| Project World [12 February 2026] Discussion Materials |

| Table of Contents 01 Asset Overview 02 02 Italy’s Historical Trading Performance 04 03 Overview of Proposed Transaction and Illustrative Pro Forma Impact 09 1 |

| Asset Overview 01 |

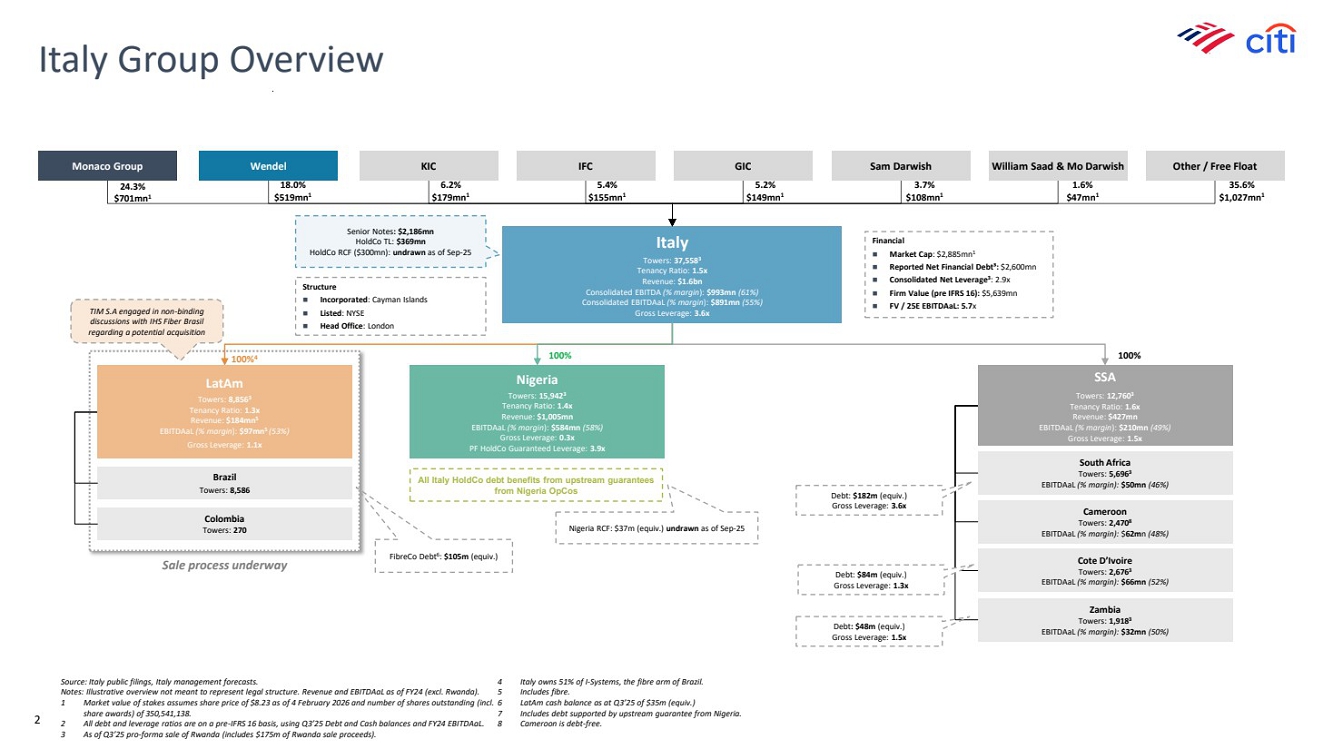

| Italy Group Overview Source: Italy public filings, Italy management forecasts. Notes: Illustrative overview not meant to represent legal structure. Revenue and EBITDAaL as of FY24 (excl. Rwanda). 1 Market value of stakes assumes share price of $8.23 as of 4 February 2026 and number of shares outstanding (incl. share awards) of 350,541,138. 2 All debt and leverage ratios are on a pre-IFRS 16 basis, using Q3’25 Debt and Cash balances and FY24 EBITDAaL. 3 As of Q3’25 pro-forma sale of Rwanda (includes $175m of Rwanda sale proceeds). 4 Italy owns 51% of I-Systems, the fibre arm of Brazil. 5 Includes fibre. 6 LatAm cash balance as at Q3’25 of $35m (equiv.) 7 Includes debt supported by upstream guarantee from Nigeria. 8 Cameroon is debt-free. Italy Towers: 37,5583 Tenancy Ratio: 1.5x Revenue: $1.6bn Consolidated EBITDA (% margin): $993mn (61%) Consolidated EBITDAaL (% margin): $891mn (55%) Gross Leverage: 3.6x Nigeria Towers: 15,9423 Tenancy Ratio: 1.4x Revenue: $1,005mn EBITDAaL (% margin): $584mn (58%) Gross Leverage: 0.3x PF HoldCo Guaranteed Leverage: 3.9x 100%4 100% 100% Structure ◼ Incorporated: Cayman Islands ◼ Listed: NYSE ◼ Head Office: London Financial ◼ Market Cap: $2,885mn1 ◼ Reported Net Financial Debt³: $2,600mn ◼ Consolidated Net Leverage3 : 2.9x ◼ Firm Value (pre IFRS 16): $5,639mn ◼ FV / 25E EBITDAaL: 5.7x Brazil Towers: 8,586 Colombia Towers: 270 LatAm Towers: 8,8563 Tenancy Ratio: 1.3x Revenue: $184mn5 EBITDAaL (% margin): $97mn5 (53%) Gross Leverage: 1.1x South Africa Towers: 5,6963 EBITDAaL (% margin): $50mn (46%) Cameroon Towers: 2,4708 EBITDAaL (% margin): $62mn (48%) Cote D’Ivoire Towers: 2,6763 EBITDAaL (% margin): $66mn (52%) Zambia Towers: 1,9183 EBITDAaL (% margin): $32mn (50%) SSA Towers: 12,7603 Tenancy Ratio: 1.6x Revenue: $427mn EBITDAaL (% margin): $210mn (49%) Gross Leverage: 1.5x Debt: $182m (equiv.) Gross Leverage: 3.6x Debt: $84m (equiv.) Gross Leverage: 1.3x Debt: $48m (equiv.) Gross Leverage: 1.5x FibreCo Debt6 : $105m (equiv.) Senior Notes: $2,186mn HoldCo TL: $369mn HoldCo RCF ($300mn): undrawn as of Sep-25 Nigeria RCF: $37m (equiv.) undrawn as of Sep-25 All Italy HoldCo debt benefits from upstream guarantees from Nigeria OpCos Wendel 18.0% $519mn1 Monaco Group 24.3% $701mn1 KIC 6.2% $179mn1 Other / Free Float 35.6% $1,027mn 1 GIC 5.2% $149mn1 Sam Darwish 3.7% $108mn1 William Saad & Mo Darwish 1.6% $47mn1 IFC 5.4% $155mn1 Sale process underway TIM S.A engaged in non-binding discussions with IHS Fiber Brasil regarding a potential acquisition 2 |

