| PROJECT MANGO | NON-BINDING PROPOSAL SUMMARY 28 AUGUST 2025 |

| 2 EXECUTIVE SUMMARY On 19-August-25 MTN Group submitted a Non-Binding Proposal to acquire IHS Holding Limited for an all-cash offer price of $7.50 / share (the “Cash Offer”) Cash Offer represents premium of 30% to IHS’ 90-day volume weighted average share price (VWAP) of $5.76 as of 15-Aug-25 As of 22-Aug-25, represents 6% premium to current and 15% premium to 30-day VWAP During Strategic Review process, there has been interest in IHS’ country-level asset portfolios from different geographically-focused bidders, however there are few buyers interested in WholeCo Proposed Transaction conditioned upon IHS Latam (Towers and I-Systems) being disposed for cash consideration at a valuation of not less than 10.0x 2025E EBITDAaL ($1.1bn firm value), with proceeds from disposal received by IHS prior to the consummation of the Proposed Transaction Project Iguazu (Latam Towers) engaged with 5 financial sponsors (Actis, CDPQ, I Squared, Macquarie, OTPP) and expecting Non-Binding Offers by the week of 08-Sep-25 Project Mancini (I-Systems) conversations progressing with TIM Brasil and parent Telecom Italia after receipt of Non-Binding Offer on 04-Aug-25 Proposed response for Board’s consideration to be delivered by J.P. Morgan to MTN’s advisors, Bank of America and Citi, focusing on: Counterproposal of an increased Cash offer [range TBD] Cash Offer does not reflect full Cash on IHS’ Balance Sheet, Rwanda sale proceeds, or potential Holding company synergies Removing firm value threshold for Latam disposal and maintaining flexibility for an alternative structure in both parties’ interest to ensure deal certainty |

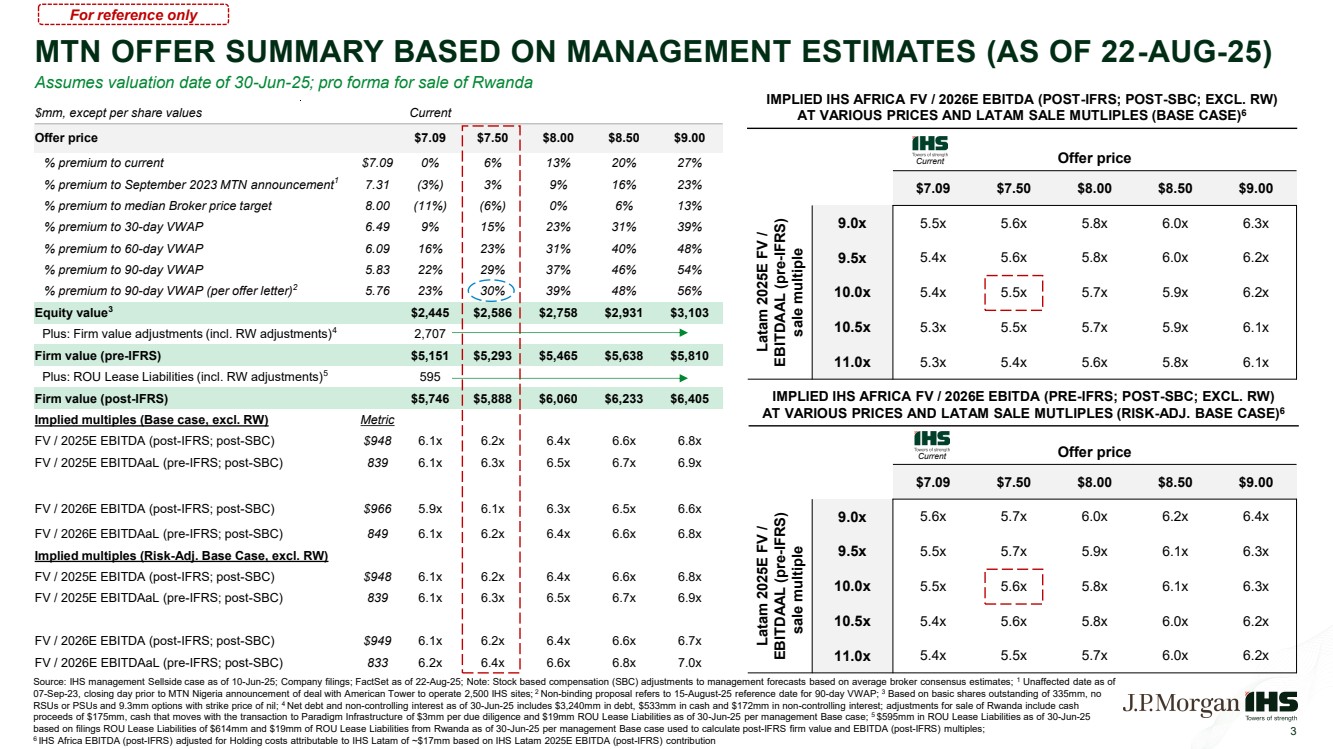

| 3 MTN OFFER SUMMARY BASED ON MANAGEMENT ESTIMATES (AS OF 22-AUG-25) $mm, except per share values Current Offer price $7.09 $7.50 $8.00 $8.50 $9.00 % premium to current $7.09 0% 6% 13% 20% 27% % premium to September 2023 MTN announcement1 7.31 (3%) 3% 9% 16% 23% % premium to median Broker price target 8.00 (11%) (6%) 0% 6% 13% % premium to 30-day VWAP 6.49 9% 15% 23% 31% 39% % premium to 60-day VWAP 6.09 16% 23% 31% 40% 48% % premium to 90-day VWAP 5.83 22% 29% 37% 46% 54% % premium to 90-day VWAP (per offer letter)2 5.76 23% 30% 39% 48% 56% Equity value3 $2,445 $2,586 $2,758 $2,931 $3,103 Plus: Firm value adjustments (incl. RW adjustments)4 2,707 2,707 2,707 2,707 2,707 Firm value (pre-IFRS) $5,151 $5,293 $5,465 $5,638 $5,810 Plus: ROU Lease Liabilities (incl. RW adjustments)5 595 595 595 595 595 Firm value (post-IFRS) $5,746 $5,888 $6,060 $6,233 $6,405 Implied multiples (Base case, excl. RW) Metric FV / 2025E EBITDA (post-IFRS; post-SBC) $948 6.1x 6.2x 6.4x 6.6x 6.8x FV / 2025E EBITDAaL (pre-IFRS; post-SBC) 839 6.1x 6.3x 6.5x 6.7x 6.9x FV / 2026E EBITDA (post-IFRS; post-SBC) $966 5.9x 6.1x 6.3x 6.5x 6.6x FV / 2026E EBITDAaL (pre-IFRS; post-SBC) 849 6.1x 6.2x 6.4x 6.6x 6.8x Implied multiples (Risk-Adj. Base Case, excl. RW) FV / 2025E EBITDA (post-IFRS; post-SBC) $948 6.1x 6.2x 6.4x 6.6x 6.8x FV / 2025E EBITDAaL (pre-IFRS; post-SBC) 839 6.1x 6.3x 6.5x 6.7x 6.9x FV / 2026E EBITDA (post-IFRS; post-SBC) $949 6.1x 6.2x 6.4x 6.6x 6.7x FV / 2026E EBITDAaL (pre-IFRS; post-SBC) 833 6.2x 6.4x 6.6x 6.8x 7.0x Offer price $7.09 $7.50 $8.00 $8.50 $9.00 Latam 2025E FV / EBITDAAL (pre-IFRS) sale multiple 9.0x 5.6x 5.7x 6.0x 6.2x 6.4x 9.5x 5.5x 5.7x 5.9x 6.1x 6.3x 10.0x 5.5x 5.6x 5.8x 6.1x 6.3x 10.5x 5.4x 5.6x 5.8x 6.0x 6.2x 11.0x 5.4x 5.5x 5.7x 6.0x 6.2x Source: IHS management Sellside case as of 10-Jun-25; Company filings; FactSet as of 22-Aug-25; Note: Stock based compensation (SBC) adjustments to management forecasts based on average broker consensus estimates; 1 Unaffected date as of 07-Sep-23, closing day prior to MTN Nigeria announcement of deal with American Tower to operate 2,500 IHS sites; 2 Non-binding proposal refers to 15-August-25 reference date for 90-day VWAP; 3 Based on basic shares outstanding of 335mm, no RSUs or PSUs and 9.3mm options with strike price of nil; 4 Net debt and non-controlling interest as of 30-Jun-25 includes $3,240mm in debt, $533mm in cash and $172mm in non-controlling interest; adjustments for sale of Rwanda include cash proceeds of $175mm, cash that moves with the transaction to Paradigm Infrastructure of $3mm per due diligence and $19mm ROU Lease Liabilities as of 30-Jun-25 per management Base case; 5 $595mm in ROU Lease Liabilities as of 30-Jun-25 based on filings ROU Lease Liabilities of $614mm and $19mm of ROU Lease Liabilities from Rwanda as of 30-Jun-25 per management Base case used to calculate post-IFRS firm value and EBITDA (post-IFRS) multiples; 6 IHS Africa EBITDA (post-IFRS) adjusted for Holding costs attributable to IHS Latam of ~$17mm based on IHS Latam 2025E EBITDA (post-IFRS) contribution Offer price $7.09 $7.50 $8.00 $8.50 $9.00 Latam 2025E FV / EBITDAAL (pre-IFRS) sale multiple 9.0x 5.5x 5.6x 5.8x 6.0x 6.3x 9.5x 5.4x 5.6x 5.8x 6.0x 6.2x 10.0x 5.4x 5.5x 5.7x 5.9x 6.2x 10.5x 5.3x 5.5x 5.7x 5.9x 6.1x 11.0x 5.3x 5.4x 5.6x 5.8x 6.1x Current Current IMPLIED IHS AFRICA FV / 2026E EBITDA (POST-IFRS; POST-SBC; EXCL. RW) AT VARIOUS PRICES AND LATAM SALE MUTLIPLES (BASE CASE)6 IMPLIED IHS AFRICA FV / 2026E EBITDA (PRE-IFRS; POST-SBC; EXCL. RW) AT VARIOUS PRICES AND LATAM SALE MUTLIPLES (RISK-ADJ. BASE CASE)6 For reference only Assumes valuation date of 30-Jun-25; pro forma for sale of Rwanda |

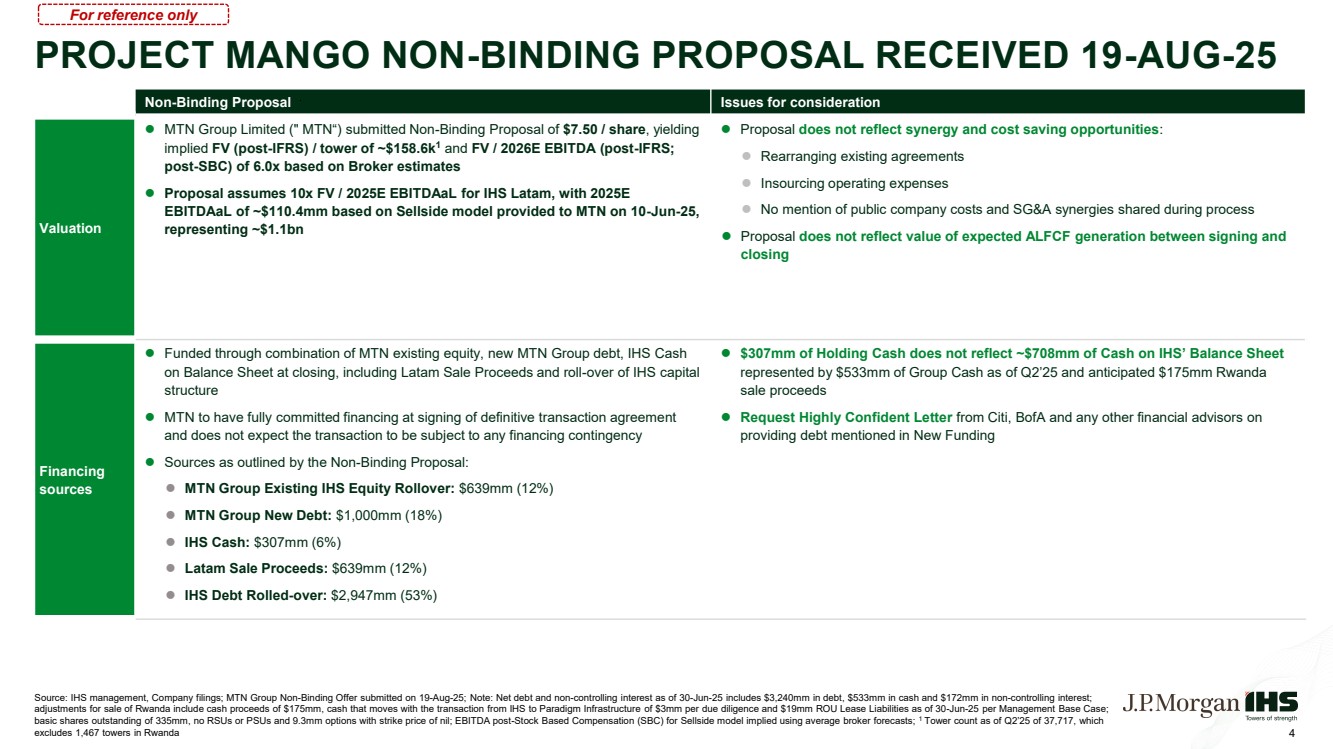

| PROJECT MANGO NON-BINDING PROPOSAL RECEIVED 19-AUG-25 Non-Binding Proposal Issues for consideration Valuation MTN Group Limited (" MTN“) submitted Non-Binding Proposal of $7.50 / share, yielding implied FV (post-IFRS) / tower of ~$158.6k1 and FV / 2026E EBITDA (post-IFRS; post-SBC) of 6.0x based on Broker estimates Proposal assumes 10x FV / 2025E EBITDAaL for IHS Latam, with 2025E EBITDAaL of ~$110.4mm based on Sellside model provided to MTN on 10-Jun-25, representing ~$1.1bn Proposal does not reflect synergy and cost saving opportunities: Rearranging existing agreements Insourcing operating expenses No mention of public company costs and SG&A synergies shared during process Proposal does not reflect value of expected ALFCF generation between signing and closing Financing sources Funded through combination of MTN existing equity, new MTN Group debt, IHS Cash on Balance Sheet at closing, including Latam Sale Proceeds and roll-over of IHS capital structure MTN to have fully committed financing at signing of definitive transaction agreement and does not expect the transaction to be subject to any financing contingency Sources as outlined by the Non-Binding Proposal: MTN Group Existing IHS Equity Rollover: $639mm (12%) MTN Group New Debt: $1,000mm (18%) IHS Cash: $307mm (6%) Latam Sale Proceeds: $639mm (12%) IHS Debt Rolled-over: $2,947mm (53%) $307mm of Holding Cash does not reflect ~$708mm of Cash on IHS’ Balance Sheet represented by $533mm of Group Cash as of Q2’25 and anticipated $175mm Rwanda sale proceeds Request Highly Confident Letter from Citi, BofA and any other financial advisors on providing debt mentioned in New Funding 4 Source: IHS management, Company filings; MTN Group Non-Binding Offer submitted on 19-Aug-25; Note: Net debt and non-controlling interest as of 30-Jun-25 includes $3,240mm in debt, $533mm in cash and $172mm in non-controlling interest; adjustments for sale of Rwanda include cash proceeds of $175mm, cash that moves with the transaction from IHS to Paradigm Infrastructure of $3mm per due diligence and $19mm ROU Lease Liabilities as of 30-Jun-25 per Management Base Case; basic shares outstanding of 335mm, no RSUs or PSUs and 9.3mm options with strike price of nil; EBITDA post-Stock Based Compensation (SBC) for Sellside model implied using average broker forecasts; 1 Tower count as of Q2’25 of 37,717, which excludes 1,467 towers in Rwanda For reference only |

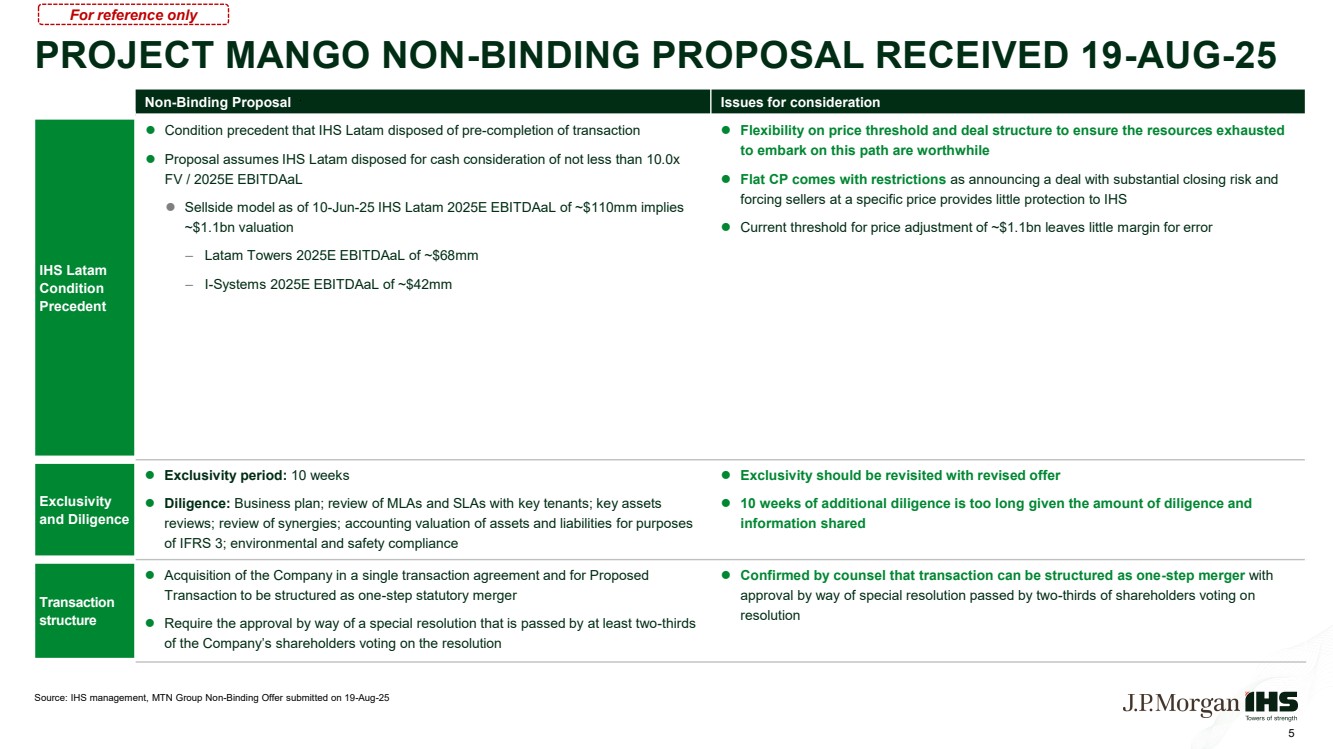

| PROJECT MANGO NON-BINDING PROPOSAL RECEIVED 19-AUG-25 Non-Binding Proposal Issues for consideration IHS Latam Condition Precedent Condition precedent that IHS Latam disposed of pre-completion of transaction Proposal assumes IHS Latam disposed for cash consideration of not less than 10.0x FV / 2025E EBITDAaL Sellside model as of 10-Jun-25 IHS Latam 2025E EBITDAaL of ~$110mm implies ~$1.1bn valuation – Latam Towers 2025E EBITDAaL of ~$68mm – I-Systems 2025E EBITDAaL of ~$42mm Flexibility on price threshold and deal structure to ensure the resources exhausted to embark on this path are worthwhile Flat CP comes with restrictions as announcing a deal with substantial closing risk and forcing sellers at a specific price provides little protection to IHS Current threshold for price adjustment of ~$1.1bn leaves little margin for error Exclusivity and Diligence Exclusivity period: 10 weeks Diligence: Business plan; review of MLAs and SLAs with key tenants; key assets reviews; review of synergies; accounting valuation of assets and liabilities for purposes of IFRS 3; environmental and safety compliance Exclusivity should be revisited with revised offer 10 weeks of additional diligence is too long given the amount of diligence and information shared Transaction structure Acquisition of the Company in a single transaction agreement and for Proposed Transaction to be structured as one-step statutory merger Require the approval by way of a special resolution that is passed by at least two-thirds of the Company’s shareholders voting on the resolution Confirmed by counsel that transaction can be structured as one-step merger with approval by way of special resolution passed by two-thirds of shareholders voting on resolution 5 For reference only Source: IHS management, MTN Group Non-Binding Offer submitted on 19-Aug-25 |

