SUBJECT TO EXECUTED NDA | CONFIDENTIAL Con | fid CO en NT tia AINS l | CoNON ntain- sP No UBLIC n-PuINFORMAT blic InformaIO tioN n Exhibit 99.1 Project Huskies Management Presentation May 2026 THIS PRESENTATION MAY CONTAIN MATERIAL NON-PUBLIC INFORMATION CONCERNING THE COMPANY (AS DEFINED HEREIN) AND ITS SUBSIDIARIES. BY ACCEPTING THIS PRESENTATION, THE RECIPIENT AGREES TO USE ANY SUCH INFORMATION IN ACCORDANCE WITH ITS COMPLIANCE POLICIES, CONTRACTUAL OBLIGATIONS AND APPLICABLE LAW, INCLUDING UNITED STATES FEDERAL AND STATE SECURITIES LAWS. Ducera © 2026 Confidential & Proprietary Information | Provided Pursuant to Executed NDA Ducera

SU SUBJ BJECT ECT T TO O EX EXECU ECUT TED ED ND NDA A || CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -P P PU U UBLIC BLIC BLIC INFORMAT INFORMAT INFORMATIO IO ION N N Disclaimer Presentation This presentation and the information contained herein is confidential and proprietary to Accendra Health, Inc. and its subsidiaries (“Accendra Health” or the “Company”) and is being provided to you subject to certain confidentiality obligations to which you are a party (including any confidentiality obligations pursuant to agreements that govern the Company’s indebtedness that you are a party to) (collectively, the “Confidentiality Agreements”). By accepting and/or viewing the contents of this presentation, you expressly agree to maintain the confidentiality of this presentation (including its existence) in accordance with the terms of the applicable Confidentiality Agreements and you further agree to the special notice set forth on the cover page hereof. If you are not willing to accept this presentation on the terms set forth herein and the special notice on the cover page hereof, you must return the presentation immediately without making any copies or extracts or using or viewing the information contained herein in any manner. If you are not the intended recipient of this presentation, you may not disclose or use the information in this presentation in any way. This presentation is being shared with you for informational purposes only and does not represent any commitment, promise or legal obligation, nor is it intended as an offer or solicitation with respect to the purchase or sale of any security. This presentation does not constitute an offer or commitment to lend, syndicate or arrange a financing, underwrite or purchase or act as an agent or advisor or in any other capacity with respect to any transaction. This presentation does not constitute and should not be considered as any form of legal, financial, accounting, investment or tax advice. This document is not, and under no circumstances is to be construed as, a prospectus, a public offering or an offering memorandum as defined under any applicable securities laws. None of Accendra Health, its affiliates, officers, directors, employees, professional advisors, agents or other representatives (collectively with Accendra Health, the “Company Representatives”) make any representation or warranty, express or implied, as to, and no reliance should be placed on, the fairness, accuracy, completeness or correctness of any of the information or opinions contained in this presentation. Furthermore, none of the Company Representatives shall have liability for damages of any kind, including, without limitation: direct, special, indirect or consequential damages that may result from the use of or reliance upon this presentation. Accendra Health has no obligation to pursue any course of business outlined in this presentation or any related documentation, and Accendra Health’s strategy and possible future developments, products and/or directions are all subject to change and may be changed by Accendra Health at any time for any reason without notice. Forward-Looking Statements This presentation contains certain “forward-looking” statements made pursuant to the Safe Harbor provisions of the Private Securities Litigation Reform Act of 1995. These statements include, but are not limited to, the statements in this presentation regarding our future prospects and performance, including our expectations with respect to our financial performance and financial results (and other financial projections), our expectations regarding the performance of our business following the completion of the sale of the Products & Healthcare Service business, our cost saving initiatives, future indebtedness and growth, industry trends, as well as statements related to our expectations regarding the performance of our business, including our ability to address macro and market conditions. Forward-looking statements involve known and unknown risks and uncertainties that may cause our actual results in future periods to differ materially from those projected or contemplated in the forward-looking statements. Investors should refer to Accendra Health’s Annual Report on Form 10-K for the year ended December 31, 2025, filed with the SEC on February 20, 2026, including the section captioned “Item 1A. Risk Factors,” as applicable, and subsequent quarterly reports on Form 10-Q and current reports on Form 8-K filed with or furnished to the SEC, for a discussion of certain known risk factors that could cause the Company’s actual results to differ materially from its current estimates. These filings are available at www.accendrahealth.com. Given these risks and uncertainties, Accendra Health can give no assurance that any forward-looking statements will, in fact, transpire and, therefore, cautions investors not to place undue reliance on them. Accendra Health specifically disclaims any obligation to update or revise any forward-looking statements, whether as a result of new information, future developments or otherwise. Financial Information Certain financial measures included herein are not prepared in accordance with U.S. GAAP, including Adjusted EBITDA, Adjusted EBITDA-Capex, Levered Free Cash Flow, Unlevered Free Cash Flow, Normalized Unlevered Free Cash Flow, Interest Coverage Ratio, Weighted Average Life, Implied Net 1L Leverage, and Implied Net Leverage, and use of such terms varies from others in the same industry. Management uses these non-GAAP financial measures internally to evaluate our performance, evaluate the balance sheet, engage in financial and operational planning and determine incentive compensation. Non-GAAP financial measures should not be considered as alternatives to measures derived in accordance with U.S. GAAP. Non-GAAP financial measures have important limitations as analytical tools and you should not consider them in isolation or as substitutes for results as reported in accordance with U.S. GAAP. Reconciliations of projected or targeted non-GAAP financial measures are not provided herein because such GAAP financial measures are not available on a forward-looking basis and such reconciliations could not be derived without unreasonable effort. We present certain potential add-backs as an adjustment to Adjusted EBITDA because we expect them to be a permitted add-back pursuant to agreements that govern or will govern our indebtedness. These potential add-backs are based on assumptions and estimates that could prove to be incorrect, and accordingly should not be viewed as a projection of future performance. Unless otherwise indicated, projected and forward-looking financial information and operating data presented herein reflect Accendra Health on a post-divestiture basis and exclude the results of operations of the Products & Healthcare Services business (“P&HS”). © 2026 Confidential & Proprietary to Accendra Health, Inc. p. p. 2 2 Ducera

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Table of Contents I. Accendra Health Overview II. Recent Financial Performance III. Key Investment Highlights IV. Capital Structure Optimization V. Appendix p. 3 p. 3 © 2026 Confidential & Proprietary to Accendra Health, Inc. Ducera

SU SUBJ BJECT ECT T TO O EX EXECU ECUT TED ED ND NDA A || CO CONFID NFIDEN ENT TIAL IAL || CO CONT NTAINS AINS NON NON- -P PU UBLIC BLIC INFORMAT INFORMATIO ION N I. Accendra Health Overview p. p. 4 4 Ducera

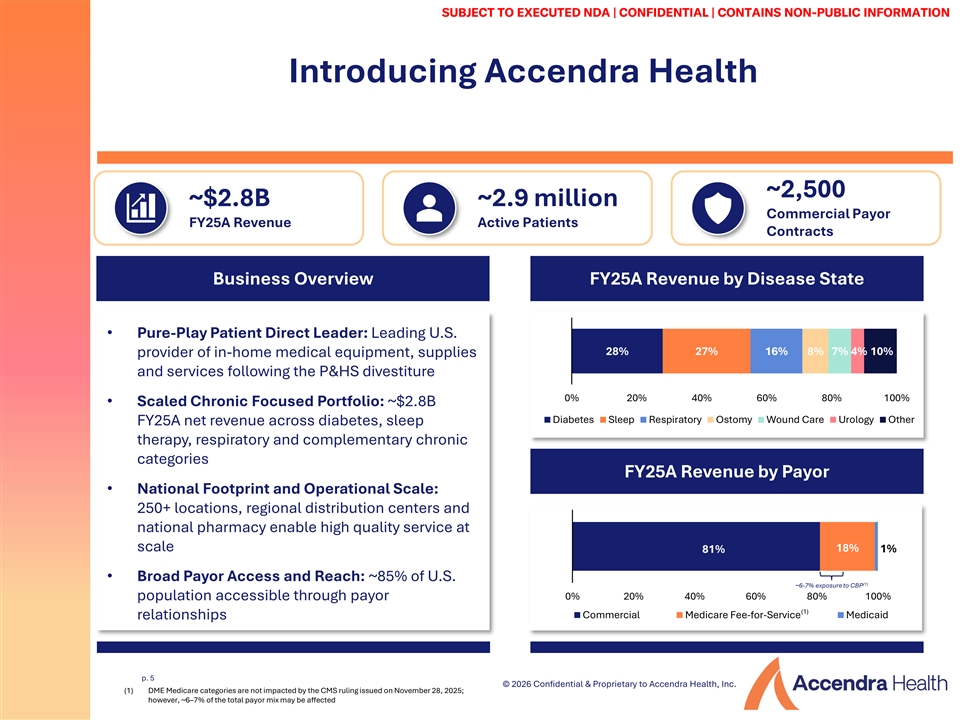

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Introducing Accendra Health ~2,500 ~$2.8B ~2.9 million Commercial Payor FY25A Revenue Active Patients Contracts Business Overview FY25A Revenue by Disease State • Pure-Play Patient Direct Leader: Leading U.S. 28% 27% 16% 8% 7% 4% 10% provider of in-home medical equipment, supplies and services following the P&HS divestiture 0% 20% 40% 60% 80% 100% • Scaled Chronic Focused Portfolio: ~$2.8B Diabetes Sleep Respiratory Ostomy Wound Care Urology Other FY25A net revenue across diabetes, sleep therapy, respiratory and complementary chronic categories FY25A Revenue by Payor • National Footprint and Operational Scale: 250+ locations, regional distribution centers and national pharmacy enable high quality service at scale 18% 1% 81% • Broad Payor Access and Reach: ~85% of U.S. (1) ~6-7% exposure to CBP population accessible through payor 0% 20% 40% 60% 80% 100% (1) Commercial Medicare Fee-for-Service Medicaid relationships p. 5 p. 5 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) DME Medicare categories are not impacted by the CMS ruling issued on November 28, 2025; Ducera however, ~6–7% of the total payor mix may be affected

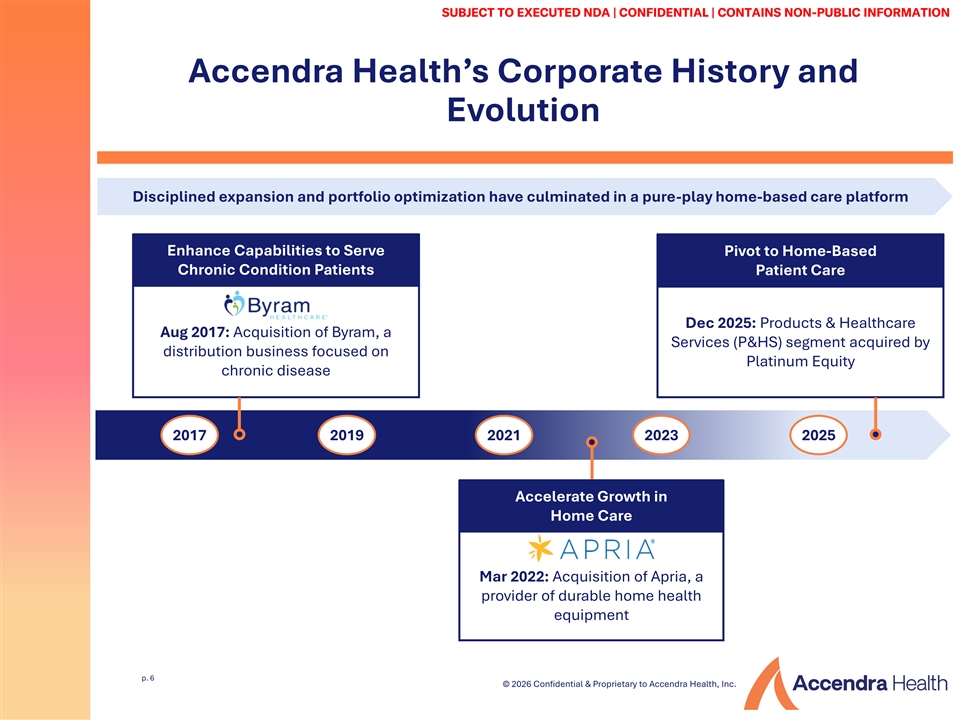

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Accendra Health’s Corporate History and Evolution Disciplined expansion and portfolio optimization have culminated in a pure-play home-based care platform Enhance Capabilities to Serve Pivot to Home-Based Chronic Condition Patients Patient Care Dec 2025: Products & Healthcare Aug 2017: Acquisition of Byram, a Services (P&HS) segment acquired by distribution business focused on Platinum Equity chronic disease 2017 2019 2021 2023 2025 Accelerate Growth in Home Care Mar 2022: Acquisition of Apria, a provider of durable home health equipment p. 6 p. 6 © 2026 Confidential & Proprietary to Accendra Health, Inc. Ducera

