Exhibit 99.2

| CONTACT | ||

| DR. REDDY'S LABORATORIES LTD. | Investor relationS | Media relationS |

|

8-2-337, Road No. 3, Banjara Hills, Hyderabad - 500034. Telangana, India. |

AISHWARYA SITHARAM aishwaryasitharam@drreddys.com |

PRIYA K priyak@drreddys.com |

Dr. Reddy’s Q4 & Full Year FY26 Financial Results

Hyderabad, India, May 12, 2026: Dr. Reddy’s Laboratories Ltd. (BSE: 500124 | NSE: DRREDDY | NYSE: RDY | NSEIFSC: DRREDDY) today announced its consolidated financial results for the quarter and year ended March 31, 2026. The information mentioned in this release is based on consolidated financial statements under International Financial Reporting Standards (IFRS).

| Particulars | Q4FY26 | FY26 |

Revenues1

|

₹ 75,162 Mn [Down: 11.6% YoY; 13.9% QoQ] |

₹ 335,933 Mn [Up: 3.2% YoY] |

Gross Margin2

|

44.8% [Q4FY25: 55.6%; Q3FY26: 53.6%] |

52.8% [FY25: 58.5%] |

EBITDA3

|

₹ 9,807 Mn [13.0% of Revenues] |

₹ 76,595 Mn [22.8% of Revenues] |

Profit before Tax4

|

₹ 1,991 Mn [2.6% of Revenues] |

₹ 54,817 Mn [16.3% of Revenues] |

Profit after Tax attributable to Equity Holders |

₹ 2,201 Mn [2.9% of Revenues] |

₹ 42,850 Mn [12.8% of Revenues] |

Notes: The results include the adverse impact of a Shelf Stock Adjustment (‘SSA’) related to lenalidomide of ₹ 4,530 Mn, impairment of CAR-T assets and Eftilagimod Alfa of a total of ₹2,277 Mn, provisions related to VAT liability of ₹1,141 Mn in Q4FY26. In addition to the above, FY26 includes adverse impact of VAT liability provision of ₹695 Mn and New Labour Codes of ₹ 1,170 Mn. The above items impacted :

| · | Revenue growth by 5.3% YoY and 5.2% QoQ in Q4FY26 and 1.4% in FY26. |

| · | Gross Margin by 3.2% in Q4FY26 and 0.7% in FY26. |

| · | EBITDA Margin by 6.5% in Q4FY26 and 1.9% in FY26. |

| · | PBT Margin by 9.9% in Q4FY26 and 2.7% in FY26. |

Commenting on the results, Co-Chairman & MD, G V Prasad said: “Our performance this year reflects the impact of lower lenalidomide sales and several one-offs. The resilience of our branded businesses and currency tailwinds helped partially mitigate this impact. We remain focused on strengthening our base business and improving margins, through cost efficiencies and portfolio optimization. In parallel, we continue to build long-term franchises in biosimilars, consumer health and innovation to deliver sustainable value.”

| 1 |

| All amounts in millions, except EPS | All US dollar amounts based on convenience translation rate of 1 USD = ₹93.83 |

Dr. Reddy’s Laboratories Limited & Subsidiaries

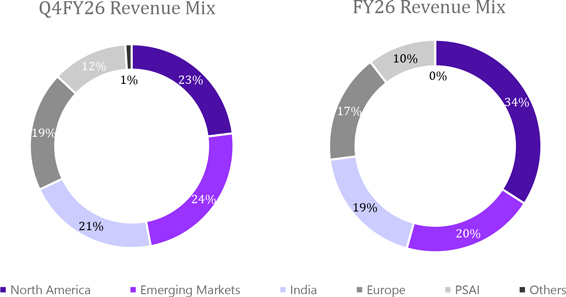

Revenue Mix by Segment for the quarter

| Particulars | Q4FY26 | Q4FY25 | YoY | Q3FY26 | QoQ | |||||||||||||||

| (₹) | (₹) | Gr % | (₹) | Gr % | ||||||||||||||||

| Global Generics | 65,802 | 75,365 | (13 | ) | 79,113 | (17 | ) | |||||||||||||

| North America | 17,562 | 35,586 | (51 | ) | 29,644 | (41 | ) | |||||||||||||

| Emerging Markets | 18,057 | 13,981 | 29 | 18,961 | (5 | ) | ||||||||||||||

| India | 15,663 | 13,047 | 20 | 16,032 | (2 | ) | ||||||||||||||

| Europe | 14,520 | 12,750 | 14 | 14,476 | 0.3 | |||||||||||||||

| Pharmaceutical Services and Active Ingredients (PSAI) | 9,124 | 9,563 | (5 | ) | 8,018 | 14 | ||||||||||||||

