PUBLIC

March 2026

Management’s Discussion and Analysis

and Annual Financial Statements: 31 December 2025

This document is being disclosed to the public in accordance with ADB’s Access to Information Policy.

CONTENTS

Management’s Discussion and Analysis

Executive Summary

| I. | Overview | 1 | ||

| II. | Ordinary Capital Resources | 2 | ||

| A. | Basis of Financial Reporting | 2 | ||

| B. | Overall Financial Results | 4 | ||

| C. | Operating Activities | 7 | ||

| 1. | Loans | 8 | ||

| 2. | Equity Investments | 16 | ||

| 3. | Guarantees | 16 | ||

| 4. | Other Debt Securities | 18 | ||

| 5. | Nonsovereign Cofinancing and Direct Mobilization | 18 | ||

| 6. | Transaction Advisory Services | 18 | ||

| 7. | Debt Management Products | 19 | ||

| D. | Funding Resources | 19 | ||

| 1. | Equity | 19 | ||

| 2. | Borrowings | 20 | ||

| E. | Liquidity Management | 23 | ||

| 1. | Liquidity Portfolio | 23 | ||

| 2. | Prudential Minimum Liquidity | 24 | ||

| 3. | Contractual Cash Obligations | 25 | ||

| F. | Risk Management | 25 | ||

| 1. | Credit Risk | 26 | ||

| 2. | Market Risk | 34 | ||

| 3. | Liquidity Risk | 35 | ||

| 4. | Operational Risk | 35 | ||

| 5. | Capital Adequacy | 36 | ||

| 6. | Asset and Liability Management | 37 | ||

| G. | Internal Control over Financial Reporting | 37 | ||

| H. | Critical Accounting Policies and Estimates | 37 | ||

| III. | Special Funds | 39 | ||

| A. | Asian Development Fund | 39 | ||

| B. | Technical Assistance Special Fund | 41 | ||

| C. | Japan Special Fund | 42 | ||

| D. | Asian Development Bank Institute | 42 | ||

| E. | Regional Cooperation and Integration Fund | 43 | ||

| F. | Climate Change Fund | 43 | ||

| G. | Asia Pacific Disaster Response Fund | 44 | ||

| H. | Financial Sector Development Partnership Special Fund | 44 | ||

| IV. | Trust Funds and Cofinancing Under Administration | 45 | ||

| Appendix: | Ordinary Capital Resources Condensed Management Reporting (Non-GAAP measure) Balance Sheets | 47 |

Financial Statements, Management’s Report on Internal Control over Financial Reporting, and Independent Auditor’s Reports

| I. Ordinary Capital Resources (OCR) | ||

| Management’s Report on Internal Control over Financial Reporting | 50 | |

| Independent Auditor’s Report on Internal Control over Financial Reporting | 51 | |

| Independent Auditor’s Report on Financial Statements | 53 | |

| OCR-1 | Balance Sheet | 56 |

| OCR-2 | Statement of Income and Expenses | 58 |

| OCR-3 | Statement of Comprehensive Income | 59 |

| OCR-4 | Statement of Changes in Equity | 60 |

| OCR-5 | Statement of Cash Flows | 61 |

| OCR-6 | Summary Statement of Loans — Operations | 62 |

| OCR-7 | Summary Statement of Borrowings | 64 |

| OCR-8 | Statement of Subscriptions to Capital Stock and Voting Power | 66 |

| OCR-9 | Notes to Financial Statements | 68 |

| II. Asian Development Fund (ADF) | ||

| Management’s Report on Internal Control over Financial Reporting | 119 | |

| Independent Auditor’s Report on Internal Control over Financial Reporting | 120 | |

| Independent Auditor’s Report on Financial Statements | 122 | |

| ADF-1 | Balance Sheet | 125 |

| ADF-2 | Statement of Income and Expenses | 126 |

| ADF-3 | Statement of Comprehensive Loss | 127 |

| ADF-4 | Statement of Changes in Fund Balances | 127 |

| ADF-5 | Statement of Cash Flows | 128 |

| ADF-6 | Statement of Resources | 129 |

| ADF-7 | Notes to Financial Statements | 130 |

| III. Technical Assistance Special Fund (TASF) | ||

| Management’s Report on Internal Control over Financial Reporting | 139 | |

| Independent Auditor’s Report on Internal Control over Financial Reporting | 140 | |

| Independent Auditor’s Report on Financial Statements | 142 | |

| TASF-1 | Statement of Financial Position | 145 |

| TASF-2 | Statement of Activities and Changes in Net Assets | 146 |

| TASF-3 | Statement of Cash Flows | 147 |

| TASF-4 | Statement of Resources | 148 |

| TASF-5 | Notes to Financial Statements | 149 |

| IV. Japan Special Fund (JSF) | ||

| Management’s Report on Internal Control over Financial Reporting | 157 | |

| Independent Auditor’s Report on Internal Control over Financial Reporting | 158 | |

| Independent Auditor’s Report on Financial Statements | 160 | |

| JSF-1 | Statement of Financial Position | 163 |

| JSF-2 | Statement of Activities and Changes in Net Assets | 164 |

| JSF-3 | Statement of Cash Flows | 165 |

| JSF-4 | Notes to Financial Statements | 166 |

| V. Asian Development Bank Institute (ADBI) | ||

| Independent Auditor’s Report on Financial Statements | 172 | |

| ADBI-1 | Statement of Financial Position | 175 |

| ADBI-2 | Statement of Activities and Changes in Net Assets | 176 |

| ADBI-3 | Statement of Cash Flows | 177 |

| ADBI-4 | Notes to Financial Statements | 178 |

| VI. Regional Cooperation and Integration Fund (RCIF) | ||

| Management’s Report on Internal Control over Financial Reporting | 191 | |

| Independent Auditor’s Report on Internal Control over Financial Reporting | 192 | |

| Independent Auditor’s Report on Financial Statements | 194 | |

| RCIF-1 | Statement of Financial Position | 197 |

| RCIF-2 | Statement of Activities and Changes in Net Assets | 198 |

| RCIF-3 | Statement of Cash Flows | 199 |

| RCIF-4 | Notes to Financial Statements | 200 |

| VII. Climate Change Fund (CCF) | ||

| Management’s Report on Internal Control over Financial Reporting | 206 | |

| Independent Auditor’s Report on Internal Control over Financial Reporting | 207 | |

| Independent Auditor’s Report on Financial Statements | 209 | |

| CCF-1 | Statement of Financial Position | 212 |

| CCF-2 | Statement of Activities and Changes in Net Assets | 213 |

| CCF-3 | Statement of Cash Flows | 214 |

| CCF-4 | Notes to Financial Statements | 215 |

| VIII. Asia Pacific Disaster Response Fund (APDRF) | ||

| Management’s Report on Internal Control over Financial Reporting | 221 | |

| Independent Auditor’s Report on Internal Control over Financial Reporting | 222 | |

| Independent Auditor’s Report on Financial Statements | 224 | |

| APDRF-1 | Statement of Financial Position | 227 |

| APDRF-2 | Statement of Activities and Changes in Net Assets | 228 |

| APDRF-3 | Statement of Cash Flows | 229 |

| APDRF-4 | Notes to Financial Statements | 230 |

| IX. Financial Sector Development Partnership Special Fund (FSDPSF) | ||

| Management’s Report on Internal Control over Financial Reporting | 236 | |

| Independent Auditor’s Report on Internal Control over Financial Reporting | 237 | |

| Independent Auditor’s Report on Financial Statements | 239 | |

| FSDPSF-1 | Statement of Financial Position | 242 |

| FSDPSF-2 | Statement of Activities and Changes in Net Assets | 243 |

| FSDPSF-3 | Statement of Cash Flows | 244 |

| FSDPSF-4 | Notes to Financial Statements | 245 |

|

1

|

ADB. 2024. Strategy 2030 Midterm Review: An Evolution Approach for the Asian Development Bank.

|

|

2

|

The figures are for ordinary capital resources (OCR) and Special Funds. Special Funds include the Asian Development Fund (ADF), Technical Assistance Special Fund (TASF), Japan Special Fund (JSF), Regional

Cooperation and Integration Fund (RCIF), Asia Pacific Disaster Response Fund (APDRF), Climate Change Fund (CCF) and Financial Sector Development Partnership Special Fund (FSDPSF).

|

|

3

|

US dollar equivalent based on the Board of Governors’ Resolution No. 427 exchange rates.

|

|

4

|

ADB. 2025. Board of Governors’ Resolution No. 437 – Removal of the ADB Charter Lending Limitation.

|

|

1

|

ADB. 1966. Agreement Establishing the Asian Development Bank.

|

|

2

|

Following the provisions of Board of Governors’ Resolution No. 431, one nonregional member became a regional member effective 30 April 2025.

|

|

3

|

The figures are for ordinary capital resources (OCR) and Special Funds. Special Funds include the Asian Development Fund (ADF), Technical Assistance Special Fund (TASF), Japan Special Fund (JSF), Regional

Cooperation and Integration Fund (RCIF), Asia Pacific Disaster Response Fund (APDRF), Climate Change Fund (CCF) and Financial Sector Development Partnership Special Fund (FSDPSF).

|

|

4

|

ADB. 2025. Capital Utilization Plan. https://www.adb.org/documents/capital-utilization-plan

|

|

A.

|

Basis of Financial Reporting |

|

5

|

ADB’s Charter stipulates that the Board of Governors shall determine the allocation of net income annually.

|

|

B.

|

Overall Financial Results

|

|

Item

|

2025

|

2024

|

Change

|

|||||||||

|

Revenue from loans—operationsa

|

7,102

|

8,038

|

(936

|

)

|

||||||||

|

Sovereign regular

|

5,927

|

6,841

|

(914

|

)

|

||||||||

|

Sovereign concessional

|

721

|

717

|

4

|

|||||||||

|

Nonsovereign

|

454

|

480

|

(26

|

)

|

||||||||

|

Revenue from investments for liquidity purpose

|

2,553

|

2,713

|

(160

|

)

|

||||||||

|

Interest

|

2,551

|

2,731

|

(180

|

)

|

||||||||

|

Realized gains (losses) on sale of investments

|

2

|

(18

|

)

|

20

|

||||||||

|

Revenue from equity investments—operations

|

169

|

115

|

54

|

|||||||||

|

Net realized gainsb, c

|

8

|

13

|

(5

|

)

|

||||||||

|

Dividends and others

|

9

|

4

|

5

|

|||||||||

|

Realized gains on equity method investmentsd

|

45

|

71

|

(26

|

)

|

||||||||

|

Unrealized gains on equity method investmentsd

|

107

|

27

|

80

|

|||||||||

|

Revenue from guarantees—operations

|

27

|

27

|

0

|

|||||||||

|

Revenue from other debt securities—operations

|

47

|

47

|

(0

|

)

|

||||||||

|

Interest and others

|

45

|

47

|

(2

|

)

|

||||||||

|

Realized gains

|

2

|

–

|

2

|

|||||||||

|

Revenue from other sources

|

94

|

84

|

10

|

|||||||||

|

Borrowings and related expensese

|

(7,520

|

)

|

(8,717

|

)

|

1,197

|

|||||||

|

(Provision) Release of provision for credit losses

|

(24

|

)

|

45

|

(69

|

)

|

|||||||

|

Administrative expenses—OCR

|

(817

|

)

|

(729

|

)

|

(88

|

)

|

||||||

|

Other expenses

|

(44

|

)

|

(30

|

)

|

(14

|

)

|

||||||

|

Net unrealized gains

|

316

|

36

|

280

|

|||||||||

|

Fair value changes

|

313

|

41

|

272

|

|||||||||

|

Reclassification of unrealized gains on divested equity investmentsc

|

–

|

(2

|

) |

2

|

||||||||

|

Translation adjustments of nonfunctional currencies

|

3 | (3 | ) | 6 |

||||||||

| Net income | 1,903 | 1,629 |

274 |

|||||||||

|

Appropriation of guarantee fees to special reserve

|

(20 | ) | (27 | ) | 7 |

|||||||

| Net income after appropriation of guarantee fees to special reserve | 1,883 | 1,602 |

