As filed with the Securities and Exchange Commission on May 11, 2026.

Registration No. 333‑

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT UNDER

THE SECURITIES ACT OF 1933

INNIO Holding GmbH*

(Exact name of registrant as specified in its charter)

|

|

|

Germany |

3621 |

Not Applicable |

(State or other jurisdiction of incorporation or organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

|

|

Nymphenburger Strasse 5 80335 Munich Germany +49.89.89.82.7221 |

1101 W. St. Paul Ave. Waukesha, WI 53188 +1.262.547.3311 |

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

INNIO Holding Inc.

1101 W. St. Paul Ave.

Waukesha, WI 53188

+1.262.547.3311

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

|

|

|

Marc D. Jaffe Ian D. Schuman Oliver Seiler Jennifer M. Gascoyne Latham & Watkins LLP 1271 Avenue of the Americas New York, NY 10020 (212) 906-1200 |

Paul van der Bijl

NautaDutilh N.V. Beethovenstraat 400

1082 PR Amsterdam The Netherlands +31 20 717 1000 |

Rod Miller David Dixter Philipp Klöckner Milbank LLP 55 Hudson Yards New York, NY 10001 (212) 530-5000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box: ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

|

|

|

Large accelerated filer |

☐ |

Accelerated filer |

☐ |

Non-accelerated filer |

☒ |

Smaller reporting company |

☐ |

|

|

Emerging growth company |

☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 7(a)(2)(B) of the Securities Act. ☐

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

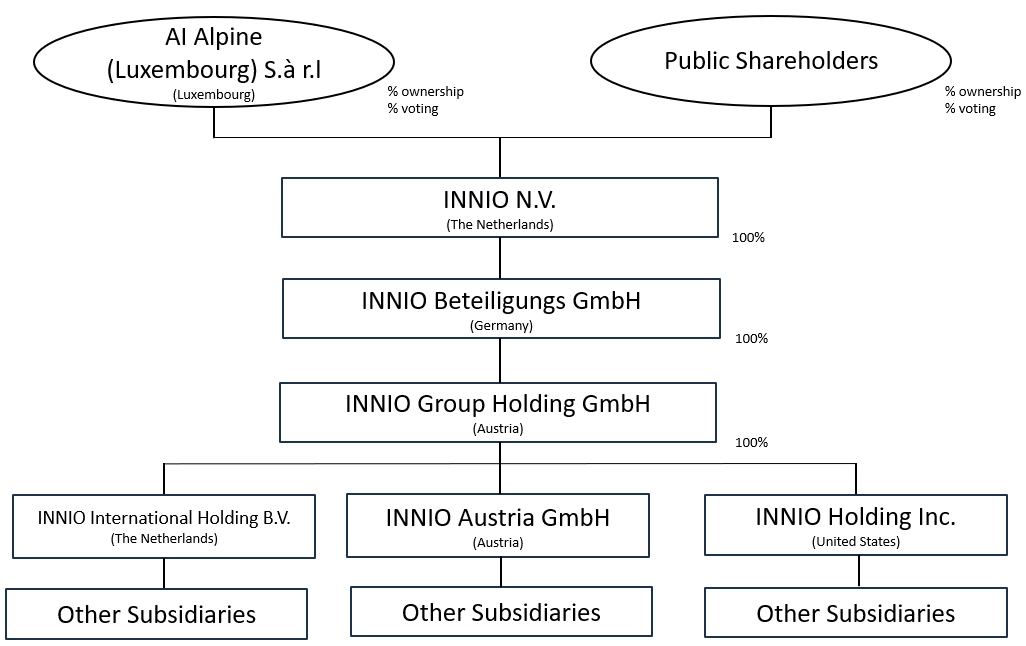

(*) We intend to convert the legal form of our company from a German limited liability company (Gesellschaft mit beschränkter Haftung) to a Dutch private company with limited liability (besloten vennootschap met beperkte aansprakelijkheid) and then to a Dutch public company (naamloze vennootschap) under Dutch law and to change our name from INNIO Holding GmbH to INNIO Group Holding B.V. and then to INNIO N.V. prior to the closing of this offering.

The information contained in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, Dated , 2026

PRELIMINARY PROSPECTUS

Common Shares

INNIO Holding GmbH

to be converted into and renamed

INNIO N.V.

This is the initial public offering of the common shares of INNIO Holding GmbH (to be converted into and renamed INNIO N.V.). We are offering common shares, nominal value EUR per common share. The selling shareholders identified in this prospectus are selling common shares. We will not receive any proceeds from the sale of the common shares by the selling shareholders in this offering.

Prior to this offering, there has been no public market for our common shares. It is currently estimated that the initial public offering price will be between $ and $ per common share.

We have applied to list our common shares on the Nasdaq Global Select Market (“Nasdaq”) under the symbol “INIO.”

Immediately following the completion of this offering, AI Alpine (Luxembourg) S.à r.l. (our “Principal Shareholder”), which will be a selling shareholder in this offering, will hold an aggregate of common shares, representing approximately % of the voting power of our outstanding share capital, assuming no exercise of the underwriters’ option to purchase additional common shares. As a result, following this offering we will be a “controlled company” within the meaning of the corporate governance rules of Nasdaq. For additional information, see the section titled “Management—Controlled Company.”

Investing in our common shares involves risks. See the section titled “Risk Factors” beginning on page 26 to read about factors you should consider before deciding to invest in our common shares.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

|

|

|

|

|

|

|

|

|

Per Share |

|

Total |

Initial public offering price |

|

$ |

|

|

$ |

|

Underwriting discounts and commissions(1) |

|

$ |

|

|

$ |

|

Proceeds to us, before expenses |

|

$ |

|

|

$ |

|

Proceeds to the selling shareholders, before expenses |

|

$ |

|

|

$ |

|

(1) See the section titled “Underwriting” for a description of the compensation payable to the underwriters.

The selling shareholders have granted the underwriters an option to purchase up to an additional common shares from them at the initial public offering price, less underwriting discounts and commissions. We will not receive any proceeds from the sale of such additional common shares by the selling shareholders.

The underwriters expect to deliver the shares against payment in New York, New York on or about , 2026.

|

|

|

Joint Lead Bookrunning Managers |

Goldman Sachs & Co. LLC* |

J.P. Morgan* |

Morgan Stanley* |

Bookrunners |

BofA Securities |

Barclays |

Citigroup |

|

|

|

|

|

Baird |

BNP PARIBAS |

Deutsche Bank Securities |

RBC Capital Markets |

UBS Investment Bank |

Co-Managers |

|

|

|

Credit Agricole CIB |

Erste Group |

UniCredit |

|

|

Academy Securities |

Drexel Hamilton |

*listed in alphabetical order

Prospectus dated , 2026

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by or on behalf of us that we have referred to you. Neither we, the selling shareholders, nor the underwriters have authorized anyone to provide you with additional or different information. If anyone provides you with additional, different or inconsistent information, you should not rely on it. Offers to sell, and solicitations of offers to buy, our common shares are being made only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common shares. Our business, financial condition, operating results and prospects may have changed since such date.

For investors outside the United States: Neither we, the selling shareholders, nor any of the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside of the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, this offering of our common shares and the distribution of this prospectus outside of the United States.

About this Prospectus

Prior to the closing of this offering, we will complete a corporate reorganization described in more detail under “Corporate Reorganization,” in the course of which we will be converted into a Dutch private company (besloten vennootschap met beperkte aansprakelijkheid), and our legal name will change to INNIO Group Holding B.V. We will then be converted into a public company under Dutch law (naamloze vennootschap), and our legal name will change to INNIO N.V. (the “Reorganization”).

As used in this prospectus, unless the context otherwise indicates, any reference to the “Group,” “INNIO,” “our Company,” “us,” “we,” and “our” refers to (i) INNIO Holding GmbH, incorporated under the laws of Germany, together with its consolidated subsidiaries, prior to the completion of its conversion into INNIO Group Holding B.V. (the “Conversion”), (ii) INNIO Group Holding B.V. together with its consolidated subsidiaries, as of the completion of the Conversion and (iii) INNIO N.V. and its consolidated subsidiaries after the completion of the Reorganization.