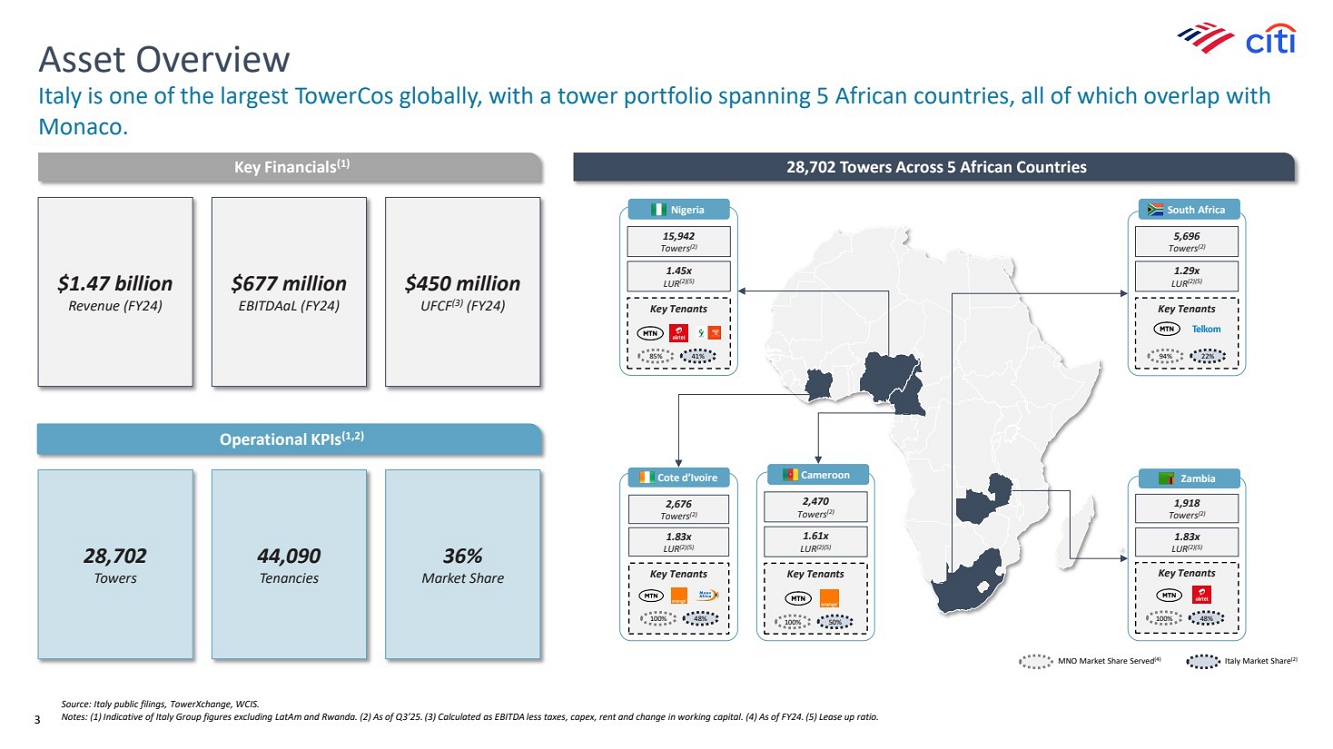

| 5,696 Towers(2) 1.29x LUR(2)(5) Key Tenants South Africa 94% 22% 15,942 Towers(2) 1.45x LUR(2)(5) Key Tenants Nigeria 85% 41% Asset Overview Italy is one of the largest TowerCos globally, with a tower portfolio spanning 5 African countries, all of which overlap with Monaco. Key Financials(1) $677 million EBITDAaL (FY24) $1.47 billion Revenue (FY24) 28,702 Towers Across 5 African Countries 36% Market Share 44,090 Tenancies 28,702 Towers Operational KPIs(1,2) Source: Italy public filings, TowerXchange, WCIS. Notes: (1) Indicative of Italy Group figures excluding LatAm and Rwanda. (2) As of Q3’25. (3) Calculated as EBITDA less taxes, capex, rent and change in working capital. (4) As of FY24. (5) Lease up ratio. MNO Market Share Served(4) Italy Market Share (2) 1,918 Towers(2) 1.83x LUR(2)(5) Key Tenants Zambia 100% 48% 2,676 Towers(2) 1.83x LUR(2)(5) Key Tenants Cote d’Ivoire 100% 48% 2,470 Towers(2) 1.61x LUR(2)(5) Key Tenants Cameroon 100% 50% $450 million UFCF(3) (FY24) 3 |

| 02 Italy’s Historical Trading Performance |

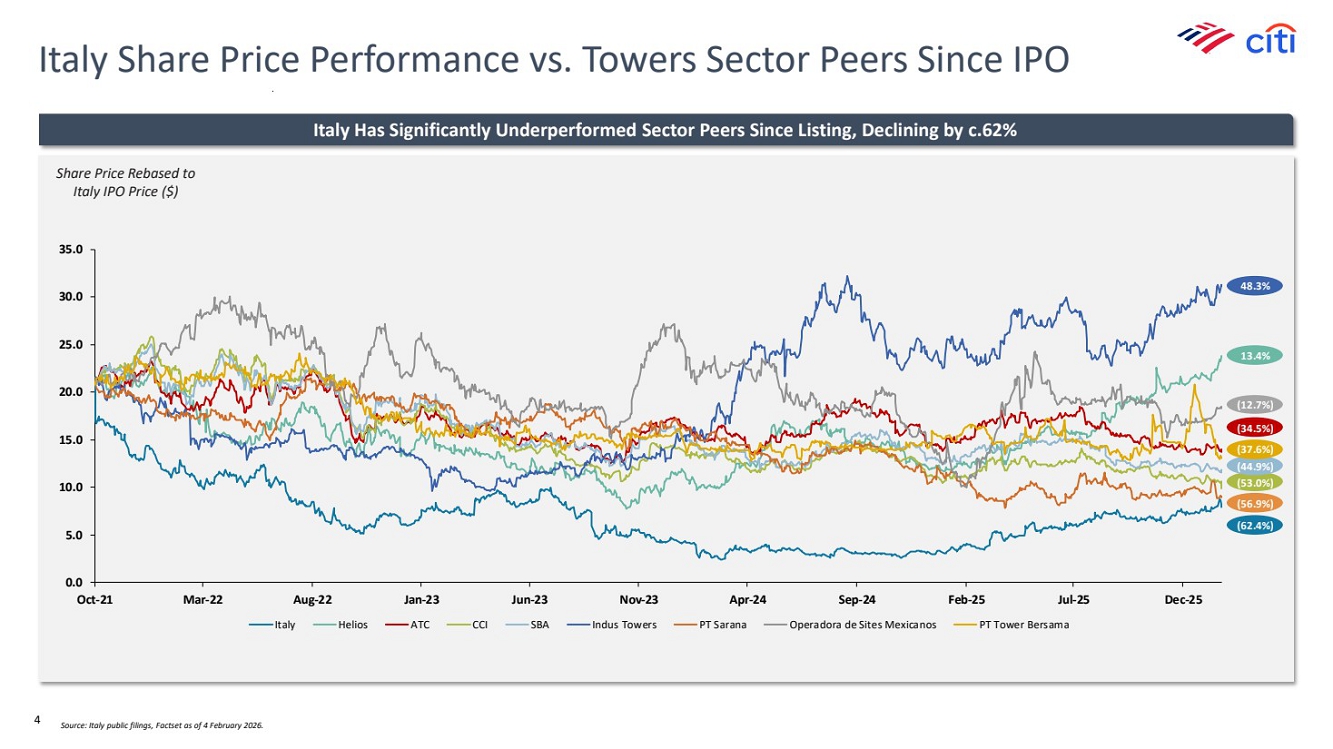

| 0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 Oct-21 Apr-22 Oct-22 Apr-23 Oct-23 Apr-24 Oct-24 Apr-25 Oct-25 Italy Helios ATC CCI SBA Indus Towers PT Sarana Operadora de Sites Mexicanos PT Tower Bersama (70.1%) (56.5%) (47.0%) (40.3%) (27.5%) (4.6%) 33.0% (29.9%) (32.0%) Italy Share Price Performance vs. Towers Sector Peers Since IPO Source: Italy public filings, Factset as of 4 February 2026. Italy Has Significantly Underperformed Sector Peers Since Listing, Declining by c.62% Share Price Rebased to Italy IPO Price ($) 0.0 5.0 10.0 15.0 20.0 25.0 30.0 35.0 Oct-21 Mar-22 Aug-22 Jan-23 Jun-23 Nov-23 Apr-24 Sep-24 Feb-25 Jul-25 Dec-25 Italy Helios ATC CCI SBA Indus Towers PT Sarana Operadora de Sites Mexicanos PT Tower Bersama (62.4%) (56.9%) (53.0%) (44.9%) (12.7%) 13.4% 48.3% (37.6%) (34.5%) 4 |