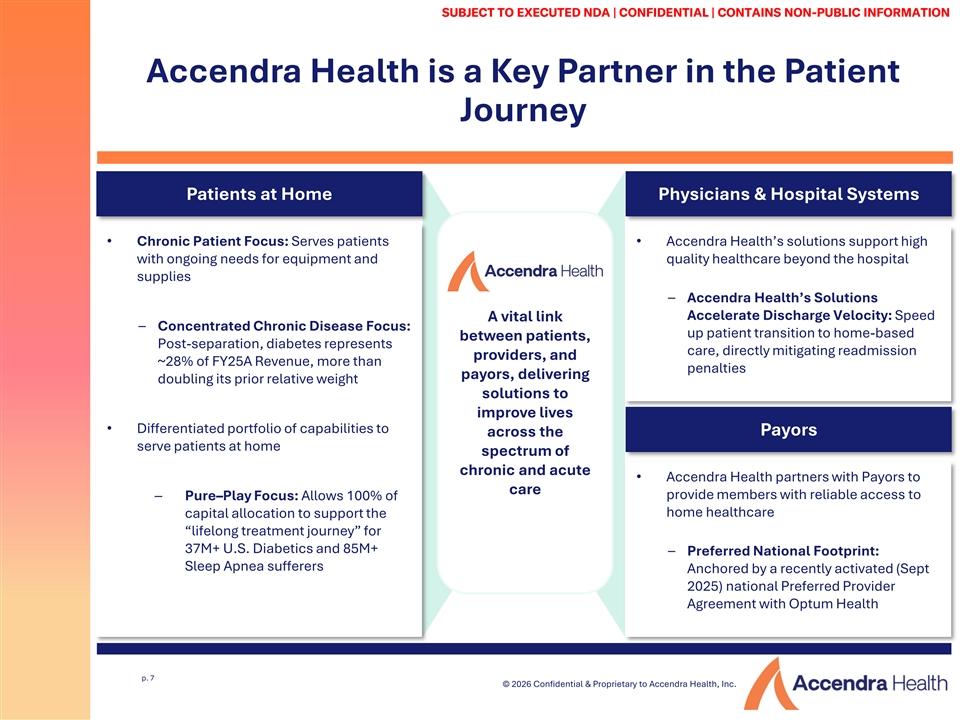

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Accendra Health is a Key Partner in the Patient Journey Patients at Home Physicians & Hospital Systems • Chronic Patient Focus: Serves patients • Accendra Health’s solutions support high with ongoing needs for equipment and quality healthcare beyond the hospital supplies – Accendra Health’s Solutions Accelerate Discharge Velocity: Speed A vital link – Concentrated Chronic Disease Focus: up patient transition to home-based between patients, Post-separation, diabetes represents care, directly mitigating readmission providers, and ~28% of FY25A Revenue, more than penalties payors, delivering doubling its prior relative weight solutions to improve lives • Differentiated portfolio of capabilities to Payors across the serve patients at home spectrum of chronic and acute • Accendra Health partners with Payors to care ─ Pure–Play Focus: Allows 100% of provide members with reliable access to home healthcare capital allocation to support the “lifelong treatment journey” for 37M+ U.S. Diabetics and 85M+ – Preferred National Footprint: Sleep Apnea sufferers Anchored by a recently activated (Sept 2025) national Preferred Provider Agreement with Optum Health p. 7 p. 7 © 2026 Confidential & Proprietary to Accendra Health, Inc. Ducera

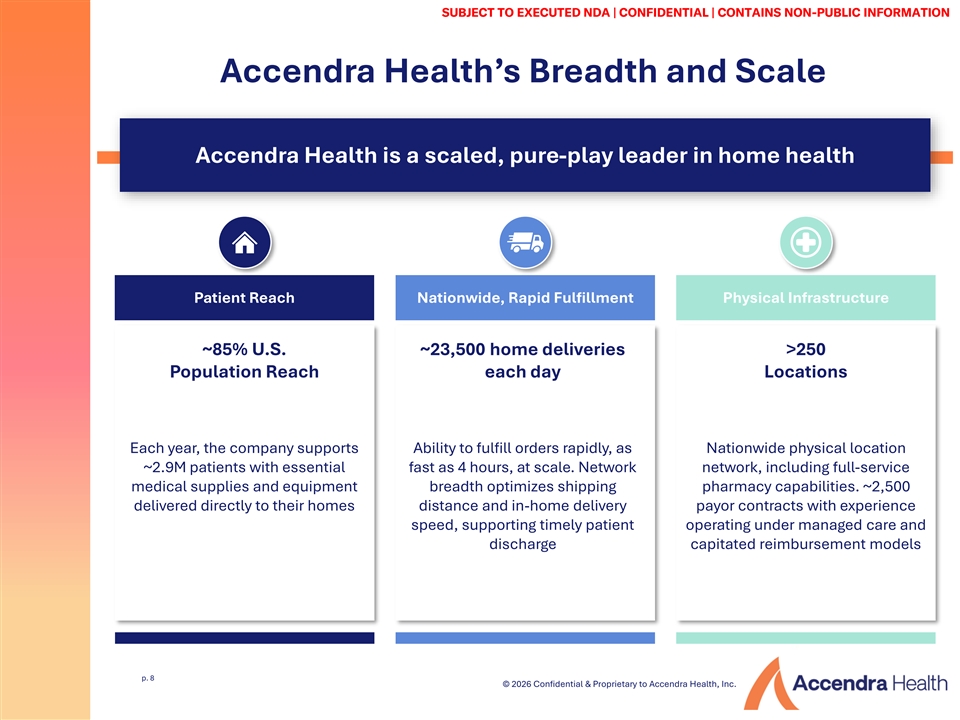

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Accendra Health’s Breadth and Scale Accendra Health is a scaled, pure-play leader in home health Patient Reach Nationwide, Rapid Fulfillment Physical Infrastructure ~85% U.S. ~23,500 home deliveries >250 Population Reach each day Locations Each year, the company supports Ability to fulfill orders rapidly, as Nationwide physical location ~2.9M patients with essential fast as 4 hours, at scale. Network network, including full-service medical supplies and equipment breadth optimizes shipping pharmacy capabilities. ~2,500 delivered directly to their homes distance and in-home delivery payor contracts with experience speed, supporting timely patient operating under managed care and discharge capitated reimbursement models p. 8 p. 8 © 2026 Confidential & Proprietary to Accendra Health, Inc. Ducera

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Accendra Health’s Vision and Strategic Mission Making healthcare more accessible and personalized, supporting patients' quality of life through nationwide clinical support Vision Mission Approach Large Physician & Clinical Network Reimagine the Future of Improve the Quality of Life Improve Quality Home-Based Care for our Patients at Home Patient Reach of Care at Home Innovative At- Home Solutions p. 9 p. 9 © 2026 Confidential & Proprietary to Accendra Health, Inc. Ducera Source: Company Materials

SU SUBJ BJECT ECT T TO O EX EXECU ECUT TED ED ND NDA A || CO CONFID NFIDEN ENT TIAL IAL || CO CONT NTAINS AINS NON NON- -P PU UBLIC BLIC INFORMAT INFORMATIO ION N II. Recent Financial Performance p. p. 10 10 Ducera

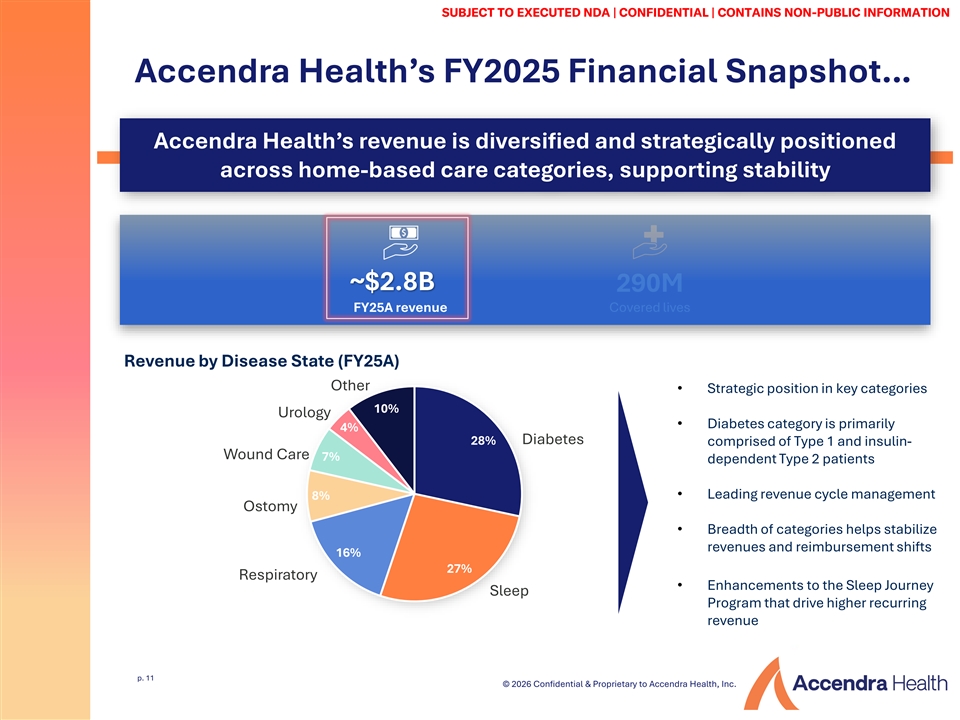

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Accendra Health’s FY2025 Financial Snapshot… Accendra Health’s revenue is diversified and strategically positioned across home-based care categories, supporting stability ~$2.8B FY25A revenue Revenue by Disease State (FY25A) Other • Strategic position in key categories 10% Urology • Diabetes category is primarily 4% Diabetes 28% comprised of Type 1 and insulin- Wound Care 7% dependent Type 2 patients • Leading revenue cycle management 8% Ostomy • Breadth of categories helps stabilize revenues and reimbursement shifts 16% 27% Respiratory • Enhancements to the Sleep Journey Sleep Program that drive higher recurring revenue p. 11 p. 11 © 2026 Confidential & Proprietary to Accendra Health, Inc. Ducera