Certain monetary amounts, percentages and other figures included in this prospectus have been subject to rounding adjustments. Percentage amounts included in this prospectus have not in all cases been calculated on the basis of such rounded figures, but on the basis of such amounts prior to rounding. For this reason, percentage amounts in this prospectus may vary from those obtained by performing the same calculations using the figures in our consolidated financial statements included elsewhere in this prospectus. Certain other amounts that appear in this prospectus may not sum due to rounding.

Financial information presented in parentheses denotes the negative of such number presented. A dash (“–”) signifies that the relevant figure is not available or zero, while a zero (“0.0”) signifies that the relevant figure has been rounded to zero.

Compression metrics in this prospectus have been converted from horsepower to megawatts for consistency across metrics.

Basis of Presentation

Except as otherwise disclosed in this prospectus, the historical consolidated financial statements, the summary historical consolidated financial data and the other financial information included elsewhere in this prospectus have been prepared in U.S. dollars in accordance with accounting principles generally accepted in the United States (“GAAP”). This historical financial information does not give effect to this offering.

Glossary of Certain Terms

AI infrastructure. The combination of high-performance computing, networking and storage components that collectively enables the development and deployment of AI models.

AI workloads. The computing tasks specifically related to artificial intelligence applications. These include activities such as training machine learning models, running inference (making predictions with trained models), processing large datasets, natural language processing, computer vision and other AI-driven tasks. AI workloads typically require significant computational resources, often using specialized hardware like GPUs to handle complex calculations efficiently.

Backup power. A secondary source of electricity that automatically activates when the primary power supply fails, ensuring power supply for critical equipment and systems during outages.

Baseload. The minimum level of electricity demand that a power grid must continuously meet.

Behind-the-meter. Power generation equipment or energy systems that are installed on the customer's side of the electric utility meter, allowing the customer to generate and consume electricity on-site without relying on the public grid.

Capital expenditures. The sum of the additions to property, plant and equipment and additions to intangible assets over a given period.

Colocation operator. A third-party company that owns and manages data center facilities, renting out space, power, cooling and security to other businesses. They provide the infrastructure to host client-owned servers, enabling companies to reduce IT overhead, improve security and ensure high uptime.

Combined heat and power (“CHP”). A system that simultaneously generates electricity and useable heat from the same energy source.

Compute. The processing power required to execute software tasks and applications, such as running AI workloads, and typically provided by GPUs, CPUs or other specialized chips.

Conversions, modifications and upgrades (“CM&U”). Service activities that convert, modify or upgrade existing equipment to improve performance or extend life.

Digital-twin. A virtual replica of a physical asset, such as an engine or power generation system, that uses real-time data and simulation to monitor performance, predict maintenance needs and optimize operations.

Distributed power generation. Electricity generation that occurs at or near the point of use, rather than at a large, centralized facility.

Energy-as-a-Service (“EaaS”). A business model where customers pay for energy services rather than purchasing equipment directly.

Equipment Order Backlog. Equipment Order Intake that has not yet been fulfilled towards the customer. Equipment Order Backlog is measured as of the end of a given period.

Equipment Order Intake. The booking of a new sales order for our Equipment segment within a given year when specific criteria are met, including a signed contract, defined scope, fixed price, delivery schedule, and fully defined terms and conditions. The order must have a low probability of cancellation, all necessary approvals and risk reviews completed, and any required down payment (if any) received. Equipment Order Intake is measured over a given period.

Firm capacity. The uninterruptible and reliable amount of energy, utility or production output that a provider promises to deliver at any given time, regardless of conditions.

Full-time equivalent (“FTE”). Each of our employees or employees of record, which are employees hired on behalf of us by a third-party organization, excluding interns, contractors, apprentices, passive employees and employees on leaves of absence.

Genset. A generator set. A self-contained unit including an engine and an electrical generator.

Graphics Processing Unit (“GPU”). A type of processor optimized for parallel data processing, widely used in graphics rendering and high-performance computing tasks. GPUs are built on underlying design architectures that define how the GPU will operate, including its processing cores, memory systems, data pathways and features.

Grid balancing/grid firming/firming. The continuous process of matching electricity supply with demand across the power grid, often achieved by adjusting the output of flexible power sources like gas engines to maintain stable grid frequency and voltage.

Hyperscaler. A cloud provider or technology company that is capable of delivering computing infrastructure and services at massive scale, typically through large data centers and geographically distributed networks.

In-front-of-the-meter. Power generation equipment or energy systems that are installed on the utility’s side of the electric meter and connected directly to the public grid, typically delivering electricity to multiple customers or the wholesale power market.

Independent power producer (“IPP”). A non-utility company that owns and operates power generation facilities and sells the electricity it produces to utilities, end users or into wholesale markets but typically does not own or operate the transmission or distribution grid.

Installed base. All active Jenbacher and Waukesha engines with their corresponding power output, measured in gigawatts (“GW”). Active is defined as operationally available for the customer without implying any operational running profile. Active excludes all inactive engines (i.e. engines on stock or not yet commissioned, engines decommissioned) and all engines owned or controlled by customers for whom the provision of services is restricted or prohibited where we are unable to deliver the full service scope.

Islanded. A mode of operation in which a power generation system operates independently from the main electric grid, providing electricity to a localized area or facility without any grid connection.

Microgrid. A localized group of electricity sources and loads that can disconnect from the traditional grid.

N+x. A measure of redundancy in power or cooling systems where “N” represents the capacity needed to meet operational requirements and “x” represents the number of additional backup units available to take over if one or more primary units fail.

Peaking. Power generation that operates during periods of highest electricity demand, typically for short durations, to supplement baseload power and prevent grid shortages.

Power Delivered. The aggregate electrical power output, measured in GW, of engines/gensets for which revenue has been recognized in the relevant period. Specifically, Power Delivered is calculated as the sum across all delivered units of the nameplate electrical output, measured in megawatts (“MW”) of each engine/genset multiplied by the respective quantity recognized. For our compression business line, Power Delivered is calculated by converting horsepower output into megawatts. Power Delivered is measured over a given period.

Prime power. A power system designed to serve as the primary and continuous source of electricity for a facility, operating for extended or unlimited periods rather than as a backup solution.

Time-to-power. The total duration required to move a new electricity generation asset from conception to full commercial operation.

Workloads. The computational tasks or applications, such as training AI models or running inference, that consume resources like GPUs, memory and storage in a computing environment.

MARKET, INDUSTRY, AND OTHER DATA

This prospectus contains estimates, projections and information concerning our industry, including the size of the markets in which we participate, that are based on various third-party sources, industry publications and reports, as well as our own internal information.

This information involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates and information. The markets in which we operate are subject to a high degree of uncertainty and risk due to a variety of factors, including those described in the section titled “Risk Factors.” These and other factors could cause results to differ materially from those expressed in these sources, publications, and reports.

Certain information in the text of this prospectus is contained in publicly available reports, as well as third-party sources, including:

•BCG, Energy Demand from Compute November 2025 Update Whitepaper (“BCG Whitepaper”).

•BloombergNEF, New Energy Outlook 2025 Report (“BloombergNEF”).

•Center for Strategic and International Studies, Powering the Commanding Heights: The Strategic Context of Emergent U.S. Electricity Demand Growth, October 2024 (“CSIS”).

•CoreSite, Breaking Down Data Center Tier Level Classifications (“CoreSite”).

•datacenterhawk, data center market intelligence platform (“Datacenter Hawk”).

•Datacenters.com Energy, Data Center Construction in 2025: Permitting, Power, and Pitfalls to Avoid, October 2025 (“Datacenters Energy”).

•Enverus, 2026 Interconnection Queue Outlook & ISO Market Trends (“Enverus”).

•EMBER, Grids for Data Centers in Europe, June 2025 (“EMBER”).

