As filed with the Securities and Exchange Commission on May 11, 2026.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

Under

The Securities Act of 1933

NEPTUNE INSURANCE HOLDINGS INC.

(Exact name of registrant as specified in its charter)

Delaware | 6411 | 33-4189588 | ||

(State or other jurisdiction of incorporation or organization) | (Primary standard industrial code number) | (I.R.S. employer identification no.) |

400 6th Street S, Suite 2

St. Petersburg, Florida 33701

(727) 202-4815

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Trevor Burgess

Chief Executive Officer

Neptune Insurance Holdings Inc.

400 6th Street S, Suite 2

St. Petersburg, Florida 33701

(727) 202-4815

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Michael J. Sullivan Mark Mushkin Albert Vanderlaan Orrick, Herrington & Sutcliffe LLP The Orrick Building 405 Howard Street San Francisco, CA 94105 (415) 773-5700 | Joseph A. Hall Pedro J. Bermeo Steven J. Glendon Davis Polk & Wardwell LLP 450 Lexington Avenue New York, NY 10017 United States (212) 450-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities

Act of 1933, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the

Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act

registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act

registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an

emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in

Rule 12b-2 of the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

Non-accelerated filer | ☒ | Smaller reporting company | ☐ |

Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new

or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act ☐

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a

further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the

Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may

determine.

The information in this preliminary prospectus is not complete and may be changed. The selling stockholders may not sell these securities until our

registration statement filed with the U.S. Securities and Exchange Commission is declared effective. This preliminary prospectus is not an offer to sell

these securities and it is not soliciting offers to buy these securities in any state or jurisdiction where the offer or sale is not permitted.

PROSPECTUS (Subject to Completion)

Issued , 2026

8,355,615 Shares

Neptune Insurance Holdings Inc.

CLASS A COMMON STOCK

The selling stockholders identified in this prospectus are offering 8,355,615 shares of our Class A common stock. We will not be selling any shares in this

offering and will not receive any of the proceeds from the sale of our Class A common stock being sold by the selling stockholders.

We intend to purchase from the underwriters 835,561 shares of our Class A common stock at a price per share equal to the price per share to be paid by

the underwriters to the selling stockholders. The underwriters will not receive any compensation for the shares of our Class A common stock being repurchased

by us. The completion of the share repurchase is contingent on the satisfaction of customary closing conditions and conditioned upon the completion of this

offering.

Our Class A common stock is listed on the NYSE under the symbol “NP.” On May 8, 2026, the last reported sale price of our Class A common stock was

$29.92 per share. The public offering price will be determined between us, the selling stockholders, and the underwriters at the time of pricing and may be at a

discount to the current market price. Accordingly, the recent market price used throughout this prospectus may not be indicative of the public offering price.

Our Chief Executive Officer and Chairman of our board of directors, Trevor Burgess, beneficially owns approximately 84.0% of the voting power of our

outstanding voting securities (and approximately 84.1% of the voting power of our outstanding voting securities after giving effect to this offering and the

share repurchase) and we are, and as long as Mr. Burgess beneficially owns more than 50% of the voting power of our company, we will be, a “controlled

company” within the meaning of the listing rules of the NYSE. As a result, we qualify for, and rely on, exemptions from certain corporate governance

requirements, and you will not have the same protections as those afforded to stockholders of companies that are subject to such governance requirements. See

“Prospectus Summary — Implications of Being a Controlled Company.” We are an “emerging growth company” as defined under the federal securities laws

and, as such, are eligible for reduced public company reporting requirements. See “Prospectus Summary — Implications of Being an Emerging Growth

Company.”

Investing in our Class A common stock involves risks that are described in the “Risk Factors” section beginning on page 35 of this prospectus.

PRICE $ A SHARE

Price to Public(1) | Underwriting Discounts and Commissions(2) | Proceeds, before expenses, to Selling Stockholders | |||

Per Share ................................................................................................................................................... | $ | $ | $ | ||

Total .......................................................................................................................................................... | $ | $ | $ |

__________________

(1)The 835,561 shares of Class A common stock that we expect to purchase from the underwriters in the share repurchase will be purchased at a price per share equal to the

price per share to be paid by the underwriters to the selling stockholders.

(2)See the section titled “Underwriting” for a description of the compensation payable to the underwriters. The underwriters will not receive any discount or commission on the

835,561 shares of our Class A common stock that we expect to repurchase from the underwriters in the share repurchase.

The selling stockholders have granted the underwriters the right to purchase up to an additional 1,253,342 shares of Class A common stock

from the selling stockholders.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed

upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of Class A common stock against payment in New York, New York on or about ,

2026.

Joint Book-Runners | ||||

Morgan Stanley | J.P. Morgan | Goldman Sachs & Co. LLC | ||

i

TABLE OF CONTENTS

Page | |

Market and Industry Data ................................................................................................................................. | |

Select Defined Terms ........................................................................................................................................ | |

Prospectus Summary ......................................................................................................................................... | |

Risk Factors ...................................................................................................................................................... | |

Special Note Regarding Forward-Looking Statements .................................................................................... | |

Use of Proceeds ................................................................................................................................................. | |

Dividend Policy ................................................................................................................................................ | |

Capitalization .................................................................................................................................................... | |

Certain Relationships and Related Party Transactions ..................................................................................... | |

Principal and Selling Stockholders ................................................................................................................... | |

Description of Capital Stock ............................................................................................................................. | |

Stock .............................................................................................................................................................. | |

Underwriting ..................................................................................................................................................... | |

Legal Matters .................................................................................................................................................... | |

Experts .............................................................................................................................................................. | |

Where You Can Find Additional Information .................................................................................................. | |

Unless the context requires otherwise, the words “we,” “us,” “our,” the “Company,” and “Neptune” refer to

Neptune Insurance Holdings Inc. and its subsidiaries, taken as a whole, “Neptune Holdings” refers only to Neptune

Insurance Holdings Inc., and “Neptune Flood” refers only to Neptune Flood Incorporated. For purposes of this

prospectus, unless the context otherwise requires, the term “stockholders” shall refer to the holders of our Class A

common stock and Class B common stock.

We have not, and the selling stockholders and the underwriters have not, authorized anyone to provide you with

additional information or information that is different from or to make any representations other than those

contained in this prospectus or in any free-writing prospectus prepared by or on behalf of us to which we may have

referred you in connection with this offering. We, the selling stockholders and the underwriters, take no

responsibility for, and can provide no assurances as to the reliability of, any other information that others may give

you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in

jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of

the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock.

Our business, financial condition, results of operations, and future growth prospects may have changed since that

date.

Through and including , 2026 (the 25th day after the date of this prospectus), U.S. federal

securities laws may require all dealers that effect transactions in our common stock, whether or not

participating in this offering, to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a

prospectus when acting as underwriters and with respect to any unsold allotments or subscriptions.

For investors outside the United States, neither we, the selling stockholders nor any of the underwriters have

done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction

where action for that purpose is required, other than in the United States. Persons who come into possession of this

prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any

restrictions as to this offering and the distribution of this prospectus and any such free-writing prospectus outside the

United States.

ii

TRADEMARKS, TRADE NAMES AND SERVICE MARKS

“Neptune,” “Neptune Flood,” “Triton,” the Neptune stylized design logo, and our other registered or common

law trademarks, trade names, and service marks appearing in this prospectus are our property. Solely for

convenience, our trademarks, trade names, and service marks referred to in this prospectus appear without the ®, ™,

and ℠ symbols, but those references are not intended to indicate, in any way, that we will not assert, to the fullest

extent under applicable law, our rights to these trademarks and trade names. This prospectus contains additional

trademarks, trade names, and service marks of other companies that are the property of their respective owners.

NON-GAAP FINANCIAL MEASURES AND KEY PERFORMANCE INDICATORS

This prospectus and the documents incorporated by reference herein contain certain financial measures,

including Adjusted EBITDA, Adjusted EBITDA margin, Adjusted net income, Adjusted EBITDA (basic and

diluted) per share, and Adjusted earnings (basic and diluted) per share, that are not required by, or prepared in

accordance with, U.S. generally accepted accounting principles. We refer to these measures as “non-GAAP”

financial measures. See “Management’s Discussion and Analysis of Financial Condition and Results of

Operations — Non-GAAP Financial Measures” in our Annual Report on Form 10-K for the year ended December

31, 2025 (the “Annual Report”) and our Quarterly Report on Form 10-Q for the quarter ended March 31, 2026 (the

“Q1 Quarterly Report”), respectively, each incorporated by reference herein, for our definitions of these non-GAAP

measures, information about how and why we use these non-GAAP measures and a reconciliation of each of these

non-GAAP measures to its most directly comparable financial measure calculated in accordance with GAAP.