281

|

|||||||||

| Adjustments |

(423

|

)

|

(63

|

)

|

(360

|

)

|

||||||

|

Net unrealized gains

|

(316

|

)

|

(36

|

)

|

(280

|

)

|

||||||

|

Unrealized gains on equity method investmentsd

|

(107 | ) | (27 | ) | (80 | ) | ||||||

|

Allocable net income (non-GAAP measure)

|

1,460 |

1,539 |

(79 | ) | ||||||||

|

a

|

Includes interest revenue, commitment charges, amortization of front-end fees and loan origination cost and interest on asset swaps. Excludes funding costs.

|

|

b

|

Includes $10 million ($13 million – 2024) realized gains on disposal of equity investments, net of $2 million (nil – 2024) impairment loss on equity method investments.

|

|

c

|

Sale of equity investments in 2024 resulted in reclassification of the unrealized gains up to 31 December 2023 of $2 million to realized gains. The net realized gains up to the date of sale in 2025

amounted to $10 million ($13 million – 2024).

|

|

d

|

Pertains to ADB’s proportionate share of gains or losses from equity method investments.

|

|

e

|

Net of $1 million (nil – 2024) realized gains from early redemption of borrowings.

|

|

-

|

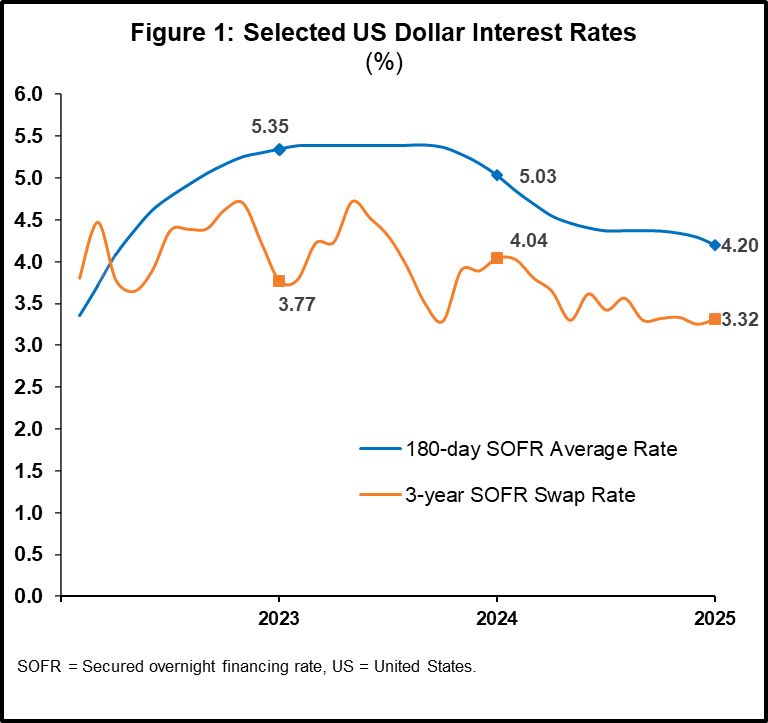

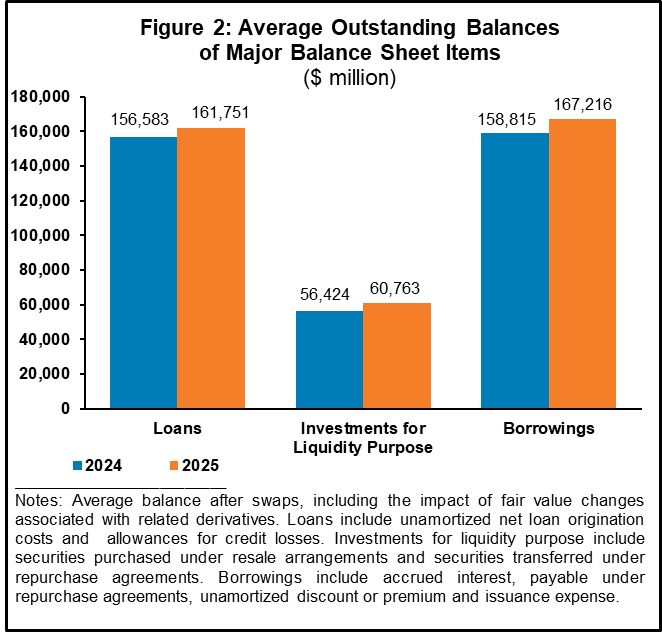

Revenue from loans, excluding funding costs, decreased by $936 million primarily because of the lower average interest rates (Figure 1) applied to regular OCR loans partially offset by the

increase in average loans outstanding in 2025 (Figure 2),

|

|

-

|

Revenue from investments for liquidity purpose decreased by $160 million mainly because of the $180 million decrease in interest revenue driven by the lower short-term interest rates

on debt-funded liquidity investments compared to 2024 (Figure 1),

|

|

-

|

Revenue from equity investments, excluding unrealized gains on equity method investments, decreased by $26 million ($62 million – 2025, $88 million – 2024) mainly due to the lower

realized gains on equity method investments,

|

|

-

|

Borrowings and related expenses decreased by $1,197 million mainly because of the lower level of short-term interest rates (Figure 1). Consistent with the market movements, average

cost of borrowings under management reporting basis decreased to 4.5% in 2025 from 5.5% in 2024,

|

|

-

|

Provision for credit losses amounted to $24 million for the year ended 31 December 2025. The provision in 2025 was mainly driven by a weaker macroeconomic outlook amid geopolitical

tensions and global trade uncertainties,

|

|

-

|

Administrative expenses of OCR increased by $88 million primarily because of the higher salaries and benefits expenses, and

|

|

|

|

6

|

Allocable net income is defined as net income after appropriation of guarantee fees to special reserve and certain adjustments set aside in the cumulative revaluation adjustments account.

|

| - |

$316 million net unrealized gains for the year ended 31 December 2025 ($36 million – 2024) was largely due to the fair value gains of derivatives driven mainly by the change in medium-and long-term interest rates from end of

2024 levels (Table 2).

|

|

Item

|

2025

|

2024

|

Change

|

|||||||||

|

Fair value changes from:

|

313

|

41

|

272

|

|||||||||

|

Borrowings and related derivatives

|

106

|

485

|

(379

|

)

|

||||||||

|

Loans related derivatives

|

139

|

(401

|

)

|

540

|

||||||||

|

Investments related derivatives

|

59

|

(25

|

)

|

84

|

||||||||

|

Equity investments

|

9

|

(18

|

)

|

27

|

||||||||

|

Reclassification of unrealized gains on divested equity investment

|

–

|

(2

|

)

|

2

|

||||||||

|

Translation adjustments of nonfunctional currencies

|

3

|

(3

|

)

|

6

|

||||||||

|

Total

|

316

|

36

|

280

|

|||||||||

|

Item

|

2025

|

2024

|

2023

|

|||||||||

|

Operational Highlights ($ million)

|

||||||||||||

|

Loans, Guarantees, EI, and ODS Committeda

|

27,717

|

22,920

|

22,518

|

|||||||||

|

Loans, EI, and ODS Disbursements

|

18,171

|

17,911

|

17,077

|

|||||||||

|

Loans and ODS Principal Repayments and Prepayments

|

13,232

|

12,956

|

10,585

|

|||||||||

|

Loans, EI, and ODS Outstanding

|

163,607

|

156,112

|

153,088

|

|||||||||

|

Statutory Reporting Basis

|

||||||||||||

|

Net Income ($ million)

|

1,903

|

1,629

|

938

|

|||||||||

|

Return on Earning Assetsb

|

0.9

|

0.8

|

0.5

|

|||||||||

|

Return on Equityc

|

3.3

|

2.9

|

1.7

|

|||||||||

|

Return on Loansd

|

4.5

|

4.9

|

4.7

|

|||||||||

|

Return on Investments for Liquidity Purposee

|

4.3

|

4.8

|

3.9

|

|||||||||

|

Cost of Borrowingsf

|

4.4

|

5.2

|

5.2

|

|||||||||

|

Management Reporting Basis (non-GAAP measure)g

|

||||||||||||

|

Allocable Net Incomeh ($ million)

|

1,460

|

1,539

|

1,423

|

|||||||||

|

Return on Earning Assetsb

|

0.7

|

0.7

|

0.7

|

|||||||||

|

Return on Equityc

|

2.6

|

2.8

|

2.7

|

|||||||||

|

Return on Loansd

|

4.4

|

5.2

|

5.0

|

|||||||||

|

Return on Investments for Liquidity Purposee

|

4.2

|

4.8

|

4.5

|

|||||||||

|

Cost of Borrowingsf

|

4.5

|

5.5

|

5.2

|

|||||||||

|

Capital Utilization Ratioi

|

72.6

|

71.5

|

70.0

|

|||||||||

|

a

|

Includes commitments under the private sector programs namely, the Trade and Supply Chain Finance and the Microfinance Program.

|

|

b

|

Net income (for statutory reporting basis) or allocable net income (for management reporting basis) divided by average earning assets. Earning assets comprise investments for

liquidity purpose, loans outstanding, equity investments, and other debt securities (all after swaps, if applicable).

|

|

c

|

Net income (for statutory reporting basis) or allocable net income (for management reporting basis) divided by average equity balances.

|

|

d

|

Interest revenue on loans, commitment fees, other revenue or expenses on loans and related swaps, and gains or losses on related swaps divided by average outstanding loans

after swaps. For the year ended 31 December 2025, under statutory basis reporting, the return on regular and concessional OCR loans was 5.0% and 2.7%, respectively, while under management basis reporting, the return on regular

and concessional OCR loans was 5.0% and 2.1%, respectively.

|

|

e

|

Interest revenue and gains or losses on investments and related swaps divided by average balances of investments after swaps.

|

|

f

|

Financial expenses and gains or losses on borrowings and related swaps divided by average outstanding borrowings after swaps.

|

|

g

|

Management reporting basis ratios exclude impact of unrealized gains or losses from fair value changes associated with certain financial instruments, unrealized gains or

losses on equity method investments, and nonnegotiable and noninterest-bearing demand obligations on account of subscribed capital.

|

|

h

|

Allocable net income is defined as net income after appropriation of guarantee fees to special reserve and certain adjustments set aside in the cumulative revaluation

adjustments account.

