Exhibit 99.2

First Quarter 2026 Results May 5, 2026 COMMERCIAL REAL ESTATE SERVICES | ENGINEERING | INVESTMENT MANAGEMENT

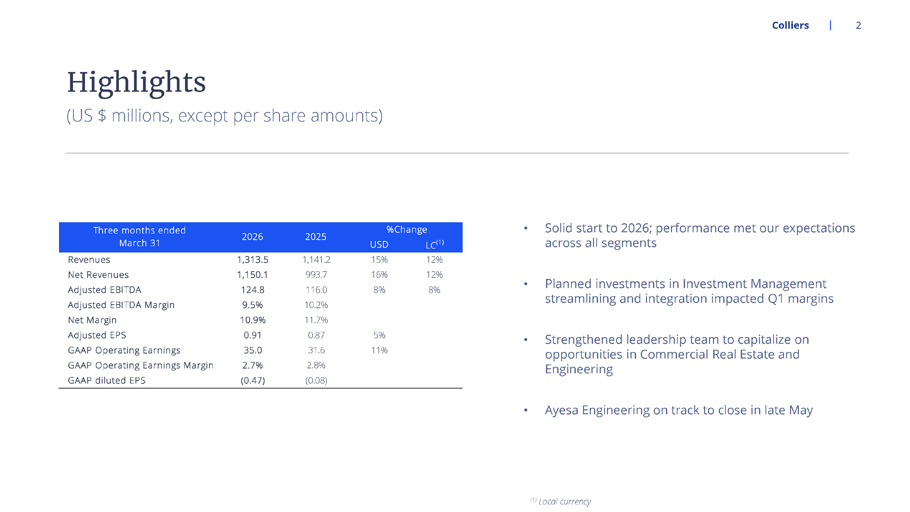

2 Colliers (US $ millions, except per share amounts) Highlights • Solid start to 2026; performance met our expectations across all segments • Planned investments in Investment Management streamlining and integration impacted Q1 margins • Strengthened leadership team to capitalize on opportunities in Commercial Real Estate and Engineering • Ayesa Engineering on track to close in late May USD LC (1) Revenues 1,313.5 1,141.2 15% 12% Net Revenues 1,150.1 993.7 16% 12% Adjusted EBITDA 124.8 116.0 8% 8% Adjusted EBITDA Margin 9.5% 10.2% Net Margin 10.9% 11.7% Adjusted EPS 0.91 0.87 5% GAAP Operating Earnings 35.0 31.6 11% GAAP Operating Earnings Margin 2.7% 2.8% GAAP diluted EPS (0.47) (0.08) Three months ended March 31 2026 2025 %Change (1) Local currency

21% 51% 28% 70% Resilient TTM Q1 2026 AEBITDA by Segment 25% 66% 9% TTM Q1 2026 Revenue by Segment 63% Resilient Colliers Commercial Real Estate Engineering Investment Management Global diversification with 70%+ resilient earnings High value, resilient growth engines Please refer to Appendix 3