This prospectus and the documents incorporated by reference herein also include certain key performance

indicators, including revenue per employee, Adjusted EBITDA per employee, premium in force, policies in force,

policy retention rate, premium retention rate, revenue retention rate, organic revenue, organic revenue growth, and

written premium, that Neptune’s management regularly reviews in managing its business to evaluate its business and

operations, guide decision-making, measure progress and understand growth and retention, and ultimately help drive

profitability. Organic revenue and organic revenue growth are common non-GAAP financial measures reported by

others in the insurance industry. We use “organic revenue” and “organic revenue growth” in this prospectus to

facilitate investors’ understanding of our operating performance and comparison with our peers. However, as of the

date of this prospectus and for the relevant periods presented or incorporated by reference herein, we have not

completed any relevant acquisitions or divestitures, therefore our organic revenue and organic revenue growth

reflect our total revenue and total revenue growth, respectively, as determined in accordance with GAAP. For

definitions of these key performance indicators, see “Management’s Discussion and Analysis of Financial Condition

and Results of Operations — Key Performance Indicators” in our Annual Report and our Q1 Quarterly Report,

respectively, each incorporated by reference herein.

1

MARKET AND INDUSTRY DATA

This prospectus and the documents incorporated by reference herein contain estimates and information

concerning our industry, our business, and the market for our products and solutions, including our general

expectations of our market position, market growth forecasts, our market opportunity, and size of the markets in

which we participate, that are based on industry publications, surveys, and reports that have been prepared by

independent third parties. This information involves assumptions and limitations, and you are cautioned not to give

undue weight to these estimates. Although we have not independently verified the accuracy or completeness of the

data contained in these industry publications, surveys, and reports, we believe the publications, surveys, and reports

are generally reliable, although such information is inherently subject to uncertainties and imprecision. The industry

in which we operate is subject to a high degree of uncertainty and risk due to a variety of factors, including those

described in the sections titled “Risk Factors” beginning on page 35 of this prospectus and in our Annual Report and

our Q1 Quarterly Report, each incorporated by reference herein. These and other factors could cause results to differ

materially from those expressed in these publications and reports.

The source of certain statistical data, estimates, and forecasts contained in this prospectus are the following

industry publications or reports that have been prepared by independent third parties:

•Federal Emergency Management Agency, “FEMA Exercises Borrowing Authority for National Flood

Insurance Program,” February 10, 2025 (accessed on May 25, 2025);

•National Association of Insurance Commissioners, Tableau dashboard (accessed on May 25, 2025);

•Congressional Budget Office, “Federal Spending for Flood Adaptations,” September 30, 2024 (accessed on

May 25, 2025);

•First Street ®, “First Street Foundation releases new data disclosing the flood risk of every home in the

contiguous U.S.,” June 29, 2020 (accessed on May 25, 2025);

•Federal Emergency Management Agency, OpenFEMA Dataset: FEMA NFIP Redacted Policies — v2

(accessed on May 25, 2025);

•U.S. Government Accountability Office, “Flood Insurance: FEMA’s New Rate-Setting Methodology

Improves Actuarial Soundness but Highlights Need for Broader Program Reform,” July 31, 2023 (accessed

on May 25, 2025);

•Federal Emergency Management Agency, “National Flood Insurance Program Continues to Pay Interest on

its Treasury Debt,” October 24, 2023 (accessed on May 25, 2025);

•Federal Emergency Management Agency, Risk Rating 2.0 (accessed on May 25, 2025);

•California Department of Insurance, “Earthquake Premium and Policy Count Data Call, Summary of 2023

Residential Totals” (accessed on May 25, 2025);

•United States Census Bureau, QuickFacts: California (accessed on May 25, 2025); and

•United States Government Accountability Office, “Better Planning and Analysis Needed to Address

Current and Future Flood Hazards,” October 2021 (accessed on May 25, 2025).

2

SELECT DEFINED TERMS

“2019 Stock Plan” means the stock plan adopted by Neptune Flood on April 23, 2019, and approved by the

stockholders of Neptune Flood on April 24, 2019.

“2025 Amended and Restated Credit Agreement” means the Amended and Restated Credit Agreement, dated

as of April 10, 2025, by and among Neptune Holdings, Neptune Flood, the other loan parties party thereto from time

to time, the lenders party thereto from time to time, and JPMorgan Chase Bank, N.A., as administrative agent.

“2025 Equity Incentive Plan” means our 2025 Equity Incentive Plan, which was adopted by our board of

directors on September 19, 2025, and approved by our stockholders on September 21, 2025, and which became

effective on September 29, 2025.

“AGI” means artificial general intelligence, which refers to the hypothetical ability of an intelligent computer to

understand or learn any intellectual task that a human being can. AGI is a theoretical stage in AI development that

has likely not yet been achieved.

“AI” means artificial intelligence. As discussed herein, the term “AI” refers to the broad discipline concerned

with developing systems capable of performing tasks that traditionally require human intelligence (including, but not

limited to, natural language understanding, pattern recognition, complex problem-solving, and decision-making)

while “machine learning” refers to a subset of AI that concentrates on enabling computers to learn from data and

enhance their performance over time without explicit programming for each specific task. In other words, AI

represents the overarching field dedicated to the development of intelligent systems, while machine learning

constitutes one of the primary methodologies for realizing this objective. The Company’s Triton and Poseidon

platforms each utilize “machine learning” models to conduct predictive analysis on prospective underwriting results

and generate pricing and coverage determinations. As we continue to advance and refine our Triton and Poseidon

systems, we intend to continue to leverage both AI and machine learning. See also “ML.”

“amended and restated bylaws” means our second amended and restated bylaws, effective as of October 2,

2025.

“amended and restated certificate of incorporation” means our second amended and restated certificate of

incorporation, filed with the Secretary of State of the State of Delaware on October 2, 2025, and effective as of

October 2, 2025.

“Amended and Restated 2019 Stock Plan” means the 2019 Stock Plan, as amended and restated on each of

May 8, 2023, and November 10, 2023.

“Amended and Restated 2025 Stock Plan” means the Amended and Restated 2019 Stock Plan, as assumed by

Neptune Holdings and amended and restated as of April 10, 2025.

“Annual Report” means our Annual Report on Form 10-K for the fiscal year ended December 31, 2025, filed

with the SEC on February 26, 2026.

“API” means application programming interface.

“Bregal Sagemount” means Bregal Sagemount Management, L.P.

“BSIV 101” means BSIV Hold 101, LP.

“BSIV 102” means BSIV Hold 102, LP.

“CAGR” means compound annual growth rate.

“capacity provider” means an insurance carrier or reinsurance company that partners with a managing general

agent to underwrite, manage, and take insurance risk related to insurance policies.

“Charles River Data” means Charles River Data LLC.

3

“Code” refers to the Internal Revenue Code of 1986, as amended.

“Congress” means the United States Congress.

“DGCL” means the Delaware General Corporation Law.

“Effective Time” means the time of effectiveness of the filing of our amended and restated certificate of

incorporation with the Secretary of State of the State of Delaware in connection with the IPO.

“EGC” means an emerging growth company, as defined in the JOBS Act.

“Exchange Act” means the Securities Exchange Act of 1934, as amended.

“FDPA” means the Flood Disaster Protection Act of 1973.

“FEMA” means the Federal Emergency Management Agency.

“FINRA” means the Financial Industry Regulatory Authority.

“fiscal year” means the fiscal year ended December 31, and references throughout this prospectus to a given

fiscal year are to the twelve months ended on that date.

“FTV VII” means FTV VII, L.P.

“FTV Capital” means FTV Management Company, L.P. and/or its affiliates (including its investment vehicles).

“FTV-NE Aggregator” means FTV-NE Aggregator, LLC.

“GAAP” means U.S. generally accepted accounting principles.

“Growth VII-Centre” means Growth VII-Centre, L.P.

