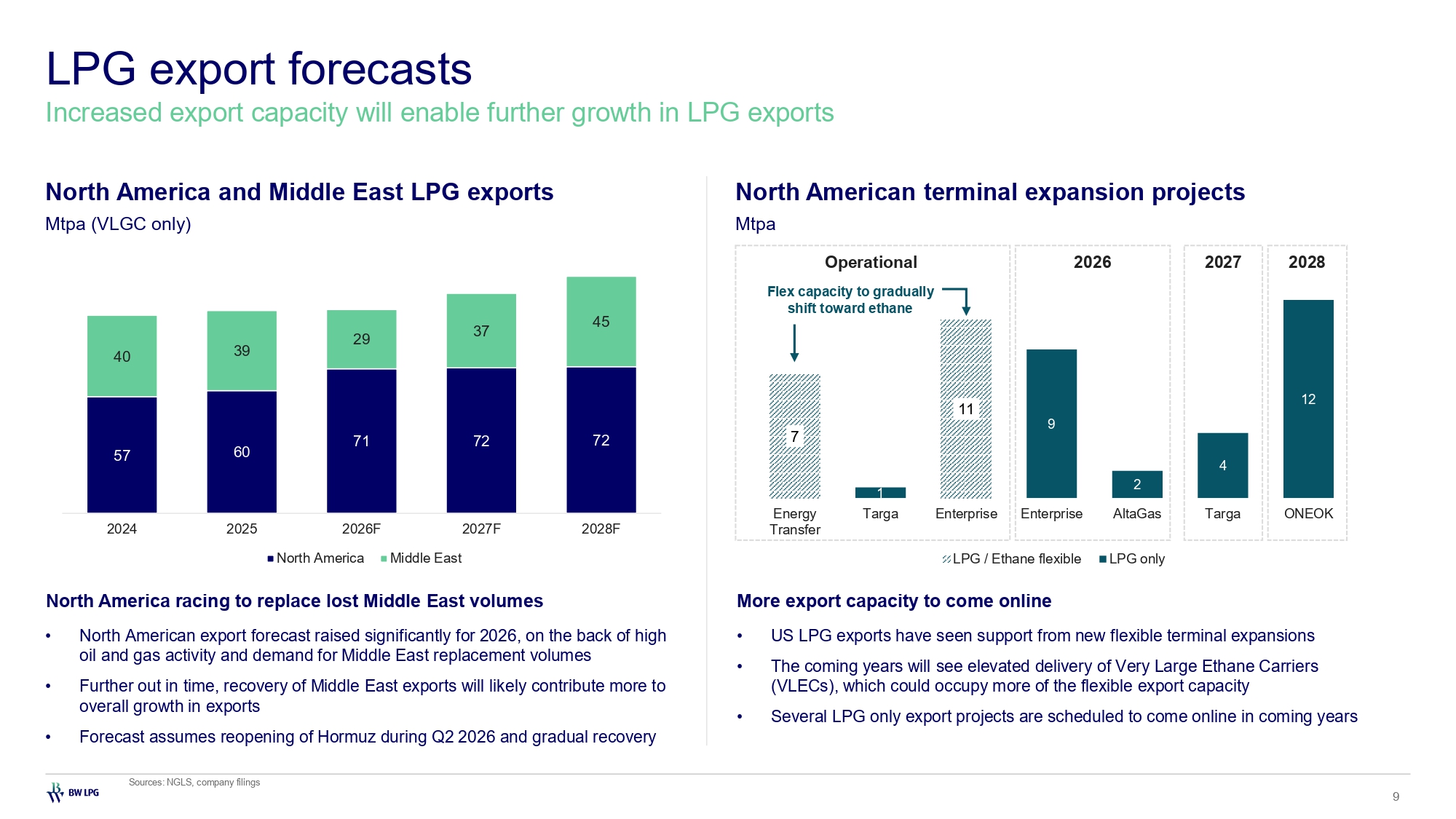

7 11 1 9 2 4 12 Energy Transfer Targa Enterprise Enterprise AltaGas Targa ONEOK LPG / Ethane flexible LPG only LPG export forecasts Increased export capacity will enable further growth in LPG exports • North American export forecast raised significantly for 2026, on the back of high oil and gas activity and demand for Middle East replacement volumes • Further out in time, recovery of Middle East exports will likely contribute more to overall growth in exports • Forecast assumes reopening of Hormuz during Q2 2026 and gradual recovery North America racing to replace lost Middle East volumes • US LPG exports have seen support from new flexible terminal expansions • The coming years will see elevated delivery of Very Large Ethane Carriers (VLECs), which could occupy more of the flexible export capacity • Several LPG only export projects are scheduled to come online in coming years More export capacity to come online North America and Middle East LPG exports Mtpa (VLGC only) North American terminal expansion projects Mtpa Sources: NGLS, company filings 9 57 60 71 72 72 40 39 29 37 45 2024 2025 2026F 2027F 2028F North America Middle East Operational 2026 2028 2027 Mtpa (VLGC only) Flex capacity to gradually shift toward ethane

