http://fasb.org/us-gaap/2026#LeaseholdImprovementsMember

Exhibit 99.1

BUUU GROUP LIMITED AND SUBSIDIARIES

INDEX TO UNAUDITED INTERIM CONDENSED CONSOLIDATED

FINANCIAL STATEMENTS

| |

|

Page |

| Unaudited Interim Condensed Consolidated Balance Sheets as of December 31, 2025 and June 30, 2025 |

|

F-2 |

| Unaudited Interim Condensed Consolidated Statements of Operations for the six months ended December 31, 2025, 2024 and 2023 |

|

F-3 |

| Unaudited Interim Condensed Consolidated Statements of Comprehensive (Loss) Income for the six months ended December 31, 2025, 2024 and 2023 |

|

F-4 |

| Unaudited Interim Condensed Consolidated Statements of Changes in Equity for the six months ended December 31, 2025, 2024 and 2023 |

|

F-5 |

| Unaudited Interim Condensed Consolidated Statements of Cash Flows for the six months ended December 31, 2025, 2024 and 2023 |

|

F-6 |

| Notes to the Unaudited Interim Condensed Consolidated Financial Statements |

|

F-7 – F-23 |

BUUU GROUP LIMITED AND SUBSIDIARIES

UNAUDITED INTERIM CONDENSED CONSOLIDATED BALANCE SHEETS

(Amounts expressed in US dollars (“$”) except for numbers of shares and par value)

| | |

As of | |

| | |

December 31, 2025 (unaudited) | | |

June 30, 2025 (audited) | |

| Assets | |

| | |

| |

| Current Assets: | |

| | |

| |

| Cash and cash equivalents | | $ | 5,715,857 | | | $ | 101,535 | |

| Trade receivables | | | 1,227,833 | | | | 1,320,983 | |

| Deposits, prepayments and other current assets | | | 180,345 | | | | 172,299 | |

| Contract assets | | | 405,318 | | | | 571,982 | |

| Deferred initial public offering (“IPO”) costs | | | — | | | | 204,964 | |

| Total Current Assets | | | 7,529,353 | | | | 2,371,763 | |

| | |

| | | |

| | |

| Non-Current Assets: | |

| | | |

| | |

| Property, plant and equipment, net | | | 152,699 | | | | 69,684 | |

| Right of use assets – operating lease | | | 130,612 | | | | 42,084 | |

| Cash surrender value of life insurance policies | | | 56,081 | | | | 55,587 | |

| Deferred tax assets, net | | | — | | | | 123 | |

| Total Non-Current Assets | | | 339,392 | | | | 167,478 | |

| Total Assets | | $ | 7,868,745 | | | $ | 2,539,241 | |

| | |

| | | |

| | |

| Liabilities and Equity | |

| | | |

| | |

| Current Liabilities: | |

| | | |

| | |

| Trade payables | | $ | 633,996 | | | $ | 318,350 | |

| Other payables and accruals | | | 105,540 | | | | 139,528 | |

| Advance from customers | | | 37,741 | | | | 21,212 | |

| Bank borrowings | | | 384,396 | | | | 432,101 | |

| Current portion of operating lease liabilities | | | 65,626 | | | | 42,830 | |

| Loan payables | | | — | | | | 180,000 | |

| Current portion of finance lease liabilities | | | 57,314 | | | | 26,585 | |

| Income tax payable | | | 308,371 | | | | 316,724 | |

| Total Current Liabilities | | | 1,592,984 | | | | 1,477,330 | |

| | |

| | | |

| | |

| Non-Current Liabilities: | |

| | | |

| | |

| Deferred tax liabilities, net | | | 295 | | | | — | |

| Operating lease liabilities | | | 65,037 | | | | — | |

| Finance lease liabilities | | | 62,996 | | | | 18,364 | |

| Total Non-Current Liabilities | | | 128,328 | | | | 18,364 | |

| Total Liabilities | | $ | 1,721,312 | | | $ | 1,495,694 | |

| | |

| | | |

| | |

| Equity | |

| | | |

| | |

| Share capital* (500,000,000 shares authorized, no-par value, 11,695,000 and 10,000,000 Class A shares issued and outstanding as of December 31, 2025 and June 30, 2025, respectively, 5,000,000 and 5,000,000 Class B shares issued and outstanding as of December 31, 2025 and June 30, 2025, respectively) | | $ | 5,538,141 | | | $ | 19,823 | |

| Subscription receivable | | | (19,801 | ) | | | (19,801 | ) |

| Additional paid-in capital | | | 422,991 | | | | — | |

| Retained earnings | | | 120,106 | | | | 1,021,335 | |

| Accumulated other comprehensive income (loss) | | | 25,561 | | | | (12,642 | ) |

| Capital and reserves attributable to equity holders of the Company | | | 6,086,998 | | | | 1,008,715 | |

| Non-controlling interests | | | 60,435 | | | | 34,832 | |

| Total Equity | | | 6,147,433 | | | | 1,043,547 | |

| Total Liabilities and Equity | | $ | 7,868,745 | | | $ | 2,539,241 | |

| * | Retrospectively presented for the effect of 15,000,000 shares issued on various dates between April 16, 2024 and November 18, 2024 in preparation of the Company’s initial public offering (Note 1). |

The accompanying notes are an integral part

of these unaudited interim condensed consolidated financial statements.

BUUU GROUP LIMITED AND SUBSIDIARIES

UNAUDITED INTERIM CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

| | |

Six Months Ended

December 31, | |

| | |

2025 (unaudited) | | |

2024 (unaudited) | | |

2023 (unaudited) | |

| Revenue | | $ | 3,222,435 | | | $ | 2,868,494 | | | $ | 2,926,578 | |

| Cost of revenue | | | (2,870,376 | ) | | | (2,120,486 | ) | | | (2,210,424 | ) |

| Gross profit | | | 352,059 | | | | 748,008 | | | | 716,154 | |

| | |

| | | |

| | | |

| | |

| Operating expenses | |

| | | |

| | | |

| | |

| General administrative expenses | | | (1,234,567 | ) | | | (519,272 | ) | | | (220,831 | ) |

| (Loss) profit from operations | | | (882,508 | ) | | | 228,736 | | | | 495,323 | |

| | |

| | | |

| | | |

| | |

| Other income, net | | | 31,570 | | | | 1,077 | | | | 957 | |

| Finance costs | | | (17,514 | ) | | | (10,279 | ) | | | (12,766 | ) |

| (Loss) income before income tax | | | (868,452 | ) | | | 219,534 | | | | 483,514 | |

| Provision for income tax expense | | | (7,541 | ) | | | (58,965 | ) | | | (48,060 | ) |

| Net (loss) income for the period | | | (875,993 | ) | | | 160,569 | | | | 435,454 | |

| Less: Net income attributable to non-controlling interests | | | (25,236 | ) | | | (4,105 | ) | | | (24,393 | ) |

| Net (loss) income attributable to equity holders of the Company | | $ | (901,229 | ) | | $ | 156,464 | | | $ | 411,061 | |

| | |

| | | |

| | | |

| | |

| Basic and diluted (loss) earnings per ordinary share | | $ | (0.06 | ) | | $ | 0.01 | | | $ | 0.03 | |

| | |

| | | |

| | | |

| | |

| Weighted average number of ordinary shares outstanding | | | 16,243,071 | * | | | 15,000,000 | * | | | 15,000,000 | * |

| * | Retrospectively presented for the effect of 15,000,000 shares issued on various dates between April 16, 2024 and November 18, 2024 in preparation of the Company’s initial public offering (Note 1). |

The accompanying notes are an integral part

of these unaudited interim condensed consolidated financial statements.

BUUU GROUP LIMITED AND SUBSIDIARIES

UNAUDITED INTERIM CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE (LOSS) INCOME

(Amounts expressed in US dollars (“$”) except for numbers of shares)

| | |

Six Months Ended

December 31, | |

| | |

2025 (unaudited) | | |

2024 (unaudited) | | |

2023 (unaudited) | |

| Net (loss) income for the period | | $ | (875,993 | ) | | $ | 160,569 | | | $ | 435,454 | |

| Currency translation differences | | | 38,570 | | | | 7,994 | | | | 2,305 | |

| Total comprehensive (loss) income for the period | | $ | (837,423 | ) | | $ | 168,563 | | | $ | 437,759 | |

| | |

| | | |

| | | |

| | |

| Attributable to: | |

| | | |

| | | |

| | |

| Equity holders of the Company | | | (863,026 | ) | | $ | 164,977 | | | $ | 413,462 | |

| Non-controlling interests | | | 25,603 | | | | 3,586 | | | | 24,297 | |

| Total comprehensive (loss) income for the period | | $ | (837,423 | ) | | $ | 168,563 | | | $ | 437,759 | |

The accompanying notes are an integral part

of these unaudited interim condensed consolidated financial statements.

