Registered in England and Wales No. 3688365

Exhibit 96.2

| AMC Consultants (UK) Limited Registered in England and Wales No. 3688365 |

|

| Office 336a, Davidson House, Forbury Square | |

| Reading RG1 3EU | |

| United Kingdom | |

| T +44 1628 778 256 | |

| E unitedkingdom@amcconsultants.com | |

| amcconsultants.com |

Report

S-K 1300 Technical Report Summary: KCM Integrated Operations (Preliminary Feasibility Study)

Konkola Copper Mines Plc

AMC Project 0424076

2 June 2026

mine smarter

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

QUALIFIED PERSON — DATE AND SIGNATURE PAGE

This Technical Report Summary has been prepared by AMC Consultants (UK) Limited, acting as the Qualified Person for all sections of this report. In accordance with Instruction 5 to Item 601(b)(96) of Regulation S-K, AMC Consultants (UK) Limited is an entity that satisfies the requirements of a qualified person under § 229.1300(b) and assumes responsibility for the Technical Report Summary as a whole.

AMC Consultants (UK) Limited confirms that it has the relevant experience, competence, and professional qualifications required to prepare and take responsibility for all sections of this TRS. The individual professionals within AMC who contributed to this report possess qualifications and experience appropriate to the subject matter of their contributions and are members of recognised professional organizations.

| Qualified Person: | Sections Responsible: |

|

AMC Consultants (UK) Limited Registered in England and Wales No. 3688365 Office 336a, Davidson House, Forbury Square Reading RG1 3EU, United Kingdom |

All sections (Sections 1 through 25) |

| Signature: | Date: |

| Karl van Olden | 2 June 2026 |

|

Authorised Signatory AMC Consultants (UK) Limited |

| Effective Date of TRS: | 1 April 2026 |

| Date of Report: | 2 June 2026 |

| AMC Project Number: | 0424076 |

Note: Pursuant to Instruction 5 to Item 601(b)(96), where an entity rather than an individual serves as the qualified person, the entity assumes responsibility for the Technical Report Summary. The authorised signatory executes this page on behalf of AMC Consultants (UK) Limited in its capacity as Qualified Person.

amcconsultants.com | i |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

Contents

| 1 | Executive summary | 15 | ||

| 1.1 | Introduction | 15 | ||

| 1.2 | Property description and ownership | 15 | ||

| 1.3 | Mineral rights | 16 | ||

| 1.4 | Geology and mineralisation | 16 | ||

| 1.5 | Exploration status | 16 | ||

| 1.6 | Development and operations status | 17 | ||

| 1.7 | Mineral Reserve estimate | 17 | ||

| 1.8 | Mineral Resources | 19 | ||

| 1.9 | Mining methods | 20 | ||

| 1.10 | Processing and recovery methods | 21 | ||

| 1.11 | Infrastructure | 22 | ||

| 1.12 | Economic analysis summary | 22 | ||

| 1.13 | Sensitivity analysis | 25 | ||

| 1.14 | Environmental studies, permitting, and social or community impact | 26 | ||

| 1.15 | Qualified Person's conclusions | 26 | ||

| 2 | Introduction | 27 | ||

| 2.1 | Registrant for whom the TRS was prepared | 27 | ||

| 2.2 | Terms of reference and purpose | 27 | ||

| 2.3 | Units of measure | 27 | ||

| 2.4 | Defined terms and abbreviations | 27 | ||

| 2.5 | Sources of information | 28 | ||

| 2.6 | Personal inspection of the property | 29 | ||

| 2.7 | Summary of previously filed technical report | 29 | ||

| 2.8 | Qualified Persons | 29 | ||

| 2.9 | Reliance on the registrant | 29 | ||

| 3 | Property description | 30 | ||

| 3.1 | Property description | 30 | ||

| 3.2 | Project location | 30 | ||

| 3.3 | Description of property rights | 32 | ||

| 3.3.1 | Surface and access rights | 33 | ||

| 3.4 | Mineral rights | 33 | ||

| 3.5 | Royalty payments | 34 | ||

| 3.6 | Significant encumbrances to the property | 34 | ||

| 3.6.1 | Environmental compliance obligations | 35 | ||

| 3.6.2 | Permit conditions | 35 | ||

| 3.6.3 | Social and land use obligations | 35 | ||

| 3.7 | Significant factors and risks affecting access | 35 | ||

| 3.7.1 | Operational risks | 35 | ||

| 3.7.2 | Regulatory and social risks | 36 | ||

| 4 | Accessibility, climate, local resources, infrastructure, and physiography | 37 | ||

| 4.1 | Topography and land description | 37 | ||

| 4.1.1 | Flora and fauna | 37 | ||

| 4.2 | Access to the property | 37 | ||

| 4.2.1 | Regional access | 37 | ||

| 4.2.2 | Highways and roads | 37 | ||

| 4.2.3 | Rivers and waterways | 38 | ||

| 4.2.4 | Railroads | 38 | ||

| 4.2.5 | Airports and air access | 38 | ||

| 4.2.6 | Inter-site access and product transport routes | 39 | ||

| 4.3 | Climate description | 41 | ||

amcconsultants.com | ii |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| 4.4 | Availability of required infrastructure | 41 | |||

| 4.4.1 | Power | 41 | |||

| 4.4.2 | Water | 41 | |||

| 4.4.3 | Supplies | 41 | |||

| 4.4.4 | Personnel | 41 | |||

| 5 | History | 42 | |||

| 5.1 | Early exploration and discovery (pre-1950) | 42 | |||

| 5.1.1 | Nchanga | 42 | |||

| 5.1.2 | Konkola | 42 | |||

| 5.2 | Systematic development and state ownership (1950s–1999) | 42 | |||

| 5.2.1 | Expansion under colonial and early independence era (1950s–1969) | 42 | |||

| 5.2.2 | Nationalisation and ZCCM era (1969–1999) | 43 | |||

| 5.3 | Privatisation and Anglo American Corporation (2000–2002) | 43 | |||

| 5.4 | Vedanta Resources (2004–2019) | 43 | |||

| 5.5 | Provisional liquidation (2019–2024) | 44 | |||

| 5.5.1 | Production curtailment | 44 | |||

| 5.5.2 | Exploration and development activity | 45 | |||

| 5.5.3 | Infrastructure condition | 45 | |||

| 5.5.4 | Resolution and resumption of control | 45 | |||

| 5.6 | Production history | 45 | |||

| 5.7 | Key development milestones | 47 | |||

| 6 | Geological setting, mineralisation, and deposit | 48 | |||

| 6.1 | Regional geology | 48 | |||

| 6.1.1 | Lithostratigraphy of the Central African Copperbelt | 50 | |||

| 6.1.2 | Mineralisation genesis | 51 | |||

| 6.1.3 | Structural and tectonic evolution | 51 | |||

| 6.2 | Local and property geology | 52 | |||

| 6.2.1 | Stratigraphy | 52 | |||

| 6.2.2 | Mineralisation | 53 | |||

| 6.2.2.1 | Primary sulfide mineralisation | 54 | |||

| 6.2.2.2 | Supergene enrichment and secondary mineralisation | 55 | |||

| 6.2.2.3 | Hydrothermal alteration | 56 | |||

| 6.2.2.4 | Variability in mineralisation across mining areas | 56 | |||

| 6.2.3 | Major structural controls on mineralisation | 56 | |||

| 6.2.3.1 | Summary of geological characteristics | 57 | |||

| 6.3 | Nchanga – deposit geology summary | 59 | |||

| 6.4 | TD03 and TD04 – tailings characterisation | 60 | |||

| 6.5 | Nampundwe – pyrite deposit summary | 60 | |||

| 7 | Exploration | 61 | |||

| 7.1 | Konkola Mine | 61 | |||

| 7.1.1 | Exploration history | 61 | |||

| 7.1.2 | Drilling methods | 62 | |||

| 7.1.3 | Core recovery | 62 | |||

| 7.1.4 | Core logging | 62 | |||

| 7.1.5 | Sample selection | 62 | |||

| 7.1.6 | QAQC program | 63 | |||

| 7.1.7 | Drillhole locations | 63 | |||

| 7.1.8 | Hydrogeology | 64 | |||

| 7.1.8.1 | Hydrogeological setting | 64 | |||

| 7.1.8.2 | Stratigraphic hydrogeological units | 64 | |||

| 7.1.8.3 | Hydrogeological investigations and data | 66 | |||

| 7.1.8.4 | Groundwater inflow summary | 66 | |||

| 7.1.8.5 | Aquifer characterisation | 67 | |||

| 7.1.8.6 | Assessment status and data gaps | 67 | |||

amcconsultants.com | iii |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| 7.1.9 | Geotechnical data, testing, and analysis | 68 | |||

| 7.1.9.1 | Geotechnical data sources | 68 | |||

| 7.1.9.2 | Geotechnical testing – rock properties | 69 | |||

| 7.1.9.3 | Rock mass classification summary by domain | 71 | |||

| 7.1.9.4 | Seismicity | 71 | |||

| 7.1.9.5 | In situ stress | 72 | |||

| 7.1.9.6 | Geotechnical data gaps and recommended actions | 72 | |||

| 7.2 | TD03 and TD04 – exploration and characterisation | 73 | |||

| 7.3 | Nchanga – exploration summary | 73 | |||

| 7.4 | Nampundwe – exploration summary | 74 | |||

| 8 | Sample preparation, analyses, and security | 75 | |||

| 8.1 | Sample preparation and analysis | 75 | |||

| 8.2 | Sample preparation method | 75 | |||

| 8.3 | Analytical method | 75 | |||

| 8.4 | Bulk density measurement | 75 | |||

| 8.5 | Quality assurance quality control | 76 | |||

| 8.5.1 | QAQC protocols | 76 | |||

| 8.5.2 | QAQC assessment — Konkola | 76 | |||

| 8.5.2.1 | CRM analysis — Konkola | 77 | |||

| 8.5.2.2 | Repeat analysis — Konkola | 80 | |||

| 8.5.2.3 | Blank analysis — Konkola | 81 | |||

| 8.5.3 | QAQC conclusion | 81 | |||

| 8.6 | Qualified Person’s opinion | 82 | |||

| 8.6.1 | Historical data | 82 | |||

| 8.6.2 | QP’s opinion on sample preparation, security and analytical procedures | 82 | |||

| 8.6.3 | Assessment of QAQC findings | 82 | |||

| 8.6.4 | Implication for Mineral Resource confidence | 83 | |||

| 8.6.5 | Laboratory condition and umpire laboratory | 83 | |||

| 8.6.6 | QAQC recommendations for DFS | 83 | |||

| 9 | Data verification | 85 | |||

| 9.1 | Historic data | 85 | |||

| 9.2 | Modern data | 85 | |||

| 9.2.1 | Database | 85 | |||

| 9.2.2 | Exported data validation | 85 | |||

| 9.2.3 | Data verification | 86 | |||

| 9.2.4 | Database security | 86 | |||

| 9.3 | Data verification limitations | 86 | |||

| 9.4 | Qualified Person’s opinion | 87 | |||

| 10 | Mineral processing and metallurgical testing | 89 | |||

| 10.1 | Testing nature, extent, and analytical procedures | 89 | |||

| 10.2 | Testing laboratories | 89 | |||

| 10.3 | Test sample representativity | 89 | |||

| 10.4 | Testing results, assumptions, and deleterious elements | 90 | |||

| 10.4.1 | Konkola Concentrator | 90 | |||

| 10.4.1.1 | Processing factors | 91 | |||

| 10.4.1.2 | Deleterious elements and gangue mineralogy | 91 | |||

| 10.4.1.3 | Qualified Person’s opinion | 92 | |||

| 10.4.2 | Nchanga TLP | 93 | |||

| 10.4.2.1 | Processing factors | 95 | |||

| 10.4.2.2 | Deleterious elements and gangue factors | 96 | |||

| 10.4.2.3 | Qualified Person’s opinion | 96 | |||

| 10.5 | Qualified Person’s opinion — Mineral processing and metallurgical testing | 97 | |||

amcconsultants.com | iv |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| 11 | Mineral Resource estimates | 99 | |||

| 11.1 | Context | 99 | |||

| 11.2 | Konkola Mineral Resource estimate | 100 | |||

| 11.2.1 | Classification criteria | 101 | |||

| 11.2.2 | Cut-off grade derivation | 102 | |||

| 11.2.2.1 | Mineral Resource cut-off grade | 102 | |||

| 11.2.2.2 | Mineral Reserve cut-off — relationship to Mineral Resource COG | 103 | |||

| 11.2.3 | Mineral Resource uncertainty | 103 | |||

| 11.2.3.1 | Data | 103 | |||

| 11.2.3.2 | Data quality and QAQC | 104 | |||

| 11.2.3.3 | Geological model | 104 | |||

| 11.2.3.4 | Estimation | 104 | |||

| 11.2.3.5 | Economic assumptions | 104 | |||

| 11.2.4 | Uncertainty by classification — integrated assessment | 105 | |||

| 11.2.5 | Mineral Resource estimate | 107 | |||

| 11.3 | TD03 and TD04 | 108 | |||

| 11.3.1 | Data | 108 | |||

| 11.3.2 | Generation of volume / tonnage and grade | 108 | |||

| 11.3.3 | Mining, processing, and recovery | 109 | |||

| 11.3.4 | Classification criteria | 109 | |||

| 11.3.5 | Mineral Resource uncertainty | 110 | |||

| 11.3.6 | Mineral Resource estimate | 110 | |||

| 11.4 | Qualified Person’s opinion | 111 | |||

| 12 | Mineral Reserve estimates | 112 | |||

| 12.1 | Konkola Mine - Mineral Reserves | 112 | |||

| 12.1.1 | Scope of Mineral Reserves and relationship to companion IA TRS | 112 | |||

| 12.1.2 | Reserve classification and statement | 113 | |||

| 12.2 | Key assumptions, parameters, and methods used | 114 | |||

| 12.3 | Modifying factors | 115 | |||

| 12.3.1 | Dilution and mining recovery | 115 | |||

| 12.3.2 | Cut-off value | 115 | |||

| 12.3.3 | Konkola NSR | 116 | |||

| 12.3.4 | Royalty payments | 117 | |||

| 12.3.5 | NSR cut-off value | 117 | |||

| 12.4 | Mineral Reserve risk factors | 117 | |||

| 13 | Mining methods | 118 | |||

| 13.1 | Cautionary statement regarding forward-looking information | 118 | |||

| 13.2 | Mining method selection | 118 | |||

| 13.3 | Geotechnical models and parameters | 121 | |||

| 13.3.1 | Rock mass classification | 121 | |||

| 13.3.2 | Geotechnical domains | 121 | |||

| 13.3.3 | Structural geology | 130 | |||

| 13.3.4 | Geotechnical considerations for mining | 130 | |||

| 13.3.5 | Ground support and numerical modelling | 131 | |||

| 13.4 | Hydrogeology | 131 | |||

| 13.4.1 | Hydrogeology - Konkola Mine | 132 | |||

| 13.4.2 | Aquifer parameters and testing | 132 | |||

| 13.4.3 | Dewatering volumes and rates | 132 | |||

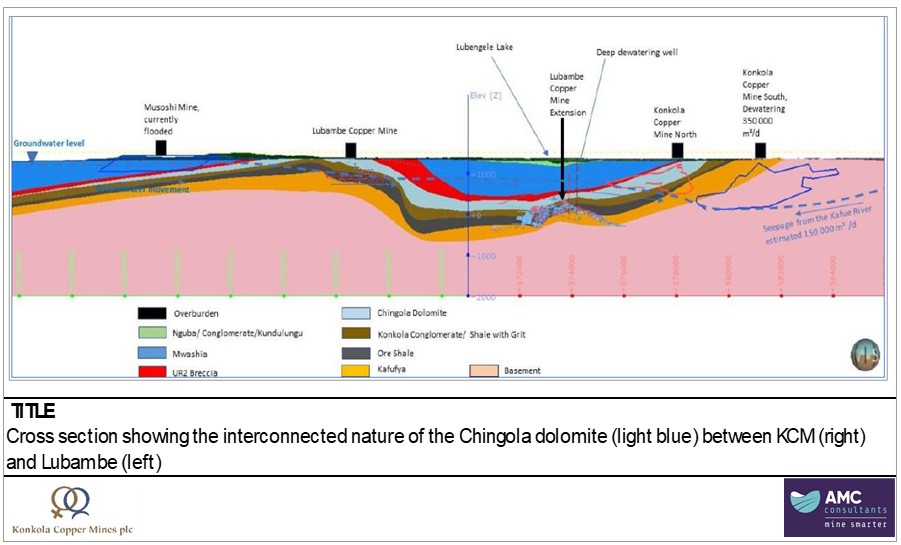

| 13.4.4 | Chingola dolomite | 133 | |||

| 13.4.5 | Recharge | 133 | |||

amcconsultants.com | v |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| 13.4.6 | Dewatering system and boreholes | 134 | |||

| 13.4.7 | Water Balance and groundwater model status | 135 | |||

| 13.4.8 | Water quality | 136 | |||

| 13.4.9 | Mine schedule and dewatering plan | 136 | |||

| 13.4.10 | Future dewatering rates | 138 | |||

| 13.4.11 | Pumping infrastructure – Konkola Mine | 139 | |||

| 13.4.12 | Konkola Mine water management infrastructure | 140 | |||

| 13.4.13 | Upgrade of existing pumping infrastructure | 141 | |||

| 13.4.14 | Dewatering risks | 142 | |||

| 13.5 | Existing mining operations | 142 | |||

| 13.6 | Production rates, mine life, mining unit dimensions, and dilution and recovery factors | 143 | |||

| 13.6.1 | Production rates and expected mine life | 143 | |||

| 13.6.2 | Mining unit dimensions | 144 | |||

| 13.6.3 | Mining dilution and recovery factors | 145 | |||

| 13.7 | Underground development and backfilling requirements | 145 | |||

| 13.7.1 | Underground development | 145 | |||

| 13.7.1.1 | Materials handling | 148 | |||

| 13.7.2 | Backfill requirements | 148 | |||

| 13.7.2.1 | Paste fill geomechanics and fill strength | 148 | |||

| 13.7.2.2 | Paste fill placement and retention | 150 | |||

| 13.7.2.3 | Paste fill costs | 150 | |||

| 13.7.2.4 | Paste fill project timeline and future test work | 151 | |||

| 13.8 | Ventilation | 151 | |||

| 13.8.1 | Air requirements | 151 | |||

| 13.8.2 | Ventilation design parameters | 151 | |||

| 13.8.3 | Development ventilation | 151 | |||

| 13.8.4 | Stoping ventilation | 152 | |||

| 13.8.5 | Temperature and refrigeration requirements | 152 | |||

| 13.8.6 | Ventilation requirements for diesel equipment | 152 | |||

| 13.8.7 | Primary ventilation | 153 | |||

| 13.9 | Mining equipment fleet | 155 | |||

| 13.10 | Mining personnel | 155 | |||

| 13.11 | Mining development and production schedule | 156 | |||

| 13.12 | Nchanga mining operations (Excluded from PFS) | 159 | |||

| 13.13 | Tailings reclamation | 159 | |||

| 13.13.1 | Sources of production TD03, TD04 | 159 | |||

| 13.13.2 | Tailings dam inventory | 160 | |||

| 13.13.3 | Processing methodology and plant design | 160 | |||

| 13.13.4 | Production schedule | 161 | |||

| 13.13.5 | Materials handling, slurry pumping | 161 | |||

| 13.13.6 | Tailings reclamation - Capital and operating costs | 161 | |||

| 13.13.6.1 | TD03 reclaim costs | 161 | |||

| 13.13.6.2 | TD04 reclaim costs | 161 | |||

| 13.13.6.3 | Capital provisions for TD04 | 161 | |||

| 14 | Processing and recovery methods | 162 | |||

| 14.1 | Konkola Concentrator | 163 | |||

| 14.1.1 | Konkola process description | 163 | |||

| 14.1.1.1 | Historical performance | 164 | |||

| 14.1.1.2 | Restart performance | 165 | |||

| 14.1.2 | Plant design and equipment | 168 | |||

| 14.1.3 | Plant operations | 168 | |||

| 14.1.4 | Konkola Concentrator production schedule | 170 | |||

| 14.2 | Nchanga concentrators | 172 | |||

amcconsultants.com | vi |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| 14.3 | Nchanga TLP | 172 | |||

| 14.3.1 | Historical performance | 174 | |||

| 14.3.2 | Restart performance | 175 | |||

| 14.3.2.1 | Plant design and equipment | 177 | |||

| 14.3.2.2 | Nchanga TLP production schedule | 177 | |||

| 14.4 | Nchanga Smelter | 178 | |||

| 14.4.1 | Recent smelter performance | 179 | |||

| 14.4.2 | Smelter condition | 183 | |||

| 14.4.3 | Concentrate blending and third-party feed requirements | 183 | |||

| 14.4.3.1 | Sources of third-party concentrate | 184 | |||

| 14.4.3.2 | Availability of third-party concentrate | 185 | |||

| 14.4.3.3 | Existing contracts and commercial terms | 186 | |||

| 14.4.3.4 | Alternatives to third-party concentrate procurement | 187 | |||

| 14.4.3.5 | Assessment of supply certainty | 188 | |||

| 14.5 | Nkana Refinery | 188 | |||

| 14.5.1 | Mode of operation, general condition | 188 | |||

| 14.5.2 | Production | 190 | |||

| 14.6 | Nampundwe Mine – pyrite flux production | 192 | |||

| 14.7 | Sulfuric acid plant | 192 | |||

| 14.8 | Proposed processing methods | 192 | |||

| 14.9 | Proposed flow sheet | 192 | |||

| 14.10 | Plant design and equipment | 192 | |||

| 14.11 | Plant operations | 193 | |||

| 15 | Infrastructure | 194 | |||

| 15.1 | Roads | 194 | |||

| 15.2 | Rail | 195 | |||

| 15.3 | Port facilities | 196 | |||

| 15.4 | Water dams | 196 | |||

| 15.5 | Dumps | 196 | |||

| 15.6 | Licensing and permitting | 197 | |||

| 15.7 | Konkola operation waste dumps | 197 | |||

| 15.8 | Tailings disposal | 198 | |||

| 15.8.1 | Tailings deposition locations | 198 | |||

| 15.8.2 | LOM capacity and expansion opportunities | 201 | |||

| 15.8.3 | Licensing and permitting | 202 | |||

| 15.8.3.1 | Stability and TSF management processes | 202 | |||

| 15.9 | Power | 203 | |||

| 15.9.1 | Existing operating power supply capacity and expansion | 204 | |||

| 15.9.2 | Emergency power supply and expansion | 204 | |||

| 15.10 | Water | 204 | |||

| 15.10.1 | Raw water | 204 | |||

| 15.10.2 | Konkola Mine raw water balance | 205 | |||

| 15.10.3 | Potable water (domestic water) | 205 | |||

| 15.11 | Pipelines | 205 | |||

| 15.12 | Ancillary surface infrastructure and expansions | 206 | |||

| 15.12.1 | Internal rail network | 206 | |||

| 15.12.2 | Office building | 206 | |||

| 15.12.3 | Change houses and other buildings | 206 | |||

| 15.13 | Nampundwe Mine infrastructure | 207 | |||

| 16 | Market studies | 208 | |||

| 16.1 | Market information | 208 | |||

| 16.1.1 | Market for KCM’s products | 208 | |||

| 16.1.2 | Copper demand | 208 | |||

amcconsultants.com | vii |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| 16.1.3 | Copper supply | 209 | |||