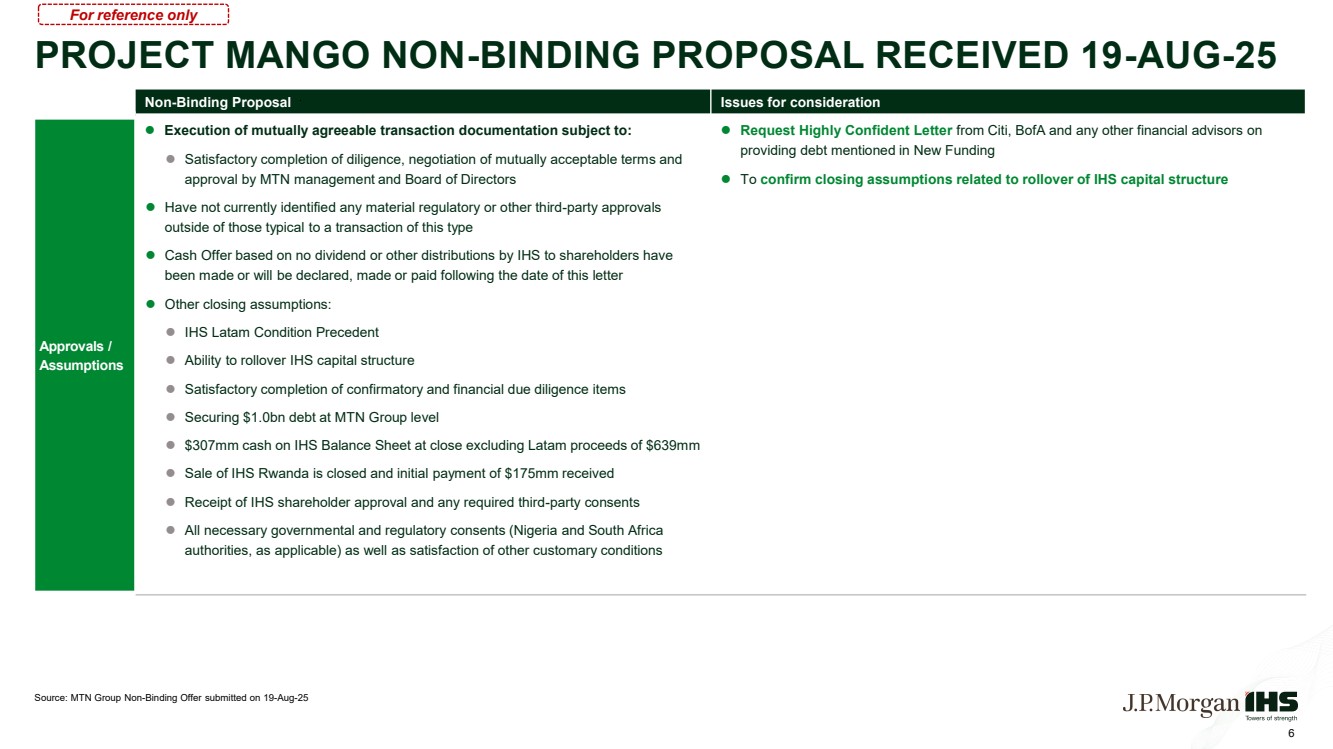

| PROJECT MANGO NON-BINDING PROPOSAL RECEIVED 19-AUG-25 Non-Binding Proposal Issues for consideration Approvals / Assumptions Execution of mutually agreeable transaction documentation subject to: Satisfactory completion of diligence, negotiation of mutually acceptable terms and approval by MTN management and Board of Directors Have not currently identified any material regulatory or other third-party approvals outside of those typical to a transaction of this type Cash Offer based on no dividend or other distributions by IHS to shareholders have been made or will be declared, made or paid following the date of this letter Other closing assumptions: IHS Latam Condition Precedent Ability to rollover IHS capital structure Satisfactory completion of confirmatory and financial due diligence items Securing $1.0bn debt at MTN Group level $307mm cash on IHS Balance Sheet at close excluding Latam proceeds of $639mm Sale of IHS Rwanda is closed and initial payment of $175mm received Receipt of IHS shareholder approval and any required third-party consents All necessary governmental and regulatory consents (Nigeria and South Africa authorities, as applicable) as well as satisfaction of other customary conditions Request Highly Confident Letter from Citi, BofA and any other financial advisors on providing debt mentioned in New Funding To confirm closing assumptions related to rollover of IHS capital structure 6 For reference only Source: MTN Group Non-Binding Offer submitted on 19-Aug-25 |

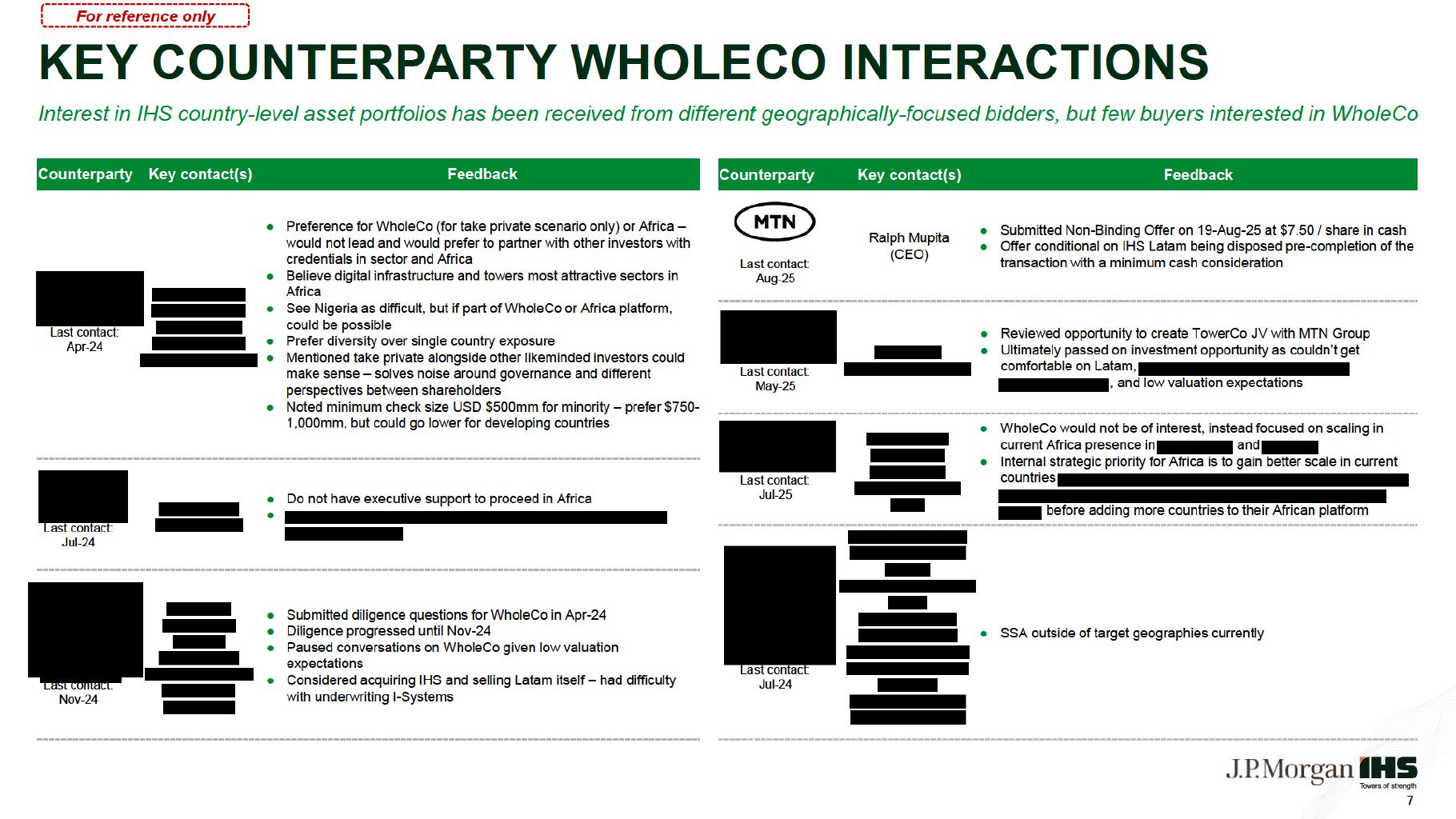

| Counterparty Key contact(s) Feedback Ralph Mupita (CEO) ● Submitted Non-Binding Offer on 19-Aug-25 at $7.50 / share in cash ● Offer conditional on IHS Latam being disposed pre-completion of the transaction with a minimum cash consideration Sunil Mittal (Founder, Chairman) ● Reviewed opportunity to create TowerCo JV with MTN Group ● Ultimately passed on investment opportunity as couldn’t get comfortable on Latam, operations in only two IHS markets post-Rwanda sale, and low valuation expectations Neil Seidman (SVP, M&A) Junaid Shafi (VP, International M&A) ● WholeCo would not be of interest, instead focused on scaling in current Africa presence in South Africa and Tanzania ● Internal strategic priority for Africa is to gain better scale in current countries (#4 independent TowerCo in South Africa behind Swiftnet, IHS and AMT, and #2 independent TowerCo in Tanzania behind Helios) before adding more countries to their African platform Emmanuel Léonard (Chief International Officer) Mohammed Alhakbani (CEO) Steven Marshall (Board Member, Former EVP of AMT and President of US Business) Charles Desjardins (General Manager) ● SSA outside of target geographies currently Counterparty Key contact(s) Feedback Mamoun Jamai (Head of Digital Infrastructure) Blake Calogero (Portfolio Manager) ● Preference for WholeCo (for take private scenario only) or Africa – would not lead and would prefer to partner with other investors with credentials in sector and Africa ● Believe digital infrastructure and towers most attractive sectors in Africa ● See Nigeria as difficult, but if part of WholeCo or Africa platform, could be possible ● Prefer diversity over single country exposure ● Mentioned take private alongside other likeminded investors could make sense – solves noise around governance and different perspectives between shareholders ● Noted minimum check size USD $500mm for minority – prefer $750- 1,000mm, but could go lower for developing countries Robin Weber (VP, M&A BD) ● Do not have executive support to proceed in Africa ● In 2025, CEO, Steve Vondran publicly commenting on focus on Developed Markets Jas Khaira (Sr. MD, BX TacOps) John Watson (MD, BX TacOps) Chad Crank (MD, Grain) ● Submitted diligence questions for WholeCo in Apr-24 ● Diligence progressed until Nov-24 ● Paused conversations on WholeCo given low valuation expectations ● Considered acquiring IHS and selling Latam itself – had difficulty with underwriting I-Systems KEY COUNTERPARTY WHOLECO INTERACTIONS 7 Last contact: Apr-24 Last contact: Jul-24 TacOps Last contact: Nov-24 Last contact: Jul-25 Last contact: Jul-24 For reference only Interest in IHS country-level asset portfolios has been received from different geographically-focused bidders, but few buyers interested in WholeCo Last contact: May-25 Last contact: Aug-25 |

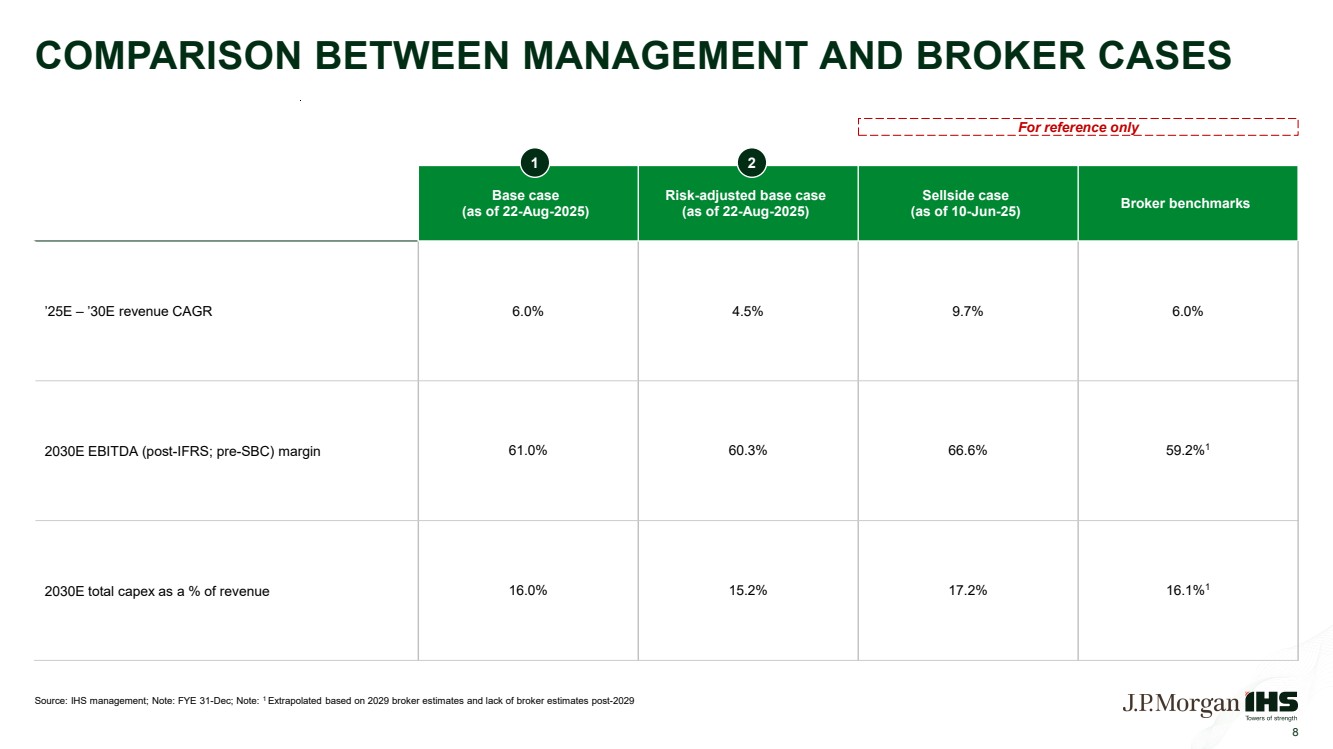

| Source: IHS management; Note: FYE 31-Dec; Note: 1 Extrapolated based on 2029 broker estimates and lack of broker estimates post-2029 8 COMPARISON BETWEEN MANAGEMENT AND BROKER CASES Base case (as of 22-Aug-2025) Risk-adjusted base case (as of 22-Aug-2025) Sellside case (as of 10-Jun-25) Broker benchmarks ’25E – ’30E revenue CAGR 6.0% 4.5% 9.7% 6.0% 2030E EBITDA (post-IFRS; pre-SBC) margin 61.0% 60.3% 66.6% 59.2%1 2030E total capex as a % of revenue 16.0% 15.2% 17.2% 16.1%1 1 2 For reference only |

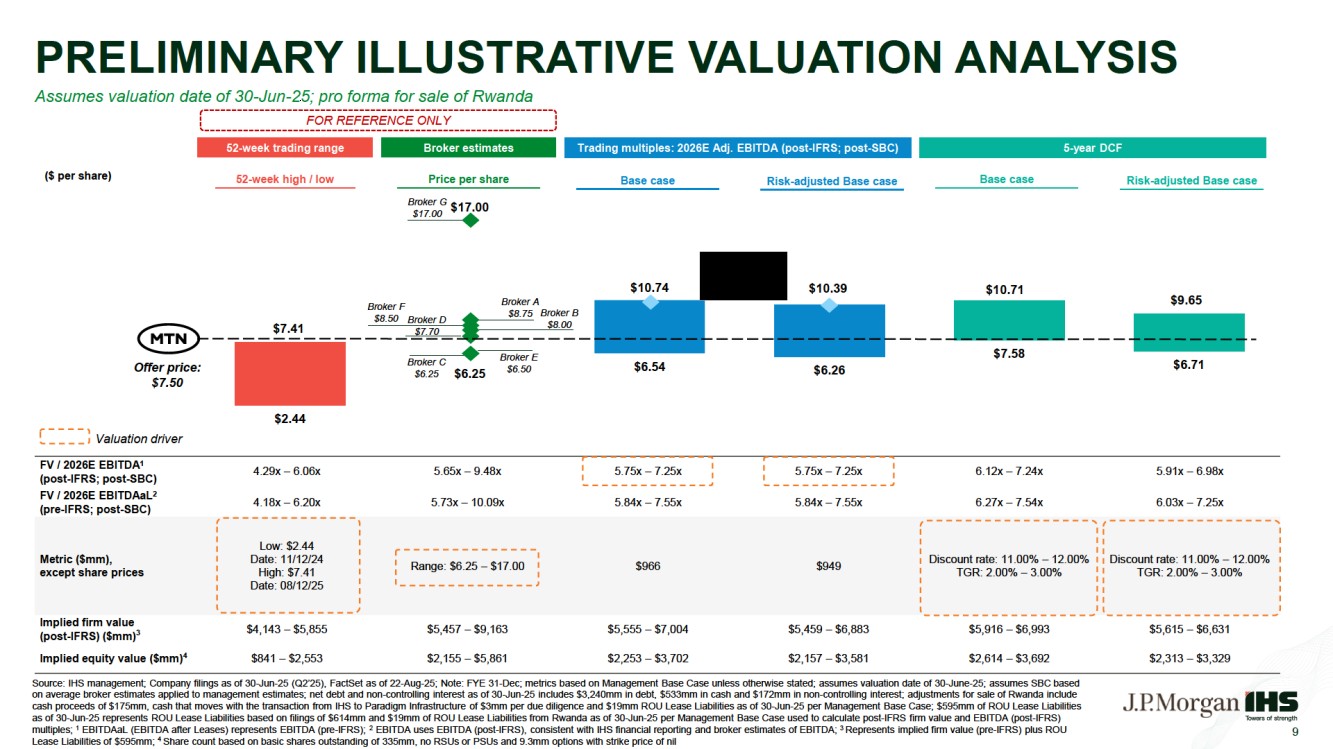

| FV / 2026E EBITDA1 (post-IFRS; post-SBC) 4.29x – 6.06x 5.65x – 9.48x 5.75x – 7.25x 5.75x – 7.25x 6.12x – 7.24x 5.91x – 6.98x FV / 2026E EBITDAaL2 (pre-IFRS; post-SBC) 4.18x – 6.20x 5.73x – 10.09x 5.84x – 7.55x 5.84x – 7.55x 6.27x – 7.54x 6.03x – 7.25x Metric ($mm), except share prices Low: $2.44 Date: 11/12/24 High: $7.41 Date: 08/12/25 Range: $6.25 – $17.00 $966 $949 Discount rate: 11.00% – 12.00% TGR: 2.00% – 3.00% Discount rate: 11.00% – 12.00% TGR: 2.00% – 3.00% Implied firm value (post-IFRS) ($mm)3 $4,143 – $5,855 $5,457 – $9,163 $5,555 – $7,004 $5,459 – $6,883 $5,916 – $6,993 $5,615 – $6,631 Implied equity value ($mm)4 $841 – $2,553 $2,155 – $5,861 $2,253 – $3,702 $2,157 – $3,581 $2,614 – $3,692 $2,313 – $3,329 9 PRELIMINARY ILLUSTRATIVE VALUATION ANALYSIS 52-week trading range ($ per share) Broker estimates Trading multiples: 2026E Adj. EBITDA (post-IFRS; post-SBC) 5-year DCF $7.41 $17.00 $10.74 $10.39 $10.71 $9.65 $2.44 $6.25 $6.54 $6.26 $7.58 $6.71 52-week high / low Price per share Base case Valuation driver Base case Risk-adjusted Base case Broker G $17.00 Broker A $8.75 Broker F $8.50 Broker D $7.70 Broker C $6.25 Broker B $8.00 Broker E $6.50 Assumes valuation date of 30-Jun-25; pro forma for sale of Rwanda FOR REFERENCE ONLY Offer price: $7.50 Risk-adjusted Base case Source: IHS management; Company filings as of 30-Jun-25 (Q2’25), FactSet as of 22-Aug-25; Note: FYE 31-Dec; metrics based on Management Base Case unless otherwise stated; assumes valuation date of 30-June-25; assumes SBC based on average broker estimates applied to management estimates; net debt and non-controlling interest as of 30-Jun-25 includes $3,240mm in debt, $533mm in cash and $172mm in non-controlling interest; adjustments for sale of Rwanda include cash proceeds of $175mm, cash that moves with the transaction from IHS to Paradigm Infrastructure of $3mm per due diligence and $19mm ROU Lease Liabilities as of 30-Jun-25 per Management Base Case; $595mm of ROU Lease Liabilities as of 30-Jun-25 represents ROU Lease Liabilities based on filings of $614mm and $19mm of ROU Lease Liabilities from Rwanda as of 30-Jun-25 per Management Base Case used to calculate post-IFRS firm value and EBITDA (post-IFRS) multiples; 1 EBITDAaL (EBITDA after Leases) represents EBITDA (pre-IFRS); 2 EBITDA uses EBITDA (post-IFRS), consistent with IHS financial reporting and broker estimates of EBITDA; 3 Represents implied firm value (pre-IFRS) plus ROU Lease Liabilities of $595mm; 4 Share count based on basic shares outstanding of 335mm, no RSUs or PSUs and 9.3mm options with strike price of nil |

