EXHIBIT (e)

Management report

General information about Rentenbank

Promotional mandate

Rentenbank is a promotional bank operating throughout Germany. Under the Law Governing Landwirtschaftliche Rentenbank, its mandate is to promote agriculture, related upstream and downstream sectors, and rural areas in general. Its business model is defined by the framework set out in the Law Governing Rentenbank and its Articles of Incorporation.

As a promotional bank for agribusiness and rural areas, Rentenbank provides earmarked funding for a wide range of investments and initiatives. It grants special promotional loans to local banks on a competitively neutral basis for the financing of projects in Germany. These loans are granted to enterprises in the agriculture and forestry, viticulture and horticulture, and aquaculture and fisheries sectors. Rentenbank also supports projects in the food industry and in other sectors upstream and downstream of agriculture, as well as investments in renewable energy and infrastructure projects in rural areas. In addition, Rentenbank carries out promotional activities on behalf of the federal government and the federal states. The appropriation of profits is aligned with the promotional mandate: One half of distributable profit is allocated to Rentenbank’s Promotional Fund and the other half to the Federal Government’s Special-Purpose Fund administered by Rentenbank. The Special-Purpose Fund is used to promote innovation in agriculture on the basis of the guidelines issued by the Federal Ministry of Agriculture, Food and Regional Identity (BMLEH). Rentenbank also promotes innovative business models by investing in venture capital funds that provide targeted financing to start-ups in the ag-tech and food-tech sectors and help them gain a foothold in the market. In addition, Rentenbank provides refinancing to banks, savings banks and public authorities, including through the purchase of registered bonds, promissory note loans and securities.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 1 |

Management system

Rentenbank’s strategic objectives and the measures required to achieve them, as well as the strategic control parameters, are derived from its business strategy. The strategic objectives are operationalised through a number of sub-strategies.

The strategic control parameters are applied in four categories to assess the effectiveness of strategic measures at the bank-wide level:

| • | Attractive promotional programmes |

| • | Efficient bank operations |

| • | Appropriate risk culture |

| • | Compliance with the capital and liquidity requirements defined in the Risk Appetite Statement |

Segments

Rentenbank is managed on the basis of three segments:

| • | Promotional Activity |

| • | Capital Investment |

| • | Treasury Management |

In the “Promotional Activity” segment, Rentenbank promotes investment in the agricultural sector and in rural areas. This is done by refinancing earmarked loans granted by local banks to ultimate borrowers for use in Germany in accordance with the terms and conditions of the special promotional lending programmes.

In addition, Rentenbank fulfils its promotional mandate by acting as a refinancing partner to local banks with business activities in the agricultural sector and in rural areas, as well as to domestic public authorities. This is achieved through various forms of funding, including registered bonds, promissory note loans and securities. Some of these transactions also contribute to meeting regulatory liquidity requirements. Rentenbank manages both its business volume and its risk structure. Rentenbank’s promotional offering for the financing of start-ups related to its promotional mandate also includes investments in venture capital funds, which are reported in the “Promotional Activity” segment.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 2 |

Refinancing, which is largely maturity-matched, is also allocated to the “Promotional Activity” segment.

The “Capital Investment” comprises the investment of equity and long-term provisions. Investments are made primarily in registered bonds, promissory note loans and securities issued by banks and public-sector issuers.

Short-term liquidity and short-term interest rate risk are managed in the “Treasury Management” segment. Rentenbank has a range of instruments with maturities of up to one year at its disposal both for the short-term investment of surplus liquidity and for raising the liquidity required. In addition to entering into money market transactions, debt securities with longer maturities may also be acquired to manage the Rentenbank’s liquidity profile.

Financial key performance indicators

Financial key performance indicators (KPI) are the principal metrics used within the internal management system to measure the achievement of strategic objectives in financial reporting. These KPIs reflect Rentenbank’s business activities. They include:

| • | Operating result (operating result before loan loss provisions and valuation effects) |

Rentenbank’s business activities are not

primarily aimed at generating profits, but

at fulfilling its statutory promotional mandate. At the same time, sound

business management principles must be observed in order to enable Rentenbank to conduct its promotional activities on a

self-supporting basis. In particular, this means that Rentenbank’s activities must be economically efficient so that it

can sustain its promotional activities on a permanent basis and adapt them where necessary. In view of increasing regulatory

requirements, the operating result is retained in order to strengthen Rentenbank’s capital base. As a promotional

institution under public law, Rentenbank relies on its high credit rating, combined with an appropriate capital markets

strategy, to raise funding on favourable terms.

| • | Cost-income ratio1 |

As a key performance indicator measuring costs in relation to income, the cost-income ratio is used to ensure the efficient use of Rentenbank’s resources. As it reflects the relationship between costs and income, it is influenced by changes in both variables. In order to enhance operational transparency, allocations to promotional contributions and reversals of promotional grants from previous years are excluded from the calculation of the cost-income ratio. The cost-income ratio is monitored over a longer period and supplemented by periodic analyses of changes in costs.

| 1 | The cost-income ratio is calculated as the ratio of costs to income. The numerator comprises the sum of general administrative expenses, depreciation, amortisation and impairment losses on intangible assets and property and equipment, other operating expenses and income taxes. The denominator comprises the sum of interest income and current income less interest expenses (plus allocations to interest subsidies and less reversals from previous years), other operating income and fee and commission income less fee and commission expenses. |

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 3 |

| • | Promotional activity volume |

Promotional activity volume refers to the volume of new special promotional loans granted in a given year. The special promotional loans granted to promote agribusiness and rural areas form the core of Rentenbank’s promotional activities. These loans are granted as earmarked funding instruments. Loans granted to the promotional institutions of the federal states may also be bundled.

These three financial key performance indicators and their principal components are calculated and compared with the corresponding budget figures as part of the monthly reporting process. They are also included as separate indicators in the multi-year plan. Further information on the financial key performance indicators is provided in the section on Rentenbank’s net assets, financial position and results of operations, as well as in the forecast report.

Non-financial key performance indicators

| • | Employees |

Highly qualified and committed employees are the basis for Rentenbank’s long-term success. The objectives of the related HR strategy, which is consistently derived from the business strategy, include ensuring adequate staffing in quantitative and qualitative terms, promoting equal opportunities, and providing and further developing HR management instruments and processes.

| • | Corporate social responsibility |

A key aspect of Rentenbank’s corporate social responsibility is closely linked to its promotional mandate. However, as a direct public law institution, Rentenbank is also committed to serving the public good beyond the scope of that mandate.

| • | ESG ratings |

An enterprise’s sustainability management activities are reflected in its ESG ratings, which assess the enterprise’s overall efforts in this area. ESG ratings are an important indicator for external stakeholders, but they also serve as a measure of the effectiveness of implemented sustainability measures. Rentenbank aims to continuously improve its ESG ratings or maintain them at a consistently high level.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 4 |

Affiliated companies

Rentenbank’s direct and indirect subsidiaries are:

| • | LR Beteiligungsgesellschaft mbH (LRB) |

| • | DSV Silo- und Verwaltungsgesellschaft mbH (DSV) |

All material risks of the subsidiaries are concentrated at Rentenbank and managed centrally by it. As in previous years, the scope of the subsidiaries’ business activities remained strictly limited in the 2025 financial year. DSV’s principal activity was limited to fulfilling pension obligations towards its former employees and employees of Getreide-Import-Gesellschaft mbH (GIG), the former subsidiary of LRB, which was merged into DSV with retroactive effect from 1 January 2024, with the result that DSV is now its legal successor. LRB’s business activity essentially consists in the management as a holding company and business management agent of the affiliate DSV and the investment of liquid funds. Rentenbank has issued a letter of comfort in favour of LRB, under it which it undertakes, insofar as and for as long as it holds 100% of LRB’s equity, to provide it with enough financial resources that it will be able to fulfil its obligations punctually at all times.

