Exhibit 99.1

Management’s Discussion and Analysis of

Triple Flag Precious Metals Corp.

For the three months ended March 31, 2026

(Expressed in United States Dollars)

Exhibit 99.1

Management’s Discussion and Analysis of

Triple Flag Precious Metals Corp.

For the three months ended March 31, 2026

(Expressed in United States Dollars)

MANAGEMENT’S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

This Management’s Discussion and Analysis (‘‘MD&A’’) is intended to help the reader understand Triple Flag Precious Metals Corp. (‘‘TF Precious Metals’’), its operations, financial performance and the present and anticipated future business environment. This MD&A, which has been prepared as of May 5, 2026, should be read in conjunction with the unaudited condensed interim consolidated financial statements of TF Precious Metals as at and for the three months ended March 31, 2026 (the “Interim Financial Statements”), which have been prepared in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board (“IFRS Accounting Standards” or “IFRS”), applicable to the preparation of interim financial statements, including International Accounting Standard (“IAS”) 34, Interim Financial Reporting. The unaudited condensed interim consolidated financial statements have been prepared on a basis consistent with the audited consolidated financial statements of TF Precious Metals as at December 31, 2025, and for the years ended December 31, 2025 and 2024 (the “Annual Financial Statements”), which have been prepared in accordance with IFRS Accounting Standards. Certain notes to the Annual Financial Statements are specifically referred to in this MD&A. All amounts in this MD&A are in U.S. dollars unless otherwise indicated. References to “US$”, “$” or “dollars” are to United States dollars, references to “C$” are to Canadian dollars and references to “A$” are to Australian dollars. In this MD&A, all references to ‘‘Triple Flag’’, the ‘‘Company’’, ‘‘we’’, ‘‘us’’ or ‘‘our’’ refer to TF Precious Metals together with its subsidiaries, on a consolidated basis.

This MD&A contains forward-looking information. Forward-looking information is necessarily based on a number of opinions, estimates and assumptions that we considered appropriate and reasonable as of the date such statements were made, and are subject to known and unknown risks, uncertainties, assumptions and other factors that may cause the actual results, level of activity, performance or achievements to be materially different from those expressed or implied by such forward-looking information, including but not limited to the risk factors described in the ‘‘Risk Factors” section of the Company’s most recent annual information form available from time to time on SEDAR+ at www.sedarplus.ca and on EDGAR at www.sec.gov. There can be no assurance that such forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Accordingly, users should not place undue reliance on forward-looking information, which speaks only as of the date made. See ‘‘Forward-Looking Information’’ in this MD&A.

2

| |

4 | |

5 | |

7 | |

8 | |

Portfolio of Streaming and Related Interests and Royalty Interests | 9 |

11 | |

12 | |

16 | |

17 | |

19 | |

21 | |

22 | |

23 | |

25 | |

25 | |

25 | |

IFRS Accounting Standards Critical Accounting Policies and Accounting Estimates | 26 |

26 | |

29 | |

30 | |

31 | |

31 |

3

Triple Flag is a precious metals streaming and royalty company. We offer investors exposure to gold and silver, primarily from the Americas and Australia. Our mission is to be a preferred funding partner to mining companies throughout the commodity cycle by providing customized streaming and royalty financing.

Since inception, we have invested in and systematically developed a long-life, high-margin, top-tier diversified portfolio of streams and royalties providing exposure primarily to gold and silver. As at May 5, 2026, our portfolio is comprised of 240 assets, consisting of 16 streams and 224 royalties.

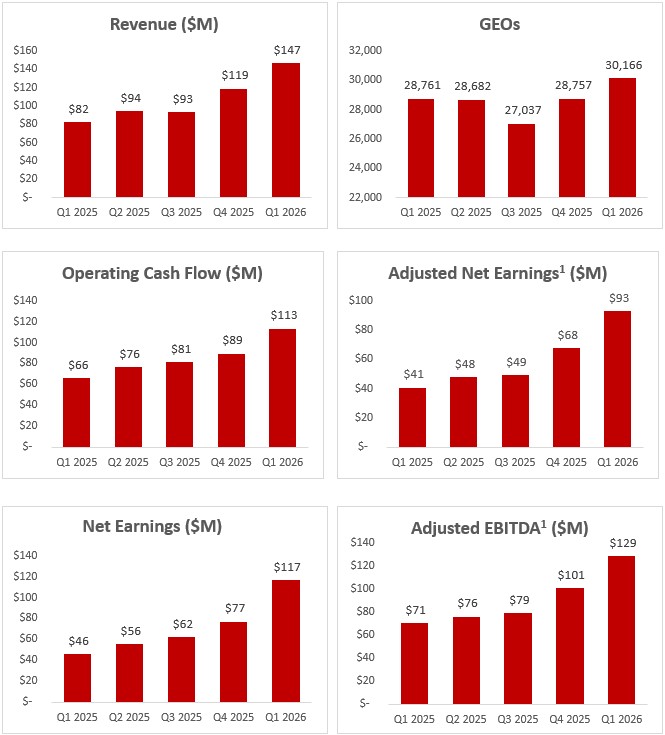

The following charts highlight our recent quarterly performance:

| 1. | Adjusted EBITDA and adjusted net earnings are non-IFRS financial performance measures with no standardized meaning under IFRS Accounting Standards and therefore may not be comparable to similar measures presented by other issuers. For further information and a detailed reconciliation of each non-IFRS measure to the most directly comparable IFRS Accounting Standards measure, see ‘‘Non-IFRS Financial Performance Measures’’ in this MD&A. |

4

Asset Count1 | | |

Producing |

| 34 |

Development & Exploration |

| 206 |

Total |

| 240 |

| 1. | Asset count as at May 5, 2026. |

Our portfolio is underpinned by a stable base of cash flow generating streams and royalties and is designed to grow intrinsically over time through exposure to potential mine life extensions, exploration success, new mine builds and throughput expansions. In addition, we are focused on further enhancing portfolio quality by executing accretive investments to grow the scale and enhance the quality of our portfolio of precious metals streams and royalties. We focus on ‘‘per share’’ metrics with the objective of pursuing accretive new investments while managing the capital structure to effectively compete for quality assets without incurring long-term financial leverage.

The market prices of gold and silver are primary drivers of our profitability and ability to generate operating cash flow per share.

The following table sets forth the average gold and silver prices, and the average exchange rate between the Canadian and U.S. dollars, for the periods indicated.

| | Three months ended March 31, | ||

Average Metal Prices/Exchange rate | | 2026 | | 2025 |

Gold (US$/oz)1 | | 4,873 | | 2,860 |

Silver (US$/oz)2 |

| 84.33 | | 31.88 |

Exchange rate (US$/C$)3 |

| 1.3717 | | 1.4352 |

| 1. | Based on the London Bullion Market Association (“LBMA”) PM fix. |

| 2. | Based on the LBMA fix. |

| 3. | Based on the Bank of Canada daily average exchange rate. |

Gold

The market price of gold is subject to significant volatility over relatively short periods of time in response to a broad range of macroeconomic and geopolitical developments. Gold prices are particularly sensitive to movements in the U.S. dollar, real and nominal interest rate expectations, inflation trends, fiscal and monetary policy decisions, and to changes in central bank reserve management, including ongoing purchases and sales of gold. In addition, global and regional supply and demand conditions, shifts in investment flows and broader political and economic uncertainty can all influence the pricing environment for gold. The market price of gold remains a key driver of the performance of our gold streams and related interests and royalty portfolio.

During the three months ended March 31, 2026, the gold price continued to exhibit meaningful day‑to‑day and intra‑quarter volatility and remained at historically elevated levels, supported by persistent safe‑haven demand and ongoing uncertainty around global economic and policy conditions. For the quarter, the gold price (based on the LBMA PM fix) ranged from approximately $4,353 to $5,405 per ounce, averaging approximately $4,873 per ounce, representing an increase of 70% compared to the same period in the prior year (average of approximately $2,860 per ounce for the three months ended March 31, 2025), extending the trend of strengthening prices observed over the second half of 2025 and into 2026. As at March 31, 2026, the gold price was $4,608 per ounce (based on the LBMA PM fix), highlighting the strong pricing environment prevailing at quarter end.

5

Following the end of the quarter, the gold price has largely remained at elevated levels. This performance has been underpinned by continued safe‑haven demand amid heightened geopolitical tensions, including the ongoing conflict in the Middle East, heightened global security concerns and increased uncertainty regarding the outlook for fiscal and monetary policy. In addition, sustained central bank demand for gold as a reserve asset, alongside the effects of renewed trade tensions and supply-chain disruptions, have contributed to the current pricing environment. These factors, individually or collectively, may continue to contribute to increased price volatility and could have a material impact, positive or negative, on the value and cash flows associated with our gold streams and related interests and royalty portfolio.

