As filed with the U.S. Securities and Exchange Commission on May 11, 2026.

Registration No. 333-295165

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

Amendment No. 3 to

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Fervo Energy Company

(Exact name of registrant as specified in its charter)

Delaware | 4911 | 823168838 |

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification No.) |

811 Main Street,

Suite 1700

Houston, TX 77002

(832) 554-3253

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Gustavo Torres

811 Main Street,

Suite 1700

Houston, TX 77002

(832) 554-3253

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Ryan J. Maierson Nick S. Dhesi John J. Slater Latham & Watkins LLP 811 Main Street, Suite 3700 Houston, Texas 77002 (713) 546-5400 | Sarah K. Morgan Jackson A. O’Maley Alexandra M. Lewis Vinson & Elkins L.L.P. 845 Texas Avenue, Suite 4700 Houston, Texas 77002 (713) 758-2222 |

APPROXIMATE DATE OF COMMENCEMENT OF PROPOSED SALE TO THE PUBLIC: AS SOON AS PRACTICABLE AFTER THIS

REGISTRATION STATEMENT IS DECLARED EFFECTIVE.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check

the following box. ☐

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities

Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same offering. ☐

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration

statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging

growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of

the Exchange Act.

Large accelerated filer | ☐ | Accelerated filer | ☐ |

Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

Emerging growth company | ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised

financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall

file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the

Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant

to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed

with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities, and it is not soliciting an offer

to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion. Dated May 11, 2026.

70,000,000 Shares

Fervo Energy Company

Class A Common Stock

This is the initial public offering of shares of Class A common stock of Fervo Energy Company. We are offering 70,000,000 shares of our Class A common

stock.

Prior to this offering, there has been no public market for our Class A common stock. We expect that the initial public offering price per share of our Class A

common stock will be between $25.00 and $26.00. We intend to apply to list our Class A common stock on the NASDAQ under the symbol “FRVO.”

Following this offering, we will have two series of authorized common stock, Class A common stock and Class B common stock. The rights of the holders of

our Class A common stock and Class B common stock are identical, except with respect to voting, conversion and transfer rights. Each share of our Class A

common stock is entitled to one vote per share. Each share of our Class B common stock is entitled to 40 votes per share and is convertible at any time, subject to

the satisfaction of certain conditions as described herein, into one share of Class A common stock. Immediately following the completion of this offering, all

outstanding shares of Class B common stock will be beneficially owned by Tim Latimer, our Chief Executive Officer and Chair of our board of directors, and Jack

Norbeck, PhD., our Chief Technical Officer. Assuming no exercise of the underwriters’ option to purchase additional shares to cover over-allotments, if any, and

assuming Mr. Latimer and Dr. Norbeck do not purchase any shares of Class A common stock pursuant to the reserved share program, Mr. Latimer and Dr. Norbeck

will beneficially own, in the aggregate, approximately 2.75% of our outstanding capital stock and control approximately 53.03% of the voting power of our

outstanding capital stock. As a result, Mr. Latimer and Dr. Norbeck may have significant influence over the outcome of matters submitted to our stockholders for

approval, including the election of our directors and the approval of any change of control transaction. See “Principal Stockholders.”

We are an “emerging growth company” and a smaller reporting company as defined under the federal securities laws, and, as such, may elect to comply with

certain reduced public company reporting requirements. See “Prospectus Summary — Implications of Being an Emerging Growth Company and Smaller Reporting

Company.”

Investing in our Class A common stock involves risks. See “Risk Factors” beginning on page 39 to read about factors you should consider before

buying shares of our Class A common stock.

Per Share | Total | ||

Initial public offering price .............................................................................................................................................................. | $ | $ | |

Underwriting discounts and commissions(1) ..................................................................................................................................... | $ | $ | |

Proceeds, before expenses, to us ...................................................................................................................................................... | $ | $ |

__________________

(1)See the section titled “Underwriting” for a description of the compensation payable to the underwriters.

At our request, an affiliate of BofA Securities, Inc., a participating underwriter has reserved for sale, at the initial public offering price, up to 5% of the shares

of Class A common stock to be issued by us and offered by this prospectus for sale, to some of our directors, officers and employees and related persons. If these

persons purchase reserved shares it will reduce the number of shares available for sale to the general public. Any reserved shares that are not so purchased will be

offered by the underwriters to the general public on the same basis as the other shares offered by this prospectus. See “Underwriting—Reserved Share Program.”

We have granted the underwriters an option for a period of 30 days from the date of this prospectus to purchase up to an additional 10,500,000 shares of our

Class A common stock from us at the initial public offering price, less the underwriting discounts and commissions.

Atlas Point Energy Infrastructure Fund, LLC, Norges Bank Investment Management, a division of Norges Bank, Wellington Management, and one or more

funds and/or accounts managed by Capital Research Global Investors (collectively, the “Cornerstone Investors”) have, severally and not jointly, indicated an interest

in purchasing up to an aggregate of $350 million in shares of our Class A common stock in this offering at the initial public offering price and on the same terms and

conditions as the other purchasers in this offering. The shares of Class A common stock to be purchased by the Cornerstone Investors will not be subject to a lock-

up agreement with the underwriters. Because this indication of interest is not a binding agreement or commitment to purchase, the Cornerstone Investors may

determine to purchase more, fewer, or no shares in this offering, or the underwriters may determine to sell more, fewer, or no shares to the Cornerstone Investors.

The underwriters will receive the same underwriting discount on any shares of our Class A common stock purchased by the Cornerstone Investors as they will from

the other shares sold to the public in this offering.

Neither the Securities and Exchange Commission nor any state securities commission or any other regulatory body has approved or disapproved of these

securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares to purchasers on or about , 2026.

Joint Lead Bookrunning Managers

J.P. Morgan | BofA Securities | RBC Capital Markets | Barclays |

Bookrunning Managers

Baird | BBVA | Guggenheim Securities | MUFG |

Societe Generale | William Blair | Piper Sandler | Wolfe | Nomura Alliance |

Prospectus dated , 2026.

i

TABLE OF CONTENTS

Page | |

Letter from Tim Latimer, Chief Executive Officer ........................................................................................... | |

Prospectus Summary ......................................................................................................................................... | |

The Offering ...................................................................................................................................................... | |

Market and Industry Data ................................................................................................................................. | |

Estimates of Capacity Potential ........................................................................................................................ | |

Cautionary Note Regarding Forward-Looking Statements .............................................................................. | |

Risk Factors ...................................................................................................................................................... | |

Use of Proceeds ................................................................................................................................................. | |

Dividend Policy ................................................................................................................................................ | |

Capitalization .................................................................................................................................................... | |

Dilution ............................................................................................................................................................. | |

Management's Discussion and Analysis of Financial Condition and Results of Operations ........................... | |

Business ............................................................................................................................................................ | |

Management ...................................................................................................................................................... | |

Executive and Director Compensation ............................................................................................................. | |

Principal Stockholders ...................................................................................................................................... | |

Certain Relationships and Related Party Transactions ..................................................................................... | |

Description of Capital Stock ............................................................................................................................. | |

Shares Eligible for Future Sale ......................................................................................................................... | |

Material U.S. Federal Income Tax Considerations for Non-U.S. Holders of Common Stock ........................ | |

Underwriting ..................................................................................................................................................... | |

Legal Matters .................................................................................................................................................... | |

Experts .............................................................................................................................................................. | |

Where You Can Find More Information .......................................................................................................... | |

Through and including , 2026 (the 25th day after the date of this prospectus), all dealers effecting

transactions in these securities, whether or not participating in this offering, may be required to deliver a

prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter

and with respect to an unsold allotment or subscription.

You should rely only on the information contained in this prospectus, any amendment or supplement to this

prospectus or any free writing prospectus we may authorize to be delivered or made available to you. Neither we nor

the underwriters have authorized anyone to provide you with additional or different information. If anyone provides

you with additional, different or inconsistent information, you should not rely on it. Offers to sell, and solicitations

of offers to buy, shares of our Class A common stock are being made only in jurisdictions where offers and sales are

permitted. The information contained in this prospectus, any amendment or supplement to this prospectus or any

applicable free writing prospectus is accurate only as of its date, regardless of the time of delivery of this prospectus,

any amendment or supplement to this prospectus, any applicable free writing prospectus or of any sale of our Class

A common stock. Our business, financial condition, operating results and prospects may have changed since such

date.

ii

You should not consider any information in this prospectus, any amendment or supplement to this prospectus or

any applicable free writing prospectus to be investment, legal or tax advice. You should consult your own counsel,

accountant and other advisors for legal, tax, business, financial and related advice regarding the purchase of our

Class A common stock. Neither we nor any underwriter (nor any of our or their affiliates) are making any

representation to you regarding the legality of an investment in our Class A common stock by you under applicable

investment or similar laws.

