Exhibit 99.2

Corporate Overview May 11, 2026

This presentation contains forward - looking statements about us, including our clinical trials and development plans, and our industry, that are based on management’s beliefs and assumptions and on information currently available to our management . The words “anticipate,” “believe,” “continue,” “could,” “estimate,” “expect,” “intend,” “may,” “might,” “ongoing,” “plan,” “potential,” “predict,” “project,” “should,” “target,” “will,” “would,” o r the negative of these terms o r other comparable terminology are intended to identify forward - looking statements, although not all forward - looking statements contain these identifying words . All statements, other than statements related to present facts o r current conditions or of historical facts, contained in this presentation are forward - looking statements . Accordingly, these statements involve estimates, assumptions, substantial risks and uncertainties which could cause actual results to differ materially from those expressed in them, including bu t not limited to that we have incurred significant operating losses, and we expect that we will incur significant operating losses for the foreseeable future ; that our financial condition raises substantial doubt as to our ability to continue as a going concern and we require additional capital to finance our operations beyond the second quarter of fiscal year 2026 , and a failure to obtain this necessary capital in the near term on acceptable terms, o r at all, could force us to delay, limit, reduce o r terminate our development programs, commercialization efforts o r other operations ; that we have a high risk of never generating revenue o r becoming profitable or, if we achieve profitability, we may not b e able to sustain it ; that clinical and preclinical drug development involves a lengthy and expensive process with uncertain timelines and outcomes, and results of prior preclinical studies and early clinical trials are not necessarily predictive of future results, and elraglusib may not achieve favorable results in clinical trials o r preclinical studies, and we may not be able to make regulatory submissions o r receive regulatory approval on a timely basis, if at all ; that we may not successfully enroll additional patients o r establish o r advance plans for hase 2 o r other development, including through conversations with the FDA o r EMA and the standards such bodies may impose for such development ; that regulatory approval processes may involve delays, unfavorable determinations or other challenges due to various factors, including government funding, staffing and political uncertainties ; the risk that clinical trial data are subject to differing interpretations and assessments by regulatory authorities and within the medical community ; that elraglusib could b e associated with side effects, adverse events o r other properties o r safety risks, which could delay o r preclude regulatory approval, cause us to suspend o r discontinue clinical trials or result in other negative consequences ; that this presentation includes preliminary and unpublished data which may be subject to change following the availability of more data o r following a more comprehensive review of the data and should not b e relied upon as a final analysis ; that w e do not have, and may never have, any approved products on the market and our business is highly dependent upon receiving approvals from various U . S . and international governmental agencies and will b e severely harmed if we are not granted approval to manufacture and sell our product candidates ; our reliance on third parties to conduct our non - clinical studies and our clinical trials ; our reliance on third - party licensors and ability to preserve and protect our intellectual property rights ; that we currently depend entirely on the success of elraglusib, which is our only product candidate, and if we are unable to advance elraglusib in clinical development, obtain regulatory approval and ultimately commercialize elraglusib, or experience significant delays in doing so, our business will b e materially harmed ; that we face significant competition from other biotechnology and pharmaceutical companies ; that we may not b e successful in our efforts to investigate elraglusib in additional indications and we may expend our limited resources to pursue a new product candidate o r a particular indication for elraglusib and fail to capitalize on product candidates o r indications that may b e more profitable o r for which there is a greater likelihood of success ; that the termination of third - party licenses could adversely affect our rights to important compounds o r technologies ; and our ability to fund development activities, including because our financial condition raises substantial doubt as to our ability to continue as a going concern and w e require additional capital to finance our operations beyond July 2026 , and a failure to obtain this necessary capital in the near term on acceptable terms, o r at all, could force us to delay, limit, reduce o r terminate our development programs, commercialization efforts o r other operations . You are cautioned not to place undue reliance on these forward - looking statements, which speak only as of the date hereof, and we undertake no obligation to update such statements to reflect events that occur o r circumstances that exist after the date hereof . In addition, any forward - looking statements are qualified in their entirety by reference to the factors discussed under the heading “Risk Factors” in our Annual Report on Form 10 - K filed with the SEC on March 26 , 2026 , our Quarterly Reports on Form 10 - Q, and other filings with the SEC . This presentation also contain estimates and other statistical data that we obtained from industry publications and research and studies conducted by third parties relating to market size and growth and other data about our industry . This data involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates . 1 Forward - Looking Statements

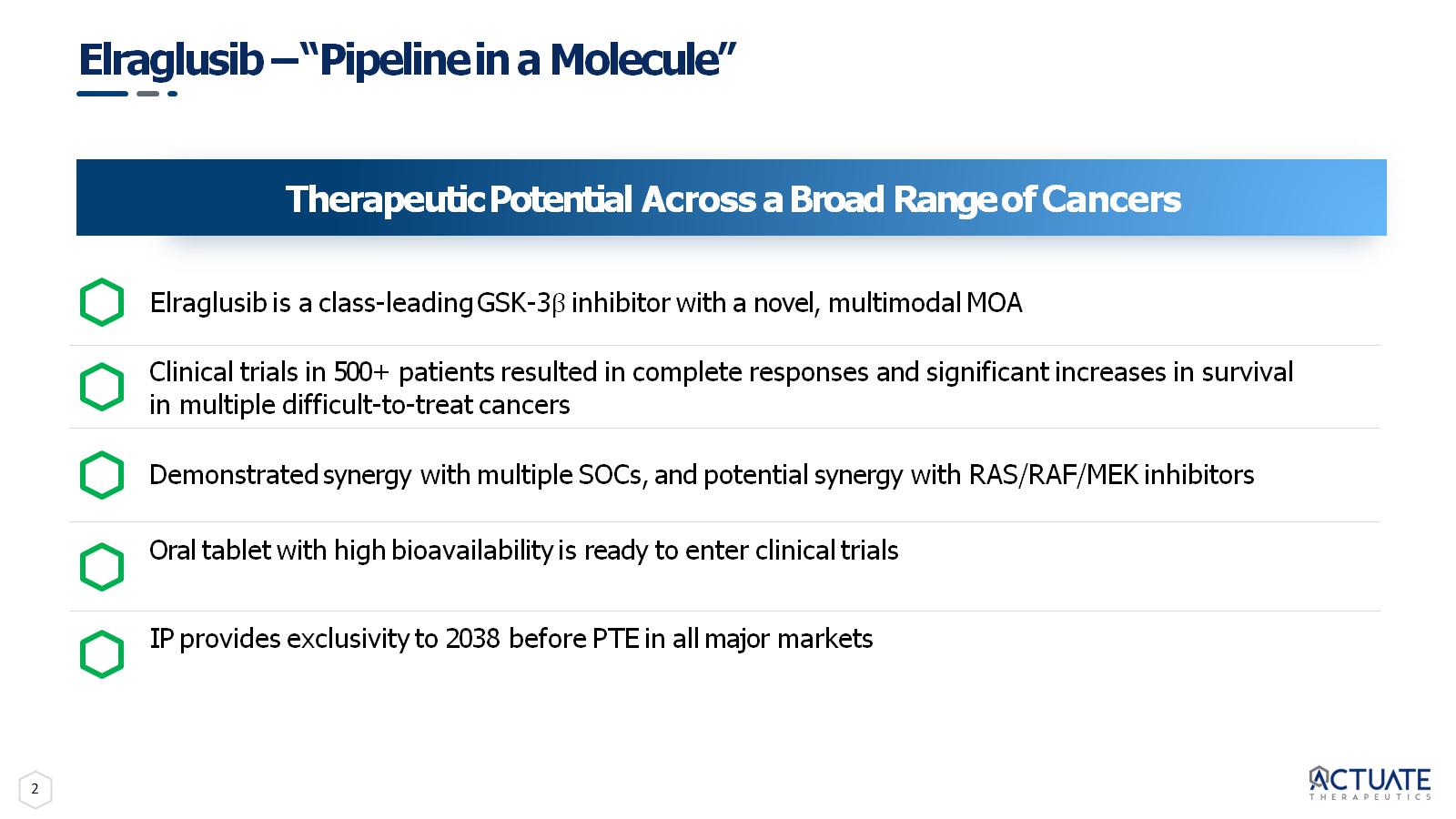

2 Elraglusib – “Pipeline in a Molecule” Therapeutic Potential Across a Broad Range of Cancers Elraglusib is a class - leading GSK - 3 β inhibitor with a novel, multimodal MOA Clinical trials in 500+ patients resulted in complete responses and significant increases in survival in multiple difficult - to - treat cancers Demonstrated synergy with multiple SOCs, and potential synergy with RAS/RAF/MEK inhibitors Oral tablet with high bioavailability is ready to enter clinical trials IP provides exclusivity to 2038 before PTE in all major markets