•The International Energy Agency, Renewables 2025 Analysis and forecasts to 2030, October 2025 (“IEA Forecast Report”) and Energy Employment has Surged, but Growing Skills Shortages Threaten Future Momentum, December 2025 (“IEA Report”).

•Jaime Sevilla et al. (2024), "Can AI scaling continue through 2030?". Published online at epoch.ai. (the “Epoch AI Analysis”).

•JLL, 2026 Global Data Center Outlook, Navigating AI Demand, Power Constraints and Global Opportunities in 2026 (“JLL”).

•North American Electric Reliability Company (“NERC”), Characteristics and Risks of Emerging Large Loads, Large Load Tasks Force White Paper, July 2025 and 2024 Summer Reliability Assessment, May 2024 (“NERC Reports”).

•Oxcap Analytics, Power Generation: The Fourth Cycle (“Oxcap Analytics”).

•Semianalysis, How AI Labs are Solving the Power Crisis: the Onsite Gas Deep Dive, December 2025 (“Semianalysis”).

•Spears & Associates, The Upstream Gas Compression Market: October 2025 (“Spears & Associates”).

•S&P Capital IQ, a financial data and analytics platform provided by S&P Global (“S&P”).

•The U.S. Department of Energy (“DOE”) Report on Evaluating U.S. Grid Reliability and Security, July 2025 (the “DOE Report”) and Fact Sheet: The Department of Energy is Ending the War on Beautiful, Clean Oil, January 2026 (the “DOE Fact Sheet”).

•The U.S. Environmental Protection Agency (“EPA”), CHP’s Role Providing Reliability and Resiliency, December 2025 and CHP Benefits, August 2025 (the “EPA CHP Articles”).

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our common shares, you should carefully read this entire prospectus. In particular, you should carefully read the sections entitled “Risk Factors,” “Special Note Regarding Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated historical financial statements and the accompanying notes included elsewhere in this prospectus.

Overview

We are a leading global distributed energy solutions provider that delivers reliable, flexible, transient, decentralized, modular and efficient power. Our reciprocating gas engines convert gaseous fuels, such as natural, renewable and specialty gases, into electricity and heat or compression for a wide array of critical infrastructure, including the grid, data centers and industrial applications. Our solution portfolio is fully focused on gaseous fuels rather than diesel-based solutions. With an installed base of approximately 44 GW and 3.4 GW of power delivered as of December 31, 2025, compared to an installed base of 42 GW and 2.5 GW of power delivered as of December 31, 2024, our technology platforms have proven themselves for decades in a variety of demanding applications and environments.

We operate through two primary segments: Equipment and Services. Our Equipment segment addresses the data center, power solutions and compression end-markets through our modular, flexible and highly efficient engine-based solutions, providing high quality power characteristics for their applications. In our data center business line, our modular, high-efficiency systems are ideally positioned to deliver the prime and backup power required to sustain intensive artificial intelligence (“AI”) workloads. By minimizing the complex auxiliary subsystems often required by alternative power sources, our technology offers a scalable, capital efficient behind-the-meter solution specifically optimized for rapid data center deployment. Our power solutions provide baseload and peaking power to stabilize utility grids (in-front-of-the-meter) and power independent microgrids (behind-the-meter). Our compression solutions support the full energy value chain, including gas lift, gathering, processing, storage and transmission, enabling efficient gaseous fuel transport. These solutions are mission critical and non-discretionary; our systems help our customers maintain operational continuity, generate electricity and produce oil and natural gas. As the backbone of resilient energy infrastructure, our equipment and services enable operators to mitigate grid capacity shortfalls and reduce reliance on unstable centralized power and intermittent renewables.

Our sizable and growing installed base drives our Services segment, as our gas engine solutions require regular maintenance and replacement of parts to deliver reliable performance. The proprietary design of many critical components positions us to capture a substantial majority of the life cycle service and parts opportunity. Given the critical role our equipment plays in our customers’ operations, we have strong uptake of, and a steady demand for, our support and maintenance offerings. For customers seeking long-term certainty of maintenance costs, we offer multi-year service agreements, which can extend to ten years or more. We also offer upgrades and overhaul services, which substantially extend the life of our engines. Supported by an internal service team of over 1,600 specialists as of March 31, 2026, our Services segment generates highly predictable, recurring and high-margin revenue streams. This near-captive aftermarket business underpins a compounding business model characterized by a virtuous cycle of equipment placement, service attachment and long-term customer loyalty. The expected growth of our installed base and our aftermarket exposure provide significant Services revenue visibility extending well beyond 2030.

The table below gives an overview of our two segments, Equipment and Services, Equipment Order Intake and our revenue, along with customer types and use cases.

|

|

|

|

|

|

Equipment |

Services |

|

Data Center |

Power Solutions |

Compression |

|

LTM Q1 2026 Equipment

Order Intake (% of LTM Total Equipment Order Intake) |

$2,979M (61%) |

$1,522M (31%) |

$348M (7%) |

N/A |

LTM Q1 2026 Revenue

(% of LTM Total Revenue)

|

$317M (11%) |

$946M (34%) |

$215M (8%) |

$1,334M (47%) |

Customers |

•Energy-as-a-Service providers |

•Data center co-located

power generation |

•Exploration &

production companies •Oil companies (international and national) |

•Same customers as Equipment

segment |

Use Cases |

•Behind-the-meter

prime power •Behind-the-meter

backup power |

•Decentralized behind

the meter •Heat and power application |

|

•Minor overhaul (approx. 30-40k operating hours) •Major overhaul (approx. 60-80k operating hours) •Long-term service agreements |

Our global manufacturing footprint spans more than seven million square feet of land, anchored by production hubs in Austria (Jenbach, Hall, Kapfenberg) and North America (Welland, Ontario, Canada; Waukesha, Wisconsin, USA; Waller, Texas, USA and Trenton, New Jersey, USA) as of March 31, 2026. We have strengthened our North American footprint, including targeted investments in U.S. manufacturing and assembly capacity, to support growing demand for distributed and behind-the-meter power solutions and to improve proximity to key data center development regions. These facilities enable localized production and testing, shorter lead times and increased capacity and flexibility, supporting projects that need power quickly. We have global coverage across approximately 100 countries, as of March 31, 2026, through a robust commercial network that integrates direct sales, authorized distributors and channel partners, packagers and strategic key accounts. This extensive global reach, combined with our localized service capabilities, ideally positions us to effectively capture the growing demand for our energy solutions.

Although the Jenbacher and Waukesha brands possess a rich heritage established within major industrial conglomerates, our trajectory accelerated in 2018 when Advent International (“Advent”) carved out the businesses from General Electric Company (“GE”) to form INNIO as a standalone entity. In 2023, we further strengthened our capital base when Luxinva S.A. (“Luxinva”), a wholly owned subsidiary of the Abu Dhabi Investment Authority (“ADIA”), acquired a significant minority stake. Our Principal Shareholder is co-owned by funds managed by Advent and ADIA. For further information on our organizational history, see “—Organizational History.” Following our separation from GE, we have delivered record performance by enhancing our operational agility, digital capabilities and technological leadership. We have specifically focused on high-growth opportunities through substantial investments in our U.S. manufacturing infrastructure, targeted research and development (“R&D”), containerized solutions and service distribution network. With approximately 5,200 full-time equivalents (“FTEs”) as of March 31, 2026, our team is united by a vision to deliver the mission-critical power required for the economy’s vital operations.

For the three months ended March 31, 2026, we had an Equipment Order Intake (as defined in “Summary Historical Consolidated Financial and Other Data—Key Operating Metrics and Non-GAAP Financial Measures”) of $1,617.5 million (resulting in a 147.7% period-over-period increase, from $652.8 million for the three months ended March 31, 2025), $668.6 million in revenue (resulting in a 35.3% period-over-period increase from $494.0 million for the three months ended March 31, 2025), net loss of $9.0 million (reflecting a 125.7% period-over-period change from a net income of $35.0 million for the three months ended March 31, 2025) and an Adjusted EBITDA of $122.5 million (reflecting a 7.5% period-over-period increase from $114.0 million for the three months ended March 31, 2025).

