Filed by Evernorth Holdings Inc.

pursuant to Rule 425 of the Securities Act of 1933, as amended

and deemed filed pursuant to Rule 14a-12

of the Securities Exchange Act of 1934, as amended

Subject Company: Evernorth Holdings Inc.

Commission File Number of Subject Company: 132-02881

As previously disclosed, on October 19, 2025, Armada Acquisition Corp. II, a Cayman Islands exempted company (“SPAC”), entered into a Business Combination Agreement, dated as of October 19, 2025 (the “Business Combination Agreement”), with Evernorth Holdings Inc., a Nevada corporation (“Pubco”), Pathfinder Digital Assets LLC, a Delaware limited liability company (the “Company”), Evernorth Corporate Merger Sub Inc., a Delaware corporation and wholly owned subsidiary of Pubco, Evernorth Company Merger Sub LLC, a Delaware limited liability company and wholly owned subsidiary of Pubco, and Ripple Labs Inc., a Delaware corporation.

The following communications were published by Pubco and Sagar Shah, Pubco’s Chief Business Officer, on May 8, 2026:

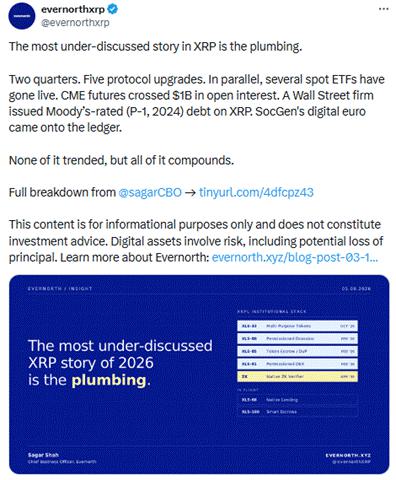

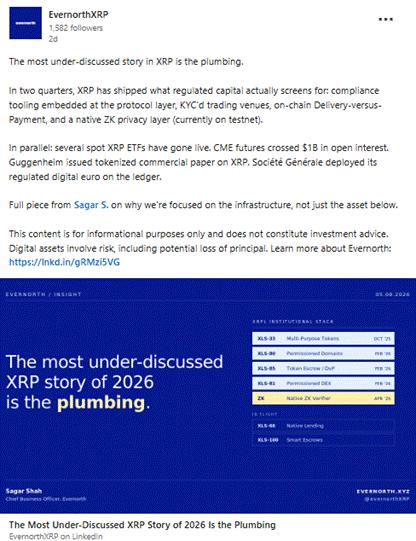

The Most Under-Discussed XRP Story of 2026 Is the Plumbing

By Sagar Shah, Chief Business Officer, Evernorth

The most overlooked development on XRP right now is the institutional plumbing, not a price chart, ETF flows, or a tokenization headline.

Over the last six months, the XRP Ledger has shipped key capabilities that regulated capital needs to operate on a public blockchain. None of it is individually a major development on its own, but collectively it provides a comprehensive solution for regulated institutions to bring capital onchain .

What's gone live

October 2025 — Multi-Purpose Tokens (XLS-33). A token standard with compliance rules baked into the token itself.

What this actually does: A bank can issue a tokenized money market fund share, commercial paper or corporate bond directly on XRPL with transfer restrictions, KYC requirements, allowlists and freeze/clawback controls coded into the token. The compliance tooling travels with the asset and is enforced at the ledger layer, rather than bolted on through off-chain infrastructure.

February 4, 2026 — Permissioned Domains (XLS-80). Restricted environments where only accounts holding approved credentials can participate.

What this actually does: Defines the trust boundary. A bank can establish a domain where every participating wallet has been KYC'd and credentialed. Think of the on-chain equivalent of a closed-network membership.

February 12, 2026 — Token Escrow (XLS-85). Extends XRPL's native escrow primitive beyond XRP to multi-purpose tokens and issued currencies (IOUs).