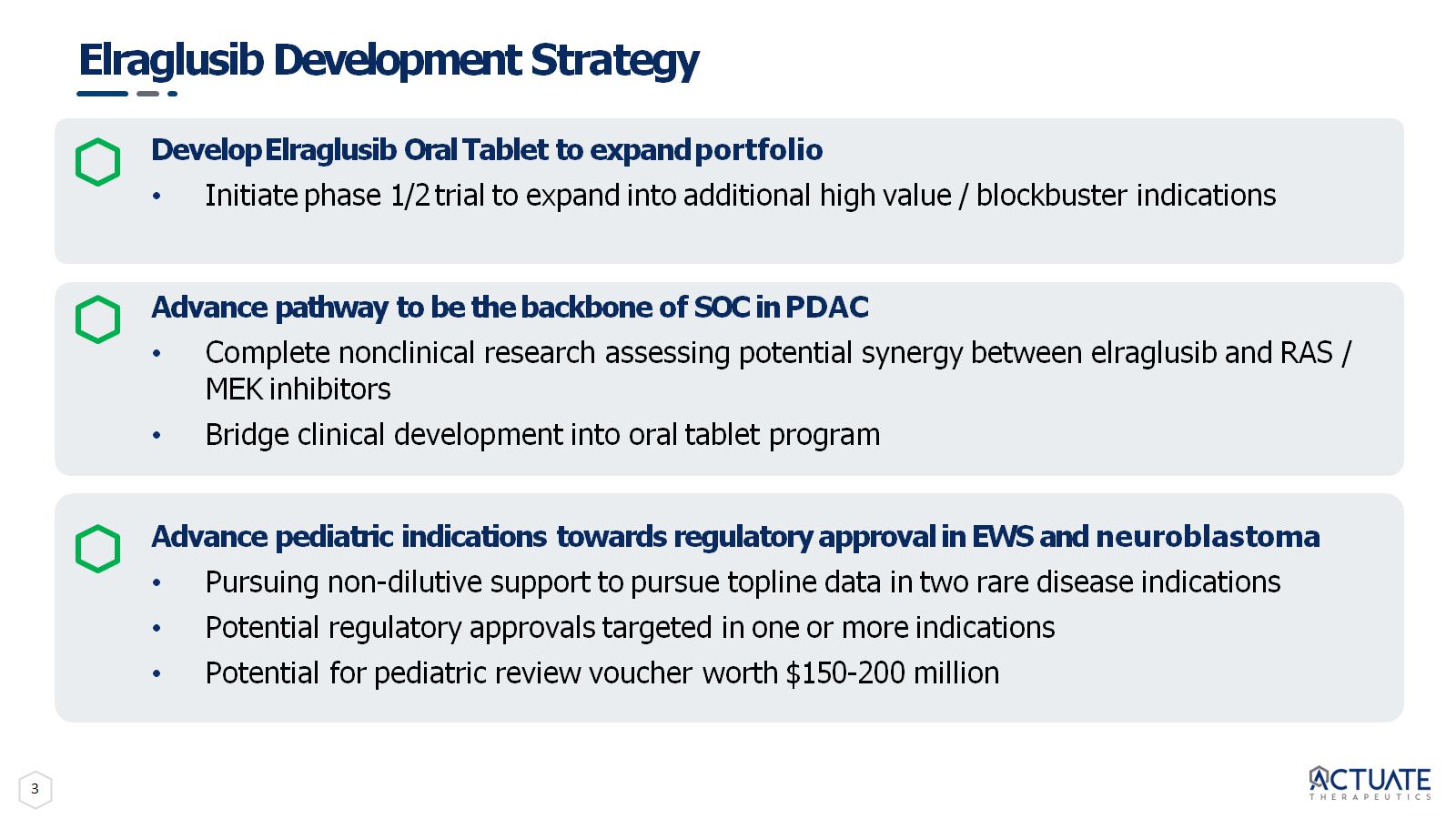

3 Elraglusib Development Strategy Develop Elraglusib Oral Tablet to expand portfolio • Initiate phase 1/2 trial to expand into additional high value / blockbuster indications Advance pathway to be the backbone of SOC in PDAC • Complete nonclinical research assessing potential synergy between elraglusib and RAS / MEK inhibitors • Bridge clinical development into oral tablet program Advance pediatric indications towards regulatory approval in EWS and neuroblastoma • Pursuing non - dilutive support to pursue topline data in two rare disease indications • Potential regulatory approvals targeted in one or more indications • Potential for pediatric review voucher worth $150 - 200 million

