Exhibit 99.2 Q1 2026 Financial Results 13 May 2026 Q1 2026 Results | 13 May 2026 1

Disclaimer No Offer to Sell or Solicit environment and competitive dynamics and are subject to a wide variety of significant operating trends, (b) perform analytical comparisons and benchmarking between segments and (c) identify strategies to improve operating performance. Sunrise believes risks and uncertainties, some of which are beyond the control of Sunrise, that could cause Adjusted EBITDA and Adjusted EBITDAaL are useful to investors because they provide a This presentation is not an offer to sell or a solicitation of offers to purchase or subscribe actual results to differ materially from those expressed or implied by these statements. basis for comparing Sunrise performance with the performance of other companies in the for any securities of Sunrise Communications AG (Sunrise) in any jurisdiction. This Such risks and uncertainties include, among others, Sunrise’s ability to successfully same or similar industries. document is not a prospectus within the meaning of the Swiss Financial Services Act, the execute on its plans and strategies, Sunrise’s ability to realize the expected benefits from Adjusted EBITDAaL less P&E Additions: Adjusted EBITDAaL less P&E Additions is defined Prospectus Regulation (EU) 2017/1129 or the UK version of Regulation (EU) 2017/1129 as the series of transactions that closed on 8 November 2024 that resulted in the spin-off of as Adjusted EBITDAaL less property and equipment additions on an accrual basis it forms part of domestic law by virtue of the European Union (Withdrawal) Act 2018 (as Liberty Global Ltd.'s Swiss telecommunications operations to Sunrise (the Transaction), (excluding those P&E additions under finance lease). Adjusted EBITDAaL less P&E amended) or under any other applicable laws. This document may constitute advertising Additions is a meaningful measure because it provides (i) a transparent view of Adjusted unanticipated difficulties or costs in connection with the Transaction, Sunrise’s ability to in accordance with article 68 of the Swiss Financial Services Act. Such advertisements are EBITDAaL that remains after capital spend, which Sunrise believes is important to take successfully operate as an independent public company and maintain its relationships with communications to investors aiming to draw their attention to financial instruments. Any into account when evaluating overall performance and (ii) a comparable view of Sunrise material counterparties after the Transaction, and other factors, including those detailed performance relative to other telecommunications companies. investment decisions with respect to any securities should not be made based on such from time to time in Sunrise’s filings with the U.S. Securities and Exchange Commission Adjusted Free Cash Flow: Adjusted FCF is defined as net cash provided by operating advertisement. (the SEC), including Sunrise’s most recently filed Form 20-F and in subsequent reports activities, plus (a) operating-related vendor financed additions (which represents an filed with the SEC. These forward-looking statements speak only as of the date hereof. increase in the period to actual cash available as a result of extending vendor payment Forward-Looking Statements Although Sunrise believes that its expectations reflected in any such forward-looking terms beyond normal payment terms, which are typically 90 days or less, through non- cash financing activities), and (b) cash receipts in the period from interest-related statement are based upon reasonable assumptions, no assurance can be given that these This presentation contains forward-looking statements within the meaning of the Private derivatives, less (i) cash payments in the period for interest, (ii) cash payments in the expectations will be achieved. Sunrise expressly disclaims any obligation or undertaking to Securities Litigation Reform Act of 1995, including statements regarding certain forecasted period for capital expenditures, (iii) principal payments on amounts financed by vendors disseminate any updates or revisions to any forward-looking statement contained herein financial information, including Sunrise’s 2026 Guidance and dividend growth and intermediaries (which represents a decrease in the period to actual cash available as a to reflect any change in their expectations with regard thereto or any change in events, expectations, its financial condition, results of operations, business, market share, result of paying amounts to vendors and intermediaries where Sunrise previously had conditions or circumstances on which any such statement is based. You are cautioned not extended vendor payments beyond the normal payment terms), and (iv) principal network, subscription Revenue, Sunrise’s expected Adjusted Free Cash Flow generation, to place undue reliance on any forward-looking statement. payments on lease liabilities (which represents a decrease in the period to actual cash including the timing and expected use thereof, expectations with respect to customer available). Sunrise believes its presentation of Adjusted FCF provides useful information to trading volumes, Sunrise’s growth and other strategies, future growth prospects and Non-IFRS Financial Measures investors because this measure can be used to gauge its ability to (i) service debt and (ii) anticipated methods of achieving growth, including its B2B strategies, expectations, plans fund new investment opportunities after consideration of all actual cash payments related and opportunities of Sunrise, including its new product and service offerings, pricing to its working capital activities and expenses that are capital in nature, whether paid This presentation includes financial measures not presented in accordance with actions and anticipated impacts thereof, market and competitive dynamics, capital inside normal vendor payment terms or paid later outside normal vendor payment terms International Financial Reporting Standards (IFRS), including Adjusted EBITDA, Adjusted expenditure levels and phasing, cost optimization initiatives, artificial intelligence-related (in which case payment is typically made in less than 365 days). Adjusted FCF should not EBITDAaL, Adjusted EBITDAaL less P&E Additions, and Adjusted FCF. be understood to represent Sunrise’s ability to fund discretionary amounts, as they have products, services and partnerships, which remain subject to technological development various mandatory and contractual obligations, including debt repayments, that are not and customer adoption, as well as the expected timing and benefits to be derived Adjusted EBITDA: Adjusted EBITDA is defined as net income (loss) before income tax deducted to arrive at these amounts. therefrom, expectations with respect to net adds, including the reasons for such benefit (expense), share of losses (gains) of affiliates, financial income, financial expectations, ongoing operational efficiencies, expectations with respect to Sunrise’s expenses, depreciation and amortisation, share-based compensation expense, and These non-IFRS financial measures should be viewed as supplements to, and not charges, the macroeconomic environment, Sunrise’s future dividends and growth thereof, impairment, restructuring and other operating items. Other operating items include (a) substitutes for, IFRS measures of performance or liquidity as presented in Sunrise’s IFRS the impact of the Sunrise rewards programme on customer relationships, Sunrise’s provisions and provision releases related to significant litigation, (b) certain related-party financial statements. These non-IFRS financial measures have no standardized meaning under IFRS and may not be comparable to similarly titled measures reported by other intention to terminate its U.S. Securities and Exchange Act reporting obligations, including charges and (c) gains and losses on the disposition of long-lived assets. companies. They should not be considered in isolation or as an alternative for or superior the timing thereof, the amount, cost and tenor of Sunrise’s third-party debt, including to IFRS measures. These measures are presented and described in order to provide anticipated future repayments of debt and other information and statements that are not Adjusted EBITDAaL: Adjusted EBITDAaL is defined as Adjusted EBITDA after lease-related additional means of understanding Sunrise’s results in the same manner as its expenses. historical fact. These forward-looking statements are based on current expectations, management team. Sunrise believes Adjusted EBITDA and Adjusted EBITDAaL are meaningful measures estimates and projections about the factors that may affect Sunrise’s future performance, because they represent a transparent view of Sunrise’s recurring operating performance including assumptions regarding market conditions, customer behaviour, regulatory that is unaffected by its capital structure and allows management to (a) readily view Q1 2026 Results | 13 May 2026 2 Not for release, publication or distribution, in whole or in part, directly or indirectly, in any jurisdiction in which the release, publication or distribution would be unlawful.

Summary Q1 2026 results Key commercial roadmap deliverables executed, reinforcing momentum • Connect complete check 2026: “Best Overall Package” in Switzerland • Sunrise Rewards Programme launched to increase loyalty and accelerate cross- and upselling • Exclusive strategic partnership with PHOENIQS to offer unique sovereign Swiss AI solutions • Market liquidity seasonally lower in Q1, driving internet (1k) and postpaid +10k, visible sales acceleration from March • Price increase announced (effective from 1 August 2026) in a market that continues to be promotional within stable price bands 1 Q1 revenue in line; strong Adj. EBITDAaL growth and FY guidance reiterated • Revenue +0.1% YoY, with ongoing underlying fixed subscription revenue trends offset by stronger handset & other sales. Q1 Adj. EBITDAaL +2.5% YoY, driven by continued cost optimisation and YoY phasing • Capex spend frontloaded yet driving Adj. EBITDAaL less P&E Additions increase of +15.9% YoY • Successful implementation of new organisational set-up in Q1, with financial contributions starting from Q2 1 • FY 2026 Guidance reconfirmed, including expected DPS of CHF 3.49 with a +>2% growth YoY 2 Dividend approved and paid following AGM • FY 2025 dividend approved: CHF 3.42 per Class A Share / CHF 0.34 per Class B Share 2 • Not subject to Swiss withholding tax • Dividend payment date 13 May 2026 3 1 Per Class A Share. To be proposed by the Sunrise Board of Directors upon achieving the FY 2026 financial Guidance and subject to the approval by the Annual General Meeting of Sunrise Q1 2026 Results | 13 May 2026 3 2 Dividends for the FY 2025 have been exclusively paid out of reserves from foreign capital contributions and hence treated as a repayment of qualifying additional paid-in capital for Swiss tax purposes. Accordingly, the dividend for the 2025 financial year is not be subject to Swiss Withholding Tax of 35%. The disclosed reserves (after FY 2025 dividend payout) from foreign capital contributions amount to CHF 2.32 bn.

Commercial Performance Q1 2026 Results | 13 May 2026

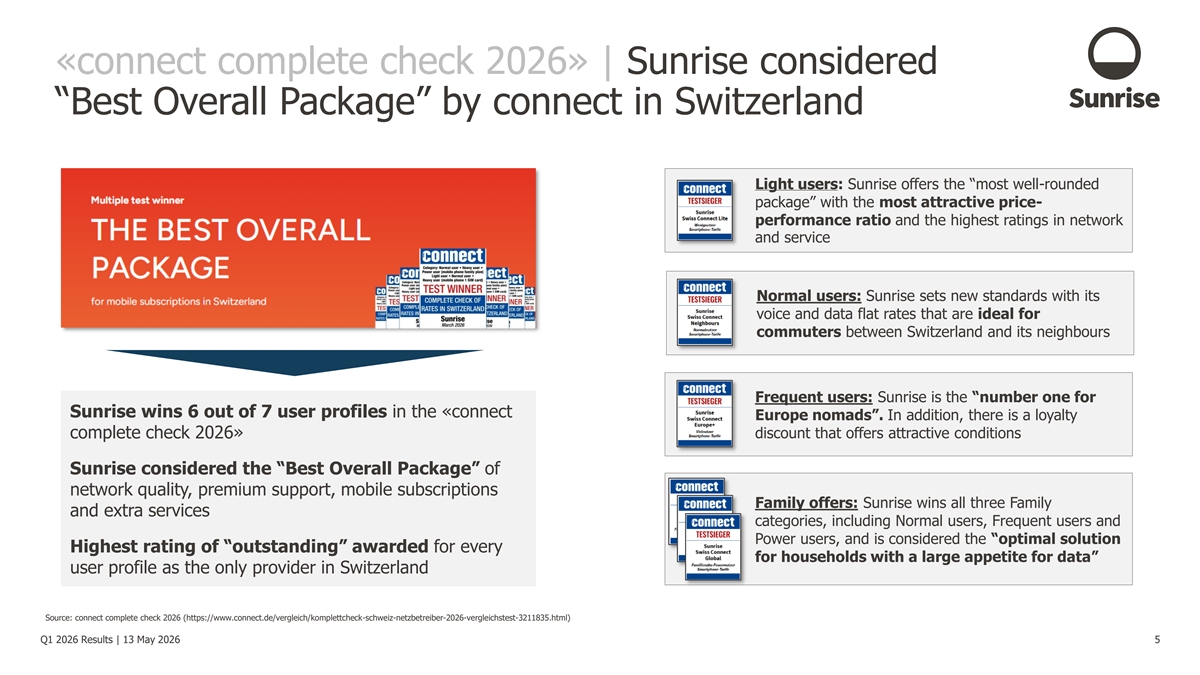

«connect complete check 2026» | Sunrise considered “Best Overall Package” by connect in Switzerland Light users: Sunrise offers the “most well-rounded package” with the most attractive price- performance ratio and the highest ratings in network and service Normal users: Sunrise sets new standards with its voice and data flat rates that are ideal for commuters between Switzerland and its neighbours Frequent users: Sunrise is the “number one for Sunrise wins 6 out of 7 user profiles in the «connect Europe nomads”. In addition, there is a loyalty complete check 2026» discount that offers attractive conditions Sunrise considered the “Best Overall Package” of network quality, premium support, mobile subscriptions Family offers: Sunrise wins all three Family and extra services categories, including Normal users, Frequent users and Power users, and is considered the “optimal solution Highest rating of “outstanding” awarded for every for households with a large appetite for data” user profile as the only provider in Switzerland Source: connect complete check 2026 (https://www.connect.de/vergleich/komplettcheck-schweiz-netzbetreiber-2026-vergleichstest-3211835.html) Q1 2026 Results | 13 May 2026 5