BUUU GROUP LIMITED AND SUBSIDIARIES

UNAUDITED INTERIM CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN EQUITY

(Amounts expressed in US dollars (“$”) except for numbers of shares)

| | |

For the six months ended December 31, 2023 | |

| | |

Ordinary Shares | | |

| | |

Accumulated | | |

| | |

| | |

| |

| | |

Number of

Shares* | | |

Amount

(no-par

value)* | | |

Subscription

Receivable | | |

Other

Comprehensive

(Loss) Income | | |

Retained

Earnings | | |

Non-

Controlling

Interests | | |

Total

Equity | |

| Balance as of June 30, 2023 (audited) | | | 15,000,000 | | | $ | 19,823 | | | $ | (19,801 | ) | | $ | (455 | ) | | $ | 431,994 | | | $ | 53,809 | | | $ | 485,370 | |

| Disposal of BU Production (Note 10) | | | — | | | | — | | | | — | | | | — | | | | — | | | | (26,546 | ) | | | (26,546 | ) |

| Net income for the period | | | — | | | | — | | | | — | | | | — | | | | 411,061 | | | | 24,393 | | | | 435,454 | |

| Foreign currency translation | | | — | | | | — | | | | — | | | | 2,401 | | | | — | | | | (96 | ) | | | 2,305 | |

| Balance as of December 31, 2023 (unaudited) | | | 15,000,000 | | | $ | 19,823 | | | $ | (19,801 | ) | | $ | 1,946 | | | $ | 843,055 | | | $ | 51,560 | | | $ | 896,583 | |

| | |

For

the six months ended December 31, 2024 | |

| | |

Ordinary Shares | | |

| | |

Accumulated | | |

| | |

| | |

| |

| | |

Number of

Shares* | | |

Amount

(no-par

value)* | | |

Subscription

Receivable | | |

Other

Comprehensive

Income | | |

Retained

Earnings | | |

Non-

Controlling

Interests | | |

Total

Equity | |

| Balance as of June 30, 2024 (audited) | | | 15,000,000 | | | $ | 19,823 | | | $ | (19,801 | ) | | $ | 2,676 | | | $ | 1,266,145 | | | $ | 73,198 | | | $ | 1,342,041 | |

| Net income for the period | | | — | | | | — | | | | — | | | | — | | | | 156,464 | | | | 4,105 | | | | 160,569 | |

| Foreign currency translation | | | — | | | | — | | | | — | | | | 8,513 | | | | — | | | | (519 | ) | | | 7,994 | |

| Dividend declared during the period | | | — | | | | — | | | | — | | | | — | | | | (1,049,158 | ) | | | (45,056 | ) | | | (1,094,214 | ) |

| Balance as of December 31, 2024 (unaudited) | | | 15,000,000 | | | $ | 19,823 | | | $ | (19,801 | ) | | $ | 11,189 | | | $ | 373,451 | | | $ | 31,728 | | | $ | 416,390 | |

| | |

For the six months ended December 31, 2025 | |

| | |

Ordinary Shares | | |

| | |

| | |

Accumulated | | |

| | |

| | |

| |

| | |

Number of

Shares* | | |

Amount

(no-par

value)* | | |

Subscription

Receivable | | |

Additional

Paid-In

Capital | | |

Other

Comprehensive

(Loss) Income | | |

Retained

Earnings | | |

Non-

Controlling

Interests | | |

Total

Equity | |

| Balance as of June 30, 2025 (audited) | | | 15,000,000 | | | $ | 19,823 | | | $ | (19,801 | ) | | $ | — | | | $ | (12,642 | ) | | $ | 1,021,335 | | | $ | 34,832 | | | $ | 1,043,547 | |

| Net loss (income) for the period | | | — | | | | — | | | | — | | | | — | | | | — | | | | (901,229 | ) | | | 25,236 | | | | (875,993 | ) |

| Foreign currency translation | | | — | | | | — | | | | — | | | | — | | | | 38,203 | | | | — | | | | 367 | | | | 38,570 | |

| Issuance of ordinary shares pursuant to the IPO, net of offering cost | | | 1,675,000 | | | | 5,350,318 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 5,350,318 | |

| Issuance of ordinary shares under 2025 equity incentive plan | | | 20,000 | | | | 168,000 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 168,000 | |

| Share-based compensation | | | — | | | | — | | | | — | | | | 422,991 | | | | — | | | | — | | | | — | | | | 422,991 | |

| Balance as of December 31, 2025 (unaudited) | | | 16,695,000 | | | $ | 5,538,141 | | | $ | (19,801 | ) | | $ | 422,991 | | | $ | 25,561 | | | $ | 120,106 | | | $ | 60,435 | | | $ | 6,147,433 | |

| * | Retrospectively presented for the effect of 15,000,000 shares issued on various dates between April 16, 2024 and November 18, 2024 in preparation of the Company’s initial public offering (Note 1). |

The accompanying notes are an integral part

of these unaudited interim condensed consolidated financial statements.

BUUU GROUP LIMITED AND SUBSIDIARIES

UNAUDITED INTERIM CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Amounts expressed in US dollars (“$”)

| | |

Six Months Ended

December 31, | |

| | |

2025 (unaudited) | | |

2024 (unaudited) | | |

2023 (unaudited) | |

| Cash Flows From Operating Activities: | |

| | |

| | |

| |

| Net (loss) income for the period | | $ | (875,993 | ) | | $ | 160,569 | | | $ | 435,454 | |

| Adjustments to reconcile net income to net cash used in (generated from) operating activities: | |

| | | |

| | | |

| | |

| Depreciation of property, plant and equipment | | | 25,247 | | | | 23,468 | | | | 24,064 | |

| Lease expenses | | | 36,749 | | | | 35,214 | | | | 15,304 | |

| Finance costs | | | 17,514 | | | | 10,279 | | | | 12,766 | |

| Deferred income tax | | | 418 | | | | 292 | | | | 149 | |

| Gain on disposal of property, plant and equipment | | | (898 | ) | | | — | | | | — | |

| Loss on lease modification | | | 1,323 | | | | — | | | | — | |

| Share-based compensation | | | 590,991 | | | | — | | | | — | |

| | |

| | | |

| | | |

| | |

| Changes in operating assets and liabilities: | |

| | | |

| | | |

| | |

| Trade receivables | | | 104,656 | | | | (191,795 | ) | | | (689,224 | ) |

| Deposits, prepayments and other current assets | | | (6,496 | ) | | | (158,486 | ) | | | (130,344 | ) |

| Contract asset | | | 171,343 | | | | (174,883 | ) | | | (53,236 | ) |

| Trade payables | | | 312,063 | | | | 522,017 | | | | 448,655 | |

| Other payables and accruals | | | (41,414 | ) | | | 686 | | | | 96,543 | |

| Advance from customers | | | 16,301 | | | | 11,316 | | | | (8,965 | ) |

| Operating lease liabilities | | | (38,772 | ) | | | (36,986 | ) | | | (14,770 | ) |

| Income tax payable | | | (11,144 | ) | | | 58,672 | | | | 47,911 | |

| Amounts due with related parties | | | — | | | | 203,955 | | | | (156,636 | ) |

| Net Cash Provided By Operating Activities | | | 301,888 | | | | 464,318 | | | | 27,671 | |

| | |

| | | |

| | | |

| | |

| Cash Flows From Investing Activities: | |

| | | |

| | | |

| | |

| Acquisition of property, plant and equipment | | | — | | | | — | | | | (3,708 | ) |

| Proceeds from disposal of property, plant and equipment | | | 898 | | | | — | | | | — | |

| Disposal of a subsidiary, net of cash disposed | | | — | | | | — | | | | (1,599 | ) |

| Net Cash Provided By (Used In) Investing Activities | | | 898 | | | | — | | | | (5,307 | ) |

| | |

| | | |

| | | |

| | |

| Cash Flows From Financing Activities: | |

| | | |

| | | |

| | |

| Payment of dividend to shareholders* | | | — | | | | (508,205 | ) | | | — | |

| Proceeds from loan payables | | | — | | | | 180,000 | | | | — | |

| Repayment of loan payables | | | (180,000 | ) | | | — | | | | — | |

| Repayment of bank borrowings | | | (57,440 | ) | | | (60,941 | ) | | | (48,591 | ) |