|

|

i

|

Capital utilization ratio is the ratio of the total economic capital used to usable equity. The capital utilization ratios are computed based on the 2023 capital adequacy

framework.

|

| C. |

Operating Activities

|

| 1. |

Loans

|

| 7 |

ADB. 2025. Board of Governors’ Resolution No. 437 – Removal of the ADB Charter Lending Limitation.

|

|

-

|

Project –Also known as investment lending, it finances expenditures incurred for discrete investment projects and focuses on project implementation. Disbursements in this modality are linked

to expenditures for inputs. Nonsovereign loans fall under this modality.

|

|

-

|

Policy-based – This modality provides sovereign budget support for structural reforms and development expenditure programs in DMCs. In certain circumstances, it may also be used to provide

balance of payments or counter-cyclical fiscal support. It is linked to the implementation of policy reforms, disbursed quickly, and targeted to sector-wide and economy-wide impact.

|

|

-

|

Results-based – It supports government-owned sector programs and disburses ADB funds based on the achievement of program results.

|

| Sovereign |

||||||||||||||||

| Regular |

Concessional |

NSO | Total | |||||||||||||

|

2025

|

||||||||||||||||

|

Project Loan

|

73,812

|

22,327

|

6,683

|

102,822

|

||||||||||||

|

Policy-based Loan

|

39,310

|

12,193

|

–

|

51,503

|

||||||||||||

|

Results-based Loan

|

6,791

|

1,194

|

–

|

7,985

|

||||||||||||

|

Total Outstanding

|

119,913

|

35,714

|

6,683

|

162,310

|

||||||||||||

|

Accounting adjustmentsa

|

(551

|

)

|

(88

|

)

|

(39

|

)

|

(678

|

)

|

||||||||

|

119,361

|

35,626

|

6,644

|

161,631

|

|||||||||||||

|

Allowance for credit losses on loans

|

(84

|

)

|

(168

|

)

|

(316

|

)

|

(568

|

)

|

||||||||

|

Loans Outstanding

|

119,277

|

35,458

|

6,328

|

161,063

|

||||||||||||

|

2024

|

||||||||||||||||

|

Project Loan

|

72,968

|

21,441

|

5,754

|

100,163

|

||||||||||||

|

Policy-based Loan

|

36,537

|

11,133

|

–

|

47,670

|

||||||||||||

|

Results-based Loan

|

5,872

|

866

|

–

|

6,738

|

||||||||||||

|

Total Outstanding

|

115,377

|

33,439

|

5,754

|

154,570

|

||||||||||||

|

Accounting adjustmentsa

|

(25

|

)

|

(107

|

)

|

(34

|

)

|

(166

|

)

|

||||||||

|

115,352

|

33,332

|

5,720

|

154,404

|

|||||||||||||

|

Allowance for credit losses on loans

|

(91

|

)

|

(163

|

)

|

(286

|

)

|

(540

|

)

|

||||||||

|

Loans Outstanding

|

115,261

|

33,169

|

5,434

|

153,864

|

|

a

|

Includes fair value adjustment on loans, unamortized loan origination cost, and unamortized front-end fee.

|

|

|

Figure 3: Sectoral Breakdown of OCR Loans Outstanding

as of 31 December 2025 and 2024

($ billion)

|

|

|

|

|

2025: $162.3 billion

|

2024: $154.6 billion

|

|

|

|

|

|

|

|

|

OCR = ordinary capital resources.

Notes: OCR loans include sovereign and nonsovereign loans outstanding and exclude $568 million ($540 million – 2024) allowance for credit losses, and $678

million ($166 million – 2024) accounting adjustments for fair value adjustment on loans, unamortized loan origination cost, and unamortized front-end fee.

|

|

|

|

Item

|

2025

|

2024

|

||||||

|

Allowance for credit losses on loans

|

568

|

540

|

||||||

|

Sovereign regular OCR loans

|

84

|

91

|

||||||

|

Sovereign concessional OCR loansa

|

168

|

163

|

||||||

|

Nonsovereign loans

|

316

|

286

|

||||||

|

Allowance for credit losses on other debt securities

|

21

|

14

|

||||||

|

Liability for credit losses on off-balance sheet exposures

|

144

|

121

|

||||||

|

Totalb

|

733 |

675 |

||||||

| 2025 |

2024 | |||||||||||||||||||

|

Numbera

|

Amount

($ million)

|

Numbera

|

Amount

($ million)

|

Change

($ million)

|

||||||||||||||||

|

Sovereign Regular

|

72

|

18,238

|

60

|

13,473

|

4,765

|

|||||||||||||||

|

Project

|

46

|

9,047

|

36

|

6,390

|

2,657

|

|||||||||||||||

|

Policy-based

|

16

|

6,131

|

20

|

5,651

|

480

|

|||||||||||||||

|

Results-based

|

10

|

3,059

|

4

|

1,431

|

1,628

|

|||||||||||||||

|

Sovereign Concessional

|

44

|

3,479

|

56

|

4,610

|

(1,131

|

)

|

||||||||||||||

|

Project

|

28

|

1,689

|

37

|

2,773

|

(1,084

|

)

|

||||||||||||||

|

Policy-based

|

12

|

1,370

|

17

|

1,480

|

(110

|

)

|

||||||||||||||

|

Results-based

|

4

|

420

|

2

|

357

|

63

|

|||||||||||||||

|

Nonsovereign—Project

|

49

|

2,258

|

39

|

2,029

|

229

|

|||||||||||||||

|

Total

|

165

|

23,974

|

155

|

20,111

|

3,863

|

|||||||||||||||

|

a

|

Commitments for sovereign loans and nonsovereign project loans are counted based on the number of loans committed.

|

|

2025

|

2024 | |||||||||||||||

|

Disbursements

|

Repaymentsa

|

Disbursements

|

Repaymentsa

|

|||||||||||||

|

Sovereign Regular

|

11,865

|

9,330

|

12,898

|

9,319

|

||||||||||||

|

Project

|

5,541

|

5,353

|

6,278

|

4,831

|

||||||||||||

|

Policy-based

|

5,234

|

3,703

|

5,611

|

4,294

|

||||||||||||

|

Results-based

|

1,090

|

274

|

1,009

|

194

|

||||||||||||

|

Sovereign Concessional

|

3,322

|

2,015

|

3,367

|

1,982

|

||||||||||||

|

Project

|

1,593

|

1,464

|

1,697

|

1,457

|

||||||||||||

|

Policy-based

|

1,370

|

507

|

1,459

|

486

|

||||||||||||

|

Results-based

|

359

|

44

|

212

|

39

|

||||||||||||

|

Nonsovereignb

|

2,529

|

1,683

|

1,346

|

1,590

|

||||||||||||

|

Total

|

17,716

|

13,028

|

17,610

|

12,891

|

||||||||||||

|

a

|

Includes prepayment of $479 million for nine sovereign regular OCR loans, $2 million for one sovereign concessional OCR loan, and $105 million for 17

nonsovereign loans for the year ended 31 December 2025 ($606 million for six sovereign regular OCR loans and $210 million for 18 nonsovereign loans – 2024). Amounts are based on the United States dollar equivalent as of

receipt of payment.

|

|

b

|

Includes loan disbursement and repayments under the private sector programs.

|

| Sovereign |

||||||||||||||||||||||||

|

Product

|

Regular |

Concessional

|

Nonsovereign

|

|||||||||||||||||||||

|

2025

|

2024 |

2025

|

2024 | 2025 |

2024 | |||||||||||||||||||

|

Flexible loan producta

|

116,460

|

114,212 |

n/a

|

n/a

|

4,591

|

4,172

|

||||||||||||||||||

|

Local currency loans

|

3,360

|

1,013 |

n/a

|

n/a

|

2,092

|

1,582

|

||||||||||||||||||

|

Concessional loans

|

n/a

|

n/a |

35,714

|

33,439

|

n/a

|

n/a

|

||||||||||||||||||

|

Pool-based single currency loansb

|

93

|

152 |

n/a

|

n/a |

n/a

|

n/a | ||||||||||||||||||

|

Total Outstanding

|

119,913

|

115,377 |

35,714

|

33,439

|

6,683

|

5,754

|

||||||||||||||||||

|

Accounting adjustmentsc

|

(551

|

)

|

(25 | ) |

(88

|

)

|

(107

|

)

|

(39

|

)

|

(34

|

)

|

||||||||||||

|

Allowance for credit losses

|

(84

|

)

|

(91 | ) |

(168

|

)

|

(163

|

)

|

(316

|

)

|

(286

|

)

|

||||||||||||

|

Loans Outstanding

|

119,277

|

115,261 |

35,458

|

33,169

|

6,328

|

5,434

|

||||||||||||||||||

|

a

|

Includes fixed rate loans amounting to $5,509 million for sovereign regular OCR loans and $496 million for nonsovereign loans as of 31 December 2025 ($7,474 million for sovereign

regular OCR and $500 million for nonsovereign loans – 2024).

|

| b |

PSCLs are legacy loan products and are no longer offered.

|

| c |

Includes fair value adjustment on loans, unamortized loan origination cost, and unamortized front-end fee.

|

|

8

|

The Euro Interbank Offered Rate (EURIBOR) and New Zealand Dollar (NZD) bank bill rate will continue to be used for Euro and NZD loans, respectively.

|

|

Item

|

FLP

|

CSF

|

SPBL

|

LCL

|

|

A. Loan Term

|

For project and results-based,

flexible loan terms of up to 19 years of average loan maturity; For policy-based, loan term of 15 years including a grace period of up to 3 years |

Loan term of 7 years, including

a grace period of up to 3 years |

Loan term of 5 to 8 years,

including a grace period of up

to 3 years |

For project and results-based,

flexible loan terms of up to 19 years of average loan maturity; For policy-based, loan term of 15 years including a grace period of up to 3 years |

|

B. Cost-Base Ratea

|

|

|||

|

1. US dollar

|

6-month SOFR compounded in arrears

6-month TONA compounded in arrears

6-month EURIBOR

6-month Bank Bill Rate

|

|

||

|

2. Yen

|

|

|||

|

3. Euro

|

|

|||

|

4. New Zealand dollar

|

|

|||

|

5. Yuan

|

|

3-month SHIBOR

|

||

|

6. Tenge

|

|

ADB Funding Rate

|

||

|

7. Lari

|

|

ADB Funding Rate

|

||

|

C. Lending Spreadb

|

50

|

75

|

200

|

50

|

|

D. Maturity Premiumc for loans

with average maturity of

|

|

|||

|

1. < 9 years

|

0

|

|||

|

2. 9 years up to 13 years

|

0–40

|

|||

|

3. >13 years up to 16 years

|

0–50

|

|||

|

4. >16 years up to 19 years

|

0–75

|

|||

|

E. Surcharge or (Rebate)d

|

|

|

|

|

|

1. US dollar

|

37

|

42

|

|

|

|

2. Yen

|

(10)

|

|

|

|

|

3. Euro

|

23

|

|

|

|

|

4. New Zealand dollar

|

51

|

|

|

|

|

5. Yuan

|

|

|

(35)

|

|

|

F. Commitment Chargese

|

15

|

15

|

75

|

15

|

|

a

|

The LCL cost-base rate depends on whether financing in a local currency is based on back-to-back funding or the pool-based approach. For back-to-back funding, the cost-base rate comprises ADB’s

cost of a funding transaction undertaken to finance a specific loan. For a pool-based funding approach, the cost-base rate is based on the local floating-rate benchmark.

