EXHIBIT V

| Corporate Use# EIB Group Reconciliation of the Consolidated Financial Statements of the EIB Group as at 31 December 2025 prepared in accordance with EU Accounting Directives and IFRS 1 |

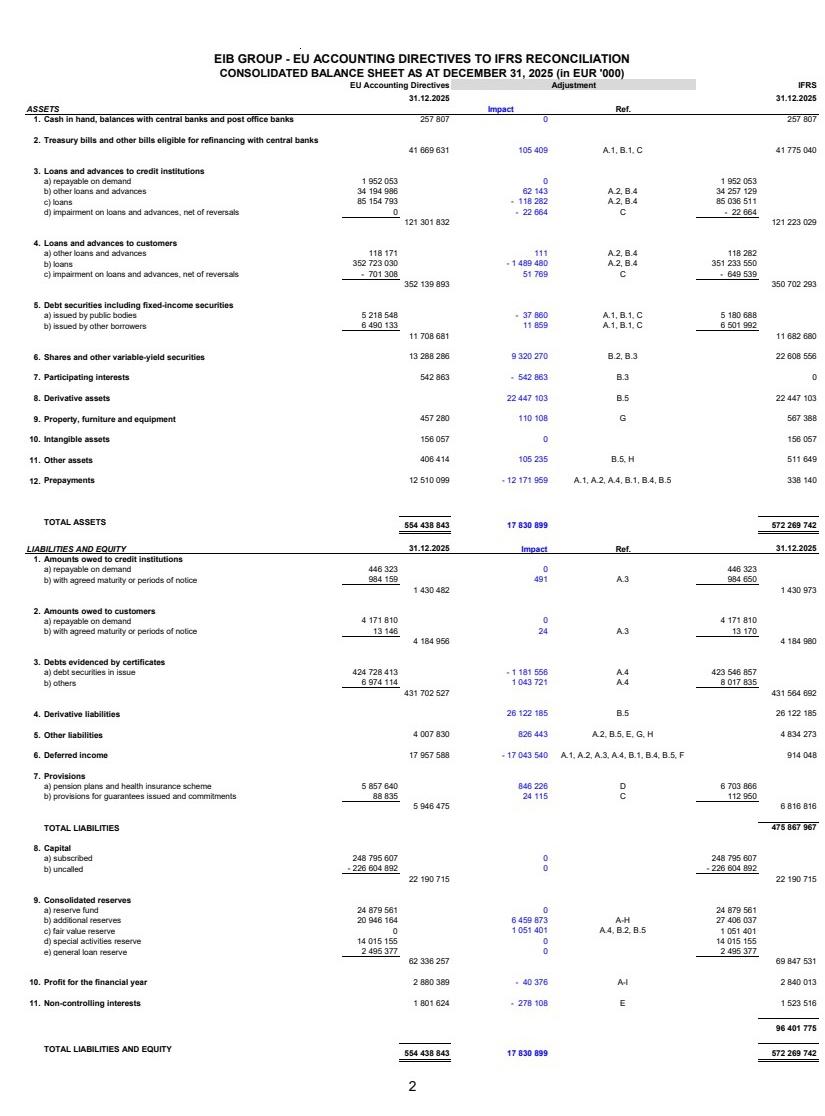

| Corporate Use# 31.12.2025 31.12.2025 ASSETS Impact Ref. 1. Cash in hand, balances with central banks and post office banks 257 807 0 257 807 2. Treasury bills and other bills eligible for refinancing with central banks 41 669 631 105 409 A.1, B.1, C 41 775 040 3. Loans and advances to credit institutions a) repayable on demand 1 952 053 0 1 952 053 b) other loans and advances 34 194 986 62 143 A.2, B.4 34 257 129 c) loans 85 154 793 - 118 282 A.2, B.4 85 036 511 d) impairment on loans and advances, net of reversals 0 - 22 664 C - 22 664 121 301 832 121 223 029 4. Loans and advances to customers a) other loans and advances 118 171 111 A.2, B.4 118 282 b) loans 352 723 030 - 1 489 480 A.2, B.4 351 233 550 c) impairment on loans and advances, net of reversals - 701 308 51 769 C - 649 539 352 139 893 350 702 293 5. Debt securities including fixed-income securities a) issued by public bodies 5 218 548 - 37 860 A.1, B.1, C 5 180 688 b) issued by other borrowers 6 490 133 11 859 A.1, B.1, C 6 501 992 11 708 681 11 682 680 6. Shares and other variable-yield securities 13 288 286 9 320 270 B.2, B.3 22 608 556 7. Participating interests 542 863 - 542 863 B.3 0 8. Derivative assets 22 447 103 B.5 22 447 103 9. Property, furniture and equipment 457 280 110 108 G 567 388 10. Intangible assets 156 057 0 156 057 11. Other assets 406 414 105 235 B.5, H 511 649 12. Prepayments 12 510 099 - 12 171 959 A.1, A.2, A.4, B.1, B.4, B.5 338 140 TOTAL ASSETS 554 438 843 17 830 899 572 269 742 LIABILITIES AND EQUITY 31.12.2025 Impact Ref. 31.12.2025 1. Amounts owed to credit institutions a) repayable on demand 446 323 0 446 323 b) with agreed maturity or periods of notice 984 159 491 A.3 984 650 1 430 482 1 430 973 2. Amounts owed to customers a) repayable on demand 4 171 810 0 4 171 810 b) with agreed maturity or periods of notice 13 146 24 A.3 13 170 4 184 956 4 184 980 3. Debts evidenced by certificates a) debt securities in issue 424 728 413 - 1 181 556 A.4 423 546 857 b) others 6 974 114 1 043 721 A.4 8 017 835 431 702 527 431 564 692 4. Derivative liabilities 26 122 185 B.5 26 122 185 5. Other liabilities 4 007 830 826 443 A.2, B.5, E, G, H 4 834 273 6. Deferred income 17 957 588 - 17 043 540 A.1, A.2, A.3, A.4, B.1, B.4, B.5, F 914 048 7. Provisions a) pension plans and health insurance scheme 5 857 640 846 226 D 6 703 866 b) provisions for guarantees issued and commitments 88 835 24 115 C 112 950 5 946 475 6 816 816 TOTAL LIABILITIES 475 867 967 8. Capital a) subscribed 248 795 607 0 248 795 607 b) uncalled - 226 604 892 0 - 226 604 892 22 190 715 22 190 715 9. Consolidated reserves a) reserve fund 24 879 561 0 24 879 561 b) additional reserves 20 946 164 6 459 873 A-H 27 406 037 c) fair value reserve 0 1 051 401 A.4, B.2, B.5 1 051 401 d) special activities reserve 14 015 155 0 14 015 155 e) general loan reserve 2 495 377 0 2 495 377 62 336 257 69 847 531 10. Profit for the financial year 2 880 389 - 40 376 A-I 2 840 013 11. Non-controlling interests 1 801 624 - 278 108 E 1 523 516 96 401 775 TOTAL LIABILITIES AND EQUITY 554 438 843 17 830 899 572 269 742 EIB GROUP - EU ACCOUNTING DIRECTIVES TO IFRS RECONCILIATION CONSOLIDATED BALANCE SHEET AS AT DECEMBER 31, 2025 (in EUR '000) EU Accounting Directives Adjustment IFRS 2 |

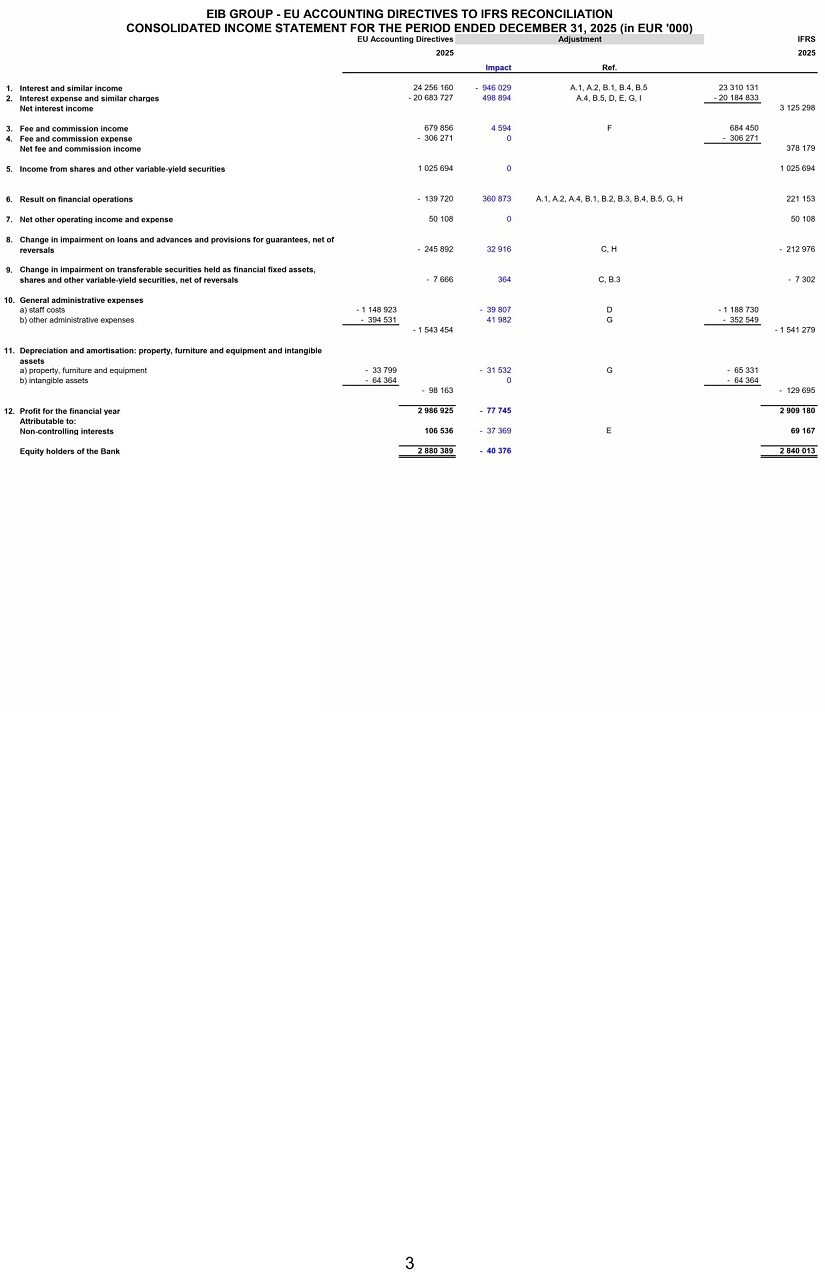

