Exhibit 99.1

| Hogan Lovells US LLP is a limited liability partnership registered in the District of Columbia. Hogan Lovells refers to the international legal practice comprising Hogan Lovells US LLP, Hogan Lovells International LLP, Hogan Lovells Worldwide Group (a Swiss Verein), and their affiliated businesses with offices in: Abu Dhabi Alicante Amsterdam Baltimore Beijing Berlin Boulder Brussels Caracas Colorado Springs Denver Dubai Dusseldorf Frankfurt Hamburg Hanoi Ho Chi Minh City Hong Kong Houston London Los Angeles Madrid Miami Milan Moscow Munich New York Northern Virginia Paris Philadelphia Prague Rome San Francisco Shanghai Silicon Valley Singapore Tokyo Ulaanbaatar Warsaw Washington DC Associated offices: Budapest Jeddah Riyadh Zagreb Hogan Lovells US LLP Columbia Square 555 Thirteenth Street, NW Washington, DC 20004 T +1 202 637 5600 F +1 202 637 5910 www.hoganlovells.com Douglas A. Fellman Partner 202.637.5714 douglas.fellman@hoganlovells.com April 20, 2026 BY ECF The Honorable Margo K. Brodie United States District Judge Eastern District of New York United States Courthouse 225 Cadman Plaza East Brooklyn, NY 11201 RE: SEC v. GPB Capital Holdings LLC, et al., No. 21-cv-00583-MKB-VMS Dear Chief Judge Brodie: We represent the Court-appointed receiver, Joseph T. Gardemal III, in the above-referenced matter. Pursuant to Paragraph 45 of this Court’s December 8, 2023 order establishing the Receivership in this matter, we are respectfully submitting Receiver Joseph T. Gardemal III’s Sixth Status Report, for the Period January 1, 2026, through March 31, 2026 (“Sixth Status Report”). The Sixth Status Report is attached to this letter as Exhibit A. Respectfully submitted, HOGAN LOVELLS US LLP By: _________________ Douglas A. Fellman Counsel to Joseph T. Gardemal III, Receiver Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 1 of 27 PageID #: 12726 |

| Exhibit A Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 2 of 27 PageID #: 12727 |

| -1- UNITED STATES DISTRICT COURT EASTERN DISTRICT OF NEW YORK SECURITIES AND EXCHANGE COMMISSION, Plaintiff, -against-GPB CAPITAL HOLDINGS, LLC; ASCENDANT CAPITAL, LLC; ASCENDANT ALTERNATIVE STRATEGIES, LLC; DAVID GENTILE; JEFFRY SCHNEIDER; and JEFFREY LASH, Defendants. : : : : : : : : : : : : : : : : : 21-cv-00583-MKB-VMS ______________________________________________ RECEIVER JOSEPH T. GARDEMAL III’S SIXTH STATUS REPORT, FOR THE PERIOD JANUARY 1, 2026, THROUGH MARCH 31, 2026 Joseph T. Gardemal III was appointed the Receiver (“Receiver”) of GPB Capital Holdings, LLC (“GPB” or the “Company”) and the Receivership Entities1 pursuant to the Order Appointing Receiver and Imposing Litigation Injunction, entered on December 8, 2023. See SEC v. GPB Capital Holdings, LLC, et al., No. 21-cv-00583 (E.D.N.Y. Dec. 8, 2023), Dkt. No. 187 (the 1 The “Receivership Entities” are Armada Waste Management GP, LLC (fka GPB Waste Management GP, LLC); Armada Waste Management, LP (fka GPB Waste Management, LP); Armada WM SLP, LLC (fka GPB WM SLP, LLC); GPB Auto SLP, LLC; GPB Automotive Income Fund, LTD.; GPB Automotive Income Sub-Fund, LTD.; GPB Automotive Portfolio, LP; GPB Capital Holdings, LLC; GPB Cold Storage, LP; GPB H2 SLP, LLC; GPB H3 SLP, LLC; GPB Holdings II, LP; GPB Holdings III GP, LLC; GPB Holdings III, LP; GPB Holdings Qualified, LP; GPB Holdings, LP; GPB NYC Development, LP; GPB NYCD SLP LLC; GPB SLP, LLC; and Highline Management Inc. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 3 of 27 PageID #: 12728 |

| -2- “Receivership Order”). Mr. Gardemal submits this Sixth Status Report (“Sixth Status Report” or “Report”) pursuant to paragraph 45 of the Receivership Order. By way of summary, the Receivership Estate consists of, among other things, the Receivership Entities and their holdings, including all assets, property, rights, and interests owned or controlled by those entities. As of March 31, 2026, the current cash2 balance of the Receivership Estate was $704,954,050.3 This Report, which covers the period from January 1, 2026, through March 31, 2026, provides an accounting of the Receivership Estate and discusses certain actions the Receiver has taken or will take pursuant to the Receivership Order to prudently manage the assets entrusted to him. I. Background A. Procedural History On February 4, 2021, the United States Securities and Exchange Commission (the “SEC”) filed a civil law enforcement action against GPB, Ascendant Capital, LLC (“Ascendant Capital”), Ascendant Alternative Strategies, LLC (“AAS”), David Gentile (“Gentile”), Jeffry Schneider (“Schneider”), and Jeffrey Lash (“Lash”) (collectively, the “Defendants”) in the United States District Court for the Eastern District of New York (the “SEC Complaint”). 4 2 For the purposes of this Report, the term “cash” refers to both cash and cash equivalents, unless otherwise specified. Cash equivalents are short-term, highly liquid investments that are readily convertible to known amounts of cash (e.g., treasury bills, commercial paper, and money market funds). Cash reported at Receivership Entities does not include cash at portfolio companies or non-reporting entities of approximately $7.6 million. 3 All financial data is calculated as of March 31, 2026. 4 Complaint, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 1. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 4 of 27 PageID #: 12729 |

| -3- The SEC Complaint alleged that the Defendants perpetrated a fraudulent securities scheme that raised more than $1.7 billion for at least five limited partnership funds from approximately 17,000 retail investors.5 The limited partnership funds acquired various portfolio companies (the “GPB Portfolio Companies”) that were operated by GPB.6 Specifically, the SEC Complaint alleged that while GPB had told investors it consistently paid an 8% annualized distribution, as well as periodic “special distributions” ranging from 0.5% to 3%, from the funds generated by the operations of the GPB Portfolio Companies, in reality, GPB used investor funds to pay distributions when the operating funds were insufficient.7 Further, the SEC Complaint alleged that the Defendants concealed the truth from investors by manipulating financial statements for two of the limited partnership funds to give the false appearance that the portfolio company income was sufficient to fund the investor distributions.8 The SEC Complaint also alleged that GPB and Ascendant Capital deceived investors about fees and compensation paid to Gentile, Schneider, and Ascendant Capital, and failed to disclose Gentile’s and Schneider’s conflicts of interest in executing acquisitions because of undisclosed fees. 9 Finally, the SEC Complaint alleged that GPB impeded former employees from communicating directly with the SEC and retaliated against a known whistleblower who raised concerns about GPB’s use of investor funds to make distribution payments to investors.10 5 SEC Complaint ¶¶ 2-3. 6 SEC Complaint ¶ 2. 7 SEC Complaint ¶¶ 2-4. 8 SEC Complaint ¶ 4. 9 SEC Complaint ¶ 5. 10 SEC Complaint ¶ 7. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 5 of 27 PageID #: 12730 |

| -4- On the basis of this alleged conduct, the SEC charged that the Defendants (other than Lash) had violated antifraud provisions of Section 17(a) of the Securities Act of 1933 (the “Securities Act”), and Section 10(b) and Rule 10b-5 of the Securities Exchange Act of 1934 (the “Exchange Act”). 11 The SEC also alleged that GPB and Gentile violated antifraud provisions of Sections 206(1) and 206(2) of the Investment Advisers Act of 1940 (the “Advisers Act”), and that GPB violated Section 206(4) of the Advisers Act. 12 The SEC also alleged that GPB violated whistleblower-protection and reporting and disclosure requirements under Sections 21F and 12(g) of the Exchange Act.13 The SEC further alleged that Gentile and Schneider aided and abetted certain antifraud violations by the entity defendants pursuant to Section 15(b) of the Securities Act, and Section 20(e) of the Exchange Act.14 Finally, the SEC alleged various aiding and abetting antifraud violations by Lash.15 The SEC sought permanent injunctions against each Defendant, disgorgement of Defendants’ ill-gotten gains, together with prejudgment interest, and civil penalties.16 On February 4, 2021, the same day that the SEC filed its civil enforcement action, the United States District Court for the Eastern District of New York unsealed a grand jury indictment charging Gentile, Schneider, and Lash with conspiracy to commit securities fraud, conspiracy to commit wire fraud, and securities fraud, and Gentile and Lash with wire fraud (the “Indictment”). 17 11 SEC Complaint ¶¶ 9-14. 12 SEC Complaint ¶¶ 9, 12. 13 SEC Complaint ¶ 9. 14 SEC Complaint ¶¶ 12-13. 15 SEC Complaint ¶ 14. 16 SEC Complaint ¶ 17. 17 See Unsealing Order, USA v. Gentile, et. al., Case No. 21-cr-00054 (E.D.N.Y.), ECF No. 5; Indictment, USA v. Gentile, et. al., Case No. 21-cr-00054 (E.D.N.Y.), ECF No. 1. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 6 of 27 PageID #: 12731 |