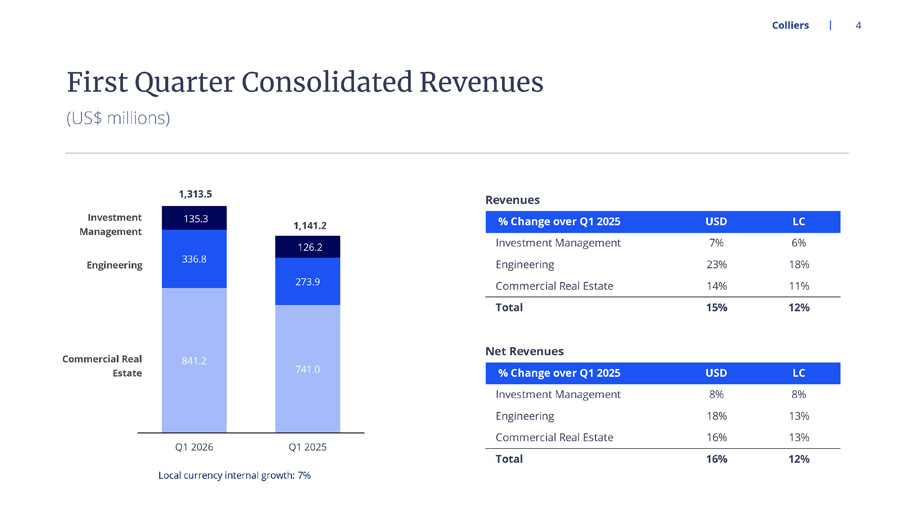

4 Colliers First Quarter Consolidated Revenues Engineering Investment Management Commercial Real Estate % Change over Q1 2025 USD LC Investment Management 7% 6% Engineering 23% 18% Commercial Real Estate 14% 11% Total 15% 12% 841.2 741.0 336.8 273.9 135.3 126.2 1,313.5 1,141.2 Q1 2026 Q1 2025 (US$ millions) Local currency internal growth: 7% Revenues % Change over Q1 2025 USD LC Investment Management 8% 8% Engineering 18% 13% Commercial Real Estate 16% 13% Total 16% 12% Net Revenues

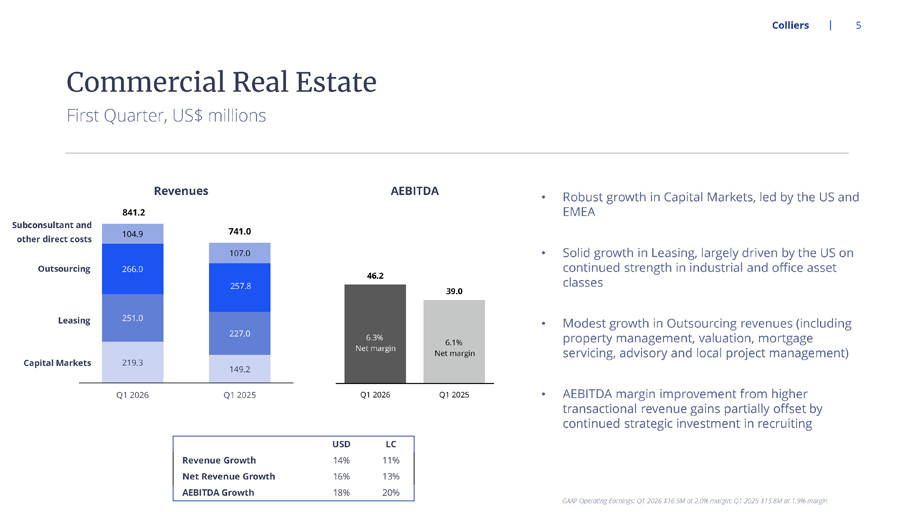

219.3 149.2 251.0 227.0 266.0 257.8 104.9 107.0 841.2 741.0 Q1 2026 Q1 2025 5 Colliers First Quarter, US$ millions Commercial Real Estate • Robust growth in Capital Markets, led by the US and EMEA • Solid growth in Leasing, largely driven by the US on continued strength in industrial and office asset classes • Modest growth in Outsourcing revenues (including property management, valuation, mortgage servicing, advisory and local project management) • AEBITDA margin improvement from higher transactional revenue gains partially offset by continued strategic investment in recruiting 46.2 39.0 Q1 2026 Q1 2025 6.3% Net margin 6.1% Net margin USD LC Revenue Growth 14% 11% Net Revenue Growth 16% 13% AEBITDA Growth 18% 20% Revenues AEBITDA Outsourcing Leasing Capital Markets Subconsultant and other direct costs GAAP Operating Earnings: Q1 2026 $16.5M at 2.0% margin; Q1 2025 $13.8M at 1.9% margin