“insurance carrier” means a company that issues, underwrites, manages, and takes economic risk related to

insurance policies.

“insurance program” means a structured arrangement with one or more insurance carriers designed to offer

specific types of insurance coverage.

“IPO” means the initial public offering of our Class A common stock, which the Company completed on

October 2, 2025.

“IRS” means the United States Internal Revenue Service.

“JOBS Act” means the Jumpstart Our Business Startups Act of 2012.

“Jumpstart” means Jumpstart Insurance Solutions.

“KPI” means a key performance indicator.

“MGA” means a managing general agent.

“ML” means machine learning, which is a subset of AI that concentrates on enabling computers to learn from

data and enhance their performance over time without explicit programming for each specific task. Machine learning

algorithms employ statistical models and computational techniques to analyze data, discern patterns, and generate

predictions or decisions. The principal objective of machine learning is to construct systems that can autonomously

improve through experience, thereby facilitating accurate predictions or decisions when presented with new data.

The Company’s Triton and Poseidon platforms each utilize “machine learning” models to conduct predictive

analysis on prospective underwriting results and generate pricing and coverage determinations. See also “AI”.

“NAIC” means the National Association of Insurance Commissioners.

4

“NFIP” means the National Flood Insurance Program.

“NYSE” means the New York Stock Exchange.

“policyholder” means the individual owner or named insured listed on an issued policy.

“Poseidon” means Neptune’s proprietary policy management platform.

“Proxy Statement” means our definitive proxy statement on Schedule 14A filed with the SEC on April 17,

2026.

“Q1 Quarterly Report” means our Quarterly Report on Form 10-Q for the quarter ended March 31, 2026, filed

with the SEC on April 29, 2026.

“reinsurance company” or “reinsurer” means a company that provides coverage to an insurance company

through a reinsurance agreement. The reinsurer agrees to cover certain losses incurred by the insurer in exchange for

reinsurance premiums, while the insurer continues to issue policies to policyholders.

“SEC” means the United States Securities and Exchange Commission.

“SFHA” means Special Flood Hazard Area, as designated by FEMA.

“U.S. Treasury” means the United States Department of the Treasury.

“Triton” means Neptune’s proprietary underwriting engine.

“Voting Threshold Date” means the first date falling after 11:59 p.m. (Eastern Time) on the date on which the

outstanding shares of our Class B common stock represent less than a majority of the combined voting power of our

then-outstanding Class A common stock and Class B common stock entitled to vote generally in the election of

directors.

“whole board of directors” means the total number of authorized directors on the board of directors of the

Company, whether or not there exist any vacancies in previously authorized directorships.

“written loss ratio” means a ratio, expressed as a percentage, of, (i) for any given period of time, (1) the losses

actually incurred (or expected to be incurred) for observed events during that period on all policies written during

that period, to (2) the aggregate amount of premiums written on policies that became effective during that period or,

(ii) for any given catastrophic event (1) the losses incurred (or expected to be incurred) in connection with that

event, to (2) the aggregate amount of premiums written on policies in force as of the event date.

“written premium” means the total premium we placed with insurance programs during a reporting period, less

“return premiums” refunded to policyholders due to cancellations, endorsement of policies, or otherwise.

5

PROSPECTUS SUMMARY

This summary highlights selected information contained in greater detail elsewhere in this prospectus. This

summary is not complete and does not contain all of the information you should consider in making your investment

decision. You should carefully read this entire prospectus and the information incorporated by reference herein,

including any free writing prospectus prepared by us or on our behalf, including the sections entitled “Risk

Factors” and “Forward-Looking Statements” included elsewhere in this prospectus and “Risk Factors,”

“Management’s Discussion and Analysis of Financial Condition and Results of Operations,” our audited

consolidated financial statements and related notes thereto in the Annual Report incorporated by reference herein,

and our unaudited interim consolidated financial statements and related notes thereto in the Q1 Quarterly Report

incorporated by reference herein, before making an investment decision. Some of the statements in this prospectus

are forward-looking statements. See “Special Note Regarding Forward-Looking Statements.”

Our Mission

Our mission is to create a smarter, more resilient insurance platform powered by AI, data science, and

technology, enabling insurers to deploy capacity with confidence and delivering instant access to coverage for

policyholders and agents.

Company Overview

Neptune is a leading, high-growth, highly profitable, data-driven managing general agent that is revolutionizing

the way homeowners and businesses protect against the growing risks of flooding. We offer a range of easy-to-

purchase residential and commercial insurance products — including primary flood insurance, excess flood

insurance, and parametric earthquake insurance — distributed through a nationwide network of agencies. Neptune

does not take any balance sheet insurance risk or have claims handling responsibility relating to the policies we sell.

We underwrite and administer the issuance of insurance policies on behalf of a diverse panel of insurance and

reinsurance companies, whom we refer to as capacity providers, that manage both this risk and the associated claims

handling. From day one, we have built our business on a foundation of advanced data science and AI, leveraging

proprietary ML algorithms, which has led to superior underwriting results, outsized growth, recurring revenue, and

robust margins, including delivering a lifetime written loss ratio of just 24.7% to our capacity providers from our

inception through June 30, 2025. In addition, for the year ended December 31, 2025, we achieved 33.7% organic

revenue growth, 23.4% net income margin, and 59.5% Adjusted EBITDA margin, and for the three months ended

March 31, 2026, we achieved 28.8% organic revenue growth, 19.4% net income margin and 57.1% Adjusted

EBITDA margin.

Neptune was founded to solve the inefficiencies and poor product-market fit we saw in the traditional flood

insurance market, which we believe represents a significant and underpenetrated opportunity. According to the

American Housing Survey and the Energy Information Administration, there are over 100 million residential and

commercial buildings in the U.S., many of which face flood risk, yet only a small fraction are covered by flood

insurance. Today, the largest provider of flood insurance in the United States — and the holder of the majority

market share — is the National Flood Insurance Program, a U.S. government-run entity and our main competitor.

We believe purchasing insurance from the NFIP is relatively burdensome and time-consuming for policyholders and

agents, and that its limited product offerings often fail to meet policyholder needs. In addition, the NFIP has

historically received substantial government subsidies that have enabled it to limit premiums to rates that have been

challenging for private flood insurance providers to compete with, a dynamic that is shifting with the NFIP’s 2021

introduction of its “Risk Rating 2.0” pricing model, discussed in more detail below. Private market participation has

also historically been constrained by regulatory barriers, a lack of innovation expertise, and limited access to

sufficient claims and performance data to optimize pricing and underwriting decisions. We believe that Neptune’s

position as the first scaled private flood platform, including the years of claims and performance data we have

generated through our operations, provides a key early-mover advantage in addressing all of these challenges and

disrupting the industry.

With Neptune’s use of AI, our technology platform, and our data-driven approach, we believe we have

delivered the promise of disrupting the insurance industry. Not only have our innovation efforts delivered vastly

6

improved policyholder and agent experiences through the ease-of-use of our proprietary underwriting (Triton) and

policy management (Poseidon) platforms, we have also demonstrated superior risk selection and underwriting

through our top-tier financial performance and sustained growth. Utilizing AI and ML algorithms with no human

underwriters, Neptune has redefined how flood insurance can be underwritten, creating value for policyholders and

agents while producing consistent, long-term positive returns for our insurance and reinsurance partners. Further, as

the NFIP moves away from its historical subsidized pricing model, we believe our Triton platform, backed by years

of proprietary data derived from our business operations, positions us to optimize pricing determinations and

compete for existing NFIP policyholders in a way that would be challenging for a new entrant to replicate until it is

able to generate, or otherwise gain access to, comparable claims and performance data.

