NOTE 21 - SUBSEQUENT EVENTS

The Company has evaluated subsequent events through the filing of this report and determined that there have not been any events, other than those described below, that have occurred that would require adjustments to or disclosures in the consolidated financial statements.

As previously announced, on April 29, 2026, the Company entered into an Agreement and Plan of Merger (the “Merger Agreement”) with ACRES Holdings Sub LLC (“Merger Sub”), a subsidiary of the Company, on one hand and ACRES Capital Corp (“ACC”) and ACRES Capital, LLC, a subsidiary of ACC and the external manager of the Company (the “Manager”), on the other hand, pursuant to which ACC will be merged with and into Merger Sub, with Merger Sub surviving as a wholly-owned subsidiary of the Company (the “Merger”). As a result of the Merger, among other things, (i) the Company will acquire the Manager, (ii) the Manager will cease to perform any outside management services for the Company, (iii) the Company and the Manager will terminate the existing Management Agreement (as defined below) between the parties, and (iv) the Company will become internally managed (the “Internalization”).

The closing of the Merger (the “Closing”) is subject to a number of conditions, including the issuance of common stock at the Closing which is subject to approval by the Company’s common stockholders at the Company’s 2026 Annual Meeting. The Company expects to hold its 2026 Annual Meeting in June 2026, and close the Merger (and consummate the Internalization) early in the third quarter of 2026.

Pursuant to the Merger Agreement, at Closing, (i) each outstanding share of common stock, $0.0001 par value per share, of ACC (“ACC Common Stock”) will be converted into the right to receive 2.61882 shares of common stock, $0.001 par value per share, of the Company (the “ACR Common Stock”) and (ii) the Fourth Amended and Restated Management Agreement, dated as of July 31, 2020, as amended, by and among the Company, the Manager and ACC (the “Management Agreement”), will terminate for no additional consideration. The Company expects to issue a maximum of approximately 7.487 million shares of ACR Common Stock at Closing (the “Stock Issuance”), the exact number of which will be determined based on the number of outstanding shares of ACC Common Stock immediately prior to the Closing.

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

References in this quarterly report to "we," "us" or the "Company" refer to ACRES Commercial Realty Corp. The following discussion and analysis of the Company’s financial condition and results of operations should be read in conjunction with the consolidated financial statements and accompanying notes appearing elsewhere in this report. Certain information contained in the discussion and analysis set forth below includes forward-looking statements that involve risks and uncertainties.

Special Note Regarding Forward-Looking Statements

This report contains certain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Such forward-looking statements can generally be identified by our use of forward-looking terminology such as "may," "will," "continue," "expect," "intend," "anticipate," "estimate," "believe," "look forward" or other similar words or terms. Because such statements include risks, uncertainties and contingencies, actual results may differ materially from the expectations, intentions, beliefs, plans or predictions of the future expressed or implied by such forward-looking statements. Factors that could cause actual results to differ materially from those anticipated in the forward-looking statements include:

• changes in our industry, interest rates, the debt securities markets, real estate markets or the general economy;

• increased rates of default and/or decreased recovery rates on our investments;

• the performance and financial condition of our borrowers;

• our ability to consummate the proposed Merger (as defined below) and achieve the expected cost savings or other benefits therefrom;

•if we fail to consummate the proposed Merger, our dependence on our Manager and ability to find a suitable replacement in a timely manner, or at all, if our Manager or we were to terminate the management agreement;

• the cost and availability of our financings, which depend in part on our asset quality, the nature of our relationships with our lenders and other capital providers, our business prospects and outlook and general market conditions;

• the availability and attractiveness of terms of additional debt repurchases;

• availability, terms and deployment of short-term and long-term capital;

• events giving rise to increases in our current expected credit loss reserve, including the impact of the current economic environment;

• availability of, and ability to retain, qualified personnel;

• changes in our business strategy;

• the degree and nature of our competition;

• the resolution of our non-performing and sub-performing assets;

• our ability to comply with financial covenants in our debt instruments;

• the adequacy of our cash reserves and working capital;

• the timing of cash flows, if any, from our investments;

• unanticipated increases in financial and other costs, including a rise in interest rates;

• our ability to maintain compliance with over-collateralization and interest coverage tests in our collateralized loan obligations (“CLOs”);

• environmental and/or safety requirements;

• our ability to satisfy complex rules in order for us to qualify as a real estate investment trust (“REIT”), for federal income tax purposes and qualify for our exemption under the Investment Company Act of 1940, as amended, and our ability and the ability of our subsidiaries to operate effectively within the limitations imposed by these rules;

• legislative and regulatory changes (including changes to laws governing the taxation of REITs or the exemptions from registration as an investment company); and

• the factors described in this report and the Company’s Annual Report on Form 10-K for the year ended December 31, 2025, including those set forth under the sections captioned “Risk Factors,” “Business” and “Management’s Discussion and Analysis of Financial Conditions and Results of Operations,” as applicable.

We caution you not to place undue reliance on these forward-looking statements, which speak only as of the date of this report. All subsequent written and oral forward-looking statements attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Except to the extent required by applicable law or regulation, we undertake no obligation to update these forward-looking statements to reflect events or circumstances after the date of this report or to reflect the occurrence of unanticipated events.

Overview

We are a Maryland corporation and an externally-managed real estate investment trust ("REIT") that is primarily focused on originating, holding and managing commercial real estate ("CRE") mortgage loans and equity investments in commercial real estate properties through direct ownership and joint ventures. Our manager is ACRES Capital, LLC (our "Manager"), a subsidiary of ACRES Capital Corp. ("ACC," and collectively with our Manager, "ACRES"), a private commercial real estate lender exclusively dedicated to nationwide middle market CRE lending with a focus on multifamily, student housing, hospitality, office and industrial properties in top United States ("U.S.") markets. Our Manager draws upon the management team of ACRES and its collective investment experience to provide its services. Our longer-term objective is to provide our stockholders with total returns over time, including quarterly distributions and capital appreciation, while seeking to manage the risks associated with our investment strategies, as well as to maximize long-term stockholder value by maintaining stability through our available liquidity and diversified CRE loan portfolio.

Currently, markets are grappling with trade tensions, geopolitical tensions, the risk of increased tariffs, inflation and labor volatility. These market pressures have caused continued disruption in many market segments, including the financial services, real estate and credit markets and these disruptions have affected the availability and the cost of capital. The increase in the cost of capital is expected to cause dislocations in various investment and financing markets in which we participate as we and other market participants adjust to the new financing environment.

Since September 2024, the U.S. Federal Reserve lowered the Federal Funds rate by 1.75% in six rate cuts reaching its lowest levels since 2022. Lowering rates and decreasing costs may encourage consumer spending and accelerate corporate profit growth, which may positively impact the credit profile of the collateral underlying our loans and positively impact our borrowers' ability to sell or refinance in the current market; however, lower rates would also correlate to decreases in our net income. There is also no certainty with respect to the direction, timing, or pace of change for future interest rates.

The multifamily real estate market continues to be a competitive market, and as a result of investors' continued confidence in that asset class, the market for those assets continues to experience spread compression on newly originated deals. Furthermore, the office property market continues to experience high vacancies, slower leasing activity and current tenants reevaluating their needs for physical office space due to remote-work trends across the country. These factors, coupled with inflation, higher interest rates and dislocations in market liquidity, have converged to create higher levels of uncertainty surrounding property values, which in turn, also negatively impact borrowers' ability and willingness to financially support and standby their investments in their office properties, their abilities to sell or refinance their positions in the current market and ultimately our financial results.