For investors outside the United States: Neither we nor any of the underwriters have done anything that would

permit this offering or possession or distribution of this prospectus, any amendment or supplement to this prospectus

or any applicable free writing prospectus in any jurisdiction where action for that purpose is required, other than in

the United States. Persons outside of the United States who come into possession of this prospectus, any amendment

or supplement to this prospectus or any applicable free writing prospectus must inform themselves about, and

observe any restrictions relating to, this offering of our Class A common stock and the distribution of this

prospectus, any amendment or supplement to this prospectus or any applicable free writing prospectus outside of the

United States.

1

Table of Contents

DEFINED TERMS AND PRESENTATION

As used in this prospectus, unless the context otherwise requires, references to “we,” “us,” “our,” the

“Company,” “Fervo Energy,” and similar references refer to Fervo Energy Company and its subsidiaries. In

addition, the terms below that are used frequently in this prospectus have the following meanings:

•“2019 Plan” means the Fervo Energy Company 2019 Stock Incentive Plan, as amended.

•“2026 Plan” means the Fervo Energy Company 2026 Incentive Award Plan.

•“Amended Bylaws” means our amended and restated bylaws.

•“Amended Charter” means our amended and restated certificate of incorporation.

•“BLM” means the Bureau of Land Management.

•“Cape Station” means our GeoCluster located in Milford, Utah, the first approximately 100 megawatts of

which we expect will be delivered to the grid by early 2027.

•“Carbon-free” (or similar constructs) means carbon-free solely with respect to electricity generation from

our EGS processes once our facilities are producing. The term is not intended to capture nor represent any

other GHG emissions in our value chain, including other Scope 1 emissions (directly arising from

operations), Scope 2 (indirect emissions from purchased electricity), or Scope 3 (upstream and downstream,

including transportation and distribution). We do not make any claims regarding lifecycle greenhouse gas

accounting.

•“Class A common stock” means Class A common stock, par value $0.0001 per share, of Fervo Energy

Company.

•“Class B common stock” means Class B common stock, par value $0.0001 per share, of Fervo Energy

Company.

•“COD” means commercial operation date.

•“Code” means the U.S. Internal Revenue Code of 1986, as amended.

•“Co-Founders” means, together, Tim Latimer and Jack Norbeck, PhD.

•“Credit Agreement” means that certain Credit Agreement, dated November 20, 2024, as amended on May

21, 2025, July 23, 2025 and March 6, 2026 with Mercuria Energy Trading SA.

•“Credit Facility” means the $100.0 million term loan facility governed by the Credit Agreement and $80.0

million letter of credit facility governed by the Letter of Credit Facility Agreement.

•“D&M” means DeGolyer and MacNaughton, an independent engineering consulting firm.

•“EGS” means enhanced geothermal systems.

•“ESPP” means the Fervo Energy Company 2026 Employee Stock Purchase Plan.

•“Exchange Act” means the U.S. Securities and Exchange Act of 1934, as amended.

•“FERC” means the Federal Energy Regulatory Commission.

•“FervoFlex” means our approach to delivering flexible, dispatchable geothermal power by using our EGS

systems to provide long-duration, in-reservoir energy storage and rapid load following capability. During

periods of low electricity demand or high renewable generation, production wells are choked back,

allowing for pressure buildup within the reservoir. When grid demand rises, production wells are opened,

releasing stored thermal energy and rapidly ramping power output. This operational flexibility enables

geothermal to complement variable renewables and support a stable, decarbonized grid.

2

•“GAAP” means accounting principles generally accepted in the United States.

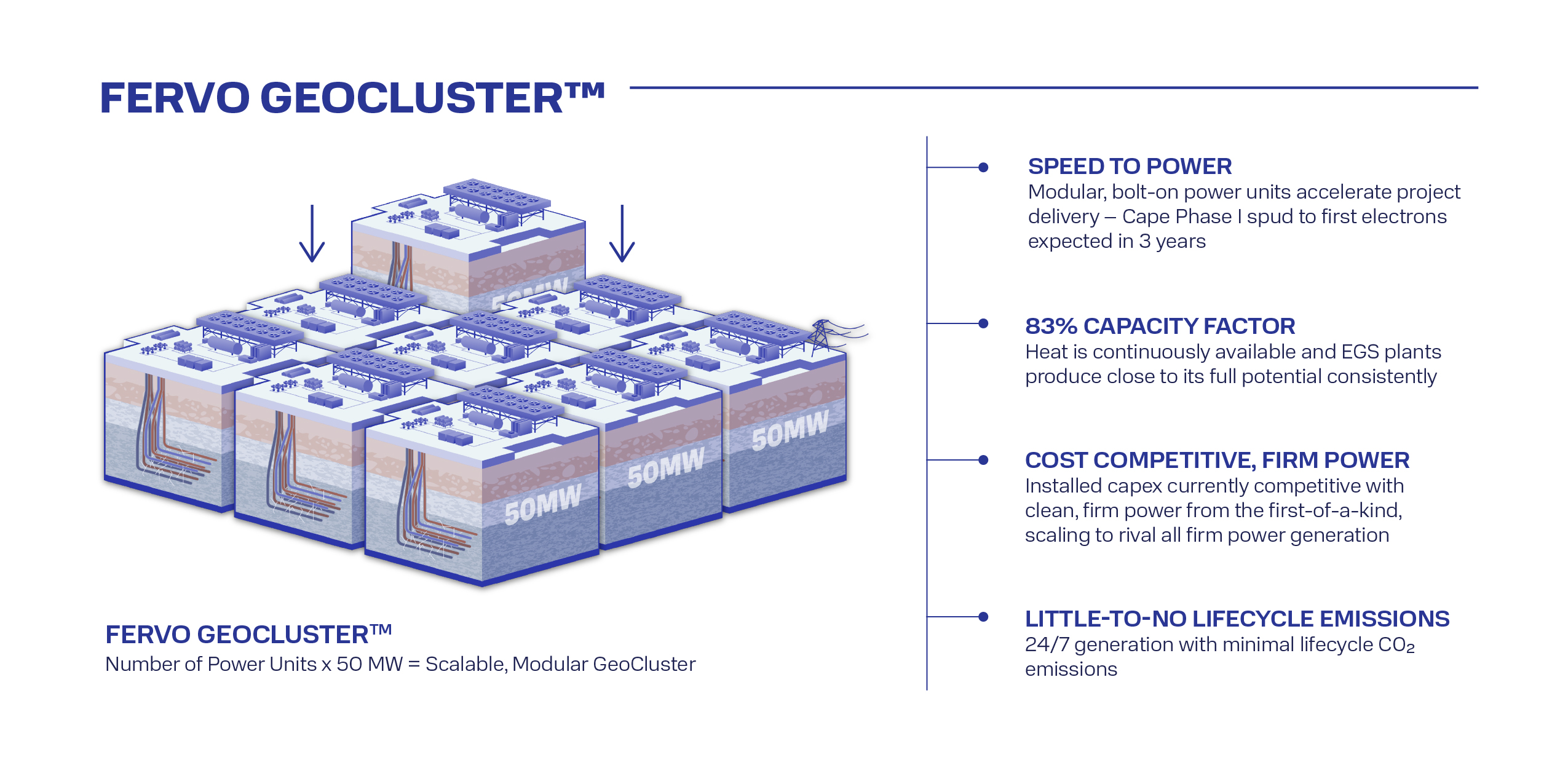

•“GeoBlock” means our standardized, 50-megawatt Organic Rankine Cycle power plants.

•“GeoClusters” means our leased acreage positions that we expect to support multi-gigawatt power

developments.

•“Geothermal resources” means thermal energy derived from the Earth’s natural heat and stored in a

reservoir.

•“GFA” means the Geothermal Framework Agreement, dated March 19, 2026, with Google Energy LLC.

•“GWh” means gigawatt-hours.

•“HIIP” or “heat initially in place” means those estimates of quantities of thermal energy generated from

geothermal resources.

•“LCOE” means levelized cost of energy.

•“Letter of Credit Facility Agreement” means that certain Letter of Credit Facility Agreement, dated

November 20, 2024, with Mercuria Energy Trading SA.

•“NEPA” means the National Environmental Policy Act.

•“NERC” means the North American Electric Reliability Corporation.

•“ORC” means Organic Rankine Cycle.

•“PPAs” means power purchase agreements or any other agreements pursuant to which we sell power or

related attributes to our customers.

•“Project Red” means our commercial pilot use of horizontal wells in an EGS system in northern Nevada,

which was a limited-scope, proof-of-concept initiative designed to demonstrate certain technical

capabilities.

•“Project Granite Facility” means the construction loan facility, ITC Transfer bridge loan facility, letter of

credit facilities, and a term loan facility, dated March 6, 2026 in the aggregate amount of approximately

$421.4 million.

•“R&D” means research and development.

•“SEC” means Securities and Exchange Commission.

•“Securities Act” means the U.S. Securities Act of 1933, as amended.

•“Stock Split” means the 0.7194-for-1 reverse stock split of our common stock, which will occur upon the

filing of our Amended Charter after the effectiveness of the registration statement to which this offering

relates and prior to the completion of this offering.

•“TWh” means terawatt-hours.

•“VRE” means variable renewable energy.

