This document is important and requires your immediate attention. Inquiries concerning the information in this document should be directed to Laurel Hill Advisory Group, the strategic shareholder advisor and information agent retained by Pacific Booker, by calling 1-877-452-7184 (toll-free in North America) or 1-416-304-0211 (collect calls outside North America), by texting "INFO" to either number, or by email at assistance@laurelhill.com. |

DIRECTORS' CIRCULAR |

RECOMMENDING |

REJECTION |

(NO ACTION NEEDED BY SHAREHOLDERS) |

of American Eagle Gold Corp.'s unsolicited offer |

to purchase all of the Common Shares of |

PACIFIC BOOKER MINERALS INC. |

for consideration per Common Share of 1.41 common shares of American Eagle Gold Corp. |

The Pacific Booker Board, based on the unanimous recommendation of the Special Committee comprised of independent directors, and after receiving advice from its financial and legal advisors, has unanimously concluded that the Hostile Bid is inadequate, does not reflect full and fair value for the Common Shares and is not in the best interests of Pacific Booker or its Shareholders and recommends that you Shareholders are encouraged to visit our website for up-to-date information relating to the Hostile Bid at www.pacificbooker.com or contact Laurel Hill Advisory Group, by calling 1-877-452-7184 (toll-free in North America) or 1-416-304-0211 (collect calls outside North America), by texting "INFO" to either number, or by email at assistance@laurelhill.com. |

|

|

|

|

|

|

| ii |

|

The Pacific Booker Board recommends that Shareholders NOT TAKE ANY ACTION to ensure that Shareholders are able to consider all of the options available to them. |

If you have already tendered your Common Shares to the Hostile Bid, you can withdraw your Common Shares by contacting your broker or Laurel Hill Advisory Group, by calling 1-877-452-7184 (toll-free in North America) or 1-416-304-0211 (collect calls outside North America), by texting "INFO" to either number, or by email at assistance@laurelhill.com. To keep current with and obtain information about the Hostile Bid, please visit www.pacificbooker.com.

|

April 29, 2026 |

|

|

|

|

|

|

| iii |

|

April 29, 2026 |

Dear Shareholder, |

Pacific Booker owns a great asset with tremendous value potential. In an effort to take control of this asset, American Eagle Gold Corp. (the "Offeror" or "American Eagle") has commenced an opportunistic hostile take-over bid (the "Hostile Bid") to acquire all of the common shares (the "Common Shares") of Pacific Booker Minerals Inc. ("Pacific Booker" or the "Company" or "we" or "our"). This asset rightfully belongs to you, our shareholders, and not to an outside buyer attempting to purchase the Company below its fair value. |

After careful consideration, and with the advice of external financial and legal advisors, and having received the unanimous recommendation of the Special Committee (the "Special Committee") comprised of independent directors of the board of directors (the "Board" or "Pacific Booker Board") of the Company, the Board believes that the Hostile Bid is inadequate and unanimously recommends that you REJECT the Hostile Bid and NOT TENDER your Common Shares. |

To reject the Hostile Bid, shareholders simply do not need to do anything – TAKE NO ACTION. |

The Board has established the Special Committee, chaired by Jonathan McCullough and including Gregory Anderson, each of whom are independent directors, to oversee Pacific Booker's response to the Hostile Bid and make recommendations in respect thereof. As the Special Committee evaluates alternatives to maximize shareholder value, we believe a superior offer or alternatives may emerge prior to the scheduled expiry of the Hostile Bid, which is not until 5:00 p.m. (Toronto time) on July 29, 2026. |

By any measure, Pacific Booker's Morrison Project is worth substantially more than the consideration offered under the Hostile Bid. We urge you to carefully read the attached directors' circular (the "Directors' Circular"), which provides background to the Hostile Bid and outlines compelling reasons to REJECT it. |