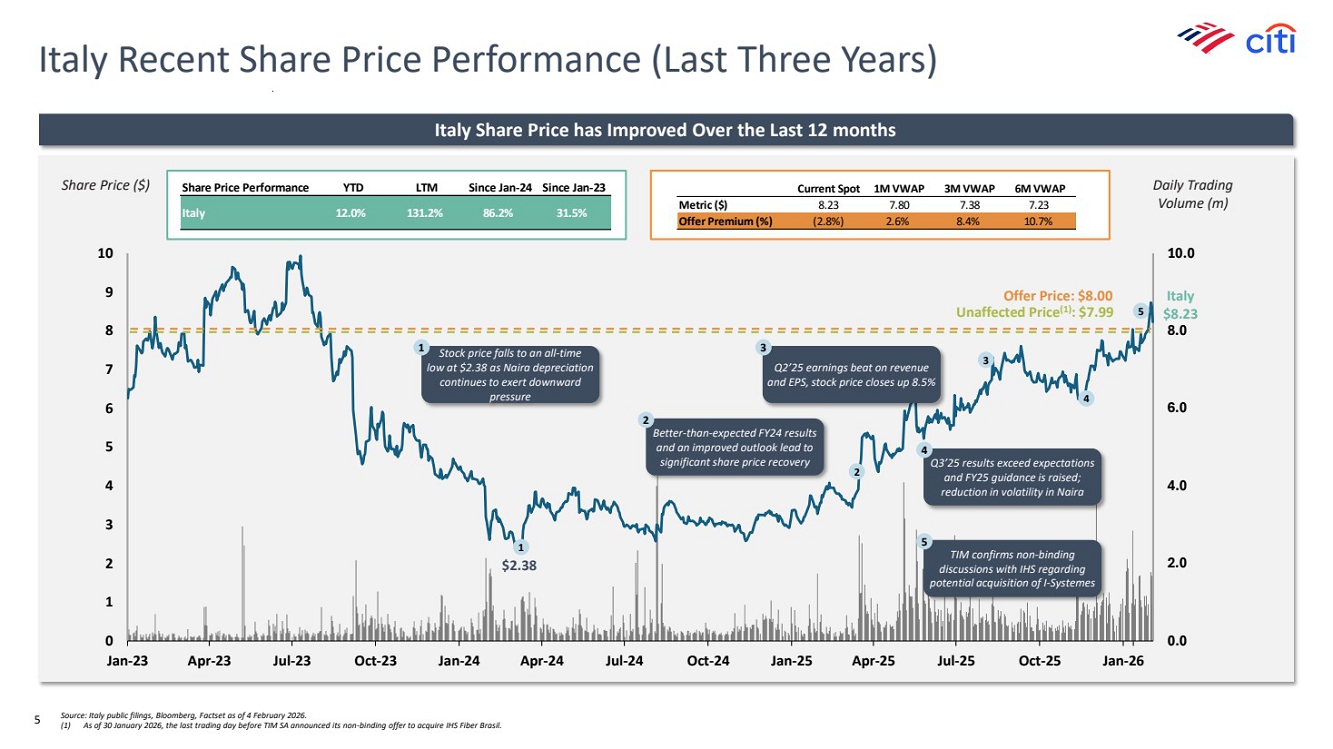

| 0.0 2.0 4.0 6.0 8.0 10.0 0 1 2 3 4 5 6 7 8 9 10 Jan-23 Apr-23 Jul-23 Oct-23 Jan-24 Apr-24 Jul-24 Oct-24 Jan-25 Apr-25 Jul-25 Oct-25 Jan-26 Italy Recent Share Price Performance (Last Three Years) Source: Italy public filings, Bloomberg, Factset as of 4 February 2026. (1) As of 30 January 2026, the last trading day before TIM SA announced its non-binding offer to acquire IHS Fiber Brasil. Share Price ($) Italy Share Price has Improved Over the Last 12 months Current Spot 1M VWAP 3M VWAP 6M VWAP Metric ($) 8.23 7.80 7.38 7.23 Offer Premium (%) (2.8%) 2.6% 8.4% 10.7% Daily Trading Volume (m) Offer Price: $8.00 $2.38 Stock price falls to an all-time low at $2.38 as Naira depreciation continues to exert downward pressure 1 Better-than-expected FY24 results and an improved outlook lead to significant share price recovery 2 Q2’25 earnings beat on revenue and EPS, stock price closes up 8.5% 3 Q3’25 results exceed expectations and FY25 guidance is raised; reduction in volatility in Naira 4 1 3 2 4 Unaffected Price(1): $7.99 TIM confirms non-binding discussions with IHS regarding potential acquisition of I-Systemes 5 5 Share Price Performance YTD LTM Since Jan-24 Since Jan-23 Italy 12.0% 131.2% 86.2% 31.5% Italy $8.23 5 |

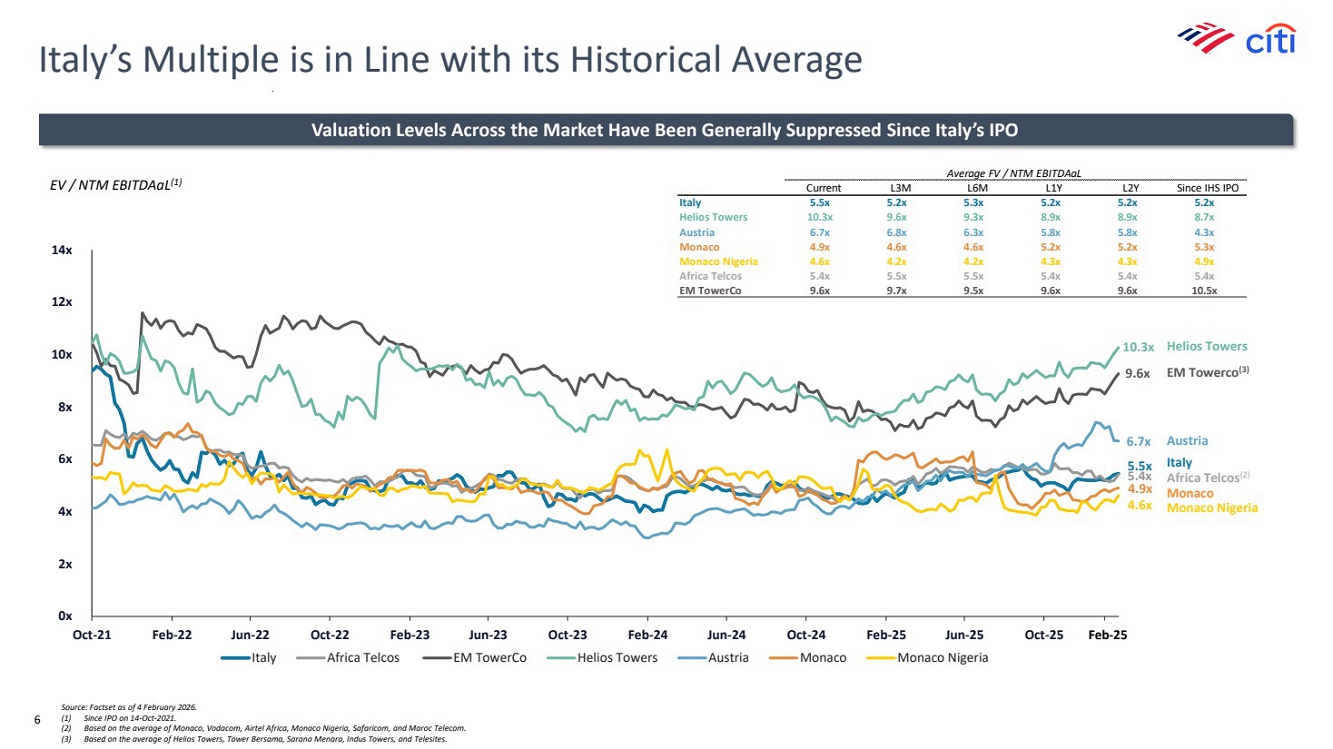

| Average FV / NTM EBITDAaL Current L3M L6M L1Y L2Y Since IHS IPO Italy 5.5x 5.2x 5.3x 5.2x 5.2x 5.2x Helios Towers 10.3x 9.6x 9.3x 8.9x 8.9x 8.7x Austria 6.7x 6.8x 6.3x 5.8x 5.8x 4.3x Monaco 4.9x 4.6x 4.6x 5.2x 5.2x 5.3x Monaco Nigeria 4.6x 4.2x 4.2x 4.3x 4.3x 4.9x Africa Telcos 5.4x 5.5x 5.5x 5.4x 5.4x 5.4x EM TowerCo 9.6x 9.7x 9.5x 9.6x 9.6x 10.5x Italy’s Multiple is in Line with its Historical Average EV / NTM EBITDAaL(1) Valuation Levels Across the Market Have Been Generally Suppressed Since Italy’s IPO Source: Factset as of 4 February 2026. (1) Since IPO on 14-Oct-2021. (2) Based on the average of Monaco, Vodacom, Airtel Africa, Monaco Nigeria, Safaricom, and Maroc Telecom. (3) Based on the average of Helios Towers, Tower Bersama, Sarana Menara, Indus Towers, and Telesites. EM Towerco(3) Helios Towers Austria Africa Telcos(2) Italy Monaco Nigeria Monaco 5.5x 5.4x 9.6x 10.3x 6.7x 4.9x 4.6x 0x 2x 4x 6x 8x 10x 12x 14x Oct-21 Feb-22 Jun-22 Oct-22 Feb-23 Jun-23 Oct-23 Feb-24 Jun-24 Oct-24 Feb-25 Jun-25 Oct-25 Italy Africa Telcos EM TowerCo Helios Towers Austria Monaco Monaco Nigeria Feb-25 6 |

