Exhibit 99.1

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the Three Months Ended March 31, 2026 and 2025

Dated: May 6, 2026

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

GENERAL INFORMATION

This Management’s Discussion and Analysis (“MD&A”) is management’s interpretation of the results and financial condition of IsoEnergy Ltd. and its subsidiaries (“IsoEnergy” or the “Company”) for the three months ended March 31, 2026 and includes events up to the date of this MD&A. This discussion should be read in conjunction with the unaudited condensed consolidated interim financial statements for the three months ended March 31, 2026 and 2025 and the notes thereto (the “Interim Financial Statements”) and other corporate filings, including the Company’s audited consolidated financial statements for the years ended December 31, 2025 and 2024 and the notes thereto (the “Annual Financial Statements”) and the Annual Information Form for the year ended December 31, 2025 (the “AIF”), which have been filed on and are available under the Company’s profile on SEDAR+ at www.sedarplus.ca and EDGAR at www.sec.gov. All dollar figures stated herein are expressed in Canadian dollars and referenced as “$”, unless otherwise specified. Monetary amounts expressed in US dollars and Australian dollars are referenced as “US$” and “AUD$”, respectively. This MD&A contains forward-looking information. Please see “Note Regarding Forward-Looking Information” for a discussion of certain of the risks, uncertainties and assumptions used to develop the Company’s forward-looking information.

Technical Disclosure

All scientific and technical information in this MD&A has been reviewed and approved by Dr. Dan Brisbin, P.Geo., Ph.D., IsoEnergy’s Vice-President, Exploration. Dr. Brisbin is a “Qualified Person” for the purposes of National Instrument 43-101 - Standards of Disclosure for Mineral Projects (“NI 43-101”). Dr. Brisbin has verified the data disclosed, including sampling, analytical and test data.

All chemical analyses disclosed in this MD&A were completed for the Company by SRC Geoanalytical Laboratories in Saskatoon, Saskatchewan, which is independent of the Company.

All references in this MD&A to “Mineral Resource”, “Inferred Mineral Resource”, “Indicated Mineral Resource”, and “Mineral Reserve” have the meanings ascribed to those terms by the Canadian Institute of Mining, Metallurgy and Petroleum, as the CIM Definition Standards on Mineral Resources and Mineral Reserves adopted by CIM Council, as amended.

For additional information regarding the Company’s 100% owned Larocque East, Tony M, and Radio Projects and its 50% owned Thorburn Lake Project, including its Quality Assurance and Quality Control (“QA/QC”) and data verification procedures, please see the AIF and corresponding technical reports entitled “Technical Report on the Larocque East Project, Northern Saskatchewan, Canada” prepared by SLR Consulting (Canada) Ltd. and dated effective July 8, 2022 (the “Larocque East Technical Report”), “Technical Report on the Tony M Mine, Utah, USA, Report for NI 43-101” prepared by SLR International Corporation and dated effective September 9, 2022 (the “Tony M Technical Report”), “Technical Report for the Radio Project, Northern Saskatchewan” prepared by Tim Maunula, P. Geo. and dated effective August 19, 2016 and “Technical Report for the Thorburn Lake Project, Northern Saskatchewan” prepared by Tim Maunula, P. Geo. and dated effective September 26, 2016, all of which are available under the Company’s profile on SEDAR+ at www.sedarplus.ca.

Each of the Mineral Resource estimates with respect to the properties of IsoEnergy contained in this MD&A, except for the Larocque East Project and the Tony M Mine, are considered to be “historical estimates” as defined under NI 43-101 and are not considered to be current by IsoEnergy. See “Historical Estimates” for additional details.

1

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

Differences in United States and Canadian Reporting Practices

This MD&A has been prepared in accordance with the requirements of the securities laws in effect in Canada, which differ in certain material respects from the disclosure requirements promulgated by the Securities and Exchange Commission (the “SEC”). For example, the terms “mineral reserve”, “proven mineral reserve”, “probable mineral reserve”, “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are Canadian mining terms as defined in accordance with NI 43-101 and the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) - CIM Definition Standards on Mineral Resources and Mineral Reserves, adopted by the CIM Council, as amended. These definitions differ from the definitions in the disclosure requirements promulgated by the SEC. Accordingly, information contained in this MD&A may not be comparable to similar information made public by U.S. companies reporting pursuant to SEC disclosure requirements. The Company prepares its financial statements, which are referred to in this MD&A, in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”), and the audit of its annual financial statements is subject to auditing and independence standards of the Public Company Accounting Oversight Board in the United States.

Industry and Economic Factors that May Affect the Business

The business of mining for minerals involves a high degree of risk. IsoEnergy is an exploration and development company and is subject to risks and challenges similar to companies in a comparable stage and industry. These risks include, but are not limited to, the challenges of securing adequate capital; exploration, development and operational risks inherent in the mining industry; changes in government policies and regulations; the ability to obtain the necessary permitting; as well as global economic and uranium price volatility; all of which are uncertain.

As with other companies involved with mineral exploration and development, the Company is subject to cost inflation on exploration drilling and development activities and the Company may experience difficulty and / or delays in securing goods (including spare parts) and services from time-to-time.

The underlying value of the Company’s exploration and development assets is dependent upon the existence and economic recovery of Mineral Reserves and is subject to, among others, the risks and challenges identified above. Changes in future conditions could require material write-downs of the carrying value of the Company’s exploration and development assets. The Company does not have any current Mineral Reserves.

In particular, the Company does not generate revenue. As a result, IsoEnergy continues to be dependent on third party financing to continue exploration and development activities on the Company’s properties. Accordingly, the Company’s future performance will be most affected by its access to financing, whether debt, equity or other means. Access to such financing, in turn, is affected by general economic conditions, the price of uranium, exploration risks and the other factors some of which are described in the section entitled “Risk Factors” included below.

ABOUT ISOENERGY

IsoEnergy’s principal business activity is the acquisition, exploration and development of uranium mineral properties in Canada, the United States, and Australia. The Company’s common shares trade on the Toronto Stock Exchange (the “TSX”) under the trading symbol “ISO”, and as of May 5, 2025, trade on the NYSE American LLC (the “NYSE American”) under the trading symbol “ISOU”. The Company exists under the Business Corporations Act (Ontario).

On March 20, 2025, the Company completed the consolidation of its issued and outstanding common shares on the basis of one post-consolidation common share for every four pre-consolidation common shares and any fractional shares were rounded down to the nearest whole common share (the “Share Consolidation”). The Share Consolidation was implemented in connection with the Company’s application to list its common shares on the NYSE American.

As of the date hereof, NexGen Energy Ltd. (“NexGen”) holds approximately 29.9% of IsoEnergy’s outstanding common shares.

