Exhibit 99.6

VALUATION REPORT CONSIDERING THE MARKET VALUES OF 100 ƒ /o EQUITY INTEREST OF FUTURE VISION II ACQUISITION CORP. Client: FUTURE VISION II ACQUISITION CORP. Contact No. : KKG2026J010008 Report date : 13 January 2026

KINC KEE 2 Valuation Report - 100% Equity Interest of Micro Touch Technology Inc 13 January 2026 The Directors FUTURE VISION II ACQUISITION CORP. Dear Sirs , In accordance with your instructions, we have undertaken an investigation and analysis to express an independent opinion of 100 % equity value of MicroTouch Technology Inc ("MicroTouch" or the "Company") as at 30 September 2025 (the "Valuation Date") . The report which follows is dated 13 January 2026 (the "Report Date") . The purpose of this valuation is to express an independent opinion of the fair value of 100 % equity value of MicroTouch for internal reference . Our valuation was carried out on a fair value basis . Fair value is defined as "the price that would be received to sell an asset , or paid to transfer a liability, in an orderly transaction between market participants at the measurement date" .

KINC KEE 3 Valuation Report - 100% Equity Interest of Micro Touch Technology Inc We have conducted our valuation in accordance with International Valu . ation Standards issued by the International Valuation Standards Council and US Generally Accepted Accounting Principles . We planned and performed our valuation so as to obtain all the information and explanations which we considered necessary in order to provide us with sufficient evidence to express our opinion on the subject asset . We believe that the valuation procedures we employed provide a reasonable basis for our opinion . Our valu . ation of the 100 % equity interest in MicroTouch was developed through the application of an income approach known as discount cash flow methodology . Under discount cash flow method, the equity result depends on the present wo 1 th of future economic benefits to be derived from the projected sales income . Indication of the result is developed by discounting projected future net cash flows available for payment of shareholders' interest to their present worth . As part of our analysis, we have reviewed information prepared by the Company and relevant operational information regarding the subject business from public sources . We have relied to a considerable extent on such information in arriving at our opinion of value . The conclusion of value is based on accepted valuation procedures and practices that rely substantially on our use of numerous assumptions and our consideration of various factors that are relevant to the operation of Company . We have also considered various risks and uncertainties that have potential impact on the businesses . Further, while the assumptions and consideration of such matters are considered by us to be reasonable, they are inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond the control of the Company and King Kee Appraisal and Advisory Limited ("KKG") . We do not intend to express any opinion on matters which require legal or other specialized expertise or knowledge, beyond what is customarily employed by valuers . Our conclusions assume continuation of prudent management of the Company over whatever period of time that is reasonable and necessary to maintain the character and integrity of the assets valued .

KINC KEE 4 Valuation Report - 100% Equity Interest of Micro Touch Technology Inc The prospective financial information ("PFI") is based on judgmental estimates and assumptions made by the Company's management about circumstances and events that have not yet taken place. In performing its valuation, KKG has challenged management's assumptions, estimates, or cash flow projections with respect to the future performance of the Company, which involve matters of opinion, projection, or forecast (whether or not expressly stated). The forecast of future developments is made solely for the purposes of the valuation. We have not provided any opinion or any type of assurance about specific assumptions or components of the PFI or on the PFI as a whole. There will usually be differences between estimated and actual r esu lt s , because events and circumstances frequently do not occur as expected, and those differences may be material. We take no responsibility for the achievement of projected results, if any. Based on the investigation and analyses outlined in the report which follows , we are of the opinion that the fair value of 100% equity value of MicroTouch as at the Valuation Date is reasonably stated as below: Currency Fair value of 100%equity interest In USD'OOO 92,000

KINC KEE 5 Valuation Report - 100% Equity Interest of Micro Touch Technology Inc The following pages outline the factors considered, methodology and assumptions employed in formulating our opinions and conclusions. Any opinions are subject to the assumptions and limiting conditions contained therein. Yours faithfully, For and on behalf of King Kee Appraisal and Advisory Limited Richard Zhang Managing Director ASA, MRICS, CPV

KINC KEE 1 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc REMARK: This report has been prepared solely for the internal use purpose. The report should not be other1 - vise referred to, in 1 - vhole or in part, or quoted in any document, circular or statement in any manner, or distributed in whole or in part or copied to any their party 1 - vithout our prior 1 - vritten consent. We shall not under any circumstances whatsoever be liable to any third party except where we specifically agreed in 1 - vriting to accept such liability. This report and the conclusion of values arrived at herein are for the exclusive use of our client for the sole and specific purposes as noted herein. Furthermore, the report and conclusion of values are not intended by the author, and should not be construed by the reader, to be investment advice in any manner whatsoever. The conclusion of values represents the consideration based on informationfurnished by the Company/engagement parties and other sources. TABLE OF CONTENTS • Introduction • Purpose of Valuation • Basis of Value • Basis of Opinion • Company Background • Sources of Information • Methodology • Major Assumptions • • Valuation Comments Discount Rate • Risk Factors • Opinion of Value • Exhibit A - Limiting Conditions • Exhibit B - Valuers' Professional Declaration • Exhibit C - Valuation Result of Company 100% Equity • Exhibit D - Comparable Company Method - Cross - check 2 2 2 2 3 4 5 7 9 12 13 14 15 18 19 21

KINC KEE 2 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Introduction This report has been prepared in accordance with instructions from you to express an independent opinion of the fair value of 100% equity value of MicroTouch Technology Inc ("MicroTouch" or the "Company") as at 30 September 2025 (the "Valuation Date"). The report which follows is dated 13 January 2026 (the "Report Date"). Purpose of Valuation The purpose of this valuation is to express an independent opinion of the 100 % equity value of MicroTouch as at Valuation Date for internal reference only . Basis of Value Our valuation was carried out on a fair value basis . Fair value is defined as "the price that would be received to sell an asset, or paid to transfer a liability, in an orderly transaction between market participants at the measurement date" . Basis of Opinion We have conducted our valuation in accordance with International Valuation Standards issued by the International Valuation Standards Council and US Generally Accepted Accounting Principles . We planned and performed our valuation so as to obtain all the information and explanations which we considered necessary in order to provide us with sufficient evidence to express our opinion on the subject asset . The valuation procedures employed include the review of physical and economic condition of the subject asset, an assessment of key assumptions, estimates, and representations made by the proprietor or the operator of the subject asset . All matters we consider essential to the proper understanding of the valuation will be disclosed in the valuation report .

KINC KEE 3 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc The following factors form an integral part of our basis of op 1 • n 1 • on: • Assumptions on the market and the asset that are considered to be fair and reasonable; • Financial performance that shows a consistent trend of the operation; • Consideration and analysis on the micro and macro economy affecting the subject asset; • Analysis on tactical planning, management standard and synergy of the subject asset; • Analytical review of the subject asset; and • Assessment of the leverage and liquidity of the subject asset. Company Background MicroTouch is a technology - focused company specializing in information technology services. The main businesses include: 1. SmartFlow Real - Time Matching Information Technology Services (SFM): This service connects premium traffic suppliers with advertisers through a proprietary real - time matching algorithm . It enables precise traffic aggregation and efficient distribution without using standardized advertising modules . 2 . Custom Software Development : MicroTouch provides end - to - end customized software solutions for enterprise clients . Services include requirement analysis, system design, development, testing, and long - term maintenance - all built from scratch according to specific business scenarios .