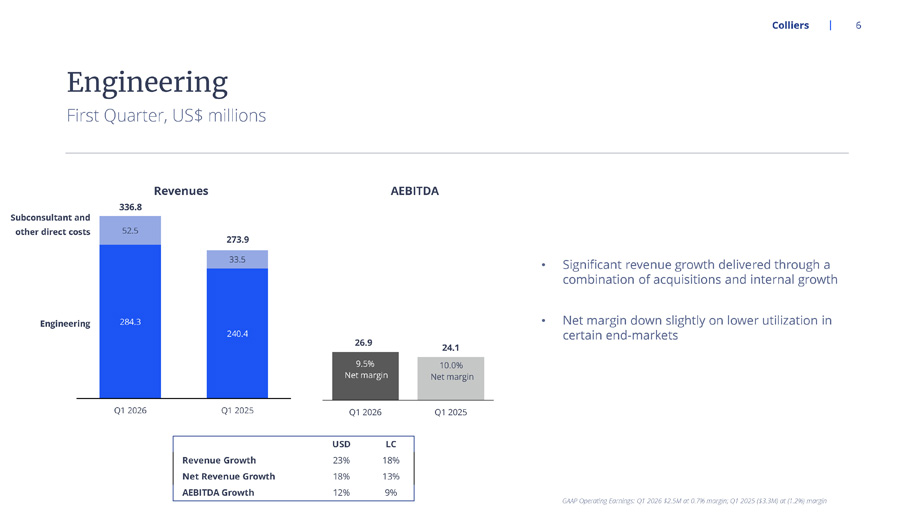

6 Colliers First Quarter, US$ millions Engineering • Significant revenue growth delivered through a combination of acquisitions and internal growth • Net margin down slightly on lower utilization in certain end - markets 284.3 240.4 52.5 33.5 336.8 273.9 Q1 2026 Q1 2025 GAAP Operating Earnings: Q1 2026 $2.5M at 0.7% margin; Q1 2025 ($3.3M) at (1.2%) margin 26.9 24.1 Q1 2026 Q1 2025 9.5% Net margin 10.0% Net margin USD LC Revenue Growth 23% 18% Net Revenue Growth 18% 13% AEBITDA Growth 12% 9% Revenues AEBITDA Engineering Subconsultant and other direct costs

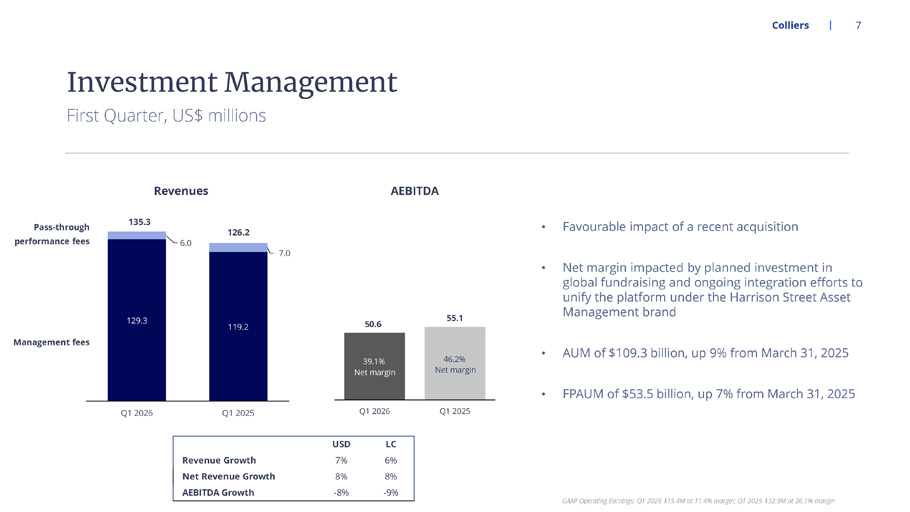

7 Colliers First Quarter, US$ millions Investment Management • Favourable impact of a recent acquisition • Net margin impacted by planned investment in global fundraising and ongoing integration efforts to unify the platform under the Harrison Street Asset Management brand • AUM of $109.3 billion, up 9% from March 31, 2025 • FPAUM of $53.5 billion, up 7% from March 31, 2025 129.3 119.2 6.0 7.0 135.3 126.2 Q1 2026 Q1 2025 GAAP Operating Earnings: Q1 2026 $15.4M at 11.4% margin; Q1 2025 $32.9M at 26.1% margin 50.6 55.1 Q1 2026 Q1 2025 39.1% Net margin 46.2% Net margin USD LC Revenue Growth 7% 6% Net Revenue Growth 8% 8% AEBITDA Growth -8% -9% Management fees Pass - through performance fees Revenues AEBITDA