| Payment of finance lease liabilities | | | (36,838 | ) | | | (14,108 | ) | | | (14,049 | ) |

| Proceeds from issuance of ordinary shares pursuant to IPO, net of offering cost | | | 5,804,648 | | | | — | | | | — | |

| Payments of offering costs related to initial public offering | | | (249,366 | ) | | | (119,969 | ) | | | — | |

| Net Cash Provided By (Used In) Financing Activities | | | 5,281,004 | | | | (523,223 | ) | | | (62,640 | ) |

| | |

| | | |

| | | |

| | |

| Effect of movements in exchange rates on cash held | | | 30,532 | | | | 2,703 | | | | 1,788 | |

| | |

| | | |

| | | |

| | |

| Net changes in cash | | | 5,614,322 | | | | (56,202 | ) | | | (38,488 | ) |

| Cash at beginning of the period | | | 101,535 | | | | 448,888 | | | | 515,931 | |

| Cash at end of the period | | $ | 5,715,857 | | | $ | 392,686 | | | $ | 477,443 | |

| | |

| | | |

| | | |

| | |

| Supplemental Disclosure of Cash Flow Information: | |

| | | |

| | | |

| | |

| Cash paid for interest | | $ | 17,514 | | | $ | 10,984 | | | $ | 12,766 | |

| Cash paid for taxes | | $ | 18,267 | | | | — | | | | — | |

| | |

| | | |

| | | |

| | |

| Supplemental Disclosure of Non-Cash Financing Activities: | |

| | | |

| | | |

| | |

| Property, plant and equipment obtained in exchange of new finance lease liabilities | | $ | 107,445 | | | | — | | | | — | |

| * | A special dividend of $1,082,817 was declared on September 1, 2024 and of which $574,745 was offset with the amount due from related parties. |

The accompanying notes are an integral part

of these unaudited interim condensed consolidated financial statements.

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 1. Organization and nature of operations

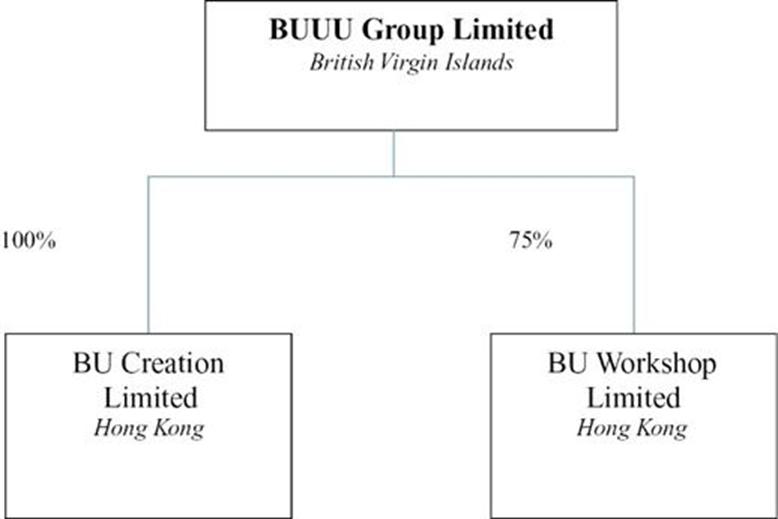

BUUU Group Limited (“BUUU” or the “Company”) is a business company established under the laws of the British Virgin Islands on April 16, 2024. It is a holding company with no business operation. It is authorised to issue a maximum of 500,000,000 no par value shares divided into (i) 250,000,000 Class A Ordinary Shares with no par value each and (ii) 250,000,000 Class B Ordinary Shares with no par value each. On August 13, 2025, the Company was listed on the Nasdaq Capital Market and began trading under the ticker symbol “BUUU”.

The Company, through its subsidiaries incorporated and domiciled in Hong Kong (collectively referred to as the “Company”), specializes in all aspects of the design, planning and production of face-to-face events, immersive environments and brand-based experiences for clients and venues, including event organizers, consumer brand marketers and retail shopping centers.

BU Creation Limited (“BU Creation”) was incorporated in Hong Kong under the Hong Kong Companies Ordinance (Chapter 622) on May 11, 2017. BU Creation is a 100% owned subsidiary of BUUU. BU Creation engages principally in providing fully integrated event design, event planning, event production, and on-site event management services.

BU Workshop Limited (“BU Workshop”) was incorporated in Hong Kong under the Hong Kong Companies Ordinance (Chapter 622) on September 13, 2019. BU Workshop is a 75% owned subsidiary of BUUU. BU Workshop engages principally in stage production services, including merchandizing and selling event set furniture and decor.

BU Production Limited (“BU Production”) was incorporated in Hong Kong under the Hong Kong Companies Ordinance (Chapter 622) on February 14, 2023. BU Production is a 50% owned subsidiary of BU Workshop, where BU Workshop had majority voting rights to control. BU Production engages principally in the production of event set furniture and decor, including props, backdrops, and stages, substantially for BU Workshop. On September 25, 2023, BU Workshop fully disposed of this investment.

Reorganization

On October 17, 2024, BUUU resolved and approved to increase the maximum number of shares it is authorized to issue from 50,000 with no par value to 500,000,000 with no par value. On the same day, BUUU resolved and approved to re-designate (a) 249,999,999 authorized but unissued ordinary shares of no par value into 249,999,999 Class A ordinary shares (“Class A Ordinary Shares”) of no par value; and (b) 250,000,000 authorized but unissued ordinary shares of no par value into 250,000,000 Class B ordinary shares (“Class B Ordinary Shares”) of no par value, and re-designate a total of 1 issued ordinary shares of no par value owned by BUBI Services Limited (“BUBI Services”) into 1 Class A Ordinary Shares of no par value.

On October 22, 2024, 6,039,999 Class A Ordinary Shares were issued and allotted to BUBI Services at a total consideration of US$1. On November 7, 2024, A Max Holding Limited, Glitter Win International Limited, Tight Core Limited, Storm Citadel Global Limited and Virtuous Accolade Limited, subscribed for and were allotted 3,960,000 Class A ordinary shares representing approximately 25.0%, 4.8%, 4.8%, 1.0% and 4.0% of the issued share capital of BUUU. On November 18, 2024, under a share swap arrangement (the “Share Swap”), Ms. Nana CHAN, Mr. Wai Kwong POON and Perfect Wood Limited transferred their entire shareholding interest in BU Creation and BU Workshop to BUUU, in consideration of the allotment and issue an aggregate of 5,000,000 Class B ordinary shares to BUBI Services, credited as fully paid. Following the Share Swap, BU Creation and BU Workshop became a subsidiary of BUUU.

On December 13, 2024, pursuant to a sale and purchase agreement entered into between Glitter Win International Limited and Excellent Prospect Investment Holding Limited, Excellent Prospect Investment Holding Limited has acquired 480,000 Class A Ordinary Shares from Glitter Win International Limited, representing 4.8% of the Class A Ordinary Shares in issue of BUUU.

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 1. Organization and nature of operations (cont.)

The following diagram illustrates the Company’s legal entity ownership structure after the reorganization as of December 31, 2025:

Note 2. Significant Accounting Policies

The following is a summary of significant accounting policies used in the preparation of these unaudited interim condensed consolidated financial statements.

2.1 Basis of presentation and going concern

The unaudited interim condensed consolidated financial statements are prepared on the basis as if the reorganization became effective as of the beginning of the first period presented in the accompanying unaudited interim condensed consolidated financial statements in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). In the opinion of management, the unaudited interim condensed consolidated financial statements reflect all adjustments of a normal recurring nature that are necessary for a fair presentation of the results for the interim periods presented. The results of operations for the six months ended December 31, 2025 are not necessarily indicative of results to be expected for the full year ending June 30, 2026. Accordingly, these unaudited interim condensed consolidated financial statements should be read in conjunction with the Company’s audited financial statements as of and for the years ended June 30, 2025 and 2024.

The unaudited interim condensed consolidated financial statements include the financial statements of the Company and all its majority-owned subsidiaries from the dates they were incorporated. All intercompany balances and transactions have been eliminated on consolidation.