|

|

b

|

The current FLP and LCL effective contractual spread is 50 basis points for loans negotiated on or after 1 January 2014. The terms of emergency assistance loans are similar to FLP terms.

|

|

c

|

For loans which formal negotiations were completed on or after 1 April 2012, a maturity premium is added to the contractual spread and applied for the entire life of the loan. A limit of 19

years applies to the average loan maturity of FLP loans and LCLs. For all loans to regular OCR-only borrowing countries, approved on or after 1 January 2021, a new pricing structure was implemented to adjust the pricing

framework and introduce diversity in the current flat pricing structure for countries in different stages of development. The new maturity premium is applied for the life of a loan regardless of country group changes during

the tenor of the loan.

|

|

d

|

To maintain the principle of the cost pass-through pricing policy, ADB passes on its actual funding cost margin to its borrowers through a surcharge or rebate and these are incorporated into the

interest rate for the succeeding interest period. Rebates or surcharges for all FLPs are determined in January and July every year on the basis of the average funding cost margin below or above the relevant benchmark for the

preceding six months. The information presented is applicable from 1 July to 31 December 2025.

|

|

e

|

The commitment charge is levied on undisbursed balances beginning 60 days after signing of the applicable loan agreement. For loans under contingent disaster financing, the borrower will pay, in

lieu of commitment charges, a front-end fee of 25 or 10 basis points of the committed loan amount depending on the contingent disaster financing option.

|

|

Terms

|

Concessional

Assistance-Only

Countriesa

|

OCR Blend

Countriesb, c

|

SIDS

|

Emergency

Assistance

|

||||||||||||

|

A. Maturity (years)

|

24 – 32

|

25

|

40

|

40

|

||||||||||||

|

B. Grace period (years)

|

8

|

5

|

10

|

10

|

||||||||||||

|

C. Interest rate during the grace period

|

1.0

|

%

|

2.0

|

%

|

1.0

|

%

|

1.0

|

%

|

||||||||

|

D. Interest rate during the amortization period

|

1.5

|

%

|

2.0

|

%

|

1.0

|

%

|

1.0

|

%

|

||||||||

|

E. Principal repayment

|

|

|||||||||||||||

|

1. First 10 years after the grace period

|

Equal |

Equal |

2.0 |

%d | 2.0 |

%d | ||||||||||

|

2. Year thereafter

|

|

Equal |

|

Equal |

4.0

|

%d

|

4.0

|

%d

|

||||||||

|

a

|

Countries that are eligible for sovereign concessional OCR loans and/or Asian Development Fund grants.

|

|

b

|

Countries that are eligible for both sovereign regular and concessional OCR loans.

|

|

c

|

Applicable for projects with loan negotiations completed on or after 1 January 2013.

|

|

d

|

Principal repayment will be calculated based on the approved loan amount multiplied by the annual rate of 2.0% for the first 10 years after the grace

period and 4.0% thereafter.

|

|

2.

|

Equity Investments

|

|

Item

|

2025

|

2024

|

||||||

|

Direct investments

|

983

|

773

|

||||||

|

Private equity funds

|

1,009

|

854

|

||||||

|

Total equity investments

|

1,992

|

1,627

|

||||||

|

3.

|

Guarantees

|

|

9

|

Prudential buffer represents 80% and 100% of the signed and undisbursed amounts for private equity funds and direct equity investments, respectively.

|

|

-

|

Trade and Supply Chain Finance Program. The Trade Finance Program and the Supply Chain Finance Program were merged to create operational efficiency

and more holistic solutions to clients.

|

|

-

|

Microfinance Program. The MFP provides risk participation on revolving basis for loans made by commercial financial institutions to microfinance

institutions in ADB’s DMCs. As of 31 December 2025, MFP revolving cover is up to $600 million. The program provided guarantees financed by ADB amounting to $217 million in 2025 ($254 million – 2024) and the outstanding

guarantee amount as of 31 December 2025 was $167 million ($199 million – 2024).

|

|

2025

|

2024

|

Change

|

||||||||||

|

Short-term

|

1,871

|

1,789

|

81

|

|||||||||

|

Long-term

|

533

|

435

|

98

|

|||||||||

|

Totala

|

2,404

|

2,225

|

179

|

|||||||||

|

MFP = Microfinance Program, OCR = ordinary capital resources, TSCFP = Trade and Supply Chain Finance Program

|

||||||||||||

|

Notes: Short-term has maturity of less than 365 days. Long-term has maturity of 365 days or more. Numbers may not sum precisely because of rounding.

|

||||||||||||

|

a Includes $1,788 million guarantees ($1,625 million – 2024) and

$399 million loans ($346 million – 2024) under TSCFP, and $217 million ($254 million – 2024) guarantees under MFP.

|

||||||||||||

|

4.

|

Other Debt Securities

|

|

5.

|

Nonsovereign Cofinancing and Direct Mobilization

|

|

6.

|

Transaction Advisory Services

|

|

7.

|

Debt Management Products

|

|

D.

|

Funding Resources

|

|

1.

|

Equity

|

|

2025

|

2024

|

|||||||

|

Authorized (SDR106,392)

|

||||||||

|

Subscribed (SDR106,392)

|

$

|

145,833

|

$

|

138,749

|

||||

|

Less: Callable capital subscribed

|

138,525

|

131,796

|

||||||

|

Paid-in capital subscribed

|

7,308

|

6,953

|

||||||

|

Less: Other adjustmentsa

|

19

|

25

|

||||||

|

7,289

|

6,928

|

|||||||

|

Add: (1) ADF assets transferb

|

30,748

|

30,748

|

||||||

|

(2) Other reservesc

|

19,973

|

18,759

|

||||||

|

Total Equity

|

$

|

58,010

|

$

|

56,435

|

||||

|

ADF = Asian Development Fund, SDR = special drawing rights, OCR = ordinary capital resources.

|

|

|

| a |

Comprises discount and nonnegotiable, noninterest-bearing demand obligations on account of subscribed capital. (See OCR-1 of the Financial Statements).

|

|

| b | The transfer of ADF assets to OCR on 1 January 2017 was treated as a contribution from ADF which was recognized as a one-time income. | |

| c | Includes ordinary reserve, special reserve, surplus, cumulative revaluation adjustments, and net income after appropriation less net notional amounts required to maintain value of currency holdings and accumulated other comprehensive loss. (See OCR-1 of the Financial Statements). | |

|

For the years ended

|

||||||||

|

2024

|

2023

|

|||||||

|

Net Income

|

1,629

|

938

|

||||||

|

Adjustment to cumulative revaluation adjustments

|

(63

|

)

|

513

|

|||||

|

Appropriation of guarantee fees to special reserve

|

(27

|

)

|

(28

|

)

|

||||

|

Allocable net income (non-GAAP measure)

|

1,539

|

1,423

|

||||||

|

Allocation to ordinary reserve

|

1,016

|

1,005

|

||||||

|

Allocation to special funds

|

||||||||

|

Asian Development Fund

|

394

|

293

|

||||||

|

Technical Assistance Special Fund

|

130

|

110

|

||||||

|

Asia Pacific Disaster Response Fund

|

–

|

15

|

||||||

|

Total Allocated Net Income

|

1,539

|

1,423

|

||||||

|

( ) = negative, – = nil, OCR = ordinary capital resources.

Note: Numbers may not sum precisely because of rounding.

|

||||||||

|

2.

|

Borrowings

|

|

Themes

|

Amount

($ million)

|

Maturity range of

bonds issueda

|

|||

|

Green

|

9,914

|

1 to 14 years

|

|||

|

Gender

|

6,864

|

1 to 20 years

|

|||

|

Health

|

5,835

|

1 to 20 years

|

|||

|

Education

|

1,464

|

0.8 to 10 years

|

|||

|

Blue

|

539

|

5 to 15 years

|

|||

|

Water

|

401

|

1 to 15 years

|

|||

|

Biodiversity & Nature

|

97 |

10 years

|

|||

|

Total Outstanding Thematic Bonds

|

25,115

|

||||

|

Note: Numbers may not sum precisely because of rounding.

a Refers to maturity from bond’s issue date. Bonds with call options are assumed to be called on the first call or trigger date.

|

|||||

|

Item

|

2025

|

2024

|

||||||

|

Bonds

|

|

|

||||||

|

Total Principal Amount

|

41,704

|

33,130

|

||||||

|

Total Proceeds Amount

|

38,201

|

32,992

|

||||||

|

Average Maturity to First Call (years)a

|

4.6

|

4.5

|

||||||

|

Average Final Maturity (years)a

|

6.8

|

4.8

|

||||||

|

Euro Commercial Papers

|

|

|

||||||

|

Total Principal Amount

|

8,343

|

10,984

|

||||||

|

Total Proceeds Amount

|

8,308

|

10,921

|

||||||

|

Number of Transactions

|

75

|

91 |

||||||

|

a

|

Weighted average maturity calculations are based on weighted proceeds amount. 2024 figures were previously calculated based on weighted principal

amount and were restated based on weighted proceeds amount.

|

|

10

|

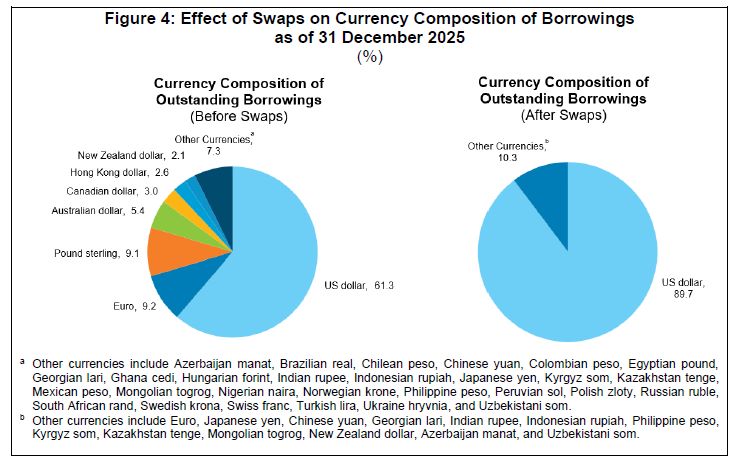

Australian dollar, Brazilian real, Canadian dollar, Chinese yuan, Egyptian pound, Euro, Georgian lari, Ghanaian cedi, Hong Kong dollar, Hungarian forint, Kazakhstan tenge, Mexican peso, Mongolian

togrog, Nigerian naira, Norwegian krone, Peruvian sol, Philippine peso, Polish zloty, Pound sterling, South African rand, Swedish krona, Swiss franc, Turkish lira, US dollar, and Uzbekistan sum.

|

|

E.

|

Liquidity Management

|

|

1.