Public Corporate Governance Code

The Statement of Compliance with the German Public Corporate Governance Code issued by the Management Board and the Supervisory Board is publicly available on Rentenbank’s website.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 5 |

Economic report

General economic and institution-specific conditions

International interest rate and monetary policy

In 2025, following two years of recession, Germany recorded only modest year-on-year growth in gross domestic product (GDP) of 0.2%. Growth was attributable primarily to higher consumer spending by households and the government. The export sector faced higher US tariffs, the appreciation of the euro and stronger competition from China. As a result, exports declined again. Investment weakness also persisted. Investment in both equipment and construction was lower than in the previous year.1

Inflation in the euro area continued to decline over the course of 2025. Growth in the Harmonised Index of Consumer Prices (HICP) initially fell from 2.5% in January to 1.9% in May. In the second half of the year, momentum picked up slightly at first before easing again. In December, consumer prices were 1.9% higher than in the same month of the previous year and, on average, 2.1% above the 2024 level.2

In line with the favourable inflation trend, the European Central Bank (ECB) lowered its deposit rate in four steps from 3.00% to 2.00% in June during the first half of 2025 and then left it unchanged until the end of the year. The ECB also announced that its holdings of securities under the Asset Purchase Programme (APP) and the Pandemic Emergency Purchase Programme (PEPP) had been declining at a measured and predictable pace, as the Eurosystem did not reinvest the principal payments from maturing securities.3

The US Federal Reserve (Fed) also continued to ease its monetary policy in 2025. From the end of October, the Fed lowered its key policy rate in three steps from a range of 4.25% to 4.50% to a range of 3.50% to 3.75% by the end of the year.4

Over the course of 2025, the euro appreciated against the US dollar. At the end of 2025, the ECB set the reference rate for the euro/US dollar exchange rate at 1.175, which was 13.1% above the rate at the end of 2024 (1.039).5

| 1 | Destatis: Press Release No. 017 of 15 January 2026. |

| 2 | Eurostat: Euro indicators June 2025, Annual inflation up to 2.0% in the euro area, 17 July 2025; Euro indicators December 2025, Annual inflation down to 1.9% in the euro area, 19 January 2026. |

| 3 | ECB press releases of 30 January, 6 March, 17 April and 5 June 2025. |

| 4 | http://www.leitzinsen.info/usa.htm |

| 5 | ECB reference exchange rates: https://www.ecb.europa.eu/stats/policy_and_exchange_rates/euro_reference_exchange_rates/html/eurofxref-graph-usd.de.html |

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 6 |

Development of long-term interest rates

In the capital market, the new federal government’s announcement at the beginning of March of a debt-financed increase in public spending on infrastructure and defence led to a marked rise in the yield on ten-year German government bonds. Although yields initially declined again in the following weeks, they rose once more towards the end of the year. As a result, at the end of 2025 the yield on ten-year German government bonds stood at 2.86%, above the year-end 2024 level of 2.36%.1

Development of the economic environment in promotional activity

According to estimates by the Federal

Information Centre for Agriculture (Bundesinformationszentrums Landwirtschaft), the production value of German

agriculture rose slightly in 2025 to EUR 76.8 billion, up 1.7% on the previous year. While production value in crop

production fell by 5.2% to EUR 32.4 billion, the value of animal production and animal products rose significantly year

on year by 8.4% to EUR 39.3 billion. Here, demand was met by relatively limited supply of livestock for slaughter,

resulting in higher producer prices. This did not apply to pigs, however, for which revenues were lower. By contrast, farmers

received higher average prices for

raw milk and eggs over the year.

In crop production, producer prices were mostly below the previous year’s level, particularly for potatoes, sugar beet, fodder crops and fresh vegetables. In the case of cereals, however, the strong harvest more than offset the decline in prices. As a result, production value increased. Higher revenues were also recorded for oilseeds and fruit.2

Overall, the economic situation of full-time agricultural enterprises in the 2024/2025 financial year (1 July 2024 to 30 June 2025) was only slightly better. On average, the business result stood at EUR 78,500, 0.4% higher than in the previous year.3

Revenue in the German food industry rose by around EUR 10 billion to EUR 240 billion in 2025. Exports accounted for 23.6% of this figure. The sector’s revenue continues to be driven above all by still high costs for consumers, particularly for fresh food.4

Electricity generation from renewable energy sources continued to gain in importance in Germany in 2025. It rose by 1% to 289.5 TWh. Onshore wind power generation accounted for the greatest share (37%), followed by photovoltaics (31%) and biomass (15%). The preliminary net increase in onshore wind power capacity was 4,605 MW in 2025, that being 7.2% more than in the

| 1 | Börsen-Zeitung of 31 December 2025, p. 45. |

| 2 | BMLEH statistics: https://www.bmel-statistik.de/landwirtschaft/landwirtschaftliche-gesamtrechnung/produktionswert |

| 3 | Situation Report 2024/2025 of the German Farmers Association (Deutscher Bauernverband, DBV), Chapter 5.2. |

| 4 | EY press release, “Revenue in agribusiness rises again, but outlook remains gloomy” (Umsatz im Agribusiness steigt wieder, Aussichten bleiben allerdings trüb), 13 January 2026. |

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 7 |

previous year. The preliminary net increase in photovoltaics capacity was 16,577 MW, which was nearly 16.5% more than in 2024.1

Business development

New business involving special promotional loans reached EUR 6.6 billion in 2025, compared with EUR 3.6 billion in the previous year. The normalisation of the yield curve led to a significant increase in loan demand, particularly in the “Renewable energy” promotional line. Volume growth was also achieved in all other promotional lines, especially in the “Agribusiness” promotional line. New business in the “Agriculture” promotional line was likewise above the previous year’s level. In this area, the upward trend seen in the previous year continued in the funding of livestock housing. In the “Rural development” promotional line, the promotional institutions of the federal states increased their demand for global loans for rural areas. To strengthen Germany’s innovation landscape, Rentenbank once again invested during the reporting year in venture capital funds focused on the AgTech and FoodTech sectors.

In the financial year under review, new business involving special promotional loans, registered debt securities, promissory notes, securities and venture capital totalled EUR 11.8 billion (EUR 7.9 billion), and was therefore significantly above the previous year’s level.

Overall, new business was as follows:

|

1/1/ to mEUR |

1/1/ to mEUR |

Change mEUR | |

| Special promotional loans | 6,559 | 3,602 | 2,957 |

| Registered bonds/ promissory notes2 |

1,725 | 2,241 | -516 |

| Securities3 | 3,464 | 2,033 | 1,431 |

| Venture capital investments | 21 | 48 | -27 |

| Total | 11,769 | 7,925 | 3,875 |

.

| 1 | German Federal Environment Agency: Monthly Report on the Development of Renewable Electricity Generation and Output in Germany, as of 13 January 2026. |

| 2 | *excluding “non-EU” |

| 3 | *excluding “non-EU” |

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 8 |

In the reporting year, Rentenbank raised EUR 10.9 billion (EUR 8.2 billion) in medium and long-term funding in the national and international financial markets. Rentenbank used the following instruments for medium- and long-term refinancing:

|

1/1/ to bEUR |

1/1/ to bEUR |

Change bEUR | |

| Euro Medium-Term Note (EMTN) | 7.6 | 6.2 | 1.4 |

| Global bonds | 2.6 | 1.4 | 1.2 |

| AUD Medium-Term Note (MTN) | 0.6 | 0.6 | 0.0 |

| Domestic capital market instruments | 0.1 | 0.0 | 0.1 |

| Total | 10.9 | 8.2 | 2.6 |

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 9 |

Economic position

Financial performance

The Bank’s financial performance is presented in the table below:

|

1/1/ to mEUR |

1/1/ to mEUR |

Change mEUR | |

| Net interest income1 | 228.8 | 287.5 | -58.7 |

| Net commission income | -4.6 | -4.7 | 0.1 |

| Administrative expenses | 146.2 | 130.8 | 15.4 |

| Other operating result | 10.3 | 11.3 | -1.0 |

| Income taxes / other taxes | 1.7 | 1.7 | 0.1 |

| Operating result before loan loss provisions and valuation effects | 86.6 | 161.6 | -75.0 |

| Loan loss provisions and valuation effects | 47.6 | 123.6 | -76.0 |

| Net income for the year | 39.0 | 38.0 | 1.0 |

1 Net interest income including income from equity interests.

Operating result before loan loss provisions and valuation effects

The operating result before loan loss provisions and valuation amounted to EUR 86.6 million. It was therefore significantly below the previous year’s level (EUR 161.6 million). The year-on-year decline was attributable primarily to a higher promotional contribution and thus lower income in the “Promotional Activity” segment. In addition, administrative expenses increased.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 10 |

