| S T R I C T L Y P R I V A T E A N D C O N F I D E N T I A L 16 February 2026 Project Mango | Valuation materials |

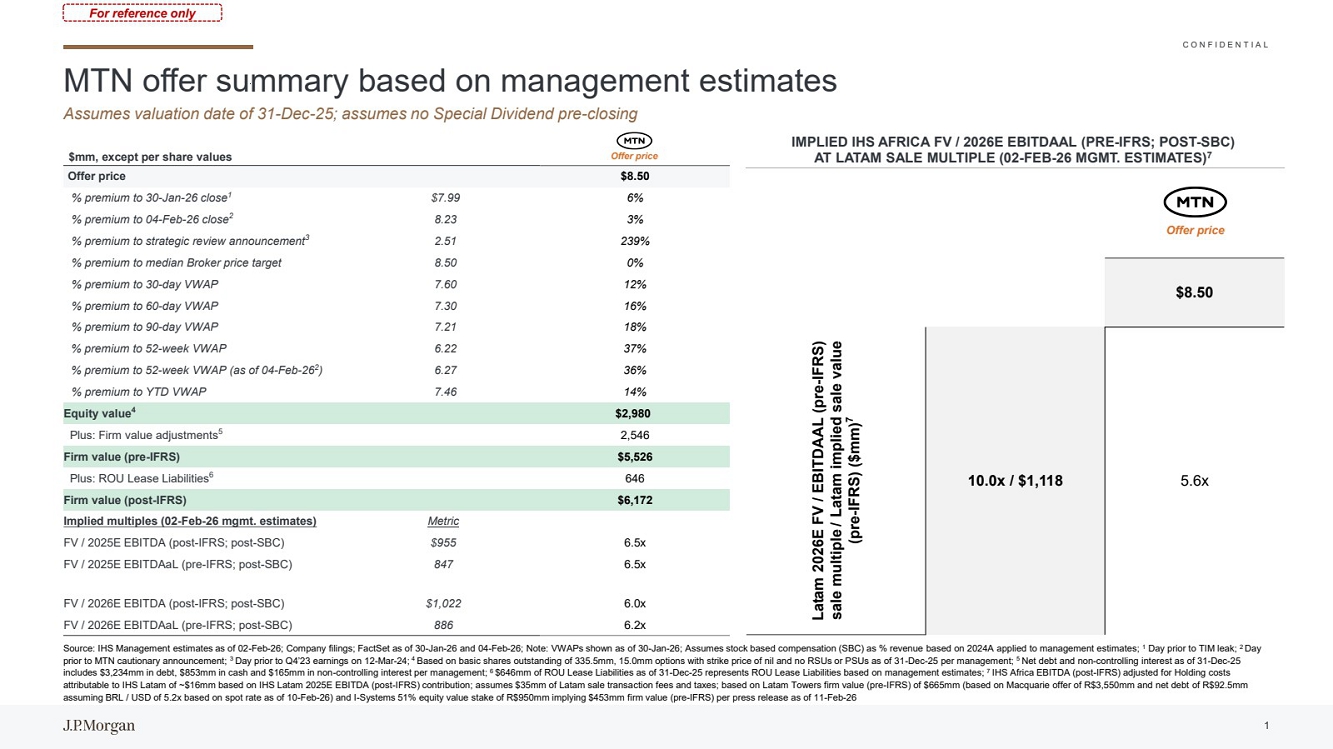

| C O N F I D E N T I A L $8.50 Latam 2026E FV / EBITDAAL (pre-IFRS) sale multiple / Latam implied sale value (pre-IFRS) ($mm) 7 10.0x / $1,118 5.6x MTN offer summary based on management estimates Assumes valuation date of 31-Dec-25; assumes no Special Dividend pre-closing Source: IHS Management estimates as of 02-Feb-26; Company filings; FactSet as of 30-Jan-26 and 04-Feb-26; Note: VWAPs shown as of 30-Jan-26; Assumes stock based compensation (SBC) as % revenue based on 2024A applied to management estimates; 1 Day prior to TIM leak; 2 Day prior to MTN cautionary announcement; 3 Day prior to Q4’23 earnings on 12-Mar-24; 4 Based on basic shares outstanding of 335.5mm, 15.0mm options with strike price of nil and no RSUs or PSUs as of 31-Dec-25 per management; 5 Net debt and non-controlling interest as of 31-Dec-25 includes $3,234mm in debt, $853mm in cash and $165mm in non-controlling interest per management; 6 $646mm of ROU Lease Liabilities as of 31-Dec-25 represents ROU Lease Liabilities based on management estimates; 7 IHS Africa EBITDA (post-IFRS) adjusted for Holding costs attributable to IHS Latam of ~$16mm based on IHS Latam 2025E EBITDA (post-IFRS) contribution; assumes $35mm of Latam sale transaction fees and taxes; based on Latam Towers firm value (pre-IFRS) of $665mm (based on Macquarie offer of R$3,550mm and net debt of R$92.5mm assuming BRL / USD of 5.2x based on spot rate as of 10-Feb-26) and I-Systems 51% equity value stake of R$950mm implying $453mm firm value (pre-IFRS) per press release as of 11-Feb-26 $mm, except per share values Offer price $8.50 % premium to 30-Jan-26 close1 $7.99 6% % premium to 04-Feb-26 close2 8.23 3% % premium to strategic review announcement3 2.51 239% % premium to median Broker price target 8.50 0% % premium to 30-day VWAP 7.60 12% % premium to 60-day VWAP 7.30 16% % premium to 90-day VWAP 7.21 18% % premium to 52-week VWAP 6.22 37% % premium to 52-week VWAP (as of 04-Feb-262 ) 6.27 36% % premium to YTD VWAP 7.46 14% Equity value4 $2,980 Plus: Firm value adjustments5 2,546 Firm value (pre-IFRS) $5,526 Plus: ROU Lease Liabilities6 646 Firm value (post-IFRS) $6,172 Implied multiples (02-Feb-26 mgmt. estimates) Metric FV / 2025E EBITDA (post-IFRS; post-SBC) $955 6.5x FV / 2025E EBITDAaL (pre-IFRS; post-SBC) 847 6.5x FV / 2026E EBITDA (post-IFRS; post-SBC) $1,022 6.0x FV / 2026E EBITDAaL (pre-IFRS; post-SBC) 886 6.2x IMPLIED IHS AFRICA FV / 2026E EBITDAAL (PRE-IFRS; POST-SBC) AT LATAM SALE MULTIPLE (02-FEB-26 MGMT. ESTIMATES) 7 For reference only Offer price Offer price 1 |