|

Liquidity Portfolio

|

|

Investments

Outstandinga

($ million)

|

Return on Investment Portfolio

|

|||||||||||||||||||||||

|

Amortized Costb

(%)

|

Fair Valuec

(%)

|

|||||||||||||||||||||||

|

Item

|

2025

|

2024

|

2025

|

2024

|

2025

|

2024

|

||||||||||||||||||

|

Equity-Funded Liquidity Portfolio

|

19,842

|

19,817

|

3.2

|

3.0

|

5.8

|

3.8

|

||||||||||||||||||

|

Debt-Funded Liquidity Portfoliod

|

23,723

|

22,264

|

0.3

|

0.4

|

0.3

|

0.4

|

||||||||||||||||||

|

Cash Cushion Portfolio

|

15,693

|

6,199

|

4.6

|

5.7

|

4.7

|

6.0

|

||||||||||||||||||

|

Operational Cash Portfolio

|

206

|

214

|

3.3

|

4.7

|

3.3

|

4.7

|

||||||||||||||||||

|

Ad hoc Portfolio

|

1,344

|

1,236

|

2.6

|

2.6

|

6.3

|

3.6

|

||||||||||||||||||

|

Total

|

60,808

|

49,730

|

||||||||||||||||||||||

|

a

|

Includes securities transferred under repurchase agreements, securities purchased under resale arrangements, and investment related

swaps. The composition of the liquidity portfolio may shift from year to year as part of ongoing liquidity management.

|

|

b

|

Based on income from investments and realized gains and losses reported in the Statement of Income and Expenses.

|

|

c

|

Includes unrealized gains and losses reported in other comprehensive income and losses and movements are dependent on prevailing market

environment.

|

|

d

|

The return on debt-funded liquidity portfolio is presented as spread over funding cost on both amortized and fair value basis.

|

|

2.

|

Prudential Minimum Liquidity

|

| 3. |

Contractual Cash Obligations

|

|

Maturities

|

||||||||||||

|

Item

|

within

one year

|

more than one year

|

Total

|

|||||||||

|

Long-Term Debt

|

37,653

|

128,298

|

165,951

|

|||||||||

|

Undisbured Commitmentsa

|

15,075

|

42,851

|

57,925

|

|||||||||

|

Other Liabilities

|

2,402

|

79

|

2,480

|

|||||||||

|

Total

|

55,129

|

171,227

|

226,356

|

|||||||||

|

a

|

Includes undisbursed commitments for loans, equity investments, and other debt securities.

|

| F. |

Risk Management

|

|

11

|

ADB. 1966. By-Laws of the Asian Development Bank.

|

| 1. |

Credit Risk

|

|

ADB Internal

Rating Scale

|

Credit Rating

Agency Equivalent

|

ADB Definitions

|

|

1

|

AAA / Aaa to A / A2

|

Lowest expectation of credit risk

|

|

2

|

A– / A3

|

Very low credit risk

|

|

3

|

BBB+ / Baa1

|

Low credit risk

|

|

4

|

BBB / Baa2

|

Low credit risk

|

|

5

|

BBB– / Baa3

|

Low to moderate credit risk

|

|

6

|

BB+ / Ba1

|

Moderate credit risk

|

|

7

|

BB / Ba2

|

Moderate credit risk

|

|

8

|

BB– / Ba3

|

Moderate credit risk

|

|

9

|

B+ / B1

|

Significant credit risk

|

|

10

|

B / B2

|

Significant credit risk

|

|

11

|

B– / B3

|

High credit risk

|

|

12

|

CCC+ / Caa1

|

High credit risk

|

|

13

|

CCC / Caa2 to C

|

Very high credit risk

|

|

14

|

D

|

Nonaccrual

|

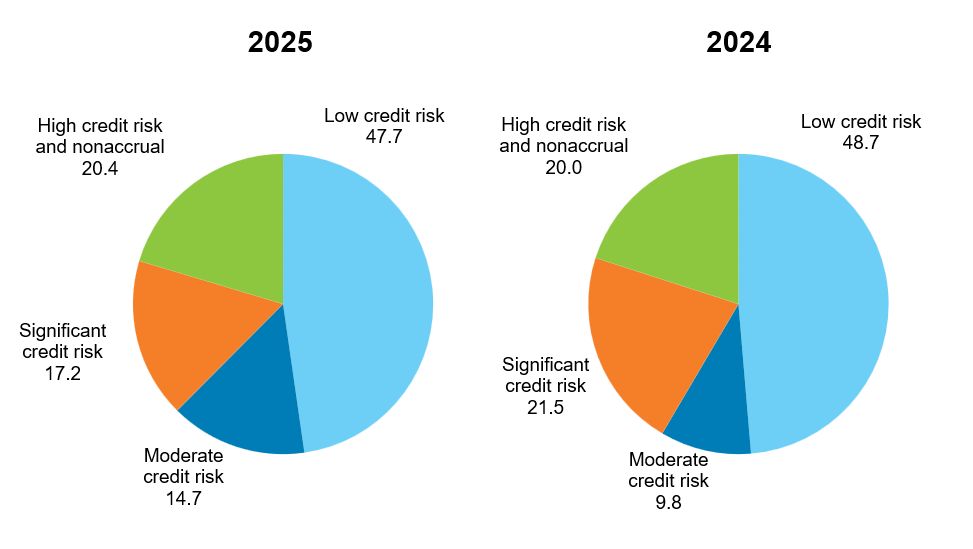

|

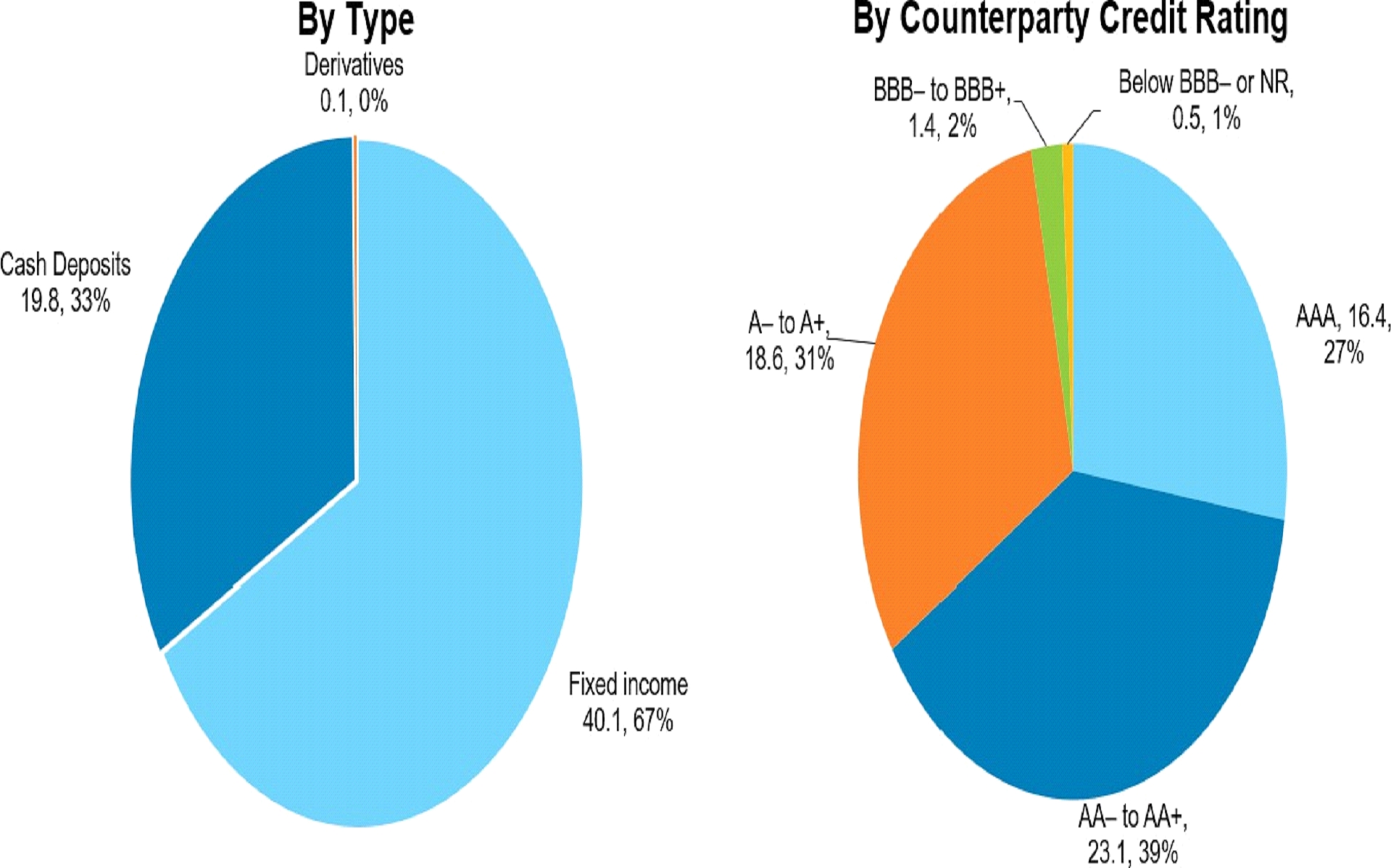

2025

|

2024

|

|||||||||||||||

|

Exposure

|

Rating

|

Exposure

|

Rating

|

|||||||||||||

|

Item

|

($ million)

|

(1–14)

|

($ million)

|

(1–14)

|

|

|||||||||||

|

Loans and guaranteesa

|

165,205

|

156,970

|

||||||||||||||

|

a. Sovereign operationsb

|

156,220

|

10.0 / B

|

|

149,030

|

10.1 / B

|

|

||||||||||

|

1. Regular OCR Loans and guarantees

|

120,563

|

9.4 / B+

|

|

115,647

|

9.4 / B+

|

|

||||||||||

|

2. Concessional OCR Loans

|

35,657

|

10.8 / B–

|

33,384

|

11.2 / B–

|

||||||||||||

|

b. Nonsovereign operations

|

8,985

|

8.9 / B+

|

|

7,939

|

9.8 / B

|

|

||||||||||

|

Equity Investmentsc

|

1,992

|

1,627

|

||||||||||||||

|

a. Sovereign operations

|

187

|

n/a

|

177

|

n/a

|

||||||||||||

|

b. Nonsovereign operations

|

1,805

|

n/a

|

1,450

|

n/a

|

||||||||||||

|

Treasuryd

|

60,724

|

|

AA |

50,198

|

|

AA

|

||||||||||

|

a. Fixed income

|

40,030

|

|

AA

|

38,041

|

|

AA | ||||||||||

|

b. Cash instruments

|

20,577

|

|

AA–

|

12,046

|

|

AA–

|

||||||||||

|

c. Derivatives

|

117

|

|

AA |

110

|

|

AA–

|

||||||||||

|

Aggregate Exposure

|

227,922

|

208,795

|

||||||||||||||

|

a

|

Sum of outstanding loan balances, present value of guaranteed obligation, and securities classified as debt net of specific provision.

|

|

b

|

As of 31 December 2025, $9 billion of the sovereign loan and guarantee credit exposure is part of the exposure exchange mechanism with

peer MDBs ($6 billion – 2024). The amount indicated excludes the ADB sovereign loans which are guaranteed by the MDB and includes the same amount of ADB guarantee issued to that MDB as

part of the exchange.