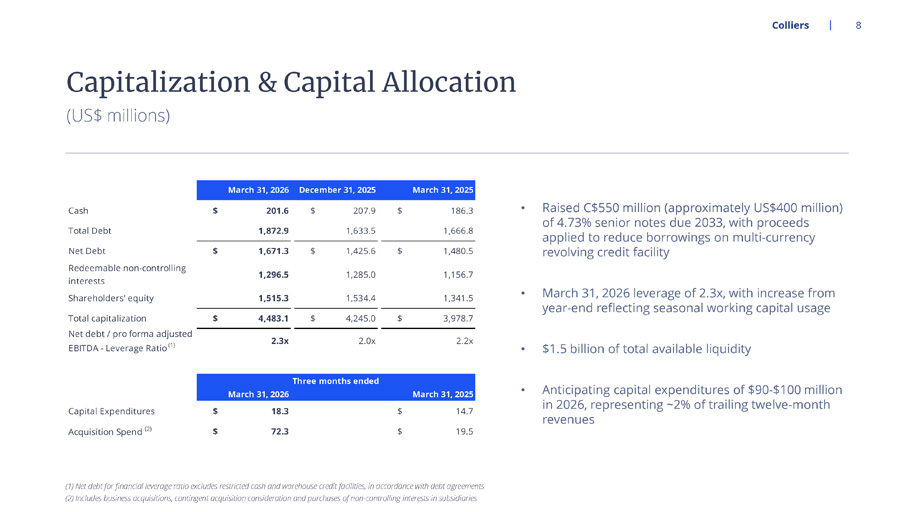

8 Colliers (US$ millions) Capitalization & Capital Allocation • Raised C$550 million (approximately US$400 million) of 4.73% senior notes due 2033, with proceeds applied to reduce borrowings on multi - currency revolving credit facility • March 31, 2026 leverage of 2.3x, with increase from year - end reflecting seasonal working capital usage • $1.5 billion of total available liquidity • Anticipating capital expenditures of $90 - $100 million in 2026, representing ~2% of trailing twelve - month revenues Cash $ 201.6 $ 207.9 $ 186.3 Total Debt 1,872.9 1,633.5 1,666.8 Net Debt $ 1,671.3 $ 1,425.6 $ 1,480.5 Redeemable non-controlling interests 1,296.5 1,285.0 1,156.7 Shareholders' equity 1,515.3 1,534.4 1,341.5 Total capitalization $ 4,483.1 $ 4,245.0 $ 3,978.7 Net debt / pro forma adjusted EBITDA - Leverage Ratio (1) 2.3x 2.0x 2.2x Capital Expenditures $ 18.3 $ 14.7 Acquisition Spend (2) $ 72.3 $ 19.5 Three months ended March 31, 2026 March 31, 2025 March 31, 2026 December 31, 2025 March 31, 2025 (1) Net debt for financial leverage ratio excludes restricted cash and warehouse credit facilities, in accordance with debt a gre ements (2) Includes business acquisitions, contingent acquisition consideration and purchases of non - controlling interests in subsidiar ies