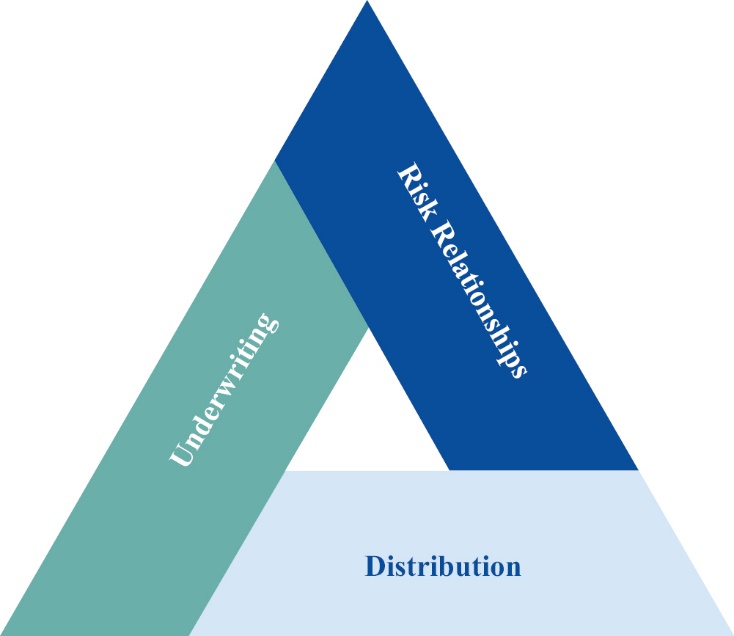

Technology and data science are the foundation of Neptune’s business model, driving our three core pillars:

•Our Underwriting Engine: Our entirely digital underwriting engine, Triton, uses advanced technology,

including proprietary AI and ML models, without any human underwriters, to assess risk with speed and

precision. Powered by predictive analytics and loss estimation, Triton has enabled Neptune’s policies to

consistently outperform the NFIP in written loss ratio despite 21 landfall hurricanes — including 4 of the

10 largest flood events in U.S. history — taking place since Neptune’s founding.

•Our Risk Relationships: Our risk relationships are built on performance and trust, and we currently have

42 capacity providers, including 34 reinsurance providers, backing 8 distinct insurance programs to help

minimize concentration risk while delivering consistent returns. In turn, the accuracy of our risk assessment

and our precision pricing have delivered hundreds of millions of dollars of underwriting profit for our

capacity providers since inception, leading to high rates of capacity renewals and increases in committed

capacity.

•Our Distribution: Our distribution strategy is primarily focused on deep partnerships across agencies

with tens of thousands of agents who benefit from the ease-of-use of our automated underwriting platform,

seamless API integrations, instantaneous bindable quotes and proprietary Agent Portal built with an AI-

powered sales enablement and education platform. We believe this is a meaningful departure from industry

norms and makes our approach to distribution attractive to the agents with whom we work.

The three pillars above interlock, creating a powerful and reinforcing loop. Unlike traditional insurance

underwriting that historically relied on humans, static models, and infrequent adjustments, we leverage an iterative

approach that allows us to consistently and rapidly integrate new data and models into our underwriting engine,

thereby refining our processes and adapting to evolving market and environmental conditions. As our models

constantly evolve and improve, they are able to deliver superior results that minimize losses for our capacity

providers, which in turn grant us additional underwriting capacity. With more capacity available, we can offer

coverages our policyholders want, enhancing the ability for our agency partners to easily sell policies while

expanding our distribution and reach. The resulting increase in quoted and bound policies provides us with access to

more data, enhancing the predictive capabilities of our underlying models.

We operate as an MGA, with a highly profitable, recurring, fee-based revenue model derived from two primary

sources: commissions paid by capacity providers, and fees paid by policyholders. Commissions are calculated as a

negotiated percentage of premium for each policy. As of March 31, 2026, our average commission rates have

increased by 4.7% since 2018, as capacity providers continue to recognize our superior underwriting performance.

Given our high retention rates to date, we believe that we have a high degree of visibility into our future revenue

streams. For example, for the three-month period ended March 31, 2026, our eligible policy and premium retention

rates at renewal were 86.2% and 92.9%, respectively. The difference between policy and premium retention rates

reflects increases to the rates charged to renewing policyholders.

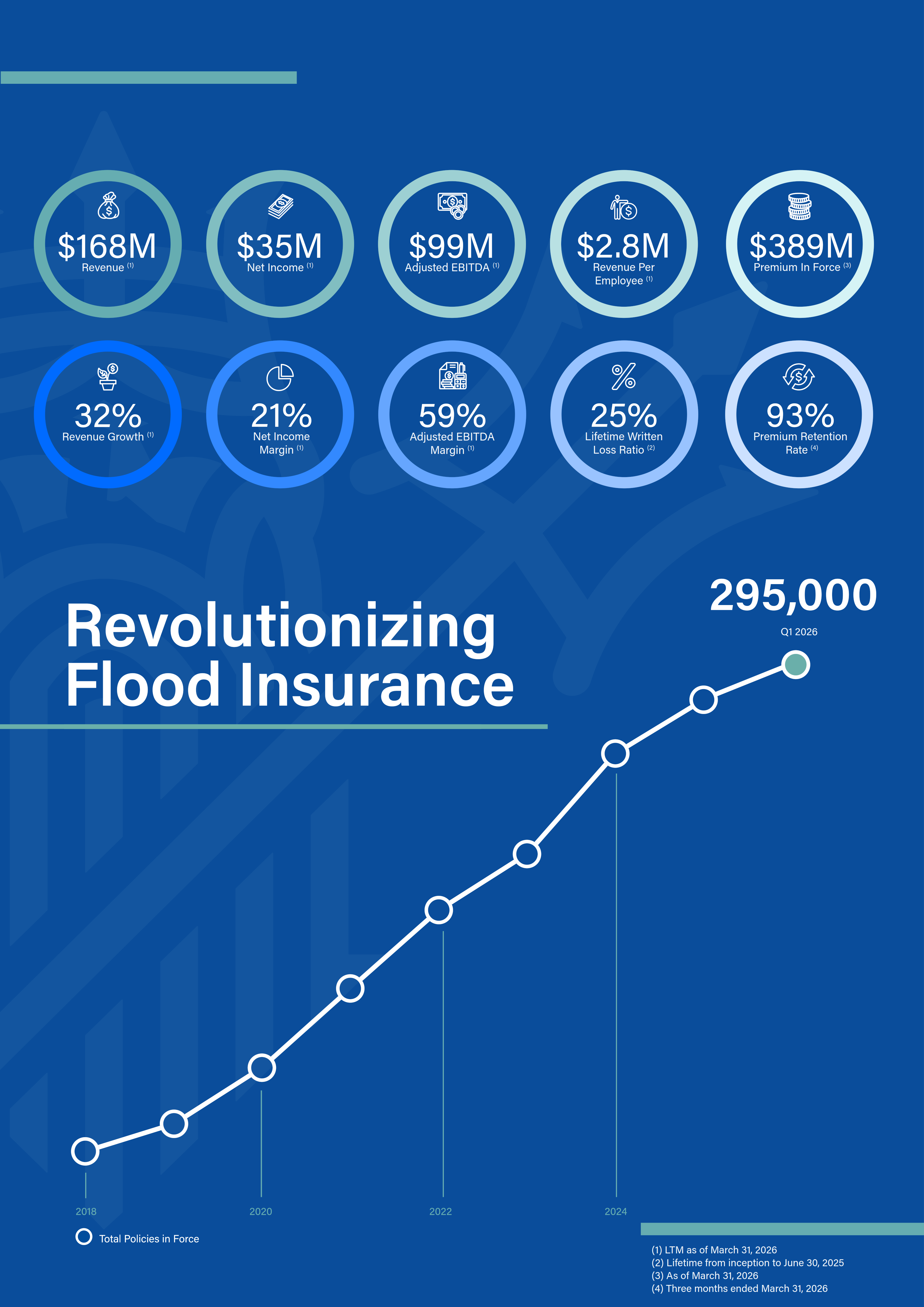

As of December 31, 2018, the end of our first full year of operations, we had $4.4 million of premium in force

with one insurance program. As of March 31, 2026, we have achieved remarkable growth. Since 2018, our premium

in force has increased at a CAGR of 88.3% to $370.2 million as of December 31, 2025, and $388.7 million as of

March 31, 2026. For the year ended December 31, 2025, we generated $159.6 million in revenue, $37.4 million in

net income, and $95.0 million in Adjusted EBITDA, which translates to $2.8 million in revenue per employee and

7

$1.6 million in Adjusted EBITDA per employee, a 23.4% net income margin and a 59.5% Adjusted EBITDA

margin. In addition, for the three months ended March 31, 2026, we generated $37.8 million in revenue, $7.3 million

in net income, and $21.6 million in Adjusted EBITDA, which translates to a 19.4% net income margin and a 57.1%

Adjusted EBITDA margin. For the twelve months ended March 31, 2026, we generated $168.0 million in revenue,

$34.8 million in net income, and $99.5 million in Adjusted EBITDA, which translates to $2.8 million in revenue per

employee and $1.7 million in Adjusted EBITDA per employee, a 20.7% net income margin and a 59.2% Adjusted

EBITDA margin. Our Adjusted EBITDA margin has consistently exceeded 54.0% over the past four years, thanks

to the operational leverage inherent in our technology-first business model. Notably, our organic revenue for the

year ended December 31, 2025, increased by $40.3 million, or 33.7%, year-over-year. For the year ended

December 31, 2025, we also generated net cash provided by operating activities of $51.7 million. As of March 31,

2026, we had negative book value per share due to our history of paying dividends to our stockholders, which have

been financed through a combination of debt and redeemable, convertible preferred stock financings, and cash flows

generated from our business operations. Since inception, we have made dividend payments to our stockholders

totaling approximately $605.0 million.