| Corporate Use# Impact Ref. 1. Interest and similar income 24 256 160 - 946 029 A.1, A.2, B.1, B.4, B.5 23 310 131 2. Interest expense and similar charges - 20 683 727 498 894 A.4, B.5, D, E, G, I - 20 184 833 Net interest income 3 125 298 3. Fee and commission income 679 856 4 594 F 684 450 4. Fee and commission expense - 306 271 0 - 306 271 Net fee and commission income 378 179 5. Income from shares and other variable-yield securities 1 025 694 0 1 025 694 6. Result on financial operations - 139 720 360 873 A.1, A.2, A.4, B.1, B.2, B.3, B.4, B.5, G, H 221 153 7. Net other operating income and expense 50 108 0 50 108 8. Change in impairment on loans and advances and provisions for guarantees, net of reversals - 245 892 32 916 C, H - 212 976 9. Change in impairment on transferable securities held as financial fixed assets, shares and other variable-yield securities, net of reversals - 7 666 364 C, B.3 - 7 302 10. General administrative expenses a) staff costs - 1 148 923 - 39 807 D - 1 188 730 b) other administrative expenses - 394 531 41 982 G - 352 549 - 1 543 454 - 1 541 279 11. Depreciation and amortisation: property, furniture and equipment and intangible assets a) property, furniture and equipment - 33 799 - 31 532 G - 65 331 b) intangible assets - 64 364 0 - 64 364 - 98 163 - 129 695 12. Profit for the financial year 2 986 925 - 77 745 2 909 180 Attributable to: Non-controlling interests 106 536 - 37 369 E 69 167 Equity holders of the Bank 2 880 389 - 40 376 2 840 013 CONSOLIDATED INCOME STATEMENT FOR THE PERIOD ENDED DECEMBER 31, 2025 (in EUR '000) EIB GROUP - EU ACCOUNTING DIRECTIVES TO IFRS RECONCILIATION EU Accounting Directives IFRS 2025 2025 Adjustment 3 |

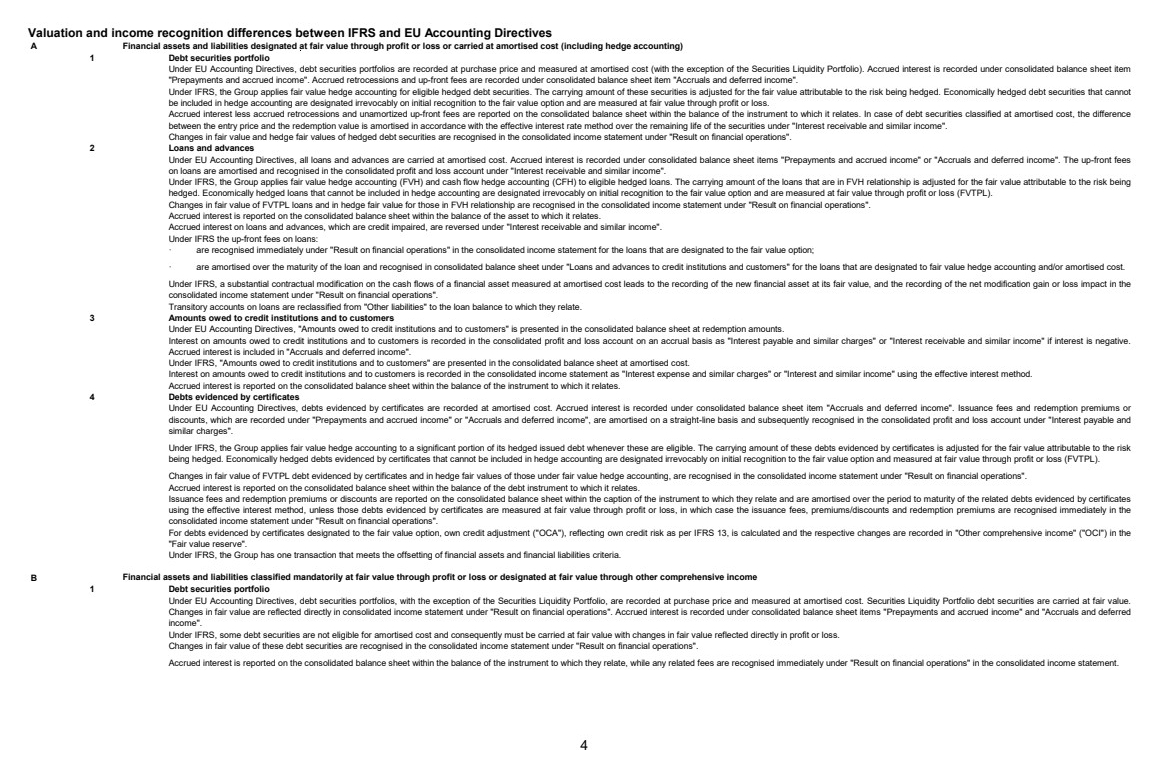

| Corporate Use# Valuation and income recognition differences between IFRS and EU Accounting Directives A 1 Debt securities portfolio Under EU Accounting Directives, debt securities portfolios are recorded at purchase price and measured at amortised cost (with the exception of the Securities Liquidity Portfolio). Accrued interest is recorded under consolidated balance sheet item "Prepayments and accrued income". Accrued retrocessions and up-front fees are recorded under consolidated balance sheet item "Accruals and deferred income". Under IFRS, the Group applies fair value hedge accounting for eligible hedged debt securities. The carrying amount of these securities is adjusted for the fair value attributable to the risk being hedged. Economically hedged debt securities that cannot be included in hedge accounting are designated irrevocably on initial recognition to the fair value option and are measured at fair value through profit or loss. Accrued interest less accrued retrocessions and unamortized up-front fees are reported on the consolidated balance sheet within the balance of the instrument to which it relates. In case of debt securities classified at amortised cost, the difference between the entry price and the redemption value is amortised in accordance with the effective interest rate method over the remaining life of the securities under "Interest receivable and similar income". Changes in fair value and hedge fair values of hedged debt securities are recognised in the consolidated income statement under "Result on financial operations". 