2

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

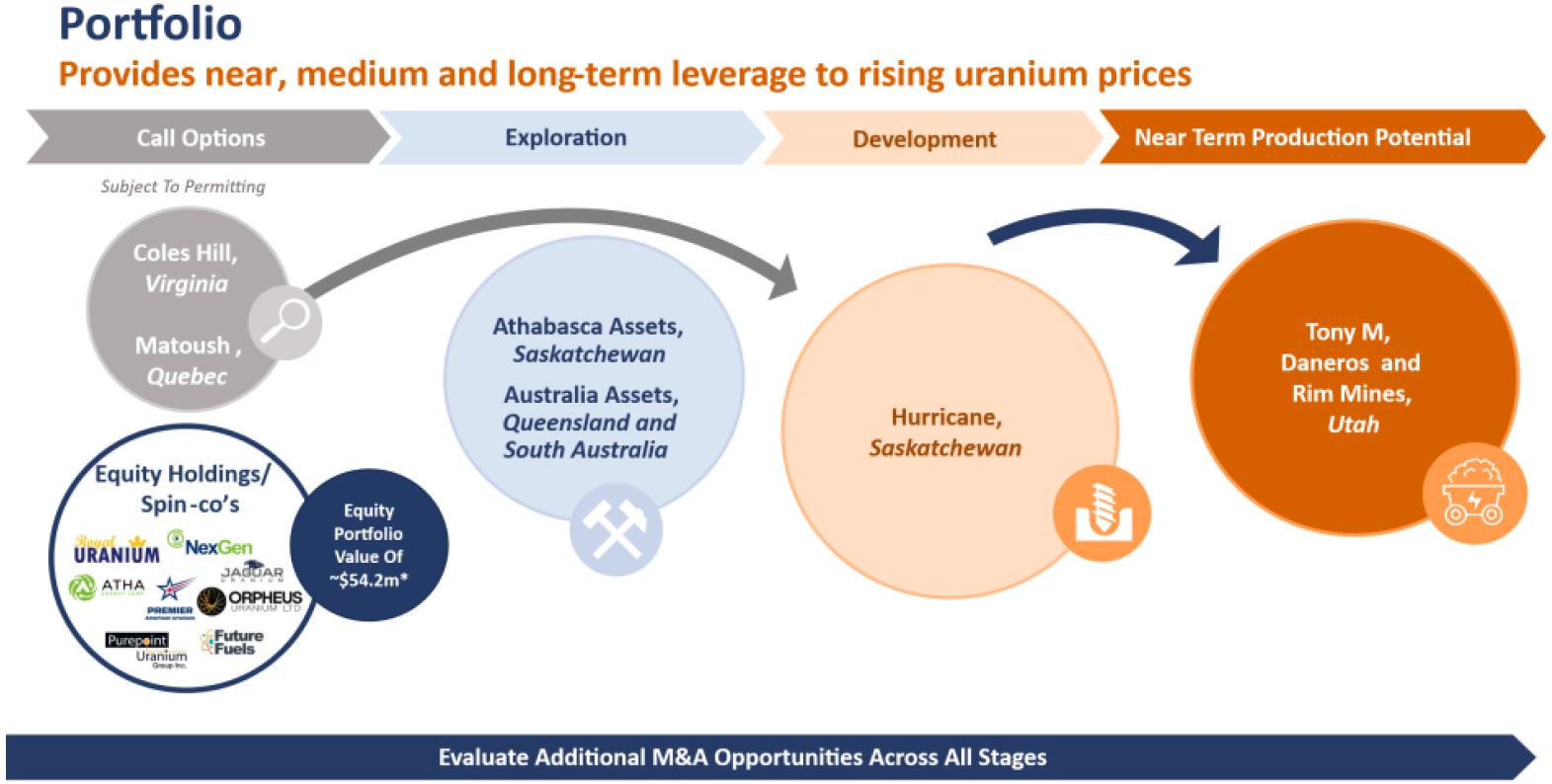

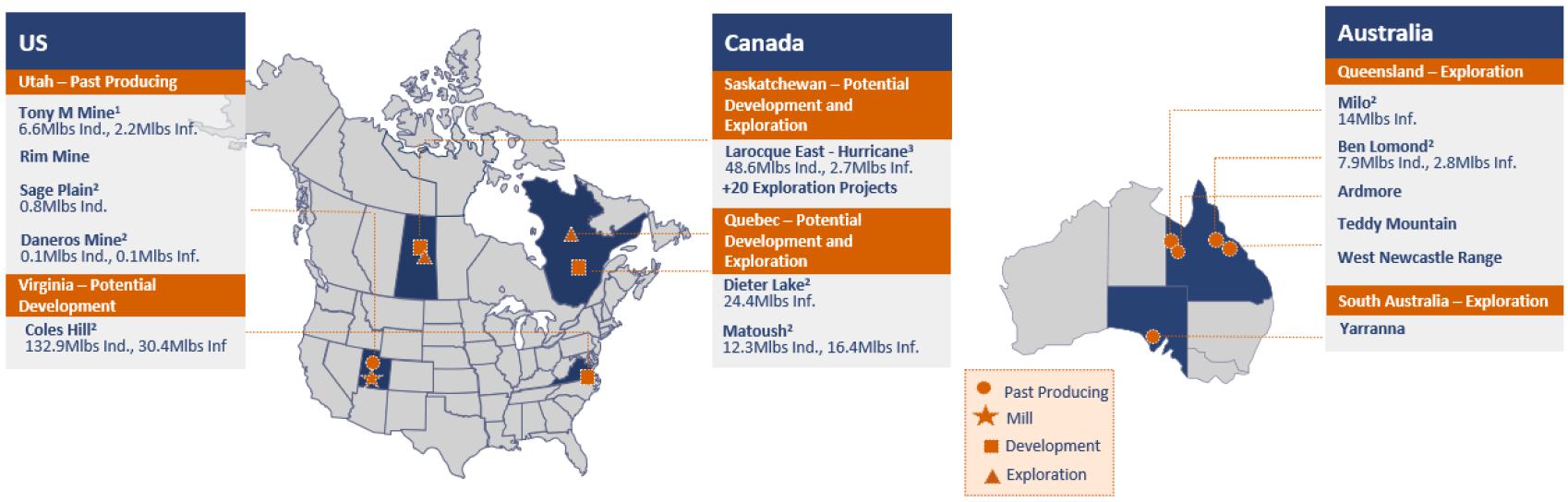

The Company is currently advancing its Larocque East Project in the Athabasca Basin, Saskatchewan, Canada, which is home to the Hurricane deposit (“Hurricane” or the “Hurricane Deposit”), which has the world's highest grade published Indicated uranium Mineral Resource – 48.6 million pounds of U3O8 at an average grade of 34.5% contained in 63,800 tonnes. The Company also holds a portfolio of permitted, past-producing conventional uranium mines in Utah with toll milling agreements in place with Energy Fuels Inc. (“Energy Fuels”). These mines are currently on stand-by, ready for a potential restart as market conditions permit, positioning IsoEnergy as a near-term uranium producer. The Company also has a 50% interest in a joint venture with Purepoint Uranium Group Inc. (“Purepoint Uranium”), with respect to a portfolio of exploration projects in the Athabasca Basin (the “Purepoint Joint Venture”). The Company’s portfolio includes projects and equity holdings in companies with uranium assets at varying stages of exploration and development, providing near, medium, and long-term leverage to rising uranium prices. None of the Company’s projects are currently in production and no decisions have been made to bring any of the Company’s projects to the production stage.

* Equity holdings include investments in NexGen, Premier American Uranium Inc., Atha Energy Corp., Purepoint Uranium, Future Fuels Inc., Jaguar Uranium Corp., and Orpheus Uranium Ltd. based on market close of April 27, 2026, and Royal Uranium Inc. at its implied fair value on the same date.

IsoEnergy’s uranium mineral properties are reflected below.

| 1. | For additional information please refer to the Tony M Technical Report (as defined herein). |

| 2. | This estimate is a “historical estimate” as defined under NI 43-101. A Qualified Person has not done sufficient work to classify the historical estimate as current Mineral Resources and the Company is not treating the historical estimate as current Mineral Resources. See “Historical Estimates” below for additional details. |

| 3. | For additional information please refer to the Larocque East Technical Report (as defined herein). |

As an exploration stage company, IsoEnergy does not have revenues and is expected to generate operating losses. As of March 31, 2026, the Company had cash and cash equivalents of $130,537,804, an accumulated deficit of $105,174,420, and adjusted working capital of $183,253,876 (as defined in “Non-IFRS Financial Measures” below).

3

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

YEAR-TO-DATE 2026 HIGHLIGHTS

| · | Exploration update in the Athabasca Basin and Utah |

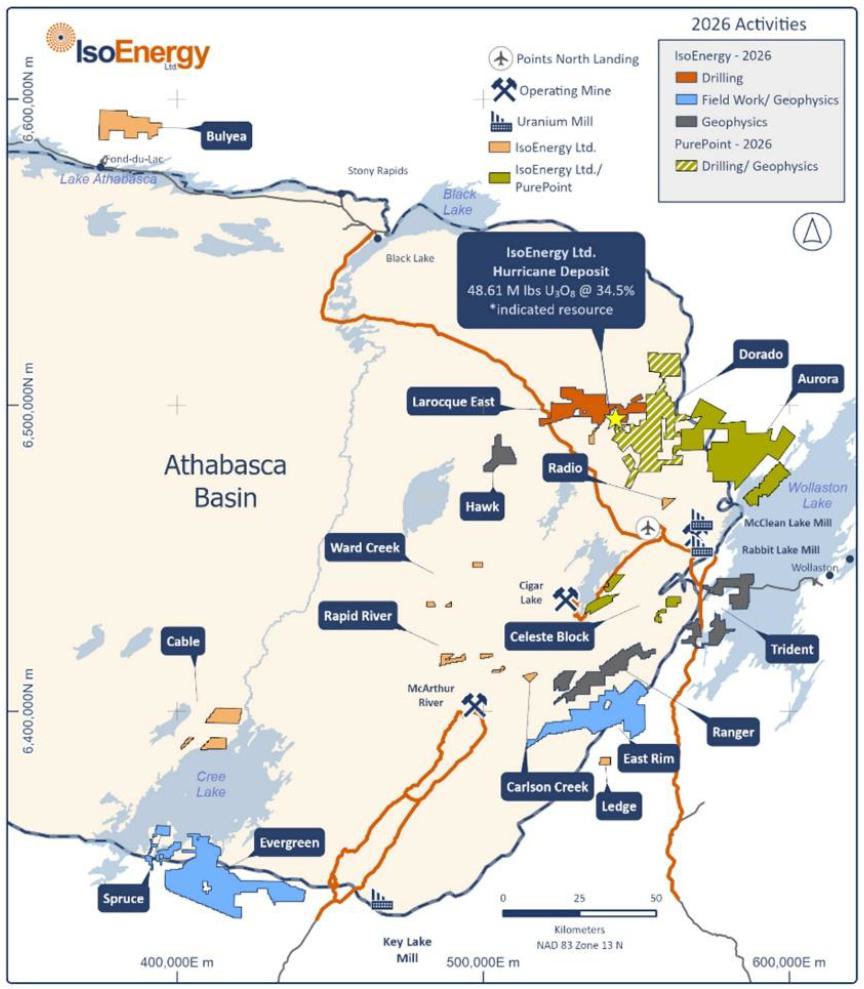

A total of 6,804 metres of drilling in 17 diamond drill holes were completed for the 2026 winter exploration program at the Larocque East Project. The program focused on drilling at the Hurricane Deposit and testing greenfield targets up to three kilometers along the Larocque regional geological-geophysical corridor (the “Larocque Trend”) (Figure 2). Mineralization was intersected in multiple holes along the South Trend of the Larocque East Project. The 2026 exploration program at the Dorado Project, operated through the Purepoint Joint Venture, was completed in nine holes totalling 5,210 metres which was successful in extending the uranium mineralization at the project.

Mobilization of drilling equipment for the exploration program at the Flatiron Project in Utah has been completed. The drilling program at the Flatiron Project is expected to commence shortly, which plans for the drilling of seven surface rotary holes totalling 11,000 feet.

| · | Commencement of key work programs at Tony M |

The Company completed the mining component of a bulk sample program, which is a critical step in defining the scope and economics of potential future production. The results of the bulk sample program are currently being evaluated, and its results are intended to be used as inputs in other studies planned for 2026. The Tony M Mine remains fully permitted and the results of the completed bulk sample program and planned technical studies are expected to assist in the planning of future mining activities and the determination of a uranium price that may support mining activities at the Tony M Mine.

| · | Base Shelf Prospectus |

The Company filed a final base shelf prospectus (the “Prospectus”) in Canada and a registration statement in the United States on January 13, 2026. The Prospectus provided for the offering up to $250 million in aggregate of common shares, warrants, units, debt securities, and subscription receipts of the Company in Canada and the United States for a period of 25 months following the filing of the Prospectus.

| · | 2026 Financing and Concurrent Private Placement |

On January 27, 2026, the Company closed a “bought deal” financing whereby the Company issued 3,833,410 common shares at a price of $15.00 per share for gross proceeds of approximately $57.5 million (the “2026 Financing”). The underwriters were paid a cash commission of 5% of the gross proceeds of the 2026 Financing.

Concurrent with the 2026 Financing, the Company completed a non-brokered private placement whereby the Company issued 1,666,667 common shares to NexGen at a price of $15.00 per share for gross proceeds of approximately $25.0 million (the “2026 Concurrent Private Placement”). The 2026 Concurrent Private Placement enabled NexGen to maintain its pro-rata ownership interest in the Company.

| · | Launch of At-The-Market equity program |

On April 17, 2026, the Company entered into an equity distribution agreement (the “Distribution Agreement”) with a group of agents (the “Agents”). The Distribution Agreements allows to Company to distribute up to $50.0 million of its common shares, through the Agents, through the NYSE American or TSX (the “ATM Program”) at prices related to prevailing market prices or at negotiated prices.