| -5- Specifically, the Indictment alleged that between 2015 and 2018, Gentile, Schneider, Lash, and others engaged in a scheme to defraud investors and prospective investors in GPB investment funds through material misrepresentations and omissions relating to, among other things: (a) the source of funds used to pay monthly distribution payments to investors in several of the GPB investment funds, including GPB Holdings, LP, (“Holdings I”), and GPB Holdings II, LP (“Holdings II”), and (b) the revenue generated by Holdings I in 2014 and GPB Automotive Portfolio, LP (“Automotive Portfolio”) in 2015.18 The Indictment alleged that in furtherance of this fraudulent scheme, Gentile, Schneider, Lash, and others made material misrepresentations and omissions to investors and prospective investors in certain of the GPB investment funds. 19 On February 8, 2021, the SEC moved for the appointment of an independent monitor (the “Monitor”) to oversee the operations of GPB and its affiliates.20 On February 12, 2021, now-Receiver Joseph T. Gardemal III was appointed as the Monitor over GPB pursuant to an order entered by the Honorable Margo K. Brodie, United States District Judge for the Eastern District of New York (the “Initial Order”).21 GPB consented to the Initial Order. 22 On April 14, 2021, the Initial Order was amended (the “Amended Order,” and together with the Initial Order, the “Monitor Order”). 18 Indictment ¶ 15. 19 Indictment ¶ 16. 20 Plaintiff’s Application for Order to Show Cause, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 10. 21 Order, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 23. 22 See SEC’s Letter re: Application for Order to Show Cause to inform Court of parties’ agreement to terms of proposed Order Appointing Monitor, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 21. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 7 of 27 PageID #: 12732 |

| -6- The Monitor Order provided that, among other things, the Monitor had the power to approve or disapprove: any proposed material corporate transactions by GPB, Highline Management, Inc. (“Highline”), the GPB Funds, 23 or the GPB Portfolio Companies; 24 any extension of credit by GPB, Highline, the GPB Funds, or the GPB Portfolio Companies; any material change in business strategy by GPB, Highline, the GPB Funds, or the GPB Portfolio Companies; any material change to compensation of any executive officer, affiliate, or related party of GPB, Highline, the GPB Funds, or the GPB Portfolio Companies; any retention by GPB, Highline, the GPB Funds, or the GPB Portfolio Companies of any management-level professional; any decision to resume distributions to investors in any of the GPB Funds, consistent with the investment objectives of the GPB Funds; and any decision to prepare for, file, or cause to be filed, any bankruptcy or receivership petition for GPB or its affiliates.25 The Monitor Order also provided that if the Monitor believes GPB is in some way not materially in compliance with the terms of this Order, upon notice of noncompliance to GPB, GPB shall have ten business days in which to cure any claimed material noncompliance (the “Cure Period”) and that, “[i]f GPB does not comply with the above provisions and does not make requested changes within the Cure Period, upon motion of the SEC resulting in a Court Order, the Monitorship shall convert to a Receivership.”26 23 As defined in Exhibit B to the Amended Order, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 39. 24 As defined in Exhibit A to the Amended Order, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 39. 25 Amended Order, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 39 ¶ 6. 26 Amended Order, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 39 ¶ 21. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 8 of 27 PageID #: 12733 |

| -7- B. Conversion from Monitorship to Receivership On May 29, 2022, Mayer Brown LLP, in its capacity as counsel to GPB, informed the Monitor that Gentile had documents delivered to the Company reflecting that Gentile had purported to take actions, as of May 27, 2022, (i) expanding the number of managers of the Company from one to four and appointing each of Rick Murphy, Michael Fasano, and Matt Judkin as managers, and (ii) amending the limited liability company agreement of the Company to, among other things, provide for new compensation arrangements with respect to non-employee managers (collectively, the “May 27, 2022 Purported Actions”).27 On May 31, 2022, the Monitor provided formal notice to GPB that the May 27, 2022 Purported Actions, among other things, violated Sections 6(d) and 6(e) of the Monitor Order (the “Material Non-Compliance”), which meant that the Company had ten business days in which to cure the Material Non-Compliance, and that if such cure did not occur within ten business days, then the Monitorship would be converted to a Receivership pursuant to Sections 20 and 21 of the Monitor Order. 28 27 SEC’s Memorandum of Law in Support of Its Motion for an Order Appointing a Receiver and Imposing a Litigation Injunction, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 89 at 5; Declaration of the Monitor, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 90 ¶ 18. 28 Declaration of the Monitor, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 90 ¶ 22. See also Amended Order, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 39 ¶ 20 (If the Monitor believes GPB is in some way not materially in compliance with the terms of this Order, upon notice of noncompliance to GPB, GPB shall have 10 business days in which to cure any claimed material noncompliance (the “Cure Period”)); ¶ 21 (“If GPB does not comply with the above provisions and does not make requested changes within the Cure Period, upon motion of the SEC resulting in a Court Order, the Monitorship shall convert to a receivership. GPB shall be afforded an opportunity to oppose any such application by the SEC before conversion to a receivership.”). Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 9 of 27 PageID #: 12734 |

| -8- On June 13, 2022, following the notice provided by the Monitor and pursuant to the remedies provided for in Section 21 of the Monitor Order, the SEC filed a motion to request the conversion of the Monitorship to a Receivership as a result of the continuing violations of the Monitor Order. 29 On July 1, 2022, GPB filed a memorandum in response to the SEC’s motion for the appointment of a receiver, stating that the Company consented to the relief sought by the SEC.30 On July 28, 2023, the Honorable Vera M. Scanlon, United States Magistrate Judge for the Eastern District of New York, issued a Report and Recommendation that recommended that the SEC’s motion to convert the Monitorship to a Receivership and for the imposition of a litigation injunction be granted. 31 On September 8, 2023, Gentile and Schneider filed objections to Magistrate Judge Scanlon’s Report and Recommendation with Chief Judge Margo K. Brodie, the District Court Judge overseeing the SEC case.32 Two weeks later, on September 22, 2023, the SEC and GPB filed responses to the objections, in which they asked Chief Judge Brodie to reject the objections and accept Magistrate Judge Scanlon’s recommendations.33 29 Plaintiff’s Application for Order to Show Cause, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 88. 30 Defendant GPB’s Memorandum in Response to the SEC’s Motion for an Order Appointing a Receiver and Imposing a Litigation Injunction, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 101. 31 Report and Recommendation, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 157 at 33. 32 Defendant’s Objection, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 167; Defendant’s Objection, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 168. 33 Notice by SEC, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 170; Notice by GPB, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 171. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 10 of 27 PageID #: 12735 |

| -9- On December 7, 2023, Chief Judge Brodie entered an Order adopting the Report and Recommendation. 34 The next day, Chief Judge Brodie entered the Receivership Order, which (i) converted the Monitorship into a Receivership and converted Mr. Gardemal’s role from Monitor to Receiver over GPB and related entities, and (ii) imposed a litigation injunction.35 On December 12, 2023, Gentile, and on December 13, 2023, Schneider and Ascendant Capital, appealed the Receivership Order to the United States Court of Appeals for the Second Circuit.36 On December 14, 2023, upon motion by Gentile, Schneider and Ascendant Capital, Chief Judge Brodie temporarily stayed the Receivership Order so that the parties could seek a stay pending appeal from the Second Circuit.37 On December 21, 2023, Gentile, Schneider and Ascendant Capital filed a motion to stay the Receivership Order with the Second Circuit, which the SEC did not oppose.38 The Second Circuit entered its own stay on May 14, 2024.39 While the appeal of the Receivership Order was pending, the criminal trial of Gentile and Schneider commenced on June 12, 2024. On August 1, 2024, following an eight-week jury trial, Gentile and Schneider were found guilty of securities fraud, conspiracy to commit securities fraud, 34 Memorandum & Order, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 186. 35 Receivership Order, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 187. 36 Notice of Appeal, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 188; Notice of Appeal, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 191. 37 Order, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. N/A (December 14, 2023). 38 Defendants’ Unopposed Motion to Stay Order Pending Appeal, SEC v. GPB Capital Holdings, LLC, No. 23- 08010 (2d Cir.), ECF No. 18. 39 Order, SEC v. GPB Capital Holdings, LLC, No. 23-08010 (2d Cir.), ECF No. 71. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 11 of 27 PageID #: 12736 |