Organic Revenue

($MM)

YoY Organic Revenue Growth % | 63% | 37% | 41% | 34% | 32% |

YoY Premium in Force Growth % | 61% | 41% | 36% | 33% | 32% |

Net Income

($MM)

Premium in Force

($MM)

Adjusted EBITDA

($MM)

Net Income Margin % | |||||

34% | 29% | 21% | 29% | 23% | 21% |

Adjusted EBITDA Margin % | |||||

50% | 55% | 57% | 60% | 60% | 59% |

8

Our Technology and AI

We built Neptune as an AI-native, API-first platform from the ground up with machine learning models that

underpin pricing, underwriting, portfolio management, and distribution across what we believe is the largest private

flood dataset in the United States. Approximately 40% of our employees are engineers or data scientists and by

design, our entire infrastructure was built to evolve. We believe AI is a tailwind for us – our workflows are natively

digital; we do not have manual underwriters to replace; and we are not burdened by legacy technology systems.

Additionally, our continued focus on automation, model enhancements, and platform scalability using the latest

tools continues to deliver measurable performance improvements and productivity gains. Our 12-month revenue per

employee increased 17.3% to $2.8 million and Adjusted EBITDA per employee increased 14.8% to $1.7 million.

Our flexible platform supports the scalability and reach of our business. The faster, easier, and more

comprehensive flood product we are able to offer to agents and customers, the more volume we see and the stronger

our dataset gets. Over years, we have assembled proprietary flood risk data, behavioral retention data, claims

performance insights, and real-time transaction signals that we believe no competitors can replicate by just adopting

a large language model. We believe the data at our scale in our domain is a structural barrier to entry and we believe

the moat widens over time.

Our Unique, Data-Driven Approach

Data science is our guiding principle, driving innovation that we believe enables us to deliver fast and accurate

insurance solutions that are policyholder-centric, more efficient for our agents, and that deliver consistent

underwriting profits for our capacity providers.

Our internally-developed and proprietary technology platforms include Triton, our underwriting engine, and

Poseidon, our policy management system, which are closely integrated and easy to use. The key features of our data

science approach that underpin our platforms include:

•Precise Pricing Models: Our models leverage advanced ML and data analysis to evaluate flood risks at

the individual property level. By incorporating real-time data, including from geospatial mapping as well as

predictive analytics, we deliver competitive, risk-adjusted pricing that reflects the unique risk of each

property. The precision of this data-driven approach empowers us to offer instant underwriting decisions

and bindable quotes at scale, with a level of intention and sophistication in our risk selection that we believe

sets us apart in the industry and that results in a high degree of predictability in our business outcomes.

•Automation and Efficiency: We operate with the mantra of “automating everything.” We constantly

focus on reducing manual processes across our operations and enabling our team to concentrate on more

complex and high-value tasks.

•Scalability: Our emphasis on automation in our technology infrastructure allows us to process tens of

thousands of quotes daily, providing the scale necessary for rapid growth and market expansion without a

proportional increase in headcount. The elevated volume we experienced during the federal government

shutdown in October and November 2025 highlighted the best-in-class, fully digital nature of our platform.

Increased activity drove strong growth in sign-ups, quotes, and bound policies, all while performance,

reliability, and service levels remained constant.

•Agility: Our platform has demonstrated a great degree of flexibility, seamlessly incorporating new perils

and geographies over time in response to the evolving needs of policyholders and agency partners, and with

minimal incremental costs.

•Ease of Use: Our platforms are designed with a focus on simplicity and accessibility. Agents and

policyholders can obtain quotes, purchase policies, and manage policyholder coverage in just minutes

through our streamlined online interface. In many cases, the creation of a Neptune quote is automatic and

instantaneous for agents via our API, allowing seamless cross-sell opportunities alongside standard home

and business insurance quotes. We believe this ease of use and quote-to-issue process differentiates

Neptune from traditional insurance providers and has been a key driver of our success.

9

Triton and Poseidon were built entirely in-house by our Neptune Engineering Group. These platforms are

powered by ML models centered around our vast proprietary datasets, which are developed and maintained by the

in-house Neptune Data Science Group and are generated from data collected through the operation of our business,

including quote requests, the policies we have bound, and the losses incurred on the policies we have sold. Triton

processes over 20,000 quotes on a typical day. As of March 31, 2026, Triton has provided approximately 34.4

million quotes, underwritten 13.3 million properties, and bound 1.4 million policies across the U.S. since inception,

providing Neptune with what we believe is the largest flood insurance sales and claims database outside of the

NFIP.

Our systems continually update and constantly learn and improve from the expansive datasets generated by our

daily operations, helping us stay ahead of the curve in understanding flood risk. In March 2026, we released the

570th product version of our underwriting model, demonstrating our commitment to continued improvements.

From a risk selection perspective, we believe our focus on data science has allowed us to provide a more

accurate estimate of likelihood of loss across our portfolio compared to the industry. This has allowed us to deliver

superior written loss ratios for our capacity providers. Despite navigating some of the largest flood disasters in

U.S. history, our Triton underwriting platform has delivered a lifetime written loss ratio of just 24.7% from our

inception through June 30, 2025. For example, in 2024, Hurricane Helene devastated parts of Florida and North

Carolina as the fourth most expensive flooding event in NFIP history. The written loss ratio on that storm for

policies sold by Neptune was 17.0% while the NFIP produced a written loss ratio of 169.6%. At the time of the

storm, we had approximately 74,000 policies in force in the affected states of Florida, North Carolina, and

Tennessee.

In 2024, we also implemented an ML-driven renewal optimization model, which has had a measurable impact

on policy retention rates. This model enabled more precise identification of policyholders at risk of non-renewal and

allowed for targeted engagement strategies, driving an increase in policy retention from 85.7% for the three months

ended March 31, 2025, to 86.2% for the three months ended March 31, 2026.

As our business grows, this strong retention rate has resulted in an increasing share of our portfolio consisting of

tenured policyholders. As of March 31, 2026, 68.5% of our premium in force was associated with policies in a

renewal term, and these policies accounted for 64.3% of our policies in force.

Our Industry

Our Market Opportunity

We operate in the large and growing flood insurance market. According to FEMA, flooding is the most

common and costly natural disaster in the U.S., causing damages that exceed $40 billion annually according to the

Congressional Budget Office, and is expected to continue to grow with progressing climate change. Despite the

growing risk, flood insurance penetration remains low.

10

In the U.S., there are more than 100 million residential and commercial buildings, and we believe more of these

buildings are likely to be at risk of flooding than is currently identified by FEMA. According to First Street’s First

National Flood Risk Assessment, in 2020 there were approximately 22 million buildings at risk of flooding and over

14 million buildings at risk of substantial flooding over the following 30 years. However, only approximately

9 million buildings are identified by FEMA as being within Special Flood Hazard Areas — regions with 1% or

higher annual probability of flooding. Properties in SFHAs with federally backed mortgages are required by the

FDPA and related regulations to have flood insurance. Yet FEMA has noted that flood maps that underlie the SFHA

designations are outdated and require extensive updates, as they do not currently take into account key types of

precipitation. This was highlighted during Hurricane Harvey (2017) when, despite lower flood insurance penetration

rates than in SFHAs, 68% of reported claims in Harris County were outside SFHAs according to Harris County

Flood Control District.