4

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

DISCUSSION OF OPERATIONS

Three months ended March 31, 2026

During the three months ended March 31, 2026, the Company incurred $7,172,099 of exploration and evaluation spending on its exploration properties globally, as set out below. Most of the expenditures were at the Company’s Larocque East Project in the Athabasca Basin as further discussed below. See “Outlook” below for future exploration plans.

Exploration and evaluation spending

| Canada | United States | Australia | Total | |||||||||||||

| Drilling | $ | 2,552,686 | $ | 12,416 | $ | - | $ | 2,565,102 | ||||||||

| Studies and mine site management | - | 1,272,651 | - | 1,272,651 | ||||||||||||

| Labour and wages | 606,642 | 311,685 | 46,248 | 964,575 | ||||||||||||

| Camp costs | 742,870 | 9,813 | - | 752,683 | ||||||||||||

| Community relations | 146,489 | - | - | 146,489 | ||||||||||||

| Geological and geophysical | 116,860 | 27,742 | - | 144,602 | ||||||||||||

| Geochemistry and assays | 125,201 | 6,477 | - | 131,678 | ||||||||||||

| Claim holding costs and advance royalties | 47,223 | 38,988 | 34,202 | 120,413 | ||||||||||||

| Travel | 99,110 | 18,492 | 1,724 | 119,326 | ||||||||||||

| Health, safety and environmental | 58,523 | 32,336 | 21,661 | 112,520 | ||||||||||||

| Net extension of claim payments | 74,125 | - | - | 74,125 | ||||||||||||

| Other | 231,905 | 53,844 | 22,799 | 308,548 | ||||||||||||

| Cash expenditures | $ | 4,801,634 | $ | 1,784,444 | $ | 126,634 | $ | 6,712,712 | ||||||||

| Share-based compensation | 304,431 | 154,956 | - | 459,387 | ||||||||||||

| Total expenditures | $ | 5,106,065 | $ | 1,939,400 | $ | 126,634 | $ | 7,172,099 | ||||||||

5

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

Canada

Expenditures on the Company’s properties in Canada were primarily focused on the following projects in the Athabasca Basin (Figure 1) during the year ended December 31, 2025:

| Larocque East | Dorado | Other | Total | |||||||||||||

| Drilling | $ | 1,950,885 | $ | 601,801 | $ | - | $ | 2,552,686 | ||||||||

| Camp costs | 441,211 | 217,064 | 84,595 | 742,870 | ||||||||||||

| Labour and wages | 378,668 | 113,925 | 114,049 | 606,642 | ||||||||||||

| Community Relations | 97,191 | 26,303 | 22,995 | 146,489 | ||||||||||||

| Geochemistry and assays | 112,450 | - | 12,751 | 125,201 | ||||||||||||

| Geological and geophysical | 9,153 | 1,750 | 105,957 | 116,860 | ||||||||||||

| Travel | 51,095 | 46,925 | 1,090 | 99,110 | ||||||||||||

| Net extension of claim payments | - | - | 74,125 | 74,125 | ||||||||||||

| Health, safety and environmental | 50,118 | 86 | 8,319 | 58,523 | ||||||||||||

| Claim holding costs | - | - | 47,223 | 47,223 | ||||||||||||

| Other | 34,572 | 158,767 | 38,566 | 231,905 | ||||||||||||

| Cash expenditures | $ | 3,125,343 | $ | 1,166,621 | $ | 509,670 | $ | 4,801,634 | ||||||||

| Share-based compensation | 192,587 | - | 111,844 | 304,431 | ||||||||||||

| Total expenditures | $ | 3,317,930 | $ | 1,166,621 | $ | 621,514 | $ | 5,106,065 | ||||||||

Figure 1 – Location of the Company’s exploration projects in the eastern Athabasca Basin, highlighting projects on which work is planned in 2026

6

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

Larocque East Project

Winter 2026 – Diamond Drilling

The winter 2026 drilling program focused on testing resource expansion targets at the Hurricane Deposit and testing greenfield targets up to three kilometres east along the Larocque Trend. The Company initially planned for 13 diamond drill holes totalling 5,200 metres and successfully expanded the program to complete 17 diamond drill holes totaling 6,804 metres.

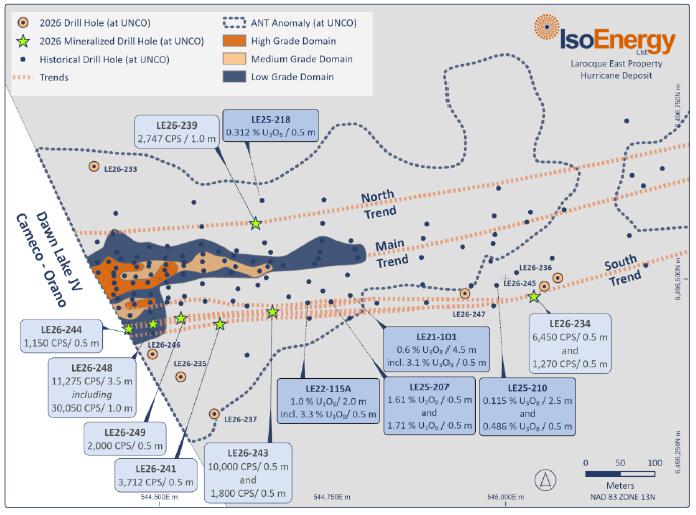

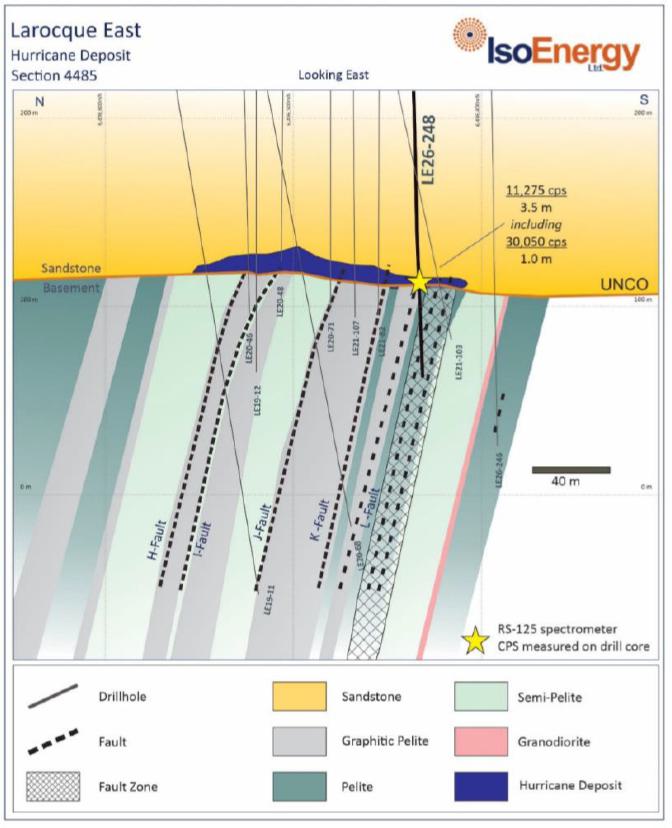

The winter 2026 drilling program focused on resource expansion targets along the North and South Trends (Figure 2). Uranium mineralization was intersected on both trends, which built upon intersections along these two trends from the 2025 exploration programs. Strongly elevated radioactivity was intersected in multiple holes along the South Trend in winter 2026, which emphasizes the growing scale and prospectivity of this trend. This was highlighted by drill hole LE26-248 which returned an average RS-125 spectrometer reading on drill core of 30,050 counts per second (“cps”) over 1.0 metres within a broader zone of 11,275 cps over 3.5 meters, in the newly interpreted L Fault Zone within the South Trend (Figure 3).

The full suite of geochemical assays and structural interpretations of the winter 2026 drill program, once received, will be used to fully inform drill targets and exploration targets for the summer 2026 drill and exploration programs at Larocque East.

See the Company’s press releases dated January 20, 2026 entitled “IsoEnergy Commences 2026 Winter Drilling Program at the Larocque East Project, Athabasca Basin” and April 7, 2026 entitled “IsoEnergy Winter Drilling Intersects Radioactivity in Multiple Holes, Including 30,050 cps over 1.0 Metre, in a Newly Reinterpreted Fault Zone on the South Trend of the Hurricane Deposit” for additional information regarding the plans and results for the winter 2026 exploration program.

Figure 2 – 2026 winter drill holes in the Hurricane Deposit area. Mineralization highlights are U3O8 for selected pre-2026 drill holes and cps measured on drill core with an RS-125 handheld spectrometer for 2026 drill holes.

7

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

Figure 3 – Hurricane deposit cross section 4485E showing location of strongly elevated radioactivity intersected at the unconformity in 2026 drill hole LE26-248 along the newly reinterpreted L Fault Zone with the Hurricane South Trend. The cross section is drawn looking east and depicts geology from approximately 100 metres above the unconformity to approximately 150 metres below the unconformity.