What this actually does: This is on-chain Delivery-versus-Payment (DvP), the settlement standard that backs trillions of dollars of traditional securities trades every day. Buyer's cash and seller's bond are locked simultaneously and only released when both sides deliver. This is designed to significantly reduce counterparty risk and failed settlement. It also enables time-locked structures: vesting schedules, milestone payments, conditional disbursements, performance-linked payouts. Anything that used to require a custodian, a paying agent or a transfer agent to coordinate.

February 18, 2026 — Permissioned DEX (XLS-81). Trading venues built on top of permissioned domains, where only approved counterparties can place and accept offers.

What this actually does: The on-chain equivalent of a private OTC desk or regulated dark pool. A bank can list a tokenized Treasury and trade it knowing every counterparty has been onboarded. So there are no anonymous wallets, sanctions exposure or hostile MEV. Institutions get the liquidity benefits of a shared ledger without taking on the counterparty risk of a permissionless DEX.

April 14, 2026 — Native ZK Proof Verifier (Boundless × XRPL Commons). A programmable privacy layer on a public blockchain.

What this actually does: A bank can settle a large trade on a public blockchain without broadcasting the size, parties or terms to competitors. The transaction is valid on-chain but opaque off-chain. This is the same privacy institutions expect from traditional clearing systems. Currently live on testnet with mainnet integration tied to upcoming Smart Escrow functionality.

What's actively in development

Two protocols in flight take XRPL from "compliant token venue with programmable settlement" to a working financial system:

Native Lending — XLS-66 Lending Protocol + XLS-65 Single-Asset Vaults. Pooled lending markets at the protocol layer.

What this actually does: A corporate treasurer can deposit idle stablecoins (RLUSD, USDC) into a vault and earn yield, the on-chain version of sweeping cash into a money market fund. A market maker can borrow against tokenized Treasuries to fund inventory. An asset manager can lend out tokenized bonds for a fee. The standard specifies fixed-term, fixed-rate loans with first-loss capital cover, which is closer to traditional credit underwriting than typical DeFi over-collateralization. It's the missing primitive for treasury management, prime brokerage and programmatic credit.

Smart Escrows (XLS-100). Programmable escrow with conditional release.

What this actually does: Combines the ZK verifier above with the Token Escrow primitive. An escrow can release only when a valid zero-knowledge proof is presented, meaning settlement can be conditional on private off-chain events (compliance checks, oracle data, counterparty performance) without revealing them on-chain. This is the building block for confidential structured products.

Lending and programmable escrow are how a token venue becomes a system institutions can actually run capital through.

The institutional access layer is moving in parallel

Protocol upgrades only matter if regulated capital can actually reach the asset. That layer has been compounding for a year:

| · | May 19, 2025 — CME Group launches XRP futures. CME is the regulated exchange where Wall Street trades gold, oil and S&P 500 futures. Within three months, open XRP futures positions crossed $1 billion, the fastest any CME crypto contract has hit that mark. |

| · | June 10, 2025 — Guggenheim issues tokenized commercial paper on XRPL. Guggenheim, a Wall Street firm managing hundreds of billions, issued short-term corporate debt directly on XRP. Backed by U.S. Treasuries, rated by Moody's (Prime-1, 2024), $280M+ in volume. That’s real Wall Street fixed income, on-chain. |

| · | November 13–24, 2025 — US spot XRP ETF wave. Canary (Nasdaq), Bitwise (NYSE), Grayscale (NYSE Arca), Franklin Templeton, and 21Shares launched XRP ETFs, making XRP buyable in any brokerage account. Inflows crossed $1 billion by mid-December, the fastest of any digital asset since Ethereum's ETFs. |

| · | February 18, 2026 — Société Générale's regulated digital euro goes live on XRPL. SG, a roughly $1.8 trillion European bank, picked XRP as one of only three public blockchains to host its EU-regulated euro stablecoin. Major banks don't pick blockchains casually. |

| · | Ongoing — Archax brings tokenized funds and securities to XRPL. The UK's first government-licensed digital asset exchange is moving institutional products onto XRP — including a £3.8B fund from abrdn — and acquired a US broker-dealer in March 2025. Target: $1B+ of traditional assets on XRP by mid-2026. Traditional institutional-grade fund products are beginning to move on-chain. |

Set against the protocol roadmap, the full institutional stack is coming into focus.