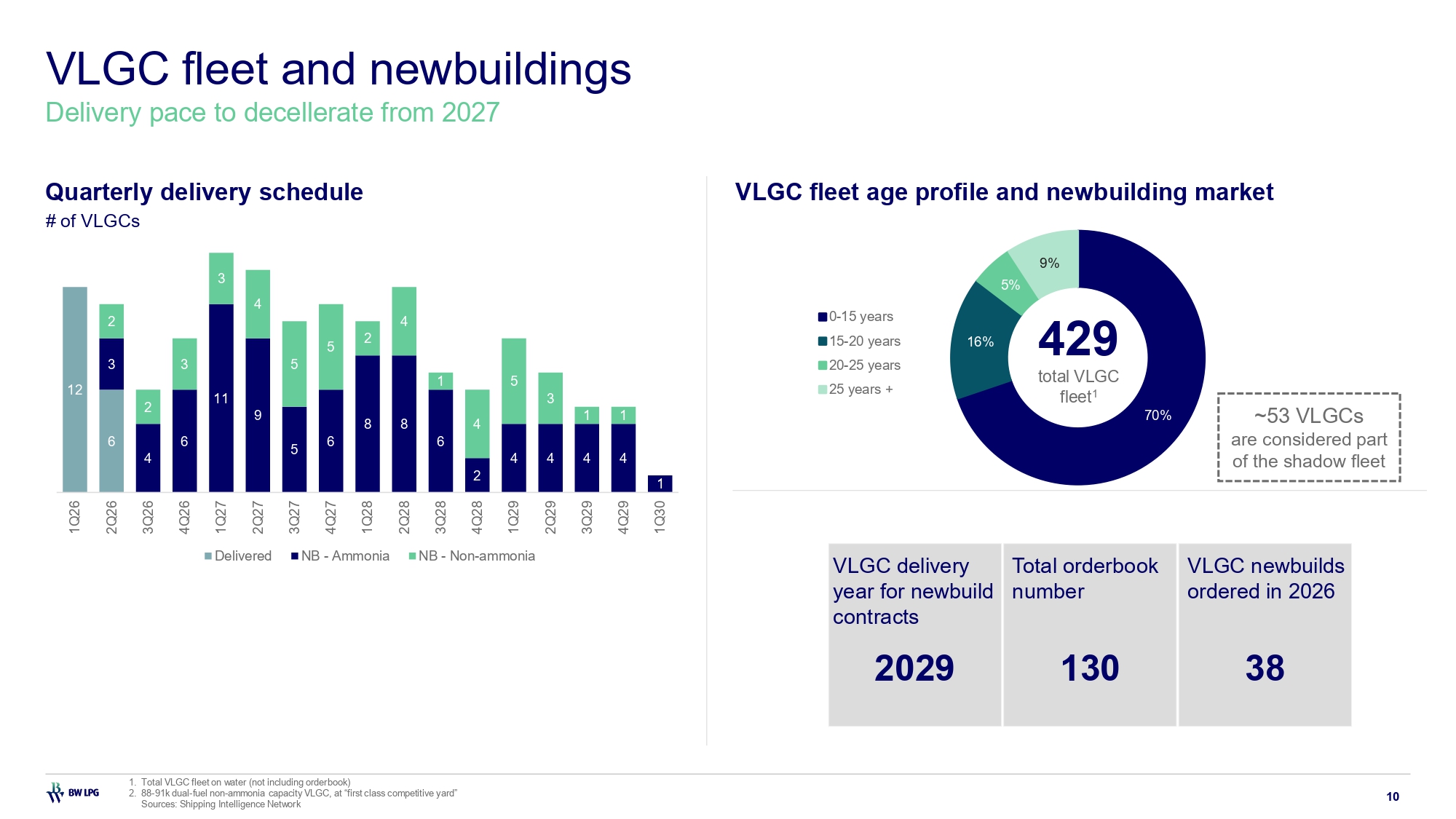

VLGC fleet and newbuildings 10 Delivery pace to decellerate from 2027 Quarterly delivery schedule # of VLGCs VLGC fleet age profile and newbuilding market VLGC delivery year for newbuild contracts Total orderbook number 130 VLGC newbuilds ordered in 2026 38 2029 1. Total VLGC fleet on water (not including orderbook) 2. 88 - 91k dual - fuel non - ammonia capacity VLGC, at “first class competitive yard” Sources: Shipping Intelligence Network 70% 16% 5% 9% 0-15 years 15-20 years 20-25 years 25 years + 429 total VLGC fleet 1 12 6 3 4 6 11 9 5 6 8 8 6 2 4 4 4 4 1 2 2 3 3 4 5 5 2 4 1 4 5 3 1 1 1Q26 2Q26 3Q26 4Q26 1Q27 2Q27 3Q27 4Q27 1Q28 2Q28 3Q28 4Q28 1Q29 2Q29 3Q29 4Q29 1Q30 Delivered NB - Ammonia NB - Non-ammonia ~53 VLGCs are considered part of the shadow fleet

Market outlook US LPG export growth has been front - loaded due to lost Middle East volumes • 429 VLGCs are currently on the water • 18 VLGCs have been delivered so far in 2026, with 20 more scheduled for delivery before 2027 • VLGC orderbook currently consists of 130 ships, with deliveries slowing down after 2027 LPG exports US / Middle East Simultaneous market reactions are reshaping trade dynamics, increasing inefficiencies, absorbing shipping capacity, and supporting higher freight rates Market dynamics VLGC global fleet Panama v. Cape routing • Growth to see support from high LPG production and commissioning of new export infrastructure • Middle East exports likely to remain heavily restricted for the duration of the Middle East war • Repairs of Middle East LPG export infrastructure needed to fully recover to pre - war export levels • Strong demand for - and growing supply of US LPG to continue to support freight rates • High demand for using the Panama Canal and vessels idling in the Middle East elevate market inefficiencies • Longer sailing distances to stretch global fleet capacity • High competition for transiting the Neo - Panamax locks drive VLGCs to sail around Cape of Good Hope • Demand for canal usage likely to stay high with fleet growth in ethane, LPG and LNG segments 11

Agenda Q1 2026 Q1 2026 highlights and market outlook Market overview Company performance Q&A

13 Achieved 92% utilisation generating TCE income – Shipping of US$55,500 per available day 2026 Q1 performance Guidance Q2 2026 • Fixed 85% of our available fleet days at an average rate of ~US$81,000 per day 4 1. TCE rates per day are inclusive of both commercial waiting and technical offhire days (i.e. 100% of calendar days) 2. TCE rates per day are inclusive of commercial waiting days and exclusive of technical offhire days (i.e. 100% of available days) 3. TCE rates per day are exclusive of both commercial waiting and technical offhire days 7% 93% TCE income by calendar days US$51,300/day 1 Technical off - hire Available days 53% 46% TCE income by available days US$55,500/day 2 US$ 63,7 00 2 (incl. waiting time and FFA) Spot US$ 68,100 3 (excl. waiting time and FFA) Waiting 1% Time Charter US$48, 2 00 5 4. Discharge to discharge basis 5. Time charter includes fixed and variable rate FY 2026 Time charter Average day rate Revenue/ (Cost) in US$M % of total Fleet $44,800 $19 3% TC out – Fixed rate $37,700 ($16) 3% TC in – Fixed rate $3 Net $44,800 $242 36% Remaining TC out – Fixed rate Shipping – Performance FY 2026 Charter portfolio • 39 % covered by fixed rate TC out at US$ 44,800/ day • 3 % covered by FFA hedges at avg. of US$ 48,100/ day

53 - 10 145 - 8 - 30 150 69 Net assets Q4 2025 Realised positions MTM change in unrealised cargo MTM change in unrealised paper Other expenses Net assets Q1 2026 Unrealised physical shipping Product Services – Performance 14 Strong Q1 trading performance driven largely by positive unrealised mark - to - market changes from open cargo contracts 1. Gross profit from Product Services represents the net trading results which comprise revenue and cost of LPG cargo, derivativ e g ains and losses, and other trading attributable costs, including depreciation from Product Services’ lease - in vessels 2. Included within Other expenses, ~$1M effects relating to currency translation of foreign operations which is not part of Net pro fit/loss 3. Unrealised physical shipping is a Non - IFRS measure and refers to the forward value of Time Charter - in contracts based on forward market fr eight indexes Q1 2026 performance Book equity US$M Net asset value end of Q1 Net profit Gross profit 1 Average VAR Unrealised physical shipping 3 BW LPG VLGC cargoes lifted by BW PS Net Profit: $98m Currency translation: ($1m) 2

