Management's Discussion and Analysis

For the three months ended March 31, 2026 and 2025

(Expressed in United States dollars, unless otherwise stated)

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

This Management's Discussion and Analysis ("MD&A") of Galiano Gold Inc. ("Galiano" or the "Company") has been prepared by management and approved by the Board of Directors as of May 13, 2026 and should be read in conjunction with the Company's unaudited condensed consolidated interim financial statements and the notes thereto for the three months ended March 31, 2026 and 2025, the audited consolidated annual financial statements and the notes thereto for the years ended December 31, 2025 and 2024 and the related MD&A. The unaudited condensed consolidated interim financial statements have been prepared in accordance with International Accounting Standard 34 - Interim Financial Reporting of the International Financial Reporting Standards ("IFRS") as issued by the International Accounting Standards Board ("IASB").

This discussion covers the three months ended March 31, 2026 and the subsequent period up to the date of issuance of this MD&A. All dollar amounts herein are expressed in United States dollars ("US dollars") unless otherwise stated. References to $ means US dollars and C$ are to Canadian dollars. The first, second, third, and fourth quarters of the Company's fiscal years ("FY") are referred to as "Q1", "Q2", "Q3", and "Q4", respectively.

The Company has included certain non-IFRS performance measures throughout this MD&A. These performance measures are monitored by management to assess the Company's operating and financial performance and to assist in business decision-making. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors and other stakeholders use this information to evaluate the Company's operating and financial performance; however, as explained elsewhere herein, these non-IFRS performance measures do not have any standardized meaning and therefore may not be comparable to similar measures presented by other issuers. Accordingly, these performance measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. Refer to section "Non-IFRS Measures" of this MD&A for additional information regarding these non-IFRS measures.

This MD&A contains forward-looking statements and should be read in conjunction with the risk factors described in sections "Risks and Uncertainties" and "Cautionary Statements" at the end of this MD&A.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

TABLE OF CONTENTS

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

BUSINESS OVERVIEW

Galiano was incorporated on September 23, 1999, under the Business Corporations Act of British Columbia, Canada. Galiano is a gold mining company with a strategic vision to become a mid-tier producer. The Company's operating gold mine is the Asanko Gold Mine ("AGM") located on the Asankrangwa Gold Belt in the Republic of Ghana ("Ghana"), West Africa. The AGM consists of four primary open-pit deposits: Abore, Nkran, Esaase and Miradani North, multiple satellite deposits and a carbon-in-leach processing plant, with a capacity of 5.8 million tonnes ("Mt") per annum. The AGM also owns various exploration licenses across the highly prospective and underexplored Asankrangwa Gold Belt.

Galiano is focused on growing a sustainable business to create value for all stakeholders through production, exploration, and disciplined deployment of its financial resources.

The Company's common shares trade under the symbol "GAU" on the Toronto Stock Exchange in Canada and the NYSE American Stock Exchange in the United States.

Additional information on the Company, including its most recent Annual Information Form ("AIF"), is available under the Company's SEDAR+ profile at www.sedarplus.ca and the Company's website: www.galianogold.com.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

Q1 2026 HIGHLIGHTS

Safety

No lost-time injuries ("LTI") nor total recordable injuries (inclusive of LTIs) ("TRI") recorded. The AGM has achieved 8.8 million hours worked without an LTI as of March 31, 2026.

12‐month rolling LTI and TRI frequency rates as of March 31, 2026 of 0.00 and 0.11 per million hours worked, respectively.

Financial

Cash and cash equivalents of $114.9 million as of March 31, 2026 and no debt.

Generated cash flow from operating activities of $46.7 million during Q1 2026, an 80% increase from Q1 2025.

Income from mine operations of $72.5 million during Q1 2026.

Net income of $0.13 and adjusted net income1 of $0.11 per common share (basic) during Q1 2026.

Adjusted EBITDA1 of $93.4 million during Q1 2026, an increase of 364% from Q1 2025.

Mining Operations

Processing

1.3 Mt of ore was milled at an average feed grade of 0.9 g/t, with metallurgical recovery averaging 90%. Mill availability during Q1 2026 was 89% due to a planned 5-day maintenance shutdown.

Produced 34,747 ounces of gold, a 68% increase compared to Q1 2025, and in line with the Company's first half indicative production range.

Sold 34,181 ounces of gold at a record quarterly average price of $4,857 per ounce ("/oz"), excluding the effect of realized losses on gold hedging instruments.

Nkran Cut 3 Development

Development of Cut 3 at the Nkran deposit continued with 4.7 Mt of waste mined. Additional mining equipment is expected to be mobilized during Q2 2026 and, thereafter, mined volumes at Nkran are forecast to increase significantly.

Capitalized development pre-stripping costs at Nkran Cut 3 of $13.5 million.

Costs

All-in sustaining costs1 ("AISC") of $2,361/oz, a 6% decrease compared to Q1 2025 despite higher royalties expense.

FY 2026 AISC1 guidance has been revised to between $2,300/oz and $2,600/oz (previously $2,000/oz and $2,300/oz), resulting from the amendment to Ghana’s royalty framework.

____________________________________________

1 Non-IFRS measure. Refer to "Non-IFRS Measures" in this MD&A.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

Exploration

Drilled 11,578 meters (“m”) at the Abore deposit, which consisted of infill and step-out drilling up to 200m below the existing underground Mineral Resource boundary. Drilling successfully indicated extension of mineralization at depth, along strike, and across previously untested areas outside the current underground Mineral Resource. Highlights from the Q1 2026 Abore drilling program, as reported in the Company’s news release dated May 11, 2026, included:

Main pit ore shoot expanded ~95m further down dip to the north;

~200m of strong mineralization defined between the Main pit ore shoot and the saddle zone;

High-grade intercept below the northern end of Main pit, which remains open; and

High-grade mineralization intersected up to 180m below the current underground Mineral Resource.

Completed 2,501m of infill drilling at Esaase to support the conversion of Inferred Mineral Resources to the Indicated category. Following successful initial results, the Company has expanded the FY 2026 exploration budget by $7.5 million to complete a total program of 33,000m at Esaase.

RECENT DEVELOPMENTS

The Company published updated mineral reserve and mineral resource estimates for the AGM on February 12, 2026. Refer to the Company’s news release dated February 12, 2026, a copy of which is available under the Company’s SEDAR+ profile at www.sedarplus.ca, for additional disclosure regarding the AGM’s Mineral Reserve and Mineral Resource estimates, including key assumptions underlying the estimates.

Effective March 10, 2026, the Government of Ghana passed into law a bill to amend the country's royalty framework applicable to gold miners. Under this amendment, gold royalties payable are subject to a sliding scale, starting at 5% (if gold prices are below $1,900/oz) and increasing to 12% (if gold prices exceed $4,500/oz).

On March 13, 2026, the Government of Ghana passed into law an amendment to the Growth and Sustainability Levy ("GSL") rate, reducing it from 3% to 1% of gold revenues.

On March 20, 2026, the Company was added to the VanEck Junior Gold Miners ETF ("GDXJ"), following the GDXJ's most recent semi-annual review and rebalancing.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

2026 GUIDANCE AND OUTLOOK

FY 2026 production guidance for the AGM remains between 140,000 ounces and 160,000 ounces of gold. As a result of the amendment to Ghana’s royalty law applicable to gold miners, which had an effective date of March 10, 2026, FY 2026 AISC1 is now guided to between $2,300/oz and $2,600/oz (previously $2,000/oz and $2,300/oz) at an assumed gold price of $4,500/oz. If diesel prices in Ghana remain elevated for a prolonged period, the AGM’s forecast AISC1 for FY 2026 would be approximately $100/oz to $130/oz higher.

AISC1 for the AGM is anticipated to reduce over 2026 and in 2027 as grades from Abore increase and drive higher production.

The Abore deposit is expected to provide the majority of mill feed in FY 2026, with the Esaase deposit providing supplementary ore. Higher mined grades are expected from Abore in the second half of the year, therefore gold production is forecast to be weighted to the back half of FY 2026. Given the expected ramp-up of gold production over FY 2026, the Company reaffirms indicative production ranges for the first and second half of 2026 as follows.

| Unit | H1 2026 | H2 2026 | |

| Gold production | Oz | 60,000 to 70,000 | 80,000 to 90,000 |

Total sustaining capital expenditures are guided to between $16 million to $18 million for FY 2026, excluding sustaining capitalized stripping costs. Sustaining capital expenditures in FY 2026 include the expansion of the tailings facility, minor upgrades to the processing plant, and upgrades to mine camp infrastructure.