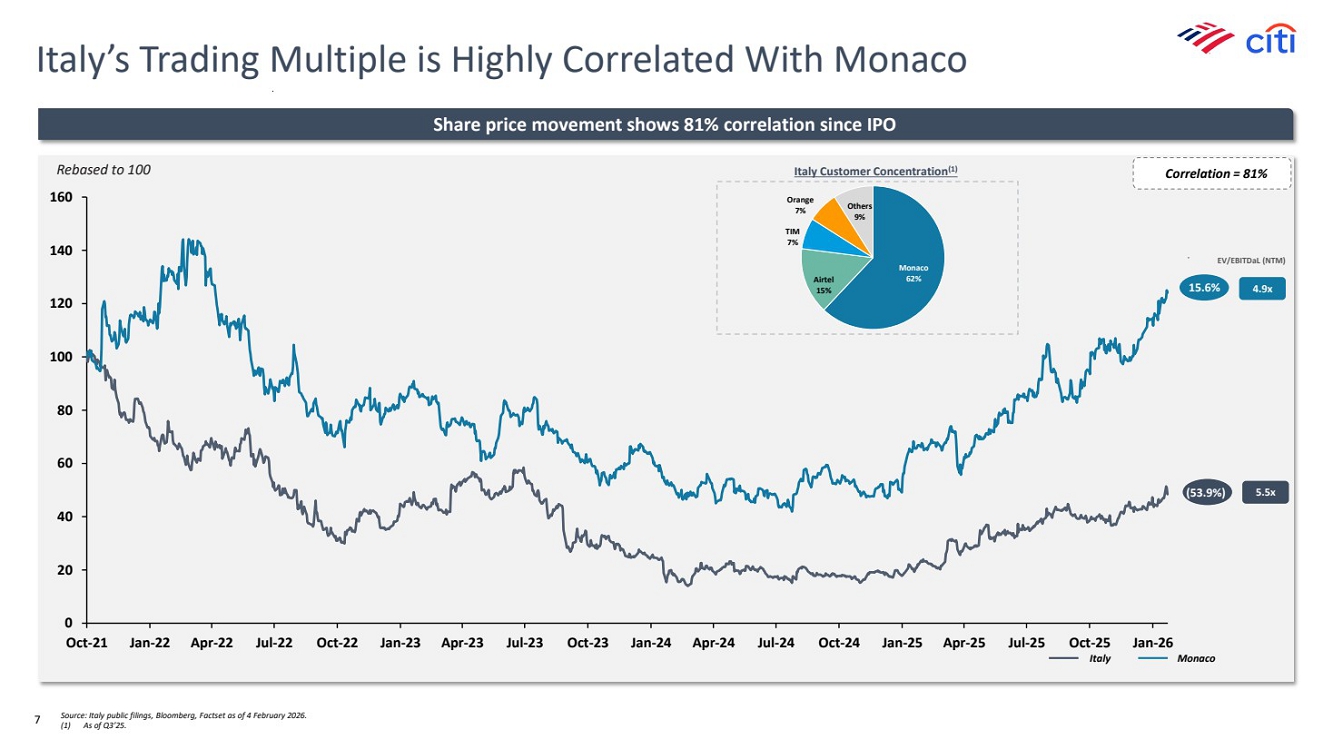

| 0 20 40 60 80 100 120 140 160 Oct-21 Jan-22 Apr-22 Jul-22 Oct-22 Jan-23 Apr-23 Jul-23 Oct-23 Jan-24 Apr-24 Jul-24 Oct-24 Jan-25 Apr-25 Jul-25 Oct-25 Jan-26 Italy’s Trading Multiple is Highly Correlated With Monaco EV/EBITDaL (NTM) 15.6% (53.9%) 5.5x 4.9x Rebased to 100 Share price movement shows 81% correlation since IPO Correlation = 81% Monaco Airtel 62% 15% TIM 7% Orange 7% Others 9% Italy Customer Concentration(1) Italy Monaco Source: Italy public filings, Bloomberg, Factset as of 4 February 2026. (1) As of Q3’25. 7 |

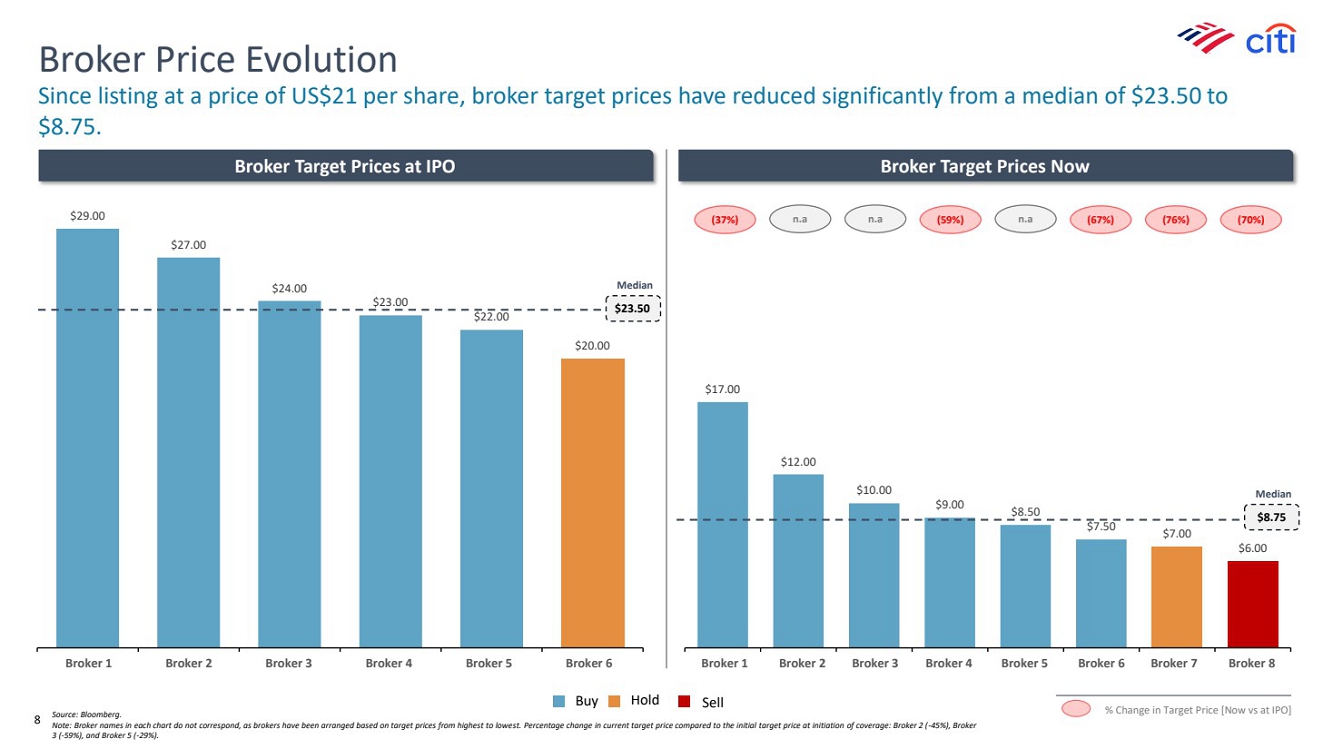

| $29.00 $27.00 $24.00 $23.00 $22.00 $20.00 GS TD Cowen Barclays RBC Capital Citi JP Morgan Broker Price Evolution Since listing at a price of US$21 per share, broker target prices have reduced significantly from a median of $23.50 to $8.75. Buy Hold Sell Source: Bloomberg. Note: Broker names in each chart do not correspond, as brokers have been arranged based on target prices from highest to lowest. Percentage change in current target price compared to the initial target price at initiation of coverage: Broker 2 (-45%), Broker 3 (-59%), and Broker 5 (-29%). Broker Target Prices at IPO Broker Target Prices Now $17.00 $12.00 $10.00 $9.00 $8.50 $7.50 $7.00 $6.00 (37%) (59%) (67%) (76%) (70%) Median $23.50 Median $8.75 n.a n.a n.a % Change in Target Price [Now vs at IPO] Broker 1 Broker 2 Broker 3 Broker 4 Broker 5 Broker 6 Broker 1 Broker 2 Broker 3 Broker 4 Broker 5 Broker 6 Broker 7 Broker 8 8 |