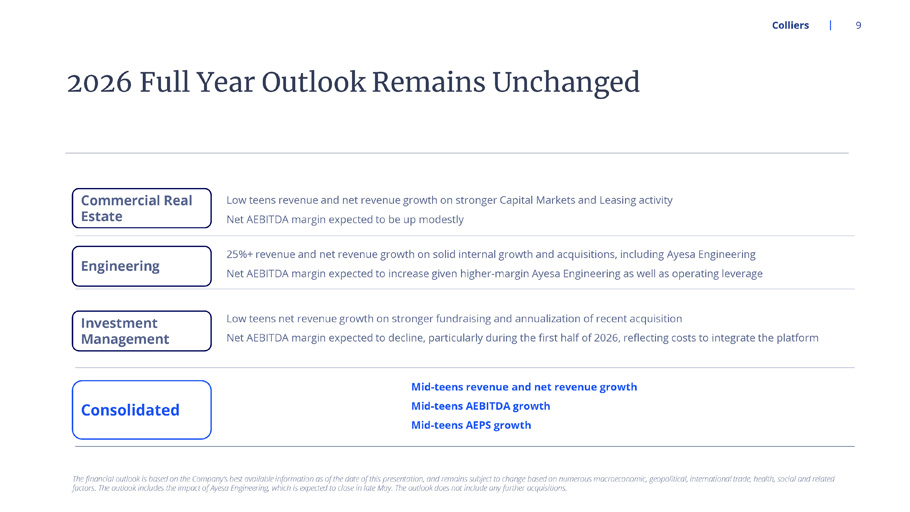

Colliers 9 2026 Full Year Outlook Remains Unchanged The financial outlook is based on the Company’s best available information as of the date of this presentation, and remains s ubj ect to change based on numerous macroeconomic, geopolitical, international trade, health, social and related factors. The outlook includes the impact of Ayesa Engineering, which is expected to close in late May. The outlook does not include any further acquisitions. Commercial Real Estate Engineering Investment Management Consolidated Mid - teens revenue and net revenue growth Mid - teens AEBITDA growth Mid - teens AEPS growth Low teens revenue and net revenue growth on stronger Capital Markets and Leasing activity Net AEBITDA margin expected to be up modestly 25%+ revenue and net revenue growth on solid internal growth and acquisitions, including Ayesa Engineering Net AEBITDA margin expected to increase given higher - margin Ayesa Engineering as well as operating leverage Low teens net revenue growth on stronger fundraising and annualization of recent acquisition Net AEBITDA margin expected to decline, particularly during the first half of 2026, reflecting costs to integrate the platform

Appendix Colliers 10 Reconciliation of non - GAAP Measures

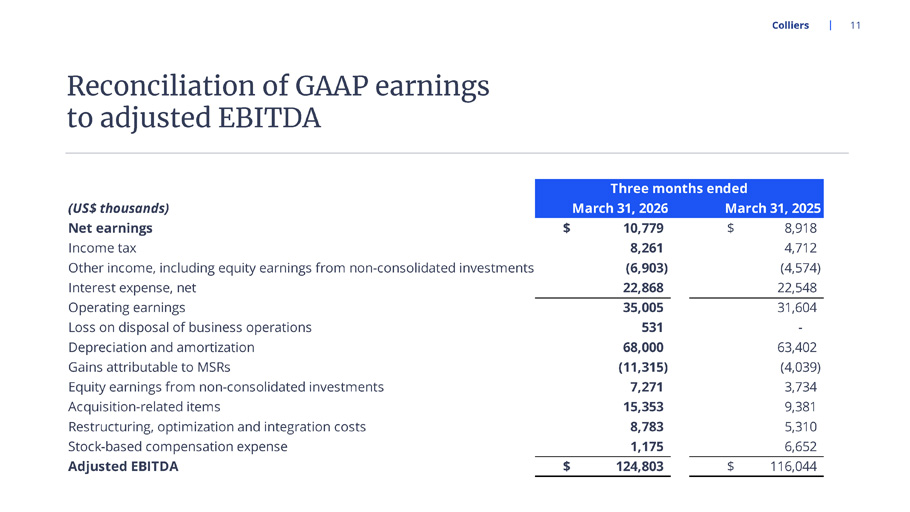

Colliers 11 (US$ thousands) Net earnings $ 10,779 $ 8,918 Income tax 8,261 4,712 Other income, including equity earnings from non-consolidated investments (6,903) (4,574) Interest expense, net 22,868 22,548 Operating earnings 35,005 31,604 Loss on disposal of business operations 531 - Depreciation and amortization 68,000 63,402 Gains attributable to MSRs (11,315) (4,039) Equity earnings from non-consolidated investments 7,271 3,734 Acquisition-related items 15,353 9,381 Restructuring, optimization and integration costs 8,783 5,310 Stock-based compensation expense 1,175 6,652 Adjusted EBITDA $ 124,803 $ 116,044 Three months ended March 31, 2026 March 31, 2025 Reconciliation of GAAP earnings to adjusted EBITDA