For the year ended December 31, 2025, we had an Equipment Order Intake of $3,884.0 million (resulting in a 187.8% year-over-year increase, from $1,349.6 million for the year ended December 31, 2024), $2,636.8 million in revenue (resulting in a 22.1% year-over-year increase from $2,159.1 million for the year ended December 31, 2024), net income of $141.8 million (reflecting a 54.1% year-over-year increase from $92.0 million for the year ended December 31, 2024) and an Adjusted EBITDA of $549.0 million (reflecting a 19.4% year-over-year increase from $459.9 million for the year ended December 31, 2024). See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Non-GAAP Financial Measures” for a reconciliation of Adjusted EBITDA to net income.

Our Markets

Global power demand is entering a new growth phase, driven by a step-change in electricity consumption from data centers to enable the AI revolution, alongside broader electrification across industrial, commercial and residential end markets. Based on third-party research, we estimate that the average annual growth in electricity consumption across the US and Europe will step up from 0.3% from 2010 to 2025, to 1.6%, from 2025 to 2035, resulting in an incremental annual consumption of around 1.2 billion MWh.

AI-driven compute workloads are particularly power intensive, continuous and highly concentrated, requiring not just increased power, but a differentiated power, distinguished by high-quality capacity with fast start capability, strong transient response and the ability to manage rapid load fluctuations. As a result, data centers account for a disproportionate share of incremental load growth and are reshaping requirements for power supply at the gigawatt scale with global data center power demand expected to grow by around 14% to 18% per annum over the next five years according to JLL and Company estimates based on third-party sources.

At the same time, grid reliability and availability have become binding constraints. Years of underinvestment in generation, transmission and distribution infrastructure, combined with permitting complexity, interconnection queues and skilled-labor shortages, have extended time-to-power to multiple years in many regions. According to

Enverus and EMBER, the average interconnection queue in the U.S. and key European countries now exceeds six years.

Rapid growth in large, concentrated loads, most notably data centers, has outpaced grid expansion, creating localized supply and demand imbalances that existing networks are structurally unable to absorb. Rising renewable penetration further increases system volatility, structurally elevating the need for firming and balancing capacity.

As a result, governments and regulators are increasingly intervening to protect residential consumers and incumbent industries from reliability risks and rising system costs associated with large, concentrated electricity loads. These interventions include connection moratoria, explicit load caps, curtailment obligations, large-load tariff structures and requirements for on-site or dedicated power supply.

These measures reflect growing recognition that existing grids are increasingly constrained. According to the DOE Fact Sheet, the U.S. power system is not positioned to sustain the combined impact of coal and other plant retirements, increasing reliance on intermittent generation sources such as wind and solar, and rapid growth in data center demand, underscoring the urgency of adding new dispatchable and locally available power capacity. The utility of behind-the-meter power generation is growing as U.S. interconnection rates have slowed in recent years. The miles of transmission lines added per year would require a multiple-fold increase to meet the required average build rate to comply with DOE 2030 or 2035 targets, according to our estimates based on third-party reports.

In this environment, certainty and speed of power delivery are central to project success and help to shift power generation from a basic utility to a strategic asset. Behind-the-meter power solutions are increasing sharply in share and are becoming a permanent component of data center and industrial power architectures rather than a temporary bridge to grid connection. These behind-the-meter solutions directly address availability, reliability and performance requirements, while mitigating regulatory risk and preserving long-term optionality as grid conditions evolve. Together, these dynamics are driving sustained demand for distributed, fast-ramping and highly reliable gas-based solutions across our end markets.

As dispatchable generation becomes essential for reliability and firming, natural gas gains importance in the power mix due to its scalability, availability and flexibility. Growing gas-fired generation, expanding liquified natural gas (“LNG”) exports and higher utilization of existing pipeline infrastructure are increasing compression intensity across the value chain, particularly as maturing fields and higher throughput require more frequent and higher-performance compression. As a result, demand for efficient, reliable compression equipment and services is structurally supported by the same trends driving growth in data centers and distributed power generation.

Within the broader power market, data centers represent one of the fastest-growing and most power-intensive end markets. Power availability has emerged as a binding constraint on computation growth and AI advancement, directly limiting the pace at which large-scale compute capacity can be deployed. Power constraints are expected to become a key factor restricting data center operators from deploying capacity and expanding on AI training capabilities, stifling growth earlier and more acutely than other potential supply chain limitations such as chip production. For example, Epoch AI Analysis estimates that by 2030, the power demand implied by available computing chips could exceed available power generation capacity by approximately four to five times. In this environment, timely access to reliable, scalable power is becoming a decisive factor in determining how quickly more capable AI models can be trained and deployed and, ultimately, a critical determinant of who can remain competitive in the global development of advanced AI systems.

As AI-driven load growth accelerates, existing transmission and distribution networks, which have been severely underinvested for decades, are increasingly unable to absorb large, concentrated demand. Consequently, grid availability and time-to-power have become binding constraints in many regions. In response, the adoption of behind-the-meter power is growing significantly faster than overall data center capacity, with the penetration of behind-the-meter and hybrid solutions in new-build projects expected to expand from around 10-20% in 2025 to around 50-60% by 2030, according to the DOE Report and Oxcap Analytics, as operators prioritize supply certainty, deployment speed and insulation from grid constraints.

As a result, we believe we are well positioned in the disproportionately fast-growing data center power end-market. Our focus on flexible, dispatchable, behind-the-meter gas power generation aligns with multiple, layered demand drivers: rapid growth in overall data center electricity consumption, a rising share of new capacity requiring dedicated prime power and an increasing preference for such prime power to be deployed on-site or in hybrid configurations. As these trends compound, the addressable market for modular, rapidly deployable, behind-the-meter solutions is expanding materially faster than data center power demand overall, which we believe allows us to benefit from growth on top of growth as power architectures evolve.

This structural shift is underpinned by accelerating legislative momentum supporting decentralized generation. This trend was pioneered in Europe by Ireland’s Commission for Regulation of Utilities (the “CRU”), which first required on-site generation for data centers in November 2021. This regulatory trajectory was further cemented by the CRU’s recent December 2025 decision, which reinforced and expanded mandates for dispatchable, on-site power to mitigate grid instability. This legislative pivot has also gained momentum in the United States, evidenced by the passage of Texas Senate Bill 6 and evolving guidance from the PJM Interconnection, a regional transmission organization in the United States, both of which establish frameworks to standardize and facilitate co-located loads. In particular, Texas Senate Bill 6 effectively requires large, new power consumers to bring their own firm power or accept the risk of being curtailed. As a result, behind-the-meter power has evolved from a temporary fix into a primary enabler of data center growth globally. This shift also makes gas-based backup solutions more appealing to our data center customers given they are used more often and run longer than our customers would typically expect, becoming more economical and more emissions compliant than diesel-based alternatives.

Data center operators face stringent requirements around reliability, availability, power quality and emissions performance, reflecting the continuous, latency-sensitive nature of AI workloads. Power systems must deliver fast start-up, strong transient response and stable voltage and frequency given that power performance directly impacts server utilization and overall economics. These requirements favor dispatchable, highly transient and power dense solutions that can operate reliably across variable load profiles, support both grid-connected and islanded operation and comply with increasingly stringent emissions standards.

According to S&P, hyperscalers’ capex expectations for 2028 have almost doubled over the last 12 months. While hyperscale campuses are often planned at gigawatt scale, they are typically executed in phased increments, reinforcing the need for modular power solutions that can be deployed rapidly, energized independently and expanded in line with staged compute rollouts. More than 90% of planned data center capacity additions relate to incremental building blocks of up to 200 MW, according to Datacenter Hawk and Datacenters Energy. This development model increases the value proposition of prefabricated, modular power blocks. These standardized units not only compress time-to-power and reduce execution risk but also provide significant operational flexibility, serving as the primary energy source during initial phases with the potential to transition into a permanent backup or peaking role once permanent grid infrastructure is established. Semianalysis has found that, when comparing different power nodes, larger power nodes per unit necessitate a greater redundancy overbuild. This highlights a key advantage of our 5 MW engines for data center campuses, especially when compared to larger power nodes such as 50 MW turbines.