Quite simply, American Eagle is offering to buy your shares at a price well below what they are worth. The Morrison Project is a large-scale copper-gold-molybdenum deposit in a Tier-1 jurisdiction (British Columbia) with mineral resources of over two billion pounds of copper and over two million ounces of gold supported by a completed Technical Report. The Hostile Bid values the Morrison Project at approximately US$0.01 per pound of copper in resources, which is the low end of the peer group range between US$0.02 and US$0.05 per pound (or as much as an 80% discount) and well below the comparable precedent transactions ranging between US$0.04 per pound and US$0.09 per pound (or as much as an 89% discount).1 American Eagle is opportunistically attempting to acquire this asset at distressed pricing before the Company has had the opportunity to re-engage with First Nations stakeholders, reset the permitting pathway, or conduct a competitive strategic process. Our view is that tendering your Common Shares at the low price offered by American Eagle would deprive you of significant upside potential in your investment by crystallizing value before the Company has had a chance to remedy the above items. |

|

|

1 Refer to Appendix "C" of the Directors' Circular for the Company's mineral resource estimate, derived from the Technical Report. | |

|

|

|

|

|

|

| iv |

|

Significant standalone and strategic value |

Your decision comes down to whether you believe that the Morrison Project is worth more than the implied consideration being offered by American Eagle, or alternatively, that 1.41 common shares of American Eagle per Common Share (representing an implied offer price of $1.551 based on the closing price of American Eagle's common shares on the TSXV on April 28, 2026) reflects full value for the Company. The market clearly does not see the Hostile Bid's value as adequate, as Pacific Booker's shares have closed above the Hostile Bid's value each day since announcement, and traded at prices representing more than double the implied consideration. |

The Board and its advisors believe that the Morrison Project is a restart-able, permitted-scale copper asset with significant optionality value under current and projected copper price environments. The Morrison Project is not a "stranded" project, as American Eagle has characterized it. |

The share consideration offered under the Hostile Bid exposes our shareholders to a company with inferior assets. The consideration offered under the Hostile Bid is comprised entirely of shares of American Eagle, a pre-revenue, exploration-stage company. American Eagle has no mineral resource or reserve estimates at its NAK project, no history of mineral production, negative operating cash flow, and is dependent on third-party financing. American Eagle reported a net loss of approximately $7.3 million for the nine months ended September 30, 2025. There is significant risk to Pacific Booker shareholders in accepting American Eagle shares, since there is insufficient drilling to determine the ultimate average grade and continuity of the mineralization at the NAK project. Assuming American Eagle would be valued at the peer group average valuation, it would need to produce a mineral resource estimate of approximately the same size as Morrison in order to justify its current market value, which is a highly uncertain outcome. |

Moreover, American Eagle opted to make the Hostile Bid and file the American Eagle Circular mere days before its audited annual financial statements were due to be filed, compromising the ability of Shareholders to properly value the Offeror Common Shares and leaving Shareholders with nearly seven month old financial information which may no longer accurately reflect the Offeror's financial state. |

Board actively pursuing strategic alternatives |

The Pacific Booker Board, on the recommendation of the Special Committee and with the assistance of its financial and legal advisors, is actively evaluating strategic alternatives designed to maximize value for all our shareholders, including both seeking to engage with third parties on potential alternative transactions that would offer fair value to shareholders and also exploring standalone scenarios. |

Undervalued compared to peers and comparable transactions |

The Hostile Bid values Pacific Booker at approximately US$0.01 per pound of copper in resources, which is in the low-end valuation range of between US$0.02 per pound and US$0.05 per pound for comparable |

|

|

|

|

|

|

| v |

|

|

|

2 Refer to Appendix "C" of the Directors' Circular for the Company's mineral resource estimate, derived from the Technical Report.. | |

|

|

|

|

|

|

| vi |

|

On behalf of the Board, the Special Committee and management of Pacific Booker, we would like to thank you for your consideration and your support. | ||

Signed | ||

|

"Jonathan McCullough" Chair of the Special Committee | John Plourde "John Plourde" Director, President & CEO | |

The Pacific Booker Board has unanimously concluded that the Hostile Bid does not reflect Pacific Booker's full and fair value, and recommends that you: |

If you have already tendered your Common Shares to the Hostile Bid, you can WITHDRAW your Common Shares by contacting your broker or Laurel Hill Advisory Group, by calling 1-877-452-7184 (toll-free in North America) or 1-416-304-0211 (collect calls outside North America), by texting "INFO" to either number, or by email at assistance@laurelhill.com.. To keep current with and obtain information about the Hostile Bid, please visit www.pacificbooker.com. |

|

|

|

|

|

|

| vii |

|

The information set out below is a summary only and is qualified in its entirety by the more detailed information appearing elsewhere in this Directors' Circular. This Directors' Circular should be read carefully and in its entirety as it provides important information regarding Pacific Booker and the Hostile Bid. Capitalized terms used but not defined in this summary have the meanings ascribed to them in the Glossary attached as Appendix "B" to this Directors' Circular or elsewhere in this Directors' Circular. |