These unaudited interim condensed consolidated financial statements have been prepared on a going concern basis, which assumes that the Company will be able to continue in operation for the foreseeable future and will be able to realize its assets and discharge its liabilities and commitments in the normal course of business. Management of the Company is satisfied that the Company’s operating profit has provided the Company adequate financial resources to continue in operational existence for the foreseeable future, a period of at least 12 months from the date of this report.

2.2 Basis of consolidation

The Company and its subsidiaries resulting from Reorganization has always been under the common control of the same controlling shareholders before and after the Reorganization. Accordingly, the combination of these entities has been accounted for as a reorganization of entities under common control in accordance with ASC 805 guidelines, whereby the resulting controlling entity, namely, BUUU recognized the assets and liabilities of the Subsidiaries transferred at their carrying amounts with a carry-over basis. The reorganization of entities under common control was retrospectively applied to the financial statements of all prior periods when the financial statements are issued for a period that includes the date the share exchange transaction occurred.

Equity interests in BU Workshop held by parties other than BUUU are presented as non-controlling interests in equity.

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 2. Significant Accounting Policies (cont.)

2.3 Use of estimates

The preparation of the unaudited interim condensed consolidated financial statements in conformity with U.S. GAAP requires the management of the Company to make estimates and assumptions relating to the reported amounts of assets and liabilities and the disclosures of contingent assets and liabilities at the balance sheet dates and the reported amounts of revenue and expenses during the reporting periods. Areas involving significant estimates and assumptions include revenue recognition for contracts, expected credit loss assessment, determination of useful lives of property, plant and equipment, principles of consolidation and reverse recapitalization. Actual results could differ from those estimates. These estimates are reviewed periodically, and as adjustments become necessary, they are reported in earnings in the period in which they become known.

2.4 Foreign currency translation

The reporting currency of the Company is United States Dollar (“USD”) and the accompanying unaudited interim condensed consolidated financial statements have been expressed in “$”. The Company’s operating subsidiaries are based in Hong Kong, with its books and records maintained in its local currency, the Hong Kong Dollar (“HKD”), which is the functional currency as being the primary currency of the economic environment in which their operations are conducted. In general, for consolidation purposes, assets and liabilities of its subsidiaries whose functional currency is not USD are translated into USD, in accordance with ASC Topic 830-30, “Translation of Financial Statement”, using the exchange rate on the balance sheet date. Shareholders’ equity is translated using the historical rates and adjustments resulting from the translation, if any, are included in accumulated other comprehensive income or loss. Revenue and expenses are translated at average rates prevailing during the years. The gains and losses resulting from the translation of financial statements of foreign subsidiaries are recorded as a separate component of accumulated other comprehensive income within the statements of changes in shareholders’ equity.

The currency exchange rates were utilized as follows:

| | | December 31,

2025 | | | June 30,

2025 | |

| Period-end HKD exchange rate | | | 0.1285 | | | | 0.1274 | |

| | | Six Months Ended December 31, | |

| | | 2025 | | | 2024 | | | 2023 | |

| Period average HKD exchange rate | | | 0.1282 | | | | 0.1284 | | | | 0.1279 | |

2.5 Cash and cash equivalents

The Company considers all highly liquid investments purchased with original maturities of three months or less to be cash equivalents. As of December 31, 2025 and June 30, 2025, substantially all the Company’s cash and cash equivalents were deposited with financial institutions with high credit ratings and quality.

2.6 Deposits, prepayments and other current assets

Deposits, prepayments and other current assets primarily consists of advances to suppliers for purchasing furniture and decor, rental deposits made to the landlord, prepaid expenses and other receivables. Deposits, prepayments and other current assets are classified as either current or non-current based on the terms of the respective agreements. These advances are unsecured and are reviewed periodically to determine whether their carrying value has become impaired.

2.7 Trade receivables

Trade receivables are recorded at the invoiced amount less expected credit losses as needed.

To estimate expected credit losses, the Company has identified the relevant risk characteristics of its customers and considers past collection experience, current economic conditions, and expected future economic conditions. The Company did not record provision for expected credit losses for the six months ended December 31, 2025, 2024 and 2023.

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 2. Significant Accounting Policies (cont.)

2.8 Property, plant and equipment, net

Property, plant and equipment are stated at cost less accumulated depreciation and accumulated impairment losses. Cost represents the purchase price of the asset and other costs incurred to bring the asset into its existing use. Maintenance and repairs are charged to general administrative expenses; major additions to improve service potential or extend economic life are capitalized.

Depreciation of property, plant and equipment is computed using the straight-line method over the estimated useful lives of the assets with no residual value. The estimated useful lives are as follows:

| | | Useful life |

| Motor vehicles | | 5 years |

| Furniture and fixtures | | 4 years |

| Computer equipments | | 4 years |

| Leasehold improvements | | Shorter of useful life or remaining lease term |

2.9 Impairment of Long-Lived Assets

The Company tests its long-lived assets for impairment at least annually and whenever events or circumstances change that indicate impairment may have occurred. A significant amount of judgment is involved in determining if an indicator of impairment has occurred. Such indicators may include, among others and without limitation: a significant decline in the Company’s expected future cash flows; a significant adverse change in legal factors or in the business climate of the Company’s operations; unanticipated competition; and slower growth rates. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss (if any). Where it is not possible to estimate the recoverable amount of an individual asset, the Company estimates the recoverable amount of the cash-generating unit to which the asset belongs.

2.10 Life insurance policies

In September 2022 and February 2023, the Company purchased two life insurance policies (the “policies”) on a director that the Company is the policyholder and are recorded at the amount that can be realized under the insurance contracts at the balance sheet date, which is the cash surrender value adjusted for other charges or other amounts due that are probable at settlement. The Company may terminate the policies at any time and receive the cash surrender value at the date of withdrawal calculated by the insurance company. The gain or loss related to the change in cash value of these life insurance policies at the balance sheet date is recorded as other income under the Company’s unaudited interim condensed consolidated statements of operations.

As of December 31, 2025 and June 30, 2025, the cash surrender values of the life insurance policies of $56,081 and $55,587 were measured at fair value (Note 2.13) and classified as non-current assets.

2.11 Leases

The Company leases all the office space, warehouse and motor vehicles to conduct the business. Leases are classified as either finance leases or operating leases. A lease is classified as a finance lease if any one of the following criteria is met: the lease transfers ownership of the asset by the end of the lease term, the lease contains an option to purchase the asset that is reasonably certain to be exercised, the lease term is for a major part of the remaining useful life of the asset or the present value of the lease payments equals or exceeds substantially all of the fair value of the asset. A lease is classified as an operating lease if it does not meet any one of these criteria. The Company’s operating leases are comprised of office space and warehouse leases, and finance leases are comprised of motor vehicles.

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 2. Significant Accounting Policies (cont.)

The Company recognizes a lease liability and a right-of-use (“ROU”) asset at the commencement date of a lease. A lease liability is initially measured as the Company’s obligation for the future fixed lease payments that will be made over the lease term, measured on a discounted basis. An ROU asset is an asset that represents the Company’s right to use or control the use of specified assets for the lease term. The lease term includes periods for which it’s reasonably certain that the renewal options will be exercised and periods for which it’s reasonably certain that the termination options will not be exercised. The future fixed lease payments are discounted using the rate implicit in the lease. If the rate implicit in the leases is not readily determinable, the lessee should use the incremental borrowing rate as the discount rate, which approximates the interest rate at which the lessee could borrow on a collateralized basis with similar terms and payments and in similar economic environments. The Company elected not to recognize any leases with lease terms of 12 months or less at the commencement date in the unaudited interim condensed consolidated balance sheets.

The ROU asset is subsequently measured at the amount of the lease liability with adjustments, if applicable. The Company will evaluate the carrying value of ROU assets if there are indicators of impairment and review the recoverability of the related asset group. If the carrying value of the asset group is determined to not be recoverable and is in excess of the estimated fair value, the Company will record an impairment loss in other expenses in the unaudited interim condensed consolidated statements of operations.

Operating leases are included in operating lease ROU assets and operating lease liabilities in the unaudited interim condensed consolidated balance sheets. Operating lease liabilities that become due within one year of the balance sheet date are classified as current portion of operating lease liabilities. Finance leases are included in motor vehicles and finance lease liabilities in the unaudited interim condensed consolidated balance sheets. Finance lease liabilities that become due within one year of the balance sheet date are classified as current portion of finance lease liabilities.