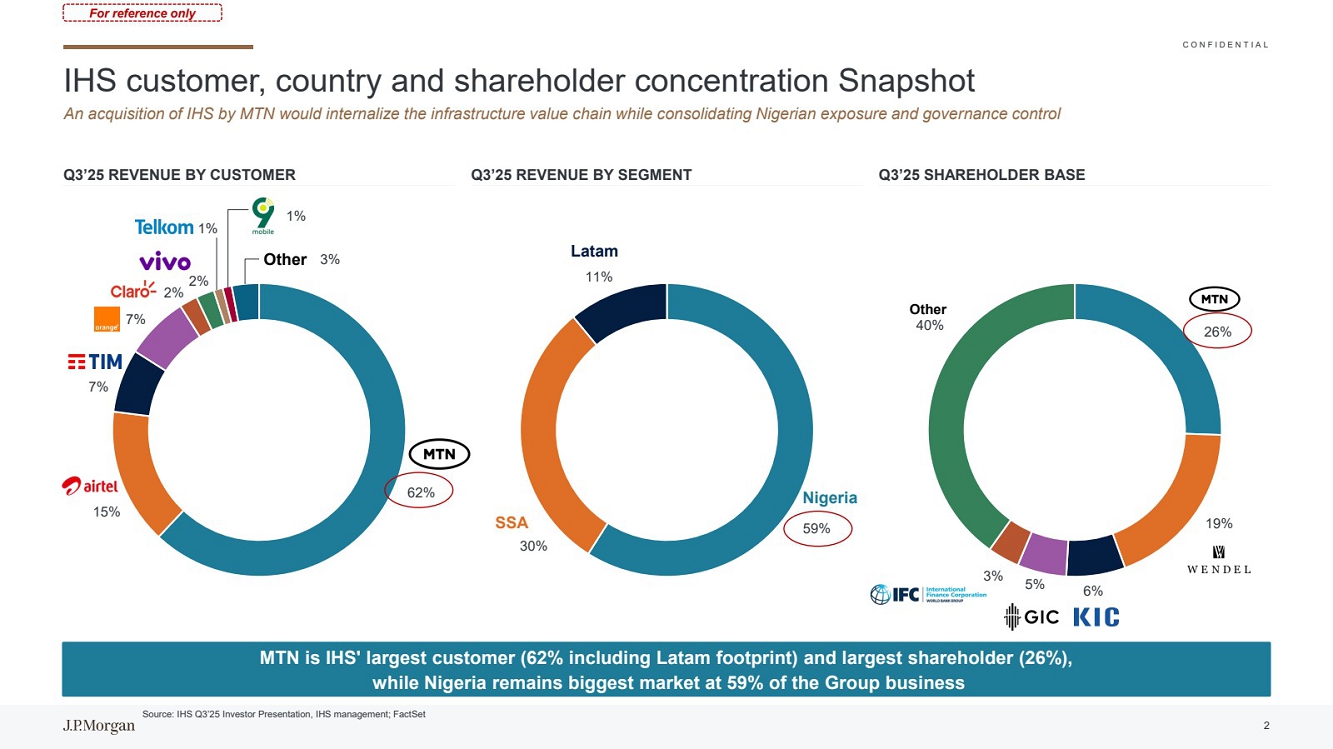

| C O N F I D E N T I A L IHS customer, country and shareholder concentration Snapshot For reference only Source: IHS Q3’25 Investor Presentation, IHS management; FactSet Q3’25 REVENUE BY CUSTOMER Q3’25 REVENUE BY SEGMENT Q3’25 SHAREHOLDER BASE 62% 15% 7% 7% 2% 2% 1% 1% 3% 59% 30% 11% 26% 19% 6% 5% 3% 40% Other Nigeria Latam SSA Other An acquisition of IHS by MTN would internalize the infrastructure value chain while consolidating Nigerian exposure and governance control MTN is IHS' largest customer (62% including Latam footprint) and largest shareholder (26%), while Nigeria remains biggest market at 59% of the Group business 2 |

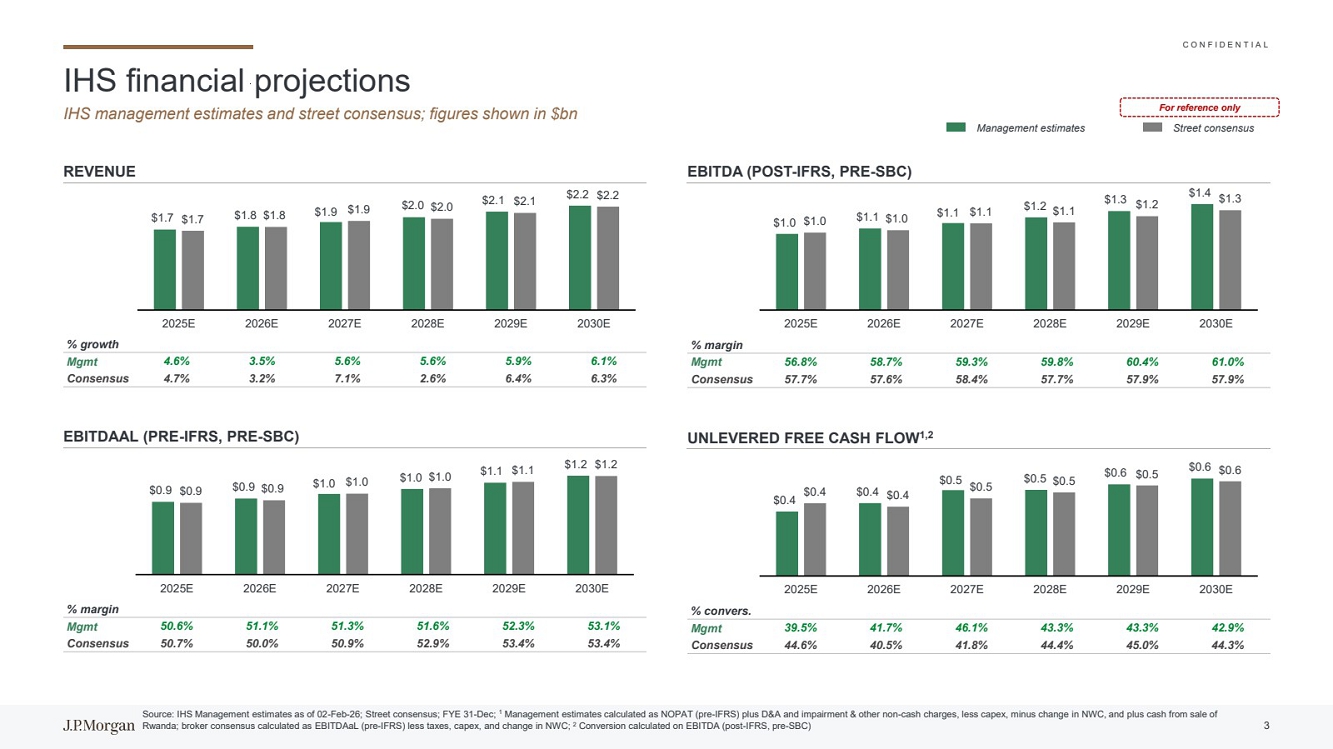

| C O N F I D E N T I A L IHS financial projections IHS management estimates and street consensus; figures shown in $bn EBITDA (POST-IFRS, PRE-SBC) UNLEVERED FREE CASH FLOW1,2 REVENUE EBITDAAL (PRE-IFRS, PRE-SBC) Source: IHS Management estimates as of 02-Feb-26; Street consensus; FYE 31-Dec; 1 Management estimates calculated as NOPAT (pre-IFRS) plus D&A and impairment & other non-cash charges, less capex, minus change in NWC, and plus cash from sale of Rwanda; broker consensus calculated as EBITDAaL (pre-IFRS) less taxes, capex, and change in NWC; 2 Conversion calculated on EBITDA (post-IFRS, pre-SBC) $1.0 $1.1 $1.1 $1.2 $1.3 $1.4 $1.0 $1.0 $1.1 $1.1 $1.2 $1.3 2025E 2026E 2027E 2028E 2029E 2030E $0.4 $0.4 $0.5 $0.5 $0.6 $0.6 $0.4 $0.4 $0.5 $0.5 $0.5 $0.6 2025E 2026E 2027E 2028E 2029E 2030E $0.9 $0.9 $1.0 $1.0 $1.1 $1.2 $0.9 $0.9 $1.0 $1.0 $1.1 $1.2 2025E 2026E 2027E 2028E 2029E 2030E % growth Mgmt 4.6% 3.5% 5.6% 5.6% 5.9% 6.1% Consensus 4.7% 3.2% 7.1% 2.6% 6.4% 6.3% % margin Mgmt 56.8% 58.7% 59.3% 59.8% 60.4% 61.0% Consensus 57.7% 57.6% 58.4% 57.7% 57.9% 57.9% % convers. Mgmt 39.5% 41.7% 46.1% 43.3% 43.3% 42.9% Consensus 44.6% 40.5% 41.8% 44.4% 45.0% 44.3% % margin Mgmt 50.6% 51.1% 51.3% 51.6% 52.3% 53.1% Consensus 50.7% 50.0% 50.9% 52.9% 53.4% 53.4% Management estimates Street consensus For reference only $1.7 $1.8 $1.9 $2.0 $2.1 $2.2 $1.7 $1.8 $1.9 $2.0 $2.1 $2.2 2025E 2026E 2027E 2028E 2029E 2030E 3 |