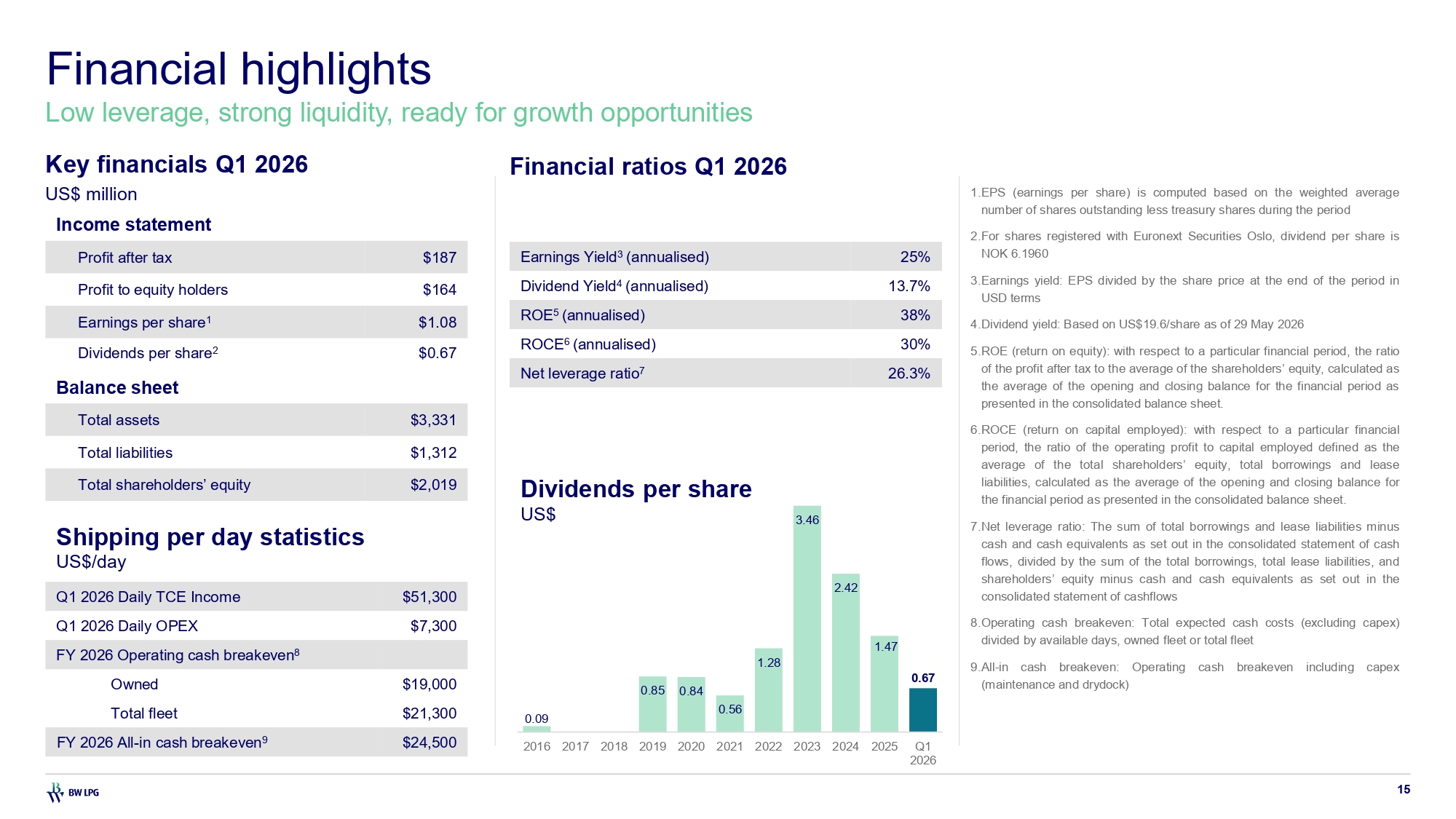

$51,300 Q1 2026 Daily TCE Income $7,300 Q1 2026 Daily OPEX FY 2026 Operating cash breakeven 8 $19,000 Owned $21,300 Total fleet $24,500 FY 2026 All - in cash breakeven 9 Income statement $187 Profit after tax $164 Profit to equity holders $1.08 Earnings per share 1 $0.67 Dividends per share 2 Balance sheet $3,331 Total assets $1,312 Total liabilities $2,019 Total shareholders’ equity 25% Earnings Yield 3 (annualised) 13.7% Dividend Yield 4 (annualised) 38% ROE 5 (annualised) 30% ROCE 6 (annualised) 26.3% Net leverage ratio 7 0.09 0.85 0.84 0.56 1.28 3.46 2.42 1.47 0.67 2016 2017 2018 2019 2020 2021 2022 2023 2024 2025 Q1 2026 1. EPS (earnings per share) is computed based on the weighted average number of shares outstanding less treasury shares during the period 2. For shares registered with Euronext Securities Oslo, dividend per share is NOK 6 . 1960 3. Earnings yield : EPS divided by the share price at the end of the period in USD terms 4. Dividend yield : Based on US $ 19 . 6 /share as of 29 May 2026 5. ROE (return on equity) : with respect to a particular financial period, the ratio of the profit after tax to the average of the shareholders’ equity, calculated as the average of the opening and closing balance for the financial period as presented in the consolidated balance sheet . 6. ROCE (return on capital employed) : with respect to a particular financial period, the ratio of the operating profit to capital employed defined as the average of the total shareholders’ equity, total borrowings and lease liabilities, calculated as the average of the opening and closing balance for the financial period as presented in the consolidated balance sheet . 7. Net leverage ratio : The sum of total borrowings and lease liabilities minus cash and cash equivalents as set out in the consolidated statement of cash flows, divided by the sum of the total borrowings, total lease liabilities, and shareholders’ equity minus cash and cash equivalents as set out in the consolidated statement of cashflows 8. Operating cash breakeven : Total expected cash costs (excluding capex) divided by available days, owned fleet or total fleet 9. All - in cash breakeven : Operating cash breakeven including capex (maintenance and drydock) Financial highlights Low leverage, strong liquidity, ready for growth opportunities Key financials Q1 2026 US$ million Financial ratios Q1 2026 Dividends per share US$ Shipping per day statistics US$/day 15