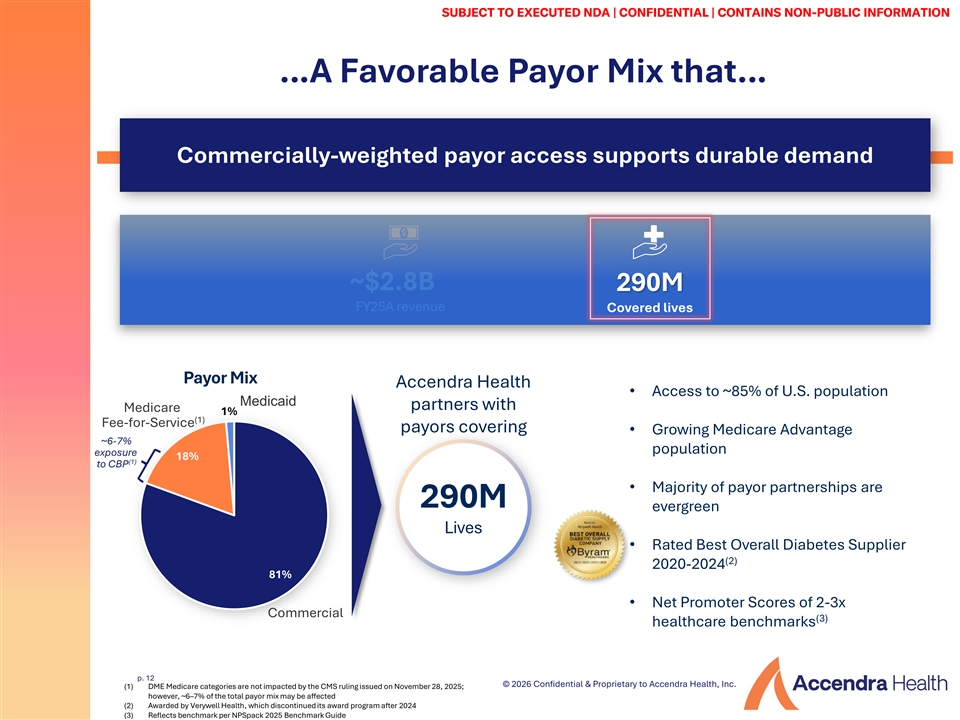

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N …A Favorable Payor Mix that… Commercially-weighted payor access supports durable demand 290M Covered lives Payor Mix Accendra Health • Access to ~85% of U.S. population Medicaid partners with Medicare 1% (1) Fee-for-Service payors covering • Growing Medicare Advantage ~6-7% population exposure 18% (1) to CBP • Majority of payor partnerships are 290M evergreen Lives • Rated Best Overall Diabetes Supplier (2) 2020-2024 81% • Net Promoter Scores of 2-3x Commercial (3) healthcare benchmarks p. 12 p. 12 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) DME Medicare categories are not impacted by the CMS ruling issued on November 28, 2025; Ducera however, ~6–7% of the total payor mix may be affected (2) Awarded by Verywell Health, which discontinued its award program after 2024 (3) Reflects benchmark per NPSpack 2025 Benchmark Guide

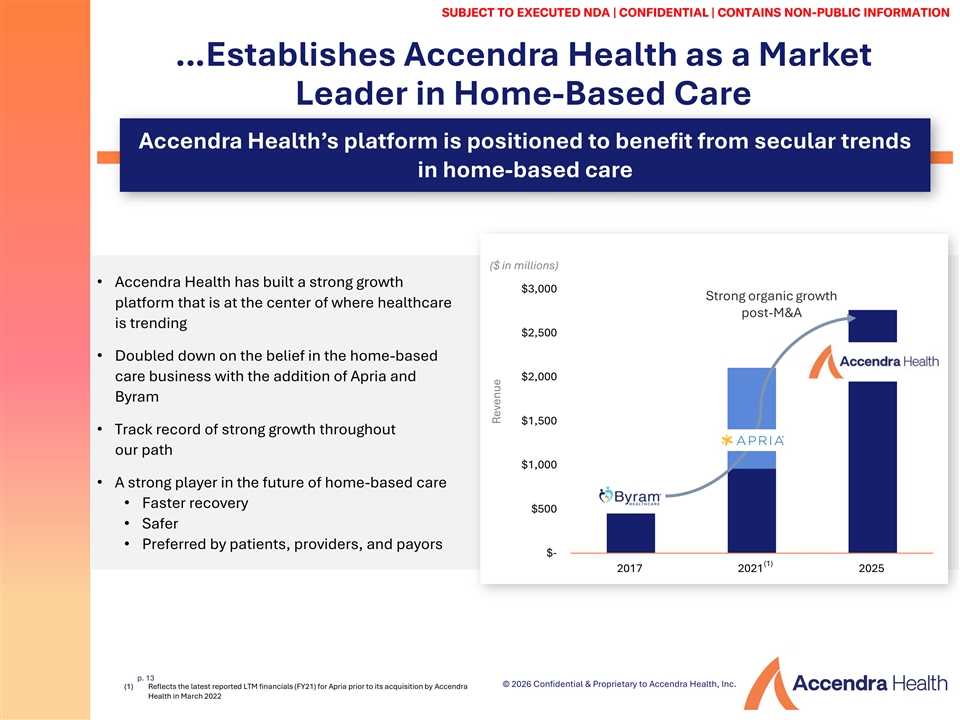

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N …Establishes Accendra Health as a Market Leader in Home-Based Care Accendra Health’s platform is positioned to benefit from secular trends in home-based care ($ in millions) • Accendra Health has built a strong growth $3,000 Strong organic growth platform that is at the center of where healthcare post-M&A is trending $2,500 • Doubled down on the belief in the home-based $2,000 care business with the addition of Apria and Byram $1,500 • Track record of strong growth throughout our path $1,000 • A strong player in the future of home-based care • Faster recovery $500 • Safer • Preferred by patients, providers, and payors $- (1) 2017 2021 2025 p. 13 p. 13 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Reflects the latest reported LTM financials (FY21) for Apria prior to its acquisition by Accendra Ducera Health in March 2022 Revenue

SU SUBJ BJECT ECT T TO O EX EXECU ECUT TED ED ND NDA A || CO CONFID NFIDEN ENT TIAL IAL || CO CONT NTAINS AINS NON NON- -P PU UBLIC BLIC INFORMAT INFORMATIO ION N III. Key Investment Highlights p. p. 14 14 Ducera

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Key Investment Highlights Accendra Health demonstrates clear credit strengths that support its position as a leading, scaled platform in the home-based care industry 1 Experienced Management with Proven Track Record 2 Favorable Industry Tailwinds 3 Accendra Health’s Capabilities Versus Industry Landscape 4 Resilient, High-Margin Home-Based Care Business Diversified Earnings Profile and Cash Flow Generation 5 p. 15 p. 15 © 2026 Confidential & Proprietary to Accendra Health, Inc. Ducera

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Highly Experienced Management Team with 1 Proven Track Record of Success Accendra Health’s management team has successfully navigated various market cycles and established an actionable go-forward strategy Years of Experience Previous Experience Accomplishments ED PESICKA ✓ Successful rebrand and launch of the Accendra President & 25+ Health name following the divestiture of the P&HS Chief Executive Officer business, accelerating the transformation to a pure-play home-based care business JON LEON EVP & 25+✓ Fully integrated Apria and Byram Health Chief Financial Officer acquisitions ✓ Improved shipping accuracy to ~99.9% PERRY BERNOCCHI EVP & 25+ ✓ Successfully navigated shifting demands of Chief Operating Officer COVID-19 pandemic ✓ Continued delivery of consistent, high-quality HEATH GALLOWAY patient services, establishing Accendra Health as EVP, General Counsel, & 20+ an industry leader Corporate Secretary WILLIAM PARRISH VP of Strategy, Corporate 15+ Development, Investor Relations p. 16 p. 16 © 2026 Confidential & Proprietary to Accendra Health, Inc. Ducera

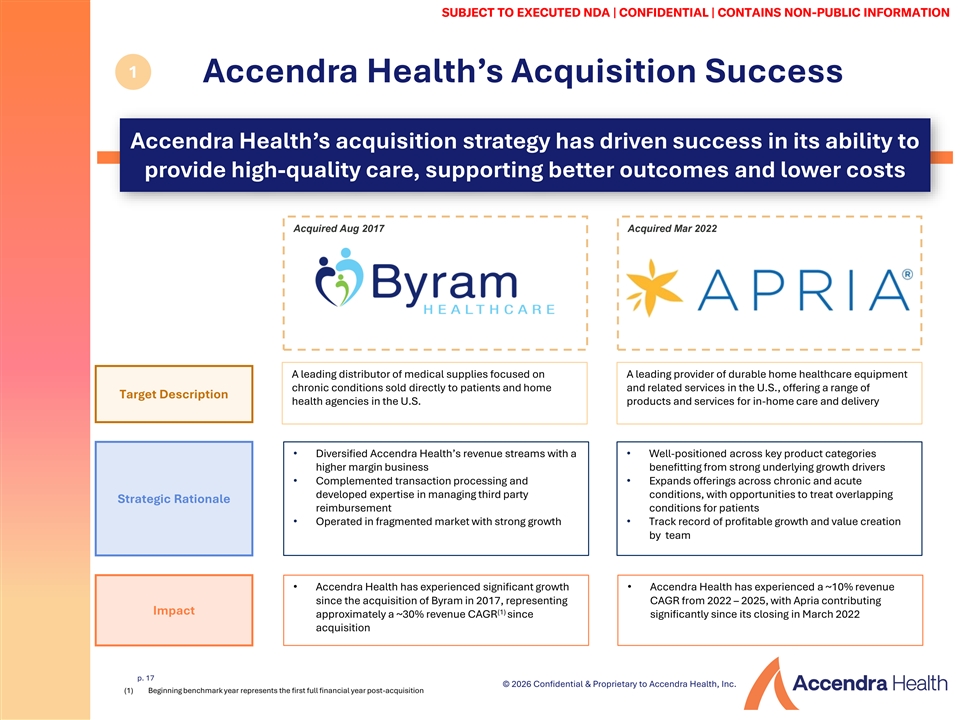

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N 1 Accendra Health’s Acquisition Success Accendra Health’s acquisition strategy has driven success in its ability to provide high-quality care, supporting better outcomes and lower costs Acquired Aug 2017 Acquired Mar 2022 A leading distributor of medical supplies focused on A leading provider of durable home healthcare equipment chronic conditions sold directly to patients and home and related services in the U.S., offering a range of Target Description health agencies in the U.S. products and services for in-home care and delivery • Diversified Accendra Health’s revenue streams with a • Well-positioned across key product categories higher margin business benefitting from strong underlying growth drivers • Complemented transaction processing and • Expands offerings across chronic and acute developed expertise in managing third party conditions, with opportunities to treat overlapping Strategic Rationale reimbursement conditions for patients • Operated in fragmented market with strong growth • Track record of profitable growth and value creation by team • Accendra Health has experienced significant growth • Accendra Health has experienced a ~10% revenue since the acquisition of Byram in 2017, representing CAGR from 2022 – 2025, with Apria contributing Impact (1) approximately a ~30% revenue CAGR since significantly since its closing in March 2022 acquisition p. 17 p. 17 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Beginning benchmark year represents the first full financial year post-acquisition Ducera