Unanimous Recommendation of the Pacific Booker Board: | The Pacific Booker Board, based on the unanimous recommendation of the Special Committee comprised entirely of independent directors, and after receiving advice from its financial and legal advisors, has unanimously concluded that the Hostile Bid is inadequate, does not reflect full and fair value for the Common Shares and is not in the best interests of Pacific Booker or its Shareholders. Accordingly, for the reasons described in more detail below, the Pacific Booker Board UNANIMOUSLY recommends that you REJECT the Hostile Bid and NOT TENDER your Common Shares to the Hostile Bid. |

The Pacific Booker Board and the Special Committee carefully reviewed and evaluated, together with their external financial and legal advisors and with the benefit of their advice, the Hostile Bid. The following is a summary of the principal reasons for the UNANIMOUS recommendations of the Special Committee and of the Pacific Booker Board that you REJECT the Hostile Bid and NOT TENDER your Common Shares to the Hostile Bid. The Pacific Booker Board believes that: ·the Hostile Bid is highly opportunistic bid that does not reflect Pacific Booker's full and fair value; othe Hostile Bid values the Morrison Project at approximately US$0.01 per pound of copper in resources, the low end of the valuation range of the peer group average of between US$0.02 per pound and US$0.05 per pound (or as much as an 80% discount) and well below precedent transactions of between US$0.04 per pound and US$0.09 per pound (or as much as an 89% discount); 3 ·the market views the Hostile Bid as inadequate; othe Common Shares have traded significantly above the Hostile Bid price every day since the Hostile Bid was launched, and traded at prices representing more than double the implied consideration; ·the Hostile Bid is financially inadequate;

|

|

|

3 Refer to Appendix "C" of the Directors' Circular for the Company's mineral resource estimate, derived from the Technical Report. | |

|

|

| |

|

|

| |

| viii |

| |

|

|

| |

oRCI Capital has delivered an opinion that the consideration offered to Shareholders (other than American Eagle and its affiliates) under the Hostile Bid is inadequate, from a financial point of view, to such Shareholders; othe value of the Hostile Bid is inadequate compared to the estimated $43 million that has been expended on Morrison, and the extensive documentation tabled in support of the mine development permit; ·Pacific Booker has a technical report on the Morrison Project with a published mineral resource estimate; American Eagle does not have any published mineral resources or mineral reserves; ·the standalone case has strong upside potential for Shareholders and superior offers or other alternatives have the potential to emerge as the Special Committee considers all alternatives to maximize shareholder value; and ·the Hostile Bid is highly conditional. See "Reasons for Rejecting the Hostile Bid". | |||

The Hostile Bid: | The Offeror has offered to purchase all of the outstanding Common Shares, including any Common Shares that may become issued and outstanding after the date of the Hostile Bid but before the Expiry Time, on the basis of 1.41 Offeror Common Shares per Common Share. As the Hostile Bid is open for acceptance until 5:00 p.m. (Toronto time) on July 29, 2026, there is no need for Shareholders to take any action with respect to the Hostile Bid. Shareholders who have tendered Common Shares to the Hostile Bid and who wish to obtain advice or assistance in withdrawing their Common Shares are urged to contact their broker or Laurel Hill Advisory Group, the strategic shareholder advisor and information agent retained by |

|

|

|

|

|

|

| ix |

|

Pacific Booker, by North American toll free phone at 1-877-452-7184, collect calls outside North America at 1-416-304-0211, or by email at assistance@laurelhill.com. | |