Loyalty Programme | Innovative Sunrise Rewards Programme launched as part of customer-centric consumer strategy Sunrise Rewards Programme • Innovative loyalty programme with attractive benefits including Sunrise services and exclusive access to special offers and experiences • Loyalty programme designed as a structural, long-term lever to deepen customer relationships and support the growth and value of our base, in turn improving churn and driving cross- and upselling in the base • Sunrise Rewards creates a new currency for customers to purchase incremental Sunrise products, while strong deals from the Sunrise portfolio, including Swiss Ski, Knie, FC Basel and Pathé, ensure top-quality rewards and experiences • Successful soft-launch in March 2026, broad campaign launch and full roll- out into the Sunrise base in May 2026 (reward examples) (supporting partners) (campaign launch) Q1 2026 Results | 13 May 2026 6

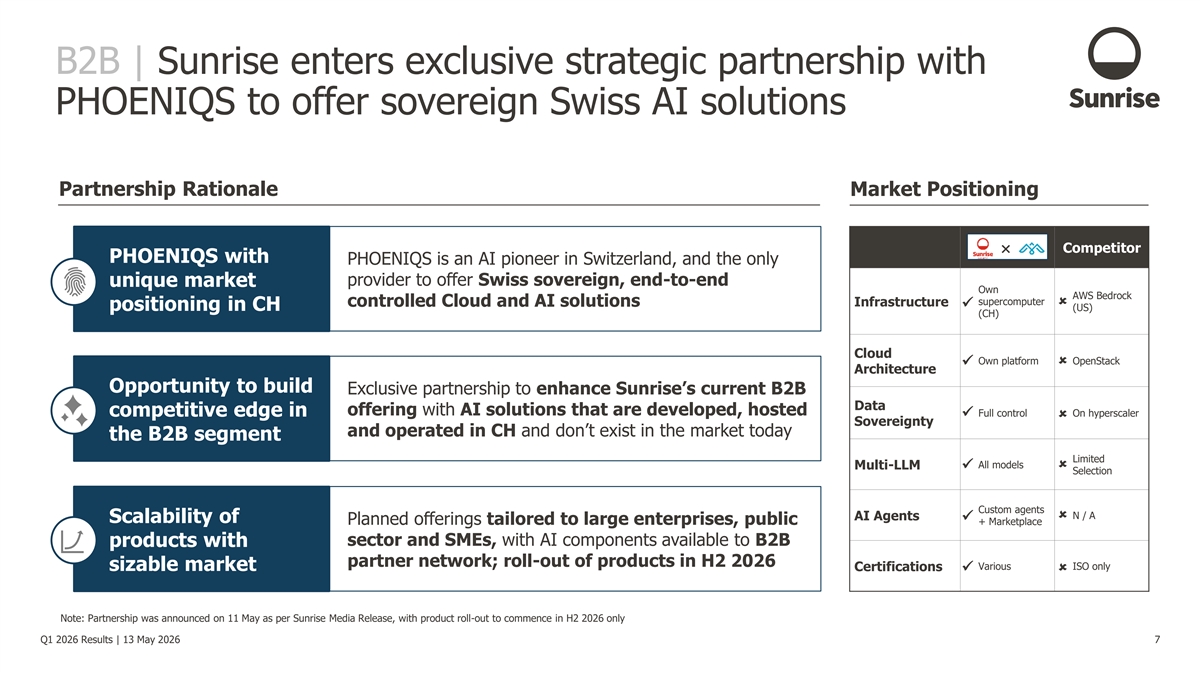

B2B | Sunrise enters exclusive strategic partnership with PHOENIQS to offer sovereign Swiss AI solutions Partnership Rationale Market Positioning Competitor PHOENIQS with PHOENIQS is an AI pioneer in Switzerland, and the only provider to offer Swiss sovereign, end-to-end unique market Own AWS Bedrock supercomputer Infrastructureû controlled Cloud and AI solutions ✓ positioning in CH (US) (CH) Cloud Own platform OpenStack ✓û Architecture Opportunity to build Exclusive partnership to enhance Sunrise’s current B2B Data competitive edge in offering with AI solutions that are developed, hosted ✓ Full control On hyperscaler û Sovereignty and operated in CH and don’t exist in the market today the B2B segment Limited All models Multi-LLM✓û Selection Custom agents N / A AI Agentsû ✓ Scalability of Planned offerings tailored to large enterprises, public + Marketplace sector and SMEs, with AI components available to B2B products with partner network; roll-out of products in H2 2026 Various ISO only sizable market Certifications ✓û Note: Partnership was announced on 11 May as per Sunrise Media Release, with product roll-out to commence in H2 2026 only Q1 2026 Results | 13 May 2026 7

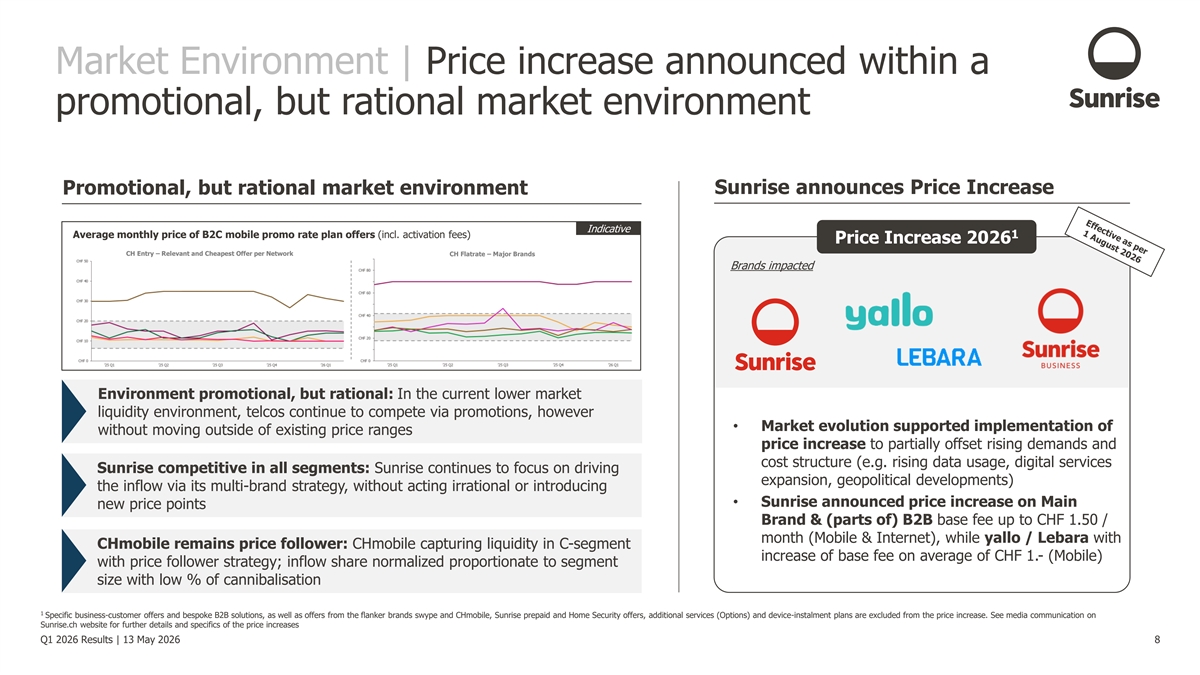

Market Environment | Price increase announced within a promotional, but rational market environment Sunrise announces Price Increase Promotional, but rational market environment Indicative Average monthly price of B2C mobile promo rate plan offers (incl. activation fees) 1 Price Increase 2026 CH Entry – Relevant and Cheapest Offer per Network CH Flatrate – Major Brands Brands impacted Environment promotional, but rational: In the current lower market liquidity environment, telcos continue to compete via promotions, however • Market evolution supported implementation of without moving outside of existing price ranges price increase to partially offset rising demands and cost structure (e.g. rising data usage, digital services Sunrise competitive in all segments: Sunrise continues to focus on driving expansion, geopolitical developments) the inflow via its multi-brand strategy, without acting irrational or introducing • Sunrise announced price increase on Main new price points Brand & (parts of) B2B base fee up to CHF 1.50 / month (Mobile & Internet), while yallo / Lebara with CHmobile remains price follower: CHmobile capturing liquidity in C-segment increase of base fee on average of CHF 1.- (Mobile) with price follower strategy; inflow share normalized proportionate to segment size with low % of cannibalisation 1 Specific business-customer offers and bespoke B2B solutions, as well as offers from the flanker brands swype and CHmobile, Sunrise prepaid and Home Security offers, additional services (Options) and device-instalment plans are excluded from the price increase. See media communication on Sunrise.ch website for further details and specifics of the price increases Q1 2026 Results | 13 May 2026 8

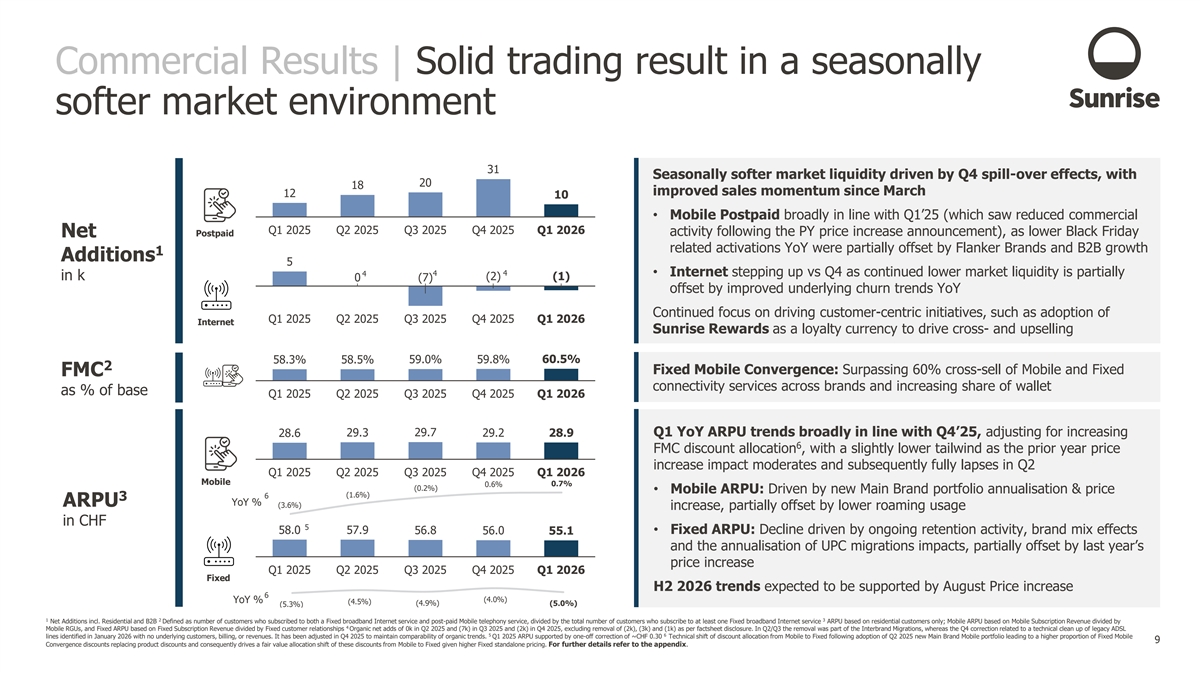

Commercial Results | Solid trading result in a seasonally softer market environment 31 Seasonally softer market liquidity driven by Q4 spill-over effects, with 20 18 improved sales momentum since March 12 10 • Mobile Postpaid broadly in line with Q1’25 (which saw reduced commercial Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Postpaid activity following the PY price increase announcement), as lower Black Friday Net related activations YoY were partially offset by Flanker Brands and B2B growth 1 Additions 5 4 4 4• Internet stepping up vs Q4 as continued lower market liquidity is partially in k (2) (1) 0 (7) offset by improved underlying churn trends YoY Continued focus on driving customer-centric initiatives, such as adoption of Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Internet Sunrise Rewards as a loyalty currency to drive cross- and upselling 58.3% 58.5% 59.0% 59.8% 60.5% 2 Fixed Mobile Convergence: Surpassing 60% cross-sell of Mobile and Fixed FMC connectivity services across brands and increasing share of wallet as % of base Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 29.3 29.7 Q1 YoY ARPU trends broadly in line with Q4’25, adjusting for increasing 28.6 29.2 28.9 6 FMC discount allocation , with a slightly lower tailwind as the prior year price increase impact moderates and subsequently fully lapses in Q2 Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Mobile 0.7% 0.6% (0.2%) • Mobile ARPU: Driven by new Main Brand portfolio annualisation & price (1.6%) 6 3 YoY % ARPU (3.6%) increase, partially offset by lower roaming usage in CHF 5 58.0 57.9• Fixed ARPU: Decline driven by ongoing retention activity, brand mix effects 56.8 56.0 55.1 and the annualisation of UPC migrations impacts, partially offset by last year’s price increase Q1 2025 Q2 2025 Q3 2025 Q4 2025 Q1 2026 Fixed H2 2026 trends expected to be supported by August Price increase 6 (4.0%) YoY % (4.5%) (4.9%) (5.0%) (5.3%) 1 2 3 Net Additions incl. Residential and B2B Defined as number of customers who subscribed to both a Fixed broadband Internet service and post-paid Mobile telephony service, divided by the total number of customers who subscribe to at least one Fixed broadband Internet service ARPU based on residential customers only; Mobile ARPU based on Mobile Subscription Revenue divided by 4 Mobile RGUs, and Fixed ARPU based on Fixed Subscription Revenue divided by Fixed customer relationships Organic net adds of 0k in Q2 2025 and (7k) in Q3 2025 and (2k) in Q4 2025, excluding removal of (2k), (3k) and (1k) as per factsheet disclosure. In Q2/Q3 the removal was part of the Interbrand Migrations, whereas the Q4 correction related to a technical clean up of legacy ADSL 5 6 lines identified in January 2026 with no underlying customers, billing, or revenues. It has been adjusted in Q4 2025 to maintain comparability of organic trends. Q1 2025 ARPU supported by one-off correction of ~CHF 0.30 Technical shift of discount allocation from Mobile to Fixed following adoption of Q2 2025 new Main Brand Mobile portfolio leading to a higher proportion of Fixed Mobile Q1 2026 Results | 13 May 2026 9 Convergence discounts replacing product discounts and consequently drives a fair value allocation shift of these discounts from Mobile to Fixed given higher Fixed standalone pricing. For further details refer to the appendix.