Silver

The market price of silver is also subject to significant volatility and is shaped by its distinct position at the intersection of industrial demand and investment demand. Unlike gold, a substantial portion of silver consumption is tied directly to manufacturing and technological applications, including electronics, photovoltaic solar panels, automotive and other electrification‑related uses, as well as various specialty chemical and industrial processes. Silver prices are therefore influenced by trends in global industrial production and capital spending, alongside broader macroeconomic conditions, investor sentiment, currency movements and expectations for monetary policy and real interest rates. The performance of our silver streams and related interests and royalty portfolio is closely correlated with these dynamics in the silver market.

In recent periods, demand for silver has been supported by structural growth in renewable energy and electrification‑related applications, with solar and broader energy‑transition technologies emerging as increasingly important end‑markets. At the same time, supply growth has remained constrained, reflecting a limited pipeline of new primary silver projects, the dependence of supply on by‑product output from other metals and the impact of disciplined capital allocation by producers. Against this backdrop, the silver price exhibited pronounced volatility during the three months ended March 31, 2026 but remained at historically high levels, reflecting tight physical market conditions, strong investor participation and ongoing macroeconomic uncertainty. For the quarter, the silver price (based on the LBMA fix) ranged from approximately $67.23 to $118.45 per ounce, averaging approximately $84.33 per ounce, representing an increase of approximately 165% compared to the same period in the prior year (average of approximately $31.88 per ounce for the three months ended March 31, 2025). As at March 31, 2026, the silver price was $72.69 per ounce (based on the LBMA fix), underscoring the robust pricing environment at quarter end. The average silver price also increased during the three months ended March 31, 2026 compared to the prior quarter, in line with the broader upward trend observed since the second half of 2025.

Subsequent to quarter end, silver has continued to trade at elevated levels, with periods of heightened price volatility reflecting both evolving industrial demand expectations and episodic risk‑on and risk‑off investment flows. Price performance has been supported, in part, by continued safe‑haven interest amid geopolitical tensions, including the ongoing conflict in the Middle East, as well as broader uncertainty regarding the trajectory of global economic growth and monetary policy. In addition, persistent structural tightness associated with energy transition‑related demand have all contributed to this backdrop. These elements, individually or in combination, may continue to drive elevated silver price volatility and could have a material impact, positive or negative, on the value and cash flows associated with our silver streams and related interests and royalty portfolio.

Currency Exchange Rates

We are subject to minimal currency fluctuations as the majority of our revenue and cost of sales are denominated in U.S. dollars, with the majority of general administration costs denominated in Canadian dollars. The Company monitors foreign currency risk as part of its risk management program. As at March 31, 2026, there were no hedging programs in place for non-U.S. denominated dollar expenses.

6

Financial and Operating Highlights

Three months ended March 31, 2026, compared to the three months ended March 31, 2025

| | Three months ended March 31, |

| ||||

($ thousands except GEOs, per share metrics, and asset margin) | | | 2026 | | | 2025 |

|

Financial measures: | | | | | | | |

Revenue | | $ | 146,993 | | $ | 82,245 | |

Gross Profit | |

| 105,886 | |

| 49,934 | |

Depletion | |

| 20,142 | |

| 20,549 | |

General Administration Costs | |

| 6,314 | |

| 5,121 | |

Net Earnings | |

| 116,929 | |

| 45,521 | |

Net Earnings per Share – basic | |

| 0.57 | |

| 0.23 | |

Net Earnings per Share – diluted | | | 0.56 | | | 0.23 | |

Operating Cash Flow | |

| 113,331 | |

| 65,854 | |

Operating Cash Flow per Share - basic and diluted | |

| 0.55 | |

| 0.33 | |

GEOs | |

| 30,166 | |

| 28,761 | |

| | | | | | | |

Non-IFRS measures1: | |

| | |

| | |

Adjusted Net Earnings | | $ | 92,707 | | $ | 40,677 | |

Adjusted Net Earnings per Share - basic and diluted | |

| 0.45 | |

| 0.20 | |

Adjusted EBITDA | |

| 128,570 | |

| 70,694 | |

Free Cash Flow | |

| 113,331 | |

| 65,854 | |

Asset Margin | |

| 93% | |

| 93% | |

| 1. | Adjusted net earnings, adjusted net earnings per share, adjusted EBITDA, free cash flow and asset margin as presented above are non-IFRS financial performance measures with no standardized meaning under IFRS Accounting Standards and therefore may not be comparable to similar measures presented by other issuers. For further information and a detailed reconciliation of each non-IFRS measure to the most directly comparable IFRS Accounting Standards measure, see ‘‘Non-IFRS Financial Performance Measures’’ in this MD&A. |

7

The following contains forward-looking information. Reference should be made to the “Forward-Looking Information” and “Technical and Third-Party Information” sections at the end of this MD&A.

In 2026, we expect stream sales and royalty revenue of 95,000 to 105,000 GEOs.

Our 2026 outlook on stream and royalty interests is based on publicly available forecasts of the owners or operators of the underlying properties and/or operations on which we have stream and royalty interests. When publicly available forecasts on properties are not available, we obtain internal forecasts from the owners or operators or use our own best estimate. We conduct our own independent analysis of this information to reflect our expectations based on an operator’s historical performance and track record of replenishing mineral reserves and their publicly disclosed guidance on future production, the conversion of mineral resources to mineral reserves, timing risk adjustments, drill results, our view on opportunities for mine plan optimization and other factors. We may also make allowances for the risk of uneven stream deliveries, timing differences in the deliveries under our streams or the payment of our royalties, and the attainment of public guidance ranges for our counterparties. Achievement of the GEOs and the other metrics set forth in the guidance above is subject to risks and uncertainties, including changes in commodity prices and the ability of operators to attain the results set out in their forecasts. Accordingly, we can provide no assurance that the actual GEOs and such other metrics for 2026 will be within the ranges set forth below. In addition, we may revise our guidance during the year to reflect more current information. If we are unable to achieve our anticipated guidance, or if we revise our guidance, our future results of operations may be adversely affected, and our share price may decline.

Key assumptions include:

| ● | The expected mine sequencing at Northparkes. High-grade gold production at the operation has transitioned from the E31 and E31N open pits to the E48 sub-level cave, which started production in the third quarter of 2025 and is expected to ramp-up through 2026. |

| ● | A step-down in the stream rate from 65% to 25% at Cerro Lindo starting in the second quarter, following the cumulative delivery of 19.5 million ounces of silver since we acquired the stream in 2016. |

| ● | The ramp-up of the Arcata silver and gold mine, which commenced production in the fourth quarter of 2025. |

The following table provides our full year 2026 guidance:

| | 2026 Guidance |

GEOs1 |

| 95,000 to 105,000 GEOs |

Depletion | | $65 million to $75 million |

General administration costs | | $30 million to $32 million |

Australian cash tax rate2 | | ~25% |

| 1. | A gold-to-silver price ratio assumption of 64x in the first quarter, 70x in the second quarter, 75x in the third quarter and 80x in the fourth quarter. We have not assumed any GEOs from Altan Tsagaan Ovoo (“ATO”) in 2026. |

| 2. | Australian Cash Taxes are payable for Triple Flag’s Australian royalty interests, which include Beta Hunt, Fosterville, Stawell and Henty. |

8

Portfolio of Streaming and Related Interests and Royalty Interests

The following tables present our revenue and GEOs sold by asset for the periods indicated. GEOs are based on stream and related interests as well as royalty interests and are calculated on a quarterly basis by dividing all revenue from such interests for the quarter by the average gold price during that quarter. The gold price is determined based on the LBMA PM fix. For periods greater than one quarter, GEOs are summed for each quarter in the period. Management uses this measure internally to evaluate our underlying operating performance across our stream and royalty portfolio for the reporting period presented and to assist with the planning and forecasting of future operating results.