| -10- and conspiracy to commit wire fraud.40 Gentile was also convicted on two counts of wire fraud.41 On May 9, 2025, Judge Rachel P. Kovner sentenced Gentile and Schneider principally to seven years in prison and six years in prison, respectively.42 On November 14, 2025, Gentile surrendered to the Bureau of Prisons to serve his sentence.43 However, on November 26, 2025, President Donald J. Trump issued an executive grant of clemency, which resulted in a commutation of Gentile’s sentence with “[n]o further fines, restitution, probation, or other conditions.”44 On January 14, 2026, Schnieder surrendered to the Bureau of Prisons to serve his sentence.45 On August 30, 2024, in light of the guilty verdicts against Gentile and Schneider, the SEC filed a motion in the Second Circuit requesting that the Court lift the stay of the Receivership Order, which Gentile and Schneider opposed.46 On September 17, 2024, the Second Circuit referred the SEC’s motion to lift the stay to the panel of Second Circuit judges assigned to 40 Jury Verdict, USA v. Gentile, et. al., Case No. 21-cr-00054 (E.D.N.Y.), ECF No. 472; Jury Verdict, USA v. Gentile, et. al., Case No. 21-cr-00054 (E.D.N.Y.), ECF No. 473. 41 USA v. Gentile, et. al., Case No. 21-cr-00054 (E.D.N.Y.), ECF No. 472. 42 Judgment, USA v. Gentile, et. al., Case No. 21-cr-00054 (E.D.N.Y.), ECF Nos. 596, 598. 43 See November 21, 2025 Letter to Court from A. Riviere-Badell, USA v. Gentile, et. al., Case No. 21-cr-00054 (E.D.N.Y.), ECF No. 655. 44 Donald J. Trump, “Executive Grant of Clemency – David Gentile” (President of the United States, Washington, DC, November 26, 2025). 45 See January 15, 2026 Letter to Court from G. Colton, USA v. Gentile, et. al., Case No. 21-cr-00054 (E.D.N.Y.), ECF No. 663. 46 SEC’s Motion to Lift Stay of the Orders Appointing a Receiver, SEC v. GPB Capital Holdings, LLC, No. 23- 08010 (2d Cir.), ECF No. 76; Opposition to Motion, SEC’s Motion to Lift Stay of the Orders Appointing a Receiver, SEC v. GPB Capital Holdings, LLC, No. 23-08010 (2d Cir.), ECF No. 79; Letter Regarding Joining in Support of Opposition, SEC v. GPB Capital Holdings, LLC, No. 23-08010 (2d Cir.), ECF No. 80. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 12 of 27 PageID #: 12737 |

| -11- determine the merits of the appeal and directed expedited oral argument, which was held on November 6, 2024.47 On December 3, 2024, the Second Circuit affirmed the Receivership Order and lifted the stay, thereby requiring the Receiver to implement the receivership pursuant to the Receivership Order.48 On April 8, 2025, the District Court approved the Receiver’s proposed Distribution Plan in its entirety, which the Receiver had previously submitted to the Court as required by the Receivership Order. 49 II. Summary of Operations for the Receiver50 In the first quarter of 2026, the Receiver has continued to focus on and prioritize the protection, preservation, and maximization of distributable proceeds for investors, while also complying with the Receivership Order and the Distribution Plan (the “Plan”). This includes adhering to provisions related to, among other things, accounting, banking, insurance, asset control, and litigation management, as well as implementation of the Distribution Plan. The 47 Motion Order, SEC’s Motion to Lift Stay of the Orders Appointing a Receiver, SEC v. GPB Capital Holdings, LLC, No. 23-08010 (2d Cir.), ECF No. 82; Motion Order, SEC’s Motion to Lift Stay of the Orders Appointing a Receiver, SEC v. GPB Capital Holdings, LLC, No. 23-08010 (2d Cir.), ECF No. 92. 48 Summary Order and Judgment, SEC’s Motion to Lift Stay of the Orders Appointing a Receiver, SEC v. GPB Capital Holdings, LLC, No. 23-08010 (2d Cir.), ECF No. 93. 49 Memorandum and Order, SEC v. GPB Capital Holdings, LLC, et. al., Case No. 21-cv-00583 (E.D.N.Y.), ECF No. 271 (April 8, 2025). 50 Unless otherwise indicated, capitalized terms not defined in this Sixth Status Report have the meaning given to such terms in the Distribution Plan. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 13 of 27 PageID #: 12738 |

| -12- following is a non-exhaustive summary of the actions taken by the Receiver between January 1, 2026, and March 31, 2026: 1) Continued to analyze and respond to numerous inquiries from investors and investor representatives regarding, among other matters, distributions, the claims process, check issues, transfers, and settlements. 2) Managed the claims process established by the Distribution Plan by (i) reviewing newly filed late claims, including claims from various non-investor claimants, (ii) preparing responses, requests for information, and objections to or denials of claims, (iii) preparing responses for a separate claims process for investors in the Cayman-based GPB Automotive Income Fund, Ltd. (“AIF”), (iv) continuing to identify AIF investors who are represented by banks and nominees, and (v) working with AIF directors on the claims process for offshore funds. 3) Continued the development and implementation of transfer procedures and related documentation to facilitate investor-broker settlements requiring partnership interest transfers by (i) setting a deadline for transfer submissions resulting in more than fifty additional submissions, (ii) reviewing all transfer-related documentation for completeness and approval, (iii) continued attention to transfer-specific questions from investors and brokers, and (iv) developing procedures for uncompleted transfers. 4) Continued the development and implementation of distribution procedures for investor-broker settlements that did not require a transfer of partnership interests to prevent “double recoveries” by (i) setting a deadline for submission of settlement information, and (ii) analyzing circumstances where investor-broker settlements covered multiple investments, including GPB funds. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 14 of 27 PageID #: 12739 |

| -13- 5) Continued determination of accounting/tax allocations for investors in transferred accounts. 6) Continued to review and facilitate transfers related to a fund-of-funds that invested in GPB partnerships by (i) verifying and confirming accuracy of fund-of-funds investor data, (ii) communicating status updates to fund-of-funds investors, and (iii) preparing forms and other documentation necessary to facilitate potential future distributions by the appropriate GPB partnerships directly to the fund-of-fund investors. 7) Filed a motion seeking preliminary approval of, and authorization to enter into a settlement agreement on behalf of GPB related to claims asserted in a significant class action lawsuit, and responded to objections made by various parties to such preliminary approval and authorization. 8) Continued to manage the distribution check cashing process, by reissuing checks for individuals with address changes, reissuing checks for non-US bank custodians, and assessing voided checks, among other issues. Additionally, developed and implemented procedures to verify the information of investors whose checks remained uncashed. 9) Continued to revise and update the FAQ and Letters to Investors sections on the Claims Agent website to reflect updated guidance and information on the distribution process including information related to (i) potential timing of distributions, (ii) potential settlement of a significant class-action lawsuit, (iii) claim notice forms related to proposed class action settlements in lawsuits brought on behalf of certain investors, and (iv) information about settlements, transfers, and distribution of tax forms. 10) Continued to actively manage the Receivership Estate’s portfolio of Treasury Bill investments, which has a current annual yield to maturity of approximately 3.65%. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 15 of 27 PageID #: 12740 |