•“XRC Facility” means three promissory notes in the aggregate amount of $145.6 million under a loan

agreement with XRL ALC, LLC. This facility was terminated on April 14, 2026.

Certain monetary amounts, percentages, and other figures included in this prospectus have been subject to

rounding adjustments. Percentage amounts included in this prospectus have not in all cases been calculated on the

basis of such rounded figures, but on the basis of such amounts prior to rounding. For this reason, percentage

amounts in this prospectus may vary from those obtained by performing the same calculations using the figures in

3

our consolidated financial statements included elsewhere in this prospectus. Certain other amounts that appear in this

prospectus may not sum due to rounding.

This prospectus includes our registered or common law trademarks, service marks and trade names, including

but not limited to our design logo, Fervo Energy™, FervoFlex™, FERVO50 GEOBLOCK™, GEOCLUSTER™,

GEOBLOCK™, GEOCLUSTERS™ and GEOBLOCKS™, which are protected under applicable intellectual

property laws. This prospectus also contains trademarks, trade names, and service marks of other companies, which

are the property of their respective owners. We do not intend our use or display of other parties’ trademarks, service

marks or trade names to imply, and such use or display should not be construed to imply, a relationship with, or

endorsement or sponsorship of us by, these other parties. Solely for convenience, trademarks, service marks and

trade names referred to in this prospectus may appear without the ®, ™, or SM symbols, but such references are not

intended to indicate, in any way, that we will not assert, to the fullest extent permitted under applicable law, our

rights or the right of the applicable licensor to these trademarks, service marks and trade names.

Our audited consolidated financial statements as of and for the years ended December 31, 2025 and 2024

included in this prospectus have been prepared in accordance with GAAP.

4

LETTER FROM TIM LATIMER, CHIEF EXECUTIVE OFFICER

American economic prosperity has always depended on affordable, reliable energy. And as the U.S. confronts a

global AI race, and increasing geopolitical and environmental uncertainty, this fundamental truth will only deepen.

There is no AI revolution without power for data centers. There is no industrial renaissance without power for

manufacturing facilities and military bases. There is no future where we address the emissions causing climate

change without power for mass electrification.

But energy abundance is not guaranteed. In the 1970s, a prolonged energy crisis stifled American growth. Fuel

rations became commonplace, and across U.S. cities, lines at gas stations stretched for miles as drivers clamored for

fuel.

This crisis eventually gave rise to the Shale Revolution. Unwilling to accept stagnant domestic oil production,

policymakers, companies, and investors pushed for unconventional fossil fuel extraction. Horizontal drilling and

hydraulic fracturing offered an answer. And with continuous engineering improvements enabled by learning curves

and economies of scale, developers unlocked oil and gas in previously inaccessible locations. By the early-2010s,

horizontal drilling and hydraulic fracturing had transformed the global energy landscape by providing a new way to

access affordable energy.

The U.S. now faces a new energy crisis, a crisis driven by breakneck AI advancements, competition with China,

and climate instability. And though this crisis is novel, the technology needed to solve it is not.

The EGS approach we have pioneered on the back of over a decade of learnings from the Shale Revolution is

now sparking a revolution in clean, around-the-clock geothermal power. Fervo launched in 2017 with a simple

thesis: the same tools and engineering undergirding shale can make geothermal a scalable, cost-competitive clean

energy solution capable of addressing dramatic load growth. Unlike shale, which depletes hydrocarbons, EGS

leverages a heat reservoir for steady, renewable output. And while shale playbooks front-load production with

depletion and declines thereafter, EGS enables long-term, steady electricity generation.

To date, this thesis has proven correct. Horizontal drilling and hydraulic fracturing remove geographic

constraints on geothermal production, increasing capacity potential by orders of magnitude. According to Rystad,

conventional geothermal currently supplies the U.S. with roughly 3.8 gigawatts of energy. By contrast, Fervo’s Cape

Station site alone offers approximately 4.3 gigawatts of capacity potential, while a broader subset of our reviewed

leases represents over 40 gigawatts. EGS has the potential to make geothermal generation as ubiquitous as solar

generation is in the U.S. today.

Rapid buildout is already underway. Fervo has 500 megawatts currently under construction and 658 megawatts

of contracted offtake with tier-one partners like Southern California Edison, Google / NV Energy, and Shell,

providing a clear roadmap for potential near-term growth. We have entered a new era of geothermal development.

Relying on proven oil and gas technology allows for this scale. We do not need to build domestic supply chains

from scratch; we can leverage existing oilfield services providers. We do not need to retrain or reskill hundreds of

workers to drill our wells; we can leverage the U.S.’s robust oil and gas labor force. Our ability to provide reliable,

carbon-free electricity and also tap the traditional oil and gas industry workforce has made geothermal a bipartisan

solution, even as other resources become politically polarized.

Ultimately, though, the engineering mentality behind the Shale Revolution is just as important to our success as

the underlying technology. Shale transformed American energy thanks to learning curves—meaningful cost

reduction over repeated operations. In conventional oil and gas, producers targeted unique and complex systems

hoping for outsized returns. Shale, however, prioritized highly predictable basins spanning hundreds of square miles.

Repetitive basin-wide drilling allowed for standardization and simplification, increasing per-well productivity while

lowering costs.

This powerful combination—standardization and simplification—is critical to technology revolutions. It helped

Toyota become a global automotive juggernaut, leveraging “lean manufacturing” to popularize Japanese cars. It

helped SpaceX reinvigorate space travel, reducing rocket system complexity from the Raptor 1 to the Raptor 2 to the

5

Raptor 3. It will now help Fervo provide 24/7 clean energy at the speed, scale, and cost needed to achieve an

American-led AI future.

Fervo is working to build a different type of energy company—one that treats each geothermal power facility as

a repeatable product, not a one-off, complicated project. We intend to deliver power in standardized, 50-megawatt

ORC units, relentlessly reducing complexity with every well drilled and every turbine installed. With few locational

constraints on our subsurface operations, we can develop sites to multi-gigawatt sites, harnessing learning curves to

drive continuous improvement and make geothermal cheaper than it has ever been.

Our first utility-scale deployment in the Cape Station site will provide a baseline for our core product. We

expect that each power unit built thereafter will improve on this baseline by using learnings to streamline

engineering design.

Our commitment to continuous improvement rests on four core corporate values that have guided Fervo since

our inception. First, we Build Things That Last, prioritizing health, safety, and the environment above all else. No

matter how quickly we grow, we will not compromise the safety of our workers or the communities in which we

operate.

Second, we Do What We Say We Are Going To Do, assessing each task honestly and holding employees, and

the company, accountable to transparent, quantifiable performance targets.

Third, we Innovate Through Collaboration, seeking ideas from all sources and forging relationships with best-

in-class partners.

Finally, we Stop And Smell The Roses, because a company that celebrates its wins and genuinely values the

wellbeing of its people is a company positioned for lasting, sustainable growth. By keeping employees for the long

term, we can realize the engineering and commercial learning curves so central to our business.

Together, these four values define Fervo’s culture.

Today, miles-long lines for gasoline have been replaced by lines for electricity. Tech companies compete for

megawatts to claim AI market share. Manufacturers jockey for power to strengthen American industry. Utilities

demand clean, firm electricity to stabilize the grid. Fervo is prepared to serve all of these customers. Not with

complex, idiosyncratic projects but with a simplified, standardized product capable of delivering around-the-clock,

carbon-free power using proven oil and gas technology.

American economic dynamism has long depended on reliable energy. The reliable energy of our time is next-

generation geothermal.

6

PROSPECTUS SUMMARY

This summary highlights selected information that is presented in greater detail elsewhere in this prospectus.

This summary does not contain all of the information you should consider before investing in our Class A common

stock. You should read this entire prospectus carefully, including the sections titled “Risk Factors,” “Special Note

Regarding Forward-Looking Statements,” and “Management’s Discussion and Analysis of Financial Condition and

Results of Operations,” and our consolidated financial statements and related notes included elsewhere in this

prospectus, before making an investment decision. Unless the context otherwise requires, the terms “Fervo,” the

“Company,” “we,” “us,” and “our” in this prospectus refer to Fervo Energy Company and its consolidated

subsidiaries.

Our Mission

To transform geothermal energy into America’s most dependable and affordable source of clean, 24/7 power.

Fervo Energy

The U.S. is in critical need of firm, reliable power. Rapid growth in data centers, the resurgence of domestic

manufacturing, and accelerating electrification are driving electricity demand that outpaces new planned generation.

Rystad reports that by 2035, the country is expected to face a 98-gigawatt accredited capacity shortfall, highlighting

an urgent need for new, scalable sources of 24/7 power.

As the pioneer of enhanced geothermal systems (“EGS”), we are commercializing a new category of firm power

that is scalable, rapidly deployable, readily available, and geographically flexible. By applying proven technologies

like horizontal drilling and multi-stage hydraulic fracturing, we are transforming geothermal energy from a niche

resource into a utility-scale power solution that is clean, reliable, cost-competitive, and suited to the needs of

hyperscalers and utilities alike.