|

|

c

|

At fair values.

|

|

d

|

Average rating based on ratings from international credit rating agencies.

|

|

12

|

The average risk ratings are based on the average probability of default weighted by the outstanding credit exposure which is related back

to the internal rating scale based on the probability of default for each internal risk rating category. The probabilities of default are updated regularly. The computation of the average

risk rating for the period uses the most recent set of probabilities of default available at the end of the corresponding period. Starting year-end 2025, the calculation excludes exposures

in nonaccrual status (14 or D), which are already in default.

|

|

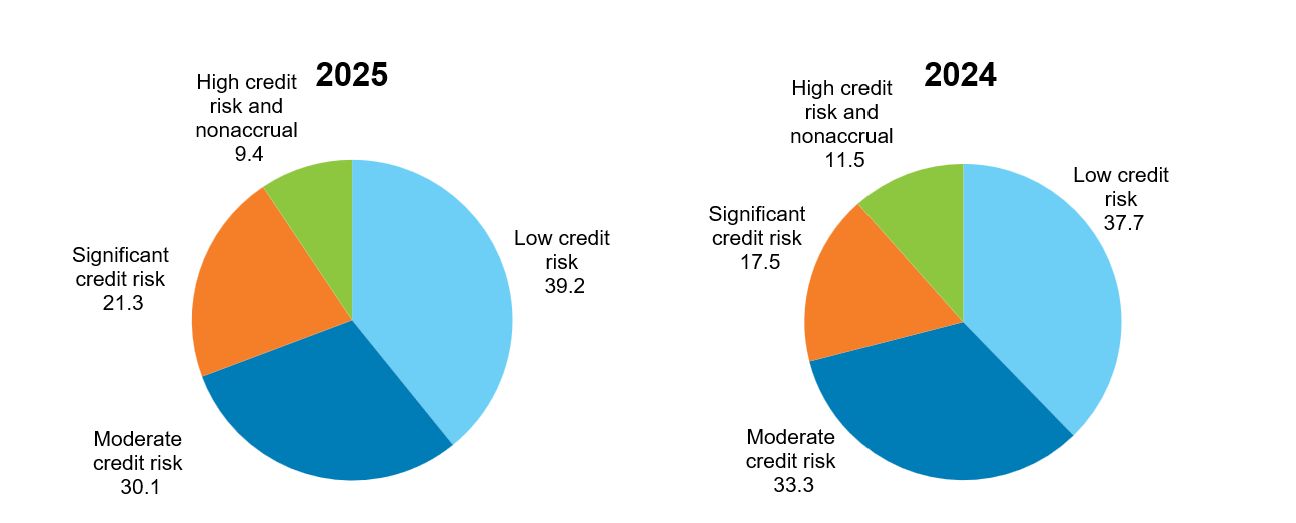

Figure 6: Sovereign Loan and Guarantee Exposure by Credit Quality

as of 31 December 2025 and 2024

(%)

|

||

Notes: Low credit risk = exposures with risk rating 1–5, moderate credit risk = exposures with risk rating 6–8, significant credit risk

= exposures with risk rating 9–10, high credit risk and nonaccrual = exposures with risk rating 11–14.

|

||

|

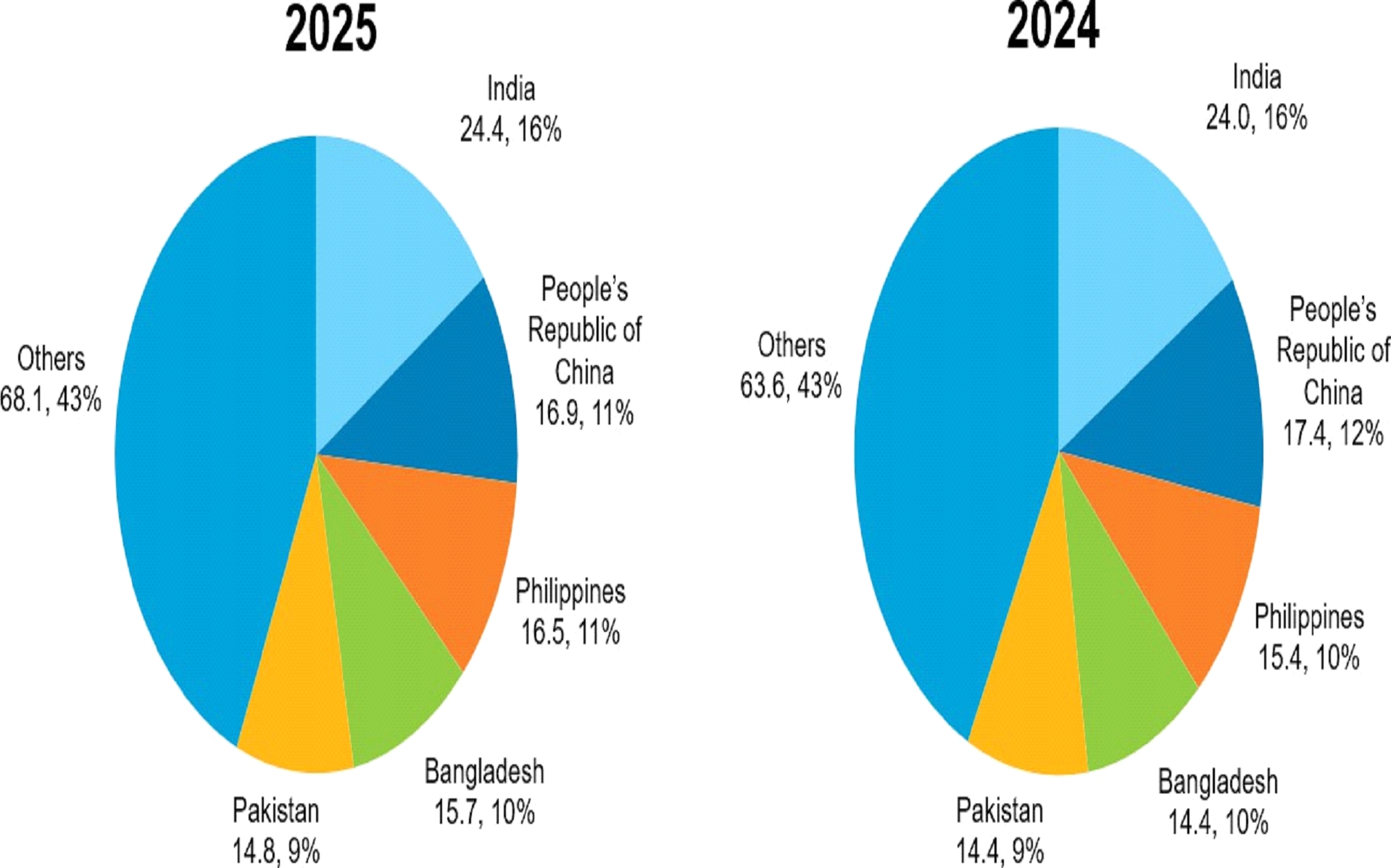

Figure 7: Sovereign Country Exposure

as of 31 December 2025 and 2024

($ billion, unless otherwise stated)

|

||

Note: The sum of disbursed and outstanding loan balances, present value of guaranteed obligations and fair values of equities.

|

||

|

Figure 8: Nonsovereign Loan and Guarantee Exposure by Credit Quality

as of 31 December 2025 and 2024

(%)

|

||

|

||

|

Notes: Low credit risk = exposures with risk rating 1–5, moderate credit risk = exposures with risk rating 6–8, significant credit risk =

exposures with risk rating 9–10, high credit risk and nonaccrual = exposures with risk rating 11–14. The breakdown represents the split of net exposure after allowance for credit

losses for individually impaired transactions.

|

|

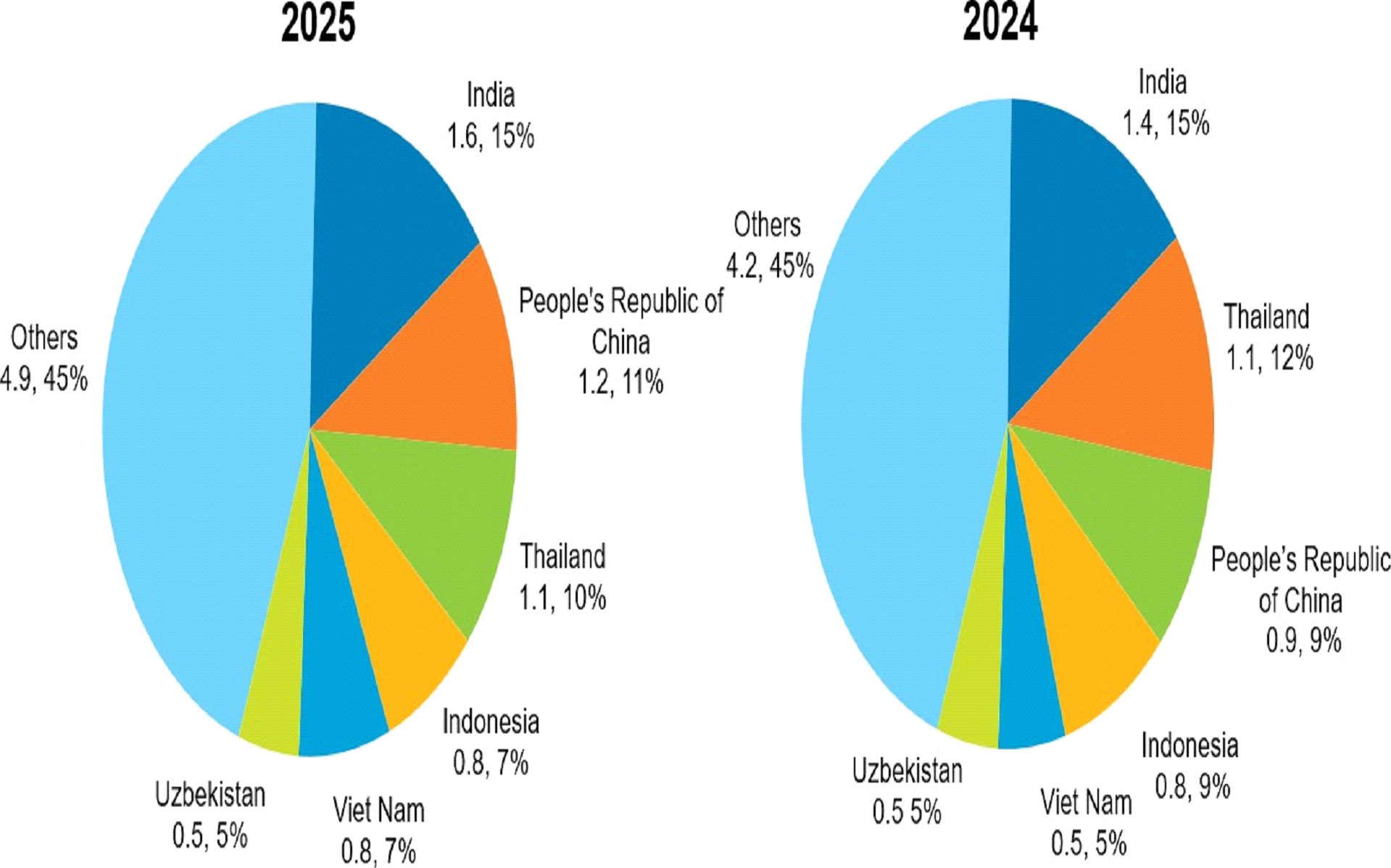

Figure 9: Nonsovereign Country Exposurea

as of 31 December 2025 and 2024

($ billion, unless otherwise stated)

|

||

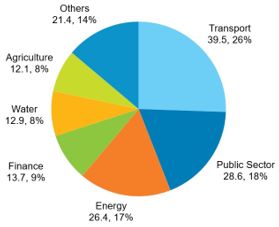

Note: Numbers may not sum precisely because of rounding.