Three months ended March 31, 2026, compared to three months ended March 31, 2025

| | Three months ended March 31, | ||||

Revenue ($000s) | | 2026 | | 2025 | ||

Stream and Related Interests | | | | | | |

Cerro Lindo | | $ | 39,243 | | $ | 14,503 |

Northparkes | | | 32,688 | | | 25,547 |

Bonikro | | | 12,472 | | | 3,635 |

Buriticá | |

| 6,994 | |

| 3,592 |

Impala Bafokeng | |

| 6,761 | |

| 4,759 |

Auramet | | | 5,628 | | | 3,635 |

El Mochito | | | 5,250 | | | 91 |

Agbaou | | | 5,104 | | | 3,148 |

La Colorada | | | 762 | | | 1,878 |

Other | |

| 1,240 | |

| 2,705 |

| | $ | 116,142 | | $ | 63,493 |

Royalty Interests | |

| | |

| |

Beta Hunt | | $ | 6,649 | | $ | 4,642 |

Fosterville | | | 3,429 | | | 2,962 |

Young-Davidson | |

| 2,505 | |

| 1,699 |

Camino Rojo | | | 2,338 | | | 1,953 |

Agbaou | | | 2,266 | | | 1,653 |

Florida Canyon | | | 2,153 | | | 1,539 |

Kensington | | | 1,743 | | | 917 |

Stawell | | | 1,449 | | | 803 |

Johnson Camp | | | 1,037 | | | — |

Henty | | | 797 | | | 658 |

Other | |

| 6,485 | |

| 1,926 |

| | $ | 30,851 | | $ | 18,752 |

Total | | $ | 146,993 | | $ | 82,245 |

| | Three months ended March 31, | ||||

Revenue ($000s) | | 2026 | | 2025 | ||

Gold | | $ | 88,924 | | $ | 62,752 |

Silver | |

| 56,361 | |

| 19,493 |

Copper and other | |

| 1,708 | |

| - |

Total | | $ | 146,993 | | $ | 82,245 |

9

The following table reconciles Revenue with GEOs:

| | Three months ended March 31, | |||

($ thousands, except average gold price and GEOs information) | | 2026 | | 2025 | |

Revenue | | 146,993 |

| 82,245 | |

Average gold price per ounce | | 4,873 |

| 2,860 | |

GEOs1 | | 30,166 |

| 28,761 | |

| 1. | GEOs are calculated on a quarterly basis by dividing all revenue from such interests for the quarter by the average gold price during such quarter. The gold price is determined based on the LBMA PM fix. For periods longer than one quarter, GEOs are summed for each quarter in the period. |

| | Three months ended March 31, | ||

GEOs (ounces) | | 2026 | | 2025 |

Stream and Related Interests | | |

| |

Cerro Lindo | | 8,053 |

| 5,072 |

Northparkes | | 6,708 |

| 8,934 |

Bonikro | | 2,559 | | 1,271 |

Buriticá | | 1,435 |

| 1,256 |

Impala Bafokeng | | 1,387 |

| 1,664 |

Auramet | | 1,155 | | 1,271 |

El Mochito | | 1,077 |

| 32 |

Agbaou | | 1,047 | | 1,101 |

La Colorada | | 156 | | 657 |

Other | | 257 |

| 946 |

| | 23,834 |

| 22,204 |

Royalty Interests | | |

| |

Beta Hunt | | 1,364 | | 1,623 |

Fosterville | | 704 |

| 1,036 |

Young-Davidson | | 514 |

| 594 |

Camino Rojo | | 480 | | 683 |

Agbaou | | 465 | | 578 |

Florida Canyon | | 442 | | 538 |

Kensington | | 358 | | 321 |

Stawell | | 297 | | 281 |

Johnson Camp | | 213 | | — |

Henty | | 164 | | 230 |

Other | | 1,331 |

| 673 |

| | 6,332 |

| 6,557 |

Total | | 30,166 |

| 28,761 |

| | Three months ended March 31, | ||

GEOs (ounces) | | 2026 | | 2025 |

Gold | | 18,249 | | 21,944 |

Silver |

| 11,567 |

| 6,817 |

Copper and other | | 350 | | — |

Total |

| 30,166 |

| 28,761 |

For the three months ended March 31, 2026, we sold 30,166 GEOs, an increase of approximately 5% from 28,761 GEOs sold for the same period in the prior year, largely due to higher GEOs from Cerro Lindo, Bonikro and El Mochito driven by higher deliveries. This was partially offset by lower GEOs from Northparkes due to lower deliveries.

10

During and subsequent to the three months ended March 31, 2026

Acquisition of 3% gross revenue (“GR”) royalty on the Gunnison Project

On March 30, 2026, Triple Flag acquired a 3% GR royalty from Greenstone Excelsior Holdings L.P. (“Greenstone”) on the Gunnison Project in Arizona, United States, operated by Gunnison Copper Corp. (“Gunnison”) for total cash consideration of $23.0 million. This royalty was in addition to Triple Flag’s existing stream on the Gunnison Project and its existing royalty on the Johnson Camp Mine.

On May 5, 2026, Triple Flag entered into an agreement (the “Gunnison Option Agreement”) with Gunnison and Altius Royalty Corporation (“Altius”) providing that, if Gunnison is the subject of a change of control on or before March 31, 2028, the acquiror will receive a single option, which must be exercised in full to do all of the following: (a) reduce Triple Flag's 3% gross revenue royalty by 1% for a payment of $20.0 million and (b) reduce Altius' 1.5% gross revenue royalty by 0.5% for a payment of $10.0 million; and (c) terminate Triple Flag’s expansion option for the stream for a payment of $35.0 million. Pursuant to the Gunnison Option Agreement, Triple Flag and Altius have a veto right on additional royalties, streams or similar burdens on the Gunnison project.

For the three months ended March 31, 2026, and March 31, 2025

Investment in the Northparkes E44 deposit

On February 10, 2026, Triple Flag and Evolution Mining Limited (“Evolution”), entered into an agreement whereby Triple Flag will invest $84.3 million into the development of the high-grade E44 gold open pit at Northparkes, which includes a seven-year period of minimum guaranteed stream deliveries to Triple Flag. Under the terms of the agreement, Triple Flag will be entitled to purchase 20% of payable gold and 30% of payable silver from the E44 deposit for an ongoing payment of 10% of the spot gold and silver price for each ounce delivered. Triple Flag’s existing gold and silver stream on Northparkes is unaffected, other than with respect to the E44 Gold Deposit. The transaction is expected to be funded during the fourth quarter of 2026.

Acquisition of 0.5% GR royalty on the Tres Quebradas lithium project

On March 19, 2025, Triple Flag completed the acquisition of an existing 0.5% GR royalty from Lithium Royalty Corp. for total cash consideration of $28.0 million. The royalty covers all mineral properties comprising the Tres Quebradas lithium project. Tres Quebradas, located in Catamarca province, Argentina, is 100%-owned and operated by Zijin Mining Group Co., Ltd. through its subsidiary Liex SA.

Acquisition of 5% silver and gold streams on Arcata and Azuca mines

On February 27, 2025, Triple Flag completed the acquisition of 5% silver and gold streams on each of the Arcata and Azuca mines (the “Sierra Sun Streams”) operated by Sierra Precious Metals S.A.C., for total cash consideration of $35.0 million. Triple Flag will make ongoing payments of 10% of the spot silver and gold price for each ounce delivered under the Sierra Sun Streams. The Sierra Sun Streams cover the existing mining and exploration licenses for the Arcata and Azuca mines, both located in Peru, for the life of the operations. There is no step-down in stream rates.

Operating Assets – Performance

Our business is organized into one single operating segment, consisting of acquiring and managing precious metals and other high-quality streams and related interests and royalties. Our chief operating decision-maker, the CEO, makes capital allocation decisions, reviews operating results and assesses performance on a single operating segment basis.

11

Asset Performance — Streams and related assets (producing)

| 1. | Northparkes (Operator: Evolution) |

Under the stream agreement, we receive 54% of payable gold until an aggregate of 630,000 ounces have been delivered and 27% of payable gold thereafter. We also receive 80% of payable silver until an aggregate of 9 million ounces of silver have been delivered, and 40% of payable silver thereafter for the remainder of the life of mine. Typically, deliveries under the stream may lag production by approximately two months. As at March 31, 2026, 100,480 ounces of gold and 1,316,862 ounces of silver had been delivered under the stream agreement since inception.

For the three months ended March 31, 2026, we sold 5,867 ounces of gold and 50,023 ounces of silver delivered under the agreement. This compares to 8,424 ounces of gold and 34,508 ounces of silver delivered and sold for the same period in the prior year. GEOs sold were 6,708 for the three months ended March 31, 2026, compared to GEOs of 8,934 for the same period in the prior year, representing a decrease of 25% period over period, driven by lower deliveries.

High-grade gold production has transitioned from the E31 and E31N open pits to the E48 Sub-level cave, which started production in the third quarter of 2025 and is expected to ramp up through 2026. During the first quarter of 2026, Evolution completed the first cut for the E22 block cave. Surface works have also commenced to enable twin access between E48 and E22, which will optimize access, ventilation and materials-handling.

The pre-feasibility study on the potential 10.0 Mtpa mill expansion at Northparkes is on track for completion during Evolution’s fiscal year ending in June 2027. The completion of this study is expected to drive further reserve and resource growth.

On February 10, 2026, Triple Flag and Evolution entered into an agreement whereby the Company will invest $84.3 million into the development of the high-grade E44 gold open pit at Northparkes, refer to the “Key Developments” section above for more details.

| 2. | Cerro Lindo (Operator: Nexa Resources S.A. (“Nexa”)) |

Under the stream agreement with Nexa, we receive 65% of payable silver produced from the Cerro Lindo mine until 19.5 million ounces have been delivered and 25% thereafter. Typically, deliveries under the stream lag production by up to four months. As at March 31, 2026, 19.4 million ounces of silver had been delivered under the stream agreement with Nexa since inception. The step-down in the stream rate at Cerro Lindo from 65% to 25% commenced with silver deliveries starting in late April 2026.