Geothermal is a highly attractive energy resource – it is clean, firm, and reliable. But traditional geothermal

projects depend on rare geologic conditions like volcanic systems with highly conductive natural fracture networks,

which has constrained development to places like Iceland, Kenya, California, and Hawaii. Additionally, traditional

geothermal projects have carried significant development risk because wells either succeed or fail entirely with

natural fracture networks. This uncertainty has made these projects unpredictable, expensive, and hard to scale.

Our EGS technology addresses the scalability limitations and key development risks of traditional geothermal

energy. By designing and controlling subsurface flow pathways, we can predictably recover heat without relying on

naturally occurring permeability. Additionally, we deploy innovative subsurface monitoring technologies such as

AI-enhanced fiber optic sensing that enable us to monitor and predict geothermal heat transfer at high spatial and

temporal resolution. We believe these capabilities will enable us to standardize project development, optimize power

facility placement and design, and capture economies of scale previously unavailable to the geothermal industry. We

expect this innovative approach to position us to deliver predictable, cost-effective, and scalable geothermal power

that follows learning curve cost declines, thereby providing the dependable energy needed to help close the nation’s

capacity shortfall.

Our EGS technology has been delivering clean electrons to the grid and generating revenue since 2023 at our

commercial pilot called Project Red, differentiating us from certain other energy alternatives still grappling with

technology risk, long development timelines, permitting uncertainty and supply chain constraints. Expanding upon

this success, we are now building Cape Station, a 500-megawatt greenfield project, where we expect to deliver first

power by late 2026. Our proven technical approach and track record of execution has generated meaningful

commercial traction. Across our full portfolio, we have signed 658 megawatts of binding power purchase

agreements (“PPAs”) with investment-grade utility and corporate energy buyers including Southern California

Edison and Shell. Beyond our current contracted backlog, we have also entered into a 3-gigawatt framework

agreement with Google (the “Geothermal Framework Agreement” or “GFA”) to advance and structure potential

power offtake opportunities for current and planned data centers in both grid-connected and alternative energy

solutions.

7

Our Project Pipeline

We are a geothermal energy developer that builds, owns, and operates geothermal power facilities. We construct

projects in phases across leased acreage positions that can support multi-gigawatt power developments

(“GeoClusters”). Our leasing strategy is focused on securing high-quality, geothermal resources in prime locations,

the vast majority of which have existing deep wells that confirm significantly elevated temperatures at shallow

depths and near-term commercial viability. We pair detailed geologic analysis with commercial assessments, such as

transmission access, market conditions, and permitting, so that each opportunity meets our development standards.

In June 2023, we broke ground on our first GeoCluster – Cape Station – located in Milford, Utah, which we

expect will become the world’s largest EGS project in terms of total installed capacity. At Cape Station, we have

500 megawatts under construction and expect to deliver first power in late 2026, reaching approximately 100

megawatts of operating capacity by early 2027. These 500 megawatts represent only the first two phases of the Cape

Station GeoCluster. We also have a permit in place to develop an incremental 1.5 gigawatts at the site, and based

upon a combination of internal estimates and findings from an independent engineer assessment, estimate that we

have a total of approximately 4.3 gigawatts of capacity potential at Cape Station.

Cape Station is expected to be the first in a large portfolio of high-capacity factor, carbon-free, baseload power

GeoClusters, supporting the company’s runway for significant, near-term organic growth across our 595,900 acre

land position as of December 31, 2025.

We classify our portfolio into three distinct categories: Mature, Pipeline, and Prospects.

As of December 31, 2025, our Mature, Pipeline, and Prospects portfolio consisted of the following:

Mature

•Operating: 3 megawatts are currently online and generating power from our pilot project, Project Red.

•Under Construction: 500 megawatts are currently in construction at Cape Station, with commercial

contracts in place and physical work underway.

•Ready to Build: 550 megawatts across two different GeoClusters were shovel-ready with initial permits

secured to begin construction. These megawatts are backed by calibrated subsurface models, validated

against well data and geophysical surveys, and have a clear wellfield development strategy in place.

8

Commercially, we have secured or are in advanced negotiation for offtake and have either obtained

interconnection or established a clear, achievable path.

Pipeline

•Advanced Development: 2.6 gigawatts were in advanced development. These projects have a go-to-market

strategy established, with key development milestones progressing and active origination efforts underway.

Typical activities include preliminary permit filings, on-site geological studies work, and submission of

interconnection applications.

•Early Development: Over 38 gigawatts were in early-stage development across ten GeoClusters where we

have commissioned and received independent HIIP studies and are conducting feasibility activities to

validate and confirm the path toward commercial development.

Prospects

•Land Holdings: Our remaining portfolio consists of approximately 256,000 acres of leased acreage as of

December 31, 2025, with differentiated geothermal resource quality currently maintained in our portfolio.

For this category, we have secured leases and identified project areas, but have not commenced initial

development work.

These three categories (Mature, Pipeline and Prospects) represent the expected progression of our megawatts

from those in early development stages to revenue-generating operations.

9

As of December 31, 2025, our generation portfolio was comprised of the following:

__________________

Note: Capacity Potential estimates are based on “Best Estimate” HIIP estimates presented in reports prepared by D&M using assumptions

regarding notional EGS development plans, ORC turbine efficiency, parasitic loads, and other assumed recovery factors, and are subject to

change with additional data.

Our Project Economics

Our business model combines technological innovation with disciplined project development and seeks to

deliver predictable returns and strong cash generation. In addition to advancing the technical boundaries of

geothermal energy, we are implementing a development approach that leverages repeatability, enhanced production

performance, and economies of scale. We believe relentless focus on these three areas will enable us to

systematically improve the economics of geothermal power generation and increase the value of each megawatt

produced across our portfolio.

•Repeatability – Freed from the constraints of conventional geothermal systems, our approach emphasizes

standardization and repetition in order to capture and integrate geological, technical, and experiential

learnings to meaningfully reduce costs. Since 2022, the company has demonstrated a steep drilling learning

curve, reducing drilling times by approximately 75% from 2022 to 2025 and lowering per-foot drilling

costs by approximately 70% over the same period. We employ advanced data analytics and proprietary AI-

based modeling to better predict operational conditions and accelerate design optimization, drawing on

more than 500 terabytes of high-fidelity operational data collected to date. To extend these efficiencies

from the wellfield to the surface facilities, we plan to deploy standardized 50-megawatt ORC power plants

10

that we call GeoBlocks—which aggregated together form GeoClusters— that we expect will yield power

projects that are modular and reliable. By modularizing capacity into standardized 50‑megawatt GeoBlocks

and scaling them in GeoClusters, we believe we can create a repeatable, bolt-on development model that

compounds learning across projects, shortens delivery timelines, and enables predictable, utility‑scale

expansion. The chart below illustrates the impact of learning curves on our business over time,

demonstrating the decrease in cost per foot and days spent drilling to total depth per well across our Project

Red and initial Cape Station subsurface construction.

Source: Fervo Data

For our two Project Red wells, total vertical depths were approximately 7,500 feet and total measured depths

were approximately 11,000 feet, with a horizontal section of approximately 3,000 feet. For our Cape Station Phase I

subsurface construction, we increased the total vertical depths to approximately 9,000 feet and total measured depths

to approximately 14,000 feet, with a horizontal section of approximately 5,000 feet. We plan to drill approximately

8–10 wells per standardized GeoBlock. Planned well depths will vary and will be refined based on site‑specific

geology and geography, including subsurface thermal gradient, stress conditions, and structural or tectonic setting

pertinent to EGS, to intersect target heat‑bearing formations at the depths required for effective reservoir creation.

•Enhanced Production Performance – We seek to continue to increase output and efficiency through

improvements in well design, reservoir engineering, and surface facility optimization. We have already

deployed progressively longer lateral wells and have targeted progressively higher temperature formations

to enhance heat recovery from each well and improve power conversion efficiency. For example, our

Project Red wells have maximum lateral lengths of approximately 3,000 feet and target formation

temperatures of approximately 350°F, whereas the Cape Station Phase I wells have maximum lateral

lengths of approximately 5,000 feet and target higher formation temperatures of approximately 400°F.

These design choices reflect our progression toward longer laterals and hotter reservoirs in successive

phases, with Cape Station Phase I representing a step-change relative to Project Red. Proprietary

stimulation techniques and real-time monitoring allow us to optimize flow distribution and thermal

recovery. We continuously refine our approaches to drilling, completions, and facility configuration to

deliver incremental performance gains with each successive phase of each project.

11

•Economies of Scale – Our GeoCluster-focused approach supports the development of shared infrastructure

and streamlined supply chains. By replicating uniform GeoBlocks across multiple sites, the company

achieves procurement leverage, lowering capital intensity and increasing the predictability of long-lead

time equipment supply. We expect multi-gigawatt GeoClusters will allow us to capture scale efficiencies

across engineering, construction, manufacturing, workforce, and operations, further enhancing project

returns and improving overall company economics.