We address these requirements with gas engine-based power solutions deployed in behind-the-meter and hybrid configurations. Our solutions support both primary and backup power applications and are well suited to phased campus development, high-availability architectures and sustained long-duration operation. As data center operators increasingly prioritize speed of deployment, reliability and independence from constrained grids, we believe our solutions directly align with the evolving power architecture of the data center end market.

Power Solutions

Power systems globally are facing accelerating demand growth alongside the tightening availability of firm, reliable energy supply. Electrification of transportation and heat, together with AI-related load growth, is increasing both absolute electricity demand and peak volatility, while coal retirements and rising renewable energy penetration are reducing firm capacity, system inertia and grid stability. Reserve margins have declined to 15-20% in some regions in the United States, underscoring the growing need for flexible, dispatchable generation to support peaking, firming, balancing and grid stability, according to NERC Reports, IEA Report and Company estimates. As power systems become more unpredictable and less stable, value is shifting away from baseload generation toward assets that can start quickly, cycle frequently, provide stability and operate reliably and efficiently under variable load conditions.

Within this context, natural gas is gaining share in power generation as a reliable and scalable fuel, particularly within flexible gas capacity, which is growing materially faster than baseload gas generation due to the operational requirements of renewable-heavy systems. Even under decarbonization and net-zero transition pathways, dispatchable thermal capacity remains critical to complement intermittent renewables and storage, according to the IEA Forecast Report. Flexible gas-based power solutions are therefore expected to grow three to four times faster than other gas-fired capacity between 2025 and 2030, according to BloombergNEF.

Grid constraints, interconnection delays, congestion and multi-year grid modernization timelines are further accelerating the structural adoption of on-site, decentralized and microgrid-based power solutions, which are increasingly viewed as permanent components of future power architectures rather than temporary bridges to grid connection. Demand for power solutions is broad-based, spanning utilities and independent power producers (“IPPs”), commercial and industrial customers, combined heat and power (“CHP”) applications and off-grid and mobile use cases. CHP plays a central role in applications requiring reliable heat and power, particularly where renewable electricity alone cannot meet continuous or high-temperature heat requirements. At the same time, tightening emissions standards and decarbonization objectives are increasing demand for lower-emissions, fuel-flexible and hydrogen-ready solutions capable of supporting biogas, renewable gases and staged hydrogen adoption over time.

We are well positioned to address these market conditions through our portfolio of flexible, dispatchable gas engine-based power solutions. Our platforms are designed for fast start, frequent cycling, high part-load efficiency and reliable operation under variable load profiles, directly aligning with the technical requirements of peaking, balancing, firming and CHP applications in increasingly volatile power systems. Modular, multi-engine architectures enable scalable deployment across utility, microgrid, industrial and on-site configurations, while fuel flexibility and hydrogen-ready capability provide customers with a pathway to comply with tightening emissions standards over time. As a result, our solutions are structurally aligned with fast-growing segments of gas-fired capacity and decentralized power architectures globally.

The same megatrends driving growth in our data center and power solutions business lines, including accelerating electricity demand, tightening reliability requirements and increased reliance on dispatchable generation, are also strengthening the role of natural gas in the global energy system. As a reliable and scalable fuel supporting power generation, industrial demand and energy security, natural gas is seeing rising utilization across global infrastructure, reinforced by the rapid expansion of LNG trade, with U.S. LNG export volumes forecast to grow at approximately 12% per year through 2030 based on currently planned projects, according to Spears & Associates.

Beyond higher volumes, compression demand is supported by structural changes in production and transport. Maturing reservoirs, declining pressures, basin mix shifts toward lower-pressure regions and increasingly complex gathering and pipeline networks are driving higher compression intensity across existing infrastructure. At the same time, aging compression fleets and high utilization levels limit further sweating of assets, necessitating replacement, restaging and incremental additions of compression capacity. Electrification of compression remains constrained by grid availability, permitting timelines and power congestion, particularly in regions experiencing rapid data center-driven load growth, supporting continued reliance on engine-driven solutions.

We address this demand through gas compression solutions deployed across upstream and midstream applications. Our solutions support higher volume and increasing compression needs associated with LNG-linked flows and broader gas infrastructure utilization for power generation, residential and petrochemical end markets. Increased regulatory focus on methane and emissions may further support modernization and upgrade activity across compressor stations.

Our Competitive Strengths

Our position as a trusted global distributed energy platform providing mission-critical applications is underpinned by our distinctive gas engine portfolio, long-standing customer relationships, differentiated technology and a compounding service business model. Unlike nascent technologies with limited operational history, our reciprocating gas engines represent a commercially mature standard known for exceptional reliability and performance. This track record is evidenced by our large installed base of approximately 44 GW as of December 31,

2025, validating our technology on a global scale. Our strengths differentiate us from our competitors and drive growth over time.

Proven Growth Platform Well Positioned to Provide Behind-the-Meter and Co-location Solutions to Data Centers

One of the most prevalent constraints on data center growth is the availability of power sources that can handle AI-driven workload requirements and that can operate in locations without grid connectivity. Our gas engines are ideally positioned for data center use given they address many of the technical challenges facing our customers across the data center ecosystem, especially delivering the power characteristics required for AI workloads. By streamlining the power architecture, our solutions reduce the need for costly auxiliary infrastructure, such as batteries or supercapacitors, thereby driving higher total capex efficiency. We offer behind-the-meter solutions underpinned by modularity and fast three-month deployment timeframe to reduce time-to-power and service campuses of all sizes.

Our high-speed engine platforms, anchored by the up to 5 MW Jenbacher Type 6, are engineered to deliver rapid start-up capabilities and superior part-load efficiency, making them suited to handle large load fluctuations. These engines achieve start-to-first-load in approximately 15 seconds for backup operation and can manage dynamic load swings of 25-40% without requiring extensive battery buffering, all while maintaining strict power quality tolerances, a key value requirement for AI training and inferencing data center workloads.

To accelerate deployment, customers use our engines in pre-engineered containerized solutions scaling up to approximately 25 MW per module. Our units deliver competitive power density with built-in redundancy and “plug-and-play” integration, significantly shortening project timelines and reducing risks associated with implementation. Our systems achieve high electrical efficiency (43-45%) with minimal degradation at partial loads, allowing for N+x configurations, which allow for flexibility and reliability even under partial failure conditions, with lower total redundancy capacity than competing technologies. Notably, our fast start capability enables these assets to serve dual roles: operating as reliable prime power while simultaneously preserving the optionality to switch to backup power or grid-support services in the future. While our engines are already deployed as backup solutions for grid-connected sites today, this flexibility allows customers to monetize unused backup capacity and adapt to evolving regulatory frameworks without compromising availability standards.

Our customer value proposition is characterized by accountability and efficiency. Our go-to-market model and service network have allowed us to streamline execution and maximize accountability with our customer base, including hyperscalers, colocation operators and data center developers. Furthermore, the strength of our customer relationships and service network have allowed us to quickly enhance our product capabilities to meet AI workloads across prime and backup power. Approximately 80% of our data center Equipment Order Backlog as of December 31, 2025 was associated with prime power applications, while the remaining 20% was associated with backup power applications.

Our annual data center Equipment Order Intake increased from $27 million as of December 31, 2023 to $2,282 million as of December 31, 2025 due to the strength of our solutions and quality of our platform. Our data center Equipment Order Intake continued growing through the first quarter and was $1,005 million as of March 31, 2026, compared to $309 million as of March 31, 2025. These orders have included some marquee wins, including our agreement for a multi gigawatt power plant for one of the largest data centers in the world, utilizing our high-efficiency gas engines as the core technology.

