UNITED

STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

N-CSR

CERTIFIED

SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

| Investment

Company Act file number |

811-23611 |

| James

Alpha Funds Trust |

| (Exact

name of registrant as specified in charter) |

| 515

Madison Avenue, 24th Floor, New York, NY |

10022 |

| (Address

of principal executive offices) |

(Zip

code) |

| Emile

R. Molineaux |

| 80

Arkay Drive, Suite 110, Hauppauge, NY 11788 |

| (Name

and address of agent for service) |

| Registrant’s

telephone number, including area code: |

888-814-8180 |

| Date

of fiscal year end: |

8/31 |

| |

|

| Date

of reporting period: |

2/28/26 |

Item

1. Reports to Stockholders.

0001829774falseN-CSRSJames Alpha Funds TrustN-1A2026-02-280001829774jaft:C000248910Member2025-09-012026-02-2800018297742025-09-012026-02-280001829774jaft:C000248910Member2026-02-280001829774jaft:C000248910Memberjaft:Financials21258BAA8SectorMember2026-02-280001829774jaft:C000248910Memberjaft:HealthCare866973AD2SectorMember2026-02-280001829774jaft:C000248910Memberjaft:Energy8AMCSHVS8SectorMember2026-02-280001829774jaft:C000248910Memberjaft:A21258BAA8Convivial2022IIILLCCTIMember2026-02-280001829774jaft:C000248910Memberjaft:A866973AD2SunlandMedicalFoundationCTIMember2026-02-280001829774jaft:C000248910Memberjaft:A8AMCSHVS8NextRenewableFuelsCTIMember2026-02-280001829774jaft:C000248909Member2025-09-012026-02-280001829774jaft:C000248909Member2026-02-280001829774jaft:C000248909Memberjaft:Financials21258BAA8SectorMember2026-02-280001829774jaft:C000248909Memberjaft:HealthCare866973AD2SectorMember2026-02-280001829774jaft:C000248909Memberjaft:Energy8AMCSHVS8SectorMember2026-02-280001829774jaft:C000248909Memberjaft:A21258BAA8Convivial2022IIILLCCTIMember2026-02-280001829774jaft:C000248909Memberjaft:A866973AD2SunlandMedicalFoundationCTIMember2026-02-280001829774jaft:C000248909Memberjaft:A8AMCSHVS8NextRenewableFuelsCTIMember2026-02-280001829774jaft:C000248908Member2025-09-012026-02-280001829774jaft:C000248908Member2026-02-280001829774jaft:C000248908Memberjaft:Financials21258BAA8SectorMember2026-02-280001829774jaft:C000248908Memberjaft:HealthCare866973AD2SectorMember2026-02-280001829774jaft:C000248908Memberjaft:Energy8AMCSHVS8SectorMember2026-02-280001829774jaft:C000248908Memberjaft:A21258BAA8Convivial2022IIILLCCTIMember2026-02-280001829774jaft:C000248908Memberjaft:A866973AD2SunlandMedicalFoundationCTIMember2026-02-280001829774jaft:C000248908Memberjaft:A8AMCSHVS8NextRenewableFuelsCTIMember2026-02-28iso4217:USDxbrli:sharesiso4217:USDxbrli:sharesxbrli:pureutr:Djaft:Holding

Easterly ROCMuni High Income Municipal Bond Fund

Semi-Annual Shareholder Report - February 28, 2026

This semi-annual shareholder report contains important information about Easterly ROCMuni High Income Municipal Bond Fund for the period of September 1, 2025 to February 28, 2026. You can find additional information about the Fund at https://funds.easterlyam.com/resources/. You can also request this information by contacting us at 1-833-999-2636. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund’s costs for the last six months?

(based on a hypothetical $10,000 investment)

Table SummaryClass Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

Class A | $270 | 6.17%Footnote Reference* |

|---|

| Footnote | Description |

Footnote* | Annualized |

Table SummaryNet Assets | $9,104,375 |

|---|

Number of Portfolio Holdings | 3 |

|---|

Advisory Fee (net of waivers) | $0 |

|---|

Portfolio Turnover | 0% |

|---|

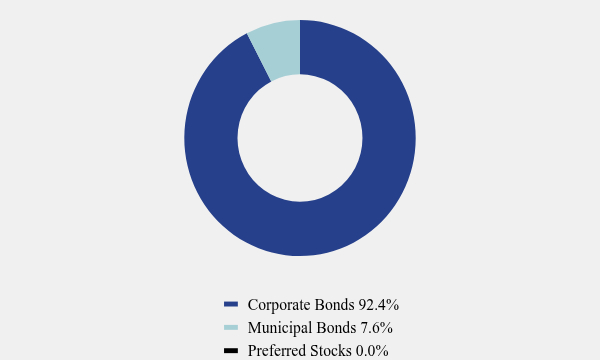

Asset Weighting (% of total investments)

Table SummaryValue | Value |

|---|

Corporate Bonds | 92.4% |

Municipal Bonds | 7.6% |

Preferred Stocks | 0.0% |

Top 10 Holdings (% of net assets)

Table SummaryHolding Name | % of Net Assets |

|---|

Convivial 2022 III LLC | 55.2% |

|---|

Sunland Medical Foundation | 4.5% |

|---|

Next Renewable Fuels | 0.0% |

|---|

This is a summary of certain changes to the Fund since September 1, 2025. For more complete information, you may review the Fund’s prospectus, as supplemented, at https://funds.easterlyam.com/resources/ or upon request at 1-833-999-2636.

The Fund is in the process of liquidating its assets and winding up its business pursuant to a plan of liquidation. As a result, the Fund is no longer actively pursuing its investment objective and will deviate from its principal investment strategies in order to facilitate the orderly disposition of its remaining portfolio holdings. As a result, shareholders may experience a taxable event upon redemption or liquidation of the fund’s assets.* The Fund is currently closed to investors.

*Not to be construed as tax advice. Investors are encouraged to speak with their financial and tax advisor.

Easterly ROCMuni High Income Municipal Bond Fund - Class A (RMJAX)

Semi-Annual Shareholder Report - February 28, 2026

Where can I find additional information about the Fund?

Additional information is available on the Fund's website (https://funds.easterlyam.com/resources/), including its:

Prospectus

Financial information

Holdings

Proxy voting information

To reduce expenses, the Fund will mail only one copy of the prospectus and each annual and semi-annual report to those addresses shared by two or more accounts. If you wish to receive individual copies of these documents, please call the Fund at (833) 999-2636 on days the Fund is open for business or contact your financial institution. The Fund will begin sending you individual copies thirty days after receiving your request.

Easterly ROCMuni High Income Municipal Bond Fund

Semi-Annual Shareholder Report - February 28, 2026

This semi-annual shareholder report contains important information about Easterly ROCMuni High Income Municipal Bond Fund for the period of September 1, 2025 to February 28, 2026. You can find additional information about the Fund at https://funds.easterlyam.com/resources/. You can also request this information by contacting us at 1-833-999-2636. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund’s costs for the last six months?