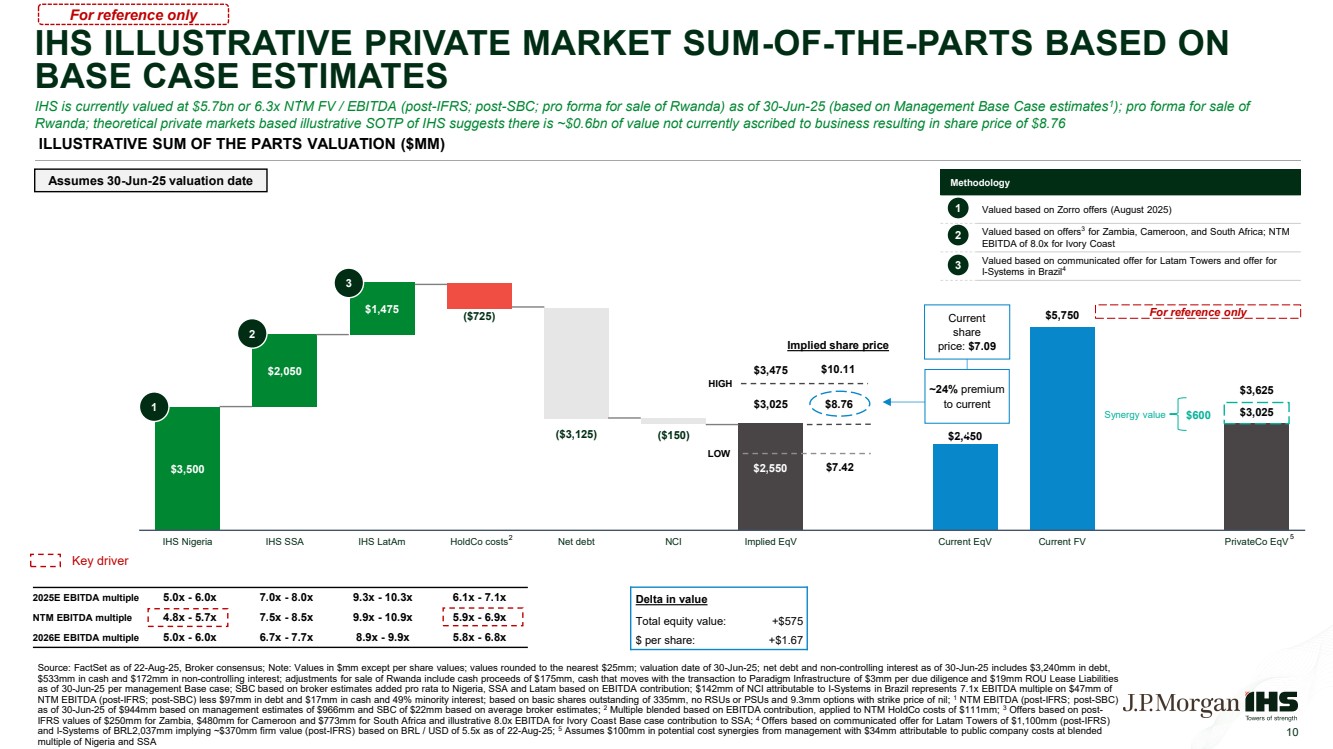

| $3,500 $3,025 $2,450 $5,750 $3,025 ($725) ($3,125) ($150) $600 $2,050 $1,475 $0 $3,625 IHS Nigeria IHS SSA IHS LatAm HoldCo costs Net debt NCI Implied EqV Current EqV Current FV PrivateCo EqV IHS ILLUSTRATIVE PRIVATE MARKET SUM-OF-THE-PARTS BASED ON BASE CASE ESTIMATES 10 IHS is currently valued at $5.7bn or 6.3x NTM FV / EBITDA (post-IFRS; post-SBC; pro forma for sale of Rwanda) as of 30-Jun-25 (based on Management Base Case estimates1 ); pro forma for sale of Rwanda; theoretical private markets based illustrative SOTP of IHS suggests there is ~$0.6bn of value not currently ascribed to business resulting in share price of $8.76 2025E EBITDA multiple 5.0x - 6.0x 7.0x - 8.0x 9.3x - 10.3x 6.1x - 7.1x NTM EBITDA multiple 4.8x - 5.7x 7.5x - 8.5x 9.9x - 10.9x 5.9x - 6.9x 2026E EBITDA multiple 5.0x - 6.0x 6.7x - 7.7x 8.9x - 9.9x 5.8x - 6.8x Source: FactSet as of 22-Aug-25, Broker consensus; Note: Values in $mm except per share values; values rounded to the nearest $25mm; valuation date of 30-Jun-25; net debt and non-controlling interest as of 30-Jun-25 includes $3,240mm in debt, $533mm in cash and $172mm in non-controlling interest; adjustments for sale of Rwanda include cash proceeds of $175mm, cash that moves with the transaction to Paradigm Infrastructure of $3mm per due diligence and $19mm ROU Lease Liabilities as of 30-Jun-25 per management Base case; SBC based on broker estimates added pro rata to Nigeria, SSA and Latam based on EBITDA contribution; $142mm of NCI attributable to I-Systems in Brazil represents 7.1x EBITDA multiple on $47mm of NTM EBITDA (post-IFRS; post-SBC) less $97mm in debt and $17mm in cash and 49% minority interest; based on basic shares outstanding of 335mm, no RSUs or PSUs and 9.3mm options with strike price of nil; 1 NTM EBITDA (post-IFRS; post-SBC) as of 30-Jun-25 of $944mm based on management estimates of $966mm and SBC of $22mm based on average broker estimates; 2 Multiple blended based on EBITDA contribution, applied to NTM HoldCo costs of $111mm; 3 Offers based on post-IFRS values of $250mm for Zambia, $480mm for Cameroon and $773mm for South Africa and illustrative 8.0x EBITDA for Ivory Coast Base case contribution to SSA; 4 Offers based on communicated offer for Latam Towers of $1,100mm (post-IFRS) and I-Systems of BRL2,037mm implying ~$370mm firm value (post-IFRS) based on BRL / USD of 5.5x as of 22-Aug-25; 5 Assumes $100mm in potential cost synergies from management with $34mm attributable to public company costs at blended multiple of Nigeria and SSA Delta in value Total equity value: +$575 $ per share: +$1.67 ILLUSTRATIVE SUM OF THE PARTS VALUATION ($MM) Key driver 2 3 $2,550 $7.42 $3,475 $10.11 Implied share price HIGH LOW 1 2 $8.76 5 Current share price: $7.09 ~24% premium to current 1 2 3 Methodology Valued based on Zorro offers (August 2025) Valued based on offers3 for Zambia, Cameroon, and South Africa; NTM EBITDA of 8.0x for Ivory Coast Valued based on communicated offer for Latam Towers and offer for I-Systems in Brazil4 For reference only Synergy value Assumes 30-Jun-25 valuation date For reference only |

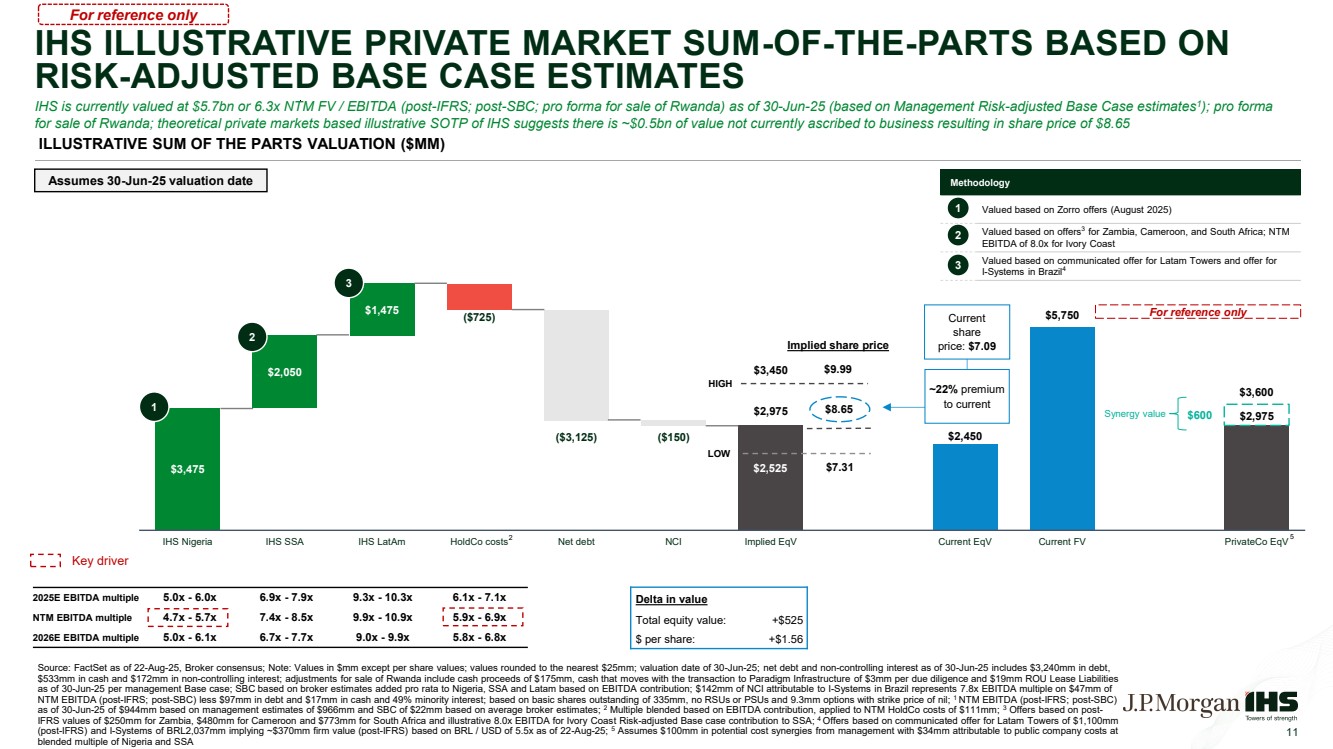

| $3,475 $2,975 $2,450 $5,750 $2,975 ($725) ($3,125) ($150) $600 $2,050 $1,475 IHS Nigeria IHS SSA IHS LatAm HoldCo costs Net debt NCI Implied EqV Current EqV Current FV PrivateCo EqV IHS ILLUSTRATIVE PRIVATE MARKET SUM-OF-THE-PARTS BASED ON RISK-ADJUSTED BASE CASE ESTIMATES 11 IHS is currently valued at $5.7bn or 6.3x NTM FV / EBITDA (post-IFRS; post-SBC; pro forma for sale of Rwanda) as of 30-Jun-25 (based on Management Risk-adjusted Base Case estimates1 ); pro forma for sale of Rwanda; theoretical private markets based illustrative SOTP of IHS suggests there is ~$0.5bn of value not currently ascribed to business resulting in share price of $8.65 2025E EBITDA multiple 5.0x - 6.0x 6.9x - 7.9x 9.3x - 10.3x 6.1x - 7.1x NTM EBITDA multiple 4.7x - 5.7x 7.4x - 8.5x 9.9x - 10.9x 5.9x - 6.9x 2026E EBITDA multiple 5.0x - 6.1x 6.7x - 7.7x 9.0x - 9.9x 5.8x - 6.8x Source: FactSet as of 22-Aug-25, Broker consensus; Note: Values in $mm except per share values; values rounded to the nearest $25mm; valuation date of 30-Jun-25; net debt and non-controlling interest as of 30-Jun-25 includes $3,240mm in debt, $533mm in cash and $172mm in non-controlling interest; adjustments for sale of Rwanda include cash proceeds of $175mm, cash that moves with the transaction to Paradigm Infrastructure of $3mm per due diligence and $19mm ROU Lease Liabilities as of 30-Jun-25 per management Base case; SBC based on broker estimates added pro rata to Nigeria, SSA and Latam based on EBITDA contribution; $142mm of NCI attributable to I-Systems in Brazil represents 7.8x EBITDA multiple on $47mm of NTM EBITDA (post-IFRS; post-SBC) less $97mm in debt and $17mm in cash and 49% minority interest; based on basic shares outstanding of 335mm, no RSUs or PSUs and 9.3mm options with strike price of nil; 1 NTM EBITDA (post-IFRS; post-SBC) as of 30-Jun-25 of $944mm based on management estimates of $966mm and SBC of $22mm based on average broker estimates; 2 Multiple blended based on EBITDA contribution, applied to NTM HoldCo costs of $111mm; 3 Offers based on post-IFRS values of $250mm for Zambia, $480mm for Cameroon and $773mm for South Africa and illustrative 8.0x EBITDA for Ivory Coast Risk-adjusted Base case contribution to SSA; 4 Offers based on communicated offer for Latam Towers of $1,100mm (post-IFRS) and I-Systems of BRL2,037mm implying ~$370mm firm value (post-IFRS) based on BRL / USD of 5.5x as of 22-Aug-25; 5 Assumes $100mm in potential cost synergies from management with $34mm attributable to public company costs at blended multiple of Nigeria and SSA Delta in value Total equity value: +$525 $ per share: +$1.56 ILLUSTRATIVE SUM OF THE PARTS VALUATION ($MM) Key driver 2 3 $2,525 $7.31 $3,450 $9.99 Implied share price HIGH LOW 1 2 $8.65 5 Current share price: $7.09 ~22% premium to current 1 2 3 Methodology Valued based on Zorro offers (August 2025) Valued based on offers3 for Zambia, Cameroon, and South Africa; NTM EBITDA of 8.0x for Ivory Coast Valued based on communicated offer for Latam Towers and offer for I-Systems in Brazil4 For reference only Synergy value Assumes 30-Jun-25 valuation date For reference only $3,600 |

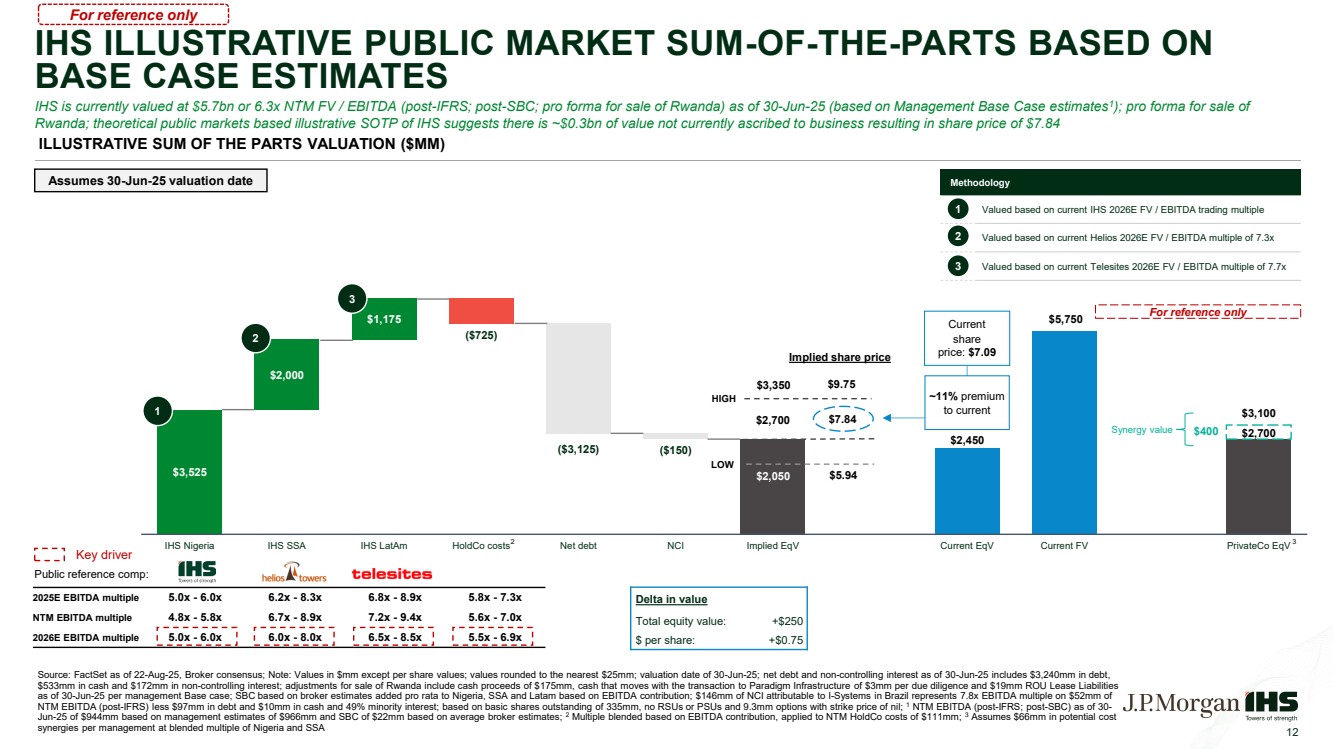

| $3,525 $2,700 $2,450 $5,750 $2,700 ($725) ($3,125) ($150) $400 $2,000 $1,175 $3,100 IHS Nigeria IHS SSA IHS LatAm HoldCo costs Net debt NCI Implied EqV Current EqV Current FV PrivateCo EqV IHS ILLUSTRATIVE PUBLIC MARKET SUM-OF-THE-PARTS BASED ON BASE CASE ESTIMATES 12 IHS is currently valued at $5.7bn or 6.3x NTM FV / EBITDA (post-IFRS; post-SBC; pro forma for sale of Rwanda) as of 30-Jun-25 (based on Management Base Case estimates1 ); pro forma for sale of Rwanda; theoretical public markets based illustrative SOTP of IHS suggests there is ~$0.3bn of value not currently ascribed to business resulting in share price of $7.84 Source: FactSet as of 22-Aug-25, Broker consensus; Note: Values in $mm except per share values; values rounded to the nearest $25mm; valuation date of 30-Jun-25; net debt and non-controlling interest as of 30-Jun-25 includes $3,240mm in debt, $533mm in cash and $172mm in non-controlling interest; adjustments for sale of Rwanda include cash proceeds of $175mm, cash that moves with the transaction to Paradigm Infrastructure of $3mm per due diligence and $19mm ROU Lease Liabilities as of 30-Jun-25 per management Base case; SBC based on broker estimates added pro rata to Nigeria, SSA and Latam based on EBITDA contribution; $146mm of NCI attributable to I-Systems in Brazil represents 7.8x EBITDA multiple on $52mm of NTM EBITDA (post-IFRS) less $97mm in debt and $10mm in cash and 49% minority interest; based on basic shares outstanding of 335mm, no RSUs or PSUs and 9.3mm options with strike price of nil; 1 NTM EBITDA (post-IFRS; post-SBC) as of 30- Jun-25 of $944mm based on management estimates of $966mm and SBC of $22mm based on average broker estimates; 2 Multiple blended based on EBITDA contribution, applied to NTM HoldCo costs of $111mm; 3 Assumes $66mm in potential cost synergies per management at blended multiple of Nigeria and SSA Delta in value Total equity value: +$250 $ per share: +$0.75 Key driver 2 3 $2,050 $5.94 $3,350 $9.75 Implied share price HIGH LOW Methodology Valued based on current IHS 2026E FV / EBITDA trading multiple Valued based on current Helios 2026E FV / EBITDA multiple of 7.3x Valued based on current Telesites 2026E FV / EBITDA multiple of 7.7x 1 2025E EBITDA multiple 5.0x - 6.0x 6.2x - 8.3x 6.8x - 8.9x 5.8x - 7.3x NTM EBITDA multiple 4.8x - 5.8x 6.7x - 8.9x 7.2x - 9.4x 5.6x - 7.0x 2026E EBITDA multiple 5.0x - 6.0x 6.0x - 8.0x 6.5x - 8.5x 5.5x - 6.9x ~11% premium to current Current share price: $7.09 2 ILLUSTRATIVE SUM OF THE PARTS VALUATION ($MM) $7.84 Public reference comp: 3 1 2 3 Synergy value For reference only Assumes 30-Jun-25 valuation date For reference only |