2 Loans and advances Under EU Accounting Directives, all loans and advances are carried at amortised cost. Accrued interest is recorded under consolidated balance sheet items "Prepayments and accrued income" or "Accruals and deferred income". The up-front fees on loans are amortised and recognised in the consolidated profit and loss account under "Interest receivable and similar income". Under IFRS, the Group applies fair value hedge accounting (FVH) and cash flow hedge accounting (CFH) to eligible hedged loans. The carrying amount of the loans that are in FVH relationship is adjusted for the fair value attributable to the risk being hedged. Economically hedged loans that cannot be included in hedge accounting are designated irrevocably on initial recognition to the fair value option and are measured at fair value through profit or loss (FVTPL). Changes in fair value of FVTPL loans and in hedge fair value for those in FVH relationship are recognised in the consolidated income statement under "Result on financial operations". Accrued interest is reported on the consolidated balance sheet within the balance of the asset to which it relates. Accrued interest on loans and advances, which are credit impaired, are reversed under "Interest receivable and similar income". Under IFRS the up-front fees on loans: · are recognised immediately under "Result on financial operations" in the consolidated income statement for the loans that are designated to the fair value option; · are amortised over the maturity of the loan and recognised in consolidated balance sheet under "Loans and advances to credit institutions and customers" for the loans that are designated to fair value hedge accounting and/or amortised cost. Under IFRS, a substantial contractual modification on the cash flows of a financial asset measured at amortised cost leads to the recording of the new financial asset at its fair value, and the recording of the net modification gain or loss impact in the consolidated income statement under "Result on financial operations". Transitory accounts on loans are reclassified from "Other liabilities" to the loan balance to which they relate. 3 Amounts owed to credit institutions and to customers Under EU Accounting Directives, "Amounts owed to credit institutions and to customers" is presented in the consolidated balance sheet at redemption amounts. Interest on amounts owed to credit institutions and to customers is recorded in the consolidated profit and loss account on an accrual basis as "Interest payable and similar charges" or "Interest receivable and similar income" if interest is negative. Accrued interest is included in "Accruals and deferred income". Under IFRS, "Amounts owed to credit institutions and to customers" are presented in the consolidated balance sheet at amortised cost. Interest on amounts owed to credit institutions and to customers is recorded in the consolidated income statement as "Interest expense and similar charges" or "Interest and similar income" using the effective interest method. Accrued interest is reported on the consolidated balance sheet within the balance of the instrument to which it relates. 4 Debts evidenced by certificates Under EU Accounting Directives, debts evidenced by certificates are recorded at amortised cost. Accrued interest is recorded under consolidated balance sheet item "Accruals and deferred income". Issuance fees and redemption premiums or discounts, which are recorded under "Prepayments and accrued income" or "Accruals and deferred income", are amortised on a straight-line basis and subsequently recognised in the consolidated profit and loss account under "Interest payable and similar charges". Under IFRS, the Group applies fair value hedge accounting to a significant portion of its hedged issued debt whenever these are eligible. The carrying amount of these debts evidenced by certificates is adjusted for the fair value attributable