Outside SFHAs, we estimate that flood insurance uptake in general is inadequate, with only approximately 2%

of properties being covered by flood insurance, representing vast underinsurance and what we believe is a

significant and untapped addressable market for our products. Even in high-risk states such as Florida, Texas, and

Louisiana, combined residential penetration is below 13% according to NFIP Residential Penetration Rates as of

January 2, 2025. We believe this gap in flood insurance coverage, together with the limited designation of SFHAs,

creates significant financial vulnerabilities for millions of American home and business owners and lenders and

presents a substantial opportunity for innovative private-sector insurance solutions like Neptune.

NFIP Challenges and Developments

Historically, the flood insurance market offered limited options, as regulated lending institutions were required

to accept only policies underwritten by the NFIP to satisfy mortgage requirements. In 2012, however, Congress

passed the Biggert-Waters Flood Insurance Reform Act of 2012, mandating that lenders also accept private flood

insurance policies if written on an NFIP-equivalent form. Despite this regulatory opening, to date, the NFIP has

continued to dominate the market, as private insurers have lacked the expertise, innovation, and access to historical

claims data necessary to profitably underwrite flood risk. In addition, the NFIP historically received substantial

government subsidies that enabled it to limit premiums to rates that were challenging for private flood insurance

providers to compete with, a dynamic that is shifting with the NFIP’s introduction of “Risk Rating 2.0,” discussed in

more detail below.

As of December 31, 2025, the NFIP insured approximately 3.6 million properties and collected approximately

$5.5 billion in total policy cost, with an average annual policy cost of $1,548 per policy, according to FEMA. We

believe the NFIP falls short in meeting the evolving needs of homeowners and businesses. For decades, its policies

have provided low coverage limits that often fail to address the true costs of rebuilding. Moreover, the process of

purchasing NFIP coverage can be slow and cumbersome for both policyholders and agents, in contrast to the

instantaneous and accessible Neptune quote-to-issue process.

Operational and financial challenges have also persisted throughout the NFIP’s history. We believe these issues

stem from its subsidized and rudimentary pricing methodology, which has frequently failed to accurately reflect the

underlying risk of policies. As a result, the NFIP has accumulated substantial financial losses, currently owing

$22.525 billion to the U.S. Treasury and accruing approximately $2 million in daily interest, according to FEMA

and the Congressional Research Service.

In 2021, the NFIP launched Risk Rating 2.0, a new pricing methodology aimed at better aligning premiums

with the risk profile of a given property. Under Risk Rating 2.0, most policyholders will experience annual rate

increases of up to 18%, the maximum allowed under congressional caps, until their premiums reach full risk-based

levels. The U.S. Government Accountability Office estimates that approximately $27 billion in additional subsidies

will be required for the NFIP portfolio between 2022 and 2037 due to these price caps. While this subsidized pricing

model historically allowed the NFIP to price policies at rates that limited our ability to compete for those policies, as

subsidies phase out under Risk Rating 2.0, we expect the gap between NFIP rates and actual risk costs to narrow,

positioning Neptune to offer more affordable coverage to approximately 50-60% of current NFIP policyholders,

representing approximately 50-70% of the NFIP’s premium base.

11

We believe the NFIP’s legacy pricing model, cumbersome processes, and limited coverage have created

significant market dislocation and inefficiencies, resulting in a compelling opportunity for private flood insurers like

Neptune to capture market share.

Industry Tailwinds

We believe there are several additional structural shifts that will continue to drive opportunities in the flood

insurance market broadly and for private providers such as Neptune, including:

•Increased Demand Driven by Growing Natural Disaster and Flood Damage: As climate change

intensifies, areas with low perceived flood risk today (e.g., non-coastal regions) could face increased

frequency and intensity of flooding due to additional rainfalls and storms. As climate change continues to

intensify, associated with increasing severity of storms and resulting losses, we expect the demand for flood

insurance to increase. Additionally, more areas with severe inland flooding could be designated as

mandatory flood insurance zones for policyholders with federally-backed mortgages.

•Underlying Housing Market Backdrop: The housing market significantly influences property and flood

insurance sales, as a substantial portion of policies are purchased during home acquisitions or refinancings.

If housing market activity were to increase, a revitalized housing market would likely also stimulate growth

in the property and flood insurance sector, presenting opportunities for insurers to expand their

policyholder base and enhance market share. At the same time, with housing prices increasing above the

rate of inflation, the NFIP coverage limit of $250,000 — which was first implemented in 1994 and has

remained static since — grows more outdated each year, prompting policyholders to look to the private

market for excess or replacement coverage. We believe that Neptune, with its advanced technology,

policyholder and agent-first approach, coverage limit of over $7,000,000 for residential properties, and

innovative products, can be at the forefront of capitalizing on this potential growth, were it to materialize,

and closing the insurance gap.

Our Business Model

Our team’s energy is focused, every day, on advancing the three pillars of our business: underwriting, risk

relationships, and distribution.

Underwriting

Our automated underwriting engine, Triton, is at the core of everything we do. Our use of the latest ML

technology, advanced data science, AI, and behavioral economics allows us to execute key underwriting

12

tasks — including risk selection, accurate risk pricing, aggregation management, and carrier assignment — in less

than two seconds. This combination of speed and precision provides robust scalability and enables us to process high

volumes of quotes and policies efficiently while maintaining industry-leading performance. We have no human

underwriters and 100% of our underwriting is performed instantaneously by our Triton engine.

__________________

(1)We had approximately 27,021 policies in force in states with flood insurance claims related to Hurricane Ida.

(2)We had approximately 51,562 policies in force in states with flood insurance claims related to Hurricane Ian.

(3)We had approximately 102,426 policies in force in states with flood insurance claims related to Hurricane Helene.

(4)We had approximately 80,266 policies in force in states with flood insurance claims related to Hurricane Milton.

Our underwriting engine has delivered positive results, including a lifetime written loss ratio of just 24.7% from

our inception through June 30, 2025. This performance has spanned some of the largest flooding disasters in

U.S. history — including four of the ten largest flooding events in U.S. history, as measured by NFIP insured loss:

Hurricane Ida (2021), Hurricane Ian (2022), Hurricane Helene (2024), and Hurricane Milton (2024). By contrast,

from 2018 to 2024, the NFIP has delivered an 86% written loss ratio according to FEMA and the U.S. property and

casualty industry in general has seen an average written loss ratio of 54% according to NAIC statutory data.

Our underwriting philosophy is generally built around three fundamental principles:

•Risk Selection: Our approach to risk selection is driven by data science and informed by what we believe

is the most comprehensive claims dataset in the private flood insurance market, generated predominantly

from our operations to date. With over a quarter billion dollars in paid claims across our portfolio since

inception, and our extensive analysis of industry claims and performance data, we have developed deep

insights into identifying and managing properties with the highest probability of flood losses.

We believe we can evaluate property-specific risks with exceptional accuracy. Our proprietary models

identify the characteristics and factors most likely to contribute to large-scale losses, allowing us to focus

on selecting risks that align with the risk tolerances of our capacity providers. This granular approach helps

us avoid adverse selection and has allowed us to deliver consistent, positive underwriting results. It has also

allowed us to provide quotes for 95% of all submissions, optimizing the identification of properties with the

highest probability of flood losses.

Through ongoing analysis of claims data and continuous refinement of our underwriting models, we ensure

that our risk selection process remains sophisticated and nimble. By focusing on selecting the right risks,

we aim to deliver value to both our capacity providers and our policyholders while maintaining a

sustainable and profitable portfolio.

•Pricing: Our pricing is a sophisticated, data-driven process that incorporates advanced ML and

behavioral economics to ensure accuracy and market competitiveness. Rather than relying on static or

13

simplistic pricing models, we use a proprietary technology-driven framework to evaluate the unique

characteristics of each property and its risk profile. Our pricing methodology is informed by a combination

of flood risk data, customer behavior, and market dynamics. Behavioral economics plays a crucial role in

determining how customers perceive and value coverage, and incorporating customer behavioral factors

into our methodology enables us to tailor pricing to increase adoption while maintaining underwriting

integrity. By understanding not only the risk, but also the behavior of customers, we believe we can

optimize premium structures to drive growth and retention.