| 16.1.4 | Cobalt demand | 210 | |||

| 16.1.5 | Cobalt supply | 210 | |||

| 16.1.6 | Study price and sales terms | 210 | |||

| 16.1.7 | Copper pricing for NSR cut-off grade estimation | 211 | |||

| 16.2 | Contracts and status | 211 | |||

| 16.2.1 | Forward sales and hedging | 211 | |||

| 16.2.2 | Site development contracts | 212 | |||

| 16.2.3 | Operating contracts | 214 | |||

| 16.2.4 | Other agreements and contracts | 216 | |||

| 17 | Environmental studies, permitting, and social or community impact | 217 | |||

| 17.1 | Environmental studies, permitting, and social or community impact | 217 | |||

| 17.2 | Environmental studies, permitting, and social or community impact | 217 | |||

| 17.3 | Permitting requirements | 218 | |||

| 17.4 | Rehabilitation, closure, and post closure planning | 218 | |||

| 18 | Capital and operating costs | 219 | |||

| 18.1 | Cost estimate basis and accuracy | 219 | |||

| 18.1.1 | Estimation methodology | 219 | |||

| 18.1.2 | Cost estimate accuracy and contingency disclosure | 219 | |||

| 18.1.3 | Key assumptions and exclusions | 219 | |||

| 18.2 | Operating cost summary | 220 | |||

| 18.2.1 | Operating development | 220 | |||

| 18.2.2 | Stoping production cost | 220 | |||

| 18.2.3 | Power supply and consumption | 221 | |||

| 18.2.3.1 | Dewatering power consumption | 223 | |||

| 18.2.3.2 | Ventilation power consumption | 223 | |||

| 18.2.4 | Backfill | 223 | |||

| 18.2.5 | Underground rail tramming operations | 224 | |||

| 18.2.6 | Mine service functions | 224 | |||

| 18.2.7 | Labor and workforce costs | 224 | |||

| 18.2.8 | Mill consumable costs | 224 | |||

| 18.2.9 | Freight cost of concentrate | 224 | |||

| 18.2.10 | Maintenance services and operating lease hire | 224 | |||

| 18.2.11 | Water | 225 | |||

| 18.2.12 | Stores and spares and operating projects | 225 | |||

| 18.2.13 | Administrative operating costs | 225 | |||

| 18.2.14 | Corporate allocations | 225 | |||

| 18.2.15 | Summary | 225 | |||

| 18.3 | Capital cost summary | 227 | |||

| 18.3.1 | Growth capital | 227 | |||

| 18.3.2 | Sustaining capital and capitalised mining development | 228 | |||

| 18.3.3 | Form of capital cost estimate | 229 | |||

| 18.3.4 | Capital cost estimation methodology | 229 | |||

| 18.3.5 | Lateral and vertical underground development | 229 | |||

| 18.3.6 | Konkola Mine capital fit out | 229 | |||

| 18.3.7 | Konkola diamond drilling capital campaigns | 230 | |||

| 18.3.8 | Konkola Concentrator facility capital estimate | 230 | |||

| 18.3.9 | TD03 AND TD04 tailings reclamation capital costs | 230 | |||

| 18.3.10 | Smelter and refinery capital costs | 230 | |||

| 18.4 | Mine closure | 231 | |||

| 18.5 | Risk mitigation and cost control measures | 231 | |||

amcconsultants.com | viii |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| 19 | Economic analysis | 232 | |||

| 19.1 | Basis of economic analysis | 232 | |||

| 19.2 | Key assumptions | 232 | |||

| 19.2.1 | Byproducts included in the cash flow model | 232 | |||

| 19.2.2 | Production plan | 233 | |||

| 19.2.3 | Revenue | 235 | |||

| 19.2.4 | Third-party concentrate: basis for inclusion in economic analysis | 236 | |||

| 19.2.4.1 | Third-party concentrate sensitivity | 237 | |||

| 19.2.5 | Taxation and royalties | 238 | |||

| 19.3 | Economic results | 238 | |||

| 19.4 | Sensitivity analysis | 243 | |||

| 20 | Adjacent properties | 244 | |||

| 20.1 | Chililabombwe area | 244 | |||

| 20.1.1 | Lubambe Copper Mine | 245 | |||

| 20.1.2 | Mingomba Project | 246 | |||

| 20.2 | Chingola area | 246 | |||

| 20.2.1 | Mimbula Copper Project | 246 | |||

| 20.3 | Kitwe area | 246 | |||

| 20.3.1 | Mopani Copper Mines – Nkana Complex | 246 | |||

| 20.4 | Qualified Person’s statement on adjacent properties | 246 | |||

| 21 | Other relevant data and information | 247 | |||

| 22 | Interpretation and conclusions | 248 | |||

| 22.1 | Mineral Resource data | 248 | |||

| 22.2 | Mineral Reserves | 248 | |||

| 22.3 | Mining and infrastructure | 249 | |||

| 22.4 | Processing and recovery methods | 249 | |||

| 22.5 | Project economics | 249 | |||

| 22.6 | Effective date and subsequent events | 249 | |||

| 23 | Recommendations | 250 | |||

| 23.1 | Mineral Resource and geological recommendations | 250 | |||

| 23.1.1 | Resource infill and extension drilling | 250 | |||

| 23.1.2 | QAQC and data management | 250 | |||

| 23.2 | Mining recommendations | 251 | |||

| 23.2.1 | Konkola Mine | 251 | |||

| 23.2.2 | TD03 AND TD04 tailings reclamation | 251 | |||

| 23.3 | Processing and metallurgical recommendations | 251 | |||

| 23.3.1 | Konkola Concentrator | 251 | |||

| 23.3.2 | Nchanga TLP | 251 | |||

| 23.4 | Infrastructure recommendations | 251 | |||

| 23.5 | Economic and commercial recommendations | 251 | |||

| 23.6 | Summary of recommended work program | 252 | |||

| 24 | References | 253 | |||

| 24.1 | List of references | 253 | |||

| 24.2 | Units of measurement and abbreviations | 254 | |||

| 24.2.1 | Units of measurement | 254 | |||

| 24.2.2 | Abbreviations | 254 | |||

| 25 | Reliance on information provided by the Registrant | 256 | |||

| 25.1 | Legal matters | 256 | |||

| 25.2 | Environmental Management and Community Engagement | 256 | |||

| 25.2.1 | Environmental and community matters | 256 | |||

| 25.2.2 | Tailings storage facility facilities | 256 | |||

| 25.3 | Economic assumptions | 257 | |||

| 25.3.1 | Macroeconomic assumptions | 257 | |||

| 25.3.2 | Market information | 257 | |||

| 25.4 | Community accommodations | 257 | |||

| 25.5 | Governmental Factors | 257 | |||

amcconsultants.com | ix |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

Tables

| Table 1.1 | KCM mineral rights and licenses | 16 |

| Table 1.2 | KCM Mineral Reserve estimate summary – 1 April 2026 | 18 |

| Table 1.3 | KCM Mineral Resource estimate summary (Exclusive of Mineral Reserves) – 1 April 2026 | 20 |

| Table 1.4 | Capital cost summary – Mineral Reserve case | 23 |

| Table 1.5 | Operating cost summary – Mineral Reserve case | 23 |

| Table 1.6 | Summarised economic results | 24 |

| Table 1.7 | Sensitivity analysis results | 25 |

| Table 2.1 | Defined terms and abbreviations | 28 |

| Table 3.1 | KCM Integrated Operations — facility coordinates (WGS84 datum) | 32 |

| Table 3.2 | KCM mineral rights and tenure details | 34 |

| Table 4.1 | Inter-site distances and access routes | 39 |

| Table 5.1 | Principal capital investments by Vedanta Resources (2004–2019) | 44 |

| Table 5.2 | Cumulative copper production by operation | 46 |

| Table 5.3 | Key development milestones | 47 |

| Table 6.1 | KCM deposit mineralisation extent | 57 |

| Table 6.2 | Summary of geological characteristics of KCM operations | 57 |

| Table 6.3 | Summary of TCu variogram ranges by estimation domain — Konkola | 58 |

| Table 7.1 | Local geology and hydrogeological units — Konkola | 64 |

| Table 7.2 | Summary of hydrogeological investigations — Konkola | 66 |

| Table 7.3 | Principal aquifer units — Konkola | 67 |

| Table 7.4 | Hydrogeological data gaps and recommended actions | 68 |

| Table 7.5 | Geotechnical data sources — Konkola | 69 |

| Table 7.6 | Elastic rock properties | 69 |

| Table 7.7 | Material geotechnical assumptions - Konkola | 70 |

| Table 7.8 | Rock mass conditions by geotechnical domain - Konkola | 71 |

| Table 7.9 | Geotechnical data gaps and recommended actions | 73 |

| Table 8.1 | List of corrected outcomes for 16 GBM911-16 CRMs | 77 |

| Table 8.2 | Summary of QAQC performance by deposit | 82 |

| Table 8.3 | QP assessment of QAQC findings by deposit | 82 |

| Table 8.4 | QAQC recommendations for DFS | 84 |

| Table 9.1 | QP assessment of data verification limitations | 88 |

| Table 10.1 | Key processing factors — Konkola Concentrator | 91 |

| Table 10.2 | Deleterious elements and gangue — Konkola concentrate | 92 |

| Table 10.3 | Historical, restart, and planed Nchanga TLP recoveries | 94 |

| Table 10.4 | Key processing factors — Nchanga TLP | 95 |

| Table 10.5 | Deleterious factors — Nchanga TLP | 96 |

| Table 11.1 | Key assumptions, parameters, and methods — Mineral Resource estimation | 100 |

amcconsultants.com | x |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| Table 11.2 | Cut-off grade input assumptions by asset | 102 |

| Table 11.3 | Uncertainty factor assessment by Mineral Resource classification — Konkola Mine | 103 |

| Table 11.4 | Mineral Resource Konkola Mine (Exclusive of Mineral Reserves) – 1 April 2026 | 107 |

| Table 11.5 | Summary statistics total copper tailings dam samples | 108 |

| Table 11.6 | Summary statistics acid soluble copper tailings dam samples | 109 |

| Table 11.7 | Mineral Resource TD03 and TD04 (exclusive of Reserves) – 1 April 2026 | 110 |

| Table 11.8 | Mineral Resource TD03 and TD04 (inclusive of Reserves) – 1 April 2026 | 111 |

| Table 12.1 | Konkola Mineral Reserve estimate – 1 April 2026 | 113 |

| Table 12.2 | Mining dilution and recovery factors | 115 |

| Table 12.3 | Konkola NSR elements (average across mining blocks) | 116 |

| Table 12.4 | Royalty charge relation to copper price | 117 |

| Table 12.5 | NSR cut-off by mining block | 117 |

| Table 13.1 | Mining method selection assessment | 119 |

| Table 13.2 | Mining method assignment by zone | 120 |

| Table 13.3 | KCM Shaft 3 summary of rock mass properties | 123 |

| Table 13.4 | KCM Shaft 4 summary of rock mass properties | 125 |

| Table 13.5 | Summary of water capture extrapolated over time | 136 |

| Table 13.6 | Indicative future mine inflow rates for the next 7-year mine plan | 139 |

| Table 13.7 | Mining methods currently employed by mining area at Konkola Mine | 142 |

| Table 13.8 | Typical stope dimensions | 144 |

| Table 13.9 | Mining dilution and recovery factors | 145 |

| Table 13.10 | Key development designs | 146 |

| Table 13.11 | Konkola paste fill design strengths (FoS=1.5) and paste fill recipes at 28 days curing | 150 |

| Table 13.12 | Paste fill capital cost estimation | 150 |

| Table 13.13 | Planned velocity ranges for different mine airways | 151 |

| Table 13.14 | Maximum temperature limits for acclimatised and non-acclimatised workers | 152 |

| Table 13.15 | Ventilation design criteria for diesel-powered equipment | 153 |

| Table 13.16 | Machine types, counts, and utilisation factors | 153 |

| Table 13.17 | Summary of primary ventilation airflows | 153 |

| Table 13.18 | Mining equipment fleet — steady state | 155 |

| Table 13.19 | Estimated mining workforce summary | 155 |

| Table 13.20 | Available inventory from TD03 and TD04 for the Nchanga TLP from 1 April 2026 | 160 |

| Table 14.1 | Konkola Concentrator major equipment | 168 |

| Table 14.2 | Capacity criteria | 168 |

| Table 14.3 | Comminution criteria | 169 |

| Table 14.4 | Flotation criteria | 169 |

| Table 14.5 | Konkola Concentrator key assumptions | 170 |

| Table 14.6 | Nchanga Concentrator nominal capacities | 172 |

| Table 14.7 | Nchanga TLP highest annual performance | 175 |

| Table 14.8 | Copper production estimate | 175 |

| Table 14.9 | Nchanga TLP major unit processes | 177 |

| Table 14.10 | Nchanga Smelter – basic design production parameters | 179 |

| Table 14.11 | Nchanga Smelter – historical production | 180 |

| Table 14.12 | Nchanga Smelter production – October 2024 | 182 |

amcconsultants.com | xi |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| Table 14.13 | Smelter rebuild CAPEX – by section | 183 |

| Table 14.14 | Example monthly concentrate blend plan – June 2025 | 184 |

| Table 14.15 | Concentrate blending plan – FY25/26 business plan | 187 |

| Table 14.16 | Nkana Refinery production – 2024-2025 | 191 |

| Table 15.1 | Summary of infrastructure by operating site | 194 |

| Table 15.2 | Operational TSF conditions, TD05 (Muntimpa) and Lubengele | 202 |

| Table 16.1 | Five-year copper forward prices (real US$ 2025) | 211 |

| Table 16.2 | Five-year copper trailing prices | 211 |

| Table 16.3 | Copper payability terms for Konkola and Nchanga Copper Concentrate | 211 |

| Table 16.4 | Major development contracts | 212 |

| Table 16.5 | Example of long-term contract components | 214 |

| Table 16.6 | Royalty charge relation to copper price | 216 |

| Table 18.1 | Cost estimate accuracy and contingency disclosure | 219 |

| Table 18.2 | Rates assumed for operating lateral development | 220 |

| Table 18.3 | Stoping production cost | 221 |

| Table 18.4 | Konkola applicable power tariff assumptions | 221 |

| Table 18.5 | Konkola power estimate | 222 |

| Table 18.6 | Konkola operating costs – Mineral Reserve case | 225 |

| Table 18.7 | Capital cost summary | 227 |

| Table 18.8 | Growth capital summary for the Mineral Reserve | 227 |

| Table 18.9 | Development, sustaining and growth capital by complex (5 year and LOM) for Mineral Reserve | 228 |

| Table 18.10 | Summary by category | 228 |

| Table 18.11 | Smelter and refinery capital estimate schedule (first five years) | 231 |

| Table 19.1 | Byproducts: Type, quantity, and price assumption | 232 |

| Table 19.2 | Consensus pricing forecast – Mineral Reserve case | 235 |

| Table 19.3 | Economic analysis summary – Mineral Reserve case | 239 |

| Table 19.4 | Mineral Reserve production and cashflow schedule | 242 |

| Table 19.5 | Sensitivity analysis table – Mineral Reserve | 243 |

| Table 20.1 | Summary of adjacent properties | 244 |

| Table 23.1 | Recommended work program | 252 |

| Table 24.1 | TRS data and information sources | 253 |

Figures

| Figure 1.1 | Sensitivity analysis graph | 25 |

| Figure 3.1 | Map of Zambia showing the Copperbelt Region | 30 |

| Figure 3.2 | Property location map – KCM Integrated Operations | 31 |

| Figure 4.1 | Inter site logistics map | 40 |

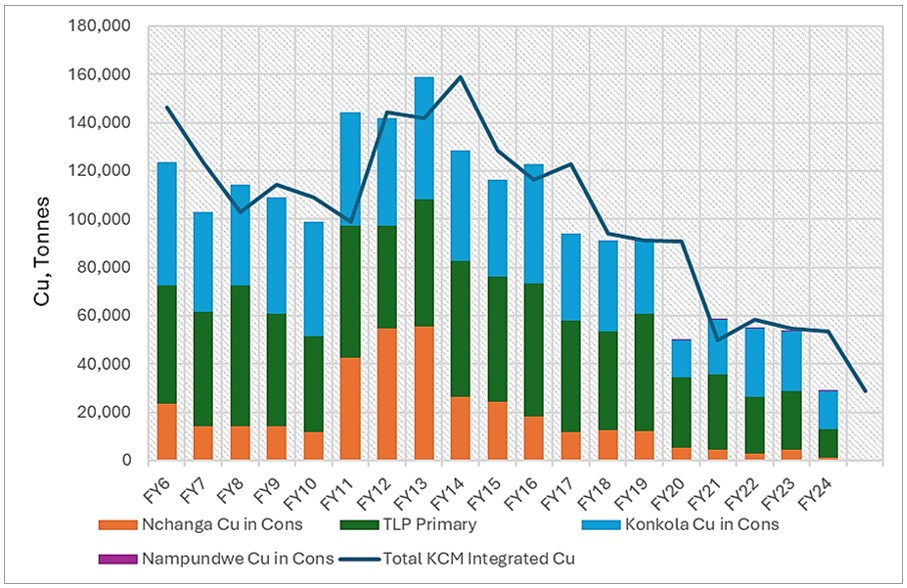

| Figure 5.1 | KCM historical production FY06-FY24 | 46 |

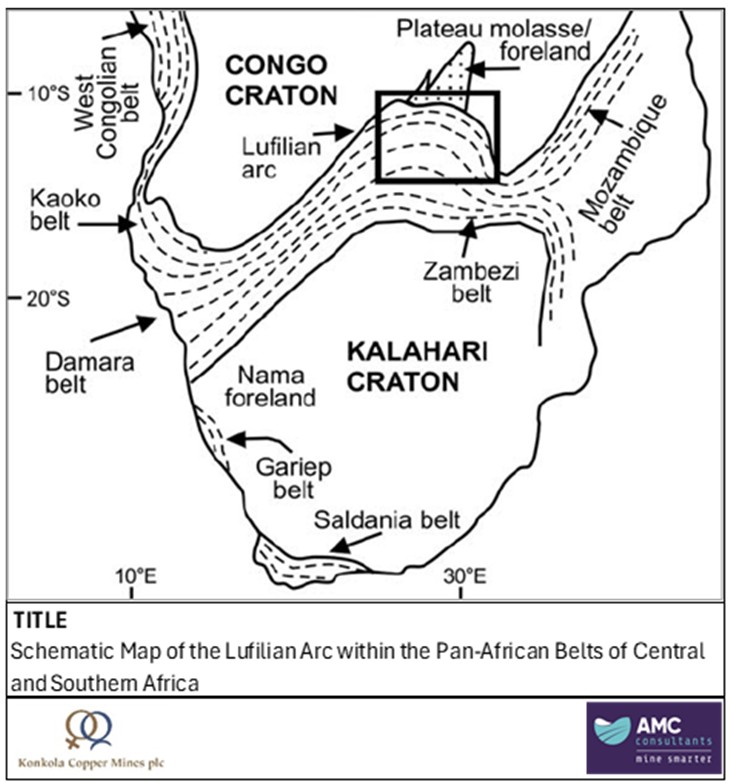

| Figure 6.1 | Location of Lufilian Arc within Pan-African Belts of Central and Southern Africa | 48 |