to the risk being hedged. Economically hedged debts evidenced by certificates that cannot be included in hedge accounting are designated irrevocably on initial recognition to the fair value option and measured at fair value through profit or loss (FVTPL). Changes in fair value of FVTPL debt evidenced by certificates and in hedge fair values of those under fair value hedge accounting, are recognised in the consolidated income statement under "Result on financial operations". Accrued interest is reported on the consolidated balance sheet within the balance of the debt instrument to which it relates. Issuance fees and redemption premiums or discounts are reported on the consolidated balance sheet within the caption of the instrument to which they relate and are amortised over the period to maturity of the related debts evidenced by certificates using the effective interest method, unless those debts evidenced by certificates are measured at fair value through profit or loss, in which case the issuance fees, premiums/discounts and redemption premiums are recognised immediately in the consolidated income statement under "Result on financial operations". For debts evidenced by certificates designated to the fair value option, own credit adjustment ("OCA"), reflecting own credit risk as per IFRS 13, is calculated and the respective changes are recorded in "Other comprehensive income" ("OCI") in the "Fair value reserve". Under IFRS, the Group has one transaction that meets the offsetting of financial assets and financial liabilities criteria. B 1 Debt securities portfolio Under EU Accounting Directives, debt securities portfolios, with the exception of the Securities Liquidity Portfolio, are recorded at purchase price and measured at amortised cost. Securities Liquidity Portfolio debt securities are carried at fair value. Changes in fair value are reflected directly in consolidated income statement under "Result on financial operations". Accrued interest is recorded under consolidated balance sheet items "Prepayments and accrued income" and "Accruals and deferred income". Under IFRS, some debt securities are not eligible for amortised cost and consequently must be carried at fair value with changes in fair value reflected directly in profit or loss. Changes in fair value of these debt securities are recognised in the consolidated income statement under "Result on financial operations". Accrued interest is reported on the consolidated balance sheet within the balance of the instrument to which they relate, while any related fees are recognised immediately under "Result on financial operations" in the consolidated income statement. Financial assets and liabilities designated at fair value through profit or loss or carried at amortised cost (including hedge accounting) Financial assets and liabilities classified mandatorily at fair value through profit or loss or designated at fair value through other comprehensive income 4 |

| Corporate Use# 2 Shares and other variable-yield securities Under EU Accounting Directives, shares and other variable-yield securities are initially recorded at acquisition cost reduced by any reflow resulting from repayments. Their carrying value is subsequently adjusted to the lower of cost or market value at each balance sheet date. Respective value adjustments are recorded under "Result on financial operations". Under IFRS, shares and other variable-yield securities are carried at fair value with changes in fair value reflected directly in the consolidated income statement under "Result on financial operations", except of the investment in European Bank for Reconstruction and Development ("EBRD") whose fair value changes are reflected in OCI under "Fair value reserve". 