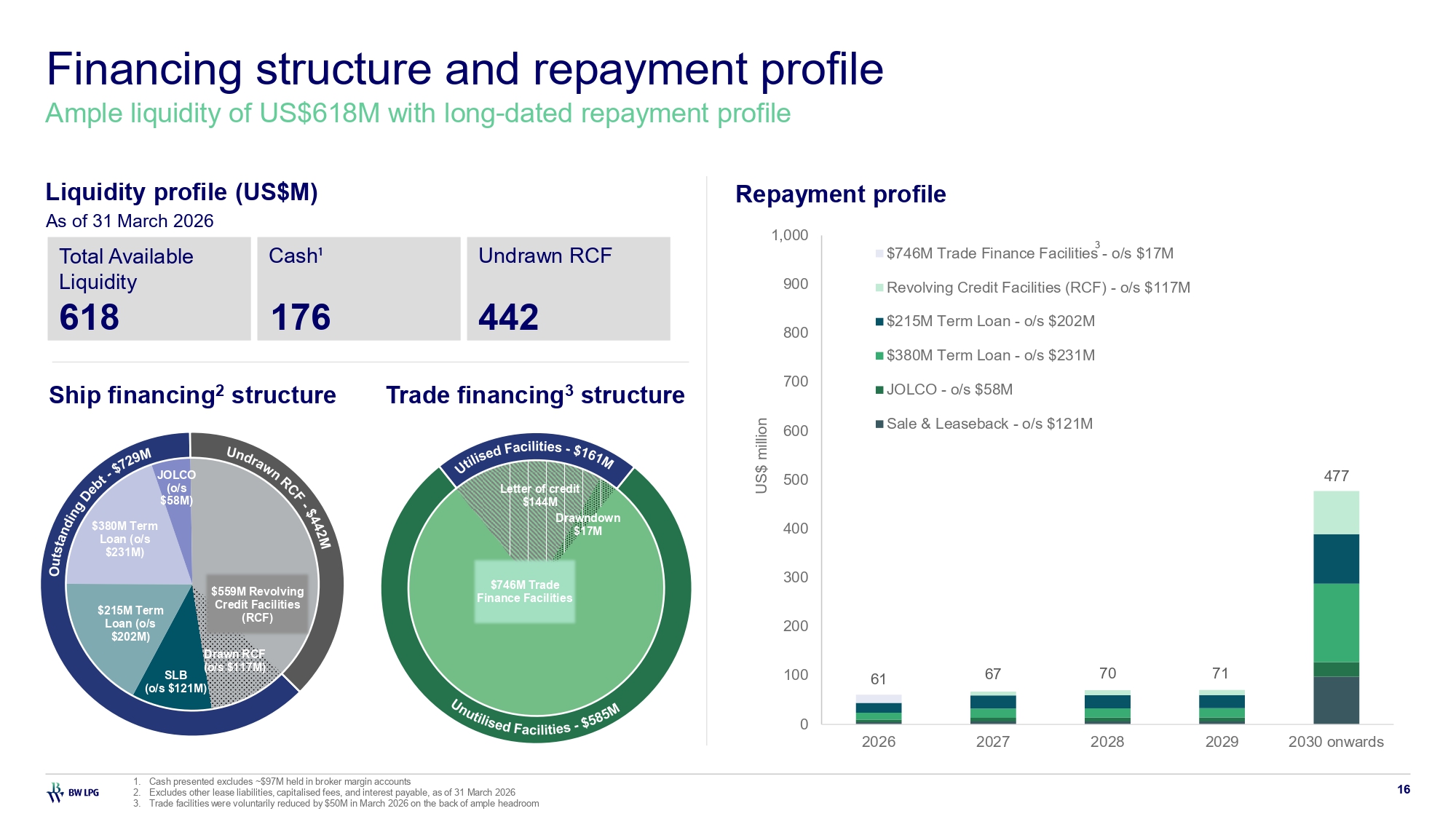

61 67 70 71 477 0 100 200 300 400 500 600 700 800 900 1,000 2026 2027 2028 2029 2030 onwards US$ million $746M Trade Finance Facilities - o/s $17M Revolving Credit Facilities (RCF) - o/s $117M $215M Term Loan - o/s $202M $380M Term Loan - o/s $231M JOLCO - o/s $58M Sale & Leaseback - o/s $121M Total Available Liquidity 618 Undrawn RCF 442 Cash ¹ 176 Financing structure and repayment profile Ample liquidity of US$618M with long - dated repayment profile 1. Cash presented excludes ~$97M held in broker margin accounts 2. Excludes other lease liabilities, capitalised fees, and interest payable, as of 31 March 2026 3. Trade facilities were voluntarily reduced by $50M in March 2026 on the back of ample headroom Liquidity profile (US$M) As of 31 March 2026 Repayment profile Ship financing 2 structure Trade financing 3 structure 16 SLB (o/s $121M) $215M Term Loan (o/s $202M) $380M Term Loan (o/s $231M) JOLCO (o/s $58M) $559M Revolving Credit Facilities (RCF) Drawn RCF (o/s $117M) Letter of credit $144M Drawndown $17M $746M Trade Finance Facilities 3

Agenda Q1 2026 Q1 2026 highlights and market outlook Market overview Company performance Q&A

Q&A Kristian Sørensen CEO Samantha Xu CFO

Thank you Investor Relations investor.relations@bwlpg.com Ticker Oslo Stock Exchange “ BWLPG” New York Stock Exchange “BWLP” LinkedIn linkedin.com/company/ bwlpg Website https://www.bwlpg.com/investor/ Telephone +65 6705 5588 Address 10 Pasir Panjang Road Mapletree Business City #17 - 02 Singapore 117438