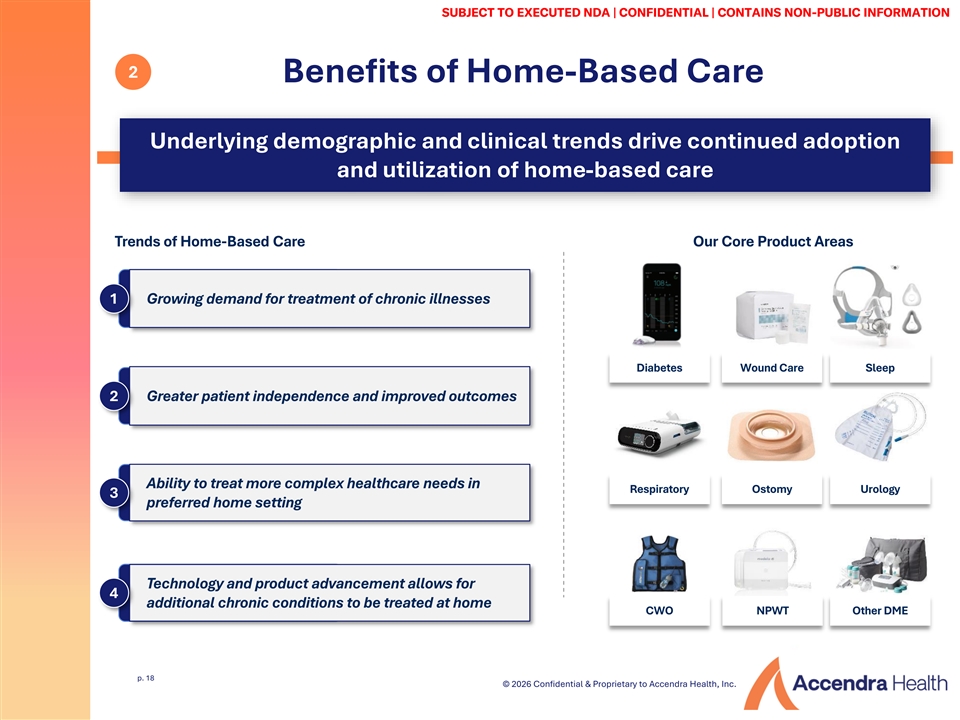

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N 2 Benefits of Home-Based Care Underlying demographic and clinical trends drive continued adoption and utilization of home-based care Trends of Home-Based Care Our Core Product Areas 1 Growing demand for treatment of chronic illnesses Diabetes Wound Care Sleep 2 Greater patient independence and improved outcomes Ability to treat more complex healthcare needs in Respiratory Ostomy Urology 3 preferred home setting Technology and product advancement allows for 4 additional chronic conditions to be treated at home CWO NPWT Other DME p. 18 p. 18 © 2026 Confidential & Proprietary to Accendra Health, Inc. Ducera

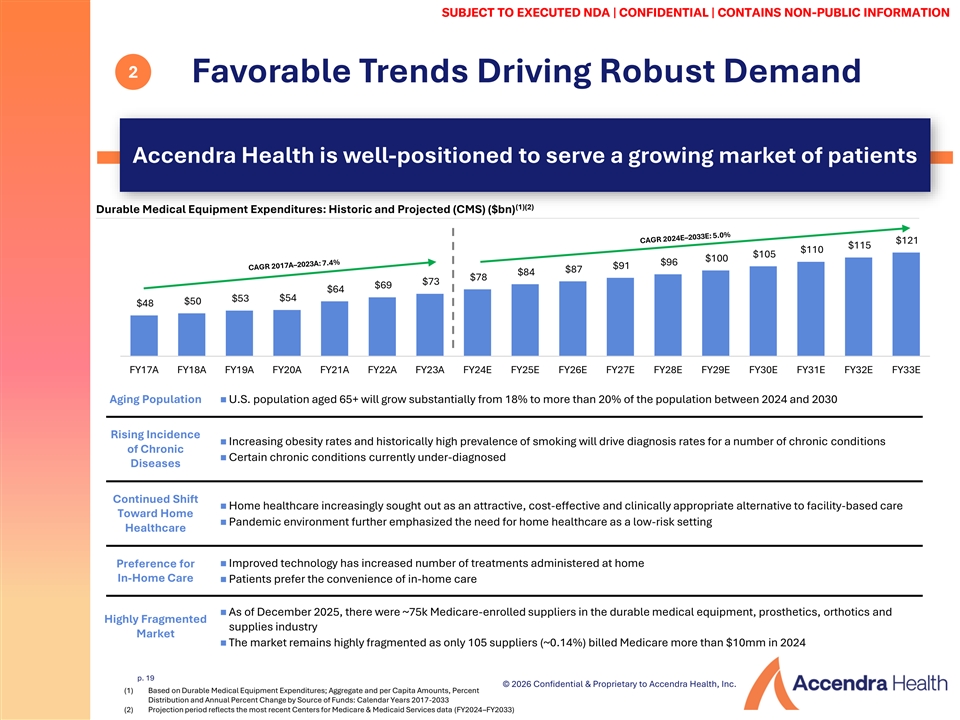

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N 2 Favorable Trends Driving Robust Demand Accendra Health is well-positioned to serve a growing market of patients (1)(2) Durable Medical Equipment Expenditures: Historic and Projected (CMS) ($bn) $121 $115 $110 $105 $100 $96 $91 $87 $84 $78 $73 $69 $64 $53 $54 $50 $48 FY17A FY18A FY19A FY20A FY21A FY22A FY23A FY24E FY25E FY26E FY27E FY28E FY29E FY30E FY31E FY32E FY33E Aging Population ◼ U.S. population aged 65+ will grow substantially from 18% to more than 20% of the population between 2024 and 2030 Rising Incidence ◼ Increasing obesity rates and historically high prevalence of smoking will drive diagnosis rates for a number of chronic conditions of Chronic ◼ Certain chronic conditions currently under-diagnosed Diseases Continued Shift ◼ Home healthcare increasingly sought out as an attractive, cost-effective and clinically appropriate alternative to facility-based care Toward Home ◼ Pandemic environment further emphasized the need for home healthcare as a low-risk setting Healthcare ◼ Improved technology has increased number of treatments administered at home Preference for In-Home Care◼ Patients prefer the convenience of in-home care ◼ As of December 2025, there were ~75k Medicare-enrolled suppliers in the durable medical equipment, prosthetics, orthotics and Highly Fragmented supplies industry Market ◼ The market remains highly fragmented as only 105 suppliers (~0.14%) billed Medicare more than $10mm in 2024 p. 19 p. 19 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Based on Durable Medical Equipment Expenditures; Aggregate and per Capita Amounts, Percent Ducera Distribution and Annual Percent Change by Source of Funds: Calendar Years 2017-2033 (2) Projection period reflects the most recent Centers for Medicare & Medicaid Services data (FY2024–FY2033)

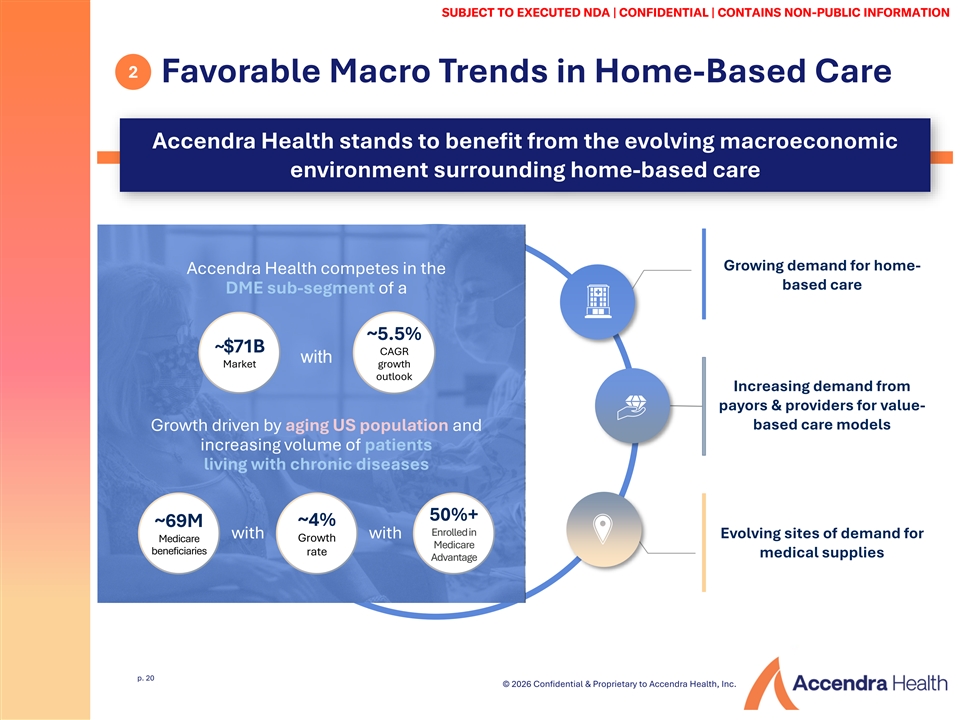

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N 2 Favorable Macro Trends in Home-Based Care Accendra Health stands to benefit from the evolving macroeconomic environment surrounding home-based care Growing demand for home- Accendra Health competes in the based care DME sub-segment of a ~5.5% ~$71B CAGR with Market growth outlook Increasing demand from payors & providers for value- based care models Growth driven by aging US population and increasing volume of patients living with chronic diseases 50%+ ~69M ~4% Enrolled in with with Evolving sites of demand for Medicare Growth Medicare beneficiaries rate medical supplies Advantage p. 20 p. 20 © 2026 Confidential & Proprietary to Accendra Health, Inc. Ducera

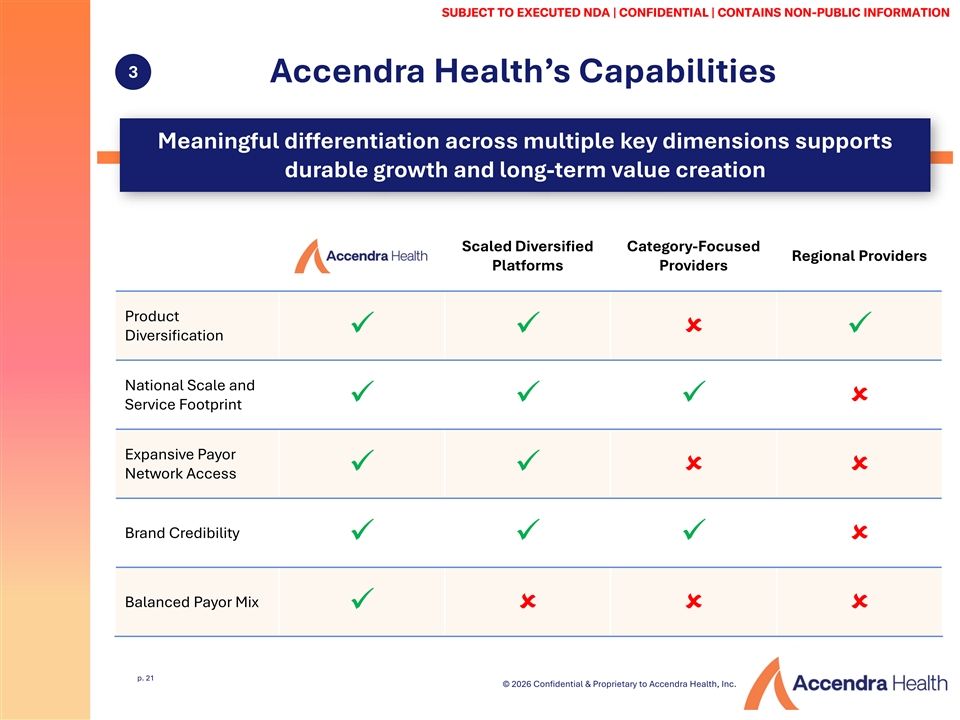

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N 3 Accendra Health’s Capabilities Meaningful differentiation across multiple key dimensions supports durable growth and long-term value creation Scaled Diversified Category-Focused Regional Providers Platforms Providers Product ✓✓û✓ Diversification National Scale and ✓✓✓û Service Footprint Expansive Payor ✓✓ûû Network Access Brand Credibility ✓✓✓û Balanced Payor Mix ✓ûûû p. 21 p. 21 © 2026 Confidential & Proprietary to Accendra Health, Inc. Ducera