Financial Results [background image] Q1 2026 Results | 13 May 2026

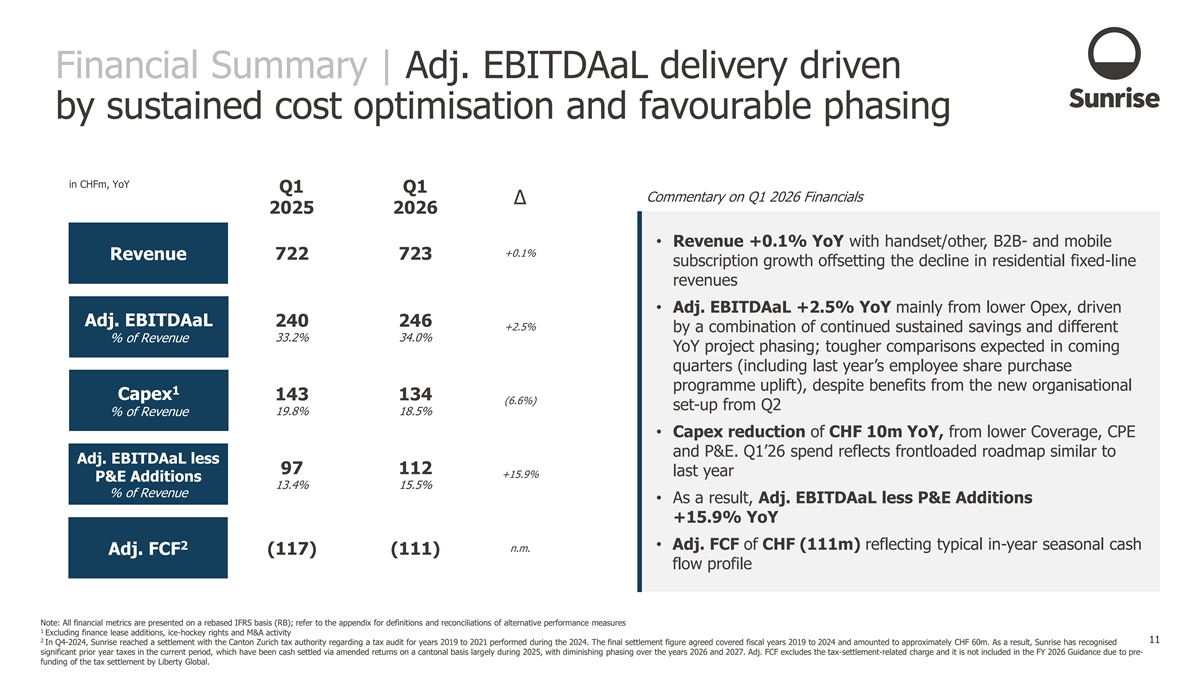

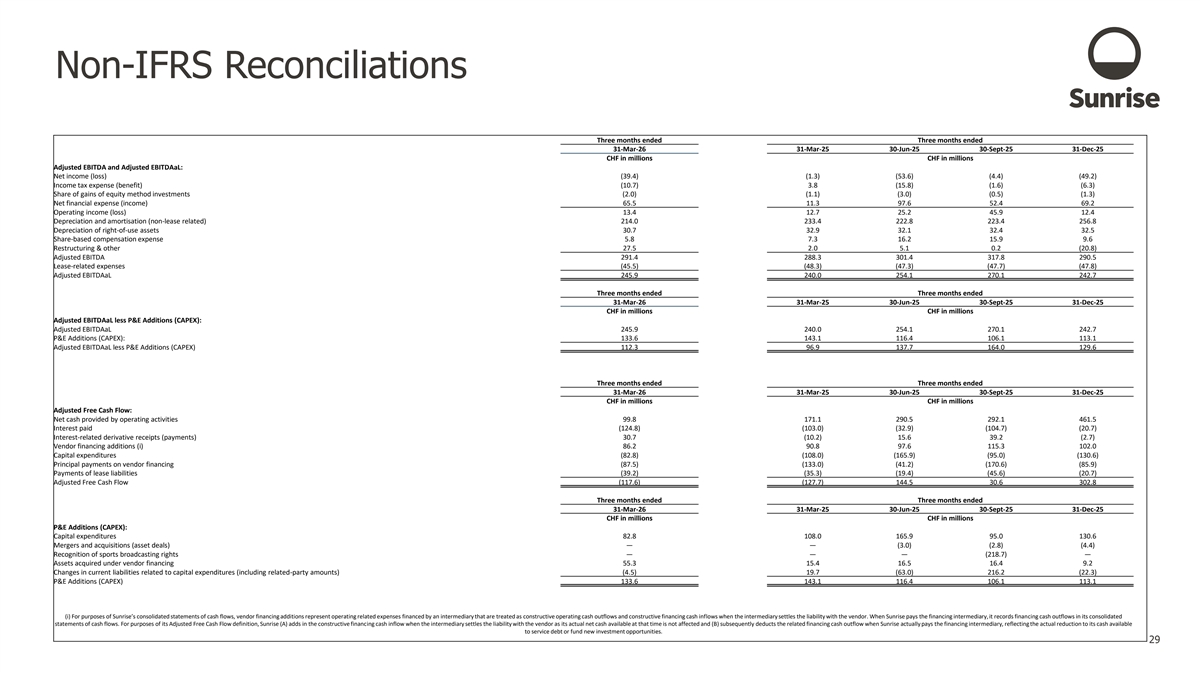

Financial Summary | Adj. EBITDAaL delivery driven by sustained cost optimisation and favourable phasing in CHFm, YoY Q1 Q1 Commentary on Q1 2026 Financials Δ 2025 2026 • Revenue +0.1% YoY with handset/other, B2B- and mobile +0.1% Revenue 722 723 subscription growth offsetting the decline in residential fixed-line revenues • Adj. EBITDAaL +2.5% YoY mainly from lower Opex, driven Adj. EBITDAaL 240 246 +2.5% by a combination of continued sustained savings and different 33.2% 34.0% % of Revenue YoY project phasing; tougher comparisons expected in coming quarters (including last year’s employee share purchase programme uplift), despite benefits from the new organisational 1 Capex 143 134 (6.6%) set-up from Q2 19.8% 18.5% % of Revenue • Capex reduction of CHF 10m YoY, from lower Coverage, CPE and P&E. Q1’26 spend reflects frontloaded roadmap similar to Adj. EBITDAaL less 97 112 last year +15.9% P&E Additions 13.4% 15.5% % of Revenue • As a result, Adj. EBITDAaL less P&E Additions +15.9% YoY 2• Adj. FCF of CHF (111m) reflecting typical in-year seasonal cash n.m. Adj. FCF (117) (111) flow profile Note: All financial metrics are presented on a rebased IFRS basis (RB); refer to the appendix for definitions and reconciliations of alternative performance measures 1 Excluding finance lease additions, ice-hockey rights and M&A activity 2 Q1 2026 Results | 13 May 2026 11 11 In Q4-2024, Sunrise reached a settlement with the Canton Zurich tax authority regarding a tax audit for years 2019 to 2021 performed during the 2024. The final settlement figure agreed covered fiscal years 2019 to 2024 and amounted to approximately CHF 60m. As a result, Sunrise has recognised significant prior year taxes in the current period, which have been cash settled via amended returns on a cantonal basis largely during 2025, with diminishing phasing over the years 2026 and 2027. Adj. FCF excludes the tax-settlement-related charge and it is not included in the FY 2026 Guidance due to pre- funding of the tax settlement by Liberty Global.

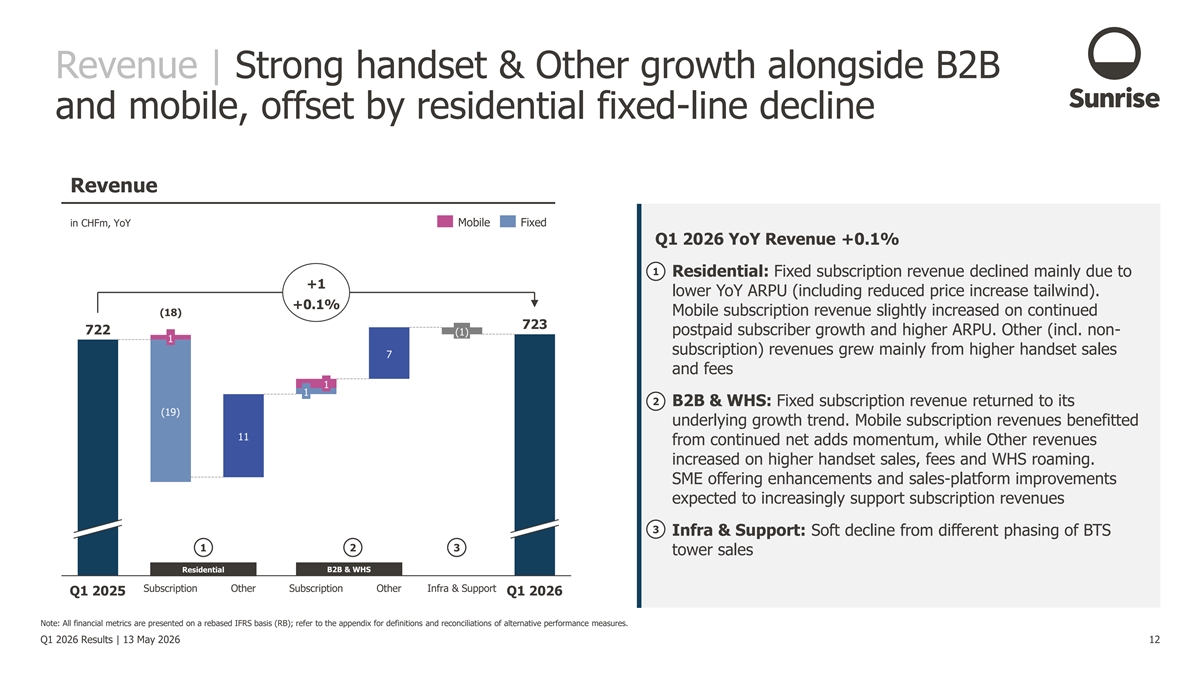

Revenue | Strong handset & Other growth alongside B2B and mobile, offset by residential fixed-line decline Revenue in CHFm, YoY Mobile Fixed Q1 2026 YoY Revenue +0.1% 1 • Residential: Fixed subscription revenue declined mainly due to +1 lower YoY ARPU (including reduced price increase tailwind). +0.1% (18) Mobile subscription revenue slightly increased on continued 723 722 postpaid subscriber growth and higher ARPU. Other (incl. non- (1) 1 subscription) revenues grew mainly from higher handset sales 7 and fees 1 1 2 • B2B & WHS: Fixed subscription revenue returned to its (19) underlying growth trend. Mobile subscription revenues benefitted 11 from continued net adds momentum, while Other revenues increased on higher handset sales, fees and WHS roaming. SME offering enhancements and sales-platform improvements expected to increasingly support subscription revenues 3 • Infra & Support: Soft decline from different phasing of BTS 1 2 3 tower sales Residential B2B & WHS Subscription Other Subscription Other Infra & Support Q1 2025 Q1 2026 Note: All financial metrics are presented on a rebased IFRS basis (RB); refer to the appendix for definitions and reconciliations of alternative performance measures. Q1 2026 Results | 13 May 2026 12