Net interest income

Net interest income by segment:

|

1/1/ to mEUR |

1/1/ to mEUR |

Change mEUR | |

| Net interest income | |||

| Promotional Activity | 128.6 | 195.0 | -66.4 |

| Capital Investment | 88.5 | 75.6 | 12.9 |

| Treasury Management | 11.7 | 16.9 | -5.2 |

| Total net interest income | 228.8 | 287.5 | -58.7 |

Net interest income in the “Promotional Activity” segment amounted to EUR 128.6 million and was therefore significantly below the previous year’s level (EUR 195.0 million). As the volume of special promotional loans increased significantly compared with the previous year, more grants were once again granted, which had an adverse effect on net interest income. In addition, the higher issuance volume, combined with a declining funding margin, had a negative impact on results.

In the “Capital Investment” segment, net interest income was slightly above our planning and increased by 17% year on year to EUR 88.5 million. This was due not only to the additional income from the higher investment volume resulting from the new allocation, but also to reinvestment yields that were above the yields on maturing investments.

Net interest income in the “Treasury Management” segment, at EUR 11.7 million, was below the previous year’s figure of EUR 16.9 million. The 2025 financial year was marked by a continued narrowing of margins in the money market business, which had a corresponding adverse effect on results.

Administrative expenses

Administrative expenses increased by 12% to EUR 146.2 million (EUR 130.8 million). This was due primarily to an increase of EUR 9.2 million in personnel expenses. At the same time, other operating expenses rose by EUR 3.9 million and depreciation, amortisation and impairments by EUR 2.3 million.

The increase in personnel expenses was attributable mainly to an average increase of 22 employees (as defined in Section 267 (5) of the German Commercial Code [Handelsgesetzbuch; HGB]), as well as to collectively agreed pay increases and higher pension expenses (special effect in 2024 due to a reduced inflation assumption).

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 11 |

The increase in other operating expenses resulted primarily from the continued implementation of the IT roadmap and from targeted investment in the IT landscape.

Depreciation, amortisation and impairments of intangible assets as well as property and equipment rose to EUR 16.5 million (EUR 14.2 million), due in particular to higher amortisation of software.

Other operating result

Other operating result declined from EUR 11.3 million to EUR 10.3 million. This was due mainly to lower reimbursements of costs arising from the settlement of the federal programmes.

Loan loss provisions / valuation effects

Under “Loan loss provisions / valuation effects”, a net amount of EUR 47.8 million was used to increase the contingency reserve. Of this amount, EUR 22.8m was allocated to the fund for general banking risks.

Net income for the year / distributable profit

Net income for the year increased from EUR 38.0 million to EUR 39.0 million in the financial year under review.

Subject to the approval of the Supervisory Board, a total of EUR 19.5 million (EUR 19.0 million) from net income for the year was allocated to the principal reserve in the preparation of the annual financial statements.

After the allocation to the principal reserve, distributable profit amounted to EUR 19.5 million, slightly above the previous year’s level (EUR 19.0 million). Distributable profit is to be allocated in equal parts to the Federal Government’s Special-Purpose Fund at Rentenbank and to Rentenbank’s Promotional Fund.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 12 |

Net assets and financial position

Rentenbank’s net assets and financial position as presented in the annual financial statements are as follows:

Changes in significant asset items

|

31 December 2025 mEUR |

31 December 2024 mEUR |

Change mEUR | |

| Loans and advances to banks |

57,827.5 | 65,615.4 | -7,787.9 |

| Loans and advances to customers |

7,100.8 | 7,003.2 | 97.6 |

| Bonds and other fixed-income securities | 18,949.0 | 16,742.6 | 2,206.4 |

Loans and advances to banks amounted to EUR 57.8 billion at the year-end reporting date (EUR 65.6 billion). Their share of total assets was 63.9% and was lower than in the previous year. However, they continued to represent the largest asset class. The decline in loans and advances to banks was attributable mainly to a reduction in money market business. In addition, the stock of special promotional loans declined slightly. In the 2025 financial year, new business involving special promotional loans increased significantly. As a substantial portion of the committed funds has not yet been drawn down, the stock of special promotional loans is expected to rise again in 2026 as these commitments are utilised, thereby offsetting the current decline.

Loans and advances to customers consist primarily of promissory notes issued by the federal states and municipalities. Overall, this balance sheet item increased slightly year on year by EUR 0.1 billion to EUR 7.1 billion.

At the year-end reporting date, the stock of bonds and other

fixed-income securities had increased by EUR 2.2 billion year on year to EUR 18.9 billion. As in the previous year, the

entire stock was classified as fixed assets.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 13 |

Changes in key items of liabilities and equity

|

31 December 2025 mEUR |

31 December 2024 mEUR |

Change mEUR | |

| Liabilities | |||

| Liabilities to banks | 814.3 | 1,528.3 | -714.0 |

| Liabilities to customers | 1,497.4 | 1,490.4 | 7.0 |

| Securitised liabilities | 80,523.4 | 83,752.3 | -3,228.9 |

| Total | 82,835.1 | 86,771.0 | -3,935.9 |

| Equity (including the fund for general banking risks) | |||

| Subscribed capital | 135.0 | 135.0 | 0.0 |

| Retained earnings | 1,272.1 | 1,252.6 | 19.5 |

| Distributable profit | 19.5 | 19.0 | 0.5 |

| Fund for general banking risks | 3,576.3 | 3,553.5 | 22.8 |

| Total | 5,002.9 | 4,960.1 | 42.8 |

Liabilities

Liabilities to banks, at EUR 0.8 billion, were EUR 0.7 billion below the previous year’s level. The decline in outstanding amounts was attributable mainly to the maturity of global loans totalling EUR 0.5 billion. In addition, liabilities to customers, at EUR 1.5 billion, remained at the previous year’s level.

Securitised liabilities declined by EUR 3.2 billion, or 3.9%, to EUR 80.5 billion. At EUR 63.7 billion, the Medium-Term Note (MTN) programmes remained the most important source of funding and increased by EUR 2.2 billion compared with the previous year. The stock of outstanding Euro Commercial Paper (ECP) issuances declined to EUR 3.7 billion (EUR 7.0 billion). Likewise, the stock of outstanding global bonds decreased to EUR 12.6 billion (EUR 14.8 billion).

Equity

Equity, including the fund for general banking risks pursuant to section 340g HGB, increased by EUR 42.8 million to EUR 5,002.9 million. Net income for the year of EUR 39.0 million was allocated in equal parts to retained earnings and recognised as distributable profit, respectively. The fund for general banking risks was increased by EUR 22.8 million.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 14 |

Regulatory capital ratios

The total capital ratio and the Common Equity Tier 1 capital ratio both stood at 32.6% (38.3%). They reflect Rentenbank’s strong capital base even upon initial application of CRR III and continue to remain well above the regulatory minimum requirements.

For the amount and development of regulatory own funds and risk-weighted assets (RWA), please refer to the “Risk-bearing capacity” section.

Capital expenditures

In the year under review, capital expenditures continued to focus on modernising the IT landscape, in particular replacing the proprietary host-based core banking system. In this context, major milestones were successfully achieved through implementations in SAP and Murex. In addition, further implementation measures were launched. Substantial funds were also invested in implementing regulatory requirements and enhancing IT security.