For the three months ended March 31, 2026, we sold 485,951 ounces of silver delivered under the agreement, compared to 463,524 ounces of silver delivered for the same period in the prior year. GEOs sold were 8,053 for the three months ended March 31, 2026, compared to GEOs of 5,072 for the same period in the prior year due to higher deliveries as well as a lower ratio of gold to silver prices during the three months ended March 31, 2026, as compared to the prior period.

Based on the success of the 2025 exploration program, Nexa has highlighted that the current reserve life at Cerro Lindo has been extended to 2032 (from 2031).

12

| 3. | Impala Bafokeng Operations (Operator: Impala Platinum Holdings Limited (“Implats”)) |

Under the stream agreement, we receive 70% of payable gold until 261,000 ounces are delivered and 42% of payable gold thereafter from the Impala Bafokeng Operations (“Impala Bafokeng”). Typically, deliveries under the stream may lag production by approximately five months. As at March 31, 2026, 41,878 ounces of gold had been delivered under the stream agreement since inception.

For the three months ended March 31, 2026, we sold 1,528 ounces of gold delivered under the stream agreement, compared to 1,663 ounces delivered and sold for the same period in the prior year. GEOs sold were 1,387 for the three months ended March 31, 2026, compared to GEOs of 1,664 for the same period in the prior year.

Development of the asset’s value driver, Styldrift, remains ongoing, with a steady ramp-up expected to deliver improved efficiencies.

| 4. | Buriticá (Operator: Zijin Gold International Company Limited (“Zijin”)) |

Under the stream agreement, we receive 100% of payable silver based on a fixed silver-to-gold ratio of 1.84 over the life of the asset and there is no step-down in stream rates. As at March 31, 2026, 2.5 million ounces of silver had been delivered under the stream agreement since inception.

For the three months ended March 31, 2026, we sold 98,765 ounces of silver delivered to the Company under the agreement, compared to 111,382 ounces of silver delivered and sold for the same period in the prior year. GEOs sold were 1,435 for the three months ended March 31, 2026, compared to GEOs of 1,256 for the same period in the prior year.

Zijin expects throughput at Buriticá to ramp up to 5,000 tpd in 2028 – a material increase from current throughput of 4,000 tpd and Triple Flag’s initial investment base case of 3,000 tpd. This higher-than-expected performance from Buriticá is a testament to the quality of Triple Flag’s top-tier portfolio.

| 5. | Agbaou and Bonikro (Operator: Allied Gold Corp. (“Allied”)) |

Under the stream agreements, we receive 3% of payable gold on each of the Agbaou and Bonikro mines until an aggregate of 29,000 ounces and 39,300 ounces, respectively, have been delivered, and 2% of payable gold thereafter. As at March 31, 2026, 5,903 ounces and 8,954 ounces have been delivered under the Agbaou and Bonikro stream agreements, respectively, since inception.

We also own a separate 2.5% NSR royalty interest on all gold production from the Agbaou mine.

For the three months ended March 31, 2026, we sold 1,120 ounces of gold delivered under the Agbaou stream agreement and 2,620 ounces of gold delivered under the Bonikro stream agreement. In the prior year comparable period, 1,133 ounces of gold were delivered under the Agbaou stream agreement and 1,285 ounces of gold under the Bonikro stream agreement. GEOs sold were 1,047 and 2,559 under the Agbaou and Bonikro streams, respectively, for the three months ended March 31, 2026, compared to GEOs of 1,101 and 1,271 under the Agbaou and Bonikro streams, respectively, for the same period in the prior year. GEOs earned from the Agbaou royalty were 465 for the three months ended March 31, 2026, compared to GEOs of 578 for the same period in the prior year.

In February 2026, Allied announced 2026 gold production guidance of 80,000 to 85,000 ounces for Agbaou and 105,000 to 110,000 ounces for Bonikro.

In March 2026, shareholders of Allied approved the previously announced acquisition of Allied by Zijin.

13

Asset Performance — Royalties (Producing)

| 1. | Beta Hunt (Operator: Westgold Resources Limited (“Westgold”)) |

We own a 3.25% gross revenue return (“GRR”) and 1.5% NSR royalties on all gold production, as well as a 1.0% GRR and 0.5% NSR royalty on all nickel production, from the Beta Hunt mine, located in Australia.

GEOs earned were 1,364 for the three months ended March 31, 2026, compared to GEOs of 1,623 for the same period in the prior year.

Westgold continues to advance the expansion project to achieve consistent underground mining rates at Beta Hunt of 2 million tonnes per annum by the end of the first half of 2026.

Following the declaration of a maiden resource for the Fletcher Zone in June 2025, which effectively doubled the previous Beta Hunt resource, substantial exploration and definition drilling to determine its potential scale is ongoing before its integration into a life-of-mine plan. The Fletcher Zone is a significant discovery at Beta Hunt that is interpreted to represent a new gold mineralized structure parallel to the Western Flanks deposit of the mine and is located 50 meters to the west. The Fletcher Zone is within Triple Flag’s royalty coverage area. Western Flanks is currently the primary source of gold ore for Beta Hunt. The maiden resource remains open at depth and represents exploration drilling from only approximately half of the known strike length.

In March 2026, Westgold approved an expansion of the Higginsville mill to a nameplate capacity of 2.6 Mtpa (from 1.6 Mtpa), which is expected to be completed during its 2028 fiscal year. Notably, Westgold has assumed that the main Beta Hunt operation will provide 2.0 Mtpa of feed to Higginsville, with the remaining balance from the Fletcher Zone during Westgold’s fiscal 2029 year. The 2.6 Mtpa expansion flowsheet has been engineered to support future potential growth to 4.0 Mtpa.

| 2. | Fosterville Gold Mine (Operator: Agnico Eagle Mines Limited (“Agnico Eagle")) |

We own a 2% NSR royalty interest in Agnico Eagle’s Fosterville mine in Australia.

GEOs earned were 704 for the three months ended March 31, 2026, compared to GEOs of 1,036 for the same period in the prior year.

In February 2026, Agnico Eagle released an updated three-year outlook. The operator expects Fosterville to produce between 140,000 to 160,000 ounces of gold in each of 2026 and 2027. Notably, annual production is now expected to further increase to a new steady-state of 160,000 to 190,000 in 2028 and remain at that level through the early 2030s, following the completion of mining and processing initiatives that will drive a 65% boost in throughput to 3,300 tpd.

These initiatives at Fosterville include stope-cycle optimization, an increase in development rates to sustain 12 kilometers of annual development, upgrades to ventilation infrastructure, new tailings cells and upgrades to the grinding circuit.

| 3. | Camino Rojo (Operator: Orla Mining Ltd. (“Orla”)) |

We own a 2% NSR royalty interest on oxide material at Orla‘s Camino Rojo mine in Mexico.

GEOs earned were 480 for the three months ended March 31, 2026, compared to GEOs of 683 for the same period in the prior year.

In March 2026, Orla reiterated production guidance for Camino Rojo of 110,000 to 120,000 ounces of gold. Due to grade sequencing, production is expected to be weighted towards the second half of the year.

14

In March 2026, Orla received federal government approval for the mining and processing of the remainder of oxide open pit material at Camino Rojo.

| 4. | Young-Davidson Gold Mine (Operator: Alamos Gold Inc. (“Alamos”)) |

We own a 1.5% NSR royalty interest in Alamos’ Young-Davidson mine in Canada.

GEOs earned were 514 for the three months ended March 31, 2026, compared to GEOs of 594 for the same period in the prior year.

In February 2026, Alamos released three-year production guidance of 155,000 to 175,000 ounces of gold for each of 2026, 2027 and 2028.

Based on current reserves and underground mining rates of 8,000 tpd, the reserve life at Young-Davidson remains at 14 years. Alamos highlighted that the asset has sustained at least a 13-year reserve life since 2011.