Dorado Project (Purepoint Joint Venture)

Winter 2026 – Drilling

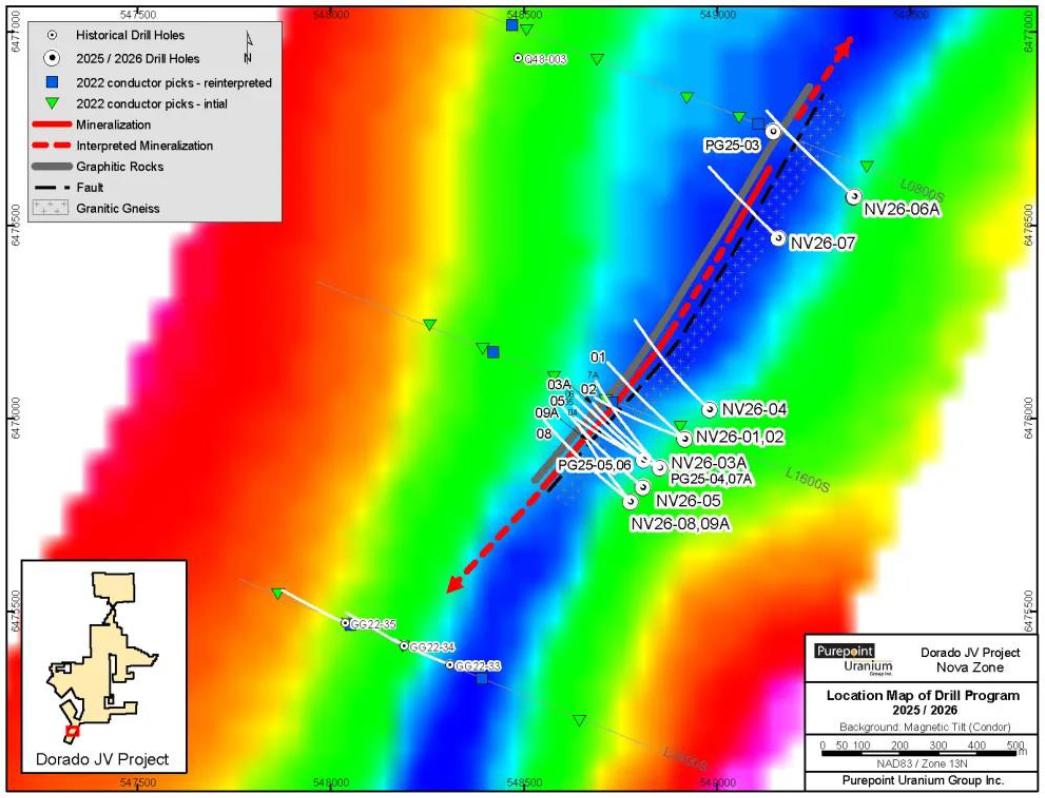

The winter 2026 drilling program at the Dorado Project, operated by Purepoint Uranium, was completed with nine holes totaling 5,210 metres. The winter 2026 drilling program focused on expanding the high-grade Nova Discovery (Figure 4) and the holes drilled successfully expanded uranium mineralization at the Nova Discovery and extended the geologic contact for a strike length of one kilometre. This was highlighted by drill holes NV26-05 which had an average of 17,700 cps over 1.8 metres and NV26-03A which had an average of 10,600 cps over 1.7 metres. The winter 2026 drill program resulted in establishing a refined targeting framework for continued expansion.

Drilling is planned at the Dorado Project in late June 2026 and an airborne Mobile MagnetoTellurics (“MobileMT”) survey is planned over the entire Dorado project in the summer of 2026. Once the 2026 exploration programs at Dorado are completed and the full suite of geochemical assays and structural interpretations are received, the results will be used to fully inform future drill targets and exploration targets at the Dorado project.

8

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

Figure 4 – Location Map of Winter 2026 Drill Program at the Nova Discovery in the Dorado Project

Other Canadian projects

The majority of spending at other Canadian projects was for planning 2026 fieldwork and reporting on 2025 fieldwork at the Matoush project in Quebec. The Company also spent $8,276 to stake several claims extensions along the Larocque East, Hawk, and East Rim projects in the Athabasca Basin.

United States

Expenditure on the Company’s properties in the United States during the three months ended March 31, 2026 was primarily at the Tony M Mine in Utah.

Tony M Mine

The Company completed a bulk sample program, which involved the extraction of approximately 2,100 wet tons of mineralized material. The bulk sample program was executed by the Company using contract mining services provided by GenX Mining Contractors, LLC. The results of the bulk sample program, once fully evaluated, are intended to be inputs in other studies planned for 2026. See the Company’s press release dated April 23, 2026 entitled “IsoEnergy Continues Systematic Drill Testing at Flatiron, Targeting Growth Near Tony M Mine, Utah and Provides Bulk Sample Update” and “Outlook” below for additional information regarding an update of the bulk sample program and the Company’s planned 2026 work program at the Tony M Mine, respectively.

9

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

Claim Staking and Claim Maintenance

The Company incurred $38,988 in expenditure on annual state lease fees, advance royalties, other short-term lease payments, and land management fees related to the Company’s properties in Utah during the three months ended March 31, 2026.

Year ended December 31, 2025

During the year ended December 31, 2025, the Company incurred $24,392,910 of exploration and evaluation spending on its exploration properties globally, as set out below. Most of the expenditures were at the Company’s Larocque East Project in the Athabasca Basin.

Exploration and evaluation spending

| Canada | United States | Australia | Total | |||||||||||||

| Drilling | $ | 7,821,156 | $ | 397,746 | $ | - | $ | 8,218,902 | ||||||||

| Geological and geophysical | 3,330,111 | 134,975 | 283,024 | 3,748,110 | ||||||||||||

| Labour and wages | 1,913,377 | 1,311,461 | 8,871 | 3,233,709 | ||||||||||||

| Camp costs | 2,180,807 | 41,733 | 69,269 | 2,291,809 | ||||||||||||

| Studies and mine site management | 124,041 | 1,525,816 | - | 1,649,857 | ||||||||||||

| Claim holding costs and advance royalties | 73,058 | 765,577 | 228,458 | 1,067,093 | ||||||||||||

| Travel | 385,270 | 101,682 | 64,016 | 550,968 | ||||||||||||

| Community relations | 541,625 | - | - | 541,625 | ||||||||||||

| Geochemistry and assays | 415,649 | 25,929 | 23,744 | 465,322 | ||||||||||||

| Health and safety and environmental | 289,535 | 11,533 | 66,696 | 367,764 | ||||||||||||

| Net extension of claim refunds | (71,408 | ) | - | - | (71,408 | ) | ||||||||||

| Other | 569,380 | 359,155 | 20,031 | 948,566 | ||||||||||||

| Cash expenditures | $ | 17,572,601 | $ | 4,675,607 | $ | 764,109 | $ | 23,012,317 | ||||||||

| Share-based compensation | 893,360 | 476,215 | 11,018 | 1,380,593 | ||||||||||||

| Total expenditures | $ | 18,465,961 | $ | 5,151,822 | $ | 775,127 | $ | 24,392,910 | ||||||||

10

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

Expenditures on the Company’s properties in the Athabasca Basin (Figure 1) and Quebec were primarily focused on the following projects during the year ended December 31, 2025:

| Larocque East | Hawk | Purepoint JV | East Rim | Other | Total | |||||||||||||||||||

| Drilling | $ | 4,725,149 | $ | 1,809,965 | $ | 1,286,042 | $ | - | $ | - | $ | 7,821,156 | ||||||||||||

| Geological and geophysical | 122,066 | 911,135 | 62,584 | 799,979 | 1,434,347 | 3,330,111 | ||||||||||||||||||

| Camp costs | 1,170,260 | 606,487 | 255,907 | - | 148,153 | 2,180,807 | ||||||||||||||||||

| Labour and wages | 1,014,640 | 319,034 | 247,224 | 75,689 | 256,790 | 1,913,377 | ||||||||||||||||||

| Community Relations | 279,082 | 138,051 | 67,506 | 20,592 | 36,394 | 541,625 | ||||||||||||||||||

| Geochemistry and assays | 257,665 | 39,744 | 75,515 | - | 42,725 | 415,649 | ||||||||||||||||||

| Travel | 224,865 | 16,286 | 34,281 | - | 109,838 | 385,270 | ||||||||||||||||||

| Health and safety and environmental | 274,047 | 8,074 | 2,903 | 1,208 | 3,303 | 289,535 | ||||||||||||||||||

| Studies | - | - | - | - | 124,041 | 124,041 | ||||||||||||||||||

| Claim holding costs | - | - | - | - | 73,058 | 73,058 | ||||||||||||||||||

| Net extension of claim refunds | - | - | - | - | (71,408 | ) | (71,408 | ) | ||||||||||||||||

| Other | 68,456 | 29,710 | 196,595 | 1,981 | 272,638 | 569,380 | ||||||||||||||||||

| Cash expenditures | $ | 8,136,230 | $ | 3,878,486 | $ | 2,228,557 | $ | 899,449 | $ | 2,429,879 | $ | 17,572,601 | ||||||||||||

| Share-based compensation | 432,835 | 216,281 | 120,406 | 50,101 | 73,737 | 893,360 | ||||||||||||||||||

| Total expenditures | $ | 8,569,065 | $ | 4,094,767 | $ | 2,348,963 | $ | 949,550 | $ | 2,503,616 | $ | 18,465,961 | ||||||||||||

Expenditure on the Company’s properties in the United States was as follows during the year ended December 31, 2025:

| Tony M | Henry Mountains | Coles Hill | Other | Total | ||||||||||||||||

| Studies and mine site management | $ | 805,029 | $ | - | $ | 720,787 | $ | - | $ | 1,525,816 | ||||||||||

| Labour and wages | 834,536 | 419,183 | 35,283 | 22,459 | 1,311,461 | |||||||||||||||

| Claim holding costs and advance royalties | 464,482 | 80,920 | - | 220,175 | 765,577 | |||||||||||||||

| Drilling | - | 397,746 | - | - | 397,746 | |||||||||||||||

| Geological and geophysical | - | 13,723 | - | 121,252 | 134,975 | |||||||||||||||

| Travel | 10,887 | 51,462 | 12,117 | 27,216 | 101,682 | |||||||||||||||

| Camp costs | - | 41,244 | - | 489 | 41,733 | |||||||||||||||

| Geochemistry and assays | - | 25,929 | - | - | 25,929 | |||||||||||||||

| Health, safety and environmental | 4,347 | - | - | 7,186 | 11,533 | |||||||||||||||

| Other | 69,503 | - | - | 289,652 | 359,155 | |||||||||||||||

| Cash expenditures | $ | 2,188,784 | $ | 1,030,207 | $ | 768,187 | $ | 688,429 | $ | 4,675,607 | ||||||||||

| Share-based compensation | 257,179 | 160,279 | - | 58,757 | 476,215 | |||||||||||||||

| Total expenditures | $ | 2,445,963 | $ | 1,190,486 | $ | 768,187 | $ | 747,186 | $ | 5,151,822 | ||||||||||

11

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

OUTLOOK

The Company intends to actively explore all its exploration projects as and when resources permit (other than at the Bulyea River project as discussed below in “Summary of Quarterly Results”). The nature and extent of further exploration on any of the Company’s properties, however, will depend on the results of completed and ongoing exploration activities, an assessment of the Company’s recently acquired properties and the Company’s financial resources.