(based on a hypothetical $10,000 investment)

Table SummaryClass Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

Class I | $258 | 5.91%Footnote Reference* |

|---|

| Footnote | Description |

Footnote* | Annualized |

Table SummaryNet Assets | $9,104,375 |

|---|

Number of Portfolio Holdings | 3 |

|---|

Advisory Fee (net of waivers) | $0 |

|---|

Portfolio Turnover | 0% |

|---|

Asset Weighting (% of total investments)

Table SummaryValue | Value |

|---|

Corporate Bonds | 92.4% |

Municipal Bonds | 7.6% |

Preferred Stocks | 0.0% |

Top 10 Holdings (% of net assets)

Table SummaryHolding Name | % of Net Assets |

|---|

Convivial 2022 III LLC | 55.2% |

|---|

Sunland Medical Foundation | 4.5% |

|---|

Next Renewable Fuels | 0.0% |

|---|

This is a summary of certain changes to the Fund since September 1, 2025. For more complete information, you may review the Fund’s prospectus, as supplemented, at https://funds.easterlyam.com/resources/ or upon request at 1-833-999-2636.

The Fund is in the process of liquidating its assets and winding up its business pursuant to a plan of liquidation. As a result, the Fund is no longer actively pursuing its investment objective and will deviate from its principal investment strategies in order to facilitate the orderly disposition of its remaining portfolio holdings. As a result, shareholders may experience a taxable event upon redemption or liquidation of the fund’s assets.* The Fund is currently closed to investors.

*Not to be construed as tax advice. Investors are encouraged to speak with their financial and tax advisor.

Easterly ROCMuni High Income Municipal Bond Fund - Class I (RMHIX)

Semi-Annual Shareholder Report - February 28, 2026

Where can I find additional information about the Fund?

Additional information is available on the Fund's website (https://funds.easterlyam.com/resources/), including its:

Prospectus

Financial information

Holdings

Proxy voting information

To reduce expenses, the Fund will mail only one copy of the prospectus and each annual and semi-annual report to those addresses shared by two or more accounts. If you wish to receive individual copies of these documents, please call the Fund at (833) 999-2636 on days the Fund is open for business or contact your financial institution. The Fund will begin sending you individual copies thirty days after receiving your request.

Easterly ROCMuni High Income Municipal Bond Fund

Semi-Annual Shareholder Report - February 28, 2026

This semi-annual shareholder report contains important information about Easterly ROCMuni High Income Municipal Bond Fund for the period of September 1, 2025 to February 28, 2026. You can find additional information about the Fund at https://funds.easterlyam.com/resources/. You can also request this information by contacting us at 1-833-999-2636. This report describes changes to the Fund that occurred during the reporting period.

What were the Fund’s costs for the last six months?

(based on a hypothetical $10,000 investment)

Table SummaryClass Name | Costs of a $10,000 investment | Costs paid as a percentage of a $10,000 investment |

|---|

Investor Class | $297 | 6.80%Footnote Reference* |

|---|

| Footnote | Description |

Footnote* | Annualized |

Table SummaryNet Assets | $9,104,375 |

|---|

Number of Portfolio Holdings | 3 |

|---|

Advisory Fee (net of waivers) | $0 |

|---|

Portfolio Turnover | 0% |

|---|

Asset Weighting (% of total investments)

Table SummaryValue | Value |

|---|

Corporate Bonds | 92.4% |

Municipal

Bonds | 7.6% |

Preferred Stocks | 0.0% |

Top 10 Holdings (% of net assets)

Table SummaryHolding Name | % of Net Assets |

|---|

Convivial 2022 III LLC | 55.2% |

|---|

Sunland Medical Foundation | 4.5% |

|---|

Next Renewable Fuels | 0.0% |

|---|

This is a summary of certain changes to the Fund since September 1, 2025. For more complete information, you may review the Fund’s prospectus, as supplemented, at https://funds.easterlyam.com/resources/ or upon request at 1-833-999-2636.

The Fund is in the process of liquidating its assets and winding up its business pursuant to a plan of liquidation. As a result, the Fund is no longer actively pursuing its investment objective and will deviate from its principal investment strategies in order to facilitate the orderly disposition of its remaining portfolio holdings. As a result, shareholders may experience a taxable event upon redemption or liquidation of the fund’s assets.* The Fund is currently closed to investors.

*Not to be construed as tax advice. Investors are encouraged to speak with their financial and tax advisor.

Easterly ROCMuni High Income Municipal Bond Fund - Investor Class (RMHVX)

Semi-Annual Shareholder Report - February 28, 2026

Where can I find additional information about the Fund?

Additional information is available on the Fund's website (https://funds.easterlyam.com/resources/), including its:

Prospectus

Financial information

Holdings

Proxy voting information

To reduce expenses, the Fund will mail only one copy of the prospectus and each annual and semi-annual report to those addresses shared by two or more accounts. If you wish to receive individual copies of these documents, please call the Fund at (833) 999-2636 on days the Fund is open for business or contact your financial institution. The Fund will begin sending you individual copies thirty days after receiving your request.

Item

2. Code of Ethics.

Not

applicable.

Item

3. Audit Committee Financial Expert.

Not

applicable.

Item

4. Principal Accountant Fees and Services.

Not

applicable.

Item

5. Audit Committee of Listed Registrants.

Not

applicable

Item

6. Investments.

(a) The

Registrant’s schedule of investments in unaffiliated issuers is included in the Financial Statements under Item 7 of this form.