| Overview of Proposed Transaction and Illustrative Pro Forma Impact 03 |

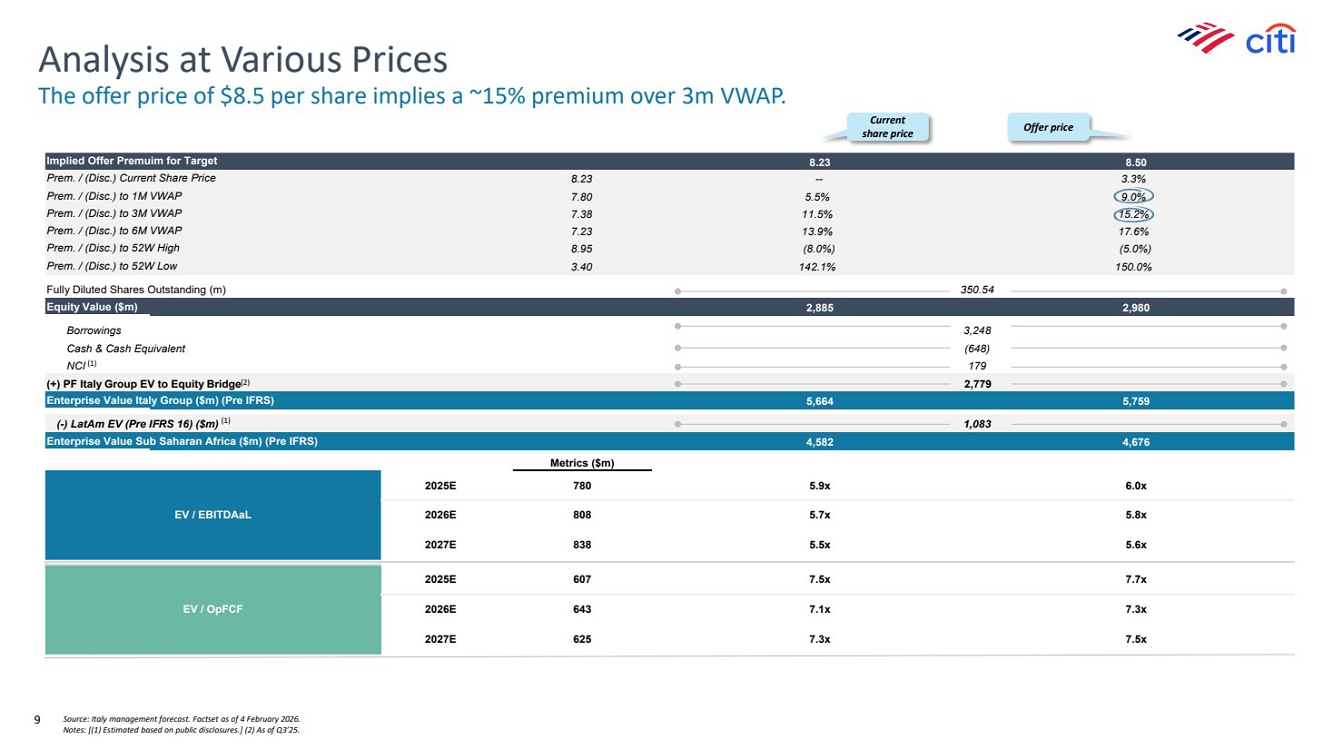

| Implied Offer Premuim for Target 8.23 8.50 Prem. / (Disc.) Current Share Price 8.23 -- 3.3% Prem. / (Disc.) to 1M VWAP 7.80 5.5% 9.0% Prem. / (Disc.) to 3M VWAP 7.38 11.5% 15.2% Prem. / (Disc.) to 6M VWAP 7.23 13.9% 17.6% Prem. / (Disc.) to 52W High 8.95 (8.0%) (5.0%) Prem. / (Disc.) to 52W Low 3.40 142.1% 150.0% Fully Diluted Shares Outstanding (m) 350.54 Equity Value ($m) 2,885 2,980 Borrowings 3,248 Cash & Cash Equivalent (648) NCI 179 (+) PF Italy Group EV to Equity Bridge 2,779 Enterprise Value Italy Group ($m) (Pre IFRS) 5,664 5,759 (-) LatAm EV (Pre IFRS 16) ($m) 1,083 Enterprise Value Sub Saharan Africa ($m) (Pre IFRS) 4,582 4,676 Metrics ($m) 2025E 780 5.9x 6.0x 2026E 808 5.7x 5.8x 2027E 838 5.5x 5.6x 2025E 607 7.5x 7.7x 2026E 643 7.1x 7.3x 2027E 625 7.3x 7.5x EV / EBITDAaL EV / OpFCF The offer price of $8.5 per share implies a ~15% premium over 3m VWAP. Analysis at Various Prices Current share price Offer price Source: Italy management forecast. Factset as of 4 February 2026. Notes: [(1) Estimated based on public disclosures.] (2) As of Q3’25. (2) (1) (1) 9 |

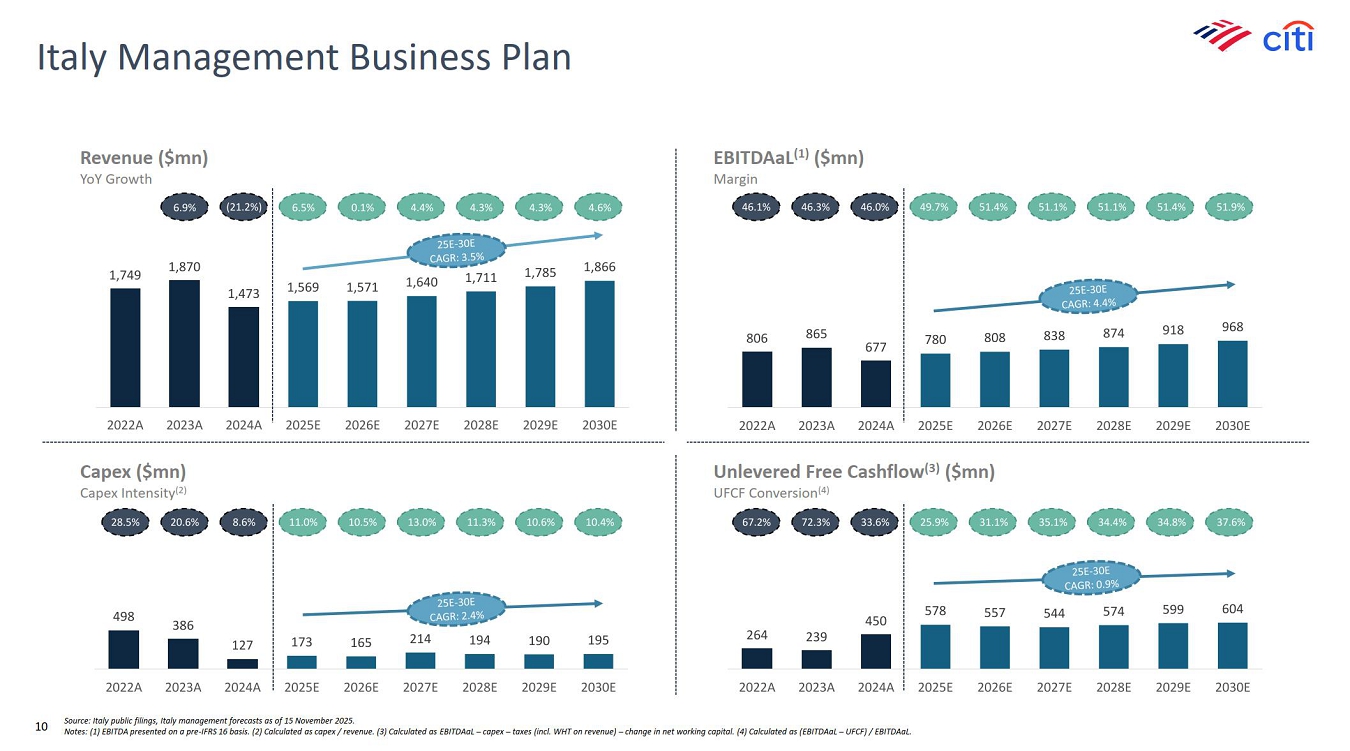

| 498 386 127 173 165 214 194 190 195 2022A 2023A 2024A 2025E 2026E 2027E 2028E 2029E 2030E 264 239 450 578 557 544 574 599 604 2022A 2023A 2024A 2025E 2026E 2027E 2028E 2029E 2030E 806 865 677 780 808 838 874 918 968 2022A 2023A 2024A 2025E 2026E 2027E 2028E 2029E 2030E 1,749 1,870 1,473 1,569 1,571 1,640 1,711 1,785 1,866 2022A 2023A 2024A 2025E 2026E 2027E 2028E 2029E 2030E 46.1% 46.3% 46.0% 49.7% 51.4% 51.1% 51.1% 51.4% 51.9% Italy Management Business Plan Source: Italy public filings, Italy management forecasts as of 15 November 2025. Notes: (1) EBITDA presented on a pre-IFRS 16 basis. (2) Calculated as capex / revenue. (3) Calculated as EBITDAaL – capex – taxes (incl. WHT on revenue) – change in net working capital. (4) Calculated as (EBITDAaL – UFCF) / EBITDAaL. Revenue ($mn) YoY Growth EBITDAaL(1) ($mn) Margin Unlevered Free Cashflow(3) ($mn) UFCF Conversion(4) Capex ($mn) Capex Intensity(2) 28.5% 20.6% 8.6% 11.0% 10.5% 13.0% 11.3% 10.6% 10.4% Awaiting JPM confirmation for inclusion 67.2% 72.3% 33.6% 25.9% 31.1% 35.1% 34.4% 34.8% 37.6% 6.9% (21.2%) 6.5% 0.1% 4.4% 4.3% 4.3% 4.6% 10 |