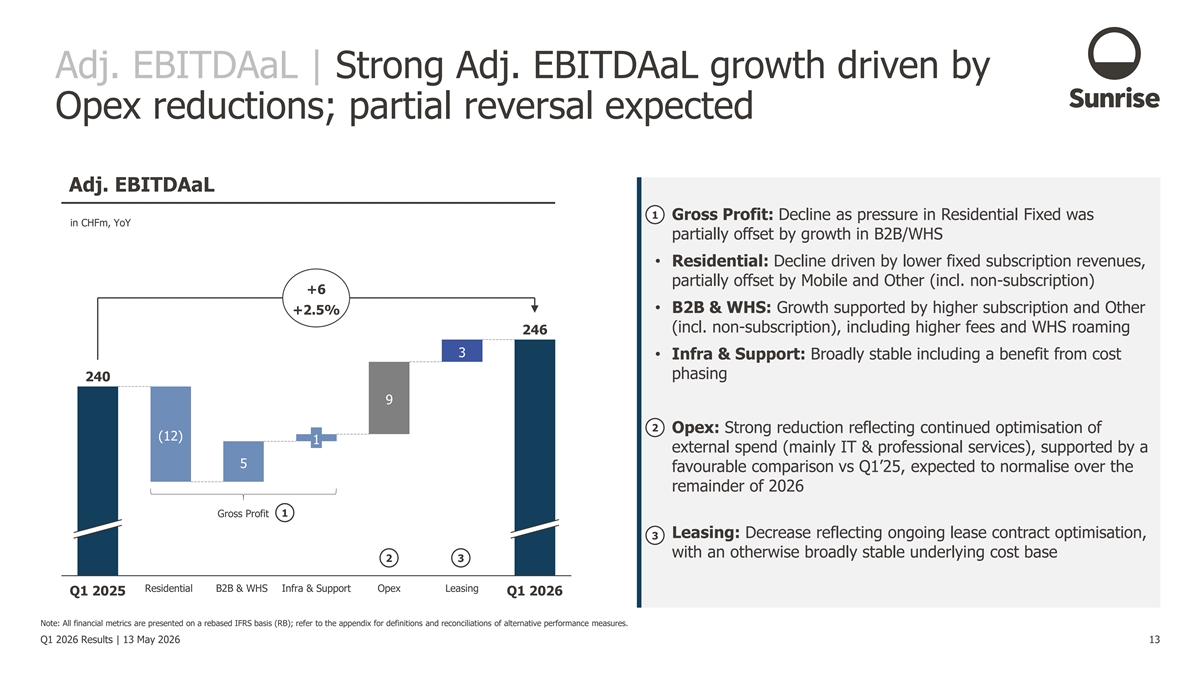

Adj. EBITDAaL | Strong Adj. EBITDAaL growth driven by Opex reductions; partial reversal expected Adj. EBITDAaL 1 • Gross Profit: Decline as pressure in Residential Fixed was in CHFm, YoY partially offset by growth in B2B/WHS • Residential: Decline driven by lower fixed subscription revenues, partially offset by Mobile and Other (incl. non-subscription) +6 • B2B & WHS: Growth supported by higher subscription and Other +2.5% (incl. non-subscription), including higher fees and WHS roaming 246 3 • Infra & Support: Broadly stable including a benefit from cost phasing 240 9 2 • Opex: Strong reduction reflecting continued optimisation of (12) 1 external spend (mainly IT & professional services), supported by a 5 favourable comparison vs Q1’25, expected to normalise over the remainder of 2026 Gross Profit 1 • Leasing: Decrease reflecting ongoing lease contract optimisation, 3 with an otherwise broadly stable underlying cost base 2 3 Residential B2B & WHS Infra & Support Opex Leasing Q1 2025 Q1 2026 Note: All financial metrics are presented on a rebased IFRS basis (RB); refer to the appendix for definitions and reconciliations of alternative performance measures. Q1 2026 Results | 13 May 2026 13

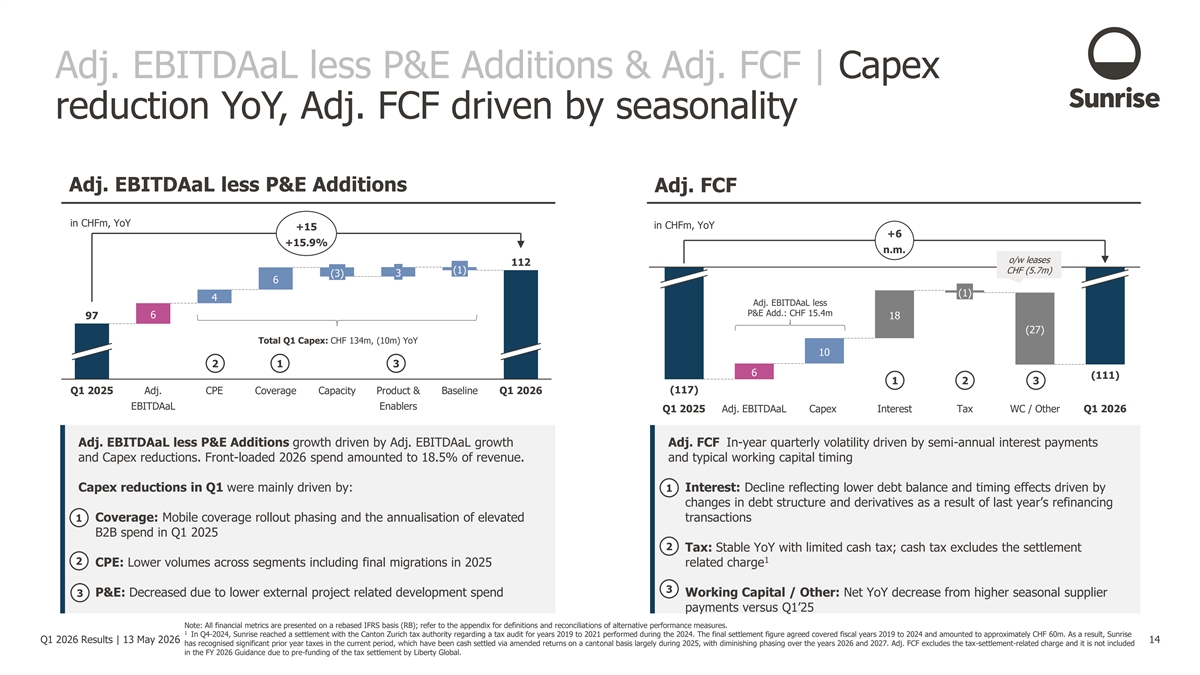

Adj. EBITDAaL less P&E Additions & Adj. FCF | Capex reduction YoY, Adj. FCF driven by seasonality Adj. EBITDAaL less P&E Additions Adj. FCF in CHFm, YoY in CHFm, YoY +15 +6 +15.9% n.m. o/w leases 112 (1) CHF (5.7m) (3) 3 6 (1) 4 Adj. EBITDAaL less P&E Add.: CHF 15.4m 6 97 18 (27) Total Q1 Capex: CHF 134m, (10m) YoY 10 2 1 3 6 (111) 1 2 3 (117) Q1 2025 Adj. CPE Coverage Capacity Product & Baseline Q1 2026 EBITDAaL Enablers Q1 2025 Adj. EBITDAaL Capex Interest Tax WC / Other Q1 2026 Adj. EBITDAaL less P&E Additions growth driven by Adj. EBITDAaL growth Adj. FCF In-year quarterly volatility driven by semi-annual interest payments and Capex reductions. Front-loaded 2026 spend amounted to 18.5% of revenue. and typical working capital timing Capex reductions in Q1 were mainly driven by: • Interest: Decline reflecting lower debt balance and timing effects driven by 1 changes in debt structure and derivatives as a result of last year’s refinancing • Coverage: Mobile coverage rollout phasing and the annualisation of elevated transactions 1 B2B spend in Q1 2025 2 • Tax: Stable YoY with limited cash tax; cash tax excludes the settlement 1 2 • CPE: Lower volumes across segments including final migrations in 2025 related charge 3 • P&E: Decreased due to lower external project related development spend • Working Capital / Other: Net YoY decrease from higher seasonal supplier 3 payments versus Q1’25 Note: All financial metrics are presented on a rebased IFRS basis (RB); refer to the appendix for definitions and reconciliations of alternative performance measures. 1 In Q4-2024, Sunrise reached a settlement with the Canton Zurich tax authority regarding a tax audit for years 2019 to 2021 performed during the 2024. The final settlement figure agreed covered fiscal years 2019 to 2024 and amounted to approximately CHF 60m. As a result, Sunrise Q1 2026 Results | 13 May 2026 14 has recognised significant prior year taxes in the current period, which have been cash settled via amended returns on a cantonal basis largely during 2025, with diminishing phasing over the years 2026 and 2027. Adj. FCF excludes the tax-settlement-related charge and it is not included in the FY 2026 Guidance due to pre-funding of the tax settlement by Liberty Global.

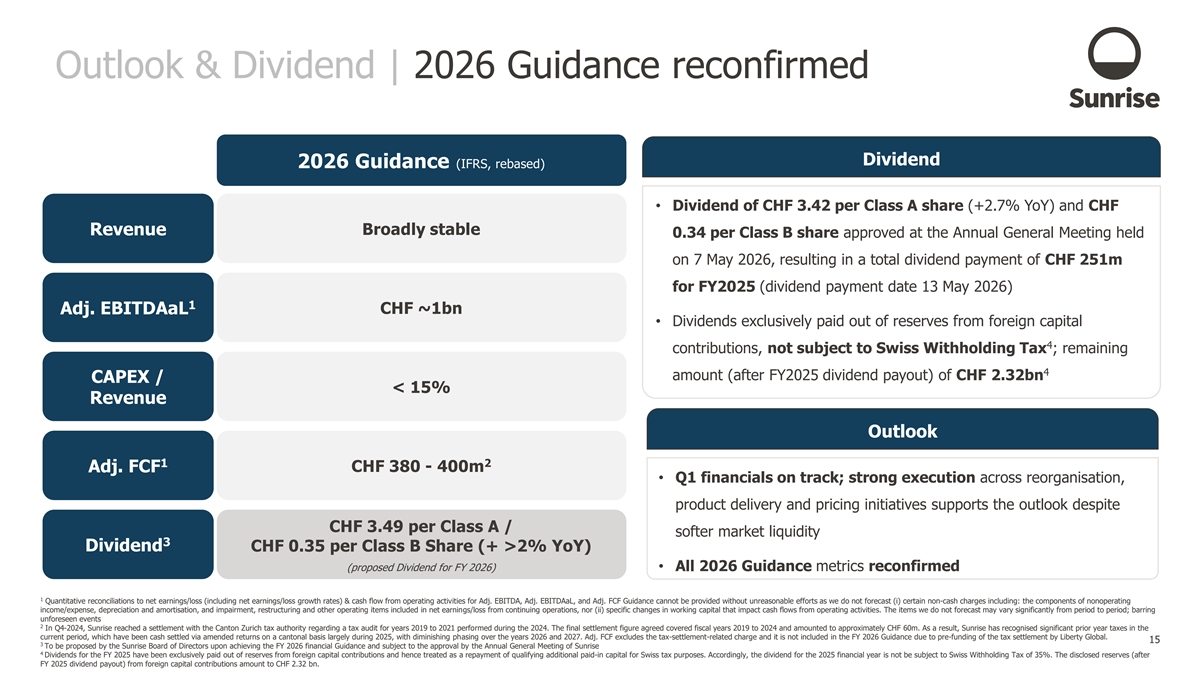

Outlook & Dividend | 2026 Guidance reconfirmed Dividend 2026 Guidance (IFRS, rebased) • Dividend of CHF 3.42 per Class A share (+2.7% YoY) and CHF Revenue Broadly stable 0.34 per Class B share approved at the Annual General Meeting held on 7 May 2026, resulting in a total dividend payment of CHF 251m for FY2025 (dividend payment date 13 May 2026) 1 CHF ~1bn Adj. EBITDAaL • Dividends exclusively paid out of reserves from foreign capital 4 contributions, not subject to Swiss Withholding Tax ; remaining 4 amount (after FY2025 dividend payout) of CHF 2.32bn CAPEX / < 15% Revenue Outlook 1 2 Adj. FCF CHF 380 - 400m • Q1 financials on track; strong execution across reorganisation, product delivery and pricing initiatives supports the outlook despite CHF 3.49 per Class A / softer market liquidity 3 Dividend CHF 0.35 per Class B Share (+ >2% YoY) (proposed Dividend for FY 2026)• All 2026 Guidance metrics reconfirmed 1 Quantitative reconciliations to net earnings/loss (including net earnings/loss growth rates) & cash flow from operating activities for Adj. EBITDA, Adj. EBITDAaL, and Adj. FCF Guidance cannot be provided without unreasonable efforts as we do not forecast (i) certain non-cash charges including: the components of nonoperating income/expense, depreciation and amortisation, and impairment, restructuring and other operating items included in net earnings/loss from continuing operations, nor (ii) specific changes in working capital that impact cash flows from operating activities. The items we do not forecast may vary significantly from period to period; barring unforeseen events 2 In Q4-2024, Sunrise reached a settlement with the Canton Zurich tax authority regarding a tax audit for years 2019 to 2021 performed during the 2024. The final settlement figure agreed covered fiscal years 2019 to 2024 and amounted to approximately CHF 60m. As a result, Sunrise has recognised significant prior year taxes in the current period, which have been cash settled via amended returns on a cantonal basis largely during 2025, with diminishing phasing over the years 2026 and 2027. Adj. FCF excludes the tax-settlement-related charge and it is not included in the FY 2026 Guidance due to pre-funding of the tax settlement by Liberty Global. Q1 2026 Results | 13 May 2026 15 3 To be proposed by the Sunrise Board of Directors upon achieving the FY 2026 financial Guidance and subject to the approval by the Annual General Meeting of Sunrise 4 Dividends for the FY 2025 have been exclusively paid out of reserves from foreign capital contributions and hence treated as a repayment of qualifying additional paid-in capital for Swiss tax purposes. Accordingly, the dividend for the 2025 financial year is not be subject to Swiss Withholding Tax of 35%. The disclosed reserves (after FY 2025 dividend payout) from foreign capital contributions amount to CHF 2.32 bn.