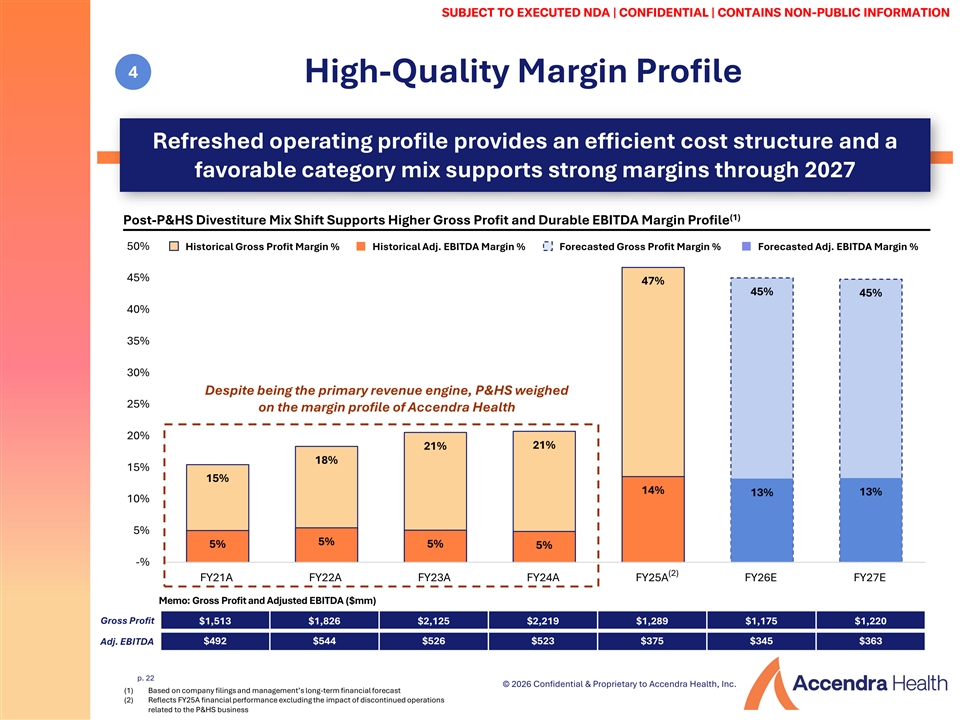

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N 4 High-Quality Margin Profile Refreshed operating profile provides an efficient cost structure and a favorable category mix supports strong margins through 2027 (1) Post-P&HS Divestiture Mix Shift Supports Higher Gross Profit and Durable EBITDA Margin Profile 50% Historical Gross Profit Margin % Historical Adj. EBITDA Margin % Forecasted Gross Profit Margin % Forecasted Adj. EBITDA Margin % 45% 47% 45% 45% 40% 35% 30% Despite being the primary revenue engine, P&HS weighed 25% on the margin profile of Accendra Health 20% 21% 21% 18% 15% 15% 14% 13% 13% 10% 5% 5% 5% 5% 5% -% (2) FY21A FY22A FY23A FY24A FY25A FY26E FY27E Memo: Gross Profit and Adjusted EBITDA ($mm) Gross Profit $1,513 $1,826 $2,125 $2,219 $1,289 $1,175 $1,220 $492 $544 $526 $523 $375 $345 $363 Adj. EBITDA p. 22 p. 22 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Based on company filings and management’s long-term financial forecast Ducera (2) Reflects FY25A financial performance excluding the impact of discontinued operations related to the P&HS business

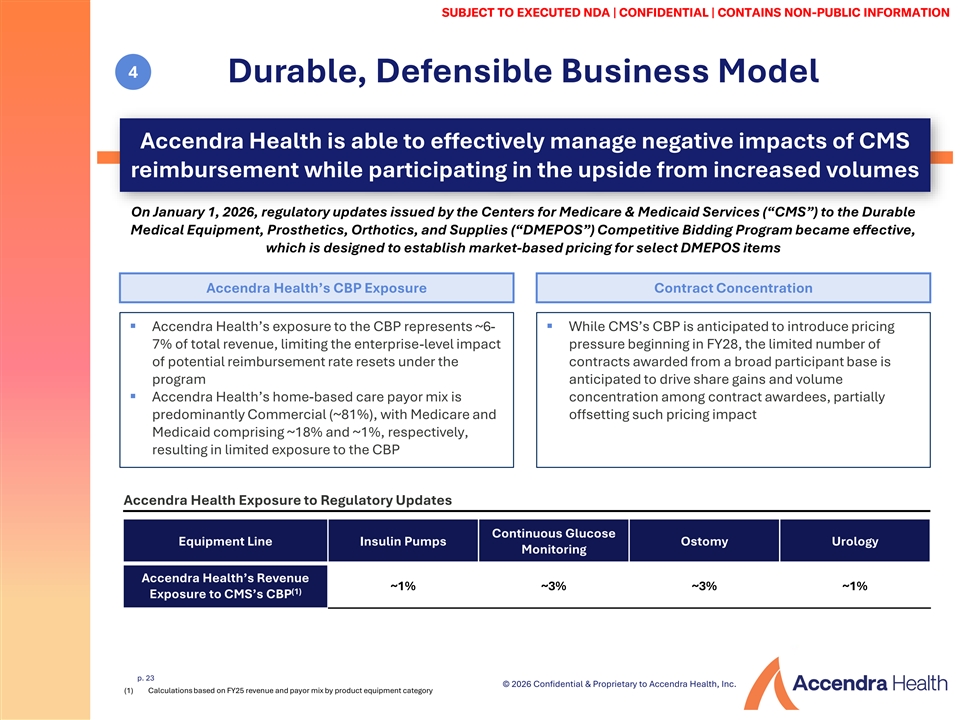

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N 4 Durable, Defensible Business Model Accendra Health is able to effectively manage negative impacts of CMS reimbursement while participating in the upside from increased volumes On January 1, 2026, regulatory updates issued by the Centers for Medicare & Medicaid Services (“CMS”) to the Durable Medical Equipment, Prosthetics, Orthotics, and Supplies (“DMEPOS”) Competitive Bidding Program became effective, which is designed to establish market-based pricing for select DMEPOS items Accendra Health’s CBP Exposure Contract Concentration ▪ Accendra Health’s exposure to the CBP represents ~6-▪ While CMS’s CBP is anticipated to introduce pricing 7% of total revenue, limiting the enterprise-level impact pressure beginning in FY28, the limited number of of potential reimbursement rate resets under the contracts awarded from a broad participant base is program anticipated to drive share gains and volume ▪ Accendra Health’s home-based care payor mix is concentration among contract awardees, partially predominantly Commercial (~81%), with Medicare and offsetting such pricing impact Medicaid comprising ~18% and ~1%, respectively, resulting in limited exposure to the CBP Accendra Health Exposure to Regulatory Updates Continuous Glucose Equipment Line Insulin Pumps Ostomy Urology Monitoring Accendra Health’s Revenue ~1% ~3% ~3% ~1% (1) Exposure to CMS’s CBP p. 23 p. 23 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Calculations based on FY25 revenue and payor mix by product equipment category Ducera

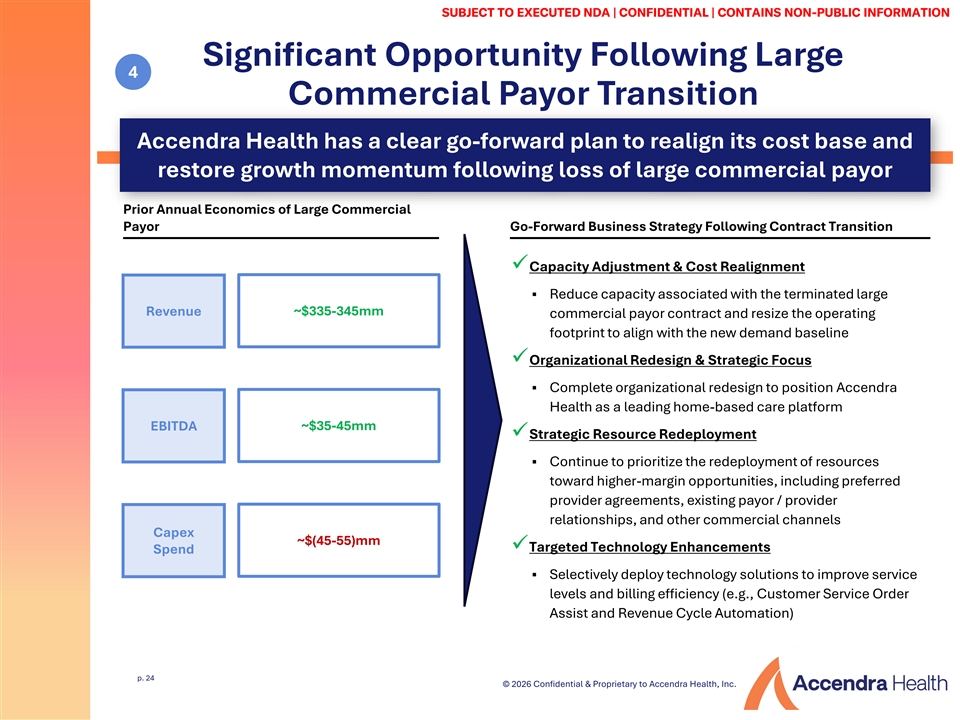

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Significant Opportunity Following Large 4 Commercial Payor Transition Accendra Health has a clear go-forward plan to realign its cost base and restore growth momentum following loss of large commercial payor Prior Annual Economics of Large Commercial Payor Go-Forward Business Strategy Following Contract Transition ✓Capacity Adjustment & Cost Realignment ▪ Reduce capacity associated with the terminated large Revenue ~$335-345mm commercial payor contract and resize the operating footprint to align with the new demand baseline ✓Organizational Redesign & Strategic Focus ▪ Complete organizational redesign to position Accendra Health as a leading home-based care platform EBITDA ~$35-45mm ✓Strategic Resource Redeployment ▪ Continue to prioritize the redeployment of resources toward higher-margin opportunities, including preferred provider agreements, existing payor / provider relationships, and other commercial channels Capex ~$(45-55)mm ✓Targeted Technology Enhancements Spend ▪ Selectively deploy technology solutions to improve service levels and billing efficiency (e.g., Customer Service Order Assist and Revenue Cycle Automation) p. 24 p. 24 © 2026 Confidential & Proprietary to Accendra Health, Inc. Ducera