15

Prepaid Gold Interests, Investments and other

The following table summarizes prepaid gold interests and investments as at March 31, 2026, and December 31, 2025:

| | As at | | As at | ||

($ thousands) |

| March 31, 2026 |

| December 31, 2025 | ||

Auramet1 | | $ | 75,830 | | $ | 65,320 |

Steppe Gold Ltd. ("Steppe Gold")2 | |

| 2,570 | |

| 2,570 |

Total Prepaid Gold Interests | | $ | 78,400 | | $ | 67,890 |

Investments3 | | | 20,552 | | | 17,421 |

El Mochito4 | | | 29,564 | | | 23,125 |

Total Prepaid Gold Interests, Investments and other | | $ | 128,516 | | $ | 108,436 |

| 1. | The prepaid gold interest contract requires Auramet to deliver 1,250 ounces of gold to Triple Flag per quarter. Triple Flag is required to make ongoing cash payments equal to 16% of the spot gold price for each gold ounce delivered. On September 27, 2031, and after 50,000 ounces of gold have been delivered, Auramet will have the option to terminate the prepaid interest agreement. As at March 31, 2026, 26,250 ounces of gold remains to be delivered under the contract. The Auramet Prepaid Gold Interest is accounted for as a financial asset at fair value through profit or loss and is classified as level 3 of the fair value hierarchy. |

| 3. | Investments comprise equity interests and warrants in publicly traded and private companies and have been recorded at fair value. The fair value of the public equity investments is classified as level 1 of the fair value hierarchy, as the primary valuation inputs used are quoted prices in active markets. The fair value of the private equity investments is classified as level 3 of the fair value hierarchy, as the relevant observable inputs are not available. |

| 4. | The Settlement Agreement requires delivery of 500,000 ounces of silver in 20 equal monthly instalments of 25,000 ounces of silver to Triple Flag. As at March 31, 2026, 400,000 ounces of silver remains to be delivered under the Settlement Agreement. The right to silver deliveries is accounted for as a financial asset at fair value through profit or loss and is classified as level 3 of the fair value hierarchy. |

16

Financial Condition and Shareholders’ Equity Review

Summary Condensed Consolidated Balance Sheets

The following table presents summarized consolidated balance sheet information as at March 31, 2026, and December 31, 2025:

| | As at | | As at | ||

($ thousands) |

| March 31, 2026 | | December 31, 2025 | ||

Cash and cash equivalents | | $ | 144,319 | | $ | 71,284 |

Other current assets | |

| 97,851 | |

| 81,513 |

Non‑current assets | |

| 1,976,385 | |

| 1,960,681 |

Total assets | | $ | 2,218,555 | | $ | 2,113,478 |

| | | | | | |

Current liabilities | | $ | 38,373 | | $ | 38,947 |

Non‑current liabilities | |

| 30,846 | |

| 29,314 |

Total liabilities | |

| 69,219 | |

| 68,261 |

Total shareholders’ equity | |

| 2,149,336 | |

| 2,045,217 |

Total liabilities and shareholders’ equity | | $ | 2,218,555 | | $ | 2,113,478 |

Total assets were $2,218.6 million as at March 31, 2026, compared to $2,113.5 million as at December 31, 2025. Our asset base primarily consists of non-current assets such as mineral interests, which consist of our interests in streams and related interests and royalties. Our asset base also includes current assets, which generally includes cash and cash equivalents, receivables, metal inventory and investments. The increase in total assets from December 31, 2025 was largely driven by the increase in the cash balance and the acquisition of mineral interests, largely from the GR royalty acquired on the Gunnison project, partially offset by the depletion of mineral interests.

Total liabilities were $69.2 million as at March 31, 2026, compared to $68.3 million as at December 31, 2025. Total liabilities consist largely of amounts payable and other liabilities, deferred tax liabilities and lease obligations. The Credit Facility was undrawn at both March 31, 2026 and December 31, 2025. For information about the Credit Facility, see “Liquidity and Capital Resources” below.

Total shareholders’ equity as at March 31, 2026, was $2,149.3 million, compared to $2,045.2 million as at December 31, 2025. The increase in shareholders’ equity from December 31, 2025 largely reflects net earnings generated during the period, partially offset by dividends paid and shares repurchased under the Company’s Normal Course Issuer Bid (“NCIB”).

17

Shareholders’ Equity

As at March 31, 2026 | | Number of shares |

Common shares |

| 206,603,912 |

As at December 31, 2025 |

| Number of shares |

Common shares |

| 206,531,806 |

As at December 31, 2024 |

| Number of shares |

Common shares |

| 201,211,843 |

Our common shares are listed on the Toronto Stock Exchange (“TSX’) in Canadian dollars and on the New York Stock Exchange (“NYSE”) in U.S. dollars, in each case under the symbol “TFPM”.

The NCIB was further renewed in November 2025. Daily repurchases on the TSX will be limited to a maximum of 43,278 common shares, representing 25% of the average daily trading volume on the TSX of 173,115 common shares for the period from May 1, 2025, to October 31, 2025 (net of repurchases made by Triple Flag on the TSX during that time period), except where purchases are made in accordance with the “block purchase exception” of the TSX rules. All common shares that are repurchased by the Company under the NCIB will be canceled. Under the current NCIB, the Company may acquire up to 10,328,075 of its common shares from time to time in accordance with the NCIB procedures of the TSX. Repurchases under the NCIB are authorized until November 16, 2026.

For the three months ended March 31, 2026, the Company purchased 26,459 of its common shares under the NCIB, (2025: 488,600) for $1.0 million (2025: $8.0 million).

In connection with the NCIB, the Company established an automatic share purchase plan (“ASPP”) with the designated broker responsible for the NCIB. The ASPP is intended to allow for the purchase of common shares under the NCIB at times when the Company would ordinarily not be permitted to purchase its common shares due to regulatory restrictions and customary self-imposed blackout periods.

As at May 5, 2026, 206,603,912 common shares are issued and outstanding and stock options are outstanding to purchase a total of 1,073,014 common shares.

For the three months ended March 31, 2026, we declared and paid dividends in United States dollars totaling $11.9 million (2025: $11.0 million). No shares were issued from treasury for participation in the Dividend Reinvestment Plan during the three months ended March 31, 2026 (2025: nil).

18

Condensed Interim Consolidated Statements of Income

The following table presents summarized condensed interim consolidated statements of income information for the three months ended March 31, 2026, compared to the three months ended March 31, 2025:

| | Three months ended March 31, | ||||

($ thousands except share and per share information) |

| | 2026 | | | 2025 |

Revenue | | $ | 146,993 | | $ | 82,245 |

Cost of sales | | | (41,107) | | | (32,311) |

Gross profit | |

| 105,886 | |

| 49,934 |

| | | | | | |

General administration costs | |

| (6,314) | |

| (5,121) |

Business development costs | |

| (1,174) | |

| (262) |

Operating income | |

| 98,398 | |

| 44,551 |

| | | | | | |

Increase in fair value of investments, prepaid gold interests and other | |

| 32,133 | |

| 5,617 |

Finance costs, net | |

| (108) | |

| (601) |

Sustainability initiatives | |

| (31) | |

| (134) |

Foreign currency translation (loss) gain | |

| (110) | |

| 89 |

Other income | |

| 31,884 | |

| 4,971 |

Earnings before income taxes | |

| 130,282 | |

| 49,522 |

Income tax expense | |

| (13,353) | |

| (4,001) |

Net earnings | | $ | 116,929 | | $ | 45,521 |

Weighted average shares outstanding – basic | |

| 206,573,855 | |

| 200,944,812 |

Weighted average shares outstanding – diluted | |

| 207,255,406 | |

| 201,329,822 |

Earnings per share – basic | | $ | 0.57 | | $ | 0.23 |

Earnings per share – diluted | | $ | 0.56 | | $ | 0.23 |

Three months ended March 31, 2026, compared to three months ended March 31, 2025

Revenue was $147.0 million, a quarterly record, and an increase of 79% from $82.2 million for the same period in the prior year. The increase was largely driven by $41.8 million higher revenue due to higher gold prices, $30.1 million higher revenue due to higher silver prices, partially offset by a $5.1 million decrease due to lower volume from streams and related interests, and $2.1 million decrease in revenue from lower volumes from attributable royalty ounces. Lower volumes from streams and related interests were driven by lower deliveries from ATO, Buriticá and Northparkes, partially offset by higher deliveries from Cerro Lindo and Bonikro. Lower revenue from royalties was largely due to lower attributable royalty ounces from Fosterville and Camino Rojo.

The average market gold price and actual gold sales volume for our streams and related interests were $4,873 per ounce and 12,583 ounces, respectively, compared to $2,860 per ounce and 15,424 ounces, respectively, in the prior year. The average market silver price and actual silver sales volume were $84.33 per ounce and 715,639 ounces, respectively, compared to $31.88 per ounce and 612,413 ounces, respectively, in the prior year.

Cost of sales primarily represented the price of metals acquired under our stream agreement and related interests as well as the depletion expense for streams and royalties, both of which are calculated based on units of metal sold or attributable royalty ounces received. Cost of sales was $41.1 million (including depletion) from streams and related interests and royalties, compared to $32.3 million (including depletion) from streams and related interests and royalties for the same period in the prior year. Higher cost of sales was largely driven by the increase in the gold and silver price. Cost of sales for the three months ended March 31, 2026, included $10.0 million in non-cash cost of sales related to

19

prepaid gold interests and other, compared to $5.6 million for the same period in the prior year. The increase in non-cash cost of sales was driven by the El Mochito interest as well as higher metal prices.

Gross profit was $105.9 million, an increase of 112% from $49.9 million for the same period in the prior year. The increase was largely driven by higher gold and silver prices, combined with higher stream deliveries from the Bonikro and Cerro Lindo streams, partially offset by lower gross profit from the Northparkes stream due to lower deliveries.