Lease expense for operating leases consists of the fixed lease payments recognized on a straight-line basis over the lease term. Lease expense for finance leases consists of the amortization of the right-of-use asset over the shorter of the lease term or useful life of the underlying asset. Interest accretion on the finance lease liabilities is recorded as finance costs. For both operating and finance leases, lease expense related to variable payments is recognized as incurred based on performance or usage in accordance with the contractual agreements.

2.12 Trade payables, other payables and accruals

Trade payables, other payables and accruals are liabilities for unpaid goods and services provided to the Company prior to the end of each reporting period. They are recognized initially at their fair value and subsequently measured at amortized cost using the effective interest method. They are classified as current liabilities if payment is due within one year or less. If not, they are presented as non-current liabilities.

2.13 Fair value measurements

The Company uses a three-tier fair value hierarchy to classify and disclose all assets and liabilities measured at fair value on a recurring basis, as well as assets and liabilities measured at fair value on a non-recurring basis, in periods subsequent to their initial measurement. The hierarchy requires the Company to use observable inputs when available and to minimize the use of unobservable inputs when determining fair value. The three tiers are defined as follows:

| ● | Level 1 — Observable inputs that reflect quoted market prices (unadjusted) for identical assets or liabilities in active markets; |

| ● | Level 2 — Observable inputs other than quoted prices in active markets that are observable either directly or indirectly in the marketplace for identical or similar assets and liabilities; and |

| ● | Level 3 — Unobservable inputs that are supported by little or no market data, which require the Company to develop its own assumptions. |

The cash surrender value of life insurance policies is classified as Level 2. The value was determined by inputs that are readily available in a public market or can be derived from information available in publicly quoted markets. These inputs include the underwriting insurance company’s valuation models, which take into account the passage of time, mortality tables, interest rates, cash values for paid-up additions and dividend accumulations. The cash surrender value represents the guaranteed value the Company would receive upon surrender of these policies held on a director as of December 31, 2025 and June 30, 2025. The fair value of the life insurance policies is marked to market at each reporting period and any changes in fair value is reflected in the unaudited interim condensed consolidated statements of operations for that period.

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 2. Significant Accounting Policies (cont.)

The carrying values of the Company’s financial instruments, including cash, trade receivables, deposits, prepayments and other assets, trade payables, other payables and accruals, approximate their fair values as of December 31, 2025 and June 30, 2025 due to the short-term nature of these instruments.

2.14 Revenue from contracts with customers

The Company adopts Accounting Standards Update (“ASU”) 2014-09, Revenue from Contracts with Customers (ASC Topic 606) for all periods presented and determines revenue recognition by applying the following five-step model:

| ● | Identification of the contract, or contracts, with a customer; |

| ● | Identification of the performance obligations in the contract; |

| ● | Determination of the transaction price; |

| ● | Allocation of the transaction price to the performance obligations in the contract; and |

| ● | Recognition of revenue when, or as, the Company satisfies a performance obligation. |

Segment reporting

In accordance with ASC 280, Segment Reporting, the Company is required to report financial and descriptive information about its reportable segments. Reportable segments are operating segments or aggregations of operating segments that meet specific quantitative thresholds. The identification of operating segments is based on the internal reporting used by the Chief Operating Decision Maker (“CODM”) to assess performance and allocate resources.

The Company has determined that it operates as a single operating and reportable segment. This conclusion is based on the following considerations:

| ● | The Company is managed as a single business, with a single set of operating metrics used to assess performance and allocate resources; |

| ● | The CODM, who is the Company’s Chief Executive Officer, reviews consolidated financial information to make operational and strategic decisions; |

| ● | The nature of the products and services, customer base, and methods of distribution are consistent across the business. |

The CODM uses revenue to evaluate segment performance and allocate resources.

The following table identifies the disaggregation of the Company’s revenue for the six months ended December 31, 2025, 2024 and 2023, respectively:

| | | For the six months ended June 30, | |

| Service Type | | 2025 | | | Percentage of

Total

revenue

(in %) | | | 2024 | | | Percentage of

Total

revenue

(in %) | | | 2023 | | | Percentage of

Total

revenue

(in %) | |

| Event management services | | $ | 2,488,183 | | | | 77.2 | | | $ | 2,235,481 | | | | 77.9 | | | $ | 2,267,221 | | | | 77.5 | |

| Stage production services | | | 734,252 | | | | 22.8 | | | | 633,013 | | | | 22.1 | | | | 659,357 | | | | 22.5 | |

| Total | | $ | 3,222,435 | | | | 100.0 | | | $ | 2,868,494 | | | | 100.0 | | | $ | 2,926,578 | | | | 100.0 | |

During the six months ended December 31, 2025, 2024 and 2023, all revenue was generated from Hong Kong and from third parties.

Event management services

The Company provides customized event management services upon requests from its customers in exchange for a fixed transaction price. The service generally entail design, logistics, layout of events and coordination and supervision of the actual event set-up and implementation. These services are not distinct within the context of the contracts and are considered as a single performance obligation.

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 2. Significant Accounting Policies (cont.)

The Company recognizes revenue that are satisfied over time by measuring the progress toward complete satisfaction of the performance obligation using a single method of measuring progress which depicts the performance in transferring control of the associated goods or services to the customers. The Company uses input methods to measure the progress toward the complete satisfaction of performance obligations satisfied over time. Significant management judgment is required in determining the level of effort required under an arrangement and the period over which the Company is expected to complete the performance obligations under an arrangement. At each reporting period, the Company measures the progress based on the budgeting and costing systems and estimates the proportion of service rendered based on the ratio of costs incurred to estimated total costs.

Stage production services

Apart from the event management services, the Company also provides stage production services, including sales of furniture pieces, essential decor items, stage equipment and the corresponding installation service to its customers. The transaction price is fixed. The Company recognizes revenues from stage production services at a point of time when the goods are delivered to the customer.

Contract balances

Contract assets

The Company recognizes a contract asset when revenue is recognized in advance of invoicing on a customer contract, unless the right to payment for that revenue is unconditional (i.e. requiring no further performance and only the passage of time). If a right to payment is determined to meet the criteria to be considered ‘unconditional’, then the Company will recognize a trade receivable. As of December 31, 2025 and June 30, 2025, the balances of contract asset amounted to $405,318 and $571,982, respectively.

Contract liability

The Company presents the consideration that a customer pays before the Company transfers the service to the customer as a contract liability (advance from customers) when the payment is made. An advance from customers is the Company’s obligation to transfer services to a customer for which the Company has received consideration from the customer. As of December 31, 2025 and June 30, 2025, the balances of advance from customers amounted to $37,741 and $21,212, respectively. For the six months ended December 31, 2025, 2024 and 2023, $13,707, $21,910 and $23,053 of revenue recognized was included in the Company’s advance from customers’ balance as of June 30, 2025, 2024 and 2023, respectively. The Company expects to recognize December 31, 2025 advance from customers’ balance of $37,741 in revenue over the next twelve months.

Contract costs

The Company applies the practical expedient in ASC Topic 606 that permits the recognition of incremental costs of obtaining contracts as an expense when incurred if the amortization period of such costs is one year or less. These costs are included in cost of revenue.

2.15 Cost of revenue

Cost of revenue is recognized when incurred. Cost of revenue consists primarily of subcontracting costs associated with the tasks outsourced to a subcontractor to fulfill the Company’s revenue contracts and staff costs incurred that are directly attributable to the revenue-generating services to clients.

2.16 Income Taxes

The Company accounts for income taxes in accordance with ASC 740 “Income Taxes”.

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 2. Significant Accounting Policies (cont.)

Current taxes are the expected tax receivable or payable on the taxable income or loss for the current period, using tax rates enacted or substantively enacted at the reporting date, and any adjustment to tax receivable or payable in respect of previous years. Deferred taxes are recognized in respect of temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. The Company conducts business activities and is subject to taxes in Hong Kong. The Company files tax returns in Hong Kong and is subject to examination by the Hong Kong tax authority.

Deferred tax assets and liabilities are recognized for the future tax consequences of transactions that have been recognized in the Company’s financial statements or tax returns. A valuation allowance is provided when it is more likely than not that some portion, or all, of the deferred tax asset will not be realized.