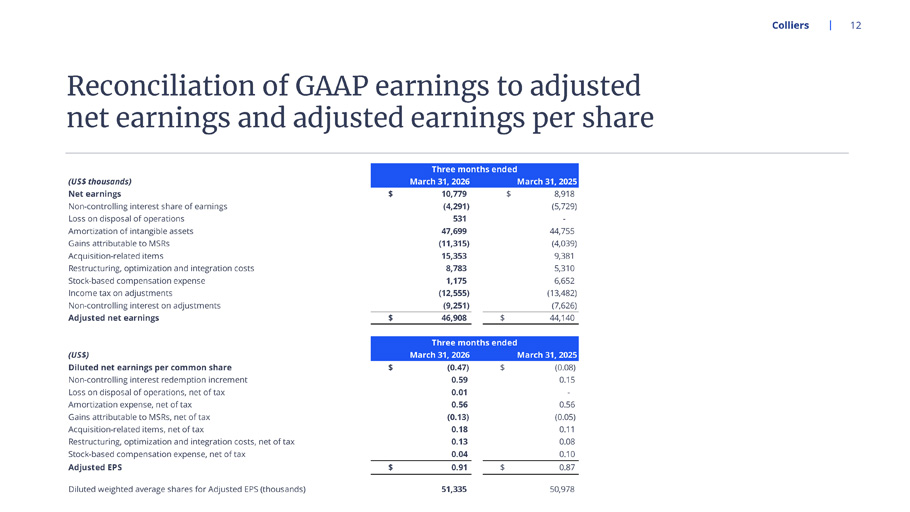

Colliers 12 (US$ thousands) Net earnings $ 10,779 $ 8,918 Non-controlling interest share of earnings (4,291) (5,729) Loss on disposal of operations 531 - Amortization of intangible assets 47,699 44,755 Gains attributable to MSRs (11,315) (4,039) Acquisition-related items 15,353 9,381 Restructuring, optimization and integration costs 8,783 5,310 Stock-based compensation expense 1,175 6,652 Income tax on adjustments (12,555) (13,482) Non-controlling interest on adjustments (9,251) (7,626) Adjusted net earnings $ 46,908 $ 44,140 (US$) Diluted net earnings per common share $ (0.47) $ (0.08) Non-controlling interest redemption increment 0.59 0.15 Loss on disposal of operations, net of tax 0.01 - Amortization expense, net of tax 0.56 0.56 Gains attributable to MSRs, net of tax (0.13) (0.05) Acquisition-related items, net of tax 0.18 0.11 Restructuring, optimization and integration costs, net of tax 0.13 0.08 Stock-based compensation expense, net of tax 0.04 0.10 Adjusted EPS $ 0.91 $ 0.87 Diluted weighted average shares for Adjusted EPS (thousands) 51,335 50,978 Three months ended March 31, 2026 March 31, 2025 Three months ended March 31, 2026 March 31, 2025 Reconciliation of GAAP earnings to adjusted net earnings and adjusted earnings per share

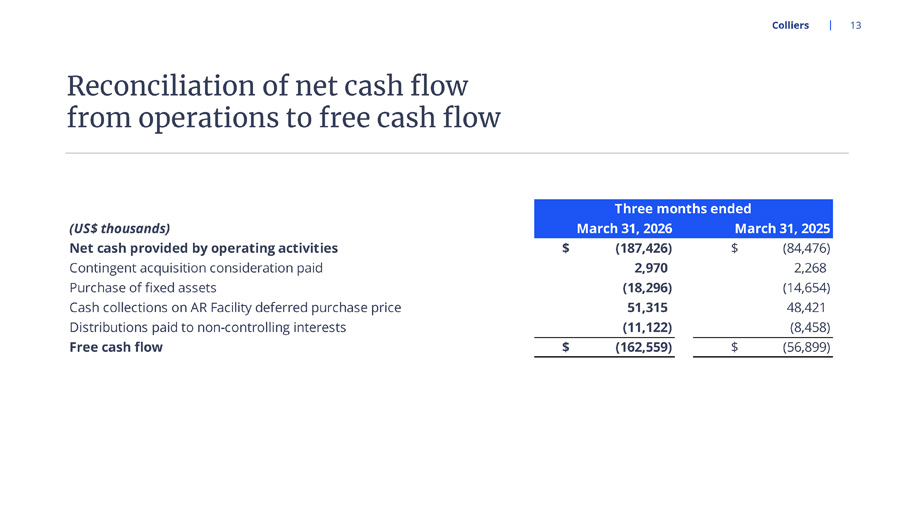

Colliers 13 Reconciliation of net cash flow from operations to free cash flow (US$ thousands) Net cash provided by operating activities $ (187,426) $ (84,476) Contingent acquisition consideration paid 2,970 2,268 Purchase of fixed assets (18,296) (14,654) Cash collections on AR Facility deferred purchase price 51,315 48,421 Distributions paid to non-controlling interests (11,122) (8,458) Free cash flow $ (162,559) $ (56,899) Three months ended March 31, 2026 March 31, 2025