a

The sum of disbursed and outstanding loan balances and other debt securities, present value of guaranteed obligations and fair values of equities.

|

|

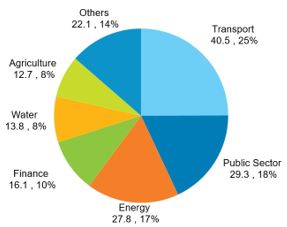

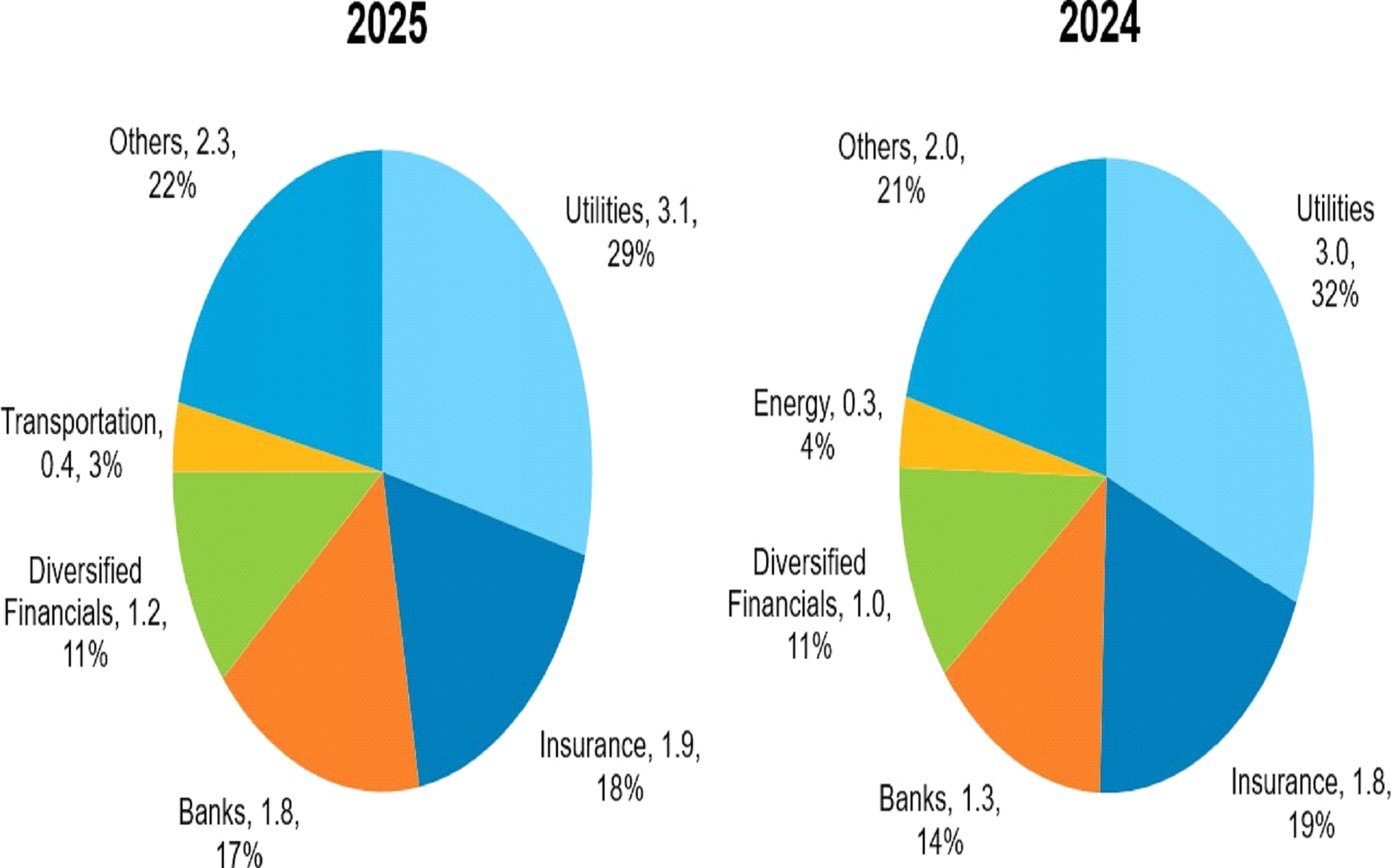

Figure 10: Nonsovereign Sector Exposure

as of 31 December 2025 and 2024

($ billion, unless otherwise stated)

|

||

Notes: Numbers may not sum precisely because of rounding. Percentages may not total 100% because of rounding.

|

|

Figure 11: Breakdown of Treasury Credit Exposure

as of 31 December 2025

($ billion, unless otherwise stated)

|

||

Notes: Numbers may not sum precisely because of rounding. Percentages may not total 100% because of rounding. 0% = percentage less than 0.5%.

|

|

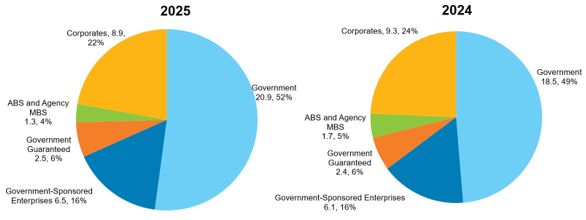

Figure 12: Fixed Income Portfolio by Asset Class

as of 31 December 2025 and 2024

($ billion, unless otherwise stated)

|

||

|

|

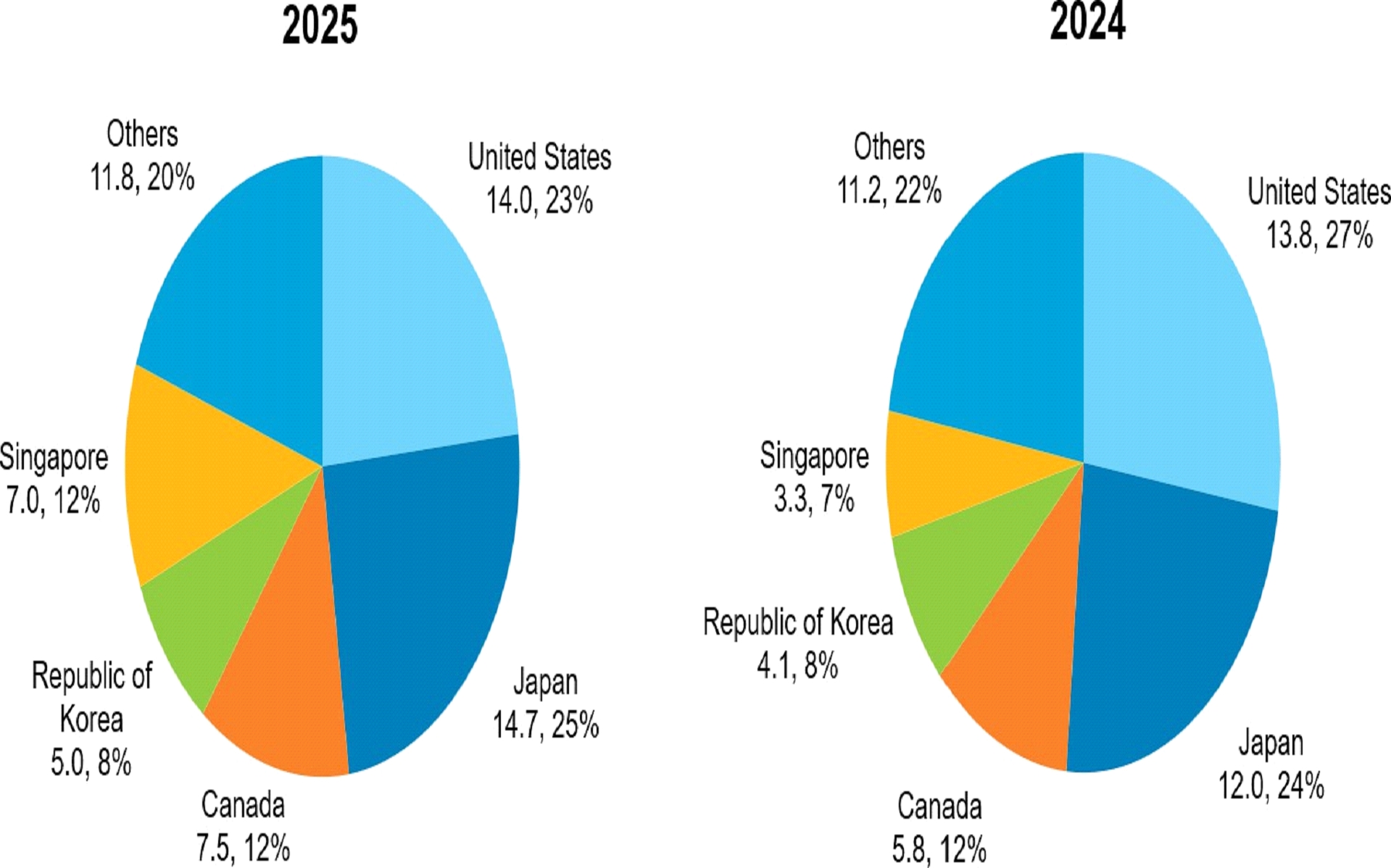

Figure 13: Treasury Country Exposure as

of 31 December 2025 and 2024

($ billion, unless otherwise stated)

|

||

Note: Numbers may not sum precisely because of rounding.

|

| 2. |

Market Risk

|

| 3. |

Liquidity Risk

|

| 4. |

Operational Risk

|

|

13

|

These changes in fair valuation would only be realized in case the investments are sold prior to maturity. ADB typically does not sell the bond

investments in the liquidity portfolio prior to maturity and thus the fluctuations in the fair value remain unrealized.

|

| 5. |

Capital Adequacy

|

| 6. |

Asset and Liability Management

|

| G. |

Internal Control over Financial Reporting

|

| H. |

Critical Accounting Policies and Estimates

|

| A. |

Asian Development Fund

|

|

14

|

US dollar equivalent based on the Board of Governors’ Resolution No. 427 exchange rates.