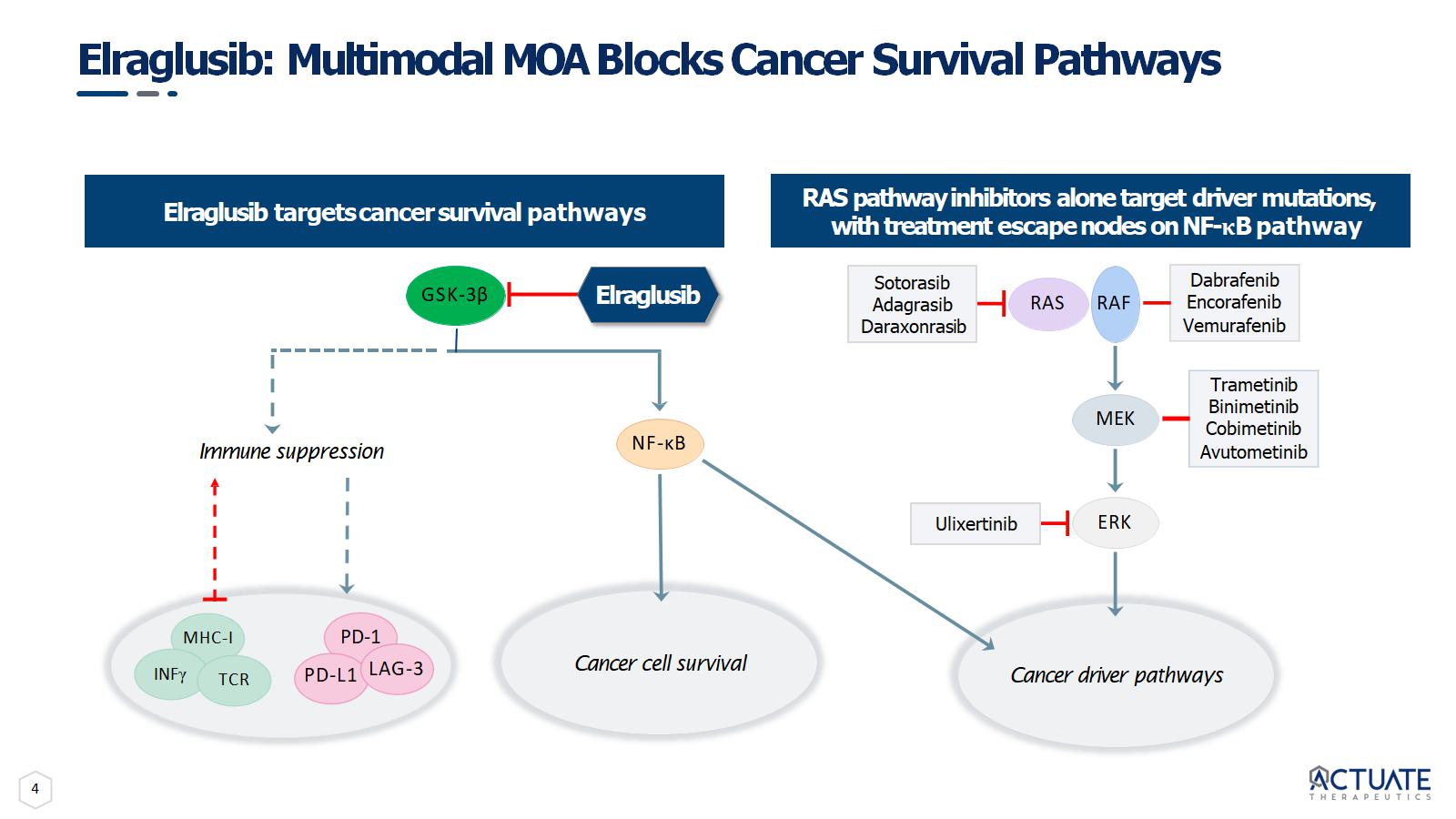

4 Elraglusib: Multimodal MOA Blocks Cancer Survival Pathways Elraglusib targets cancer survival pathways ERK Dabrafenib Encorafenib Vemurafenib Trametinib Binimetinib Cobimetinib Avutometinib Sotorasib Adagrasib Daraxonrasib RAS RAF MEK Ulixertinib Cancer driver pathways NF - κB Cancer cell survival GSK - 3β MHC - I Immune suppression INF γ PD - 1 PD - L1 LAG - 3 TCR Elraglusib RAS pathway inhibitors alone target driver mutations, with treatment escape nodes on NF - κ B pathway

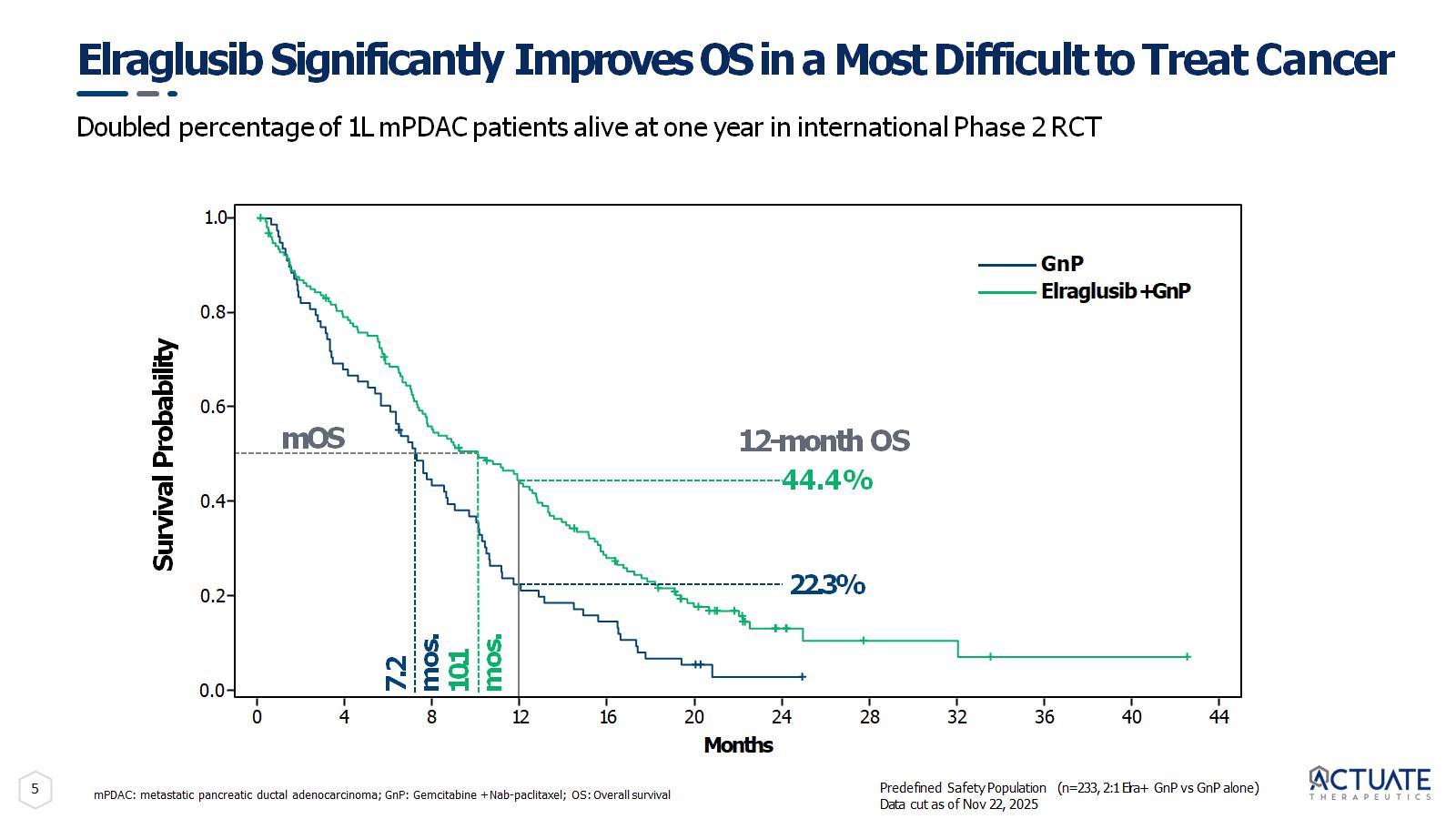

5 Elraglusib Significantly Improves OS in a Most Difficult to Treat Cancer mPDAC: metastatic pancreatic ductal adenocarcinoma; GnP: Gemcitabine + Nab - paclitaxel; OS: Overall survival Survival Probability 0.0 1.0 0.8 0.6 0.4 0.2 Months 7.2 mos. 10.1 mos. 22.3% 12 - month OS 44.4% mOS GnP Elraglusib + GnP 0 4 8 16 20 24 28 32 36 40 44 12 Predefined Safety Population (n=233, 2:1 Elra+ GnP vs GnP alone) Data cut as of Nov 22, 2025 Doubled percentage of 1L mPDAC patients alive at one year in international Phase 2 RCT

6 Elraglusib Significantly Improves Survival with Weekly IV Dosing Randomized Phase 2 trial met primary endpoint SOC: Standard of Care Elraglusib + GnP doubled 1 - year OS vs. GnP alone (p=0.0004) 2.5x increase in 1 - year OS in patients with liver metastases (p=0.0003) Elraglusib + SOC (GnP) improved median OS by 40% ( HR: 0.62 ; p=0.02) Greater benefit seen in patients receiving at least one full cycle (4 weeks) of treatment ( HR:0.58 ; p=0.035) Excellent safety profile with TEAEs/SAEs and discontinuations balanced between treatment groups