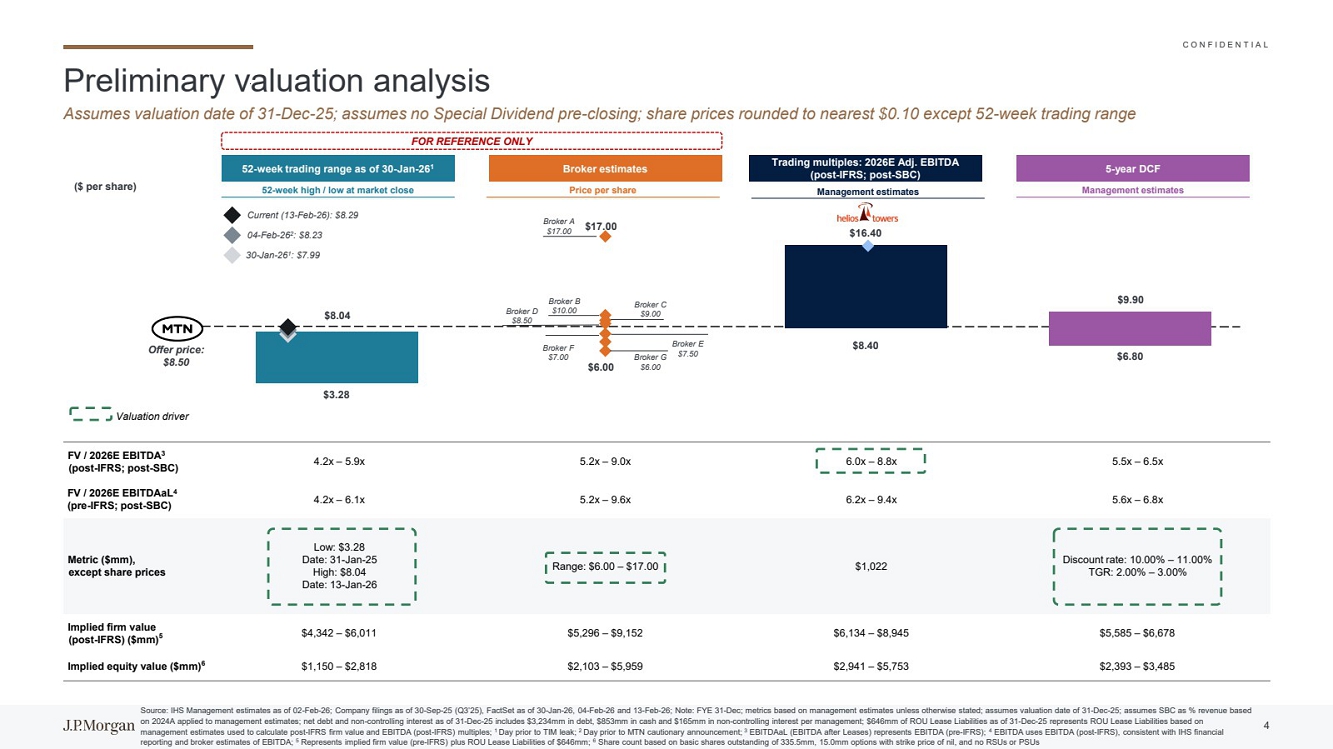

| C O N F I D E N T I A L Preliminary valuation analysis Assumes valuation date of 31-Dec-25; assumes no Special Dividend pre-closing; share prices rounded to nearest $0.10 except 52-week trading range Source: IHS Management estimates as of 02-Feb-26; Company filings as of 30-Sep-25 (Q3’25), FactSet as of 30-Jan-26, 04-Feb-26 and 13-Feb-26; Note: FYE 31-Dec; metrics based on management estimates unless otherwise stated; assumes valuation date of 31-Dec-25; assumes SBC as % revenue based on 2024A applied to management estimates; net debt and non-controlling interest as of 31-Dec-25 includes $3,234mm in debt, $853mm in cash and $165mm in non-controlling interest per management; $646mm of ROU Lease Liabilities as of 31-Dec-25 represents ROU Lease Liabilities based on management estimates used to calculate post-IFRS firm value and EBITDA (post-IFRS) multiples; 1 Day prior to TIM leak; 2 Day prior to MTN cautionary announcement; 3 EBITDAaL (EBITDA after Leases) represents EBITDA (pre-IFRS); 4 EBITDA uses EBITDA (post-IFRS), consistent with IHS financial reporting and broker estimates of EBITDA; 5 Represents implied firm value (pre-IFRS) plus ROU Lease Liabilities of $646mm; 6 Share count based on basic shares outstanding of 335.5mm, 15.0mm options with strike price of nil, and no RSUs or PSUs FV / 2026E EBITDA3 (post-IFRS; post-SBC) 4.2x – 5.9x 5.2x – 9.0x 6.0x – 8.8x 5.5x – 6.5x FV / 2026E EBITDAaL4 (pre-IFRS; post-SBC) 4.2x – 6.1x 5.2x – 9.6x 6.2x – 9.4x 5.6x – 6.8x Metric ($mm), except share prices Low: $3.28 Date: 31-Jan-25 High: $8.04 Date: 13-Jan-26 Range: $6.00 – $17.00 $1,022 Discount rate: 10.00% – 11.00% TGR: 2.00% – 3.00% Implied firm value (post-IFRS) ($mm)5 $4,342 – $6,011 $5,296 – $9,152 $6,134 – $8,945 $5,585 – $6,678 Implied equity value ($mm)6 $1,150 – $2,818 $2,103 – $5,959 $2,941 – $5,753 $2,393 – $3,485 ($ per share) 52-week high / low at market close Management estimates Valuation driver Management estimates Offer price: $8.50 52-week trading range as of 30-Jan-261 Trading multiples: 2026E Adj. EBITDA (post-IFRS; post-SBC) 5-year DCF FOR REFERENCE ONLY $8.04 $17.00 $16.40 $9.90 $3.28 $6.00 $8.40 $6.80 04-Feb-262 : $8.23 30-Jan-261 : $7.99 Price per share Broker estimates Broker A $17.00 Broker C $9.00 Broker D $8.50 Broker B $10.00 Broker F $7.00 Broker G $6.00 Broker E $7.50 Current (13-Feb-26): $8.29 4 |