Final remarks Q1 2026 Results | 13 May 2026

Key Takeaways Launch of Innovative Sunrise Rewards programme to increase loyalty and accelerate cross- and upselling; Exclusive strategic B2B partnership with PHOENIQS to offer sovereign AI solutions 1 Product enhancements combined with sales and churn improvements, alongside the August price increase, strengthen momentum 2 FY 2025 dividend approved and paid; Q1 financials on track and supporting reconfirmation of FY 2026 Guidance incl. 1 progressive DPS (CHF 3.49 +>2% YoY) 3 1 17 Q1 2026 Results | 13 May 2026 Per Class A Share. To be proposed by the Sunrise Board of Directors upon achieving the FY 2026 financial Guidance and subject to the approval by the Annual General Meeting of Sunrise

Q&A Q1 2026 Results | 13 May 2026 18

Appendix Q1 2026 Results | 13 May 2026

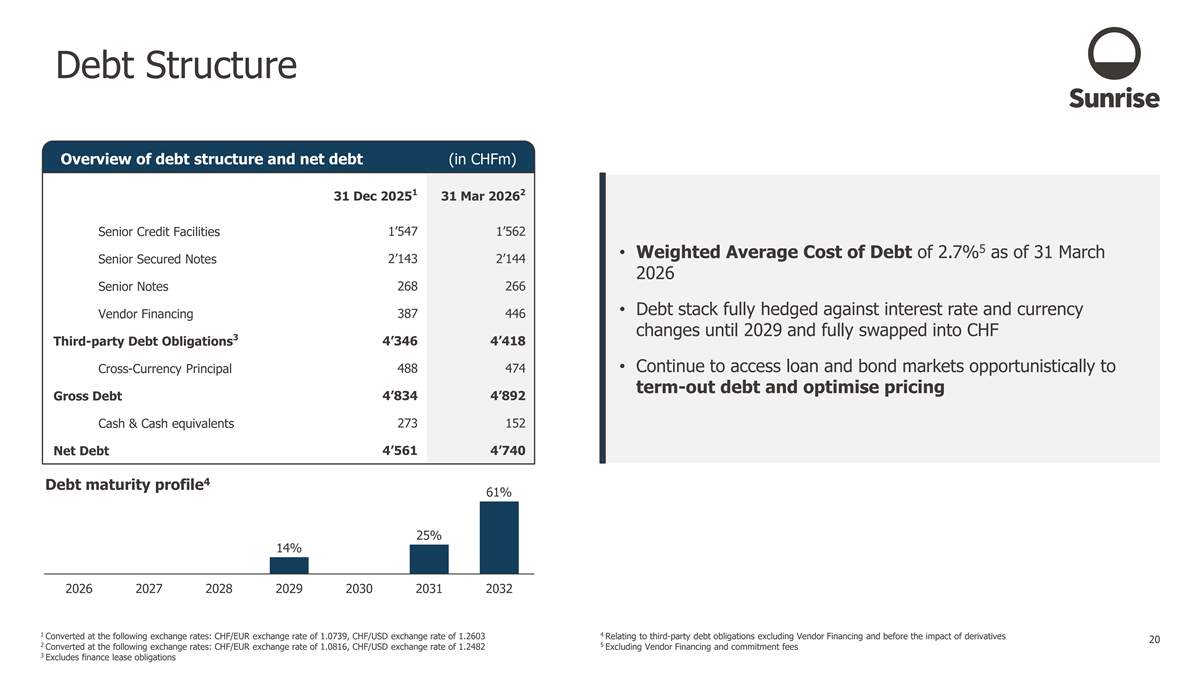

Debt Structure Overview of debt structure and net debt (in CHFm) 1 2 31 Dec 2025 31 Mar 2026 Senior Credit Facilities 1’547 1’562 5 • Weighted Average Cost of Debt of 2.7% as of 31 March Senior Secured Notes 2’143 2’144 2026 Senior Notes 268 266 • Debt stack fully hedged against interest rate and currency Vendor Financing 387 446 changes until 2029 and fully swapped into CHF 3 4’346 4’418 Third-party Debt Obligations 488 474• Continue to access loan and bond markets opportunistically to Cross-Currency Principal term-out debt and optimise pricing 4’834 4’892 Gross Debt Cash & Cash equivalents 273 152 Net Debt 4’561 4’740 4 Debt maturity profile 61% 25% 14% 2026 2027 2028 2029 2030 2031 2032 1 4 Converted at the following exchange rates: CHF/EUR exchange rate of 1.0739, CHF/USD exchange rate of 1.2603 Relating to third-party debt obligations excluding Vendor Financing and before the impact of derivatives Q1 2026 Results | 13 May 2026 20 2 5 Converted at the following exchange rates: CHF/EUR exchange rate of 1.0816, CHF/USD exchange rate of 1.2482 Excluding Vendor Financing and commitment fees 3 Excludes finance lease obligations

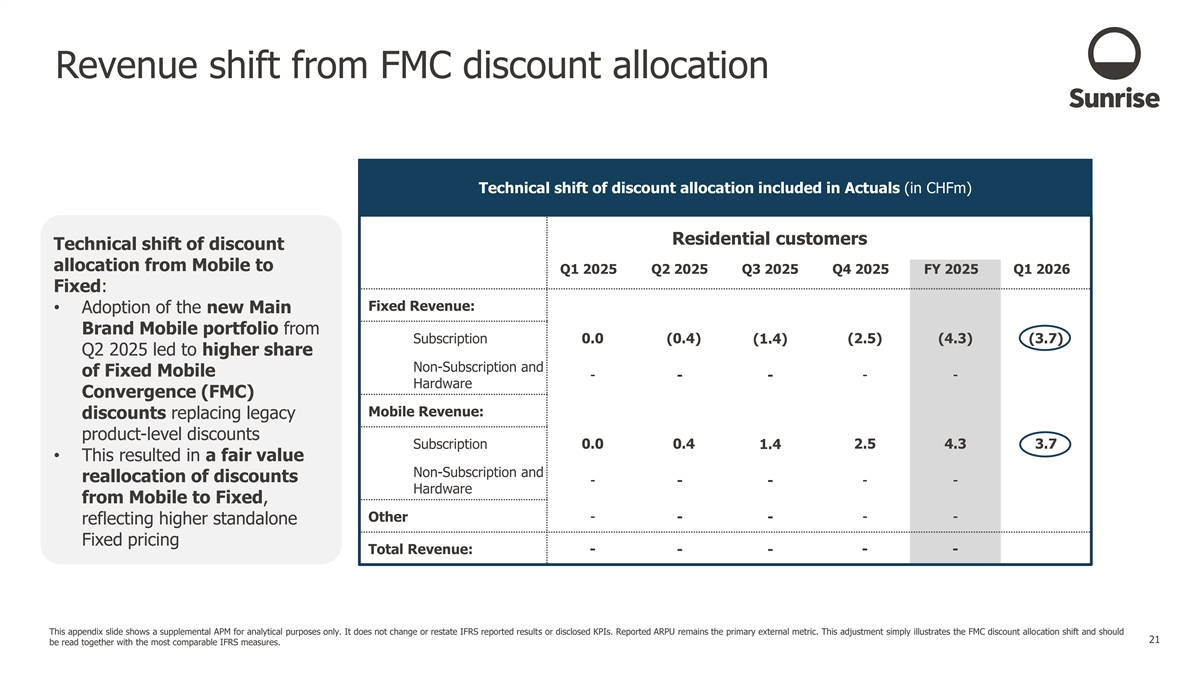

Revenue shift from FMC discount allocation Technical shift of discount allocation included in Actuals (in CHFm) Residential customers Technical shift of discount allocation from Mobile to Q1 2025 Q2 2025 Q3 2025 Q4 2025 FY 2025 Q1 2026 Fixed: Fixed Revenue: • Adoption of the new Main Brand Mobile portfolio from Subscription 0.0 (0.4) (1.4) (2.5) (4.3) (3.7) Q2 2025 led to higher share Non-Subscription and of Fixed Mobile - - - - - Hardware Convergence (FMC) Mobile Revenue: discounts replacing legacy product-level discounts Subscription 0.0 0.4 1.4 2.5 4.3 3.7 • This resulted in a fair value Non-Subscription and reallocation of discounts - - - - - Hardware from Mobile to Fixed, - - - Other - - reflecting higher standalone Fixed pricing Total Revenue: - - - - - This appendix slide shows a supplemental APM for analytical purposes only. It does not change or restate IFRS reported results or disclosed KPIs. Reported ARPU remains the primary external metric. This adjustment simply illustrates the FMC discount allocation shift and should Q1 2026 Results | 13 May 2026 21 be read together with the most comparable IFRS measures.