Appendix Q1 2026

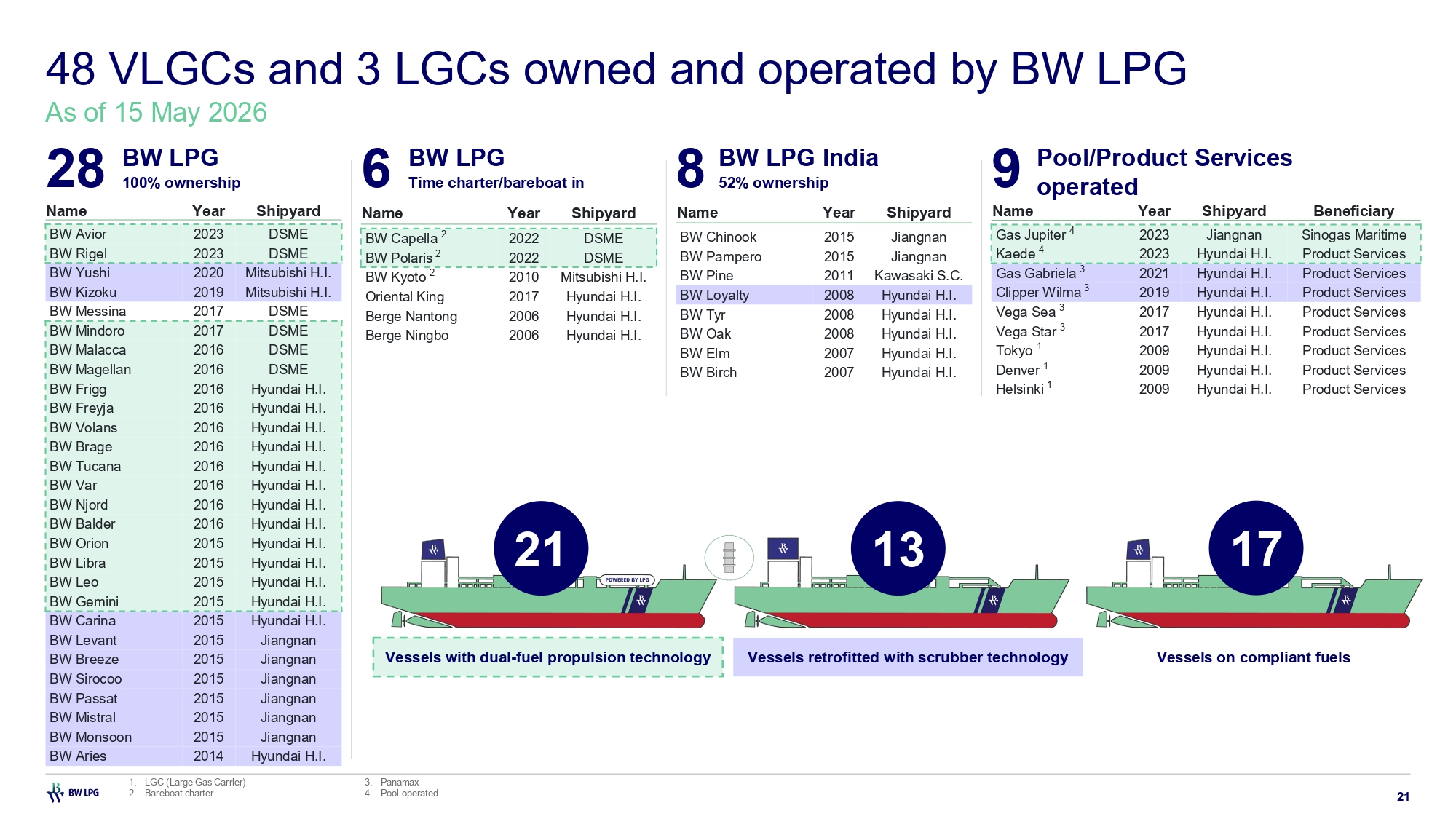

BW LPG 100% ownership 48 VLGCs and 3 LGCs owned and operated by BW LPG 1. LGC (Large Gas Carrier) 2. Bareboat charter As of 15 May 2026 Vessels with dual - fuel propulsion technology Vessels on compliant fuels 21 28 BW LPG Time charter/bareboat in 6 BW LPG India 52% ownership 8 Pool/Product Services operated 9 3. Panamax 4. Pool operated Vessels retrofitted with scrubber technology 13 17 Shipyard Year Name DSME 2023 BW Avior DSME 2023 BW Rigel Mitsubishi H.I. 2020 BW Yushi Mitsubishi H.I. 2019 BW Kizoku DSME 2017 BW Messina DSME 2017 BW Mindoro DSME 2016 BW Malacca DSME 2016 BW Magellan Hyundai H.I. 2016 BW Frigg Hyundai H.I. 2016 BW Freyja Hyundai H.I. 2016 BW Volans Hyundai H.I. 2016 BW Brage Hyundai H.I. 2016 BW Tucana Hyundai H.I. 2016 BW Var Hyundai H.I. 2016 BW Njord Hyundai H.I. 2016 BW Balder Hyundai H.I. 2015 BW Orion Hyundai H.I. 2015 BW Libra Hyundai H.I. 2015 BW Leo Hyundai H.I. 2015 BW Gemini Hyundai H.I. 2015 BW Carina Jiangnan 2015 BW Levant Jiangnan 2015 BW Breeze Jiangnan 2015 BW Sirocoo Jiangnan 2015 BW Passat Jiangnan 2015 BW Mistral Jiangnan 2015 BW Monsoon Hyundai H.I. 2014 BW Aries Shipyard Year Name DSME 2022 BW Capella 2 DSME 2022 BW Polaris 2 Mitsubishi H.I. 2010 BW Kyoto 2 Hyundai H.I. 2017 Oriental King Hyundai H.I. 2006 Berge Nantong Hyundai H.I. 2006 Berge Ningbo Shipyard Year Name Jiangnan 2015 BW Chinook Jiangnan 2015 BW Pampero Kawasaki S.C. 2011 BW Pine Hyundai H.I. 2008 BW Loyalty Hyundai H.I. 2008 BW Tyr Hyundai H.I. 2008 BW Oak Hyundai H.I. 2007 BW Elm Hyundai H.I. 2007 BW Birch Beneficiary Shipyard Year Name Sinogas Maritime Jiangnan 2023 Gas Jupiter 4 Product Services Hyundai H.I. 2023 Kaede 4 Product Services Hyundai H.I. 2021 Gas Gabriela 3 Product Services Hyundai H.I. 2019 Clipper Wilma 3 Product Services Hyundai H.I. 2017 Vega Sea 3 Product Services Hyundai H.I. 2017 Vega Star 3 Product Services Hyundai H.I. 2009 Tokyo 1 Product Services Hyundai H.I. 2009 Denver 1 Product Services Hyundai H.I. 2009 Helsinki 1 21