Deferred tax asset is recognized for unused tax losses, tax credits and deductible temporary differences, to the extent that it is probable that future taxable profits will be available against which they can be utilized. Deferred tax assets are reviewed at each reporting date and are reduced to the extent that it is no longer probable that the related tax benefit will be realized. The Company considers positive and negative evidence to determine whether some portion or all of the deferred tax assets will more likely than not be realized. This assessment considers, among other matters, the nature, frequency and severity of recent losses, forecasts of future profitability, the duration of statutory carry forward periods, the Company’s experience with tax attributes expiring unused and tax planning alternatives. Valuation allowances have been established for deferred tax assets based on a more-likely-than-not threshold. The Company’s ability to realize deferred tax assets depends on its ability to generate sufficient taxable income within the carry forward periods provided for in the tax law.

Deferred taxes are not recognized for the following temporary differences: the initial recognition of assets or liabilities in a transaction that is not a business combination and that affects neither accounting nor taxable profit or loss, and differences relating to investments in subsidiaries and jointly controlled entities to the extent that it is probable that they will not reverse in the foreseeable future.

2.17 Earnings per share (“EPS”)

Basic EPS is calculated by dividing the net income attributable to ordinary equity holders by the weighted average number of ordinary shares outstanding during the period. Diluted EPS is calculated by using the weighted average number of ordinary shares outstanding adjusted to include the potentially dilutive effect of ordinary shares outstanding during the period using the treasury stock method and as if converted method, unless their inclusion in the calculation is anti-dilutive.

As of December 31, 2025, potentially dilutive securities (including 360,000 share options) were excluded from the computation of diluted EPS because their inclusion would be anti-dilutive due to the net loss for the period. As a result, basic and diluted EPS are the same for the six months ended December 31, 2025. As of December 31, 2024 and 2023, there were no potentially dilutive securities outstanding.

2.18 Non-controlling interests

A non-controlling interest in a subsidiary of the Company represents the portion of the equity (net assets) in the subsidiary not directly or indirectly attributable to the Company. Non-controlling interests are presented as a separate component of equity on the unaudited interim condensed consolidated balance sheets and net income and other comprehensive income attributable to non-controlling shareholders are presented as a separate component on the unaudited interim condensed consolidated statements of operations.

2.19 Related Parties

The Company follows ASC 850, “Related Party Disclosures,” for the identification of related parties and disclosure of related party transactions and balances. Parties are considered to be related if one party has the ability, directly or indirectly, to control the other party or exercise significant influence over the other party in making financial and operating decisions. Parties are also considered to be related if they are subject to common control or significant influence, such as a family member or relative, shareholder, or a related corporation.

2.20 Commitments and Contingencies

In the normal course of business, the Company is subject to loss contingencies, such as legal proceedings and claims arising out of its business, that cover a wide range of matters, including, among others, government investigations and tax matters. In accordance with ASC No. 450-20, “Loss Contingencies”, the Company will record accruals for such loss contingencies when it is probable that a liability has been incurred and the amount of loss can be reasonably estimated.

In the opinion of the management of the Company, there were no pending or threatened claims and litigation as of December 31, 2025, and through the date of this report.

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 2. Significant Accounting Policies (cont.)

2.21 Deferred IPO costs

Deferred IPO costs consist primarily of direct expenses paid to attorneys, consultants, underwriters, and other parties related to the Company’s IPO. Pursuant to ASC 340-10-S99-1, IPO costs directly attributable to an offering of equity securities are deferred and would be charged against the gross proceeds of the initial public offering as a reduction of capital. During the six months ended December 31, 2025, 2024 and 2023, deferred IPO costs of $454,330, nil and nil, respectively, were charged against the gross proceeds of the initial public offering as a reduction of share capital.

2.22 Share-based compensation

Share-based awards granted are measured at fair value on grant date and share-based compensation expense is recognized (i) immediately at the grant date if no vesting conditions are required, or (ii) using the straight-line attribution method, net of estimated forfeitures, over the requisite service period. The fair values of restricted stock units (“RSUs”) and restricted shares are determined with reference to the fair value of the underlying shares and the fair value of share options is generally determined using the binomial option pricing model. The value is recognized as an expense over the respective service period, net of estimated forfeitures. Share-based compensation expense, when recognized, is charged to the unaudited condensed consolidated statements of operations with the corresponding credit to additional paid-in capital for the share options and RSUs to the extent that such awards are to be settled only in stock.

On each measurement date, the Company reviews internal and external sources of information to assist in the estimation of various attributes to determine the fair value of the share-based awards granted by the Company, including the fair value of the underlying shares, expected life and expected volatility. The Company recognizes the impact of any revisions to the original forfeiture rate assumptions in the unaudited condensed consolidated statements of operations, with a corresponding adjustment to equity.

2.23 Recent Accounting Pronouncements

In December 2023, the FASB issued ASU 2023-09, Income Taxes (Topic 740): Improvements to Income Tax Disclosures (ASU 2023-09), which requires disclosure of incremental income tax information within the rate reconciliation and expanded disclosures of income taxes paid, among other disclosure requirements. ASU 2023-09 is effective for fiscal years beginning after December 15, 2024. Early adoption is permitted. The Company adopted the ASU on July 1, 2025. The additional required disclosures did not have a material impact on our unaudited interim condensed consolidated financial statements.

In November 2024, the FASB issued ASU no. 2024-03, Income Statement — Reporting Comprehensive Income — Expense Disaggregation Disclosure (Subtopic 220-40). The amendments in this update enhance disclosures about a public business entity’s expense and provide more detailed information about the types of expenses included in certain notes in the consolidated financial statements. ASU no. 2024-03 is effective for annual periods beginning after December 15, 2026, and interim reporting periods beginning after December 15, 2027. Early adoption permitted. The amendments may be applied prospectively to reporting periods after the effective date or retrospectively to all periods presented in the unaudited interim condensed consolidated financial statements. The Company’s management is currently evaluating any new disclosures that may be required upon adoption of ASU 2024-03.

In May 2025, the FASB issued ASU No. 2025-03, Business Combinations (Topic 805) and Consolidation (Topic 810): Accounting Acquirer in a Business Combination Involving a Variable Interest Entity. This ASU clarifies that when a business that is a VIE is acquired primarily with equity interests, the determination of the accounting acquirer should follow ASC 805 rather than defaulting to the primary beneficiary under ASC 810. The standard is effective for fiscal years beginning after December 15, 2026, including interim periods within those fiscal years. Early adoption is permitted. The Company’s management is currently evaluating the impact of adopting this ASU 2025-03 on its unaudited interim condensed consolidated financial statements.

In May 2025, the FASB issued ASU No. 2025-04, Compensation—Stock Compensation (Topic 718) and Revenue from Contracts with Customers (Topic 606): Clarifications to Share-Based Consideration Payable to a Customer. This ASU clarifies how entities account for share-based consideration payable to a customer. The ASU requires customer awards with vesting conditions tied to purchases to be treated as performance conditions, eliminates the forfeiture policy election, and states that the variable consideration constraint under ASC 606 does not apply to these awards. The standard is effective for annual periods beginning after December 15, 2026, with early adoption permitted. The Company’s management is currently evaluating the impact of adopting this ASU 2025-04 on its unaudited interim condensed consolidated financial statements.

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 3. Risks and uncertainties

In July 2025, the FASB issued ASU No. 2025-05, Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses for Accounts Receivable and Contract Assets. This ASU provides a practical expedient for all entities related to the estimation of expected credit losses for current accounts receivable and current contract assets that arise from transactions accounted for under Topic 606. The standard is effective for annual periods beginning after December 15, 2025. Early adoption of ASU 2025-05 is permitted and should be applied prospectively. The Company’s management is currently evaluating the impact of adopting this ASU 2025-05 on its unaudited interim condensed consolidated financial statements.

Except for the above-mentioned pronouncements, there are no new recent issued accounting standards that will have a material impact on the unaudited interim condensed consolidated balance sheets, statements of operations and cash flows.

Economic and political risk

The Company’s operating subsidiaries conduct business in Hong Kong, a Special Administrative Region of the PRC. Accordingly, the Company’s business, financial condition and results of operations may be influenced by the political, economic and legal environment in the PRC, and by the general state of the PRC economy.

The Company’s operations in Hong Kong are subject to special considerations and significant risks not typically associated with companies in North America and Western Europe. These include risks associated with, among others, the political, economic and legal environment and foreign currency exchange. The Company’s results may be adversely affected by changes in the political and social conditions in the PRC, and by changes in governmental policies with respect to laws and regulations, anti-inflationary measures, currency conversion, remittances abroad, and rates and methods of taxation.