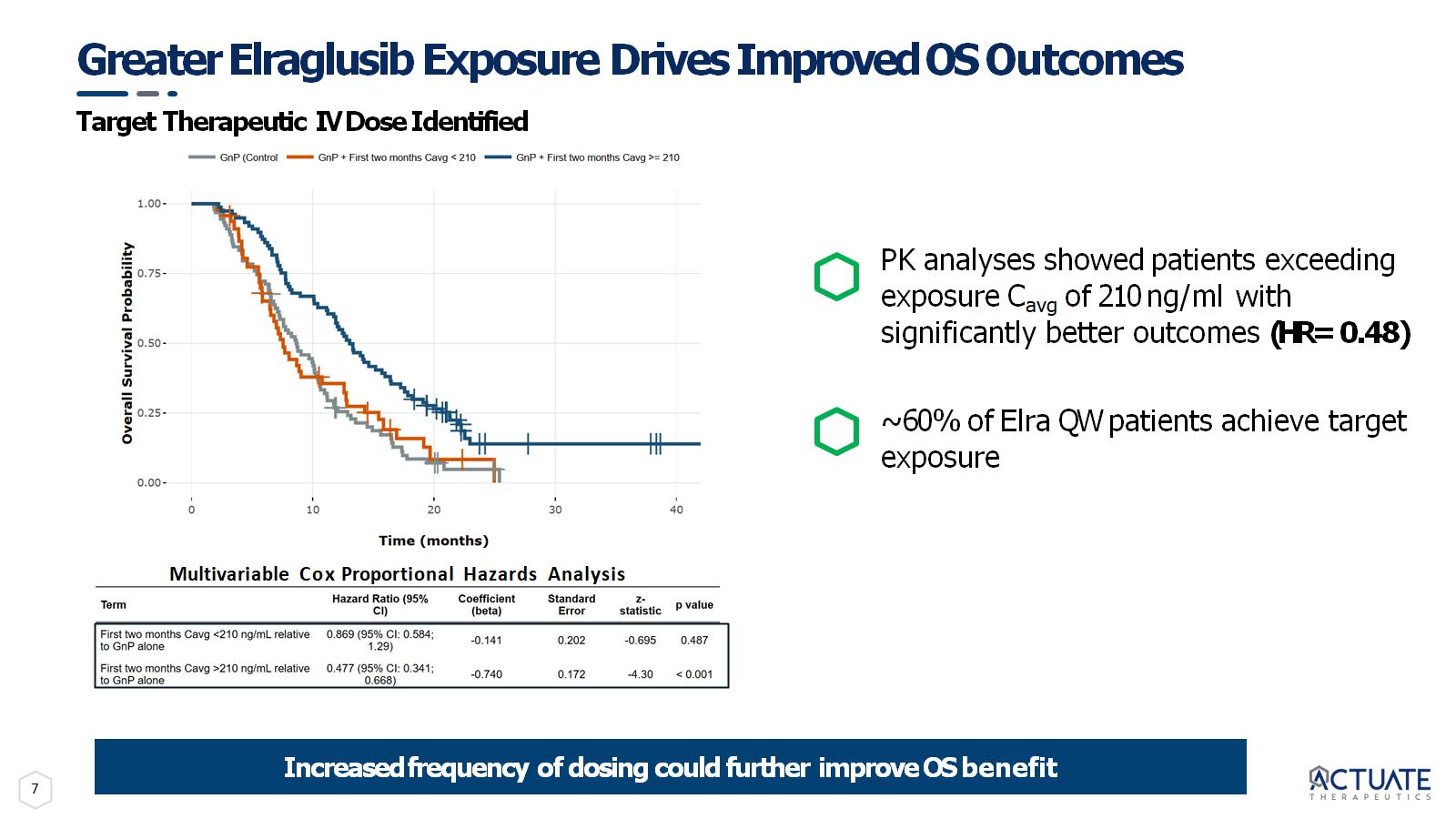

7 Greater Elraglusib Exposure Drives Improved OS Outcomes Target Therapeutic IV Dose Identified Multivariable Cox Proportional Hazards Analysis Increased frequency of dosing could further improve OS benefit PK analyses showed patients exceeding exposure C avg of 210 ng/ml with significantly better outcomes (HR= 0.48) ~ 60% of Elra QW patients achieve target exposure

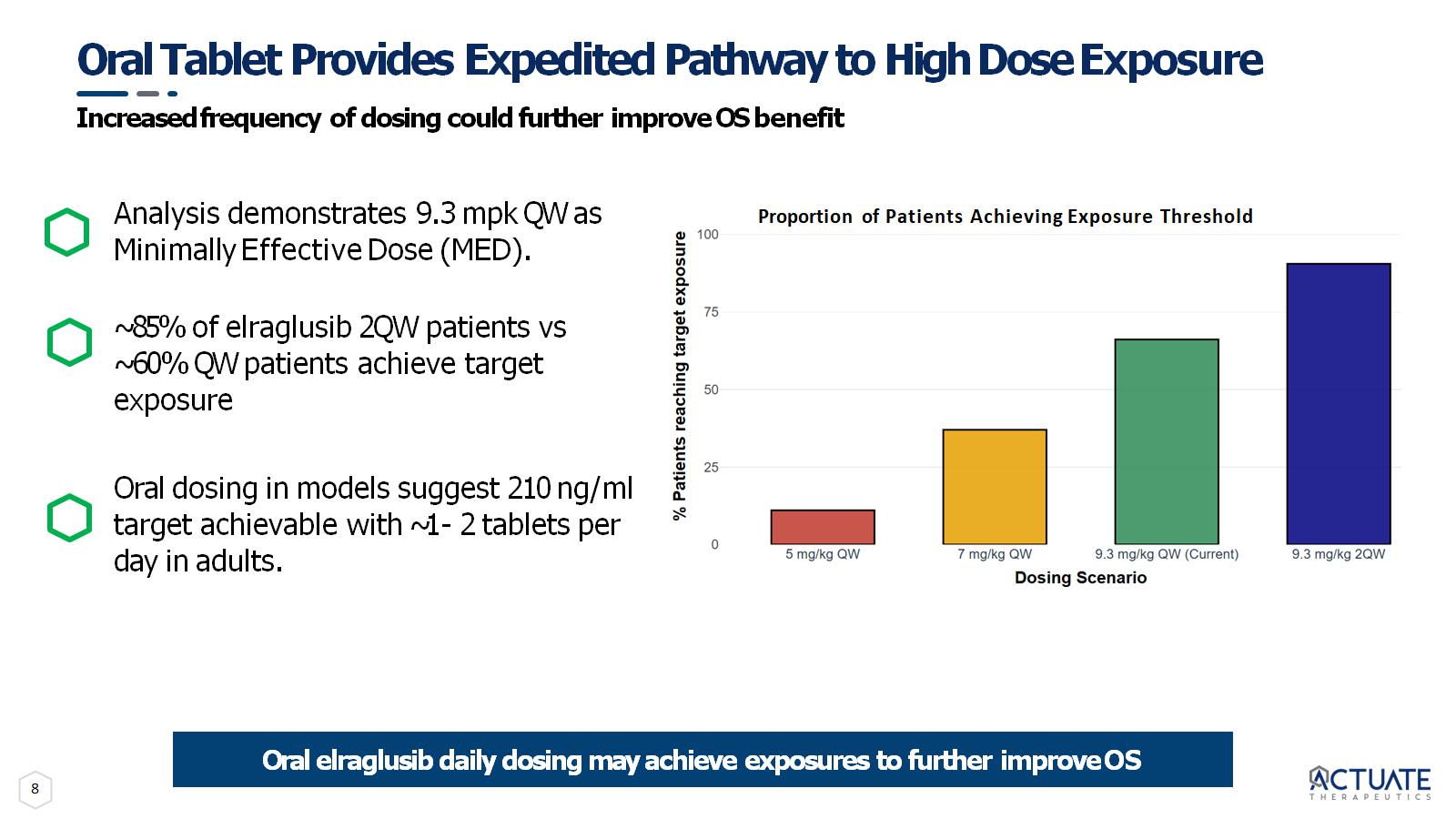

8 Oral Tablet Provides Expedited Pathway to High Dose Exposure Increased frequency of dosing could further improve OS benefit Analysis demonstrates 9.3 mpk QW as Minimally Effective Dose (MED). ~85% of elraglusib 2QW patients vs ~60% QW patients achieve target exposure Oral dosing in models suggest 210 ng/ml target achievable with ~1 - 2 tablets per day in adults. Oral elraglusib daily dosing may achieve exposures to further improve OS Proportion of Patients Achieving Exposure Threshold