Development capital for FY 2026 is guided at between $120 million to $140 million, which primarily relates to Nkran Cut 3 waste stripping ($100 million to $120 million) and village resettlement costs. Mined volumes at Nkran Cut 3 are expected to increase significantly from Q2 2026 onwards as additional mining equipment is mobilized to the AGM.

Following positive results from the initial phase of infill drilling at the Esaase deposit, the program has been expanded by 24,000m with an estimated cost of $7.5 million. Exploration expenditures at the AGM are now guided to between $24 million to $26 million (previously $17 million to $19 million), targeting Mineral Reserve growth at Esaase, underground Mineral Resource expansion at Abore, and priority greenfield areas on the AGM's tenements.

(1) Non-IFRS measure. Refer to section "Non-IFRS Measures" in this MD&A.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

SELECTED OPERATIONAL AND FINANCIAL HIGHLIGHTS

| Q1 2026 | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 | |

| Mining Operations | |||||

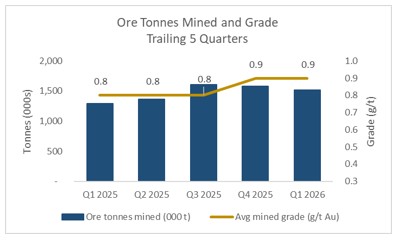

| Ore mined ('000t) | 1,521 | 1,575 | 1,605 | 1,365 | 1,296 |

| Waste mined ('000t) | 9,084 | 8,337 | 9,067 | 8,101 | 8,314 |

| Strip ratio (waste-to-ore) | 6.0 | 5.3 | 5.7 | 5.9 | 6.4 |

| Average gold grade mined (g/t) | 0.9 | 0.9 | 0.8 | 0.8 | 0.8 |

| Mining costs ($/t mined) | 3.73 | 3.94 | 3.38 | 3.59 | 3.31 |

| Ore tonnes trucked ('000 t) | 1,163 | 1,069 | 1,288 | 1,030 | 1,053 |

| Ore transportation costs ($/t trucked) | 4.42 | 4.45 | 4.35 | 4.49 | 4.43 |

| Processing | |||||

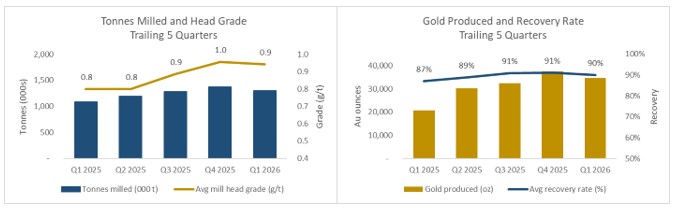

| Ore milled ('000t) | 1,305 | 1,369 | 1,283 | 1,193 | 1,086 |

| Average mill head grade (g/t) | 0.9 | 1.0 | 0.9 | 0.8 | 0.8 |

| Average recovery rate (%) | 90 | 91 | 91 | 89 | 87 |

| Processing costs ($/t milled) | 12.79 | 12.13 | 12.57 | 12.89 | 14.37 |

| General and administrative costs ($/t milled) | 7.09 | 7.58 | 6.62 | 6.24 | 5.78 |

| Gold produced (oz) | 34,747 | 37,574 | 32,533 | 30,350 | 20,734 |

| Development Stripping - Nkran Cut 3 | |||||

| Waste mined ('000t) | 4,707 | 4,324 | 3,426 | 1,723 | 810 |

| Mining costs ($/t mined) | 2.85 | 2.48 | 3.29 | 4.00 | 3.98 |

| Development capitalized stripping costs ($m) | 13.5 | 11.1 | 12.0 | 6.9 | 3.2 |

| Capital Expenditures | |||||

| Sustaining capital ($m) | 3.6 | 4.4 | 4.2 | 2.2 | 1.3 |

| Development capital ($m) | 3.4 | 0.7 | 2.9 | 4.9 | 3.3 |

| Sustaining capitalized stripping costs ($m) | 6.4 | 11.7 | 11.9 | 15.1 | 11.9 |

| Financial, Costs and Cash Flow | |||||

| Revenue ($m) | 166.5 | 159.7 | 114.2 | 97.3 | 76.6 |

| Gold sold (oz) | 34,181 | 38,276 | 32,577 | 29,287 | 26,994 |

| Average gold sales price - gross ($/oz)(1) | 4,857 | 4,164 | 3,501 | 3,317 | 2,833 |

| Average gold sales price - net ($/oz)(2) | 4,122 | 3,744 | 3,099 | 2,951 | 2,651 |

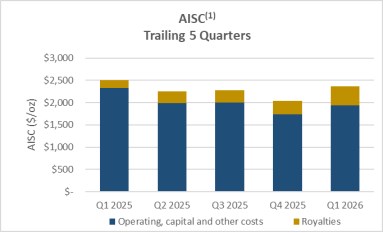

| AISC ($/oz sold)(3) | 2,361 | 2,033 | 2,283 | 2,251 | 2,501 |

| Income (loss) from mine operations ($m) | 72.5 | 51.1 | 10.0 | 24.7 | (19.8) |

| Adjusted net income (loss) ($m)(3) | 29.5 | 40.0 | (2.8) | 21.0 | 1.4 |

| Adjusted EBITDA ($m)(3) | 93.4 | 85.5 | 37.8 | 39.9 | 20.1 |

| Cash flow from operating activities ($m) | 46.7 | 55.8 | 40.4 | 35.8 | 25.9 |

(1) Gross average gold sales price is a non-IFRS measure and calculated by dividing revenue, as reported in the Company's consolidated financial statements, by the number of gold ounces sold during the period.

(2) Net average gold sales price is a non-IFRS measure and calculated by dividing revenue less realized losses on gold hedge derivative instruments, as reported in the Company's consolidated financial statements, by the number of gold ounces sold during the period.

(3) Non-IFRS measure. Refer to "Non-IFRS Measures" in this MD&A.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

Q1 2026 Operational Analysis for the Asanko Gold Mine

Mining Operations

Abore

Mined 1.1 Mt of ore, consistent with Q4 2025, at an average grade of 0.9 g/t gold.

Strip ratio of 6.1:1, in line with Q4 2025.

Esaase

Mined 0.4 Mt of ore, an increase of 123% from Q4 2025, at an average grade of 0.7 g/t gold. Ore tonnes mined were lower in Q4 2025 due to the temporary suspension of mining at Esaase that resulted from a community incident.

Strip ratio of 5.9:1, an increase of 28% from Q4 2025.

Mining Operating Costs

Mining costs per tonne at Abore and Esaase for Q1 2026 amounted to $3.73 per tonne ("/t") compared to $3.31/t in Q1 2025. The increase in mining costs per tonne in Q1 2026 was attributable to higher drill and blast costs, resulting from mining a higher proportion of fresh rock at Abore, and increasing mining depths and haul distances.

Ore Transportation

Ore transportation reflects ore transported from mined deposits located greater than 5 kilometers ("km") from the processing plant, which currently includes the Abore and Esaase deposits. Ore transported from closer deposits is considered rehandling, the costs of which are included within mining costs. During the quarter, 1.2 Mt of ore was trucked from the Abore and Esaase deposits to the processing plant, compared to 1.1 Mt in Q4 2025.

Ore transportation unit costs in Q1 2026 were in line with Q1 2025, as material was trucked from both Abore and Esaase to the AGM processing plant in each period.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

Processing

Gold Production

The AGM produced 34,747 ounces of gold during Q1 2026, a decrease of 8% from Q4 2025, as the processing plant in Q1 2026 milled 1.3 Mt of ore at an average grade of 0.9 g/t with metallurgical recovery averaging 90%. Approximately 60% of the mill feed was sourced from mined ore at Abore, with the remainder of mill feed primarily from the Esaase deposit.

Milled Tonnes

Mill throughput in Q1 2026 was 5% lower than Q4 2025 due to a planned 5-day shutdown of the processing plant to complete a mill reline and other planned maintenance. This resulted in mill availability of 89% during Q1 2026.

Mill throughput was 20% higher in Q1 2026 than the comparative period of 2025 due to the commissioning of the permanent secondary crushing circuit in July 2025, as well as an unplanned mill shutdown in Q1 2025.

Average Head Grade

Average mined grades in Q1 2026 were slightly lower than Q4 2025 due to spatial differences in the areas mined.

Processing Costs

Processing costs per tonne for Q1 2026 was $12.79, an 11% decrease from Q1 2025. The decrease in processing costs per tonne was largely driven by higher mill throughput volumes, partly offset by costs associated with a mill reline and other maintenance activities in Q1 2026.