| Others | 236 | 132 | 79 | 137 | 73 | |||||||||||||||

| Total | 75,162 | 85,060 | (12 | ) | 87,268 | (14 | ) | |||||||||||||

Revenue Mix by Segment for the year

| Particulars | FY26 | FY25 | YoY | |||||||||

| (₹) | (₹) | Gr% | ||||||||||

| Global Generics | 299,033 | 289,552 | 3 | |||||||||

| North America | 113,737 | 1,45,164 | (22 | ) | ||||||||

| Emerging Markets | 67,608 | 54,772 | 23 | |||||||||

| India | 62,186 | 53,734 | 16 | |||||||||

| Europe | 55,501 | 35,882 | 55^ | |||||||||

| PSAI | 34,774 | 33,846 | 3 | |||||||||

| Others | 2,127 | 2,137 | (0 | ) | ||||||||

| Total | 335,933 | 325,535 | 3 | |||||||||

^Excluding acquired Consumer Healthcare business in Nicotine Replacement Therapy (NRT) sales; revenue growth is at 14% YoY.

| 2 |

Consolidated Income Statement for the quarter

| Particulars | Q4FY26 | Q4FY25 | YoY | Q3FY26 | QoQ | |||||||||||||||||||||||||||

| ($) | (₹) | ($) | (₹) | Gr% | ($) | (₹) | Gr% | |||||||||||||||||||||||||

| Revenues | 801 | 75,162 | 907 | 85,060 | (12) | 930 | 87,268 | (14) | ||||||||||||||||||||||||

| Cost of Revenues | 442 | 41,471 | 403 | 37,797 | 10 | 431 | 40,462 | 2 | ||||||||||||||||||||||||

| Gross Profit | 359 | 33,691 | 504 | 47,263 | (29 | ) | 499 | 46,806 | (28 | ) | ||||||||||||||||||||||

| % of Revenues | 44.8 | % | 55.6 | % | 53.6 | % | ||||||||||||||||||||||||||

| Selling, General & Administrative Expenses | 296 | 27,762 | 256 | 24,055 | 15 | 287 | 26,918 | 3 | ||||||||||||||||||||||||

| % of Revenues | 36.9 | % | 28.3 | % | 30.8 | % | ||||||||||||||||||||||||||

| Research & Development Expenses | 58 | 5,463 | 77 | 7,258 | (25 | ) | 66 | 6,149 | (11 | ) | ||||||||||||||||||||||

| % of Revenues | 7.3 | % | 8.5 | % | 7.0 | % | ||||||||||||||||||||||||||

| Impairment of Non-Current Assets, net | 28 | 2,586 | 8 | 768 | 237 | 3 | 271 | 854 | ||||||||||||||||||||||||

| Other (Income)/Expense, net | (37 | ) | (3,445 | ) | (26 | ) | (2,465 | ) | 40 | (8 | ) | (770 | ) | 347 | ||||||||||||||||||

| Results from Operating Activities | 14 | 1,325 | 188 | 17,647 | (92 | ) | 152 | 14,238 | (91 | ) | ||||||||||||||||||||||

| Finance (Income)/Expense, net | (7 | ) | (620 | ) | (25 | ) | (2,352 | ) | (74 | ) | (12 | ) | (1,168 | ) | (47 | ) | ||||||||||||||||

| Share of Profit of Equity Investees, net of tax | (0 | ) | (46 | ) | (1 | ) | (55 | ) | (16 | ) | (0 | ) | (23 | ) | 100 | |||||||||||||||||

| Profit before Income Tax | 21 | 1,991 | 214 | 20,054 | (90 | ) | 164 | 15,429 | (87 | ) | ||||||||||||||||||||||

| % of Revenues | 2.6 | % | 23.6 | % | 17.7 | % | ||||||||||||||||||||||||||

| Income Tax Expense/(Benefit) | (2 | ) | (214 | ) | 45 | 4,181 | (105 | ) | 38 | 3,533 | (106 | ) | ||||||||||||||||||||

| Profit for the Period | 23 | 2,205 | 169 | 15,873 | (86 | ) | 127 | 11,896 | (81 | ) | ||||||||||||||||||||||

| % of Revenues | 2.9 | % | 18.7 | % | 13.6 | % | ||||||||||||||||||||||||||

| Attributable to Equity holders of the Parent Co. | 23 | 2,201 | 170 | 15,939 | (86 | ) | 128 | 12,098 | (82 | ) | ||||||||||||||||||||||

| % of Revenues | 2.9 | % | 18.7 | % | 13.9 | % | ||||||||||||||||||||||||||

| Attributable to Non-controlling interests | 0.04 | 3 | (1 | ) | (66 | ) | (105 | ) | (1 | ) | (202 | ) | (102 | ) | ||||||||||||||||||

| Diluted Earnings per Share (EPS) | 0.03 | 2.64 | 0.18 | 16.94 | (84 | ) | 0.15 | 14.51 | (82 | ) | ||||||||||||||||||||||