General administration costs were $6.3 million, compared to $5.1 million for the same period in the prior year. Higher costs for the three months ended March 31, 2026, were largely driven by an increase in employee costs.

Business development costs were $1.2 million, compared to $0.3 million for the same period in the prior year. Business development costs represent ongoing costs incurred throughout the year including use of third-party service providers, net of costs capitalized, and costs reimbursed from our counterparties.

The increase in fair value of investments, prepaid gold interests and other for the three months ended March 31, 2026, was $32.1 million, compared to $5.6 million for the same period in the prior year. The increase related primarily to an increase in the fair value of our prepaid gold interests and other, which was driven by higher market gold and silver prices during the period as well as mark-to-market adjustments on the Company’s equity investments.

Finance costs, net were $0.1 million, compared to $0.6 million for the same period in the prior year. The finance costs, net largely reflect interest charges and standby fees on the Credit Facility, net of interest earned on cash and loan balances. The decrease is largely driven by higher interest income earned on cash balances for the three months ended March 31, 2026.

Income tax expense was $13.4 million, compared to $4.0 million for the same period in the prior year. The increase in income tax expense was due to higher taxes from higher income driven by the increase in fair value of investments, prepaid gold interests and other, as well as the current period sales mix.

Net earnings were $116.9 million, compared to $45.5 million for the same period in the prior year. Net earnings were largely driven by higher gross profit across the portfolio, as well as an increase in the fair value of investments, prepaid gold interests and other, driven by higher metal prices, partially offset by higher taxes.

Condensed Interim Consolidated Statements of Cash Flows

The following table presents summarized consolidated statements of cash flow information for the three months ended March 31, 2026, compared to the three months ended March 31, 2025:

| | Three months ended March 31, | ||||

($ thousands) | | 2026 | | 2025 | ||

Operating cash flow before working capital and taxes | | $ | 130,673 | | $ | 74,242 |

Income taxes paid | |

| (3,874) | |

| (1,970) |

Operating cash flow before working capital | | | 126,799 | | | 72,272 |

Change in working capital | |

| (13,468) | |

| (6,418) |

Operating cash flow | |

| 113,331 | |

| 65,854 |

Net Cash used in investing activities | |

| (27,266) | |

| (63,511) |

Net Cash used in financing activities | |

| (13,017) | |

| (19,834) |

Effect of exchange rate changes on cash and cash equivalents | |

| (13) | |

| 3 |

Increase (decrease) in cash during the period | |

| 73,035 | |

| (17,488) |

Cash and cash equivalents at beginning of period | |

| 71,284 | |

| 36,245 |

Cash and cash equivalents at end of period | | $ | 144,319 | | $ | 18,757 |

20

Three months ended March 31, 2026, compared to three months ended March 31, 2025

Operating cash flow was $113.3 million, a quarterly record, representing an increase of 72% from $65.9 million for the same period in the prior year. The increase was largely driven by higher cash flows from streams, royalties and related interests driven by higher realized metal prices.

Net cash used in investing activities was $27.3 million, compared to $63.5 million for the same period in the prior year. Net cash used in investing activities for the three months ended March 31, 2026, consisted of the acquisition of the Gunnison GR royalty for $23.0 million and the Eskay Creek royalty milestone payment of $6.0 million, partially offset by proceeds from the sale of equity investments of $4.0 million. Net cash used in investing activities for the three months ended March 31, 2025, consisted of the acquisition of the Tres Quebradas lithium royalty for $28.0 million, the acquisition of the Arcata and Azuca streams for $35.0 million, and the associated transaction costs of these acquisitions.

Net cash used in financing activities was $13.0 million, compared to net cash from financing activities of $19.8 million for the same period in the prior year. Net cash used in financing activities for the three months ended March 31, 2026, largely consisted of dividend payments of $11.9 million and shares purchased under the NCIB of $1.0 million. Net cash from financing activities for the three months ended March 31, 2025, largely consisted of dividend payments of $11.0 million, shares purchased under the NCIB of $8.0 million and interest payments of $0.8 million.

Liquidity and Capital Resources

As at March 31, 2026, our cash and cash equivalents were $144.3 million, compared to $71.3 million as at December 31, 2025. Significant variations in the liquidity and capital resources during the period are explained in the ‘‘Condensed Interim Consolidated Statements of Cash Flows’’ section of this MD&A.

Our primary uses of capital are to finance operations, acquire new stream and royalty assets, and for general working capital and payment of dividends. Our objectives when managing capital are to ensure that we will continue to have enough liquidity to achieve our acquisition growth strategy, finance working capital requirements and provide returns to our shareholders. The timing of metal sales from inventory from our stream and related interests is based on commercial considerations, including our assessment of market conditions and our financial requirements. We believe our cash on hand, estimated cash flow from royalties and the sales of metal will be sufficient to fund our anticipated operating cash requirements, payment of dividends and share repurchases under the NCIB for the next 12 months and beyond.

Credit Facility

The Company has a Credit Facility of $700.0 million with an additional uncommitted accordion of up to $300.0 million for a total availability of up to $1.0 billion, maturing on April 22, 2029. As at March 31, 2026, the Credit Facility balance was $nil.

Finance costs relating to the Credit Facility for the three months ended March 31, 2026, were $0.6 million, including interest charges, amortization of debt issue costs and standby fees. This compares to finance costs of $0.7 million for the three months ended March 31, 2025.

The Credit Facility includes covenants that require us to maintain certain financial ratios, including leverage ratios, as well as certain non-financial requirements. As at March 31, 2026, all such ratios and requirements were met. The Credit Facility is used for general corporate purposes and investments in the mineral industry, including the acquisition of streams and related interests and royalty assets.

21

| | 2026 | | 2025 | | 2024 | | ||||||||||

| | Q1 | | Q4 | | Q3 | | Q2 | | Q1 | | Q4 | | Q3 | | Q2 | |

Financial measures: | | | | | | | | | | | | | | | | | |

Cash and cash equivalents |

| 144,319 | | 71,284 | | 8,914 | | 81,770 | | 18,757 | | 36,245 | | 23,602 | | 21,063 |

|

Total assets |

| 2,218,555 | | 2,113,478 | | 2,046,309 | | 1,848,480 | | 1,794,055 | | 1,769,979 | | 1,773,227 | | 1,740,847 |

|

Revenue |

| 146,993 | | 118,916 | | 93,456 | | 94,087 | | 82,245 | | 74,213 | | 73,669 | | 63,581 |

|

Net earnings (loss) |

| 116,929 | | 76,832 | | 61,916 | | 55,736 | | 45,521 | | 41,280 | | 29,649 | | (111,437) |

|

Earnings (loss) per share - basic |

| 0.57 | | 0.37 | | 0.30 | | 0.28 | | 0.23 | | 0.20 | | 0.15 | | (0.55) |

|

Earnings (loss) per share - diluted | | 0.56 | | 0.37 | | 0.30 | | 0.28 | | 0.23 | | 0.20 | | 0.15 | | (0.55) | |

Operating cash flow |

| 113,331 | | 89,497 | | 81,366 | | 76,114 | | 65,854 | | 63,473 | | 61,798 | | 49,357 |

|

Operating cash flow per share - basic and diluted |

| 0.55 | | 0.43 | | 0.39 | | 0.38 | | 0.33 | | 0.32 | | 0.31 | | 0.25 |

|

GEOs |

| 30,166 | | 28,757 | | 27,037 | | 28,682 | | 28,761 | | 27,864 | | 29,773 | | 27,192 |

|

| | | | | | | | | | | | | | | | | |

Non-IFRS measures3: | | | | | | | | | | | | | | | | |

|

Adjusted Net Earnings |

| 92,707 | | 67,561 | | 49,292 | | 47,935 | | 40,677 | | 36,252 | | 28,327 | | 22,903 |

|

Adjusted Net Earnings per share |

| 0.45 | | 0.33 | | 0.24 | | 0.24 | | 0.20 | | 0.18 | | 0.14 | | 0.11 |

|

Adjusted EBITDA |

| 128,570 | | 101,000 | | 78,509 | | 76,166 | | 70,694 | | 62,980 | | 61,702 | | 49,553 |

|

| | | | | | | | | | | | | | | | | |

Average gold price4 |

| 4,873 | | 4,135 | | 3,457 | | 3,280 | | 2,860 | | 2,663 | | 2,474 | | 2,338 |

|

Average silver price5 |

| 84.33 | | 54.73 | | 39.40 | | 33.68 | | 31.88 | | 31.38 | | 29.43 | | 28.84 |

|

| 1. | All amounts in thousands of U.S. dollars except for GEOs, per share information, and average gold and silver price. |

| 2. | Sum of all the quarters may not add up to the annual total due to rounding. |

| 3. | Adjusted net earnings, adjusted net earnings per share and adjusted EBITDA as presented above are non-IFRS financial performance measures with no standardized meaning under IFRS Accounting Standards and therefore may not be comparable to similar measures presented by other issuers. For further information and a detailed reconciliation of adjusted net earnings, adjusted net earnings per share and adjusted EBITDA to the most directly comparable IFRS Accounting Standards measure, see ‘‘Non-IFRS Financial Performance Measures’’ in this MD&A. |

| 4. | Based on the LBMA PM fix. |

| 5. | Based on the LBMA fix. |

In the first quarter of 2026 we achieved record revenue and operating cash flows driven by higher metal prices and higher deliveries from Cerro Lindo and Bonikro. We also entered into an agreement to fund $84.3 million into the development of the high-grade E44 gold open pit at Northparkes and we acquired the Gunnison 3% GR Royalty for $23.0 million.