3 Participating interests Under EU Accounting Directive, "Participating interests" are accounted for using the equity method as defined under EU-AD based on methods consistent with the Group’s accounting policies. Respective value adjustments are recorded under "Value (re-)adjustments in respect of transferable securities held as financial fixed assets and participating interests". Under IFRS, participating interests are included within "Shares and other variable-yield securities" and respective fair value adjustments are recorded in "Result on financial operations". 4 Loans and advances Under EU Accounting Directives, all loans and advances are carried at amortised cost. Accrued interest is recorded under consolidated balance sheet items "Prepayments and accrued income" or "Accruals and deferred income". The up-front fees on loans are amortised and recognised in the consolidated profit and loss account under "Interest receivable and similar income". Under IFRS, loans that are not eligible for amortised cost, are classified as measured at fair value through profit or loss. The up-front fees on these loans are recognised at inception under "Result on financial operations" in the consolidated income statement. Changes in fair value of loans are recognised in the consolidated income statement under "Result on financial operations". 5 Derivative assets and liabilities a Treasury derivatives Under EU Accounting Directives, derivative instruments in the Securities Liquidity Portfolio are marked to market and recorded under "Other assets" or "Other liabilities". Interest accrued under derivative instruments is presented under "Prepayments and accrued income" or "Accruals and deferred income". Under IFRS, all derivative assets and derivative liabilities are recognised on the consolidated balance sheet and measured at fair value through profit or loss. Accrued interest is reported on the consolidated balance sheet within the balance of the instrument to which it relates. Credit valuation adjustment ("CVA"), Debit valuation adjustment ("DVA") and Collateral Value adjustment ("CollVA") are included in the fair valuation of derivatives. Changes in fair value of derivatives are recognised in the consolidated income statement under "Result on financial operations". b Derivatives and hedging activities Under EU Accounting Directives, hedging derivative instruments are not recognised on balance sheet. They are reported off balance sheet at nominal amount. Interest accrued under derivative instruments is presented under "Prepayments and accrued income" or "Accruals and deferred income". Up-front fees, redemption premiums or premiums/discounts are amortised over the period to maturity of the related derivatives under "Interest payable and similar charges". In case of currency swaps, the revaluation of the spot leg of a currency swap is neutralised in "Accruals and deferred income" or "Prepayments and accrued income". Under IFRS, all derivative assets and derivative liabilities are recognised on balance sheet and measured at fair value through profit or loss. Accrued interest is reported on the consolidated balance sheet within the balance of the instrument to which it relates. CVA, DVA and CollVA are included in the fair valuation of derivatives. Changes in fair value of derivatives are recognised in the consolidated income statement under "Result on financial operations". The amortisation of premiums and