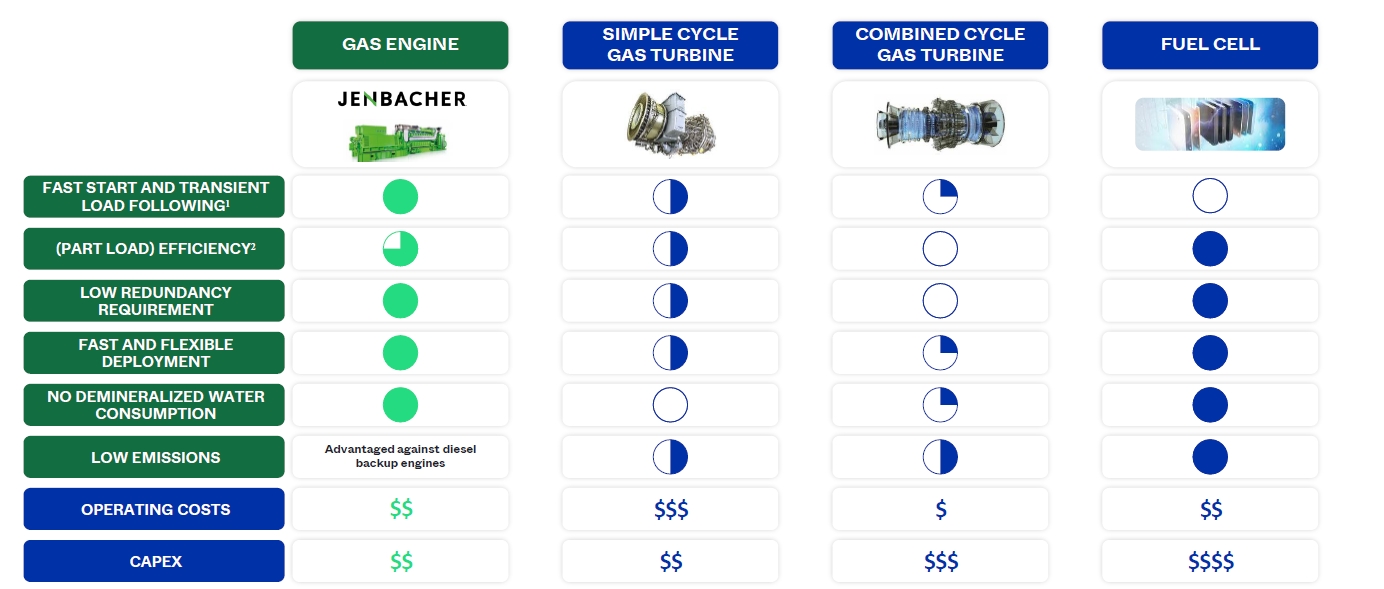

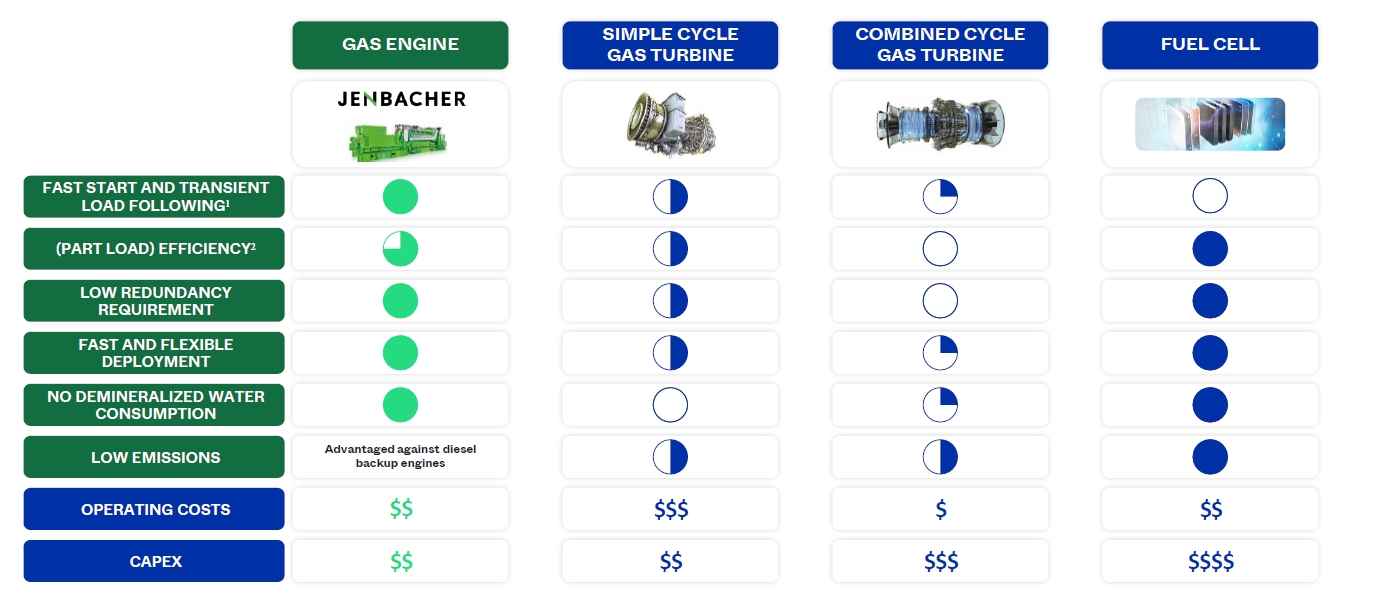

Our behind-the-meter solutions provide a structural cost advantage over grid reliance. Depending on the specific regulatory jurisdiction, grid-related charges, including transmission, capacity and, where applicable, distribution, can alone be equal to the total variable cash operating costs of an on-site INNIO engine once the engine has been installed. This allows our technology to serve as a long-term power solution, rather than a temporary bridge during grid interconnection delays. The chart below illustrates key attributes that underpin our competitive advantage and drive customer adoption of our gas engine solutions over alternative power generation solutions.

Source: Company information and estimates based on third-party sources.

(1)Transient capability refers to the ability to rapidly change power output in response to sudden changes in load or grid conditions while maintaining stable operation.

(2)Part load efficiency is calculated as electrical output divided by fuel energy input at a defined load level. It is commonly assessed by comparing efficiency at 50%, 75% and 100% of rated load to evaluate how performance changes across the operating range.

Established Leadership Position in Gas Engines for Balancing, Firming, CHP and Specialty Gas Applications

Our success in decentralized power generation is rooted in a long-standing focus on gaseous-fuel engine technology and a deliberate concentration on stationary power generation. Unlike diversified engine manufacturers that also serve marine, transportation or off-highway markets, our solutions have been engineered specifically for gas-based power generation and CHP applications.

We distinguish ourselves through deep specialization in gaseous fuels, with engines optimized for natural gas, associated petroleum gas, coal mine gas, biogases, such as landfill and sewage gas, and industrial waste gases. Our engine portfolio spans outputs from 220 kW to 10.6 MW, enabling deployment across a broad range of balancing, firming, CHP and specialty gas applications. All relevant Jenbacher engine platforms are ready to run on 25% hydrogen, and our Type 4 engine is capable of operating on up to 100% hydrogen. Additionally, as of April 15, 2026, our 3 MW Jenbacher engines have been validated to run on 100% hydrogen. This achievement was validated using various AI load profiles and large, rapid load fluctuations to simulate real-world data center conditions, demonstrating that our 3 MW engine can meet the demanding response profiles required for critical data center operations while running on 100% hydrogen.

High start-stop capability, strong part-load efficiency and stable performance under frequent cycling make our engines well suited for balancing and firming applications, which are critically required in power systems facing increasing volatility from renewable penetration. In CHP and district heating applications, modular factory-tested heat exchanger configurations enable customer-specific temperature levels at high total efficiency.

In addition, our engine platforms are designed to accommodate increasing shares of renewable and low-carbon fuels, including hydrogen blends, providing customers with future pathways toward low-carbon operation. This combination of gas specialization, power-focused engineering, operational flexibility and reliability underpins our established leadership position in flexible decentralized power generation.