The funding portal introduced in December 2020 as part of the Federal Forestry Programme was further optimised, and the internal IT systems were integrated.

To further digitalise processes, additional bots were developed to handle routine tasks in application processing and thereby contribute to greater efficiency.

Aside from modernising the IT landscape, Rentenbank is investing in the energy-efficient refurbishment of the listed building at its Hochstrasse site in Frankfurt am Main.

Liquidity

The Federal Republic of Germany bears institutional responsibility for Rentenbank and has assumed liability for Rentenbank’s obligations (refinancing guarantee).

On the basis of the resulting AAA ratings, liquidity can be raised

in the market without difficulty. The high volume of debt securities eligible for refinancing with Deutsche Bundesbank constitutes

an additional liquidity reserve. For further details, please refer

to the presentation of liquidity risks in the risk report forming part of this management report.

Overall assessment of business development and economic position

The Management Board considers business development and the development of Rentenbank’s net assets, financial position and results of operations to have been solid overall, albeit below expectations. This also applies to the financial and non-financial key performance indicators defined in the “Management system” section.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 15 |

Financial and non-financial key performance indicators

Financial key performance indicators

The operating result before “Loan loss provisions / valuation effects” (operating result) amounted to EUR 86.6 million and was therefore 46% below the previous year’s figure of EUR 161.6 million. Expectations for 2025 were not met. Net interest income declined by 20% year on year, while administrative expenses increased by 12%.

The developments in income and administrative expenses described above also affected the cost-income ratio key performance indicator. In addition, allocations to promotional contributions (EUR 66.6m) and reversals of promotional subsidies from previous years (EUR 4.1 million) are excluded. Accordingly, the cost-income ratio increased to 50.7% (41.8%) compared with the previous year. Overall, the cost-income ratio remains at a solid level.

The promotional volume key performance indicator comprises the annual volume of new special promotional loans committed, which amounted to EUR 6.6 billion (EUR 3.6 billion) in the reporting year and was therefore above expectations.

Non-financial key performance indicators

With regard to the key performance indicator “Employees”, a total of 492 (459) employees worked at Rentenbank at the end of 2025, excluding trainees, interns, employees on parental leave and members of the Management Board.

In 2025, employee training averaged 2.9 days per person, below the previous year’s level (3.3 days).

The proportion of women at the top management level below the Management Board (FK I) stood at 33% at year-end. Among all other managers (FK II), the figure was 38%.

Rentenbank is committed to society in a variety of ways. Through the Promotional Fund, agribusiness funding, innovation funding and general sponsorship, the forest project in the Buchenborn forestry district, as well as donations to cultural institutions and social organisations in Frankfurt am Main, a total of EUR 9.87 million in support was provided in 2025.

Rentenbank’s sustainability performance is regularly assessed by rating agencies specialising in sustainability. Rentenbank receives regular ratings from ISS ESG, MSCI ESG and Sustainalytics. In 2025, our ISS ESG rating remained unchanged at C- (48.6 points). Our MSCI ESG rating was downgraded from AA to A (on a scale from AAA to CCC). In the 2025 financial year, the Sustainalytics rating deteriorated from 9.1 to 10.9.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 16 |

Despite the slight deterioration in the MSCI ESG and Sustainalytics ratings, Rentenbank remains at a level that is average for the sector in these ratings. Accordingly, the development of the ESG ratings was slightly below expectations.

Overview

| • | ISS ESG (as at 21 December 2025): C- (on a scale from A+ to D-) |

| • | MSCI ESG Ratings (as at 22 April 2025): A (on a scale from AAA to CCC) |

| • | Sustainalytics (as at 20 February 2025): Low Risk, with a score of 10.9 out of a possible 100 points, where 0 represents the best score |

We will continue to make further efforts in the coming years to improve our ESG ratings on an ongoing basis.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 17 |

Forecast and opportunities report

Development

of business conditions and the

operating environment

Rentenbank’s economic performance is shaped primarily by conditions in the lending and financial markets. These are influenced to a significant extent by central bank monetary policy, price and exchange rate developments, and trends in public finances.

Macroeconomic outlook

The persistent uncertainties seen in 2025, caused by geopolitical conflicts, erratic US tariff policy and further trade tensions, will continue in 2026 and weigh on economic activity worldwide to varying degrees. As an exporting nation, Germany is particularly affected by these developments.

According to the International Monetary Fund (IMF), global economic growth of 3.3% is expected in 2026. For Germany, however, the IMF anticipates a much lower increase in gross domestic product (GDP) of only 1.1% year on year.1 According to Deutsche Bundesbank, this growth is likely to be driven primarily by the federal government’s expansionary fiscal stance, with additional public spending on defence and infrastructure.2

The price trend is expected to continue broadly sideways. According to Deutsche Bundesbank, growth in the Harmonised Index of Consumer Prices (HICP) will remain almost unchanged in 2026 compared with the previous year, averaging 2.2% for the year after 2.3% in the previous year.3 This would leave it only slightly above the European Central Bank’s (ECB) target of 2%.

Against the backdrop of low inflation rates, key interest rate increases are not currently expected either in the euro area or in the United States. However, owing to the rising financing needs of sovereign issuers and the first interest rate increases in Japan, Rentenbank expects the capital market yield curve to steepen over the further course of the year, while volatility remains elevated. If geopolitical tensions intensify, a flight to safe government bonds can no longer be taken for granted; instead, investors may also demand higher risk premiums in this segment in future.

Outlook for the economic environment in promotional activity

Investment activity in the agriculture and agribusiness sector, and thus also demand for special promotional loans, is influenced by a wide range of factors. These include the development of general economic conditions, which affect demand and prices in agricultural

| 1 | IMF: World Economic Outlook Update, January 2026: https://www.imf.org/en/publications/weo/issues/2026/01/19/world-economic-outlook-update-january-2026 |

| 2 | Deutsche Bundesbank Monthly Report, December 2025, p. 6. |

| 3 | Deutsche Bundesbank Monthly Report, December 2025, p. 6. |

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 18 |

markets. However, investment behaviour in agriculture also depends heavily on political and regulatory conditions as well as on public funding.

The Association of Chambers of Agriculture (Verband der Landwirtschaftskammern; VLK) expects declining business results for agricultural enterprises of all types in the current financial year 2025/26. Despite high yields of market crops and basic fodder from the 2025 harvest across Germany, farms face significant economic challenges, as market prices – particularly for arable crops and most animal products – are under pressure, not least due to challenging conditions in national and international agricultural markets. With regard to agricultural inputs, the VLK expects some easing in expenditure on seeds and planting materials as well as fuels. By contrast, higher costs are anticipated for fertilisers, crop protection, services and personnel.1

The “Rentenbank Agricultural Barometer” survey commissioned by Rentenbank reflects farmers’ assessment of their current and future economic situation in Germany. According to the latest survey results from December 2025, the assessment of the future economic situation has deteriorated further compared with the September survey. Farms engaged in pig and poultry farming assess their future economic situation somewhat more positively than other types of operations. High agricultural input costs, agricultural policy and low producer prices are the main reasons for negative assessments. Despite the subdued sentiment, 62% of respondents are planning investments (previous survey: 60%), albeit with a somewhat lower average investment volume.2

The economic recovery in Germany also offers growth opportunities for companies in the agribusiness sector. Nevertheless, challenges remain, particularly with regard to labour and energy costs, while uncertainties arising from geopolitical crises and US tariffs continue to weigh on exports. Certain food trends observed in recent years are expected to persist, such as health awareness, sustainability and convenience.3

In the field of renewable energy, Rentenbank expects further growth momentum. For 2026, the German Wind Energy Association (Bundesverband Windenergie; BWE) anticipates additional gross installations of wind power capacity of between 8 and 8.5 GW.4 By contrast, the German Solar Association (Bundesverband Solarwirtschaft; BSW) expects a slight decline in photovoltaic expansion and anticipates a deterioration in the funding environment and regulatory framework.5