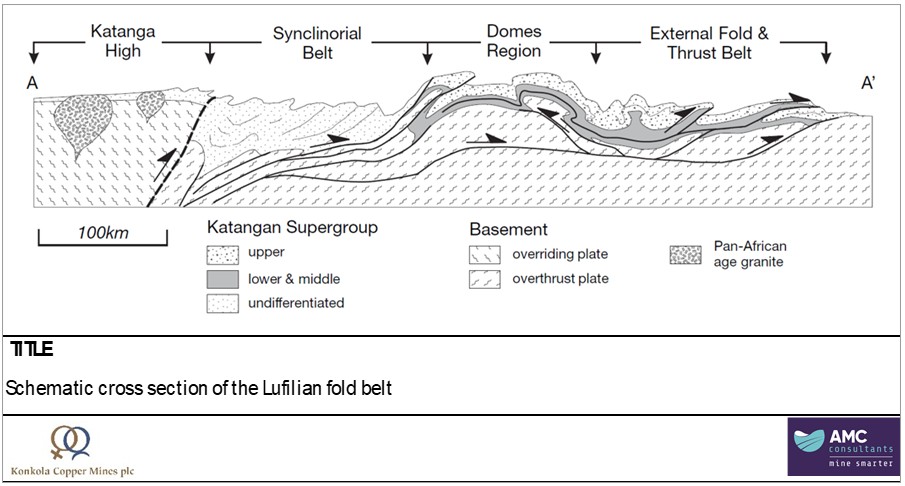

| Figure 6.2 | Schematic cross section of the Lufilian fold belt | 49 |

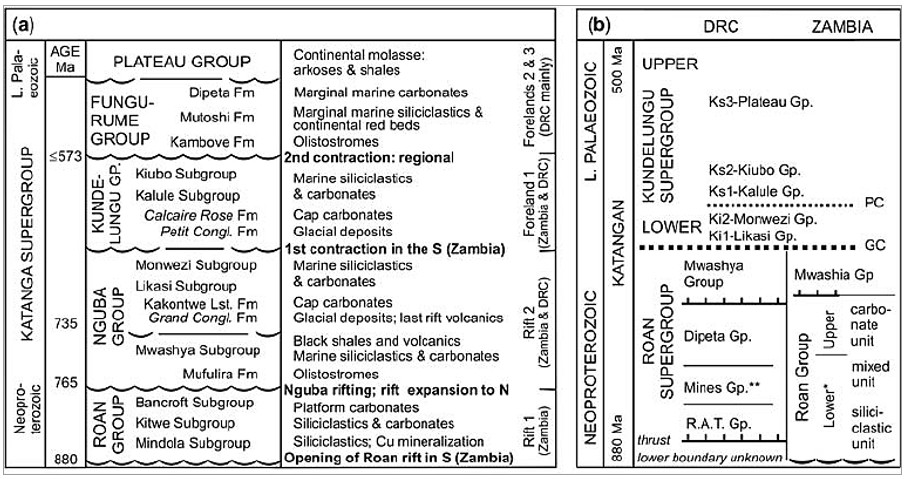

| Figure 6.3 | Simplified Katanga Supergroup stratigraphy | 51 |

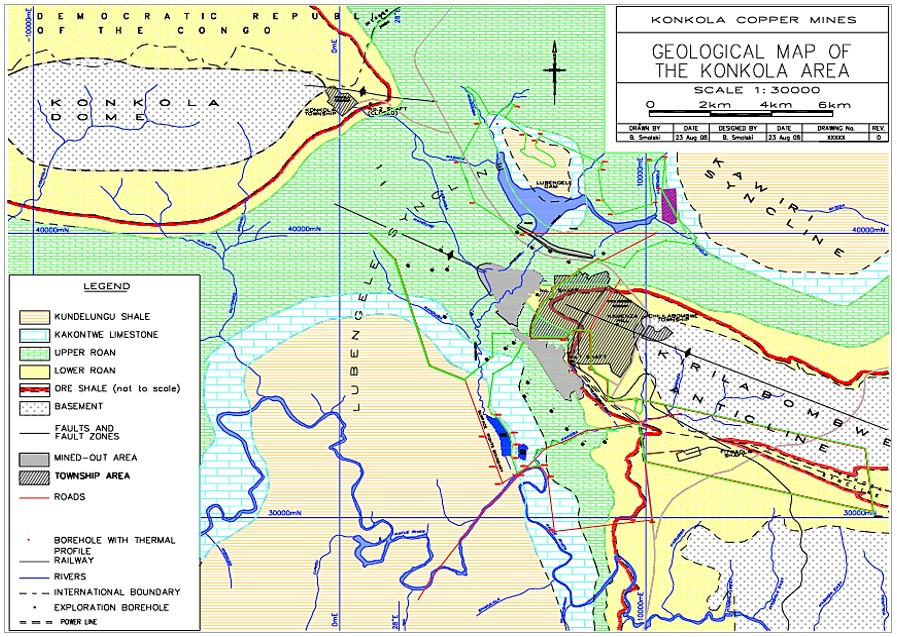

| Figure 6.4 | Geological map of the greater Konkola area | 52 |

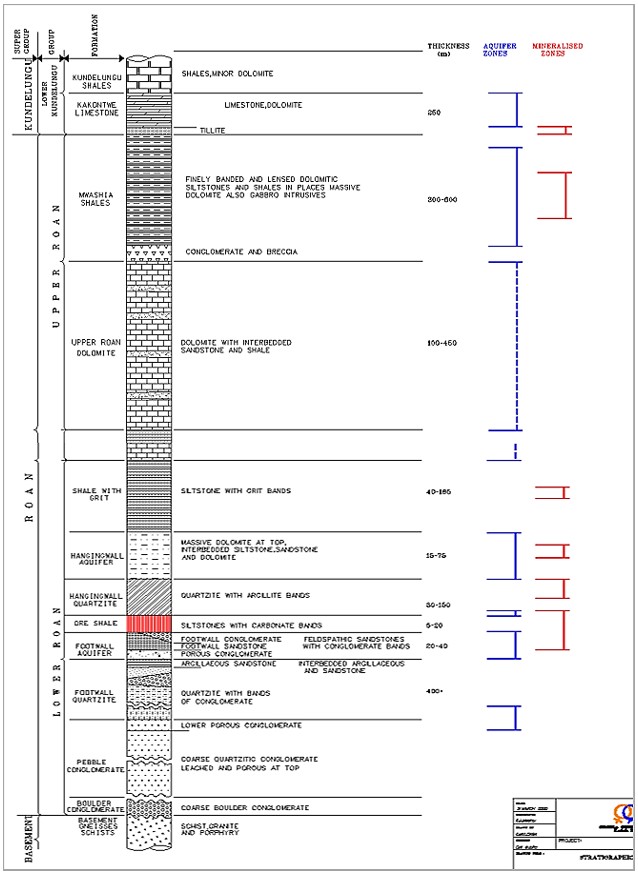

| Figure 6.5 | Stratigraphic column of the Konkola geology | 53 |

amcconsultants.com | xii |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

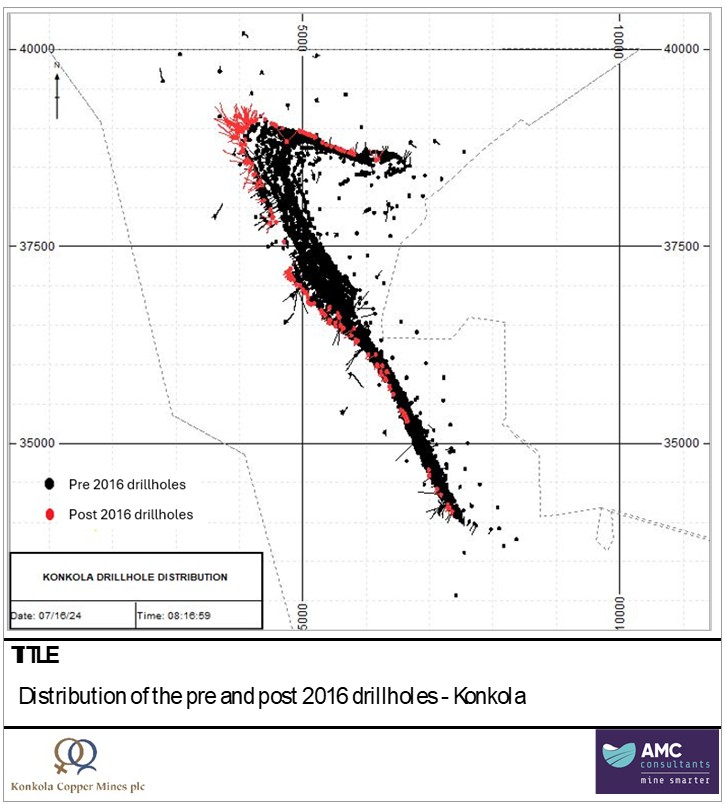

| Figure 7.1 | Drillhole location plan - Konkola | 63 |

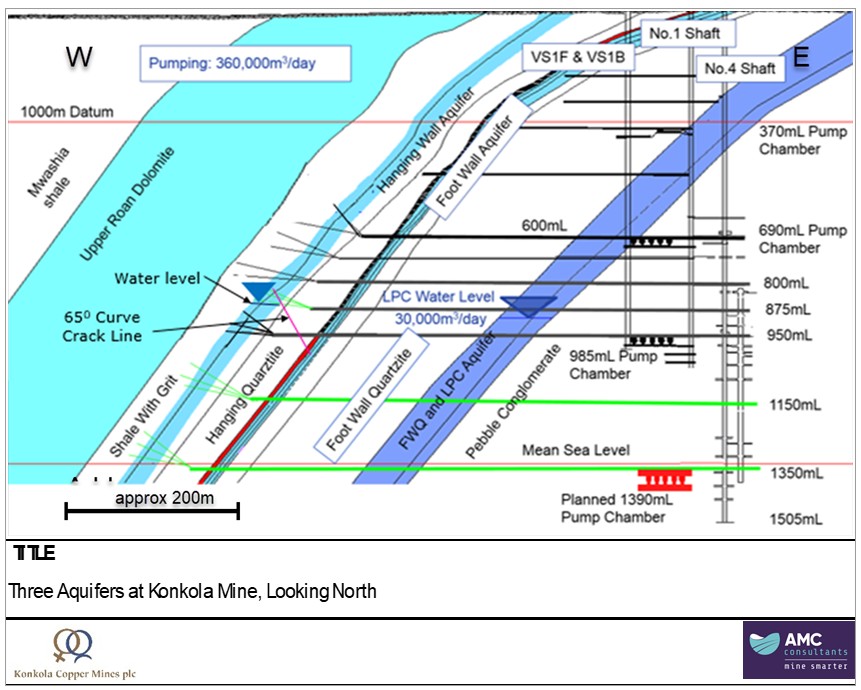

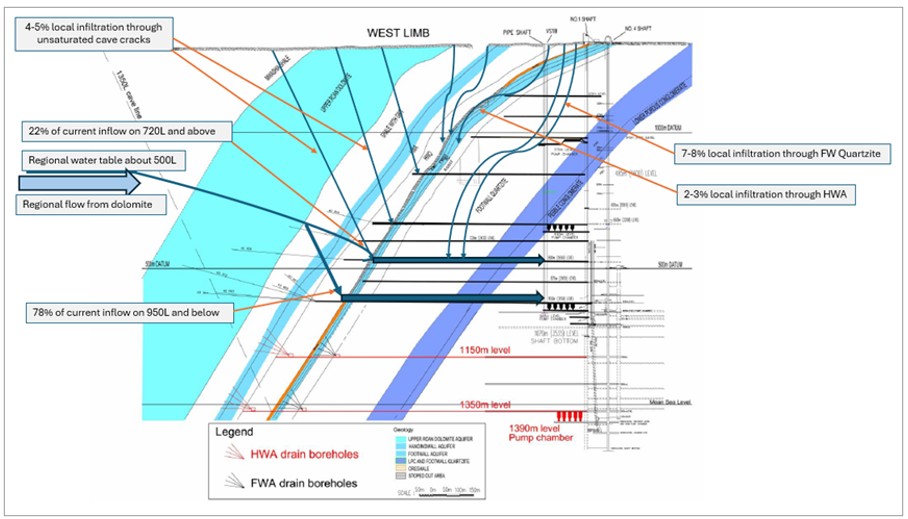

| Figure 7.2 | Location of three main aquifers in the Konkola Mine, section looking north | 65 |

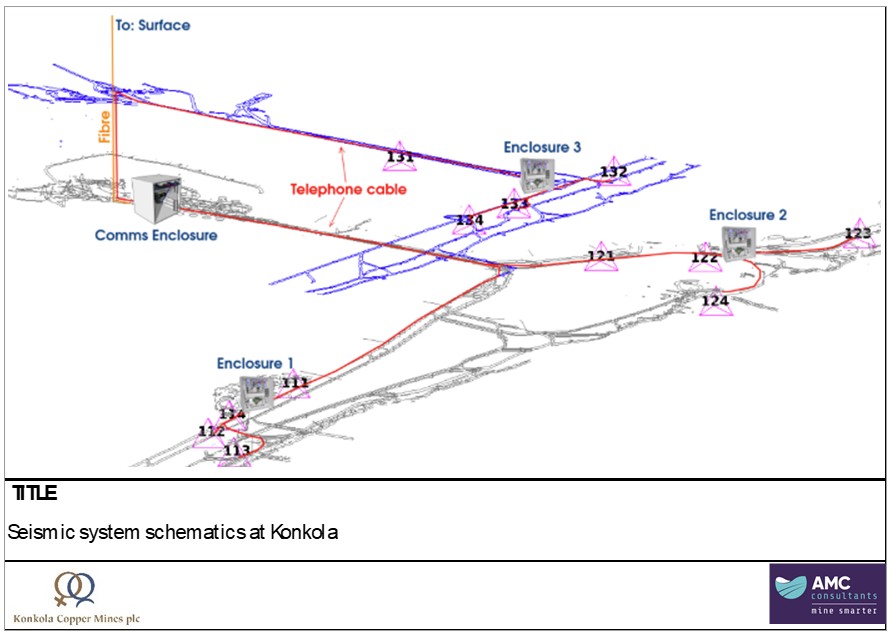

| Figure 7.3 | Seismic system schematics at Konkola | 72 |

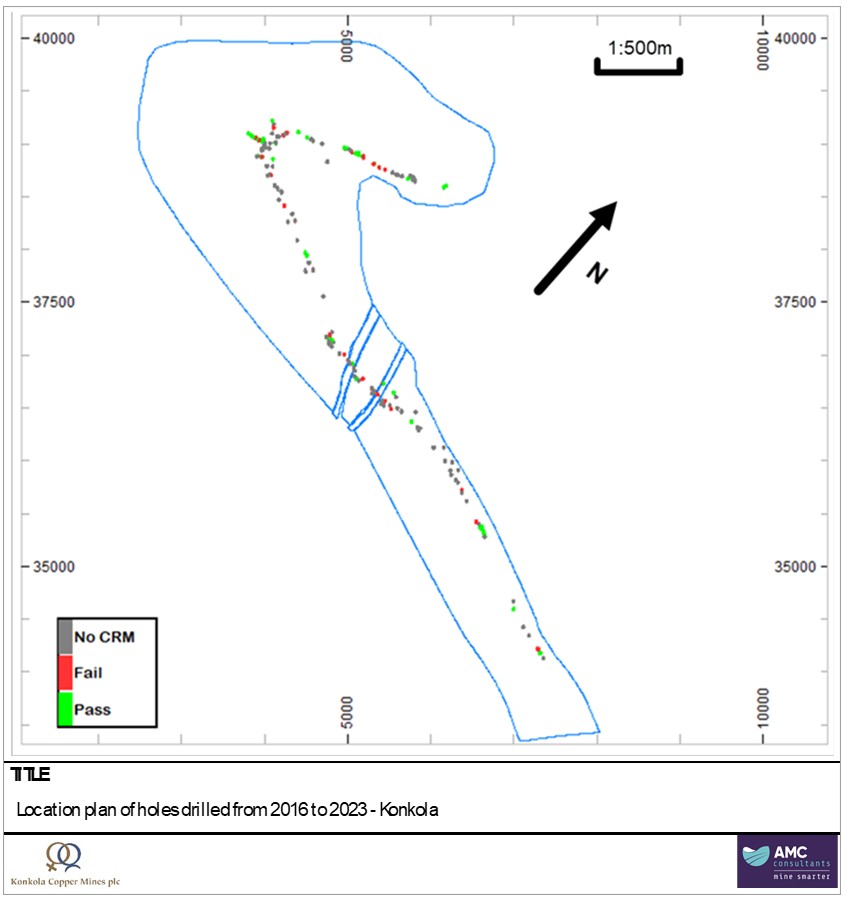

| Figure 8.1 | Location plan of holes drilled from 2016 to 2023 - Konkola | 78 |

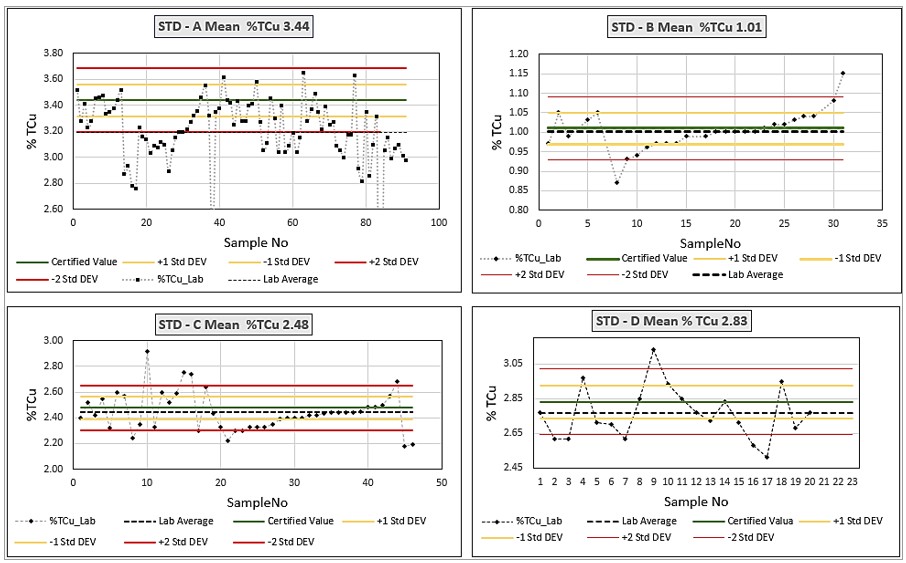

| Figure 8.2 | Shewhart plots for CRMs A, B, C, and D - Konkola | 79 |

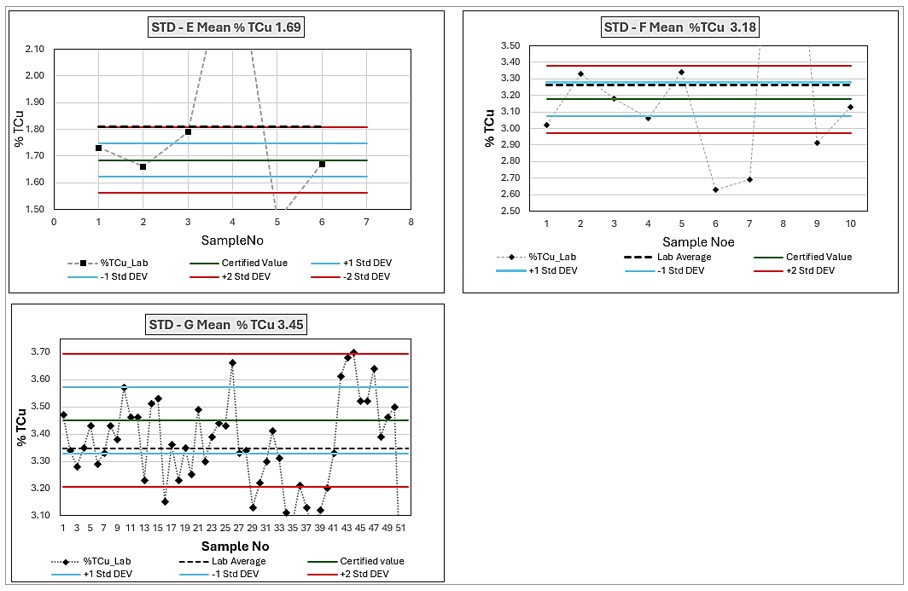

| Figure 8.3 | Shewhart plots for CRMs E, F, and G - Konkola | 79 |

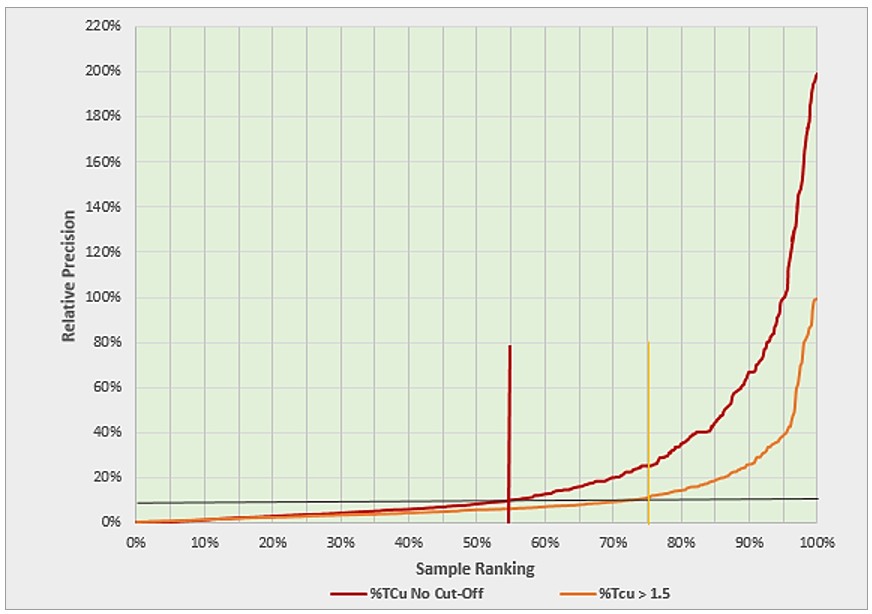

| Figure 8.4 | RPD plot TCu repeat samples no cut-off and at 1.5% TCu- Konkola - post 2016 data | 80 |

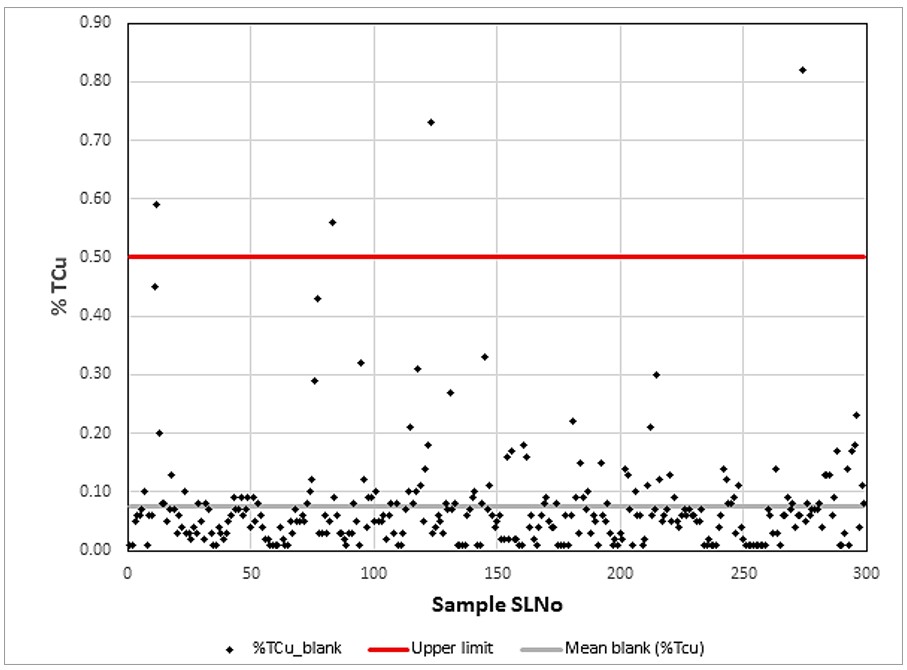

| Figure 8.5 | Blank samples plot showing 0.5% TCu upper limit | 81 |

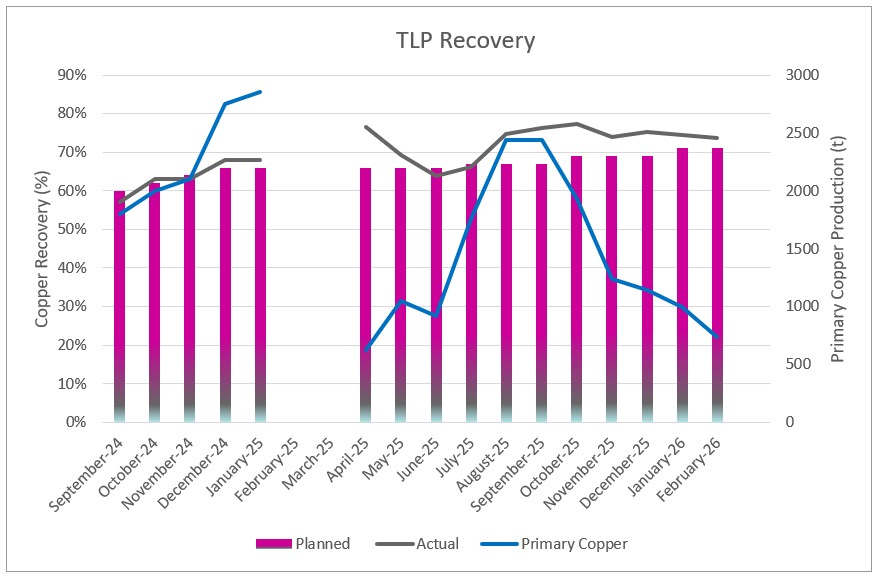

| Figure 10.1 | Nchanga TLP copper production and recoveries - Restart and FY25-26 plan | 93 |