| -14- 11) Established three new interest-bearing bank accounts yielding approximately 3.4% on an annualized basis to further diversify Receivership Assets and mitigate risk. 12) Prepared and issued all vendor IRS Form 1099s for fiscal year 2025. 13) Consolidated portfolio company tax preparation services with a single accounting firm, increasing efficiency and decreasing costs. 14) Reduced letters of credit for GPB Automotive Portfolio, LP by $250,000, freeing up previously restricted cash. 15) Continued work with outside counsel to prosecute action in Bankruptcy Court in Arkansas over a judgment that GPB Holdings II, LP negotiated as part of a settlement with a former portfolio company. 16) Continued work with outside counsel to support and advance active litigation efforts on behalf of the Receivership Estate. 17) Responded to extensive document and information requests from the New York Attorney General (“NYAG”) in connection with New York State’s action against GPB and other defendants, including production of more than one million pages of documents. 18) Prepared and filed proposed amicus curiae brief on behalf of the Receiver in support of GPB Capital’s motion to dismiss the NYAG’s enforcement action against it on the grounds that the action is duplicative of the SEC’s further-progressed enforcement action and of the relief already being achieved for investors by the federal Receivership. The Receiver’s proposed amicus curiae brief explained that active litigation of the NYAG’s duplicative action against GPB Capital would ultimately harm investors by unnecessarily diminishing the funds available for distribution to them and by delaying future distributions of available funds. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 16 of 27 PageID #: 12741 |

| -15- 19) Began facilitating the realization of approximately $600,000 related to the shutdown of AMR Automotive Reinsurance Ltd. (“AMR Reinsurance”). 20) Continued to manage FINRA arbitration subpoenas and document requests. 21) Continued efforts to secure the release of $100,000 from escrow related to the procurement of tax clearance certificates from a 2020 sale of automotive dealerships. 22) Continued work on comments related to claims notice forms for class action settlements in lawsuits brought on behalf of certain investors related to Receivership Entities. 23) Continued work on motions and responses related to actions taken by certain state attorneys general and securities commissions. 24) Reviewed and reconciled all vendor bills to comply with the OCP billing and review process. 25) Continued review and attend to advancement demands from relevant parties consistent with the procedures established by the Delaware courts and the Eastern District of New York. 26) Continued to wind down the Prime Automotive Group 401(k) plan. 27) Continued to evaluate and terminate unnecessary vendor relationships to reduce Receivership expenses. 28) Reduced overall payroll expenses and increased workforce efficiency through reductions in force, compensation reductions, and workload transitions. 29) Negotiated new insurance policies on behalf of the Receivership Estate, including general liability, cyber security, and property and casualty. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 17 of 27 PageID #: 12742 |

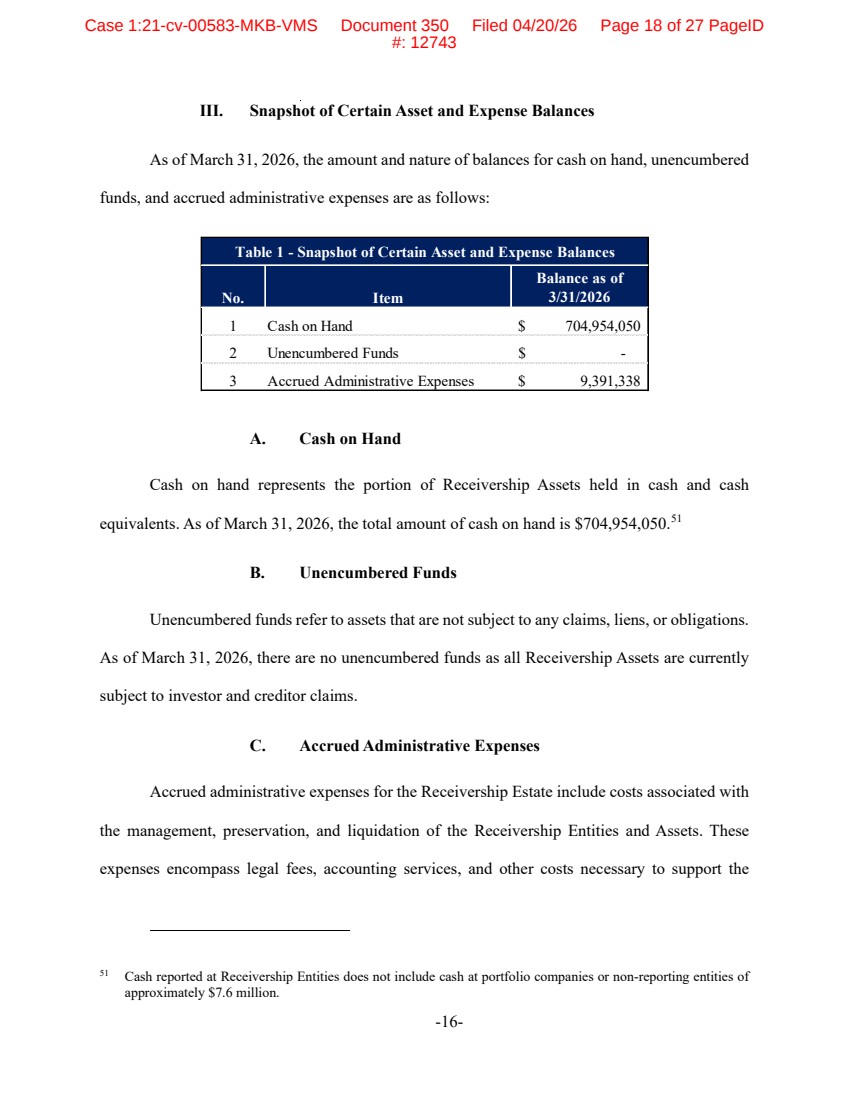

| -16- III. Snapshot of Certain Asset and Expense Balances As of March 31, 2026, the amount and nature of balances for cash on hand, unencumbered funds, and accrued administrative expenses are as follows: A. Cash on Hand Cash on hand represents the portion of Receivership Assets held in cash and cash equivalents. As of March 31, 2026, the total amount of cash on hand is $704,954,050.51 B. Unencumbered Funds Unencumbered funds refer to assets that are not subject to any claims, liens, or obligations. As of March 31, 2026, there are no unencumbered funds as all Receivership Assets are currently subject to investor and creditor claims. C. Accrued Administrative Expenses Accrued administrative expenses for the Receivership Estate include costs associated with the management, preservation, and liquidation of the Receivership Entities and Assets. These expenses encompass legal fees, accounting services, and other costs necessary to support the 51 Cash reported at Receivership Entities does not include cash at portfolio companies or non-reporting entities of approximately $7.6 million. No. Item Balance as of 3/31/2026 1 Cash on Hand $ 704,954,050 2 Unencumbered Funds $ - 3 Accrued Administrative Expenses $ 9,391,338 Table 1 - Snapshot of Certain Asset and Expense Balances Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 18 of 27 PageID #: 12743 |