KINC KEE 4 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Sources of Information We also government . conducted research using vanous statistics and other sources including Our valuation is based on data and information furnished by the Company's management ("Management"), which includes , but not limited to , the following ; publications to verify the reasonableness and fairness of information provided and we believe that the information is reasonable and reliable. Background information and future business plan of Company; Management accounts of Company ended 30 September 2023, 30 September 2024, and 30 September 2025; Company's future business plan including sales forecast from 2026 to 2030 ; Other operational and market information in relation to the Company's business . We have also discussed and examined other operational and business information through interviews with relevant senior management . We have relied to a considerable extent on such information in arriving at our opinion of value . We assumed that the data we obtained in the course of the valuation, along with the opinions and representations provided to us by the Company, are true and accurate .

KINC KEE 5 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Methodology In arriving at our assessed value, we have considered three generally accepted approaches, namely , market approach, cost approach and income approach . Market Approach considers prices recently paid for similar assets, with adjustments made to market prices to reflect condition and utility of the appraised assets relative to the market comparative . Assets for which there is an established secondary market may be valued by this approach . Cost Approach considers the cost to reproduce or replace in new condition the assets appraised in accordance with current market prices for similar assets, with allowance for accrued depreciation or obsolescence present , whether arising from physical, functional or economic causes . The cost approach generally furnishes the most reliable indication of value for assets without a known secondary market . Despite the simplicity and transparency of this approach, it does not directly incorporate information about the contributed by the subject asset. . economic benefits Benefits of using this approach include its simplicity, clarity, speed and the need for few or no assumptions . It also introduces objectivity in application as publicly available inputs are used . However , one has to be wary of the hidden assumptions in those inputs as there are inherent assumptions on the value of those comparable assets . It is also difficult to find comparable assets . Furthermore, this approach relies exclusively on the efficient market hypothesis .

KINC KEE 5 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Methodology (continued) Income Approach is the conversion of expected periodic benefits of ownership into an indication of value . It is based on the principle that an informed buyer would pay no more for the project than an amount equal to the present wo 1 th of anticipated future benefits (income) from the same or a substantially similar project with a similar risk profile . Selection of Valuation Approach and Methodology In our opinion, management provided the detailed cash flow forecasts of Company, and these companies operates sustainably, thus we believe that the income method is suitable for the valuation of the Company's equity value . We have therefore relied solely on the income approach in determining our opinion of value , and performed a cross - check using market approach . This approach allows for the prospective valuation of future profits and there are numerous empirical and theoretical justifications for the present value of expected future cash flows . However, this approach relies on numerous assumptions over a long time horizon and the result may be very sensitive to certain inputs . It also presents a single scenario only . Income approach In this study, the valuation result was developed through the application of an income approach technique known as discounted cash flow method to devolve the future value of the business into a present market value . This method eliminates the discrepancy in time value of money by using a discount rate to reflect all business risks including intrinsic and extrinsic uncertainties in relation to the business . Under this method , the result depends on the present worth of future economic benefits to be derived from the projected service income . Indications of the result have been developed by discounting projected future net cash flows available for payment of shareholders' interest to their present worth at discount rates which in our opinion are appropriate for the risks of the business . In considering the appropriate discount rate to be applied, we have taken into account a number of factors including the current cost of finance and the considered risk inherent in the business .

KINC KEE 6 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Major Assumptions Assumptions considered to have significant sensitivity effects in this valuation have been evaluated in order to provide a more accurate and reasonable basis for arriving at our assessed value . In determining the fair value of equity interest in the Company, the following key assumptions have been made : The facilities and systems proposed are assumed to be sufficient for future expansion in order to realize the growth potential of the business and maintain a competitive edge . There will be no material change in the ex 1 st 1 ng political , legal, technological, fiscal or economic conditions, which might adversely affect the business of the Company The projected business performance can be achieved with the effort of the management of the Company . The financial and operational information provided to us by the Company is true and accurate . There are no hidden or unexpected conditions associated with the assets valued that might adversely affect the reported value . Further, we assume no responsibility for changes in market conditions after the Valuation Date . Management has confirmed that there is no significant difference of the financial positions including the balance sheet between 30 September 2025 and 30 June 2025 , and as such given the availability of the financial statements, the latest financial statement as of 30 June 2025 is used in this valuation .