In the fourth quarter of 2025, we divested the El Mochito silver stream, recognizing a gain of $5.4 million. In the third quarter of 2025, we completed the acquisition of Orogen and its 1.0% NSR royalty on the Arthur gold project in Nevada and acquired a portfolio of royalties on the Minera Florida gold mine in Chile. In the second quarter of 2025, we renewed and upsized our Credit Facility and acquired an additional 1.5% GR on the Johnson Camp Mine. In the first quarter of 2025, we completed the acquisition of the 0.5% GR Tres Quebradas lithium royalty and the Sierra Sun Streams.

In the fourth quarter of 2024, we achieved significant growth in revenue and operating cash flows driven by higher metal prices and higher deliveries from Cerro Lindo, Northparkes and Buriticá. In the third quarter of 2024, we completed the acquisition of 3% gold streams on each of the Agbaou and Bonikro mines, as well as the acquisition of an additional royalty on the Tamarack project.

22

From time to time, we are and may be involved in disputes with other parties arising in the ordinary course of business that may result in litigation. If we are unable to resolve these disputes favorably, it may have a material adverse impact on our financial condition, cash flow and results of operations. We record a liability when it is probable that a loss has been incurred and the amount can be reasonably estimated. We are not currently involved in any material legal proceedings.

Contractual Obligations and Commitments

In the normal course of business, we enter into contracts that give rise to commitments for future minimum payments.

As of March 31, 2026, we had significant commitments to make per ounce cash payments for precious metals and copper pursuant to the terms of the metals purchase and sale agreements and prepaid interests, as detailed in the following table:

| | | | | | | | Attributable | | | | |

|

| | | | | | | | volume | | Per unit | | |

|

Mineral interest | | Commodity | | Inception date | | Unit | | purchased | | cash payment | | Term |

|

Cerro Lindo |

| Silver |

| Dec. 20, 2016 |

| Ounce |

| 65%1 |

| 10% of monthly average |

| Life of mine | |

ATO |

| Gold |

| Aug. 11, 2017 |

| Ounce |

| 25%2 |

| 17% of spot |

| Life of mine | |

ATO |

| Silver |

| Aug. 11, 2017 |

| Ounce |

| 50%3 |

| 17% of spot |

| Life of mine | |

Gunnison |

| Copper |

| Oct. 30, 2018 |

| Pound |

| 16.5%4 |

| 25% of spot |

| Life of mine | |

Buriticá |

| Silver |

| Mar. 15, 2019 |

| Ounce |

| 100%5 |

| 5% of spot |

| Life of mine | |

Impala Bafokeng |

| Gold |

| Jan. 23, 2020 |

| Ounce |

| 70%6 |

| 5% of spot |

| Life of mine | |

Northparkes |

| Gold |

| Jul. 10, 2020 |

| Ounce |

| 54%7 |

| 10% of spot |

| Life of mine | |

Northparkes |

| Silver |

| Jul. 10, 2020 |

| Ounce |

| 80%7 |

| 10% of spot |

| Life of mine | |

La Bolsa | | Gold | | Jan. 19, 2023 | | Ounce | | 5% | | Lesser of $450 and spot | | Life of mine | |

La Colorada | | Gold | | Jan. 19, 2023 | | Ounce | | 100% | | Lesser of $650 and spot | | Life of mine | |

Agbaou | | Gold | | Aug. 14, 2024 | | Ounce | | 3%8 | | 10% of spot |

| Life of mine | |

Bonikro | | Gold | | Aug. 14, 2024 | | Ounce | | 3%9 | | 10% of spot |

| Life of mine | |

Arcata and Azuca | | Gold | | Feb. 27, 2025 | | Ounce | | 5% | | 10% of spot |

| Life of mine | |

Arcata and Azuca | | Silver | | Feb. 27, 2025 | | Ounce | | 5% | | 10% of spot |

| Life of mine | |

Northparkes E44 |

| Gold |

| Feb. 10, 2026 |

| Ounce |

| 20% |

| 10% of spot |

| Life of mine | |

Northparkes E44 |

| Silver |

| Feb. 10, 2026 |

| Ounce |

| 30% |

| 10% of spot |

| Life of mine | |

| | | | | | | | | | | | | |

Prepaid interests | | | | | | | | | | | | | |

Auramet |

| Gold |

| Jan. 19, 2023 | | Ounce |

| 1,250 ounces per |

| 16% of spot |

| Commercial conditions milestones | 10 |

| 1. | 65% of payable silver produced from Cerro Lindo until 19.5 million ounces have been delivered and 25% thereafter. |

| 2. | 25% of gold from ATO until 46,000 ounces of gold have been delivered and thereafter, 25% of gold subject to an annual cap of 7,125 ounces. |

| 3. | 50% of silver from ATO until 375,000 ounces of silver have been delivered and thereafter, 50% of silver subject to an annual cap of 59,315 ounces. |

| 4. | The stream percentage of refined copper produced from the Gunnison mine ranges from 3.5% to 16.5% depending on the Gunnison mine’s total production capacity, with the stream percentage starting at 16.5% and decreasing as the Gunnison mine’s production capacity increases. We have the option to increase our stream participation percentage by paying an additional deposit of an amount up to $65 million. |

| 5. | Streamed silver is to be based on a fixed silver-to-gold ratio of 1.84 over the life of the asset. |

| 6. | 70% of the payable gold until 261,000 ounces have been delivered and 42% thereafter. |

| 7. | 54% of the payable gold produced from the Northparkes mine, except for the E44 Gold Deposit, until 630,000 ounces have been delivered and 27% thereafter; 80% of payable silver produced from the Northparkes mine, except for the E44 Gold Deposit, until 9 million ounces have been delivered and 40% thereafter. |

| 8. | 3% of payable gold until 29,000 ounces have been delivered and 2% thereafter. |

| 9. | 3% of payable gold until 39,300 ounces have been delivered and 2% thereafter. |

| 10. | On and after September 27, 2031 and the delivery of 50,000 ounces of gold. |

23

Investments in Stream and Royalty Interests

As of March 31, 2026, we had commitments related to the acquisition of streams and royalties as detailed in the following table:

Company | | Project (Asset) | | | | Triggering Event |

Centerra Gold Inc.1 | | Kemess | | $10 million |

| Positive construction decision |

| | | | $10 million |

| 1st anniversary of positive construction decision |

| | | | $12.5 million |

| 2nd anniversary of positive construction decision |

| | | | $12.5 million |

| 3rd anniversary of positive construction decision |

Silvercorp Metals2 | | Silvertip | | Payment of deferred | | Payment contingent upon commencement of commercial production and cumulative throughput of 400,000 tonnes of ore |

Barrick Mining Corporation3 | | Portfolio of royalties | | Up to $4 million | | Payment contingent upon certain commercial conditions |

Orion Minerals Ltd.4 | | Prieska Copper‐Zinc | | $80 million | | Conditional upon certain conditions |

Evolution Mining (HK) Limited5 | | Northparkes E44 deposit (Gold and Silver Stream) | | $84.3 million | | Payment due on December 15, 2026. |

| 1. | Kemess stream agreement is with AuRico Metals Inc., a subsidiary of Centerra Gold Inc. |

| 2. | Maverix acquired the Silvertip royalty from 0875786 BC. Ltd., a subsidiary of Silvercorp Metals Inc. (“Silvercorp”). The payment of the deferred equity consideration is payable to Silvercorp. |

| 3. | During the three months ended March 31, 2026, Skeena Gold + Silver announced that it had completed the permitting process for its Eskay Creek Gold-Silver Project. Receipt of permits to advance Eskay Creek into commercial production triggered the payment of contingent consideration to Barrick Mining Corporation (“Barrick”) of $6.0 million. Following this payment, the remaining additional contingent consideration payment obligations owed to Barrick of up to $4.0 million will continue to be outstanding. |

| 4. | Upon the condition of obtaining the South African Reserve Bank exchange control approvals, the mine being fully funded and the finalization of an executable mine plan to Triple Flag’s satisfaction. If the above conditions are met, funding is to be provided in tranches with each tranche subject to the mine continuing to be fully funded to production, among other conditions, and of an amount not to exceed planned expenditures for the next 90 days. Triple Flag has the option to reject the mine plan and supporting documentation, entitling either party to terminate the Stream Agreement. |

| 5. | Refer to the “Key Developments” section above for more details. |

The commitments noted in the table above are expected to be funded from operating cash flow over the next few years.