|

|

Item

|

Amount

|

|||

|

Carryover of ADF 13 Commitment Authority

|

415

|

|||

|

Other sources from previous ADF cyclesa

|

506

|

|||

|

ADF 14 contributions

|

445

|

|||

|

ADF 13 contributionsb

|

34

|

|||

|

Grant and guarantee savings and cancellations

|

3

|

|||

|

Income from liquidity investment

|

88

|

|||

|

OCR net income transfer

|

394

|

|||

|

Resources available for regular ADF

|

1,885

|

|||

|

ADF 14 Commitments

|

(1,310

|

)

|

||

|

Administrative expensesc

|

(98

|

)

|

||

|

ADF Commitment Authority Available for Future Commitments

|

476

|

|||

|

Notes: Numbers may not sum precisely because of rounding. Numbers are valued at exchange rates as of 31 December 2025. Commitments include grants and

guarantees under the private sector window, including the Wayfinder Program approved by the Board in June 2025.

a Resources earmarked for ADF 14

represent savings and cancellations from previous ADF cycles, as well as partial releases of ADF 13 funds allocated to the expanded disaster and pandemic response facility and debt

distress reserve (ADB. 2024. Thirteenth Replenishment of the Asian Development Fund and Eighth Regularized Replenishment of the Technical Assistance

Special Fund. Manila)

b

Represents payment from the United States.

c

Represents ADF’s share in the administrative expenses for 2025.

|

||||

|

15

|

ADF 14 encashment included encashment of promissory notes and cash payments. US dollar equivalent based on exchange rates as of 31 December 2025.

|

|

16

|

Includes securities purchased under resale arrangements.

|

ADB MANAGEMENT’S DISCUSSION AND ANALYSIS: 31 DECEMBER 2025

| B. |

Technical Assistance Special Fund

|

|

Item

|

2025

|

2024

|

||||||

|

Regularized Replenishment

|

||||||||

|

Contributions

|

2,642

|

2,128

|

||||||

|

Allocations from OCR Net Income

|

1,849

|

1,719

|

||||||

|

Direct Voluntary Contributions

|

91

|

91

|

||||||

|

Income from Investment and

|

||||||||

|

Other Sources

|

334

|

286

|

||||||

|

Transfers from the TASF to the ADF

|

(3

|

)

|

(3

|

)

|

||||

|

Total

|

4,913

|

4,222

|

||||||

|

( ) = negative, ADF = Asian Development Fund, OCR = ordinary capital resources,

TASF = Technical Assistance Special Fund.

Note: Numbers may not sum precisely because of rounding

|

||||||||

| C. |

Japan Special Fund

|

|

D.

|

Asian Development Bank Institute

|

|

17

|

In the event of a nonaccrual in the reference portfolio under the IF-CAP Guarantee Mechanism, the Government of Japan’s payment of its share of risk

participation will be channeled through the JSF IF-CAP Window.

|

| E. |

Regional Cooperation and Integration Fund

|

| F. |

Climate Change Fund

|

| G. |

Asia Pacific Disaster Response Fund

|

| H. |

Financial Sector Development Partnership Special Fund

|

|

18

|

B-loan is a tranche of a direct loan nominally advanced by ADB, subject to eligible financial institutions taking funded risk participation within such a tranche and without

recourse to ADB. It complements an A-loan financed by ADB.

|

| Item |

Amount |

Item | Amount | ||||||

|

Bilateral Partners

|

Multilateral Partners

|

||||||||

|

Australia

|

325.9

|

ADB Ventures Investment Fund 1

|

13.0

|

||||||

|

Austria

|

14.4

|

ADB Ventures Investment Fund 2

|

26.4

|

||||||

|

Canada

|

518.8

|

Clean Technology Fund

|

982.1

|

||||||

|

People’s Republic of China

|

90.0

|

Clean Technology Fund Parallel Fund

|

218.5

|

||||||

|

Finland

|

42.4

|

European Union

|

246.3

|

||||||

|

France

|

13.7

|

GEF/Least Developed Countries Fund

|

45.5

|

||||||

|

Germany

|

164.3

|

GEF/Special Climate Change Fund

|

12.2

|

||||||

|

Ireland

|

19.7

|

Global Agriculture and Food Security Program

|

87.1

|

||||||

|

Japan

|

3,293.3

|

Global Concessional Finance Facility

|

16.5

|

||||||

|

Korea, Republic of

|

271.7

|

Global Environment Facility

|

295.6

|

||||||

|

Luxembourg

|

11.1

|

Global Infrastructure Facility Partnership Program

|

1.4

|

||||||

|

Netherlands

|

37.8

|

Global Partnership for Education Fund

|

23.1

|

||||||

|

New Zealand

|

72.3

|

Green Climate Fund

|

1,451.1

|

||||||

|

Norway

|

162.6

|

International Finance Facility for Education Trust Fund

|

0.1

|

||||||

|

Spain

|

59.6

|

International Fund for Agricultural Development

|

0.1

|

||||||

|

Sweden

|

67.5

|

Nordic Development Fund

|

60.0

|

||||||

|

Switzerland

|

23.8

|

Pandemic Prevention, Preparedness and Response Trust Fund

|

19.8

|

||||||

|

Taipei,China

|

2.0

|

Strategic Climate Fund

|

466.1

|

||||||

|

United Kingdom

|

873.5

|

Women Entrepreneurs Finance Initiative Trust Fund

|

35.1

|

||||||

|

United States

|

461.1

|

World Bank

|

10.0

|

||||||

|

Subtotal

|

6,525.8

|

Subtotal

|

4,010.0

|

||||||

|

Private Partners

|

|||||||||

|

Gates Foundation

|

27.0

|

||||||||

|

Bloomberg Philanthropies

|

12.5

|

||||||||

|

Education Above All Foundation

|

24.5

|

||||||||

|

Global Energy Allicance for People and Planet LLC

|

25.8

|

||||||||

|

Goldman Sachs

|

12.5

|

||||||||

|

Korea Energy Agency

|

0.4

|

||||||||

|

Korea Venture Investment Corp.

|

10.0

|

||||||||

|

Ocean Risk and Resilience Action Alliance

|

0.3

|

||||||||

|

The OPEC Fund for International Development

|

5.4

|

||||||||

|

The Rockefeller Foundation

|

2.6

|

||||||||

|

Subtotal

|

120.8

|

||||||||

|

Grand Total

|

10,656.5

|

||||||||

| 2025 | 2024 |

|||||||||||||||

|

Item

|

Statutory

Reporting Basis

|

Adjustmentsa

|

Management

Reporting Basis

|

Management

Reporting Basis

|

||||||||||||

|

Due from banks

|

496

|

–

|

496

|

2,235

|

||||||||||||

|

Investments for liquidity purpose

|

57,725

|

–

|

57,725

|

46,695

|

||||||||||||

|

Securities transferred under repurchase agreements

|

872

|

–

|

872

|

–

|

||||||||||||

|

Securities purchased under resale arrangements

|

252

|

–

|

252

|

260

|

||||||||||||

|

Loans outstanding — operations

|

161,063

|

–

|

161,063

|

153,864

|

||||||||||||

|

Equity investments — operations

|

1,992

|

(413

|

)

|

1,579

|

1,329

|

|||||||||||

|

Other debt securities — operations

|

552

|

–

|

552

|

621

|

||||||||||||

| Derivative Assets |

||||||||||||||||

|

Borrowings

|

75,750

|

(32

|

)

|

75,718

|

62,476

|

|||||||||||

|

Investments for liquidity purpose

|

29,554

|

(299

|

)

|

29,255

|

25,669

|

|||||||||||

|

Loans — operations

|

17,391

|

(225

|

)

|

17,166

|

18,149

|

|||||||||||

|

Accrued interest receivable

|

1,684

|

–

|

1,684

|

1,697

|

||||||||||||

|

Other assets

|

1,719

|

5

|

1,724

|

2,010

|

||||||||||||

|

TOTAL

|

349,050

|

(964

|

)

|

348,086

|

315,005

|

|||||||||||

|

Borrowings and accrued interest

|

165,951

|

2,819

|

168,770

|

151,959

|

||||||||||||

| Derivative Liabilities | ||||||||||||||||

|

Borrowings

|

78,627

|

(3,249

|

)

|

75,378

|

66,906

|

|||||||||||

|

Investments for liquidity purpose

|

27,596

|

(86

|

)

|

27,510

|

23,058

|

|||||||||||

|

Loans — operations

|

15,501

|

392

|

15,893

|

15,675

|

||||||||||||

|

Payable under securities repurchase agreements

|

881

|

–

|

881

|

–

|

||||||||||||

|

Payable for swap related and other collateral

|

1,258

|

–

|

1,258

|

857

|

||||||||||||

|

Accounts payable and other liabilities

|

1,226

|

–

|

1,226

|

977

|

||||||||||||

|

Total Liabilities

|

291,040

|

(124

|

)

|

290,916

|

259,432

|

|||||||||||

|

Paid-in capital

|

7,289

|

5

|

7,294

|

6,940

|

||||||||||||

|

Net notional maintenance of value receivable

|

(1,651

|

)

|

–

|

(1,651

|

)

|

(1,481

|

)

|

|||||||||

|

Ordinary reserve

|

48,556

|

–

|

48,556

|

47,542

|

||||||||||||

|

Special reserve

|

578

|

–

|

578

|

558

|

||||||||||||

|

Surplus

|

1,065

|

–

|

1,065

|

1,065

|

||||||||||||

|

Cumulative revaluation adjustments account

|

525

|

(525

|

)

|

–

|

–

|

|||||||||||

|

Unallocated net incomeb

|

1,883

|

(423

|

)

|

1,460

|

1,539

|

|||||||||||

|

Accumulated other comprehensive loss

|

(235

|

)

|

103

|

(132

|

)

|

(590

|

)

|

|||||||||

|

Total Equity

|

58,010

|

(840

|

)

|

57,170

|

55,573

|

|||||||||||

|

TOTAL

|

349,050

|

(964

|

)

|

348,086

|

315,005

|

|||||||||||

|

a

|

Unrealized gains or losses from fair value adjustments associated with certain financial instruments, share of unrealized gain or loss from equity method investments, and nonnegotiable and noninterest-bearing

demand obligations on account of subscribed capital.

|

|

b

|

After appropriation of net guarantee fees to the Special Reserve.

|

|

|

Masato Kanda

|

|

President

|

|

| Roberta Casali |

| Vice-President (Finance and Risk Management) |

|

|

Helen Hall

|

|

Controller

|

|

Deloitte & Touche LLP Unique Entity No. T08LL0721A 6 Shenton Way OUE Downtown 2 #33-00 Singapore 068809 Tel: +65 6224 8288 Fax: +65 6538 6166 www.deloitte.com/sg |

| • |

Exercise professional judgment and maintain professional skepticism throughout the audit.

|

| • |

Obtain an understanding of internal control over financial reporting, assess the risks that a material weakness exists, and test and evaluate the design and operating effectiveness of

internal control over financial reporting based on the assessed risk.

|

|

|

Deloitte & Touche LLP

Unique Entity No. T08LL0721A 6 Shenton Way OUE Downtown 2 #33-00 Singapore 068809 Tel: +65 6224 8288 Fax: +65 6538 6166 www.deloitte.com/sg |

| • |

Exercise professional judgment and maintain professional skepticism throughout the audit.

|

| • |

Identify and assess the risks of material misstatement of the financial statements, whether due to fraud or error, and design and perform audit procedures

responsive to those risks. Such procedures include examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements.

|

| • |