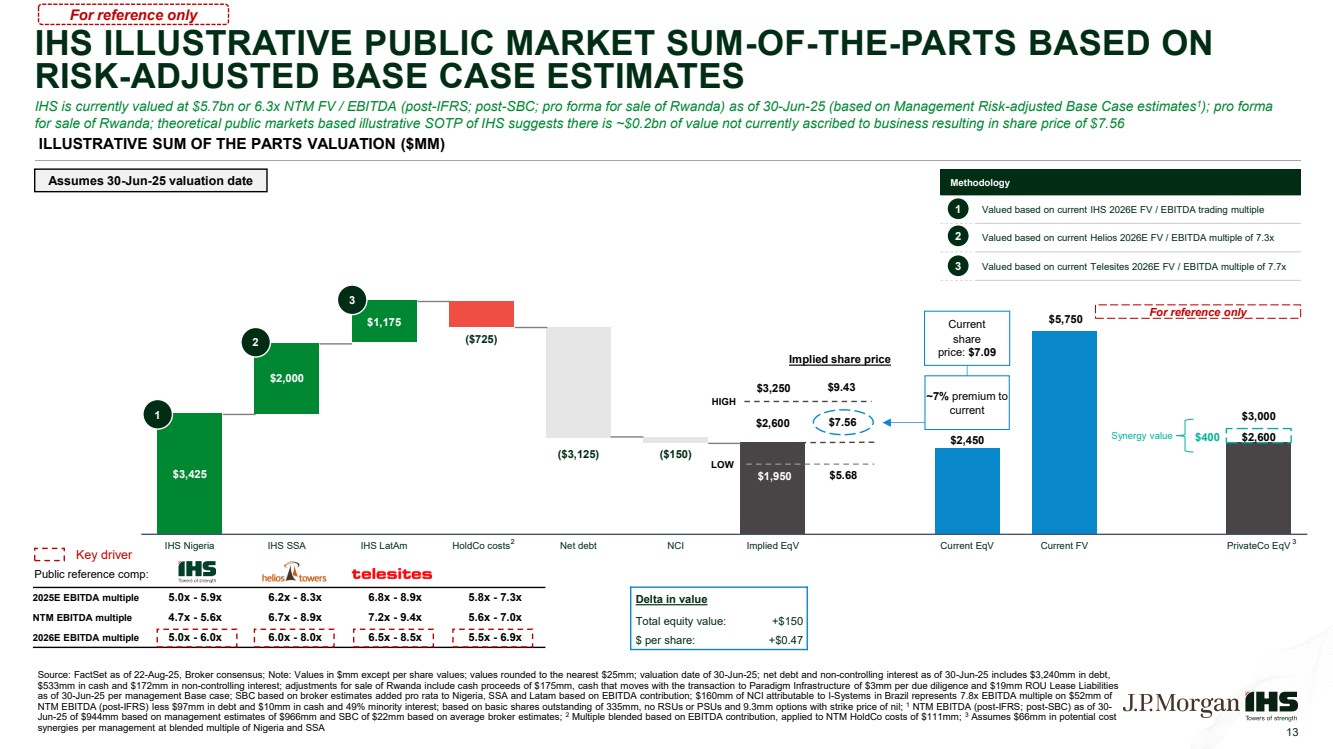

| $3,425 $2,600 $2,450 $5,750 $2,600 ($725) ($3,125) ($150) $400 $2,000 $1,175 $3,000 IHS Nigeria IHS SSA IHS LatAm HoldCo costs Net debt NCI Implied EqV Current EqV Current FV PrivateCo EqV IHS ILLUSTRATIVE PUBLIC MARKET SUM-OF-THE-PARTS BASED ON RISK-ADJUSTED BASE CASE ESTIMATES 13 IHS is currently valued at $5.7bn or 6.3x NTM FV / EBITDA (post-IFRS; post-SBC; pro forma for sale of Rwanda) as of 30-Jun-25 (based on Management Risk-adjusted Base Case estimates1 ); pro forma for sale of Rwanda; theoretical public markets based illustrative SOTP of IHS suggests there is ~$0.2bn of value not currently ascribed to business resulting in share price of $7.56 Source: FactSet as of 22-Aug-25, Broker consensus; Note: Values in $mm except per share values; values rounded to the nearest $25mm; valuation date of 30-Jun-25; net debt and non-controlling interest as of 30-Jun-25 includes $3,240mm in debt, $533mm in cash and $172mm in non-controlling interest; adjustments for sale of Rwanda include cash proceeds of $175mm, cash that moves with the transaction to Paradigm Infrastructure of $3mm per due diligence and $19mm ROU Lease Liabilities as of 30-Jun-25 per management Base case; SBC based on broker estimates added pro rata to Nigeria, SSA and Latam based on EBITDA contribution; $160mm of NCI attributable to I-Systems in Brazil represents 7.8x EBITDA multiple on $52mm of NTM EBITDA (post-IFRS) less $97mm in debt and $10mm in cash and 49% minority interest; based on basic shares outstanding of 335mm, no RSUs or PSUs and 9.3mm options with strike price of nil; 1 NTM EBITDA (post-IFRS; post-SBC) as of 30- Jun-25 of $944mm based on management estimates of $966mm and SBC of $22mm based on average broker estimates; 2 Multiple blended based on EBITDA contribution, applied to NTM HoldCo costs of $111mm; 3 Assumes $66mm in potential cost synergies per management at blended multiple of Nigeria and SSA Delta in value Total equity value: +$150 $ per share: +$0.47 Key driver 2 3 $1,950 $5.68 $3,250 $9.43 Implied share price HIGH LOW Methodology Valued based on current IHS 2026E FV / EBITDA trading multiple Valued based on current Helios 2026E FV / EBITDA multiple of 7.3x Valued based on current Telesites 2026E FV / EBITDA multiple of 7.7x 1 2025E EBITDA multiple 5.0x - 5.9x 6.2x - 8.3x 6.8x - 8.9x 5.8x - 7.3x NTM EBITDA multiple 4.7x - 5.6x 6.7x - 8.9x 7.2x - 9.4x 5.6x - 7.0x 2026E EBITDA multiple 5.0x - 6.0x 6.0x - 8.0x 6.5x - 8.5x 5.5x - 6.9x ~7% premium to current Current share price: $7.09 2 ILLUSTRATIVE SUM OF THE PARTS VALUATION ($MM) $7.56 Public reference comp: 3 1 2 3 Synergy value For reference only Assumes 30-Jun-25 valuation date For reference only |

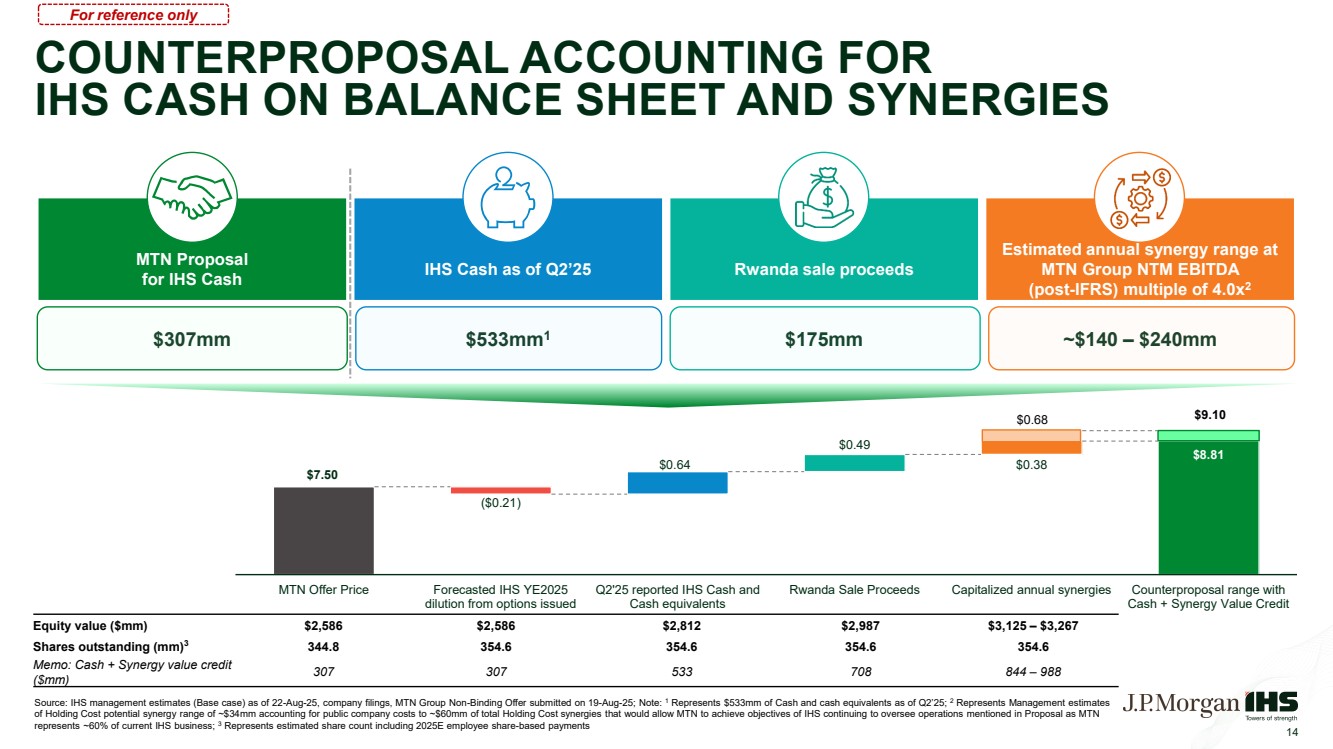

| MTN Proposal for IHS Cash IHS Cash as of Q2’25 Rwanda sale proceeds Estimated annual synergy range at MTN Group NTM EBITDA (post-IFRS) multiple of 4.0x2 $307mm $533mm1 $175mm ~$140 – $240mm 14 COUNTERPROPOSAL ACCOUNTING FOR IHS CASH ON BALANCE SHEET AND SYNERGIES Source: IHS management estimates (Base case) as of 22-Aug-25, company filings, MTN Group Non-Binding Offer submitted on 19-Aug-25; Note: 1 Represents $533mm of Cash and cash equivalents as of Q2’25; 2 Represents Management estimates of Holding Cost potential synergy range of ~$34mm accounting for public company costs to ~$60mm of total Holding Cost synergies that would allow MTN to achieve objectives of IHS continuing to oversee operations mentioned in Proposal as MTN represents ~60% of current IHS business; 3 Represents estimated share count including 2025E employee share-based payments For reference only Equity value ($mm) $2,586 $2,586 $2,812 $2,987 $3,125 – $3,267 Shares outstanding (mm)3 344.8 354.6 354.6 354.6 354.6 Memo: Cash + Synergy value credit ($mm) 307 307 533 708 844 – 988 $7.50 $8.81 ($0.21) $0.64 $0.49 $0.38 MTN Offer Price Forecasted IHS YE2025 dilution from options issued Q2'25 reported IHS Cash and Cash equivalents Rwanda Sale Proceeds Capitalized annual synergies Counterproposal range with Cash + Synergy Value Credit $9.10 $0.68 |

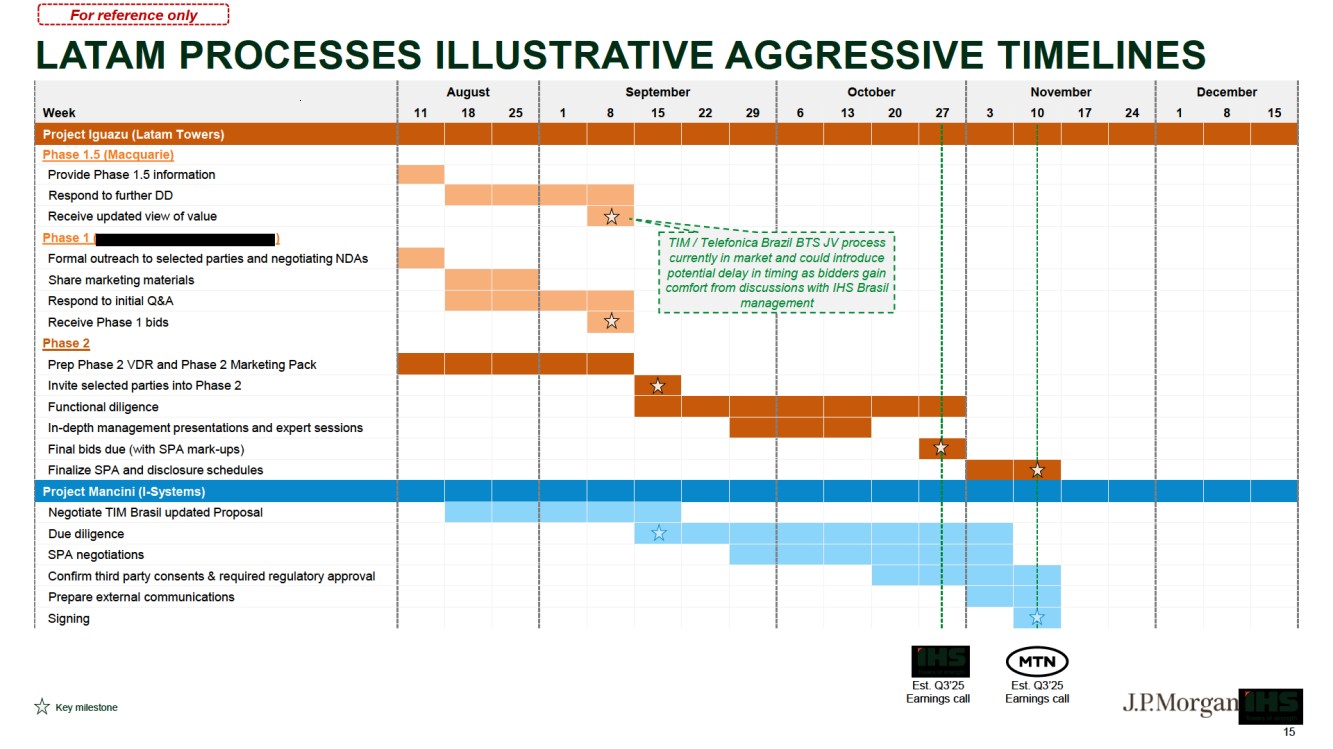

| LATAM PROCESSES ILLUSTRATIVE AGGRESSIVE TIMELINES Key milestone 15 August September October November December Week 11 18 25 1 8 15 22 29 6 13 20 27 3 10 17 24 1 8 15 Project Iguazu (Latam Towers) Phase 1.5 (Macquarie) Provide Phase 1.5 information Respond to further DD Receive updated view of value Phase 1 (CDPQ, I Squared, OTPP, Actis) Formal outreach to selected parties and negotiating NDAs Share marketing materials Respond to initial Q&A Receive Phase 1 bids Phase 2 Prep Phase 2 VDR and Phase 2 Marketing Pack Invite selected parties into Phase 2 Functional diligence In-depth management presentations and expert sessions Final bids due (with SPA mark-ups) Finalize SPA and disclosure schedules Project Mancini (I-Systems) Negotiate TIM Brasil updated Proposal Due diligence SPA negotiations Confirm third party consents & required regulatory approval Prepare external communications Signing Est. Q3’25 Earnings call Est. Q3’25 Earnings call For reference only TIM / Telefonica Brazil BTS JV process currently in market and could introduce potential delay in timing as bidders gain comfort from discussions with IHS Brasil management |

| APPENDIX 16 |

| MTN NON-BINDING PROPOSAL 17 |

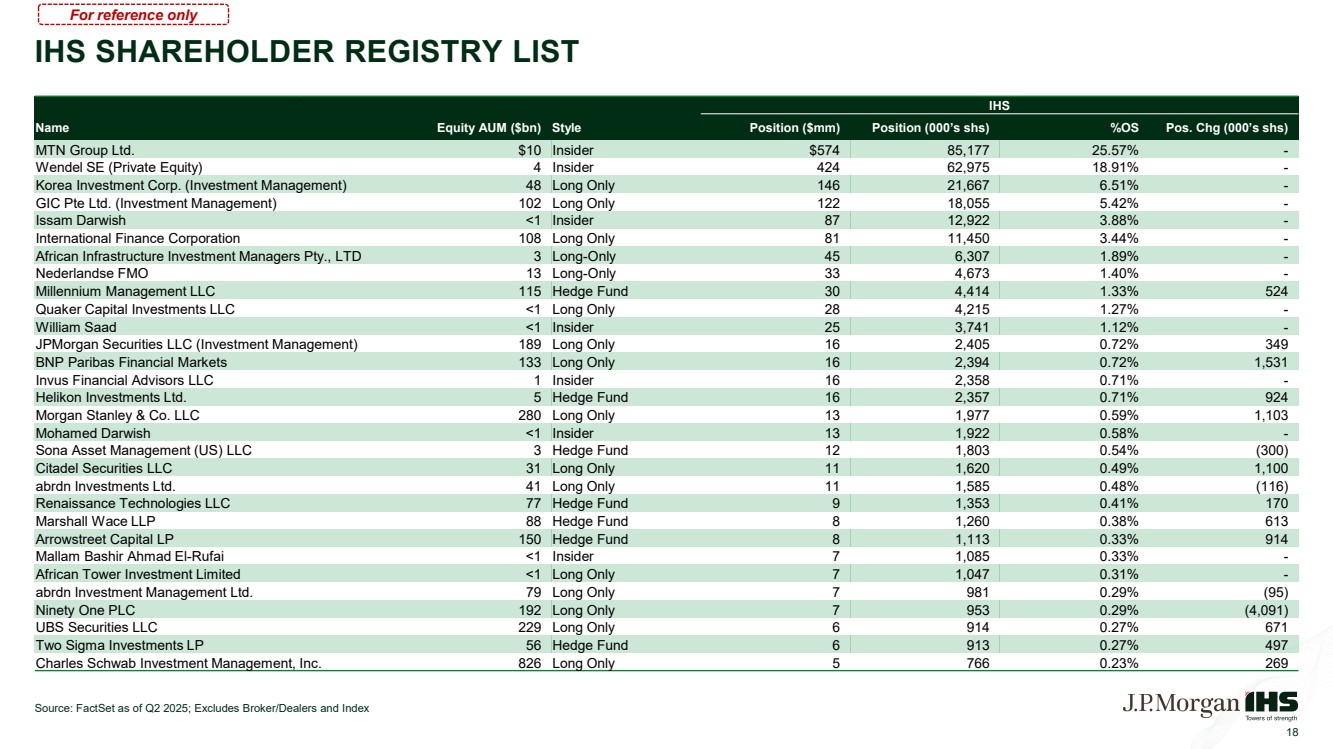

| IHS SHAREHOLDER REGISTRY LIST Source: FactSet as of Q2 2025; Excludes Broker/Dealers and Index 18 IHS Name Equity AUM ($bn) Style Position ($mm) Position (000’s shs) %OS Pos. Chg (000’s shs) MTN Group Ltd. $10 Insider $574 85,177 25.57% - Wendel SE (Private Equity) 4 Insider 424 62,975 18.91% - Korea Investment Corp. (Investment Management) 48 Long Only 146 21,667 6.51% - GIC Pte Ltd. (Investment Management) 102 Long Only 122 18,055 5.42% - Issam Darwish <1 Insider 87 12,922 3.88% - International Finance Corporation 108 Long Only 81 11,450 3.44% - African Infrastructure Investment Managers Pty., LTD 3 Long-Only 45 6,307 1.89% - Nederlandse FMO 13 Long-Only 33 4,673 1.40% - Millennium Management LLC 115 Hedge Fund 30 4,414 1.33% 524 Quaker Capital Investments LLC <1 Long Only 28 4,215 1.27% - William Saad <1 Insider 25 3,741 1.12% - JPMorgan Securities LLC (Investment Management) 189 Long Only 16 2,405 0.72% 349 BNP Paribas Financial Markets 133 Long Only 16 2,394 0.72% 1,531 Invus Financial Advisors LLC 1 Insider 16 2,358 0.71% - Helikon Investments Ltd. 5 Hedge Fund 16 2,357 0.71% 924 Morgan Stanley & Co. LLC 280 Long Only 13 1,977 0.59% 1,103 Mohamed Darwish <1 Insider 13 1,922 0.58% - Sona Asset Management (US) LLC 3 Hedge Fund 12 1,803 0.54% (300) Citadel Securities LLC 31 Long Only 11 1,620 0.49% 1,100 abrdn Investments Ltd. 41 Long Only 11 1,585 0.48% (116) Renaissance Technologies LLC 77 Hedge Fund 9 1,353 0.41% 170 Marshall Wace LLP 88 Hedge Fund 8 1,260 0.38% 613 Arrowstreet Capital LP 150 Hedge Fund 8 1,113 0.33% 914 Mallam Bashir Ahmad El-Rufai <1 Insider 7 1,085 0.33% - African Tower Investment Limited <1 Long Only 7 1,047 0.31% - abrdn Investment Management Ltd. 79 Long Only 7 981 0.29% (95) Ninety One PLC 192 Long Only 7 953 0.29% (4,091) UBS Securities LLC 229 Long Only 6 914 0.27% 671 Two Sigma Investments LP 56 Hedge Fund 6 913 0.27% 497 Charles Schwab Investment Management, Inc. 826 Long Only 5 766 0.23% 269 For reference only |