Top Two Position in Gas Engine Driven Gas Compression with Leading Technology in Gas Compression Applications that have Significant Barriers to Entry

Gas compression applications require equipment that can withstand harsher fuel and ambient conditions compared to other engine applications. Our engines are designed to operate in constantly changing conditions. Our engines’ hardware and controls are extremely flexible to maximize uptime during fuel, load and ambient condition changes. Our rich burn combustion technology provides the widest operating window compared to other engines in the category. This provides customers with the flexibility to deploy our engines in compression applications without modification or adjustment. It also achieves extremely low emissions without requiring expensive and complex exhaust aftermarket treatment systems.

Our engines perform particularly well in high-intensity compression applications characterized by higher pressures and output per unit, making them well suited for evolving field developments where declining gas well counts are offset by increasing production volumes.

Our strategy also aims to minimize the number of service intervals required for the entire compression package. We work to align the maintenance requirements with the compressor by reducing the number of maintenance events needed to keep the equipment operating to promote operational efficiency. We have simplified the digital interface with our equipment to expedite troubleshooting and remote support needed to bring the equipment back to operating condition.

Additionally, our extensive network of distributors and packagers can support sophisticated planned and unplanned maintenance activities. The combination of application-specific design and service access enables our engines to positively influence our customers’ ability to meet their production goals at low operating cost.

Service Capture Enabled by Proprietary, High-Performance Parts and a Global Service Network Drives Highly Profitable Recurring Revenues

The stable operation and availability of our engines are critical to our customers’ operations, making service an essential and structurally defensible component of our business model. Our service offerings are not only reliable but also strengthen customer relationships, generate recurring multi-year Services revenue for us and deliver higher margins, helping mitigate the impact of economic cyclicality.

Our strong Equipment Order Intake continues to expand our active fleet of engines. With approximately 44 GW of installed base as of December 31, 2025, the fleet forms the foundation of a growing and highly visible service business. Given the mission-critical nature of our engines, customers are structurally incentivized to source parts and services directly from us as the original equipment manufacturer (“OEM”). Our Equipment Order Intake is centered around engines at the higher end of our power generation capability portfolio where proprietary components, engine specifications and integrated control systems may make it more expensive to switch providers, as even a single component failure or improper intervention can materially increase the total cost of an outage. As a result, service capture is driven by risk management and operational certainty on top of discretionary customer choice.

Our strong Equipment Order Intake provides Services revenue visibility well beyond 2030, as each newly installed engine enables a long-duration service relationship over its operating life. We deliver services both transactionally and through long-term service agreements (“LSAs”), which can extend to ten years or more, supporting recurring and predictable revenue streams.

To maintain seamless performance and maximize useful life, our engines require comprehensive overhauls at specific operating intervals. We leverage these requisite milestones to deploy next-generation technology upgrades, a process that revitalizes the customer’s asset while driving predictable, accretive revenue growth for our platform. For the majority of the engines in our portfolio, minor overhauls are typically due between 30,000 to 40,000 operating hours. At this stage, key components are exchanged at mid-life. Major overhauls occur after 60,000 to 80,000 operating hours, and significant upgrades to new specifications are made. These major overhauls give the engines

performance upgrades plus second and third working lives, which could extend an engine’s life to over 40 years in some cases.

Our “local-for-local” strategy in direct, strategic markets such as the United States and Germany, enables us to deliver fast, reliable support where it matters most—close to our customers’ operations—and assists us with mitigating our potential exposure to tariffs. By leveraging regional service hubs and local expertise, we minimize downtime and ensure rapid response for products that are critical to our customers’ business continuity. This proximity-driven approach reinforces trust and positions us as a dependable partner in the markets we serve. This has been particularly true in the United States, where, as of March 31, 2026, we have more than doubled service headcount since 2024 to prepare for data center growth.

System Integration and Execution Capability

Our ability to deliver fully integrated, turnkey power systems sets us apart in the distributed energy market. Unlike providers that supply only engines, we offer complete solutions, including generation, controls, containerization and grid interface, designed to meet the most demanding operational requirements. By maintaining our own distribution channels, we achieve superior customer intimacy and a localized presence, enabling us to provide tailored solutions that align with customer requirements. Our execution capabilities extend beyond product delivery. We operate effectively in complex and multi-vendor environments, facilitating seamless integration across diverse project stakeholders. By providing accountability from initial design and engineering through commissioning and lifecycle service, we simplify project management for our customers and reduce execution risk.

This integrated approach shortens time-to-power, a critical advantage for customers operating under tight delivery timelines, such as data centers and industrial facilities facing urgent capacity needs. Our track record in delivering projects on schedule and within scope reinforces our reputation as a trusted partner for mission-critical applications.

We complement these capabilities with a robust network of long-term supply chain and channel partners, enabling reliability and scalability across global markets. This ecosystem enables us to maintain quality standards, accelerate deployment and support customers throughout the asset lifecycle.

Global Manufacturing and Distribution Footprint

We serve our customers through an integrated global footprint spanning approximately seven million square feet of land for manufacturing spaces across North America and Europe, with global direct and indirect coverage across approximately 100 countries, supported by an internal service team of over 1,600 specialists as of March 31, 2026.

Our production capabilities are anchored by major manufacturing hubs on both sides of the Atlantic. In Europe, our Jenbach, Austria campus serves as a fully integrated center of excellence, housing our primary R&D, customer engineering and gas engine manufacturing operations. This hub is supported by specialized component and machining facilities in Hall and Kapfenberg, Austria.

In North America, our facilities in Welland, Ontario; Waukesha, Wisconsin and Waller, Texas serve as key regional hubs. Crucially, our Trenton, New Jersey facility operates as a dedicated containerization center specifically optimized for our data center business line. Recent investments in our North American footprint underscore our commitment to a “local-for-local” strategy, enhancing our in-region maintenance, component manufacturing and assembly capabilities to reduce lead times and mitigate supply chain and tariff risks.

This level of integration enables us to serve customers across the full asset lifecycle: from initial sale to recurring maintenance and replacement. This comprehensive approach deepens customer intimacy and positions us to capture significant upselling opportunities over time. Furthermore, between 2020 and 2025, we strategically expanded our value chain by acquiring the businesses and assets of six distributors or system integrators and a white-label service provider. These acquisitions have allowed us to internalize critical sales and distribution capabilities and more effectively serve our global customer base.

Established Track Record of Innovation

Our track record of innovation reflects more than 100 years of sustained investment and strategic focus, spanning power density, efficiency, fuel technology, solution modularity and digital capabilities. In recent years, this innovation has increasingly been directed toward the specific requirements of data center applications, where power quality, transient performance and rapid load-following are critical to the reliable operation of AI-driven computing infrastructure.

Most recently, we introduced the latest generation of the Jenbacher Type 6 engine, incorporating a set of design innovations specifically targeted at improving power quality, transient response and deployment speed under the highly dynamic load conditions typical for modern data center applications. These include (i) an optimized generator module that improves frequency stability during rapid load changes, (ii) a decentralized gas addition that enhances fuel availability during block load events and materially reduces frequency and voltage deviations and (iii) turbocharging optimized for transient operation to support fast AI-driven load ramps. Within the Type 6 engine, a large-bore, 24-cylinder engine architecture further increases power density, delivering up to approximately 5 MW of peak power per unit while maintaining strong transient behavior. Together, these features reduce reliance on external inertia and battery systems, increase power density per genset (which combine engine and alternator together with controls) (“genset”), and lower overall system footprint, capex and complexity. These engine-level innovations are complemented by expanded, containerized solutions tailored for data center deployments, enabling aggregation of units, rapid installation, accelerated time-to-power and compliance with increasingly stringent emissions standards through proprietary in-house exhaust aftertreatment solutions.

As pioneers in alternative gaseous fuel technology, we are recognized as a leading provider of gas engines for renewables (e.g., biogas, landfill gas and sewage gas) and specialty gases (e.g., industrial waste, pyrolysis and coal mine gases). Our leadership, spanning decades, is reflected in our comprehensive portfolio. By 2020, our Jenbacher Type 4 platform demonstrated the capability to operate on up to 100% hydrogen, and as of 2022, all Jenbacher products were ready for hydrogen blends of up to 25% by volume. This offers customers the flexibility to decarbonize as supply chains for low-carbon molecules mature.