Rejection of the Hostile Bid by Directors and Officers: | The directors and officers of Pacific Booker have indicated their intention to REJECT the Hostile Bid and NOT TENDER their Common Shares to the Hostile Bid. |

|

|

|

|

|

|

| xi |

|

|

|

|

|

|

|

xii |

|

|

| |

|

|

|

| xiii |

|

|

|

|

|

|

|

| xiv |

|

|

|

|

|

| |

| xv |

|

TABLE OF CONTENTS

| SUMMARY | vii |

|

|

|

| QUESTIONS AND ANSWERS ABOUT THE HOSTILE BID | x |

|

|

|

| ABOUT PACIFIC BOOKER | 1 |

|

|

|

| GENERAL INFORMATION | 1 |

|

|

|

| CAUTIONARY STATEMENT ON FORWARD-LOOKING STATEMENTS | 2 |

|

|

|

| SCIENTIFIC AND TECHNICAL DISCLOSURE | 6 |

|

|

|

| NOTICE TO NON-CANADIAN SHAREHOLDERS | 6 |

|

|

|

| AVAILABILITY OF DISCLOSURE DOCUMENTS | 7 |

|

|

|

| INFORMATION REGARDING AMERICAN EAGLE | 7 |

|

|

|

| MARKET DATA | 7 |

|

|

|

| DIRECTORS' CIRCULAR | 8 |

|

|

|

| DIRECTORS' RECOMMENDATION | 14 |

|

|

|

| REASONS FOR REJECTING THE HOSTILE BID | 15 |

|

|

|

| CONCLUSION AND RECOMMENDATION | 18 |

|

|

|

| REJECTION OF THE HOSTILE BID | 18 |

|

|

|

| OPINION OF THE FINANCIAL ADVISOR | 19 |

|

|

|

| BACKGROUND TO THE HOSTILE BID AND RESPONSE OF PACIFIC BOOKER | 20 |

|

|

|

| ALTERNATIVES TO THE HOSTILE BID | 22 |

|

|

|

| HOW TO WITHDRAW YOUR DEPOSITED COMMON SHARES | 23 |

|

|

|

| PACIFIC BOOKER SHARES | 23 |

|

|

|

| OWNERSHIP OF SECURITIES OF PACIFIC BOOKER | 24 |

|

|

|

| PRINCIPAL HOLDERS OF COMMON SHARES OF PACIFIC BOOKER | 25 |

|

|

|

| INTENTION OF DIRECTORS, OFFICERS AND OTHER SHAREHOLDERS WITH RESPECT TO THE HOSTILE BID |

25 |

|

| |

| TRADING IN SECURITIES OF PACIFIC BOOKER | 25 |

|

|

|

| ISSUANCES OF SECURITIES OF PACIFIC BOOKER | 25 |

|

|

|

| ARRANGEMENTS BETWEEN THE OFFEROR AND THE DIRECTORS, OFFICERS AND SECURITYHOLDERS OF PACIFIC BOOKER |

26 |

|

|

|

| ARRANGEMENTS BETWEEN PACIFIC BOOKER AND ITS DIRECTORS AND OFFICERS |

26 |

|

|

|

| OWNERSHIP OF SECURITIES OF THE OFFEROR | 27 |

|

|

|

| INTERESTS OF DIRECTORS AND OFFICERS IN MATERIAL TRANSACTIONS WITH THE OFFEROR |

27 |

|

|

|

| MATERIAL CHANGES IN THE AFFAIRS OF PACIFIC BOOKER | 27 |

|

|

|

| OTHER TRANSACTIONS | 27 |

|

|

|

| OTHER MATERIAL INFORMATION | 28 |

|

|

|

|

|

|

| xvi |

|

| OTHER PERSONS RETAINED IN CONNECTION WITH THE HOSTILE BID | 28 |

|

|

|

| STATUTORY RIGHTS | 28 |

|

|

|

| APPROVAL OF DIRECTORS' CIRCULAR | 28 |

|

|

|

| CONSENT OF RCI CAPITAL GROUP INC. | 29 |

|

|

|

| CERTIFICATE | 30 |

|

|

|

| APPENDIX "A" OPINION OF RCI CAPITAL GROUP INC. | A-1 |

|

|

|

| APPENDIX "B" GLOSSARY | B-1 |

|

|

|

| APPENDIX "C" MINERAL RESOURCES | C-1 |

|

|

|

|

|

|

| 1 |

|

|

|

|

|

|

|

| 2 |

|

|

|

|

|

|

|

| 3 |

|

|

|

|

|

|

|

| 4 |

|

|

|

|

|

|

|

| 5 |

|

|

|

|

|

|

|

| 6 |

|

|

|

|

|

|

|

| 7 |

|

|

|

|

|

|

|

| 8 |

|

|

|

|

|

|

|

| 9 |

|

(including the adoption or implementation of any shareholder rights plan, change in capital structure of the Company, issuance of any Common Shares or securities convertible into Common Shares, or taken any other action that provides rights to the Shareholders to purchase any securities of the Company as a result of the Hostile Bid or any Compulsory Acquisition or Subsequent Acquisition Transaction); (f)the Offeror shall have determined, in its reasonable judgment, that: (i)no inquiry, act, action, suit, demand, objection, opposition or proceeding shall have been threatened in writing, pending, taken or commenced by or before, and no judgment, decree or order shall have been issued by, any Governmental Entity or by any elected or appointed public official or private person (including, without