Why this matters

XRPL has been shipping real utility for real use cases for two quarters straight. Amendment votes. Validator activations. Custody onboardings. Compliance integrations. Standards-track protocol drafts. None of it trends, but all of it compounds.

Regulated capital chooses a venue based on whether the rails can do the boring, essential things: enforce who can hold and trade an asset, settle a trade without counterparty risk, keep large transactions confidential, custody assets with a regulated counterparty, finance positions, and produce an audit trail. On that test, the answer is becoming straightforward.

Where Evernorth fits

We see this story clearly because we're building our strategy around it. Evernorth's role is to be a long-term participant in a venue we believe is well positioned to serve regulated capital.

That's why we view the plumbing as the overlooked part of the XRP story. By the time the headlines catch up, the rails will already be operating.

This content is for informational purposes only and does not constitute investment advice, an offer to sell, or a solicitation of an offer to buy any securities or digital assets. Digital assets are speculative and involve a high degree of risk, including the potential for total loss of principal. Past performance is not indicative of future results. Learn more about Evernorth: https://www.evernorth.xyz/blog-post-03-18-2026

Additional Information and Where to Find It

On March 18, 2026, Evernorth filed with the SEC the "Registration Statement"), which includes a preliminary proxy statement of Armada II and a prospectus of Evernorth (the "Proxy Statement/Prospectus") in connection with the proposed business combination (the "Business Combination"), the private placements of securities in connection with the Business Combination (the "Private Placement Transactions") and the other transactions contemplated by the Business Combination Agreement and/or as described in this press release (together with the Business Combination and the Private Placement Transactions, the "Proposed Transactions"). The Registration Statement is not yet effective. The definitive proxy statement and other relevant documents will be mailed to shareholders of Armada II as of the record date to be established for voting on the Business Combination and other matters as described in the Proxy Statement/Prospectus. Armada II and Evernorth have also filed other documents regarding the Proposed Transactions with the SEC. This press release does not contain all of the information that should be considered concerning the Proposed Transactions and is not intended to form the basis of any investment decision or any other decision in respect of the Proposed Transactions. BEFORE MAKING ANY VOTING OR INVESTMENT DECISION, SHAREHOLDERS OF ARMADA II AND OTHER INTERESTED PARTIES ARE URGED TO READ, WHEN AVAILABLE, THE PRELIMINARY PROXY STATEMENT/PROSPECTUS, AND AMENDMENTS THERETO, AND THE DEFINITIVE PROXY STATEMENT/PROSPECTUS AND ALL OTHER RELEVANT DOCUMENTS FILED OR THAT WILL BE FILED WITH THE SEC IN CONNECTION WITH ARMADA II'S SOLICITATION OF PROXIES FOR THE EXTRAORDINARY GENERAL MEETING OF ITS SHAREHOLDERS TO BE HELD TO APPROVE THE PROPOSED TRANSACTIONS AND OTHER MATTERS AS DESCRIBED IN THE PROXY STATEMENT/PROSPECTUS BECAUSE THESE DOCUMENTS WILL CONTAIN IMPORTANT INFORMATION ABOUT ARMADA II, PATHFINDER DIGITAL ASSETS, EVERNORTH AND THE PROPOSED TRANSACTIONS. Investors and security holders will also be able to obtain copies of the Registration Statement and the Proxy Statement/Prospectus and all other documents filed or to be filed with the SEC by Armada II and Evernorth, without charge, once available, on the SEC's website at www.sec.gov, or by directing a request to: Armada Acquisition Corp. II, 382 NE 191st St., Suite 52895, Miami, Florida 33179-3899; e-mail: finance@arringtoncapital.com, or to: Evernorth Holdings Inc., 600 Battery St, San Francisco, CA 94111, email: finance@evernorth.xyz.