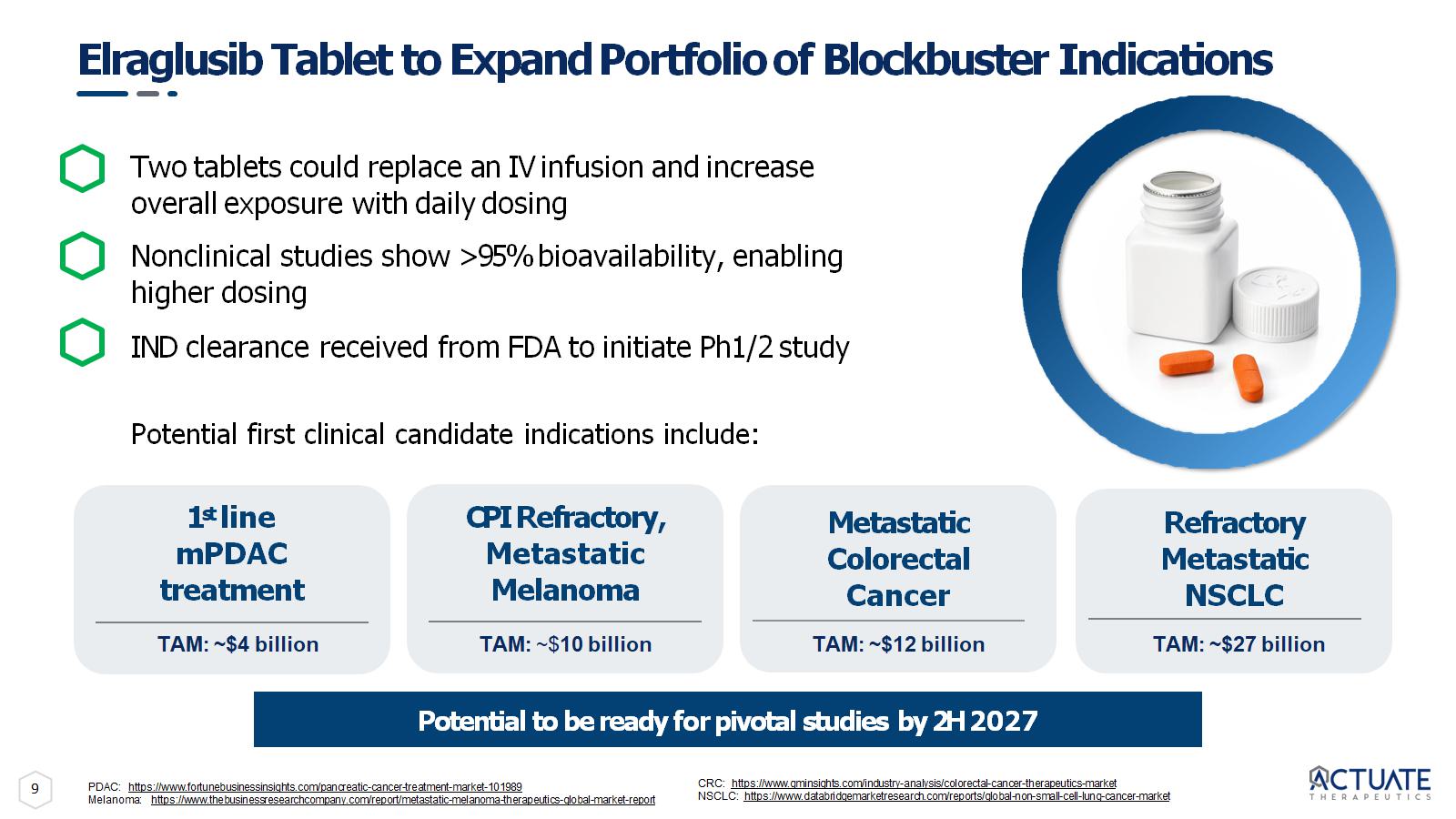

9 Two tablets could replace an IV infusion and increase overall exposure with daily dosing Nonclinical studies show >95% bioavailability, enabling higher dosing IND clearance received from FDA to initiate Ph1/2 study Potential first clinical candidate indications include: Elraglusib Tablet to Expand Portfolio of Blockbuster Indications Potential to be ready for pivotal studies by 2H 2027 Refractory Metastatic NSCLC 1 st line mPDAC treatment Metastatic Colorectal Cancer CPI Refractory, Metastatic Melanoma TAM: ~$4 billion TAM: ~$ 10 billion TAM: ~$12 billion TAM: ~$27 billion PDAC: https://www.fortunebusinessinsights.com/pancreatic - cancer - treatment - market - 101989 Melanoma: https://www.thebusinessresearchcompany.com/report/metastatic - melanoma - therapeutics - global - market - report CRC: https://www.gminsights.com/industry - analysis/colorectal - cancer - therapeutics - market NSCLC: https://www.databridgemarketresearch.com/reports/global - non - small - cell - lung - cancer - market