Earnings before Interest, Tax, Depreciation & Amortization (EBITDA) Computation for the quarter

| Particulars | Q4FY26 | Q4FY25 | Q3FY26 | |||||||||||||||||||||

| ($) | (₹) | ($) | (₹) | ($) | (₹) | |||||||||||||||||||

| Profit before Income Tax | 21 | 1,991 | 214 | 20,054 | 164 | 15,429 | ||||||||||||||||||

| Interest (Income) / Expense, net* | (4 | ) | (346 | ) | (7 | ) | (627 | ) | (4 | ) | (422 | ) | ||||||||||||

| Depreciation | 37 | 3,459 | 28 | 2,636 | 34 | 3,178 | ||||||||||||||||||

| Amortization | 23 | 2,117 | 20 | 1,919 | 22 | 2,037 | ||||||||||||||||||

| Impairment | 28 | 2,586 | 8 | 768 | 3 | 271 | ||||||||||||||||||

| EBITDA | 105 | 9,807 | 264 | 24,749 | 218 | 20,493 | ||||||||||||||||||

| % of Revenues | 13.0 | % | 29.1 | % | 23.5 | % | ||||||||||||||||||

*Includes income from Investment

| 3 |

Consolidated Income Statement for the year

| Particulars | FY26 | FY25 | YoY | |||||||||||||||||

| ($) | (₹) | ($) | (₹) | Gr% | ||||||||||||||||

| Revenues | 3,580 | 335,933 | 3,469 | 325,535 | 3 | |||||||||||||||

| Cost of Revenues | 1,691 | 158,669 | 1,440 | 135,107 | 17 | |||||||||||||||

| Gross Profit | 1,889 | 177,264 | 2,030 | 190,428 | (7 | ) | ||||||||||||||

| % of Revenues | 52.8 | % | 58.5 | % | ||||||||||||||||

| Selling, General & Administrative Expenses | 1,138 | 106,763 | 1,000 | 93,870 | 14 | |||||||||||||||

| % of Revenues | 31.8 | % | 28.8 | % | ||||||||||||||||

| Research & Development Expenses | 256 | 24,058 | 292 | 27,380 | (12 | ) | ||||||||||||||

| % of Revenues | 7.2 | % | 8.4 | % | ||||||||||||||||

| Impairment of Non-Current Assets, net | 38 | 3,519 | 18 | 1,693 | 108 | |||||||||||||||

| Other (Income)/Expense, net | (81 | ) | (7,627 | ) | (46 | ) | (4,358 | ) | 75 | |||||||||||

| Results from Operating Activities | 539 | 50,551 | 766 | 71,843 | (30 | ) | ||||||||||||||

| Finance (Income)/Expense, net | (44 | ) | (4,132 | ) | (50 | ) | (4,724 | ) | (13 | ) | ||||||||||

| Share of Profit of Equity Investees, net of tax | (1 | ) | (134 | ) | (2 | ) | (217 | ) | (38 | ) | ||||||||||

| Profit before Income Tax | 584 | 54,817 | 818 | 76,784 | (29 | ) | ||||||||||||||

| % of Revenues | 16.3 | % | 23.6 | % | ||||||||||||||||

| Income Tax Expense | 132 | 12,351 | 208 | 19,539 | (37 | ) | ||||||||||||||

| Profit for the Period | 453 | 42,466 | 610 | 57,245 | (26 | ) | ||||||||||||||

| % of Revenues | 12.6 | % | 17.6 | % | ||||||||||||||||

| Attributable to Equity holders of the Parent Co. | 457 | 42,850 | 603 | 56,544 | (24 | ) | ||||||||||||||

| % of Revenues | 12.8 | % | 17.4 | % | ||||||||||||||||

| Attributable to Non-controlling interests | (4 | ) | (384 | ) | 7 | 701 | (155 | ) | ||||||||||||

| Diluted Earnings per Share (EPS) | 0.55 | 51.42 | 0.72 | 67.78 | (24 | ) | ||||||||||||||

EBITDA Computation for the year

| Particulars | FY26 | FY25 | ||||||||||||||

| ($) | (₹) | ($) | (₹) | |||||||||||||

| Profit before Income Tax | 584 | 54,817 | 818 | 76,784 | ||||||||||||

| Interest (Income) / Expense, net* | (25 | ) | (2,347 | ) | (36 | ) | (3,402 | ) | ||||||||

| Depreciation | 135 | 12,621 | 112 | 10,505 | ||||||||||||

| Amortization | 85 | 7,985 | 70 | 6,553 | ||||||||||||

| Impairment | 38 | 3,520 | 18 | 1,693 | ||||||||||||

| EBITDA | 816 | 76,595 | 982 | 92,133 | ||||||||||||

| % of Revenues | 22.8 | % | 28.3 | % | ||||||||||||

*Includes income from Investment

Key Balance Sheet Items

| Particulars | As on 31st Mar 2026 | As on 31st Dec 2025 | As on 31st Mar 2025 | |||||||||||||||||||||