Activities in Canada for 2026 include completing analysis of the results of the 2026 winter exploration program and preparing for drilling in the summer of 2026 at Larocque East, with the continued focus of testing resource expansion potential near the Hurricane Deposit and evaluating greenfield targets along the Larocque Trend, as further outlined in “Discussion of Operations” above. Other planned activities in Canada for 2026 include completing geophysical surveys and interpretation at the Evergreen, East Rim, Ranger, Trident, and Hawk projects in the Athabasca Basin, as well as completing geological fieldwork at the Matoush project in Quebec. Remaining activities at the Dorado Project, operated by Purepoint Uranium, include completing a drilling program and a MobileMT survey during the summer of 2026. Once the evaluation of exploration results from the 2026 exploration programs are completed, this information will be used to propose future detailed exploration work.

The Company’s planned work program at the Tony M Mine in 2026 includes completing the analysis of the results of the bulk sample program. The Company intends to commence a Preliminary Economic Assessment (“PEA”) in 2026, incorporating the results from the bulk sample program. The PEA will provide an incentive uranium price for production and a basis for advancing detailed mine planning, finalizing potential restart sequencing, and assessing possible timing of a potential production decision. Activities in the US in 2026 also include completing the 2026 drilling program at the Flatiron Project and the 2026 exploration programs at the Daneros, and Sage Plain projects, in Utah. The target area of the planned drilling at the Flatiron Project is intended to follow up on the three drill holes completed in 2025.

The Company intends to complete internal technical studies on several non-material properties in 2026.

SELECTED FINANCIAL INFORMATION

Management is responsible for the Interim Financial Statements referred to in this MD&A. The Audit Committee of the Board of Directors (the “Board”) has been delegated the responsibility to review the Interim Financial Statements and MD&A and make recommendations to the Board. The Board is responsible for final approval of the Interim Financial Statements and MD&A.

The Interim Financial Statements have been prepared in accordance with IAS 34, Interim Financial Reporting (“IAS 34”) as issued by the IFRS and interpretations of the International Financial Reporting Interpretations Committee (“IFRIC”). The Company’s presentation currency and the functional currency of its Canadian operations is Canadian dollars; the functional currency of its Australian operations is the Australian dollar; and the functional currency of its United States operations is the US dollar.

The Company’s Interim Financial Statements have been prepared using IFRS applicable to a going concern, which assumes that the Company will be able to realize its assets and discharge its liabilities in the normal course of business for the foreseeable future. The ability of the Company to continue as a going concern is dependent on its ability to obtain financing and achieve future profitable operations.

12

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

Financial Position

The following financial data is derived from and should be read in conjunction with the Interim Financial Statements and the Annual Financial Statements. As an exploration stage company, IsoEnergy does not have revenues.

| March 31, 2026 | December 31, 2025 | December 31, 2024 | ||||||||||

| Exploration and evaluation assets | $ | 289,997,926 | $ | 279,091,819 | $ | 262,291,098 | ||||||

| Total assets | 494,317,459 | 416,958,281 | 340,835,023 | |||||||||

| Total current liabilities | 10,853,370 | 12,399,489 | 35,103,977 | |||||||||

| Total non-current liabilities | 3,113,351 | 3,132,706 | 2,567,887 | |||||||||

| Adjusted working capital(1) | 183,253,876 | 116,743,618 | 56,116,942 | |||||||||

| Cash dividends declared per share | Nil | Nil | Nil | |||||||||

| (1) | Adjusted working capital is a non-IFRS financial measure, as discussed below, and is defined as current assets less current liabilities, excluding flow-though share premium liabilities and convertible debenture liabilities. |

In the three months ended March 31, 2026, the Company capitalized $7,172,099 of exploration and evaluation costs, before movements in foreign exchange rates, as further described in “Discussion of Operations” above. Total assets increased primarily due to $57,501,150 raised in the 2026 Financing and $25,000,005 raised in the January 2026 Concurrent Private Placement, with associated share issuance costs of $4,022,591. Total assets also increased from the receipt of $4,498,560 of common shares of Jaguar Uranium Corp. (“Jaguar Uranium”) as the remaining consideration pursuant to the sale of the Company’s Argentina assets that was completed in July 2024. Increases to total assets were partially offset by a decrease in the fair value of marketable securities of $9,857,333 during the three months ended March 31, 2026.

Current liabilities as at March 31, 2026, include a flow-through share premium liability of $2,909,206 relating to the February 2025 Financing (as defined herein). Accounts payable and accrued liabilities decreased by $338,873 during the three months ended March 31, 2026 mostly due to the completion of the 2026 winter exploration program at Larocque East. The fair value of the US$4 million in principle of unsecured convertible debentures issued on December 6, 2022 (the “2022 Debentures”) increased by $574,096 during the three months ended March 31, 2026. Adjusted working capital increased during the three months ended March 31, 2026 mainly due to the 2026 Financing and 2026 Concurrent Private Placement.

Proposed Transaction

On October 12, 2025, the Company and Toro Energy Limited (“Toro Energy”) entered into a scheme implementation deed (the “SID”) pursuant to which IsoEnergy, through one of its wholly owned subsidiaries, has agreed to acquire all of the issued and outstanding ordinary shares of Toro Energy (the “Toro Energy Shares”) by way of a scheme of arrangement under Australia’s Corporations Act 2001 (Cth) (the “Toro Scheme”). Toro Energy is an Australian Securities Exchange (“ASX”) listed company that owns 100% of the Wiluna uranium project in Western Australia, Australia, as well as other exploration stage uranium properties in Australia.

Under the terms of the SID, shareholders of Toro Energy (the “Toro Energy Shareholders”) will receive 0.036 of a common share of IsoEnergy for each Toro Energy Share. Completion of the Toro Scheme is subject to various conditions, including but not limited to: approval of Toro Energy Shareholders; court approval; applicable regulatory approvals, including approval of the ASX, TSX, and NYSE American; and an independent expert concluding and continuing to conclude that the Toro Scheme is in the best interests of Toro Energy Shareholders. Following the completion of the Toro Scheme, the IsoEnergy common shares will continue to trade on the TSX and NYSE American and the Toro Energy Shares will be delisted from the ASX. The Toro Scheme is expected to close in the first half of 2026.

13

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

Subsequent to March 31, 2026, IsoEnergy agreed to provide an unsecured bridge loan of up to AUD$2,000,000 million to Toro Energy (the “Loan Agreement”), with an interest rate of 10% per annum up to and including June 30, 2026, increasing to 15% per annum thereafter. The Loan Agreement has a maturity date of December 31, 2026, or earlier under certain circumstances. The principal amount and accrued interest on the Loan Agreement can be prepaid by Toro Energy, in its sole discretion, prior to the maturity date. Drawdowns pursuant to the Loan Agreement will be utilized for working capital and to satisfy other obligations of Toro Energy through to the closing of the SID. On May 6, 2026, Toro Energy drew down AUD$750,000 under the Loan Agreement.

Results of Operations

The following financial data is derived from and should be read in conjunction with the Interim Financial Statements.

For the three months ended March 31 | ||||||||

| 2026 | 2025 | |||||||

| General and administrative costs | ||||||||

| Share-based compensation | $ | 2,624,482 | $ | 1,945,839 | ||||

| Administrative salaries, contractor and directors’ fees | 858,797 | 795,314 | ||||||

| Investor relations | 368,255 | 220,956 | ||||||

| Office and administrative | 262,276 | 244,000 | ||||||

| Professional and consultant fees | 717,903 | 1,060,811 | ||||||

| Travel | 180,903 | 176,025 | ||||||

| Public company costs | 567,778 | 145,726 | ||||||

| Total general and administrative costs | $ | (5,580,394 | ) | $ | (4,588,671 | ) | ||

| Interest income | 789,414 | 310,297 | ||||||

| Interest expense | (35,140 | ) | (41,879 | ) | ||||

| Interest on convertible debentures | (137,187 | ) | (262,550 | ) | ||||

| Fair value loss on convertible debentures | (573,612 | ) | (288,582 | ) | ||||

| Gain on disposal of assets | 4,498,560 | 10,369,031 | ||||||

| Foreign exchange gain | 149,395 | 6,919 | ||||||

| Other income | 19,240 | 431,921 | ||||||

| (Loss) income from operations | $ | (869,724 | ) | $ | 5,936,486 | |||

| Deferred income tax expense | (633,051 | ) | (830,871 | ) | ||||

| (Loss) income for the period | $ | (1,502,775 | ) | $ | 5,105,615 | |||

| (Loss) income per share – basic | $ | (0.03 | ) | $ | 0.11 | |||

| (Loss) income per share – diluted | $ | (0.03 | ) | $ | 0.10 | |||

Three months ended March 31, 2026

During the three months ended March 31, 2026, the Company recorded a net loss of $1,502,775, compared to net income of $5,105,615 in the three months ended March 31, 2025. The main driver of the difference between the two periods was a gain on disposal of $4,498,560 recorded in the current period from the receipt of the remaining consideration from the sale of the Argentina reporting segment, which was accounted for as a contingent asset until it was received, compared to $10,369,031 recorded in the prior period relating to the sale of the Mountain Lake property. The decrease from net income in the prior period to a net loss in the current period was also due to an increase in general and administrative costs of $991,723, as further described below. Other factors causing the difference between the two periods are further described below.

14

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

General and administrative costs

Share-based compensation was $2,624,482 in the three months ended March 31, 2026, compared to $1,945,839 in the three months ended March 31, 2025. The share-based compensation expense is a non-cash charge based on the Black-Scholes value of stock options, calculated using the graded vesting method. Stock options granted to directors, consultants and employees typically vest in three tranches – 1/3 immediately, 1/3 on the first anniversary of the grant date, and the remaining 1/3 on the second anniversary of the grant date, with the corresponding share-based compensation expense being recognized over this period. The increase in the current period was primarily due to a higher number of stock options granted during the three months ended March 31, 2026 compared to the prior period.

Administrative salaries, contractor and directors’ fees increased slightly from the prior period primarily due to the addition of the Vice President, Strategy and Commercial in the three months ended December 31, 2025.

Investor relations expenses relate primarily to costs incurred in communicating with existing and potential shareholders, conferences and marketing. The increase in the current period is primarily due to additional marketing activities in the United States, Europe, and Asia.