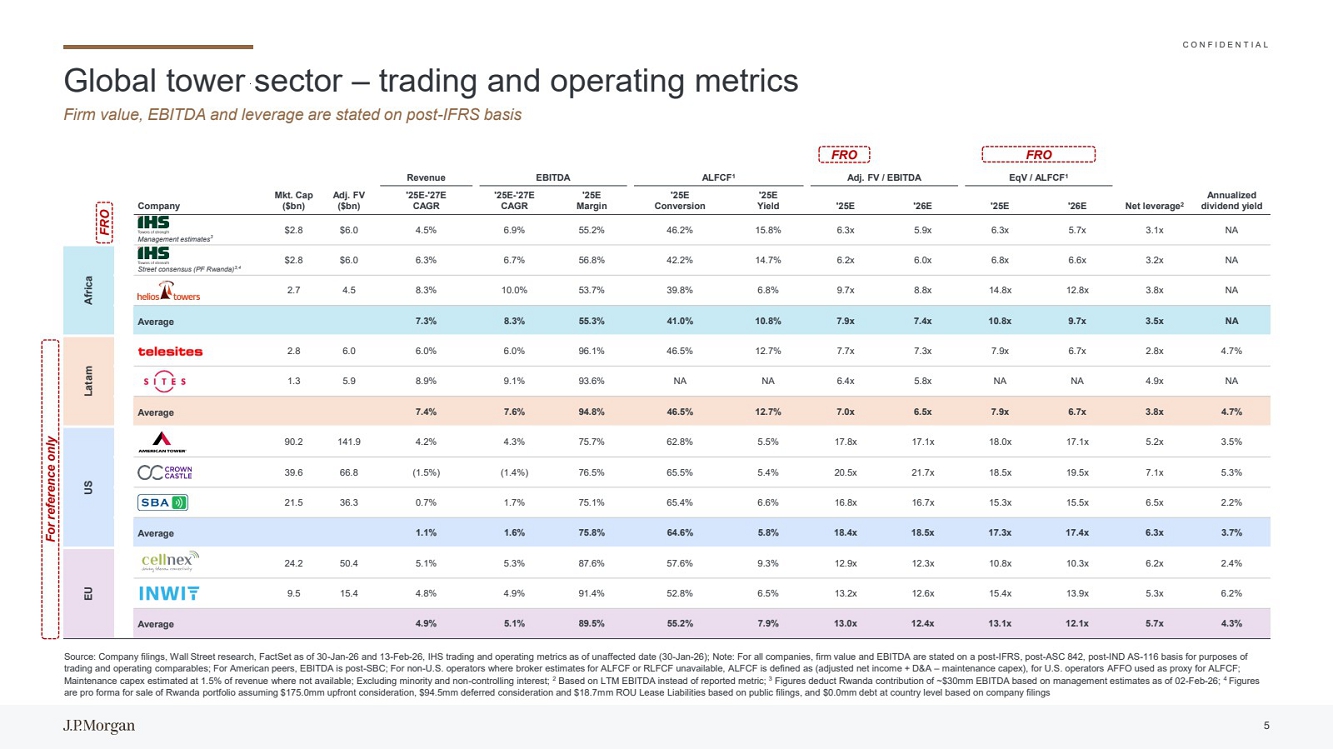

| C O N F I D E N T I A L Global tower sector – trading and operating metrics Firm value, EBITDA and leverage are stated on post-IFRS basis Source: Company filings, Wall Street research, FactSet as of 30-Jan-26 and 13-Feb-26, IHS trading and operating metrics as of unaffected date (30-Jan-26); Note: For all companies, firm value and EBITDA are stated on a post-IFRS, post-ASC 842, post-IND AS-116 basis for purposes of trading and operating comparables; For American peers, EBITDA is post-SBC; For non-U.S. operators where broker estimates for ALFCF or RLFCF unavailable, ALFCF is defined as (adjusted net income + D&A – maintenance capex), for U.S. operators AFFO used as proxy for ALFCF; Maintenance capex estimated at 1.5% of revenue where not available; Excluding minority and non-controlling interest; 2 Based on LTM EBITDA instead of reported metric; 3 Figures deduct Rwanda contribution of ~$30mm EBITDA based on management estimates as of 02-Feb-26; 4 Figures are pro forma for sale of Rwanda portfolio assuming $175.0mm upfront consideration, $94.5mm deferred consideration and $18.7mm ROU Lease Liabilities based on public filings, and $0.0mm debt at country level based on company filings Company Mkt. Cap ($bn) Adj. FV ($bn) Revenue EBITDA ALFCF1 Adj. FV / EBITDA EqV / ALFCF1 Net leverage2 Annualized dividend yield '25E-'27E CAGR '25E-'27E CAGR '25E Margin '25E Conversion '25E Yield '25E '26E '25E '26E Management estimates3 $2.8 $6.0 4.5% 6.9% 55.2% 46.2% 15.8% 6.3x 5.9x 6.3x 5.7x 3.1x NA Africa Street consensus (PF Rwanda)3,4 $2.8 $6.0 6.3% 6.7% 56.8% 42.2% 14.7% 6.2x 6.0x 6.8x 6.6x 3.2x NA 2.7 4.5 8.3% 10.0% 53.7% 39.8% 6.8% 9.7x 8.8x 14.8x 12.8x 3.8x NA Average 7.3% 8.3% 55.3% 41.0% 10.8% 7.9x 7.4x 10.8x 9.7x 3.5x NA Latam 2.8 6.0 6.0% 6.0% 96.1% 46.5% 12.7% 7.7x 7.3x 7.9x 6.7x 2.8x 4.7% 1.3 5.9 8.9% 9.1% 93.6% NA NA 6.4x 5.8x NA NA 4.9x NA Average 7.4% 7.6% 94.8% 46.5% 12.7% 7.0x 6.5x 7.9x 6.7x 3.8x 4.7% US 90.2 141.9 4.2% 4.3% 75.7% 62.8% 5.5% 17.8x 17.1x 18.0x 17.1x 5.2x 3.5% 39.6 66.8 (1.5%) (1.4%) 76.5% 65.5% 5.4% 20.5x 21.7x 18.5x 19.5x 7.1x 5.3% 21.5 36.3 0.7% 1.7% 75.1% 65.4% 6.6% 16.8x 16.7x 15.3x 15.5x 6.5x 2.2% Average 1.1% 1.6% 75.8% 64.6% 5.8% 18.4x 18.5x 17.3x 17.4x 6.3x 3.7% EU 24.2 50.4 5.1% 5.3% 87.6% 57.6% 9.3% 12.9x 12.3x 10.8x 10.3x 6.2x 2.4% 9.5 15.4 4.8% 4.9% 91.4% 52.8% 6.5% 13.2x 12.6x 15.4x 13.9x 5.3x 6.2% Average 4.9% 5.1% 89.5% 55.2% 7.9% 13.0x 12.4x 13.1x 12.1x 5.7x 4.3% For reference only FRO FRO FRO 5 |