Item

7. Financial Statements and Financial Highlights for Open-End Management Investment Companies.

|

(a) |

Long Form Financial Statements |

| |

| |

| |

| |

| |

| |

| |

| |

|

| |

| JAMES

ALPHA FUNDS TRUST d/b/a EASTERLY FUNDS TRUST |

| |

| |

| |

| |

| |

| |

| SEMI-ANNUAL

FINANCIAL |

| STATEMENTS

AND ADDITIONAL |

| INFORMATION |

| FEBRUARY

28, 2026 |

| |

| |

| |

| |

| |

| |

| |

| |

| THIS

REPORT IS AUTHORIZED FOR DISTRIBUTION ONLY TO SHAREHOLDERS AND TO OTHERS WHO |

| HAVE

RECEIVED A COPY OF THE PROSPECTUS. |

| |

| |

| |

| |

| EASTERLY

ROCMUNI HIGH INCOME MUNICIPAL BOND FUND |

| SCHEDULE OF

INVESTMENTS (Unaudited) |

| February 28,

2026 |

| |

|

|

|

|

Coupon Rate |

|

|

|

|

|

| Shares |

|

|

|

|

(%) |

|

Maturity |

|

Fair Value |

|

| |

|

|

|

CONVERTIBLE

PREFERRED STOCKS — 0.0%(a) |

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

8 |

|

|

Next

Renewable Fuels - Series A(b),(c) |

|

6.0000 |

|

|

|

$ |

— |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

TOTAL CONVERTIBLE PREFERRED

STOCKS (Cost $5,715,285) |

|

|

|

|

|

|

— |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Principal |

|

|

|

|

|

|

|

|

|

|

| Amount ($) |

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

CORPORATE BONDS — 55.2% |

|

|

|

|

|

|

|

|

| |

5,025,000 |

|

|

Convivial

2022 III LLC(b),(d) |

|

12.0000 |

|

11/15/56 |

|

|

5,025,000 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

TOTAL CORPORATE BONDS (Cost

$5,025,000) |

|

|

|

|

|

|

5,025,000 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

MUNICIPAL BONDS — 4.5% |

|

|

|

|

|

|

|

|

| |

|

|

|

NEW MEXICO — 4.5% |

|

|

|

|

|

|

|

|

| |

8,669,836 |

|

|

Sunland

Medical Foundation(b),(d) |

|

12.0000 |

|

04/01/26 |

|

|

411,817 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

TOTAL MUNICIPAL BONDS (Cost

$8,669,836) |

|

|

|

|

|

|

411,817 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

TOTAL INVESTMENTS - 59.7% (Cost $19,410,121) |

|

|

|

|

|

$ |

5,436,817 |

|

| |

|

|

|

OTHER ASSETS IN EXCESS OF

LIABILITIES - 40.3% |

|

|

|

|

|

|

3,667,558 |

|

| |

|

|

|

NET ASSETS - 100.0% |

|

|

|

|

|

$ |

9,104,375 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

(a) |

Percentage less than 0.1%. |

|

(b) |

The value of these securities have

been determined in good faith by the Adviser as the Valuation Designee pursuant to valuation procedures approved by the Board of Trustees.

These securities are deemed illiquid and represent 59.7% of net assets. |

|

(d) |

Security exempt from registration

under Rule 144A or Section 4(2) of the Securities Act of 1933. The security may be resold in transactions exempt from registration, normally

to qualified institutional buyers. As of February 28, 2026 the total market value of 144A securities is $5,436,817 or 59.7% of net assets. |

See

accompanying notes to financial statements.

| EASTERLY

ROCMUNI HIGH INCOME MUNICIPAL BOND FUND |

| STATEMENT

OF ASSETS AND LIABILITIES (Unaudited) |

| February 28,

2026 |

| Assets: |

|

|

|

|

| Total Investments, at cost |

|

$ |

19,410,121 |

|

| Total Investments, at value |

|

|

5,436,817 |

|

| Cash |

|

|

3,458,340 |

|

| Interest and dividends receivable |

|

|

185,542 |

|

| Receivable from manager |

|

|

36,581 |

|

| Prepaid expenses and other assets |

|

|

50,784 |

|

| Total Assets |

|

|

9,168,064 |

|

| |

|

|

|

|

| Liabilities: |

|

|

|

|

| Payable for distribution (12b-1) fees |

|

|

40,319 |

|

| Administration fees payable |

|

|

9,923 |

|

| Trustee fees payable |

|

|

2,468 |

|

| Interest expense payable |

|

|

556 |

|

| Accrued expenses and other liabilities |

|

|

10,423 |

|

| Total Liabilities |

|

|

63,689 |

|

| |

|

|

|

|

| Net Assets |

|

$ |

9,104,375 |

|

| |

|

|

|

|

| Net Assets: |

|

|

|

|

| Paid in capital |

|

|

203,854,881 |

|

| Accumulated loss |

|

|

(194,750,506 |

) |

| Net Assets |

|

$ |

9,104,375 |

|

| |

|

|

|

|

| Net Asset Value Per Share |

|

|

|

|

| Class A |

|

|

|

|

| Net Assets |

|

$ |

273,807 |

|

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] |

|

|

122,247 |

|

| Net asset value, redemption price per share |

|

$ |

2.24 |

|

Offering price per share

(maximum sales charge of 2.00%) |

|

$ |

2.29 |

|

| |

|

|

|

|

| Class I |

|

|

|

|

| Net Assets |

|

$ |

8,803,959 |

|

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] |

|

|

3,906,426 |

|

| Net asset value, redemption price and offering price per share |

|

$ |

2.25 |

|

| |

|

|

|

|

| Investor Class |

|

|

|

|

| Net Assets |

|

$ |

26,609 |

|

| Shares of beneficial interest outstanding [$0 par value, unlimited shares authorized] |

|

|

11,774 |

|

| Net asset value, redemption price and offering price per share |

|

$ |

2.26 |

|

See

accompanying notes to financial statements.

| EASTERLY

ROCMUNI HIGH INCOME MUNICIPAL BOND FUND |

| STATEMENT

OF OPERATIONS (Unaudited) |

| For the Six

Months Ended February 28, 2026 |

| Investment Income: |

|

|

|

|

| Interest income |

|

|

701,525 |

|

| Total Investment Income |

|

|

701,525 |

|

| |

|

|

|

|

| Operating Expenses: |

|

|

|

|

| Management fees |

|

|

22,767 |

|

| Distribution (12b-1) fees |

|

|

|

|

| Class A Shares |

|

|

432 |

|

| Investor Class |

|

|

526 |

|

| Interest Expense |

|

|

285,143 |

|

| Legal fees |

|

|

81,111 |

|

| Registration fees |

|

|

20,884 |

|

| Transfer Agent |

|

|

12,519 |

|

| Trustees’ fees |

|

|

9,494 |

|

| Custodian fees |

|

|

9,074 |

|

| Administration fees |

|

|

6,403 |

|

| Compliance officer fees |

|

|

4,674 |

|

| Shareholder servicing fees |

|

|

3,731 |

|

| Audit fees |

|

|

3,044 |

|

| Insurance expense |

|

|

855 |

|

| Miscellaneous expenses |

|

|

545 |

|

| Total Operating Expenses |

|

|

461,202 |

|

| Less: Expenses waived/reimbursed |

|

|

(130,228 |

) |

| Net Operating Expenses |

|

|

330,974 |

|

| |

|

|

|

|

| Net Investment Income |

|

|

370,551 |

|

| |

|

|

|

|

| Realized and Unrealized Gain (Loss) on Investments: |

|

|

|

|

| Net realized loss from: |

|

|

|

|

| Investments |

|

|

(2,722,968 |

) |

| Net realized loss |

|

|

(2,722,968 |

) |

| |

|

|

|

|

| Net change in unrealized depreciation on: |

|

|

|

|

| Investments |

|

|

(598,477 |

) |

| Net change in unrealized depreciation |

|

|

(598,477 |

) |

| |

|

|

|

|

| Net Realized and Unrealized

Loss On Investments |

|

|

(3,321,445 |

) |

| |

|

|

|

|

| Net Decrease in Net Assets

Resulting From Operations |

|

$ |

(2,950,894 |

) |

See

accompanying notes to financial statements.