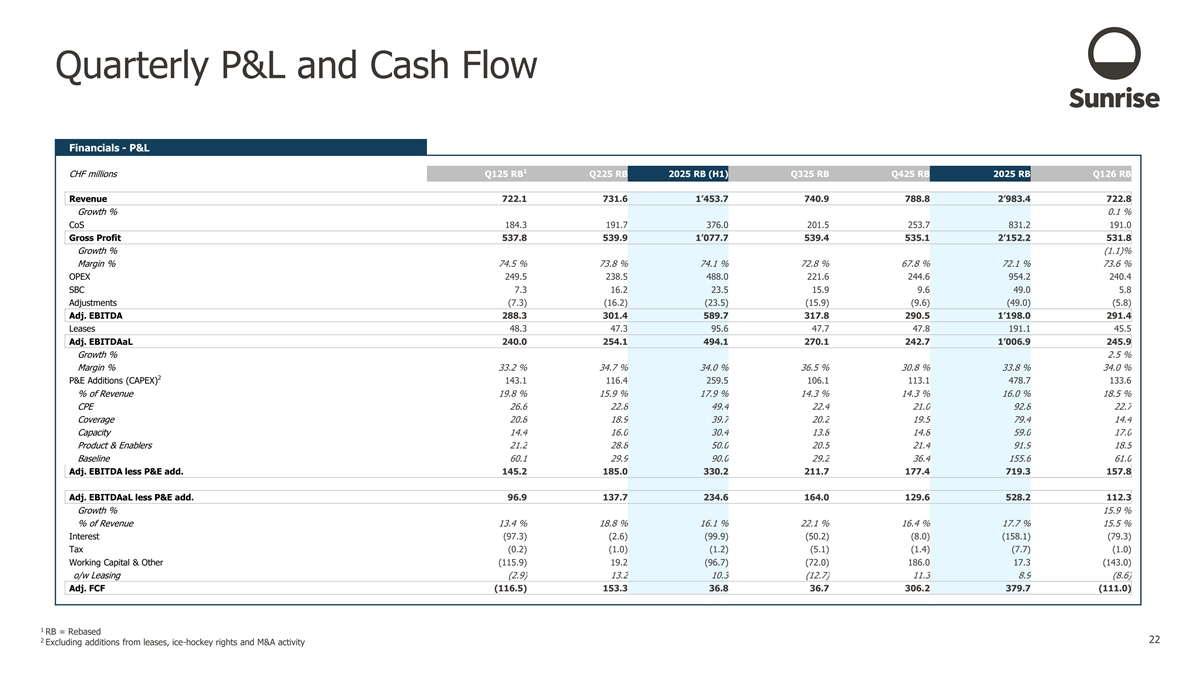

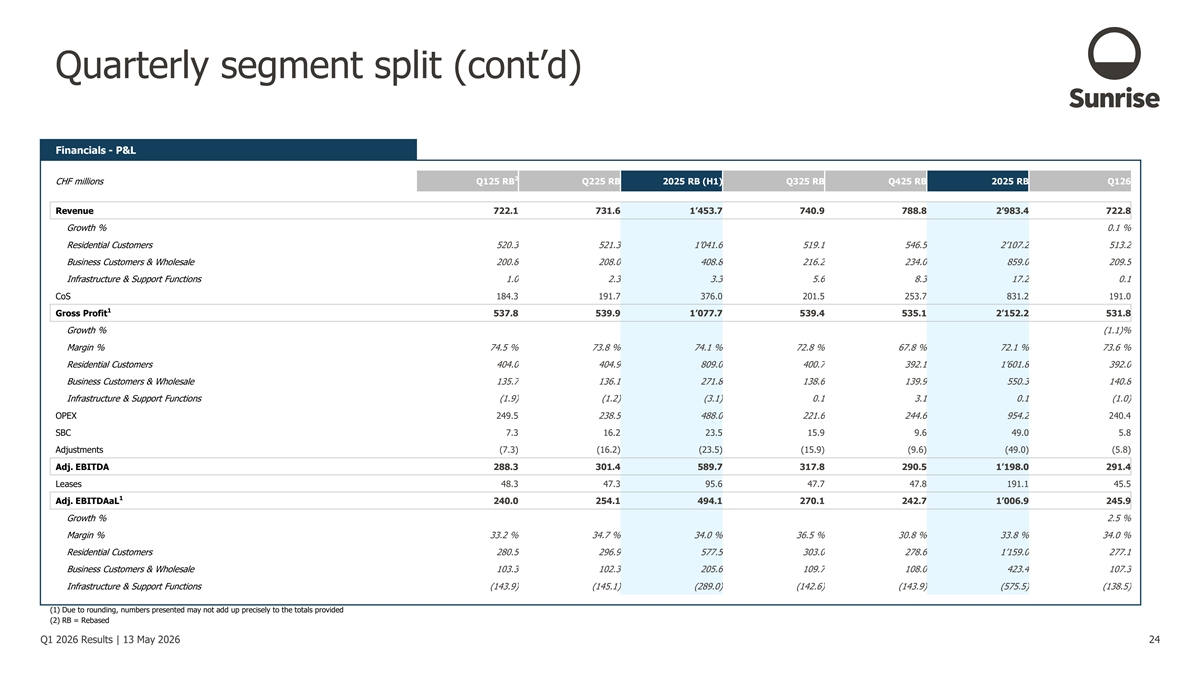

Quarterly P&L and Cash Flow Financials - P&L 1 CHF millions Q125 RB Q225 RB 2025 RB (H1) Q325 RB Q425 RB 2025 RB Q126 RB Revenue 722.1 731.6 1’453.7 740.9 788.8 2’983.4 722.8 Growth % 0.1 % CoS 184.3 191.7 376.0 201.5 253.7 831.2 191.0 Gross Profit 537.8 539.9 1’077.7 539.4 535.1 2’152.2 531.8 Growth % (1.1)% Margin % 74.5 % 73.8 % 74.1 % 72.8 % 67.8 % 72.1 % 73.6 % OPEX 249.5 238.5 488.0 221.6 244.6 954.2 240.4 SBC 7.3 16.2 23.5 15.9 9.6 49.0 5.8 Adjustments (7.3) (16.2) (23.5) (15.9) (9.6) (49.0) (5.8) Adj. EBITDA 288.3 301.4 589.7 317.8 290.5 1’198.0 291.4 Leases 48.3 47.3 95.6 47.7 47.8 191.1 45.5 Adj. EBITDAaL 240.0 254.1 494.1 270.1 242.7 1’006.9 245.9 Growth % 2.5 % Margin % 33.2 % 34.7 % 34.0 % 36.5 % 30.8 % 33.8 % 34.0 % 2 P&E Additions (CAPEX) 143.1 116.4 259.5 106.1 113.1 478.7 133.6 % of Revenue 19.8 % 15.9 % 17.9 % 14.3 % 14.3 % 16.0 % 18.5 % CPE 26.6 22.8 49.4 22.4 21.0 92.8 22.7 Coverage 20.8 18.9 39.7 20.2 19.5 79.4 14.4 Capacity 14.4 16.0 30.4 13.8 14.8 59.0 17.0 Product & Enablers 21.2 28.8 50.0 20.5 21.4 91.9 18.5 Baseline 60.1 29.9 90.0 29.2 36.4 155.6 61.0 Adj. EBITDA less P&E add. 145.2 185.0 330.2 211.7 177.4 719.3 157.8 Adj. EBITDAaL less P&E add. 96.9 137.7 234.6 164.0 129.6 528.2 112.3 Growth % 15.9 % % of Revenue 13.4 % 18.8 % 16.1 % 22.1 % 16.4 % 17.7 % 15.5 % Interest (97.3) (2.6) (99.9) (50.2) (8.0) (158.1) (79.3) Tax (0.2) (1.0) (1.2) (5.1) (1.4) (7.7) (1.0) Working Capital & Other (115.9) 19.2 (96.7) (72.0) 186.0 17.3 (143.0) o/w Leasing (2.9) 13.2 10.3 (12.7) 11.3 8.9 (8.6) Adj. FCF (116.5) 153.3 36.8 36.7 306.2 379.7 (111.0) 1 RB = Rebased 2 Q1 2026 Results | 13 May 2026 22 Excluding additions from leases, ice-hockey rights and M&A activity

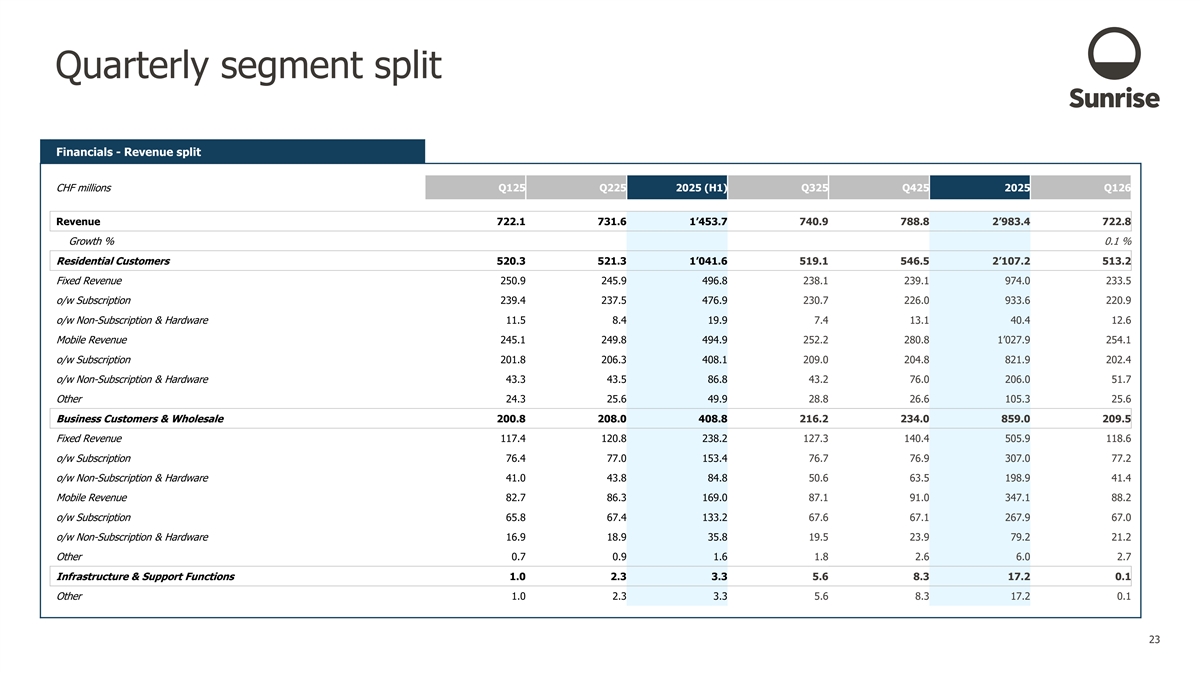

Quarterly segment split Financials - Revenue split CHF millions Q125 Q225 2025 (H1) Q325 Q425 2025 Q126 Revenue 722.1 731.6 1’453.7 740.9 788.8 2’983.4 722.8 Growth % 0.1 % Residential Customers 520.3 521.3 1’041.6 519.1 546.5 2’107.2 513.2 Fixed Revenue 250.9 245.9 496.8 238.1 239.1 974.0 233.5 o/w Subscription 239.4 237.5 476.9 230.7 226.0 933.6 220.9 o/w Non-Subscription & Hardware 11.5 8.4 19.9 7.4 13.1 40.4 12.6 Mobile Revenue 245.1 249.8 494.9 252.2 280.8 1’027.9 254.1 o/w Subscription 201.8 206.3 408.1 209.0 204.8 821.9 202.4 o/w Non-Subscription & Hardware 43.3 43.5 86.8 43.2 76.0 206.0 51.7 Other 24.3 25.6 49.9 28.8 26.6 105.3 25.6 Business Customers & Wholesale 200.8 208.0 408.8 216.2 234.0 859.0 209.5 Fixed Revenue 117.4 120.8 238.2 127.3 140.4 505.9 118.6 o/w Subscription 76.4 77.0 153.4 76.7 76.9 307.0 77.2 o/w Non-Subscription & Hardware 41.0 43.8 84.8 50.6 63.5 198.9 41.4 Mobile Revenue 82.7 86.3 169.0 87.1 91.0 347.1 88.2 o/w Subscription 65.8 67.4 133.2 67.6 67.1 267.9 67.0 o/w Non-Subscription & Hardware 16.9 18.9 35.8 19.5 23.9 79.2 21.2 Other 0.7 0.9 1.6 1.8 2.6 6.0 2.7 Infrastructure & Support Functions 1.0 2.3 3.3 5.6 8.3 17.2 0.1 Other 1.0 2.3 3.3 5.6 8.3 17.2 0.1 Q1 2026 Results | 13 May 2026 23

Quarterly segment split (cont’d) Financials - P&L 2 CHF millions Q125 RB Q225 RB 2025 RB (H1) Q325 RB Q425 RB 2025 RB Q126 Revenue 722.1 731.6 1’453.7 740.9 788.8 2’983.4 722.8 Growth % 0.1 % Residential Customers 520.3 521.3 1’041.6 519.1 546.5 2’107.2 513.2 Business Customers & Wholesale 200.8 208.0 408.8 216.2 234.0 859.0 209.5 Infrastructure & Support Functions 1.0 2.3 3.3 5.6 8.3 17.2 0.1 CoS 184.3 191.7 376.0 201.5 253.7 831.2 191.0 1 Gross Profit 537.8 539.9 1’077.7 539.4 535.1 2’152.2 531.8 Growth % (1.1)% Margin % 74.5 % 73.8 % 74.1 % 72.8 % 67.8 % 72.1 % 73.6 % Residential Customers 404.0 404.9 809.0 400.7 392.1 1’601.8 392.0 Business Customers & Wholesale 135.7 136.1 271.8 138.6 139.9 550.3 140.8 Infrastructure & Support Functions (1.9) (1.2) (3.1) 0.1 3.1 0.1 (1.0) OPEX 249.5 238.5 488.0 221.6 244.6 954.2 240.4 SBC 7.3 16.2 23.5 15.9 9.6 49.0 5.8 Adjustments (7.3) (16.2) (23.5) (15.9) (9.6) (49.0) (5.8) Adj. EBITDA 288.3 301.4 589.7 317.8 290.5 1’198.0 291.4 Leases 48.3 47.3 95.6 47.7 47.8 191.1 45.5 1 Adj. EBITDAaL 240.0 254.1 494.1 270.1 242.7 1’006.9 245.9 Growth % 2.5 % Margin % 33.2 % 34.7 % 34.0 % 36.5 % 30.8 % 33.8 % 34.0 % Residential Customers 280.5 296.9 577.5 303.0 278.6 1’159.0 277.1 Business Customers & Wholesale 103.3 102.3 205.6 109.7 108.0 423.4 107.3 Infrastructure & Support Functions (143.9) (145.1) (289.0) (142.6) (143.9) (575.5) (138.5) (1) Due to rounding, numbers presented may not add up precisely to the totals provided (2) RB = Rebased Q1 2026 Results | 13 May 2026 24