Together, we believe these capabilities create a compounding advantage across our portfolio. We expect that

repeatability, enhanced production performance, and economies of scale will contribute to lower capital intensity

and higher margins on a per-megawatt basis and enhance project-level cash generation. As additional GeoBlocks are

deployed across GeoClusters, we expect continued reductions in cost per megawatt and improvements in return on

invested capital, reinforcing the company’s ability to deliver sustained value.

Source: Midpoint for geothermal capacity factor, Rystad Energy.

Our Opportunity

Driven by surging load from AI and data centers and accelerating electrification across transportation,

buildings, and industry, the U.S. power market is approaching a decisive inflection point as electricity demand

outpaces new planned generation. At the same time, Rystad notes that roughly 66 gigawatts of aging accredited

capacity are expected to retire by 2035, which is projected to lead to a nationwide accredited capacity shortfall of

approximately 98 gigawatts by 2035. Underlying this accredited capacity shortfall is the disproportionate retirement

of baseload power sources, namely coal, which comprises 80% of net power retirement through 2035. To close the

projected capacity shortfall, the market will require substantial incremental firm generation.

A firm energy resource, like geothermal, natural gas, nuclear or coal, can reliably deliver electricity at consistent

levels for long durations and typically has a capacity factor above 75%. Because of its reliable nature, firm power is

critical for the inflexible demand profiles of data centers, as well as industrial and commercial consumers. However,

market participants expect the projected shortfall in firm power generation to be increasingly plugged by intermittent

renewables (wind, solar, often paired with batteries to extend availability); Rystad predicts that renewables could

comprise 32% of all U.S. power generation by 2035. Meanwhile, rising peak demand, in conjunction with planned

firm power retirements, is driving down reserve margins across the U.S., making additional firm capacity critical.

This mismatch in supply and demand has manifested itself in progressively higher PPA prices for firm energy

resources. Rystad reports that clean, firm energy sources, like EGS, can command pricing in the range of $100-130

per megawatt-hour.

12

According to Rystad, if EGS were to meet the emerging accredited capacity gap in the U.S. alone, the annual

addressable market would be approximately $70.0 billion by 2035. Assuming a 30-year asset life, this represents a

$2.1 trillion revenue potential opportunity.

We believe we are well positioned to meet this moment. Our EGS technology is proven and scalable. Our

modular engineering approach supports rapid deployment. Our commercial pipeline is advanced, our wellfield

supply chain and labor force are mature, and our intellectual property is broad, while our acreage holdings contain

approximately 595,900 acres of geothermal leases that provide significant room for expansion. These advantages

position us to become one of the largest providers of scalable, carbon-free baseload power over the next decade.

The following factors highlight the structural demand-supply imbalance in U.S. power markets and underscore

why we believe that scalable, firm, carbon-free solutions like EGS are positioned to capture outsized value in the

decade ahead.

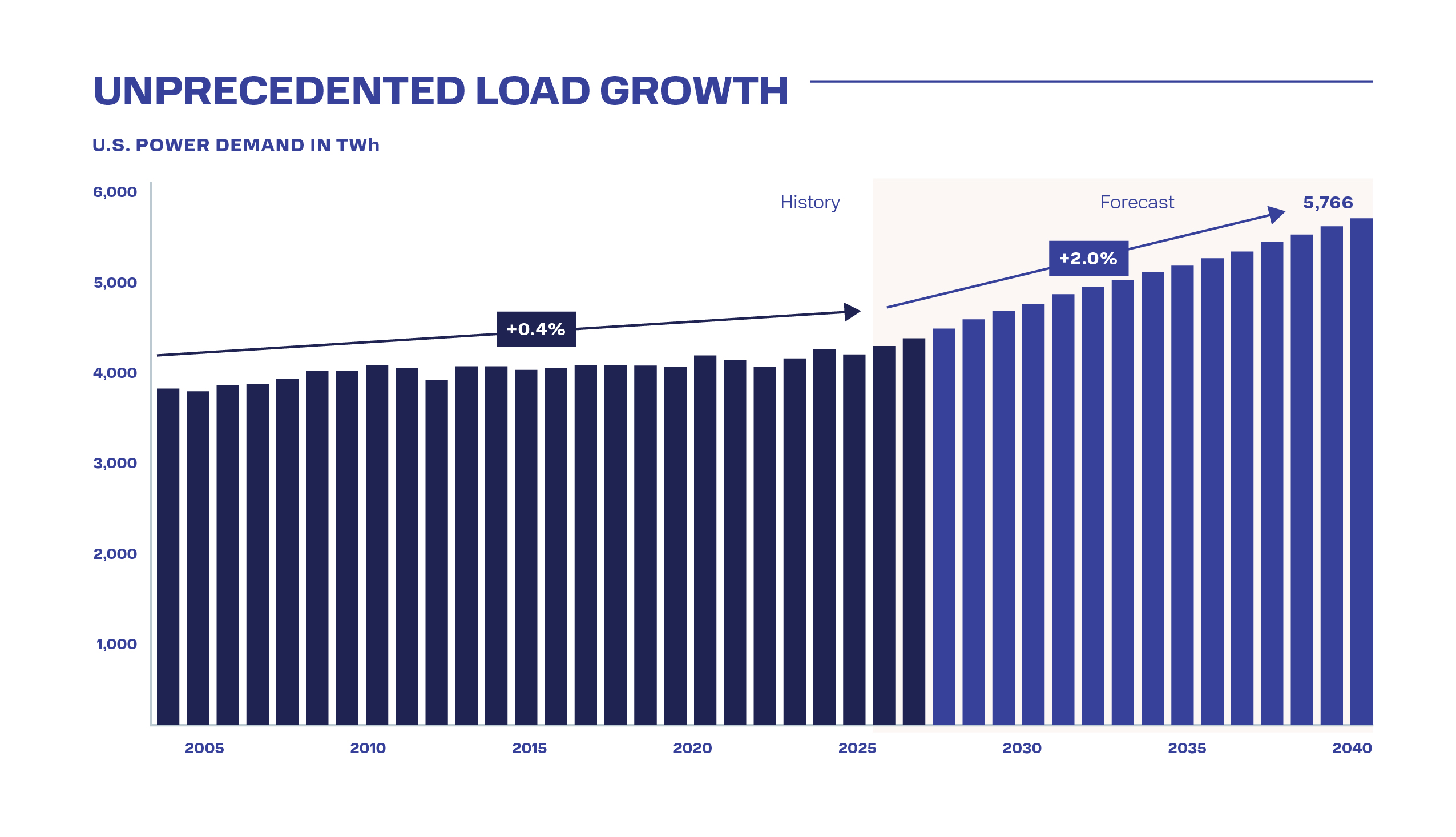

•All-Time High Power Demand – After two decades of relatively stable load growth between 2000 and

2020, energy demand is rising steeply and rapidly driven by the artificial intelligence (“AI”) boom,

renewed onshoring of manufacturing and economy-wide electrification. The chart below demonstrates the

accelerating pace of load growth in the United States.

Source: Rystad Energy.