NEITHER THE SEC NOR ANY STATE SECURITIES REGULATORY AGENCY HAS APPROVED OR DISAPPROVED THE PROPOSED TRANSACTIONS DESCRIBED HEREIN, PASSED UPON THE MERITS OR FAIRNESS OF THE BUSINESS COMBINATION, OR ANY RELATED TRANSACTIONS OR PASSED UPON THE ADEQUACY OR ACCURACY OF THE DISCLOSURE IN THIS PRESS RELEASE. ANY REPRESENTATION TO THE CONTRARY CONSTITUTES A CRIMINAL OFFENSE.

The securities to be issued by Evernorth and the units to be issued by Pathfinder Digital Assets LLC ("Pathfinder"), in each case, in connection with the Proposed Transactions, have not been registered under the Securities Act of 1933, as amended (the "Securities Act") and may not be offered or sold in the United States absent registration or an applicable exemption from the registration requirements of the Securities Act.

Participants in the Solicitation

SPAC, Pubco, Company and their respective directors and executive officers may be deemed under SEC rules to be participants in the solicitation of proxies from SPAC’s shareholders in connection with the Business Combination. A list of the names of such directors and executive officers, and information regarding their interests in the Business Combination and their ownership of SPAC’s securities is, or will be, contained in SPAC’s filings with the SEC. Additional information regarding the interests of the persons who may, under SEC rules, be deemed participants in the solicitation of proxies from SPAC’s shareholders in connection with the Business Combination, including the names and interests of Company and Pubco’s directors and executive officers, will be set forth in the Proxy Statement/Prospectus, which is expected to be filed by SPAC and Pubco with the SEC. Investors and security holders may obtain free copies of these documents as described above.

No Offer or Solicitation

This communication is for informational purposes only and is not a proxy statement or solicitation of a proxy, consent or authorization with respect to any securities or in respect of the Proposed Transactions and shall not constitute an offer to sell or exchange, or a solicitation of an offer to buy or exchange the securities of SPAC, the Company or Pubco, or any commodity or instrument or related derivative, nor shall there be any sale of any such securities in any state or jurisdiction in which such offer, solicitation, sale or exchange would be unlawful prior to registration or qualification under the securities laws of any such state or jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of the Securities Act or an exemption therefrom. Investors should consult with their counsel as to the applicable requirements for a purchaser to avail itself of any exemption under the Securities Act.

Forward-Looking Statements

This communication contains certain forward-looking

statements within the meaning of the U.S. federal securities laws with respect to the Proposed Transactions and the parties thereto. All

statements contained in this communication other than statements of historical fact, including, without limitation, statements regarding

the Business Combination between SPAC and Pubco; the anticipated benefits and timing of the transaction; expected trading of the combined

company’s securities on Nasdaq; the completion of investments from certain institutional investors; the expected amount of gross

proceeds from the Private Placement Transactions; the anticipated use of proceeds from such Private Placement Transactions; the building

of the world’s leading institutional XRP treasury; the amount of XRP expected to be held by the combined company; the combined company’s

future financial performance, the ability of the combined company to execute its business strategy, its market opportunity and positioning;

expectations regarding institutional and retail adoption of XRP and participation in DeFi yield strategies; the combined company’s

contributions to the growth and maturity of the ecosystem, using an approach designed to generate returns for shareholders, supporting

XRP’s utility and adoption, alignment with the growth of the XRP ecosystem, and becoming the leading institutional vehicle for XRP;

management ensuring operational independence, taking XRP’s presence in capital markets to the next level, and other statements regarding

management’s intentions, beliefs, or expectations with respect to the combined company’s future performance, are forward-looking

statements.