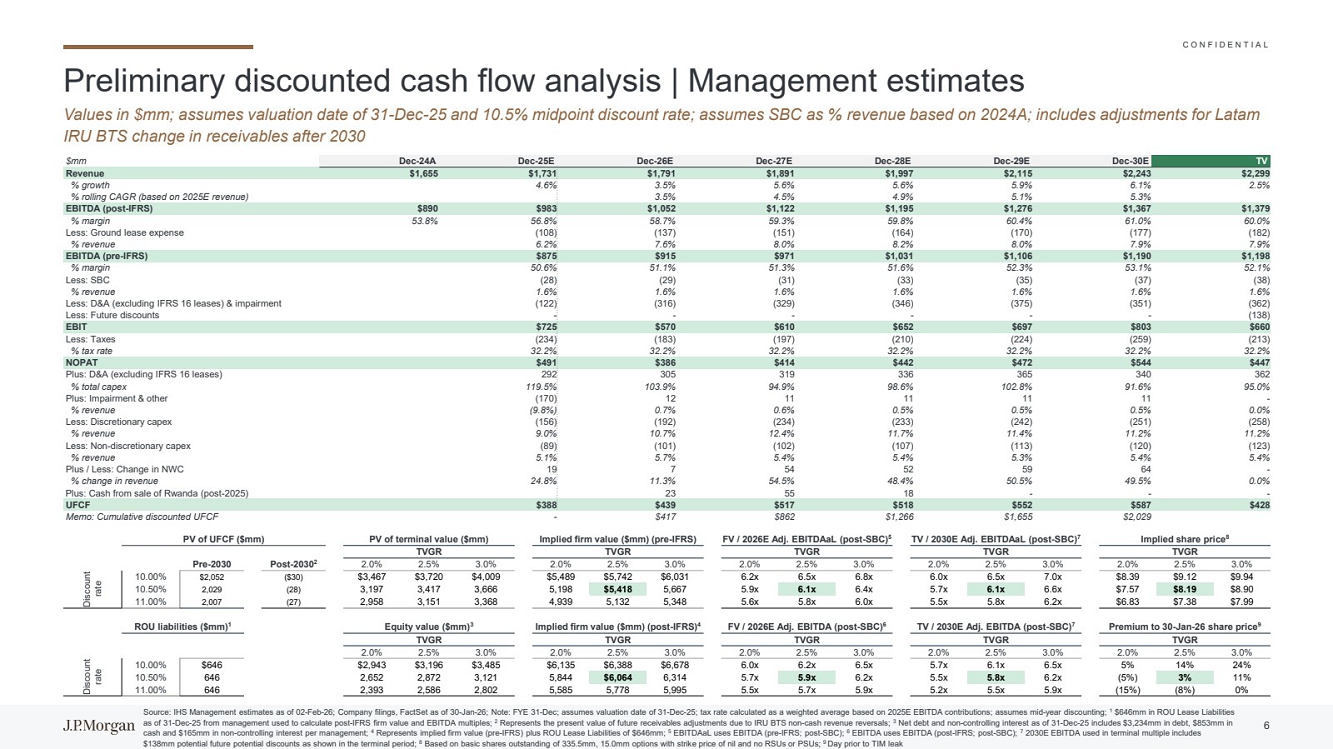

| C O N F I D E N T I A L Preliminary discounted cash flow analysis | Management estimates Values in $mm; assumes valuation date of 31-Dec-25 and 10.5% midpoint discount rate; assumes SBC as % revenue based on 2024A; includes adjustments for Latam IRU BTS change in receivables after 2030 Source: IHS Management estimates as of 02-Feb-26; Company filings, FactSet as of 30-Jan-26; Note: FYE 31-Dec; assumes valuation date of 31-Dec-25; tax rate calculated as a weighted average based on 2025E EBITDA contributions; assumes mid-year discounting; 1 $646mm in ROU Lease Liabilities as of 31-Dec-25 from management used to calculate post-IFRS firm value and EBITDA multiples; 2 Represents the present value of future receivables adjustments due to IRU BTS non-cash revenue reversals; 3 Net debt and non-controlling interest as of 31-Dec-25 includes $3,234mm in debt, $853mm in cash and $165mm in non-controlling interest per management; 4 Represents implied firm value (pre-IFRS) plus ROU Lease Liabilities of $646mm; 5 EBITDAaL uses EBITDA (pre-IFRS; post-SBC); 6 EBITDA uses EBITDA (post-IFRS; post-SBC); 7 2030E EBITDA used in terminal multiple includes $138mm potential future potential discounts as shown in the terminal period; 8 Based on basic shares outstanding of 335.5mm, 15.0mm options with strike price of nil and no RSUs or PSUs; 9 Day prior to TIM leak $mm Dec-24A Dec-25E Dec-26E Dec-27E Dec-28E Dec-29E Dec-30E TV Revenue $1,655 $1,731 $1,791 $1,891 $1,997 $2,115 $2,243 $2,299 % growth 4.6% 3.5% 5.6% 5.6% 5.9% 6.1% 2.5% % rolling CAGR (based on 2025E revenue) 3.5% 4.5% 4.9% 5.1% 5.3% EBITDA (post-IFRS) $890 $983 $1,052 $1,122 $1,195 $1,276 $1,367 $1,379 % margin 53.8% 56.8% 58.7% 59.3% 59.8% 60.4% 61.0% 60.0% Less: Ground lease expense (108) (137) (151) (164) (170) (177) (182) % revenue 6.2% 7.6% 8.0% 8.2% 8.0% 7.9% 7.9% EBITDA (pre-IFRS) $875 $915 $971 $1,031 $1,106 $1,190 $1,198 % margin 50.6% 51.1% 51.3% 51.6% 52.3% 53.1% 52.1% Less: SBC (28) (29) (31) (33) (35) (37) (38) % revenue 1.6% 1.6% 1.6% 1.6% 1.6% 1.6% 1.6% Less: D&A (excluding IFRS 16 leases) & impairment (122) (316) (329) (346) (375) (351) (362) Less: Future discounts - - - - - - (138) EBIT $725 $570 $610 $652 $697 $803 $660 Less: Taxes (234) (183) (197) (210) (224) (259) (213) % tax rate 32.2% 32.2% 32.2% 32.2% 32.2% 32.2% 32.2% NOPAT $491 $386 $414 $442 $472 $544 $447 Plus: D&A (excluding IFRS 16 leases) 292 305 319 336 365 340 362 % total capex 119.5% 103.9% 94.9% 98.6% 102.8% 91.6% 95.0% Plus: Impairment & other (170) 12 11 11 11 11 - % revenue (9.8%) 0.7% 0.6% 0.5% 0.5% 0.5% 0.0% Less: Discretionary capex (156) (192) (234) (233) (242) (251) (258) % revenue 9.0% 10.7% 12.4% 11.7% 11.4% 11.2% 11.2% Less: Non-discretionary capex (89) (101) (102) (107) (113) (120) (123) % revenue 5.1% 5.7% 5.4% 5.4% 5.3% 5.4% 5.4% Plus / Less: Change in NWC 19 7 54 52 59 64 - % change in revenue 24.8% 11.3% 54.5% 48.4% 50.5% 49.5% 0.0% Plus: Cash from sale of Rwanda (post-2025) 23 55 18 - - - UFCF $388 $439 $517 $518 $552 $587 $428 Memo: Cumulative discounted UFCF - $417 $862 $1,266 $1,655 $2,029 PV of UFCF ($mm) PV of terminal value ($mm) Implied firm value ($mm) (pre-IFRS) FV / 2026E Adj. EBITDAaL (post-SBC)5 TV / 2030E Adj. EBITDAaL (post-SBC)7 Implied share price 8 TVGR TVGR TVGR TVGR TVGR Pre-2030 Post-20302 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% Discount rate 10.00% $2,052 ($30) $3,467 $3,720 $4,009 $5,489 $5,742 $6,031 6.2x 6.5x 6.8x 6.0x 6.5x 7.0x $8.39 $9.12 $9.94 10.50% 2,029 (28) 3,197 3,417 3,666 5,198 $5,418 5,667 5.9x 6.1x 6.4x 5.7x 6.1x 6.6x $7.57 $8.19 $8.90 11.00% 2,007 (27) 2,958 3,151 3,368 4,939 5,132 5,348 5.6x 5.8x 6.0x 5.5x 5.8x 6.2x $6.83 $7.38 $7.99 ROU liabilities ($mm)1 Equity value ($mm)3 Implied firm value ($mm) (post-IFRS)4 FV / 2026E Adj. EBITDA (post-SBC)6 TV / 2030E Adj. EBITDA (post-SBC)7 Premium to 30-Jan-26 share price 9 TVGR TVGR TVGR TVGR TVGR 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% Discount rate 10.00% $646 $2,943 $3,196 $3,485 $6,135 $6,388 $6,678 6.0x 6.2x 6.5x 5.7x 6.1x 6.5x 5% 14% 24% 10.50% 646 2,652 2,872 3,121 5,844 $6,064 6,314 5.7x 5.9x 6.2x 5.5x 5.8x 6.2x (5%) 3% 11% 11.00% 646 2,393 2,586 2,802 5,585 5,778 5,995 5.5x 5.7x 5.9x 5.2x 5.5x 5.9x (15%) (8%) 0% 6 |