Elraglusib in Rare Pediatric Cancers

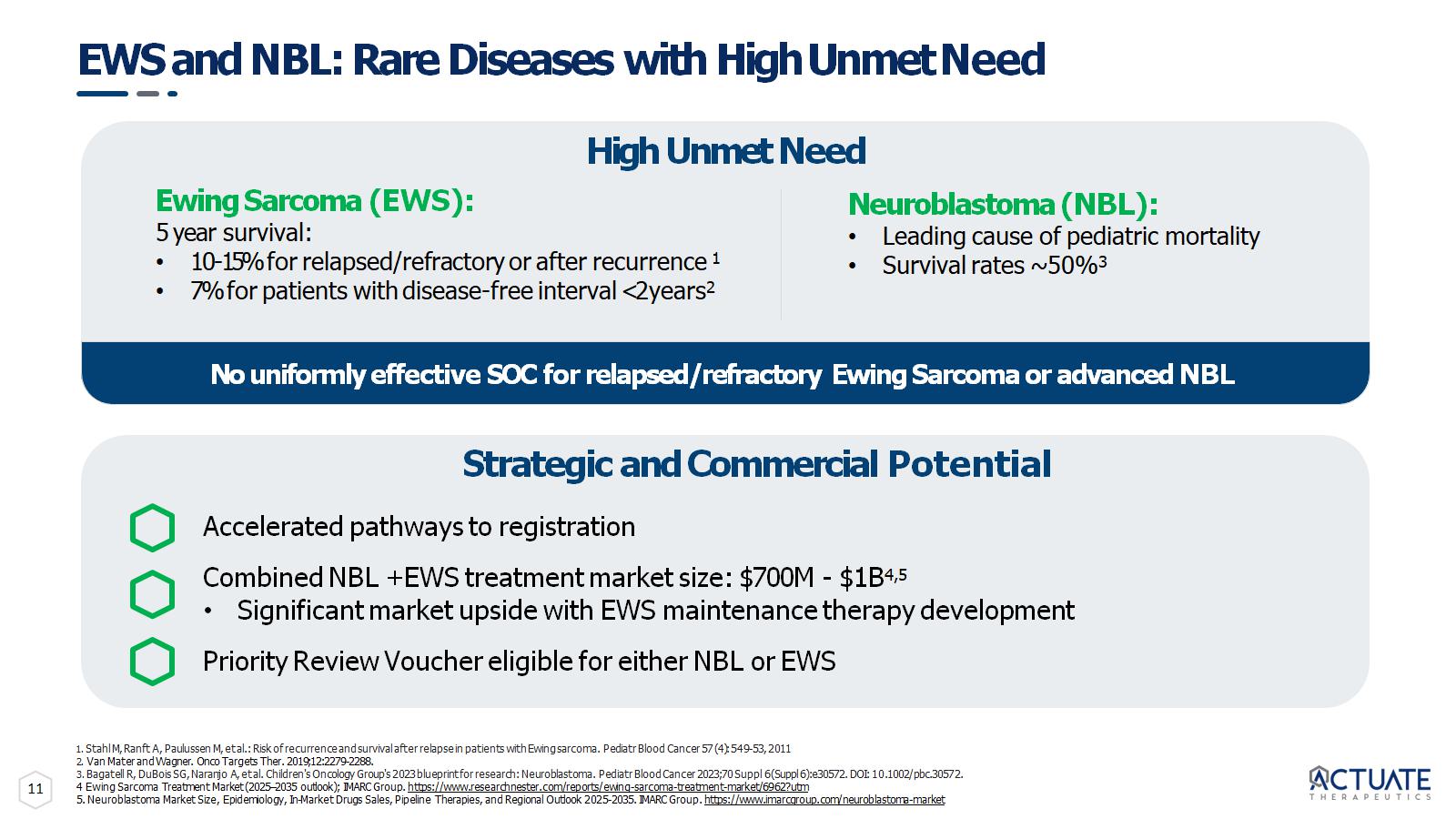

11 EWS and NBL: Rare Diseases with High Unmet Need 1. Stahl M, Ranft A, Paulussen M, et al.: Risk of recurrence and survival after relapse in patients with Ewing sarcoma. Pediatr Blood Cancer 57 (4): 549 - 53, 2011 2. Van Mater and Wagner. Onco Targets Ther. 2019;12:2279 - 2288. 3. Bagatell R, DuBois SG, Naranjo A, et al. Children's Oncology Group's 2023 blueprint for research: Neuroblastoma. Pediatr Blood Cancer 2023;70 Suppl 6(Suppl 6):e30572. DOI: 10.1002/pbc.30572. 4 Ewing Sarcoma Treatment Market (2025 – 2035 outlook); IMARC Group. https://www.researchnester.com/reports/ewing - sarcoma - treatment - market/6962?utm 5. Neuroblastoma Market Size, Epidemiology, In - Market Drugs Sales, Pipeline Therapies, and Regional Outlook 2025 - 2035. IMARC Group. https://www.imarcgroup.com/neuroblastoma - market Ewing Sarcoma (EWS): 5 year survival: • 10 - 15% for relapsed/refractory or after recurrence 1 • 7% for patients with disease - free interval <2 years 2 Strategic and Commercial Potential Accelerated pathways to registration Combined NBL + EWS treatment market size: $700M - $1B 4,5 • Significant market upside with EWS maintenance therapy development Priority Review Voucher eligible for either NBL or EWS Neuroblastoma (NBL): • Leading cause of pediatric mortality • Survival rates ~ 50% 3 High Unmet Need No uniformly effective SOC for relapsed/refractory Ewing Sarcoma or advanced NBL

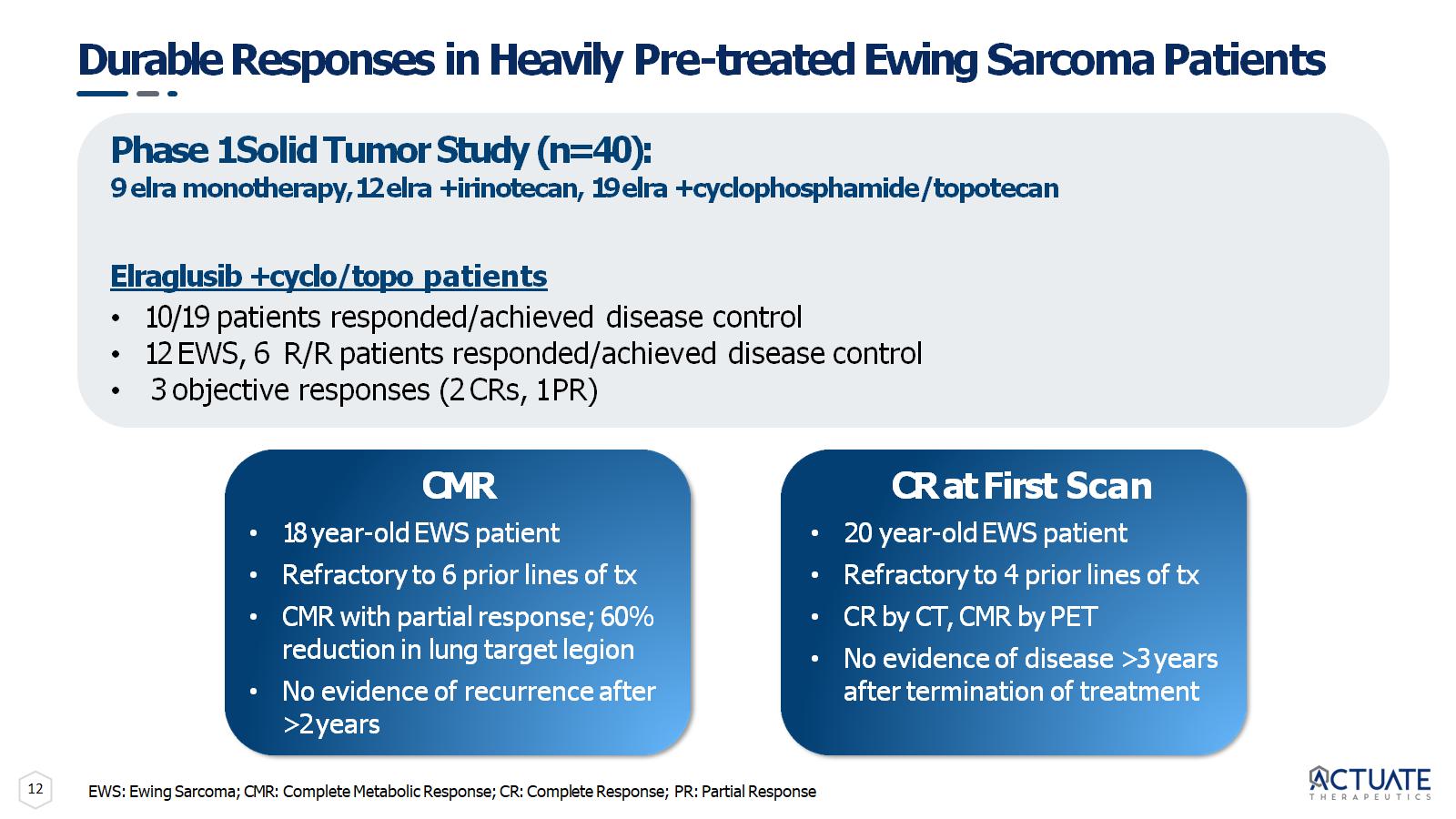

12 Durable Responses in Heavily Pre - treated Ewing Sarcoma Patients Phase 1 Solid Tumor Study (n=40): 9 elra monotherapy, 12 elra + irinotecan, 19 elra + cyclophosphamide/topotecan Elraglusib + cyclo/topo patients • 10/19 patients responded/achieved disease control • 12 EWS, 6 R/R patients responded/achieved disease control • 3 objective responses (2 CRs, 1 PR) CMR • 18 year - old EWS patient • Refractory to 6 prior lines of tx • CMR with partial response; 60% reduction in lung target legion • No evidence of recurrence after >2 years CR at First Scan • 20 year - old EWS patient • Refractory to 4 prior lines of tx • CR by CT, CMR by PET • No evidence of disease >3 years after termination of treatment EWS: Ewing Sarcoma; CMR: Complete Metabolic Response; CR: Complete Response; PR: Partial Response