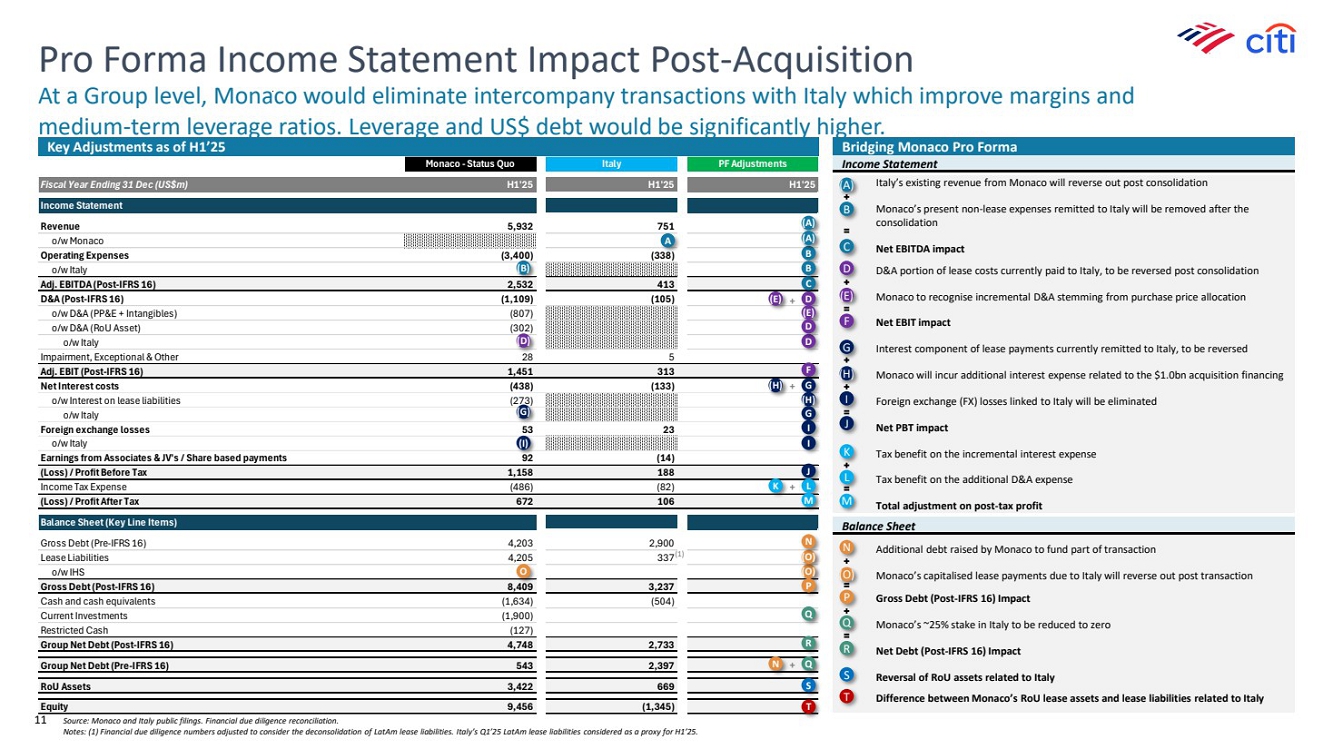

| Monaco - Status Quo Italy PF Adjustments Fiscal Year Ending 31 Dec (US$m) H1'25 H1'25 H1'25 Income Statement Revenue 5,932 751 o/w Monaco Operating Expenses (3,400) (338) o/w Italy Adj. EBITDA (Post-IFRS 16) 2,532 413 D&A (Post-IFRS 16) (1,109) (105) o/w D&A (PP&E + Intangibles) (807) o/w D&A (RoU Asset) (302) o/w Italy Impairment, Exceptional & Other 2 8 5 Adj. EBIT (Post-IFRS 16) 1,451 313 Net Interest costs (438) (133) o/w Interest on lease liabilities (273) o/w Italy Foreign exchange losses 5 3 2 3 o/w Italy Earnings from Associates & JV's / Share based payments 9 2 (14) (Loss) / Profit Before Tax 1,158 188 Income Tax Expense (486) (82) (Loss) / Profit After Tax 672 106 Balance Sheet (Key Line Items) Gross Debt (Pre-IFRS 16) 4,203 2,900 Lease Liabilities 4,205 337 o/w IHS Gross Debt (Post-IFRS 16) 8,409 3,237 Cash and cash equivalents (1,634) (504) Current Investments (1,900) Restricted Cash (127) Group Net Debt (Post-IFRS 16) 4,748 2,733 Group Net Debt (Pre-IFRS 16) 543 2,397 RoU Assets 3,422 669 Equity 9,456 (1,345) ▪ Italy’s existing revenue from Monaco will reverse out post consolidation ▪ Monaco’s present non-lease expenses remitted to Italy will be removed after the consolidation ▪ Net EBITDA impact ▪ D&A portion of lease costs currently paid to Italy, to be reversed post consolidation ▪ Monaco to recognise incremental D&A stemming from purchase price allocation ▪ Net EBIT impact ▪ Interest component of lease payments currently remitted to Italy, to be reversed ▪ Monaco will incur additional interest expense related to the $1.0bn acquisition financing ▪ Foreign exchange (FX) losses linked to Italy will be eliminated ▪ Net PBT impact ▪ Tax benefit on the incremental interest expense ▪ Tax benefit on the additional D&A expense ▪ Total adjustment on post-tax profit Pro Forma Income Statement Impact Post-Acquisition At a Group level, Monaco would eliminate intercompany transactions with Italy which improve margins and medium-term leverage ratios. Leverage and US$ debt would be significantly higher. Key Adjustments as of H1’25 Bridging Monaco Pro Forma (A) B C D (E) F G (H) I J K L M (B) (E) (D) A (H) (I) K (G) (A) B C D D F G (H) G I I J L M + + + B (A) (E) D O (O) (O) N P Q R S Income Statement Balance Sheet ▪ Additional debt raised by Monaco to fund part of transaction ▪ Monaco’s capitalised lease payments due to Italy will reverse out post transaction ▪ Gross Debt (Post-IFRS 16) Impact ▪ Monaco’s ~25% stake in Italy to be reduced to zero ▪ Net Debt (Post-IFRS 16) Impact ▪ Reversal of RoU assets related to Italy ▪ Difference between Monaco’s RoU lease assets and lease liabilities related to Italy N (O) P Q R S N + Q T T Source: Monaco and Italy public filings. Financial due diligence reconciliation. Notes: (1) Financial due diligence numbers adjusted to consider the deconsolidation of LatAm lease liabilities. Italy’s Q1’25 LatAm lease liabilities considered as a proxy for H1’25. (1) 11 |