discounts of FX swaps and FX forwards are recorded under "Result on financial operations". For derivatives used in fair value hedge accounting (FVH), the gain or loss of the designated part of the hedging instrument is recognised in the consolidated income statement. In addition, the Group separates the fair value of the foreign currency basis spread ("CBS") from the hedging instruments and applies a dedicated accounting treatment. The initial CBS amount, measured at the date of designation, is recorded under OCI and is amortised linearly over the residual lifetime of the hedge in the consolidated income statement. Subsequent changes in the fair value of the CBS are recognised directly in OCI. For derivatives used in cash flow hedge accounting (CFH), the gain or loss on the effective portion of the hedging instrument is recognised under OCI. When cash flows relating to the hedged items (e.g. interest income) are reported in the income statement, amounts in OCI are reclassified to the consolidated income statement. For derivatives used in fair value hedge accounting, up-front fees or redemption premiums are amortised over the period to maturity of the related derivative using the effective interest method under "Interest payable and similar charges", unless these derivatives are not designated to hedge accounting, in which case they are recognised immediately under "Result on financial operations". Under IFRS, the Group has two transactions that meet the offsetting of financial assets and financial liabilities criteria. C Under EU Accounting Directives, value adjustments on loans and advances are recorded where: (i) there is a risk of non-recovery of all or part of their amounts, or (ii) to capture loans in the portfolio which are impaired but have not yet been identified as such or for losses which have been incurred but not yet reported. These value adjustments are accounted for in the consolidated profit and loss account as "Value (re-)adjustments in respect of loans and advances and provisions for contingent liabilities" and are deducted from the appropriate asset items on the consolidated balance sheet. Value adjustments for debt securities are recorded, if these are other than temporary, or to capture debt securities which are impaired but have not yet been identified as such or for losses which have been incurred but not yet reported. These value adjustments are accounted for in the consolidated profit and loss account under "Value (re-)adjustments in respect of transferable securities held as financial fixed assets and participating interests" and are deducted from the appropriate asset items on the consolidated balance sheet. Under IFRS, the Group is required to recognise a loss allowance for all loans and advances, and debt securities measured at amortised cost as well as for off-balance sheet loan commitments. This allowance is based on either lifetime Expected Credit Loss ("ECL"), if there has been a significant increase in credit risk since initial recognition or the instrument is considered as being credit-impaired or otherwise on 12-months ECL. Depending on the nature of the financial instrument, the ECL allowances are deducted from the appropriate asset items on the consolidated balance sheet. For off-balance sheet items, a provision for credit loss is reported under "Provisions b) provisions for guarantees issued and commitments". Changes in the ECL allowances are recorded in the consolidated income statement either under: · "Change in impairment on loans and advances and provisions for guarantees, net of reversals" for loans and loan commitments or; · "Change in impairment on transferable securities held as financial fixed assets, shares and other variable - yield securities, net of reversals" for debt securities. Impairment of financial assets measured at amortised cost and loan commitments 5 |