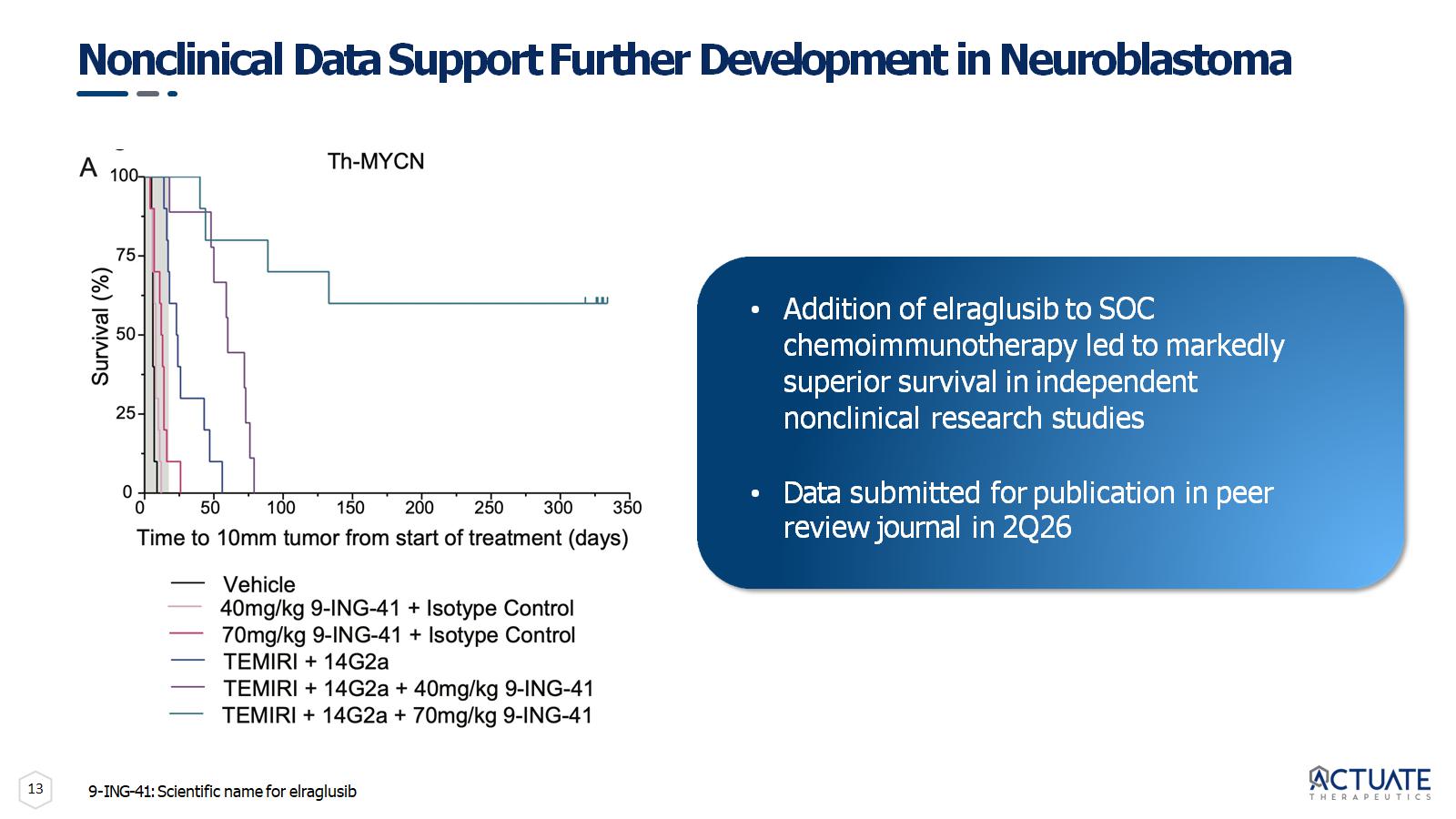

13 Nonclinical Data Support Further Development in Neuroblastoma • Addition of elraglusib to SOC chemoimmunotherapy led to markedly superior survival in independent nonclinical research studies • Data submitted for publication in peer review journal in 2Q26 9 - ING - 41: Scientific name for elraglusib