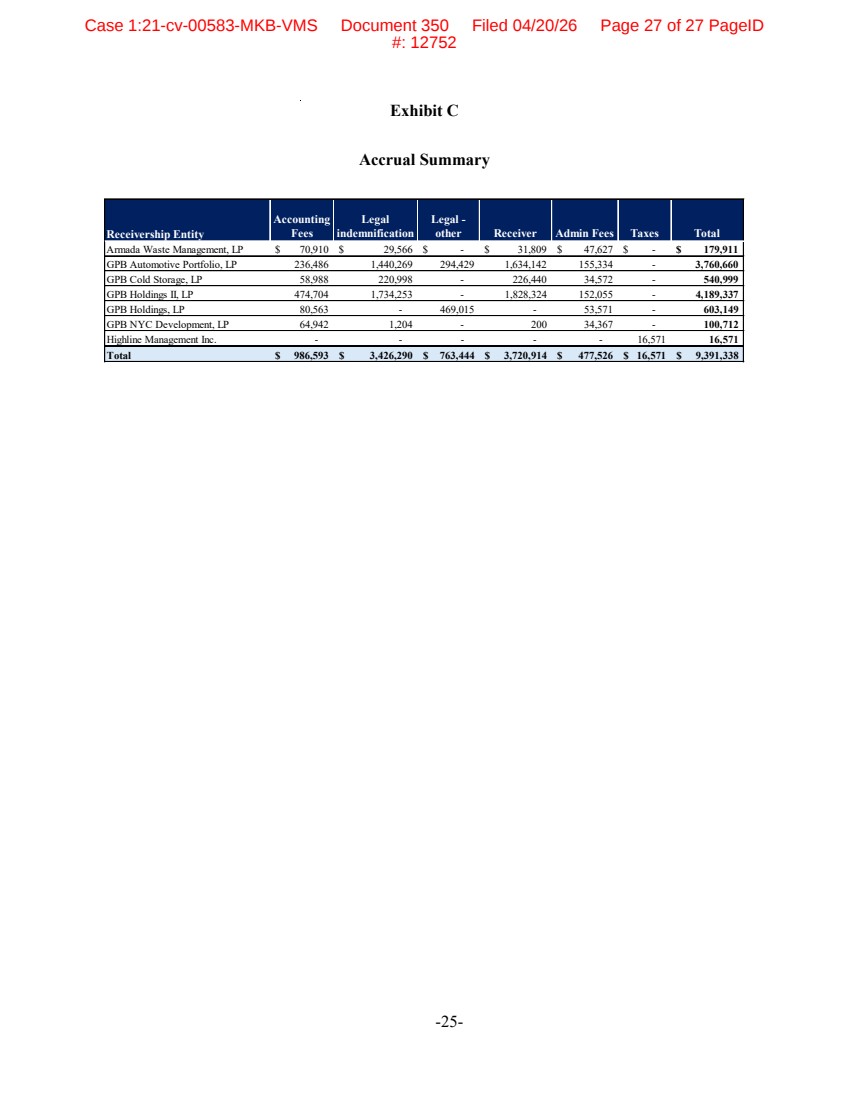

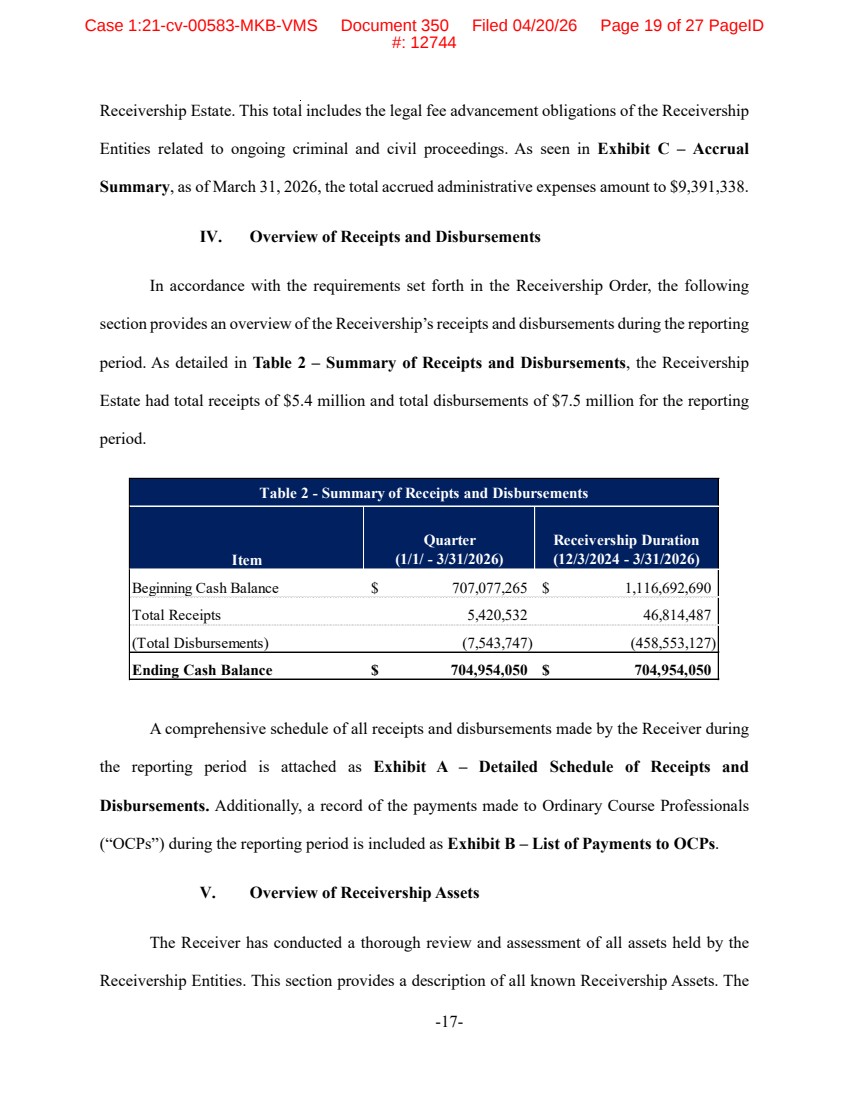

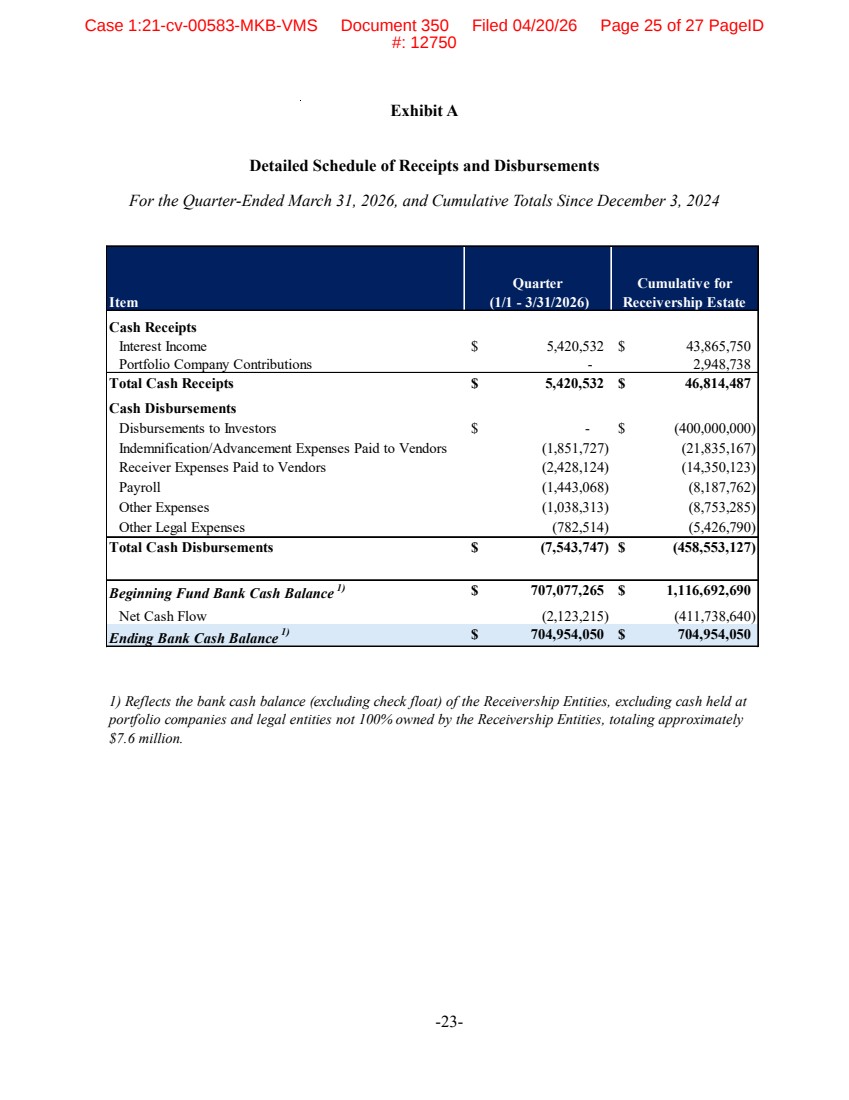

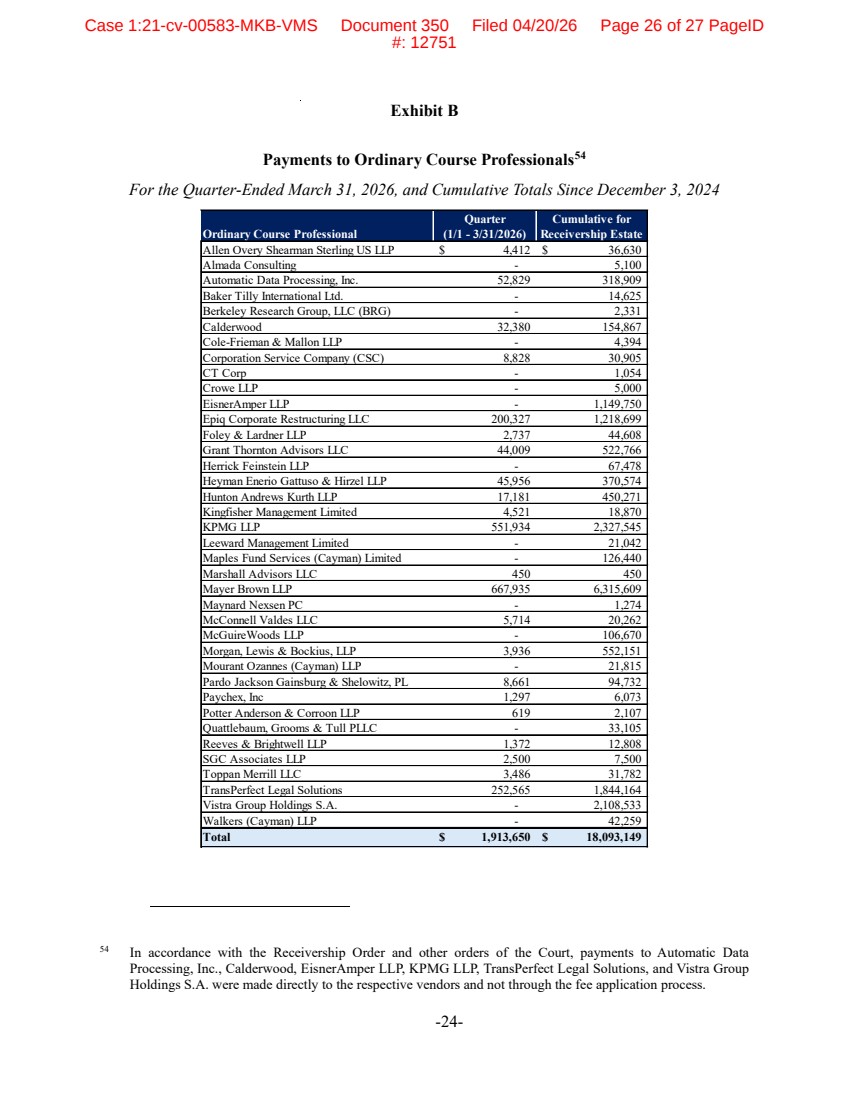

| -17- Receivership Estate. This total includes the legal fee advancement obligations of the Receivership Entities related to ongoing criminal and civil proceedings. As seen in Exhibit C – Accrual Summary, as of March 31, 2026, the total accrued administrative expenses amount to $9,391,338. IV. Overview of Receipts and Disbursements In accordance with the requirements set forth in the Receivership Order, the following section provides an overview of the Receivership’s receipts and disbursements during the reporting period. As detailed in Table 2 – Summary of Receipts and Disbursements, the Receivership Estate had total receipts of $5.4 million and total disbursements of $7.5 million for the reporting period. A comprehensive schedule of all receipts and disbursements made by the Receiver during the reporting period is attached as Exhibit A – Detailed Schedule of Receipts and Disbursements. Additionally, a record of the payments made to Ordinary Course Professionals (“OCPs”) during the reporting period is included as Exhibit B – List of Payments to OCPs. V. Overview of Receivership Assets The Receiver has conducted a thorough review and assessment of all assets held by the Receivership Entities. This section provides a description of all known Receivership Assets. The Item Quarter (1/1/ - 3/31/2026) Receivership Duration (12/3/2024 - 3/31/2026) Beginning Cash Balance $ 707,077,265 $ 