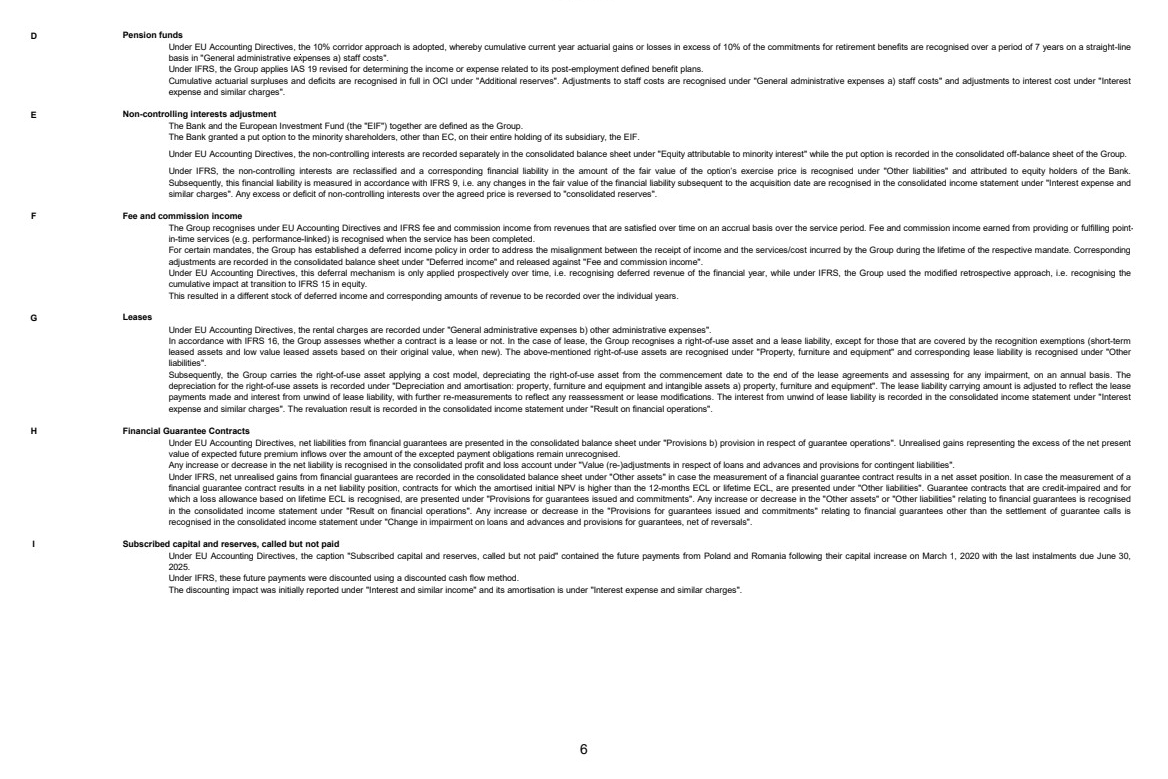

| Corporate Use# D Under EU Accounting Directives, the 10% corridor approach is adopted, whereby cumulative current year actuarial gains or losses in excess of 10% of the commitments for retirement benefits are recognised over a period of 7 years on a straight-line basis in "General administrative expenses a) staff costs". Under IFRS, the Group applies IAS 19 revised for determining the income or expense related to its post-employment defined benefit plans. Cumulative actuarial surpluses and deficits are recognised in full in OCI under "Additional reserves". Adjustments to staff costs are recognised under "General administrative expenses a) staff costs" and adjustments to interest cost under "Interest expense and similar charges". E The Bank and the European Investment Fund (the "EIF") together are defined as the Group. The Bank granted a put option to the minority shareholders, other than EC, on their entire holding of its subsidiary, the EIF. Under EU Accounting Directives, the non-controlling interests are recorded separately in the consolidated balance sheet under "Equity attributable to minority interest" while the put option is recorded in the consolidated off-balance sheet of the Group. Under IFRS, the non-controlling interests are reclassified and a corresponding financial liability in the amount of the fair value of the option’s exercise price is recognised under "Other liabilities" and attributed to equity holders of the Bank. Subsequently, this financial liability is measured in accordance with IFRS 9, i.e. any changes in the fair value of the financial liability subsequent to the acquisition date are recognised in the consolidated income statement under "Interest expense and similar charges". Any excess or deficit of non-controlling interests over the agreed price is reversed to "consolidated reserves". F The Group recognises under EU Accounting Directives and IFRS fee and commission income from revenues that are satisfied over time on an accrual basis over the service period. Fee and commission income earned from providing or fulfilling point-in-time services (e.g. performance-linked) is recognised when the service has been completed. For certain mandates, the Group has established a deferred income policy in order to address the misalignment between the receipt of income and the services/cost incurred by the Group during the lifetime of the respective mandate. Corresponding adjustments are recorded in the consolidated balance sheet under "Deferred income" and released against "Fee and commission income". Under EU Accounting Directives, this deferral mechanism is only applied prospectively over time, i.e. recognising deferred revenue of the financial year, while under IFRS, the Group used the modified retrospective approach, i.e. recognising the cumulative impact at transition to IFRS 15 in equity. This resulted in a different stock of deferred income and corresponding amounts of revenue to be recorded over the individual years. G Under EU Accounting Directives, the rental charges are recorded under "General administrative expenses b) other administrative expenses". In accordance with IFRS 16, the Group assesses whether a contract is a lease or not. In the case of lease, the Group recognises a right-of-use asset and a