13

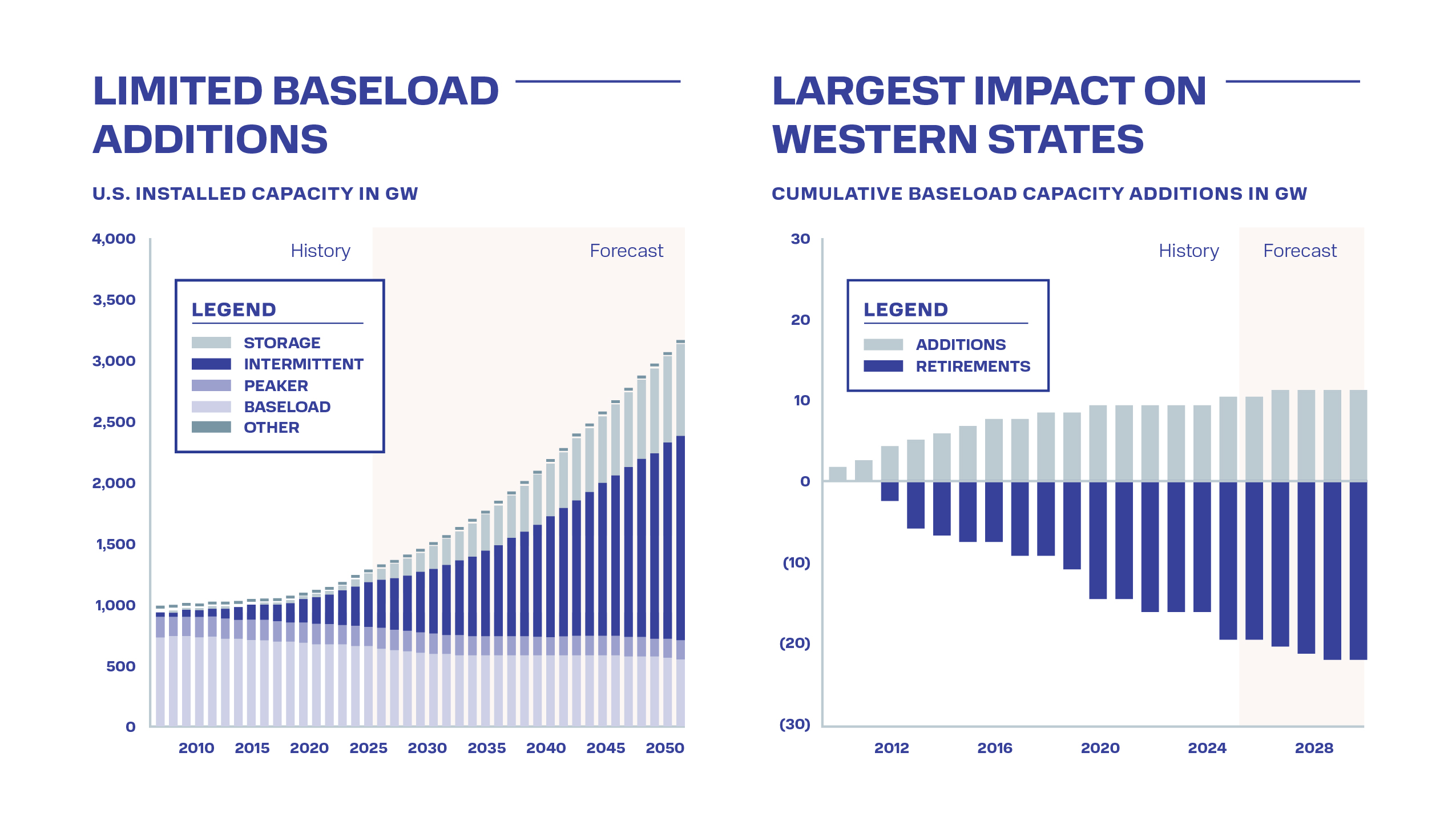

•Deficient Supply Alternatives. – The U.S. energy system is facing a severe supply constraint caused by

insufficient new capacity additions and aging infrastructure. Existing power supply alternatives face various

limitations in this time of great need. Variable renewable energy resources (“VREs”) like solar and wind

have expanded rapidly but can only meet certain hours of demand, even when coupled with battery storage.

Firm energy resources like natural gas face supply chain bottlenecks and volatile fuel pricing. Nuclear

power remains a critical firm energy resource, but new large-scale projects are battling high costs and long

development timelines. The charts below demonstrate the lack of baseload power expected to be added to

the U.S. energy system, and the particular impact on the Western U.S., our current area of operations.

Source: Rystad Energy.

Our Innovative Solution

We have successfully applied proven technological innovations from the American oil and gas industry to

kickstart what we expect to be another great American industry: next-generation geothermal. Across every layer of

our technology stack, we endeavor to target and systematically eliminate key constraints to traditional geothermal

development to make geothermal energy the most dependable and affordable source of power in America.

Conventional geothermal developers cede control of their projects to the whims of subsurface geology, relying

on natural fracture networks in hot rock to access heat for power generation. This approach restricts development to

a select few locations with adequate subsurface conditions, introduces binary dry hole risk given the unpredictability

of natural fractures, and imposes a fixed upper bound on reservoir-wide power output. Constrained by the resource

size available in natural fractures, conventional geothermal developers have historically been unable to drill new

wells to make up additional capacity if projects underperform, adding additional tail risk after the project is built.

Rather than accept the variability of drilling vertical wells into a natural fracture network, we use proven

technology from the oil and gas industry to build a tightly controlled system for heat extraction in low-permeability

geothermal formations. We engineer these reservoirs by drilling sets of parallel horizontal injection and production

wells through hot rock, accessing a zone of the geothermal reservoir with a highly predictable volume of heat in

place. We then use multistage hydraulic fracturing to connect the wells, establishing pathways and sufficient surface

area in the rock through which water can flow, heat up, and return to the surface for power generation. We also

install AI-enhanced fiber optic sensing cables to measure reservoir conditions in real-time. This data is then used to

14

continuously monitor flow rates, pressures, and temperatures across the wellfield, allowing us to predict and

optimize future well output. Our proprietary, data‑assimilative models integrate continuous temperature and pressure

profiles to update reservoir state in real time, enabling more accurate production forecasts and proactive decisions to

sustain deliverability and recoverable heat. Our approach allows us to actively manage long-term reservoir

performance; if production falls off in any part of the field, we are able to drill infill wells or simply drill new wells

to mine additional heat and extend overall reservoir lifetime.

Instead of creating separate one-off vertical wells (each with a separate well pad) across a field, we can access

vast quantities of subsurface heat by drilling many horizontal wells from a single pad with a compact footprint,

dramatically reducing land disturbance. This approach replicates the successful wellfield design used in the shale oil

and gas revolution. However, unlike in shale, where operators typically target specific and sometimes narrow

payzones, we can access progressively hotter rock the deeper we drill. Our reservoir is only bounded by temperature,

with the minimum temperature established by power plant efficiency and the maximum temperature established by

the temperature limits of subsurface equipment. At present, we apply a minimum reservoir temperature of

approximately 300°F and a maximum reservoir temperature of approximately 625°F, and we utilize a cutoff vertical

depth of about 13,000 feet to define resources we consider technically and commercially viable. These parameters

may evolve over time with improvements in drilling and subsurface technology or changes in market conditions (for

example, higher PPA pricing can support lower temperatures or deeper drilling). As a result, our payzones already

extend thousands of feet in thickness, and we expect these will continue to grow over time as better drilling

technology is developed.

Our Wellfield Production

Data observed from our projects to date has validated our approach. In 2023, we brought our pilot, Project Red,

online. The project quickly demonstrated record 24/7 carbon-free power production, generating three megawatts of

gross power production to the Nevada grid and proving the commercial viability of our innovative drilling

technology. Additionally, at our Project Red commercial pilot, we have observed consistent, stable temperature

output in line with our modeling and expectations. To date, Project Red has not experienced the kind of premature

thermal decline that has long plagued traditional geothermal projects.

15

We apply advanced data analytics, computational modeling, and data-driven empirical modeling to generate

high-fidelity production forecasts to optimize the economics of our projects. After pioneering the installation of

permanent AI-enhanced fiber optics in geothermal wells, we have collected over 500 terabytes of downhole data that

have been analyzed and used to improve well spacing, completion design, and wellfield optimization. With every

well drilled, casing string installed, and flow test completed, we deepen our knowledge of EGS reservoirs and

extend our first-mover advantage.

Our Scalable Deployment

Our approach is designed specifically with scale in mind. With geothermal heat recovery substantially de-

risked, we can leverage a modular, standardized approach to on-surface power generation to drive cost reductions,

increase deployment speed, and leverage economies of scale and flexibility in our supply chain. We plan to deploy

standardized, 50-megawatt ORC power facilities that we call GeoBlocks. Production wells send hot geothermal

brine to a heat exchanger, where it transfers heat to a working fluid. After transferring heat, the cooled geothermal

brine is reinjected underground to cycle through the geothermal reservoir again. In the heat exchanger, the working

fluid is vaporized, ultimately spinning a turbine to create electricity. The vapor is then cooled back into a liquid

using air-cooled condensers to minimize water usage.

We have already secured binding contracts for 500 megawatts of ORC turbine capacity through partnerships

with Baker Hughes and Turboden (a wholly-owned subsidiary of Mitsubishi) for our projects under construction,

and have further expanded this supply through a 1.7 gigawatt ORC turbine framework agreement with Turboden.

These manufacturers have longstanding ORC business units that stand apart from natural gas turbines, helping

support near-term ORC supply even as gas turbines remain backlogged.

GeoBlocks are engineered for rapid scalability. When aggregated, multiple GeoBlocks make up a GeoCluster,

which we define as a multi-gigawatt geothermal power hub designed to provide substantial generation while

streamlining construction and operations. With approximately 595,900 acres of geothermal leases across the United

States as of December 31, 2025, we are primed to implement several GeoCluster power hubs in the next decade with

the potential to support more than one power market. A majority of our leases have a 10-year initial term, and in

most cases, extension options.

To date, all of our commercial contracts feed electrons to the power grid. But by deploying multi-gigawatt

GeoClusters, we can mitigate transmission risk associated with our projects. First, the size and capacity factor of our

projects are catalyzing partnerships with transmission developers who seek project certainty and high line

utilization. We are also pursuing behind-the-meter partnerships with hyperscalers who seek large generation and

high uptime. We believe that our GeoCluster approach for AI data center development pairs a repeatable, flexible

commercial framework with a modular, scalable power solution aligned with hyperscale customer demand and

supports definitive offtake agreements over time. Ultimately, we can blend behind-the-meter and transmission

solutions, maximizing resilience and redundancy at a single site.

Our Customers

Our customers have the following profile:

•Customers who want reliability. Utilities cannot replace baseload coal and nuclear plants with solely

intermittent resources such as wind and solar power. To ensure a safe, functional and reliable grid capable

of addressing demand peaks, utilities must procure a new generation of baseload options. Likewise,

hyperscalers demand reliability to maximize uptime for their AI models.