We continue to invest in extending our technological leadership. Since 2024, we have increased annual R&D expense by over 15% in 2025, focusing on emissions performance, fuel flexibility, electrical efficiency, power density and ramp rates. In parallel, we have developed digital solutions for the energy technology sector. As of March 31, 2026, our workforce included over 450 employees with R&D capabilities and we hold 1,132 issued patents, reinforcing that innovation remains central to both our heritage and our long-term growth strategy.

Digital Leadership Through myplant and Proprietary AI Enhance Both Our Customer Value Proposition and Operations

Our digital ecosystem enhances the reliability, performance and lifecycle economics of our equipment and services. At its core is myplant, our proprietary, AI-enabled fleet management platform. The platform uses high-frequency operational data to enable predictive maintenance, remote diagnostics, automated optimization and fleet-level analytics, improving asset availability and allowing a significant share of service events to be resolved remotely.

Myplant is built on machine-learning, AI, and digital-twin technologies and is integrated into our internal service processes. This strengthens service attachment, supports performance commitments, improves resource utilization and enables scalable growth with limited incremental cost. Our proprietary digital approach enables us to maintain control over the development of our solutions, reinforcing long-term customer relationships and creating a defensible competitive moat.

By separately embedding AI across corporate functions, including operations, sales, engineering, service, HR, IT and legal, we aim to improve productivity, optimize resource allocation and strengthen margins.

Our Growth Strategies

We believe our strengths and competitive position enable us to capitalize on the evolving market opportunity, differentiate us from our competitors and drive highly profitable growth over time.

Order intake and revenue trends demonstrate our strong exposure to structurally high-growth segments of the global power generation market, reflecting our established positioning and leading technology in flexible, modular, gas-based power solutions.

We are particularly well placed to capture accelerating demand in behind-the-meter data center applications, notably in North America, where our solutions align closely with customer requirements for speed of deployment, reliability and dispatchability. The resulting step-up in Equipment Order Intake is materially expanding the installed base and is expected to translate into a sustained increase in Services revenues over the coming years, as reflected in the long-term revenue mix. In parallel, we are executing a disciplined, self-funded capacity expansion and advancing product innovation, partnerships and may conduct selective M&A to support continued growth and reinforce our leadership across these attractive end markets.

Capitalize on Data Center–Driven Power Demand and Energy Transition Tailwinds with Differentiated Gas Engine Solutions

We are positioned at the intersection of two powerful global trends: accelerating AI adoption and the global energy transition. All three of our Equipment business lines, data centers, power solutions and compression, benefit directly from surging data center power demand, driven by AI workloads. Our data center solutions are well positioned given our established behind-the-meter and co-location offerings. We are investing in our capacity, sales, distribution and R&D to scale these solutions through standardized, pre-engineered power blocks that can be deployed rapidly and replicated across campuses and geographies.

In parallel, rising renewable penetration and the accelerated retirement of coal‑fired capacity are structurally increasing the need for flexible, dispatchable generation to support peaking, firming, balancing and overall grid stability. As dispatchable generation becomes increasingly essential for reliability, we believe natural gas is set to play a larger role in the power mix due to its scalability, availability and flexibility, which in turn accelerates demand for our compression solutions.

Our predominantly direct go-to-market strategy enhances our ability to engage regularly with customers and adapt our offering to their requirements. Our strong position and competitive advantage in the markets in which we operate is validated by a robust and growing Equipment Order Backlog, supported by a 2.8x Equipment Order Intake book-to-bill ratio and an approximately 16 times increase in data center Equipment Order Intake from 2020 to 2025. We recently partnered with an energy-as-a-service (“EaaS”) provider to deploy 2.3 GW of advanced power-infrastructure solutions. With AI adoption and build-up of supporting infrastructure, our runway for future growth becomes stronger.

Sizable and Growing Installed Base Initiates “Service Flywheel,” Driving Resilient Growth and Profitability

The step-change in installed base that we expect in the coming years will accelerate the long-term growth of our Services segment. As our fleet expands, we are positioned to capture recurring parts and service revenues over the full lifecycle of each engine. Our Services revenue is derived from sales of parts and labor, where, as of December 31, 2025, parts represent around 85% of our Services revenue and labor represents around 15% of our Services revenue, based on management’s estimates on calculations in Euros. As a result, a substantial portion of lifecycle value is driven by parts, which are frequently proprietary and therefore naturally exhibit high OEM capture rates, particularly in high-growth applications such as data centers where reliability is paramount. To support incremental future growth, we expect to selectively expand our direct access to the labor value pool through a combination of targeted acquisitions and organic capability build-out, consistent with our historical approach. In parallel, we strive to continue strengthening customer compliance with our standard maintenance schedule and articulating the value proposition of OEM parts, reinforcing service capture across the installed base.

This structurally high service capture rate provides revenue visibility extending well beyond 2030, as a strong Equipment Order Intake expands the future service opportunity set. Equipment Order Intake has increased by 188% from 2024 to 2025, reinforcing the growth trajectory of the installed base. As the fleet grows and matures, these dynamics create a self-reinforcing service flywheel: incremental equipment deployments expand the installed base, the proprietary nature of parts and LSAs drive recurring aftermarket activity and deep customer relationships support incremental future equipment sales.

The impact of this flywheel is evident in our recent financial performance, including Services revenue growth of 15% between 2023 and 2025, and Services revenue growth for seven consecutive years as of December 31, 2025. Together, these dynamics position us to sustain long-term value creation through continued investment in innovation, operational excellence and market expansion.

Execute on Our Self-Funded Global Manufacturing Capacity Expansion

In response to accelerating demand for our Equipment and Services segments, we are executing a series of self-funded manufacturing capacity expansion initiatives, with a particular focus on capturing U.S. data center demand. In 2025, our annual capital expenditures represented approximately 6.5% of revenue, with the majority allocated to growth initiatives and funded from operating cash flow. A significant portion of recent and planned growth capital expenditures are directed towards North America, reflecting the strength of U.S. data center demand and our strategic focus on local manufacturing and execution.

Investments such as our Trenton, New Jersey facility are designed to expand containerization capabilities that are supporting data center deployments in the U.S. market. Across our manufacturing network, our current investment plan is expected to provide us with sufficient headroom and flexibility to deliver our growth plan and capture incremental market opportunities. The flexibility of our supply chain and long-standing supplier relationships further enable efficient scaling with controlled execution risk.

Our ability to bring incremental capacity online is supported by a proven execution track record, including the recent opening of our second facility in Hall, Austria. Building on this foundation, we are continuing to expand capacity, with our current plans designed to significantly increase MW output, targeting approximately a tripling of our total capacity. These plans include a near-term, elevated investment phase, where we expect spending to temporarily rise meaningfully as we accelerate build-out, followed by a return to our historical, normalized investment cadence once the additional capacity is in place.

Commercialize New Products and Solutions to Meet Evolving End Market Needs

Our ability to commercialize new products and solutions is underpinned by a long-standing engineering track record across gas engine technology, controls and system integration. This includes a series of category-defining milestones such as leadership in cogeneration, development of large-bore high-speed and high-efficiency engine platforms, advances in fast start and transient-capable designs, early innovation in alternative and hydrogen-ready gaseous fuels and the introduction of digital engine management and asset performance solutions.

This innovation capability is shaped through close collaboration and co-creation with key customers, technology partners and system integrators, ensuring new technologies are engineered for operational relevance, rapid deployment and scalability from inception. Innovations are industrialized into standardized platforms that can be deployed repeatedly across end markets rather than developed as one-off solutions.

Importantly, this long-term innovation capability is not episodic but platform-based, allowing new technologies to be consistently translated into commercially relevant products and solutions. The same engineering depth that enabled historical milestones now underpins recent innovations targeted at data centers, power solutions and compression, supporting advances in transient performance, power quality, power density, containerized deployment, digital optimization and hydrogen readiness as end-market requirements continue to evolve.

Pursue Targeted Partnerships and Selective M&A Opportunities