Unlike traditional insurance underwriting, our pricing does not depend on manual adjustments or broad risk

groupings. Instead, it is dynamically informed by hundreds of data points to assess factors such as property

characteristics, geographic exposure, and historical loss data. This property-specific, data-first approach

allows us to quickly offer fair and competitive pricing while aligning with the risk tolerance of our capacity

providers and continuously improving the accuracy of our Triton underwriting system.

•Aggregation Management (Disaggregation): Our approach to aggregation management is a key

differentiator that sets us apart from industry norms. Traditional underwriting and risk assessment methods

often rely on generalized risk aggregation based on administrative boundaries, such as states or counties,

which serve as crude proxies for exposure to catastrophic events. In contrast, we have developed a patented

technology that enables us to manage maximum loss scenarios at the individual property level through an

analysis that uses radial circles to assess policy concentration in any given area in real time. This advanced

methodology, which we refer to as “disaggregation,” allows us to optimize risk exposure in real time and

align each policy with the specific risk appetite of our capacity providers.

By moving beyond man-made legacy geographic boundaries, we can more effectively distribute exposure

to minimize concentration risk while focusing on the actual drivers of loss, such as property-specific

vulnerability to flood. This precision also allows us to confidently underwrite in high-cost insurance

markets, including hurricane-prone areas, while continuously informing and refining our pricing models to

remain both responsive and data-driven.

Our disaggregation framework also leverages real-time data to adjust exposure dynamically as policies are

written. This sophisticated approach enables us to manage risk with precision, which we believe maintains our

capacity providers’ confidence in our ability to deliver consistent, positive underwriting performance. Through our

patented technology and innovative methodology, we not only provide accurate risk management for our capacity

providers but also ensure long-term scalability and sustainability for our business.

Risk Relationships

Neptune does not take any balance sheet insurance risk or have claims handling responsibility relating to the

policies we sell. We currently contract with 8 distinct insurance programs, which are supported by 34 reinsurance

providers, all of whom collectively provide underwriting capacity for the policies we sell. We refer to this panel of

global insurers and reinsurers as our “capacity providers,” who bear all of the balance sheet insurance risk associated

with our underwriting. Although we do not directly contract with the reinsurance providers who support our

insurance programs, we engage and cultivate relationships with them, and believe that the superior written loss ratios

and underwriting results we are able to deliver on the policies we sell incentivizes these reinsurance providers to

provide underwriting capacity in support of our insurance programs.

Over the past 8 years, we have built and expanded a panel of 42 capacity providers, including some of the

largest insurance and reinsurance companies in the world. The strength and reputation of our capacity providers

underscores the market’s confidence in our ability to deliver consistent results and manage risk effectively. Our

insurance carriers are high-quality international insurers with A.M. Best ratings of A- or higher and our 34

reinsurance providers, supporting 8 distinct insurance programs, diversify our risk across both program structures

and ultimate risk takers. As of March 31, 2026, our largest capacity provider accounted for 15.3% of our dollar-one

premium risk. In addition, all of our insurance programs are eligible to write policies in all 50 states and Washington

D.C. This approach mitigates concentration risk on both a financial and geographic basis, provides stability for both

14

our business and our capacity providers, and ensures our portfolios remain resilient with access to ample future

capacity to continue to grow our business.

In the twelve months ended March 31, 2026, we doubled the number of capacity providers on our panel,

growing reinsurance panels on existing programs, and adding two new programs. Included in this growth was a new

relationship with Palomar, through which Neptune became Palomar’s exclusive MGA for flood insurance.

The relationships we have cultivated with our capacity providers are built on transparency, trust, and our

unwavering commitment to delivering value. A key driver of our success is the availability of detailed data and

insights, paired with our ability to deliver results with speed and efficiency. We provide real-time access to

performance metrics, maintain an open and continuous dialogue with our capacity providers, and consistently

exceed expectations with profitable underwriting results.

We have also delivered consistent and substantial premium growth for our capacity providers and our proven

performance has been instrumental in driving partner confidence and growth and engagement with additional

reinsurers who may wish to provide underwriting capacity for our insurance programs. Through the exceptional

written loss ratios experienced by our capacity providers on policies sold by Neptune, driven by the dynamic, risk-

adjusted pricing and coverage decisions made by our Triton platform, we have been able to deliver superior returns,

even through some of the largest flooding events in U.S. history. As a result, we have delivered hundreds of millions

of dollars of underwriting profits for our capacity providers since inception and have delivered underwriting

profitability to every capacity provider in every contract year. These outcomes are a testament to our platform

capabilities and our success has led to an increase in the average commission paid to us by our capacity providers of

4.7% between 2018 and March 31, 2026.

These results, combined with our ability to provide actionable insights, have attracted new capacity providers

and strengthened relationships with existing ones. Our proven underwriting results have also generated meaningful

goodwill with our existing capacity providers, allowing us to enhance and develop our product offerings efficiently

to respond to agent and policyholder needs.

The following information showcases the expanding nature of our capacity relationships since inception.

Premium in Force by Program

($MM, colors represent each of the

respective insurance programs)

Capacity Providers

(#)

Programs

(#)

Distribution

Our distribution strategy is built to maximize market reach and provide seamless access to our innovative flood

insurance products with diversification across distribution partnerships. Leveraging a hybrid distribution model, we

utilize strong agency partnerships across the insurance industry and complement those with direct-to-customer sales

to drive efficiency, reach, and scale. Our platform is natively built in digital workflows, allowing us to seamlessly

respond to evolving consumer purchasing behaviors.

Agent and Broker Partnerships: The cornerstone of our distribution network is our deep relationships with

insurance agents and brokers. As of March 31, 2026, 96.8% of our policies in force are driven by these partnerships,

15

which include more than 25,000 unique agency codes that have bound a policy through Neptune and over 114,000

unique agency codes that have run a quote through our Triton platform.

Since inception, we have been able to grow our distribution network tremendously and uninterruptedly. As of

March 31, 2026, 25,098 cumulative agency codes have bound a policy with Neptune, an increase of 23.5% from

19,191 as of March 31, 2025.

Unique Agency Codes with Policy Bind

(thousands)

2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 | |||||||||||||||||||||

Annual Growth: | 332% | 118% | 70% | 35% | 26% | 26% | 30% | |||||||||||||||||||||

More recently, we have moved from tracking agency codes to tracking individual users. With over 45,000

active users, we believe we have greater visibility into agent-level behavior, enabling more targeted outreach, better

enablement, and a clearer picture of where production opportunities exist.

We believe that Neptune delivers significant value to agents through a combination of ease of use, a superior

product-market fit, high availability — made possible by our quoting of 95% of all submissions — and our ability to

deepen agents’ relationships with policyholders. Historically, agents have had to undergo NFIP training and engage

in the cumbersome NFIP quoting process to sell flood insurance policies. With Neptune, agents can leverage our

user-friendly Agent Portal to quickly enter customer data and receive instantaneous quotes, which they can relay in

real-time, thereby democratizing the sale of flood insurance. To further enhance the agent experience, we have

developed deep technology integrations with many of our agency partners through API links directly into their

quoting systems, allowing them to quickly quote and bind flood policies alongside homeowner policies and provide

comprehensive solutions for their customers. In addition, our Agent Portal provides our agents with up to date, data-

driven insights about flood risk in the geographies where a quote is being sought, empowering our agents to drive

further demand for our products at the time of each quote. Our recently launched AI-powered sales assistant, Atlas+,

is an entirely redesigned and proactive approach to agent engagement. Built directly into our Agent Portal interface,

Atlas+ provides agents with actionable suggestions and information to improve their ability to convert leads into

sales. Through these innovations, our platform enables agents to grow their business by enhancing the overall value

of the policyholder relationship, while offering a product that seamlessly fits the needs of both agents and

policyholders. This in turn drives increasing adoption and higher conversion rates.