•Customers who seek a near-term solution. Power buyers place a premium on near-term deliverability. In

the race for AI dominance, hyperscalers continue to construct additional data center capacity to avoid

falling behind their foreign and domestic competitors. This arms race mentality has pushed leading AI

companies to go to extreme lengths to obtain more power. For example, xAI has taken the extraordinary

step of purchasing a natural gas power plant overseas and shipping it to the U.S. to power a 2-gigawatt data

center. Utilities, too, recognize the time-sensitivity of bringing new supply online. According to Rystad,

16

many states across the western United States could face capacity shortfalls by 2031. To address this risk,

utility commissions are increasingly pushing load-serving entities to procure additional reliable power.

•Customers who demand cost-competitiveness. Even as PPA prices continue to rise, buyers maintain price

ceilings above which baseload power procurement remains unattractive. Especially as popular attention on

electricity prices increases, utilities will have to guard against serious cost inflation to remain viable.

•Customers who seek carbon-free solutions. Whether because of state-level renewable energy mandates or

voluntary emissions reduction commitments, a wide variety of buyers continue to prioritize carbon-free,

clean energy sources. For utilities in certain jurisdictions, political pressure has increased the urgency of

clean power procurement.

The EGS technology we pioneered is very well suited to meet our customers’ power procurement needs:

•We offer reliability. EGS projects provide high-capacity-factor baseload power, with no fuel price

exposure.

•We deliver power now. Our EGS technology is one of the few 24/7 power solutions capable of bringing

incremental generation online before 2030. We expect to begin delivering first power from our 500-

megawatt Cape Station project by late 2026, and to reach approximately 100 megawatts of operating

capacity by early 2027.

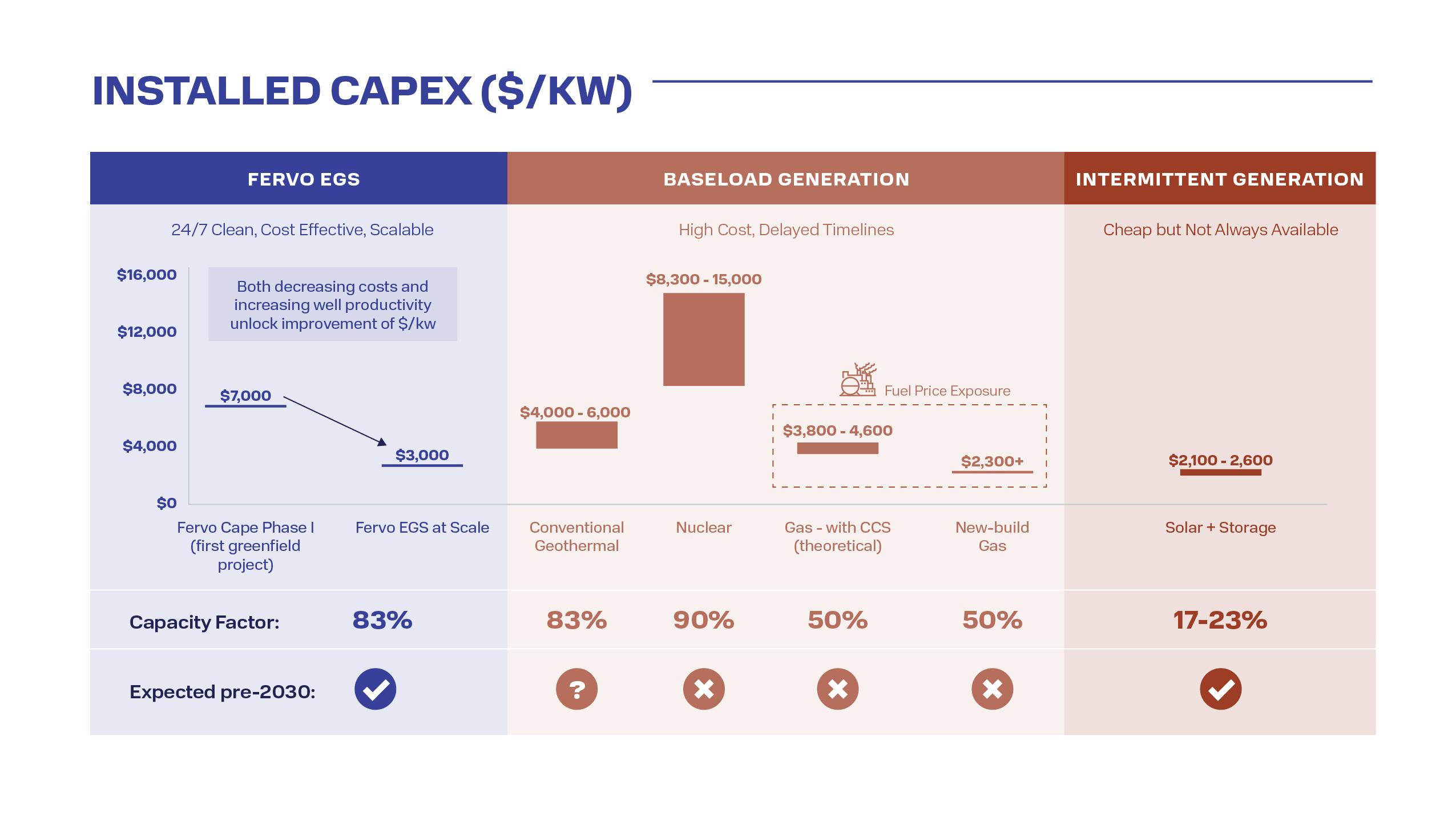

•We offer an economic, non-volatile alternative. At approximately $7,000/kW, our first Cape Station

project already outcompetes both traditional and small modular nuclear power in overnight capital costs.

Over time, our goal is to achieve scale and drive down prices such that we’re able to outcompete gas by

achieving an Nth-of-a-kind project cost of $3,000/kW without fuel price exposure. Unlike conventional

power producers, our “fuel” is geothermal heat. The cost of accessing it is embedded upfront in our

subsurface capital expenditures and water systems, not in an ongoing commodity expense. By eliminating

exposure to commodity price swings, we intend to deliver predictable, contractable pricing that reduces

hedging costs and risk premiums, which we believe provides economic value that our customers will

recognize and be willing to pay to secure. Beyond delivering power, we also sell multiple products,

including energy, capacity, and environmental attributes. This mix supports premium pricing and stronger

margins as markets increasingly value clean, 24/7 capacity and verified environmental attributes. This

fundamental advantage distinguishes us from traditional power companies and underpins the long-term

stability of our cost structure.

•We offer carbon-free, renewable power. According to the Department of Energy, EGS projects using

binary-cycle ORC power plants have a fraction of the emissions footprint as natural gas plants. The carbon-

free nature of our product makes EGS especially attractive in states with time-sensitive, ambitious

renewable portfolio standards and for corporate buyers who seek to maintain their climate goals.

17

These core attributes (reliability, deliverability, cost-competitiveness, and carbon-free) position our EGS

technology ahead of other power options, allowing us to capitalize on high, inelastic power demand.

Sources: Rystad Energy and management estimates.

Our Competitive Strengths

•First-Mover Advantage with Highly Advanced Development Portfolio: We are the global pioneer of EGS

technology. We successfully drilled and stimulated the country’s first commercial EGS wells at our pilot,

Project Red. With an operating pilot and two and a half years of 500 megawatts of greenfield construction

underway, including over 25 wells drilled, we maintain a significant first-mover lead in the EGS space.

These wells were drilled at our Cape Station project in Beaver County near Milford, Utah, and at Project

Red adjacent to the Blue Mountain geothermal field near Winnemucca in Humboldt County, Nevada. As of

December 31, 2025, our projects under construction accounted for approximately 13% of all geothermal

capacity under construction in the United States. By reducing subsurface risk in geothermal heat recovery,

we have increased the velocity with which megawatts can move through our development pipeline.

Additionally, with 595,900 leased acres as of December 31, 2025, we hold what we believe to be one of the

U.S.’s largest portfolios of high-quality geothermal leases. We assembled this position at a weighted

average of approximately $4 per acre during a period of minimal competition between 2019 and 2021, in

sharp contrast to current U.S. Bureau of Land Management lease sales in Utah and Nevada, where

maximum bids reached $344 and $410 per acre, respectively, in 2025. Many of those newly auctioned

parcels did not meet our standards for high-priority development and thus were outside our initial focus

areas, reflecting the quality of our acreage. According to Bloomberg, certain geothermal developers in Utah

and Nevada have paid hundreds of dollars per acre in 2025 for geothermal positions that failed to meet our

development standards. We are thus uniquely positioned as a first mover to capitalize on surging demand

for clean, firm, reliable power.

•Proven Ability to Secure Binding, Long-Term Offtake: We have executed 658 megawatts of binding

PPAs across each of our target customer verticals, including hyperscalers, major utilities (Southern

California Edison), community choice aggregators (Clean Power Alliance and Desert Community Energy)

and supermajor energy companies (Shell). These contracts were executed at attractive prices, representing

approximately $7.2 billion in potential revenue backlog. This commercial momentum is further bolstered

18

by a 3-gigawatt framework agreement with Google. Though not a binding, project-specific PPA, the

agreement provides a structured roadmap for future capacity expansion and establishes a repeatable model

for large-scale corporate offtake.