limitation, any individual, corporation, firm, group or other entity) in Canada, the United States or elsewhere, whether or not having the force of Law; and (ii)no Law shall have been proposed, enacted, promulgated, amended or applied (including with respect to the interpretation or administration thereof), in either case: (A) to prevent or challenge the Hostile Bid or its validity or the Offeror's ability to make or maintain the Hostile Bid or consummate any Compulsory Acquisition or Subsequent Acquisition Transaction; (B) to cease trade, enjoin, prohibit or impose material limitations or conditions on or make materially more costly the making of the Hostile Bid, the purchase by or the sale to the Offeror of the Common Shares under the Hostile Bid, the issuance and delivery of the common shares of the Offeror for Common Shares taken up and paid for by the Offeror, the right of the Offeror to own or exercise full rights of ownership over the Common Shares, or the consummation of any Compulsory Acquisition or Subsequent Acquisition Transaction, or which could have any such effect; (C) which has had or could reasonably be expected to have a Material Adverse Effect or which could reasonably be expected to materially and adversely affect the value of the Common Shares; (D) which seeks to prohibit or limit the ownership or operation by the Offeror of any material portion of the business or assets of the Company or its subsidiaries or to compel the Offeror or any of its affiliates to dispose of or hold separate any material portion of the business, properties or assets of the Company or its subsidiaries; or (E) which may make uncertain the ability of the Offeror or its affiliates to consummate the Hostile Bid, a Compulsory Acquisition or a Subsequent Acquisition Transaction; |

|

|

|

|

|

|

| 10 |

|

|

|

|

|

|

|

| 11 |

|

|

|

|

|

|

|

| 12 |

|

|

|

|

|

|

|

| 13 |

|

Common Shares, pursuant to which the Offeror has determined that this Hostile Bid will be withdrawn and/or terminated; (l)the Offeror shall not have become aware of any untrue statement of material fact, or an omission to state a material fact that is required to be stated or that is necessary to make a statement not misleading in light of the circumstances in which it was made and at the date it was made (after giving effect to all subsequent filings prior to the date of the Hostile Bid in relation to all matters covered in earlier filings), in any document filed by or on behalf of the Company with any applicable securities commission or regulatory authority in each province and territory of Canada or a similar securities regulatory authority in the United States or elsewhere, which the Offeror shall have determined, in its reasonable judgment, when considered either individually or in the aggregate, has or could reasonably be expected to have a Material Adverse Effect; and (m)the Registration Statement having become effective under the U.S. Securities Act and not becoming subject to a stop order or a proceeding seeking a stop order. |

|

|

|

|

|

|

| 14 |

|

DIRECTORS' RECOMMENDATION After careful consideration by the Pacific Booker Board, in consultation with its external financial and legal advisors, of the terms and conditions of the Hostile Bid, the Pacific Booker Board, based on the unanimous recommendation of the Special Committee comprised of independent directors upon consultation with its own external financial and legal advisors, as well as the factors described in this Directors' Circular, has unanimously concluded that the Hostile Bid is inadequate, does not reflect full and fair value for the Common Shares and is not in the best interests of Pacific Booker or its Shareholders. |