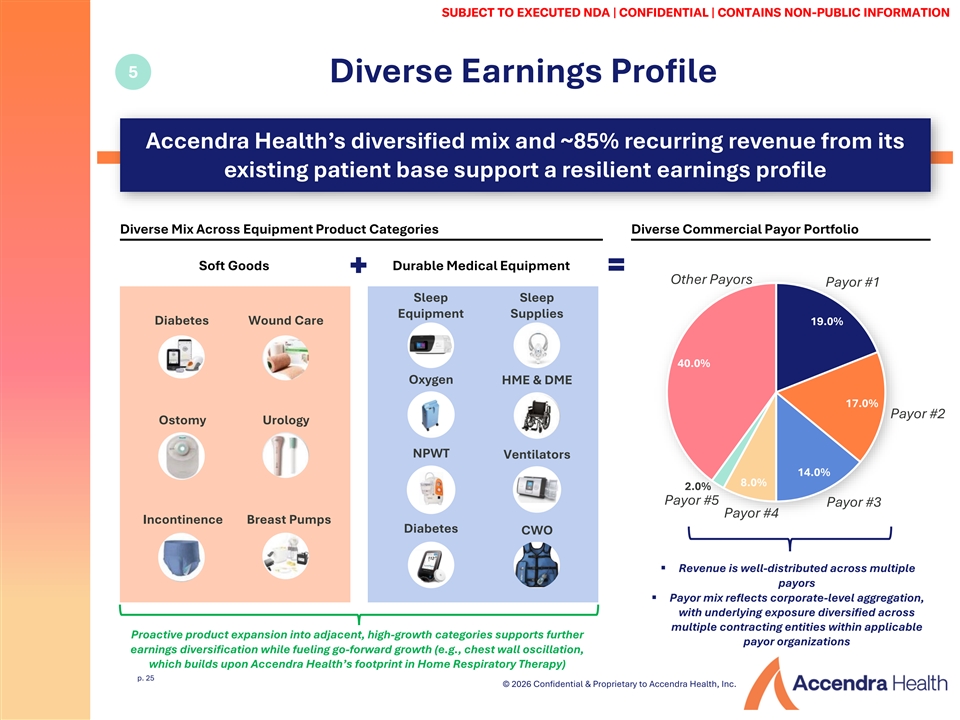

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N 5 Diverse Earnings Profile Accendra Health’s diversified mix and ~85% recurring revenue from its existing patient base support a resilient earnings profile Diverse Mix Across Equipment Product Categories Diverse Commercial Payor Portfolio Soft Goods Durable Medical Equipment Other Payors Payor #1 Sleep Sleep Equipment Supplies Diabetes Wound Care 19.0% 40.0% Oxygen HME & DME 17.0% Payor #2 Ostomy Urology NPWT Ventilators 14.0% 8.0% 2.0% Payor #5 Payor #3 Payor #4 Incontinence Breast Pumps Diabetes CWO ▪ Revenue is well-distributed across multiple payors ▪ Payor mix reflects corporate-level aggregation, with underlying exposure diversified across multiple contracting entities within applicable Proactive product expansion into adjacent, high-growth categories supports further payor organizations earnings diversification while fueling go-forward growth (e.g., chest wall oscillation, which builds upon Accendra Health’s footprint in Home Respiratory Therapy) p. 25 p. 25 © 2026 Confidential & Proprietary to Accendra Health, Inc. Ducera

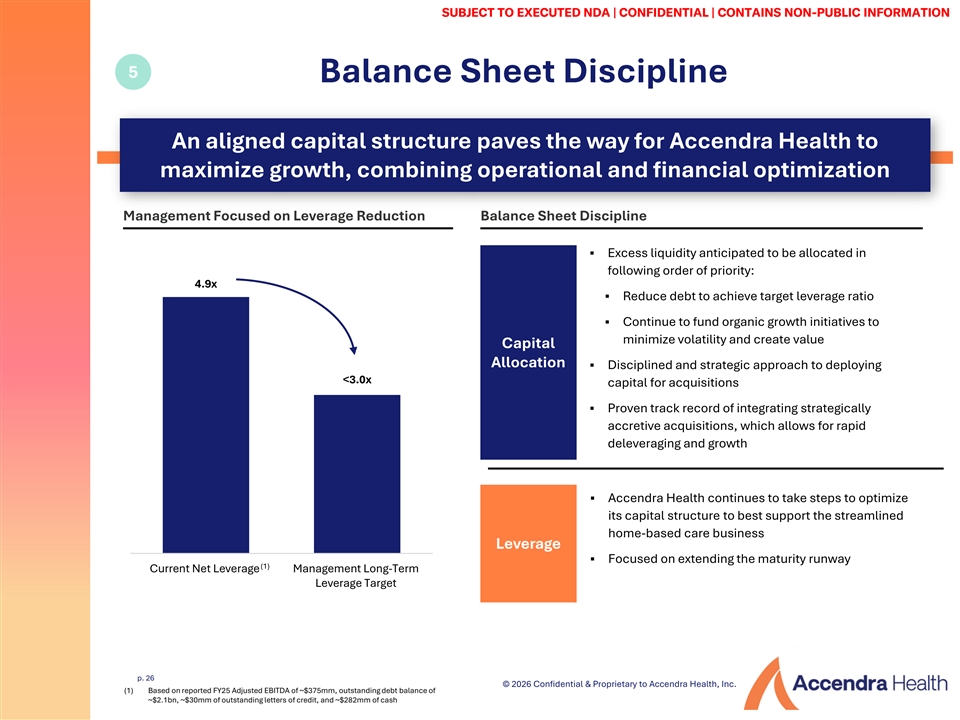

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N 5 Balance Sheet Discipline An aligned capital structure paves the way for Accendra Health to maximize growth, combining operational and financial optimization Management Focused on Leverage Reduction Balance Sheet Discipline ▪ Excess liquidity anticipated to be allocated in following order of priority: 4.9x ▪ Reduce debt to achieve target leverage ratio ▪ Continue to fund organic growth initiatives to minimize volatility and create value Capital Allocation ▪ Disciplined and strategic approach to deploying <3.0x capital for acquisitions ▪ Proven track record of integrating strategically accretive acquisitions, which allows for rapid deleveraging and growth ▪ Accendra Health continues to take steps to optimize its capital structure to best support the streamlined home-based care business Leverage ▪ Focused on extending the maturity runway (1) Current Net Leverage Management Long-Term Leverage Target p. 26 p. 26 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Based on reported FY25 Adjusted EBITDA of ~$375mm, outstanding debt balance of Ducera ~$2.1bn, ~$30mm of outstanding letters of credit, and ~$282mm of cash

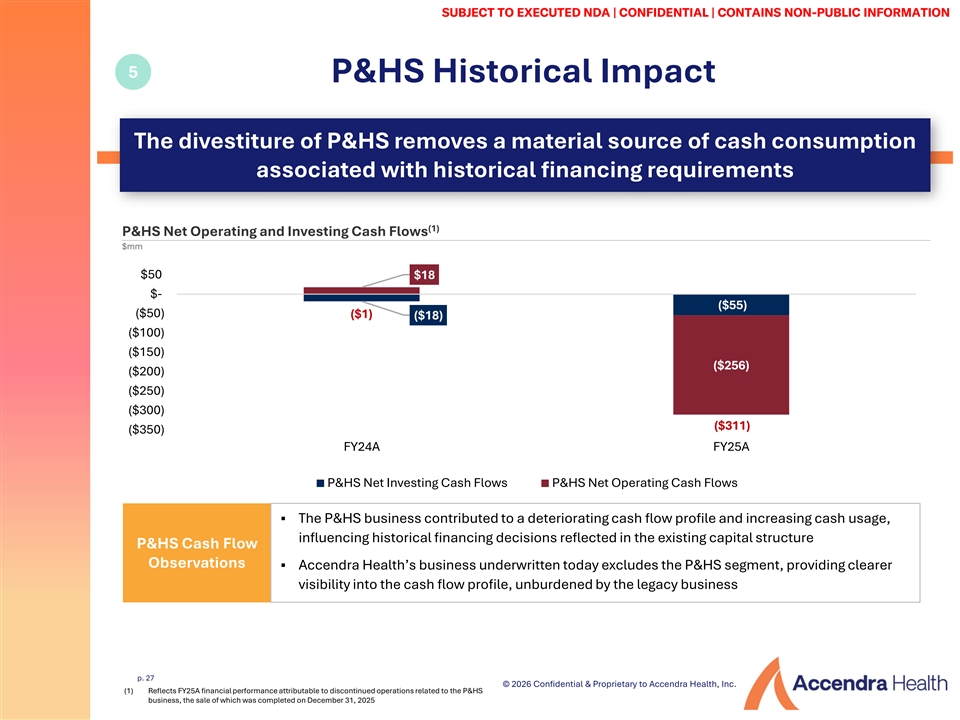

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N 5 P&HS Historical Impact The divestiture of P&HS removes a material source of cash consumption associated with historical financing requirements (1) P&HS Net Operating and Investing Cash Flows $mm $50 $18 $- ($55) ($50) ($1) ($18) ($100) ($150) ($256) ($200) ($250) ($300) ($311) ($350) FY24A FY25A P&HS Net Investing Cash Flows P&HS Net Operating Cash Flows ▪ The P&HS business contributed to a deteriorating cash flow profile and increasing cash usage, influencing historical financing decisions reflected in the existing capital structure P&HS Cash Flow Observations ▪ Accendra Health’s business underwritten today excludes the P&HS segment, providing clearer visibility into the cash flow profile, unburdened by the legacy business p. 27 p. 27 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Reflects FY25A financial performance attributable to discontinued operations related to the P&HS Ducera business, the sale of which was completed on December 31, 2025

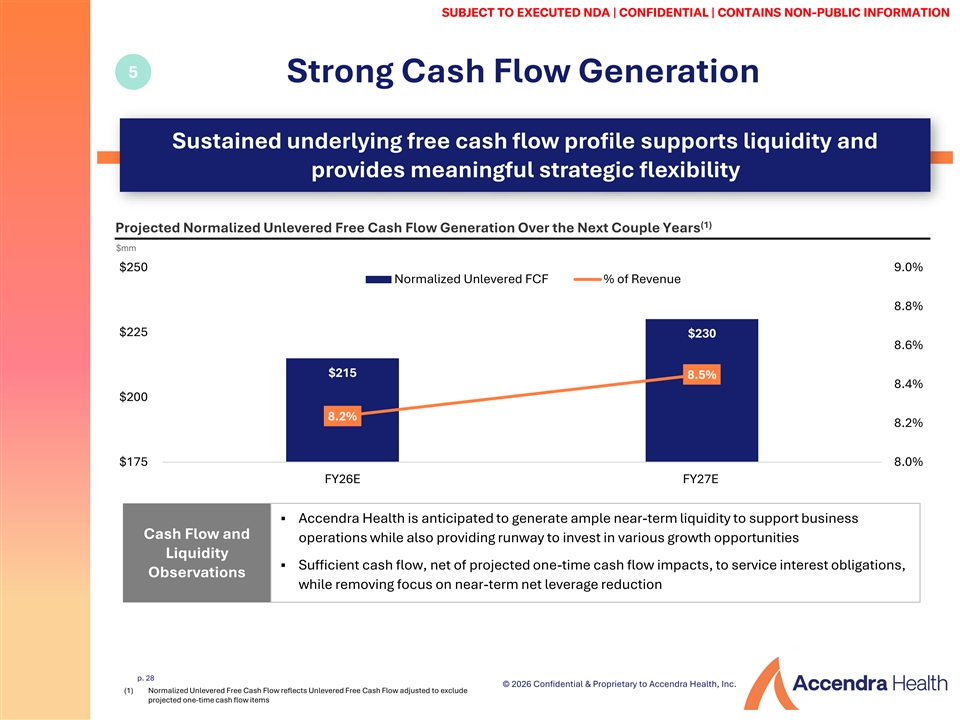

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N 5 Strong Cash Flow Generation Sustained underlying free cash flow profile supports liquidity and provides meaningful strategic flexibility (1) Projected Normalized Unlevered Free Cash Flow Generation Over the Next Couple Years $mm $250 9 9. .0 0% % $245 N Nor ormal malized ized U Un nl le ev ve er re ed d F FC CF F % % o of Rev f Reve en nu ue e $235 8 8. .8 8% % $ $2 22 25 5 $230 $230 8 8. .6 6% % $215 $215 $215 8 8.5% .5% $205 8 8. .4 4% % $200 $195 8 8.2% .2% 8 8. .2 2% % $185 $ $1 17 75 5 8 8. .0 0% % F FY26 Y26E E F FY27 Y27E E ▪ Accendra Health is anticipated to generate ample near-term liquidity to support business Cash Flow and operations while also providing runway to invest in various growth opportunities Liquidity ▪ Sufficient cash flow, net of projected one-time cash flow impacts, to service interest obligations, Observations while removing focus on near-term net leverage reduction p. 28 p. 28 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Normalized Unlevered Free Cash Flow reflects Unlevered Free Cash Flow adjusted to exclude Ducera projected one-time cash flow items