•Modular Design Enabling Speed to Power and Economies of Scale: We intend to deploy our technology

in 50-megawatt GeoBlocks, standardized ORC power units that we anticipate will extend our learning

curves from wellfield development to geothermal power plant construction. We expect to further support

these learning curves by concentrating our operations in multi-gigawatt GeoClusters. Each cluster can

support hundreds of EGS wells and dozens of adjacent GeoBlocks, creating unprecedented economies of

scale in the geothermal industry. We believe that this approach will make our cost-competitive EGS

solution increasingly attractive to high credit-quality offtakers and will assist us in catering to AI

hyperscalers that require speed-to-power, gigawatt-scale energy access, and 24/7 availability.

•Demonstrated Access to Asset-Level Capital Enables Financial Flexibility: As of December 31, 2025, we

had raised $320.6 million of project level capital, comprised of $175.0 million of project-level equity and

$145.6 million of project-level debt. Subsequently, on March 6, 2026, we closed an approximately $421.4

million project finance credit facility with a syndicate of nine lenders (the “Project Granite Facility”) for the

first phase of our Cape Station development. Our relationships with leading capital providers give us the

flexibility to secure lower-cost, non-dilutive project-level financing, extending the runway of our corporate

funds while accelerating deployment and substantially de-risking our funding strategy through diversified

sources of capital.

•Robust Intellectual Property Portfolio: We have a comprehensive intellectual property portfolio which

includes patents and trade secrets covering many material proprietary aspects of our EGS technology. Our

key patents and trade secrets deter competitors from employing critical but protected processes required to

create and manage the subsurface flow of geothermal brine.

•Resilient Development Approach Leveraging Secure Supply Chain: We have proven capable of

seamlessly scaling our operations through partnerships with well-established oilfield services providers

such as Liberty Energy, Helmerich & Payne and Vallourec. We have also developed durable partnerships

with ORC turbine manufacturers from key U.S. partner nations, such as Turboden (a wholly-owned

subsidiary of Mitsubishi) and Baker Hughes, which remain relatively insulated from tariffs and

procurement backlogs that are currently impacting natural gas turbines, along with primarily U.S.

headquartered balance of plant equipment providers.

•Founder-Led Management Team: Co-founders Tim Latimer and Dr. Jack Norbeck, along with our

executive leadership team, have over 125 years of energy experience across companies in upstream oil and

gas, oilfield services, and power and renewables, including Shell, BP, Chevron, BHP Billiton, NRG, Hess,

SLB, and NOV.

Our Growth Opportunities

Our principal growth strategies include:

•Progress GeoCluster Development: We have one gigawatt included in our Mature projects portfolio, with

500 megawatts categorized as Under Construction at our flagship GeoCluster Cape Station, with

commercial contracts in place and physical work underway. Additionally, we have 550 megawatts that we

categorize as Ready to Build across two different GeoClusters. These projects have already achieved key

development milestones, which have substantially derisked commercialization. We also have over 40

gigawatts in our Pipeline project portfolio, with 2.6 gigawatts categorized as under Advanced Development

and over 38 gigawatts under Early Development across ten GeoClusters. There are significant remaining

opportunities for development in our Prospects portfolio that spans the 595,900 acres of leased acreage

currently maintained in our portfolio. We aim to pursue development on our robust pipeline at a more

accelerated pace beyond 2030. See “Prospectus Summary—Our Project Pipeline” for more information

related to our projects.

19

•Execute Technology Roadmap and Achieve Nth-of-a-Kind Cost Structure: We believe our attractive

asset-level returns will continue to improve, following well-established learning curves observed across the

energy industry. By drilling deeper wells to access higher-temperature reservoirs, extending lateral lengths,

and widening wellbore diameters, we expect to achieve progressively higher power output per well.

Additional cost efficiencies will come from standardizing power generation equipment, securing multi-year

supply agreements, and capturing economies of scale across construction scopes. We believe these efforts

will reduce our costs from the current approximately $7,000/kW, already among the lowest-cost sources of

baseload power, toward our long-term target of $3,000/kW.

•Establish Programmatic Offtake Partnerships: We are pursuing multi-year, multi-gigawatt offtake

partnerships with both utilities and hyperscalers to substantially de-risk commercial development across

multiple GeoClusters. We believe that these offtake partnerships with hyperscalers – such as the 3-gigawatt

GFA – will provide us with a path to potentially capitalize on predictable, long-term demand, pricing

visibility, and opportunities for co-located, behind-the-meter development that will boost our positioning

among AI data centers.

•Expand Geographic Scope of Development: Building on our learning curves and demonstrated progress at

Project Red and Cape Station, we are codifying a repeatable playbook to expand commercial geothermal

development beyond beachhead locations in the western United States and into other power markets where

high wholesale power prices, particularly for baseload generation, present attractive growth opportunities.

Over time, we intend to deploy our EGS technology outside of the United States, prioritizing jurisdictions

with clear decarbonization mandates, supportive regulatory frameworks, and subsurface conditions

favorable to EGS development. We intend to advance this expansion through strategic partnerships and

targeted pilot projects to validate performance, adapt to local market requirements, and establish a

repeatable model for international scaling.

•Pursue Complementary Verticals: We believe we are well positioned to leverage our proven approach to

enter adjacent markets, including energy storage, industrial process heat, and district heating. We are one of

the leaders in innovation for subsurface energy storage through our tested and patented approach,

FervoFlex. Our ability to monetize both power and heat, moreover, distinguishes us from other power

providers. By unlocking new customer segments, we believe we will be able to meet the evolving needs of

industrial, commercial, municipal, and operating company energy buyers.

Recent Developments

Preliminary Financial and Operating Results for the Three Months Ended March 31, 2026 (Unaudited)

Set forth below are selected preliminary consolidated unaudited financial and operating results for the three

months ended March 31, 2026. Our complete consolidated financial statements for the three months ended March

31, 2026 are not yet available. The following information reflects our preliminary estimates with respect to the

results for the three months ended March 31, 2026, which are based on currently available information and are

subject to change. We have provided approximate amounts or ranges, rather than specific amounts, for the

preliminary results described below primarily because our financial closing procedures for the three months ended

March 31, 2026 are not yet complete and, as a result, our final results upon completion of our closing procedures

may vary from the preliminary estimates. These estimates should not be viewed as a substitute for interim financial

statements prepared in accordance with GAAP.

This selected preliminary consolidated financial data has been prepared by, and is the responsibility of, our

management. Our independent registered public accounting firm, Deloitte & Touche LLP, has not audited,

reviewed, compiled or performed any procedures with respect to this preliminary consolidated financial data.

Accordingly, Deloitte & Touche LLP does not express an opinion or any other form of assurance with respect

thereto.

Revenue generated during the three months ended March 31, 2026 and 2025 includes ancillary fees associated

with rights to geothermal production, which were immaterial for both periods and are not expected to be significant

to our long-term revenue generation, as we have not yet commenced large-scale commercial operations.

20

Additionally, for the three months ended March 31, 2026, we estimate net loss to be between $29.0 million and

$35.0 million as compared to net loss of $9.1 million for the three months ended March 31, 2025. The expected

increase in net loss is primarily expected to be due to increased general and administrative expenses driven by higher

employee-related costs from headcount growth to support project development and corporate operations, including

increased stock-based compensation expense related to stock options granted during the three months ended March

31, 2026, increased software and information technology costs, and costs associated with our transition to a public

company. In addition, the increase in net loss is expected to reflect non-cash valuation remeasurement losses in the

fair value of warrant liabilities during the three months ended March 31, 2026.

As of March 31, 2026, our cash and cash equivalents were approximately $280.8 million, compared to $461.8

million as of December 31, 2025. As of March 31, 2026, our long-term debt was approximately $189.8 million,

comprised of approximately $145.6 million outstanding under the XRC Facility and approximately $44.2 million

outstanding under the Credit Facility, compared to total principal due for long-term debt of $175.6 million as of

December 31, 2025. Subsequent to March 31, 2026, on April 14, 2026, we repaid all outstanding balances under the

XRC Facility using proceeds from the Project Granite Facility, an approximately $421.4 million project finance

credit facility with a syndicate of nine lenders for the first phase of our Cape Station development that we closed on

March 6, 2026. As of April 29, 2026, we had an aggregate of $64.0 million of borrowings outstanding under the

Credit Facility and $172.3 million of borrowings outstanding under the Project Granite Facility.

Preliminary Capital Expenditure and Construction Update

For the three months ended March 31, 2026, we estimate capital expenditures to be between $180.0 million and

$200.0 million, as compared to capital expenditures of $93.9 million for the three months ended March 31, 2025.

Capital expenditures during the period were primarily directed toward continued construction of our Cape Station

project in Utah, where we have approximately 500 megawatts of capacity under construction.

Preliminary Contractual and Commercial Update

As of March 31, 2026, we had 658 megawatts of binding power purchase agreements with remaining terms of

approximately 15 years, unchanged from December 31, 2025. In addition, during the three months ended March 31,