1,116,692,690 Total Receipts 5,420,532 46,814,487 (Total Disbursements) (7,543,747) (458,553,127) Ending Cash Balance $ 704,954,050 $ 704,954,050 Table 2 - Summary of Receipts and Disbursements Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 19 of 27 PageID #: 12744 |

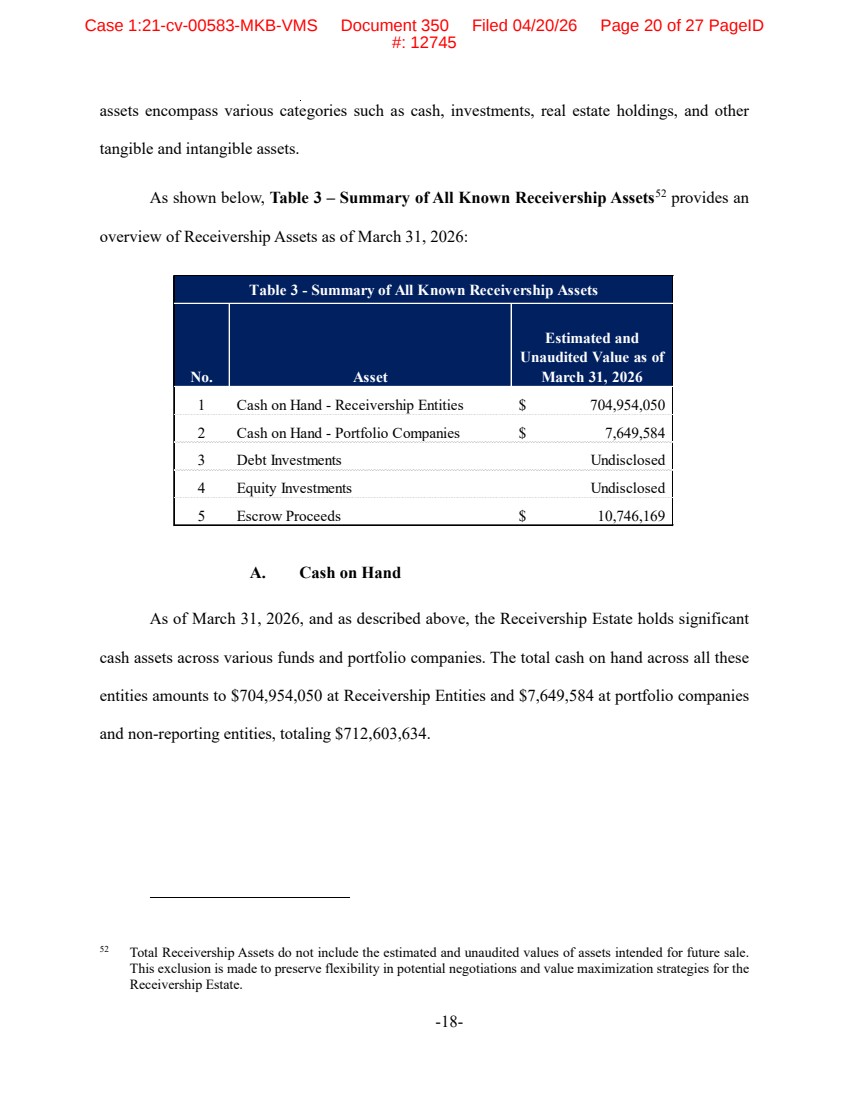

| -18- assets encompass various categories such as cash, investments, real estate holdings, and other tangible and intangible assets. As shown below, Table 3 – Summary of All Known Receivership Assets52 provides an overview of Receivership Assets as of March 31, 2026: A. Cash on Hand As of March 31, 2026, and as described above, the Receivership Estate holds significant cash assets across various funds and portfolio companies. The total cash on hand across all these entities amounts to $704,954,050 at Receivership Entities and $7,649,584 at portfolio companies and non-reporting entities, totaling $712,603,634. 52 Total Receivership Assets do not include the estimated and unaudited values of assets intended for future sale. This exclusion is made to preserve flexibility in potential negotiations and value maximization strategies for the Receivership Estate. No. Asset Estimated and Unaudited Value as of March 31, 2026 1 Cash on Hand - Receivership Entities $ 704,954,050 2 Cash on Hand - Portfolio Companies $ 7,649,584 3 Debt Investments Undisclosed 4 Equity Investments Undisclosed 5 Escrow Proceeds $ 10,746,169 Table 3 - Summary of All Known Receivership Assets Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 20 of 27 PageID #: 12745 |