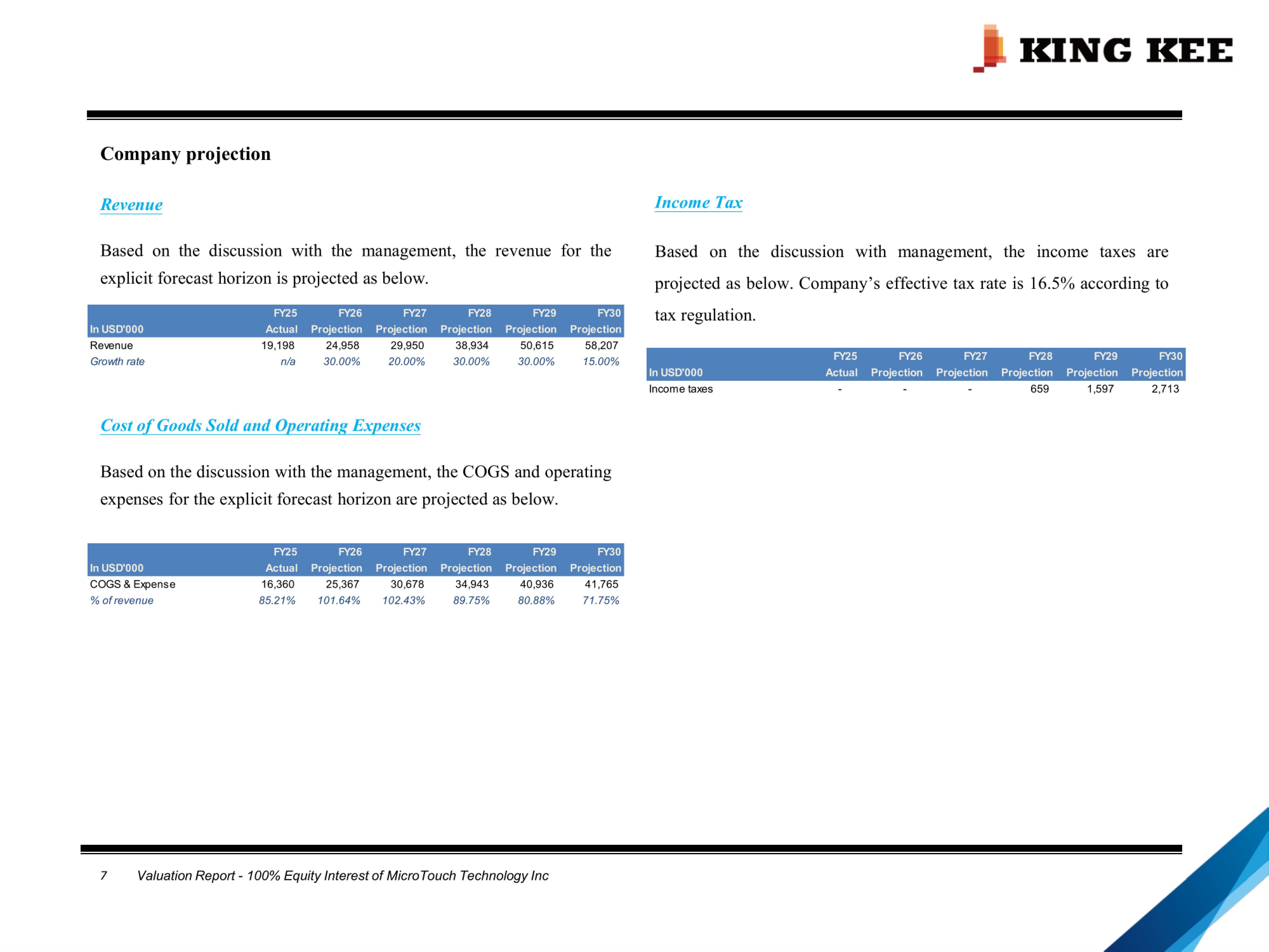

KINC KEE Company projection Revenue Income Tax Based on the discussion with the management, the revenue for the exp li cit forecast horizon is projected as below. FY30 Projection FY29 Projection FY28 Projection FY27 Projection FY26 Projection FY25 In USD'OOO Actua I 58 , 207 50 , 615 38 , 934 29,950 24,958 19,198 Revenue 15 . 00% 30.00% 30.00% 20.00% 30.00% nla Growth rate Based on the discussion with management , the income taxes are projected as below . Company's effective tax rate is 16 . 5 % according to tax regulation . FY25 FY26 FY27 FY28 FY29 7 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc FY30 In USD'OOO Actual Projection Projection Projection Projection Projection Income taxes 659 1 , 597 2,713 Cost o,f Goods Sold and Operating Expenses Based on the discussion with the management, the COGS and operating expenses for the exp licit forecast horizon are projected as below. FY25 FY26 FY27 FY28 FY29 FY30 In USD'OOO Actual Projection Projection Projection Projection Projection 41 , 765 40 , 936 34 , 943 30 , 678 25 , 367 16,360 COGS & Expense 71 . 75% 80 . 88% 89 . 75% 102.43% 101.64% 85.21% % of revenue

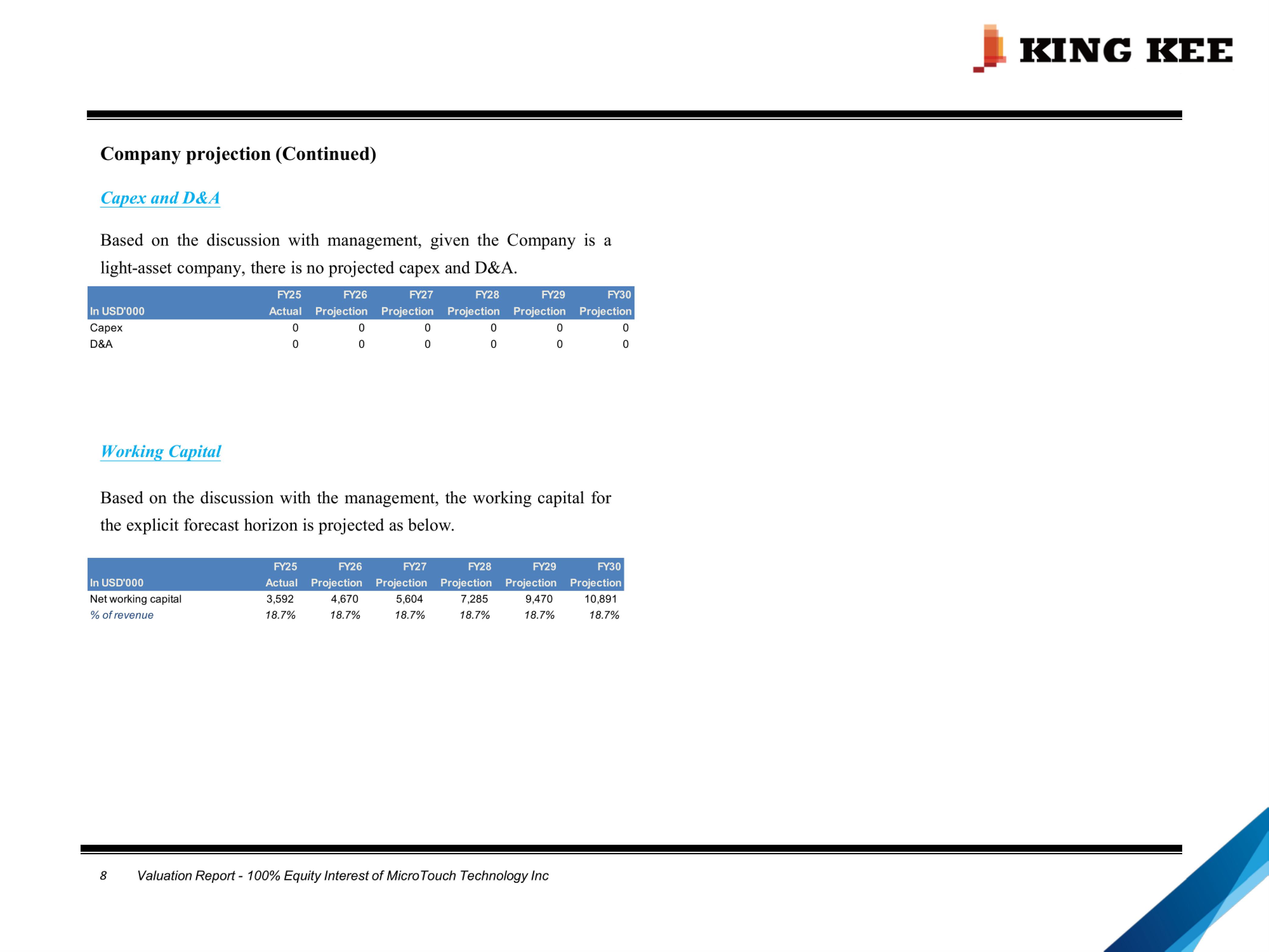

KINC KEE 8 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Company projection (Continued) Capex and D&A Based on the discussion with management, given the Company . lS a light - asset company, there is no projected capex and D&A. FY25 FY26 FY27 FY28 FY29 FY30 In USD'OOO Actual Projection Projection Projection Projection Projection 0 0 0 0 0 0 Capex 0 0 0 0 0 0 D&A Working Capital Based on the discussion with the management, the working capital for the explicit forecast horizon is projected as below. FY25 FY26 FY27 FY28 FY29 FY30 In USD'OOO Actual Projection Projection Projection Projection Projection 10,891 9,470 7,285 5,604 4,670 3,592 Net working capital 18.7% 18.7% 18.7% 18.7% 18.7% 18.7% % of revenue

KINC KEE 9 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Discount Rate In applying the discounted cash flow method, it is necessary to determine an appropriate discount rate for the assets under review. The discount rate represents an estimate of the rate of return required by a third party investor for an investment of this type. The rate of return expected from an investment by an investor relates to perceived risk. Risk factors relevant in our selection of an appropriate discount rate include: Interest rate risk, which measures variability of returns , caused by changes in the general level of interest rates. Purchasing power risk, which measures loss of purchasing power over time due to inflation. Liquidity risk , which measures the ease with which an instrument can be sold at the prevailing market price. Market risk, which measures the effects of the general market on the price behavior of securities. Business risk , which measures the uncertainty inherent in projections of operating income. Exchange rate, which measures the possible influence that changes in exchange rates , might have on the value of the investment . Consideration of risk also involves elements such as quality of management, degree of liquidity, and other factors affecting the rate of return acceptable to a given investor in a specific investment . An adjustment for risk is an increment added to a base rate to compensate for the extent of risk believed to be involved in the investment .