| Disclaimer These materials have been prepared by one or more affiliates of Bank of America Corporation (“BAC” and, together with its affiliates, the “BAC Group”) for the client or potential client to whom these materials are directly addressed and delivered (the “Company”) for discussion purposes only in connection with an actual or potential mandate or engagement and remain subject to verification and to our further review and assessment from, inter alia, a legal, tax, compliance, accounting policy and risk perspective, as appropriate. These materials were designed for discussion with and consideration by specific persons familiar with the business and affairs of the Company and are being furnished and should be considered only when taken together with any other information, oral or written, provided by us in connection herewith. These materials are not intended to provide the sole basis for evaluating, and should not be considered as, and are not intended to provide, any advice, recommendation or formal opinion with respect to, any transaction or any financial, strategic, business or other matter and do not constitute an offer or solicitation to sell or purchase any securities, nor do they constitute a commitment by BAC or any of its affiliates to provide, arrange, bookrun, underwrite or syndicate any financing for any transaction, to market, offer, place, sell, underwrite or purchase any security or to otherwise enter into any type of business relationship in connection herewith. None of BAC or its affiliates has provided or will provide legal, tax, compliance, accounting or risk advice to the Company or any recipient of these materials. These materials are not intended to provide any such advice or any consulting, rating agency or environmental, social and governance and sustainability (“ESG”) advice or ESG rating agency advice, nor are any materials provided by us intended to identify, evaluate or advise you as to any potential legal, reputational, regulatory compliance or other risks or as to the fairness, accuracy or completeness of your or any other party’s public disclosure. The information and any examples provided are illustrative, may not be reflected in the product or service you receive from BAC, and have not been evaluated or verified for effectiveness, quality, accuracy, completeness or risk and none of BAC or its affiliates is endorsing any particular approach to ESG, any particular ESG investment strategy or any particular ESG standards, ratings or metrics. These materials are subject to the Company’s own review and assessment from a legal, tax, compliance, accounting policy, financial, strategic, ESG, and risk perspective, as appropriate, and the Company should consult with its own legal, tax, compliance, accounting, financial, and ESG advisors prior to entering any transaction. The BAC Group may be engaged in certain business activities which could have increased investor, client, employee, regulatory scrutiny and/or scrutiny from other parties generally from an ESG perspective. Any ESG assessments or consideration of ESG factors by BAC in the services or information provided to you, will generally be reliant on data received from you or third parties (including ESG data vendors), which may be estimated or only consider certain ESG aspects and at certain points (rather than looking at the entire sustainability profile and actions of the Company/the BAC Group or its value chain). These materials are not intended to be legally binding or to give rise to any legal relationship between the recipient or any other person whatsoever and any person or entity within the BAC Group. No person or entity within the BAC Group will be responsible or liable (whether in tort, contract or otherwise) for any losses or damages, consequential or otherwise, that may be incurred or alleged by any person or entity as a result of these materials, any inaccurate, incomplete or misleading statement, error or omission in these materials, or any transaction (whether entered into or not) relating to or resulting from these materials, and these materials may not be used or relied upon for any purpose, other than as may be specifically agreed with us in writing. We assume no obligation to verify, update, correct or otherwise revise these materials. These materials have not been prepared with a view toward public disclosure (whether under any securities laws or otherwise), are intended solely for review and consideration by the Company, and may not be, in whole or in part, reproduced, disseminated, quoted or referred to, or shown, transmitted, or otherwise given to, any person other than the Company’s authorized representatives, without our prior written consent. These materials are based on information provided by or on behalf of the Company and/or other potential transaction participants, from public sources or otherwise reviewed by us. We assume no responsibility for independent investigation or verification of the information included in these materials (including, without limitation, data from third party suppliers) and have relied on such information being complete and accurate in all material respects. To the extent such information includes estimates and forecasts of future financial performance prepared by or reviewed with the managements of the Company and/or other potential transaction participants or obtained from public sources, we have assumed that such estimates and forecasts have been reasonably prepared on bases reflecting the best currently available estimates and judgments of such management or other parties (or, with respect to estimates and forecasts obtained from public sources, represent reasonable estimates). Any such estimates and forecasts may reflect assumptions and judgments that prove incorrect; there can be no assurance that any estimates or forecasts will be realized. No representation or warranty, express or implied, is made as to the accuracy or completeness of any such information, or of any other information in these materials, and nothing contained herein is, or shall be relied upon as, a representation, warranty or undertaking, whether as to the past, the present or the future. These materials may not reflect information known to other professionals in other business areas of the BAC Group. Any league tables referenced within these materials have been prepared using data sourced from external third-party providers as outlined in the relevant footnotes where applicable. The BAC Group comprises a full service securities firm and commercial bank engaged in securities, commodities and derivatives trading, foreign exchange and other brokerage activities, and principal investing as well as providing investment, corporate and private banking, asset and investment management, financing and strategic advisory services and other commercial services and products to a wide range of corporations, governments and individuals, in the United States and internationally, from which conflicting interests or duties, or a perception thereof, may arise. In the ordinary course of these activities, parts of the BAC Group at any time may invest on a principal basis or manage funds that invest, make or hold long or short positions, finance positions or trade or otherwise effect transactions, for their own accounts or the accounts of customers, in debt, equity or other securities or financial instruments (including derivatives, bank loans or other obligations) of the Company, potential counterparties or any other person that may be involved in a transaction. “Bank of America” and “BofA Securities” are the marketing names used by the Global Banking and Global Markets divisions of BAC. Lending, leasing, equipment finance, merchant services, derivatives and other commercial banking activities, and trading in certain financial instruments, are performed globally by banking affiliates or subsidiaries of BAC, including Bank of America, N.A., Member FDIC, or of the deposit protection scheme, if available, in the relevant jurisdiction, Equal Housing Lender. Trading in securities and financial instruments, and strategic advisory, and other investment banking activities, are performed globally by investment banking affiliates or subsidiaries of BAC (“Investment Banking Affiliates”), including, in the United States, BofA Securities, Inc which is a registered broker-dealer and Member of SIPC, and, in other jurisdictions, by locally registered entities (including Bank of America Europe Designated Activity Company, BofA Securities Europe SA and Merrill Lynch International). BofA Securities, Inc. is registered as a futures commission merchant with the CFTC and a member of the NFA. Bank of America Europe Designated Activity Company is a wholly-owned subsidiary of BAC and is regulated by the Central Bank of Ireland. Products and services that may be referenced in these materials may be provided through one or more affiliates of BAC. Bank of America and BofA Securities entities and branches provide financial services to the clients of Bank of America and BofA Securities and may outsource/delegate the marketing and/or provision of certain services or aspects of services to other branches or members of the BAC Group. Your service provider will remain the entity/branch specified in your onboarding documentation and/or other contractual or marketing documentation even where you communicate with staff that operate from a different entity or branch which is acting for and on behalf of your contractual service provider in their communications with you. Some or all products and services offered by the BAC Group may be unavailable in certain jurisdictions, or may be available only on an offshore and/or reverse solicitation basis, and availability is subject to change without notice. The BAC Group does not perform in any jurisdiction banking activities that are reserved by local law to licensed or approved banks, except in those jurisdictions where its banking affiliates or subsidiaries have procured the necessary licenses or approvals. For those jurisdictions where they are not licensed to perform banking activities, all services/products are conducted on an offshore basis for Latin America and the Caribbean. Some or all of the products may not be available in certain jurisdictions and are subject to change without notice. This document and its content are for information purposes and shall not be interpreted as banking or financial intermediation, business solicitation and/or public offering of any kind. Investment products offered by Investment Banking Affiliates: This document is NOT a research report and is NOT a product of a research department and the material in this communication is not investment research or a research recommendation. This document is not prepared as or intended to be investment advice, and the content is not and should not be considered as investment advice under any circumstances. The BAC Group has adopted policies and guidelines designed to preserve the independence of our research analysts. These policies prohibit employees from, directly or indirectly, offering research coverage, a favorable research rating or a specific price target or offering to change a research rating or price target as consideration for or an inducement to obtain business or other compensation and prohibit research analysts from being directly compensated for involvement in investment banking transactions. The views expressed herein are the views solely of the specific BAC Group line of business providing you with these materials and no inference should be made that the views expressed represent the view of the firm’s research department. Any statements contained herein as to tax matters were neither written nor intended by us to be used and cannot be used by any taxpayer for the purpose of avoiding tax penalties that may be imposed on such taxpayer. If any person uses or refers to any such tax statement in promoting, marketing or recommending a partnership or other entity, investment plan or arrangement to any taxpayer, then the statement expressed herein is being delivered to support the promotion or marketing of the transaction or matter addressed and the recipient should seek advice based on its particular circumstances from an independent tax advisor. Notwithstanding anything that may appear herein or in other materials to the contrary, the Company shall be permitted to disclose the tax treatment and tax structure of a transaction—including any materials, opinions or analyses relating to such tax treatment or tax structure, but without disclosure of identifying information or any non-public commercial or financial information (except to the extent any such information relates to the tax structure or tax treatment)—on and after