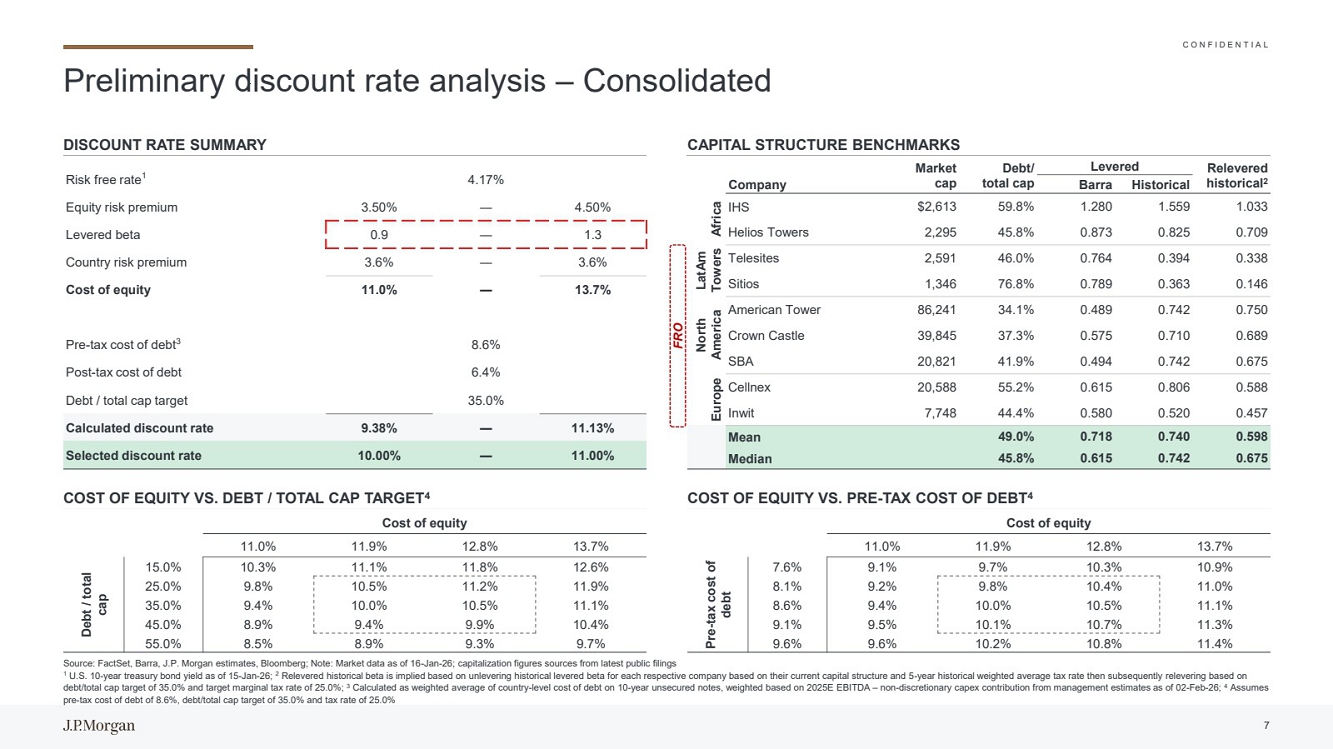

| C O N F I D E N T I A L Preliminary discount rate analysis – Consolidated Source: FactSet, Barra, J.P. Morgan estimates, Bloomberg; Note: Market data as of 16-Jan-26; capitalization figures sources from latest public filings 1 U.S. 10-year treasury bond yield as of 15-Jan-26; 2 Relevered historical beta is implied based on unlevering historical levered beta for each respective company based on their current capital structure and 5-year historical weighted average tax rate then subsequently relevering based on debt/total cap target of 35.0% and target marginal tax rate of 25.0%; 3 Calculated as weighted average of country-level cost of debt on 10-year unsecured notes, weighted based on 2025E EBITDA – non-discretionary capex contribution from management estimates as of 02-Feb-26; 4 Assumes pre-tax cost of debt of 8.6%, debt/total cap target of 35.0% and tax rate of 25.0% DISCOUNT RATE SUMMARY CAPITAL STRUCTURE BENCHMARKS Risk free rate1 4.17% Equity risk premium 3.50% ― 4.50% Levered beta 0.9 ― 1.3 Country risk premium 3.6% ― 3.6% Cost of equity 11.0% ― 13.7% Pre-tax cost of debt3 8.6% Post-tax cost of debt 6.4% Debt / total cap target 35.0% Calculated discount rate 9.38% ― 11.13% Selected discount rate 10.00% ― 11.00% Market cap Debt/ total cap Levered Relevered historical 2 Company Barra Historical Africa IHS $2,613 59.8% 1.280 1.559 1.033 Helios Towers 2,295 45.8% 0.873 0.825 0.709 LatAm Towers Telesites 2,591 46.0% 0.764 0.394 0.338 Sitios 1,346 76.8% 0.789 0.363 0.146 North America American Tower 86,241 34.1% 0.489 0.742 0.750 Crown Castle 39,845 37.3% 0.575 0.710 0.689 SBA 20,821 41.9% 0.494 0.742 0.675 Europe Cellnex 20,588 55.2% 0.615 0.806 0.588 Inwit 7,748 44.4% 0.580 0.520 0.457 Mean 49.0% 0.718 0.740 0.598 Median 45.8% 0.615 0.742 0.675 COST OF EQUITY VS. DEBT / TOTAL CAP TARGET4 COST OF EQUITY VS. PRE-TAX COST OF DEBT4 Cost of equity 11.0% 11.9% 12.8% 13.7% Pre-tax cost of debt 7.6% 9.1% 9.7% 10.3% 10.9% 8.1% 9.2% 9.8% 10.4% 11.0% 8.6% 9.4% 10.0% 10.5% 11.1% 9.1% 9.5% 10.1% 10.7% 11.3% 9.6% 9.6% 10.2% 10.8% 11.4% FRO Cost of equity 11.0% 11.9% 12.8% 13.7% Debt / total cap 15.0% 10.3% 11.1% 11.8% 12.6% 25.0% 9.8% 10.5% 11.2% 11.9% 35.0% 9.4% 10.0% 10.5% 11.1% 45.0% 8.9% 9.4% 9.9% 10.4% 55.0% 8.5% 8.9% 9.3% 9.7% 7 |