Capital Expenditures

Sustaining capital expenditures totaled $3.6 million during Q1 2026, an increase of $2.3 million compared to Q1 2025. The increase in sustaining capital expenditures was largely driven by costs associated with a tailings facility expansion.

Development capital expenditures during Q1 2026 totaled $3.4 million, in line with Q1 2025. Development capital expenditures in Q1 2026 related primarily to costs associated with relocating villages near the AGM's operations.

Nkran Cut 3 Development

Development of Cut 3 at the Nkran deposit continued during the quarter with 4.7 Mt of waste rock mined, an increase of 9% from Q4 2025. Mining costs per tonne at Nkran for Q1 2026 amounted to $2.85/t compared to $3.98/t in Q1 2025. The decrease in mining costs per tonne was attributable to higher volumes mined. At total of $13.5 million in stripping costs were capitalized at Nkran during Q1 2026. These stripping costs are classified as development capital expenditures.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

The mining contractor is currently mobilizing additional mining equipment to the AGM; therefore, mined volumes at Nkran are forecast to increase significantly in the second half of 2026.

Total Cash Costs and AISC

Total Cash Costs1

During Q1 2026, total cash costs1 were $1,735/oz, compared to $1,730/oz in the comparative period. The total cash costs1 were flat quarter-on-quarter as higher gold ounces sold were offset by higher royalties resulting from higher average gold sales prices and the amendment to Ghana's royalty framework.

Total cash costs per ounce1 in Q1 2026 were 21% higher than Q4 2025 due to higher royalties and 11% fewer gold ounces sold. The impact of the new sliding scale royalty on Q1 2026 total cash costs1 was approximately $80/oz.

AISC1

During Q1 2026, AlSC1 was $2,361/oz, compared to $2,501/oz in Q1 2025. The decrease in AlSC1 resulted from a 27% increase in gold ounces sold in Q1 2026, partly offset by a $10.0 million increase in royalties.

Relative to Q4 2025, AISC1 increased by 16% in Q1 2026 due to lower gold sales volumes and a $3.1 million increase in royalties, as discussed above.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

EXPLORATION ACTIVITIES

The Company holds a district-scale land package of 476km2 on the highly prospective and underexplored Asankrangwa Gold Belt. During Q1 2026, the AGM conducted exploration programs to assess existing mineralization and expansion potential at several deposits, while also evaluating their broader resource prospects. Concurrent efforts focused on identifying greenfield exploration opportunities throughout the regional tenement portfolio.

Following a very successful 2025 program, exploration efforts at the AGM in 2026 will be focused on supporting a revised life of mine plan and mineral reserve and mineral resource updates, anticipated in Q1 2027.

Exploration activities will be heavily focused on delivering near-term value through mineral reserve and mineral resource growth within the brownfields space, while simultaneously continuing to advance the greenfields generative portfolio at the AGM via early-stage fieldwork and drill testing at numerous high-priority regional targets.

Esaase

A phased program of infill drilling is planned for Esaase through 2026, which is designed to convert existing open pit Mineral Resources from the Inferred to Indicated category, and has the potential to significantly increase the Esaase Mineral Reserve and support planning for potential future open pit expansion.

Phase 1 of the Esaase infill drilling program consists of a planned 9,000m focused on the Main pit. The drilling commenced ahead of schedule in February with a rolling mobilization of up to four drill rigs operational by the end of Q1 2026. 2,501m of drilling was completed in Q1 2026. Partial assays have been received and are currently undergoing quality assurance and quality control (“QA/QC”) measures.

Following successful early results in Phase 1, the Company has committed to the full program of 33,000m, which is estimated to cost an additional $7.5 million in 2026 than previously guided. This program is expected to be completed in advance of the 2027 Mineral Resource and Mineral Reserve update planned for Q1 2027.

Results received to date continue to demonstrate exceptional Mineral Resource growth potential at Abore, with drilling successfully extending mineralization at depth, along strike, and across previously untested areas outside the current underground Mineral Resource.

Current step-out drilling has intersected mineralization up to 180m below the existing underground Mineral Resource, while infill drilling has improved continuity across key mineralized zones that currently sit outside the existing Mineral Resource. Drilling beneath the Main and South pit areas also continues to confirm robust extensions of mineralization both down plunge and along strike of existing mineralization. Significant intercepts from the Q1 2026 Abore drilling program included:

Refer to the Company’s news release dated May 11, 2026, a copy of which is available under the Company’s SEDAR+ profile at www.sedarplus.ca, for additional information regarding these drill results, including data verification and QA/QC measures.

Abore

Drilling at Abore continued in Q1 2026 with 11,578m completed of a planned program total of 32,000m of diamond drilling. This drilling is part of the 2026 Abore drilling program that aims to continue to grow the underground Mineral Resource through step-out drilling to at least 200m below the maiden underground Mineral Resource that was released in February 2026. Drilling consists of selective infill drilling designed to prove continuity of mineralization within and below the current underground Mineral Resource, with flexibility to step-out and test for mineralization at deeper elevations based on results as drilling progresses.

Greenfield Targets

Work on regional greenfield targets across the AGM's tenements in Q1 2026 was focused on the New Obuase prospecting lease, which contains the Nsoroma, Ahuofe and other priority targets located along strike to the southwest of the Nkran deposit. Work in Q1 2026 consisted of localized ground truthing and regolith mapping over multiple targets.

Exploration Costs

Exploration expenditure in Q1 2026 was $5.0 million and are tracking in line with guidance.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

ENVIRONMENTAL, SOCIAL AND CORPORATE GOVERNANCE

Sustainability is at the core of Galiano's business strategy. The Company believes that a comprehensive sustainability strategy is integral to meeting its strategic objectives by positively supporting stakeholder relationships, improving risk management, reducing the AGM's production costs, and benefiting host communities beyond the life of the mine.

For further details on the Company's sustainability program, refer to the Company's 2024 Sustainability Report published on May 12, 2025, which is available on the Company's website at www.galianogold.com.

Health & Safety

| Q1 2026 | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 | |

| Health and safety | |||||

| LTIs(1) | - | - | - | - | 2 |

| TRIs(1) | - | - | 1 | - | 3 |

| 12-month rolling LTI frequency rate(1) | 0.00 | 0.24 | 0.39 | 0.42 | 0.43 |

(1) The Company records and reports injuries in accordance with the International Council on Mining and Metals' (ICMM) Mining Principles.

Safety performance remained strong in Q1 2026, with no injuries recorded. The Company achieved 12 consecutive months, and 8.8 million hours worked, without a reported LTI. As of March 31, 2026, it had been 365 days since an LTI occurred.

Social Performance

Implementation of the Five-Year Socio-Economic Development Plan continued during Q1 2026, with steady progress across employment and income-generating initiatives, skills development, and infrastructure partnerships, including advancement of youth apprenticeship programs. Stakeholder engagement across catchment communities also remained strong.

Environmental Performance

Environmental monitoring during Q1 2026 indicated full compliance with regulatory standards for water, air quality, and noise. Routine quarterly regulatory inspections were completed during Q1 2026, including of the AGM's tailings facility, with no non-conformances identified.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

MACROECONOMIC FACTORS

Gold Price

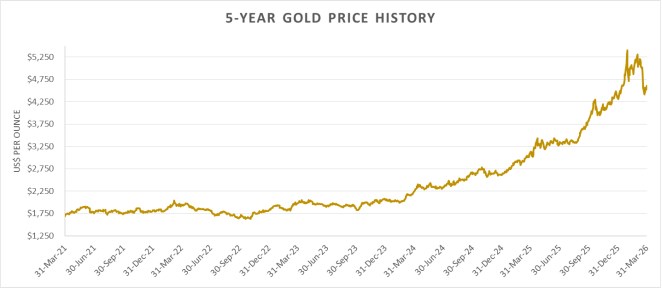

The price of gold is the largest single external factor in determining the Company's profitability and cash flow from operations. Therefore, the financial performance of the Company is expected to be closely linked to the price of gold. Historically, the price of gold has been subject to volatile price movements over short periods of time and affected by numerous macroeconomic factors that are beyond the Company's control. The price of gold may be impacted by currency exchange rate fluctuations and the relative strength of the US dollar, the supply of and demand for gold, geopolitical events, and macroeconomic factors, such as interest rates and inflation expectations. During Q1 2026, the price of gold traded between a low of $4,353/oz at the beginning of January and a high of $5,405/oz in late January. The average gold price for Q1 2026 amounted to $4,873/oz, based on the London Bullion Market Association ("LBMA") PM benchmark, compared to the Q1 2025 average price of $2,860/oz. Gold prices during Q1 2026 were influenced by central bank purchasing, geopolitical risks, and volatility in interest rates and the US dollar, among other factors. Central bank demand for gold continues to be a key driver influencing prices, as central banks diversify their reserve holdings away from treasuries and into gold.