| ($) | (₹) | ($) | (₹) | ($) | (₹) | |||||||||||||||||||

| Cash and Cash Equivalents and Other Investments | 1,050 | 98,509 | 929 | 87,191 | 728 | 68,299 | ||||||||||||||||||

| Trade Receivables | 1,079 | 101,219 | 1,100 | 103,206 | 964 | 90,420 | ||||||||||||||||||

| Inventories | 816 | 76,531 | 842 | 79,009 | 758 | 71,085 | ||||||||||||||||||

| Property, Plant, and Equipment | 1,236 | 115,930 | 1,231 | 115,544 | 1,042 | 97,761 | ||||||||||||||||||

| Goodwill and Other Intangible Assets | 1,257 | 117,952 | 1,223 | 114,727 | 1,158 | 108,613 | ||||||||||||||||||

| Loans and Borrowings (Current & Non-Current) | 824 | 77,341 | 722 | 67,732 | 498 | 46,766 | ||||||||||||||||||

| Trade Payables | 356 | 33,411 | 435 | 40,796 | 379 | 35,523 | ||||||||||||||||||

| Equity | 4,055 | 380,457 | 4,005 | 375,756 | 3,593 | 337,166 | ||||||||||||||||||

| 4 |

Key Business Highlights for Q4FY26

| · | Received the Notice of Compliance from Pharmaceutical Drugs Directorate for generic Semaglutide injection in Canada, indicated for treatment of Type 2 diabetes. |

| · | Launched generic Semaglutide Injection in India for treatment of Type 2 diabetes, under the brand name ‘Obeda®‘ on Day 1 of market formation post loss of exclusivity. |

| · | Received marketing authorization for generic Semaglutide tablets in India for treatment of Type 2 diabetes from Drugs Controller General of India (DCGI), following the recommendation of Subject Expert Committee (SEC) under Central Drugs Standard Control Organization (CDSCO). |

| · | Forayed into Hormone Replacement Therapy in India with acquisition of Progynova® and related assets. |

| · | Acceptance for review by United States Food and Drug Administration (USFDA) of the Biologics License Application (BLA) for the Intravenous (IV) presentation of our abatacept biosimilar in the US. |

| · | Integration of 95% of acquired Consumer Healthcare business in Nicotine Replacement Therapy (NRT) business by value completed as of March 2026. |

| · | First-to-market launch of Olopatadine Hydrochloride Ophthalmic Solution USP, 0.7% (OTC) in the US. |

| · | Launched Tegoprazan in Russia, following a successful launch in India. |

ESG Highlights for Q4FY26

| · | Named by BusinessWorld among India’s Top 5 Most Sustainable Companies, ranking first in the Indian healthcare and pharmaceutical industry for 2024-25. |

| · | Recognized in the ‘Leadership Category’ of the 2025 Indian Corporate Governance Scorecard for the third consecutive year, jointly by Institutional Investor Advisory Services (IiAS), the International Finance Corporation (IFC) and the Bombay Stock Exchange (BSE). |

Other Updates for Q4FY26

| · | Received ‘VAI’ classification, following a GMP and a PAI conducted by the USFDA in December 2025 at formulations manufacturing facility, FTO-SEZ PU01, in Srikakulam, Andhra Pradesh, India. |

| · | Divested two non-core brands in India. |

| · | Discontinuation of trial of licensed novel drug candidate, Eftilagimod alfa, by partner, Immutep, following a planned interim futility analysis. |

| · | Discontinuation of certain R&D programs in CAR-T therapy, as part of portfolio rationalization. |

| · | The Board has recommended a dividend payment of Rs. 8 per equity share of face value Re. 1/- each (800% of face value) for year ended March 31, 2026, subject to shareholder approval. |

| 5 |

Revenue Analysis

| · | Q4FY26 consolidated revenues at ₹75.2 billion, decline of 11.6% YoY and 13.9% QoQ. |

FY26 consolidated revenues at ₹335.9 billion, growth of 3.2% YoY.

Growth was broad-based across key markets, except for North America which declined primarily on account of lower Lenalidomide sales and a one-time Shelf Stock Adjustment (SSA) of ₹4.5 billion related to the product. Favourable foreign exchange rate movements further supported overall growth.

Excluding the one-time SSA, consolidated revenues were at ₹79.7 billion in Q4FY26, a decline of 6.3% YoY and 8.7% QoQ and ₹340.5 billion in FY26, a growth of 4.6% YoY.

Global Generics (GG)

| · | Q4FY26 revenues at ₹65.8 billion, decline of 13% YoY and 17% QoQ. |

FY26 revenues at ₹299.0 billion, growth of 3% YoY.

Excluding the one-time SSA mentioned above, revenues for the segment posted a decline of 7% YoY and 11% QoQ in Q4FY26 and a growth of 4.8% YoY in FY26.

North America

| · | Q4FY26 revenues at ₹17.6 billion, decline of 51% YoY and 41% QoQ. |

FY26 revenues at ₹113.7 billion, decline of 22% YoY.