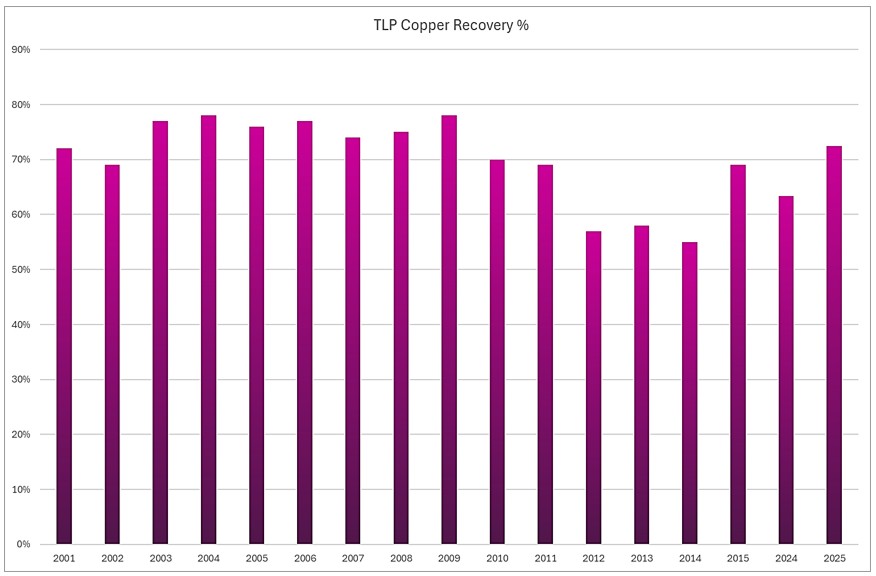

| Figure 10.2 | Historical Nchanga TLP copper recoveries | 94 |

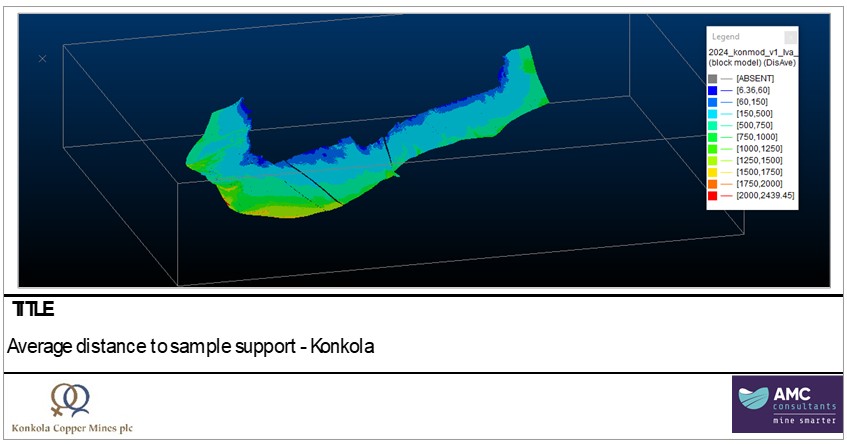

| Figure 11.1 | Average distance to sample support - Konkola | 101 |

| Figure 13.1 | Final mine outline map - plan view showing mining zone boundaries & key infrastructure | 120 |

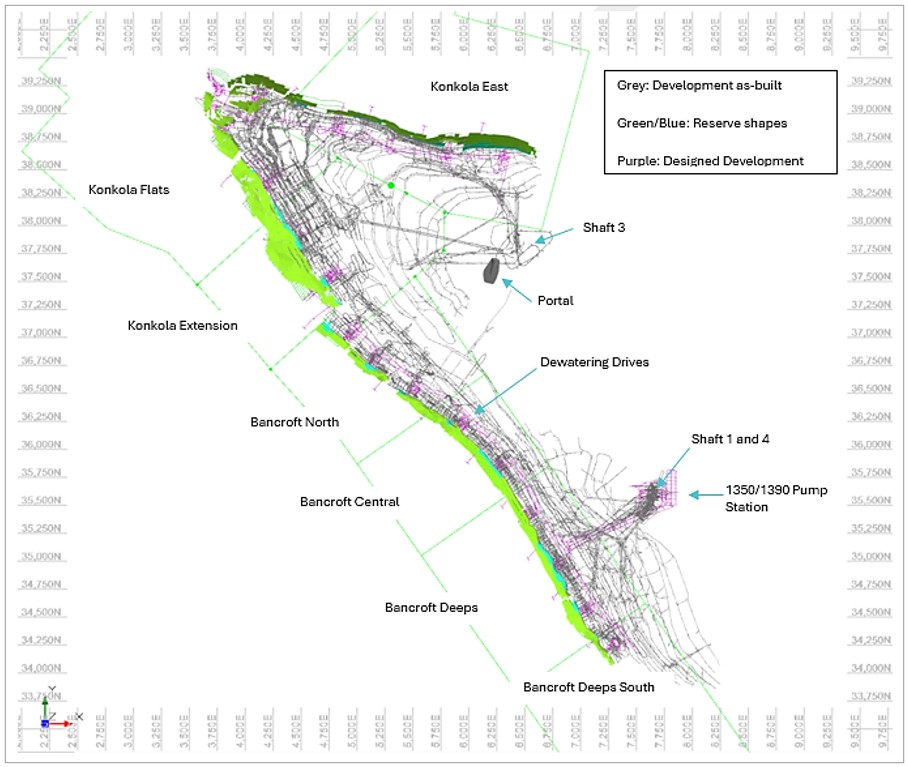

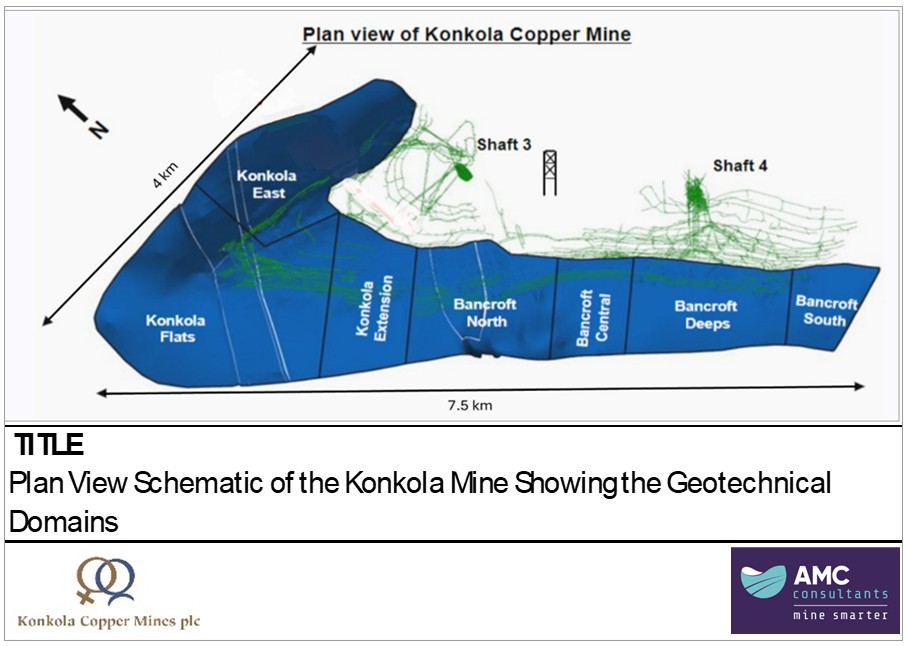

| Figure 13.2 | Plan view map of the Konkola Mine showing the geotechnical domains | 122 |

| Figure 13.3 | Cross section showing the interconnected nature of the Chingola dolomite (light blue) between KCM (right) and Lubambe (left) | 133 |

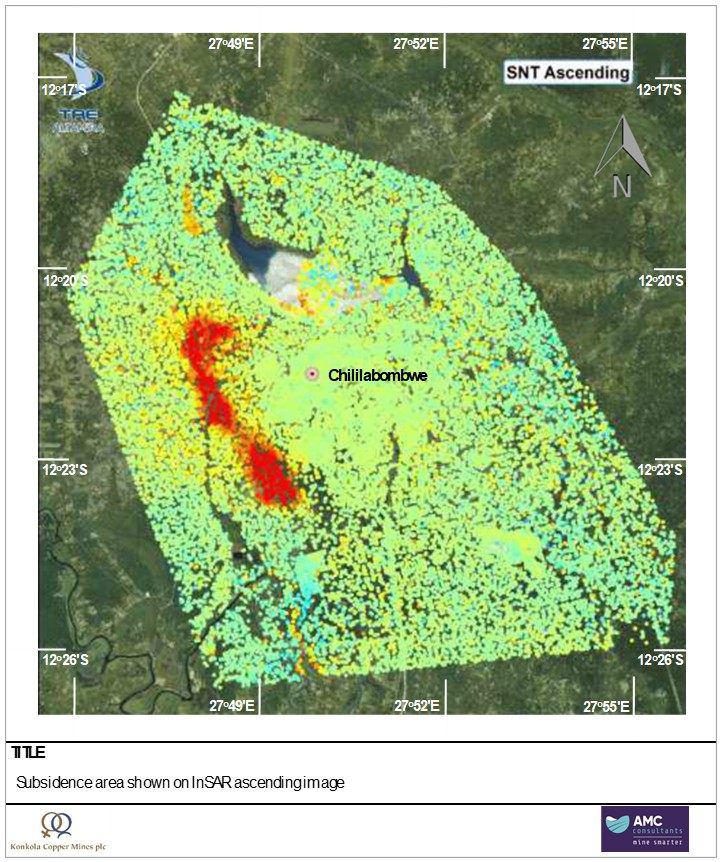

| Figure 13.4 | Subsidence area shown on InSAR ascending image | 134 |

| Figure 13.5 | Conceptual water balance | 136 |

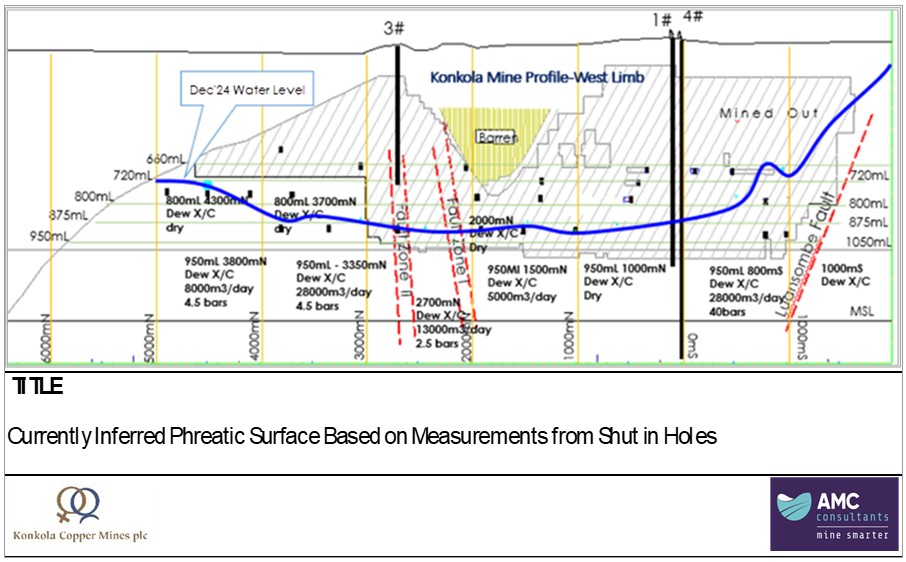

| Figure 13.6 | Currently inferred phreatic surface based on measurements from shut in holes | 137 |

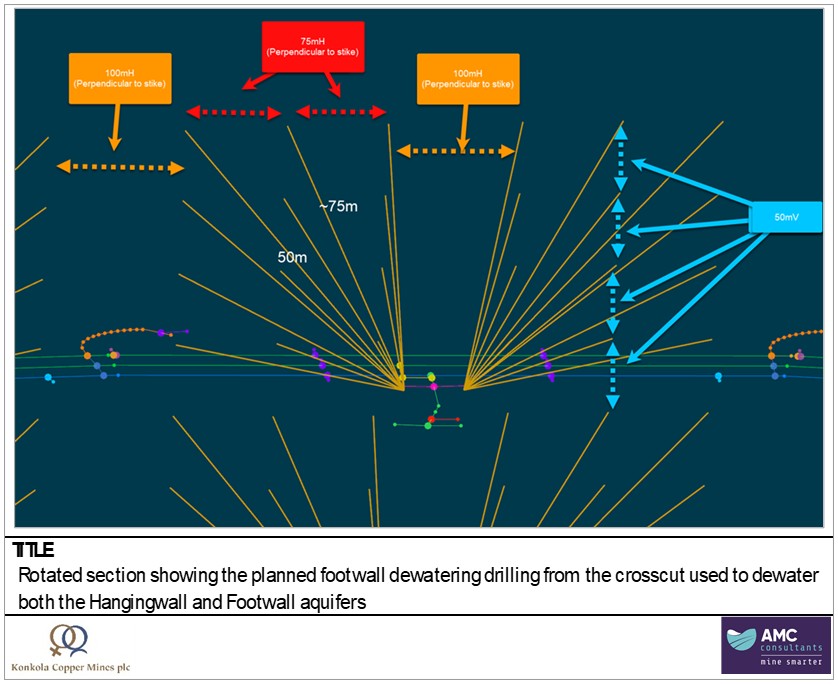

| Figure 13.7 | Rotated section showing the planned footwall dewatering drilling | 138 |

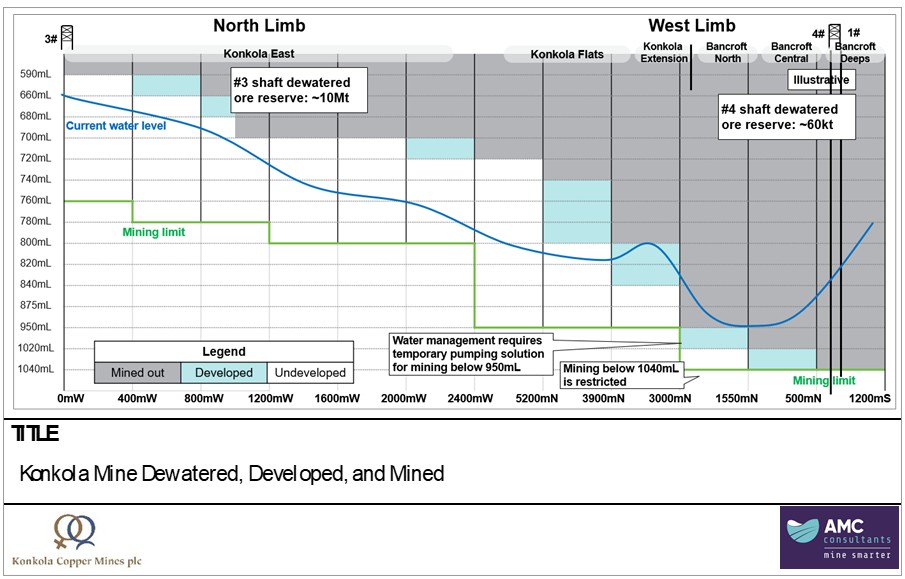

| Figure 13.8 | Konkola Mine dewatered, developed, and mined | 140 |

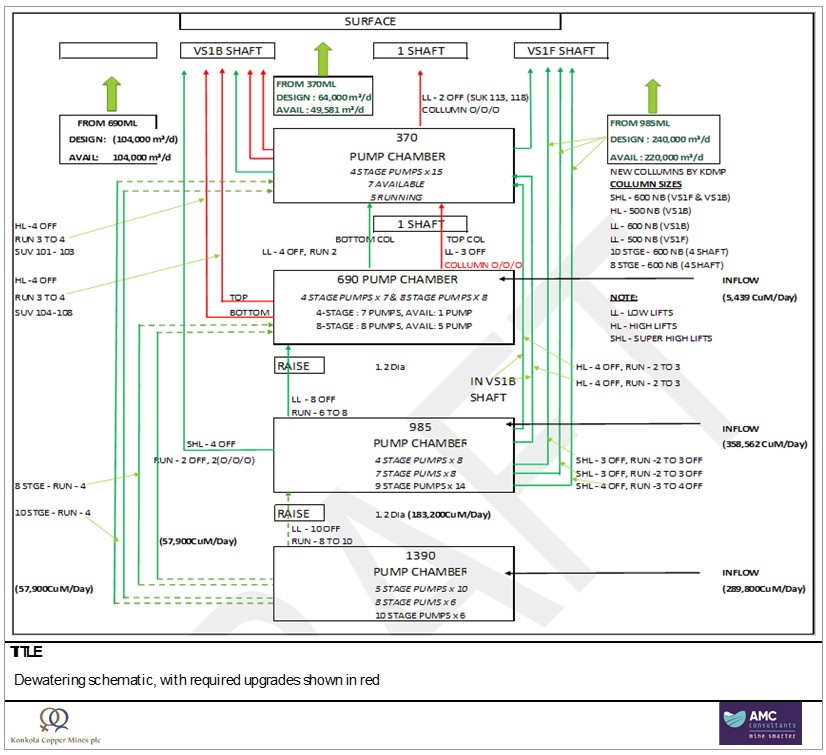

| Figure 13.9 | Dewatering schematic, with required upgrades shown in red | 141 |