In response, we continue to manage corporate liquidity actively and responsibly, manage our CRE assets through a solutions-based approach with our borrowers and manage our daily operations in light of changing macroeconomic circumstances. Our Manager also continuously monitors for new capital opportunities and selectively executes on agreements that are expected to enhance our returns.

As previously reported, on April 29, 2026, we entered into an Agreement and Plan of Merger (the “Merger Agreement”), pursuant to which we will acquire ACC in an all-stock transaction (the “Merger”). As a result of the Merger, among other things, we will acquire our Manager, and transition from an externally-managed REIT to an internally-managed REIT (the “Internalization”).

We originate transitional floating-rate CRE loans with a target size between $10.0 million and $100.0 million. During the three months ended March 31, 2026, we originated nine new CRE floating-rate whole loans, purchased one new CRE floating-rate whole loan and purchased a participation in an existing CRE floating-rate whole loan, with total commitments of $495.6 million and funded $13.6 million of loan commitments. These increases were offset by loan payoffs and sales during the three months ended March 31, 2026 in the amount of $110.6 million and unfunded commitments of $24.2 million, producing a net increase to the portfolio of $374.4 million. During the year ended December 31, 2025, we originated 14 new CRE floating-rate whole loans, with total commitments of $733.0 million, one new $15.0 million CRE mezzanine loan, one new $9.3 million CRE preferred equity investment and net funded commitments of $3.1 million. Loan payoffs and sales during the year ended December 31, 2025 were $418.9 million, producing a net increase to the portfolio of $341.5 million.

Our CRE loan portfolio, which had carrying values of $2.2 billion and $1.8 billion at March 31, 2026 and December 31, 2025, respectively, comprised:

We generate our income primarily from the spread between the revenues we receive from our assets and the cost to finance our ownership of those assets, including corporate debt.

While the CRE whole loans included in the CRE loan portfolio are substantially composed of floating-rate loans benchmarked to the one-month Term Secured Overnight Financing Rate ("Term SOFR"), asset yields are protected through the use of benchmark floors and minimum interest periods that typically range from 12 to 18 months at the time of a loan’s origination. Our benchmark floors provide asset yield protection when the benchmark rate falls below an in-place benchmark floor. Our net investment returns are enhanced by a decline in the cost of our floating-rate liabilities that do not have benchmark floors. Our net investment returns will be negatively impacted by the rising cost of our floating-rate liabilities that do not have floors until the benchmark rate is above the benchmark floor, at which point our floating-rate loans and floating-rate liabilities will be match-funded, effectively locking in our net interest margin until the benchmark floor rate is activated again or the floating-rate loan is paid off or refinanced.

In a business environment where benchmark rates are increasing significantly, cash flows of the CRE assets underlying our loans may not be sufficient to pay debt service on our loans, which could result in non-performance or default. We partially mitigate this risk by generally requiring our borrowers to purchase interest rate cap agreements with non-affiliated, well-capitalized third parties and by selectively requiring our borrowers to have and maintain debt service reserves. These interest rate caps generally mature prior to the maturity date of the loan and the borrowers are required to pay to extend them. In certain cases, the sponsors will need to fund additional equity into the properties to cover these costs as the property may not generate sufficient cash flow to pay these costs. At March 31, 2026, 74% of the par value of our CRE loan portfolio had interest rate caps or funded debt service reserves in place. Our interest rate caps have a weighted-average maturity of 15 months.

At March 31, 2026, our par-value $2.2 billion floating-rate CRE loan portfolio had a weighted average benchmark floor of 2.13%. At December 31, 2025, our par value $1.8 billion floating rate CRE loan portfolio had a weighted average benchmark floor of 1.78%. With the current trend of decreasing benchmark rates, we have seen the coupons on all of our floating-rate assets and debt decrease accordingly. Because we have equity invested in each floating-rate loan, and because in all instances the benchmark interest rates are above our loan floors, the decrease in interest rates resulted in a decrease in our net interest income. See "Interest Rate Risk" in "Item 3: Quantitative and Qualitative Disclosures About Market Risk."

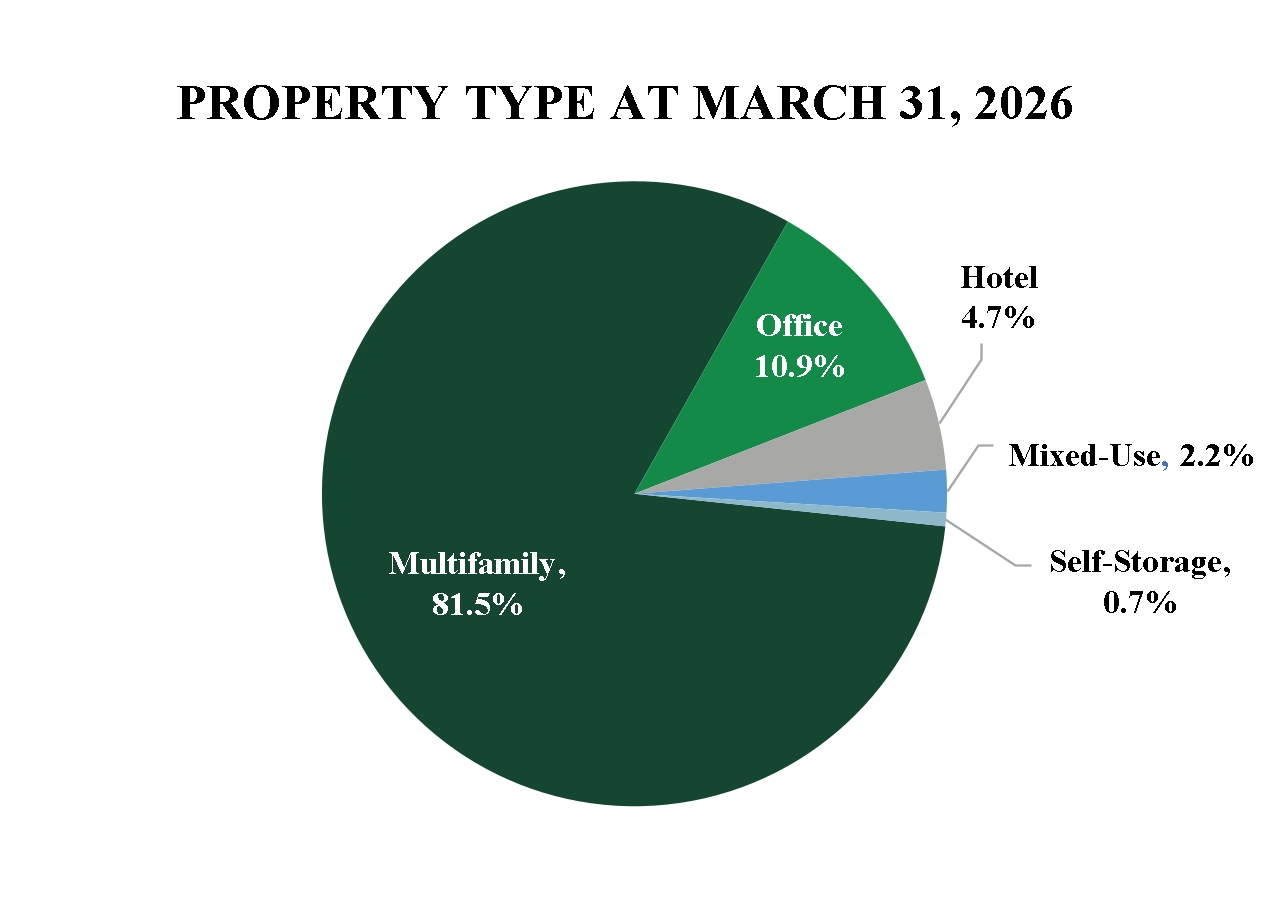

Our portfolio comprises loans with a diverse array of collateral types and locations. Multifamily continues to comprise the majority of our portfolio, with 81.5% of our portfolio allocated to multifamily at March 31, 2026 and 81.9% at December 31, 2025. The following charts show our portfolio allocation at carrying value by property type at March 31, 2026 and December 31, 2025:

From time to time, we may acquire real estate property through direct equity investments or as a result of our lending activities. We did not acquire any real estate property in the three months ended March 31, 2026.

At March 31, 2026, the net carrying value of our net real estate-related assets and liabilities was $106.3 million on five properties owned, two of which are included in investments in real estate and three of which are included in properties held for sale on our consolidated balance sheets.

We use leverage to enhance our returns. The cost of borrowings to finance our investments is a significant part of our expenses. Our net interest income depends on our ability to control these expenses relative to our revenue. Our CRE loans may initially be financed with term facilities, such as CRE loan warehouse financing facilities, in anticipation of their ultimate securitization. We ultimately seek to finance our CRE loans through the use of non-recourse long-term, match-funded CRE debt securitizations.

At March 31, 2026 and December 31, 2025, our financing arrangements were as follows (dollars in thousands):

|

|

Outstanding Borrowings |

|

|

Percentage of Borrowings |

|

||

At March 31, 2026 |

|

|

|

|

|

|

||

CRE debt securitization (1)(2) |

|

$ |

873,463 |

|

|

|

46.9 |

% |

CRE - term reinvestment financing facility (1)(3) |

|

|

709,206 |

|

|

|

38.0 |

% |

CRE - term warehouse financing facilities(1) |

|

|

18,938 |

|

|

|

1.0 |

% |

Senior secured financing facility(1) |

|

|

41,654 |

|

|

|

2.2 |

% |

Mortgage payable(1) |

|

|

20,145 |

|

|

|

1.1 |

% |

5.75% Senior Unsecured Notes |

|

|

149,717 |

|

|

|

8.0 |

% |

Unsecured junior subordinated debentures |

|

|

51,548 |

|

|

|

2.8 |

% |

Total |

|

$ |

1,864,671 |

|

|

|

100.0 |

% |

|

|

|

|

|

|

|

||

|

|

Outstanding Borrowings |

|

|

Percentage of Borrowings |

|

||

At December 31, 2025: |

|

|

|

|

|

|

||

CRE - term reinvestment financing facility (1)(2) |

|

$ |

728,167 |

|

|

|

47.1 |

% |

CRE - term warehouse financing facilities(1) |

|

|

533,862 |

|

|

|

34.6 |

% |

Senior secured financing facility(1) |

|

|

61,645 |

|

|

|

4.0 |

% |

Mortgage payable(1) |

|

|

20,185 |

|

|

|

1.3 |

% |

5.75% Senior Unsecured Notes |

|

|

149,531 |

|

|

|

9.7 |

% |

Unsecured junior subordinated debentures |

|

|

51,548 |

|

|

|

3.3 |

% |

Total |

|

$ |

1,544,938 |

|

|

|

100.0 |

% |

We reevaluate our current expected credit losses ("CECL") allowance quarterly, incorporating our current expectations of macroeconomic factors considered in the determination of our CECL reserves. At March 31, 2026, the CECL allowance on our CRE loan portfolio was $19.4 million, or 0.9% of our $2.2 billion loan portfolio. During the three months ended March 31, 2026, we recorded a reversal of credit losses primarily attributable to improvements in projected macroeconomic factors during the quarter, offset by an increase in the modeled credit risk of our loan portfolio.

At December 31, 2025, the CECL allowance on our CRE loan portfolio was $20.4 million, or 1.1% of our $1.8 billion loan portfolio. During the year ended December 31, 2025, we recorded a reversal of credit losses primarily driven by net improvements in the modeled credit risk of our loan portfolio as well as loan payoffs. These reversals were offset by a general decline in projected macroeconomic factors. We also recorded a charge-off of $4.7 million for one mezzanine loan that was fully reserved for in 2022.

Additionally, the decline in our CECL reserves from our highest reserve balance at June 30, 2020 of $61.1 million, or 3.4% of the par balance of our CRE loan portfolio, to our current reserve balance at March 31, 2026 of $19.4 million, or 0.9% of the par balance of our CRE loan portfolio, has been due to the following: the successful resolution of our individually evaluated loans with specific reserves, except for the charge-off noted above, the overall newer vintage of our CRE loan portfolio (with only 6.3% of the portfolio, at March 31, 2026, being originated prior to the fourth quarter of 2020) as well as the increased percentage allocation of our CRE loan portfolio to multifamily loans over time. Multifamily loans have historically had the lowest credit losses of any asset class, and our percentage allocation of our CRE loan portfolio to multifamily at carrying value has grown from 58.4% at June 30, 2020 to 81.5% at March 31, 2026.

Common stock book value was $29.98 per share at March 31, 2026, a $0.03 per share decrease from December 31, 2025.

Results of Operations

Our net loss allocable to common shares for the three months ended March 31, 2026 was $1.0 million or $(0.16) per share-basic ($(0.16) per share-diluted) as compared to net loss allocable to common shares for the three months ended March 31, 2025 of $5.9 million or $(0.80) per share-basic ($0.80) per share-diluted.

Net Interest Income

The following table analyzes the change in interest income and interest expense for the comparative three months ended March 31, 2026 and 2025 by changes in volume and changes in rates. The changes attributable to the combined changes in volume and rate have been allocated proportionately, based on absolute values, to the changes due to volume and changes due to rates (dollars in thousands, except amounts in footnotes):

|

|

Three Months Ended March 31, 2026 Compared to Three Months Ended March 31, 2025 |

|

|||||||||||||

|

|

|

|

|

|

|

|

Due to Changes in |

|

|||||||

|

|

Net Change |

|

|

Percent Change (1) |

|

|

Volume |

|

|

Rate |

|

||||

Increase (decrease) in interest income: |

|

|

|

|

|

|

|

|

|

|

|

|

||||

CRE whole loans (2) |

|

$ |

4,289 |

|

|

|

15 |

% |

|

$ |

8,225 |

|

|

$ |

(3,936 |

) |

CRE mezzanine loans |

|

|

(63 |

) |

|

|

(100 |

)% |

|

|

(63 |

) |

|

|

— |

|

CRE preferred equity loan |

|

|

247 |

|

|

|

100 |

% |

|

|

247 |

|

|

|

— |

|

Other |

|

|

1,161 |

|

|

|

452 |

% |

|

|

974 |

|

|

|

187 |

|

Total increase (decrease) in interest income |

|

|

5,634 |

|

|

|

20 |

% |

|

|

9,383 |

|

|

|

(3,749 |

) |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

Increase (decrease) in interest expense: |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Securitized borrowings: |