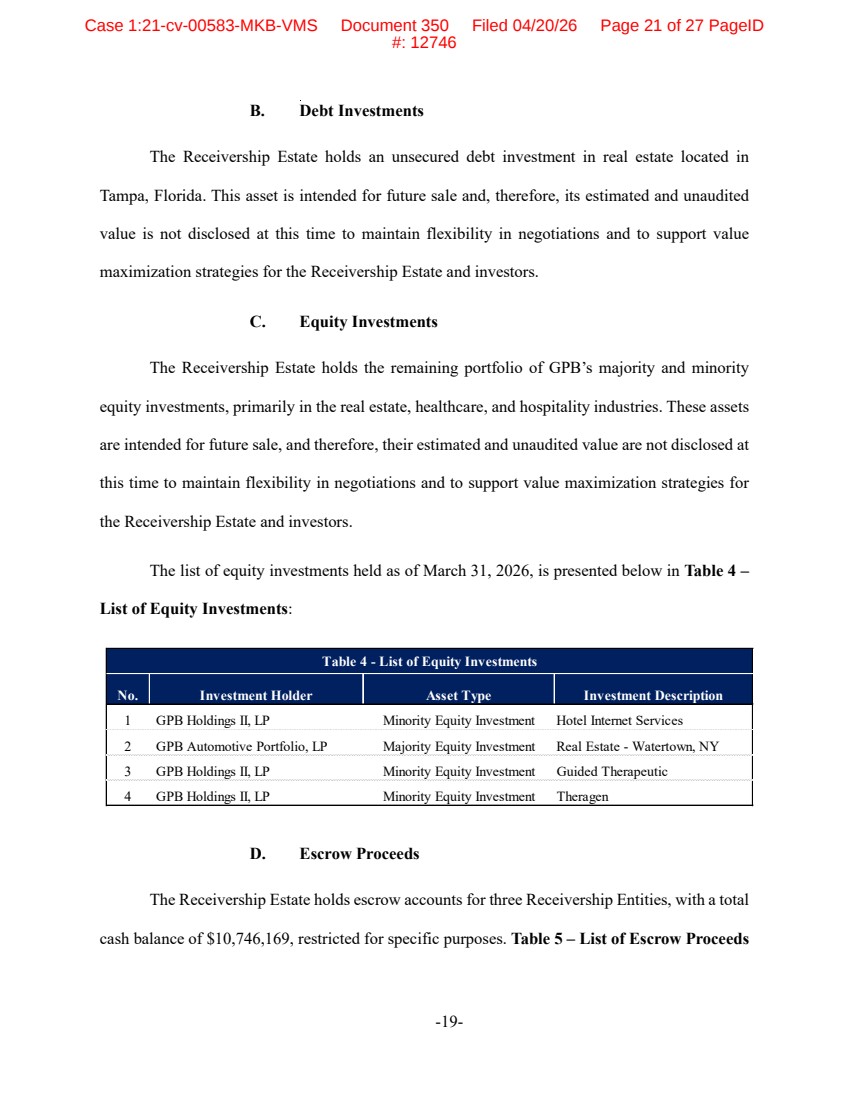

| -19- B. Debt Investments The Receivership Estate holds an unsecured debt investment in real estate located in Tampa, Florida. This asset is intended for future sale and, therefore, its estimated and unaudited value is not disclosed at this time to maintain flexibility in negotiations and to support value maximization strategies for the Receivership Estate and investors. C. Equity Investments The Receivership Estate holds the remaining portfolio of GPB’s majority and minority equity investments, primarily in the real estate, healthcare, and hospitality industries. These assets are intended for future sale, and therefore, their estimated and unaudited value are not disclosed at this time to maintain flexibility in negotiations and to support value maximization strategies for the Receivership Estate and investors. The list of equity investments held as of March 31, 2026, is presented below in Table 4 – List of Equity Investments: D. Escrow Proceeds The Receivership Estate holds escrow accounts for three Receivership Entities, with a total cash balance of $10,746,169, restricted for specific purposes. Table 5 – List of Escrow Proceeds No. Investment Holder Asset Type Investment Description 1 GPB Holdings II, LP Minority Equity Investment Hotel Internet Services 2 GPB Automotive Portfolio, LP Majority Equity Investment Real Estate - Watertown, NY 3 GPB Holdings II, LP Minority Equity Investment Guided Therapeutic 4 GPB Holdings II, LP Minority Equity Investment Theragen Table 4 - List of Equity Investments Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 21 of 27 PageID #: 12746 |

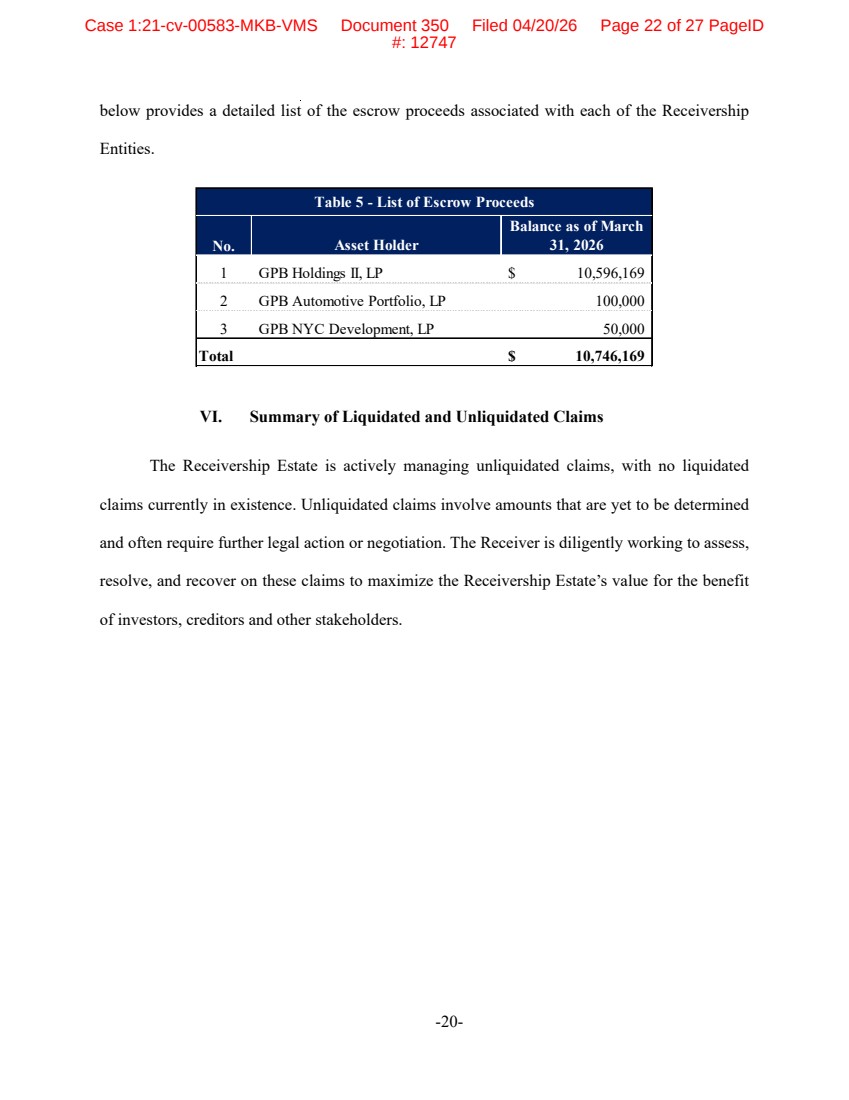

| -20- below provides a detailed list of the escrow proceeds associated with each of the Receivership Entities. VI. Summary of Liquidated and Unliquidated Claims The Receivership Estate is actively managing unliquidated claims, with no liquidated claims currently in existence. Unliquidated claims involve amounts that are yet to be determined and often require further legal action or negotiation. The Receiver is diligently working to assess, resolve, and recover on these claims to maximize the Receivership Estate’s value for the benefit of investors, creditors and other stakeholders. No. Asset Holder Balance as of March 31, 2026 1 GPB Holdings II, LP $ 10,596,169 2 GPB Automotive Portfolio, LP 100,000 3 GPB NYC Development, LP 50,000 Total $ 10,746,169 Table 5 - List of Escrow Proceeds Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 22 of 27 PageID #: 12747 |