Office and administrative expenses primarily consist of office operating costs and other general administrative costs. Office and administrative expenses were similar in both periods.

Professional fees were lower than the prior period mainly due to legal and advisory fees related to the terminated transaction with Anfield Energy Inc. during the three months ended March 31, 2025.

Travel expenses primarily relate to travel and accommodation costs for conferences, business development activities, public relations activities, and general corporate purposes. Travel costs were similar in both periods.

Public company costs consist primarily of costs associated with the Company’s continuous disclosure obligations, listing fees, directors and officers insurance, transfer agent costs, press releases and other shareholder communications. The increase in public company costs is primarily due to the additional costs of sustaining a listing on the NYSE American, including the amortization of the premium for additional Director and Officer insurance.

Other items

Interest expense on the Debentures (as defined herein) was $137,187 in the three months ended March 31, 2026, which decreased from $262,550 in the three months ended March 31, 2025. The 2022 Debentures bear interest of 10% per annum and is payable, with a combination of cash and common shares of the Company, on June 30 and December 31. The decrease is primarily due to the US$6 million principal of unsecured convertible debentures issued on August 18, 2020 (the “2020 Debentures”) being fully converted by August 1, 2025.

The fair value of the 2022 Debentures on March 31, 2026 was $6,004,955 compared to $5,430,859 on December 31, 2025. The increase in fair value includes $573,612 recorded in the statement of income and a fair value increase attributable to the change in credit risk of $484 included in other comprehensive income (loss). The 2022 Debentures are classified as measured at fair value through profit and loss. In accordance with IFRS 9 – Financial Instruments, the part of a fair value change due to an entity’s own credit risk is presented in other comprehensive income (loss). As of March 31, 2026, the time to maturity of the 2022 Debentures was 1.7 years.

Foreign exchange gain was $149,395 in the three months ended March 31, 2026, compared to a gain of $6,919 in the three months ended March 31, 2025, and mainly relates to exchange movements on an increased cash balance denominated in United States dollars held by the Company.

15

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

Other income was $19,239 in the three months ended March 31, 2026, compared to $431,921 in the three months ended March 31, 2025. This primarily relates to timber sales earned from the Company’s operations in the US in the prior period, of which no such sales occurred in the current period.

The Company records a deferred tax recovery or expense which is comprised of a recovery on losses or expense on gains recognized in the period and, when applicable, the release of flow-through share premium liability which is offset by the renunciation of flow-through share expenditures to shareholders. In the three months ended March 31, 2026, this resulted in an expense of $633,051, compared to an expense of $830,871 in the three months ended March 31, 2026. The decrease in expense is mostly due to a lower gain on sale compared to the prior period.

SUMMARY OF QUARTERLY RESULTS

The following information is derived from the Company’s Interim Financial Statements and Annual Financial Statements prepared in accordance with IFRS. The information below should be read in conjunction with the Company’s interim and annual financial statements for each of the past seven quarters.

| Mar. 31, 2026 | Dec. 31, 2025 | Sep. 30, 2025 | Jun. 30, 2025 | |||||||||||||

| Revenue | Nil | Nil | Nil | Nil | ||||||||||||

| Net (loss) income | $ | (1,502,775 | ) | $ | (4,632,620 | ) | $ | 287,876 | $ | (1,887,270 | ) | |||||

| Net (loss) income per share: | ||||||||||||||||

| Basic | $ | (0.03 | ) | $ | (0.08 | ) | $ | 0.01 | $ | (0.04 | ) | |||||

| Diluted | $ | (0.03 | ) | $ | (0.08 | ) | $ | (0.01 | ) | $ | (0.04 | ) | ||||

| Mar. 31, 2025 | Dec. 31, 2024 | Sep. 30, 2024 | Jun. 30, 2024 | |||||||||||||

| Revenue | Nil | Nil | Nil | Nil | ||||||||||||

| Net income (loss) | $ | 5,105,615 | $ | (35,505,105 | ) | $ | 4,159,285 | $ | (6,059,293 | ) | ||||||

| Net income (loss) per share: (1) | ||||||||||||||||

| Basic | $ | 0.11 | $ | (0.79 | ) | $ | 0.09 | $ | (0.13 | ) | ||||||

| Diluted | $ | 0.10 | $ | (0.89 | ) | $ | 0.00 | $ | (0.13 | ) | ||||||

| Loss from discontinued operations (2) | Nil | Nil | $ | (1,859 | ) | $ | (55,133 | ) | ||||||||

| Loss from discontinued operations per share – basic and diluted (1)(2) | Nil | Nil | $ | (0.00 | ) | $ | (0.00 | ) | ||||||||

| (1) | Net income (loss) per share amounts in the three latter quarters presented are retroactively restated on a post-Share Consolidation basis. Refer to the discussion on the Share Consolidation above in “About IsoEnergy”. |

| (2) | Loss from discontinued operations relates to the Argentina reporting segment which was disposed of during the three months ended September 30, 2024. |

IsoEnergy does not derive any revenue from its operations. Its primary focus is the acquisition, exploration and development of mineral properties. As a result, the income (loss) per period has fluctuated depending on the Company’s activity level and periodic variances in certain items. Quarterly periods are therefore not comparable. As part of the Company’s strategy to evaluate additional Merger and Acquisition (“M&A”) opportunities throughout the life cycle of mineral properties, the Company may incur gains or losses related to such transactions or incur expenses for M&A opportunities that do not materialize. In the three months ended March 31, 2026, a gain of $4,498,560 was recorded on the receipt of common shares of Jaguar Uranium as the remaining consideration pursuant to the sale of the Argentina reporting segment; in the three months December 31, 2025, a gain of $2,250,000 was recorded on the receipt of common shares of Future Fuels as the remaining consideration pursuant to the sale of the Mountain Lake property; in the three months ended June 30, 2025, a gain of $820,394 was recorded on the sale of certain of the Company’s royalty assets; in the three months ended March 31, 2025, a $10,369,031 gain was recorded on the sale of the Mountain Lake property; in the three months ended December 31, 2024, a loss of $25,616,241 was recorded from the contribution of exploration and evaluation assets to the Purepoint Joint Venture; and in the three months ended September 30, 2024, a $5,300,611 gain was recorded on the disposal of its Argentina assets.

16

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

The Company also assesses for indicators of impairment on its property and equipment and exploration and evaluation assets quarterly, as required by the relevant IFRS. If such indicators are identified, an analysis to determine its recoverable value is performed and if such amount is lower than the carrying value, a loss is recognized for the difference. In the three months ended December 31, 2025, the Company expected to not currently continue exploration work at its Bulyea River property and recorded a write-down of $935,814. In the three months ended December 31, 2024, the Company identified indicators of impairment on certain exploration and evaluation assets located in the Athabasca Basin primarily as a result of the loss on the formation of the Purepoint Joint Venture and recorded a write-down of $14,342,736.

In the third quarter of 2020, the Company issued the 2020 Debentures and in the fourth quarter of 2022 issued the 2022 Debentures, both of which were and are, respectively, accounted for as measured at fair value through profit and loss, which has resulted in a gain on the revaluation of the Debentures in the three months ended September 30, 2024, three months ended December 31, 2024, three months ended June 30, 2025, three months ended September 30, 2025, three months ended December 31, 2025, and losses in every other period.

LIQUIDITY AND CAPITAL RESOURCES

IsoEnergy has no revenue-producing operations, earns only minimal interest income on cash, and is expected to have recurring operating losses. As of March 31, 2026, the Company had an accumulated deficit of $105,174,420.

During the three months ended March 31, 2026, the Company utilized cash on hand to invest $6,427,655 (net of changes in accounts payable) in exploration and evaluation assets, $2,634,898 for expenditure on its corporate and business development activities, including movements in working capital, and spent $3,931,793 (net of proceeds from disposals) to invest in common shares and/or warrants of marketable securities.

During the three months ended March 31, 2026, the Company received $78,478,564 in net proceeds from the 2026 Financing and the 2026 Concurrent Private Placement.

As of the date of this MD&A, the Company has approximately $128.5 million in cash, $53.1 million in marketable securities and $182.5 million in adjusted working capital.

The Company has fully funded its global exploration and pre-development activities, as well as any corporate initiatives and general working capital, up to the end of December 31, 2026. This includes costs associated with completing the Toro Scheme and funding future approved expenditures on the properties to be acquired from Toro Energy. The ability of the Company to continue as a going concern is dependent on its ability to obtain financing and achieve future profitable operations.

Should the Company require additional financing under its Prospectus or otherwise, Management will determine whether to accept any offer to finance, weighing such factors as the financing terms, the results of exploration programs and technical studies, the Company’s share price at the time and current market conditions, among others.

Circumstances that could impair the Company’s ability to raise additional funds include general economic conditions, the price of uranium and certain other factors set forth under “Risk Factors” below and above under “Industry and Economic Factors that May Affect the Business”. A failure to obtain financing as and when required, could require the Company to reduce its exploration and corporate activity levels.

17

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

Use of Proceeds

On February 9, 2024, the Company completed a brokered “bought-deal” private placement for gross proceeds of $23.0 million (the “February 2024 Private Placement”). The proceeds from the February 2024 Private Placement were required to be and were spent on eligible “Canadian exploration expenses” that qualify as “flow-through critical mineral mining expenditures” by December 31, 2025.

On February 28, 2025, the Company completed a “bought deal” financing whereby the Company issued 1,333,825 “flow-through” common shares(1) at a price of $15.00 per share, for gross proceeds of approximately $20.0 million (the “February 2025 Financing”). Concurrent with the February 2025 Financing, the Company completed a non-brokered private placement whereby the Company issued 625,000 common shares(1) to NexGen for gross proceeds of approximately $6.3 million (the “2025 Concurrent Private Placement”). On June 24, 2025, the Company closed a “bought deal” financing whereby the Company issued 5,121,500 common shares at a price of $10.00 per share for gross proceeds of approximately $51.2 million (the “June 2025 Financing”). The proceeds from the February 2025 Financing are required to be spent on eligible “Canadian exploration expenses” that qualify as “flow-through critical mineral mining expenditures” (in each case as defined in the Income Tax Act (Canada) (the “Tax Act”)) by December 31, 2026 and the Company was required to and did renounce the full amount of the gross proceeds of the financing to the subscribers of the flow-through shares no later than December 31, 2025. The proceeds of 2025 Concurrent Private Placement were to be used for other non-qualifying expenditures on the exploration of the Company’s Canadian properties, costs associated with the listing on the NYSE American, and for working capital and general corporate purposes. The proceeds of the June 2025 Financing are expected to be used to fund continued development and further exploration of the Company’s mineral properties, and for general corporate purposes.