| EASTERLY

ROCMUNI HIGH INCOME MUNICIPAL BOND FUND |

| STATEMENTS

OF CHANGES IN NET ASSETS |

| |

|

Six Months ended |

|

|

|

|

| |

|

February 28, 2026 |

|

|

Year Ended |

|

| |

|

(Unaudited) |

|

|

August 31, 2025 |

|

| |

|

|

|

|

|

|

| Operations: |

|

|

|

|

|

|

|

|

| Net investment income |

|

$ |

370,551 |

|

|

$ |

5,445,273 |

|

| Net realized loss on investments |

|

|

(2,722,968 |

) |

|

|

(146,031,971 |

) |

| Net change in unrealized appreciation (depreciation)

on investments |

|

|

(598,477 |

) |

|

|

41,128,318 |

|

| Net decrease in net assets

resulting from operations |

|

|

(2,950,894 |

) |

|

|

(99,458,380 |

) |

| |

|

|

|

|

|

|

|

|

| Distributions to Shareholders: |

|

|

|

|

|

|

|

|

| Total Distributions Paid: |

|

|

|

|

|

|

|

|

| Class A |

|

|

— |

|

|

|

(518,767 |

) |

| Class I |

|

|

— |

|

|

|

(5,752,265 |

) |

| Investor Class |

|

|

— |

|

|

|

(1,005,314 |

) |

| Return of Capital |

|

|

|

|

|

|

|

|

| Class A |

|

|

— |

|

|

|

(446,401 |

) |

| Class I |

|

|

— |

|

|

|

(4,110,516 |

) |

| Investor Class |

|

|

— |

|

|

|

(881,230 |

) |

| Total Dividends and Distributions

to Shareholders |

|

|

— |

|

|

|

(12,714,493 |

) |

| |

|

|

|

|

|

|

|

|

| Share Transactions of Beneficial Interest: |

|

|

|

|

|

|

|

|

| Beneficial Interest: |

|

|

|

|

|

|

|

|

| Net proceeds from shares sold |

|

|

|

|

|

|

|

|

| Class A |

|

|

— |

|

|

|

11,832,252 |

|

| Class I |

|

|

— |

|

|

|

75,210,234 |

|

| Investor Class |

|

|

— |

|

|

|

7,103,737 |

|

| Reinvestment of dividends and distributions |

|

|

|

|

|

|

|

|

| Class A |

|

|

— |

|

|

|

762,713 |

|

| Class I |

|

|

— |

|

|

|

9,569,971 |

|

| Investor Class |

|

|

— |

|

|

|

1,693,386 |

|

| Cost of shares redeemed |

|

|

|

|

|

|

|

|

| Class A |

|

|

(134,234 |

) |

|

|

(15,289,986 |

) |

| Class I |

|

|

(1,982,551 |

) |

|

|

(262,365,402 |

) |

| Investor Class |

|

|

(358,315 |

) |

|

|

(37,513,438 |

) |

| |

|

|

|

|

|

|

|

|

| Net decrease in net assets

from share transactions of beneficial interest |

|

|

(2,475,100 |

) |

|

|

(208,996,533 |

) |

| |

|

|

|

|

|

|

|

|

| Total Decrease in Net Assets |

|

|

(5,425,994 |

) |

|

|

(321,169,406 |

) |

| |

|

|

|

|

|

|

|

|

| Net Assets: |

|

|

|

|

|

|

|

|

| Beginning of period/year |

|

|

14,530,369 |

|

|

|

335,699,775 |

|

| End of period/year |

|

$ |

9,104,375 |

|

|

$ |

14,530,369 |

|

| |

|

|

|

|

|

|

|

|

| Share Activity |

|

|

|

|

|

|

|

|

| Shares sold |

|

|

|

|

|

|

|

|

| Class A |

|

|

— |

|

|

|

1,700,412 |

|

| Class I |

|

|

— |

|

|

|

10,841,618 |

|

| Investor Class |

|

|

— |

|

|

|

1,020,288 |

|

| Shares Reinvested |

|

|

|

|

|

|

|

|

| Class A |

|

|

— |

|

|

|

119,329 |

|

| Class I |

|

|

— |

|

|

|

1,417,979 |

|

| Investor Class |

|

|

— |

|

|

|

256,004 |

|

| Shares Redeemed |

|

|

|

|

|

|

|

|

| Class A |

|

|

(45,886 |

) |

|

|

(3,879,327 |

) |

| Class I |

|

|

(723,250 |

) |

|

|

(44,214,038 |

) |

| Investor Class |

|

|

(122,286 |

) |

|

|

(8,154,712 |

) |

| Net decrease in shares

of beneficial interest |

|

|

(891,422 |

) |

|

|

(40,892,447 |

) |

See

accompanying notes to financial statements.

| EASTERLY

ROCMUNI HIGH INCOME MUNICIPAL BOND FUND |

| STATEMENT

OF CASH FLOWS (Unaudited) |

| For the Six

Months Ended February 28, 2026 |

| CASH FLOWS FROM OPERATING ACTIVITIES |

|

|

|

|

| Net decrease in net assets resulting from operations |

|

$ |

(2,950,894 |

) |

| Adjustments to reconcile net decrease in net assets resulting from

operations to net cash provided by operating activities: |

|

|

|

|

| Proceeds for sales of investments |

|

|

10,201,169 |

|

| Net realized loss from investments |

|

|

2,722,968 |

|

| Amortization (accretion) of market premium (discount), net |

|

|

(7,159 |

) |

| Net change in unrealized appreciation/depreciation on investments |

|

|

598,477 |

|

| Decrease in Receivable from Manager |

|

|

183,363 |

|

| Decrease in prepaid expenses and other assets |

|

|

40,007 |

|

| Decrease in interest and dividends |

|

|

1,864,302 |

|

| Decrease in administration fees payable |

|

|

(4,226 |

) |

| Decrease in Payable for distribution (12b-1) fees |

|

|

(2,201 |

) |

| Decrease in Trustee fees |

|

|

(3,184 |

) |

| Decrease in interest expense payable |

|

|

(47,361 |

) |

| Decrease in accrued expenses and other liabilities |

|

|

(206,805 |

) |

| Net cash provided by operating

activities |

|

|

12,388,456 |

|

| CASH FLOWS FROM FINANCING ACTIVITIES |

|

|

|

|

| |

|

|

|

|

| Payment of Shares repurchased |

|

|

(2,475,100 |

) |

| Loan repayments |

|

|

(7,187,500 |

) |

| Net cash used in financing

activities |

|

|

(9,662,600 |

) |

| |

|

|

|

|

| NET INCREASE IN CASH |

|

|

2,725,856 |

|

| CASH - BEGINNING OF PERIOD |

|

|

732,484 |

|

| CASH - END OF PERIOD |

|

$ |

3,458,340 |

|

See

accompanying notes to financial statements.