During Q1 2026, the Company's average gross gold sales price was $4,857/oz, excluding the effect of realized losses on gold hedging instruments.

Ghana Economy

In October 2023, the International Monetary Fund ("IMF") and the Ghana government reached a staff-level agreement on the first review of its $3.0 billion financing arrangement over a 3-year period (the "IMF Loan"). In December 2025, the IMF and Ghana agreed on the fifth review of the country's economic reform agenda, providing Ghana with access to an additional $385.0 million under the IMF Loan, bringing total disbursements under the IMF Loan to $2.8 billion.

Ghana's recent fiscal climate has not materially impacted the operations of the AGM, as much of the cost structure is tied to the US dollar.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

During Q1 2026, the Ghanaian Cedi ("Cedi") depreciated by approximately 5% relative to the US dollar. Periods when the Cedi demonstrates strength relative to the US dollar puts moderate pressure on the AGM's cost and capital structure. However, most of the AGM's significant cost drivers (e.g. mining contracts, diesel) are denominated in US dollars, thus isolating them from volatile movements in the Cedi.

Oil Prices

During Q1 2026, tensions in the Middle East escalated, resulting in the temporary closure of the Strait of Hormuz (“Strait”). It is estimated that 20% to 30% of global oil supply flows through the Strait and, consequently, oil prices have experienced a rapid appreciation in 2026 with Brent crude oil spot prices advancing to approximately $110 per barrel as of May 12, 2026.

Diesel fuel is a key cost driver of the AGM’s cost structure. To the extent oil prices remain at elevated levels, the AGM’s mining costs would be impacted. Since closure of the Strait in early March 2026, diesel prices in Ghana have increased by approximately 75% as of April 30, 2026.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

REVIEW OF Q1 2026 CONSOLIDATED FINANCIAL RESULTS

Selected financial results for the three months ended March 31, 2026 and 2025

| Three months ended March 31, | ||||||

| 2026 | 2025 | |||||

| (in thousands of US dollars, except per share amounts) | $ | $ | ||||

| Revenue | 166,524 | 76,590 | ||||

| Realized and unrealized losses on gold hedges | (21,896 | ) | (35,116 | ) | ||

| Net revenue | 144,628 | 41,474 | ||||

| Cost of sales: | ||||||

| Production costs | (45,250 | ) | (42,242 | ) | ||

| Depreciation and depletion | (12,380 | ) | (14,393 | ) | ||

| Royalties | (14,545 | ) | (4,595 | ) | ||

| Total cost of sales | (72,175 | ) | (61,230 | ) | ||

| Income (loss) from mine operations | 72,453 | (19,756 | ) | |||

| General and administrative expenses | (5,475 | ) | (5,100 | ) | ||

| Exploration and evaluation expenditures | (722 | ) | (1,471 | ) | ||

| Income (loss) from operations | 66,256 | (26,327 | ) | |||

| Finance income | 644 | 1,126 | ||||

| Finance expense | (5,723 | ) | (3,995 | ) | ||

| Foreign exchange loss | (1,360 | ) | (196 | ) | ||

| Income (loss) before taxes | 59,817 | (29,392 | ) | |||

| Current income tax expense | (23,236 | ) | - | |||

| Deferred income tax recovery | 279 | - | ||||

| Net income (loss) and comprehensive income (loss) | 36,860 | (29,392 | ) | |||

| Weighted average number of shares outstanding: | ||||||

| Basic | 260,277,611 | 257,172,124 | ||||

| Diluted | 269,732,725 | 257,172,124 | ||||

| Net income (loss) per share attributable to common shareholders: | ||||||

| Basic | 0.13 | (0.10 | ) | |||

| Diluted | 0.12 | (0.10 | ) | |||

Revenue

During Q1 2026, the Company sold 34,181 ounces of gold at a quarterly record average gold price of $4,857/oz for revenue of $166.5 million (including $0.5 million of by-product silver revenue). During Q1 2025, the Company sold 26,994 ounces of gold at an average gold price of $2,833/oz for gross revenue of $76.6 million (including $0.1 million of by-product silver revenue). The average gold sales price, including the effect of realized gold hedging losses, for Q1 2026 amounted to $4,122/oz.

The increase in revenue quarter-on-quarter was due to a 71% increase in average gold sales prices and a 27% increase in gold ounces sold.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

Realized and Unrealized Losses on Gold Hedges

In Q4 2025, the Company changed its presentation of realized and unrealized gains (losses) on gold hedge derivative instruments from a component of finance expense to a component of net revenue. The Q1 2025 comparative period financial information has been restated to conform with the current period presentation.

During Q1 2026, the Company recorded a $25.1 million realized loss on settled hedges, of which $18.1 million was recognized in previous periods. The Company also recorded a $14.8 million unrealized loss during the quarter on its remaining hedged gold ounces. The unrealized loss was driven by an increase in gold prices during Q1 2026.

Refer to "Liquidity and Capital Resources" in this MD&A for details regarding the Company's remaining gold hedging program.

Production Costs

During Q1 2026, the Company incurred production costs of $45.3 million, compared to $42.2 million in Q1 2025. Production costs were higher than the comparative period due to more gold ounces sold in Q1 2026.

Depreciation and Depletion

During Q1 2026, depreciation and depletion expense was $12.4 million, compared to $14.4 million in Q1 2025. The decrease in depreciation and depletion expense resulted from a change in estimate of the AGM's total mineral reserve ore tonnes effective January 1, 2026, resulting in less depletion expense on mineral properties depreciated on a units-of-production basis.

Royalties

Until March 10, 2026, all of the AGM's concessions were subject to a 5% gross revenue royalty payable to the Government of Ghana. Effective March 10, 2026, the Government of Ghana passed into law a bill to amend the country's royalty framework such that gold royalties are subject to a sliding scale, starting at 5% and increasing to 12% when gold prices exceed $4,500/oz.

On March 13, 2026, the Government of Ghana passed into law an amendment to the GSL rate, reducing it from 3% to 1% of gold revenues. The GSL is presented as a royalty expense in the Statement of Operations.

The net effect of the aforementioned royalty amendments is an increase in total royalty rates from 8% to 13% at current spot gold prices.

Royalties expense was higher in Q1 2026 due to higher recorded revenues and the previously described amendments to royalty rates.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

General and Administrative ("G&A") Expenses

G&A expenses in Q1 2026 were $0.4 million higher than Q1 2025 primarily due to an increase in share-based compensation expense, resulting from an increase in the fair value of cash-settled long-term incentive plan awards linked to the price of the Company's common shares.

Finance Expense

The following table summarizes significant components of finance expense for the three months ended March 31, 2026 and 2025:

| Three months ended March 31, | ||||||

| 2026 | 2025 | |||||

| (in thousands of US dollars) | $ | $ | ||||

| Interest on lease liabilities | (1,257 | ) | (1,563 | ) | ||

| Accretion expense on asset retirement provisions | (798 | ) | (687 | ) | ||

| Accretion expense on deferred consideration | (420 | ) | (754 | ) | ||

| Change in fair value of contingent consideration | (1,669 | ) | (892 | ) | ||

| Fair value adjustment on marketable securities | (669 | ) | - | |||

| RCF standby fee | (315 | ) | - | |||

| Other | (595 | ) | (99 | ) | ||

| Total finance expense | (5,723 | ) | (3,995 | ) | ||

Finance expense was higher in Q1 2026 due to the change in fair value of the Nkran royalty resulting from higher forecast gold prices that impact the amount of estimated future royalty payments. Additionally, the Company recorded a $0.7 million unrealized mark-to-market loss on its marketable securities in Q1 2026.

Foreign Exchange Loss

The majority of the foreign exchange loss was unrealized and related to the quarter-end revaluation of value added tax ("VAT") receivables in Ghana that are denominated in Cedis. As noted previously, the value of the Cedi depreciated against the US dollar during the quarter, resulting in an unrealized revaluation loss on VAT receivables.