If you have tendered your Common Shares, you can withdraw them. For assistance in withdrawing your Common Shares, you should contact your broker or the Company's strategic shareholder advisor and information agent, Laurel Hill Advisory Group (contact information immediately below). See "How to Withdraw Your Deposited Common Shares". To keep current with and obtain information about the Hostile Bid, please visit www.pacificbooker.com. |

|

|

|

|

|

|

| 15 |

|

|

|

4 Refer to Appendix "C" for the Company's mineral resource estimate, derived from the Technical Report. | |

|

|

|

|

|

|

| 16 |

|

|

|

|

|

|

|

| 17 |

|

|

|

|

|

|

|

18 |

|

Similarly, while American Eagle indicates it has the support of the Lake Babine Nation to pursue the Morrison Project and reset negotiations regarding Morrison, there is no certainty that this support will in fact materialize and translation to support for permitting with the British Columbia government. American Eagle does not have a management profile of development nor operating talent. Management is principally focused on exploration and a first mineral resource estimate; they have not demonstrated that they have the experience necessary to advance projects to development, let alone production, status. CONCLUSION AND RECOMMENDATION For the principal reasons outlined above, the Pacific Booker Board, based on the unanimous recommendation of the Special Committee comprised of independent directors, and after receiving advice from its financial and legal advisors, has unanimously concluded that the Hostile Bid is inadequate, does not reflect full and fair value for the Common Shares and is not in the best interests of Pacific Booker or its Shareholders. |

Accordingly, the Pacific Booker Board UNANIMOUSLY recommends that Shareholders REJECT the Hostile Bid and NOT TENDER their Common Shares. |

|

|

|

|

|

|

| 19 |

|

|

|

|

|

|

|

| 20 |

|

|

| |

|

|

|

| 21 |

|

|

|

|

|

|

|

| 22 |

|

|

|

|

|

|

|

| 23 |

|

|

|

|

|

|

|

| 24 |

|

Share Capital As at April 28, 2026, there were: (a) 16,816,969 Common Shares issued and outstanding; and (b) 3,363,000 Options issued and outstanding. The Company's authorized share capital consists of 100,000,000 Common Shares without par value. Description of Common Shares Holders of Common Shares are entitled to: (a) dividends if, as and when declared by the Pacific Booker Board, which may from time to time declare and authorize payment of such dividends as it may deem advisable; and (b) one vote per Common Share at meetings of Shareholders. OWNERSHIP OF SECURITIES OF PACIFIC BOOKER The following table sets out the names and positions of each director and officer of the Company and the number and percentage of Common Shares and Options beneficially owned, or over which control or direction is exercised, by each such person and, where known after reasonable enquiry, by each associate or affiliate of any insider of the Company, each associate or affiliate of the Company, any insider of the Company other than a director or officer of the Company and each person acting jointly or in concert with the Company as of April 28, 2026, unless stated otherwise. See also "Principal Holders of Common Shares of Pacific Booker". Securities Beneficially Owned or Controlled |

Name and Position(1)(2) | Number/Percentage | Number/Percentage of Options(4) |

John Plourde (CEO, President and Director) | 455,879 / 2.71% | 1,085,000 / 32.26% |

Ruth Swan (CFO) | 25,108 / 0.15% | 398,000 / 11.83% |

Gregory Anderson (Director) | 5,029 / 0.03% | 325,000 / 9.66% |

Victor Eng (Director) | 54,765 / 0.33% | 300,000 / 8.92% |

Jonathan McCullough (Director) | Nil | Nil(5) |

Dennis Simmons (Director) | 340,619 / 2.03% | 375,000 / 11.15% |

William Webster (Director) | 341,060 / 2.03% | 200,000 / 5.95% |

Notes: | |

(1) | The information as to securities beneficially owned, directly or indirectly, or over which control or direction is exercised, not being within the knowledge of the Company, has been furnished by the respective directors, officers and insiders or otherwise has been obtained from publicly available sources. |

(2) | In addition, as of April 28, 2026, the officers and directors as a group held an aggregate of 3,905,460 Common Shares and Options representing on a combined basis, 19.35% of the outstanding Common Shares assuming the exercise of all Options. |

(3) | As of April 28, 2026, there were 16,816,969 Common Shares issued and outstanding |

(4) | As of April 28, 2026, there were 3,363,000 Options issued and outstanding |