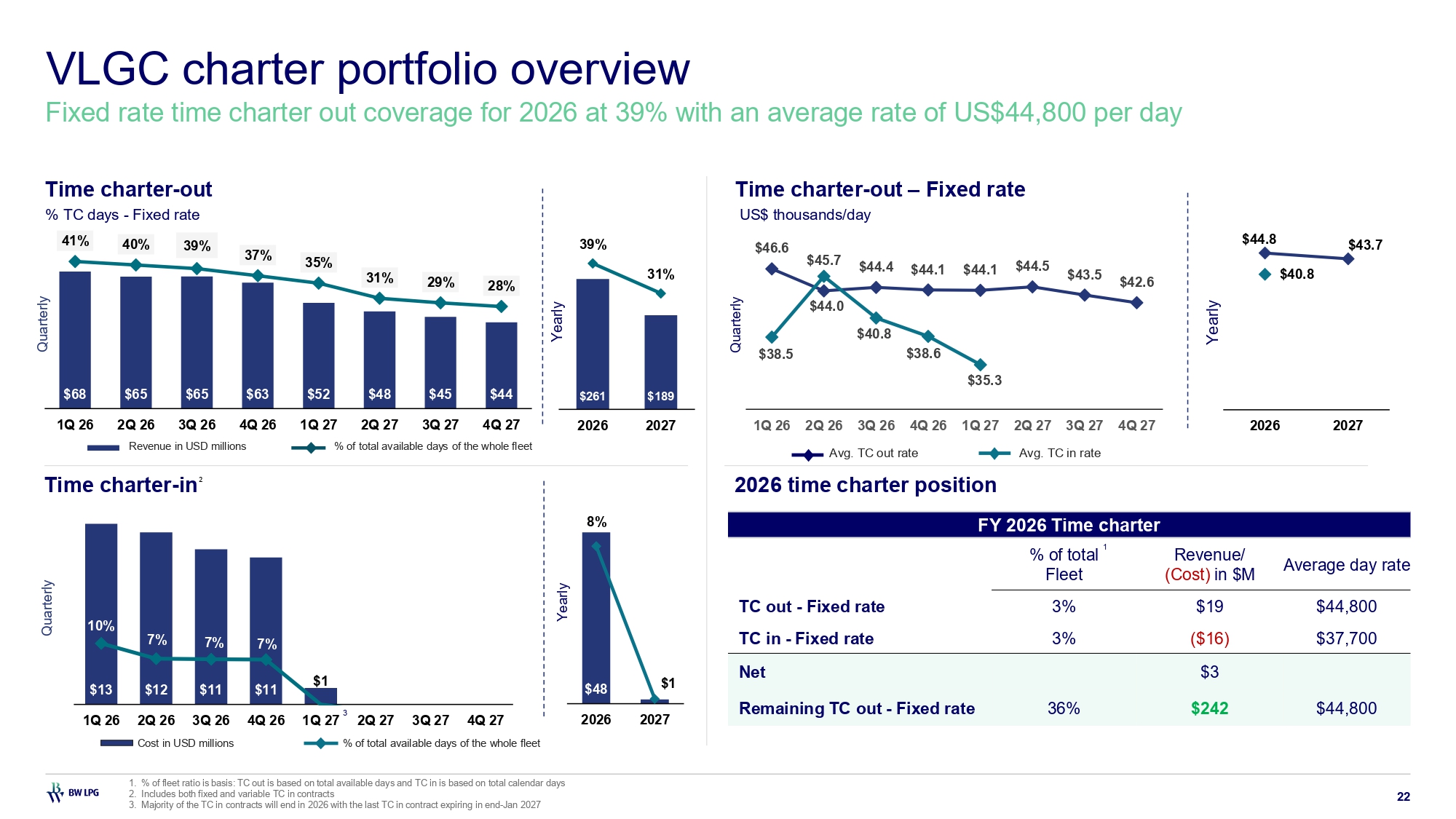

$48 $1 8% 2026 2027 $13 $12 $11 $11 $1 10% 7% 7% 7% 1Q 26 2Q 26 3Q 26 4Q 26 1Q 27 2Q 27 3Q 27 4Q 27 Quarterly 2 $68 $65 $65 $63 $52 $48 $45 $44 41% 40% 39% 37% 35% 31% 29% 28% 1Q 26 2Q 26 3Q 26 4Q 26 1Q 27 2Q 27 3Q 27 4Q 27 Quarterly $261 $189 39% 31% 2026 2027 $46.6 $44.0 $44.4 $44.1 $44.1 $44.5 $43.5 $42.6 $38.5 $45.7 $40.8 $38.6 $35.3 1Q 26 2Q 26 3Q 26 4Q 26 1Q 27 2Q 27 3Q 27 4Q 27 Quarterly Avg. TC out rate Avg. TC in rate FY 2026 Time charter Average day rate Revenue/ (Cost) in $M % of total Fleet $44,800 $19 3% TC out - Fixed rate $37,700 ($16) 3% TC in - Fixed rate $3 Net $44,800 $242 36% Remaining TC out - Fixed rate VLGC charter portfolio overview 22 Fixed rate time charter out coverage for 2026 at 39% with an average rate of US$44,800 per day Time charter - out – Fixed rate US$ thousands/day 1. % of fleet ratio is basis: TC out is based on total available days and TC in is based on total calendar days 2. Includes both fixed and variable TC in contracts 3. Majority of the TC in contracts will end in 2026 with the last TC in contract expiring in end - Jan 2027 Time charter - in 2026 time charter position Revenue in USD millions % of total available days of the whole fleet Cost in USD millions % of total available days of the whole fleet Yearly Yearly Yearly 3 Time charter - out % TC days - Fixed rate 1 $44.8 $43.7 $40.8 2026 2027