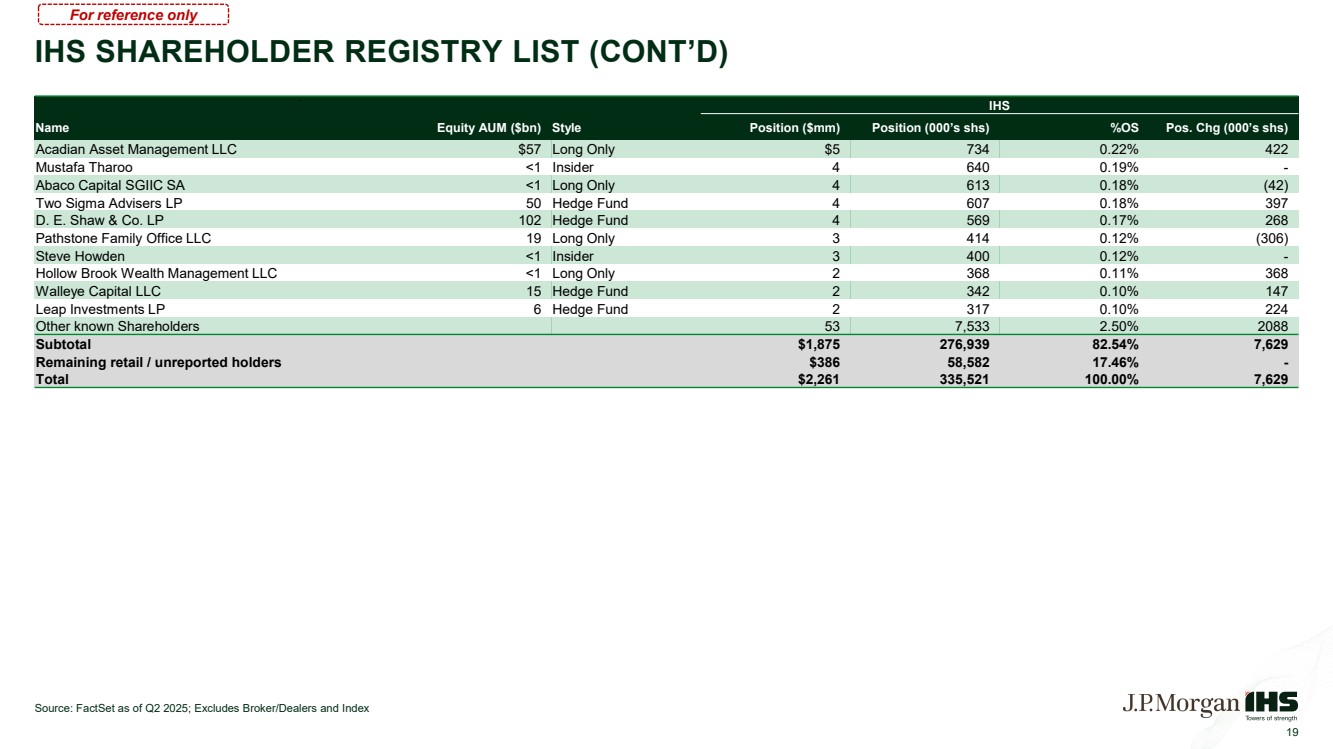

| IHS SHAREHOLDER REGISTRY LIST (CONT’D) Source: FactSet as of Q2 2025; Excludes Broker/Dealers and Index 19 IHS Name Equity AUM ($bn) Style Position ($mm) Position (000’s shs) %OS Pos. Chg (000’s shs) Acadian Asset Management LLC $57 Long Only $5 734 0.22% 422 Mustafa Tharoo <1 Insider 4 640 0.19% - Abaco Capital SGIIC SA <1 Long Only 4 613 0.18% (42) Two Sigma Advisers LP 50 Hedge Fund 4 607 0.18% 397 D. E. Shaw & Co. LP 102 Hedge Fund 4 569 0.17% 268 Pathstone Family Office LLC 19 Long Only 3 414 0.12% (306) Steve Howden <1 Insider 3 400 0.12% - Hollow Brook Wealth Management LLC <1 Long Only 2 368 0.11% 368 Walleye Capital LLC 15 Hedge Fund 2 342 0.10% 147 Leap Investments LP 6 Hedge Fund 2 317 0.10% 224 Other known Shareholders 53 7,533 2.50% 2088 Subtotal $1,875 276,939 82.54% 7,629 Remaining retail / unreported holders $386 58,582 17.46% - Total $2,261 335,521 100.00% 7,629 For reference only |

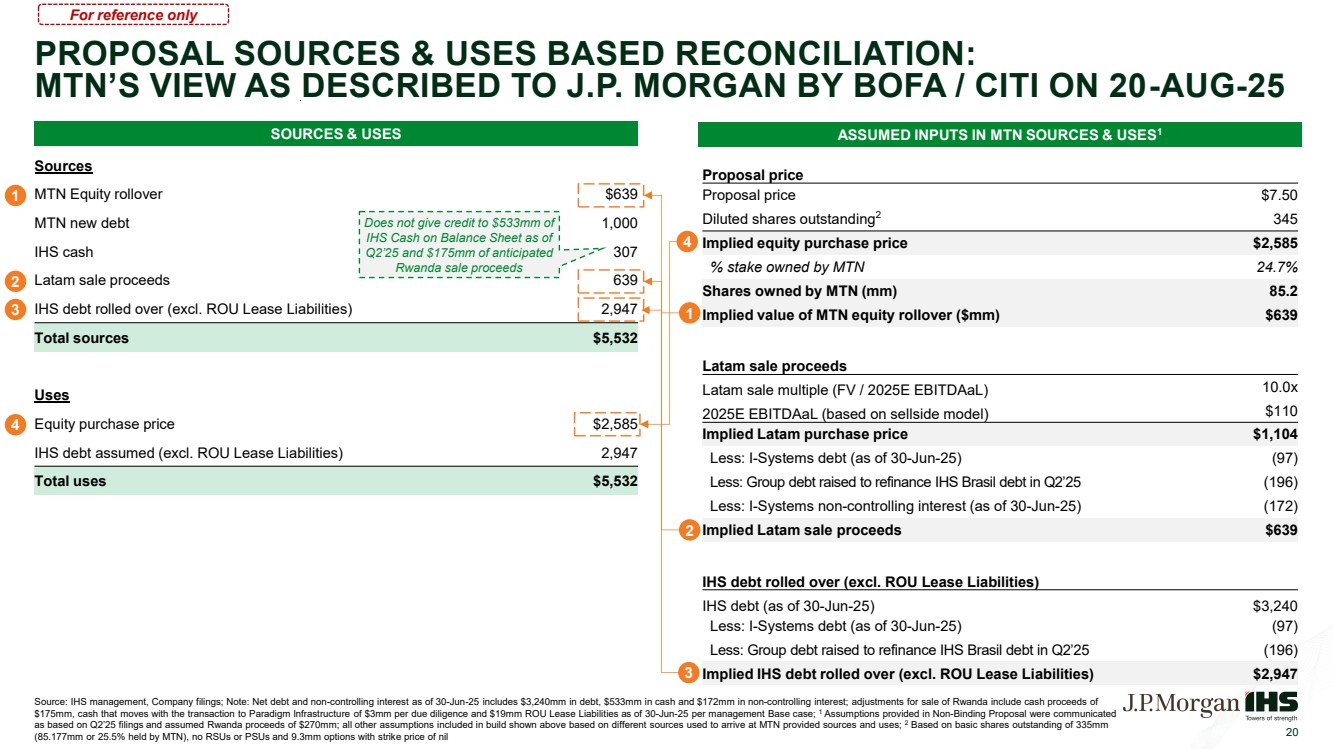

| PROPOSAL SOURCES & USES BASED RECONCILIATION: MTN’S VIEW AS DESCRIBED TO J.P. MORGAN BY BOFA / CITI ON 20-AUG-25 20 Sources MTN Equity rollover $639 MTN new debt 1,000 IHS cash 307 Latam sale proceeds 639 IHS debt rolled over (excl. ROU Lease Liabilities) 2,947 Total sources $5,532 Uses Equity purchase price $2,585 IHS debt assumed (excl. ROU Lease Liabilities) 2,947 Total uses $5,532 Proposal price Proposal price $7.50 Diluted shares outstanding2 345 Implied equity purchase price $2,585 % stake owned by MTN 24.7% Shares owned by MTN (mm) 85.2 Implied value of MTN equity rollover ($mm) $639 Latam sale proceeds Latam sale multiple (FV / 2025E EBITDAaL) 10.0x 2025E EBITDAaL (based on sellside model) $110 Implied Latam purchase price $1,104 Less: I-Systems debt (as of 30-Jun-25) (97) Less: Group debt raised to refinance IHS Brasil debt in Q2’25 (196) Less: I-Systems non-controlling interest (as of 30-Jun-25) (172) Implied Latam sale proceeds $639 IHS debt rolled over (excl. ROU Lease Liabilities) IHS debt (as of 30-Jun-25) $3,240 Less: I-Systems debt (as of 30-Jun-25) (97) Less: Group debt raised to refinance IHS Brasil debt in Q2’25 (196) Implied IHS debt rolled over (excl. ROU Lease Liabilities) $2,947 SOURCES & USES Source: IHS management, Company filings; Note: Net debt and non-controlling interest as of 30-Jun-25 includes $3,240mm in debt, $533mm in cash and $172mm in non-controlling interest; adjustments for sale of Rwanda include cash proceeds of $175mm, cash that moves with the transaction to Paradigm Infrastructure of $3mm per due diligence and $19mm ROU Lease Liabilities as of 30-Jun-25 per management Base case; 1 Assumptions provided in Non-Binding Proposal were communicated as based on Q2’25 filings and assumed Rwanda proceeds of $270mm; all other assumptions included in build shown above based on different sources used to arrive at MTN provided sources and uses; 2 Based on basic shares outstanding of 335mm (85.177mm or 25.5% held by MTN), no RSUs or PSUs and 9.3mm options with strike price of nil 1 1 2 2 4 3 ASSUMED INPUTS IN MTN SOURCES & USES1 Does not give credit to $533mm of IHS Cash on Balance Sheet as of Q2’25 and $175mm of anticipated Rwanda sale proceeds 3 4 For reference only |

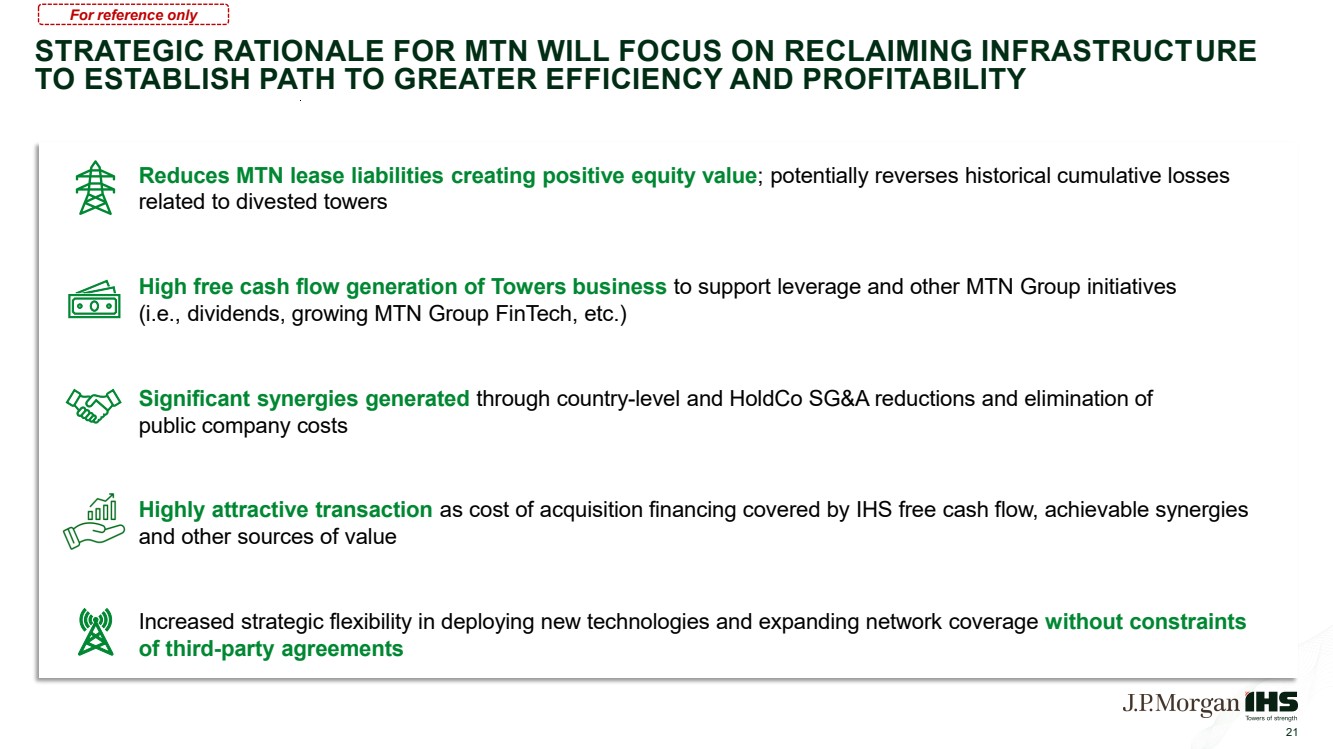

| 21 STRATEGIC RATIONALE FOR MTN WILL FOCUS ON RECLAIMING INFRASTRUCTURE TO ESTABLISH PATH TO GREATER EFFICIENCY AND PROFITABILITY Reduces MTN lease liabilities creating positive equity value; potentially reverses historical cumulative losses related to divested towers High free cash flow generation of Towers business to support leverage and other MTN Group initiatives (i.e., dividends, growing MTN Group FinTech, etc.) Significant synergies generated through country-level and HoldCo SG&A reductions and elimination of public company costs Highly attractive transaction as cost of acquisition financing covered by IHS free cash flow, achievable synergies and other sources of value Increased strategic flexibility in deploying new technologies and expanding network coverage without constraints of third-party agreements For reference only |

| VALUATION ANALYSIS 22 |

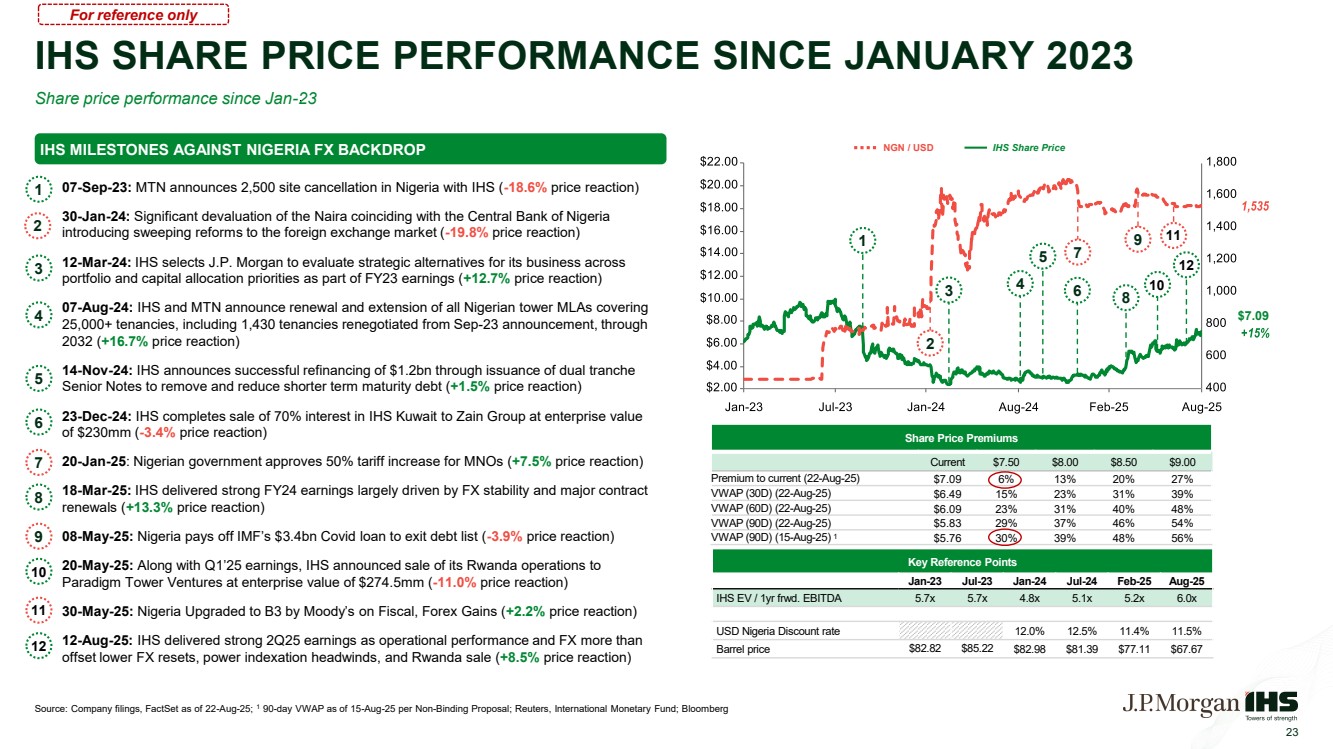

| Source: Company filings, FactSet as of 22-Aug-25; 1 90-day VWAP as of 15-Aug-25 per Non-Binding Proposal; Reuters, International Monetary Fund; Bloomberg 23 NGN / USD IHS Share Price 07-Sep-23: MTN announces 2,500 site cancellation in Nigeria with IHS (-18.6% price reaction) 30-Jan-24: Significant devaluation of the Naira coinciding with the Central Bank of Nigeria introducing sweeping reforms to the foreign exchange market (-19.8% price reaction) 12-Mar-24: IHS selects J.P. Morgan to evaluate strategic alternatives for its business across portfolio and capital allocation priorities as part of FY23 earnings (+12.7% price reaction) 07-Aug-24: IHS and MTN announce renewal and extension of all Nigerian tower MLAs covering 25,000+ tenancies, including 1,430 tenancies renegotiated from Sep-23 announcement, through 2032 (+16.7% price reaction) 14-Nov-24: IHS announces successful refinancing of $1.2bn through issuance of dual tranche Senior Notes to remove and reduce shorter term maturity debt (+1.5% price reaction) 23-Dec-24: IHS completes sale of 70% interest in IHS Kuwait to Zain Group at enterprise value of $230mm (-3.4% price reaction) 20-Jan-25: Nigerian government approves 50% tariff increase for MNOs (+7.5% price reaction) 18-Mar-25: IHS delivered strong FY24 earnings largely driven by FX stability and major contract renewals (+13.3% price reaction) 08-May-25: Nigeria pays off IMF’s $3.4bn Covid loan to exit debt list (-3.9% price reaction) 20-May-25: Along with Q1’25 earnings, IHS announced sale of its Rwanda operations to Paradigm Tower Ventures at enterprise value of $274.5mm (-11.0% price reaction) 30-May-25: Nigeria Upgraded to B3 by Moody’s on Fiscal, Forex Gains (+2.2% price reaction) 12-Aug-25: IHS delivered strong 2Q25 earnings as operational performance and FX more than offset lower FX resets, power indexation headwinds, and Rwanda sale (+8.5% price reaction) 5 4 6 8 1 4 5 6 8 7 9 7 9 IHS SHARE PRICE PERFORMANCE SINCE JANUARY 2023 Share price performance since Jan-23 12 1 12 IHS MILESTONES AGAINST NIGERIA FX BACKDROP $7.09 Key Reference Points Jan-23 Jul-23 Jan-24 Jul-24 Feb-25 Aug-25 IHS EV / 1yr frwd. EBITDA 5.7x 5.7x 4.8x 5.1x 5.2x 6.0x USD Nigeria Discount rate 12.0% 12.5% 11.4% 11.5% Barrel price $82.82 $85.22 $82.98 $81.39 $77.11 $67.67 3 10 3 11 Share Price Premiums Current $7.50 $8.00 $8.50 $9.00 Premium to current (22-Aug-25) $7.09 6% 13% 20% 27% VWAP (30D) (22-Aug-25) $6.49 15% 23% 31% 39% VWAP (60D) (22-Aug-25) $6.09 23% 31% 40% 48% VWAP (90D) (22-Aug-25) $5.83 29% 37% 46% 54% VWAP (90D) (15-Aug-25) 1 $5.76 30% 39% 48% 56% 2 11 2 10 For reference only |

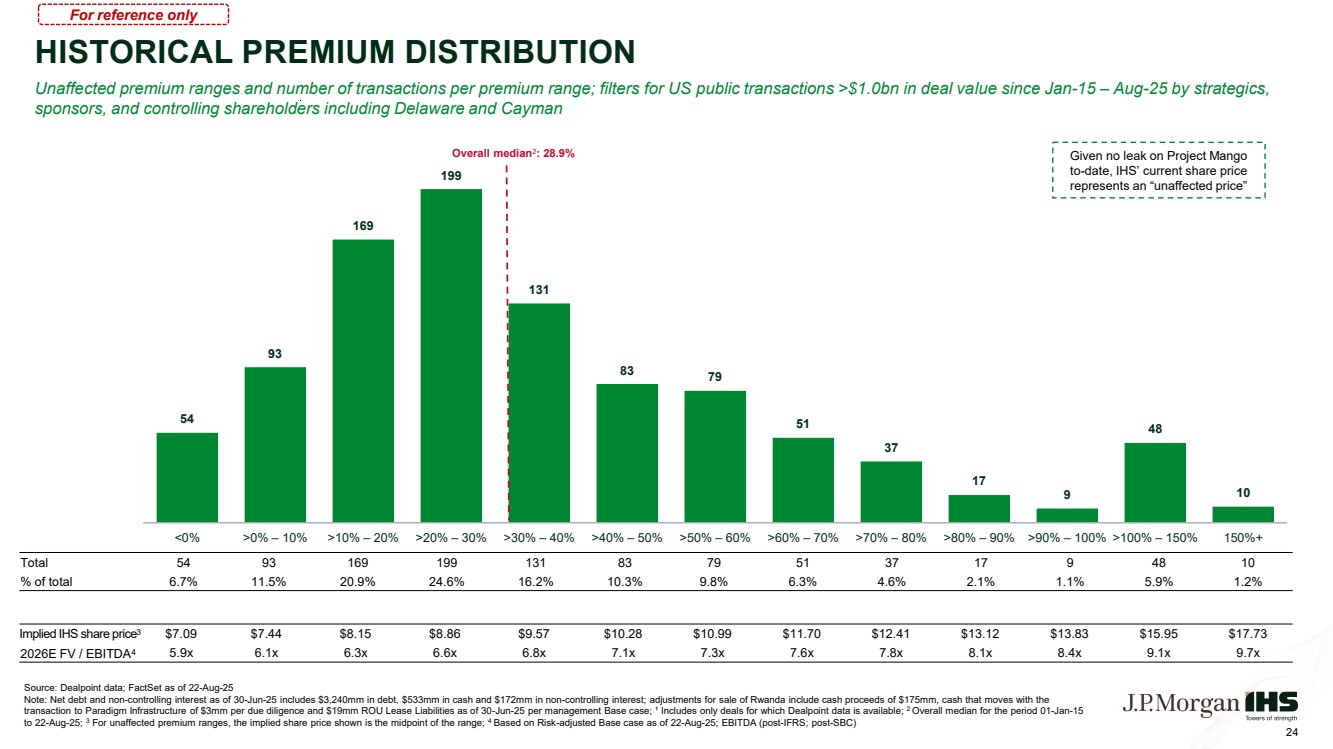

| 54 93 169 199 131 83 79 51 37 17 9 48 10 <0% >0% – 10% >10% – 20% >20% – 30% >30% – 40% >40% – 50% >50% – 60% >60% – 70% >70% – 80% >80% – 90% >90% – 100% >100% – 150% 150%+ Overall median2 : 28.9% HISTORICAL PREMIUM DISTRIBUTION Unaffected premium ranges and number of transactions per premium range; filters for US public transactions >$1.0bn in deal value since Jan-15 – Aug-25 by strategics, sponsors, and controlling shareholders including Delaware and Cayman Source: Dealpoint data; FactSet as of 22-Aug-25 Note: Net debt and non-controlling interest as of 30-Jun-25 includes $3,240mm in debt, $533mm in cash and $172mm in non-controlling interest; adjustments for sale of Rwanda include cash proceeds of $175mm, cash that moves with the transaction to Paradigm Infrastructure of $3mm per due diligence and $19mm ROU Lease Liabilities as of 30-Jun-25 per management Base case; ¹ Includes only deals for which Dealpoint data is available; 2 Overall median for the period 01-Jan-15 to 22-Aug-25; 3 For unaffected premium ranges, the implied share price shown is the midpoint of the range; 4 Based on Risk-adjusted Base case as of 22-Aug-25; EBITDA (post-IFRS; post-SBC) Total 54 93 169 199 131 83 79 51 37 17 9 48 10 % of total 6.7% 11.5% 20.9% 24.6% 16.2% 10.3% 9.8% 6.3% 4.6% 2.1% 1.1% 5.9% 1.2% 24 Given no leak on Project Mango to-date, IHS’ current share price represents an “unaffected price” Implied IHS share price3 $7.09 $7.44 $8.15 $8.86 $9.57 $10.28 $10.99 $11.70 $12.41 $13.12 $13.83 $15.95 $17.73 2026E FV / EBITDA4 5.9x 6.1x 6.3x 6.6x 6.8x 7.1x 7.3x 7.6x 7.8x 8.1x 8.4x 9.1x 9.7x For reference only |