lease liability, except for those that are covered by the recognition exemptions (short-term leased assets and low value leased assets based on their original value, when new). The above-mentioned right-of-use assets are recognised under "Property, furniture and equipment" and corresponding lease liability is recognised under "Other liabilities". Subsequently, the Group carries the right-of-use asset applying a cost model, depreciating the right-of-use asset from the commencement date to the end of the lease agreements and assessing for any impairment, on an annual basis. The depreciation for the right-of-use assets is recorded under "Depreciation and amortisation: property, furniture and equipment and intangible assets a) property, furniture and equipment". The lease liability carrying amount is adjusted to reflect the lease payments made and interest from unwind of lease liability, with further re-measurements to reflect any reassessment or lease modifications. The interest from unwind of lease liability is recorded in the consolidated income statement under "Interest expense and similar charges". The revaluation result is recorded in the consolidated income statement under "Result on financial operations". H Under EU Accounting Directives, net liabilities from financial guarantees are presented in the consolidated balance sheet under "Provisions b) provision in respect of guarantee operations". Unrealised gains representing the excess of the net present value of expected future premium inflows over the amount of the excepted payment obligations remain unrecognised. Any increase or decrease in the net liability is recognised in the consolidated profit and loss account under "Value (re-)adjustments in respect of loans and advances and provisions for contingent liabilities". Under IFRS, net unrealised gains from financial guarantees are recorded in the consolidated balance sheet under "Other assets" in case the measurement of a financial guarantee contract results in a net asset position. In case the measurement of a financial guarantee contract results in a net liability position, contracts for which the amortised initial NPV is higher than the 12-months ECL or lifetime ECL, are presented under "Other liabilities". Guarantee contracts that are credit-impaired and for which a loss allowance based on lifetime ECL is recognised, are presented under "Provisions for guarantees issued and commitments". Any increase or decrease in the "Other assets" or "Other liabilities" relating to financial guarantees is recognised in the consolidated income statement under "Result on financial operations". Any increase or decrease in the "Provisions for guarantees issued and commitments" relating to financial guarantees other than the settlement of guarantee calls is recognised in the consolidated income statement under "Change in impairment on loans and advances and provisions for guarantees, net of reversals". I Under EU Accounting Directives, the caption "Subscribed capital and reserves, called but not paid" contained the future payments from Poland and Romania following their capital increase on March 1, 2020 with the last instalments due June 30, 2025. Under IFRS, these future payments were discounted using a discounted cash flow method. The discounting impact was initially reported under "Interest and similar income" and its amortisation is under "Interest expense and similar charges". Leases Financial Guarantee Contracts Subscribed capital and reserves, called but not paid Pension funds Non-controlling interests adjustment Fee and commission income 6 |