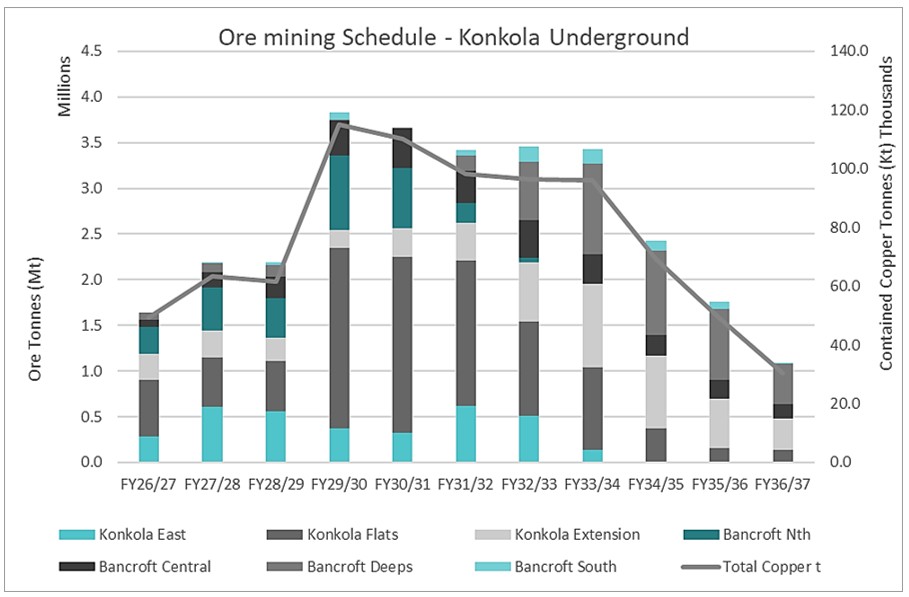

| Figure 13.10 | Konkola Mine production schedule by area | 143 |

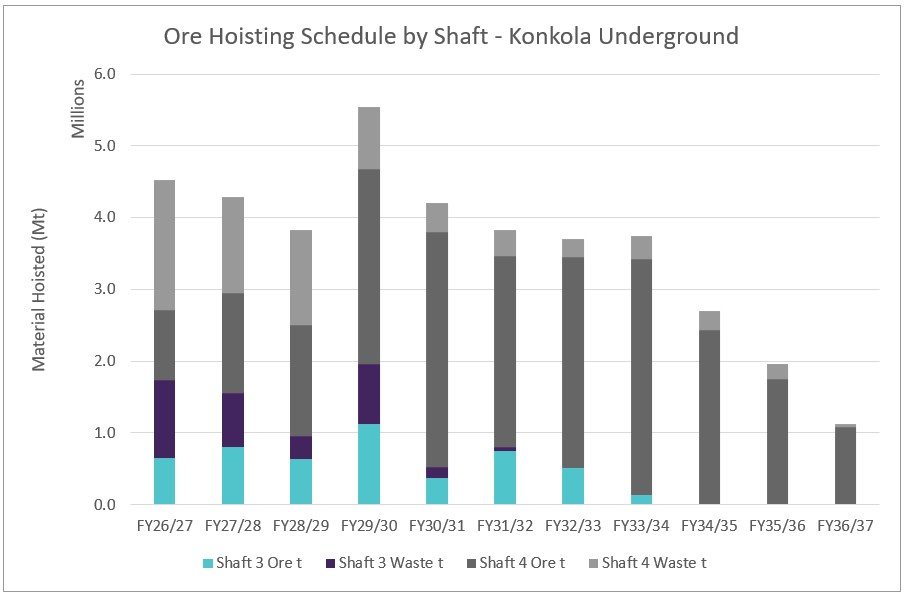

| Figure 13.11 | Konkola Mine hoisting schedule by shaft | 144 |

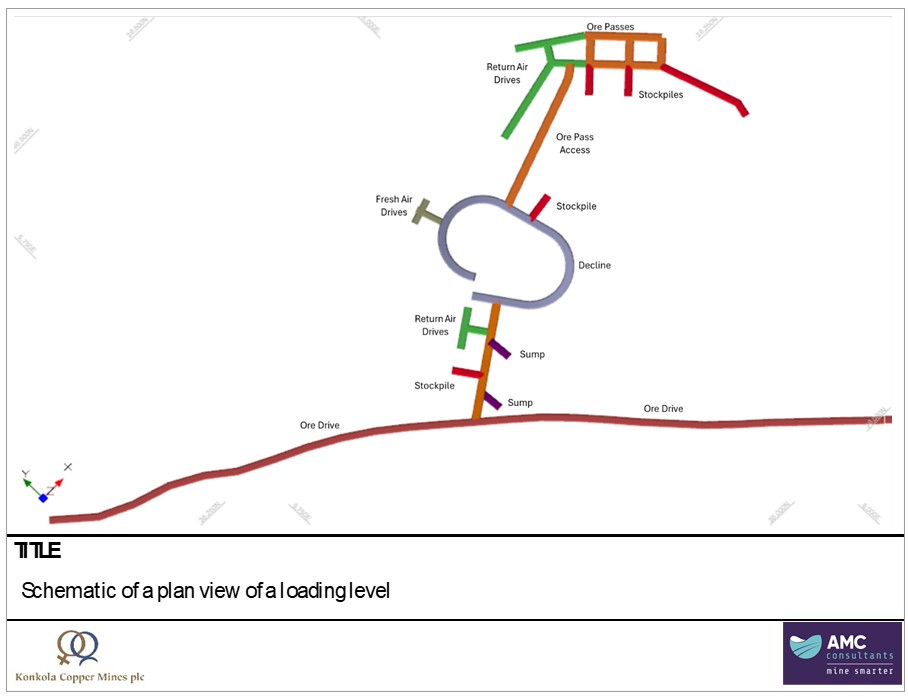

| Figure 13.12 | Plan view of a loading level | 146 |

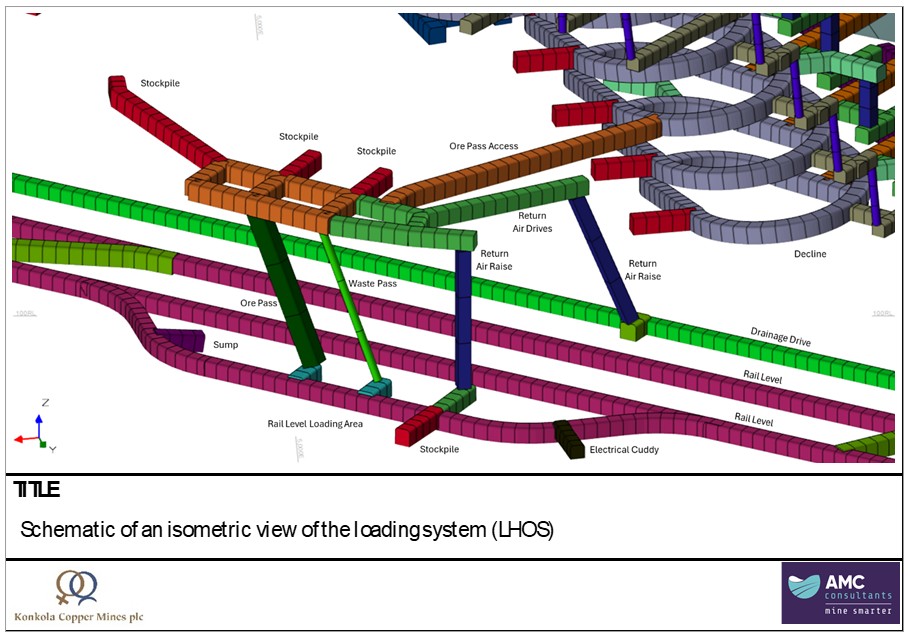

| Figure 13.13 | Isometric view of the loading system (LHOS) | 147 |

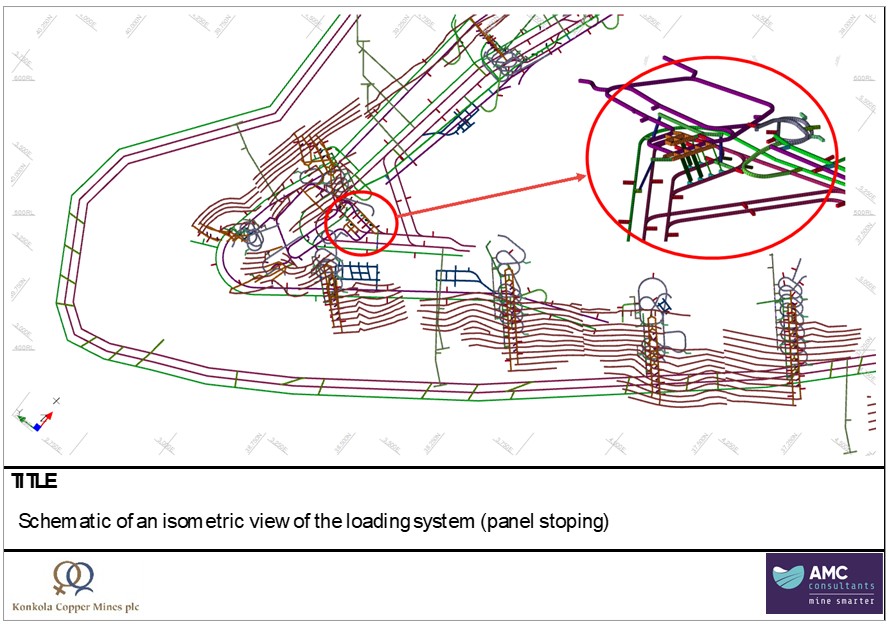

| Figure 13.14 | Isometric view of the loading system (panel stoping) | 148 |

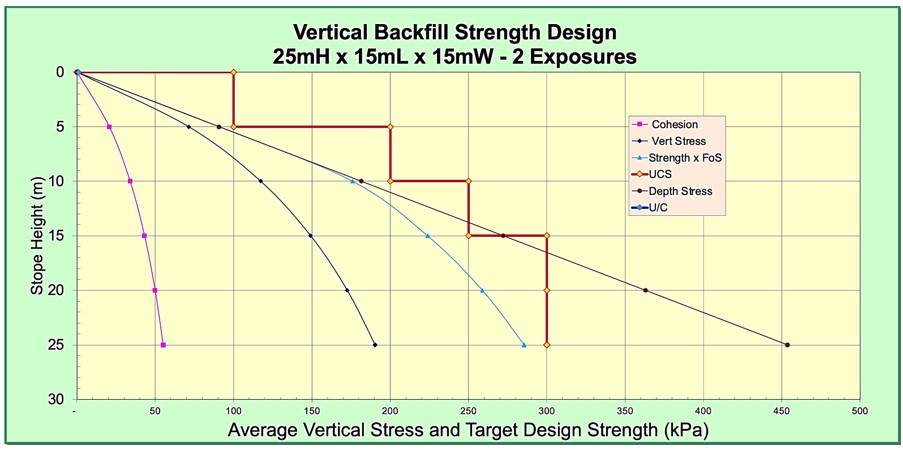

| Figure 13.15 | Target paste design strength – 2 Exposures | 149 |

| Figure 13.16 | Target paste design strength – 1 Exposure | 149 |

| Figure 13.17 | Paste fill arched shotcrete barricades | 150 |

| Figure 13.18 | Visual presentation of air flow through the mine | 154 |

| Figure 13.19 | Ventilation compared to production | 154 |

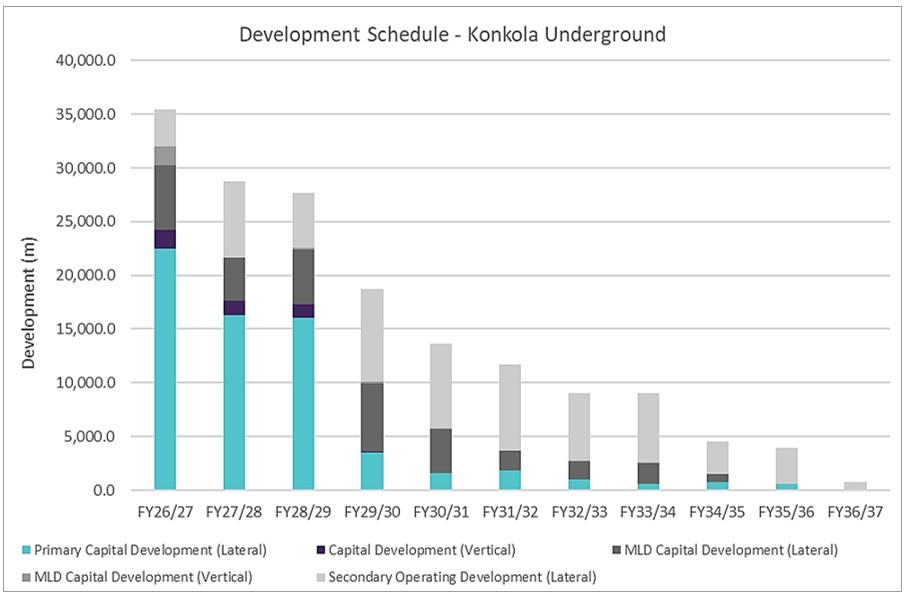

| Figure 13.20 | Konkola Mine development schedule | 156 |

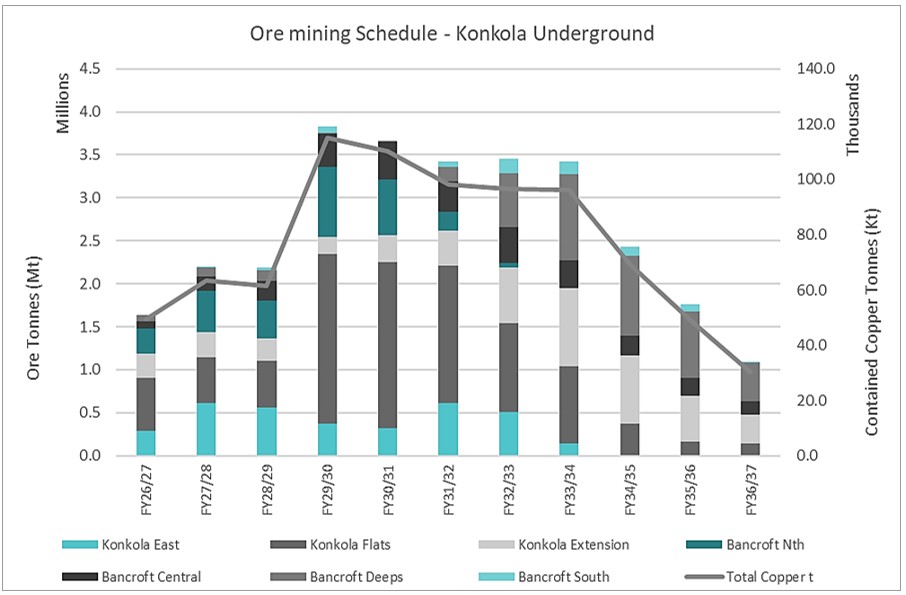

| Figure 13.21 | Konkola Mine production schedule by area | 157 |

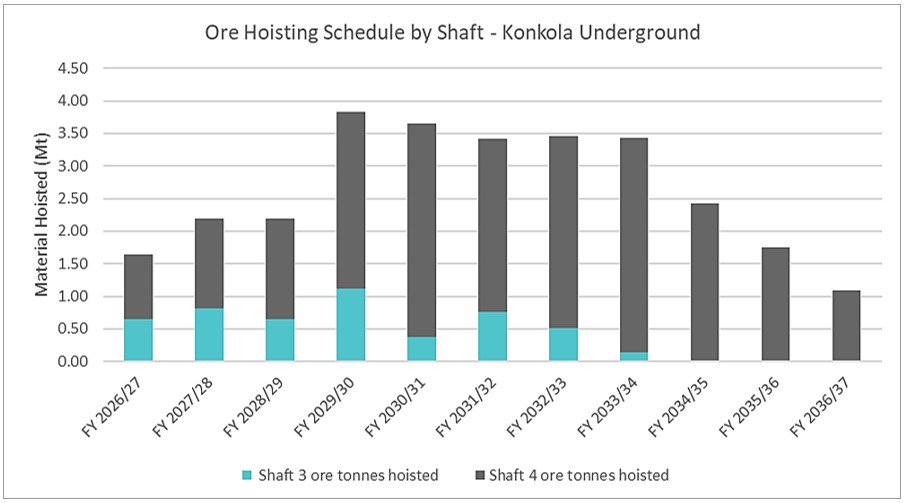

| Figure 13.22 | Ore hoisted by shaft | 157 |

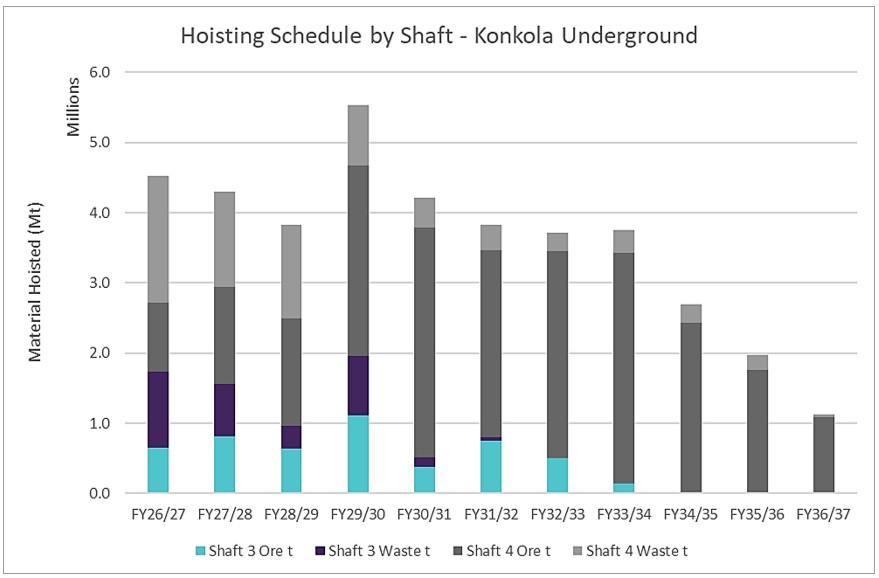

| Figure 13.23 | Total hoisting (ore and waste) by shaft | 158 |

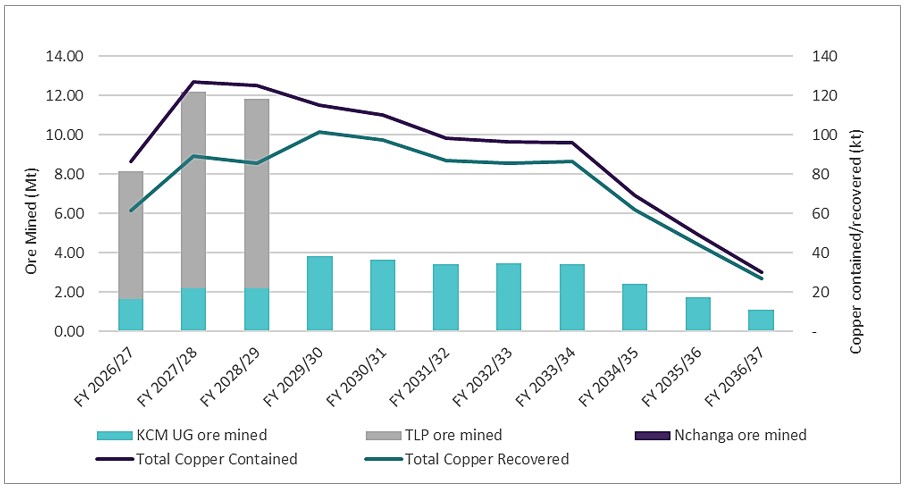

| Figure 13.24 | TD03 and TD04 mining schedule | 158 |

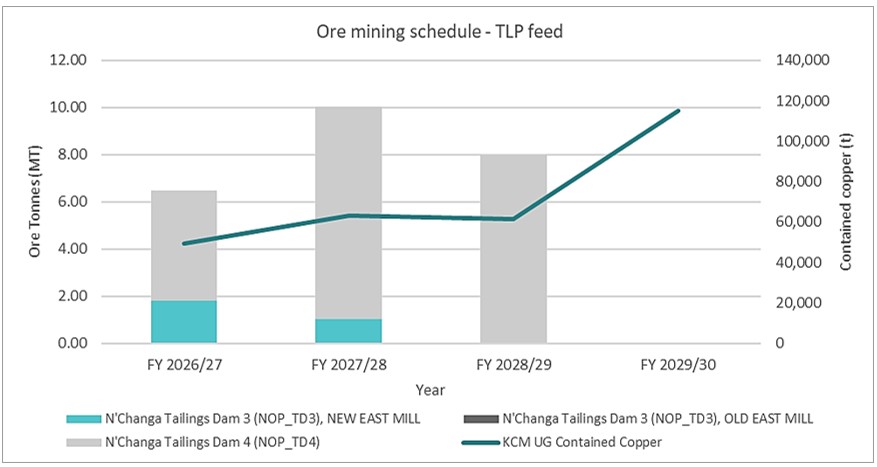

| Figure 13.25 | Total project ore mining schedule | 159 |

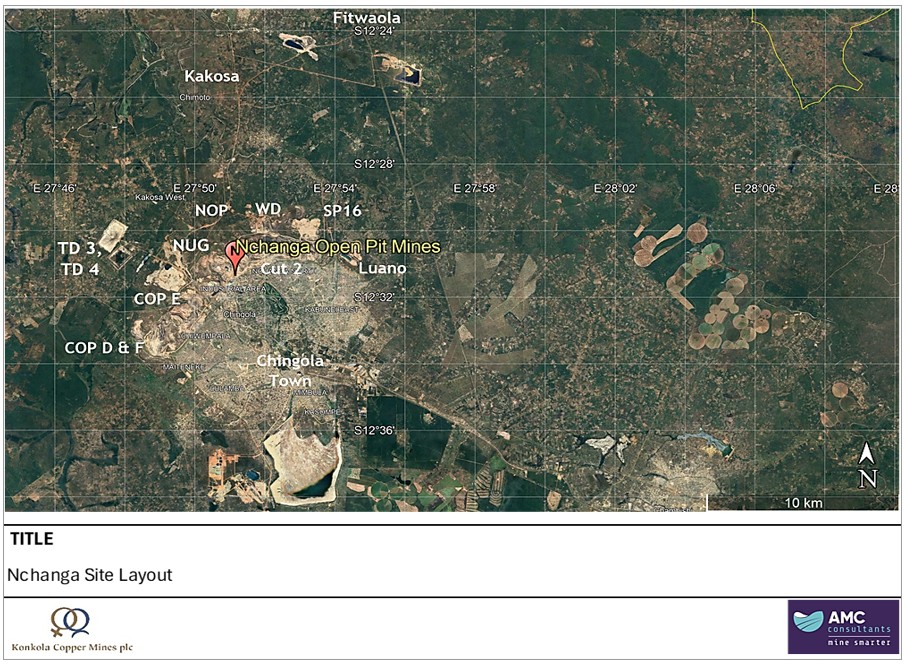

| Figure 13.26 | Nchanga site layout | 160 |

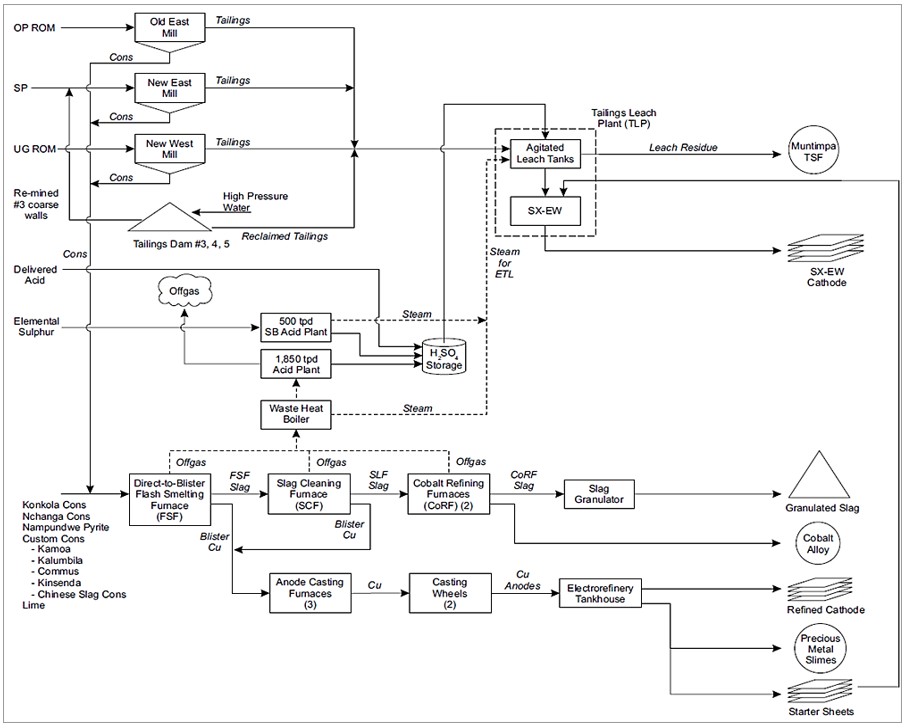

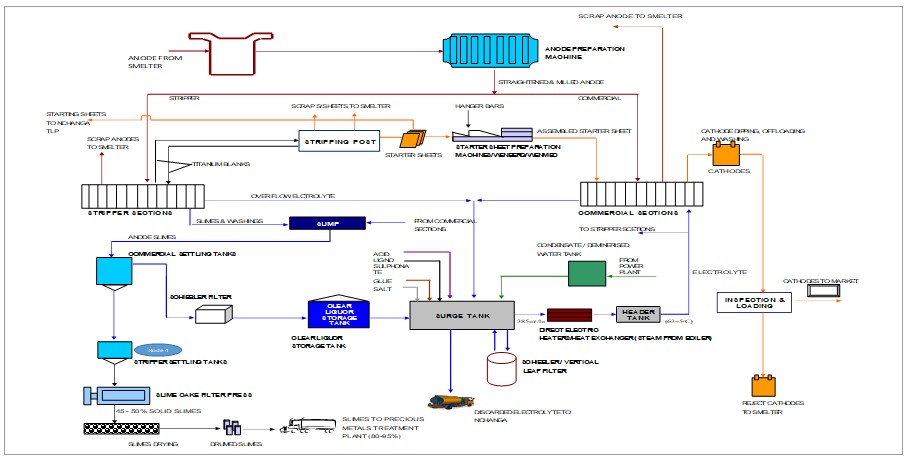

| Figure 14.1 | KCM total flowsheet | 162 |

| Figure 14.2 | Konkola Concentrator flowsheet | 163 |

| Figure 14.3 | Konkola historical ore treatment | 165 |

| Figure 14.4 | Konkola daily ore received since restart | 165 |

| Figure 14.5 | Konkola ore processed since restart | 166 |

amcconsultants.com | xiii |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| Figure 14.6 | Konkola recoveries since restart | 166 |

| Figure 14.7 | Konkola concentrate produced since restart | 166 |

| Figure 14.8 | Concentrate production and grade - Restart and FY25-25 plan | 167 |

| Figure 14.9 | Copper production and recoveries - Restart and FY25-26 plan | 167 |