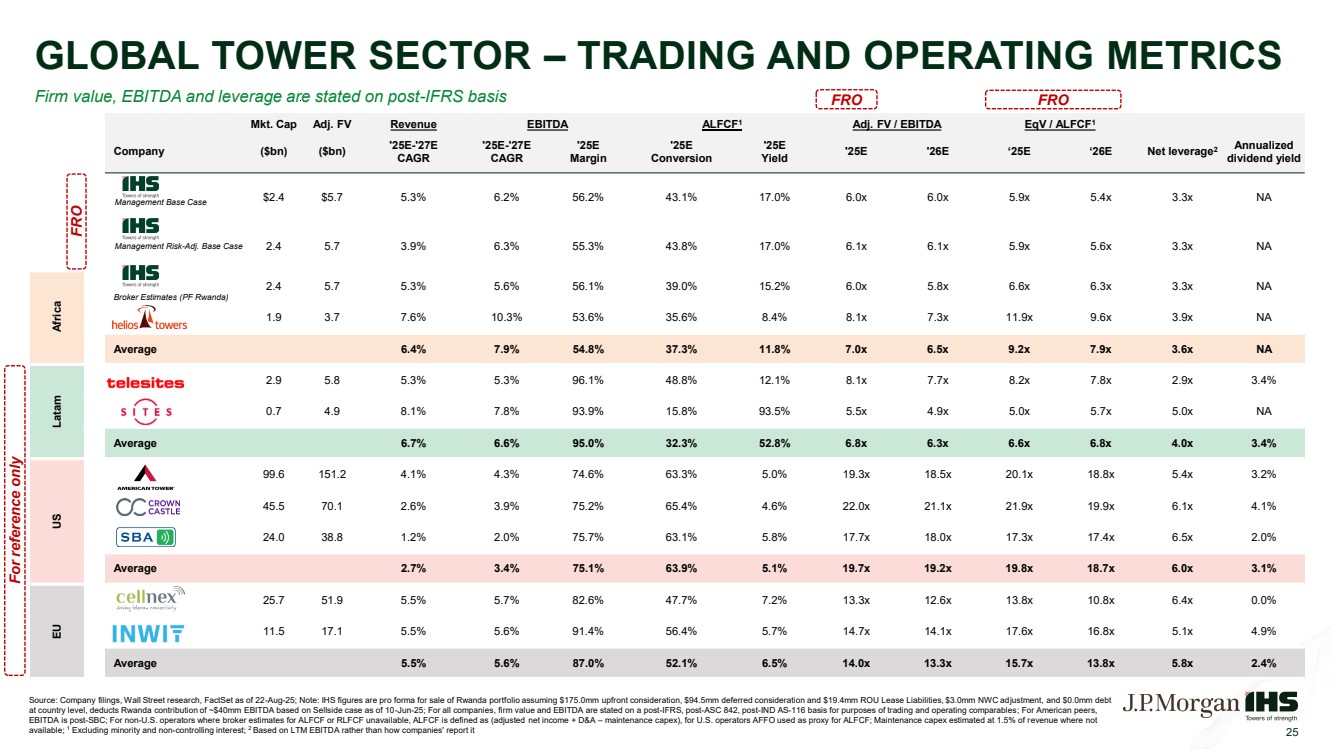

| GLOBAL TOWER SECTOR – TRADING AND OPERATING METRICS 25 Mkt. Cap Adj. FV Revenue EBITDA ALFCF1 Adj. FV / EBITDA EqV / ALFCF1 Company ($bn) ($bn) '25E-'27E CAGR '25E-'27E CAGR '25E Margin '25E Conversion '25E Yield '25E '26E ‘25E ‘26E Net leverage2 Annualized dividend yield Management Base Case $2.4 $5.7 5.3% 6.2% 56.2% 43.1% 17.0% 6.0x 6.0x 5.9x 5.4x 3.3x NA Management Risk-Adj. Base Case 2.4 5.7 3.9% 6.3% 55.3% 43.8% 17.0% 6.1x 6.1x 5.9x 5.6x 3.3x NA Africa Broker Estimates (PF Rwanda) 2.4 5.7 5.3% 5.6% 56.1% 39.0% 15.2% 6.0x 5.8x 6.6x 6.3x 3.3x NA 1.9 3.7 7.6% 10.3% 53.6% 35.6% 8.4% 8.1x 7.3x 11.9x 9.6x 3.9x NA Average 6.4% 7.9% 54.8% 37.3% 11.8% 7.0x 6.5x 9.2x 7.9x 3.6x NA Latam 2.9 5.8 5.3% 5.3% 96.1% 48.8% 12.1% 8.1x 7.7x 8.2x 7.8x 2.9x 3.4% 0.7 4.9 8.1% 7.8% 93.9% 15.8% 93.5% 5.5x 4.9x 5.0x 5.7x 5.0x NA Average 6.7% 6.6% 95.0% 32.3% 52.8% 6.8x 6.3x 6.6x 6.8x 4.0x 3.4% US 99.6 151.2 4.1% 4.3% 74.6% 63.3% 5.0% 19.3x 18.5x 20.1x 18.8x 5.4x 3.2% 45.5 70.1 2.6% 3.9% 75.2% 65.4% 4.6% 22.0x 21.1x 21.9x 19.9x 6.1x 4.1% 24.0 38.8 1.2% 2.0% 75.7% 63.1% 5.8% 17.7x 18.0x 17.3x 17.4x 6.5x 2.0% Average 2.7% 3.4% 75.1% 63.9% 5.1% 19.7x 19.2x 19.8x 18.7x 6.0x 3.1% EU 25.7 51.9 5.5% 5.7% 82.6% 47.7% 7.2% 13.3x 12.6x 13.8x 10.8x 6.4x 0.0% 11.5 17.1 5.5% 5.6% 91.4% 56.4% 5.7% 14.7x 14.1x 17.6x 16.8x 5.1x 4.9% Average 5.5% 5.6% 87.0% 52.1% 6.5% 14.0x 13.3x 15.7x 13.8x 5.8x 2.4% Source: Company filings, Wall Street research, FactSet as of 22-Aug-25; Note: IHS figures are pro forma for sale of Rwanda portfolio assuming $175.0mm upfront consideration, $94.5mm deferred consideration and $19.4mm ROU Lease Liabilities, $3.0mm NWC adjustment, and $0.0mm debt at country level, deducts Rwanda contribution of ~$40mm EBITDA based on Sellside case as of 10-Jun-25; For all companies, firm value and EBITDA are stated on a post-IFRS, post-ASC 842, post-IND AS-116 basis for purposes of trading and operating comparables; For American peers, EBITDA is post-SBC; For non-U.S. operators where broker estimates for ALFCF or RLFCF unavailable, ALFCF is defined as (adjusted net income + D&A – maintenance capex), for U.S. operators AFFO used as proxy for ALFCF; Maintenance capex estimated at 1.5% of revenue where not available; 1 Excluding minority and non-controlling interest; 2 Based on LTM EBITDA rather than how companies' report it Firm value, EBITDA and leverage are stated on post-IFRS basis For reference only FRO FRO FRO |

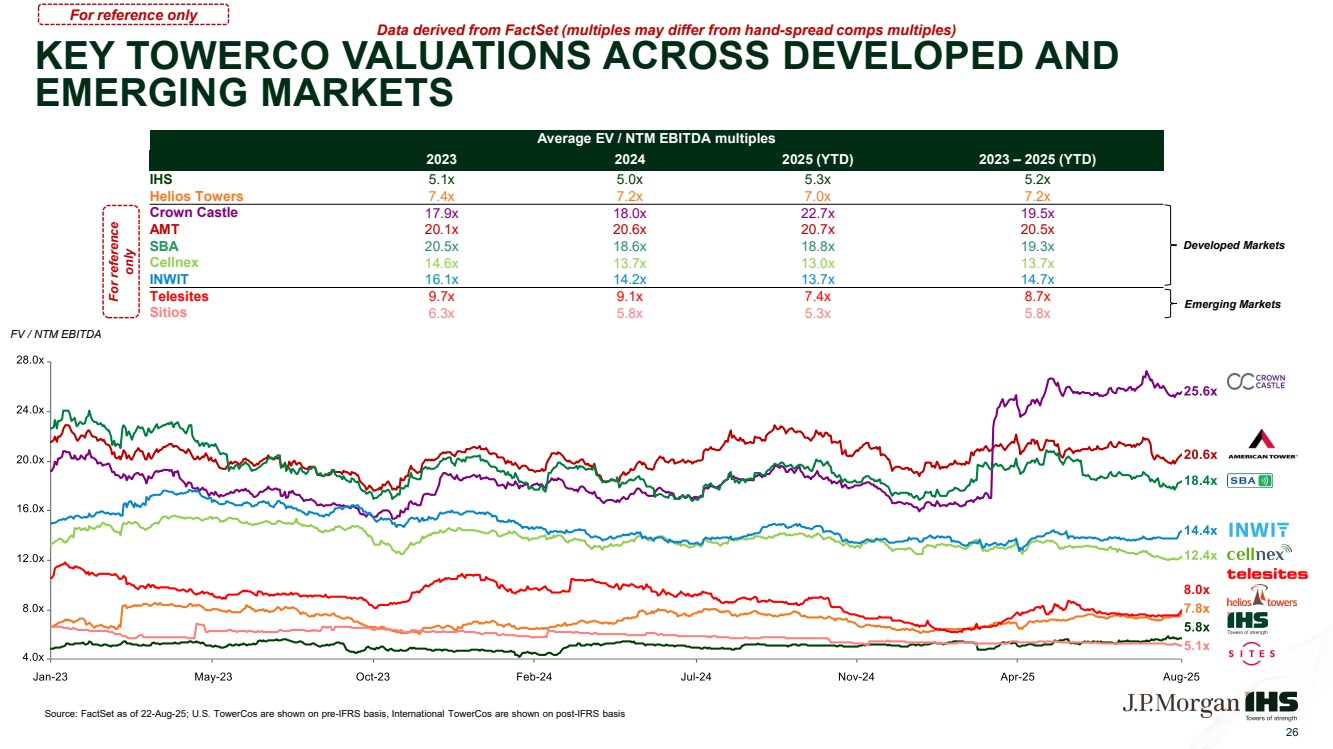

| 26 KEY TOWERCO VALUATIONS ACROSS DEVELOPED AND EMERGING MARKETS Source: FactSet as of 22-Aug-25; U.S. TowerCos are shown on pre-IFRS basis, International TowerCos are shown on post-IFRS basis Data derived from FactSet (multiples may differ from hand-spread comps multiples) Average EV / NTM EBITDA multiples 2023 2024 2025 (YTD) 2023 – 2025 (YTD) IHS 5.1x 5.0x 5.3x 5.2x Helios Towers 7.4x 7.2x 7.0x 7.2x Crown Castle 17.9x 18.0x 22.7x 19.5x AMT 20.1x 20.6x 20.7x 20.5x SBA 20.5x 18.6x 18.8x 19.3x Cellnex 14.6x 13.7x 13.0x 13.7x INWIT 16.1x 14.2x 13.7x 14.7x Telesites 9.7x 9.1x 7.4x 8.7x Sitios 6.3x 5.8x 5.3x 5.8x FV / NTM EBITDA Developed Markets Emerging Markets For reference only For reference only |

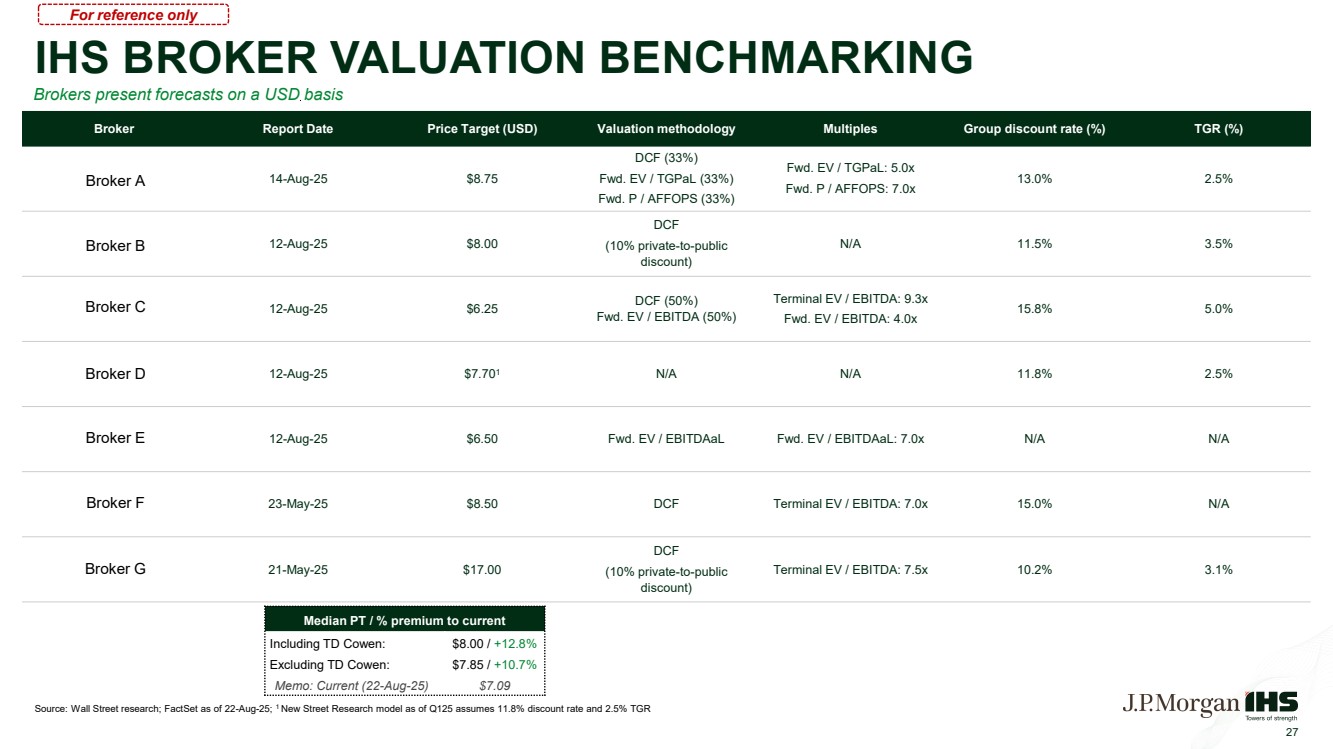

| IHS BROKER VALUATION BENCHMARKING Source: Wall Street research; FactSet as of 22-Aug-25; 1 New Street Research model as of Q125 assumes 11.8% discount rate and 2.5% TGR 27 Broker Report Date Price Target (USD) Valuation methodology Multiples Group discount rate (%) TGR (%) 14-Aug-25 $8.75 DCF (33%) Fwd. EV / TGPaL (33%) Fwd. P / AFFOPS (33%) Fwd. EV / TGPaL: 5.0x Fwd. P / AFFOPS: 7.0x 13.0% 2.5% 12-Aug-25 $8.00 DCF (10% private-to-public discount) N/A 11.5% 3.5% 12-Aug-25 $6.25 DCF (50%) Fwd. EV / EBITDA (50%) Terminal EV / EBITDA: 9.3x Fwd. EV / EBITDA: 4.0x 15.8% 5.0% 12-Aug-25 $7.701 N/A N/A 11.8% 2.5% 12-Aug-25 $6.50 Fwd. EV / EBITDAaL Fwd. EV / EBITDAaL: 7.0x N/A N/A 23-May-25 $8.50 DCF Terminal EV / EBITDA: 7.0x 15.0% N/A 21-May-25 $17.00 DCF (10% private-to-public discount) Terminal EV / EBITDA: 7.5x 10.2% 3.1% Brokers present forecasts on a USD basis Median PT / % premium to current Including TD Cowen: $8.00 / +12.8% Excluding TD Cowen: $7.85 / +10.7% Memo: Current (22-Aug-25) $7.09 For reference only Broker A Broker B Broker C Broker D Broker E Broker F Broker G |