Forward-looking statements are often identified by the use of words such as “anticipate,” “believe,” “continue,”

“could,” “estimate,” “expect,” “intend,” “may,” “might,” “plan,”

“potential,” “predict,” “project,” “should,” “will,” “would,”

and similar expressions, but the absence of these words does not mean that a statement is not forward-looking.

These forward-looking statements are based on the current expectations and assumptions of SPAC and Pubco and are subject to risks and uncertainties that could cause actual results to differ materially from those expressed or implied by such forward-looking statements. Such risks and uncertainties include, but are not limited to: (1) the occurrence of any event, change or other circumstances that could delay or prevent the consummation of the proposed Business Combination; (2) the outcome of any legal proceedings that may be instituted against SPAC, Pubco, the combined company, or others following the announcement of the Proposed Transactions; (3) the inability to complete the Business Combination due to failure to obtain shareholder approval or satisfy other closing conditions; (4) the inability to complete the Private Placement Transactions, (5) changes to the structure, timing, or terms of the Proposed Transactions; (6) the inability of the combined company to meet applicable listing standards or to maintain the listing of its securities following the closing of the Business Combination; (7) the risk that the announcement and consummation of the transaction disrupts current plans and operations; (8) the inability to recognize the anticipated benefits of the Business Combination, including the ability to build and manage an institutional XRP treasury, execute DeFi yield strategies, and drive institutional adoption of XRP; (9) changes in market, regulatory, political, and economic conditions affecting digital assets generally or XRP specifically; (10) the costs related to the Proposed Transactions and those arising as a result of becoming a public company; (11) the level of redemptions of SPAC’s public shareholders which may reduce the public float of, reduce the liquidity of the trading market of, and/or maintain the quotation, listing, or trading of securities of SPAC or of Pubco; (12) the volatility of the price of XRP and other digital assets, the correlation between XRP’s price and the value of Pubco’s securities, and the risk that the price of XRP may decrease between the signing of the definitive documents for the Proposed Transactions and the closing of the Proposed Transactions or at any time after the closing of the Proposed Transactions; (13) risks related to increased competition in the industries in which Pubco will operate; (14) risks related to changes in U.S. or foreign laws and regulations applicable to digital assets or securities; (15) the possibility that the combined company may be adversely affected by competitive factors, investor sentiment, or other macroeconomic conditions; (16) the risk of being considered to be a “shell company” by any stock exchange on which the Pubco securities will be listed or by the SEC, which may impact the ability to list Pubco’s securities and restrict reliance on certain rules or forms in connection with the offering, sale or resale of securities; (17) the outcome of any potential legal proceedings that may be instituted against the Company, SPAC, Pubco or others following announcement of the Business Combination; and (18) other risks detailed from time to time in SPAC’s filings with the SEC, including the Registration Statement and related documents filed or to be filed in connection with the Business Combination.

The foregoing list of risk factors is not exhaustive. You should carefully consider the foregoing factors and the other risks and uncertainties described in the “Risk Factors” section of the final prospectus of SPAC dated May 20, 2025 and filed by SPAC with the SEC on May 21, 2025, SPAC’s Quarterly Report on Form 10-Q filed with the SEC on August 11, 2025, and the Registration Statement and Proxy Statement/Prospectus that will be filed by Pubco and SPAC, and other documents filed by SPAC and Pubco from time to time with the SEC, as well as the list of risk factors included herein. These filings do or will identify and address other important risks and uncertainties that could cause actual results to differ materially from those contained in the forward-looking statements. Additional risks and uncertainties not currently known or that are currently deemed immaterial may also cause actual results to differ materially from those expressed or implied by such forward-looking statements. Readers are cautioned not to put undue reliance on forward-looking statements, and none of the parties or any of their representatives assumes any obligation and do not intend to update or revise these forward-looking statements, each of which is made only as of the date of this communication.