We believe our deep relationships with high quality agencies are critical in maintaining our early-mover

advantage. Our agency partners include carriers with large captive agent forces, wholesalers, agency networks, flood

specialists, and small, independent, family-owned agencies. Our ability to offer an alternative product that better fits

many customers’ needs has resonated with our agents and has been essential to driving over 60.0% of our new

policy sales in “non-mandatory flood zones” over the last three years. Furthermore, our policies in force are highly

16

diversified across a network of high-quality agents, without any material concentration risk or reliance on individual

agencies or agents. As of March 31, 2026, our largest agency partner contributed approximately 8.5% of our total

policyholder base. We maintain a robust pipeline of potential agencies interested in partnering with Neptune, while

our in-house sales team continually nurtures existing relationships, supporting strong alignment with our agency

partners and mutual growth. Our agency relationships are deeply entrenched at the agent level and play an active

role in both converting NFIP policyholders to Neptune and winning new customers to the flood insurance market to

enable our continued expansion.

Neptune Internal Agency: 2.1% of our policies in force as of March 31, 2026, were attributed to our in-

house agency, with a team of licensed agents managing a growing number of quotes from our website and a select

few of our distribution partners. These agents are also licensed to distribute NFIP policies in certain rare cases where

policies do not meet Triton’s underwriting criteria.

Direct-to-Customer Sales: 1.1% of our policies in force as of March 31, 2026, were attributed to our direct-

to-customer channel. Our easy-to-use online interface allows prospective customers in select states to quote, bind,

and manage policies directly. This option complements our agency partnerships and provides ease of access for all

property owners seeking flood insurance solutions. We support our online interface with our third-party agencies

and in-house agency able to assist when required or to otherwise finalize the sales process. We recently made

Neptune available as a native app inside ChatGPT, allowing consumers to get a preliminary quote in seconds and

explore coverage options in the chat interface. While we expect the agent channel to continue to play an important

role in expanding the market, our technology is designed to be able to capture new and evolving volume regardless

of the channel.

In addition to driving scalability and flexibility, as we rapidly expand into new markets and introduce additional

products, our distribution infrastructure is critical in reinforcing our data advantage. Our distribution and referral

partners submit over 20,000 quotes to Triton on a typical day, with approximately 34.4 million lifetime quotes and

1.4 million binds from inception through March 31, 2026. All these quotes (whether or not they lead to binds) and

binds fold into and grow our proprietary dataset, allowing us to continually build the competitive advantage

provided by our platform.

The following information illustrates the cumulative quotes and binds on our Triton and Poseidon systems since

inception in 2018.

Cumulative Triton Quotes

Proprietary Underwriting System

2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

17

Cumulative Poseidon Binds

Proprietary Policy Management System

2018 | 2019 | 2020 | 2021 | 2022 | 2023 | 2024 | 2025 |

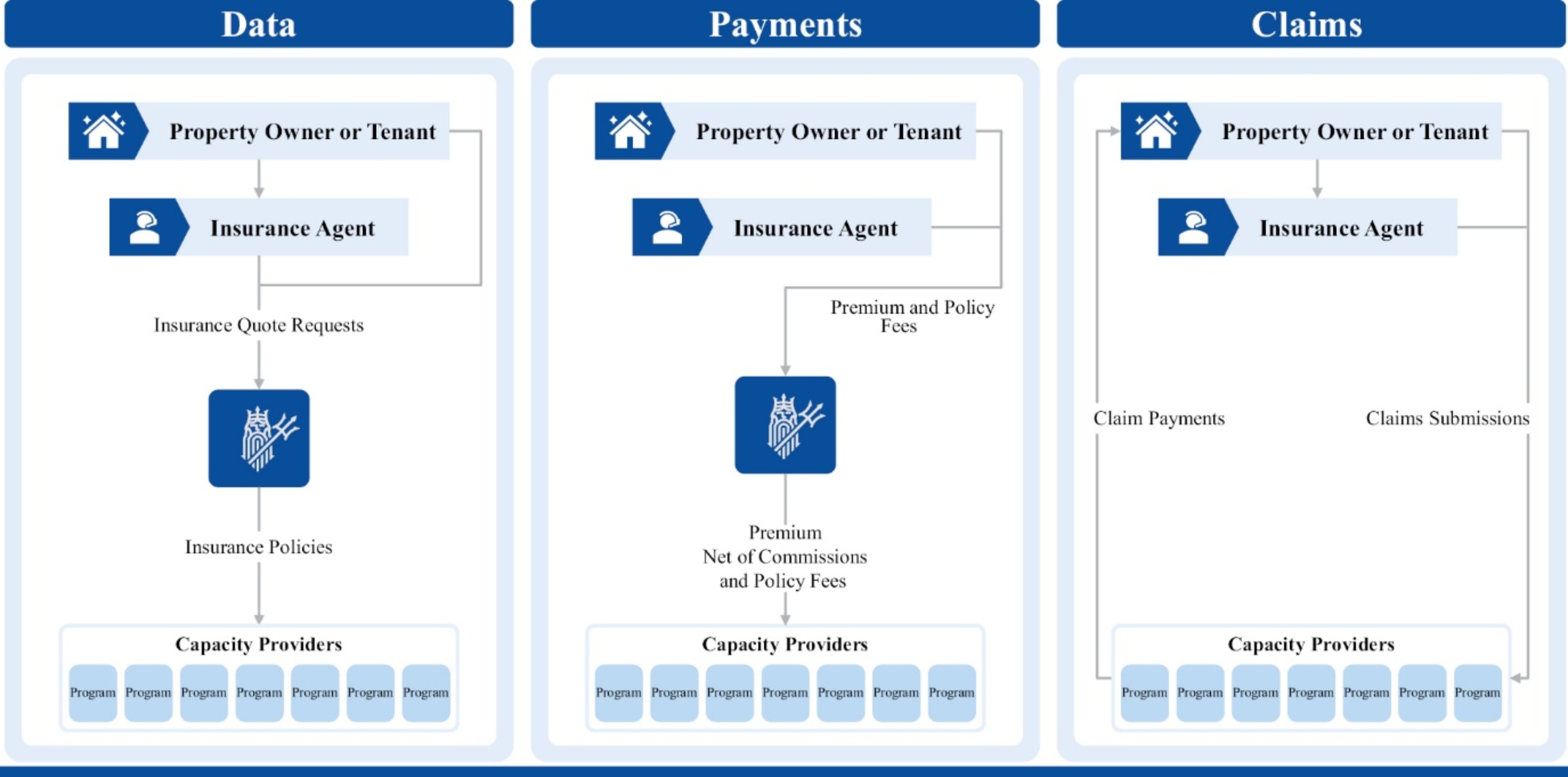

In addition, below is a chart demonstrating the roles we, our capacity providers, and our distribution partners

play in the flow of data and payments, and the role our capacity providers and distribution partners play in the flow

of claims from policyholders:

We offer a range of innovative insurance products designed to address the needs of residential and commercial

property owners facing flood and other natural disaster risks. As of March 31, 2026, across all of our insurance

product offerings, residential properties accounted for 88.1% of our premium in force and commercial properties

accounted for the remaining 11.9%. Our flagship primary residential flood insurance product accounted for 85.9% of

our premium in force as of March 31, 2026. In addition to the base policy, we offer enhanced protection through

expanded coverage options, which we believe make our flood insurance product a superior coverage alternative to

the NFIP. We also offer an excess flood insurance product, which we introduced in 2024. This product, which is

available to both residential and commercial property owners, represented 2.9% of our premium in force as of

March 31, 2026. Both our primary and excess flood insurance products are structured around the NFIP form and can

be used to supplement or fully replace existing NFIP coverage, as needed. In addition to our flood insurance

products, we offer a parametric earthquake insurance product, launched following our acquisition of Jumpstart in

September 2021, and in December 2025 we launched a beta test of an indemnity earthquake product to a small

group of agencies within the state of California. While currently less than 1% of our portfolio, these earthquake

insurance products allow us to collect data and expertise that we believe will allow us to eventually diversify into

other perils and address additional unmet insurance needs.

18

Our Geographic Presence

We operate nationwide and actively mitigate our concentration risk by expanding and diversifying our portfolio

across the country. As of December 31, 2025, Florida, Texas, and Louisiana accounted for only 48.9% of our

policies in force, compared to a much heavier exposure of 59.6% for the NFIP, according to the NFIP.

The Neptune Advantage

We believe that Neptune’s competitive advantage is driven by the three core pillars of our business model

(underwriting engine, risk relationships, and distribution) and is extended by the following:

•Technology and Data-First Culture: Technology is at the heart of our capabilities and success, enabling

us to deliver innovative, efficient, and optimized insurance solutions in a simple and accessible way. As of