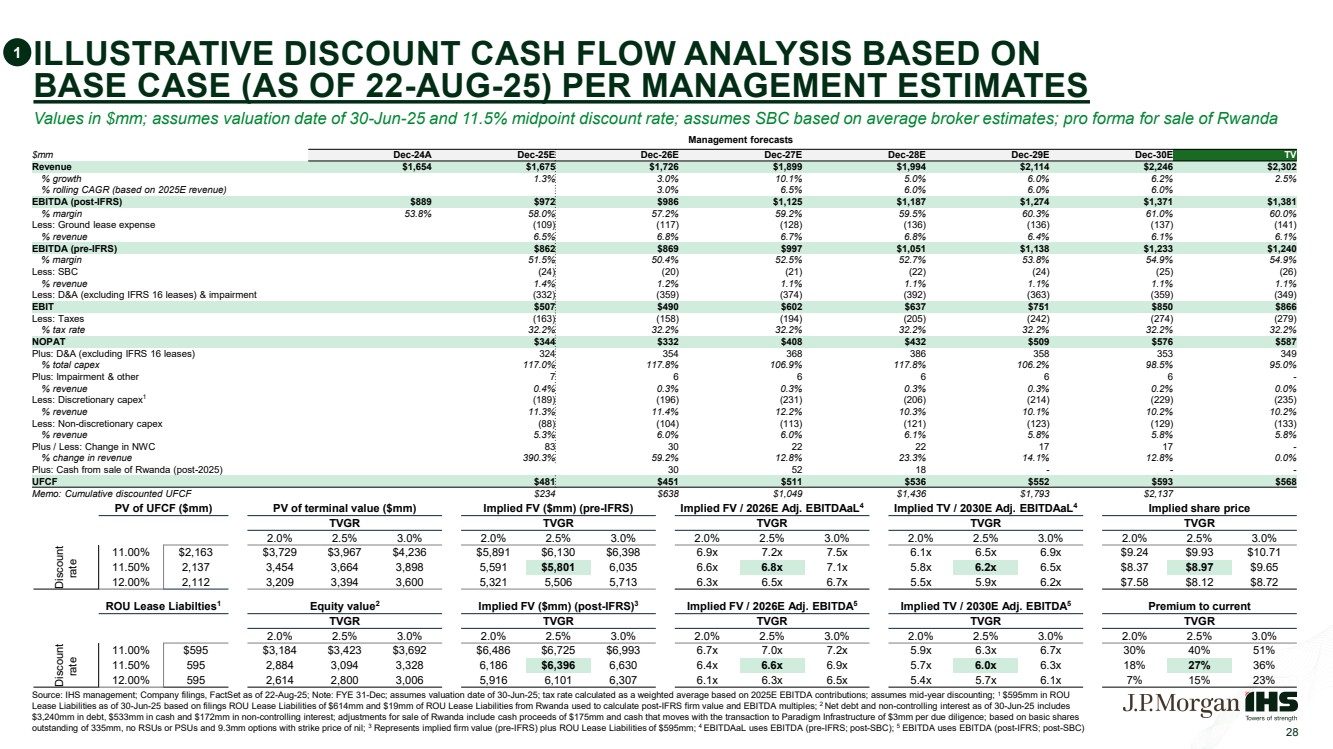

| ILLUSTRATIVE DISCOUNT CASH FLOW ANALYSIS BASED ON BASE CASE (AS OF 22-AUG-25) PER MANAGEMENT ESTIMATES 28 PV of UFCF ($mm) PV of terminal value ($mm) Implied FV ($mm) (pre-IFRS) Implied FV / 2026E Adj. EBITDAaL4 Implied TV / 2030E Adj. EBITDAaL4 Implied share price TVGR TVGR TVGR TVGR TVGR 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% Discount rate 11.00% $2,163 $3,729 $3,967 $4,236 $5,891 $6,130 $6,398 6.9x 7.2x 7.5x 6.1x 6.5x 6.9x $9.24 $9.93 $10.71 11.50% 2,137 3,454 3,664 3,898 5,591 $5,801 6,035 6.6x 6.8x 7.1x 5.8x 6.2x 6.5x $8.37 $8.97 $9.65 12.00% 2,112 3,209 3,394 3,600 5,321 5,506 5,713 6.3x 6.5x 6.7x 5.5x 5.9x 6.2x $7.58 $8.12 $8.72 ROU Lease Liabilties1 Equity value2 Implied FV ($mm) (post-IFRS)3 Implied FV / 2026E Adj. EBITDA5 Implied TV / 2030E Adj. EBITDA5 Premium to current TVGR TVGR TVGR TVGR TVGR 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% Discount rate 11.00% $595 $3,184 $3,423 $3,692 $6,486 $6,725 $6,993 6.7x 7.0x 7.2x 5.9x 6.3x 6.7x 30% 40% 51% 11.50% 595 2,884 3,094 3,328 6,186 $6,396 6,630 6.4x 6.6x 6.9x 5.7x 6.0x 6.3x 18% 27% 36% 12.00% 595 2,614 2,800 3,006 5,916 6,101 6,307 6.1x 6.3x 6.5x 5.4x 5.7x 6.1x 7% 15% 23% 1 Management forecasts $mm Dec-24A Dec-25E Dec-26E Dec-27E Dec-28E Dec-29E Dec-30E TV Revenue $1,654 $1,675 $1,726 $1,899 $1,994 $2,114 $2,246 $2,302 % growth 1.3% 3.0% 10.1% 5.0% 6.0% 6.2% 2.5% % rolling CAGR (based on 2025E revenue) 3.0% 6.5% 6.0% 6.0% 6.0% EBITDA (post-IFRS) $889 $972 $986 $1,125 $1,187 $1,274 $1,371 $1,381 % margin 53.8% 58.0% 57.2% 59.2% 59.5% 60.3% 61.0% 60.0% Less: Ground lease expense (109) (117) (128) (136) (136) (137) (141) % revenue 6.5% 6.8% 6.7% 6.8% 6.4% 6.1% 6.1% EBITDA (pre-IFRS) $862 $869 $997 $1,051 $1,138 $1,233 $1,240 % margin 51.5% 50.4% 52.5% 52.7% 53.8% 54.9% 54.9% Less: SBC (24) (20) (21) (22) (24) (25) (26) % revenue 1.4% 1.2% 1.1% 1.1% 1.1% 1.1% 1.1% Less: D&A (excluding IFRS 16 leases) & impairment (332) (359) (374) (392) (363) (359) (349) EBIT $507 $490 $602 $637 $751 $850 $866 Less: Taxes (163) (158) (194) (205) (242) (274) (279) % tax rate 32.2% 32.2% 32.2% 32.2% 32.2% 32.2% 32.2% NOPAT $344 $332 $408 $432 $509 $576 $587 Plus: D&A (excluding IFRS 16 leases) 324 354 368 386 358 353 349 % total capex 117.0% 117.8% 106.9% 117.8% 106.2% 98.5% 95.0% Plus: Impairment & other 7 6 6 6 6 6 - % revenue 0.4% 0.3% 0.3% 0.3% 0.3% 0.2% 0.0% Less: Discretionary capex1 (189) (196) (231) (206) (214) (229) (235) % revenue 11.3% 11.4% 12.2% 10.3% 10.1% 10.2% 10.2% Less: Non-discretionary capex (88) (104) (113) (121) (123) (129) (133) % revenue 5.3% 6.0% 6.0% 6.1% 5.8% 5.8% 5.8% Plus / Less: Change in NWC 83 30 22 22 17 17 - % change in revenue 390.3% 59.2% 12.8% 23.3% 14.1% 12.8% 0.0% Plus: Cash from sale of Rwanda (post-2025) 30 52 18 - - - UFCF $481 $451 $511 $536 $552 $593 $568 Memo: Cumulative discounted UFCF $234 $638 $1,049 $1,436 $1,793 $2,137 Source: IHS management; Company filings, FactSet as of 22-Aug-25; Note: FYE 31-Dec; assumes valuation date of 30-Jun-25; tax rate calculated as a weighted average based on 2025E EBITDA contributions; assumes mid-year discounting; 1 $595mm in ROU Lease Liabilities as of 30-Jun-25 based on filings ROU Lease Liabilities of $614mm and $19mm of ROU Lease Liabilities from Rwanda used to calculate post-IFRS firm value and EBITDA multiples; 2 Net debt and non-controlling interest as of 30-Jun-25 includes $3,240mm in debt, $533mm in cash and $172mm in non-controlling interest; adjustments for sale of Rwanda include cash proceeds of $175mm and cash that moves with the transaction to Paradigm Infrastructure of $3mm per due diligence; based on basic shares outstanding of 335mm, no RSUs or PSUs and 9.3mm options with strike price of nil; 3 Represents implied firm value (pre-IFRS) plus ROU Lease Liabilities of $595mm; 4 EBITDAaL uses EBITDA (pre-IFRS; post-SBC); 5 EBITDA uses EBITDA (post-IFRS; post-SBC) Values in $mm; assumes valuation date of 30-Jun-25 and 11.5% midpoint discount rate; assumes SBC based on average broker estimates; pro forma for sale of Rwanda |

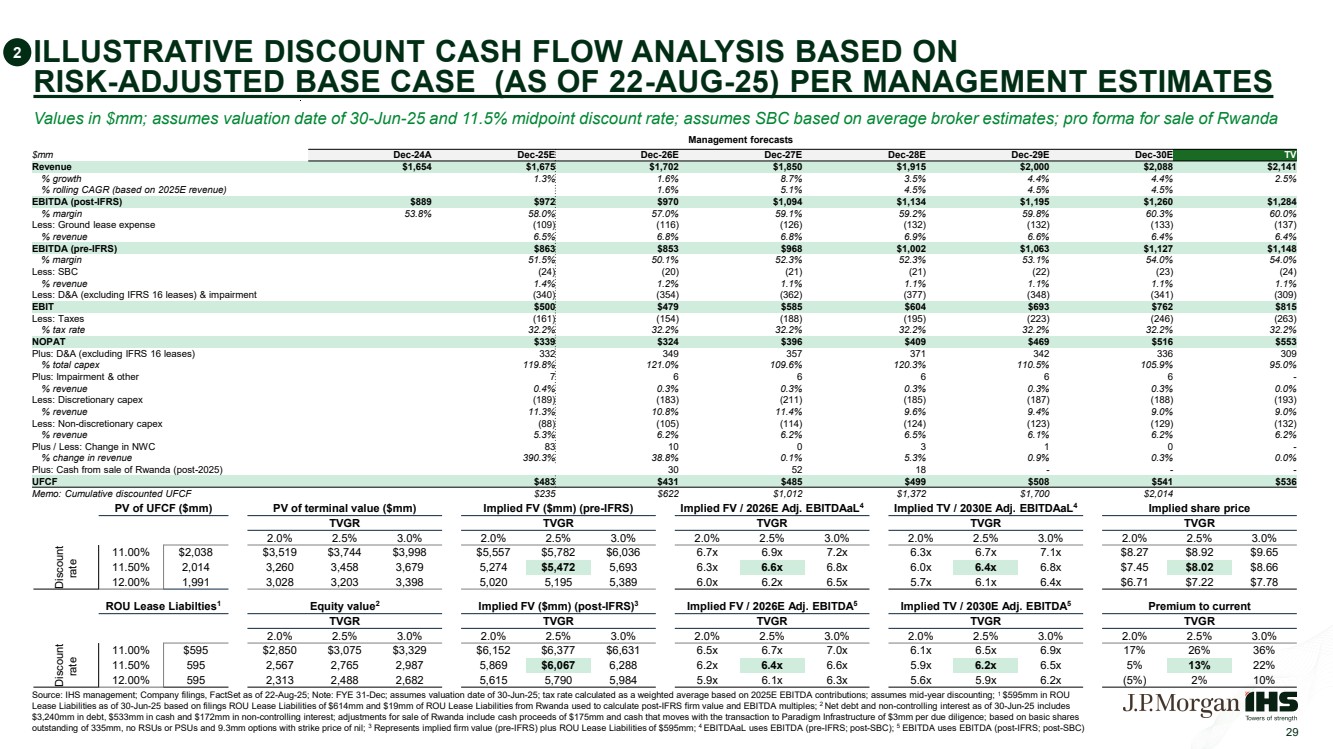

| ILLUSTRATIVE DISCOUNT CASH FLOW ANALYSIS BASED ON RISK-ADJUSTED BASE CASE (AS OF 22-AUG-25) PER MANAGEMENT ESTIMATES 29 Management forecasts $mm Dec-24A Dec-25E Dec-26E Dec-27E Dec-28E Dec-29E Dec-30E TV Revenue $1,654 $1,675 $1,702 $1,850 $1,915 $2,000 $2,088 $2,141 % growth 1.3% 1.6% 8.7% 3.5% 4.4% 4.4% 2.5% % rolling CAGR (based on 2025E revenue) 1.6% 5.1% 4.5% 4.5% 4.5% EBITDA (post-IFRS) $889 $972 $970 $1,094 $1,134 $1,195 $1,260 $1,284 % margin 53.8% 58.0% 57.0% 59.1% 59.2% 59.8% 60.3% 60.0% Less: Ground lease expense (109) (116) (126) (132) (132) (133) (137) % revenue 6.5% 6.8% 6.8% 6.9% 6.6% 6.4% 6.4% EBITDA (pre-IFRS) $863 $853 $968 $1,002 $1,063 $1,127 $1,148 % margin 51.5% 50.1% 52.3% 52.3% 53.1% 54.0% 54.0% Less: SBC (24) (20) (21) (21) (22) (23) (24) % revenue 1.4% 1.2% 1.1% 1.1% 1.1% 1.1% 1.1% Less: D&A (excluding IFRS 16 leases) & impairment (340) (354) (362) (377) (348) (341) (309) EBIT $500 $479 $585 $604 $693 $762 $815 Less: Taxes (161) (154) (188) (195) (223) (246) (263) % tax rate 32.2% 32.2% 32.2% 32.2% 32.2% 32.2% 32.2% NOPAT $339 $324 $396 $409 $469 $516 $553 Plus: D&A (excluding IFRS 16 leases) 332 349 357 371 342 336 309 % total capex 119.8% 121.0% 109.6% 120.3% 110.5% 105.9% 95.0% Plus: Impairment & other 7 6 6 6 6 6 - % revenue 0.4% 0.3% 0.3% 0.3% 0.3% 0.3% 0.0% Less: Discretionary capex (189) (183) (211) (185) (187) (188) (193) % revenue 11.3% 10.8% 11.4% 9.6% 9.4% 9.0% 9.0% Less: Non-discretionary capex (88) (105) (114) (124) (123) (129) (132) % revenue 5.3% 6.2% 6.2% 6.5% 6.1% 6.2% 6.2% Plus / Less: Change in NWC 83 10 0 3 1 0 - % change in revenue 390.3% 38.8% 0.1% 5.3% 0.9% 0.3% 0.0% Plus: Cash from sale of Rwanda (post-2025) 30 52 18 - - - UFCF $483 $431 $485 $499 $508 $541 $536 Memo: Cumulative discounted UFCF $235 $622 $1,012 $1,372 $1,700 $2,014 Source: IHS management; Company filings, FactSet as of 22-Aug-25; Note: FYE 31-Dec; assumes valuation date of 30-Jun-25; tax rate calculated as a weighted average based on 2025E EBITDA contributions; assumes mid-year discounting; 1 $595mm in ROU Lease Liabilities as of 30-Jun-25 based on filings ROU Lease Liabilities of $614mm and $19mm of ROU Lease Liabilities from Rwanda used to calculate post-IFRS firm value and EBITDA multiples; 2 Net debt and non-controlling interest as of 30-Jun-25 includes $3,240mm in debt, $533mm in cash and $172mm in non-controlling interest; adjustments for sale of Rwanda include cash proceeds of $175mm and cash that moves with the transaction to Paradigm Infrastructure of $3mm per due diligence; based on basic shares outstanding of 335mm, no RSUs or PSUs and 9.3mm options with strike price of nil; 3 Represents implied firm value (pre-IFRS) plus ROU Lease Liabilities of $595mm; 4 EBITDAaL uses EBITDA (pre-IFRS; post-SBC); 5 EBITDA uses EBITDA (post-IFRS; post-SBC) Values in $mm; assumes valuation date of 30-Jun-25 and 11.5% midpoint discount rate; assumes SBC based on average broker estimates; pro forma for sale of Rwanda PV of UFCF ($mm) PV of terminal value ($mm) Implied FV ($mm) (pre-IFRS) Implied FV / 2026E Adj. EBITDAaL4 Implied TV / 2030E Adj. EBITDAaL4 Implied share price TVGR TVGR TVGR TVGR TVGR 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% Discount rate 11.00% $2,038 $3,519 $3,744 $3,998 $5,557 $5,782 $6,036 6.7x 6.9x 7.2x 6.3x 6.7x 7.1x $8.27 $8.92 $9.65 11.50% 2,014 3,260 3,458 3,679 5,274 $5,472 5,693 6.3x 6.6x 6.8x 6.0x 6.4x 6.8x $7.45 $8.02 $8.66 12.00% 1,991 3,028 3,203 3,398 5,020 5,195 5,389 6.0x 6.2x 6.5x 5.7x 6.1x 6.4x $6.71 $7.22 $7.78 ROU Lease Liabilties1 Equity value2 Implied FV ($mm) (post-IFRS)3 Implied FV / 2026E Adj. EBITDA5 Implied TV / 2030E Adj. EBITDA5 Premium to current TVGR TVGR TVGR TVGR TVGR 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% 2.0% 2.5% 3.0% Discount rate 11.00% $595 $2,850 $3,075 $3,329 $6,152 $6,377 $6,631 6.5x 6.7x 7.0x 6.1x 6.5x 6.9x 17% 26% 36% 11.50% 595 2,567 2,765 2,987 5,869 $6,067 6,288 6.2x 6.4x 6.6x 5.9x 6.2x 6.5x 5% 13% 22% 12.00% 595 2,313 2,488 2,682 5,615 5,790 5,984 5.9x 6.1x 6.3x 5.6x 5.9x 6.2x (5%) 2% 10% 2 |

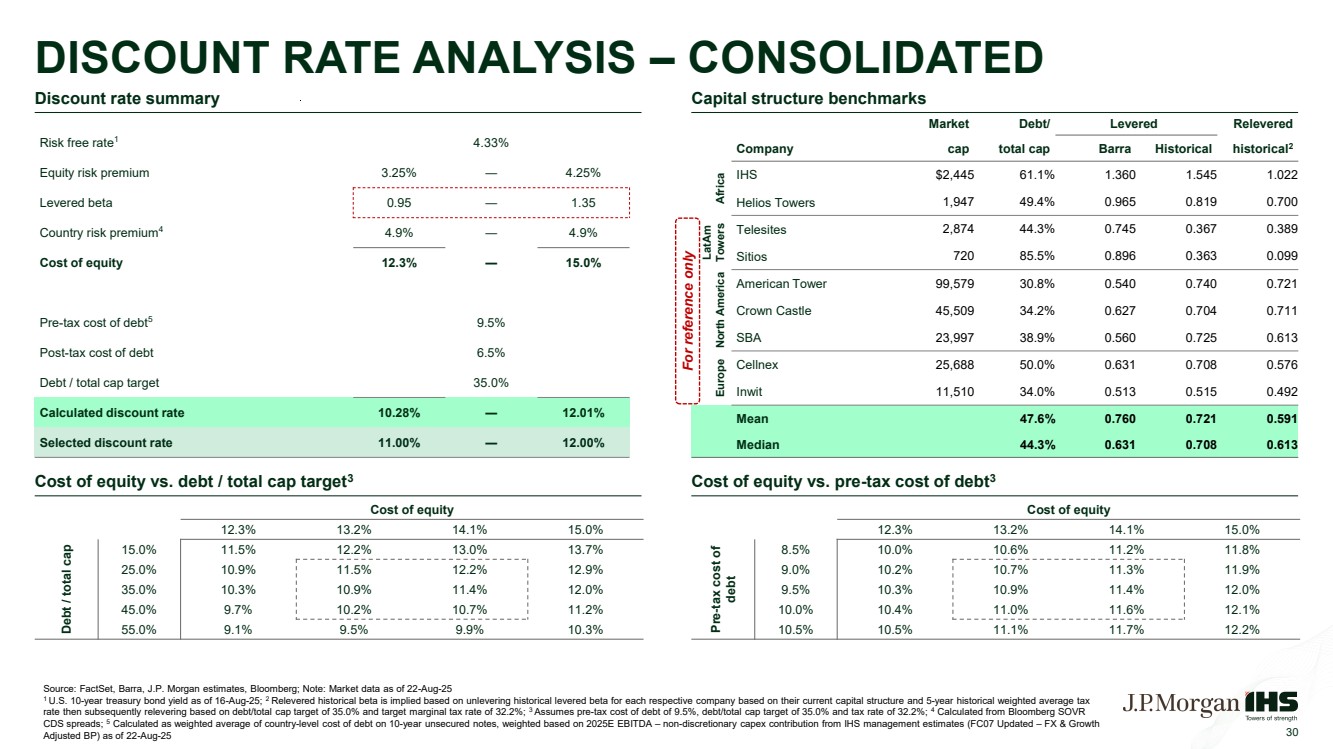

| DISCOUNT RATE ANALYSIS – CONSOLIDATED Source: FactSet, Barra, J.P. Morgan estimates, Bloomberg; Note: Market data as of 22-Aug-25 1 U.S. 10-year treasury bond yield as of 16-Aug-25; 2 Relevered historical beta is implied based on unlevering historical levered beta for each respective company based on their current capital structure and 5-year historical weighted average tax rate then subsequently relevering based on debt/total cap target of 35.0% and target marginal tax rate of 32.2%; 3 Assumes pre-tax cost of debt of 9.5%, debt/total cap target of 35.0% and tax rate of 32.2%; 4 Calculated from Bloomberg SOVR CDS spreads; 5 Calculated as weighted average of country-level cost of debt on 10-year unsecured notes, weighted based on 2025E EBITDA – non-discretionary capex contribution from IHS management estimates (FC07 Updated – FX & Growth Adjusted BP) as of 22-Aug-25 30 Cost of equity 12.3% 13.2% 14.1% 15.0% Debt / total cap 15.0% 11.5% 12.2% 13.0% 13.7% 25.0% 10.9% 11.5% 12.2% 12.9% 35.0% 10.3% 10.9% 11.4% 12.0% 45.0% 9.7% 10.2% 10.7% 11.2% 55.0% 9.1% 9.5% 9.9% 10.3% Cost of equity 12.3% 13.2% 14.1% 15.0% Pre-tax cost of debt 8.5% 10.0% 10.6% 11.2% 11.8% 9.0% 10.2% 10.7% 11.3% 11.9% 9.5% 10.3% 10.9% 11.4% 12.0% 10.0% 10.4% 11.0% 11.6% 12.1% 10.5% 10.5% 11.1% 11.7% 12.2% Risk free rate1 4.33% Equity risk premium 3.25% ― 4.25% Levered beta 0.95 ― 1.35 Country risk premium4 4.9% ― 4.9% Cost of equity 12.3% ― 15.0% Pre-tax cost of debt5 9.5% Post-tax cost of debt 6.5% Debt / total cap target 35.0% Calculated discount rate 10.28% ― 12.01% Selected discount rate 11.00% ― 12.00% Market Debt/ Levered Relevered Company cap total cap Barra Historical historical2 Africa IHS $2,445 61.1% 1.360 1.545 1.022 Helios Towers 1,947 49.4% 0.965 0.819 0.700 LatAm Towers Telesites 2,874 44.3% 0.745 0.367 0.389 Sitios 720 85.5% 0.896 0.363 0.099 North America American Tower 99,579 30.8% 0.540 0.740 0.721 Crown Castle 45,509 34.2% 0.627 0.704 0.711 SBA 23,997 38.9% 0.560 0.725 0.613 Europe Cellnex 25,688 50.0% 0.631 0.708 0.576 Inwit 11,510 34.0% 0.513 0.515 0.492 Mean 47.6% 0.760 0.721 0.591 Median 44.3% 0.631 0.708 0.613 Discount rate summary Capital structure benchmarks Cost of equity vs. debt / total cap target3 Cost of equity vs. pre-tax cost of debt3 For reference only |