| EASTERLY

ROCMUNI HIGH INCOME MUNICIPAL BOND FUND |

| FINANCIAL

HIGHLIGHTS (For a share outstanding throughout each year/period) |

| |

|

CLASS A |

|

|

|

|

|

| |

|

Six Months |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Ended |

|

|

|

|

|

|

|

|

|

|

|

For the |

|

|

|

|

|

| |

|

February 28, |

|

|

Year Ended |

|

|

Year Ended |

|

|

Year Ended |

|

|

Period Ended |

|

|

|

|

|

| |

|

2026 |

|

|

August 31, |

|

|

August 31, |

|

|

August 31, |

|

|

August 31, |

|

|

|

|

|

| |

|

(Unaudited) |

|

|

2025 |

|

|

2024 |

|

|

2023 |

|

|

2022 (1) |

|

|

|

|

|

| Net Asset Value,

Beginning of Year/Period |

|

$ |

2.93 |

|

|

$ |

7.29 |

|

|

$ |

7.11 |

|

|

$ |

7.87 |

|

|

$ |

8.74 |

|

|

|

|

|

| Income (Loss) from Investment Operations: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net investment income |

|

|

0.08 |

(2) |

|

|

0.16 |

(2) |

|

|

0.46 |

|

|

|

0.43 |

|

|

|

0.24 |

|

|

|

|

|

| Net realized and unrealized gain (loss) |

|

|

(0.77 |

) |

|

|

(4.19 |

) |

|

|

0.15 |

|

|

|

(0.74 |

) |

|

|

(0.87 |

) |

|

|

|

|

| Total from investment operations |

|

|

(0.69 |

) |

|

|

(4.03 |

) |

|

|

0.61 |

|

|

|

(0.31 |

) |

|

|

(0.63 |

) |

|

|

|

|

| Dividends and Distributions: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Dividends from net investment income |

|

|

— |

|

|

|

(0.18 |

) |

|

|

(0.43 |

) |

|

|

(0.45 |

) |

|

|

(0.24 |

) |

|

|

|

|

| Return of capital |

|

|

— |

|

|

|

(0.15 |

) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

|

|

| Total dividends and distributions |

|

|

— |

|

|

|

(0.33 |

) |

|

|

(0.43 |

) |

|

|

(0.45 |

) |

|

|

(0.24 |

) |

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net Asset Value, End of

Year/Period |

|

$ |

2.24 |

|

|

$ |

2.93 |

|

|

$ |

7.29 |

|

|

$ |

7.11 |

|

|

$ |

7.87 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Return* |

|

|

(23.55 |

)% (3) |

|

|

(57.71 |

)% |

|

|

8.76 |

% |

|

|

(4.02 |

)% |

|

|

(7.27 |

)% (3) |

|

|

|

|

| Ratios and Supplemental Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net assets, end of year/period(000s) |

|

$ |

274 |

|

|

$ |

493 |

|

|

$ |

16,241 |

|

|

$ |

5,739 |

|

|

$ |

375 |

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Ratio of gross operating expenses to average net assets (including

interest expenses) (5) |

|

|

8.51 |

% (4) |

|

|

1.42 |

% |

|

|

1.12 |

% |

|

|

1.27 |

% |

|

|

1.27 |

% (4) |

|

|

|

|

| Ratio of net operating expenses to average net assets (including

interest Expenses) (6) |

|

|

6.17 |

% (4) |

|

|

1.20 |

% |

|

|

1.12 |

% |

|

|

1.23 |

% |

|

|

1.20 |

% (4) |

|

|

|

|

| Ratio of net investment income after expense reimbursement/recoupment

to average net assets |

|

|

5.91 |

% (4) |

|

|

2.36 |

% |

|

|

6.50 |

% |

|

|

5.52 |

% |

|

|

5.44 |

% (4) |

|

|

|

|

| Portfolio Turnover Rate |

|

|

0 |

% (3) |

|

|

19 |

% |

|

|

24 |

% |

|

|

21 |

% |

|

|

53 |

% (3) |

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

CLASS I |

|

| |

|

Six Months |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Ended |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

February 28, |

|

|

Year Ended |

|

|

Year Ended |

|

|

Year Ended |

|

|

Year Ended |

|

|

Year Ended |

|

| |

|

2026 |

|

|

August 31, |

|

|

August 31, |

|

|

August 31, |

|

|

August 31, |

|

|

August 31, |

|

| |

|

(Unaudited) |

|

|

2025 |

|

|

2024 |

|

|

2023 |

|

|

2022 |

|

|

2021 |

|

| Net Asset Value, Beginning

of Year/Period |

|

$ |

2.95 |

|

|

$ |

7.32 |

|

|

$ |

7.21 |

|

|

$ |

7.91 |

|

|

$ |

9.27 |

|

|

$ |

9.12 |

|

| Income (Loss) from Investment Operations: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net investment income |

|

|

0.09 |

(2) |

|

|

0.18 |

(2) |

|

|

0.49 |

|

|

|

0.43 |

|

|

|

0.46 |

|

|

|

0.51 |

|

| Net realized and unrealized gain (loss) |

|

|

(0.79 |

) |

|

|

(4.21 |

) |

|

|

0.07 |

|

|

|

(0.67 |

) |

|

|

(1.35 |

) |

|

|

0.15 |

|

| Total from investment operations |

|

|

(0.70 |

) |

|

|

(4.03 |

) |

|

|

0.56 |

|

|

|

(0.24 |

) |

|

|

(0.89 |

) |

|

|

0.66 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Dividends and Distributions: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Dividends from net investment income |

|

|

— |

|

|

|

(0.19 |

) |

|

|

(0.45 |

) |

|

|

(0.46 |

) |

|

|

(0.47 |

) |

|

|

(0.51 |

) |

| Return of capital |

|

|

— |

|

|

|

(0.15 |

) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

| Total dividends and distributions |

|

|

— |

|

|

|

(0.34 |

) |

|

|

(0.45 |

) |

|

|

(0.46 |

) |

|

|

(0.47 |

) |

|

|

(0.51 |

) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net Asset Value, End of

Year/Period |

|

$ |

2.25 |

|

|

$ |

2.95 |

|

|

$ |

7.32 |

|

|

$ |

7.21 |

|

|

$ |

7.91 |

|

|

$ |

9.27 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Return* |

|

|

(23.73 |

)% (3) |

|

|

(57.52 |

)% |

|

|

7.94 |

% |

|

|

(2.94 |

)% |

|

|

(9.88 |

)% |

|

|

7.49 |

% |

| Ratios and Supplemental Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net assets, end of year/period(000s) |

|

$ |

8,804 |

|

|

$ |

13,640 |

|

|

$ |

267,851 |

|

|

$ |

240,235 |

|

|

$ |

272,640 |

|

|

$ |

289,438 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Ratio of gross operating expenses to average net assets (including

interest expenses) (7) |

|

|

8.24 |

% (4) |

|

|

1.20 |

% |

|

|

0.87 |

% |

|

|

1.04 |

% |

|

|

0.86 |

% |

|

|

0.78 |

% |

| Ratio of net operating expenses to average net assets (including

interest Expenses) (8) |

|

|

5.91 |

% (4) |

|

|

0.97 |

% |

|

|

0.88 |

% |

|

|

1.00 |

% |

|

|

0.83 |

% |

|

|

0.73 |

% |

| Ratio of net investment income (loss) after expense reimbursement/recoupment

to average net assets |

|

|

6.81 |

% (4) |

|

|

2.67 |

% |

|

|

6.82 |

% |

|

|

5.75 |

% |

|

|

5.35 |

% |

|

|

5.70 |

% |

| Portfolio Turnover Rate |

|

|

0 |

% (3) |

|

|

19 |

% |

|

|

24 |

% |

|

|

21 |

% |

|

|

53 |

% |

|

|

64 |

% |

|

(1) |

Inception date for the A Class was

February 16, 2022. |

|

(2) |

Per share amounts calculated using

the average shares method, which more appropriately presents the per share data for the period. |