Contractual Obligations and Commitments

($ thousands) | | Less than 1 year | | 1–3 years | | 3–5 years | | Total | ||||

Undiscounted lease obligation1 | | $ | 456 | | $ | 753 | | $ | 263 | | $ | 1,472 |

Amounts payable and other liabilities | |

| 33,477 | |

| — | |

| — | |

| 33,477 |

Stand-by fees2 | | | 2,030 | | | 4,066 | | | 122 | | | 6,218 |

| | $ | 35,963 | | $ | 4,819 | | $ | 385 | | $ | 41,167 |

| 1. | We are committed to minimum amounts under long-term lease agreements for office space, which expire in 2029. |

| 2. | Represents the Credit Facility, which matures on April 22, 2029. |

Off-Balance Sheet Arrangements or Commitments

We have not entered into any off-balance sheet arrangements or commitments other than as set forth under “Contractual Obligations and Commitments”.

24

Contingencies

Contingencies can be either possible assets or possible liabilities arising from past events which, by their nature, will be resolved only when one or more future events, not wholly within our control, occur or fail to occur. The assessment of such contingencies inherently involves the exercise of significant judgment and estimates of the outcome of future events. Refer to Note 17 of the Annual Financial Statements for further details on the contingencies.

We are not aware of any known trends, commitments (other than as described above), events or uncertainties that will materially affect the Company.

We are in the business of rational risk-taking in pursuit of value creation. Effective risk management is core to the attainment of those often-competing priorities. The ability to deliver on our vision and strategic objectives depends on our ability to understand and effectively respond to and mitigate the risks or uncertainties we face. For additional information about these risks see the “Risk and Risk Management” section of the Company’s most recent Annual Report and the “Risk Factors” section of the Company’s most recent AIF, both of which are available from time to time on SEDAR+ at www.sedarplus.ca and on EDGAR at www.sec.gov. Also see the “Cautionary Statement on Forward-Looking Information” in this MD&A.

Disclosure Controls & Procedures

Management is responsible for establishing and maintaining a system of disclosure controls and procedures to provide reasonable assurance that all material information relating to the Company is gathered and reported to senior management, including the Chief Executive Officer and Chief Financial Officer of the Company, on a timely basis so that appropriate decisions can be made regarding public disclosure, including to ensure that information required to be disclosed by the Company in reports that the Company files or submits under the U.S. Securities Exchange Act of 1934, as amended (the “U.S. Exchange Act”), and applicable Canadian securities laws is recorded, processed, summarized and reported within the time periods specified in the rules and forms of the SEC and the Canadian securities regulatory authorities. Management, under the oversight of the Chief Executive Officer and Chief Financial Officer, has evaluated the effectiveness of the Company’s disclosure controls and procedures as of March 31, 2026. Based on this evaluation, the Chief Executive Officer and Chief Financial Officer concluded that the Company’s disclosure controls and procedures (as defined in National Instrument 52-109 – Certification of Disclosure in Issuers’ Annual and Interim Filings and in Rule 13a-15(e) and Rule 15d-15(e) under the U.S. Exchange Act) were effective as of March 31, 2026.

The Company’s disclosure controls and procedures are designed to provide reasonable assurance of achieving their objectives, and the Chief Executive Officer and Chief Financial Officer do not expect that the disclosure controls and procedures will prevent all errors and fraud. A control system, no matter how well conceived or operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Disclosure controls and procedures have been designed to provide reasonable assurance that all relevant information required to be disclosed by the Company is accumulated and communicated to senior management as appropriate to allow timely decisions regarding required disclosure.

Internal Controls over Financial Reporting

The Chief Executive Officer and Chief Financial Officer are responsible for establishing and maintaining internal controls over financial reporting in order to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with IFRS Accounting Standards. The Company’s internal control framework was designed based on the criteria set forth in Internal Control – Integrated Framework (2013) issued by the Committee of Sponsoring Organizations (“COSO”) of the Treadway Commission 2013 Framework.

25

There was no change in the Company’s internal controls over financial reporting that occurred during the three months ended March 31, 2026, that has materially affected, or is reasonably likely to materially affect, the Company’s internal controls over financial reporting.

The Company’s management assessed the effectiveness of the Company’s internal control over financial reporting as at March 31, 2026, using the COSO framework. Based on management’s assessment, the Company’s internal control over financial reporting was effective as at March 31, 2026.

The Company’s management, including the Chief Executive Officer and Chief Financial Officer, believe that any internal controls over financial reporting and disclosure controls and procedures, no matter how well designed, can have inherent limitations. Therefore, even those systems determined to be effective can provide only reasonable assurance that the objectives of the control system are met.

IFRS Accounting Standards Critical Accounting Policies and Accounting Estimates

Management has discussed the development and selection of our critical accounting estimates with the Audit & Risk Committee and Board of Directors, and the Audit & Risk Committee has reviewed the disclosure relating to such estimates in conjunction with its review of this MD&A. The accounting policies and methods we utilize determine how we report our financial condition and results of operations, and they may require management to make estimates or rely on assumptions about matters that are inherently uncertain. The consolidated financial statements have been prepared in accordance with IFRS Accounting Standards. Our material accounting policies are disclosed in Note 3 to the Annual Financial Statements, including a summary of current and future changes in accounting policies, which are included in Note 5 to the Annual Financial Statements.

Critical Accounting Estimates and Judgments

Certain accounting estimates have been identified as being “critical” to the presentation of our financial condition and results of operations because they require us to make subjective and/or complex judgments about matters that are inherently uncertain; or there is a reasonable likelihood that materially different amounts could be reported under different conditions or using different assumptions and estimates. Our significant accounting judgments, estimates and assumptions are disclosed in Note 4 to the Annual Financial Statements.

Non-IFRS Financial Performance Measures

Adjusted Net Earnings and Adjusted Net Earnings per Share

Adjusted net earnings is a non-IFRS financial measure, which excludes the following from net earnings:

| ● | impairment charges, write-downs, and reversals, including expected credit losses; |

| ● | gain/loss on sale or disposition of assets/mineral interests; |

| ● | foreign currency translation gains/losses; |

| ● | increase/decrease in fair value of investments, prepaid gold interests and other; |

| ● | other non-recurring charges; and |

| ● | impact of income taxes on these items. |

26

Management uses this measure internally to evaluate our underlying operating performance for the reporting periods presented and to assist with the planning and forecasting of future operating results. Management believes that adjusted net earnings is a useful measure of our performance because impairment charges, write-downs, and reversals, including expected credit losses, gain/loss on sale or disposition of assets/mineral interests, foreign currency translation gains/losses, increase/decrease in fair value of investments, prepaid gold interests and other, and other non-recurring charges do not reflect the underlying operating performance of our core business and are not necessarily indicative of future operating results. The tax effect is also excluded by reconciling the amounts on a post-tax basis, consistent with net earnings. Management’s internal budgets and forecasts and public guidance do not reflect the types of items we adjust for. Consequently, the presentation of adjusted net earnings enables users to better understand the underlying operating performance of our core business through the eyes of management. Management periodically evaluates the components of adjusted net earnings based on an internal assessment of performance measures that are useful for evaluating the operating performance of our business and a review of the non-IFRS measures used by industry analysts and other streaming and royalty companies. Adjusted net earnings is intended to provide additional information only and does not have any standardized definition under IFRS Accounting Standards and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS Accounting Standards. This measure is not necessarily indicative of gross profit or operating cash flow as determined under IFRS Accounting Standards. Other companies may calculate these measures differently. The following table reconciles adjusted net earnings to net earnings, the most directly comparable IFRS Accounting Standards measure.

Reconciliation of Net Earnings to Adjusted Net Earnings

| | Three months ended March 31, | ||||

($ thousands, except share and per share information) | | 2026 | | 2025 | ||

Net earnings | | $ | 116,929 | | $ | 45,521 |

Foreign currency translation loss (gain) | |

| 110 | |

| (89) |

Increase in fair value of investments, prepaid gold interests and other | |

| (32,133) | |

| (5,617) |

Income tax effect | |

| 7,801 | |

| 862 |

Adjusted net earnings | | $ | 92,707 | | $ | 40,677 |

Weighted average shares outstanding – basic | |

| 206,573,855 | |

| 200,944,812 |

Weighted average shares outstanding – diluted | | | 207,255,406 | | | 201,329,822 |

Net earnings per share - basic | | $ | 0.57 | | $ | 0.23 |

Net earnings per share - diluted | | | 0.56 | | | 0.23 |

Adjusted net earnings per share - basic and diluted | | $ | 0.45 | | $ | 0.20 |

Free Cash Flow