Decline was largely due to lower Lenalidomide sales and the one-time SSA mentioned above.

Excluding this one-off, revenues for the segment posted a decline of 38% YoY and 25% QoQ in Q4FY26 and 19% YoY in FY26.

| · | During the quarter, we launched seven new products, while a total of 25 new products were launched during FY26. |

| · | We filed five new Abbreviated New Drug Applications (ANDAs) with the USFDA during the quarter, taking the total to 15 for FY26. |

| · | As of March 31, 2026, filings pending approval from USFDA were 77 including: |

| - | 75 ANDAs (43 are Paragraph IV applications, and 22 may have a ‘First to File’ status) and |

| - | Two New Drug Applications (NDAs) filed u/s 505(b)(2), of which one is a Paragraph IV application. |

Emerging Markets

| · | Q4FY26 revenues at ₹18.1 billion, growth of 29% YoY and a decline of 5% QoQ. |

FY26 revenues at ₹67.6 billion, growth of 23% YoY.

YoY growth was largely driven by new launches across markets and higher volumes, further supported by favourable forex. QoQ decline was primarily on account of lower volume uptake in Russia.

| - | Q4FY26 Russia revenues at ₹8.4 billion, growth of 28% YoY and decline of 21% QoQ. |

FY26 Russia revenues at ₹34.8 billion, growth of 34% YoY.

In Q4FY26, YoY growth was supported by new launches, price increase in certain brands and favorable foreign exchange movements, while QoQ decline was primarily on account of lower sales volumes.

| - | Q4FY26 Other Commonwealth of Independent States (CIS) countries and Romania revenues at ₹2.3 billion, decline of 4% YoY and QoQ. |

| 6 |

FY26 CIS and Romania revenues at ₹9.1 billion, growth of 2% YoY.

In Q4FY26, decline was largely on account of weaker volumes, with sequential performance further impacted by lower prices in certain products.

| - | Q4FY26 Rest of World (RoW) revenues at ₹7.3 billion, growth of 47% YoY and 23% QoQ. |

FY26 RoW revenues at ₹23.7 billion, growth of 19% YoY.

Growth was largely on account of higher sales volumes from existing products across countries.

| · | During Q4FY26, we launched 49 new products across countries, taking the total to 129 for FY26. |

India

| · | Q4FY26 revenues at ₹15.7 billion, growth of 20% YoY and decline of 2% QoQ. |

FY26 revenues at ₹62.2 billion, growth of 16% YoY.

Growth was driven by revenues from new brand launches, including our innovation portfolio, price increases, higher volumes and contributions from recently acquired portfolios.

| · | As per IQVIA data published for March 2026, our rank in the Indian Pharmaceutical Market (IPM) was at 9th on a Moving Quarterly Total (MQT) and 10th on a Moving Annual Total (MAT) basis. We continued to outperform the IPM, with secondary sales growth of 15.2% as compared to IPM growth of 11.6% on a MQT basis and 12.1% as compared to IPM growth of 9.9% on a MAT basis. |

| · | During the quarter, we launched ten new brands, taking the total to 28 for FY26. |

Europe

| · | Q4FY26 revenues at ₹14.5 billion, growth of 14% YoY and flat QoQ. |

FY26 revenues at ₹55.5 billion, growth of 55% YoY. Excluding NRT, growth was at 14% YoY.

Contributions from the NRT portfolio, revenues from new generic product launches, higher volumes and favourable forex movement were moderated by pricing pressure in generics.

| - | Q4FY26 NRT revenues at ₹7.0 billion, growth of 16% YoY and decline of 8% QoQ. |

FY26 NRT revenues at ₹28.2 billion, versus ₹12.0 billion in FY25 for the period following its acquisition.

| - | Q4FY26 Germany revenues at ₹3.8 billion, growth of 8% YoY and decline of 5% QoQ. |

FY26 Germany revenues at ₹15.0 billion, growth of 16% YoY.

| - | Q4FY26 UK revenues at ₹2.3 billion, growth of 6% YoY and 38% QoQ. |

FY26 UK revenues at ₹7.3 billion, flat YoY.

| - | Q4FY26 Rest of Europe revenues at ₹1.4 billion, growth of 35% YoY and 15% QoQ. |

FY26 Rest of Europe revenues at ₹5.1 billion, growth of 37% YoY.

| · | During the quarter, we launched seven new products in the region, taking the total to 38 for FY26. |

Pharmaceutical Services and Active Ingredients (PSAI)

| · | Q4FY26 revenues at ₹9.1 billion, decline of 5% YoY and growth of 14% QoQ. |

FY26 revenues at ₹34.7 billion, growth of 3% YoY.