| C O N F I D E N T I A L Agenda Page 1 Appendix 8 |

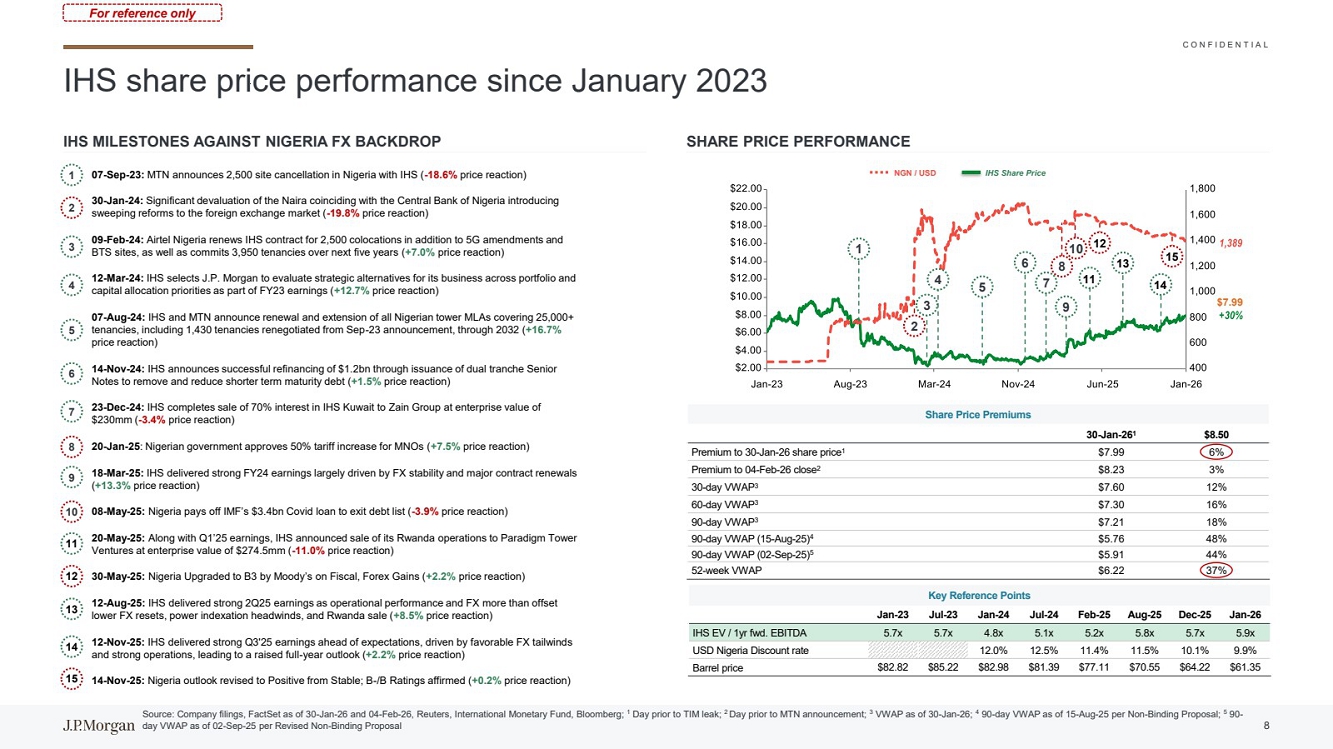

| C O N F I D E N T I A L 13 11 14 15 12 11 12 13 14 15 IHS share price performance since January 2023 Source: Company filings, FactSet as of 30-Jan-26 and 04-Feb-26, Reuters, International Monetary Fund, Bloomberg; 1 Day prior to TIM leak; 2 Day prior to MTN announcement; 3 VWAP as of 30-Jan-26; 4 90-day VWAP as of 15-Aug-25 per Non-Binding Proposal; 5 90- day VWAP as of 02-Sep-25 per Revised Non-Binding Proposal For reference only IHS MILESTONES AGAINST NIGERIA FX BACKDROP Key Reference Points Jan-23 Jul-23 Jan-24 Jul-24 Feb-25 Aug-25 Dec-25 Jan-26 IHS EV / 1yr fwd. EBITDA 5.7x 5.7x 4.8x 5.1x 5.2x 5.8x 5.7x 5.9x USD Nigeria Discount rate 12.0% 12.5% 11.4% 11.5% 10.1% 9.9% Barrel price $82.82 $85.22 $82.98 $81.39 $77.11 $70.55 $64.22 $61.35 Share Price Premiums 30-Jan-261 $8.50 Premium to 30-Jan-26 share price1 $7.99 6% Premium to 04-Feb-26 close2 $8.23 3% 30-day VWAP3 $7.60 12% 60-day VWAP3 $7.30 16% 90-day VWAP3 $7.21 18% 90-day VWAP (15-Aug-25)4 $5.76 48% 90-day VWAP (02-Sep-25)5 $5.91 44% 52-week VWAP $6.22 37% 6 5 7 9 8 10 1 4 2 3 07-Sep-23: MTN announces 2,500 site cancellation in Nigeria with IHS (-18.6% price reaction) 30-Jan-24: Significant devaluation of the Naira coinciding with the Central Bank of Nigeria introducing sweeping reforms to the foreign exchange market (-19.8% price reaction) 09-Feb-24: Airtel Nigeria renews IHS contract for 2,500 colocations in addition to 5G amendments and BTS sites, as well as commits 3,950 tenancies over next five years (+7.0% price reaction) 12-Mar-24: IHS selects J.P. Morgan to evaluate strategic alternatives for its business across portfolio and capital allocation priorities as part of FY23 earnings (+12.7% price reaction) 07-Aug-24: IHS and MTN announce renewal and extension of all Nigerian tower MLAs covering 25,000+ tenancies, including 1,430 tenancies renegotiated from Sep-23 announcement, through 2032 (+16.7% price reaction) 14-Nov-24: IHS announces successful refinancing of $1.2bn through issuance of dual tranche Senior Notes to remove and reduce shorter term maturity debt (+1.5% price reaction) 23-Dec-24: IHS completes sale of 70% interest in IHS Kuwait to Zain Group at enterprise value of $230mm (-3.4% price reaction) 20-Jan-25: Nigerian government approves 50% tariff increase for MNOs (+7.5% price reaction) 18-Mar-25: IHS delivered strong FY24 earnings largely driven by FX stability and major contract renewals (+13.3% price reaction) 08-May-25: Nigeria pays off IMF’s $3.4bn Covid loan to exit debt list (-3.9% price reaction) 20-May-25: Along with Q1’25 earnings, IHS announced sale of its Rwanda operations to Paradigm Tower Ventures at enterprise value of $274.5mm (-11.0% price reaction) 30-May-25: Nigeria Upgraded to B3 by Moody’s on Fiscal, Forex Gains (+2.2% price reaction) 12-Aug-25: IHS delivered strong 2Q25 earnings as operational performance and FX more than offset lower FX resets, power indexation headwinds, and Rwanda sale (+8.5% price reaction) 12-Nov-25: IHS delivered strong Q3'25 earnings ahead of expectations, driven by favorable FX tailwinds and strong operations, leading to a raised full-year outlook (+2.2% price reaction) 14-Nov-25: Nigeria outlook revised to Positive from Stable; B-/B Ratings affirmed (+0.2% price reaction) NGN / USD IHS Share Price 1 5 6 7 9 8 10 $7.99 4 2 3 SHARE PRICE PERFORMANCE 8 |