Current Income Tax Expense

During Q1 2026, the Company recorded current income tax ("CIT") expense of $23.2 million. The CIT expense relates entirely to taxable income generated in Ghana by the AGM, which is subject to a statutory tax rate of 35%. The increase in CIT expense quarter-on-quarter was due to higher gold prices and more gold ounces sold. Additionally, in Q1 2025, the Company's Ghanaian operating subsidiary had tax losses carried forward from prior years, which were utilized to offset taxes payable.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

FINANCIAL CONDITION

| March 31, | December 31, | ||

| 2026 | 2025 | ||

| (in thousands of US dollars) | $ | $ | |

| Cash and cash equivalents | 114,936 | 108,327 | Cash and cash equivalents increased resulting from positive operating cash flow and supported by record high gold prices, partly offset by capital expenditures and lease payments at the AGM. |

| Other current assets | 123,424 | 93,856 | Other current assets increased primarily due to a buildup of ore stockpiles and higher VAT receivables. Non-current assets increased due to capitalized stripping costs at the Abore, Esaase and Nkran deposits. |

| Non-current assets | 412,865 | 396,868 | |

| Total assets | 651,225 | 599,051 | |

| Current liabilities | 246,973 | 220,580 | Current liabilities increased due to gold hedge liabilities and higher income taxes paybale. Non-current liabilities decreased due to remaining gold hedge liabilities now being classified as current liabilities. |

| Non-current liabilities | 142,848 | 156,813 | |

| Total liabilities | 389,821 | 377,393 | |

| Common shareholders' equity | 254,433 | 218,856 | Shareholders ' equity increased as the Company reported net earnings for the three months ended March 31, 2026. |

| Non-controlling interest | 6,971 | 2,802 | |

| Total liabilities and equity | 651,225 | 599,051 |

LIQUIDITY AND CAPITAL RESOURCES

A key financial objective of the Company is actively managing its cash balance and liquidity to achieve positive operating cash flows that internally fund operating, capital and project development requirements, and generate shareholder returns. Material changes in the Company's liquidity and capital resources will be substantially determined by the success or failure of the Company's operations, exploration, and development programs, the ability to obtain equity or other sources of financing, and the price of gold.

On December 19, 2025, the Company entered into the $75.0 million revolving credit facility ("RCF") with Rand Merchant Bank ("RMB"). The purpose of the RCF is for general working capital requirements. The RCF has a 4-year term and floating interest rate based on the Secured Overnight Financing Rate (SOFR) plus a margin of 3.95% per annum, while the undrawn portion of the RCF is subject to a standby fee of 1.38% per annum. As of March 31, 2026, the Company had not drawn on the RCF and was in full compliance with all covenants.

The Company's cash and cash equivalents of $114.9 million as of March 31, 2026, together with available funds under the RCF and projected cash flows from operations over the next 12 months at current spot gold prices, are expected to be sufficient to satisfy the Company's financial, operating, capital commitments and contractual obligations requiring settlement within the next 12 months, including the $30.0 million deferred consideration payment due on December 31, 2026. However, the Company's cash flows and its ability to meet working capital requirements and contractual obligations is significantly influenced by the price of gold. Volatility in the gold price contributes to risk that cash flow from operations and other sources of liquidity will be insufficient to meet the Company's financial obligations as they become due and fund the Company's ongoing development and exploration projects. The Company aims to manage its liquidity by ensuring that it can manage spending and provide adequate cash flow to meet all commitments as they fall due.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

Working Capital

As at March 31, 2026, the Company had net working capital deficiency of $1.6 million (December 31, 2025 - $11.4 million). The increase in net working capital since December 31, 2025 was primarily due to an increase in the Company's cash and cash equivalents resulting from higher gold prices, a build-up of ore stockpiles, and higher VAT receivables. These factors were partly offset by an increase in income taxes payable.

| March 31, 2026 | December 31, 2025 | |||||

| (in thousands of US dollars) | $ | $ | ||||

| Cash and cash equivalents | 114,936 | 108,327 | ||||

| Accounts receivable | 189 | 71 | ||||

| Inventories | 86,740 | 70,802 | ||||

| Value added tax receivables | 23,769 | 10,808 | ||||

| Prepaid expenses and other | 12,726 | 12,175 | ||||

| Accounts payable and accrued liabilities | (90,435 | ) | (87,053 | ) | ||

| Income taxes payable | (19,909 | ) | (4,167 | ) | ||

| Financial liabilities | (85,061 | ) | (77,317 | ) | ||

| Lease liabilities - current | (15,911 | ) | (16,806 | ) | ||

| Deferred consideration | (28,662 | ) | (28,242 | ) | ||

| Total net working capital (deficiency) | (1,618 | ) | (11,402 | ) |

Cash Flows

The following table provides a summary of the Company's cash flows for the three months ended March 31, 2026 and 2025:

| Three months ended March 31, | ||||||

| 2026 | 2025 | |||||

| (in thousands of US dollars) | $ | $ | ||||

| Cash provided by (used in): | ||||||

| Operating activities | 46,689 | 25,892 | ||||

| Investing activities | (35,059 | ) | (21,613 | ) | ||

| Financing activities | (4,846 | ) | (3,366 | ) | ||

| Impact of foreign exchange on cash and cash equivalents | (175 | ) | (307 | ) | ||

| Increase in cash and cash equivalents during the period | 6,609 | 606 | ||||

| Cash and cash equivalents, beginning of period | 108,327 | 105,775 | ||||

| Cash and cash equivalents, end of period | 114,936 | 106,381 | ||||

Cash Flows from Operating Activities

The $20.8 million increase in operating cash flows during Q1 2026 was driven by higher revenues resulting from higher average gold sales prices and more gold ounces sold, relative to the comparative period of 2025.

Cash Flows used in Investing Activities

During Q1 2026, the Company invested $35.6 million in additions to mineral properties, plant and equipment ("MPP&E") (Q1 2025 - invested $22.1 million in additions to MPP&E). Total cash expenditures on MPP&E during the current quarter included $13.5 million of development pre-stripping costs at Nkran Cut 3, $10.7 million of sustaining waste stripping costs at the Abore and Esaase deposits, capitalized infill drilling at Abore and Esaase and costs related to a tailings facility expansion. The increase in capital expenditure during Q1 2026 was largely due to higher volumes mined at Nkran Cut 3.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

Cash Flows used in Financing Activities

Cash flows used in financing activities primarily related to capitalized lease payments on the Company's mining and other service contracts. The increase in cash flows used in financing activities in Q1 2026 was due to additional lease agreements entered into in the second half of 2025. The Company also received $1.3 million from the exercise of stock options in Q1 2026.

Commitments and Contractual Obligations

The following table summarizes the Company's commitments and contractual obligations as at March 31, 2026 and December 31, 2025.

| Less than | 1-3 | 4-5 | After | March 31, | December 31, | |||||||||||||

| (in thousands of US dollars) | 1 year | years | years | 5 years | 2026 | 2025 | ||||||||||||

| Accounts payable and accrued liabilities | 76,570 | - | - | - | 76,570 | 73,473 | ||||||||||||

| Gold hedges | 85,061 | - | - | - | 85,061 | 88,311 | ||||||||||||

| Long-term incentive plan (cash-settled awards) | 13,865 | - | - | - | 13,865 | 14,066 | ||||||||||||

| Mining and other services contracts | 21,678 | 22,270 | 14,220 | - | 58,168 | 63,901 | ||||||||||||

| Asset retirement provisions (undiscounted) | - | 2,178 | 1,453 | 79,216 | 82,847 | 81,553 | ||||||||||||

| Deferred and contingent consideration | 30,000 | 30,000 | 9,495 | 5,903 | 75,398 | 73,004 | ||||||||||||

| (undiscounted) | ||||||||||||||||||

| Corporate office lease | 114 | 236 | 174 | - | 524 | 561 | ||||||||||||

| Total commitments | 227,288 | 54,684 | 25,342 | 85,119 | 392,433 | 394,869 |

The gold hedges commitment represents the mark-to-market fair value of the Company's current gold hedging program (see "Gold Price Hedging" below) based upon a spot price of approximately $4,608/oz as of March 31, 2026. The settlement amount of these hedges will depend on the price of gold at the settlement date.

Long-term incentive plan commitments due within one year include all cash-settled deferred share unit ("DSU") awards granted to directors of the Company prior to 2025 amounting to $12.1 million. These commitments are current liabilities because the timing of payments could be accelerated if a director retires, or in the event of a change of control. DSU awards granted from the beginning of FY 2025 will be settled by the issuance of the Company's common shares.

The Company has a number of mining and other service contracts. These contracts include monthly fixed fees as well as variable cost measures. The contractual obligations disclosed in the above table relate only to the fixed fees payable to the contractors. The variable cost measures of these contracts are dependent volumes, such as bank cubic meters mined or ore tonnes transported. The expense relating to these variable payments and recognized as an operating expense was $37.5 million for the three months ended March 31, 2026 (three months ended March 31, 2025 - $25.2 million). The mining services contracts include termination clauses, which allow the Company to terminate the agreements provided a termination fee is paid to the contractor.