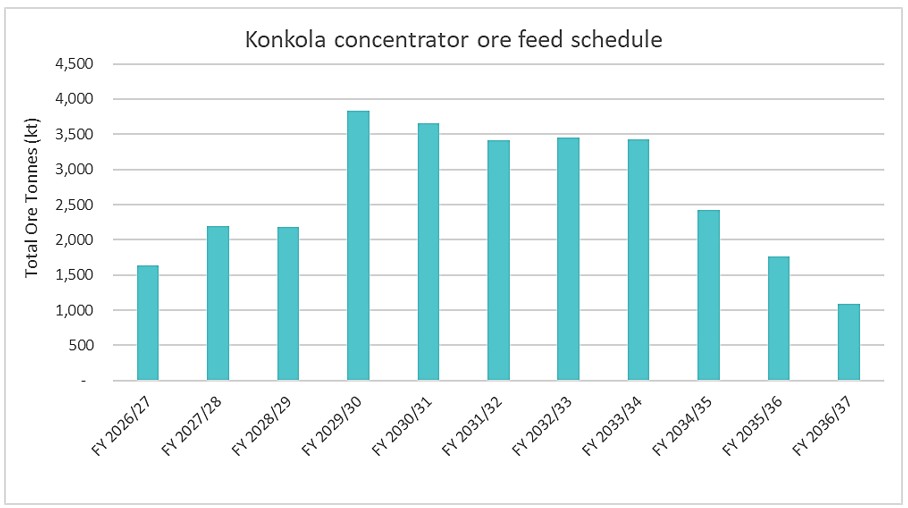

| Figure 14.10 | Konkola Concentrator ore feed schedule | 170 |

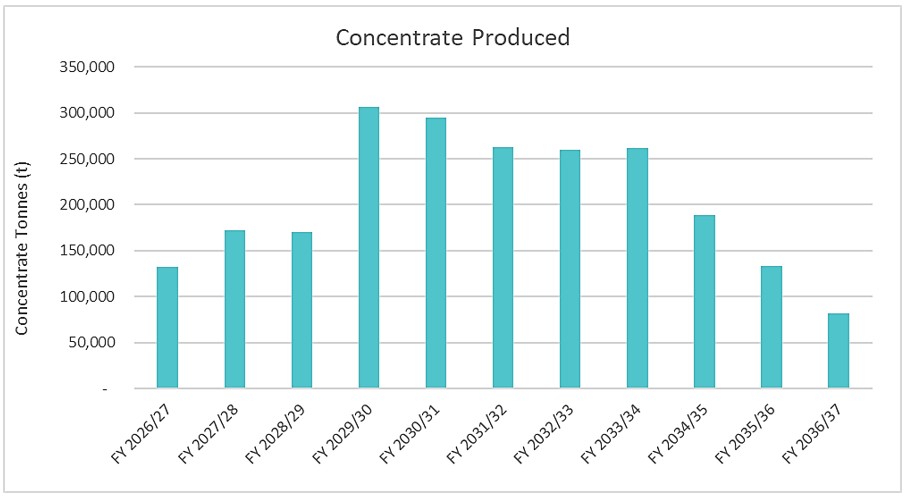

| Figure 14.11 | Konkola concentrate production | 171 |

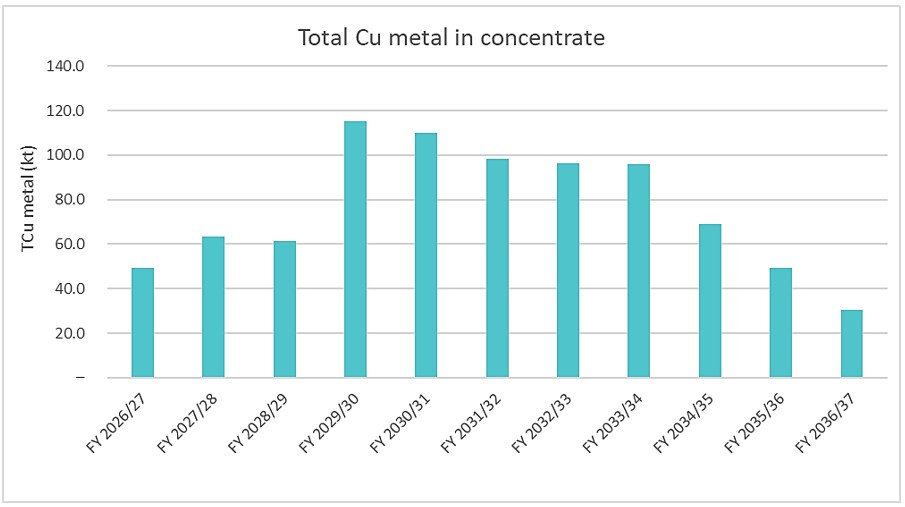

| Figure 14.12 | Total copper metal in Konkola concentrate | 171 |

| Figure 14.13 | Nchanga TLP flowsheet | 173 |

| Figure 14.14 | Historical Nchanga TLP throughput | 174 |

| Figure 14.15 | Nchanga historical recoveries | 174 |

| Figure 14.16 | Nchanga TLP copper recovery since restart | 176 |

| Figure 14.17 | Nchanga TLP throughput since restart | 176 |

| Figure 14.18 | Nchanga TLP feed schedule – Mineral Reserve case | 177 |

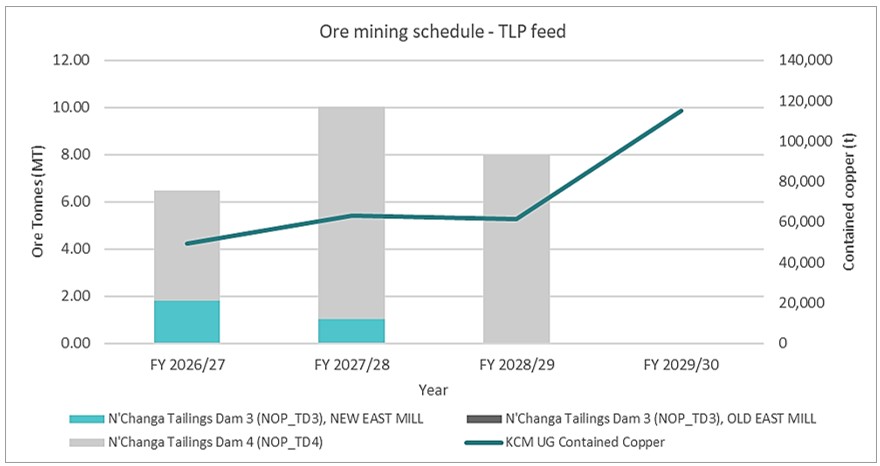

| Figure 14.19 | Nchanga TLP Mineral Reserve mine plan copper production and recovery | 178 |

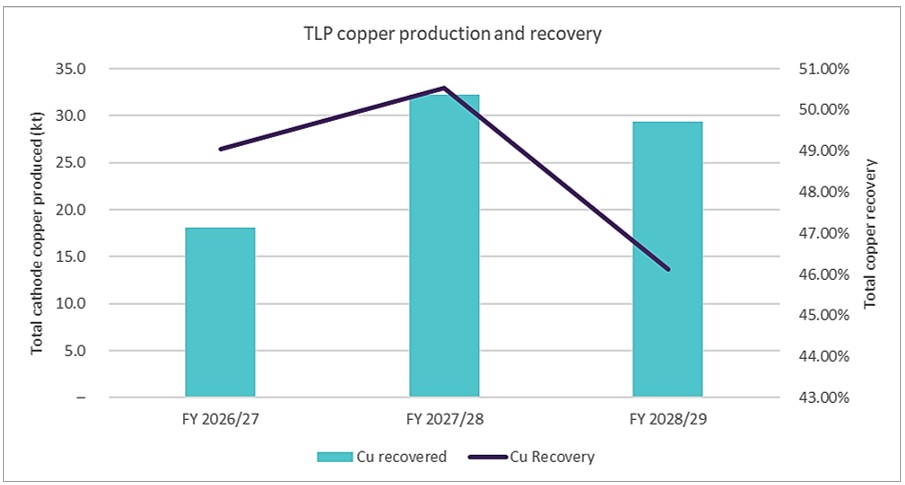

| Figure 14.20 | Nchanga Smelter block flow diagram – design rates shown | 179 |

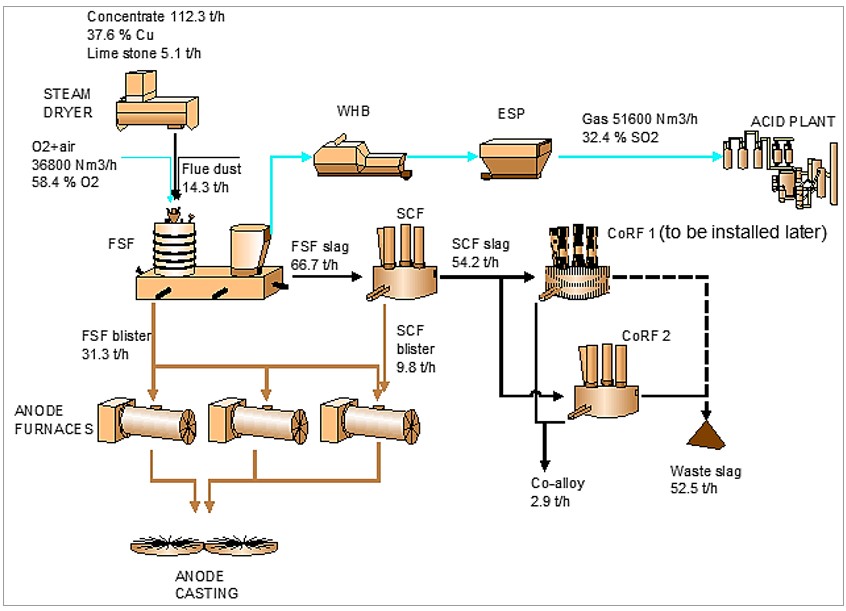

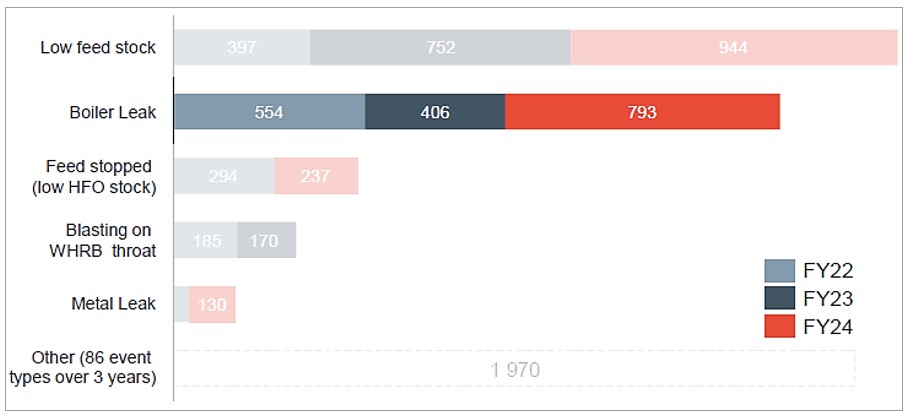

| Figure 14.21 | Smelter downtime - FY22, FY23, FY24 | 182 |

| Figure 14.22 | Nkana Refinery – process flowsheet | 189 |

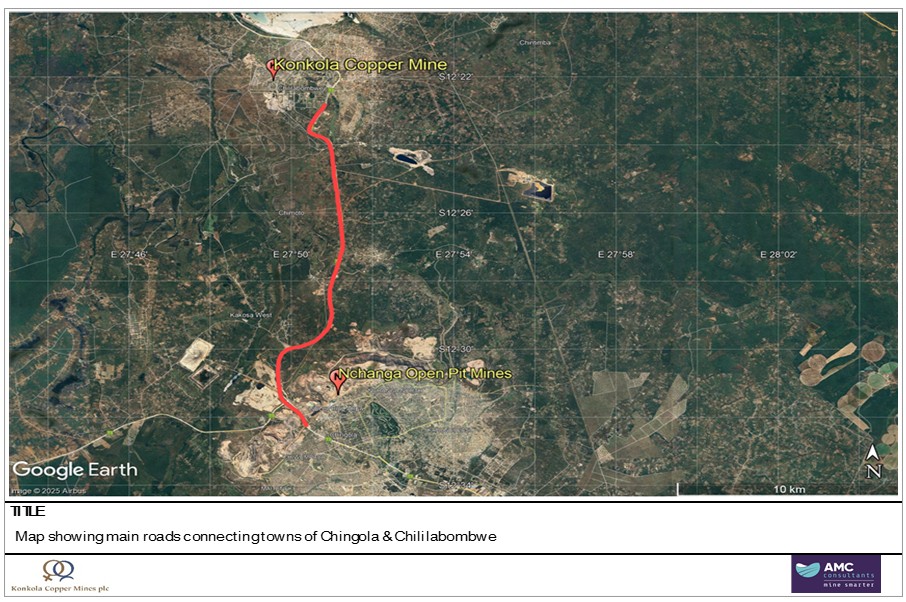

| Figure 15.1 | Map showing main roads connecting towns of Chingola and Chililabombwe | 195 |

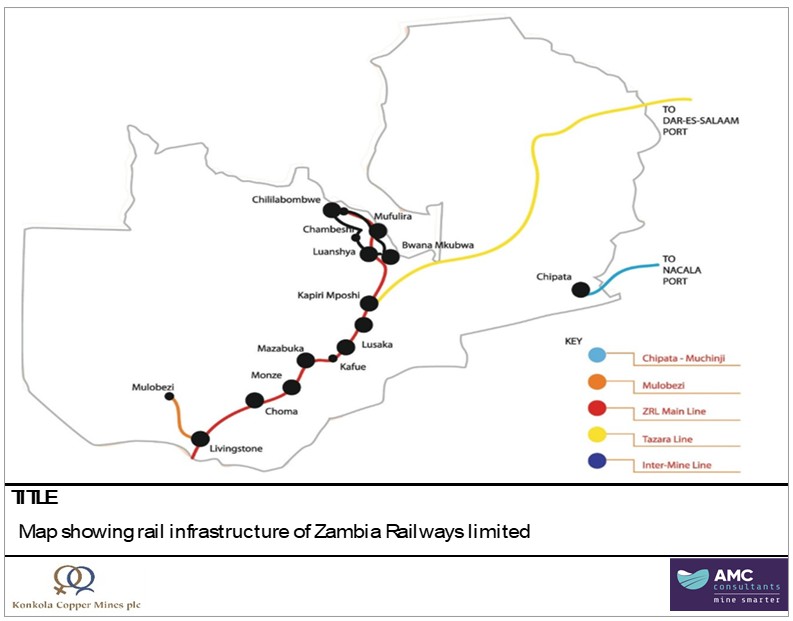

| Figure 15.2 | Map showing rail infrastructure of Zambia Railways Limited | 196 |

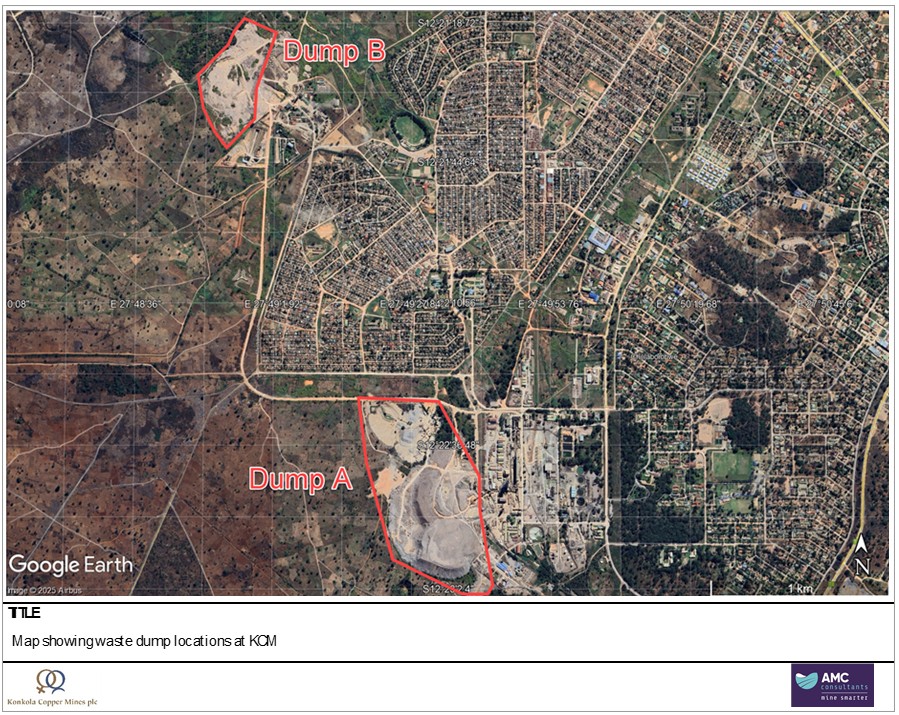

| Figure 15.3 | Map showing waste dump locations at KCM | 198 |

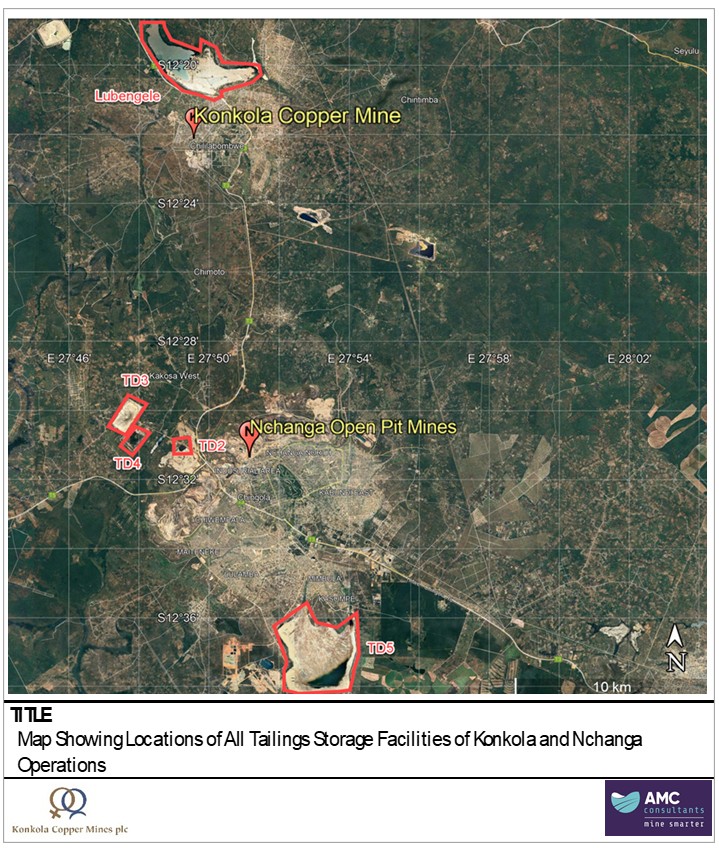

| Figure 15.4 | Map showing locations of all TSFs of Konkola and Nchanga Operations | 199 |

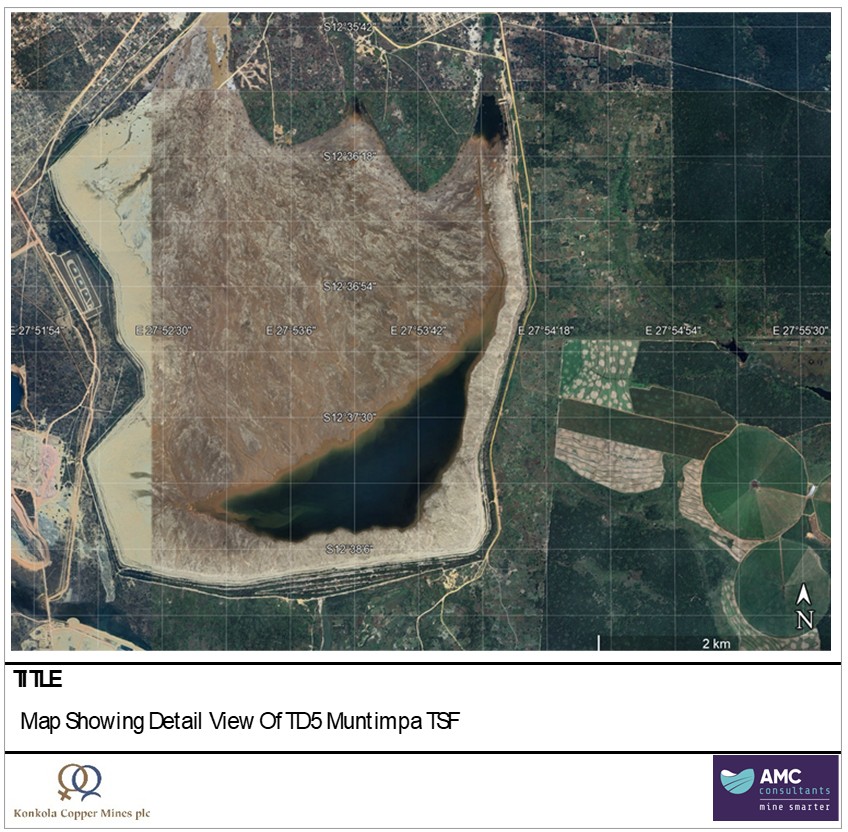

| Figure 15.5 | Map showing detail view of TD05 Muntimpa TSF | 200 |

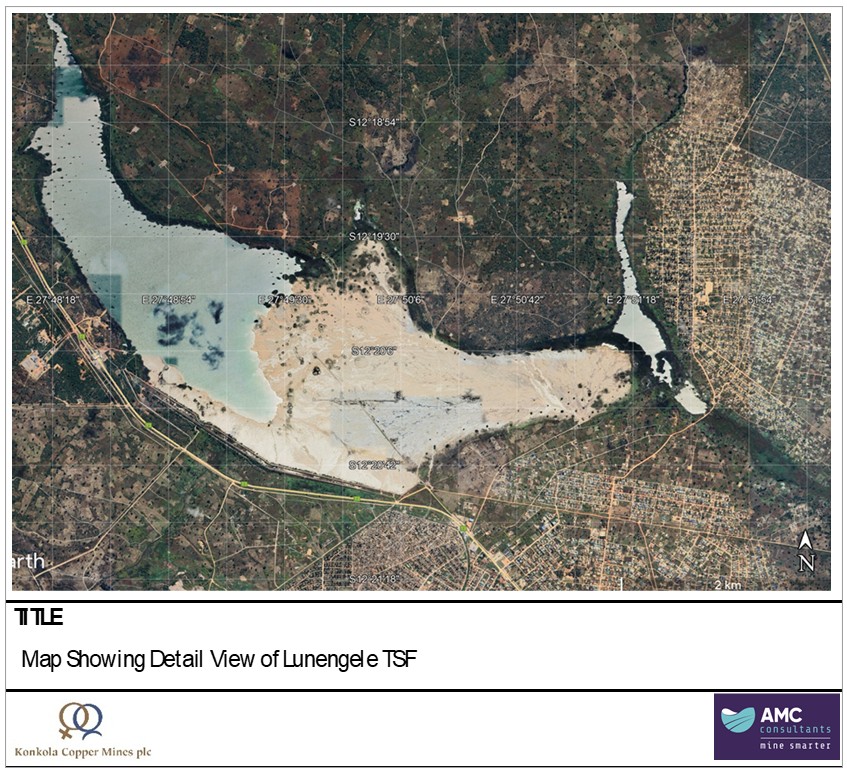

| Figure 15.6 | Map showing detail view of Lubengele TSF | 201 |

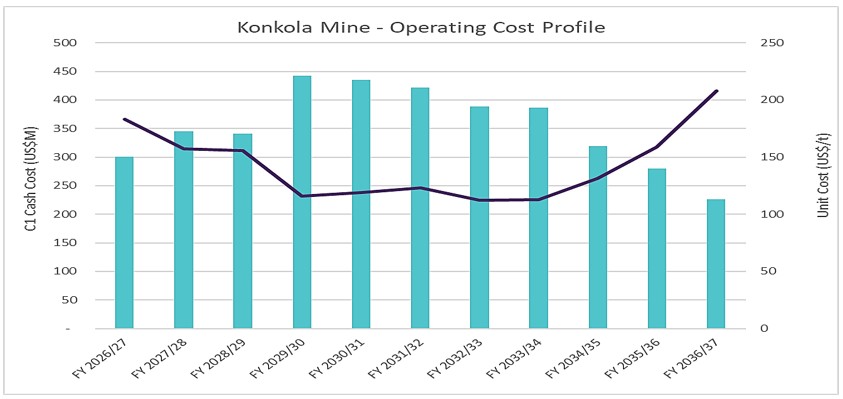

| Figure 18.1 | Konkola Mine operating cost profile – Mineral Reserve case | 226 |