Decline in Q4FY26 was on account of lower volume uptake in the API business.

| · | During the quarter, we filed 48 Drug Master Files (DMFs) globally, taking the total to 128 for FY26. |

| 7 |

Income Statement Highlights:

Gross Margin

| · | Q4FY26 at 44.8% (GG: 48.3%, PSAI: 19.9%), a decline of 1,074 basis points (bps) YoY and 881 bps QoQ. |

FY26 at 52.8% (GG: 56.7%, PSAI: 17.2%), a decline of 573 bps YoY.

The YoY decline for the quarter was primarily on account of reduced sales of Lenalidomide, price erosion in North America and Europe Generics and a one-time SSA impact indicated earlier. FY26 was further impacted by one-time new Labour Code related provision in Q3FY26.

Excluding the one-offs related to SSA and new Labour Codes, gross margin for Q4FY26 at 48.0% (GG: 51.7%) and FY26 at 53.5% (GG: 57.5%).

Selling, General & Administrative (SG&A) Expenses

| · | Q4FY26 at ₹27.8 billion, increase of 15% YoY and 3% QoQ. |

As % to Revenues – Q4FY26: 36.9% | Q4FY25: 28.3% | Q3FY26: 30.8%.

FY26 at ₹106.8 billion, increase of 14% YoY.

As % to Revenues – FY26: 31.8% | FY25: 28.8%.

The YoY increase was driven by focused investments in our branded franchises, particularly the acquired consumer healthcare business in NRT and branded generics as well as a provision related to a potential VAT liability in one of our subsidiaries of ₹1.1 billion in Q4FY26. FY26 also was impacted by a similar provision in Q2FY26 and one-time new Labour Codes related provision in Q3FY26.

Excluding the impact of VAT liability and new Labor Codes provision, SG&A as a % of revenues excluding SSA impact : Q4FY26: 33.4% | FY26 : 30.6%.

Research & Development (R&D) Expenses

| · | Q4FY26 at ₹5.5 billion, decrease of 25% YoY and 11% QoQ. |

As % to Revenues – Q4FY26: 7.3% | Q4FY25: 8.5% | Q3FY26: 7.0%.

FY26 at ₹24.1 billion, decrease of 12% YoY.

As % to Revenues – FY26: 7.2% | FY25: 8.4%.

R&D expenditure was lower due to reduced development spends in Biosimilars, following completion of a large part of the investments related to Abatacept. R&D spends remain focused on complex generics including peptides and biosimilars. Q4FY26 was also impacted by charges related to certain discontinued CAR-T assets, while FY26 included the one-time new Labour Codes provision.

Excluding the impact of CAR-T related charges and new Labor Codes provision, R&D as a % of revenues excluding SSA impact for Q4FY26 : 6.8% | FY26 : 7.1%.

Impairment

| · | Q4FY26 charge at ₹2.6 billion compared to ₹0.8 billion in Q4FY25. |

FY26 charge at ₹3.5 billion compared to ₹1.7 billion in FY25.

Q4FY26 includes charges related to discontinuation of some R&D programs within the Chimeric Antigen Receptor T cell (CAR-T) therapy portfolio of ₹1.3 billion as well as a charge on account of discontinuation of trial of Eftilagimod Alfa, by parter Immutep of ₹0.9 billion.

| 8 |

Other Income

| · | Q4FY26 income at ₹3.4 billion compared to ₹2.5 billion in Q4FY25. |

FY26 income at ₹7.6 billion compared to ₹4.4 billion in FY25.

Q4FY26 includes income from divestment of certain non-core product related intangibles i.e., trademarks and marketing rights of ₹1.89 billion.

Net Finance Income/Expense

| · | Q4FY26 income at ₹0.6 billion compared to ₹2.4 billion in Q4FY25. |

FY26 income at ₹4.1 billion compared to ₹4.7 billion in FY25.

Net finance income in Q4FY26 was lower primarily on account of lower foreign exchange gain this quarter, in comparison to the corresponding quarter last year.

Profit before Tax (PBT)

| · | Q4FY26 at ₹2.0 billion, decline of 90% YoY and 87% QoQ. |

As % to Revenues – Q4FY26: 2.6% | Q4FY25: 23.6% | Q3FY26: 17.7%.

FY26 at ₹54.8 billion, decline of 29% YoY.

As % to Revenues – FY26: 16.3% | FY25: 23.6%.

Excluding the impact of SSA, VAT liability provision, costs related to discontinued CAR-T and impairment of Eftilagimod Alfa, new Labour Codes provision, PBT as a % of revenues : 12.5% in Q4FY26 | 19.0% in FY26.

Income Tax

| · | Q4FY26 benefit at ₹0.2 billion. As % to PBT – Q4FY26: (10.8)% | Q4FY25: 20.9% | Q3FY26: 22.9%. |

FY26 at ₹12.4 billion. As % to PBT – FY26: 22.5% | FY25: 25.4%.

The ETR was lower in Q4FY26 primarily due to a recognition of deferred tax assets on carry forward losses in one of our subsidiaries and a favourable jurisdictional mix for the quarter, in comparison to the same period in the previous year.