(5) | It is expected that Mr. McCullough will be granted 250,000 Options pursuant to the Option Plan and in accordance with the Company's director compensation practices. |

|

| |

|

|

|

| 25 |

|

PRINCIPAL HOLDERS OF COMMON SHARES OF PACIFIC BOOKER To the knowledge of the directors and officers of the Company, after reasonable enquiry, as at April 28, 2026, no person owned, directly or indirectly, or exercised control or direction over 10% or more of any class of voting securities of the Company. INTENTION OF DIRECTORS, OFFICERS AND OTHER SHAREHOLDERS WITH RESPECT TO THE HOSTILE BID To the knowledge of the directors and officers of Pacific Booker, after reasonable enquiry, as at April 29, 2026, none of the directors and officers of Pacific Booker, the associates or affiliates of any insider of Pacific Booker, the associates or affiliates of Pacific Booker, other insiders of Pacific Booker or any other person or company acting jointly or in concert with Pacific Booker have accepted or indicated their intention to accept the Hostile Bid. TRADING IN SECURITIES OF PACIFIC BOOKER During the six (6) month period preceding the date hereof, none of the Company, the directors, officers or other insiders of the Company nor, to the knowledge of the directors and officers of the Company, after reasonable enquiry, any associate or affiliate of an insider of the Company, any associate or affiliate of the Company or any person or company acting jointly or in concert with Company, has traded any Common Shares. ISSUANCES OF SECURITIES OF PACIFIC BOOKER Except as set out below, no Common Shares or securities convertible into Common Shares have been issued to the directors, officers and any other insiders of the Company during the two (2) years preceding the date of this Directors' Circular. |

Name | Date | Nature of Issuance | Number of Securities Issued | Issue/Exercise Price per Common Share |

John Plourde | November 12, 2024 | Grant of Options | 700,000 | C$3.00 |

November 13, 2025 | Grant of Options | 700,000 | C$3.00 | |

Ruth Swan | May 9, 2024 | Grant of Options | 168,000 | C$1.00 |

February 25, 2026 | Grant of Options | 100,000 | C$2.00 | |

Victor Eng | May 9, 2024 | Grant of Options | 200,000 | C$1.00 |

May 12, 2025 | Grant of Options | 200,000 | C$1.30 | |

May 9, 2024 | Grant of Options | 200,000 | C$1.00 | |

May 12, 2025 | Grant of Options | 200,000 | C$1.30 |

|

|

|

|

|

|

| 26 |

|

|

|

|

|

|

|

| 27 |

|

|

|

|

|

|

|

| 28 |

|

OTHER MATERIAL INFORMATION Except as otherwise described or referred to in this Directors' Circular, or which is otherwise publicly disclosed, no other information is known to the directors or officers of Pacific Booker that would reasonably be expected to affect the decision of the Shareholders to accept or reject the Hostile Bid. OTHER PERSONS RETAINED IN CONNECTION WITH THE HOSTILE BID In addition to the external legal advisor, Bennett Jones, as to Canadian law matters and RCI Capital as financial advisor, Pacific Booker has retained the persons described below in connection with the Hostile Bid. Pacific Booker has retained Laurel Hill Advisory Group as its strategic shareholder advisor and information agent in connection with the Hostile Bid and certain related matters. Laurel Hill Advisory Group will receive reasonable and customary compensation for its services and reimbursement for its reasonable out-of-pocket expenses. Pacific Booker has agreed to indemnify Laurel Hill Advisory Group against certain liabilities arising out of or in connection with the engagement. Inquiries concerning the information in this document should be directed to Laurel Hill Advisory Group, the strategic shareholder advisor and information agent retained by Pacific Booker, by North American toll free phone at 1-877-452-7184, local and text: 1-416-304-0211 or by email at assistance@laurelhill.com. To keep current with and obtain information about the Hostile Bid, please visit www.pacificbooker.com. Except as set forth above, neither Pacific Booker nor any person acting on its behalf has employed, retained or agreed to compensate any person making solicitations or recommendations to Shareholders in connection with the Hostile Bid. STATUTORY RIGHTS Securities legislation in the provinces and territories of Canada provides securityholders of Pacific Booker with, in addition to any other rights they may have at law, one or more rights of rescission, price revision or to damages, if there is a misrepresentation in a circular or notice that is required to be delivered to those securityholders. However, such rights must be exercised within prescribed time limits. Securityholders should refer to the applicable provisions of the securities legislation of their province or territory for particulars of those rights or consult a lawyer. APPROVAL OF DIRECTORS' CIRCULAR The content of this Directors' Circular has been approved and the delivery thereof has been authorized by the Pacific Booker Board. |