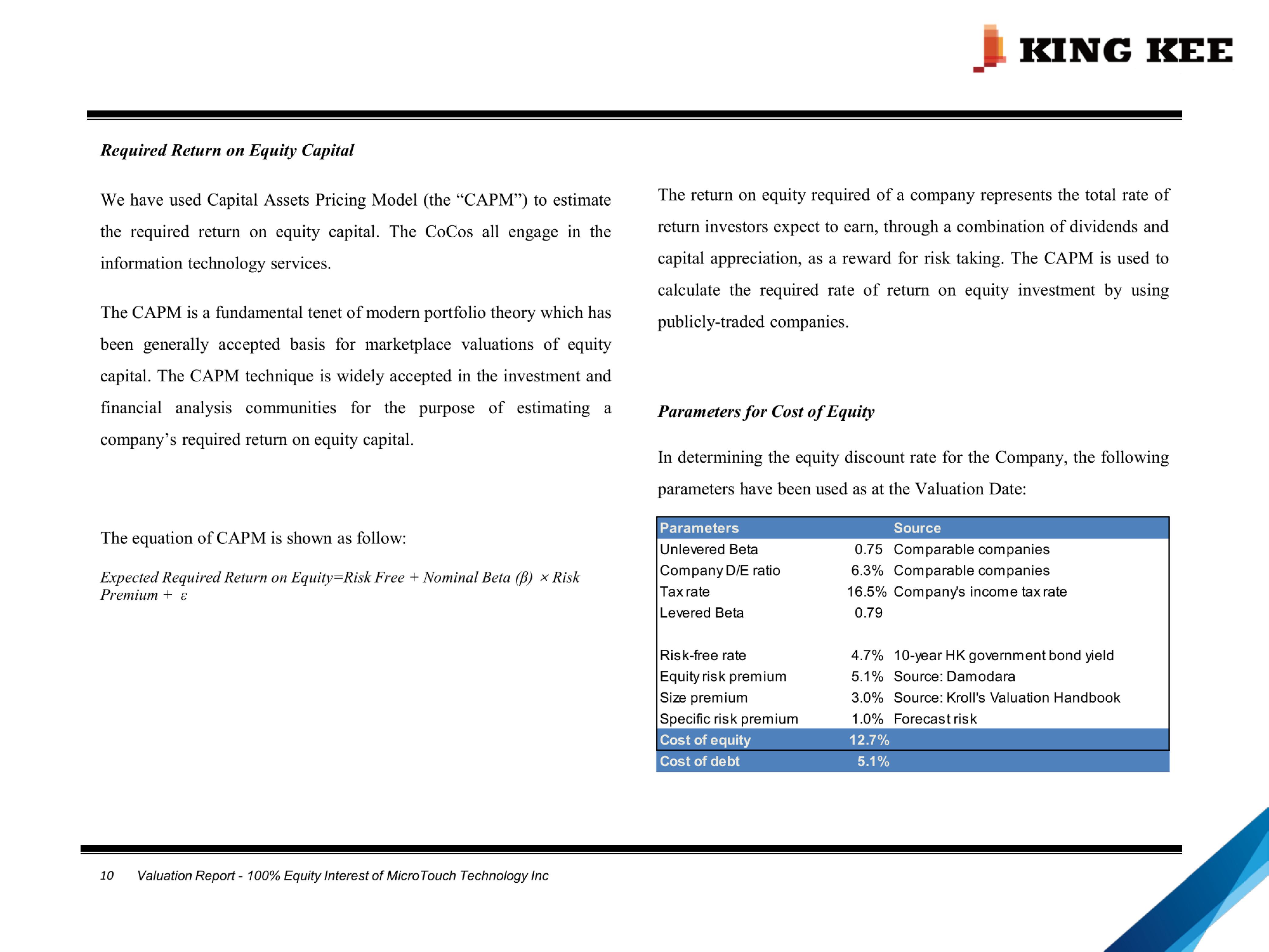

KINC KEE 10 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Required Return on Equity Capital We have used Capital Assets Pricing Model (the "CAPM") to estimate the required return on equity capital . The CoCos all engage in the information technology services . The CAPM is a fundamental tenet of modern portfolio theory which has been generally accepted basis for marketplace va lu . ations of equity capital . The CAPM technique is widely accepted in the investment and financial analysis communities for the purpose of estimating a company's required return on equity capital . The equation of CAPM is shown as follow: Expected Required Return on Equity=Risk Free + Nominal Beta (/J) x Risk Premium+ E: The return on equity required of a company represents the total rate of return investors expect to earn, through a combination of dividends and capital appreciation, as a reward for risk taking . The CAPM is used to calculate the required rate of return on equity investment by using publicly - traded companies . Parameters for Cost of Equity In determining the equity discount rate for the Company, the following parameters have been used as at the Valuation Date: Parameters Source Unlevered Beta Company D/E ratio Tax rate Levered Beta Risk - free rate Equity risk premium Size premium Specific risk premium 0.75 Comparable companies 6.3% Comparable companies 16 . 5% Company's income tax rate 0.79 4.7% 5.1% 3.0% 10 - year HK government bond yield Source:Damodara Source: Kroll's Valuation Handbook 1.0% Forecast risk