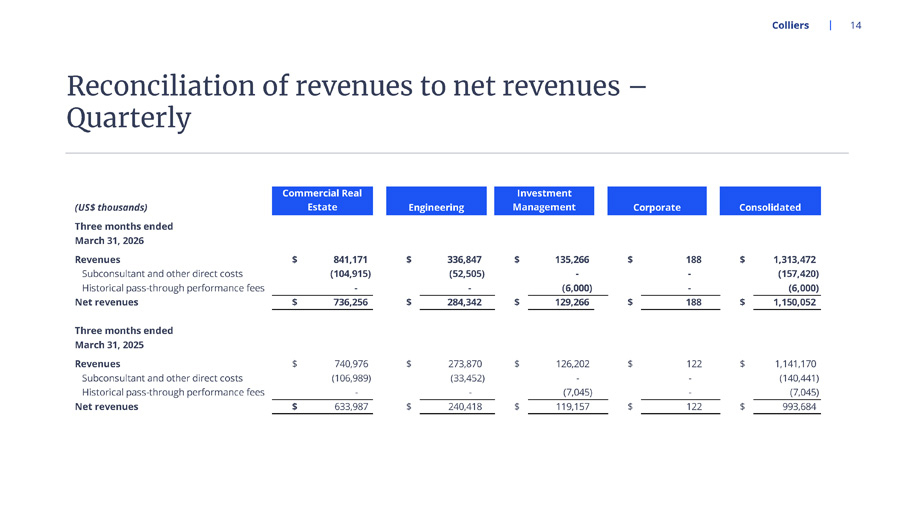

Colliers 14 Reconciliation of revenues to net revenues – Quarterly (US$ thousands) Three months ended March 31, 2026 Revenues $ 841,171 $ 336,847 $ 135,266 $ 188 $ 1,313,472 Subconsultant and other direct costs (104,915) (52,505) - - (157,420) Historical pass-through performance fees - - (6,000) - (6,000) Net revenues $ 736,256 $ 284,342 $ 129,266 $ 188 $ 1,150,052 Three months ended March 31, 2025 Revenues $ 740,976 $ 273,870 $ 126,202 $ 122 $ 1,141,170 Subconsultant and other direct costs (106,989) (33,452) - - (140,441) Historical pass-through performance fees - - (7,045) - (7,045) Net revenues $ 633,987 $ 240,418 $ 119,157 $ 122 $ 993,684 Commercial Real Estate Investment Management Engineering Corporate Consolidated

Local currency revenue and adjusted EBITDA growth rate and internal revenue growth rate measures Percentage revenue and adjusted EBITDA variances presented on a local currency basis are calculated by translating the current period results of our non - US dollar denominated operations to US dollars using the foreign currency exchange rates from the periods against which the current period results are being compared. Percentage revenue variances presented on an internal growth basis are calculated assuming no impact from acquired entities in the current and prior periods. Revenue from acquired entities, including any foreign exchange impacts, are treated as acquisition growth until the respective anniversaries of the acquisitions. We believe that these revenue growth rate methodologies provide a framework for assessing the Company’s performance and operations excluding the effects of foreign currency exchange rate fluctuations and acquisitions. Since these revenue growth rate measures are not calculated under GAAP, they may not be comparable to similar measures used by other issuers. Assets under management We use the term assets under management (“AUM”) as a measure of the scale of our Investment Management operations. AUM is defined as the gross market value of operating assets and the projected gross cost of development assets of the funds, partnerships and accounts to which we provide management and advisory services, including capital that such funds, partnerships and accounts have the right to call from investors pursuant to capital commitments. Our definition of AUM may differ from those used by other issuers and as such may not be directly comparable to similar measures used by other issuers. Fee paying assets under management We use the term fee paying assets under management (“FPAUM”) to represent only the AUM on which the Company is entitled to receive management fees. We believe this measure is useful in providing additional insight into the capital base upon which the Company earns management fees. Our definition of FPAUM may differ from those used by other issuers and as such may not be directly comparable to similar measures used by other issuers. Resilient revenue percentage Resilient revenue percentage is computed on a trailing twelve - month basis and represents the proportion that is derived from Engineering, Outsourcing and Investment Management service lines. All these service lines represent medium to long - term duration revenue streams that are either contractual or repeatable in nature. Revenue for this purpose incorporates the expected full year impact of acquisitions and dispositions. Adjusted EBITDA from resilient revenue percentage Adjusted EBITDA from Resilient for this revenue percentage is computed on a trailing twelve - month basis and represents the proportion of adjusted EBITDA that is derived from Engineering, Outsourcing and Investment Management service lines. All these service lines represent medium to long - term duration revenue streams that are either contractual or repeatable in nature. Adjusted EBITDA purpose is calculated in the same manner as calculated for our debt agreement covenant calculation purposes, incorporating the expected full year impact of business acquisitions and dispositions. Colliers 15 Other Non - GAAP Measures