Profit attributable to Equity Holders of Parent Company

| · | Q4FY26 at ₹2.2 billion, decline of 86% YoY and 82% QoQ. |

As % to Revenues – Q4FY26: 2.9% | Q4FY25: 18.7% | Q3FY26: 13.9%.

FY26 at ₹42.9 billion, decline of 24% YoY.

As % to Revenues – FY26: 12.8% | FY25: 17.4%.

Diluted Earnings per Share (EPS)

| · | Q4FY26 is ₹2.64. |

FY26 is ₹51.42.

| 9 |

Other Financial Highlights:

EBITDA

| · | Q4FY26 at ₹9.8 billion, decline of 60% YoY and 52% QoQ. |

As % to Revenues – Q4FY26: 13.0% | Q4FY25: 29.1% | Q3FY26: 23.5%.

FY26 at ₹76.6 billion, decline of 17% YoY.

As % to Revenues – FY26: 22.8% | FY25: 28.3%.

Excluding the impact of SSA, provisions related to VAT liability and new Labour Codes and CAR-T related charges, EBITDA as a % of revenues excluding SSA impact: Q4FY26: 19.5% | FY26 : 24.7%.

Others:

| · | Operating Working Capital: As on 31st March 2026 at ₹144.3 billion | As on 31st March 2025 at ₹126.0 billion |

| · | Capital Expenditure: Q4FY26 at ₹4.4 billion | FY26 at ₹23.0 billion. |

| · | Free Cash Flow (post acquisition related payout): Q4FY26 at ₹2.8 billion | FY26 at ₹16.9 billion. |

| · | Net Cash Surplus: As on 31st March 2026 at ₹32.7 billion. |

| · | Net Debt to Equity: As on 31st March 2026 is (0.09). |

| · | Return on Capital Employed (RoCE): FY26 stood at 15.8%. |

Excluding the impact of SSA, provisions related to VAT liability and new Labour Codes, costs related to discontinued CAR-T and impairment of Eftilagimod Alfa, RoCE for FY26 at 17.5%.

| 10 |

About key metrics and non-GAAP Financial Measures

This press release contains non-GAAP financial measures within the meaning of Regulation G and Item 10(e) of Regulation S-K. Such non-GAAP financial measures are measures of our historical performance, financial position or cash flows that are adjusted to exclude or include amounts from the most directly comparable financial measure calculated and presented in accordance with IFRS.

The presentation of this financial information is not intended to be considered in isolation or as a substitute for, or superior to, the financial information prepared and presented in accordance with IFRS. Our non-GAAP financial measures are not based on any comprehensive set of accounting rules or principles. These measures may be different from non-GAAP financial measures used by other companies, limiting their usefulness for comparison purposes.

We believe these non-GAAP financial measures provide investors with useful supplemental information about the financial performance of our business, enable comparison of financial results between periods where certain items may vary independent of business performance, and allow for greater transparency with respect to key metrics used by management in operating our business.

For more information on our non-GAAP financial measures and a reconciliation of GAAP to non-GAAP measures, please refer to "Reconciliation of GAAP to Non-GAAP Results" table in this press release.

| 11 |

All amounts in millions, except EPS

Reconciliation of GAAP Measures to Non-GAAP Measures

Operating Working Capital

| Particulars | As on 31st Mar 2026 | As on 31st Mar 2025 | ||||||

| (₹) | (₹) | |||||||

| Inventories | 76,531 | 71,085 | ||||||

| Trade Receivables | 101,219 | 90,420 | ||||||

| Less: | ||||||||

| Trade Payables | (33,411 | ) | (35,523 | ) | ||||

| Operating Working Capital | 144,339 | 125,982 | ||||||

Free Cash Flow

| Particulars | Three months ended 31st Mar 2026 | Year ended 31st Mar 2026 | ||||||

| (₹) | (₹) | |||||||

| Net cash generated from operating activities | 17,259 | 70,281 | ||||||

| Less: | ||||||||

| Taxes | (1,614 | ) | (13,526 | ) | ||||

| Investments in Property, Plant & Equipment and intangibles | (9,646 | ) | (36,715 | ) | ||||

| Free Cash Flow before Acquisitions | 5,999 | 20,040 | ||||||

| Less: | ||||||||

| Acquisitions related pay-out | (3,152 | ) | (3,152 | ) | ||||

| Cash Flow | 2,847 | 16,888 | ||||||

Net Cash Surplus and Debt to Equity

| Particulars | As on 31st Mar 2026 | |||

| (₹) | ||||

| Cash and Cash Equivalents | 15,368 | |||

| Investments | 83,141 | |||

| Short-term Borrowings | (65,138 | ) | ||

| Long-term Borrowings (Current & Non-current) | (12,203 | ) | ||

| Less: | ||||

| Restricted Cash Balance – Unclaimed Dividend and others | (109 | ) | ||

| Lease liabilities (Included in Short-term and Long-term Borrowings) | 14,407 | |||