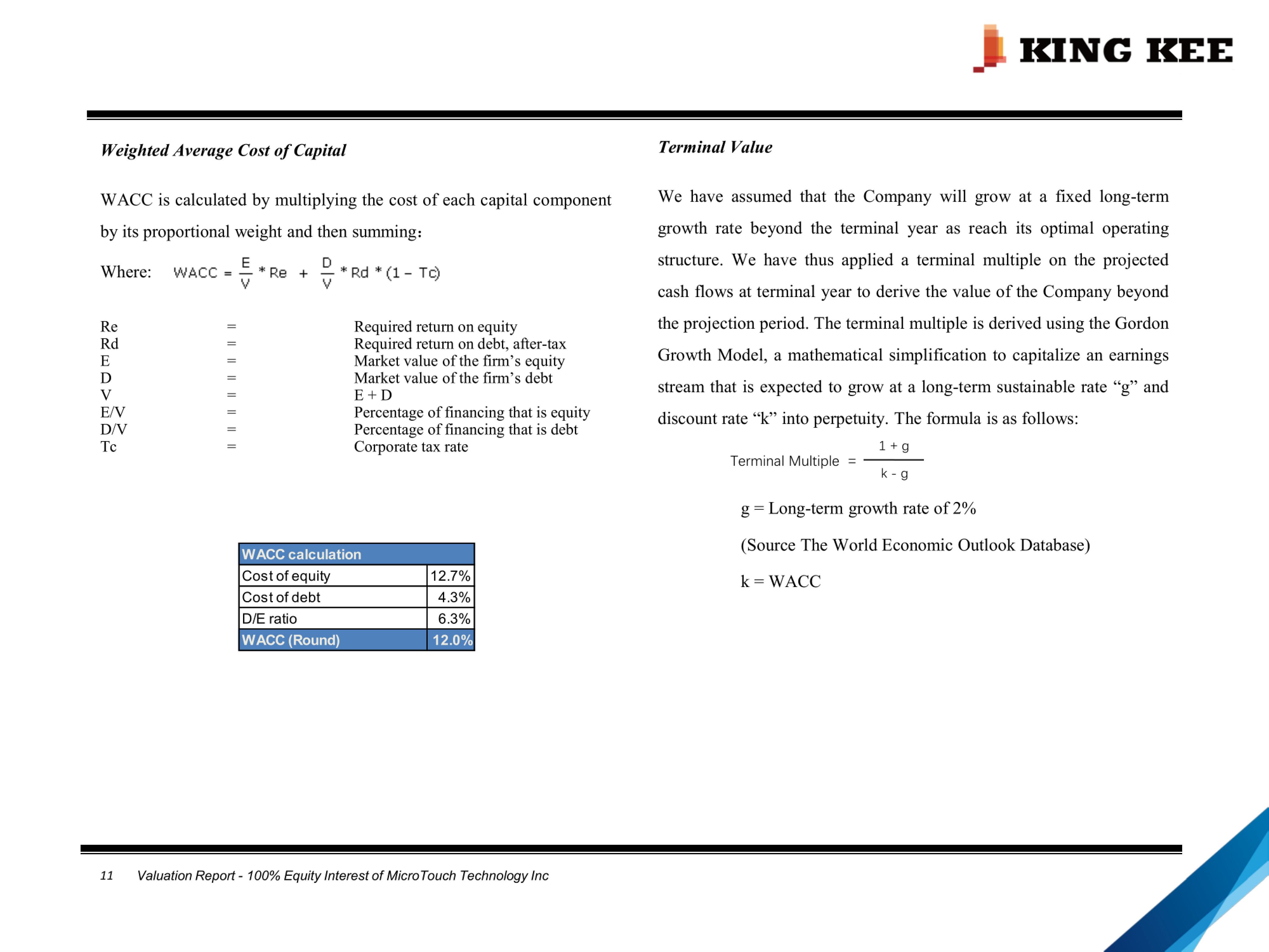

12 . 7% Cost of eq ui ty 4 .3% Cost of debt 6.3% D /E r atio KINC KEE 11 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc We i g h te d Ave r age C o st o f Ca pi ta l Te rminal Va l ue W ACC is ca l c u lated by m ul tiplying the cost of each capital component by its proportional weight and then summing: Where: WACC = - E V "'Re + � "' Rd "' ( 1 - Tc) V Re Rd E D V EN DN Tc Required return on equity Required return on debt , afte r - tax Market value of the firn1's equity Market value of the firn1's debt E+D Percentage of financing that is equity Percentage of financ i ng that i s debt Corporate tax r ate - - - - - - - - We have assumed t h at t h e Co m pany w ill grow at a fixed l ong - te rm growt h rate b eyond t h e ter m ina l year as reach i ts opt i ma l operat i ng structure . We have thus app li ed a ter mi na l m u l t i p l e on the projected cas h flows at te r m i na l year to de ri ve the va l ue of t h e Company beyond t h e p r o j ect i on per i od . T h e te r m i na l m u l t i p l e i s der i ved us i ng the Go r don Growth Mode l , a mathemat i ca l s i mp li ficat i on to cap i ta li ze an earn i ngs strea m t h at i s expected to grow at a l ong - te r m susta i na bl e rate "g" and d i scount rate "k" i nto perpetu i ty . T he fo 1 mu l a i s as fo ll ows : l+g Term i na l Mu l tip l e = k - g g = Long - term growth r ate of 2% WACC calculation WACC (Round) 12.0% (Sou r ce The Wo r ld Economic Ou tl ook Database) k = WACC

KINC KEE 12 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Valuation Comments The valuation of an interest in a business enterprise requires consideration of all relevant factors affecting the operation of the business and assets and its ability to generate future investment returns . The factors considered in the valuation includes, but not limited to , the following : the nature of the business and the historical performance of the enterprise; the financial condition of the business and the economic outlook in general; the operational contracts and agreements in relation to the business; past and projected operating results; the financial and business risk of the enterprise including the continuity of income and the projected future results; and the nature of the related agreements. obtained such further information which is considered necessary for the purposes of this valuation. In arriving at our assessed value, we have mainly considered the core business of the business . We have not made provision for other non - operating cash flow items such as interest income , exchange rate gain / loss , etc . in the valuation model . The conclusion of value is based on accepted valuation procedures and practices that rely substantially on the use of numerous assumptions and the consideration of many uncertainties , not all of which can be easily quantified or ascertained . Further, while the assumptions and consideration of such matters are considered by us to be reasonable, they are inherently subject to significant business , economic and competitive uncertainties and contingencies, many of which are beyond the control of the Company and KKG . We confirm that we have carried out an inspection on the assets of the Company and we have made relevant searches, enquiries and have

KINC KEE 13 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Risk Factors We caution readers to be aware of the following risks which we believe could influence the assessment . Such risks can range from very subject specific factors to more systematic factors . Social, Political and Macroeconomic Considerations Various economic, political and social phenomena surrounding the subject items may change so as to affect our opinion of value . International or nationwide policy and / or legislative changes that alter existing rights and obligations may directly or indirectly influence the Subject items . Macroeconomic circumstances including inflation , interest rate fluctuations and existing and forecast levels of growth in the broader economy may also have an effect . Societal factors encompassing the perception and preferences of people in general may swing rendering the Subject items more or less desirable and thus more or less valuable . The Company is subject to various laws and regulations governing its operations in Hong Kong . Future political and legal changes in Hong Kong might have either favorable or unfavorable impacts on the Company . Environmental Conditions Phenomena within the physical environment can severely impact the factors of production and demand factors within an economy for the counterparty . The occurrence of natural disasters, resource depletion and variations in climate conditions may influence resource availability and prices for inputs on the supply side or may influence market access and preferences for products and services associated to the counterparty from end - user demand . Realization of forecast and projection This valuation is premised in part on the historical financial information and projections provided by the management of the Company . We have assumed accuracy of the information provided and relied to a considerable extent on such information in a 11 ·iving at our opinion of value . Although appropriate tests and analyses have been carried out to verify the reasonableness and fairness of the information provided , events and circumstances frequently do not occur as expected . Since projections relate to the future, there will usually be differences between projections and actual results and in some cases, those variances may be material . Accordingly, to the extent any of the above mentioned information requires adjustment ; the resulting investment value may differ .