Geopolitical tensions are leading primarily to higher price volatility in agricultural markets, affecting both agricultural commodities and agricultural inputs such as energy, fertilisers and construction materials. In addition, agricultural input costs are expected to rise further as a result of the increase in CO₂ taxation on heating and motor fuels at the beginning of 2026, and from 2026 onwards the EU’s carbon border adjustment mechanism will make imported mineral fertilisers more expensive.6

| 1 | VLK: Forecast of economic developments for the 2025/26 financial year. |

| 2 | Rentenbank Agricultural Barometer, December 2025 survey. |

| 3 | EY: “Economic Barometer Agribusiness in Germany 2026”, pp. 39–40. |

| 4 | BWE press release: “Onshore wind energy expansion in 2025: sustaining strong growth, ensuring resilience” (15 January 2026) |

| 5 | BSW press release: “Photovoltaics surpass lignite and natural gas” (5 January 2026) |

| 6 | https://www.agrarheute.com/markt/duengemittel/eu-verschaerft-klimaschutz-duengerpreise-duerften-2026-deutlich-steigen-636955 |

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 19 |

In general, volatile agricultural markets (including those affected by weather events) are not a new phenomenon for agriculture. We therefore do not expect international crises to have any significant impact on our promotional activity. Only under extreme scenarios is a degree of restraint in agricultural investment to be expected. As an instrument, we offer liquidity assistance loans.

German agricultural exports to the United States are of minor importance (1.3% of total German agricultural exports)1, meaning that the imposition of tariffs by the United States has no material impact on German agriculture, with only a few exceptions (e.g. viticulture). Accordingly, US tariff policy is also unlikely to have a significant effect on our promotional activity.

In January of the current year, a comprehensive free trade agreement between the EU and South American countries (the Mercosur Agreement) was signed and is currently under review by the European Court of Justice. This will create the world’s largest free trade area, in which tariffs on more than 90% of exports are to be eliminated. This will improve access for German agribusiness to the markets of the Mercosur countries, for example for dairy products, confectionery, fresh fruit and wine, particularly also for organic products and processed foods. In addition, protection for traditional geographical indications (e.g. “Black Forest ham”) will be strengthened. The opening of the European market to imports of beef, poultry, sugar and ethanol is limited by supply quotas, long transition periods and bilateral safeguard clauses. Imports from Mercosur countries will also continue to be subject to EU regulatory requirements.2 It is currently unclear when the agreement will enter into force. No impact on our promotional activity is expected.

The same applies to the current free trade agreement between the EU and India. While this improves access for German agribusiness to the Indian market, certain European agricultural sectors remain fully protected, as products such as beef, poultry meat, rice and sugar are excluded from liberalisation. All imports from India will likewise remain subject to EU regulatory requirements.3

Business development forecast

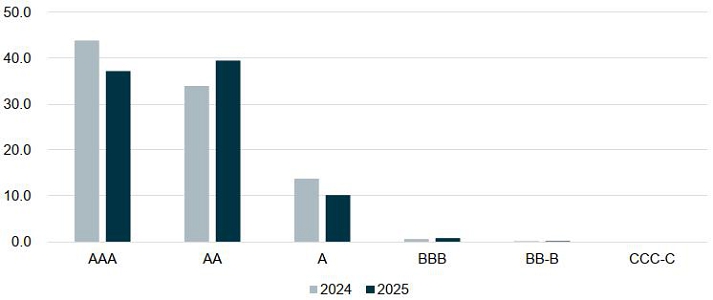

In the 2025 financial year, loan loss provisions remained largely unchanged. Rentenbank expects only minor fluctuations in loan loss provisions in 2026. No significant changes are anticipated for the volume-weighted average credit quality of the loan portfolio, which is rated AA. This is supported by the low unsecured portion of the credit portfolio of 8.1% and the stable development, with counterparties continuing to have strong credit ratings. Rentenbank continuously monitors the economic performance of its counterparties. In 2025, there was no need for specific loan loss provisions (specific valuation allowances, and none are included in the planning for 2026.

To forecast future net assets, financial position and results of operations, annual and multi-year plans are prepared over a five-year horizon. These include planning for new business, portfolio development, capital, income and costs, as well as adverse scenarios. In addition, the planning includes key regulatory metrics relevant for management purposes and a forecast of the

| 1 | https://www.bmel-statistik.de/aussenhandel/deutscher-aussenhandel/aussenhandel-mit-den-usa |

| 2 | https://www.bmleh.de/SharedDocs/FAQs/DE/faq-eu-mercosur/FAQ-eu-mercosur_List.html |

| 3 | https://germany.representation.ec.europa.eu/news/eu-und-indien-beschliessen-freihandelsabkommen-2026-01-27_de |

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 20 |

development of risk-bearing capacity. The forecasts set out below relate in each case to the plan for 2026.

Planning for the 2026 financial year

Under the current planning assumptions, the “Promotional Activity” segment is expected to show an average portfolio broadly in line with the previous year, with largely unchanged lending and funding margins in new business. Although planned new business margins for 2026 are below the margins on maturing positions, the reduction in provisions for subsidies in special promotional loans results overall in a moderate increase in planned net interest income in the “Promotional Activity” segment. The reduction in provisions is due to a change in presentation and is not related to the actual subsidies granted.

Special promotional loans will continue to be the main focus of lending activity. Rentenbank is planning new business of EUR 6.2 billion for 2026.

In the “Promotional Activity” segment, the portfolio of securities as well as registered bonds and promissory notes is expected to remain broadly at the 2025 level.

In 2022, Rentenbank expanded its promotional offering for financing start-ups aligned with its promotional mandate to include investments in venture capital funds. To date, commitments in the three-digit million euro range have already been made. Further investments in the mid double-digit million euro range are planned for 2026.

In the “Capital Investment”, Rentenbank expects interest income in 2026 to be slightly above the previous year’s level. This is due primarily to new business yields exceeding the yields on maturing investments, as well as the investment of new allocations.

Net interest income in the “Treasury Management” segment is expected to remain at the current level in 2026 due to the continued narrowing of margins.

Overall, a moderately increasing trend in net interest income across the three segments is planned for 2026.

The number of employees is expected to increase further in 2026.

Following a decline in the previous year, the number of training days per employee is expected to rise moderately.

Administrative expenses for 2026 are expected to be below the previous year’s level. The anticipated increase in personnel expenses is likely to be more than offset by a decline in IT consulting expenses. Against the backdrop of developments in income and costs, an increase in the operating result before “Loan loss provisions / valuation effects” is planned overall for 2026. Rentenbank will continue to be able to deliver its planned promotional activities in full from its ongoing income.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 21 |

As a result of the expected moderate increase in net interest income and the decline in administrative expenses, the cost-income ratio is expected to decrease slightly compared with 2025.

Rentenbank’s ESG ratings are expected to remain at least at their current level.

Its corporate citizenship is also expected to

remain broadly in line with the previous financial year.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 22 |

Opportunities and risks

Compared with the results planned for 2026, changes in the underlying

conditions may give rise to additional opportunities and risks for business development.

The further development of the economic situation in Germany will remain subject to uncertainty in 2026. In addition to weak domestic

economic momentum, geopolitical tensions are having a negative impact on the global economy. These factors could contribute to

a pronounced reluctance to invest and thereby impair economic development. Against this backdrop, the risk of a persistently subdued

or declining economic environment remains.

In such a scenario, the key factors affecting opportunities and risks, in addition to loan demand, are developments in interest rates and credit spreads. However, owing to Rentenbank’s business model as a promotional bank, the opportunities and risks for its net assets, financial position and results of operations are limited.

In an economically uncertain environment, Rentenbank’s own credit spreads have generally proved relatively stable on the basis of its rating. A widening of counterparties’ credit spreads would then have a positive effect on net interest income. Rising interest rates would likewise have a positive effect on net interest income, as Rentenbank invests its equity over the long term in fixed-income positions.