| Figure 18.2 | Konkola Mine cost breakdown – Mineral Reserve case | 226 |

| Figure 19.1 | KCM Smelter Feed Profile – Mineral Reserve Case (incl. external purchased concentrates) | 234 |

| Figure 19.2 | Projected overall mining schedule | 234 |

| Figure 19.3 | KCM Mineral Reserve production profile | 235 |

| Figure 19.4 | Copper price forecast – consensus range | 236 |

| Figure 19.5 | Mineral Reserve cashflow | 242 |

| Figure 19.6 | Sensitivity analysis graph – Mineral Reserve | 243 |

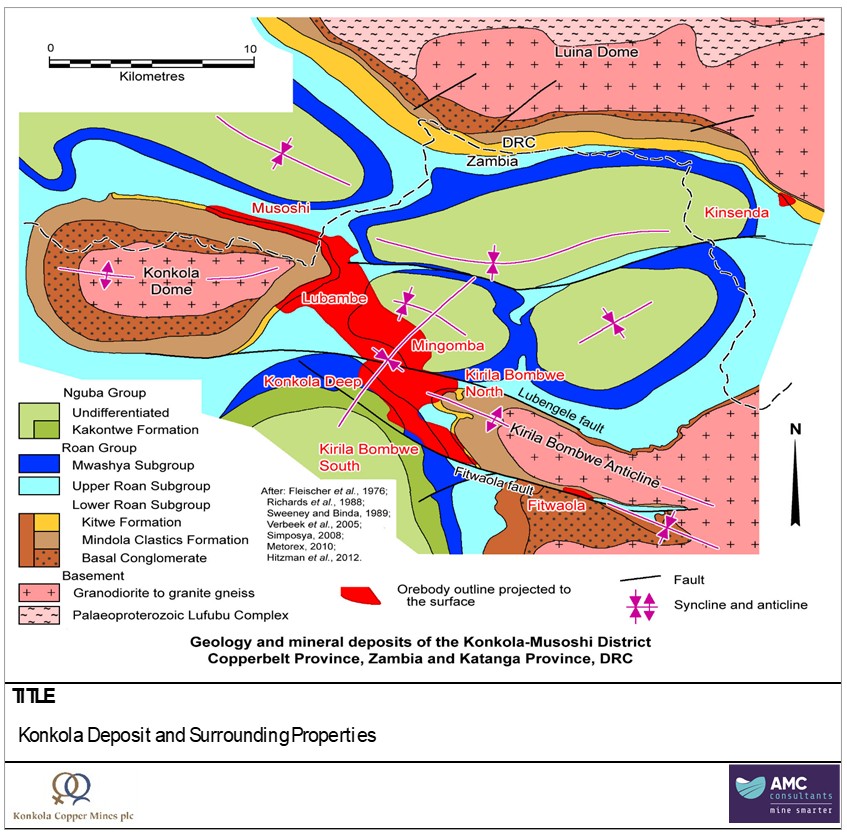

| Figure 20.1 | Konkola deposit and surrounding properties | 245 |

amcconsultants.com | xiv |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| 1 | Executive summary |

| 1.1 | Introduction |

AMC Consultants (UK) Limited (AMC) was engaged by Vedanta Resources Limited (Vedanta) to prepare this Preliminary Feasibility Study (PFS) Technical Report Summary (TRS) for the Konkola Mine and associated TD03 and TD04 tailings dam operations located in the Zambian Copperbelt. This report has been prepared in compliance with Subpart 1300 of Regulation S-K (S-K 1300) as mandated by the United States Securities and Exchange Commission (SEC).

This PFS TRS presents the economic viability of mining Mineral Reserves at the Konkola Mine and the recovery of copper from TD03 and TD04 tailings dams. The technical contents of this report adhere to requirements for reporting on Mineral Reserves, as required by S-K 1300. The effective date of this report is 1 April 2026.

| 1.2 | Property description and ownership |

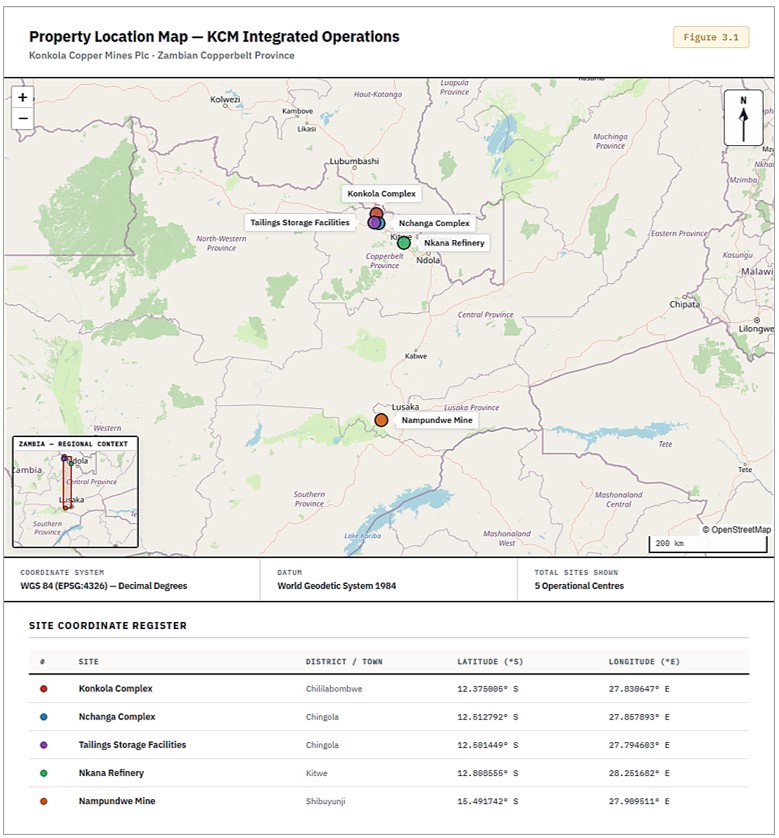

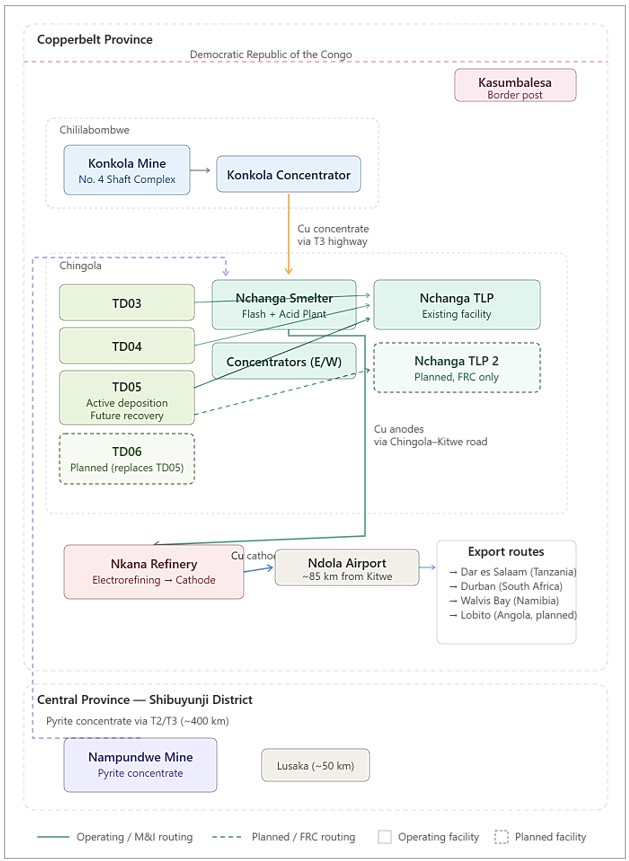

The Konkola Copper Mines Plc (KCM) Integrated Operations constitutes a single material property comprising an integrated copper production complex from ore extraction through to refined copper metal. KCM is an integrated copper mining, processing, and refining operation located in the Copperbelt Province of the Republic of Zambia. KCM’s operations produce refined copper cathode (LME Grade A) and cobalt alloy from two principal sources: underground mining at the Konkola Mine and recovery of copper from historical tailings dams at the Nchanga site. Run-of-mine ore from the Konkola Mine is processed through the Konkola Concentrator to produce copper concentrate, which is smelted at the Nchanga Smelter (an Outotec flash smelting facility) and refined at the Nkana Refinery in Kitwe. Oxide copper from tailings is recovered through the Nchanga Tailings Leach Plant (the Nchanga TLP) via sulfuric acid leaching, solvent extraction, and electrowinning.

KCM’s broader operations also include the Nchanga Business Unit (NBU), which comprises the Chingola Open Pit D and F (COP DF), underground operations (Nchanga Upper and Lower Ore Bodies), and several brownfield development prospects including COP E Extension, and Kakosa. These operations are covered in the companion Initial Assessment TRS. The Nchanga Business Unit mining operations are excluded from this PFS as they do not currently support Mineral Reserves.

KCM was privatised in March 2000 when assets were acquired from the state-owned Zambia Consolidated Copper Mines Limited (ZCCM). Following the exit of Anglo American in September 2002, Vedanta Resources assumed operational control from November 2004, investing in smelter construction, the Konkola Concentrator, Nchanga Concentrators, and the Konkola Mine, Konkola Deep Mining Project (No. 4 Shaft, 6 Mtpa hoisting capacity). KCM’s integrated metal production peaked at 160,000 tonnes per annum in FY 2013. In 2019, Zambia Consolidated Copper Mines Investment Holdings Plc (ZCCM-IH) commenced provisional liquidation proceedings, and operations were managed by a provisional liquidator until July 2024, when they were returned to Vedanta with shareholding restored to pre-liquidation status. Further details are provided in Section 5.

The properties covered by this PFS TRS are:

| · | Konkola Mine: Located near Chililabombwe, Republic of Zambia, approximately 20 kilometers (km) north of Chingola and 5 km south of the Democratic Republic of the Congo (DRC) border. The mine lies within the Zambian Copperbelt, a region known for its extensive copper deposits and well-established mining infrastructure. |

| · | TD03 and TD04: Historical tailings dams located at the Nchanga site near Chingola, containing oxide copper deposited from past Nchanga Concentrators operations. Reclaimed tailings are reclaimed and processed through the Nchanga TLP to produce copper cathode. |

KCM is a subsidiary of CopperTech Metals Inc. (the registrant). Mineral rights associated with the Konkola and Nchanga license areas are held by Konkola Mineral Resources Limited (KMRL), a subsidiary of KCM. As of the effective date of this report, Vedanta Resources holds 79.42% of KCM’s issued share capital, with ZCCM-IH holding 20.58%. Further details on the registrant are provided in Section 2.1 and on operational history, including ownership transitions, in Section 5.

amcconsultants.com | 15 |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

The Konkola Mine and adjacent mineral processing facilities contribute approximately 90% of recovered copper production over the life of the Mineral Reserve mine plan.

| 1.3 | Mineral rights |

KCM's mineral rights are governed by the Republic of Zambia's Minerals Regulation Commission Act (2024) and operate under Large-Scale Mining Licenses (LSMLs). The key licenses relevant to this PFS are shown in Table 1.1.

| Table 1.1 | KCM mineral rights and licenses |

Asset | License | Description | Area (ha) | Expiry | ||||

| Konkola | 7076-HQ-LML | Mining and concentrator operations | 4,054 | 30 Mar 2050 | ||||

| Nchanga | 7075-HQ-LML | Nchanga mining operations | 10,659 | 30 Mar 2050 | ||||

| Nchanga TLP | 28174-HQ-MPL | Nchanga TLP operations | 177 | 16 Dec 2045 | ||||

| Nkana Refinery | 20945-HQ-MPL | Refining activities at Kitwe | 50 | 18 Apr 2050 |

As of the effective date of this report, and to the Qualified Person's (QP) knowledge, there are no material encumbrances, legal proceedings, or compliance issues that would adversely affect the standing of these licenses or KCM's ability to conduct operations. Standard regulatory and environmental obligations applicable to mining operations in Zambia are described in Section 3.

| 1.4 | Geology and mineralisation |

The Konkola deposit is a stratiform, sediment-hosted copper-cobalt deposit located within the Central African Copperbelt. Mineralisation is hosted in Neoproterozoic metasedimentary rocks of the Katanga Supergroup, primarily within the Ore Shale Unit (OSU). Copper mineralisation occurs as disseminated and vein-hosted chalcopyrite and bornite, with associated cobalt mineralisation. The orebody dips between 35° and 70° with an average thickness of approximately 9 meters (m). TD03 and TD04 comprise historical tailings from Nchanga Concentrators operations containing residual copper amenable to acid leaching.

| 1.5 | Exploration status |

Exploration at the Konkola deposit has been ongoing since its discovery in 1924, with systematic diamond drilling programs conducted from the 1950s through 2019. The drilling database comprises historical and modern diamond core data collected across multiple campaigns by successive asset owners, including ZCCM (pre-2000), Anglo American (2000-2002), and Vedanta Resources (2004-2019). No exploration, infill, or extension drilling has been undertaken since the commencement of provisional liquidation in May 2019.

Drilling methods employed at Konkola include pneumatic and electric hydraulic diamond coring using BQ, NQ, HQ, and PQ diameter core, with a minimum core recovery expectation of 90% in mineralised zones. Core logging records lithology, rock type, visible mineralisation, degree of weathering, RQD, and joint density. Sampling intervals are a maximum of 1 m within mineralisation, with 0.5 m intervals in the immediate footwall and hangingwall formations.

A quality assurance and quality control (QAQC) program is in place, incorporating blank and certified reference material (CRM) samples inserted at a rate of one per five primary samples (for batches of fewer than 20 samples) or one per ten primary samples (for batches exceeding 30 samples). Repeat analyses of coarse rejects and pulp samples comprise at least 20% of combined samples. Details of the QAQC program and sample preparation methods are provided in Sections 7 and 8.

amcconsultants.com | 16 |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

Infill drilling to convert Inferred Mineral Resources to Indicated, and subsequently to support additional Mineral Reserve conversion re-commenced in late 2025 and is ongoing. This is from both underground and surface. Further drilling is recommended as a priority activity (Section 23.1.1).

| 1.6 | Development and operations status |

KCM is a brownfield operation with over 95 years of continuous mining history. The Konkola Mine, Nchanga smelter, Nkana refinery, and associated processing infrastructure are established, operational facilities. Following the return of operational control to Vedanta in July 2024, KCM has commenced a restart and ramp-up of operations.

Konkola is an established underground copper mining operation located near Chililabombwe, Republic of Zambia. Underground mining is currently operational, with ore hoisted via No. 4 Shaft, No. 3 Shaft and No. 1 Shaft. Development activities are centred on the Konkola Deep Mining Project (KDMP), which provides access to deeper sections of the orebody via underground declines, with No. 4 Shaft already extending to the lower levels of the known mineral resource. Mining is primarily undertaken using longitudinal longhole open stoping (LHOS) methods, with a planned transition from Post Pillar Cut and Fill (PPCF) to Panel Stoping with Paste Fill in flatly dipping areas of the orebody to increase resource recovery and improve the ore-to-waste development ratio. Paste fill is not currently used at the operation; however, it is a critical component for future extraction of flatly dipping areas, where panel stoping is planned, and will enable secondary stope extraction and assist with regional geotechnical stability.

The operation is characterised by exceptionally high groundwater inflows and is regarded as one of the wettest underground mines globally. A comprehensive dewatering system is in place, including staged pumping stations, sumps, and water management infrastructure to maintain mine access and safety. Ventilation systems have been progressively expanded to address increasing depth and the use of underground diesel fleets. Personnel access is provided via shaft hoisting systems and declines, supported by underground refuge chambers and surface infrastructure.

Surface processing facilities are operational, including the Konkola Concentrator (crushing, milling, flotation, and dewatering), the Nchanga Flash Smelter, the Nkana Refinery (electrorefining), and the Nchanga Tailings Leach Plant (TLP) for acid soluble copper recovery from TD03 and TD04. The integrated processing route produces LME Grade A refined copper cathode and cobalt alloy.

Key infrastructure supporting operations includes a long-term power supply agreement with Copperbelt Energy Corporation (CEC) providing 200 MW capacity, a comprehensive dewatering system managing approximately 350,000 m³/day of groundwater inflows at the Konkola Mine, and established road and logistics infrastructure connecting the Konkola, Nchanga, and Nkana sites across the Copperbelt Province.

The PFS mine plan contemplates sustained production from the existing infrastructure with capital investment in underground development, dewatering expansion (including the critical 1390 level pumping infrastructure), and sustaining capital across all facilities. No new greenfield infrastructure or major expansion capital beyond the existing operational footprint is required for the activities contemplated in this PFS.

| 1.7 | Mineral Reserve estimate |

This sub-section contains forward-looking information related to the Mineral Reserve estimates for the KCM Integrated Operations. The material factors that could cause actual results to differ materially from the conclusions, estimates, designs, forecasts, or projections in the forward-looking information include any significant differences from one or more of the material factors or assumptions set forth in this sub-section, including geological and grade interpretations, commodity prices, mining dilution and recovery assumptions, and forecasts associated with establishing the economic viability of the project.

amcconsultants.com | 17 |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

The Mineral Reserve estimates presented herein have been prepared in accordance with the U.S. SEC S-K 1300 and have been reviewed and approved by the QPs. Mineral Reserves represent the economically mineable parts of Measured and Indicated Mineral Resources and include allowances for dilution and mining losses. Mineral Reserves based on Measured Mineral Resources have been classified as Proven Mineral Reserves, and Mineral Reserves based on Indicated Mineral Resources have been classified as Probable Mineral Reserves, consistent with S-K 1300 definitions. No Inferred Mineral Resources have been included in the Mineral Reserve estimate, the production schedule, or the economic analysis presented in this PFS. The Mineral Reserve estimate has been completed to a level appropriate for a Preliminary Feasibility Study and reflects the application of modifying factors, including mine design, production scheduling, metallurgical recovery, and economic parameters, to the Measured and Indicated Mineral Resources.

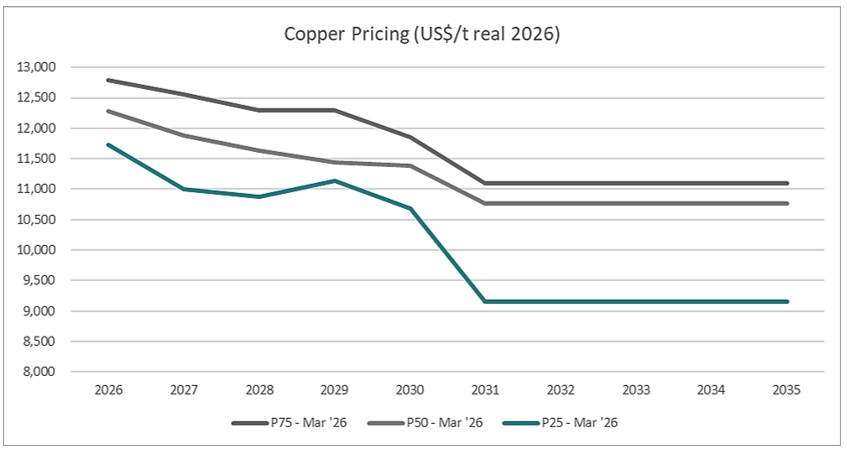

The Mineral Reserve estimates are based on a copper price assumption of US$9,000/t (US$4.08/lb) for Net Smelter Return (NSR) cut-off determination and US$28,000/t (US$12.70/lb) for cobalt. The economic analysis supporting the Mineral Reserve is based on P75 consensus copper price forecasts as detailed in Section 16. In the opinion of the QP, these price assumptions provide a reasonable basis for establishing the economic viability of the project and satisfy S-K 1300 requirements for commodity price disclosure.

The Mineral Reserve estimate as of 1 April 2026 is summarised in Table 1.2. The point of reference for Mineral Reserves is defined at the point where ore is delivered to the processing plant. As of the effective date of this report, Measured and Indicated Mineral Resources represent approximately 23% of the total Mineral Resource. The QPs consider that there is potential to increase Mineral Reserves through continued resource definition drilling as recommended in Section 23.1.1.

| Table 1.2 | KCM Mineral Reserve estimate summary – 1 April 2026 |

| Deposit | Classification | Tonnes (Mt) | TCu% | Cu (kt) | TCo% | Co (kt) | ||||||

| Konkola UG | Proven | 2.1 | 2.5 | 54.6 | 0.06 | 1.36 | ||||||

| Konkola UG | Probable | 27 | 2.9 | 784 | 0.06 | 15.5 | ||||||

| Konkola UG Total | Proven + Probable | 29 | 2.9 | 839 | 0.06 | 16.8 | ||||||

| TD03 Tailings Complex | Proven | - | - | - | - | - | ||||||

| TD03 Tailings Complex | Probable | 2.8 | 0.8 | 22 | - | - | ||||||

| TD04 Tailings Complex | Proven | - | - | - | - | - | ||||||

| TD04 Tailings Complex | Probable | 22 | 0.6 | 135 | - | - | ||||||

| Tailings Complex (Total) | Proven | - | - | - | - | - | ||||||

| Tailings Complex (Total) | Probable | 25 | 0.6 | 157 | - | - | ||||||

| Tailings Complex (Total) | Proven & Probable | 25 | 0.6 | 157 | - | - | ||||||

| KCM Total | Proven | 2.1 | 2.5 | 54.6 | 0.06 | 1.36 | ||||||

| KCM Total | Probable | 51 | 1.8 | 941 | 0.03 | 15.5 | ||||||

| KCM Total | Proven + Probable | 54 | 1.9 | 995 | 0.03 | 16.8 |

amcconsultants.com | 18 |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

Notes:

| · | Mineral Reserves are reported with an effective date of 1 April 2026. |

| · | Classification in accordance with S-K 1300. Mineral Reserves are derived from Measured and Indicated Mineral Resources by application of mining, processing, metallurgical, infrastructure, economic, marketing, legal, environmental, social, and governmental modifying factors. Inferred Mineral Resources are not included in Mineral Reserves and are not included in this table. |

| · | Mineral Reserves are reported on a 100% basis as the Mineral Reserves of Konkola Copper Mines Plc. |

| · | Cut-off grade, Konkola Mine: NSR cut-off values of US$50–125/t ROM apply, calculated using a copper price of US$9,000/t (US$4.08/lb) and a cobalt price of US$28,000/t (US$12.70/lb). Cut-off range varies by mining area and reflects underground access cost and depth. |

| · | Cut-off grade, TD03 and TD04: No cut-off applied. The Mineral Reserve represents 100% of the TD04 and TD03 Mineral Resource. |

| · | Metallurgical recovery, Konkola Mine: Concentrator 89.2% Cu (Mineral Reserve mine plan average), 60% Co; Smelter 98.1% Cu, 30% Co; Concentrate payable Cu 96.8%. |

| · | Metallurgical recovery, Nchanga TLP (ambient leach, TD03 and TD04 only): 74.8% Acid Soluble Copper (ASCu) recovery, equivalent to approximately 48.5% Total Copper (TCu) recovery to cathode, derived from the 10-year historical average TLP performance (2010–2019) and consistent with FY2025/26 actual. The Elevated Temperature Leach retrofit described in the companion Initial Assessment Technical Report Summary is not part of the Mineral Reserve scope. |

| · | Cobalt in TD03 and TD04: Cobalt is present in TD03 and TD04 tailings but is not recovered in the TLP electrowinning process. No cobalt revenue is attributed to TD03 or TD04 in the economic analysis. The "–" entries in the cobalt grade and content columns reflect non-recovery in the Mineral Reserve scope, not absence of cobalt mineralisation. |

| · | Processing route for Konkola Mineral Reserves: Konkola Concentrator → Nchanga Smelter → Nkana Refinery. Processing route for TD03 and TD04 Mineral Reserves: existing Nchanga TLP (ambient leach) → copper cathode. |

| · | Point of reference: Ore delivered to the processing plant (mill feed). For TD03 and TD04, point of reference is the reclaimed tailings stream delivered to the Nchanga TLP feed. |

| · | Pricing convention: Mineral Reserves are reported using a copper price of US$9,000/t (US$4.08/lb) and a cobalt price of US$28,000/t (US$12.70/lb) for NSR cut-off grade determination. The economic analysis in Section 19 applies P75 consensus copper pricing of US$11,101/t to US$12,793/t over the production period. The lower NSR cut-off price provides a conservative reserve declaration boundary that holds under reasonable downside copper price scenarios; the higher P75 consensus pricing applied in the economic analysis represents the consensus market view over the production period and is the appropriate basis for evaluating project NPV and IRR. This convention is consistent with industry practice for SK1300 Mineral Reserve disclosure. |

| · | Tonnage and grade are rounded; this may result in minor apparent computational discrepancies in totals. |

| · | Mineral Reserves are 100% attributable to Konkola Copper Mines Plc. |

The Measured and Indicated portion of TD05 (198 Mt - refer companion Initial Assessment TRS Table 11.28) is reported as a Mineral Resource in the companion IA TRS but has not been declared as a Mineral Reserve in this PFS. The QPs consider that the engineering and economic definition required for TD05 Mineral Reserve declaration is below the PFS threshold at the effective date, and a prefeasibility-level study addressing TD05 reclamation through the existing Nchanga TLP is identified in Section 23 as essential to support a future Mineral Reserve declaration. Accordingly, the M&I Case in the companion IA TRS - which incorporates TD05 M&I via the existing Nchanga TLP and runs approximately 15 years - has a broader scope than the Mineral Reserve case presented in this PFS (approximately 11 years).