|

|

|

|

|

|

|

|

|

|

|

|

||||

ACR 2026-FL4 Senior Notes |

|

|

6,292 |

|

|

|

100 |

% |

|

|

6,292 |

|

|

|

— |

|

ACR 2021-FL1 Senior Notes |

|

|

(6,535 |

) |

|

|

(100 |

)% |

|

|

(6,535 |

) |

|

|

— |

|

ACR 2021-FL2 Senior Notes |

|

|

(6,554 |

) |

|

|

(100 |

)% |

|

|

(6,554 |

) |

|

|

— |

|

Senior secured financing facility |

|

|

(167 |

) |

|

|

(11 |

)% |

|

|

(66 |

) |

|

|

(101 |

) |

CRE - term warehouse financing facilities |

|

|

1,537 |

|

|

|

60 |

% |

|

|

1,874 |

|

|

|

(337 |

) |

CRE - term reinvestment financing facility |

|

|

7,557 |

|

|

|

350 |

% |

|

|

7,779 |

|

|

|

(222 |

) |

5.75% Senior Unsecured Notes (3) |

|

|

11 |

|

|

|

— |

% |

|

|

11 |

|

|

|

— |

|

Unsecured junior subordinated debentures |

|

|

(84 |

) |

|

|

(8 |

)% |

|

|

— |

|

|

|

(84 |

) |

Hedging (4) |

|

|

(66 |

) |

|

|

(17 |

)% |

|

|

(66 |

) |

|

|

— |

|

Total increase (decrease) in interest expense |

|

|

1,991 |

|

|

|

9 |

% |

|

|

2,735 |

|

|

|

(744 |

) |

Net increase (decrease) increase in net interest income |

|

$ |

3,643 |

|

|

|

|

|

$ |

6,648 |

|

|

$ |

(3,005 |

) |

|

Net Change in Interest Income for the Comparative three months ended March 31, 2026 and 2025:

Aggregate interest income increased by $5.6 million for the comparative three months ended March 31, 2026 and 2025. We attribute the change to the following:

CRE whole loans. The increase of $4.3 million for the comparative three months ended March 31, 2026 and 2025 was primarily attributable to an increase in the daily average par value of our CRE portfolio resulting from loan production, offset by a decrease in the benchmark rate over the comparative period.

CRE mezzanine loans. The decrease of $63,000 for the comparative three months ended March 31, 2026 and 2025 was primarily attributable to the origination and payoff of a mezzanine loan during fiscal year 2025.

CRE preferred equity loan. The increase of $247,000 for the comparative three months ended March 31, 2026 and 2025 was primarily attributable to the origination of a preferred equity loan in September 2025.

Other. The increase of $1.2 million for the comparative three months ended March 31, 2026 and 2025, was primarily attributable to an increase in restricted cash from the close of our new CRE securitization, ACRES Commercial Realty 2026-FL4 Issuer, LLC ("ACR 2026-FL4"), and increase in yields on our interest earning money market accounts.

Net Change in Interest Expense for the Comparative three months ended March 31, 2026 and 2025:

Aggregate interest expense increased by $2.0 million for the comparative three months ended March 31, 2026 and 2025. We attribute the change to the following:

Securitized borrowings. The net decrease of $6.8 million for the comparative three months ended March 31, 2026 and 2025, was primarily attributable to the issuance of our ACR 2026-FL4 securitization, offset by the redemptions of our ACR 2021-FL1 and ACR 2021-FL2 securitizations and a decrease in the benchmark rate over the comparative periods.

Senior secured financing facility. The decrease of $167,000 for the comparative three months ended March 31, 2026 and 2025, was primarily attributable to a decrease in borrowings and benchmark rate over the comparative periods.

CRE - term warehouse financing facilities. The increase of $1.5 million for the comparative three months ended March 31, 2026 and 2025, was primarily attributable to an increase in the average daily borrowings balance, offset by a decrease in the benchmark rate over the comparative periods.

CRE - term reinvestment financing facility. The increase of $7.6 million was attributable to the close of our new CRE term reinvestment financing facility in March 2025.

Unsecured junior subordinated debentures. The decrease of $84,000 for the comparative three months ended March 31, 2026 and 2025, was primarily attributable to a decrease in the benchmark rate over the comparative periods.

Average Net Yield and Average Cost of Funds:

The following table presents the average net yield and average cost of funds for the three months ended March 31, 2026 and 2025 (dollars in thousands, except amounts in footnotes):

|

|

Three Months Ended March 31, 2026 |

|

|

Three Months Ended March 31, 2025 |

|

||||||||||||||||||

|

|

Average Amortized Cost |

|

|

Interest Income (Expense) |

|

|

Average Net Yield (Cost of Funds) (1) |

|

|

Average Amortized Cost |

|

|

Interest Income (Expense) |

|

|

Average Net Yield (Cost of Funds) (1) |

|

||||||

Interest-earning assets |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

CRE whole loans, floating-rate (2) |

|

$ |

1,848,878 |

|

|

$ |

32,694 |

|

|

|

7.17 |

% |

|

$ |

1,408,582 |

|

|

$ |

28,406 |

|

|

|

8.18 |

% |

CRE mezzanine loans |

|

|

— |

|

|

|

— |

|

|

|

— |

% |

|

|

6,367 |

|

|

|

63 |

|

|

|

3.93 |

% |

CRE preferred equity loan |

|

|

9,675 |

|

|

|

248 |

|

|

|

10.38 |

% |

|

|

— |

|

|

|

— |

|

|

|

— |

% |

Other |

|

|

138,052 |

|

|

|

1,418 |

|

|

|

4.17 |

% |

|

|

37,834 |

|

|

|

257 |

|

|

|

2.76 |

% |

Total interest income/average net yield |

|

|

1,996,605 |

|

|

|

34,360 |

|

|

|

6.98 |

% |

|

|

1,452,783 |

|

|

|

28,726 |

|

|

|

8.02 |

% |

Interest-bearing liabilities |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Collateralized by: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