the earliest to occur of the date of (i) public announcement of discussionsrelating to such transaction, (ii) public announcement of such transaction or (iii) execution of a definitive agreement (with or without conditions) to enter into such transaction; provided, however, that if such transaction is not consummated for any reason, the provisions of this sentence shall cease to apply. We are required to obtain, verify and record certain information that identifies the Company, which information includes the name and address of the Company and other information that will allow us to identify the Company in accordance, as applicable, with the USA Patriot Act (Title III of Pub. L. 107-56, as amended, which wassigned into law October 26, 2001) and such other laws, rules and regulations as applicable within and outside the United States. For more information, including who your contractualservice provider is or will be, the terms and conditions that apply to the service(s), and information regarding external third-party data providers and the criteria and methodology used to prepare a league table, please contact your Bank of America or BofA Securities representative or relationship manager. Notice regarding Bank of America or BofA Securities entities outside of the United States: For Bank of America or BofA Securities entities outside the United States, please see additional information via the following link: https://www.bofaml.com/en-us/content/baml-disclaimer.html. Notice regarding Bank of America or BofA Securities entitiesin the EEA and UK: For Bank of America or BofA Securities entities in the European Economic Area and the United Kingdom, please see additional information via the following link: www.bofaml.com/mifid2. Disclosure regarding BofA Securities Europe SA: BofA Securities Europe SA (“BofASE SA”), with registered address at 51, rue La Boétie, 75008 Paris is registered under n° 842 602 690 RCS Paris. In accordance with the provisions of French Code Monétaire et Financier (Monetary and Financial Code), BofASE SA is an établissement de crédit et d’investissement (credit and investment institution) that is authorised and supervised by the European Central Bank and the Autorité de Contrôle Prudentiel et de Résolution (ACPR) and regulated by the ACPR and the Autorité des Marchés Financiers. BofASE SA’s share capital can be found at www.bofaml.com/BofASEdisclaimer. Notice for Argentina: “Merrill Lynch” is the trademark that Bank of America Corporation uses in the Republic of Argentina for capital markets, financial advisory and investment businesses, which are conducted by and through Merrill Lynch Argentina S.A. This entity does not conduct any activities subject to banking license, such as capturing deposits from the public. Notice for Brazil: Bank of America and BofA Securities’ Ombudsman*| Toll Free: 0800 886 2000 “BofA Securities” is the marketing name of Merrill Lynch S.A. Corretora de Títulos e Valores Mobiliários*, which is a broker-dealer registered in Brazil of Bank of America Corporation. * Bank of America Merrill Lynch Banco Múltiplo S.A. (the banking affiliate in Brazil of Bank of America Corporation) and Merrill Lynch S.A. Corretora de Títulos e Valores Mobiliários (the registered broker dealer in Brazil). Notice for Chile: Bank of America N.A., Oficina de Representacion (Chile), is a representative office in Chile of Bank of America N.A., supervised by the Comisión para el Mercado Financiero and authorized to promote in Chile select products and services that Bank of America N.A. provides outside of Chile. Neither Bank of America, N.A., nor its representative office in Chile, is authorized to carry out in Chile any activities that are reserved by Chilean law to locally licensed banks. Notice for Colombia: Bank of America N.A., Oficina de Representacion (Colombia), is a representative office in Colombia of Bank of America N.A., supervised by the Superintendencia Financiera de Colombia and authorized to promote in Colombia select products and services that Bank of America N.A. and BofA Securities, Inc. provides outside of Colombia. Neither Bank of America, N.A., nor its representative office in Colombia, is authorized to carry out in Colombia any activities that are reserved by Colombian law to locally licensed banks. Notice for Dubai International Financial Centre: Merrill Lynch International is authorised and regulated by the Dubai Financial Services Authority. Principal address is ICD Brookfield Place, Level 46, Dubai International Financial Centre, Dubai, United Arab Emirates. License no. CL0322, P.O. Box 506576, Dubai, United Arab Emirates. This communication is not for distribution to the public or a large number of persons, but is personal to named recipients; it is directed to professional and market customers and not to retail customers. The financial products/financial services to which this marketing material relates is only made available to customers who in the view of Merrill Lynch International meet the regulatory criteria to be a Client under DFSA Conduct of Business rules (COB 2.3). Please note that Merrill Lynch International does not deal with retail clients. Notice for Hong Kong: Bank of America, National Association, Hong Kong Branch, is a branch of a national banking association organized and existing with limited liability under the laws of the United States of America. Notice for Kingdom of Saudi Arabia: This marketing communication is issued and approved by the Merrill Lynch Kingdom of Saudi Arabia Company which is authorised and regulated by the Kingdom of Saudi Arabia Capital Market Authority ("CMA"). Principal address is Kingdom Tower, 22 Floor, 2239 Al-Orouba Road, Olaya, Unit No: 50, Ar Riyadh 12214-9597, Saudi Arabia. This communication includes information given in compliance with the Regulations of the CMA. This communication may not be distributed in the Kingdom of Saudi Arabia except to such persons as are permitted under the regulations issued by the CMA. The CMA does not make any representation as to the accuracy or completeness of this communication, and expressly disclaims any liability whatsoever for any loss arising from, or incurred in reliance upon, any part of this communication. This material is not to be distributed to, nor to be read by, retail clients. Notice for Mexico: Bank of America México, S.A., Institución de Banca Múltiple is a banking affiliate in Mexico of Bank of America Corporation and Merrill Lynch México, S.A. de C.V., Casa de Bolsa is a registered broker dealer affiliate in Mexico of Bank of America Corporation. Bank of America, National Association, Charlotte, Carolina del Norte, Estados Unidos de Norteamérica, Representación en México is a representative office in Mexico of Bank of America, N.A., supervised by the Mexico National Commission on Banking and Securities. Notice for Peru: Bank of America N.A., Oficina de Representacion (Peru), is a representative office in Peru of Bank of America N.A., supervised by the Superintendencia de Banca, Seguros y Administradoras Privadas de Fondos de Pensiones and authorized to promote in Peru select products and services that Bank of America N.A. and its investment banking affiliates provide outside of Peru. Neither Bank of America, N.A., nor its representative office in Peru, is authorized to carry out in Peru any activities that are reserved by Peruvian law to locally licensed banks. Notice for Qatar Financial Centre: Merrill Lynch International (QFC) Branch is licensed by the Qatar Financial Centre Regulatory Authority. Principal address is Tornado Tower, Level 22, West Bay, Doha, Qatar. QFC License no. 00258, P.O. Box 27774, Doha, Qatar. This communication is not for distribution to the public or a large number of persons, but is personal to named recipients; it is directed to eligible counterparty or business customers and not to retail customers. The financial products/financial servicesto which this marketing material relates is only made available to customers who in the view of Merrill Lynch International (QFC) Branch meet the regulatory criteria to be a Client under QFCRA Customer and Investor Protection Rules 2019. Please note that Merrill Lynch International (QFC) Branch does not deal with retail customers. Bank of America Europe DAC (“BofA Europe”) is a designated activity company limited by shares. It is registered in Ireland with registered number no. 220165 and registered address at Two Park Place, Hatch Street, Dublin 2. BofA Europe is a credit institution and is authorised and supervised by the European Central Bank and the Central Bank of Ireland. BofA Europe is regulated by the Central Bank of Ireland. List of branches is at https://business.bofa.com/content/dam/boamlimages/documents/articles/ID17_1174/bofaml_entities_list.pdf. This communication is provided for informational purposes only and does not constitute, nor should it be construed as, a representation or assurance that any product, service, or transaction is aligned with the EU Taxonomy Regulation (Regulation (EU) 2020/852). BofA Europe does not make any claim of EU Taxonomy compliance unless expressly stated in formal disclosures prepared in accordance with applicable regulatory requirements. Bank of America, N.A. (“BANA”) is a national banking association organised and existing under the laws of the USA with charter number 13044 and with its registered address at 100 North Tryon Street, Charlotte, North Carolina 28202, USA. BANA (member of Federal Deposit Insurance Corporation (FDIC)) is authorised and regulated by the Office of the Comptroller of the Currency, and is subject to the supervision and regulation of the Board of Governors of the Federal Reserve System and the FDIC, each in the USA. BANA has a London branch (“BANA London Branch”) with its principal place of business in the United Kingdom at 2 King Edward Street, London EC1A 1HQ, which is authorised by the Prudential Regulation Authority and subject to regulation by the Financial Conduct Authority and limited regulation by the Prudential Regulation Authority. Details about the extent of BANA London Branch’s regulation by the Prudential Regulation Authority are available from BANA London Branch on request. Notice for Indonesia: Bank of America, National Association, Jakarta Branch (“BANA Jakarta”), is a branch of a national banking association organized and existing with limited liability under the laws of the United States of America. In Indonesia, BANA Jakarta is licensed and under the supervision of the Indonesia Financial Services Authority (“Otoritas Jasa Keuangan” or“OJK”) and Bank Indonesia, and a participant of Deposit Insurance Corporation (“Lembaga Penjamin Simpanan” or "LPS”). PT Merrill Lynch Sekuritas Indonesia is licensed and supervised by OJK. Notice for Philippines: Bank of America, National Association, Manila Branch is regulated by Bangko Sentral ng Pilipinas. https://www.bsp.gov.ph. Deposits are insured by Philippine Deposit Insurance Corporation up to PHP 1,000,000 per depositor, per bank. For queries or concerns, please contact Client Service Team at (+632) 8815-5555 or asia.sse-ph@bofa.com. ©2026 Bank of America Corporation. All rights reserved. 1/2026 Are Not FDIC Insured Are Not Bank Guaranteed May Lose Value 12 |

| Disclaimer The accompanying material has been prepared for the Company by Citigroup Global Markets Inc. (“Citi”) in connection with considering and/or negotiating a proposed transaction involving the Company. Accordingly, the accompanying material is preliminary in nature and subject to further diligence and negotiation of the terms of the proposed transaction. No other person may rely upon the accompanying material. The accompanying material is subject to the terms of our engagement letter with the Company, including the section “Use of Information” therein. The accompanying material does not constitute an opinion by Citi as to the fairness to the Company or its shareholders of the terms of any actual or proposed transaction involving the Company. Any estimates and projections contained herein have been prepared or adopted by the Company’s management, or obtained from public sources, or are based upon such estimates and projections, and involve numerous and significant subjective determinations, and there is no assurance that such estimates and projections will be realized. Citi does not take responsibility for such estimates and projections, or the basis on which they were prepared. No representation or warranty, expressed or implied, is made as to the accuracy or completeness of such information and nothing contained herein is, or shall be relied upon as, a representation, whether as to the past, the present or the future. Nothing contained herein shall be construed as legal, tax or accounting advice. 13 |