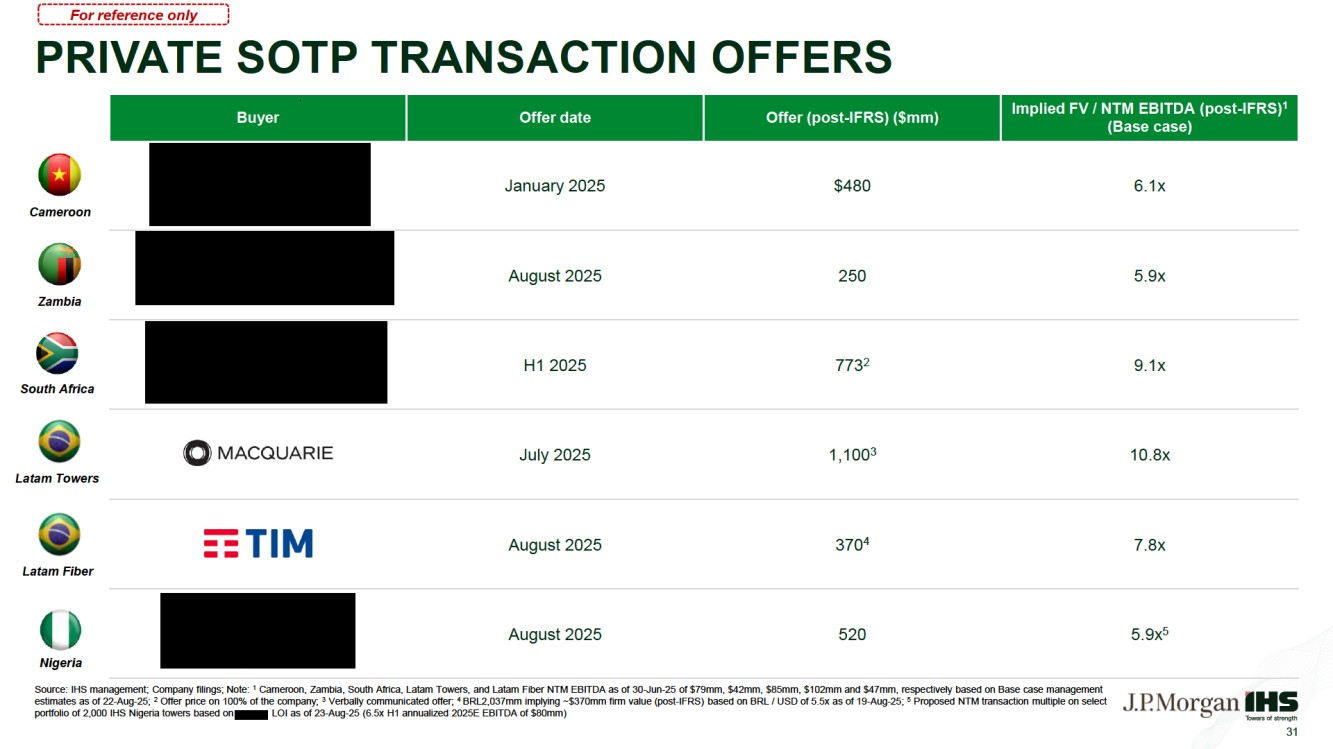

| PRIVATE SOTP TRANSACTION OFFERS Buyer Offer date Offer (post-IFRS) ($mm) Implied FV / NTM EBITDA (post-IFRS)1 (Base case) January 2025 $480 6.1x August 2025 250 5.9x H1 2025 7732 9.1x July 2025 1,1003 10.8x August 2025 3704 7.8x August 2025 520 5.9x5 31 Cameroon Zambia Source: IHS management; Company filings; Note: 1 Cameroon, Zambia, South Africa, Latam Towers, and Latam Fiber NTM EBITDA as of 30-Jun-25 of $79mm, $42mm, $85mm, $102mm and $47mm, respectively based on Base case management estimates as of 22-Aug-25; 2 Offer price on 100% of the company; 3 Verbally communicated offer; 4 BRL2,037mm implying ~$370mm firm value (post-IFRS) based on BRL / USD of 5.5x as of 19-Aug-25; 5 Proposed NTM transaction multiple on select portfolio of 2,000 IHS Nigeria towers based on Beacon LOI as of 23-Aug-25 (6.5x H1 annualized 2025E EBITDA of $80mm) Latam Towers South Africa Latam Fiber Nigeria For reference only |

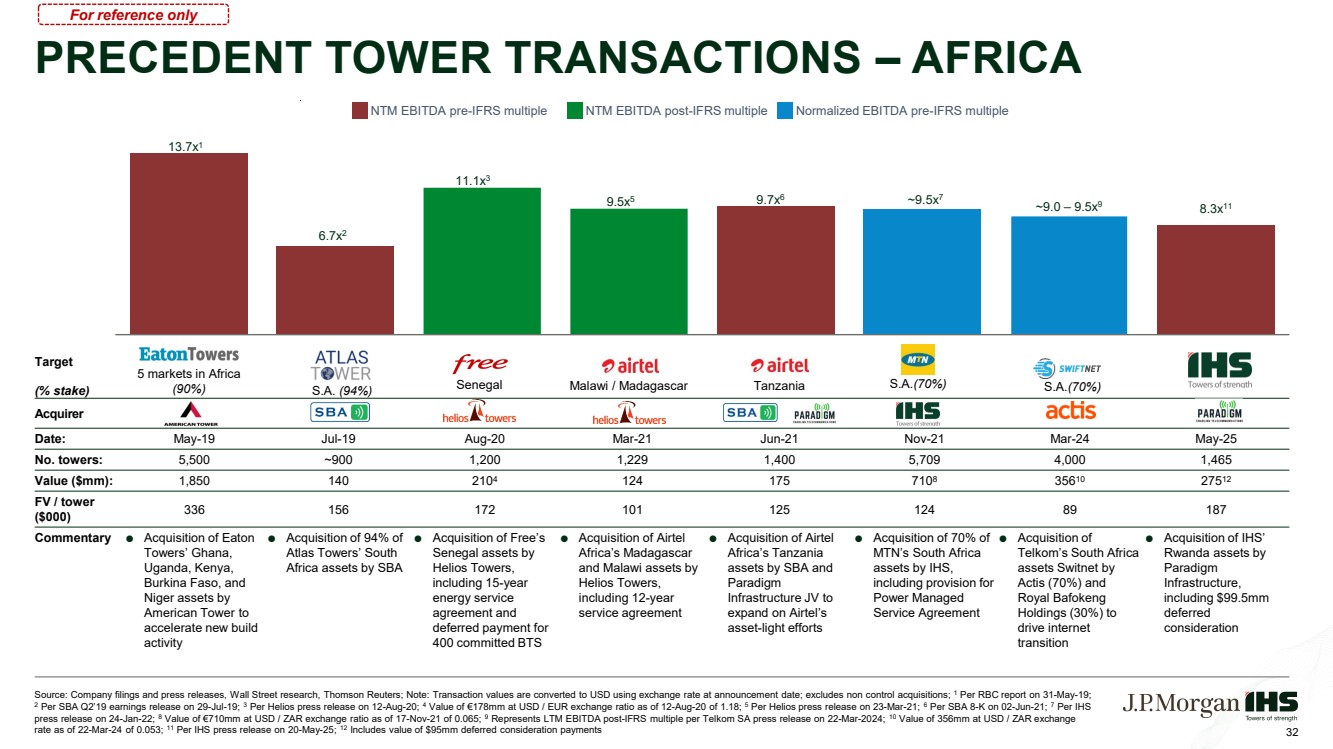

| 32 PRECEDENT TOWER TRANSACTIONS – AFRICA Source: Company filings and press releases, Wall Street research, Thomson Reuters; Note: Transaction values are converted to USD using exchange rate at announcement date; excludes non control acquisitions; 1 Per RBC report on 31-May-19; 2 Per SBA Q2’19 earnings release on 29-Jul-19; 3 Per Helios press release on 12-Aug-20; 4 Value of €178mm at USD / EUR exchange ratio as of 12-Aug-20 of 1.18; 5 Per Helios press release on 23-Mar-21; 6 Per SBA 8-K on 02-Jun-21; 7 Per IHS press release on 24-Jan-22; 8 Value of €710mm at USD / ZAR exchange ratio as of 17-Nov-21 of 0.065; 9 Represents LTM EBITDA post-IFRS multiple per Telkom SA press release on 22-Mar-2024; 10 Value of 356mm at USD / ZAR exchange rate as of 22-Mar-24 of 0.053; 11 Per IHS press release on 20-May-25; 12 Includes value of $95mm deferred consideration payments 13.7x1 6.7x2 11.1x3 9.5x5 9.7x6 ~9.5x7 ~9.0 – 9.5x9 8.3x11 Target (% stake) Acquirer Date: May-19 Jul-19 Aug-20 Mar-21 Jun-21 Nov-21 Mar-24 May-25 No. towers: 5,500 ~900 1,200 1,229 1,400 5,709 4,000 1,465 Value ($mm): 1,850 140 2104 124 175 7108 35610 27512 FV / tower ($000) 336 156 172 101 125 124 89 187 Commentary Acquisition of Eaton Towers’ Ghana, Uganda, Kenya, Burkina Faso, and Niger assets by American Tower to accelerate new build activity Acquisition of 94% of Atlas Towers’ South Africa assets by SBA Acquisition of Free’s Senegal assets by Helios Towers, including 15-year energy service agreement and deferred payment for 400 committed BTS Acquisition of Airtel Africa’s Madagascar and Malawi assets by Helios Towers, including 12-year service agreement Acquisition of Airtel Africa’s Tanzania assets by SBA and Paradigm Infrastructure JV to expand on Airtel’s asset-light efforts Acquisition of 70% of MTN’s South Africa assets by IHS, including provision for Power Managed Service Agreement Acquisition of Telkom’s South Africa assets Switnet by Actis (70%) and Royal Bafokeng Holdings (30%) to drive internet transition Acquisition of IHS’ Rwanda assets by Paradigm Infrastructure, including $99.5mm deferred consideration Senegal Malawi / Madagascar Tanzania S.A.(70%) (90%) S.A. (94%) 5 markets in Africa S.A.(70%) NTM EBITDA pre-IFRS multiple NTM EBITDA post-IFRS multiple Normalized EBITDA pre-IFRS multiple For reference only |

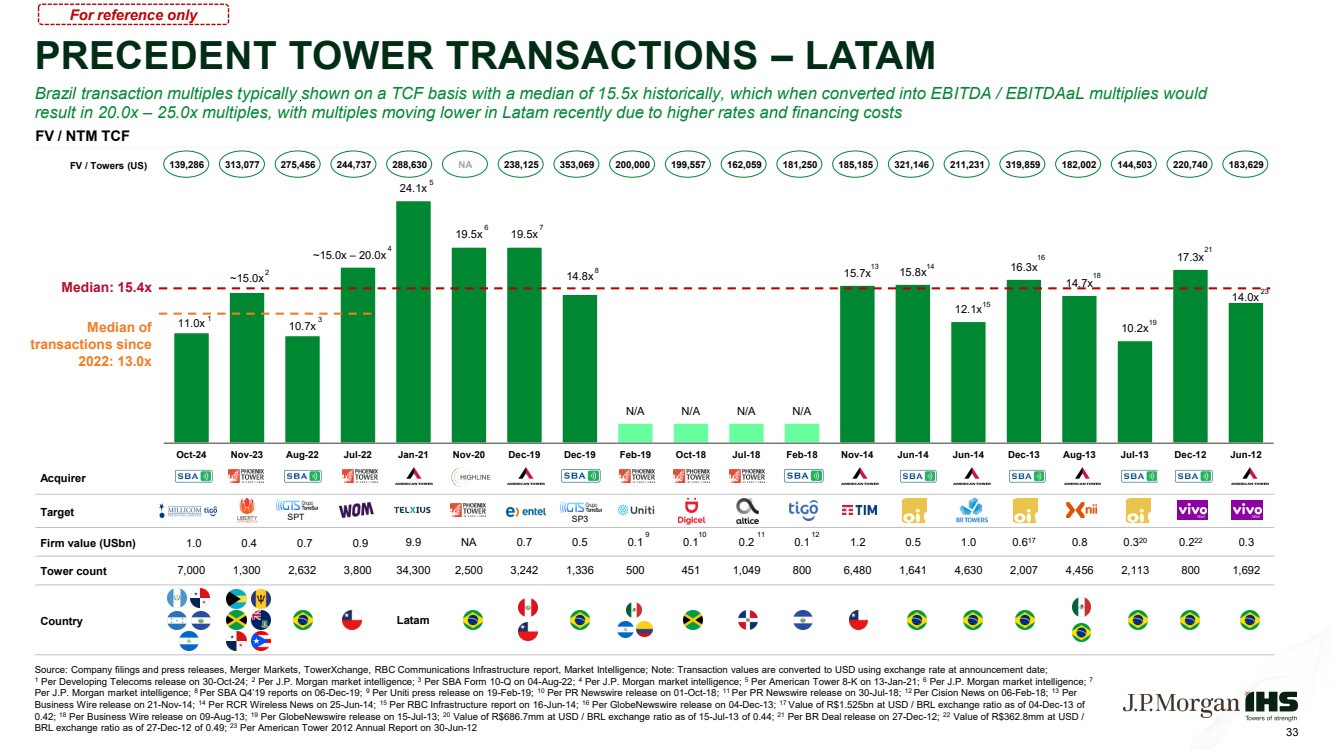

| 11.0x ~15.0x 10.7x ~15.0x – 20.0x 24.1x 19.5x 19.5x 14.8x N/A N/A N/A N/A 15.7x 15.8x 12.1x 16.3x 14.7x 10.2x 17.3x 14.0x Oct-24 Nov-23 Aug-22 Jul-22 Jan-21 Nov-20 Dec-19 Dec-19 Feb-19 Oct-18 Jul-18 Feb-18 Nov-14 Jun-14 Jun-14 Dec-13 Aug-13 Jul-13 Dec-12 Jun-12 1 2 3 4 5 6 7 8 9 10 11 12 13 14 15 16 18 19 21 23 PRECEDENT TOWER TRANSACTIONS – LATAM 33 Acquirer Target Firm value (USbn) 1.0 0.4 0.7 0.9 9.9 NA 0.7 0.5 0.1 0.1 0.2 0.1 1.2 0.5 1.0 0.617 0.8 0.320 0.222 0.3 Tower count 7,000 1,300 2,632 3,800 34,300 2,500 3,242 1,336 500 451 1,049 800 6,480 1,641 4,630 2,007 4,456 2,113 800 1,692 Country Latam Median: 15.4x FV / NTM TCF FV / Towers (US) 139,286 313,077 275,456 244,737 288,630 NA 238,125 353,069 200,000 199,557 162,059 181,250 185,185 321,146 211,231 319,859 182,002 144,503 220,740 183,629 SPT SP3 Brazil transaction multiples typically shown on a TCF basis with a median of 15.5x historically, which when converted into EBITDA / EBITDAaL multiplies would result in 20.0x – 25.0x multiples, with multiples moving lower in Latam recently due to higher rates and financing costs Median of transactions since 2022: 13.0x Source: Company filings and press releases, Merger Markets, TowerXchange, RBC Communications Infrastructure report, Market Intelligence; Note: Transaction values are converted to USD using exchange rate at announcement date; 1 Per Developing Telecoms release on 30-Oct-24; 2 Per J.P. Morgan market intelligence; 3 Per SBA Form 10-Q on 04-Aug-22; 4 Per J.P. Morgan market intelligence; 5 Per American Tower 8-K on 13-Jan-21; 6 Per J.P. Morgan market intelligence; 7 Per J.P. Morgan market intelligence; 8 Per SBA Q4’19 reports on 06-Dec-19; 9 Per Uniti press release on 19-Feb-19; 10 Per PR Newswire release on 01-Oct-18; 11 Per PR Newswire release on 30-Jul-18; 12 Per Cision News on 06-Feb-18; 13 Per Business Wire release on 21-Nov-14; 14 Per RCR Wireless News on 25-Jun-14; 15 Per RBC Infrastructure report on 16-Jun-14; 16 Per GlobeNewswire release on 04-Dec-13; 17 Value of R$1.525bn at USD / BRL exchange ratio as of 04-Dec-13 of 0.42; 18 Per Business Wire release on 09-Aug-13; 19 Per GlobeNewswire release on 15-Jul-13; 20 Value of R$686.7mm at USD / BRL exchange ratio as of 15-Jul-13 of 0.44; 21 Per BR Deal release on 27-Dec-12; 22 Value of R$362.8mm at USD / BRL exchange ratio as of 27-Dec-12 of 0.49; 23 Per American Tower 2012 Annual Report on 30-Jun-12 For reference only |

| DISCLAIMER 34 This presentation was prepared exclusively for the benefit and internal use of the J.P. Morgan client to whom it is directly addressed and delivered (including such client’s subsidiaries, the “Company”) in order to assist the Company in evaluating, on a preliminary basis, the feasibility of a possible transaction or transactions and does not carry any right of publication or disclosure, in whole or in part, to any other party. This presentation is for discussion purposes only and is incomplete without reference to, and should be viewed solely in conjunction with, the oral briefing provided by J.P. Morgan. Neither this presentation nor any of its contents may be disclosed or used for any other purpose without the prior written consent of J.P. Morgan. The information in this presentation is based upon any management forecasts supplied to us and reflects prevailing conditions and our views as of this date, all of which are accordingly subject to change. J.P. Morgan’s opinions and estimates constitute J.P. Morgan’s judgment and should be regarded as indicative, preliminary and for illustrative purposes only. In preparing this presentation, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources or which was provided to us by or on behalf of the Company or which was otherwise reviewed by us. In addition, our analyses are not and do not purport to be appraisals of the assets, stock, or business of the Company or any other entity. J.P. Morgan makes no representations as to the actual value which may be received in connection with a transaction nor the legal, tax or accounting effects of consummating a transaction. Unless expressly contemplated hereby, the information in this presentation does not take into account the effects of a possible transaction or transactions involving an actual or potential change of control, which may have significant valuation and other effects. Notwithstanding anything herein to the contrary, the Company and each of its employees, representatives or other agents may disclose to any and all persons, without limitation of any kind, the U.S. federal and state income tax treatment and the U.S. federal and state income tax structure of the transactions contemplated hereby and all materials of any kind (including opinions or other tax analyses) that are provided to the Company relating to such tax treatment and tax structure insofar as such treatment and/or structure relates to a U.S. federal or state income tax strategy provided to the Company by J.P. Morgan. J.P. Morgan's policies on data privacy can be found at http://www.jpmorgan.com/pages/privacy. J.P. Morgan is a party to the SEC Research Settlement and as such, is generally not permitted to utilize the firm's research capabilities in pitching for investment banking business. All views contained in this presentation are the views of J.P. Morgan’s Investment Bank, not the Research Department. J.P. Morgan’s policies prohibit employees from offering, directly or indirectly, a favorable research rating or specific price target, or offering to change a rating or price target, to a subject company as consideration or inducement for the receipt of business or for compensation. J.P. Morgan also prohibits its research analysts from being compensated for involvement in investment banking transactions except to the extent that such participation is intended to benefit investors. Changes to Interbank Offered Rates (IBORs) and other benchmark rates: Certain interest rate benchmarks are, or may in the future become, subject to ongoing international, national and other regulatory guidance, reform and proposals for reform. For more information, please consult: https://www.jpmorgan.com/global/disclosures/interbank_offered_rates JPMorgan Chase & Co. and its affiliates do not provide tax advice. Accordingly, any discussion of U.S. tax matters included herein (including any attachments) is not intended or written to be used, and cannot be used, in connection with the promotion, marketing or recommendation by anyone not affiliated with JPMorgan Chase & Co. of any of the matters addressed herein or for the purpose of avoiding U.S. tax-related penalties. J.P. Morgan is a marketing name for investment businesses of JPMorgan Chase & Co. and its subsidiaries and affiliates worldwide. Securities, syndicated loan arranging, financial advisory, lending, derivatives and other investment banking and commercial banking activities are performed by a combination of J.P. Morgan Securities LLC, J.P. Morgan Securities plc, J.P. Morgan SE, JPMorgan Chase Bank, N.A. and the appropriately licensed subsidiaries and affiliates of JPMorgan Chase & Co. worldwide. J.P. Morgan deal team members may be employees of any of the foregoing entities. J.P. Morgan Securities plc is authorized by the Prudential Regulation Authority and regulated by the Financial Conduct Authority and the Prudential Regulation Authority. J.P. Morgan SE is authorised as a credit institution by the German Federal Financial Supervisory Authority (Bundesanstalt für Finanzdienstleistungsaufsicht, BaFin) and jointly supervised by the BaFin, the German Central Bank (Deutsche Bundesbank) and the European Central Bank (ECB). For information on any J.P. Morgan German legal entity see: https://www.jpmorgan.com/country/US/en/disclosures/legal-entity-information#germany. For information on any other J.P. Morgan legal entity see: https://www.jpmorgan.com/country/GB/EN/disclosures/investment-bank-legal-entity-disclosures. JPMS LLC intermediates securities transactions effected by its non-U.S. affiliates for or with its U.S. clients when appropriate and in accordance with Rule 15a-6 under the Securities Exchange Act of 1934. Please consult: www.jpmorgan.com/securities-transactions This presentation does not constitute a commitment by any J.P. Morgan entity to underwrite, subscribe for or place any securities or to extend or arrange credit or to provide any other services. Copyright 2025 JPMorgan Chase & Co. All rights reserved. JPMorgan Chase Bank, N.A., organized under the laws of U.S.A. with limited liability. |