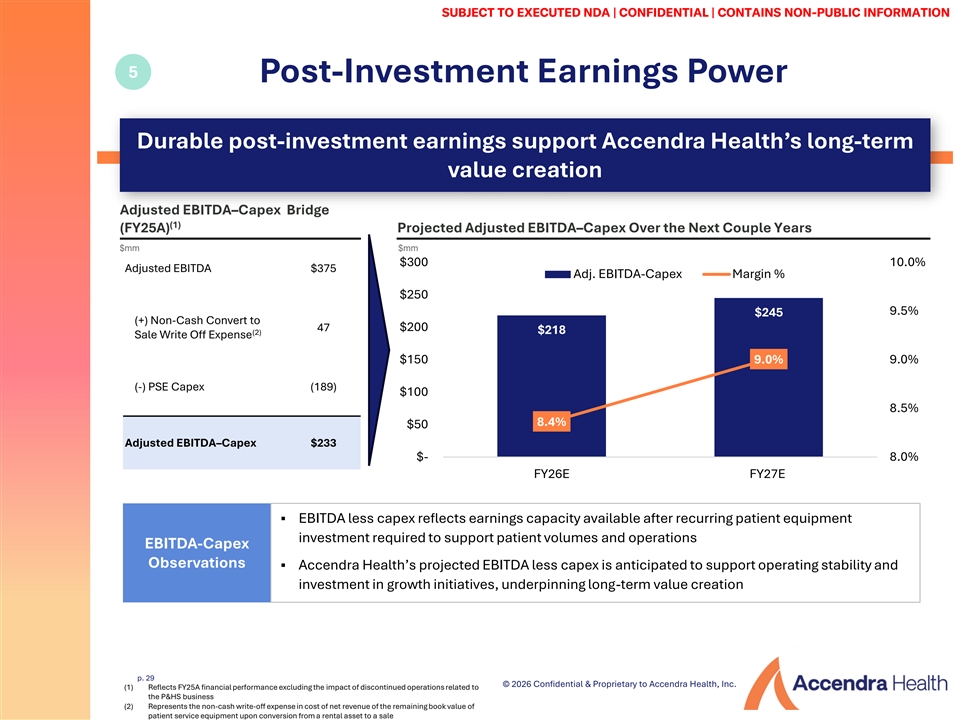

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N 5 Post-Investment Earnings Power Durable post-investment earnings support Accendra Health’s long-term value creation Adjusted EBITDA–Capex Bridge (1) (FY25A) Projected Adjusted EBITDA–Capex Over the Next Couple Years $mm $mm $300 10.0% Adjusted EBITDA $375 Adj. EBITDA-Capex Margin % $250 9.5% $245 (+) Non-Cash Convert to $200 47 (2) $218 Sale Write Off Expense $150 9.0% 9.0% (-) PSE Capex (189) $100 8.5% 8.4% $50 Adjusted EBITDA–Capex $233 $- 8.0% FY26E FY27E ▪ EBITDA less capex reflects earnings capacity available after recurring patient equipment investment required to support patient volumes and operations EBITDA-Capex Observations ▪ Accendra Health’s projected EBITDA less capex is anticipated to support operating stability and investment in growth initiatives, underpinning long-term value creation p. 29 p. 29 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Reflects FY25A financial performance excluding the impact of discontinued operations related to Ducera the P&HS business (2) Represents the non-cash write-off expense in cost of net revenue of the remaining book value of patient service equipment upon conversion from a rental asset to a sale

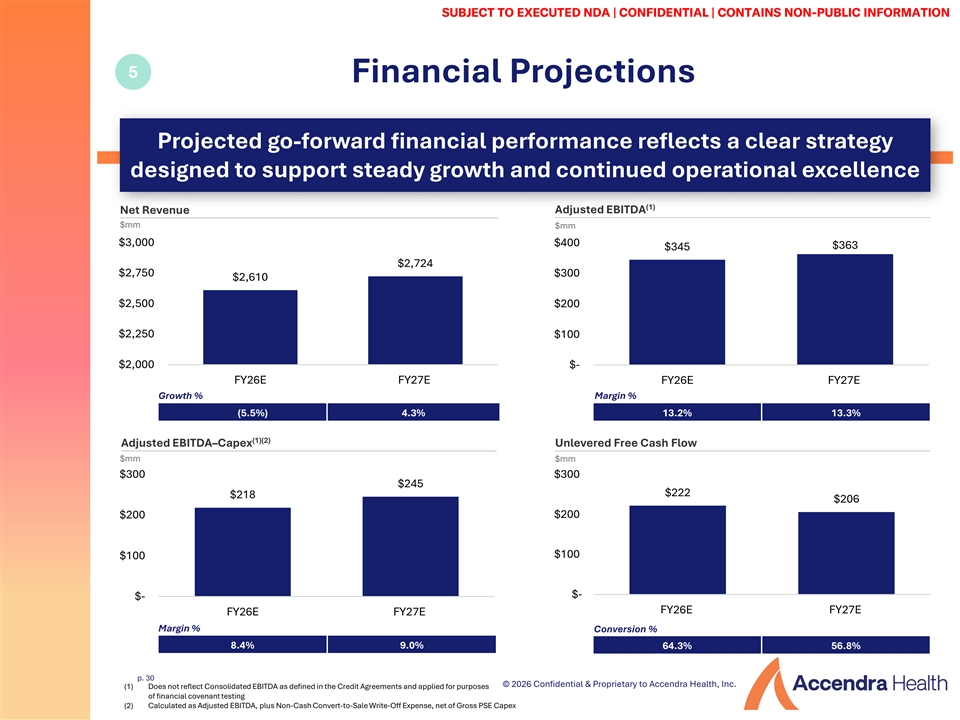

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N 5 Financial Projections Projected go-forward financial performance reflects a clear strategy designed to support steady growth and continued operational excellence (1) Adjusted EBITDA Net Revenue $mm $mm $3,000 $400 $363 $345 $2,724 $2,750 $300 $2,610 $2,500 $200 $2,250 $100 $2,000 $- FY26E FY27E FY26E FY27E Growth % Margin % (5.5%) 4.3% 13.2% 13.3% (1)(2) Adjusted EBITDA–Capex Unlevered Free Cash Flow $mm $mm $300 $300 $245 $222 $218 $206 $200 $200 $100 $100 $- $- FY26E FY27E FY26E FY27E Margin % Conversion % 8.4% 9.0% 64.3% 56.8% p. 30 p. 30 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Does not reflect Consolidated EBITDA as defined in the Credit Agreements and applied for purposes Ducera of financial covenant testing (2) Calculated as Adjusted EBITDA, plus Non-Cash Convert-to-Sale Write-Off Expense, net of Gross PSE Capex

SU SUBJ BJECT ECT T TO O EX EXECU ECUT TED ED ND NDA A || CO CONFID NFIDEN ENT TIAL IAL || CO CONT NTAINS AINS NON NON- -P PU UBLIC BLIC INFORMAT INFORMATIO ION N IV. Capital Structure Optimization p. p. 31 31 Ducera

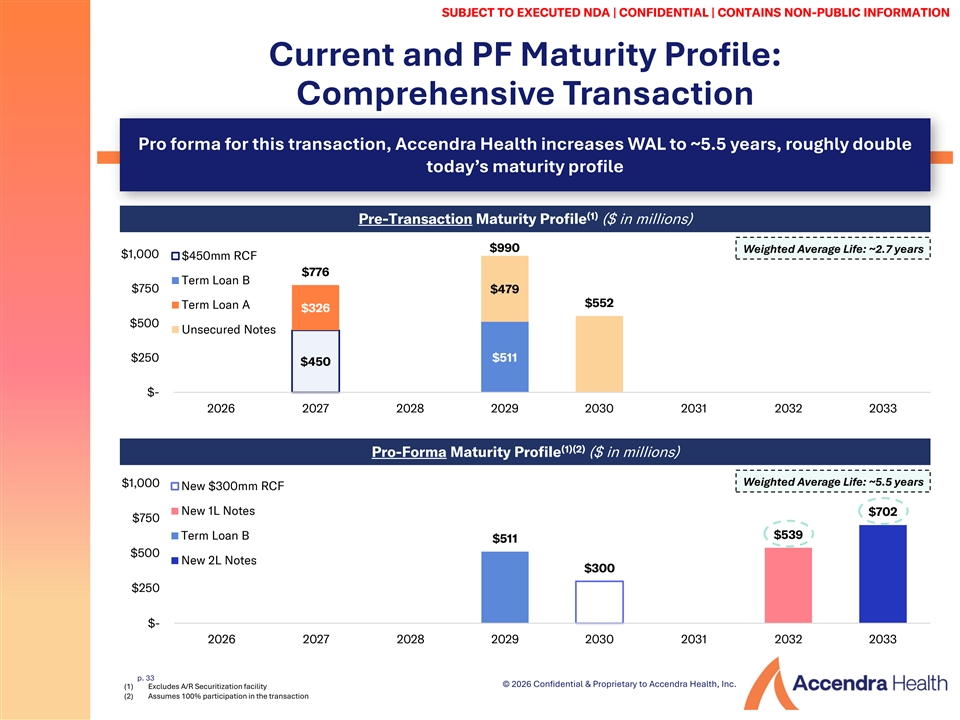

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Key Benefits of Proposed Transaction Accendra Health is proposing a Comprehensive Transaction designed to support its go-forward business alongside critical capital structure partners Transaction Summary ▪ The Comprehensive Transaction contemplates (i) replacing the existing RCF with a new longer-dated RCF of up to $300mm, (ii) refinancing the TLA through a long-dated new money 1L issuance, and (iii) exchanging the Unsecured Notes into new long-dated secured bonds ▪ Accendra Health is seeking participation from Unsecured Noteholders in the proposed transaction to build on the support of the ad hoc group of noteholders committed to the transaction (the “AHG”), which represents 90%+ of the (1) Unsecured Notes , ahead of a broader public launch. While the Unsecured Noteholders are allowed to provide a portion of the New Money 1L Notes, they are not required to do so in order to participate in the transaction Key Transaction Benefits for Company The Comprehensive Transaction enables management to shift focus from balance sheet stabilization to operational execution, business growth, and value creation, with key benefits including: (2) ✓ Near-term maturities addressed, with weighted average life roughly doubled to ~5.5 years ✓ Reduction in funded debt from the Unsecured Notes exchange ✓ More durable liquidity runway through a right-sized RCF supporting the go-forward Accendra Health business ✓ Free cash flow supported through maturity extension p. 32 p. 32 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Holdings reflected as of May 8, 2026 Ducera (2) Assumes 100% participation in the transaction

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Current and PF Maturity Profile: Comprehensive Transaction Pro forma for this transaction, Accendra Health increases WAL to ~5.5 years, roughly double today’s maturity profile (1) Pre-Transaction Maturity Profile ($ in millions) $990 Weighted Average Life: ~2.7 years $1,000 $450mm RCF $776 Term Loan B $750 $479 $552 Term Loan A $326 $500 Unsecured Notes $250 $511 $450 $- 2026 2027 2028 2029 2030 2031 2032 2033 (1)(2) Pro-Forma Maturity Profile ($ in millions) Weighted Average Life: ~5.5 years $1,000 New $300mm RCF New 1L Notes $702 $750 $539 Term Loan B $511 $500 New 2L Notes $300 $250 $- 2026 2027 2028 2029 2030 2031 2032 2033 p. 33 p. 33 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Excludes A/R Securitization facility Ducera (2) Assumes 100% participation in the transaction