Concentration of credit risk

Financial instruments that potentially expose the Company to significant concentration of credit risk consist primarily of trade receivables. The Company conducts credit evaluations of its customers, and generally does not require collateral or other security from them. The Company evaluates its collection experience and long outstanding balances to determine the need for a provision for expected credit losses. The Company conducts periodic reviews of the financial condition and payment practices of its customers to minimize collection risk on trade receivables.

Details of the customers which accounted for 10% or more of the revenue are as follows:

| | | For the six months ended December 31, | |

| | | 2025 | | | % revenue | | | 2024 | | | % revenue | | | 2023 | | | % revenue | |

| Customer A | | $ | 1,655,376 | | | | 51.4 | % | | $ | 661,010 | | | | 23.0 | % | | $ | 657,438 | | | | 22.5 | % |

| Customer B | | | — | | | | — | % | | | 547,497 | | | | 19.1 | % | | | — | | | | — | % |

| Customer C | | | 196,573 | | | | 6.1 | % | | | 200,897 | | | | 7.0 | % | | | 635,188 | | | | 21.7 | % |

| Customer D | | | — | | | | — | % | | | — | | | | — | % | | | 488,802 | | | | 16.7 | % |

| | | $ | 1,851,949 | | | | 57.5 | % | | $ | 1,409,404 | | | | 49.1 | % | | $ | 1,781,428 | | | | 60.9 | % |

Details of the customers which accounted for 10% or more of the trade receivables are as follows:

| | | As of | |

| | | December 31, 2025 | | | % trade

receivables | | | June 30, 2025 | | | % trade

receivables | |

| Customer A | | $ | 211,813 | | | | 17.3 | % | | $ | 3,822 | | | | 0.3 | % |

| Customer E | | | 321,310 | | | | 26.2 | % | | | 382,170 | | | | 28.9 | % |

| Customer F | | | 126,006 | | | | 10.3 | % | | | 57,364 | | | | 4.3 | % |

| Customer G | | | — | | | | — | % | | | 199,748 | | | | 15.1 | % |

| Customer H | | | — | | | | — | % | | | 150,002 | | | | 11.4 | % |

| | | $ | 659,129 | | | | 53.8 | % | | $ | 793,106 | | | | 60.0 | % |

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 4. Deposits, prepayments and other current assets

At December 31, 2025 and June 30, 2025, deposits and prepayments consisted of the following:

| | | As of | |

| | | December 31, 2025 | | | June 30, 2025 | |

| Refundable deposits | | | 25,011 | | | | 18,548 | |

| Advance to suppliers | | | 305 | | | | 90 | |

| Other receivables* | | | 155,029 | | | | 153,661 | |

| | | $ | 180,345 | | | $ | 172,299 | |

| * | As of December 31, 2025 and June 30, 2025, other receivables mainly represent the non-trade receivables due from BU Production. BU Production ceased to be a subsidiary of the Company upon the completion of the disposal on September 23, 2024 and the balance with BU Production ceased to be eliminated on consolidation. |

Note 5. Property, plant and equipment, net

At December 31, 2025 and June 30, 2025, property, plant and equipment consisted of the following:

| | | As of | |

| | | December 31, 2025 | | | June 30, 2025 | |

| Motor vehicles | | | 232,897 | | | | 204,587 | |

| Furniture and fixtures | | | 17,499 | | | | 17,345 | |

| Computer equipment | | | 22,867 | | | | 22,665 | |

| Leasehold improvements | | | 43,090 | | | | 42,710 | |

| | | | 316,353 | | | | 287,307 | |

| Accumulated depreciation | | | (163,654 | ) | | | (217,623 | ) |

| Property, plant and equipment, net of accumulated depreciation | | $ | 152,699 | | | $ | 69,684 | |

| * | A motor vehicle with a net carrying amount of $142,077 and $53,365 are held under a finance lease arrangement as of December 31, 2025 and June 30, 2025, respectively (Note 8). During the six months ended December 31, 2025, 2024 and 2023, the Company recorded motor vehicles obtained in exchange for finance lease liabilities of $107,445, nil and nil, respectively. |

During the six months ended December 31, 2025, 2024 and 2023, the Company recorded additions to different categories of property, plant and equipment in aggregate costs of nil, nil and $3,708, respectively. Apart from the additions, during the six months ended December 31, 2025, 2024 and 2023, the Company disposed of different categories of property, plant and equipment in aggregate costs of $81,019, nil and $9,420, respectively.

For the six months ended December 31, 2025, 2024 and 2023, depreciation expense, including the depreciation expense of fixed assets under finance leases, was $25,247, $23,468 and $24,064, respectively.

Note 6. Right-of-use assets and operating lease liabilities

The Company has leases for the office premise and warehouse in Hong Kong expiring on various dates through January 2028, which are classified as operating leases. All cash payments of operating lease cost are classified within operating activities in the unaudited interim condensed consolidated statements of cash flows. For the six months ended December 31, 2025, 2024 and 2023, lease expense included in the Company’s general administrative expenses was $36,749, $35,214 and $15,304, respectively.

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 6. Right-of-use assets and operating lease liabilities (cont.)

The carrying amounts of right-of-use assets are as below:

| | | As of | |

| | | December 31, 2025 | | | June 30, 2025 | |

| Office premise and warehouse | | $ | 150,948 | | | $ | 139,732 | |

| Less: Accumulated lease expense | | | (20,336 | ) | | | (97,648 | ) |

| ROU assets, net | | $ | 130,612 | | | $ | 42,084 | |

The Company’s future minimum payments under long-term non-cancellable operating leases are as follows:

| | | As of

December 31,

2025 | |

| Within 1 year | | $ | 68,375 | |

| 1 – 2 year | | | 66,010 | |

| Total operating lease payments | | $ | 134,385 | |

| Less: imputed interest | | | (3,722 | ) |

| Total operating lease obligation | | $ | 130,663 | |

| Less: current portion of operating lease liabilities | | | (65,626 | ) |

| Non-current portion of operating lease liabilities | | $ | 65,037 | |

Other information:

| | | For the six months ended

December 31, | |

| | | 2025 | | | 2024 | | | 2023 | |

| Cash paid for amounts included in the measurement of lease liabilities: | | | | | | | | | |

| Cash outflows from operating lease | | $ | 38,772 | | | $ | 36,986 | | | $ | 14,770 | |

| Right-of-use assets obtained in exchange for operating lease liabilities | | $ | 124,969 | | | $ | 78,464 | | | $ | — | |

| Loss on lease modification | | $ | 1,323 | | | $ | — | | | $ | — | |

| Remaining lease term for operating leases (years) | | | 1.98 | | | | 1.23 | | | | — | |

| Weighted average discount rate for operating leases | | | 2.76 | % | | | 3.61 | % | | | — | % |

Note 7. Other payables and accruals

| | | As of | |

| | | December 31, 2025 | | | June 30, 2025 | |

| Payroll payable | | $ | 5,338 | | | $ | 5,442 | |

| Other payables | | | 100,202 | | | | 134,086 | |

| | | $ | 105,540 | | | $ | 139,528 | |

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 8. Finance lease liabilities

In August 2022, July 2025 and December 2025, the Company acquired motor vehicles pursuant to a hire purchase financing arrangement. Future minimum lease payments under finance lease that have initial non-cancelable lease terms as of December 31, 2025 were as follows:

| | | As of

December 31,

2025 | |

| Within 1 year | | $ | 64,505 | |

| 1-2 year | | | 40,972 | |

| 2-3 year | | | 19,237 | |

| Over 3 years | | | 7,911 | |

| Total finance lease payments | | $ | 132,625 | |

| Less: imputed interest | | | (12,315 | ) |

| Total finance lease obligation | | $ | 120,310 | |

| Less: current portion of finance lease liabilities | | | (57,314 | ) |

| Non-current portion of finance lease liabilities | | $ | 62,996 | |

For the six months ended December 31, 2025, 2024 and 2023, interest expense of $4,175, $1,406 and $1,929 were recorded as finance costs, respectively.