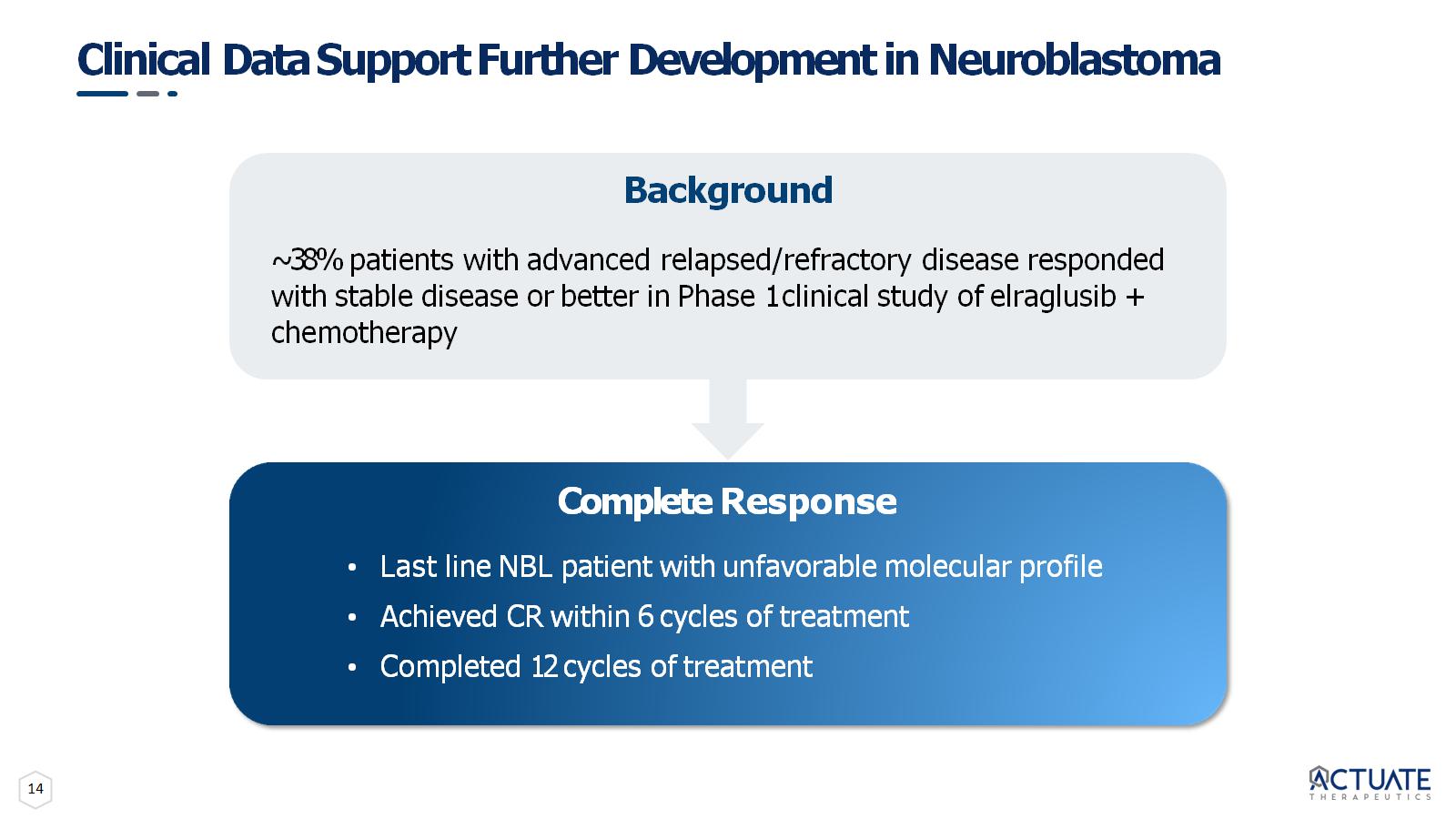

14 Clinical Data Support Further Development in Neuroblastoma Background ~38% patients with advanced relapsed/refractory disease responded with stable disease or better in Phase 1 clinical study of elraglusib + chemotherapy Complete Response • Last line NBL patient with unfavorable molecular profile • Achieved CR within 6 cycles of treatment • Completed 12 cycles of treatment

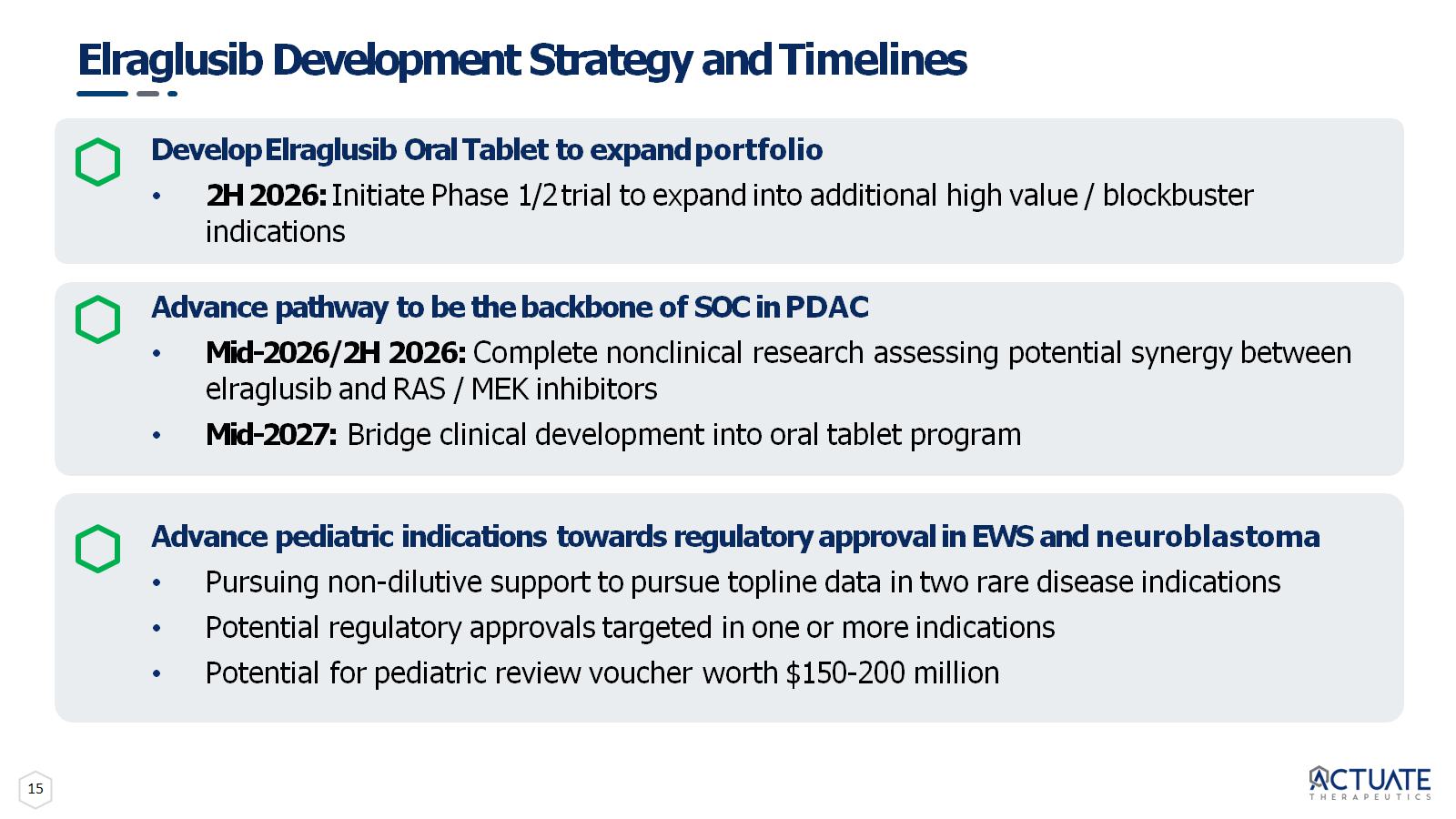

15 Elraglusib Development Strategy and Timelines Develop Elraglusib Oral Tablet to expand portfolio • 2H 2026: Initiate Phase 1/2 trial to expand into additional high value / blockbuster indications Advance pathway to be the backbone of SOC in PDAC • Mid - 2026/2H 2026: Complete nonclinical research assessing potential synergy between elraglusib and RAS / MEK inhibitors • Mid - 2027: Bridge clinical development into oral tablet program Advance pediatric indications towards regulatory approval in EWS and neuroblastoma • Pursuing non - dilutive support to pursue topline data in two rare disease indications • Potential regulatory approvals targeted in one or more indications • Potential for pediatric review voucher worth $150 - 200 million

16 Andrew Dorr, MD – VP, Clinical Development • Proven oncology drug development leader with senior roles in the development of multiple blockbuster therapies • COO (Salmedix), CMO (Isis/Ionis Pharmaceuticals), Medical Research Advisor (Eli Lilly), and former NCI leader • Extensive expertise in first - in - human studies, pivotal trial planning, and service on the Steering Committee of the Tamoxifen Breast Cancer Prevention Study; >70 peer - reviewed publications in cancer therapeutics • Eulexin, Taxol, Gemzar, Alimta, Treanda, Avastin, Talzenna Seasoned and Successful Leadership Experienced leadership team with demonstrated ability to develop and commercialize cancer drugs Daniel M. Schmitt – Chief Executive Officer and Founder • 30+ years of biotechnology and pharmaceutical experience across senior executive roles • Led and contributed to the successful development and launch of multiple pharmaceutical products • Exosurf, Zovirax, Valtrex, Adenoscan, Ambisome, Duraclon, Campath, Abraxane, enTrust • Executed ~1B+ in milestone value through licensing, acquisition, and development deals Andrew Mazar, PhD – Chief Operating Officer and Scientific Co - Founder • Co - founder, Chief Scientific Officer and Director, Monopar Therapeutics, Inc. (Nasdaq: MNPR) • Entrepreneur - in - Residence; Professor of Pharmacology; Founding Director, Center for Developmental Therapeutics, Northwestern University • Chief Scientific Officer, Attenuon, LLC • Internationally recognized expert in cancer metastasis and translational oncology • Eleven drugs from discovery through Phase 2 • >250 peer - reviewed publications and book chapters and inventor on >70 patents • Serial entrepreneur with seven start - ups founded Paul Lytle – Chief Financial Officer • 30+ years of finance and accounting experience • 25+ years of public company experience for Nasdaq listed companies • Served as co - founder, CFO, and director for multiple biotech companies • Raised in excess of $500 million in net proceeds from various equity and debt offerings

Nasdaq Global Market: ACTU