For net assets, this would have a temporary adverse effect through an increase in unrealised losses. In a deteriorating economic environment, there is a risk that credit quality in the credit portfolio could worsen and/or that loan demand, and thus the volume of new business, could decline. In such an environment, the economic conditions for venture capital investments would also deteriorate, increasing the risk of impairments and defaults.

Further reporting on risks is provided in the Risk Report section.

Additional burdens on administrative expenses could arise from

further regulatory requirements that are not yet known. This could lead to higher IT and personnel costs. In addition, further

changes to the IT infrastructure may become necessary beyond the investments already planned. As part of the refurbishment of the

listed bank building on Hochstrasse, adverse changes to planning assumptions may arise, which would result in correspondingly higher

costs.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 23 |

Development in the current financial year

At the beginning of the year, the operating result before loan loss provisions / valuation effects was above both the previous year’s level and the planned level. This was due in particular to net interest income, which benefited from several factors at the beginning of the year.

Based on developments to date in the current financial year, the Management Board currently considers the planned operating result for the 2026 financial year to be achievable.

The forecast report contains certain forward-looking statements based on the current expectations, assumptions, estimates and projections of the Management Board, as well as on the information available to it. These include, in particular, statements regarding plans, business strategy and prospects. Words such as “expect”, “anticipate”, “intend”, “plan”, “believe”, “seek”, “estimate” and similar expressions identify such forward-looking statements. These statements should not be understood as guarantees of the future developments referred to therein; rather, they depend on factors that involve risks and uncertainties and are based on assumptions that may prove to be incorrect. Unless required otherwise by law, Rentenbank assumes no obligation to update forward-looking statements after the publication of this information.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 24 |

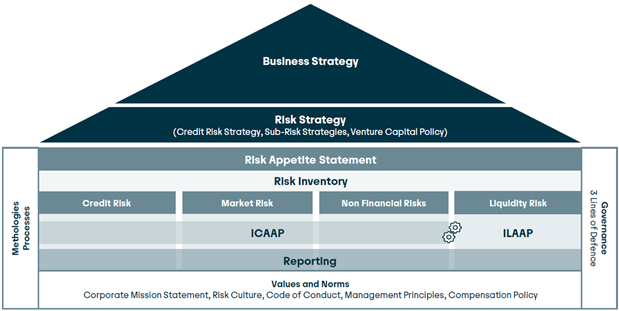

Risk report

Rentenbank’s Risk Management System (RMS) serves to identify, manage and monitor the risks arising from its business activities. Rentenbank’s risk management is based on regulatory requirements and the specific features of its business model as a promotional bank. The key elements of risk management are:

| • | the risk strategy, which is derived consistently from the market-oriented business strategy, |

| • | the Risk Appetite Framework and the Risk Appetite Statement, |

| • | the risk culture, |

| • | the ongoing review of the adequacy of capital and liquidity, |

| • | a clear organisational and procedural structure for the RMS within a three-lines-of-defence structure. |

Rentenbank is not a CRR institution within the meaning of Section 1 (3d) KWG and is supervised at national level by BaFin and Deutsche Bundesbank. Nevertheless, pursuant to Section 1a (1) KWG, the provisions of the CRR apply to Rentenbank. In addition, Rentenbank does not maintain a trading book within the meaning of Article 4 (1), items 85 and 86 CRR.

Organisation of risk management

Overall responsibility for the RMS lies with the Management Board. It is informed regularly and on an ad hoc basis about the risk situation.

As part of its regular meetings, the Supervisory Board is informed by the Management Board about the risk situation; if material risk-relevant events occur, ad hoc information is provided.

The Supervisory Board has established various committees to address specific topics. In the Risk Committee, the Management Board reports on the risk situation. In addition to discussing the risk situation, the Risk Committee addresses the risk strategy and material risk-related matters. The Audit Committee focuses in particular on the audit report and the annual financial statements. Both committees, as well as the competent supervisory authorities, receive the risk report on a quarterly basis.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 25 |

Rentenbank has established various bodies

for business and risk management. The central body for risk management is the Risk Board, which meets at least

quarterly.

It discusses key questions and topics relating to risk management and advises the Management Board on these

matters. In addition to the Management Board, its members are the heads of the Risk Controlling Department and the Cyber

Security & Non-Financial Risk Department, as well as the heads of the Credit, Finance, Treasury and Promotional activity

divisions. The Financial Board addresses Rentenbank’s financial position, while the Market Board deals with promotional

activity topics and treasury topics. The Sustainability Board addresses the requirements and the operational and strategic

implications of sustainability for Rentenbank.

To ensure a robust RMS, Rentenbank has organised its Internal Control System (ICS) within a clear three-lines-of-defence structure. The first line of defence consists of primary and key controls in the operational units. The second line of defence comprises the Regulatory Working Group (Arbeitskreis Regulatorische Themen; ART), the special MaRisk functions Risk Controlling and Compliance, the ICT risk control function under the Digital Operational Resilience Act (DORA), the Chief Information Security Officer (CISO), the Central Outsourcing Officer, the officers responsible for anti-money laundering and other criminal offences, and the Data Protection Officer. Internal Audit constitutes the third line of defence.

Responsibility for the Risk Controlling function under MaRisk (Mindestanforderungen an das Risikomanagement; minimum requirements for risk management) lies with the Chief Risk Officer (CRO). The Risk Controlling Department performs key tasks of the Risk Controlling function. These include supporting senior management in all matters of risk policy, in particular in the development and implementation of the risk strategy, regularly monitoring limits within risk-bearing capacity, risk reporting, the daily valuation of financial instruments and market conformity checks, as well as risk assessment in the New Products Process (NPP). The Cyber Security & Non-Financial Risks (CNR) Department, newly established in 2025, performs a substantial part of these tasks in relation to non-financial risks.

In accordance with the requirements of MaRisk, risk monitoring and reporting are carried out independently of the Promotional activity and Treasury market divisions.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 26 |

The back-office function is performed by the Credit division, which provides the independent second vote for lending decisions. In addition, this division monitors compliance with counterparty risk limits as part of credit portfolio management.

Rentenbank’s Compliance function reports directly to, and is directly subordinate to, the Management Board. In addition, a central office has been established for the prevention of money laundering, terrorist financing and other criminal offences. The Anti-Money Laundering Officer is organisationally directly subordinate to the Management Board and reports directly to it.

The CNR Department is also responsible for performing and ensuring all matters relating to information security. The head of the CNR Department performs the roles of ICT risk control function, Central Outsourcing Officer and Chief Information Security Officer.

Internal Audit reviews and evaluates, on a risk-oriented

and process-independent basis, the propriety of activities and processes as well as the adequacy and effectiveness of the RMS and

the ICS. It reports directly to the Management Board and performs its duties autonomously and independently.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 27 |

Business and risk strategy

Rentenbank’s risk strategy is derived from, and is consistent with, the market-oriented business strategy and comprises, in addition to the overarching cross-risk strategy, sub-strategies relating to individual risk types as well as the Venture Capital Policy.

The Risk Appetite Framework comprises all strategies and guidelines, methods, processes, responsibilities, controls, and systems from which the risk appetite is derived, communicated, and monitored. In addition to minimum target values, warning thresholds and limit systems, this also includes appropriate compliance and an appropriate risk culture.

The Risk Appetite Statement describes the extent to which Rentenbank is willing to assume risks and allocate risk coverage potential in order to achieve its strategic objectives. Risk appetite is defined on the basis of quantitative requirements and qualitative statements. These requirements are specified through the determination of limits and warning thresholds within the framework of risk-bearing capacity.

Through the risk strategy, the Risk Appetite Framework and the Risk Appetite Statement, the Management Board defines the key parameters

for risk management.