CRE whole loans (3) |

|

|

1,484,707 |

|

|

|

(21,425 |

) |

|

|

(5.85 |

)% |

|

|

1,019,882 |

|

|

|

(19,295 |

) |

|

|

(7.67 |

)% |

General corporate debt: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

5.75% Senior Unsecured Notes (4) |

|

|

149,625 |

|

|

|

(2,342 |

) |

|

|

(6.35 |

)% |

|

|

148,902 |

|

|

|

(2,331 |

) |

|

|

(6.35 |

)% |

Unsecured junior subordinated debentures |

|

|

51,548 |

|

|

|

(1,020 |

) |

|

|

(7.92 |

)% |

|

|

51,548 |

|

|

|

(1,104 |

) |

|

|

(8.57 |

)% |

Hedging (5) |

|

|

— |

|

|

|

(327 |

) |

|

|

— |

% |

|

|

— |

|

|

|

(393 |

) |

|

|

— |

% |

Total interest expense/average cost of funds |

|

|

1,685,880 |

|

|

|

(25,114 |

) |

|

|

(5.96 |

)% |

|

|

1,220,332 |

|

|

|

(23,123 |

) |

|

|

(7.55 |

)% |

Total net interest income |

|

|

|

|

$ |

9,246 |

|

|

|

|

|

|

|

|

$ |

5,603 |

|

|

|

|

||||

Real Estate Income and Other Revenue

The following table sets forth information relating to our real estate income and other revenue for the periods presented (dollars in thousands):

|

|

For the Three Months Ended March 31, |

|

|

|

|

|

|

|

|||||||

|

|

2026 |

|

|

2025 |

|

|

Dollar Change |

|

|

Percent Change |

|

||||

Real estate income and other revenue: |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Real estate income |

|

$ |

8,547 |

|

|

$ |

11,366 |

|

|

$ |

(2,819 |

) |

|

|

(25 |

)% |

Other revenue |

|

|

31 |

|

|

|

33 |

|

|

|

(2 |

) |

|

|

— |

% |

Total |

|

$ |

8,578 |

|

|

$ |

11,399 |

|

|

$ |

(2,821 |

) |

|

|

(25 |

)% |

Aggregate real estate income and other revenue decreased by $2.8 million for the comparative three months ended March 31, 2026 and 2025. The decrease in the comparative three months was attributed to: (i) a decrease in revenue related to a student housing property that was sold in September 2025, and (ii) a decrease in revenue at an office property that was sold in December 2025, partially offset by an increase in revenues at a hotel property in the northeast region that had increased occupancy and rates in the comparative period.

Operating Expenses

The following table sets forth information relating to our operating expenses for the periods presented (dollars in thousands):

|

|

For the Three Months Ended March 31, |

|

|

|

|

|

|

|

|||||||

|

|

2026 |

|

|

2025 |

|

|

Dollar Change |

|

|

Percent Change |

|

||||

Operating expenses: |

|

|

|

|

|

|

|

|

|

|

|

|

||||

General and administrative |

|

$ |

3,036 |

|

|

$ |

3,159 |

|

|

$ |

(123 |

) |

|

|

(4 |

)% |

Real estate expenses |

|

|

9,710 |

|

|

|

13,342 |

|

|

|

(3,632 |

) |

|

|

(27 |

)% |

Management fees - related party |

|

|

1,561 |

|

|

|

1,631 |

|

|

|

(70 |

) |

|

|

(4 |

)% |

Equity compensation - related party |

|

|

540 |

|

|

|

815 |

|

|

|

(275 |

) |

|

|

(34 |

)% |

Corporate depreciation and amortization |

|

|

19 |

|

|

|

18 |

|

|

|

1 |

|

|

|

6 |

% |

Reversal of credit losses, net |

|

|

(967 |

) |

|

|

(1,717 |

) |

|

|

750 |

|

|

|

(44 |

)% |

Total |

|

$ |

13,899 |

|

|

$ |

17,248 |

|

|

$ |

(3,349 |

) |

|

|

(19 |

)% |

Aggregate operating expenses decreased by $3.3 million for the comparative three months ended March 31, 2026 and 2025. We attribute the changes to the following:

General and administrative. General and administrative expenses decreased by $123,000 for the comparative three months ended March 31, 2026 and 2025. The following table summarizes the information relating to our general and administrative expenses for the periods presented (dollars in thousands):

|

|

For the Three Months Ended March 31, |

|

|

|

|

|

|

|

|||||||

|

|

2026 |

|

|

2025 |

|

|

Dollar Change |

|

|

Percent Change |

|

||||

General and administrative |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Professional services |

|

$ |

1,554 |

|

|

$ |

1,707 |

|

|

$ |

(153 |

) |

|

|

(9 |

)% |

Wages and benefits |

|

|

370 |

|

|

|

427 |

|

|

|

(57 |

) |

|

|

(13 |

)% |

D&O insurance |

|

|

242 |

|

|

|

242 |

|

|

|

- |

|

|

|

(— |

)% |

Operating expenses |

|

|

347 |

|

|

|

254 |

|

|

|

93 |

|

|

|

37 |

% |

Dues and subscriptions |

|

|

184 |

|

|

|

217 |

|

|

|

(33 |

) |

|

|

(15 |

)% |

Director fees |

|

|

204 |

|

|

|

204 |

|

|

|

— |

|

|

|

(— |

)% |

Tax penalties, interest & franchise tax |

|

|

100 |

|

|

|

88 |

|

|

|

12 |

|

|

|

14 |

% |

Travel |

|

|

35 |

|

|

|

20 |

|

|

|

15 |

|

|

|

75 |

% |

Total |

|

$ |

3,036 |

|

|

$ |

3,159 |

|

|

$ |

(123 |

) |

|

|

(4 |

)% |

The decrease in general and administrative expense for the comparative three months ended March 31, 2026 and 2025 was primarily attributable to decreased professional services related to consulting fees being paid in the first quarter of 2025 that related to prior year services.

Real estate expenses. The decrease of $3.6 million for the comparative three months ended March 31, 2026 was primarily related to (i) a decrease in expenses related to a student housing property that was sold in September 2025, (ii) a decrease in expenses at an office property that was sold in December 2025, and (iii) a decrease in expenses at a student housing property related to a decrease in marketing and other operating expenses in the comparative periods.

Equity compensation - related party. The decrease in equity compensation - related party of $275,000 is related to the amortization of unvested shares. The unvested share balance decreased period over period due to a portion of shares vesting in May 2025, thus decreasing amortization related to unvested shares in the comparable periods.

Reversal of credit losses. The decrease in the reversal for credit losses of $750,000 for the comparative three months ended March 31, 2026 was primarily driven by improvements in projected macroeconomic factors during the quarter, offset by an increase in the modeled credit risk of our loan portfolio.

Other Income (Expense)

The following table sets forth information relating to our other income (expense) incurred for the periods presented (dollars in thousands):

|

|

For the Three Months Ended March 31, |

|

|

|

|

|

|

|

|||||||

|

|

2026 |

|

|

2025 |

|

|

Dollar Change |

|

|

Percent Change |

|

||||

Other income (expense): |

|

|

|

|

|

|

|

|

|

|

|

|

||||

Equity in income (losses) of unconsolidated subsidiaries |

|

$ |

245 |

|

|

$ |

(492 |

) |

|

$ |

737 |

|

|

|

150 |

% |

Gain on sale of investment in real estate |

|

|

3,336 |

|

|

|

— |

|

|

|

3,336 |

|

|

|

100 |

% |

Other income |

|

|

23 |

|

|

|

84 |

|

|

|

(61 |

) |

|

|

(73 |

)% |

Total |

|

$ |

3,604 |

|

|

$ |

(408 |

) |

|

$ |

4,012 |

|

|

|

983 |

% |

Aggregate other income (expense) increased $4.0 million for the comparative three months ended March 31, 2026 and 2025. We attribute the change to the following:

Equity in income (losses) of unconsolidated subsidiaries. The increase of $737,000 for the comparative three months ended March 31, 2026 and 2025 was primarily related to recognizing income at one unconsolidated entity, which is partially offset by loss recognition at two other unconsolidated entities. The two unconsolidated entities with losses are off-balance sheet and losses are only recognized when contributions are made.

