The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS

Subject to Completion, Dated May 11, 2026.

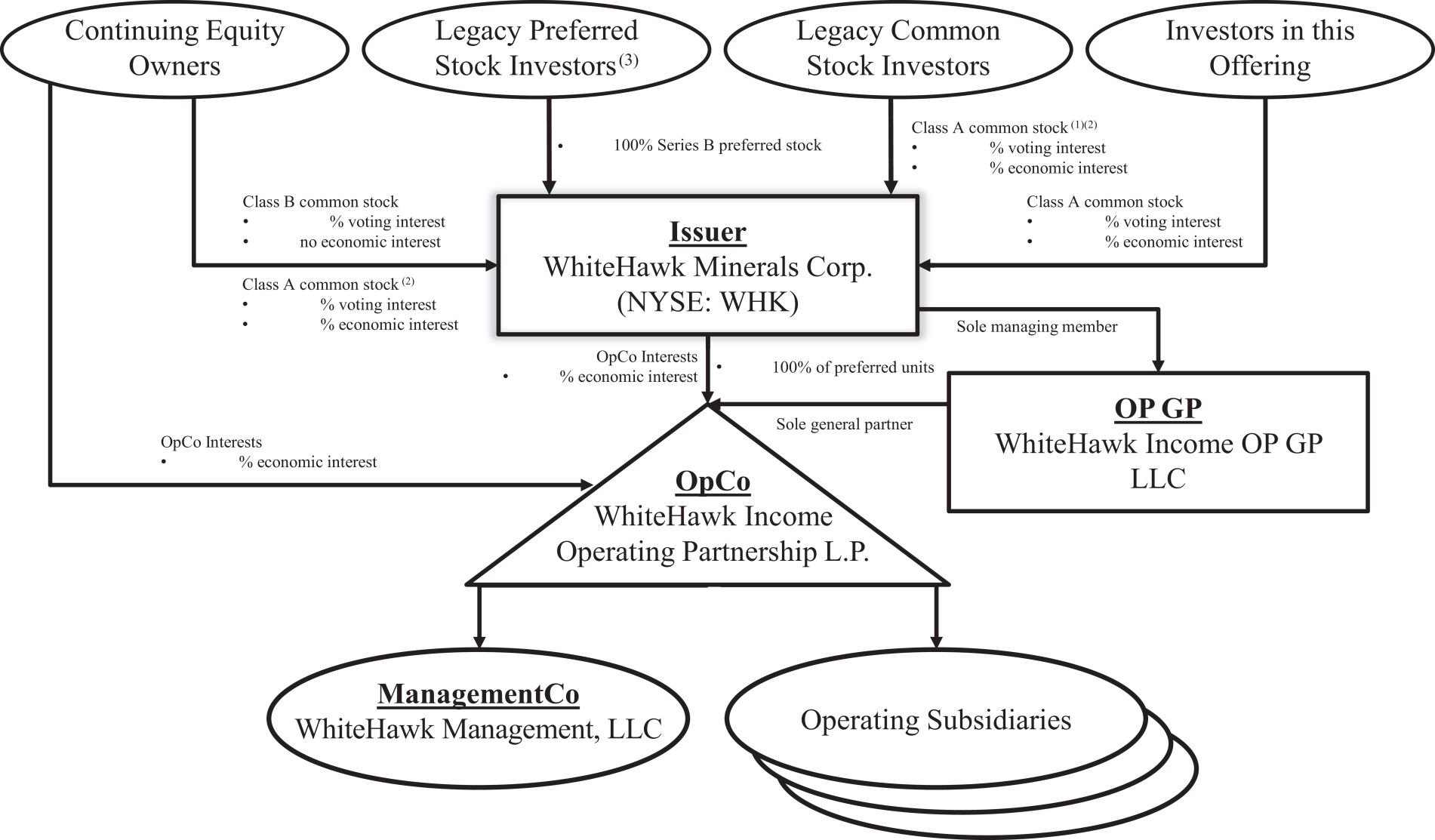

WhiteHawk Income Corporation

(to be renamed WhiteHawk Minerals Corp.)

Shares

Class A Common Stock

This is the initial public offering of shares of our Class A common stock. We are offering shares of our Class A common stock.

Prior to this offering, there has been no public market for our common stock. The initial public offering price of our common stock is expected to be between $ and $ per share. We intend to apply to list our common stock on the New York Stock Exchange (“NYSE”) under the symbol “WHK.” We intend to change our corporate name to WhiteHawk Minerals Corp. in connection with the closing of this offering. See “Prospectus Summary—Summary of the Transactions” and “Our Organizational Structure.”

To the extent that the underwriters sell more than shares of common stock, the underwriters have the option to purchase, exercisable within 30 days from the date of this prospectus, up to an additional shares from us at the public offering price, less underwriting discounts and commissions.

Upon consummation of this offering, we will be a holding company in an organizational structure commonly referred to as an umbrella partnership-C-corporation (or “Up-C”) structure, and our principal assets will consist of (i) direct ownership of % of the common units (“OpCo Interests”) of WhiteHawk Income Operating Partnership L.P. (“WhiteHawk OpCo”) (or approximately % of the OpCo Interests if the underwriters exercise in full their option to purchase additional shares of Class A common stock), which entitle us to a corresponding percentage ownership of the economic interest in WhiteHawk OpCo, and (ii) all of the member interests of WhiteHawk Income OP GP LLC (“OP GP”), the sole general partner of WhiteHawk OpCo, which entitles us to control the business and affairs of WhiteHawk OpCo. See “Risk Factors—Risks Related to Our Capital Structure.” We will operate and control all of the business and affairs of WhiteHawk OpCo and its direct and indirect subsidiaries, and conduct our business through WhiteHawk OpCo. In addition, we will own all of the Series B preferred units of WhiteHawk OpCo.

Following this offering, we will have two series of authorized common stock: shares of Class A common stock, having one vote per share and economic rights, and shares of Class B common stock, having one vote per share and no economic rights (collectively, the “Common Stock”). Holders of Class A and Class B common stock will vote together as a single class on all matters to be presented to our shareholders for their vote or approval, except as otherwise required by applicable law or our Bylaws (as defined herein). Our outstanding Class A common stock and Class B common stock will represent approximately % and %, respectively, of the total voting power of our outstanding Common Stock immediately following this offering, assuming no exercise of the underwriters’ option to purchase additional shares of Class A common stock. See “Description of Capital Stock” and “Our Organizational Structure.”

We are an “emerging growth company” as that term is used in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) and, as such, we have elected to take advantage of certain reduced public company reporting requirements for this prospectus and future filings. See “Risk Factors” and “Prospectus Summary—Emerging Growth Company.”

Investing in our Class A common stock involves risks. See “Risk Factors” starting on page 34.

| Price to Public | Underwriting Discounts and Commissions(1) |

Proceeds to Issuer |

||||||||||

| Per Share |

$ | $ | $ | |||||||||

| Total |

$ | $ | $ | |||||||||

| (1) | See “Underwriting” for additional information regarding underwriter compensation. |

Delivery of the shares of Class A common stock will be made on or about , 2026.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Joint Lead Bookrunners

| Raymond James | Stifel | J.P. Morgan |

Bookrunning Managers

| Capital One Securities | Stephens Inc. |

Prospectus dated , 2026