The credit risk strategy is shaped by the promotional mandate. To promote the agricultural sector and rural areas, financial resources are, in principle, provided only to banks established in the Federal Republic of Germany or another EU country that conduct business with agricultural enterprises, companies operating in upstream and downstream sectors, or companies active in rural areas. In this context, special promotional loans are restricted to Germany as the location for investment.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 28 |

In addition, Rentenbank may enter into participations, acquire interests in venture capital funds and provide debt capital to German federal states and German municipalities in the form of promissory notes, registered securities or bearer securities.

Accordingly, lending business is limited to the refinancing of banks or institutions and financial institutions within the meaning of Article 4 CRR, as well as to the provision of capital to domestic public authorities.

As part of the credit risk strategy, it has been stipulated that lending to companies in the direct lending business may only be undertaken through a subsidiary of Rentenbank. No corresponding new business was concluded in 2025.

Derivatives are used exclusively as hedging instruments and are only entered into with counterparties with whom Rentenbank has concluded a collateral agreement.

Rentenbank’s credit risk strategy requires prudent selection of counterparties and products in all business activities. In line with its core competencies and business model, Rentenbank focuses on the banking sector and public-sector borrowers. Rentenbank has a sectoral concentration risk vis-à-vis the banking sector, which arises from its promotional mandate. As an indicator of Rentenbank’s risk profile, the average credit quality of the overall credit portfolio – taking product ratings into account – must be at least A+.

The principal objective of the market risk strategy is to avoid risks that could jeopardise net interest income and thus the fulfilment of the promotional mandate. At the same time, market risks are limited and managed from a present-value perspective within the framework of economic risk-bearing capacity. Foreign currency positions are generally closed out.

The objectives of the liquidity risk strategy are to ensure solvency at all times, including under stress conditions, and to optimise the refinancing structure.

Non-financial risks, which include operational and strategic risks, are managed with the objective of preventing losses and thereby ensuring the quality of all operational processes at Rentenbank Compliance with regulatory requirements and the minimisation of reputational risks through appropriate communications management and a code of conduct are also integral components of the risk strategy.

Risk culture

Rentenbank’s risk culture shapes its self-image in the day-to-day handling of risks. It comprises the totality of the company’s norms, attitudes and behaviours with regard to risk awareness, risk appetite and risk management. Rentenbank has defined and established its approach to risk culture. In addition, indicators have been defined to monitor how risk culture is put into practice. Key elements of the risk culture are the autonomous and responsible handling of Rentenbank’s risks by all managers and employees within the scope of their assigned responsibilities, as well as the

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 29 |

accountability of all managers and employees for their risk behaviour. An employee survey was used to assess the current state of risk culture and to identify measures for its further improvement.

Risk inventory

Through the risk inventory, Rentenbank obtains a structured overview of all risks that may impair its net assets, capital base, results of operations or liquidity position. This also includes risk concentrations within individual risk types and across risk types.

The resulting risk profile forms the basis for the Risk Appetite Statement and for risk measurement, monitoring and management at Rentenbank. In addition, the risk inventory serves to increase risk transparency and thereby supports Rentenbank’s risk culture. The risk profile comprises counterparty default risk, market risk, liquidity risk and non-financial risks as the material risk types. Non-financial risks comprise operational risks and strategic risks. Risks arising from changes in the areas of environmental, social and governance (ESG) are also a focus of risk analysis. These are incorporated into the RMS as risk drivers of the various risk types, including through scenario analyses.

In addition, material risks are identified and reported using indicators based on quantitative and qualitative risk characteristics. Further risks are identified in the New Products Process (NPP), in key ICS controls and in day-to-day control and monitoring activities.

Validation of risk measurement

A validation framework aligned with regulatory requirements defines the modalities for validating the methods and procedures used to measure the material risk types in Rentenbank’s ICAAP and ILAAP.

The methods and procedures are validated at least

annually, with independence between method development and validation ensured through an organisational separation. The aim of

validation is to critically review, on the basis of quantitative and qualitative analyses, the quality of the methods or models

used for risk measurement, as well as their parameters and assumptions. The assessment is performed in accordance with a defined

methodology. The validation results are discussed in the Risk Committee.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 30 |

Risk-bearing capacity

Rentenbank’s risk-bearing capacity concept is the central element of the Internal Capital Adequacy Assessment Process (ICAAP) and the basis for the operational implementation of the risk strategy. The objectives of the risk-bearing capacity concept are to ensure the institution’s continuation in fulfilling its promotional mandate while complying with regulatory requirements, as well as to safeguard the institution’s substance over the long term and to protect creditors against losses from an economic perspective. These objectives are reflected in the two perspectives of the risk-bearing capacity concept, which comprises a normative approach and an economic approach. Risk management processes are designed to meet these objectives and requirements on an equal footing. Monitoring of limits within risk-bearing capacity is supplemented by stress tests. These are reported regularly to the Management Board and discussed there as well as in the Risk Committee.

Normative approach

The management objective of the normative approach is to comply with all minimum regulatory capital requirements and provisions. It is assessed whether the capital base, both on a reporting-date basis and within the multi-year capital planning horizon (covering five years), ensures compliance with all regulatory requirements and thus the institution’s continued existence in the baseline scenario and in the adverse scenarios. The capital base should also enable the sustainable pursuit of the business strategy in these scenarios.

The following table shows regulatory own funds under the normative approach at the reporting date compared with the previous year:

|

31 December 2025 mEUR |

31 December 2024 mEUR | |

| Subscribed capital | 135.0 | 135.0 |

| Retained earnings | 1,252.6 | 1,233.6 |

| Fund for general banking risks | 3,553.5 | 3,479.8 |

| Intangible assets | -56.2 | -48.4 |

| Tier 2 capital | 0.0 | 0.0 |

| Regulatory own funds | 4,884.9 | 4,800.0 |

The increase in own funds compared with the previous year resulted from an increase in retained earnings and an increase in the fund for general banking risks following the adoption of the 2024 annual financial statements.

Risk-weighted assets (RWA) are shown in the following table:

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 31 |

|

Risk amount 31 December 2025 mEUR |

Risk amount 31 December 2024 mEUR | |

| Credit risk | 13,909.6 | 11,454.8 |

| CVA charge | 612.1 | 530.5 |

| Operational risk | 487.3 | 544.3 |

| Total RWA | 15,008.9 | 12,529.6 |

The expected significant increase in RWA is due to the application of CRR III; the effect on capital ratios is mitigated to some extent by profit retention. Even after application of CRR III, the capital ratios remain well above the regulatory minimum requirements:

| Reporting date | ||||

|

(%) |

Reporting date 31 December 2025 |

2026 |

Baseline scenario 2027 |

2028 |

| Total capital ratio | 32.6 | 33.3 | 33.5 | 33.9 |

| Tier 1 capital ratio | 32.6 | 33.3 | 33.5 | 33.9 |

| Common Equity Tier 1 capital ratio | 32.6 | 33.3 | 33.5 | 33.9 |

| Leverage ratio | 11.5 | 10.7 | 11.1 | 11.8 |

In 2025, no material impact of the geopolitical crises and Germany’s economic stagnation on Rentenbank’s risk metrics could be observed. For the baseline scenario of capital planning, it is assumed that the conflicts will persist while the economy recovers slightly. Rentenbank therefore expects the portfolio to develop in a relatively stable manner from a risk perspective in the baseline scenario. This is reflected accordingly in the capital ratios.

Regulatory requirements are met at the reporting date and in the baseline scenario of capital planning at all points in time considered.

In addition to the baseline scenario, various adverse scenarios with significantly negative market-wide and institution-specific developments are analysed in the capital planning. Even taking CRR III effects into account, all regulatory requirements are met at all times.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 32 |

Economic Approach

The objectives of the economic approach are to safeguard the institution’s substance over the long term and to protect creditors against losses from an economic perspective. For this purpose, the economic risk coverage potential is compared with the aggregate risk amount and reviewed both at the reporting date and within the baseline scenario of capital planning.