The QPs are not aware of any environmental, permitting, legal, title, taxation, socio-political, marketing, or other relevant factors that could materially affect the Mineral Reserve estimates, other than as disclosed elsewhere in this report.

| 1.8 | Mineral Resources |

Mineral Resources for the KCM Integrated Operations are detailed in Section 11. Mineral Resources are reported exclusive of Mineral Reserves and do not have demonstrated economic viability. Inferred Mineral Resources are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorised as Mineral Reserves, and there is no certainty that all or any part of the Inferred Mineral Resources will be converted to Measured or Indicated Mineral Resources with additional exploration. Mineral Resources that are not Mineral Reserves have not been included in the production schedule, mine plan, or economic analysis presented in this PFS. The full Mineral Resource case is assessed in the companion Initial Assessment TRS (AMC, 2026). The Mineral Resource estimate as of 1 April 2026 is summarised in Table 1.3.

amcconsultants.com | 19 |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| Table 1.3 | KCM Mineral Resource estimate summary (Exclusive of Mineral Reserves) – 1 April 2026 |

| Deposit | Classification | Tonnes (Mt) | TCu (%) | Cu (kt) | TCo (%) | Co (kt) | ||||||

| Konkola Mine | Measured | 1.4 | 3.7 | 52 | 0.06 | 1 | ||||||

| Konkola Mine | Indicated | 5.9 | 3.8 | 221 | 0.07 | 4 | ||||||

| Konkola Mine | M + I | 7.3 | 3.8 | 273 | 0.06 | 4 | ||||||

| Konkola Mine | Inferred | 248 | 3.4 | 8,322 | 0.06 | 149 | ||||||

| Tailings Dam 03 (“TD03”) | Indicated | 0.0 | - | - | - | - | ||||||

| Tailings Dam 04 (“TD04”) | Indicated | 0.0 | - | - | - | - | ||||||

| KCM Total | M + I | 7.3 | 3.8 | 273 | 0.06 | 4 | ||||||

| KCM Total | Inferred | 248 | 3.4 | 8,322 | 0.06 | 149 |

Notes:

| · | Mineral Resources are reported with an effective date of 1 April 2026. |

| · | Mineral Resources are reported exclusive of Mineral Reserves. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability. |

| · | Classification in accordance with S-K 1300. |

| · | Point of reference: in situ material. |

| · | Cut-off grade, Konkola Mine: 1.1% TCu, based on a copper price of US$10,000/t (US$4.54/lb). |

| · | Cut-off grade, TD03 and TD04: no cut-off applied; tailings inventory not classified by grade. |

| · | TD04 Mineral Resources have been fully converted to Probable Mineral Reserves (Table 1.2; Section 12). |

| · | Inferred Mineral Resources are considered too speculative geologically to be categorised as Mineral Reserves at this time, and there is no certainty that Inferred Mineral Resources will be converted to higher confidence categories with additional exploration. As of the effective date, approximately 97% of the total Mineral Resource (exclusive of Mineral Reserves) is classified as Inferred and is concentrated at the Konkola Mine. Inferred Mineral Resources are excluded from the PFS mine plan and economic assessment; any Inferred material within mine designs has been treated as waste and assigned zero grade. The full Mineral Resource case (including Inferred) is assessed in the companion Initial Assessment Technical Report Summary (AMC, 2026). |

| · | Metallurgical recovery, Konkola Mine: Concentrator 89.2% Cu, 60% Co; Smelter 98.1% Cu, 30% Co; Concentrate payable Cu 96.8%. Overall ROM to payable Cu: 84.7%; ROM to refined Co: 18.0%. |

| · | Metallurgical recovery, Nchanga TLP (ambient leach, TD03 and TD04 only): 74.8% Acid Soluble Copper (ASCu) recovery, equivalent to approximately 48.5% Total Copper (TCu) recovery to cathode. |

| · | Mineral Resources are 100% attributable to Konkola Copper Mines Plc. |

| · | Tonnage and grade are rounded; this may result in minor apparent computational discrepancies in totals. |

As of the effective date of this report, approximately 63% of total KCM Mineral Resources are classified as Inferred and have not been included in the Mineral Reserve estimate; the Measured and Indicated Mineral Resources represent approximately 37% of the total Mineral Resource. The QPs consider that there is potential to increase Mineral Reserves through continued resource definition drilling as recommended in Section 23.1.1.

| 1.9 | Mining methods |

Konkola Mine is an established underground copper mining operation. Development activities are centered on the Konkola Deep Mining Project (KDMP), which provides access to deeper sections of the orebody via vertical shafts and underground declines. Mining is primarily undertaken using longitudinal longhole open stoping (LHOS) methods.

The orebody dips between 35° and 70°, with average thickness of 9 meters (m). A mine plan redesign of KDMP formed an integral component of the PFS. The mining method applied to flatly dipping (<40°) parts of the orebody has been changed from Post Pillar Cut and Fill (PPCF) to Panel Stoping with paste fill as a key enabler. The change in mining method increases resource recovery, thereby improving the ore to waste development ratio.

The operation is characterised by exceptionally high groundwater inflows and is regarded as one of the wettest underground mines globally, with an ore hoist-to-water pumping ratio of approximately 1:49. A comprehensive dewatering system is in place, including staged pumping stations, sumps, and water management infrastructure to maintain mine access and safety.

amcconsultants.com | 20 |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| 1.10 | Processing and recovery methods |

KCM's processing infrastructure comprises the Konkola Concentrator, Nchanga concentrators, Nchanga TLP, Nchanga flash smelter, and Nkana refinery. These assets are operationally integrated and cannot be economically separated. Surface facilities at the Konkola Complex process run-of-mine (ROM) ore through crushing, milling, flotation, and dewatering. The produced concentrate is transported to the Nchanga Smelter, with final copper production completed at the Nkana Refinery via electrorefining.

Key processing parameters:

| · | Konkola Concentrator Recovery: 89.2% copper recovery to concentrate. |

| · | Concentrate Grade: Approximately 33% copper. |

| · | Smelter Recovery: 98.1% copper recovery. |

| · | Concentrate Payable Cu: 96.8% payable copper. |

| · | Nchanga TLP Recovery: 48.5% total copper recovery (refer to Section 10 for acid soluble copper recovery details). |

The LOM plan assumes purchase of 300,000–315,000 tpa of third-party concentrate from regional Zambian and DRC Copperbelt mines to supplement KCM's own internal feed. This is a process requirement of the Nchanga Flash Smelting Furnace, which requires a specific Fe / SiO₂ ratio in the feed blend that cannot be achieved using KCM's own concentrates alone, as both the Konkola and Nchanga concentrators produce high-silica concentrate (typically 20–22% SiO₂ against a preferred limit of less than 15% SiO₂). Third-party concentrate is purchased on a metal-return basis, KCM takes ownership of the concentrate and bears the associated price risk, and is not a toll processing arrangement.

Third-party concentrate has been sourced historically from large-scale open pit and underground copper producers in the Zambian and DRC Copperbelt, providing a diverse regional supply base within 200 to 500 kilometres of the Nchanga Smelter. The Copperbelt region represents one of the world's largest copper-producing areas and output is forecast to grow across the Mineral Reserve LOM period. A structural dynamic supporting supply continuity is the Zambian government's 10% export levy on copper concentrate, which creates a material economic incentive for Zambian producers to supply domestic smelters rather than export, and the comparatively high logistics cost of shipping DRC-origin concentrate to overseas smelters relative to regional Copperbelt facilities. However, a number of the largest Copperbelt mine expansions are expected to be accompanied by dedicated on-site smelting capacity over the LOM period, which would reduce the volume of concentrate available to third-party buyers. In particular, Ivanhoe Mines has announced plans to commission an on-site direct-to-blister smelter at the Kamoa-Kakula Copper Complex in the DRC (500,000 tpa capacity), which, once operational, is expected to process Kamoa-Kakula's own concentrate internally rather than making it available to regional third-party smelters. Kamoa-Kakula concentrate has historically been one of the most desirable high-grade, low-silica feeds available to the Nchanga Flash Smelting Furnace (FSF) and its anticipated withdrawal from the regional market represents a material change in the third-party concentrate supply landscape over the LOM. Active management of the regional supply base will accordingly be required throughout the LOM to maintain the assumed 300,000–315,000 tpa of third-party concentrate.

amcconsultants.com | 21 |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

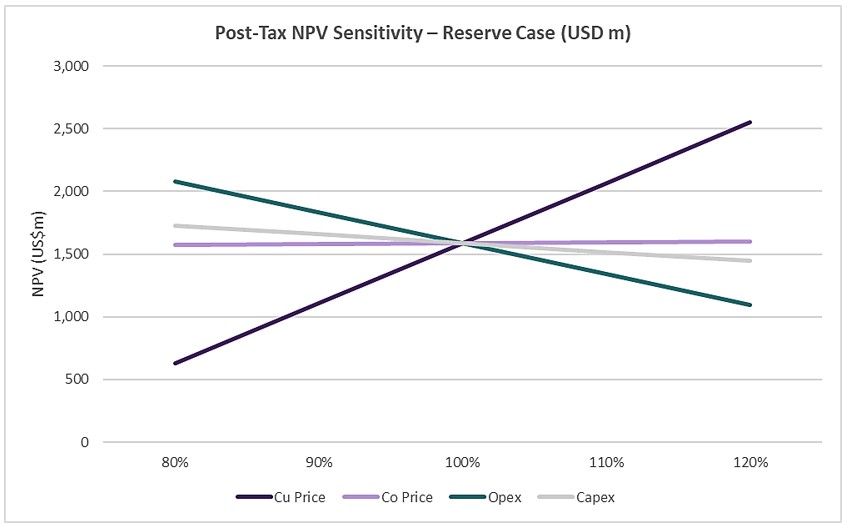

The QPs consider there is a reasonable basis to expect that sufficient concentrate will remain available at commercially reasonable terms given the scale of regional Copperbelt production, the structural inability of many smaller producers to develop proprietary smelting capacity, and the structural supply dynamics described in Section 14.4.3. However, the absence of binding supply contracts beyond FY2026 introduces commercial uncertainty that the QPs consider to be a material risk to the LOM plan, and securing ongoing supply arrangements is identified as an essential commercial requirement. The sensitivity of project economics to this dependency is assessed in Section 19.2.4, which models the removal of third-party concentrate from the LOM plan entirely. The total NPV₈% impact comprises two components: the direct smelter contribution accounts for approximately US$140M or approximately 9% of the post-tax base case NPV₈% of US$1,588M; the incremental acid procurement cost arising from reduced smelter throughput accounts for a further approximately US$70M, reflecting the delta between the external market price of US$175/t and the internal transfer price of US$130/t applied to the acid shortfall of approximately 1.6 Mt over the Mineral Reserve life of mine. The combined post-tax NPV₈% reduction is approximately US$210M or approximately 13%, reducing the post-tax base case NPV₈% to approximately US$1,378M. The KCM Integrated Operations remain economic under this sensitivity on the basis of KCM's own Mineral Reserve production, and the uninterrupted sourcing of third-party concentrate is identified as an essential operational and commercial requirement throughout the life of mine.

| 1.11 | Infrastructure |

KCM’s integrated operations span three principal sites connected by established road infrastructure across the Copperbelt Province. Run-of-mine ore from the Konkola Mine at Chililabombwe is processed through the on-site Konkola Concentrator. Copper concentrate is transported approximately 20 km by road to the Nchanga Flash Smelter at Chingola, with blister copper then transported approximately 55 km to the Nkana Refinery at Kitwe for electrorefining to LME Grade A cathode. All inter-site routes utilise high-quality tarmac roads capable of supporting loads up to 50 tonnes.

Power is supplied under a long-term agreement with CEC, providing 200 MW capacity to all KCM sites. This agreement has been in place for over 20 years. Water supply for processing operations is sourced primarily from the Kafue River system and from dewatering operations at the Konkola Mine, which pumps approximately 350,000 m³/day. The Konkola Mine operates a comprehensive staged dewatering system including pumping stations, sumps, and water management infrastructure critical to maintaining mine access and safety.

Export logistics for refined copper cathode rely on road freight to rail transfer points and onward transport to regional ports, including Dar-es-Salaam (Tanzania), Walvis Bay (Namibia), and Durban (South Africa). Further details on infrastructure and logistics are provided in Sections 4 and 15.

| 1.12 | Economic analysis summary |

The before-tax economic analysis is based on the Mineral Reserve mine plan only. The economic model incorporates the operating cost, capital cost, and pricing inputs described in this report. Revenue assumptions are:

| · | Copper Price: P75 consensus pricing as per Table 19.2 (ranging from US$11,101/t to US$12,793/t over the Mineral Reserve production period). |

| · | Cobalt Price: P50 consensus pricing (ranging from US$42,262/t to US$52,465/t over the Mineral Reserve production period). |

| · | Discount Rate: 8% real, pre-tax. |

Capital expenditure for the Mineral Reserve mine plan totals US$1,238M, comprising growth capital, capitalised mining development, and sustaining capital. A summary by category is presented in Table 1.4.

amcconsultants.com | 22 |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

| Table 1.4 | Capital cost summary – Mineral Reserve case |

| Capital category | Amount (US$M) | % of Total | ||

| Growth Capital | 208 | 16.6 | ||

| 1390 mL Pump Chamber (Konkola) | 55 | 4.4 | ||

| Tramming Upgrade Phase 2 (875 mL) (Konkola) | 22 | 1.7 | ||

| Concentrator Stream 2 Refurbishment (Konkola) | 3.6 | 0.3 | ||

| Permanent Cathodes (TLP) | 20 | 1.6 | ||

| Other growth projects (incl. EPCM & contingency) | 109 | 8.7 | ||

| Capitalised Mining Development (Sub-total) | 569 | 45.3 | ||

| Lateral Development | 505 | 40.2 | ||

| Vertical Development | 64 | 5.1 | ||

| Sustaining Capital (Sub-total) | 461 | 36.7 | ||

| KCM Underground Sustaining | 302 | 24.1 | ||

| Nchanga Smelter Sustaining | 142 | 11.3 | ||

| Other sustaining (TLP) | 17 | 1.4 | ||

| Total Capital | 1,238 | 100 | ||

| Closure Costs (additional) | 133 | - |

Note: All values in US$M. Capital cost estimates are at PFS accuracy level (±25%) with contingency of 10–15%. Totals may not sum due to rounding. Refer to Section 18 for detail.

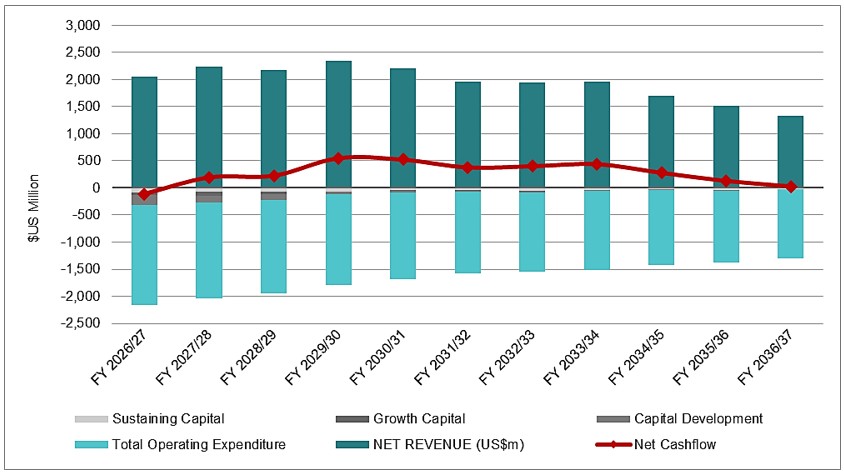

Growth capital of US$208MM comprises investments to support planned production rates, with the largest single item being the 1390 mL Pump Chamber (US$55M) for primary dewatering infrastructure. Capitalised mining development of US$569M reflects the underground lateral and vertical development required to access Mineral Reserves at the Konkola Mine. Approximately 60% of life-of-mine capital expenditure (US$742M of US$1,238M) is scheduled in the first three years (fiscal years 2027 through 2029), reflecting the front-loaded nature of the dewatering, shaft, and lateral development program. Sustaining capital of US$461M covers ongoing equipment replacement and infrastructure maintenance across both the KCM underground operations and the Nchanga Smelter and Refinery.

Life-of-mine operating costs total US$4,816, comprising KCM underground mining, Nchanga TLP tailings reclamation, and Nchanga Smelter and refinery operations, and excluding royalties. A summary by operational unit is presented in Table 1.5.

| Table 1.5 | Operating cost summary – Mineral Reserve case |

| Operating Cost Category | LOM Total (US$M) | Unit Cost | Unit | |||

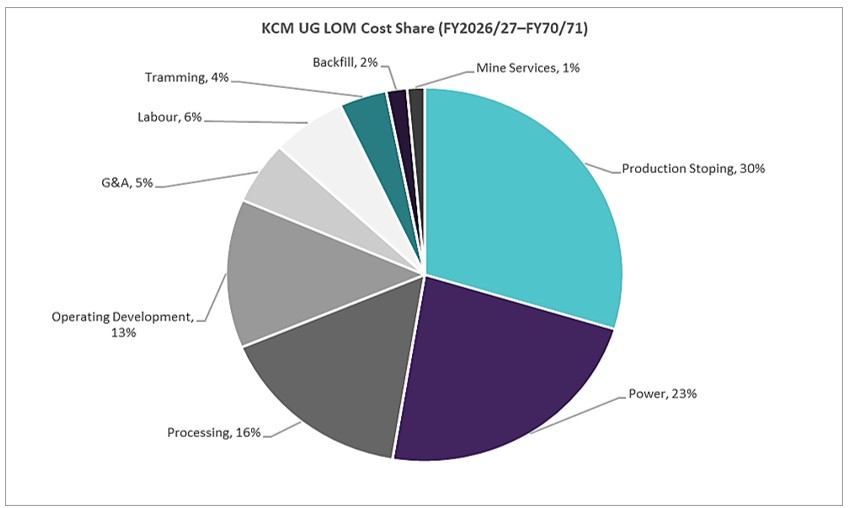

| Konkola Underground Mining (Mining + G&A) | 3,639 | 125 | US$/t ore | |||

| Nchanga Business Unit (NBU) | 11 | N/A | ||||

| Nchanga TLP Operations | 519 | 15 | US$/t ore | |||

| Subtotal — Mining Operating Costs | 4,169 | - | - | |||

| Smelter & Refinery Operating Costs | 1,376 | - | - | |||

| Smelter & Refinery Credits | (729) | - | - | |||

| Total Operating Costs | 4,816 | - | - | |||

| C1 Cash Cost1 | 4,415 | 2.46 | US$/lb Cu | |||

| All-in Sustaining Cost (AISC)1 | 5,583 | 3.11 | US$/lb Cu |

Note: 1 C1 and AISC are non-GAAP measures. C1 Cash Cost includes all direct mining, processing, and site G&A costs, net of by-product credits. AISC includes C1 plus sustaining capital, and royalties. Full definitions and reconciliation provided in Section 18. Refer to Section 18 for annual cost profiles.

KCM underground mining costs of US$3,639M (US$125/t ore average) include operating development, stoping, power, dewatering, backfill, and mine services. Nchanga TLP operating costs of US$519M, equivalent to approximately US$15/t of total TLP mill throughput, cover tailings reclamation, leach circuit processing, and site administration. Smelter and refinery operating costs of US$1376M include the Nchanga Smelter, sulfuric acid plant, and Nkana Refinery.

amcconsultants.com | 23 |

S-K 1300 TRS: KCM Integrated Operations (PFS) Konkola Copper Mines Plc | 0424076 |

The Mineral Reserve case economic results are summarised in Table 1.6.

| Table 1.6 | Summarised economic results |

| Item | Unit | Value | ||

| Production | ||||

| Konkola Ore Mined | kt | 29,066 | ||

| Konkola Underground Head Grade | %TCu | 2.89 | ||

| Konkola Underground Recovery | % | 89.2 | ||

| Nchanga TLP Ore Mined | kt | 24,522 | ||

| Nchanga TLP Head Grade | %TCu | 0.64 | ||

| Nchanga TLP Recovery (Total Cu Recovery) | % | 48.50 | ||

| Total Integrated Copper Production(1) | kt | 814 | ||

| Mine Life | years | ~11 | ||

| Economic Metrics | ||||

| Net Revenue | US$M | 9,914 | ||

| Total Operating Costs(2) | US$M | 4,816 | ||

| Total Capital Expenditure | US$M | 1,238 | ||

| C1 Cash Cost(3) | US$/lb Cu | 2.46 | ||