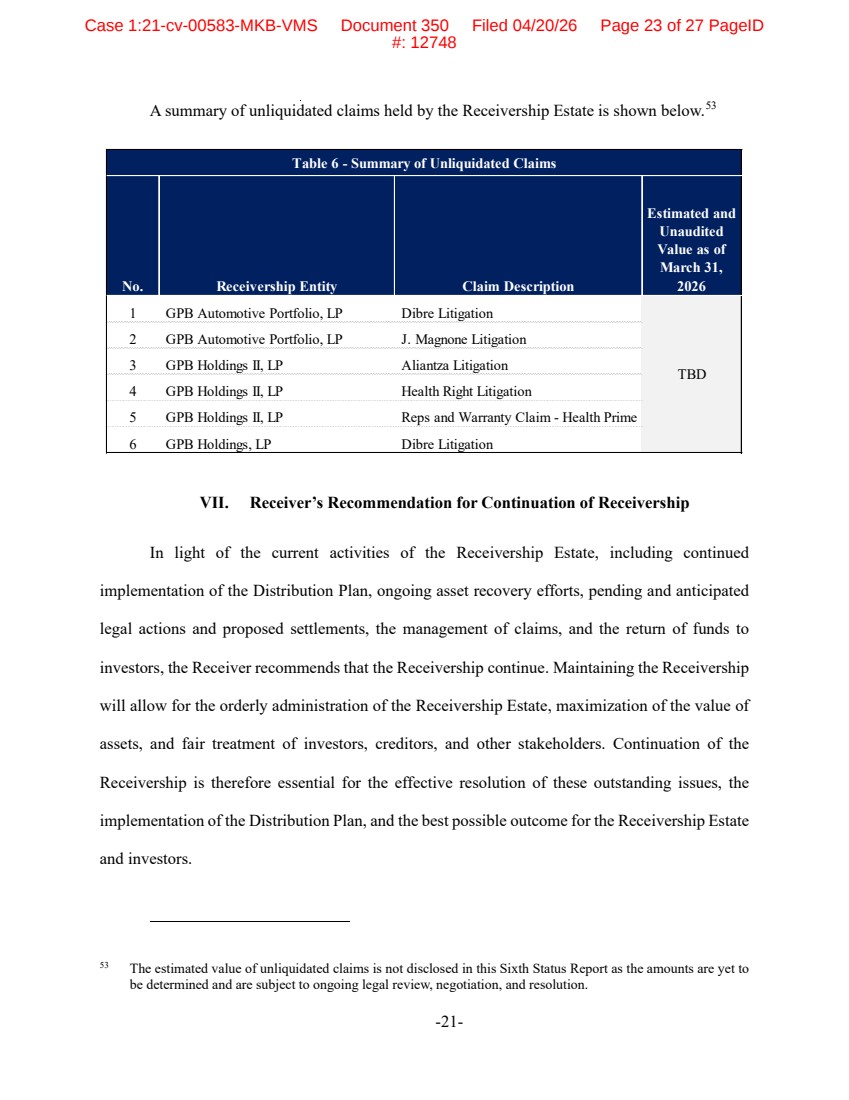

| -21- A summary of unliquidated claims held by the Receivership Estate is shown below.53 VII. Receiver’s Recommendation for Continuation of Receivership In light of the current activities of the Receivership Estate, including continued implementation of the Distribution Plan, ongoing asset recovery efforts, pending and anticipated legal actions and proposed settlements, the management of claims, and the return of funds to investors, the Receiver recommends that the Receivership continue. Maintaining the Receivership will allow for the orderly administration of the Receivership Estate, maximization of the value of assets, and fair treatment of investors, creditors, and other stakeholders. Continuation of the Receivership is therefore essential for the effective resolution of these outstanding issues, the implementation of the Distribution Plan, and the best possible outcome for the Receivership Estate and investors. 53 The estimated value of unliquidated claims is not disclosed in this Sixth Status Report as the amounts are yet to be determined and are subject to ongoing legal review, negotiation, and resolution. No. Receivership Entity Claim Description Estimated and Unaudited Value as of March 31, 2026 1 GPB Automotive Portfolio, LP Dibre Litigation 2 GPB Automotive Portfolio, LP J. Magnone Litigation 3 GPB Holdings II, LP Aliantza Litigation 4 GPB Holdings II, LP Health Right Litigation 5 GPB Holdings II, LP Reps and Warranty Claim - Health Prime 6 GPB Holdings, LP Dibre Litigation Table 6 - Summary of Unliquidated Claims TBD Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 23 of 27 PageID #: 12748 |

| Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 24 of 27 PageID #: 12749 |

| -23- Exhibit A Detailed Schedule of Receipts and Disbursements For the Quarter-Ended March 31, 2026, and Cumulative Totals Since December 3, 2024 Item Quarter (1/1 - 3/31/2026) Cumulative for Receivership Estate Cash Receipts Interest Income $ 5,420,532 $ 43,865,750 Portfolio Company Contributions - 2,948,738 Total Cash Receipts $ 5,420,532 $ 46,814,487 Cash Disbursements Disbursements to Investors $ - $ (400,000,000) Indemnification/Advancement Expenses Paid to Vendors (1,851,727) (21,835,167) Receiver Expenses Paid to Vendors (2,428,124) (14,350,123) Payroll (1,443,068) (8,187,762) Other Expenses (1,038,313) (8,753,285) Other Legal Expenses (782,514) (5,426,790) Total Cash Disbursements $ (7,543,747) $ (458,553,127) Beginning Fund Bank Cash Balance 1) $ 707,077,265 $ 1,116,692,690 Net Cash Flow (2,123,215) (411,738,640) Ending Bank Cash Balance 1) $ 704,954,050 $ 704,954,050 1) Reflects the bank cash balance (excluding check float) of the Receivership Entities, excluding cash held at portfolio companies and legal entities not 100% owned by the Receivership Entities, totaling approximately $7.6 million. Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 25 of 27 PageID #: 12750 |

| -24- Exhibit B Payments to Ordinary Course Professionals54 For the Quarter-Ended March 31, 2026, and Cumulative Totals Since December 3, 2024 54 In accordance with the Receivership Order and other orders of the Court, payments to Automatic Data Processing, Inc., Calderwood, EisnerAmper LLP, KPMG LLP, TransPerfect Legal Solutions, and Vistra Group Holdings S.A. were made directly to the respective vendors and not through the fee application process. Ordinary Course Professional Quarter (1/1 - 3/31/2026) Cumulative for Receivership Estate Allen Overy Shearman Sterling US LLP $ 4,412 $ 36,630 Almada Consulting - 5,100 Automatic Data Processing, Inc. 52,829 318,909 Baker Tilly International Ltd. - 14,625 Berkeley Research Group, LLC (BRG) - 2,331 Calderwood 32,380 154,867 Cole-Frieman & Mallon LLP - 4,394 Corporation Service Company (CSC) 8,828 30,905 CT Corp - 1,054 Crowe LLP - 5,000 EisnerAmper LLP - 1,149,750 Epiq Corporate Restructuring LLC 200,327 1,218,699 Foley & Lardner LLP 2,737 44,608 Grant Thornton Advisors LLC 44,009 522,766 Herrick Feinstein LLP - 67,478 Heyman Enerio Gattuso & Hirzel LLP 45,956 370,574 Hunton Andrews Kurth LLP 17,181 450,271 Kingfisher Management Limited 4,521 18,870 KPMG LLP 551,934 2,327,545 Leeward Management Limited - 21,042 Maples Fund Services (Cayman) Limited - 126,440 Marshall Advisors LLC 450 450 Mayer Brown LLP 667,935 6,315,609 Maynard Nexsen PC - 1,274 McConnell Valdes LLC 5,714 20,262 McGuireWoods LLP - 106,670 Morgan, Lewis & Bockius, LLP 3,936 552,151 Mourant Ozannes (Cayman) LLP - 21,815 Pardo Jackson Gainsburg & Shelowitz, PL 8,661 94,732 Paychex, Inc 1,297 6,073 Potter Anderson & Corroon LLP 619 2,107 Quattlebaum, Grooms & Tull PLLC - 33,105 Reeves & Brightwell LLP 1,372 12,808 SGC Associates LLP 2,500 7,500 Toppan Merrill LLC 3,486 31,782 TransPerfect Legal Solutions 252,565 1,844,164 Vistra Group Holdings S.A. - 2,108,533 Walkers (Cayman) LLP - 42,259 Total $ 1,913,650 $ 18,093,149 Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 26 of 27 PageID #: 12751 |

| -25- Exhibit C Accrual Summary Receivership Entity Accounting Fees Legal indemnification Legal - other Receiver Admin Fees Taxes Total Armada Waste Management, LP $ 70,910 $ 29,566 $ - $ 31,809 $ 47,627 $ - $ 179,911 GPB Automotive Portfolio, LP 236,486 1,440,269 294,429 1,634,142 155,334 - 3,760,660 GPB Cold Storage, LP 58,988 220,998 - 226,440 34,572 - 540,999 GPB Holdings II, LP 474,704 1,734,253 - 1,828,324 152,055 - 4,189,337 GPB Holdings, LP 80,563 469,015 - 53,571 - - 603,149 GPB NYC Development, LP 64,942 1,204 - 200 34,367 - 100,712 Highline Management Inc. - - - - - 16,571 16,571 Total $ 986,593 $ 3,426,290 $ 763,444 $ 3,720,914 $ 477,526 $ 16,571 $ 9,391,338 Case 1:21-cv-00583-MKB-VMS Document 350 Filed 04/20/26 Page 27 of 27 PageID #: 12752 |