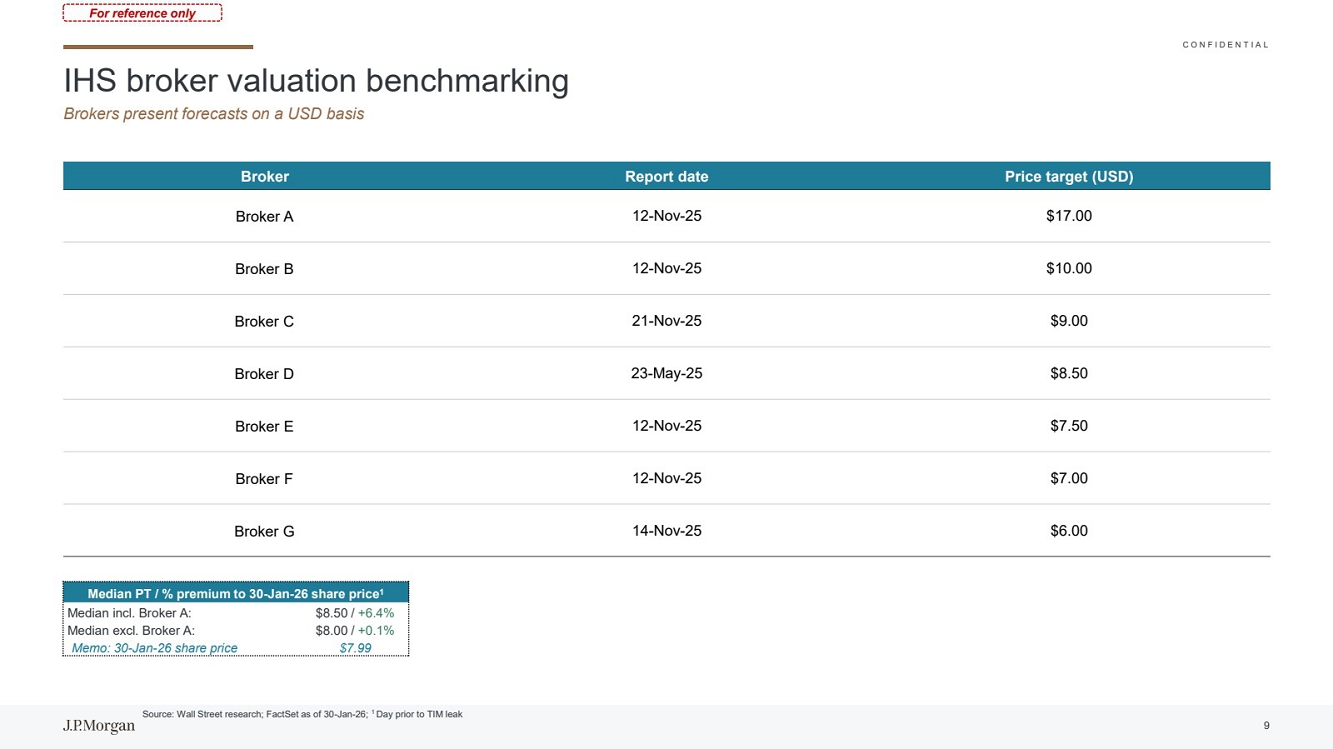

| C O N F I D E N T I A L IHS broker valuation benchmarking Brokers present forecasts on a USD basis Source: Wall Street research; FactSet as of 30-Jan-26; 1 Day prior to TIM leak Broker Report date Price target (USD) Broker A 12-Nov-25 $17.00 Broker B 12-Nov-25 $10.00 Broker C 21-Nov-25 $9.00 Broker D 23-May-25 $8.50 Broker E 12-Nov-25 $7.50 Broker F 12-Nov-25 $7.00 Broker G 14-Nov-25 $6.00 Median PT / % premium to 30-Jan-26 share price1 Median incl. Broker A: $8.50 / +6.4% Median excl. Broker A: $8.00 / +0.1% Memo: 30-Jan-26 share price $7.99 For reference only 9 |

| C O N F I D E N T I A L Disclaimer This presentation was prepared exclusively for the benefit and internal use of the J.P. Morgan client to whom it is directly addressed and delivered (including such client’s subsidiaries, the “Company”) in order to assist the Company in evaluating, on a preliminary basis, the feasibility of a possible transaction or transactions and does not carry any right of publication or disclosure, in whole or in part, to any other party. This presentation is for discussion purposes only and is incomplete without reference to, and should be viewed solely in conjunction with, the oral briefing provided by J.P. Morgan. Neither this presentation nor any of its contents may be disclosed or used for any other purpose without the prior written consent of J.P. Morgan. Additionally, this presentation may contain content initially generated by AI or other automated technologies. The information in this presentation is based upon any management forecasts supplied to us and reflects prevailing conditions and our views as of this date, all of which are accordingly subject to change. J.P. Morgan’s opinions and estimates constitute J.P. Morgan’s judgment and should be regarded as indicative, preliminary and for illustrative purposes only. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Company or which was otherwise reviewed by us. In addition, our analyses are not and do not purport to be appraisals of the assets, stock, or business of the Company or any other entity. J.P. Morgan makes no representations as to the actual value which may be received in connection with a transaction nor the legal, tax or accounting effects of consummating a transaction. Unless expressly contemplated hereby, the information in this presentation does not take into account the effects of a possible transaction or transactions involving an actual or potential change of control, which may have significant valuation and other effects. Notwithstanding anything herein to the contrary, the Company and each of its employees, representatives or other agents may disclose to any and all persons, without limitation of any kind, the U.S. federal and state income tax treatment and the U.S. federal and state income tax structure of the transactions contemplated hereby and all materials of any kind (including opinions or other tax analyses) that are provided to the Company relating to such tax treatment and tax structure insofar as such treatment and/or structure relates to a U.S. federal or state income tax strategy provided to the Company by J.P. Morgan. J.P. Morgan's policies on data privacy can be found at http://www.jpmorgan.com/pages/privacy. J.P. Morgan is a party to the SEC Research Settlement and as such, is generally not permitted to utilize the firm's research capabilities in pitching for investment banking business. All views contained in this presentation are the views of J.P. Morgan’s Investment Bank, not the Research Department. J.P. Morgan’s policies prohibit employees from offering, directly or indirectly, a favorable research rating or specific price target, or offering to change a rating or price target, to a subject company as consideration or inducement for the receipt of business or for compensation. J.P. Morgan also prohibits its research analysts from being compensated for involvement in investment banking transactions except to the extent that such participation is intended to benefit investors. Changes to Interbank Offered Rates (IBORs) and other benchmark rates: Certain interest rate benchmarks are, or may in the future become, subject to ongoing international, national and other regulatory guidance, reform and proposals for reform. For more information, please consult: https://www.jpmorgan.com/global/disclosures/interbank_offered_rates JPMorgan Chase & Co. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters included herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone not affiliated with JPMorgan Chase & Co. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties. J.P. Morgan is a marketing name for investment businesses of JPMorgan Chase & Co. and its subsidiaries and affiliates worldwide. Securities, syndicated loan arranging, financial advisory, lending, derivatives and other investment banking and commercial banking activities are performed by a combination of J.P. Morgan Securities LLC, J.P. Morgan Securities plc, J.P. Morgan SE, JPMorgan Chase Bank, N.A. and the appropriately licensed subsidiaries and affiliates of JPMorgan Chase & Co. worldwide. J.P. Morgan deal team members may be employees of any of the foregoing entities. J.P. Morgan Securities plc is authorized by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. J.P. Morgan SE is authorised as a credit institution by the German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht, BaFin) and jointly supervised by the BaFin, the German Central Bank (Deutsche Bundesbank) and the European Central Bank (ECB). For information on any J.P. Morgan German legal entity see: https://www.jpmorgan.com/country/US/en/disclosures/legal-entity-information#germany. For information on any other J.P. Morgan legal entity see: https://www.jpmorgan.com/country/GB/EN/disclosures/investment-bank-legal-entity-disclosures. JPMS LLC intermediates securities transactions effected by its non-U.S. affiliates for or with its U.S. clients when appropriate and in accordance with Rule 15a-6 under the Securities Exchange Act of 1934. Please consult: www.jpmorgan.com/securities-transactions This presentation does not constitute a commitment by any J.P. Morgan entity to underwrite, subscribe for or place any securities or to extend or arrange credit or to provide any other services. Copyright 2026 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A., organized under the laws of U.S.A. with limited liability. |