Exhibit 99.2

All amounts are in Canadian dollars and are based on financial statements presented in compliance with International Accounting Standard 34 , unless otherwise noted. Our Q2 2026 Report to Shareholders is available at rbc.com/investorrelations, sedarplus.com and sec.gov and our Q2 2026 Supplementary Financial Information is available at rbc.com/investorrelations.

Interim Financial Reporting

Net income $5.5 billion Up 25% YoY Down 5% QoQ |

Diluted EPS 1 $3.85 Up 27% YoY Down 4% QoQ |

ROE 1, 2 17.2% Up 300 bps 1 YoYDown 40 bps QoQ |

Total PCL 1 $0.9 billion PCL on loans ratio 1 down 6 bps QoQ |

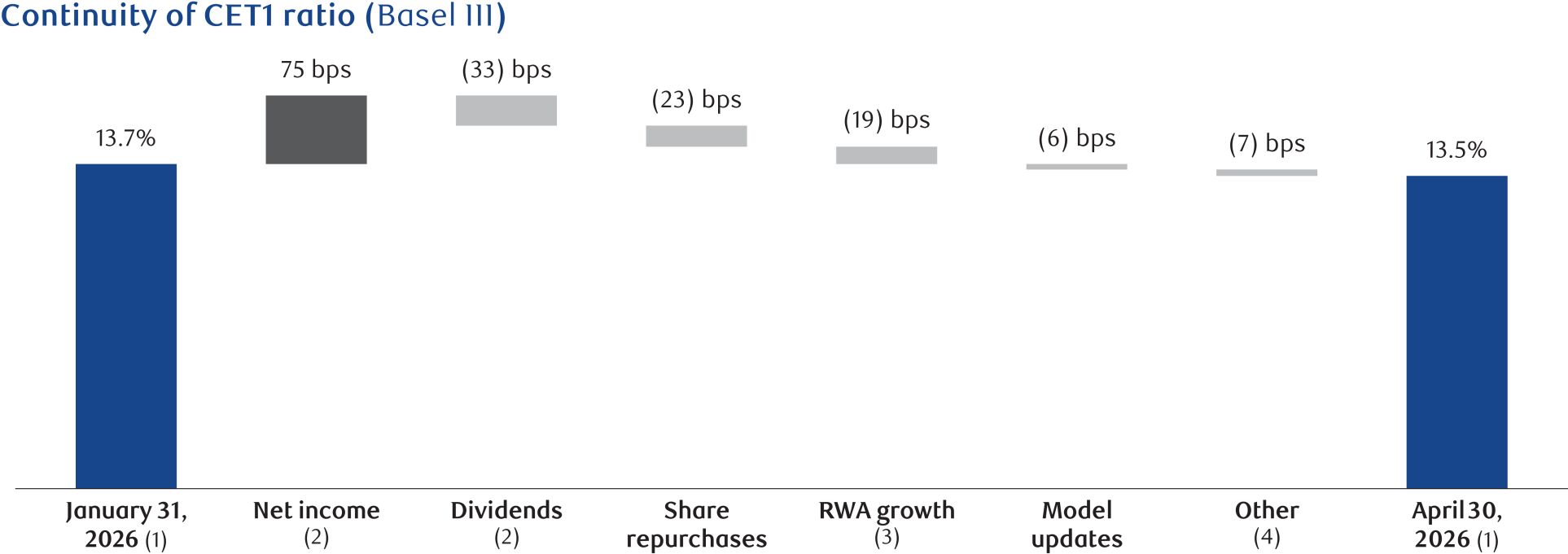

CET1 ratio 1 13.5% Above regulatory requirements and down 20 bps QoQ | ||||

Adjusted net income 3 $5.6 billion Up 23% YoY Down 5% QoQ |

Adjusted diluted EPS 3 $3.90 Up 25% YoY Down 4% QoQ |

Adjusted ROE 3 17.4% Up 270 bps YoY Down 40 bps QoQ |

Total ACL 1 $7.8 billion ACL on loans ratio 1 down 1 bp QoQ |

LCR 1 126% Up from 124% last quarter | ||||

TORONTO, May

28, 2026

4

(RY on TSX and NYSE) today reported net income of $5.5 billion for the quarter ended April 30, 2026, up $1,119 million or 25% from the prior year. Diluted EPS was $3.85, up 27% over the same period, reflecting growth across each of our business segments. Adjusted net income3

and adjusted diluted EPS3

of $5.6 billion and $3.90 were up 23% and 25%, respectively, from the prior year. “In a world that’s constantly changing and becoming more complex, our commitment to delivering trusted advice and helping clients navigate risk continues to produce exceptional outcomes. Our second quarter earnings showcase our consistency in delivering premium profitability and long-term shareholder value, underpinned by solid growth across our diversified businesses and balance sheet strength. Looking ahead, we remain focused on building the bank of the future and evolving with the needs of those we serve.” – Dave McKay, President and Chief Executive Officer of Royal Bank of Canada | ||

Pre-provision,

pre-tax

earnings5

of $8.0 billion were up $1.1 billion or 15% from last year, mainly due to higher revenue in Capital Markets, driven by strength across Global Markets and Corporate & Investment Banking, and higher fee-based revenue in Wealth Management, reflecting market appreciation and net sales. Higher net interest income in Personal Banking and Commercial Banking, reflecting average volume growth and higher spreads, also contributed to the increase. These factors were partially offset by higher compensation commensurate with increased results. Our consolidated results reflect a decrease in total PCL of $512 million from a year ago, primarily due to lower provisions in Commercial Banking and Personal Banking. The PCL on loans ratio of 35 bps decreased 23 bps from the prior year. The PCL on impaired loans ratio

1

of 34 bps decreased 1 bp, while the PCL on performing loans ratio1

of 1 bp decreased 22 bps, as the same quarter last year reflected higher provisions primarily due to the impacts of trade disruptions (including tariffs). Income before income taxes of $7.1 billion was up $1.6 billion or 29% from last year. Compared to last quarter, net income was down 5% reflecting lower results in Wealth Management, Personal Banking and Commercial Banking, which includes the impact of three fewer days in the current quarter, and in Corporate Support, partly offset by higher results in Capital Markets and Insurance. Adjusted net income

3

was down 5% over the same period. Pre-provision,

pre-tax

earnings5

were down $0.5 billion or 6% on lower revenues and flat expenses. The PCL on loans ratio of 35 bps decreased 6 bps from the prior quarter. The PCL on impaired loans ratio was 34 bps, down 6 bps from the prior quarter, primarily due to lower provisions in Capital Markets, and in Personal Banking and Commercial Banking to a lesser extent, while the PCL on performing loans ratio was 1 bp, remaining flat from the prior quarter. Our capital position remains robust, with a CET1 ratio of 13.5%, supporting solid volume growth and $4.0 billion of capital returned to our shareholders, including $1.7 billion of share buybacks and $2.3 billion of common share dividends.

Today, we declared a quarterly dividend of $1.76 per share reflecting an increase of $0.12 or 7%. We also announced our intention, subject to the approval of the Toronto Stock Exchange and the Office of the Superintendent of Financial Institutions, to commence a normal course issuer bid and to repurchase for cancellation up to 45 million of our common shares, representing approximately 3% of the bank’s outstanding common shares as at May 15, 2026.