The timing of contingent payments, totaling $45.4 million, is management's best estimate of when payments would be required to be made based upon the AGM's current life of mine plan.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

Contingencies

In 2019, a former services provider of the AGM filed a dispute with an arbitration tribunal alleging the AGM breached the terms of a services agreement and claimed approximately $25.0 million in damages. The arbitrator ruled in favour of the AGM that there had not been a breach of any terms of the contract, yet made an award to the counterparty of approximately $13.0 million plus interest for services rendered. The Company, consistent with the arbitration ruling, maintains the view that there was no breach of contract, and all contractual amounts were paid as due. The Company has sought to appeal the arbitration ruling. On March 26, 2026, the Court of Appeal dismissed the case on a procedural matter and did not consider the substantive merits of the case, so the Company will continue to follow the mandated Ghanaian judicial process until the matter is settled.

A provision of $7.0 million has been recorded as at March 31, 2026 as management's best estimate to settle the claim (December 31, 2025 - $7.0 million). While the Company cannot reasonably predict the ultimate outcome of these actions, and inherent uncertainties exist in predicting such outcomes, the Company believes the estimated provision is reasonable based on the information currently available.

Due to the nature of its business, the Company may from time to time be subject to regulatory investigations, claims, lawsuits and other proceedings in the ordinary course of its business. While the Company cannot reasonably predict the ultimate outcome of any such actions, and inherent uncertainties exist in predicting such outcomes, the Company believes that the ultimate resolution of these actions is not reasonably likely to have a material adverse effect on the Company's financial condition or future results of operations.

Off-Balance Sheet Arrangements

The Company has no off‐balance sheet arrangements.

Gold Price Hedging

The Company periodically enters into gold hedging arrangements to mitigate gold price risk during periods of planned elevated capital investment. During the three months ended March 31, 2026, the Company realized a $25.1 million loss on its gold hedging derivatives (three months ended March 31, 2025 - realized loss of $4.9 million). The Company does not apply hedge accounting to the gold hedges.

The Company has gold hedges for 45,000 gold ounces of production in 2026 and 7,500 gold ounces in 2027. The gold hedges have a weighted average put strike of $2,300/oz and a weighted average call strike of $3,060/oz.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

SUMMARY OF QUARTERLY FINANCIAL RESULTS

The following table provides a summary of unaudited financial data for the last eight quarters. Except for basic and diluted income (loss) per share, the totals in the following table are presented in thousands of US dollars.

| Q1 2026 | Q4 2025 | Q3 2025 | Q2 2025 | Q1 2025 | Q4 2024 | Q3 2024 | Q2 2024 | |||||||||||||||||

| Gross revenue | 166,524 | 159,676 | 114,197 | 97,304 | 76,590 | 64,551 | 71,130 | 63,963 | ||||||||||||||||

| Income (loss) from mine operations | 72,453 | 51,139 | 9,977 | 24,653 | (19,756 | ) | 26,114 | 7,730 | 20,646 | |||||||||||||||

| Income (loss) from operations | 66,256 | 43,915 | 176 | 18,779 | (26,327 | ) | 7,401 | 4,190 | 12,092 | |||||||||||||||

| Net income (loss) for the period | 36,860 | 19,057 | (42,020 | ) | 21,554 | (29,392 | ) | 3,369 | 1,100 | 7,280 | ||||||||||||||

| Basic net income (loss) per share | $ | 0.13 | $ | 0.06 | $ | (0.15 | ) | $ | 0.07 | $ | (0.10 | ) | $ | 0.00 | $ | 0.00 | $ | 0.03 | ||||||

| Diluted net income (loss) per share | $ | 0.12 | $ | 0.06 | $ | (0.15 | ) | $ | 0.07 | $ | (0.10 | ) | $ | 0.00 | $ | 0.00 | $ | 0.03 | ||||||

| Adjusted net income (loss) attributable to common shareholders (1) | 29,515 | 39,959 | (2,770 | ) | 21,133 | 388 | 4,646 | 17,743 | 8,805 | |||||||||||||||

| Adjusted basic net income (loss) per share (1) | $ | 0.11 | $ | 0.15 | $ | (0.01 | ) | $ | 0.08 | $ | 0.00 | $ | 0.02 | $ | 0.07 | $ | 0.03 | |||||||

| Cash provided by operating activities | 46,689 | 55,839 | 40,449 | 35,814 | 25,892 | 13,806 | 24,449 | 4,463 | ||||||||||||||||

| EBITDA(1) | 77,308 | 67,635 | 50,412 | 49,851 | (12,098 | ) | 16,424 | 30,787 | 18,972 |

(1) Non-IFRS measure. Refer to section "Non-IFRS Measures" of this MD&A.

The decrease in income from mine operations in Q3 2024 was as a result of higher realized and unrealized losses on gold hedge derivatives.

The decrease in EBITDA1 in Q4 2024 was due to the Company terminating a gold sales offtake agreement and paying a $13.1 million termination fee.

The net loss in Q1 2025 was primarily attributable to a $30.2 million unrealized loss and a $4.9 million realized loss on gold hedge derivatives.

The net loss in Q3 2025 was due to a $25.1 million unrealized loss and a $13.1 million realized loss on gold hedge derivatives. The Company also recorded CIT and deferred income tax expenses of $21.8 million and $14.7 million, respectively.

From Q2 2025 to Q1 2026, improved mining and production rates at the AGM, coupled with higher average gold sales prices, led to strong revenue, income from operations, net earnings and operating cash flow.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

NON-IFRS MEASURES

The Company has included certain non-IFRS performance measures throughout this MD&A. These performance measures are employed by management to assess the Company's operating and financial performance and to assist in business decision-making. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, certain investors and other stakeholders use this information to evaluate the Company's operating and financial performance; however, as explained elsewhere herein, these non-IFRS performance measures do not have any standardized meaning and therefore may not be comparable to similar measures presented by other issuers. Accordingly, these performance measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS.

Total Cash Costs per Gold Ounce Sold

The Company has included the non-IFRS performance measure of total cash costs per gold ounce sold throughout this MD&A. The Company follows the recommendations of the Gold Institute Production Cost Standard (the "Gold Institute"). The Gold Institute, which ceased operations in 2002, was a non-regulatory body and represented a global group of suppliers of gold and gold products. The production cost standard developed by the Gold Institute remains the generally accepted standard of reporting cash costs of production by many gold mining companies. Total cash costs are calculated by taking production costs related to gold production, removing costs allocated to by-products and then adding royalties. Management uses total cash costs per gold ounce sold to monitor the operating performance of the AGM. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, some investors use this information to evaluate the Company's performance and ability to generate cash flow.

The following table provides a reconciliation of the AGM's total cash costs per gold ounce sold to production costs of the Company (the nearest IFRS measure) as presented in the unaudited condensed consolidated interim financial statements of the Company for the three months ended March 31, 2026 and 2025.

| Three months ended March 31, | ||||||

| 2026 | 2025 | |||||

| (in thousands of US dollars, except per ounce amounts) | $ | $ | ||||

| Production costs | 45,250 | 42,242 | ||||

| Costs allocated to by-products | (491 | ) | (127 | ) | ||

| Royalties | 14,545 | 4,595 | ||||

| Total cash costs | 59,304 | 46,710 | ||||

| Gold ounces sold | 34,181 | 26,994 | ||||

| Total cash costs per gold ounce sold ($/oz) | 1,735 | 1,730 | ||||

AISC per Gold Ounce Sold

The Company has adopted the reporting of "AISC per gold ounce sold", which is a non-IFRS performance measure. The Company believes that the AISC per gold ounce measure provides additional insight into the costs of producing gold by capturing all of the expenditures required for the discovery, development and sustaining of gold production and allows the Company to assess its ability to support capital expenditures to sustain future production from the generation of operating cash flows. The Company believes that, in addition to conventional measures prepared in accordance with IFRS, some investors use this information to evaluate the AGM's performance and ability to generate cash flow.