|

(5) |

Ratio of gross expenses to average

net assets (excluding interest expenses) for the Easterly ROCMuni High Income Municipal Bond Fund - Class A: |

| |

|

|

3.40 |

% |

|

|

1.27 |

% |

|

|

1.05 |

% |

|

|

1.07 |

% |

|

|

1.06 |

% |

|

|

N/A |

|

|

(6) |

Ratio of net operating expenses to

average net assets (excluding interest expenses) for the Easterly ROCMuni High Income Municipal Bond Fund - Class A: |

| |

|

|

1.05 |

% |

|

|

1.05 |

% |

|

|

1.05 |

% |

|

|

1.03 |

% |

|

|

0.98 |

% |

|

|

N/A |

|

|

(7) |

Ratio of gross expenses to average

net assets (excluding interest expenses) for the Easterly ROCMuni High Income Municipal Bond Fund - Class I: |

| |

|

|

3.14 |

% |

|

|

1.04 |

% |

|

|

0.80 |

% |

|

|

0.81 |

% |

|

|

0.76 |

% |

|

|

0.77 |

% |

|

(8) |

Ratio of net operating expenses to

average net assets (excluding interest expenses) for the Easterly ROCMuni High Income Municipal Bond Fund - Class I: |

| |

|

|

0.80 |

% |

|

|

0.80 |

% |

|

|

0.80 |

% |

|

|

0.77 |

% |

|

|

0.73 |

% |

|

|

0.73 |

% |

|

* |

Assumes reinvestment of all dividends

and distributions and does not assume the effects of any sales charges. Aggregate (not annualized) total return is shown for any period

shorter than one year. Total return does not reflect the deduction of taxes that a shareholder would pay on distributions or on the redemption

of shares. |

See

accompanying notes to financial statements.

| EASTERLY

ROCMUNI HIGH INCOME MUNICIPAL BOND FUND |

| FINANCIAL

HIGHLIGHTS (For a share outstanding throughout each year/period) |

| |

|

Investor |

|

| |

|

Six Months |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

Ended |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

February 28, |

|

|

Year Ended |

|

|

Year Ended |

|

|

Year Ended |

|

|

Year Ended |

|

|

Year Ended |

|

| |

|

2026 |

|

|

August 31, |

|

|

August 31, |

|

|

August 31, |

|

|

August 31, |

|

|

August 31, |

|

| |

|

(Unaudited) |

|

|

2025 |

|

|

2024 |

|

|

2023 |

|

|

2022 |

|

|

2021 |

|

| Net Asset Value,

Beginning of Year/Period |

|

$ |

2.96 |

|

|

$ |

7.36 |

|

|

$ |

7.23 |

|

|

$ |

7.96 |

|

|

$ |

9.32 |

|

|

$ |

9.18 |

|

| Income (Loss) from Investment Operations: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net investment income |

|

|

(0.01 |

) (1) |

|

|

0.15 |

(1) |

|

|

0.45 |

|

|

|

0.40 |

|

|

|

0.41 |

|

|

|

0.48 |

|

| Net realized and unrealized gain (loss) |

|

|

(0.69 |

) |

|

|

(4.23 |

) |

|

|

0.09 |

|

|

|

(0.70 |

) |

|

|

(1.35 |

) |

|

|

0.13 |

|

| Total from investment operations |

|

|

(0.70 |

) |

|

|

(4.08 |

) |

|

|

0.54 |

|

|

|

(0.30 |

) |

|

|

(0.94 |

) |

|

|

0.61 |

|

| Dividends and Distributions: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Dividends from net investment income |

|

|

— |

|

|

|

(0.17 |

) |

|

|

(0.41 |

) |

|

|

(0.43 |

) |

|

|

(0.42 |

) |

|

|

(0.47 |

) |

| Return of capital |

|

|

— |

|

|

|

(0.15 |

) |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

| Total dividends and distributions |

|

|

— |

|

|

|

(0.32 |

) |

|

|

(0.41 |

) |

|

|

(0.43 |

) |

|

|

(0.42 |

) |

|

|

(0.47 |

) |

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net Asset Value, End of

Year/Period |

|

$ |

2.26 |

|

|

$ |

2.96 |

|

|

$ |

7.36 |

|

|

$ |

7.23 |

|

|

$ |

7.96 |

|

|

$ |

9.32 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Return* |

|

|

(23.65 |

)% (4) |

|

|

(57.80 |

)% |

|

|

7.66 |

% |

|

|

(3.81 |

)% |

|

|

(10.28 |

)% |

|

|

6.82 |

% |

| Ratios and Supplemental Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net assets, end of year/period (000s) |

|

$ |

27 |

|

|

$ |

397 |

|

|

$ |

51,608 |

|

|

$ |

28,801 |

|

|

$ |

20,740 |

|

|

$ |

12,420 |

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Ratio of gross operating expenses to average net assets (including

interest expenses)(2) |

|

|

9.20 |

% (5) |

|

|

1.60 |

% |

|

|

1.37 |

% |

|

|

1.54 |

% |

|

|

1.38 |

% |

|

|

1.28 |

% |

| Ratio of net operating expenses to average net assets (including

interest Expenses)(3) |

|

|

6.80 |

% (5) |

|

|

1.42 |

% |

|

|

1.38 |

% |

|

|

1.50 |

% |

|

|

1.35 |

% |

|

|

1.24 |

% |

| Ratio of net investment income after expense reimbursement/recoupment

to average net assets |

|

|

(0.72 |

)% (5) |

|

|

2.20 |

% |

|

|

6.30 |

% |

|

|

5.25 |

% |

|

|

4.89 |

% |

|

|

5.20 |

% |

| Portfolio Turnover Rate |

|

|

0 |

% (4) |

|

|

19 |

% |

|

|

24 |

% |

|

|

21 |

% |

|

|

53 |

% |

|

|

64 |

% |

|

(1) |

Per share amounts calculated using

the average shares method, which more appropriately presents the per share data for the period. |

|

(2) |

Ratio of gross expenses to average

net assets (excluding interest expenses) for the Easterly ROCMuni High Income Municipal Bond Fund - Investor Class: |

| |

|

|

3.73 |

% |

|

|

1.43 |

% |

|

|

1.30 |

% |

|

|

1.31 |

% |

|

|

1.26 |

% |

|

|

1.27 |

% |

|

(3) |

Ratio of net operating expenses to

average net assets (excluding interest expenses) for the Easterly ROCMuni High Income Municipal Bond Fund - Investor Class: |

| |

|

|

1.30 |

% |

|

|

1.30 |

% |

|

|

1.30 |

% |

|

|

1.27 |

% |

|

|

1.23 |

% |

|

|

1.23 |

% |

|

* |

Assumes reinvestment of all dividends

and distributions and does not assume the effects of any sales charges. Aggregate (not annualized) total return is shown for any period

shorter than one year. Total return does not reflect the deduction of taxes that a shareholder would pay on distributions or on the redemption

of shares. |

See

accompanying notes to financial statements.