KINC KEE 14 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Opinion of Value Limiting Conditions Based on the investigation and analyses outlined in the report, we are of the opinion that the fair value of 100 % equity value of MicroTouch as at the Valuation Date is reasonably stated as below : This report and opinion of value are subject to our Limiting Conditions as included in Exhibit A of this report. Yours faithfully, Currency Fair value of 1OO¾equity interest For and on behalf of In USD'OOO 92,000 King Kee Appraisal and Advisory Limited Richard Zhang Managing Director ASA, MRICS, CPV

KINC KEE 15 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Exhibit A - Limiting Conditions 1 . In the preparation of our reports, we relied on the accuracy, completeness and reasonableness of the Company information, assumptions and other data provided to us by the Company/engagement parties and/or its representatives . We did not carry out any work in the nature of an audit and neither are we required to express an audit or viability opinion . We take no responsibility for the accuracy of such information . The responsibility for determining expected values rests solely with the Company/engagement parties and our reports were only used as part of the Company's/engagement parties' analysis in reaching their conclusion of value. 2. We have explained as part of our service engagement procedure that it is the director's responsibility to ensure proper books of accounts are maintained, and the financial information and forecast give a true and fair view and have been prepared in accordance with the relevant standards and companies ordinance . 3. Public information and industry and statistical information have been obtained from sources we deem to be reputable ; however we make no representation as to the accuracy or completeness of such information, and have accepted the information without any verification . 4. The management and the Board of the Company has reviewed and agreed on the report and confirmed that the basis, assumptions, calculations and results are appropriate and reasonable . 5. KKG shall not be required to give testimony or attendance in court or to any government agency by reason of this exercise, with reference to the project described herein . Should there be any kind of subsequent services required, the corresponding expenses and time costs will be reimbursed from you . Such kind of additional work may incur without prior notification to you . 6. No opinion is intended to be expressed for matters which require legal or other specialized expertise or knowledge, beyond what is customarily employed by valuers . 7. The use of and/or the validity of the report is subject to the terms of engagement letter/proposal and the full settlement of the fees and all the expenses . 8. Our conclusions assume continuation of prudent management policies over whatever period of time that is considered to be necessary in order to maintain the character and integrity of the assets valued . 9. We assume that there are no hidden or unexpected conditions associated with the subject matter under review that might adversely affect the reported review result. Further, we assume no responsibility for changes in market conditions, government policy or other conditions after the Valuation/Reference Date. We cannot provide assurance on the achievability of the results forecasted by the Company/engagement parties because events and circumstances frequently do not occur as expected; difference between actual and expected results may be material; and achievement of the forecasted results is dependent on actions, plans and assumptions of management.

KINC KEE 16 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc 10. This report has been prepared solely for the internal use purpose . The report should not be otherwise referred to, in whole or in part, or quoted in any document, circular or statement in any manner, or distributed in whole or in part or copied to any their party without our prior written consent . We shall not under any circumstances whatsoever be liable to any third party except where we specifically agreed in writing to accept such liability . 11. This report is confidential to the client and the calculation of values expressed herein is valid only for the purpose Valuation / Reference Date. In accordance with standard practice, we must state that this report stated in the engagement letter/or proposal as of the our and exercise is for the use only by the party to whom it is addressed and no responsibility is accepted with respect to any third party for the whole or any part of its contents . 12. Where a distinct and definite representation has been made to us by party / parties interested in the assets valued, we are entitled to rely on that representation without further investigation into the veracity of the representation if such investigation is beyond the scope of normal scenario analysis work . 13. You agree to indemnify and hold us and our personnel harmless against and from any and all losses, claims, actions, damages, expenses or liabilities, including subjects in connection with this engagement. reasonable attorney's fees, to which we may become Our maximum liability relating to services rendered under this engagement (regardless of form of action, whether in contract, negligence or otherwise) shall be limited to the charges paid to us for the portion of its services or work products giving rise to liability . In no event shall we be liable for consequential, special, incidental or punitive loss, damage or expense (including without limitation, lost profits, opportunity costs, etc . ), even if it has been advised of their possible existence . 14. We are not environmental consultants or auditors, and we take no responsibility for any actual or potential environmental liabilities exist, and the effect on the value of the asset is encouraged to obtain a professional environmental assessment . We do not conduct or provide environmental assessments and have not performed one for the subject property . 15. This exercise is premised in part on the information and Company/engagement parties. We have assumed future estimates provided by the management of the the accuracy and reasonableness of the information provided and relied to a considerable extent on such information in arriving at our calculation of value . Since estimates relate to the future, there will usually be differences between estimates and actual results and in some cases, and those variances may be material . Accordingly, to the extent any of the above mentioned information requires adjustments, the resulting value may differ significantly . 16 . Actual transactions involving the subject assets / business might be concluded at a higher or lower value, depending upon the circumstances of the transaction and the business, and the knowledge and motivation of the buyers and sellers at that time .

KINC KEE 17 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc 17 . This report and the conclusion of values arrived at herein are for the exclusive use of our client for the sole and specific purposes as noted herein . Furthermore, the report and conclusion of values are not intended by the author, and should not be construed by the reader, to be investment advice in any manner whatsoever . The conclusion of values represents the consideration based on information furnished by the Company/engagement parties and other sources .

KINC KEE 18 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Exhibit B - Valuers' Professional Declaration bias with respect to the parties involved. The valuers certify, to the best of their knowledge and belief, that: Information has been obtained from sources that are believed to be reliable . All facts which have a bearing on the value concluded have been considered by the valuers and no important facts have been intentionally disregarded . The valuers' compensation is not contingent upon the amount of the value estimate, the attainment of a stipulated result, the occurrence of a subsequent event, or the reporting of a predetermined value or direction in value that favors the cause of the client . The analyses, opinions, and conclusions were developed, and this report has been prepared, in accordance with the International Valuation Standards published by the International Valuation Standards Council . The reported analyses, opinions, and conclusions are subject to the assumptions as stated in the report and based on the valuers' personal, unbiased professional analyses, opinions, and conclusions . The valuation exercise is also bounded by the limiting conditions . The reported analyses, op 1 • n 1 • ons, and conclusions are independent and objective. The valuers have no present or prospective interest in the asset that is the subject of this report, and have no personal interest or