On January 27, 2026, the Company received total gross proceeds of $82.5 million from the January 2026 Financing and 2026 Concurrent Private Placement. The proceeds of these two financings are expected to be used to fund continued development and further exploration of the Company’s mineral properties, corporate development activities and investments, and for general corporate purposes.

(1) The common shares issued are retroactively restated on a post-consolidation basis. Refer to the discussion on the Share Consolidation, as described above in “About IsoEnergy”.

18

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

The gross proceeds received from these financings have been used as follows as of March 31, 2026:

| Proceeds | Anticipated use of proceeds | Actual use of proceeds | Remaining in treasury | |||||||||

| February 2024 Private Placement: | ||||||||||||

| Canadian exploration expenses | $ | 23,000,000 | $ | 23,000,000 | $ | - | ||||||

| February 2025 Financing: | ||||||||||||

| Canadian exploration expenses | 20,007,375 | 12,734,361 | 7,273,014 | |||||||||

| 2025 Concurrent Private Placement: | ||||||||||||

| Other exploration expenses | 750,000 | 750,000 | - | |||||||||

| NYSE American listing costs | 2,000,000 | 1,601,097 | 398,303 | |||||||||

| Costs associated with the financing | 1,600,000 | 1,600,000 | - | |||||||||

| General corporate purposes | 1,900,000 | 596,152 | 1,303,848 | |||||||||

| June 2025 Financing: | ||||||||||||

| Development and studies (US) | 20,600,000 | 4,004,008 | 16,595,992 | |||||||||

| Exploration (US, Australia) | 12,100,000 | 1,045,415 | 11,054,585 | |||||||||

| Land acquisitions, staking and holding | 5,600,000 | 1,088,877 | 4,511,123 | |||||||||

| Equity investments | 2,500,000 | 2,500,000 | - | |||||||||

| Acquisition- related expenditures | 2,500,000 | 828,735 | 1,671,265 | |||||||||

| General corporate purposes | 5,615,000 | - | 5,615,000 | |||||||||

| Costs associated with the financing | 2,300,000 | 2,300,000 | - | |||||||||

| January 2026 Financing and Concurrent Private Placement: | ||||||||||||

| Development and studies (US) | 48,100,000 | - | 48,100,000 | |||||||||

| Exploration (US) | 6,800,000 | - | 6,800,000 | |||||||||

| Land acquisitions, staking and holding | 6,500,000 | - | 6,500,000 | |||||||||

| Corporate development and investments | 10,000,000 | 3,852,217 | 6,147,783 | |||||||||

| Corporate and working capital | 7,606,097 | - | 7,606,097 | |||||||||

| Costs associated with the offering | 3,495,058 | 3,495,058 | - | |||||||||

| $ | 182,973,530 | $ | 59,395,920 | $ | 123,577,610 | |||||||

| Remaining in treasury from previous financings | 6,960,194 | |||||||||||

| Remaining in treasury | $ | 130,537,804 | ||||||||||

The balance remaining in treasury are intended to be applied towards the intended uses of the subsequent financings described above. The Company’s properties are in good standing with applicable governmental authorities. Other than the contractually agreed upon exploration budget in 2026 for the Purepoint Joint Venture, the Company does not have any contractually imposed expenditure requirements.

The Company has not paid any dividends and management does not expect that this will change in the near future. Working capital is mainly held in cash, cash deposits available on short-term demand, and marketable securities, all of which are highly liquid.

COMMITMENTS AND CONTINGENCIES

The Company’s significant undiscounted commitments at March 31, 2026 are as follows. The 2022 Debentures are classified as a current liability, however the counterparty conversion option allows the principal to be converted to common shares.

| Less than 1 year | 1 to 3 years | More than 4 years | Total | |||||||||||||

| Accounts payable and accrued liabilities | $ | 1,770,320 | $ | - | $ | - | $ | 1,770,320 | ||||||||

| 2022 Debentures | 6,004,955 | - | - | 6,004,955 | ||||||||||||

| Flow-through share premium liabilities | 2,909,206 | - | - | 2,909,206 | ||||||||||||

| Purepoint Joint Venture advances | 2,000,000 | - | - | 2,000,000 | ||||||||||||

| Lease liabilities | 198,753 | 210,280 | 42,753 | 451,786 | ||||||||||||

| Asset retirement obligations | - | - | 2,493,605 | 2,493,605 | ||||||||||||

| $ | 12,883,234 | $ | 210,280 | $ | 2,536,358 | $ | 15,629,872 | |||||||||

19

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

The Company expects to utilize cash and cash equivalents on hand to settle the above noted commitments and contingencies, should any of the contingencies materialize.

Flow-through funding commitments

The premium received for a “flow-through share” (as defined in the Tax Act), which is the consideration received for the share in excess of the market price of the share, is recorded as a flow-through share premium liability. This liability is subsequently reduced when the required exploration expenditures are made, on a pro rata basis, and accordingly, a recovery of flow-through premium is then recorded as a reduction in the deferred tax expense to the extent that deferred income tax assets are available.

As of March 31, 2026, the Company is obligated to spend $7,273,014 on eligible exploration expenditures by December 31, 2026 related to the February 2025 Financing.

Contingent payment obligations

The Company has an obligation to make a contingent payment of $500,000 related to the acquisition of the West Newcastle Range, Teddy Mountain and Ardmore East Projects, if either of the following milestones are met by 2030:

| · | a NI 43-101 compliant Mineral Resource estimate for the West Newcastle Range and Teddy Mountain Projects is prepared where the Mineral Resource estimate is greater than or equal to 6.0 million pounds of U₃O₈; or |

| · | with respect to the Ardmore East Project, the Mineral Resources estimate is greater than or equal to 6.0 million pounds of U₃O₈ equivalent. |

Royalties and Environmental Obligations

In addition to applicable federal, provincial/state and municipal severance taxes, duties and advance royalties, the Company’s exploration and evaluation properties are subject to certain royalties, which may or may not be payable in future, depending on whether revenue is derived from the claims or leases to which these royalties are applicable.

The Company’s mining and exploration activities are subject to various laws and regulations governing the protection of the environment. These laws and regulations are continually changing and generally becoming more restrictive. The Company believes its operations are materially in compliance with all applicable laws and regulations. The Company has made, and expects to make in the future, expenditures to comply with such laws and regulations.

Contractual arrangements

The purchase agreement for the Bulyea River property, which closed on June 28, 2024, includes a provision for the return of the Bulyea River property to Critical Path Minerals Corp. (“Critical Path Minerals”), if the Company does not or chooses to not make the following payments to Critical Path Minerals by the following dates:

| · | On or before the 2nd anniversary of the closing date of sale: $300,000 in cash or common shares or a combination thereof, at the election of the Company; and |

| · | On or before the 3rd anniversary of the closing date of sale: $350,000 in cash or common shares or a combination thereof, at the election of the Company. |

The Company also agreed to:

| · | Incur minimum expenditures of $2,000,000 within 36 months of the closing date of sale; and |

20

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

| · | Within 30 days after a published technical report containing a current mineral resource estimate for the Bulyea River property, pay Critical Path Minerals $1,000,000 in cash or common shares or a combination thereof, at the election of the Company |

OUTSTANDING SHARE DATA

The authorized capital of IsoEnergy consists of an unlimited number of common shares. As of the date of this MD&A, there were 60,628,932 common shares, 4,959,016 stock options, and 145,833 RSUs outstanding, each stock option entitling the holder to purchase one common share of IsoEnergy and each RSU representing the right of the holder to receive one common share upon vesting.

During the three months ended March 31, 2026, the Company issued 5,500,077 common shares for gross proceeds of $82,501,155 pursuant to the 2026 Financing and 2026 Private Placement and issued 174,959 common shares on the exercise of stock options for proceeds of $2,159,125. The Company granted 706,375 stock options at an exercise price of $13.78.

The 2022 Debentures issued to QRC bear a 10% coupon rate, and are convertible at $17.32 per share. The Company has US$4 million principal remaining outstanding of the 2022 Debentures which mature on December 6, 2027.

Stock options(1) outstanding as of the date of this MD&A, and the range of exercise prices thereof are set forth below:

| Range of exercise prices | Number of options | Weighted average exercise price | Number of options exercisable | Weighted average exercise price | Weighted average remaining contractual life (years) | ||||||||||||||||

| $9.78 - $10.44 | 964,833 | $ | 9.94 | 475,251 | $ | 10.11 | 3.8 | ||||||||||||||

| $10.45 - $12.64 | 1,343,582 | 12.05 | 991,085 | 11.99 | 2.9 | ||||||||||||||||

| $12.65 - $15.24 | 1,312,234 | 13.78 | 842,318 | 13.77 | 3.2 | ||||||||||||||||

| $15.25 - $16.52 | 1,027,608 | 16.27 | 1,027,608 | 16.27 | 1.6 | ||||||||||||||||

| $16.53 - $20.40 | 310,759 | 19.85 | 310,759 | 19.85 | 0.7 | ||||||||||||||||

| 4,959,016 | $ | 13.46 | 3,647,021 | $ | 14.03 | 2.8 | |||||||||||||||

As of the date of this MD&A, the Company has 145,833 RSUs(1) outstanding at a weighted average grant date fair value of $11.51.

(1) Certain of the stock options, RSUs, and per share amounts included above are presented on a post-Share Consolidation basis. Refer to the discussion on the Share Consolidation above in “About IsoEnergy”.

21

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

OFF-BALANCE SHEET ARRANGEMENTS

The Company had no off-balance sheet arrangements as of March 31, 2026 or as of the date hereof.

NON-IFRS FINANCIAL MEASURES

Working capital and adjusted working capital are non-IFRS financial measures included in this MD&A, as discussed below. We believe that working capital and adjusted working capital, in addition to conventional measures prepared in accordance with IFRS, provide investors with an improved ability to evaluate the underlying financial position of the Company. These non-IFRS financial measures are intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. This financial measure does not have any standardized meaning prescribed under IFRS and therefore may not be comparable to those of other issuers.