| EASTERLY

ROCMUNI HIGH INCOME MUNICIPAL BOND FUND |

| NOTES TO FINANCIAL

STATEMENTS |

| Six Months Ended

February 28, 2026 (Unaudited) |

|

1. |

ORGANIZATION AND SIGNIFICANT ACCOUNTING

POLICIES |

The

Easterly ROCMuni High Income Municipal Bond Fund (“High Income Muni”) is a diversified series of beneficial interest of James

Alpha Funds Trust d/b/a Easterly Fund Trust (the “Trust”) organized in 2020, as a Delaware Statutory Trust and is registered

under the Investment Company Act of 1940, as amended, as an open-end management investment company. The Trust consists of seven series.

Easterly Investment Partners LLC serves as the Fund’s advisor. The Fund’s primary objective is to generate current income exempt

from regular federal income tax.

Ultimus

Fund Solutions, LLC (the “Administrator”), serves the Trust as administrator, transfer agent and fund accounting agent.

The

Principal Street High Income Municipal Fund (“Existing Fund”) was reorganized on October 4, 2024, from a series of Managed Portfolio

Series, a Delaware statutory trust, into High Income Muni a series of the Trust. The Institutional Class, Investor Class and Class A of

the Principal Street High Income Municipal Fund reorganized into Class I, Investor Class and Class A of High Income Muni, respectively.

The

Board of Trustees of the Trust has approved a Plan of Liquidation and Dissolution (“Plan”) for the High Income Muni Fund. The

High Income Muni Fund is currently closed to investors and is in the process of liquidating its assets and winding up its business pursuant

to the Plan. As a result, the High Income Muni Fund is no longer actively pursuing its investment objective and will deviate from its

principal investment strategies in order to facilitate the orderly disposition of its remaining portfolio holdings.

The

Fund consists of Class I, Investor Class and Class A shares. Class A shares have a maximum sales load of 2.00%. Each class represents

an interest in the same assets of the applicable Fund, and the classes are identical except for differences in their sales charge structures,

ongoing service and distribution charges. All classes of shares have equal voting privileges except that each class has exclusive voting

rights with respect to its service and/or distribution plans. Fund level income and expenses and realized and unrealized capital gains

and losses are allocated to each class of shares based on their relative net assets within the Fund. Class specific expenses are allocated

to that share class.

The

following is a summary of significant accounting policies followed by the Fund in preparation of its financial statements. These policies

are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The preparation of

financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of

assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts

of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting

Standards Board (FASB) Accounting Standard Codification Topic 946 “Financial Services – Investment Companies” including

FASB Accounting Standard Update ASU 2013-08.

Segment

Reporting – An operating segment is defined as a component of a public entity that engages in business activities from which

it may recognize revenues and incur expenses, has operating results that are regularly reviewed by the public entity’s chief operating

decision maker (“CODM”) to make decisions about resources to be allocated to the segment and assess its performance, and has

discrete financial information available. The CODM is comprised of the portfolio manager and Chief Financial Officer of the Trust. The

Fund operates as a single operating segment. The Fund’s income, expenses, assets, changes in net assets resulting from operations

and performance are regularly monitored and assessed as a whole by the CODM responsible for oversight functions of the Fund, using the

information presented in the financial statements and financial highlights.

(a)

Valuation of Investments

Investment

securities listed on a national securities exchange are valued at the last reported sale price on the valuation date. NASDAQ traded securities

are valued at the NASDAQ Official Closing Price (NOCP). If there are no such reported sales, the securities are valued at the mean between

current bid and ask. Debt securities (other than short-term obligations) are valued each day by an independent pricing service using methods

which include current market quotations from a major market maker in the securities and trader-reviewed “matrix” prices. Short-term

debt securities having a remaining maturity of sixty days or less may be valued at amortized cost or amortized value, which approximates

market value. U.S. Government Money Market values all of its securities on the basis of amortized cost, which approximates market value.

Any securities or other assets for which market quotations are not readily available are valued at their fair value as determined in good

faith under procedures established by the Board of Trustees (the “Board”). There

| EASTERLY

ROCMUNI HIGH INCOME MUNICIPAL BOND FUND |

| NOTES TO FINANCIAL

STATEMENTS |

| Six Months Ended

February 28, 2026 (Unaudited)(Continued) |

is

no single standard for determining the fair value of such securities. Rather, in determining the fair value of a security, the board-appointed

Valuation Designee shall take into account the relevant factors and surrounding circumstances, a few of which may include: (i) the nature

and pricing history (if any) of the security; (ii) whether any dealer quotations for the security are available; and (iii) possible valuation

methodologies that could be used to determine the fair value of a security.

The

Fund utilizes various methods to measure the fair value of most of its investments on a recurring basis. GAAP establishes a hierarchy

that prioritizes inputs to valuation methods. The three levels of input are:

Level

1 – Unadjusted quoted prices in active markets for identical assets and liabilities that the Fund has the ability to access.

Level

2 – Observable inputs other than quoted prices included in level 1 that are observable for the asset or liability, either directly

or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments,

interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data.

Level

3 – Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing

the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability, and would be based

on the best information available.

The

availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example,

the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics

particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the

market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value

is greatest for instruments categorized in Level 3.

The

inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes,

the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest

level input that is significant to the fair value measurement in its entirety.

The

inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

The following tables summarize the inputs used as of February 28, 2026, for the Fund’s assets and liabilities measured at fair value:

| High

Income Muni |

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

|

|

|

| Assets* |

|

Level 1 |

|

|

Level 2 |

|

|

Level 3 |

|

|

Total |

|

| Convertible

Preferred Stocks |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

| Corporate

Bonds |

|

|

— |

|

|

|

— |

|

|

|

5,025,000 |

|

|

|

5,025,000 |

|

| Municipal

Bonds |

|

|

— |

|

|

|

— |

|

|

|

411,817 |

|

|

|

411,817 |

|

| Total |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

5,436,817 |

|

|

$ |

5,436,817 |

|

It

is the Fund’s policy to recognize transfers into and out of Levels at the end of the reporting period.

|

* |

Refer to the Schedules of Investments

for industry or category classifications. |

The

following is a reconciliation of Level 3 assets in the High Income Fund for which significant unobservable inputs were used to determine

fair value:

| |

|

Investment |

|

| |

|

in Securities |

|

| Balance as of August 31, 2025 |

|

$ |

6,686,817 |

|

| Accrued discounts/premiums |

|

|

— |

|

| Realized gain (loss) |

|

|

— |

|

| Change in net unrealized appreciation/depreciation |

|

|

— |

|

| Paid-in-kind interest |

|

|

— |

|

| Net purchases (sales) |

|

|

(1,250,000 |

) |

| Transfers into and/or out of Level 3 |

|

|

— |

|

| Balance as of February 28, 2026 |

|

$ |

5,436,817 |

|

| |

|

|

|

|

| Change in unrealized appreciation/depreciation during the period

for Level 3 investments held at February 28, 2026 |

|

$ |

— |

|

| EASTERLY

ROCMUNI HIGH INCOME MUNICIPAL BOND FUND |

| NOTES TO FINANCIAL

STATEMENTS |

| Six Months Ended

February 28, 2026 (Unaudited)(Continued) |

The

Level 3 investments as of February 28, 2026 for the High Income Fund represented 59.7% of the Fund’s net assets.