AISC adjusts total cash costs for mine site G&A expenses, reclamation cost accretion, sustaining capitalized stripping costs, sustaining capital expenditures and sustaining lease payments on the AGM's mining and service lease agreements. Sustaining capital expenditures, capitalized stripping costs, reclamation cost accretion and lease payments are not line items on the Company's financial statements. Sustaining capital expenditures are defined as those capital expenditures which do not materially benefit annual or life of mine gold ounce production at a mine site. A material benefit to a mine site is considered to be at least a 10% increase in annual or life of mine production, net present value, or mineral reserves compared to the remaining life of mine of the operation. As such, sustaining costs exclude all expenditures at the AGM's new projects and certain expenditures at the AGM's operating sites which are deemed expansionary in nature. Capitalized stripping costs represent costs incurred at steady-state operations during the period; these costs are generally not considered expansionary in nature as the stripping phase is expected to take less than 12 months and resulting ore production is of a short-term duration. Reclamation cost accretion represents the growth in the AGM's reclamation provision due to the passage of time. This amount does not reflect cash outflows, but it is considered to be representative of the periodic costs of reclamation and remediation. Lease payments on mining and service lease agreements represent cash outflows. Reclamation cost accretion is presented in finance expense in the Company's financial results.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

The following table provides a reconciliation of AISC for the AGM to production costs and various operating expenses of the Company (the nearest IFRS measures) as presented in the unaudited condensed consolidated interim financial statements of the Company for the three months ended March 31, 2026 and 2025.

| Three months ended March 31, | ||||||

| 2026 | 2025 | |||||

| (in thousands of US dollars, except per ounce amounts) | $ | $ | ||||

| Total cash costs (as reconciled above) | 59,304 | 46,710 | ||||

| G&A expenses of the AGM (see table below) | 846 | 715 | ||||

| Sustaining capital expenditures and capitalized stripping costs (see table below) |

14,413 | 14,249 | ||||

| Reclamation accretion expense | 798 | 687 | ||||

| Sustaining lease payments(1) | 5,338 | 5,144 | ||||

| All-in sustaining costs | 80,699 | 67,505 | ||||

| Gold ounces sold | 34,181 | 26,994 | ||||

| All-in sustaining costs per gold ounce sold ($/oz) | 2,361 | 2,501 | ||||

(1) Sustaining lease payments for the three months ended March 31, 2026 were $5,989 per the Company's consolidated interim financial statements, which included $29 of lease payments for corporate office space and $622 of non-sustaining lease payments on a mining services contract.

The following table reconciles G&A expenses of the AGM to the Company's G&A expenses (the nearest IFRS measure) as presented in the Statements of Operations of the Company's unaudited condensed consolidated interim financial statements for the three months ended March 31, 2026 and 2025.

| Three months ended March 31, | ||||||

| 2026 | 2025 | |||||

| (in thousands of US dollars) | $ | $ | ||||

| Consolidated G&A expenses | 5,475 | 5,100 | ||||

| Less: | ||||||

| Corporate G&A expenses | (4,629 | ) | (4,385 | ) | ||

| G&A expenses of the AGM | 846 | 715 | ||||

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

The following table reconciles sustaining capital expenditures and sustaining capitalized stripping costs to the Company's total MPP&E additions (the nearest IFRS measure) as presented in note 7 of the Company's unaudited condensed consolidated interim financial statements for the three months ended March 31, 2026 and 2025.

| Three months ended March 31, | ||||||

| 2026 | 2025 | |||||

| (in thousands of US dollars) | $ | $ | ||||

| Additions to MPP&E (note 7 of financial statements) | 31,267 | 32,242 | ||||

| Add (less): | ||||||

| Non-sustaining capital expenditures | (21,191 | ) | (7,848 | ) | ||

| Capital expenditures - corporate | (5 | ) | (6 | ) | ||

| Non-cash additions related to leases | - | (11,157 | ) | |||

| Change in accounts payable related to capitalized stripping costs | 4,342 | 1,018 | ||||

| Sustaining capital expenditures | 14,413 | 14,249 | ||||

EBITDA and Adjusted EBITDA

Earnings before interest, taxes, depreciation, and amortization ("EBITDA") is a non-IFRS measure and provides an indication of the Company's continuing capacity to generate income from operations before considering the Company's financing decisions and costs of amortizing capital assets. Accordingly, EBITDA comprises net income (loss) excluding finance expense, finance income, depreciation and depletion expense and income taxes. Adjusted EBITDA, also a non-IFRS measure, adjusts EBITDA to exclude non-recurring items and non-cash items ("Adjusted EBITDA").

The following table provides a reconciliation of the Company's EBITDA and Adjusted EBITDA to net income (loss) of the Company (the nearest IFRS measure) as presented in the Company's unaudited condensed consolidated interim financial statements for the three months ended March 31, 2026 and 2025.

| Three months ended March 31, | ||||||

| 2026 | 2025 | |||||

| (in thousands of US dollars ) | $ | $ | ||||

| Net income (loss) | 36,860 | (29,392 | ) | |||

| Add back (deduct): | ||||||

| Depreciation and depletion expense | 12,412 | 14,425 | ||||

| Finance income | (644 | ) | (1,126 | ) | ||

| Finance expense | 5,723 | 3,995 | ||||

| Current income tax expense | 23,236 | - | ||||

| Deferred income tax recovery | (279 | ) | - | |||

| EBITDA | 77,308 | (12,098 | ) | |||

| Add back (deduct): | ||||||

| Unrealized loss on gold hedge derivatives | 14,833 | 31,321 | ||||

| Non-cash long-term incentive plan compensation | 1,284 | 907 | ||||

| Adjusted EBITDA | 93,425 | 20,130 | ||||

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

Adjusted Net Income (Loss)

The Company has included the non-IFRS performance measures of adjusted net income (loss) and adjusted net income (loss) per share throughout this MD&A. Neither adjusted net income (loss) nor adjusted net income (loss) per share have any standardized meaning and are therefore unlikely to be comparable to other measures presented by other issuers. Adjusted net income (loss) excludes certain non-cash items, and items of income or expense not expected to recur in the future, from net income (loss) to provide a measure which helps the Company and investors to evaluate the results of the underlying core operations of the Company and its ability to generate cash flows. The Company believes that the presentation of adjusted net income (loss) is appropriate to provide additional information to investors regarding items that management does not expect to continue at the same level in the future or that management does not believe to reflect the Company's ongoing operating performance or operating performance of the current period. The Company further believes that its presentation of this non-IFRS financial measure provides information that is useful to investors because it is an important indicator of the strength of operations and the performance of the Company's core business.

The following table provides a reconciliation of adjusted net income (loss) to net income (loss) of the Company (the nearest IFRS measure) as presented in the unaudited condensed consolidated interim financial statements of the Company for the three months ended March 31, 2026 and 2025.

| Three months ended March 31, | ||||||

| 2026 | 2025 | |||||

| (in thousands of US dollars, except per share amounts) | $ | $ | ||||

| Net income (loss) attributable to common shareholders | 32,691 | (26,806 | ) | |||

| Settlement of gold hedges with losses recognized in prior periods (1) | (16,275 | ) | (995 | ) | ||

| Unrealized loss on gold hedge derivatives (1) | 13,350 | 28,189 | ||||

| Deferred income tax recovery(1) | (251 | ) | - | |||

| Adjusted net income | 29,515 | 388 | ||||

| Basic weighted average common shares outstanding | 260,277,611 | 257,172,124 | ||||

| Diluted weighted average common shares outstanding | 269,732,725 | 257,172,124 | ||||

| Adjusted net income per share - basic | $ | 0.11 | $ | 0.00 | ||

| Adjusted net income per share - diluted | $ | 0.11 | $ | 0.00 | ||

(1) Reflects the Company's 90% interest in the AGM.

OUTSTANDING SHARE DATA

As of the date of this MD&A, there were 261,213,764 common shares of the Company issued and outstanding and 9,758,509 stock options outstanding (each exercisable to purchase one common share at exercise prices ranging between C$0.62 and C$4.16 per share). Additionally, there were 2,777,645 long-term incentive plan ("LTIP") awards, comprising restricted share units, performance share units and DSUs, that will be settled in equity. The maximum number of common shares issuable upon conversion of these LTIP awards is 3,366,145 common shares. The fully diluted outstanding share count at the date of this MD&A is 274,338,418.

RELATED PARTY TRANSACTIONS

As at March 31, 2026, the Company's related parties are its subsidiaries and key management personnel, defined as directors and executive officers of the Company. During the normal course of operations, the Company enters into transactions with its related parties. During the three months ended March 31, 2026, all related party transactions were in the normal course of business, including compensation payments to key management personnel.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

Estimates and Judgements

The preparation of financial statements in conformity with IFRS requires management to make estimates and assumptions that affect amounts reported in the financial statements and accompanying notes. Management believes the estimates and assumptions used in preparing the unaudited condensed consolidated interim financial statements for the three months ended March 31, 2026 and 2025 are reasonable; however, actual results could differ from those estimates and assumptions and could impact future results of operations and cash flows. The Company's significant accounting judgements and estimates are presented in note 5 of the audited consolidated annual financial statements for the years ended December 31, 2025 and 2024.