Non-IFRS financial measures are defined in National Instrument 52-112 – Non-GAAP and Other Financial Measures Disclosure as a financial measure disclosed that (a) depicts the historical or expected future financial performance, financial position or cash flow of an entity, (b) with respect to its composition, excludes an amount that is included in, or includes an amount that is excluded from, the composition of the most directly comparable financial measure disclosed in the primary financial statements of the entity, (c) is not disclosed in the financial statements of the entity, and (d) is not a ratio, fraction, percentage or similar representation.

The adjusted working capital amount disclosed in this MD&A is considered a non-IFRS financial measure and is defined as current assets less current liabilities, excluding flow-though share premium liabilities and debenture liabilities, as calculated below:

| Current assets | $ | 185,193,085 | ||

| Current liabilities | (10,853,370 | ) | ||

| Working capital | 174,339,715 | |||

| Flow-through share premium liability | 2,909,206 | |||

| Convertible debentures | 6,004,955 | |||

| Adjusted working capital | $ | 183,253,876 |

TRANSACTIONS WITH RELATED PARTIES

NexGen is a related party of the Company due to its ownership in the Company and the overlapping members of the Board of Directors between NexGen and the Company. The Company’s key management personnel and directors are related parties. Premier American Uranium is a related party due to an overlap in key management personnel.

Key management personnel include those persons having authority and responsibility for planning, directing and controlling the activities of the Company as a whole. The Company has determined that key management personnel consists of executive and non-executive members of the Company’s Board of Directors and senior officers.

Remuneration attributed to key management personnel is summarized as follows.

| Three months ended March 31, 2026 | Short term compensation | Share-based compensation | Total | |||||||||

| Expensed to the statement of income and comprehensive (loss) income | $ | 497,280 | $ | 2,171,311 | $ | 2,668,591 | ||||||

| Capitalized to exploration and evaluation assets | 64,687 | 144,291 | 208,978 | |||||||||

| $ | 561,967 | $ | 2,315,602 | $ | 2,877,569 | |||||||

22

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

| Three months ended March 31, 2025 | Short term compensation | Share-based compensation | Total | |||||||||

| Expensed to the statement of income and comprehensive (loss) income | $ | 434,963 | $ | 1,659,994 | $ | 2,094,957 | ||||||

| Capitalized to exploration and evaluation assets | 64,323 | 130,262 | 194,585 | |||||||||

| $ | 499,286 | $ | 1,790,256 | $ | 2,289,542 | |||||||

As of March 31, 2026:

| · | $19,318 (December 31, 2025: $5,908) was included in accounts payable and accrued liabilities owing to directors and officers; and |

| · | $12,945 (December 31, 2025: $nil) was included in accounts receivable owing by related parties. |

During the three months ended March 31, 2026, the Company:

| · | reimbursed NexGen $nil (2025: $5,540) for use of NexGen’s office space; and |

| · | received $32,420 (2025: $nil) from Premier American Uranium primarily as reimbursement for salaries. |

Concurrent with the flow through financing on February 28, 2025, NexGen subscribed to 625,000 common shares(1) of the Company in a private placement. NexGen participated in the bought deal financing on June 24, 2025, and bought 1,200,000 common shares. Concurrent with the bought deal financing on January 27, 2026, NexGen subscribed to 1,666,667 common shares of the Company in a private placement.

(1) The common shares issued are retroactively restated on a post-consolidation basis. Refer to the discussion on the Share Consolidation, as described above in “About IsoEnergy”.

CRITICAL ACCOUNTING JUDGMENTS, ESTIMATES AND ASSUMPTIONS

The preparation of the Interim Financial Statements requires management to make judgments, estimates and assumptions that affect the reported amounts of assets, liabilities, and contingent liabilities at the date of the Interim Financial Statements and the reported amounts of revenues and expenses during the reporting period. Estimates and assumptions are continuously evaluated and are based on management’s experience and other factors, including expectations of future events that are believed to be reasonable in the circumstances. Uncertainty about these judgments, estimates and assumptions could result in outcomes that require a material adjustment to the carrying amount of the asset or liability affected in future periods. Information about significant areas of judgement, estimation uncertainty and assumptions considered by management in preparing the Interim Financial Statements are the same as described in the Annual Financial Statements.

CHANGES IN ACCOUNTING POLICIES INCLUDING INITIAL ADOPTION

The Interim Financial Statements were prepared in accordance with IAS 34 and its interpretations adopted by the IASB, and follow the same accounting policies and methods as described in the Annual Financial Statements.

The following standard has been issued and is effective:

Amendments to IFRS 9 and IFRS 7 – Classification and Measurement of Financial Instruments

In May 2024, the IASB issued 'Amendments to the Classification and Measurement of Financial Instruments (Amendments to IFRS 9 and IFRS 7)'. The amendments clarify the date of recognition and derecognition of some financial assets and financial liabilities, with a new exception that permits companies to elect to derecognize certain financial liabilities settled via electronic payment systems earlier than the settlement date. The amendments apply for annual reporting periods beginning on or after January 1, 2026, and are applied retrospectively. There were no changes to the Interim Financial Statements from adopting these amendments.

23

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

The following new standard has been issued and is not yet effective:

IFRS 18 – Presentation and Disclosure in Financial Statements

The IASB has issued IFRS 18 – Presentation and Disclosure in Financial Statements (“IFRS 18”), which replaces IAS 1 – Presentation of Financial Statements. IFRS 18 introduces new requirements for the presentation of financial performance, including revised categories in the statements of loss, enhanced disclosures on management-defined performance measures, and greater consistency in financial statement presentation. The standard is effective for annual reporting periods beginning on or after January 1, 2027 and applies retrospectively, with early adoption permitted.

The Company has not early adopted IFRS 18 and continues to evaluate the impact of the forthcoming standard in preparing the Interim Financial Statements.

CAPITAL MANAGEMENT AND RESOURCES

The Company manages its capital structure, defined as total equity plus debt, and adjusts it, based on the funds available to the Company, in order to support the acquisition, exploration and evaluation of assets. The Board does not impose quantitative return on capital criteria for management, but rather relies on the expertise of the Company’s management to sustain the future development of the business.

In the management of capital, the Company considers all types of funding alternatives, including equity, debt and other means and is dependent on third party financing. Although the Company has been successful in raising funds to date, there is no assurance that the Company will be successful in obtaining required financing in the future or that such financing will be available on terms acceptable to the Company.

The properties in which the Company currently has an interest are in the exploration and development stage. As such the Company, has historically relied on the equity markets to fund its activities. The Company will continue to assess new properties and seek to acquire an interest in additional properties if it determines that there is sufficient geologic or economic potential and if it has adequate financial resources to do so.

Management reviews its capital management approach on an on-going basis and believes that this approach, given the relative size of the Company, is reasonable. The Company is not subject to externally imposed capital requirements. There were no changes in the Company’s approach to capital management during the period.

FINANCIAL INSTRUMENTS

The Company’s financial instruments consist of cash and cash equivalents, accounts receivable, marketable securities, accounts payable and accrued liabilities, and convertible debentures.

Fair Value Measurement

The Company classifies the fair value of financial instruments according to the following hierarchy based on the amount of observable inputs used to value the instrument:

| · | Level 1 – quoted prices in active markets for identical assets or liabilities. |

| · | Level 2 – inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly (i.e. as prices) or indirectly (i.e. derived from prices). |

| · | Level 3 – inputs for the asset or liability that are not based on observable market data. |

The fair values of the Company’s cash and cash equivalents, accounts receivable, and accounts payable and accrued liabilities approximate their carrying value, due to their short-term maturities or liquidity.

24

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

The 2022 Debentures are re-measured at fair value at each reporting date with any change in fair value recognized in profit or loss, except for the change in fair value that is attributable to change in credit risk, which is presented in other comprehensive income (loss). The 2022 Debentures are classified as Level 2.

The marketable securities are re-measured at fair value at each reporting date with any change in fair value recognized in other comprehensive income (loss). The common shares included in marketable securities are Level 1, except for the common shares of privately held marketable securities, which are Level 3 and their fair value is primarily based on the price of their most recent share issuances. The warrants included in marketable securities are Level 2. During the three months ended March 31, 2026, Jaguar Uranium and Verdera Energy Corp. completed public listings. As a result, the Company transferred its common shares held in these entities from Level 3 to Level 1. The fair value transferred is measured at the share price at the time of the public listing of each entity.

Financial instrument risk exposure

As of March 31, 2026, the Company’s financial instrument risk exposure and the impact thereof on the Company’s financial instruments are summarized below:

| (a) | Credit Risk |

Credit risk is the risk that one party to a financial instrument will fail to discharge an obligation and cause the other party to incur a financial loss. As at March 31, 2026, the Company has cash and cash equivalents on deposit with large banks in Canada, the United States, and Australia. Credit risk is concentrated as a significant amount of the Company’s cash and cash equivalents is held at a Canadian financial institution. Management believes the risk of loss to be remote.

The Company’s accounts receivable mostly consists of input tax credits receivable from the Governments of Canada and Australia and amounts receivable from related parties. Accordingly, the Company does not believe it is subject to significant credit risk.

(b) Liquidity Risk

Liquidity risk is the risk that an entity will encounter difficulty in raising funds to meet its obligations under financial instruments. The Company manages liquidity risk by maintaining sufficient cash balances that are accessible on deposit or on short-term notice. Liquidity requirements are managed based on expected cash flows to ensure that there is sufficient capital to meet short-term obligations. As at March 31, 2026, the Company had an adjusted working capital balance of $183,253,876, including cash and cash equivalents of $130,537,804.

| (c) Market Risk |

Market risk is the risk of loss that may arise from changes in market factors such as interest rates, foreign exchange rates and commodity and equity prices.

| (i) | Interest Rate Risk |

Interest rate risk is the risk that the future cash flows from a financial instrument will fluctuate due to changes in market interest rates. The Company holds its cash and cash equivalents in bank accounts that earn variable interest rates. Due to the short-term nature of these financial instruments, fluctuations in market rates do not have a significant impact on the estimated fair value of the Company’s cash and cash equivalent balances as of March 31, 2026. The interest on the 2022 Debentures is fixed and not subject to market fluctuations.

25

ISOENERGY LTD.

For the three months ended March 31, 2026 and 2025

| (ii) | Price Risk |