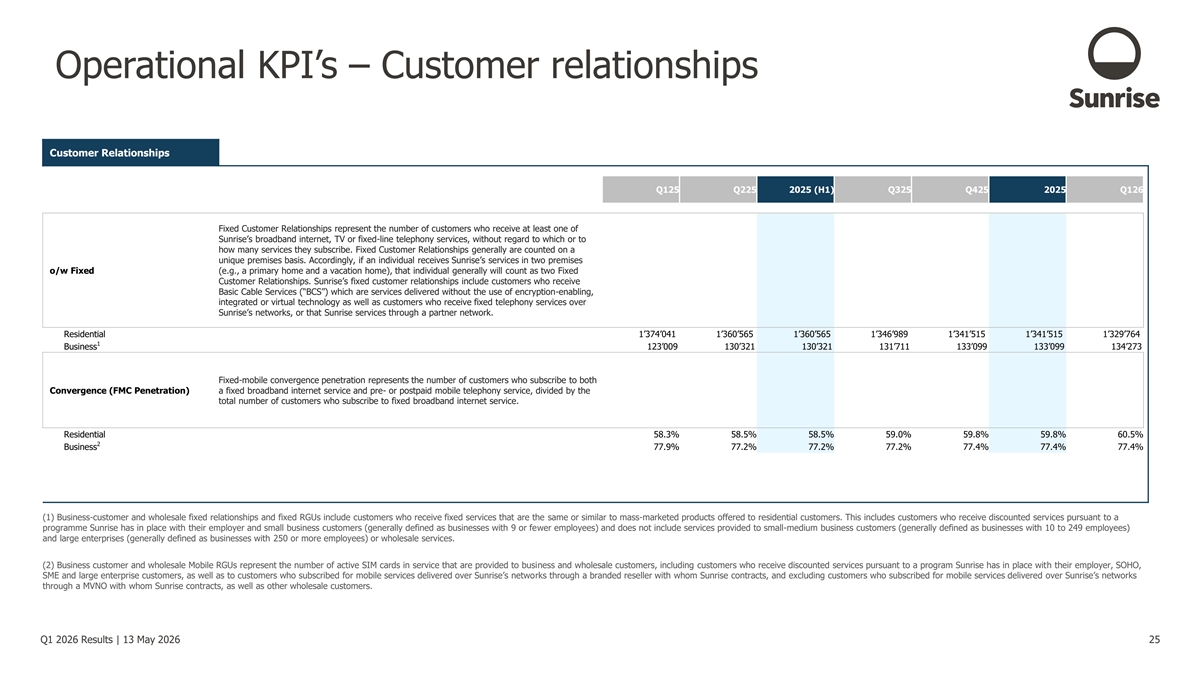

Operational KPI’s – Customer relationships Customer Relationships Q125 Q225 2025 (H1) Q325 Q425 2025 Q126 Fixed Customer Relationships represent the number of customers who receive at least one of Sunrise’s broadband internet, TV or fixed-line telephony services, without regard to which or to how many services they subscribe. Fixed Customer Relationships generally are counted on a unique premises basis. Accordingly, if an individual receives Sunrise’s services in two premises o/w Fixed (e.g., a primary home and a vacation home), that individual generally will count as two Fixed Customer Relationships. Sunrise’s fixed customer relationships include customers who receive Basic Cable Services (“BCS”) which are services delivered without the use of encryption-enabling, integrated or virtual technology as well as customers who receive fixed telephony services over Sunrise’s networks, or that Sunrise services through a partner network. Residential 1’374’041 1’360’565 1’360’565 1’346’989 1’341’515 1’341’515 1’329’764 1 Business 123’009 130’321 130’321 131’711 133’099 133’099 134’273 Fixed-mobile convergence penetration represents the number of customers who subscribe to both Convergence (FMC Penetration) a fixed broadband internet service and pre- or postpaid mobile telephony service, divided by the total number of customers who subscribe to fixed broadband internet service. Residential 58.3% 58.5% 58.5% 59.0% 59.8% 59.8% 60.5% 2 Business 77.9% 77.2% 77.2% 77.2% 77.4% 77.4% 77.4% (1) Business-customer and wholesale fixed relationships and fixed RGUs include customers who receive fixed services that are the same or similar to mass-marketed products offered to residential customers. This includes customers who receive discounted services pursuant to a programme Sunrise has in place with their employer and small business customers (generally defined as businesses with 9 or fewer employees) and does not include services provided to small-medium business customers (generally defined as businesses with 10 to 249 employees) and large enterprises (generally defined as businesses with 250 or more employees) or wholesale services. (2) Business customer and wholesale Mobile RGUs represent the number of active SIM cards in service that are provided to business and wholesale customers, including customers who receive discounted services pursuant to a program Sunrise has in place with their employer, SOHO, SME and large enterprise customers, as well as to customers who subscribed for mobile services delivered over Sunrise’s networks through a branded reseller with whom Sunrise contracts, and excluding customers who subscribed for mobile services delivered over Sunrise’s networks through a MVNO with whom Sunrise contracts, as well as other wholesale customers. Q1 2026 Results | 13 May 2026 25

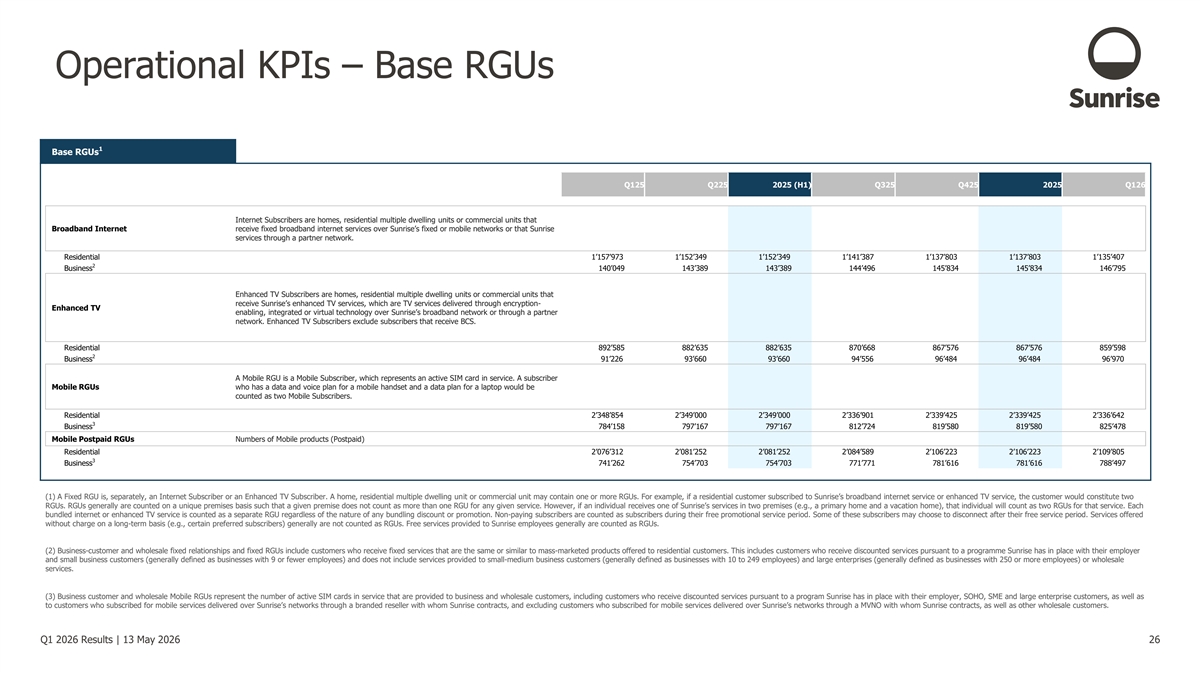

Operational KPIs – Base RGUs 1 Base RGUs Q125 Q225 2025 (H1) Q325 Q425 2025 Q126 Internet Subscribers are homes, residential multiple dwelling units or commercial units that Broadband Internet receive fixed broadband internet services over Sunrise’s fixed or mobile networks or that Sunrise services through a partner network. Residential 1’157’973 1’152’349 1’152’349 1’141’387 1’137’803 1’137’803 1’135’407 2 Business 140’049 143’389 143’389 144’496 145’834 145’834 146’795 Enhanced TV Subscribers are homes, residential multiple dwelling units or commercial units that receive Sunrise’s enhanced TV services, which are TV services delivered through encryption- Enhanced TV enabling, integrated or virtual technology over Sunrise’s broadband network or through a partner network. Enhanced TV Subscribers exclude subscribers that receive BCS. Residential 892’585 882’635 882’635 870’668 867’576 867’576 859’598 2 Business 91’226 93’660 93’660 94’556 96’484 96’484 96’970 A Mobile RGU is a Mobile Subscriber, which represents an active SIM card in service. A subscriber Mobile RGUs who has a data and voice plan for a mobile handset and a data plan for a laptop would be counted as two Mobile Subscribers. Residential 2’348’854 2’349’000 2’349’000 2’336’901 2’339’425 2’339’425 2’336’642 3 Business 784’158 797’167 797’167 812’724 819’580 819’580 825’478 Mobile Postpaid RGUs Numbers of Mobile products (Postpaid) Residential 2’076’312 2’081’252 2’081’252 2’084’589 2’106’223 2’106’223 2’109’805 3 Business 741’262 754’703 754’703 771’771 781’616 781’616 788’497 (1) A Fixed RGU is, separately, an Internet Subscriber or an Enhanced TV Subscriber. A home, residential multiple dwelling unit or commercial unit may contain one or more RGUs. For example, if a residential customer subscribed to Sunrise’s broadband internet service or enhanced TV service, the customer would constitute two RGUs. RGUs generally are counted on a unique premises basis such that a given premise does not count as more than one RGU for any given service. However, if an individual receives one of Sunrise’s services in two premises (e.g., a primary home and a vacation home), that individual will count as two RGUs for that service. Each bundled internet or enhanced TV service is counted as a separate RGU regardless of the nature of any bundling discount or promotion. Non-paying subscribers are counted as subscribers during their free promotional service period. Some of these subscribers may choose to disconnect after their free service period. Services offered without charge on a long-term basis (e.g., certain preferred subscribers) generally are not counted as RGUs. Free services provided to Sunrise employees generally are counted as RGUs. (2) Business-customer and wholesale fixed relationships and fixed RGUs include customers who receive fixed services that are the same or similar to mass-marketed products offered to residential customers. This includes customers who receive discounted services pursuant to a programme Sunrise has in place with their employer and small business customers (generally defined as businesses with 9 or fewer employees) and does not include services provided to small-medium business customers (generally defined as businesses with 10 to 249 employees) and large enterprises (generally defined as businesses with 250 or more employees) or wholesale services. (3) Business customer and wholesale Mobile RGUs represent the number of active SIM cards in service that are provided to business and wholesale customers, including customers who receive discounted services pursuant to a program Sunrise has in place with their employer, SOHO, SME and large enterprise customers, as well as to customers who subscribed for mobile services delivered over Sunrise’s networks through a branded reseller with whom Sunrise contracts, and excluding customers who subscribed for mobile services delivered over Sunrise’s networks through a MVNO with whom Sunrise contracts, as well as other wholesale customers. Q1 2026 Results | 13 May 2026 26

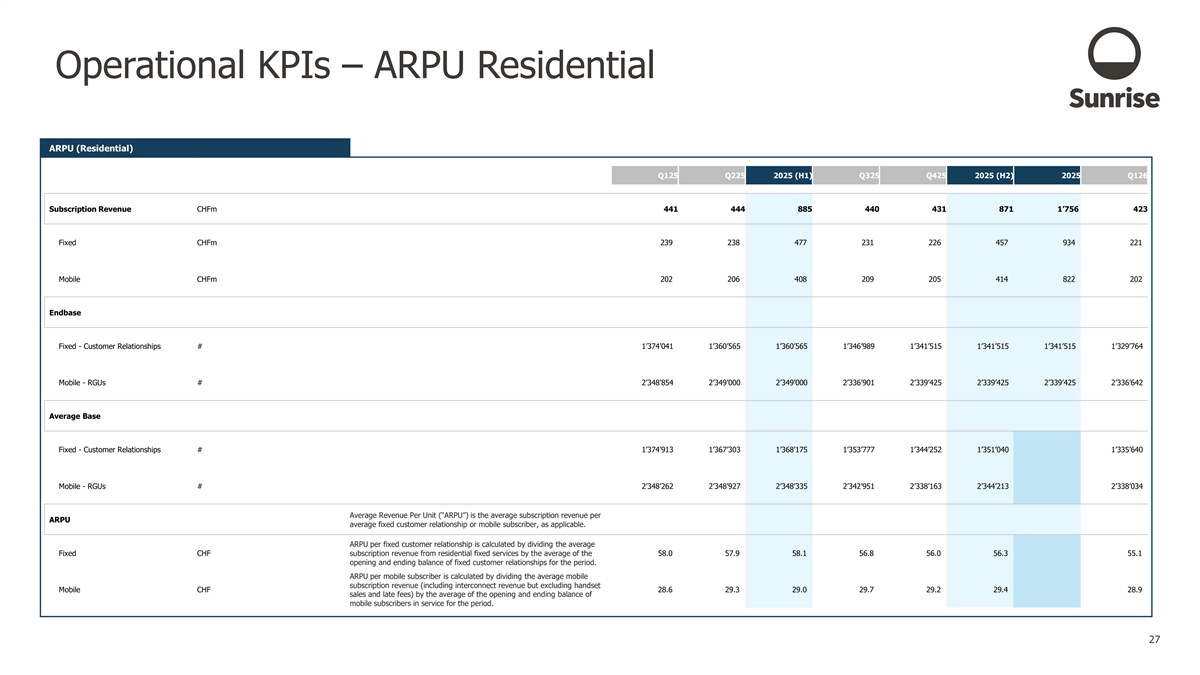

Operational KPIs – ARPU Residential ARPU (Residential) Q125 Q225 2025 (H1) Q325 Q425 2025 (H2) 2025 Q126 Subscription Revenue CHFm 441 444 885 440 431 871 1’756 423 Fixed CHFm 239 238 477 231 226 457 934 221 Mobile CHFm 202 206 408 209 205 414 822 202 Endbase Fixed - Customer Relationships # 1’374’041 1’360’565 1’360’565 1’346’989 1’341’515 1’341’515 1’341’515 1’329’764 Mobile - RGUs # 2’348’854 2’349’000 2’349’000 2’336’901 2’339’425 2’339’425 2’339’425 2’336’642 Average Base Fixed - Customer Relationships # 1’374’913 1’367’303 1’368’175 1’353’777 1’344’252 1’351’040 1’335’640 Mobile - RGUs # 2’348’262 2’348’927 2’348’335 2’342’951 2’338’163 2’344’213 2’338’034 Average Revenue Per Unit (“ARPU”) is the average subscription revenue per ARPU average fixed customer relationship or mobile subscriber, as applicable. ARPU per fixed customer relationship is calculated by dividing the average Fixed CHF subscription revenue from residential fixed services by the average of the 58.0 57.9 58.1 56.8 56.0 56.3 55.1 opening and ending balance of fixed customer relationships for the period. ARPU per mobile subscriber is calculated by dividing the average mobile subscription revenue (including interconnect revenue but excluding handset Mobile CHF 28.6 29.3 29.0 29.7 29.2 29.4 28.9 sales and late fees) by the average of the opening and ending balance of mobile subscribers in service for the period. Q1 2026 Results | 13 May 2026 27