Gain on sale of investment in real estate. The increase of $3.3 million for the comparative three months ended March 31, 2026 and 2025 was primarily attributed to the sale of a property generating a gain of $3.3 million in the first quarter of 2026 compared to no sales on real estate in the first quarter of 2025.

Financial Condition

Summary

Our total assets were $2.5 billion and $2.2 billion at March 31, 2026 and December 31, 2025, respectively.

Investment Portfolio

The tables below summarize the amortized cost and net carrying amount of our investment portfolio, classified by asset type, at March 31, 2026 and December 31, 2025 as follows (dollars in thousands, except amounts in footnotes):

At March 31, 2026 |

|

Amortized Cost |

|

|

Net Carrying Amount (1) |

|

|

Percent of Portfolio |

|

|

Weighted Average Coupon |

|||

Loans held for investment: |

|

|

|

|

|

|

|

|

|

|

|

|||

CRE whole loans |

|

$ |

2,193,165 |

|

|

$ |

2,173,945 |

|

|

|

93.73 |

% |

|

7.12% |

CRE preferred equity investment |

|

|

9,672 |

|

|

|

9,461 |

|

|

|

0.41 |

% |

|

10.00% |

|

|

|

2,202,837 |

|

|

|

2,183,406 |

|

|

|

94.14 |

% |

|

|

Other investments: |

|

|

|

|

|

|

|

|

|

|

|

|||

Investments in unconsolidated entities |

|

|

29,722 |

|

|

|

29,722 |

|

|

|

1.28 |

% |

|

N/A(4) |

Investments in real estate(2) |

|

|

38,752 |

|

|

|

38,752 |

|

|

|

1.67 |

% |

|

N/A(4) |

Properties held for sale(3) |

|

|

67,523 |

|

|

|

67,523 |

|

|

|

2.91 |

% |

|

N/A(4) |

|

|

|

135,997 |

|

|

|

135,997 |

|

|

|

5.86 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Total investment portfolio |

|

$ |

2,338,834 |

|

|

$ |

2,319,403 |

|

|

|

100.00 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|||

At December 31, 2025 |

|

Amortized Cost |

|

|

Net Carrying Amount (1) |

|

|

Percent of Portfolio |

|

|

Weighted Average Coupon |

|||

Loans held for investment: |

|

|

|

|

|

|

|

|

|

|

|

|||

CRE whole loans |

|

$ |

1,820,942 |

|

|

$ |

1,800,784 |

|

|

|

91.74 |

% |

|

7.32% |

CRE preferred equity investment |

|

|

9,425 |

|

|

|

9,185 |

|

|

|

0.47 |

% |

|

10.00% |

|

|

|

1,830,367 |

|

|

|

1,809,969 |

|

|

|

92.21 |

% |

|

|

Other investments: |

|

|

|

|

|

|

|

|

|

|

|

|||

Investments in unconsolidated entities |

|

|

29,237 |

|

|

|

29,237 |

|

|

|

1.49 |

% |

|

N/A(4) |

Investments in real estate(2) |

|

|

56,277 |

|

|

|

56,277 |

|

|

|

2.86 |

% |

|

N/A(4) |

Properties held for sale(3) |

|

|

67,509 |

|

|

|

67,509 |

|

|

|

3.44 |

% |

|

N/A(4) |

|

|

|

153,023 |

|

|

|

153,023 |

|

|

|

7.79 |

% |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Total investment portfolio |

|

$ |

1,983,390 |

|

|

$ |

1,962,992 |

|

|

|

100.00 |

% |

|

|

CRE loans. During the three months ended March 31, 2026, we originated nine new CRE floating-rate whole loans, purchased one new CRE floating-rate whole loan and purchased a participation in an existing CRE floating-rate whole loan, with total commitments of $495.6 million of floating-rate CRE whole loan commitments and funded $13.6 million of loan commitments. These increases were offset by $110.6 million in proceeds from loan payoffs and sales and unfunded loan commitments of $24.2 million, producing a net increase of $374.4 million in the par balance of the portfolio.

The following is a summary of our loans (dollars in thousands, except amounts in footnotes):

Description |

|

Quantity |

|

Principal |

|

|

Unamortized (Discount) Premium, net (1) |

|

|

Amortized Cost |

|

|

Allowance for Credit Losses |

|

|

Carrying Value |

|

|

Contractual Interest Rates (2) |

|

Maturity Dates (3)(4) |

|||||

At March 31, 2026: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Whole loans (5)(6)(7) |

|

60 |

|

$ |

2,202,675 |

|

|

$ |

(9,510 |

) |

|

$ |

2,193,165 |

|

|

$ |

(19,220 |

) |

|

$ |

2,173,945 |

|

|

1M Term SOFR + 2.50% to 1M Term SOFR + 7.00% |

|

April 2026 to May 2030 |

Preferred equity investment (see Note 3) (8) |

|

|

|

|

9,750 |

|

|

|

(78 |

) |

|

|

9,672 |

|

|

|

(211 |

) |

|

|

9,461 |

|

|

10.00% |

|

October 2028 |

Total |

|

|

|

$ |

2,212,425 |

|

|

$ |

(9,588 |

) |

|

$ |

2,202,837 |

|

|

$ |

(19,431 |

) |

|

$ |

2,183,406 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

At December 31, 2025: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Whole loans (5)(6)(7) |

|

53 |

|

$ |

1,828,299 |

|

|

$ |

(7,357 |

) |

|

$ |

1,820,942 |

|

|

$ |

(20,158 |

) |

|

$ |

1,800,784 |

|

|

1M Term SOFR + 2.50% to 1M Term SOFR + 7.00% |

|

January 2026 to May 2030 |

Preferred equity investment (see Note 3) (8) |

|

|

|

|

9,511 |

|

|

|

(86 |

) |

|

|

9,425 |

|

|

|

(240 |

) |

|

|

9,185 |

|

|

10.00% |

|

October 2028 |

Total |

|

|

|

$ |

1,837,810 |

|

|

$ |

(7,443 |

) |

|

$ |

1,830,367 |

|

|

$ |

(20,398 |

) |

|

$ |

1,809,969 |

|

|

|

|

|

At March 31, 2026, 19.0%, 16.9% and 14.1% of our CRE loan portfolio based on carrying value was concentrated in the Southeast, Southwest and East North Central regions, respectively, as defined by the NCREIF. At December 31, 2025, 24.2%, 20.6% and 14.0% of our CRE loan portfolio based on carrying value was concentrated in the Southwest, Southeast, and Pacific regions, respectively. At March 31, 2026 and December 31, 2025, no single loan or investment group represented more than 10% of our total assets and one investment group generated 12% and 14% of our revenue, respectively.

Investments in unconsolidated entities.