Note 9. Bank borrowings

| | | | | As of | |

| | | | | December 31, 2025 | | | June 30, 2025 | |

| Loan I | | (a) | | $ | — | | | $ | 27,995 | |

| Loan II | | (b) | | | 189,618 | | | | 200,640 | |

| Loan III | | (c) | | | 194,778 | | | | 203,466 | |

| Total bank borrowings | | | | $ | 384,396 | | | $ | 432,101 | |

| (a) | On December 15, 2021, the Company borrowed a term loan from a financial institution in the amount of HKD2,050,000 (approximately $264,000) (“Loan I”), which is repayable by 60 monthly installments in average amount of HKD36,888 (approximately $4,800) with the first installment to be paid on January 15, 2021. The loan bears an annual interest rate at the Hong Kong Prime Rate minus 2.5%. For the six months ended December 31, 2025, 2024 and 2023, effective interest rates for this loan were 1.73%, 3.02% and 3.31% per annum, respectively. The loan was secured by joint personal guarantee provided by Ms. Nana CHAN, shareholder of BUUU and Suk Ling CHEUNG, spouse of Wai Kwong POON who is the shareholder of BUUU. Such term loan was fully settled in December 2025. |

| (b) | On August 30, 2022, the Company borrowed a term loan from a financial institution in the amount of HKD2,100,000 (approximately $268,000) (“Loan II”), which is repayable by 120 monthly installments in average amount of HKD20,831 (approximately $2,700) with the first installment to be paid on September 30, 2022. The loan bears an annual interest rate at the Hong Kong Prime Rate minus 2.5%. For the six months ended December 31, 2025, 2024 and 2023, effective interest rates for this loan were 2.83%, 3.36% and 3.54% per annum, respectively. The loan was secured by joint personal guarantee provided by Ms. Nana CHAN, shareholder of BUUU and Suk Ling CHEUNG, spouse of Wai Kwong POON who is the shareholder of BUUU. |

| (c) | On February 27, 2023, the Company borrowed a term loan from a financial institution in the amount of HKD1,805,000 (approximately $230,000) (“Loan III”), which is repayable by 132 monthly installments in average amount of HKD16,808 (approximately $2,100) with the first installment to be paid on March 27, 2023. The loan bears an annual interest rate at the Hong Kong Prime Rate minus 2.5%. For the six months ended December 31, 2025, 2024 and 2023, effective interest rates for this loan were 2.85%, 3.38% and 3.61% per annum, respectively. The loan was secured by joint personal guarantee provided by Ms. Nana CHAN, shareholder of BUUU, Suk Ling CHEUNG, spouse of Wai Kwong POON who is the shareholder of BUUU and Sze Ho LI, minority shareholder of BU Workshop. |

All of these term loan agreements contain a repayable on demand clause that these loans shall be immediately due and payable by the Company on demand by the bank at any time. Therefore, as of December 31, 2025 and June 30, 2025, the outstanding balance of bank borrowings was classified as current liability on the Company’s unaudited interim condensed consolidated balance sheets. For the six months ended December 31, 2025, 2024 and 2023, interest expense of $6,012, $8,873 and $10,837 were recorded as finance costs, respectively.

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 10. Disposal of subsidiaries

On September 25, 2023, the Company completed the disposal of its entire 50% equity interest in BU Production. No gain or loss on disposal was recorded during the year ended June 30, 2024. This disposal was not classified as a discontinued operation as BU Production was operating within the Company’s same core business as other subsidiaries, and the operating results contributed by BU Production were immaterial to the Company’s unaudited interim condensed consolidated financial statements.

Note 11. Income tax

British Virgin Islands

The Company was incorporated in the British Virgin Islands. Under the current laws of the British Virgin Islands, the Company is not subject to income or capital gains taxes. In addition, dividend payments are not subject to withholding tax in the British Virgin Islands.

Hong Kong

BU Creation and BU Workshop were incorporated in Hong Kong and subject to the Hong Kong corporate income tax rate of 16.5% on income derived from Hong Kong.

The components of the income tax provision were as follows:

| | | For the six months ended

December 31, | |

| | | 2025 | | | 2024 | | | 2023 | |

| Current income tax expense | | | 7,123 | | | | 58,673 | | | | 47,911 | |

| Deferred income tax expense | | | 418 | | | | 292 | | | | 149 | |

| Total income tax expenses | | $ | 7,541 | | | $ | 58,965 | | | $ | 48,060 | |

Deferred tax liabilities net was $295 as at December 31, 2025 while deferred tax assets net was $123 at June 30, 2025. These deferred tax (liabilities) assets reflect the tax effect of temporary differences between the book and taxable income related to the lease expense and capital allowance claimed in Hong Kong, where the Company operates.

Deferred tax assets and liabilities are comprised of the following:

| | | As of | |

| | | December 31, 2025 | | | June 30, 2025 | |

| Deferred tax assets: | | | | | | |

| Operating lease liabilities | | $ | 21,559 | | | $ | 7,067 | |

| Total deferred tax assets | | $ | 21,559 | | | $ | 7,067 | |

| Deferred tax liabilities: | | | | | | | | |

| Right of use assets – operating lease | | $ | (21,854 | ) | | $ | (6,944 | ) |

| Total deferred tax liabilities | | $ | (21,854 | ) | | $ | (6,944 | ) |

| Deferred tax (liabilities) assets, net | | $ | (295 | ) | | $ | 123 | |

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 12. Related Party Transactions

The table below sets forth the major related parties and their relationships with the Company as of December 31, 2025 and June 30, 2025:

| Name of related parties | | Relationship with the Company |

| Poon Wai Kwong (“Mr. Poon”) | | Director and shareholder of BUUU |

| Excellent Prospect Investment Holding Limited | | Shareholder of BUUU |

On December 20, 2024, the Company and Excellent Prospect Investment Holding Limited, being a shareholder of the Company, entered into a loan agreement, pursuant to which Excellent Prospect Investment Holding Limited agreed to lend $180,000 to the Company for the payment of IPO related expenses. The loan bears 6% interest per annum and will be matured on December 19, 2025. The Company had fully repaid the outstanding balance on August 20, 2025.

Note 13. Equity

The shareholders’ equity structure as of December 31, 2025 and June 30, 2025 are presented after giving retroactive effect to the reorganization of the Company that was completed on November 18, 2024. Immediately before and after reorganization, the Company, together with its subsidiary, were effectively controlled by the same shareholder; therefore, for accounting purposes, the reorganization was accounted for as a recapitalization.

Authorized Shares

The Company has 500,000,000 authorized ordinary shares, no-par value per share.

Ordinary Shares

As of June 30, 2025, the Company has 10,000,000 Class A ordinary shares and 5,000,000 Class B outstanding and issued to the participating shareholders in connection with the reorganization of the Company.

On August 13, 2025, the Company completed its IPO the Nasdaq Capital Market and the Class A ordinary shares commenced trading under the ticker symbol “BUUU”. Under this offering, 1,500,000 Class A ordinary shares were issued at a price of $4 per share. On August 15, 2025, the Company closed its IPO of 1,500,000 Class A ordinary shares. Subsequently, on August 27, 2025, the underwriter partially exercised its over-allotment option to purchase an additional 175,000 Class A ordinary shares of the Company at the public offering price of US$4.00 per share. The closing for the sale of the over-allotment shares took place on September 3, 2025. The IPO and the exercise of the over-allotment option with net proceeds totaling $5,804,648 from the offering after deducting underwriting discounts and offering expenses of $895,352 from the gross proceeds totaling $6,700,000.

Upon the completion of IPO of the Company, IPO costs capitalized as of June 30, 2025 amounted to $204,964, together with other IPO costs incurred during the six months ended December 31, 2025 of $249,366, were charged to shareholders’ equity under share capital.

In November 2025 and December 2025, the Company issued 10,000 and 10,000 Class A ordinary shares, respectively, to the employee under 2025 equity incentive plan.

As of December 31, 2025, 11,695,000 Class A ordinary shares and 5,000,000 Class B ordinary shares were issued and outstanding.

BUUU GROUP LIMITED AND SUBSIDIARIES

NOTES TO THE UNAUDITED INTERIM CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(Amounts expressed in US dollars (“$”) except for numbers of shares)

Note 13. Equity (cont.)

Subscription receivable and share allotment

On November 7, 2024, BUUU, via a subscription agreement for aggregate proceeds of $19,800, issued 3,960,000 ordinary shares of BUUU to the pre-IPO investors. As of June 30, 2025, 2024 and 2023, proceeds to be received from this subscription were reflected in share capital and subscription receivable in the amount of $19,801.

Cash dividend

On September 1, 2024, BU Creation Limited, the subsidiary of the Company, declared a special dividend of approximately HK$71,000 per share (equivalent to approximately $9,140 per share) with respect to the 100 issued shares of BU Creation Limited or HK$7,100,000 (equivalent to $904,470) to the shareholders of BU Creation Limited, of which $495,663 was offset with the current account with shareholders. The dividend declared by BU Creation Limited has been fully paid at the date these unaudited interim condensed consolidated financial statements are issued.