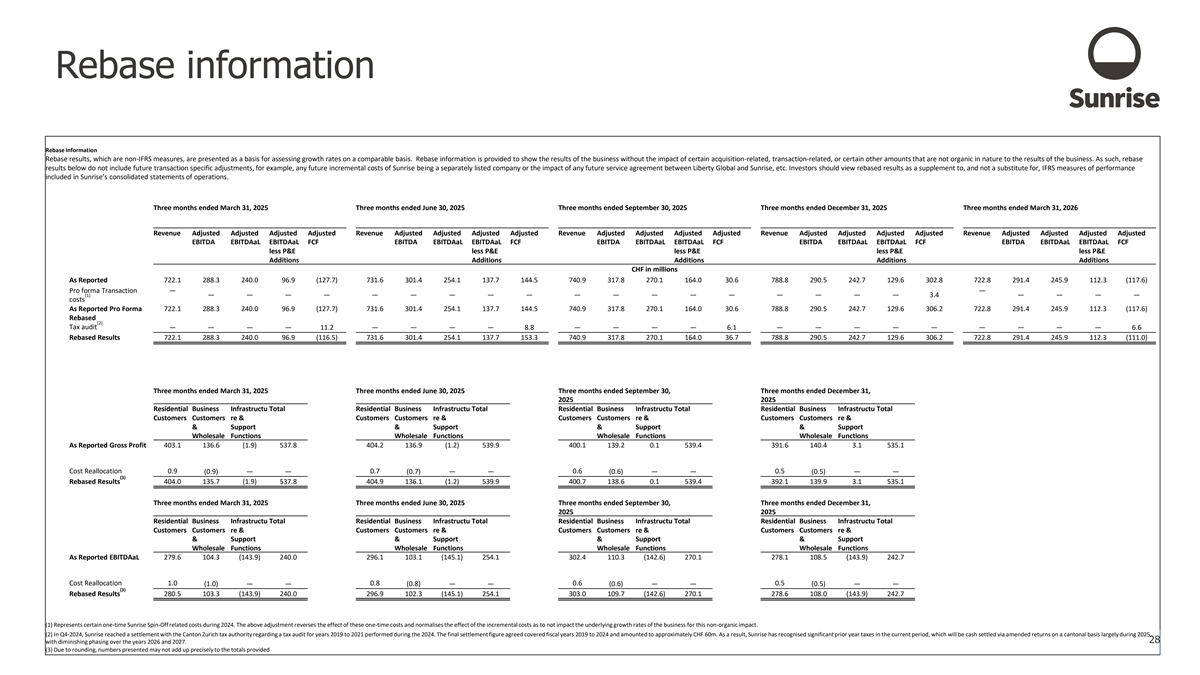

Rebase information Rebase Information Rebase results, which are non-IFRS measures, are presented as a basis for assessing growth rates on a comparable basis. Rebase information is provided to show the results of the business without the impact of certain acquisition-related, transaction-related, or certain other amounts that are not organic in nature to the results of the business. As such, rebase results below do not include future transaction specific adjustments, for example, any future incremental costs of Sunrise being a separately listed company or the impact of any future service agreement between Liberty Global and Sunrise, etc. Investors should view rebased results as a supplement to, and not a substitute for, IFRS measures of performance included in Sunrise’s consolidated statements of operations. Three months ended March 31, 2025 Three months ended June 30, 2025 Three months ended September 30, 2025 Three months ended December 31, 2025 Three months ended March 31, 2026 Revenue Adjusted Adjusted Adjusted Adjusted Revenue Adjusted Adjusted Adjusted Adjusted Revenue Adjusted Adjusted Adjusted Adjusted Revenue Adjusted Adjusted Adjusted Adjusted Revenue Adjusted Adjusted Adjusted Adjusted EBITDA EBITDAaL EBITDAaL FCF EBITDA EBITDAaL EBITDAaL FCF EBITDA EBITDAaL EBITDAaL FCF EBITDA EBITDAaL EBITDAaL FCF EBITDA EBITDAaL EBITDAaL FCF less P&E less P&E less P&E less P&E less P&E Additions Additions Additions Additions Additions CHF in millions As Reported 722.1 288.3 240.0 96.9 (127.7) 731.6 301.4 254.1 137.7 144.5 740.9 317.8 270.1 164.0 30.6 788.8 290.5 242.7 129.6 302.8 722.8 291.4 245.9 112.3 (117.6) Pro forma Transaction — — (1) — — — — — — — — — — — — — — — — — — 3.4 — — — — costs As Reported Pro Forma 722.1 288.3 240.0 96.9 (127.7) 731.6 301.4 254.1 137.7 144.5 740.9 317.8 270.1 164.0 30.6 788.8 290.5 242.7 129.6 306.2 722.8 291.4 245.9 112.3 (117.6) Rebased (2) Tax audit — — — — 11.2 — — — — 8.8 — — — — 6.1 — — — — — — — — — 6.6 Rebased Results 722.1 288.3 240.0 96.9 (116.5) 731.6 301.4 254.1 137.7 153.3 740.9 317.8 270.1 164.0 36.7 788.8 290.5 242.7 129.6 306.2 722.8 291.4 245.9 112.3 (111.0) Three months ended March 31, 2025 Three months ended June 30, 2025 Three months ended September 30, Three months ended December 31, 2025 2025 Residential Business Infrastructu Total Residential Business Infrastructu Total Residential Business Infrastructu Total Residential Business Infrastructu Total Customers Customers re & Customers Customers re & Customers Customers re & Customers Customers re & & Support & Support & Support & Support Wholesale Functions Wholesale Functions Wholesale Functions Wholesale Functions As Reported Gross Profit 403.1 136.6 (1.9) 537.8 404.2 136.9 (1.2) 539.9 400.1 139.2 0.1 539.4 391.6 140.4 3.1 535.1 Cost Reallocation 0.9 (0.9) — — 0.7 (0.7) — — 0.6 (0.6) — — 0.5 (0.5) — — (3) Rebased Results 404.0 135.7 (1.9) 537.8 404.9 136.1 (1.2) 539.9 400.7 138.6 0.1 539.4 392.1 139.9 3.1 535.1 Three months ended March 31, 2025 Three months ended June 30, 2025 Three months ended September 30, Three months ended December 31, 2025 2025 Residential Business Infrastructu Total Residential Business Infrastructu Total Residential Business Infrastructu Total Residential Business Infrastructu Total Customers Customers re & Customers Customers re & Customers Customers re & Customers Customers re & & Support & Support & Support & Support Wholesale Functions Wholesale Functions Wholesale Functions Wholesale Functions As Reported EBITDAaL 279.6 104.3 (143.9) 240.0 296.1 103.1 (145.1) 254.1 302.4 110.3 (142.6) 270.1 278.1 108.5 (143.9) 242.7 Cost Reallocation 1.0 (1.0) — — 0.8 (0.8) — — 0.6 (0.6) — — 0.5 (0.5) — — (3) Rebased Results 280.5 103.3 (143.9) 240.0 296.9 102.3 (145.1) 254.1 303.0 109.7 (142.6) 270.1 278.6 108.0 (143.9) 242.7 (1) Represents certain one-time Sunrise Spin-Off related costs during 2024. The above adjustment reverses the effect of these one-time costs and normalises the effect of the incremental costs as to not impact the underlying growth rates of the business for this non-organic impact. (2) In Q4-2024, Sunrise reached a settlement with the Canton Zurich tax authority regarding a tax audit for years 2019 to 2021 performed during the 2024. The final settlement figure agreed covered fiscal years 2019 to 2024 and amounted to approximately CHF 60m. As a result, Sunrise has recognised significant prior year taxes in the current period, which will be cash settled via amended returns on a cantonal basis largely during 2025, Q wi 1 th 2 di0 m2 ini6 shi R nge pha su sing lts over | the 13 year Msay 202 62 an 0d 2 26 027. 28 (3) Due to rounding, numbers presented may not add up precisely to the totals provided

Non-IFRS Reconciliations Three months ended Three months ended 31-Mar-26 31-Mar-25 30-Jun-25 30-Sept-25 31-Dec-25 CHF in millions CHF in millions Adjusted EBITDA and Adjusted EBITDAaL: Net income (loss) (39.4) (1.3) (53.6) (4.4) (49.2) Income tax expense (benefit) (10.7) 3.8 (15.8) (1.6) (6.3) Share of gains of equity method investments (2.0) (1.1) (3.0) (0.5) (1.3) Net financial expense (income) 65.5 11.3 97.6 52.4 69.2 Operating income (loss) 13.4 12.7 25.2 45.9 12.4 Depreciation and amortisation (non-lease related) 214.0 233.4 222.8 223.4 256.8 Depreciation of right-of-use assets 30.7 32.9 32.1 32.4 32.5 Share-based compensation expense 5.8 7.3 16.2 15.9 9.6 Restructuring & other 27.5 2.0 5.1 0.2 (20.8) Adjusted EBITDA 291.4 288.3 301.4 317.8 290.5 Lease-related expenses (45.5) (48.3) (47.3) (47.7) (47.8) Adjusted EBITDAaL 245.9 240.0 254.1 270.1 242.7 Three months ended Three months ended 31-Mar-26 31-Mar-25 30-Jun-25 30-Sept-25 31-Dec-25 CHF in millions CHF in millions Adjusted EBITDAaL less P&E Additions (CAPEX): Adjusted EBITDAaL 245.9 240.0 254.1 270.1 242.7 P&E Additions (CAPEX): 133.6 143.1 116.4 106.1 113.1 Adjusted EBITDAaL less P&E Additions (CAPEX) 112.3 96.9 137.7 164.0 129.6 Three months ended Three months ended 31-Mar-26 31-Mar-25 30-Jun-25 30-Sept-25 31-Dec-25 CHF in millions CHF in millions Adjusted Free Cash Flow: Net cash provided by operating activities 99.8 171.1 290.5 292.1 461.5 Interest paid (124.8) (103.0) (32.9) (104.7) (20.7) Interest-related derivative receipts (payments) 30.7 (10.2) 15.6 39.2 (2.7) Vendor financing additions (i) 86.2 90.8 97.6 115.3 102.0 Capital expenditures (82.8) (108.0) (165.9) (95.0) (130.6) Principal payments on vendor financing (87.5) (133.0) (41.2) (170.6) (85.9) Payments of lease liabilities (39.2) (35.3) (19.4) (45.6) (20.7) Adjusted Free Cash Flow (117.6) (127.7) 144.5 30.6 302.8 Three months ended Three months ended 31-Mar-26 31-Mar-25 30-Jun-25 30-Sept-25 31-Dec-25 CHF in millions CHF in millions P&E Additions (CAPEX): Capital expenditures 82.8 108.0 165.9 95.0 130.6 Mergers and acquisitions (asset deals) — — (3.0) (2.8) (4.4) Recognition of sports broadcasting rights — — — (218.7) — Assets acquired under vendor financing 55.3 15.4 16.5 16.4 9.2 Changes in current liabilities related to capital expenditures (including related-party amounts) (4.5) 19.7 (63.0) 216.2 (22.3) P&E Additions (CAPEX) 133.6 143.1 116.4 106.1 113.1 (i) For purposes of Sunrise’s consolidated statements of cash flows, vendor financing additions represent operating related expenses financed by an intermediary that are treated as constructive operating cash outflows and constructive financing cash inflows when the intermediary settles the liability with the vendor. When Sunrise pays the financing intermediary, it records financing cash outflows in its consolidated statements of cash flows. For purposes of its Adjusted Free Cash Flow definition, Sunrise (A) adds in the constructive financing cash inflow when the intermediary settles the liability with the vendor as its actual net cash available at that time is not affected and (B) subsequently deducts the related financing cash outflow when Sunrise actually pays the financing intermediary, reflecting the actual reduction to its cash available to service debt or fund new investment opportunities. Q1 2026 Results | 13 May 2026 29

Contact Information Investor Relations Sunrise investor.relations@sunrise.net Thurgauerstrasse 101B +41 58 777 61 00 8152 Glattpark (Opfikon) Switzerland Q1 2026 Results | 13 May 2026