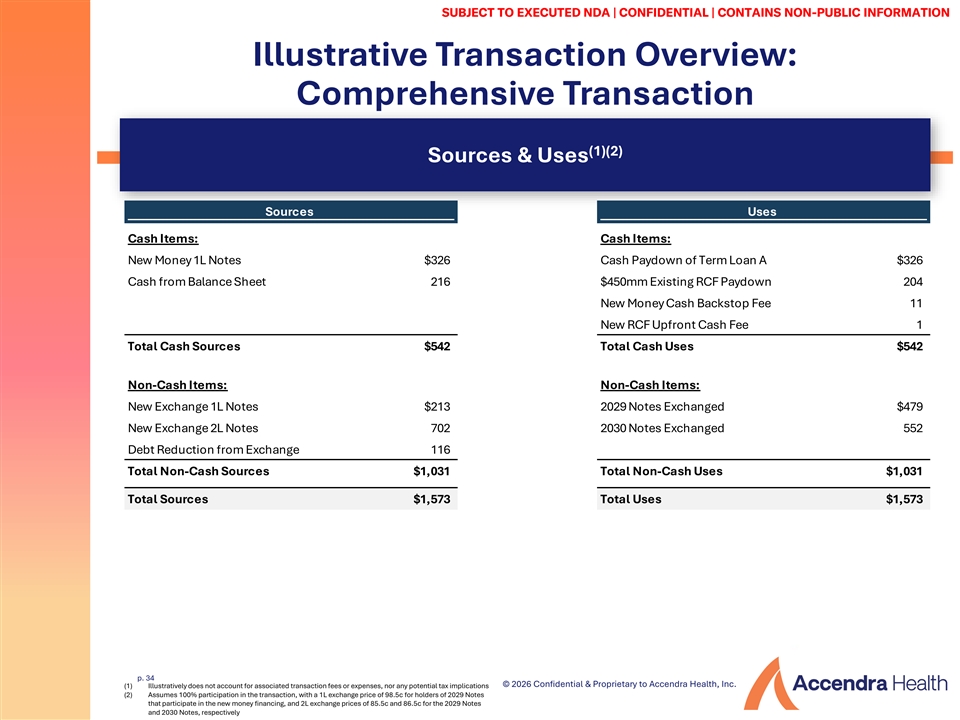

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Illustrative Transaction Overview: Comprehensive Transaction (1)(2) Sources & Uses Sources Uses Cash Items: Cash Items: New Money 1L Notes $326 Cash Paydown of Term Loan A $326 Cash from Balance Sheet 216 $450mm Existing RCF Paydown 204 New Money Cash Backstop Fee 11 New RCF Upfront Cash Fee 1 Total Cash Sources $542 Total Cash Uses $542 Non-Cash Items: Non-Cash Items: New Exchange 1L Notes $213 2029 Notes Exchanged $479 New Exchange 2L Notes 702 2030 Notes Exchanged 552 Debt Reduction from Exchange 116 Total Non-Cash Sources $1,031 Total Non-Cash Uses $1,031 Total Sources $1,573 Total Uses $1,573 p. 34 p. 34 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Illustratively does not account for associated transaction fees or expenses, nor any potential tax implications Ducera (2) Assumes 100% participation in the transaction, with a 1L exchange price of 98.5c for holders of 2029 Notes that participate in the new money financing, and 2L exchange prices of 85.5c and 86.5c for the 2029 Notes and 2030 Notes, respectively

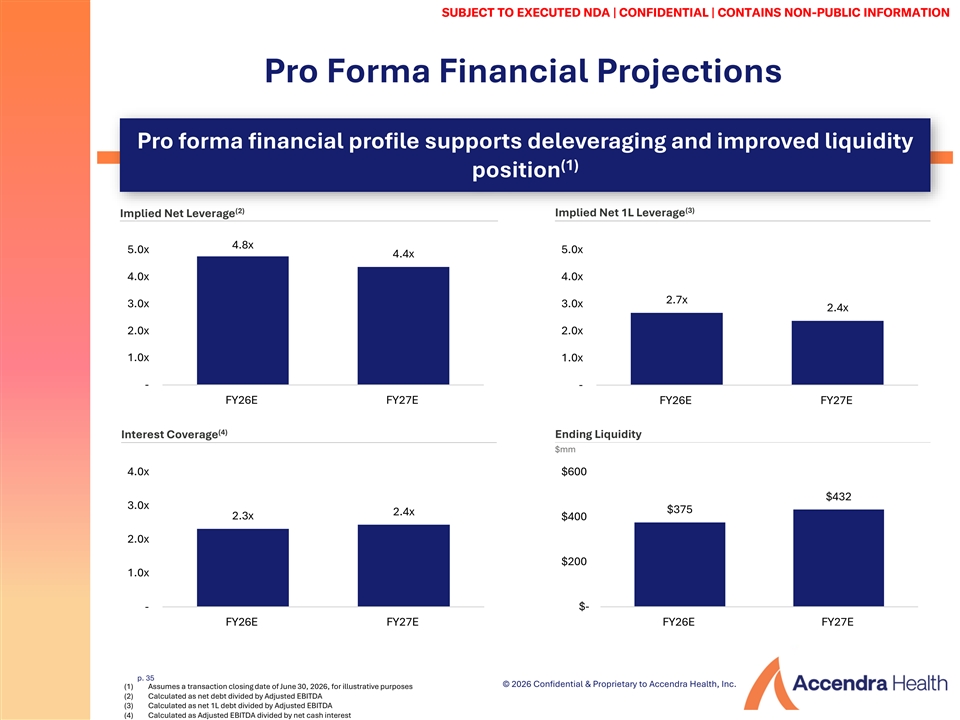

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Pro Forma Financial Projections Pro forma financial profile supports deleveraging and improved liquidity (1) position (2) (3) Implied Net Leverage Implied Net 1L Leverage 4.8x 5.0x 5.0x 4.4x 4.0x 4.0x 2.7x 3.0x 3.0x 2.4x 2.0x 2.0x 1.0x 1.0x - - FY26E FY27E FY26E FY27E (4) Interest Coverage Ending Liquidity $mm 4.0x $600 $432 3.0x $375 2.4x 2.3x $400 2.0x $200 1.0x - $- FY26E FY27E FY26E FY27E p. 35 p. 35 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Assumes a transaction closing date of June 30, 2026, for illustrative purposes Ducera (2) Calculated as net debt divided by Adjusted EBITDA (3) Calculated as net 1L debt divided by Adjusted EBITDA (4) Calculated as Adjusted EBITDA divided by net cash interest (1) Calculated as net debt divided by Consolidated EBITDA, as defined in the Credit Agreements for purposes of financial covenant testing (2) Calculated as Consolidated EBITDA divided by net cash interest

SU SUBJ BJECT ECT T TO O EX EXECU ECUT TED ED ND NDA A || CO CONFID NFIDEN ENT TIAL IAL || CO CONT NTAINS AINS NON NON- -P PU UBLIC BLIC INFORMAT INFORMATIO ION N V. Appendix p. p. 36 36 Ducera

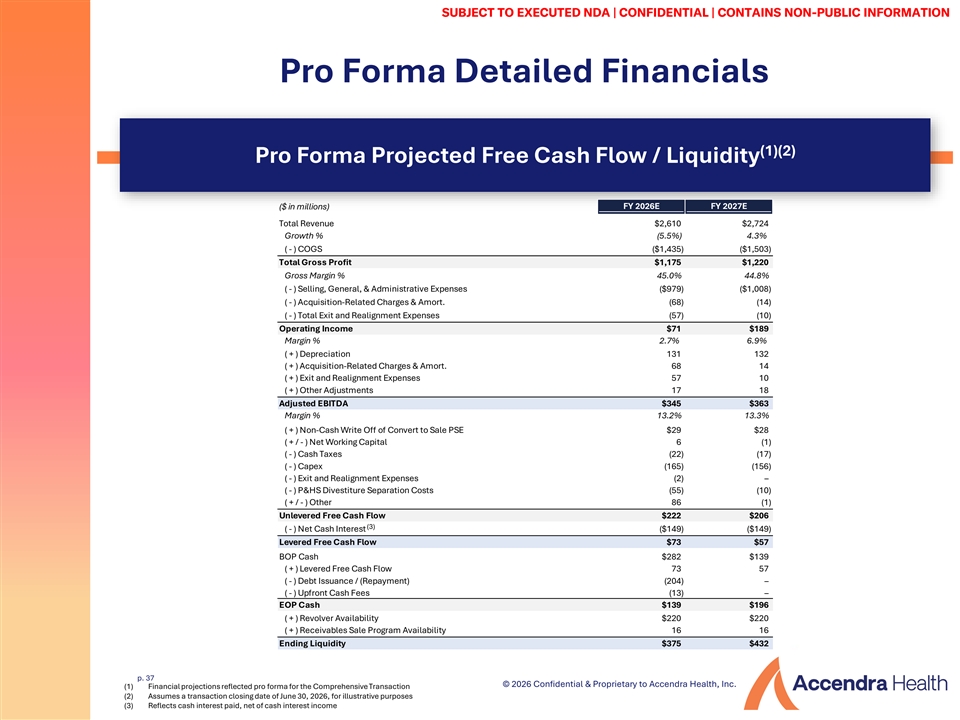

P SU SU RIBJ BJ VAT ECT ECT E SI T TD O O E EX EX INFORMAT ECU ECUT TED ED ND ND ION A A ||| CO CO CONFID NFID NFIDEN EN ENT T TIAL IAL IAL ||| CO CO CONT NT NTAINS AINS AINS NON NON NON- - -PU P PU UBLI BLIC BLIC C INFORMAT INFORMAT INFORMATIO IO ION N N Pro Forma Detailed Financials (1)(2) Pro Forma Projected Free Cash Flow / Liquidity ($ in millions) FY 2026E FY 2027E Total Revenue $2,610 $2,724 Growth % (5.5%) 4.3% ( - ) COGS ($1,435) ($1,503) Total Gross Profit $1,175 $1,220 Gross Margin % 45.0% 44.8% ( - ) Selling, General, & Administrative Expenses ($979) ($1,008) ( - ) Acquisition-Related Charges & Amort. (68) (14) ( - ) Total Exit and Realignment Expenses (57) (10) Operating Income $71 $189 Margin % 2.7% 6.9% ( + ) Depreciation 131 132 ( + ) Acquisition-Related Charges & Amort. 68 14 ( + ) Exit and Realignment Expenses 57 10 ( + ) Other Adjustments 17 18 Adjusted EBITDA $345 $363 Margin % 13.2% 13.3% ( + ) Non-Cash Write Off of Convert to Sale PSE $29 $28 ( + / - ) Net Working Capital 6 (1) ( - ) Cash Taxes (22) (17) ( - ) Capex (165) (156) ( - ) Exit and Realignment Expenses (2) – ( - ) P&HS Divestiture Separation Costs (55) (10) ( + / - ) Other 86 (1) Unlevered Free Cash Flow $222 $206 (3) ( - ) Net Cash Interest ($149) ($149) Levered Free Cash Flow $73 $57 BOP Cash $282 $139 ( + ) Levered Free Cash Flow 73 57 ( - ) Debt Issuance / (Repayment) (204) – ( - ) Upfront Cash Fees (13) – EOP Cash $139 $196 ( + ) Revolver Availability $220 $220 ( + ) Receivables Sale Program Availability 16 16 Ending Liquidity $375 $432 p. 37 p. 37 © 2026 Confidential & Proprietary to Accendra Health, Inc. (1) Financial projections reflected pro forma for the Comprehensive Transaction Ducera (2) Assumes a transaction closing date of June 30, 2026, for illustrative purposes (3) Reflects cash interest paid, net of cash interest income