The

following provides information regarding the valuation techniques, unobservable inputs used, and other information related to the fair

value of Level 3 investments for the High Income Fund as of February 28, 2026:

| |

|

|

|

Fair Value as |

|

|

|

|

|

|

|

|

|

| |

|

|

|

of February 28, |

|

|

|

|

Unobservable |

|

|

|

Weighted |

| Security Description |

|

Security Type |

|

2026 |

|

|

Valuation Technique |

|

Input* |

|

Range |

|

Average |

| Conivival Funding 2022 III, LLC

12.00%, 11/15/56 |

|

Corporate Bond |

|

|

5,025,000 |

|

|

Expected Recovery |

|

Collateral Value |

|

100.0% |

|

N/A |

| Next Renewable Fuels - Series A |

|

Convertible Preferred Stock |

|

|

— |

|

|

Expected Recovery |

|

Collateral Value |

|

0.0% |

|

N/A |

| Sunland Medical Foundation 12.00%, 4/01/26 |

|

Municipal Bond |

|

|

411,817 |

|

|

Liquidation Approach |

|

Recovery Rate |

|

5.0% |

|

N/A |

Significant

increases and decreases in the unobservable inputs used to determine fair value of Level 3 assets could result in significantly higher

or lower fair Value measurements. An increase to the unobservable input would result in an increase to the fair value. A decrease to the

unobservable input would have the opposite effect.

(b)

Federal Income Tax

As

of the end of the reporting period, the Fund no longer qualifies as a regulated investment company as it liquidates its assets. For any

taxable period in which the Fund does not qualify under the Subchapter M requirements, the Fund would be taxed as a corporation on any

income or gain.

The

Fund recognizes the tax benefits of uncertain tax positions only when the position is “more likely than not” to be sustained

assuming examination by tax authorities. Management has reviewed the tax positions taken on its 2023-2025 returns and expected to be taken

in the Fund’s 2026 returns and concluded that no liability for unrecognized tax benefits should be recorded related to uncertain

tax positions. The Fund identifies its major tax jurisdictions as U.S. Federal and foreign jurisdictions where the Fund makes significant

investments. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statements

of Operations. During the six months ended February 28, 2026, the Fund did not incur any interest or penalties.

(c)

Security Transactions and Other Income

Security

transactions are reflected for financial reporting purposes as of the trade date. Dividend income is recognized on the ex-dividend date,

and interest income is recognized on an accrual basis including premium amortized and discount accreted. All paydown gains and losses

are classified as interest income in the accompanying Statements of Operations in accordance with U.S. GAAP. Discounts and premiums on

securities purchased are accreted and amortized, over the lives of the respective securities with a corresponding increase/decrease in

the cost basis of that security using the yield to maturity method, or where applicable, the first call date of the security. Realized

gains or losses from sales of securities are determined by comparing the identified cost of the security lot sold with the net sales proceeds.

Withholding taxes on foreign dividends have been provided for in accordance with the Trust’s understanding of the applicable country’s

tax rules and rates.

(d)

Dividends and Distributions

The

following table summarizes each Fund’s intended dividend and capital gain declaration policy:

| |

|

Income |

|

Capital |

| Fund |

|

Dividends |

|

Gains |

| High Income Muni |

|

Daily |

|

Annually |

The

Fund records dividends and distributions to its shareholders on the ex-dividend date. The amount of dividends and distributions from net

investment income and net realized gains are determined in accordance with federal income tax regulations, which may differ from GAAP.

These “book-tax” differences are either permanent or temporary in nature. To the extent these differences are

| EASTERLY

ROCMUNI HIGH INCOME MUNICIPAL BOND FUND |

| NOTES TO FINANCIAL

STATEMENTS |

| Six Months Ended

February 28, 2026 (Unaudited)(Continued) |

permanent

in nature, such amounts are reclassified within the net asset accounts based on their federal tax-basis treatment; temporary differences

do not require reclassification. To the extent dividends and distributions exceed current and accumulated earnings and profits for federal

income tax purposes, they are reported as distributions of paid-in-surplus or tax return of capital. These reclassifications have no effect

on net assets, results from operations or net asset value per share of each Fund.

(e)

Allocation of Expenses

Expenses

of the Trust that are directly identifiable to a specific fund are charged to that fund. Expenses incurred by the Trust that do not relate

to a specific Fund of the Trust are allocated to the individual Fund on an equal basis or another reasonable basis.

(f)

Indemnification

The

Trust indemnifies its Officers and Trustees for certain liabilities that may arise from the performance of their duties to the Trust.

Additionally, in the normal course of business, the Fund enters into contracts that contain a variety of representations and warranties

and which provide general indemnities. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future

claims that may be made against the Fund that has not yet occurred. However, based on experience, the risk of loss due to these warranties

and indemnities appears to be remote.

(g)

Other

The

preparation of the financial statements in accordance with accounting principles generally accepted in the United States of America requires

management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results

could differ from those estimates.

Investment

and Market Risk. An investment in the Fund’s common shares is subject to investment risk, including the possible loss of the

entire principal amount invested. The value of the Fund’s securities, like other market investments, may move up or down, sometimes

rapidly and unpredictably due to changes in general market conditions, economic trends or events that are not specifically related to

the issuer of the security or other asset, or factors that affect a particular issuer or issuers, exchange, country, region, market, industry,

group of industries, sector or asset class. Social, political, economic and other conditions and events (such as war, natural disasters,

epidemics and pandemics, terrorism, supply chain disruptions, trade disputes, economic sanctions, imposition of tariffs, elevated of government

debt, recessions, a government shutdown, conflicts and social unrest) could have significant impacts on issuers, industries, governments

and other systems, including the financial markets. As global systems, economies and financial markets are increasingly interconnected,

events that once had only local impact are now more likely to have regional or even global effects.

|

2. |

MANAGEMENT FEE, ADMINISTRATION

FEE AND OTHER TRANSACTIONS WITH AFFILIATES |

(a)

Easterly Investment Partners LLC acts as investment manager for the Fund pursuant to the terms of a Management Agreement with the Trust,

on behalf of the Fund (the “Management Agreement”). Under the terms of the Management Agreement, the Manager manages

the investment operations of the Fund in accordance with the Fund’s respective investment policies and restrictions. Easterly Investment