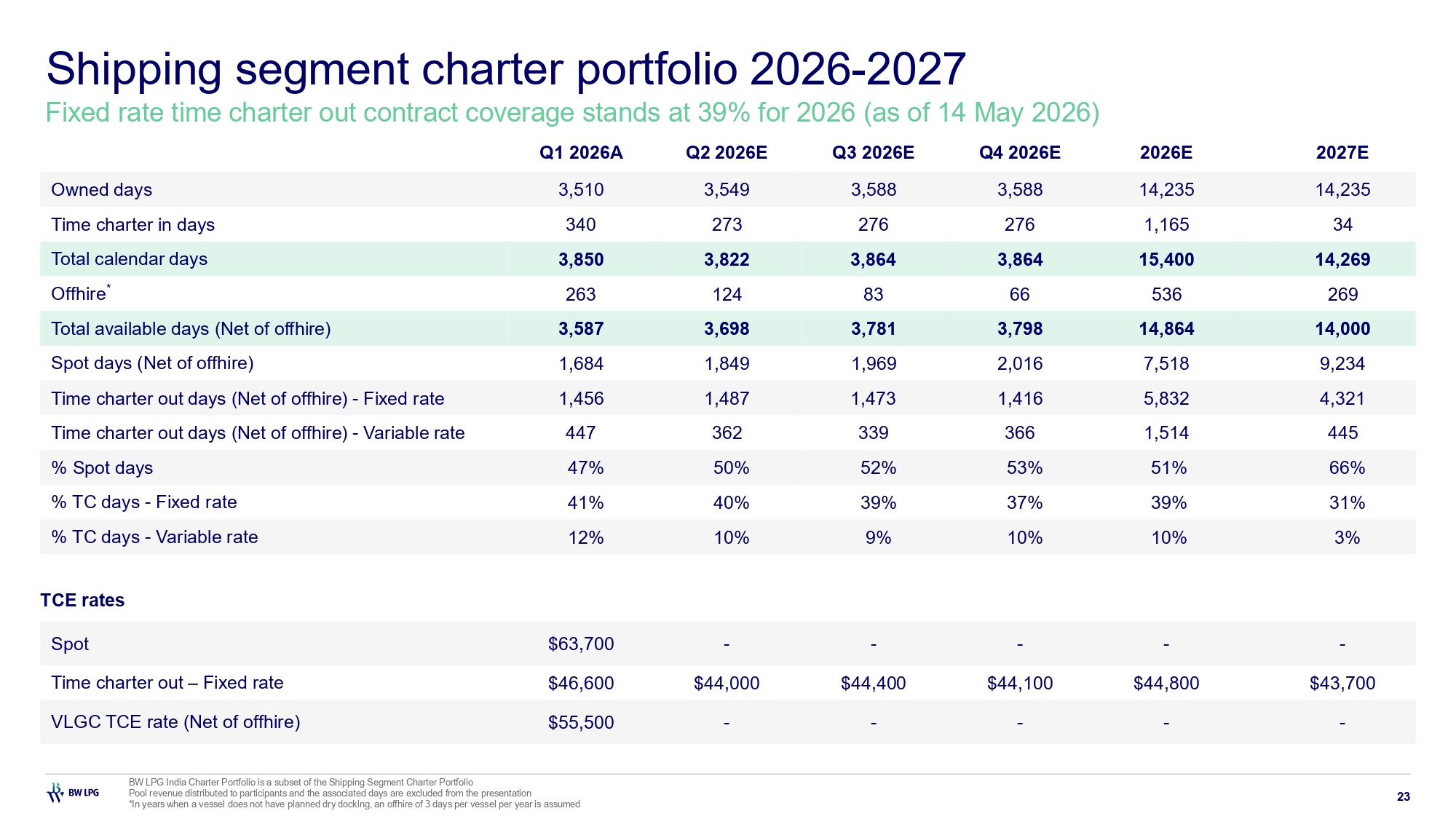

2027E 2026E Q4 2026E Q3 2026E Q2 2026E Q1 2026A 14,235 14,235 3,588 3,588 3,549 3,510 Owned days 34 1,165 276 276 273 340 Time charter in days 14,269 15,400 3,864 3,864 3,822 3,850 Total calendar days 269 536 66 83 124 263 Offhire * 14,000 14,864 3,798 3,781 3,698 3,587 Total available days (Net of offhire ) 9,234 7,518 2,016 1,969 1,849 1,684 Spot days (Net of offhire ) 4,321 5,832 1,416 1,473 1,487 1,456 Time charter out days (Net of offhire ) - Fixed rate 445 1,514 366 339 362 447 Time charter out days (Net of offhire ) - Variable rate 66% 51% 53% 52% 50% 47% % Spot days 31% 39% 37% 39% 40% 41% % TC days - Fixed rate 3% 10% 10% 9% 10% 12% % TC days - Variable rate TCE rates - - - - - $63,700 Spot $43,700 $44,800 $44,100 $44,400 $44,000 $46,600 Time charter out – Fixed rate - - - - - $55,500 VLGC TCE rate (Net of offhire ) Shipping segment charter portfolio 2026 - 2027 23 Fixed rate time charter out contract coverage stands at 39 % for 2026 (as of 14 May 2026) BW LPG India Charter Portfolio is a subset of the Shipping Segment Charter Portfolio Pool revenue distributed to participants and the associated days are excluded from the presentation *In years when a vessel does not have planned dry docking, an offhire of 3 days per vessel per year is assumed