|

|

|

|

|

|

29 |

|

CONSENT OF RCI CAPITAL GROUP INC. TO: The Special Committee of the Board of Directors of Pacific Booker Minerals Inc. ("Pacific Booker") AND TO: The Board of Directors of Pacific Booker We hereby consent to the references to our firm name and to our opinion dated April 29, 2026, contained in, and the inclusion of the text of such opinion as Appendix "A" to, the directors' circular of Pacific Booker dated April 29, 2026. Our opinion was given as at April 29, 2026 and remains subject to the assumptions, qualifications and limitations contained therein. In providing our consent, we do not intend that any person other than the Special Committee of the Board of Directors of Pacific Booker and the Board of Directors of Pacific Booker shall be entitled to rely upon our opinion. (Signed) "RCI Capital Group Inc." Dated: April 29, 2026 |

|

|

|

|

|

|

| 30 |

|

CERTIFICATE Dated: April 29, 2026 The foregoing contains no untrue statement of a material fact and does not omit to state a material fact that is required to be stated or that is necessary to make a statement not misleading in the light of the circumstances in which it was made. On behalf of the Board of Directors of Pacific Booker Minerals Inc. |

(Signed) "Dennis Simmons" | (Signed) "Jonathan McCullough" |

|

|

|

|

|

|

| A-1 |

|

|

|

|

|

|

|

| A-2 |

|

|

| |

|

|

|

| A-3 |

|

|

|

|

|

|

|

| A-4 |

|

|

|

|

|

|

|

| A-5 |

|

is not necessarily susceptible to partial analysis or summary description. Any attempt to do so could lead to undue emphasis on any particular factor or analysis. The Opinion is not to be construed as a recommendation to any Shareholder as to whether to tender its Common Shares to the American Eagle Offer. Fairness Conclusion Based upon and subject to the foregoing, RCI is of the opinion that, as of the date hereof, the consideration under the American Eagle Offer is inadequate from a financial point of view to the Shareholders (other than American Eagle and its affiliates). Yours very truly, RCI Capital Group Inc. |

|

|

|

|

|

|

| B-1 |

|

|

|

|

|

|

|

| B-2 |

|

|

|

|

|

|

|

| B-3 |

|

|

|

|

|

|

|

| B-4 |

|

"Shareholder" means a holder of Common Shares; "Special Committee" means the special committee of independent directors established by the Pacific Booker Board to, among other things, review and assess the Hostile Bid and make recommendations in respect thereof, and consisting of Jonathan McCullough (Chair) and Gregory Anderson; "Subsequent Acquisition Transaction" has the meaning given to it under the heading "Questions and Answers About the Hostile Bid"; "subsidiary" has the meaning given to it under the Securities Act; "Technical Report" has the meaning given to it under the heading "Scientific and Technical Disclosure"; "TSXV" means the TSX Venture Exchange; and "U.S. Securities Act" means the United States Securities Act of 1933, as amended. |

|

|

|

|

|

|

| C-1 |

|

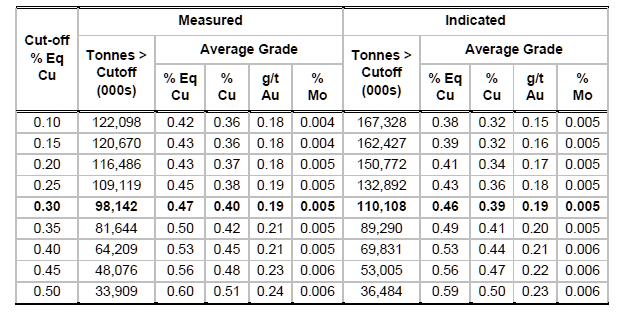

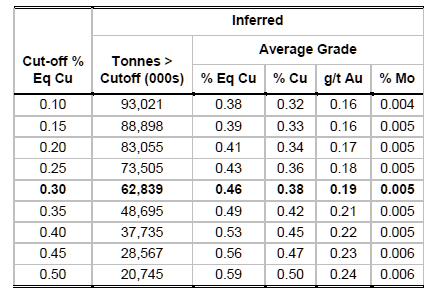

APPENDIX "C" The mineral resource estimate for the Morrison Project, as set forth in the Technical Report, is as follows: Measured and Indicated: |

|

Inferred: |

|

|

|

|

|

|

|

|

QUESTIONS MAY BE DIRECTED TO THE INFORMATION AGENT

North America Toll Free: 1-877-452-7184

Collect Calls Outside North America: 416-304-0211

Email: assistance@laurelhill.com |