The following table summarizes our investments in unconsolidated entities at March 31, 2026 and December 31, 2025 and equity in earnings (losses) of unconsolidated entities for the three months ended March 31, 2026 and 2025 (dollars in thousands, except in the footnotes):

|

|

|

|

|

|

|

|

|

|

|

Earnings (Losses) of Unconsolidated Entities |

|||||||||

|

|

Ownership % |

|

|

|

For the Three Months Ended March 31, |

|

|

||||||||||||

|

|

at March 31, 2026 |

|

March 31, 2026 |

|

|

December 31, 2025 |

|

|

|

2026 |

|

|

2025 |

|

|

||||

Unsecured Junior Subordinated Debentures(1) |

|

3% |

|

$ |

1,548 |

|

|

$ |

1,548 |

|

|

|

$ |

— |

|

|

$ |

— |

|

|

65 E. Wacker Joint Venture, LLC |

|

90% |

|

|

28,174 |

|

|

|

27,689 |

|

|

|

|

484 |

|

|

|

(188 |

) |

|

7720 McCallum JV, LLC |

|

50% |

|

|

— |

|

|

|

— |

|

|

|

|

(108 |

) |

|

|

(304 |

) |

|

Pacmulti Affiliates JV, LLC |

|

50% |

|

|

— |

|

|

|

— |

|

|

|

|

(131 |

) |

|

|

— |

|

|

Total |

|

|

|

$ |

29,722 |

|

|

$ |

29,237 |

|

|

|

$ |

245 |

|

|

$ |

(492 |

) |

|

We record our investments in RCT I’s and RCT II’s common shares as investments in unconsolidated entities using the cost method. We record our investment in the Wacker JV, the McCallum JV and the Pacmulti JV as equity method investments.

Investments in real estate and properties held for sale. At March 31, 2026, we held investments in five real estate properties, two of which are included in investments in real estate and three of which are included in properties held for sale on the consolidated balance sheets. We sold a property in March 2026 for $20.0 million, generating a gain on sale of $3.3 million, net of selling costs.

The following table summarizes the book value of our investments in real estate and related intangible assets at March 31, 2026 and December 31, 2025 (in thousands, except amounts in the footnotes):

|

|

March 31, 2026 |

|

|

December 31, 2025 |

|

||||||||||||||||||

|

|

Cost Basis |

|

|

Accumulated Depreciation & Amortization |

|

|

Carrying Value |

|

|

Cost Basis |

|

|

Accumulated Depreciation & Amortization |

|

|

Carrying Value |

|

||||||

Assets acquired: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Investments in real estate, equity: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Investments in real estate (1) |

|

$ |

58,070 |

|

|

$ |

(8,378 |

) |

|

$ |

49,692 |

|

|

$ |

74,468 |

|

|

$ |

(7,797 |

) |

|

$ |

66,671 |

|

Right of use assets (2)(3) |

|

|

19,664 |

|

|

|

(1,091 |

) |

|

|

18,573 |

|

|

|

19,665 |

|

|

|

(1,024 |

) |

|

|

18,641 |

|

Intangible assets (4) |

|

|

9,469 |

|

|

|

(3,529 |

) |

|

|

5,940 |

|

|

|

9,469 |

|

|

|

(3,342 |

) |

|

|

6,127 |

|

Subtotal |

|

|

87,203 |

|

|

|

(12,998 |

) |

|

|

74,205 |

|

|

|

103,602 |

|

|

|

(12,163 |

) |

|

|

91,439 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Investments in real estate from lending activities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Investments in real estate (1) |

|

|

10,025 |

|

|

|

(335 |

) |

|

|

9,690 |

|

|

|

10,025 |

|

|

|

(281 |

) |

|

|

9,744 |

|

Right of use assets (2)(3) |

|

|

399 |

|

|

|

(76 |

) |

|

|

323 |

|

|

|

399 |

|

|

|

(63 |

) |

|

|

336 |

|

Intangible assets (4) |

|

|

364 |

|

|

|

(304 |

) |

|

|

60 |

|

|

|

364 |

|

|

|

(270 |

) |

|

|

94 |

|

Subtotal |

|

|

10,788 |

|

|

|

(715 |

) |

|

|

10,073 |

|

|

|

10,788 |

|

|

|

(614 |

) |

|

|

10,174 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Properties held for sale (5) |

|

|

90,851 |

|

|

|

— |

|

|

|

90,851 |

|

|

|

90,825 |

|

|

|

— |

|

|

|

90,825 |

|

Total |

|

$ |

188,842 |

|

|

$ |

(13,713 |

) |

|

$ |

175,129 |

|

|

$ |

205,215 |

|

|

$ |

(12,777 |

) |

|

$ |

192,438 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Liabilities assumed: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Investments in real estate, equity: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Mortgage payables |

|

$ |

19,525 |

|

|

$ |

620 |

|

|

$ |

20,145 |

|

|

$ |

19,565 |

|

|

$ |

620 |

|

|

$ |

20,185 |

|

Lease liabilities (3)(6) |

|

|

45,145 |

|

|

|

— |

|

|

|

45,145 |

|

|

|

44,958 |

|

|

|

— |

|

|

|

44,958 |

|

Subtotal |

|

|

64,670 |

|

|

|

620 |

|

|

|

65,290 |

|

|

|

64,523 |

|

|

|

620 |

|

|

|

65,143 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Investments in real estate from lending activities: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Other liabilities |

|

|

41 |

|

|

|

(41 |

) |

|

|

— |

|

|

|

41 |

|

|

|

(41 |

) |

|

|

— |

|

Lease liabilities (3)(6) |

|

|

380 |

|

|

|

— |

|

|

|

380 |

|

|

|

378 |

|

|

|

— |

|

|

|

378 |

|

Subtotal |

|

|

421 |

|

|

|

(41 |

) |

|

|

380 |

|

|

|

419 |

|

|

|

(41 |

) |

|

|

378 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Liabilities held for sale (7) |

|

|

3,181 |

|

|

|

— |

|

|

|

3,181 |

|

|

|

3,131 |

|

|

|

— |

|

|

|

3,131 |

|

Total |

|

$ |

68,272 |

|

|

$ |

579 |

|

|

$ |

68,851 |

|

|

$ |

68,073 |

|

|

$ |

579 |

|

|

$ |

68,652 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Total net investments in real estate and properties held for sale (8) |

|

$ |

120,570 |

|

|

|

|

|

$ |

106,278 |

|

|

$ |

137,142 |

|

|

|

|

|

$ |

123,786 |

|

||

Financing Receivables

Current market conditions have resulted in, and may continue to result in, a dislocation in capital markets, declining real estate values of certain asset classes and increased delinquencies and defaults, resulting in increased loan modifications, increased allowances for credit losses and an increased risk to borrowers of foreclosure actions. We routinely employ rigorous risk management and underwriting practices to proactively evaluate and maintain the credit quality of our CRE loan portfolio and work closely with our borrowers to mitigate potential losses.

The following table shows the activity in the allowance for credit losses for the three months ended March 31, 2026 and year ended December 31, 2025 (in thousands):

|

|

Three Months Ended March 31, 2026 |

|

|

Year Ended December 31, 2025 |

|

||

Allowance for credit losses at beginning of period |

|

$ |

20,398 |

|

|

$ |

32,847 |

|

(Reversal of) provision for credit losses |

|

|

(967 |

) |

|

|

(7,749 |

) |

Charge-offs |

|

|

— |

|

|

|

(4,700 |

) |

Allowance for credit losses at end of period |

|

$ |

19,431 |

|

|

$ |

20,398 |

|

During the three months ended March 31, 2026, we recorded a reversal of expected credit losses of $967,000, primarily attributable to improvements in projected macroeconomic factors during the quarter, offset by an increase in modeled credit risk of our loan portfolio.

At both March 31, 2026 and December 31, 2025, we were not required to individually evaluate any CRE loans for credit loss.