| Equity Investments (Included in Investments) | (2,752 | ) | ||

| Net Cash Surplus | 32,714 | |||

| Equity | 380,457 | |||

| Net Debt/Equity | (0.09 | ) | ||

| 12 |

Computation of RoCE

| Particulars | As on 31st Mar 2026 | |||

| (₹) | ||||

| Profit before Tax | 54,817 | |||

| Less: | ||||

| Interest and Investment Income (Excluding forex gain/loss) | (2,347 | ) | ||

| Earnings Before Interest and taxes [A] | 52,469 | |||

| Average Capital Employed [B] | 332,856 | |||

| Return on Capital Employed (A/B) (Ratio) | 15.8 | % | ||

Computation of Capital Employed:

| Particulars | As on | |||||||

| Mar 31, 2026 | Mar 31, 2025 | |||||||

| Property Plant and Equipment | 115,930 | 97,761 | ||||||

| Intangibles | 105,059 | 96,803 | ||||||

| Goodwill | 12,893 | 11,810 | ||||||

| Investment in Equity Accounted Associates | 5,673 | 4,811 | ||||||

| Other Current Assets | 36,256 | 30,142 | ||||||

| Other Non-Current Assets | 1,226 | 972 | ||||||

| Inventories | 76,531 | 71,085 | ||||||

| Trade Receivables | 101,219 | 90,420 | ||||||

| Derivative Financial Instruments | (6,743 | ) | (729 | ) | ||||

| Less: | ||||||||

| Other Liabilities | 53,702 | 48,788 | ||||||

| Provisions | 7,659 | 6,324 | ||||||

| Trade payables | 33,411 | 35,523 | ||||||

| Operating Capital Employed | 353,272 | 312,440 | ||||||

| Average Capital Employed | 332,856 | |||||||

Computation of EBITDA

Refer page no. 3 & 4.

| 13 |

Earnings Call Details

The management of the Company will host an Earnings call to discuss the Company’s financial performance and answer any questions from the participants.

Date: Tuesday, May 12, 2026

Time: 19:30 pm IST | 10:00 am ET

| Conference Joining Information |

| Pre-register with the below link and join |

|

https://drreddys.zoom.us/webinar/register/WN_DW56_eZ6SAGF8FWL6wa-EQ |

Audio Link and Transcript will be available on the Company’s website: www.drreddys.com

About Dr. Reddy’s: Dr. Reddy’s Laboratories Ltd. (BSE: 500124, NSE: DRREDDY, NYSE: RDY, NSEIFSC: DRREDDY) is a global pharmaceutical company headquartered in Hyderabad, India. Established in 1984, we are committed to providing access to affordable and innovative medicines. Driven by our purpose of ‘Good Health Can’t Wait’, we offer a portfolio of products and services including APIs, generics, branded generics, biosimilars and OTC. Our major therapeutic areas of focus are gastrointestinal, cardiovascular, diabetology, oncology, pain management and dermatology. Our major markets include – USA, India, Russia & CIS countries, China, Brazil, and Europe. As a company with a history of deep science that has led to several industry firsts, we continue to plan and invest in businesses of the future. As an early adopter of sustainability and ESG actions, we released our first Sustainability Report in 2004. Our current ESG goals aim to set the bar high in environmental stewardship; access and affordability for patients; diversity; and governance.

For more information, log on to: www.drreddys.com.

Disclaimer: This press release may include statements of future expectations and other forward-looking statements that are based on the management’s current views and assumptions and involve known or unknown risks and uncertainties that could cause actual results, performance, or events to differ materially from those expressed or implied in such statements. In addition to statements which are forward-looking by reason of context, the words "may", "will", "should", "expects", "plans", "intends", "anticipates", "believes", "estimates", "predicts", "potential", or "continue" and similar expressions identify forward-looking statements. Actual results, performance or events may differ materially from those in such statements due to without limitation, (i) general economic conditions such as performance of financial markets, credit defaults , currency exchange rates , interest rates, persistency levels and frequency / severity of insured loss events (ii) mortality and morbidity levels and trends, (iii) changing levels of competition and general competitive factors, (iv) changes in laws and regulations and in the policies of central banks and/or governments, (v) the impact of acquisitions or reorganization , including related integration issues, and (vi) the susceptibility of our industry and the markets addressed by our, and our customers’, products and services to economic downturns as a result of natural disasters, epidemics, pandemics or other widespread illness, including coronavirus (or COVID-19), and (vii) other risks and uncertainties identified in our public filings with the Securities and Exchange Commission, including those listed under the "Risk Factors" and "Forward-Looking Statements" sections of our Annual Report on Form 20-F for the year ended March 31, 2025, our quarterly financial statements filed in Form 6-K with the US SEC for the quarter ended June 30, 2025, September 30, 2025, December 31, 2025 and our other filings with US SEC. The company assumes no obligation to update any information contained herein.

| 14 |