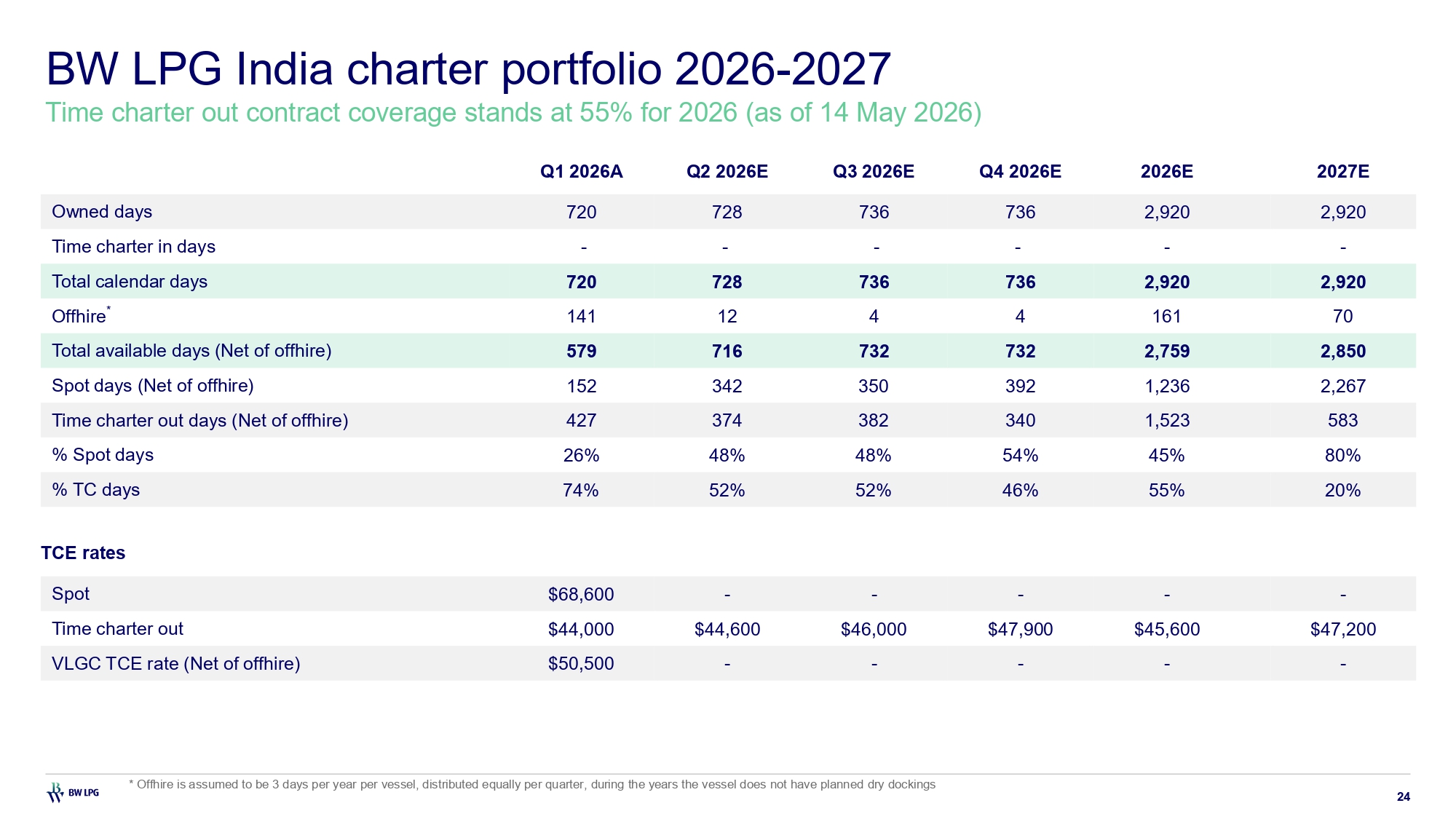

2027E 2026E Q4 2026E Q3 2026E Q2 2026E Q1 2026A 2,920 2,920 736 736 728 720 Owned days - - - - - - Time charter in days 2,920 2,920 736 736 728 720 Total calendar days 70 161 4 4 12 141 Offhire * 2,850 2,759 732 732 716 579 Total available days (Net of offhire ) 2,267 1,236 392 350 342 152 Spot days (Net of offhire ) 583 1,523 340 382 374 427 Time charter out days (Net of offhire ) 80% 45% 54% 48% 48% 26% % Spot days 20% 55% 46% 52% 52% 74% % TC days TCE rates - - - - - $68,600 Spot $47,200 $45,600 $47,900 $46,000 $44,600 $44,000 Time charter out - - - - - $50,500 VLGC TCE rate (Net of offhire ) BW LPG India charter portfolio 2026 - 2027 24 Time charter out contract coverage stands at 55% for 2026 (as of 14 May 2026) * Offhire is assumed to be 3 days per year per vessel, distributed equally per quarter, during the years the vessel does not have plann ed dry dockings

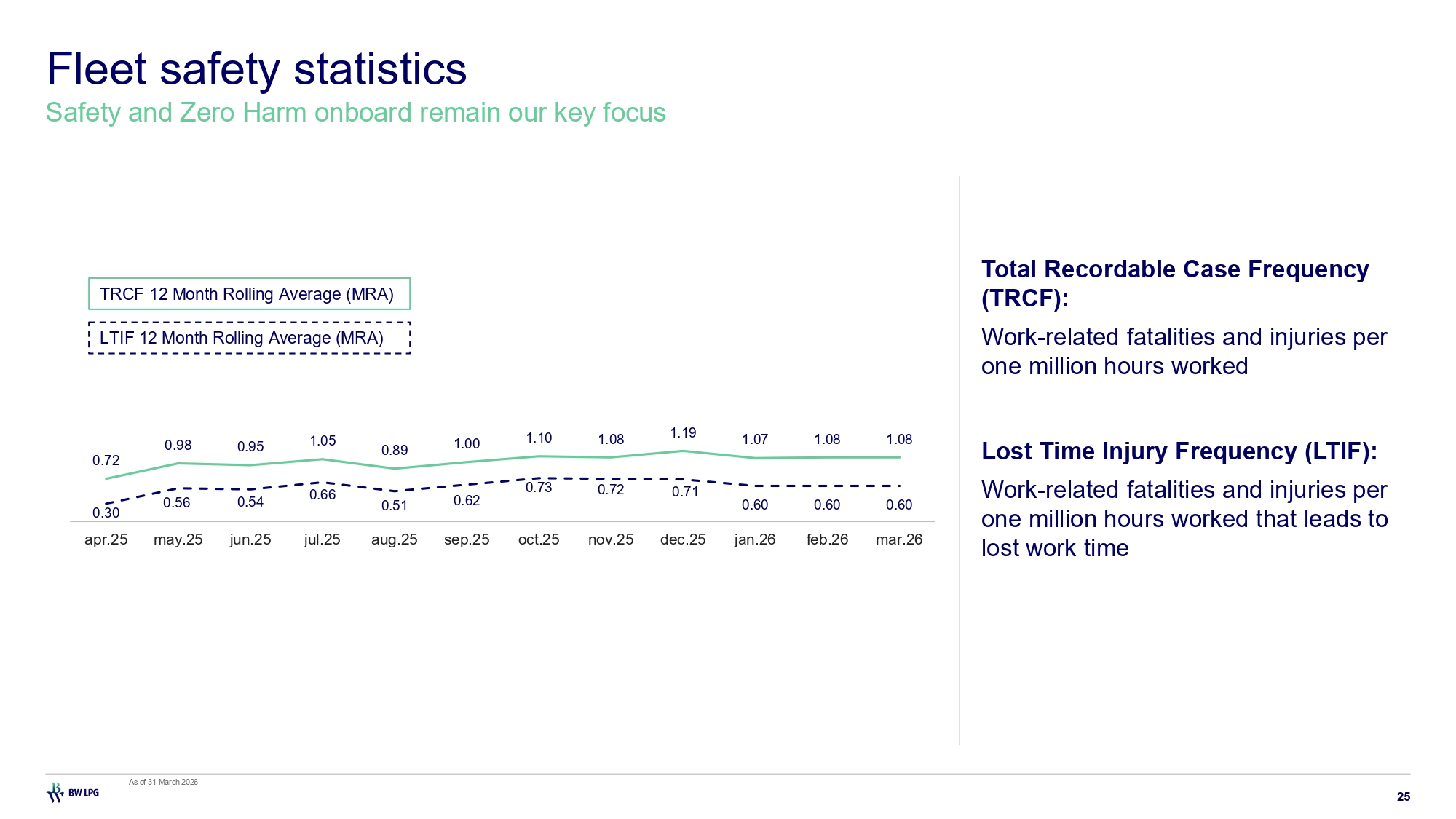

0.72 0.98 0.95 1.05 0.89 1.00 1.10 1.08 1.19 1.07 1.08 1.08 0.30 0.56 0.54 0.66 0.51 0.62 0.73 0.72 0.71 0.60 0.60 0.60 apr.25 may.25 jun.25 jul.25 aug.25 sep.25 oct.25 nov.25 dec.25 jan.26 feb.26 mar.26 Fleet safety statistics 25 Safety and Zero Harm onboard remain our key focus Total Recordable Case Frequency (TRCF): Work - related fatalities and injuries per one million hours worked Lost Time Injury Frequency (LTIF): Work - related fatalities and injuries per one million hours worked that leads to lost work time TRCF 12 Month Rolling Average ( MRA ) LTIF 12 Month Rolling Average (MRA) As of 31 March 2026