Credit quality indicators

Commercial Real Estate Loans

CRE loans are collateralized by a diversified mix of real estate properties and are assessed for credit quality based on the collective evaluation of several factors, including but not limited to: collateral performance relative to underwritten plan, time since origination, current implied and/or re-underwritten loan-to-collateral value ("LTV") ratios, loan structure and exit plan. Depending on the loan’s performance against these various factors, loans are rated on a scale from 1 to 5, with loans rated 1 representing loans with the highest credit quality and loans rated 5 representing the loans with the lowest credit quality. Loans are typically rated a 2 at origination. The factors evaluated provide general criteria to monitor credit migration in our loan portfolio; as such, a loan’s rating may improve or worsen, depending on new information received.

The criteria set forth below should be used as general guidelines and, therefore, not every loan will have all of the characteristics described in each category below.

Risk Rating |

|

Risk Characteristics |

|

|

|

1 |

|

• Property performance has surpassed underwritten expectations. |

|

|

• Occupancy is stabilized, the property has had a history of consistently high occupancy, and the property has a diverse and high quality tenant mix. |

|

|

|

2 |

|

• Property performance is consistent with underwritten expectations and covenants and performance criteria are being met or exceeded. |

|

|

• Occupancy is stabilized, near stabilized or is on track with underwriting. |

|

|

|

3 |

|

• Property performance lags behind underwritten expectations. |

|

|

• Occupancy is not stabilized and the property has some tenancy rollover. |

|

|

|

4 |

|

• Property performance significantly lags behind underwritten expectations. Performance criteria and loan covenants have required occasional waivers. |

|

|

• Occupancy is not stabilized and the property has a large amount of tenancy rollover. |

|

|

|

5 |

|

• Property performance is significantly worse than underwritten expectations. The loan is not in compliance with loan covenants and performance criteria and may be in default. Expected sale proceeds would not be sufficient to pay off the loan at maturity. |

|

|

• The property has a material vacancy rate and significant rollover of remaining tenants. |

|

|

• An updated appraisal is required upon designation and updated on an as-needed basis. |

All CRE loans are evaluated for any credit deterioration by debt asset management and certain finance personnel on at least a quarterly basis. Mezzanine loans and preferred equity investments may have experienced greater credit risks due to their nature as subordinated investments.

For the purpose of calculating the quarterly provision for credit losses under CECL, we pool CRE loans based on the underlying collateral property type and utilize a probability of default and loss given default methodology for approximately one year after which we immediately revert to a historical mean loss ratio.

Credit risk profiles of CRE loans at amortized cost were as follows (in thousands, except amounts in the footnotes):

|

|

Rating 1 |

|

|

Rating 2 |

|

|

Rating 3 |

|

|

Rating 4 |

|

|

Rating 5 |

|

|

Total (1) |

|

||||||

At March 31, 2026: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Whole loans |

|

$ |

28,154 |

|

|

$ |

1,323,792 |

|

|

$ |

455,317 |

|

|

$ |

380,288 |

|

|

$ |

5,614 |

|

|

$ |

2,193,165 |

|

Preferred equity investment |

|

|

— |

|

|

|

9,672 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

9,672 |

|

Total |

|

$ |

28,154 |

|

|

$ |

1,333,464 |

|

|

$ |

455,317 |

|

|

$ |

380,288 |

|

|

$ |

5,614 |

|

|

$ |

2,202,837 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

At December 31, 2025: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||

Whole loans |

|

$ |

28,137 |

|

|

$ |

938,416 |

|

|

$ |

470,871 |

|

|

$ |

377,904 |

|

|

$ |

5,614 |

|

|

$ |

1,820,942 |

|

Preferred equity investment |

|

|

— |

|

|

|

9,425 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

9,425 |

|

Total |

|

$ |

28,137 |

|

|

$ |

947,841 |

|

|

$ |

470,871 |

|

|

$ |

377,904 |

|

|

$ |

5,614 |

|

|

$ |

1,830,367 |

|

Credit risk profiles of CRE loans by origination year at amortized cost were as follows (in thousands, except amounts in footnotes):

|

|

2026 |

|

|

2025 (1) |

|

|

2024 (2) |

|

|

2023 |

|

|

2022 |

|

|

Prior |

|

|

Total (3) |

|

|||||||

At March 31, 2026: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Whole loans: (4) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Rating 1 |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

28,154 |

|

|

$ |

28,154 |

|

Rating 2 |

|

|

406,943 |

|

|

|

625,955 |

|

|

|

27,021 |

|

|

|

29,359 |

|

|

|

— |

|

|

|

234,514 |

|

|

|

1,323,792 |

|

Rating 3 |

|

|

16,605 |

|

|

|

10,286 |

|

|

|

— |

|

|

|

— |

|

|

|

202,888 |

|

|

|

225,538 |

|

|

|

455,317 |

|

Rating 4 |

|

|

— |

|

|

|

139,700 |

|

|

|

87,786 |

|

|

|

15,996 |

|

|

|

91,718 |

|

|

|

45,088 |

|

|

|

380,288 |

|

Rating 5 |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

5,614 |

|

|

|

5,614 |

|

Total whole loans |

|

|

423,548 |

|

|

|

775,941 |

|

|

|

114,807 |

|

|

|

45,355 |

|

|

|

294,606 |

|

|

|

538,908 |

|

|

|

2,193,165 |

|

Preferred equity investment (rating 2) |

|

|

— |

|

|

|

9,672 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

9,672 |

|

Total loans |

|

$ |

423,548 |

|

|

$ |

785,613 |

|

|

$ |

114,807 |

|

|

$ |

45,355 |

|

|

$ |

294,606 |

|

|

$ |

538,908 |

|

|

$ |

2,202,837 |

|

Current Period Gross Write-Offs |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

2025 (1) |

|

|

2024 (2) |

|

|

2023 |

|

|

2022 |

|

|

2021 |

|

|

Prior |

|

|

Total (3) |

|

|||||||

At December 31, 2025: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Whole loans: (4) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||

Rating 1 |

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

— |

|

|

$ |

28,137 |

|

|

$ |

— |

|

|

$ |

28,137 |

|

Rating 2 |

|

|

649,712 |

|

|

|

22,249 |

|

|

|

49,376 |

|

|

|

— |

|

|

|

203,263 |

|

|

|

13,816 |

|

|

|

938,416 |

|

Rating 3 |

|

|

10,283 |

|

|

|

— |

|

|

|

— |

|

|

|

235,271 |

|

|

|

214,356 |

|

|

|

10,961 |

|

|

|

470,871 |

|

Rating 4 |

|

|

137,906 |

|

|

|

87,370 |

|

|

|

15,991 |

|

|

|

91,675 |

|

|

|

— |

|

|

|

44,962 |

|

|

|

377,904 |

|

Rating 5 |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

5,614 |

|

|

|

5,614 |

|

Total whole loans |

|

|

797,901 |

|

|

|

109,619 |

|

|

|

65,367 |

|

|

|

326,946 |

|

|

|

445,756 |

|

|

|

75,353 |

|

|

|

1,820,942 |

|

Preferred equity investment (rating 2) |

|

|

9,425 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

9,425 |

|

Total loans |

|

$ |

807,326 |

|

|

$ |

109,619 |

|

|

$ |

65,367 |

|

|

$ |

326,946 |

|

|

$ |

445,756 |

|

|

$ |

75,353 |

|

|