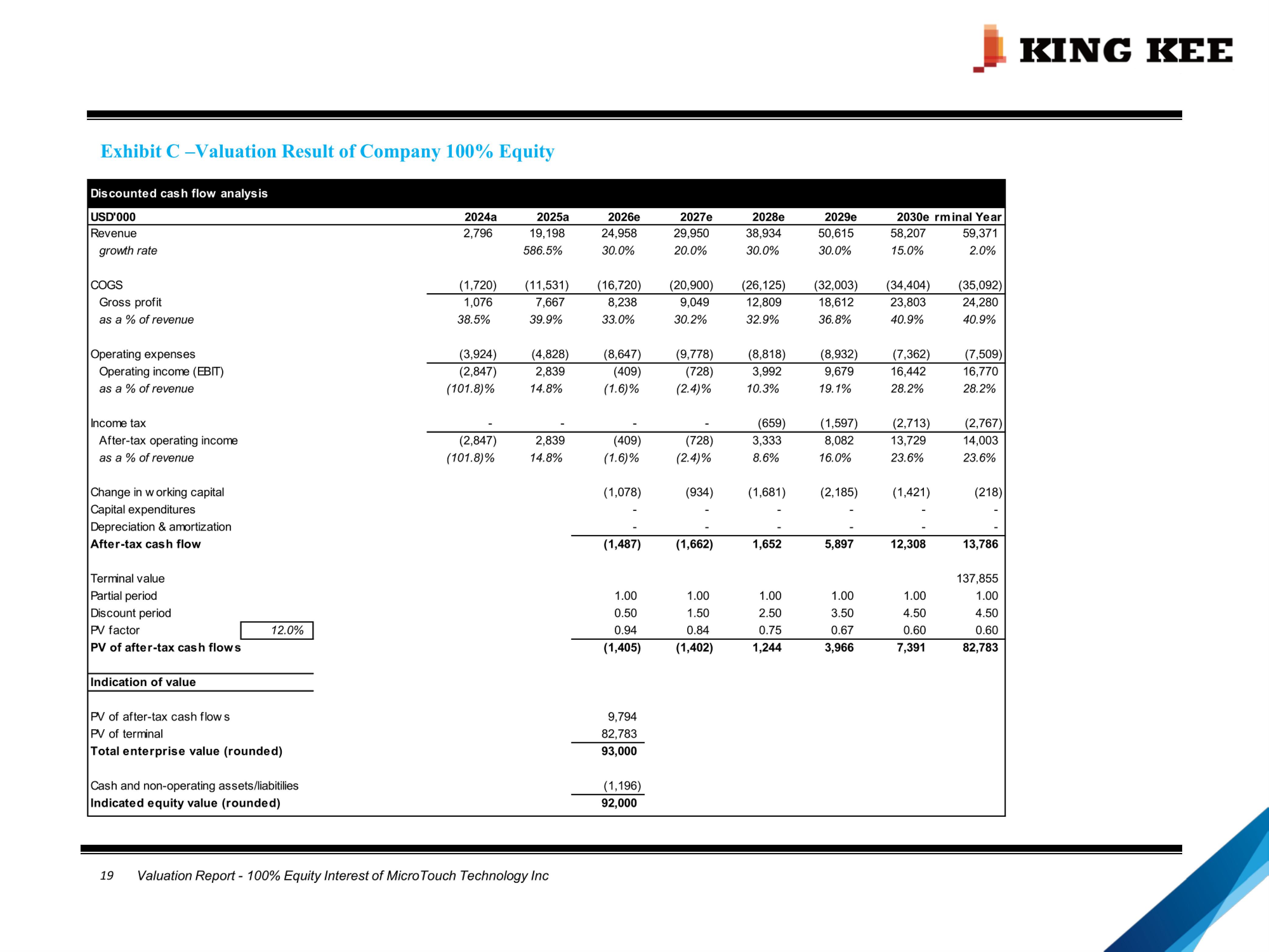

KINC KEE Exhibit C - Valuation Result of Company 100 ƒ /o Equity Discounted cash flow analysis rm inal Year 2030e 2029e 2028e 2027e 2026e 2025a 2024a USD'OOO 59,371 58,207 50,615 38,934 29,950 24,958 19,198 2,796 (1,720) 1,076 38.5% (3,924) (2,847) (101.8)% - (2,847) (101.8)% Revenue growth rate COGS Gross profit as a % of revenue Operat i ng expenses Operating incorre (EBIT) as a % of revenue lncorre tax After - tax operat i ng incorre as a % of revenue Change i n work i ng capita l Capita l expenditures Depreciation & arrortization After - tax cash flow Terninal value Partia l period Discount period Pv factor I 12.0% I PV of after - tax cash flows 2.0% 15.0% 30.0% 30.0% 20.0% 30.0% 586.5% (35,092) (34,404) (32,003) (26,125) (20,900) (16,720) (11,531) 24,280 23,803 18,612 12,809 9,049 8,238 7,667 40.9% 40.9% 36.8% 32.9% 30.2% 33.0% 39.9% (7,509) (7,362) (8,932) (8,818) (9,778) (8,647) (4,828) 16,770 16,442 9,679 3,992 (728) (409) 2,839 28.2% 28.2% 19.1% 10.3% (2.4)% (1.6)% 14.8% (2,767) (2,713) (1,597) (659) - - - 14,003 13,729 8,082 3,333 (728) (409) 2,839 23.6% 23.6% 16.0% 8.6% (2.4)% (1.6)% 14.8% (218) (1,421) (2,185) (1,681) (934) (1,078) - - - - - - - - - - - - 13,786 12 ,3 0 8 5,897 1 , 652 (1,662) (1,487) 137,855 1.00 1.00 1.00 1.00 1.00 1.00 4.50 4.50 3.50 2.50 1.50 0.50 0.60 0.60 0.67 0.75 0.84 0.94 82,783 7,391 3,966 1 , 244 (1,402) (1,405) Indication of value 9,794 Pv of after - tax cash f l ows 82,783 Pv of terninal 93,000 Total enterprise value (rounded) (1,196) Cash and non - operating assets/ l iabitilies 92,000 Indicated equity value (rounded) 19 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc

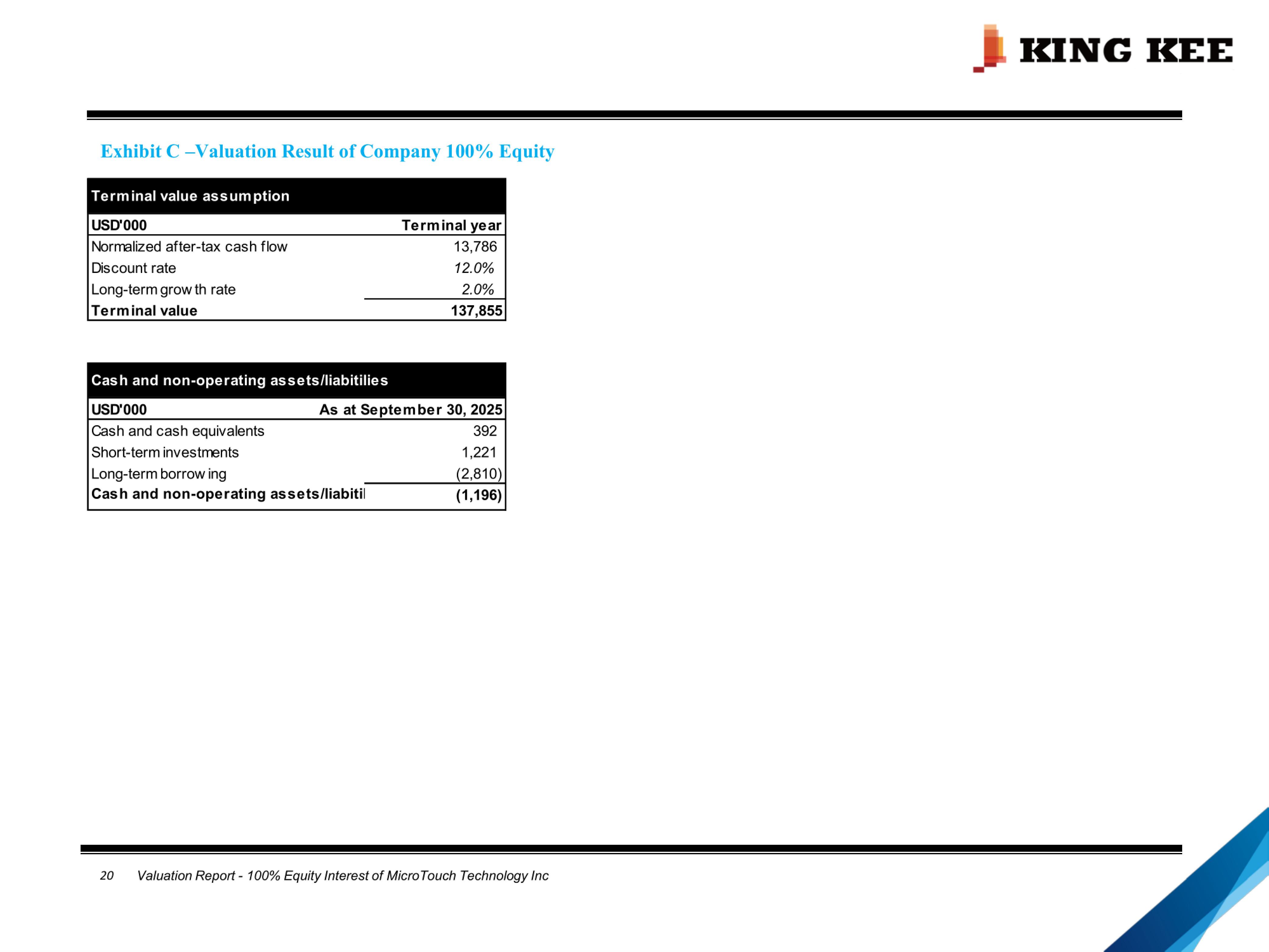

USD'OOO As at Septe m be r 30, 2025 392 Cash and cash equivalents 1 , 221 Short - term investments (2,810) Long - term borrow ing (1,196) Cash and non - operating assets/liabitil 20 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc Terminal year USD'OOO 13,786 Normalized after - tax cash flow 12.0% Discount rate 2.0% Long - term grow th rate 137,855 Terminal value KINC KEE Exhibit C - Valuation Result of Company 100 ƒ /o Equity Terminal value assumption Cash and non - operating assets/liabitilies

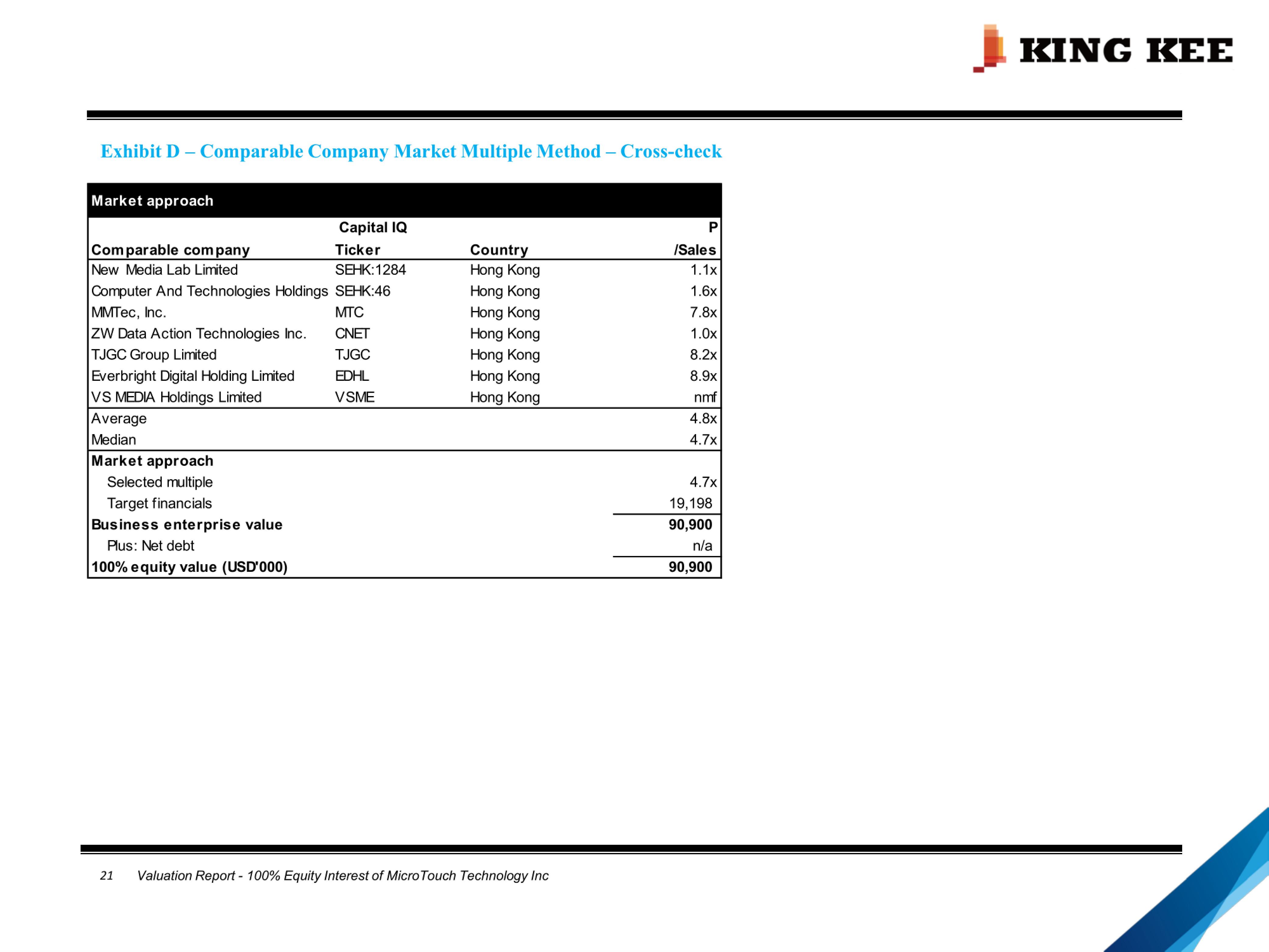

KINC KEE Exhibit D - Comparable Company Market Multiple Method - Cross - check Market approach p /Sales Country Capital IQ Com parable company Ticker 1 . 1x 1.6x 7.Bx 1.0x 8.2x 8.9x nmf Hong Kong Hong Kong Hong Kong Hong Kong Hong Kong Hong Kong Hong Kong New r \ fledia Lab Linited SEHK:1284 Computer And Technologies Holdings SEHK:46 MMTec, I nc . MTC ZW Data Action Technologies Inc . CNET TJGC Group Limited TJGC Everbright Digital Holding Limited EDHL VS MEDIA Holdings Limited VSME 4.8x 4.?x Average r \ fledian 4.?x 19,198 Market approach Selected multiple Target financials Business enterprise value Plus: Net debt 100% equity value (USO'OOO) 90,900 n/a 90,900 21 Valuation Report - 100% Equity Interest of MicroTouch Technology Inc