Changes in Accounting Policies including Initial Adoption

Accounting standards adopted during the period

IFRS 7 and 9

In May 2024, the IASB issued amendments to the classification and measurement of financial instruments (IFRS 7 and IFRS 9), which included clarification that a financial liability is derecognized on the 'settlement date'; an accounting policy option to derecognize financial liabilities that are settled through an electronic payment system before settlement date if certain conditions are met; clarification on how to assess the contractual cash flow characteristics of financial assets that include environmental, social and governance‐linked features; and requires additional disclosures under IFRS 7 for financial assets and liabilities with contractual terms that reference a contingent event. The amendments to IFRS 7 and IFRS 9 are effective for annual reporting periods beginning on or after January 1, 2026. The amendments to IFRS 7 and IFRS 9 had no material impact on the Company's consolidated financial statements.

Accounting standards and amendments issued but not yet adopted

The following standards and interpretations, which may be applicable to the Company, have been issued but are not yet effective as of March 31, 2026:

IFRS 18

On April 9, 2024, the IASB issued IFRS 18, Presentation and Disclosure in Financial Statements, a new standard on presentation and disclosure in financial statements with a focus on updates to the statement of profit or loss. The key new concepts introduced in IFRS 18 relate to: the structure of the statement of profit or loss; required disclosures in the financial statements for certain profit or loss performance measures that are reported outside an entity's financial statements; and enhanced principles on aggregation and disaggregation which apply to the primary financial statements and notes in general. IFRS 18 will not impact the recognition or measurement of items in the financial statements, but may change what an entity reports as its 'operating profit or loss'. IFRS 18 will apply for reporting periods beginning on or after January 1, 2027 and also applies to comparative information. The Company is currently evaluating how the detailed implications of applying IFRS 18 will impact the disclosures in its consolidated financial statements in future periods. Preliminarily, the Company has identified the following potential impacts, which are not exhaustive, of applying IFRS 18 on its consolidated financial statements:

– Items of income or expense may be grouped differently resulting in new subtotals or line items in the Statement of Operations and Comprehensive Income (Loss).

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

– There will be new disclosures for management-defined performance measures (“MPM”). An MPM has been defined as a subtotal of income and expenses that is used in communications outside of the financial statements to highlight a particular aspect of overall financial performance. Based on an initial review of the Company’s communications outside of the financial statements, the following financial performance measures, which are not exhaustive, may meet the definition of an MPM: adjusted net income (loss); EBITDA; and Adjusted EBITDA.

RISKS AND UNCERTAINTIES

Financial Instruments and Risk

The Company's business, operations and future prospects are subject to significant risks. For details of these risks, refer to the risk factors set forth in the Company's most recently filed AIF for the year ended December 31, 2025, which can be found under the Company's SEDAR+ profile at www.sedarplus.ca, and the Company's most recently filed Form 40-F Annual Report for the year ended December 31, 2025, which can be found on EDGAR at www.sec.gov.

Additional risks and uncertainties not presently known to the Company or that the Company currently considers immaterial may also impair the business, operations, prospects and price of the Company's common shares. If any of the risks actually occur, the business of the Company may be harmed, and its financial condition and results of operations may suffer significantly.

Financial Instruments

As at March 31, 2026, the Company's financial instruments consist of cash and cash equivalents, accounts receivable, marketable securities, accounts payable and accrued liabilities, lease liabilities, financial liabilities (gold hedge derivatives), long-term incentive plan liabilities, deferred and contingent consideration payable and the 1% net smelter return royalty on production from the Nkran deposit (the "Nkran Royalty") payable. The Company classifies cash and cash equivalents and accounts receivables as financial assets measured at amortized cost, while accounts payable and accrued liabilities, lease liabilities and deferred consideration are classified as other financial liabilities and measured at amortized cost. Marketable securities, long-term incentive plan liabilities, contingent consideration and the Nkran Royalty are financial assets and financial liabilities, respectively, measured at fair value through profit or loss. Marketable securities fall within Level 1 of the fair value hierarchy, while the aforementioned financial liabilities all fall within Level 3. The gold hedge derivative liabilities are also recorded at fair value at the reporting date and fall within Level 1 of the fair value hierarchy. Refer to note 11 of the Company's unaudited condensed consolidated interim financial statements for the three months ended March 31, 2026 and 2025 for discussion on the significant assumptions made in determining the fair value of the contingent consideration and Nkran Royalty.

The credit risk, liquidity risk and market risk associated with the Company's financial instruments are disclosed in note 25(d) of the Company's unaudited condensed consolidated interim financial statements for the three months ended March 31, 2026 and 2025.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

As at March 31, 2026, the carrying and fair values of the Company's financial instruments by category are as follows (in thousands of US dollars):

| Fair value through | ||||||||||||

| profit or loss | Amortized cost | Carrying value | Fair value | |||||||||

| As at March 31, 2026 | $ | $ | $ | $ | ||||||||

| Financial assets: | ||||||||||||

| Cash and cash equivalents | - | 114,936 | 114,936 | 114,936 | ||||||||

| Accounts receivable | - | 189 | 189 | 189 | ||||||||

| Marketable securities (1) | 3,889 | - | 3,889 | 3,889 | ||||||||

| Total financial assets | 3,889 | 115,125 | 119,014 | 119,014 | ||||||||

| Financial liabilities: | ||||||||||||

| Accounts payable and accrued liabilities (2) | 13,865 | 76,570 | 90,435 | 90,435 | ||||||||

| Financial liabilities (2) | 85,061 | - | 85,061 | 85,061 | ||||||||

| Lease liabilities | - | 32,343 | 32,343 | 32,343 | ||||||||

| Deferred consideration | - | 28,662 | 28,662 | 28,662 | ||||||||

| Contingent consideration | 19,985 | - | 19,985 | 19,985 | ||||||||

| Nkran royalty | 7,992 | - | 7,992 | 7,992 | ||||||||

| Total financial liabilities | 126,903 | 137,575 | 264,478 | 264,478 |

(1) Marketable securities are presented within prepaid expenses and other in the Statement of Financial Position.

(2) Accounts payable and accrued liabilities and financial liabilities include long-term incentive plan and gold hedge instrument liabilities, which are measured at fair value through profit or loss.

INTERNAL CONTROL

Internal Control over Financial Reporting ("ICFR")

Management, including the Chief Executive Officer ("CEO") and Chief Financial Officer ("CFO"), have evaluated the Company's ICFR to determine whether any changes occurred during the period that have materially affected, or are reasonably likely to materially affect, the Company's ICFR.

During the three months ended March 31, 2026, there have been no changes in ICFR that have materially affected, or are reasonably likely to materially affect, the Company's ICFR.

Limitations of Controls and Procedures

The Company's management, including the CEO and CFO, believes that any disclosure controls and procedures or ICFR, no matter how well conceived and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Because of the inherent limitations in all control systems, they cannot provide absolute assurance that all control issues and instances of fraud, if any, within the Company have been prevented or detected. These inherent limitations include the realities that judgements in decision-making can be faulty, and that breakdowns can occur because of simple error or mistake. Additionally, controls can be circumvented by the individual acts of some persons, by collusion of two or more people, or by unauthorized override of the control. The design of any control system also is based in part upon certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions. Accordingly, because of the inherent limitations in a cost-effective control system, misstatements due to error or fraud may occur and not be detected.

| GALIANO GOLD INC. Management's Discussion and Analysis For the three months ended March 31, 2026 and 2025 |

QUALIFIED PERSONS

The exploration information contained in this MD&A has been reviewed and approved by Mr. Chris Pettman, P.Geo, Vice President Exploration of Galiano. For further information regarding the exploration information in this MD&A, including the Quality Control and Quality Assurance and data verification measures taken with respect to such exploration information, refer to the Company's news releases dated January 29, 2026, February 12, 2026 and May 11, 2026, which are filed on the Company’s SEDAR+ profile at www.sedarplus.ca.

All other scientific and technical information contained in this MD&A has been reviewed and approved by Mr. Amri Sinuhaji, P.Eng., Vice President Technical Services of Galiano. Mr. Pettman and Mr. Sinuhaji are "Qualified Persons" as defined by National Instrument 43-101, Standards of Disclosure for Mineral Projects ("NI 43-101").

CAUTIONARY STATEMENTS

Cautionary Statement on Forward-Looking Information

The Company cautions readers regarding forward-looking statements found in this MD&A and in any other statement made by, or on behalf of the Company. Generally, forward-looking information can be identified by the use of forward-looking terminology such as "plans", "expects", "estimates", "anticipates", or variations of such words and phrases or statements that certain actions, events or results "may", "could", or "might" occur. Forward-looking statements are made based on management's beliefs, estimates and opinions and are given only as of the date of this MD&A. Such statements may constitute "forward-looking information" within the meaning of the United States Private Securities Litigation Reform Act of 1995 and applicable Canadian securities legislation.