The risk coverage potential includes hidden reserves and hidden charges from securities and promissory notes of German federal states, including the related hedging transactions, as well as the reserves pursuant to Section 340f HGB. The profit and loss result accrued during the year is taken into account, whereas planned profits that have not yet been realised are not included.

At the reporting date, the risk coverage potential under the economic approach was as follows compared with the previous year:

|

31 December 2025 mEUR |

31 December 2024 mEUR | |

| Subscribed capital | 135.0 | 135.0 |

| Retained earnings | 1,272.1 | 1,252.6 |

| Fund for general banking risks | 3,576.3 | 3,553.5 |

| Hidden charges / reserves | 596.9 | 211.1 |

| Risk coverage potential | 5,580.3 | 5,152.2 |

In the economic risk coverage potential, the planned appropriation of the result achieved in 2025 is taken into account. This results in slightly higher figures for retained earnings (+EUR 19.5 million) and for the fund for general banking risks (+EUR 22.8 million), as well as an addition to reserves. The substantial increase in risk coverage potential in 2025 is attributable mainly to higher hidden reserves or lower hidden charges on securities, promissory notes and registered bonds.

Under the economic approach, risks arising from all

positions are considered irrespective of their accounting treatment. The risks are calculated on the basis of a confidence

level of 99.9% and a time horizon of one year. The risk amounts of the individual risk types are added without

taking diversification effects into account and are distributed as follows:

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 33 |

Risk amount 31 December 2025 mEUR |

Risk amount 31 December 2024 mEUR | |

| Credit risks | 468.3 | 470.5 |

| Market risks | 1,732.8 | 1,826.6 |

| of which: interest rate risks | 562.0 | 558.6 |

| of which: CVA risk from derivatives | 43.9 | 39.6 |

of which: spread and other risks |

1,111.9 | 1,213.4 |

| of which: risk buffer | 15.0 | 15.0 |

| Non-financial risks | 101.4 | 93.1 |

| of which: operational risks | 72.8 | 62.1 |

| of which: strategic risks | 28.6 | 31.0 |

| Total risk | 2,302.5 | 2,390.2 |

Risk-bearing capacity under the economic approach was ensured at all observation dates in 2025. All limits were complied with. Owing to the higher risk coverage potential and a decline in spread risks, utilisation of risk coverage potential at the reporting date was significantly lower at 41.26% than in the previous year (46.39%).

Stress tests

The purpose of stress tests is to analyse whether Rentenbank’s risk-bearing capacity remains ensured even under extraordinary but plausible cross-risk scenarios. For this purpose, a hypothetical scenario (economic downturn) and a historical scenario (financial market crisis followed by the sovereign debt crisis) are simulated. The scenarios consider both market-wide and institution-specific aspects. In doing so, geopolitical tensions and conflicts, as well as the resulting macroeconomic uncertainties – such as volatile energy prices, recurring supply bottlenecks and increased capital market volatility – were taken into account. These developments were translated qualitatively and quantitatively into their potential effects on refinancing costs, credit risks and Rentenbank’s capital market environment, so that the key risk impulses of the global environment are adequately reflected in the scenarios.

The key risk parameters underlying the stress scenarios are the deterioration in credit quality, changes in interest rates and increases in credit spreads. In the stress tests, the effects of the stress scenarios are analysed from both the normative and the economic perspective. Under the normative approach, the effects of the scenarios on the income statement and on equity, in particular the effects on risk-weighted assets, are simulated over a three-year horizon. Under the

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 34 |

normative approach, the dominant risk is counterparty default risk, while under the economic approach counterparty default risk and market risk are particularly relevant.

Risk-bearing capacity is ensured under both approaches even in the stress scenarios without recourse to regulatory relief measures relating to capital and liquidity requirements, thereby confirming Rentenbank’s comfortable capital position. In addition to these stress scenarios, a reverse stress test is used to examine which events would cause risk-bearing capacity no longer to be ensured. Furthermore, the effects of sustainability risks are examined in various scenarios (see separate section).

Credit risks

Definition

Credit risk is the risk that a counterparty will fail to meet its payment obligations, or will meet them only in part, as well as the risk of valuation losses resulting from rating downgrades. A distinction is made between the following risk sub-types: default risk, migration risk and country risk.

Lending business is largely limited to the refinancing of banks or institutions and financial institutions within the meaning of Article 4 of the CRR, as well as other interbank business. In the case of special promotional loans, the default risk relating to the ultimate borrower lies with the local bank. In addition, German federal states, districts and municipalities are refinanced.

Risk assessment and management

The key risk parameters used to determine credit risk are probability of default, loss given default, exposure at default and the correlations between counterparties, which are used in the credit portfolio model to simulate simultaneous defaults by counterparties.

Probability of default is derived from the credit assessment of counterparties. The credit assessment is carried out using an internal risk rating system. Under this procedure, individual counterparties or types of business are assigned to one of 20 rating categories. The best ten rating categories, from AAA to BBB-, are reserved for counterparties with low risks (“investment grade”). In addition, the seven rating categories from BB+ to C are intended for latent or elevated latent risks, while the three rating classes from DDD to D are intended for non-performing loans and defaulted counterparties.

The credit assessment of counterparties is reviewed at least annually on the basis of an evaluation of their annual financial statements and an analysis of their economic circumstances. In doing so, account is taken of financial ratios, qualitative characteristics, shareholder background and further support factors, such as membership of an institutional protection scheme or government liability mechanisms. The country risk of the counterparty’s country of domicile is also taken into account in determining credit quality. For certain products, such as German mortgage bonds (Pfandbriefe), the

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 35 |

associated collateral or cover assets are taken into account as an additional criterion for determining the product rating, alongside the relevant national statutory provisions. If current information becomes available regarding negative financial data or a weakening of a counterparty’s economic outlook, the credit rating is reviewed and adjusted if necessary.

Loss given default quantifies the proportion of an exposure that remains irrecoverable after a counterparty has defaulted and the collateral provided has been realised. To quantify counterparty credit risks, Rentenbank uses product-specific or business-type-specific loss given default parameters, which are determined using analytical and expert-based methods. In particular, the recovery chain of special promotional loans granted under the so-called on-lending procedure is taken into account in the assessment and parameterisation of loss given default for special promotional loans. In addition, Rentenbank relies on external data sources for certain types of business.

Exposure at default corresponds to the reporting-date balance plus off-balance-sheet transactions of individual counterparties. This corresponds to the residual amount of the receivable or the market value. For derivatives, exposure is determined as the amount of the exposure plus an add-on for market value fluctuations, taking contractual netting and posted and received collateral (cash collateral) into account.

Credit risk under the economic approach (credit value at risk) is calculated using a credit portfolio model, taking into account correlations between counterparties and including migration risks.

The method described makes it possible to assess, monitor and manage risks within the meaning of MaRisk. Negative developments and portfolio concentrations can thus be identified at an early stage and countermeasures initiated.

Limitation and monitoring

The overall credit ceiling for all counterparty default risk limits, as well as an unsecured ceiling, are set by the Management Board and thereby limit counterparty default risks. Concentration risks within Rentenbank are managed and limited at several levels through various targeted approaches. Country lending limits and currency transfer limits are also in place to limit risk.

A limit system manages the amount and structure of all counterparty default risks. Internal limits are recorded for all borrowers, issuers and counterparties and are, where appropriate, broken down by product and maturity. Rentenbank’s risk classification system constitutes the central basis for decisions on limit allocation. In addition, specific minimum credit qualities apply to certain business types or limit types.

The limitation of credit risks within the framework of risk-bearing capacity is based on the credit value at risk determined in the credit portfolio model.

| Landwirtschaftliche Rentenbank | Annual Report 2025 | 36 |

In addition, risk indicators provide early signals of a possible increase in risk or shifts in risk within the portfolio. Warning thresholds ensure that higher levels of limit utilisation are identified at an early stage and that appropriate courses of action can be taken.

Limits are monitored on a daily basis. Limit overruns are immediately reported to the Management Board.